Heritage Commerce Corp (HTBK): The Story of Silicon Valley's Community Banking Survivor

I. Introduction and Episode Roadmap

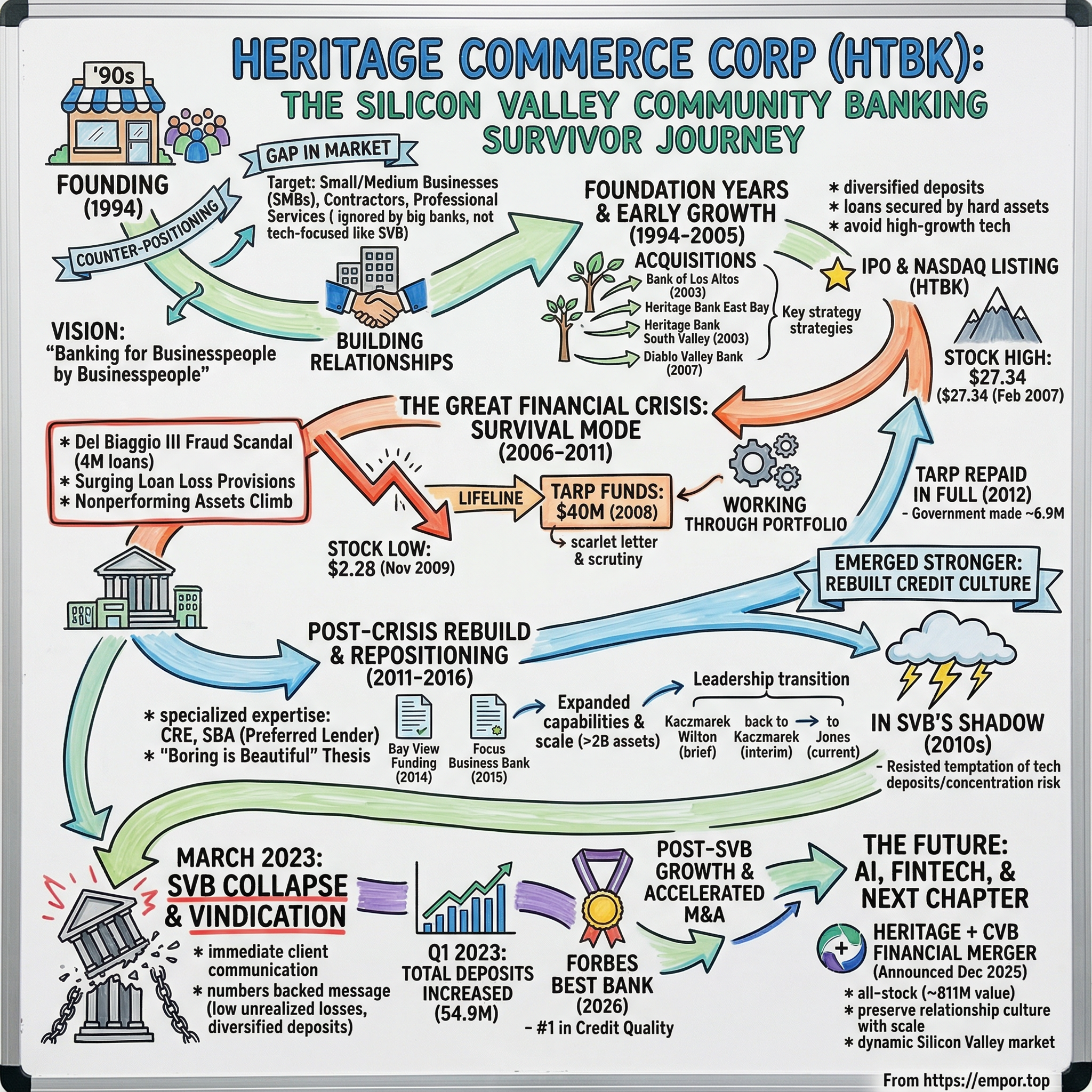

Picture this: you are standing on the corner of Santa Clara Street in downtown San Jose, California, sometime in the mid-1990s. To the north, the semiconductor giants are minting fortunes. Venture capitalists are writing checks that will fund the internet revolution. And a group of local businesspeople are doing something that seems almost quaint by comparison. They are opening a community bank. Not a tech company, not a VC fund, not a fintech startup. A bank. With tellers, and loan officers, and safe deposit boxes.

Three decades later, Heritage Bank of Commerce has grown from that modest downtown storefront into a franchise with nearly six billion dollars in assets, sixteen branches spanning the Bay Area, and a reputation so sterling that Forbes ranked it the number one bank in America for credit quality in 2026. It survived the savings and loan crisis aftermath, the dot-com bust, the worst financial meltdown since the Great Depression, a global pandemic, and the spectacular implosion of its most famous neighbor, Silicon Valley Bank.

And it did all of this by doing something that sounds almost paradoxical in the world's most innovation-obsessed ZIP code: it stayed boring.

This is the story of Heritage Commerce Corp, ticker symbol HTBK on the NASDAQ, and the holding company behind Heritage Bank of Commerce. It is a story about the power of strategic constraint, about knowing exactly what you are and, more importantly, what you are not. It is a story about how a small bank with a handful of branches and three hundred and fifty employees managed to outlast, outperform, and ultimately outlive the institution that defined Silicon Valley banking for a generation.

The narrative arc here is almost novelistic. We will trace Heritage from its founding in 1994 through the harrowing years of the Great Financial Crisis, when the stock plunged ninety-two percent and the bank took forty million dollars in government bailout money. We will examine the strategic choices that kept Heritage away from the siren song of tech banking, even as Silicon Valley Bank was growing into a two-hundred-billion-dollar colossus.

We will relive the weekend of March 10, 2023, when SVB collapsed and Heritage's decades of disciplined, boring banking were suddenly, dramatically vindicated. And we will grapple with the question that now defines Heritage's future: is this the right time to sell, or the worst possible time to give up independence?

The major themes running through this episode are ones that any business operator, founder, or investor should recognize. Relationship banking versus scale. Navigating multiple financial crises without blowing up. The art of saying no in a market that rewards saying yes. And the enduring question of whether boring can be beautiful in perpetuity, or whether even the best community banks eventually need to find a bigger partner.

Let us start at the beginning.

II. Founding Context: California Banking in the 1970s-80s

To understand why Heritage Bank of Commerce exists, you need to understand what California banking looked like in the decades before its founding. The 1970s and 1980s were a period of extraordinary upheaval in American finance, and nowhere was that upheaval more dramatic than in California. The state was home to a sprawling ecosystem of savings and loan institutions, regional banks, and community banks that operated under a patchwork of state and federal regulations. When deregulation arrived in the early 1980s, it was like throwing a match into a room full of gasoline.

The S&L crisis of the late 1980s wiped out hundreds of institutions across the state. The lesson was brutal and straightforward: when you let financial institutions chase yield without adequate risk management, bad things happen. But the crisis also created something else: a vacuum. As the big institutions consolidated and the failed ones disappeared, there were suddenly gaps in the market. Small businesses that had relied on their local S&L or regional bank for lines of credit found themselves orphaned, shuffled into the bureaucratic machinery of Bank of America or Wells Fargo, where they were account numbers rather than relationships.

Meanwhile, the San Jose and Silicon Valley landscape of the late 1980s and early 1990s was undergoing its own transformation. The semiconductor boom had given way to the early days of the software revolution. Venture capital was becoming a real industry, not just a hobby for a handful of wealthy families on Sand Hill Road. But Silicon Valley in 1994 was still, in many ways, an industrial economy. There were contractors building office parks, small manufacturers making components, professional services firms serving the emerging tech companies, healthcare practices, and light industrial operations scattered across the South Bay.

These businesses needed banks. But the big national banks treated them as afterthoughts, too small for dedicated relationship managers, too complex for cookie-cutter lending products. And the one bank that was beginning to specialize in the Silicon Valley market, a young institution called Silicon Valley Bank, was already orienting itself toward the venture capital ecosystem and high-growth tech startups. If you were a contractor in San Jose with two million dollars in annual revenue and needed a construction line of credit, SVB was not interested in your business.

This was the gap that William Del Biaggio Jr. saw and decided to fill. Del Biaggio was a prominent civic leader in San Jose, deeply embedded in the local business community through organizations like the Rotary Club and the Silicon Valley Leadership Group. He understood something fundamental about small business banking: it runs on trust, on personal relationships, on the ability to pick up the phone and talk to someone who knows your business, your industry, and your character. The big banks could not offer that. SVB was not trying to. And the S&L crisis had eliminated many of the community institutions that once did.

Heritage Bank of Commerce was founded in 1994 with a simple, almost old-fashioned proposition: be the bank for small and medium-sized businesses that the big banks ignored. The tagline was "Banking for Businesspeople by Businesspeople," and it was not just marketing copy. Del Biaggio and the founding team were themselves businesspeople, drawn from the local commercial and civic ecosystem, and they built the bank around the principle that knowing your borrower's business mattered more than any algorithm or credit model.

The early business model was straightforward: commercial real estate lending, commercial and industrial loans, personalized service delivered by experienced bankers who lived and worked in the same communities as their clients. It was relationship banking in its purest form, and in the booming Bay Area economy of the 1990s, it worked. Heritage Commerce Corp was formed as the bank holding company in October 1997, and the stock began trading on the NASDAQ under the ticker HTBK shortly thereafter, giving the bank access to public capital markets and a currency for future acquisitions.

The founding vision may have seemed modest compared to the venture-backed rockets launching all around it, but modesty, as Heritage would prove again and again, has its own kind of power.

For investors trying to understand Heritage today, this founding context is essential. The bank was not born out of a desire to disrupt or innovate. It was born out of a recognition that there was a gap in the market for something deeply traditional: a bank that treated its clients like partners rather than account numbers. That founding DNA, established in the S&L era wreckage, would prove remarkably durable across three decades and multiple financial crises. The question was never whether Heritage could compete with the giants. The question was whether it could carve out a niche that the giants could not profitably serve. The answer, as it turned out, was yes.

III. The Foundation Years and Early Growth (1994-2005)

The first decade of Heritage Bank of Commerce was a classic community banking growth story, built one relationship at a time. The initial customer base was exactly the kind of businesses that the founders understood best: contractors, small manufacturers, professional services firms, and the small-to-midsize enterprises that formed the unglamorous but essential infrastructure of Silicon Valley's economy. These were not companies that would ever appear on the cover of Wired magazine, but they were the ones that paved the roads, built the offices, managed the payrolls, and provided the dental care for the people who did.

The relationship banking playbook that Heritage employed was deceptively simple in concept but extraordinarily difficult in execution. Every borrower was more than a financial statement. The bankers at Heritage were expected to understand their clients' businesses, visit their operations, know their competitive landscape, and make lending decisions based on a combination of quantitative analysis and qualitative judgment. This is the "know your customer" model in its most literal sense, and it creates something that no algorithm can replicate: a banker who can tell the difference between a business that is struggling because of a temporary market dip and one that is structurally impaired. That distinction, when you are making lending decisions, is the difference between a performing loan and a charge-off.

Geographic expansion came through a combination of organic branch openings and targeted acquisitions. On January 1, 2003, Heritage completed three acquisitions simultaneously: Bank of Los Altos, Heritage Bank East Bay, and Heritage Bank South Valley. These were not transformative deals in terms of size, but they were strategically important, giving Heritage a presence across multiple Bay Area submarkets and demonstrating a template for growth through acquisition that the bank would refine over the following two decades. In 2007, Heritage acquired Diablo Valley Bank in Danville for seventy million dollars, further extending its East Bay footprint.

The competitive landscape during these years was challenging but navigable. Bank of America and Wells Fargo dominated the retail banking market with their massive branch networks and consumer marketing budgets. Silicon Valley Bank was emerging as the undisputed champion of tech and venture capital banking, building what would eventually become a two-hundred-billion-dollar franchise by serving the specific needs of VC-backed startups and their investors. Heritage had to find its niche in between, and it did so with a strategic decision that would prove to be the most important one in the bank's history: stay away from high-flying tech.

This was not a decision made out of ignorance or inability. The Heritage team understood the tech economy as well as anyone; they lived in it. But they also understood the risk profile. Tech and venture capital banking meant concentrated deposits from a small number of large clients, loans collateralized by intellectual property rather than hard assets, and a business model that was inherently cyclical. Heritage chose the opposite: diversified deposits from hundreds of small businesses, loans secured by commercial real estate and business assets, and a client base whose revenues were tied to the fundamental needs of the local economy rather than the whims of venture capital. Think of it this way: if a recession hits, people still need dentists, still need contractors to fix their roofs, still need accountants to file their taxes. Those businesses slow down, but they do not disappear. A VC-backed startup burning through cash, on the other hand, can go from thriving to dead in a single quarter when funding dries up.

The bank's early IPO and NASDAQ listing gave it access to public capital markets, which was unusual for a community bank of its size and an important strategic advantage. Public currency allowed Heritage to make acquisitions using stock rather than cash, preserving its capital base while growing through M&A. It also provided transparency and liquidity that attracted a base of income-oriented investors who valued the bank's steady dividend payments and conservative management.

By the mid-2000s, Heritage had built a solid franchise. The stock reached its all-time high of $27.34 on February 8, 2007, reflecting the market's confidence in a well-run community bank operating in one of the most economically vibrant markets in the world. Walter Kaczmarek had taken over as President and CEO in 2005, bringing with him fifteen years of experience at Comerica and a deep understanding of middle-market banking. Under Kaczmarek's leadership, the bank was growing, profitable, and well-regarded. Everything seemed to be going right.

Then the world fell apart.

IV. The Great Financial Crisis: Survival Mode (2006-2011)

The Great Financial Crisis arrived at Heritage Bank of Commerce with a particularly cruel twist of irony. Before the broader economic meltdown even began, the bank found itself at the center of a fraud scandal that struck at the heart of its founding family.

William "Boots" Del Biaggio III, the son of Heritage's founder, was a Silicon Valley financier who had used fraudulently obtained loans to purchase a controlling stake in the Nashville Predators NHL franchise. His scheme was brazen: he obtained approximately one hundred and ten million dollars in loans from thirteen banks and private lenders by forging financial statements, replacing the names of wealthy stockholders with his own and presenting doctored documents as collateral. Among his victims was the very bank his father had founded. Heritage Bank of Commerce had extended four million dollars in loans to the younger Del Biaggio, loans that turned out to be secured by fiction.

The bank sued its founder's son in June 2008, but the financial damage was already done. Heritage took a $5.1 million provision for loan losses in the second quarter of 2008 specifically related to the Del Biaggio loans, driving the company to a net loss of $3.1 million for the quarter, compared to net income of $4 million in the same period a year earlier. Del Biaggio III was charged federally in December 2008 and ultimately sentenced to eight years in prison. It was a painful, deeply personal crisis for a bank that had been built on the principle of trust and relationships.

But the Del Biaggio scandal was just the opening act. The broader financial crisis hit Heritage like it hit every bank with commercial real estate exposure in a market that had been booming for years. Loan loss provisions surged. In the first quarter of 2009, Heritage recorded a provision of $10.4 million. Nonperforming assets, which had been a negligible fraction of total assets, began climbing relentlessly. The stock, which had touched that all-time high of $27.34 just two years earlier, cratered to an all-time low of $2.28 on November 10, 2009. A ninety-two percent decline. For shareholders who had believed in the Heritage story, it was devastating.

On November 21, 2008, Heritage Commerce Corp received forty million dollars in capital from the U.S. Treasury through the Troubled Asset Relief Program's Capital Purchase Program. The money came in the form of preferred stock with warrants, the same structure used across hundreds of American banks during the crisis. TARP was a lifeline, but it was also a scarlet letter. Receiving government money meant heightened regulatory scrutiny, restrictions on executive compensation and dividends, and the public perception that your bank was in trouble. Which, to be fair, it was.

The dark years that followed were defined by the grinding, unglamorous work of crisis management. Heritage cut its dividend, raised additional capital, and embarked on the painstaking process of working through its portfolio of bad loans. This is the part of banking that never makes it into the glossy annual reports: the meetings with troubled borrowers, the negotiations with guarantors, the decisions about whether to extend, restructure, or foreclose. Each of these decisions carries enormous consequences, not just financially but for the real businesses and real people on the other side of the table.

What separated Heritage from the hundreds of community banks that failed during this period was a combination of factors. The capital cushion from TARP helped, certainly. But more importantly, the bank's underwriting, while not perfect, had been conservative enough to avoid the worst excesses of the pre-crisis lending boom. Heritage had not chased the most aggressive construction and development deals. It had not loaded up on exotic commercial real estate structures. Its problems were serious but manageable, and the management team under Kaczmarek had the discipline and the stomach to work through them.

The crisis permanently changed Heritage's DNA. The credit culture was rebuilt from the ground up, with new underwriting standards, new concentration limits, and a fundamentally more conservative approach to risk. The lessons of 2008-2010 were embedded in policy, in process, and most importantly, in the institutional memory of every banker who had lived through it. When Heritage finally repaid its TARP obligation in full on March 7, 2012, it emerged from government support with scars, with wisdom, and with a credit culture that would prove to be its most valuable asset in the decades to come.

The total return to taxpayers on the TARP investment was approximately $6.9 million, consisting of roughly $6.76 million in dividend payments between 2009 and 2012 and $140,000 in warrant proceeds, meaning the government made money on its bet on Heritage. Not every bank could say the same.

There is a useful myth versus reality check worth conducting here. The popular narrative about community banks during the financial crisis is that they were either reckless cowboys who blew themselves up or conservative institutions that sailed through unscathed. Heritage was neither. It made mistakes, it took losses, it needed government help, and its stock price told a story of genuine distress. But the reality is more nuanced and more instructive: Heritage's mistakes were manageable because its pre-crisis discipline, while imperfect, had kept the bank away from the worst excesses. And the management team's willingness to confront the problems honestly, to take the pain of recognizing losses rather than hiding them, ultimately allowed Heritage to emerge from the crisis faster and stronger than many of its peers. More than five hundred banks failed during the crisis and its aftermath. Heritage was not one of them, and the lessons it learned would compound in value for the next fifteen years.

V. The Post-Crisis Rebuild and Strategic Repositioning (2011-2016)

If the financial crisis was Heritage's near-death experience, the post-crisis period was its rehabilitation. And like any good rehabilitation, it started with an honest assessment of what had gone wrong and a commitment to doing things differently.

The balance sheet cleanup was the first priority. Non-performing loans had to be resolved, either through restructuring, through the long process of working out the collateral, or through the painful recognition of charge-offs. This process took years, not quarters, and it required a level of patience and discipline that not every management team possesses. The goal was not just to get the numbers to a respectable level but to rebuild credibility with regulators, with investors, and most importantly, with the business community that Heritage served.

The strategic repositioning that emerged from this period crystallized the philosophy that would define Heritage for the next decade. The bank doubled down on business banking, not consumer. On relationships, not transactions. On industries it understood deeply, not sectors where it was chasing growth. The lending teams developed specialized expertise in commercial real estate, SBA lending, and the specific needs of Bay Area small businesses. Heritage became one of the largest SBA Preferred Lenders in California, a designation that gave it the ability to approve SBA loans internally rather than waiting for government processing, a significant competitive advantage in speed and responsiveness.

The "boring is beautiful" thesis was not a marketing slogan but a genuine strategic conviction. Heritage's target clients were professional services firms, light manufacturers, healthcare practices, and the broad spectrum of small and mid-sized enterprises that constituted the real economy of the Bay Area. These were businesses that needed reliable banking partners, not flashy financial engineering. They needed someone who could approve a credit line in days rather than weeks, who understood the seasonality of their business, and who would still be there when the next downturn arrived.

In 2014, Heritage made a strategically important acquisition that expanded its capabilities beyond traditional banking. It purchased Bay View Funding, a factoring company based in Santa Clara, for $22.5 million in cash. Bay View had over thirty years of experience in accounts receivable factoring, handling facilities up to twenty million dollars for clients across the country. This gave Heritage a national specialty finance platform and added a new dimension to its product offering: factoring, asset-based lending, and the ability to serve emerging growth companies that needed flexible working capital solutions. The Specialty Finance Group, as it came to be known, served a diverse clientele of privately held, microcap, venture-backed, and even publicly traded companies.

The 2015 acquisition of Focus Business Bank was another milestone, a stock deal valued at approximately seventy-six million dollars that added $408 million in assets and pushed the combined company over two billion dollars in total assets for the first time. Focus was a natural fit: a San Jose-based community business bank with a similar culture and client profile. The integration went smoothly, reinforcing Heritage's confidence in its ability to grow through acquisition without sacrificing culture.

By 2016, Heritage had fully recovered from the crisis. The bank was consistently profitable, the credit quality metrics were excellent, and the efficiency ratio was moving in the right direction. The stock had recovered from its crisis lows, and the dividend had been reinstated in 2013, a quarterly payout that has been maintained every quarter since. Heritage had survived the crisis, learned from it, and emerged stronger.

The leadership transition during this period deserves attention. Kaczmarek, who had guided the bank through the darkest days of the financial crisis with steady, experienced leadership, began planning for succession. In January 2019, the company announced its CEO succession strategy, with Keith Wilton, who had joined Heritage in 2014 as Executive Vice President and Chief Operating Officer and been promoted to President of the Bank in 2017, designated as the successor. Kaczmarek retired in August 2019 after fourteen years at the helm, leaving behind a bank that was unrecognizable from the one he had inherited in 2005: larger, better capitalized, more disciplined, and more profitable.

But the competitive environment was about to get a lot more interesting.

VI. The Competitive Crucible: Living in SVB's Shadow (2010s)

There is a particular kind of psychological pressure that comes from operating a small, disciplined business in the shadow of a much larger, much more glamorous competitor. In Silicon Valley banking during the 2010s, that competitor was Silicon Valley Bank, and the shadow it cast was enormous.

SVB's growth during the 2010s was nothing short of extraordinary. The bank had found the perfect product-market fit: it served the venture capital ecosystem, providing banking services to VC firms and their portfolio companies, offering the specialized products that startups needed, venture debt, credit lines against future funding rounds, treasury management for companies burning through cash. By the end of the decade, SVB had grown to over two hundred billion dollars in assets and controlled an estimated sixty to seventy percent of the entire venture debt market. It was the most important financial institution in the innovation economy.

For Heritage, watching SVB's meteoric rise from just a few miles away must have been a constant test of strategic conviction. The temptation to chase even a small piece of the tech banking market was real. Here was this enormous pool of deposits and lending opportunities, growing at rates that community banks could only dream about, and Heritage was choosing to ignore it in favor of lending to contractors and dentists.

But the Heritage leadership understood something that most observers did not appreciate until much later: SVB's extraordinary growth came with extraordinary risks. The bank's deposit base was heavily concentrated in a single industry and a single type of client. VC-backed startups are, by definition, companies that are spending more money than they are making, which means their deposits are inherently unstable. When the funding environment shifts, those deposits can evaporate overnight. Moreover, SVB's clients were all connected through the same social and professional networks. The VCs talked to each other, the founders talked to each other, and when confidence wavered, the information traveled at the speed of a WhatsApp message.

Heritage's decision to stay away from this market was not cowardice or lack of ambition. It was a conscious strategic choice rooted in a deep understanding of the risk-reward trade-off. The upside of tech banking was spectacular growth. The downside was catastrophic concentration risk. Heritage chose the boring path: lower growth, lower volatility, a more diversified deposit base, and the ability to sleep at night knowing that no single industry downturn could blow up the bank.

The opportunity cost was real, and Heritage's investors felt it. During the 2010s, SVB's stock price soared while Heritage's growth was steady but unspectacular. In the parlance of portfolio management, Heritage was a classic "sleep well at night" stock in a market that rewarded "get rich or die trying." But the discipline had a payoff that was not yet visible: Heritage was building a deposit franchise of exceptional quality. Its depositors were local business owners who had been with the bank for years, sometimes decades. They were not going to pull their money because of a tweet or a WhatsApp panic. They were sticky, in banking parlance, and sticky deposits are worth their weight in gold when the tide goes out.

Heritage found its niches in the spaces between the giants. Businesses too small for SVB's attention, too boring for the tech-focused banks, too sophisticated for the credit unions. The competitive advantage was not scale or technology or brand recognition. It was speed. Heritage could make a lending decision in days that would take Bank of America weeks and Wells Fargo months. For a small business owner who needed a credit line to close on a piece of equipment or a commercial property, that speed was more valuable than any mobile banking app.

There is a concept in competitive strategy called counter-positioning, and Heritage embodied it perfectly during this period. Counter-positioning occurs when a new entrant or smaller competitor adopts a business model that the incumbent cannot copy because copying it would cannibalize its existing business. In Heritage's case, the counter-positioning was inverted: Heritage's relationship-heavy, labor-intensive, conservative model was something that SVB could not adopt because SVB's economics and growth expectations demanded a very different approach. SVB's investors wanted forty percent deposit growth and venture debt market share. Heritage's investors wanted steady dividends and pristine credit quality. Both models were internally consistent. But only one would survive the test of a real crisis.

The other dimension of competition that mattered during this period was the creeping threat from credit unions and from the growing universe of non-bank lenders. Companies like OnDeck and Fundbox were offering small business loans with rapid online applications, competing directly for the working capital lending that had traditionally been community bank territory. Heritage's response was to compete not on speed of application but on quality of relationship: an online lender could approve a fifty thousand dollar line of credit in minutes, but it could not provide the ongoing advisory relationship, the deep understanding of the borrower's business, and the flexibility to restructure terms when circumstances changed. Whether that distinction would remain meaningful to the next generation of business owners was an open question.

VII. The 2020s: Pandemic, Digital Disruption, and M&A Strategy

When COVID-19 hit in March 2020, community banks across America faced a moment of truth. Their small business clients, the ones they had cultivated relationships with for years, were in immediate, existential danger. For Heritage, the pandemic was both a crisis and a vindication of the relationship model.

Heritage Bank of Commerce threw itself into Paycheck Protection Program lending with an intensity that reflected its mission. In the first round alone, the bank processed 1,105 PPP loan applications with total principal balances of $333.4 million, a staggering volume for a bank of its size. By the second round in 2021, combined PPP balances stood at $286.5 million. These were not just numbers on a balance sheet. Each of those eleven hundred loans represented a small business, a team of employees, a family's livelihood. The fee income was welcome, but the real value was the deepened relationships: business owners who would remember that Heritage was there when they needed a bank the most.

The pandemic operating environment tested Heritage's digital capabilities, which were adequate but not exceptional. The bank offered online banking, mobile banking, remote deposit capture, and the standard suite of digital tools, but it was never going to win a technology comparison against the fintechs or the big nationals. Heritage's technology investment of approximately $12.3 million in 2023 was modest by industry standards. The bank's strategy was to be tech-enabled but human-led, using technology as a tool to enhance relationships rather than replace them.

The fintech threat was real and growing. Square, Stripe, and the neobanks like Mercury and Brex were offering business banking products that were faster, sleeker, and more convenient than anything a community bank could match. But Heritage's leadership recognized a crucial distinction: fintechs were excellent at payments, at interfaces, at the transactional layer of banking. What they could not do was sit across a table from a business owner, understand the nuances of a complicated real estate deal, and structure a loan that reflected the borrower's specific circumstances. The human element, the judgment, the relationship, that was the moat.

The M&A strategy accelerated through this period. In 2018, Heritage completed two acquisitions: Tri-Valley Bank, which brought branches in San Ramon and Livermore, and United American Bank in San Mateo, a deal valued at approximately $44.2 million. But the crown jewel was the 2019 acquisition of Presidio Bank, a San Francisco-headquartered commercial bank with offices in Palo Alto, San Mateo, San Rafael, and Walnut Creek. The Presidio deal was valued at approximately $200.3 million in an all-stock transaction, and it was transformative. It pushed Heritage's combined assets to approximately $4.1 billion, gave it a presence in San Francisco and Marin County, and expanded the branch network to seventeen locations across the Bay Area.

There was a certain symmetry to the Presidio acquisition. Clay Jones, who would eventually become Heritage's CEO, had come from Presidio Bank, where he had served as President. When Heritage acquired Presidio, it also acquired Jones, who joined as Executive Vice President and was soon elevated to President and COO. This turned out to be an exceptionally consequential hire, as the bank would need new leadership sooner than anyone expected.

There was a certain symmetry to the Presidio acquisition that revealed something about Heritage's talent strategy. Presidio's team brought deep relationships in San Francisco and the Peninsula, markets that Heritage had not previously served. By acquiring the bank, Heritage acquired not just the balance sheet but the bankers, the relationships, and the institutional knowledge that Presidio had built. This approach, growing by acquiring teams and portfolios rather than trying to build organically in new markets, had become Heritage's primary growth model, and it had worked well.

The talent wars of the Bay Area presented a persistent challenge. Silicon Valley is one of the most expensive labor markets in the world, and Heritage was competing for experienced commercial bankers against not only other banks but also the tech companies and fintechs that could offer equity compensation that a community bank simply could not match. The bank's efficiency ratio, the measure of how much it costs to generate a dollar of revenue, was always under pressure from these labor costs, a structural disadvantage of operating in an expensive market.

The leadership disruption of 2021 added an unexpected chapter to this period. Keith Wilton, who had succeeded Kaczmarek as CEO in August 2019, stepped down on March 12, 2021, after less than two years in the role. The departure was abrupt; the company's press release was terse, and Wilton also resigned from the board. Heritage's response was pragmatic and revealing: it brought Walter Kaczmarek out of retirement to serve as interim CEO, a move that American Banker noted was unusual. Kaczmarek's return provided stability during a turbulent moment, and he continued in the interim role until September 2022, when Clay Jones, who had been serving as President and COO, was formally named President and CEO. The succession saga, from Kaczmarek to Wilton to Kaczmarek again to Jones, was messier than Heritage's carefully cultivated image of stability might suggest, but the bank's operational performance remained solid throughout, a testament to the strength of the institution rather than any single individual.

VIII. March 2023: The SVB Collapse and Heritage's Moment

On the morning of Friday, March 10, 2023, Silicon Valley Bank was seized by regulators in what would become the second-largest bank failure in American history. The speed of the collapse was breathtaking. Just forty-eight hours earlier, SVB had announced a capital raise to shore up its balance sheet. The announcement triggered a panic among its depositor base, the very VC firms and tech startups that had made SVB great. Forty-two billion dollars in deposits were withdrawn in a single day. The bank run that regulators and academics had theorized about for decades had happened, not through lines of anxious depositors outside bank branches, but through mobile banking apps and wire transfers executed in minutes.

For Heritage Commerce Corp, sitting just a few miles from SVB's headquarters in Santa Clara, the weekend that followed was one of the most intense in its history. The immediate fear was contagion. Heritage was not SVB, its business model was fundamentally different, its risk profile was incomparable, but the market did not care about nuance. In the eyes of investors and, more dangerously, depositors, Heritage was a regional bank in Silicon Valley, and regional banks in Silicon Valley were failing. The stock dropped from approximately thirteen dollars per share in January 2023 to a low of just under seven dollars, a decline of roughly forty-six percent.

The Heritage team went into crisis management mode. Customer communication was paramount. Heritage's bankers, the same people who had been building relationships with business owners for years and decades, reached out to their clients directly. The message was straightforward: Heritage is not SVB. Our deposit base is different. Our balance sheet is different. Our risk profile is different. And crucially, we are here to answer your questions and help you through this.

The numbers backed up the message. At the time of SVB's collapse, Heritage's unrealized losses on its securities portfolio were approximately ninety million dollars, representing about ten percent of total shareholders' equity. SVB, by contrast, had nearly sixteen billion dollars in unrealized losses that exceeded its entire equity value. The difference was staggering and reflected fundamentally different approaches to balance sheet management. Heritage had been conservative in the duration and composition of its securities portfolio, avoiding the long-dated government bonds that had destroyed SVB's balance sheet when interest rates rose.

The deposit dynamics were equally revealing. SVB's deposits were concentrated in a small number of very large accounts, overwhelmingly from VC-backed companies, with an estimated ninety-four percent uninsured. Heritage's deposits, while still carrying a significant uninsured ratio of sixty-four percent at year-end 2022, were spread across thousands of small business relationships, with the top one hundred client relationships representing about fifty percent of total deposits and an average account size of $445,000. More importantly, Heritage's depositors were not all connected through the same social networks. A contractor in San Jose and a dental practice in Fremont do not exchange panicked WhatsApp messages about their bank's solvency.

The result was remarkable. In the first quarter of 2023, the very quarter in which SVB collapsed and Signature Bank and First Republic followed, Heritage's total deposits actually increased by $54.9 million, or one percent. The bank brought $128 million of off-balance sheet relationship-based client deposits onto its balance sheet and saw net client deposit growth of $145.8 million. In a quarter defined by bank runs and deposit flight, Heritage's deposits went up.

Heritage also took proactive steps to shore up its liquidity position. It increased its credit line availability from the Federal Reserve Bank and the Federal Home Loan Bank by $839.5 million, bringing total borrowing capacity to over two billion dollars. It borrowed $150 million from each institution as a precautionary measure and to "test the lines for future contingency planning purposes." Both lines were repaid in full by April 20, 2023.

The deposit composition shifted dramatically in the months that followed. ICS and CDARS deposits, reciprocal deposit products that provide full FDIC insurance coverage by spreading deposits across multiple banks, exploded from $30.4 million at year-end 2022 to $854.1 million by year-end 2023. The uninsured deposit ratio declined from sixty-four percent to forty-six percent. Heritage's depositors wanted to stay, but they wanted full insurance coverage, and Heritage gave them the tools to get it.

The credit rating agency KBRA affirmed all of Heritage's ratings in May 2023, just two months after SVB's collapse, citing "the Bank's conservative approach to liquidity and capital management and the stability of its core deposit balances in the first quarter of 2023 compared to year-end 2022." The senior unsecured debt rating of BBB+ and bank deposit rating of A- were maintained with a stable outlook. It was a powerful validation from an independent arbiter.

For Heritage, the SVB collapse was a vindication of forty years of strategic discipline. Every decision that had seemed overly conservative, every growth opportunity that had been passed up, every dollar of potential tech banking revenue that had been left on the table, all of it was justified in a single weekend. Boring banking, it turned out, was not just a strategy. It was a survival mechanism.

The stock market recovery was gradual. HTBK did not snap back to its pre-crisis levels quickly; the regional banking stigma lingered for months, and the broader market continued to treat all smaller banks with suspicion. But the business fundamentals told a different story. For full-year 2023, Heritage reported net income of $64.4 million, or $1.05 per share, only modestly below the prior year's $66.6 million. Tangible book value grew nine percent year-over-year. In a year defined by the worst banking crisis since 2008, Heritage delivered stable earnings and growing book value. That is the kind of performance that separates genuine franchise value from momentum.

The post-SVB world created both opportunities and challenges. Heritage was well-positioned to capture displaced customers, and the deposit account growth in the quarters that followed suggested it was doing exactly that. But the competitive landscape had also shifted: JPMorgan Chase, which acquired First Republic Bank's assets in May 2023, became an even more dominant force in Bay Area banking, combining its massive national platform with First Republic's wealthy clientele and relationship-oriented model. The large national banks experienced a surge of deposits as panicked customers fled smaller institutions for the perceived safety of "too big to fail." Heritage's ability to hold and grow its deposit base in this environment was a testament to the genuine stickiness of its relationships, but the competitive intensity had ratcheted up significantly.

Heritage Bank of Commerce was subsequently named to Forbes' 2026 America's Best Banks list, ranking among the top one hundred banks and earning the number one position in credit quality, measured by the percentage of assets classified as nonperforming. The bank also maintained its Five Star rating from Bauer Financial and was ranked twenty-fifth on S&P Global Market Intelligence's Top 50 list of best-performing community banks. In 2024, it had been named one of Forbes' World's Best Banks, ranking tenth among sixty-eight banks recognized in the United States. These are not vanity awards. They are the market recognizing what Heritage's balance sheet has been saying for years: this is an exceptionally well-run bank.

IX. Today and The Future: AI, Fintech, and Community Banking's Next Chapter

Heritage Commerce Corp entered 2026 in a position of quiet strength. The full-year 2025 results told the story: total assets of $5.76 billion, total deposits of $4.90 billion, total loans of $3.65 billion. Net income was $47.8 million, or $0.78 per diluted share on a reported basis, and $56.4 million, or $0.91 per share, on an adjusted basis after excluding the impact of a $9.2 million legal settlement and $2.1 million in merger-related costs. The net interest margin expanded to 3.56 percent for the full year, with the fourth quarter coming in at a robust 3.72 percent, reflecting the benefits of a lower interest rate environment on funding costs.

The credit quality metrics remained exceptional. Nonperforming assets stood at just $2.78 million, representing five basis points of total assets, an almost impossibly low level for a bank of any size. Net charge-offs in the fourth quarter were thirty-eight thousand dollars. Not thirty-eight million. Thirty-eight thousand. This is the legacy of the credit culture forged in the crucible of 2008-2010, embedded in every underwriting decision, every loan committee discussion, every relationship manager's daily work.

The loan portfolio reflects Heritage's strategic positioning. Commercial real estate, both owner-occupied and non-owner-occupied, constitutes approximately fifty-seven percent of total loans, a concentration that is typical for community banks but one that regulators and analysts watch closely. Commercial and industrial loans represent fifteen percent, residential mortgages twelve percent, and the remainder is spread across multifamily, construction, home equity, and consumer loans. Heritage is an SBA Preferred Lender, though the SBA portfolio is a relatively small piece of the total.

The modern Heritage operates with about three hundred and fifty employees across sixteen branches. The geographic footprint spans the Bay Area from San Rafael in Marin County to Hollister in the south, with offices in San Jose, San Francisco, Palo Alto, Oakland, Fremont, and a string of East Bay communities. It is a concentrated footprint, which is both a strength and a vulnerability: the Bay Area is one of the wealthiest and most economically dynamic markets in the world, but concentration in a single region means concentration in a single real estate market and a single economic cycle.

The biggest strategic question facing Heritage, however, has already been answered. On December 17, 2025, Heritage Commerce Corp and CVB Financial Corp, the parent company of Citizens Business Bank, announced a definitive agreement to merge. The deal is structured as an all-stock transaction valued at approximately $811 million, with Heritage shareholders receiving 0.65 shares of CVBF stock for each HTBK share, implying a price of approximately $13 per HTBK share at announcement. The combined entity will have approximately twenty-two billion dollars in assets and more than seventy-five offices across California, with Heritage shareholders owning roughly twenty-three percent of the combined company.

The merger represents the culmination of a strategic arc that has been building for years. CVB Financial, headquartered in Ontario, California, is a Southern California-based community bank with a similar culture and focus on business banking. Clay Jones, Heritage's CEO, will become President of the combined company, and two Heritage directors will join the CVB board. The deal is expected to close in the second quarter of 2026, pending regulatory and shareholder approvals.

The question of whether Heritage should have remained independent will be debated by its shareholders and by community banking observers for years. The bull case for independence was strong: exceptional credit quality, an established franchise in a wealthy market, a validated business model. But the bear case was equally compelling: at roughly six billion dollars in assets, Heritage was approaching the scale at which technology investment requirements, regulatory compliance costs, and competitive pressures make independence increasingly difficult. The merger with CVB gives Heritage the scale it needs while preserving the relationship-driven culture that made it successful.

The management transition deserves a note. Clay Jones, who had led the bank through the SVB crisis and the CVB merger negotiations, had assembled a new executive team that reflected Heritage's strategic priorities. Thomas Sa, formerly CFO at both California BanCorp and Bridge Capital Holdings, joined as Chief Operating Officer in October 2024 and assumed interim CFO duties when long-serving CFO Lawrence McGovern departed after twenty-six years with the company. Janisha Sabnani, a former Skadden Arps corporate attorney and First Republic Bank veteran, was hired as General Counsel in February 2025. And in August 2025, Christopher Abate, the CEO of Redwood Trust with deep experience in real estate finance, joined the board. The board itself underwent a generational transition, with Julianne Biagini-Komas, a CPA who had chaired the Audit Committee since 2020, replacing Jack Conner as Board Chair in May 2025. Conner, who had served as Chairman for nearly two decades, transitioned to Chair Emeritus. These moves suggest a bank that was actively preparing itself for the next chapter, whether that chapter involved independence or partnership.

The AI era presents a fascinating challenge for Heritage's model. Algorithmic underwriting, which uses machine learning to assess credit risk, has the potential to erode one of community banking's core advantages: the ability of experienced bankers to make nuanced lending decisions based on personal knowledge and professional judgment. If an algorithm can assess a small business loan as accurately as a twenty-year veteran relationship manager, the labor-intensive community banking model becomes significantly harder to justify economically. Heritage's bet, and the bet of community banks everywhere, is that the algorithm cannot fully replicate the human element, that there will always be deals where context, character, and relationship matter more than data. Whether that bet pays off will determine the future of community banking in America.

X. Business Model Deep Dive and Playbook

The unit economics of community banking are deceptively simple in theory and fiendishly difficult in practice. A bank takes in deposits, pays depositors an interest rate, lends that money out at a higher interest rate, and earns the spread. The difference between the rate earned on loans and the rate paid on deposits is the net interest margin, and it is the lifeblood of any commercial bank. Heritage's NIM expanded from approximately 3.25 percent in 2024 to 3.56 percent in 2025, with the fourth quarter reaching 3.72 percent, reflecting the benefit of declining funding costs as interest rates came down.

But NIM alone does not tell you whether a bank is profitable. You also need to understand the efficiency ratio, which measures noninterest expense as a percentage of total revenue. Think of it as the bank's operating leverage. Heritage's reported efficiency ratio for full-year 2025 was 64.75 percent, elevated by one-time items; the adjusted efficiency ratio was a more respectable 59.05 percent, with the fourth quarter adjusted ratio coming in at 54.04 percent. In community banking, an efficiency ratio below sixty percent is considered good, and below fifty-five percent is considered excellent. Heritage has been moving in the right direction, but the expensive Bay Area labor market is a persistent headwind.

The third critical variable is credit losses, and this is where Heritage truly distinguishes itself. Charge-offs consume margin, and a single bad loan can wipe out the profit from dozens of good ones. Heritage's charge-off history over the past several years has been essentially zero, a testament to the underwriting discipline forged during the financial crisis. Nonperforming assets at five basis points of total assets is not just good; it is among the best in the entire American banking industry. Forbes ranked Heritage number one in credit quality among the two hundred largest publicly traded banks in its 2026 America's Best Banks list. That ranking is the single most powerful testament to the value of Heritage's relationship lending model: when you know your borrowers deeply, you make better lending decisions.

The deposits franchise is the real moat. Heritage's deposits at year-end 2025 totaled $4.90 billion, with noninterest-bearing demand deposits representing approximately twenty-seven percent of the total. These are deposits for which the bank pays nothing. They exist because businesses need checking accounts, and Heritage has earned the right to hold those checking accounts through years of relationship building. The value of low-cost deposits in a rising rate environment is enormous, because they allow the bank to earn a wider spread without raising its funding costs. The shift in deposit composition over the past three years, with ICS and CDARS products now representing over a billion dollars, reflects a more insured deposit base, which is both a strength (stability) and a cost (reciprocal deposits typically carry slightly higher rates than traditional deposits).

Heritage's specific playbook has several distinctive elements. The "banker as advisor" model means that relationship managers are not just loan salespeople. They are expected to understand their clients' businesses well enough to provide advice on cash management, growth financing, and even operational challenges. This is a higher-cost model than transaction banking, but it creates deeper client loyalty and higher cross-sell ratios.

The capital allocation philosophy has been conservative and consistent. Heritage has paid a quarterly dividend of $0.13 per share since 2020, representing a yield of approximately four percent at current prices. The bank has maintained capital ratios well above regulatory minimums, with a CET1 ratio of 12.9 percent and total capital ratio of 15.1 percent at year-end 2025. A fifteen million dollar share repurchase program was also in place. The conservative capital management reflects the lessons of 2008: when you need capital the most, it is the hardest to get. Heritage's capital ratios at year-end 2025 told the story: CET1 at 12.9 percent, total capital at 15.1 percent, Tier 1 leverage at 9.6 percent, all well above the "well-capitalized" regulatory thresholds. The tangible common equity ratio stood at 9.59 percent, providing a significant buffer against potential losses.

One element of Heritage's playbook that deserves special attention is its approach to CRE concentration. At year-end 2025, commercial real estate loans represented approximately fifty-seven percent of total loans and stood at roughly three hundred and nineteen percent of total risk-based capital. Regulatory guidance, established jointly by the OCC, FDIC, and Federal Reserve in 2006, flags CRE concentrations above three hundred percent of risk-based capital as warranting heightened supervisory attention. Heritage operates above this threshold, which is not unusual for community banks but does invite additional regulatory scrutiny and requires robust risk management processes. The bank has managed this concentration by maintaining tight underwriting standards, diversifying within CRE across property types and geographies, and building loan loss reserves that have proven more than adequate over multiple economic cycles.

XI. Competitive Analysis: Porter's Five Forces and Hamilton's Seven Powers

To understand Heritage's competitive position, it helps to apply the two most powerful frameworks in strategic analysis: Michael Porter's Five Forces and Hamilton Helmer's Seven Powers.

Starting with the threat of new entrants: the barriers to entering banking are substantial. Getting a bank charter in the post-2008 regulatory environment is extraordinarily difficult. Capital requirements are significant, regulatory compliance is expensive, and the FDIC insurance system creates an incumbent advantage. However, the fintech revolution has introduced a class of competitors that bypass traditional banking regulations entirely. Companies like Brex and Mercury offer business banking products without being regulated as banks, giving them structural cost advantages and regulatory flexibility that traditional banks cannot match. Heritage's defense is its forty-year track record, its FDIC insurance, and the trust that comes with being a regulated, transparent institution.

The bargaining power of suppliers, meaning depositors, fluctuates with the interest rate environment. In a low-rate world, depositors have few alternatives and banks enjoy wide margins. In the high-rate environment of 2022-2024, depositors gained significant power, demanding higher rates and threatening to move their money to money market funds or Treasury bills. The SVB crisis created a test of deposit stickiness that Heritage passed emphatically, but the broader trend toward depositor empowerment through digital banking and easy account switching is real and ongoing.

The bargaining power of buyers, meaning borrowers, is moderate to high. Small business borrowers have more options than ever: big banks, credit unions, fintechs, non-bank lenders, private credit funds. Comparison shopping is easier than at any point in banking history. Heritage's advantage is that small business borrowers are less rate-sensitive than they are service-sensitive. A business owner who needs a two million dollar credit line cares more about whether the bank understands their business and can move quickly than whether the rate is twenty-five basis points lower at a competitor.

The threat of substitutes is high and growing. Fintechs are eating into the transactional layer of business banking. Non-bank lenders are competing aggressively in working capital and term lending. Private credit funds are moving down-market into deals that were once the exclusive domain of community banks. But what these substitutes cannot replicate is the human judgment and relationship understanding that Heritage brings to complex lending decisions. When a borrower needs a construction loan with a complicated draw schedule, or a line of credit secured by a mixed-use commercial property, they still need a banker who understands the deal, not an algorithm.

Rivalry among existing competitors is intense, particularly in the Bay Area. The competitive field includes the national giants (Wells Fargo, Bank of America, JPMorgan Chase post-First Republic), other community banks, credit unions, and the growing fintech sector. Post-SVB, the competition for stable, relationship-based deposits has intensified. Banks that can offer the combination of personal service, competitive products, and full FDIC insurance coverage are in a strong position, and Heritage is among them.

Turning to Hamilton Helmer's Seven Powers framework, which asks what gives a company durable competitive advantage, the picture for Heritage is nuanced. Scale economies are weak because community banks inherently do not benefit much from scale. Technology costs are somewhat fixed, but the primary costs of branch operations and personnel scale linearly with growth. Heritage's asset base may be subscale for the technology investments needed to compete with larger institutions, which is one reason the CVB merger makes strategic sense.

Network effects are essentially nonexistent in traditional banking. Each customer relationship is independent, and the bank does not become more valuable as more customers join. Counter-positioning is moderate and historically significant. Heritage's relationship model was counter-positioned against the big banks' transactional model, and its boring banking strategy was counter-positioned against SVB's innovation banking model. The 2023 SVB collapse validated this counter-positioning dramatically, proving that disciplined, conservative banking has enduring value.

Switching costs are moderate. Business banking involves deeper integration than consumer banking through treasury management systems, established credit facilities, relationship history, and the personal connections between bankers and business owners. These switching costs are meaningful but not insurmountable, and digital banking is gradually lowering them. Branding power is weak; Heritage is not a household name, though the "Heritage" brand does suggest stability and tradition, attributes that gained new currency after the SVB collapse.

The cornered resource power is weak to moderate. Heritage has experienced commercial bankers with deep Bay Area relationships, forty years of customer history, and proprietary knowledge of local markets. These are valuable resources, but they are poachable by competitors willing to pay market rates. Process power is moderate: the credit culture, underwriting expertise, relationship management processes, and local decision-making authority structure that Heritage has built over decades are real sources of advantage, but they are not impossible for competitors to replicate given sufficient time and investment.

The overall assessment is that Heritage's competitive position is fragile but defensible in specific niches. The primary powers are process power, rooted in credit discipline and relationship management, combined with moderate switching costs and a proven counter-positioning against both large banks and innovation-focused banking models. The 2023 SVB collapse provided the ultimate market test of Heritage's counter-positioning, and the bank passed emphatically. But the absence of strong scale economies and network effects means that Heritage's advantages are inherently local and relationship-dependent, which limits the bank's ability to grow rapidly or expand geographically without diluting its competitive position.

The existential question, now answered by the CVB merger, was whether these powers were sufficient to sustain independence in an increasingly digital and scale-driven banking environment. The merger represents a pragmatic acknowledgment that process power and switching costs, while valuable, are not sufficient to offset the structural disadvantages of subscale technology investment and limited geographic diversification. The combined CVB-Heritage entity, with twenty-two billion dollars in assets, will have a stronger platform from which to compete, but the challenge of preserving Heritage's relationship-driven culture within a larger organization is significant and historically difficult for acquiring banks to achieve.

XII. Bull vs. Bear Case

The bull case for Heritage Commerce Corp rests on several interlocking pillars, each reinforced by recent events. The business model has been validated in the most dramatic way possible. When SVB collapsed, Heritage's deposits went up. That single data point is worth more than a hundred analyst reports because it demonstrates, in real-time crisis conditions, that relationship banking and conservative balance sheet management create a deposit franchise of genuine durability.

The credit quality is not just good; it is among the best in the country. Forbes' ranking as number one in credit quality is a market signal that should not be dismissed. In banking, the primary way you destroy shareholder value is through credit losses, and Heritage has essentially eliminated them. The discipline required to maintain near-zero charge-offs across an economic cycle, including a pandemic and a regional banking crisis, reflects an institutional culture that is genuinely difficult to replicate.

The Bay Area market, despite its high costs, remains one of the wealthiest and most economically vibrant in the world. Heritage's established presence and deep business networks in this market constitute a franchise that took decades to build and cannot be easily recreated. The management team under Clay Jones has demonstrated stability and competence, and the recent executive hires, including a former First Republic Bank general counsel, suggest a bank that is continuing to attract quality talent.

The pending merger with CVB Financial adds a strategic dimension. At an implied value of approximately $13 per share, the deal provides Heritage shareholders with a path to participation in a larger, more diversified California business bank with twenty-two billion dollars in assets and the scale to invest in technology and compete more effectively. The deal is expected to be thirteen percent accretive to CVB's earnings per share in 2027, with tangible book value dilution of 7.7 percent and an earnback period of approximately two and a half years. The internal rate of return was projected at approximately twenty percent, suggesting meaningful value creation potential for both sets of shareholders.

The advisory roster on the deal was notable for a community bank transaction. Heritage was advised by Piper Sandler and Wachtell, Lipton, Rosen and Katz, the premier mergers and acquisitions law firm in the country. CVB was advised by J.P. Morgan and Manatt, Phelps and Phillips. The caliber of the advisors reflected the significance of the transaction and Heritage's determination to maximize shareholder value.

The bear case begins with scale. At roughly six billion dollars in assets, Heritage was arguably subscale for the technology investments required to compete in modern banking. The efficiency ratio, while improving, remained above many peers, partly reflecting the high cost of operating in Silicon Valley. Geographic concentration is both a strength and a vulnerability. A significant Bay Area real estate downturn or a tech industry recession would disproportionately impact Heritage's portfolio, particularly given that commercial real estate represents fifty-seven percent of total loans, with CRE standing at approximately three hundred and nineteen percent of total risk-based capital, a level that invites regulatory attention.

Net interest margin compression during the rising rate environment of 2022-2024 demonstrated Heritage's vulnerability to funding cost pressures. As deposits shifted from noninterest-bearing to interest-bearing accounts, and as depositors demanded higher rates for their loyalty, margins compressed significantly. Full-year 2024 net income dropped thirty-seven percent from 2023 levels, a painful decline that underscored the rate sensitivity of the business model.

The fintech disruption threat is not hypothetical. Younger business owners increasingly prefer digital-first banking experiences, and the community bank value proposition of personal relationships may resonate less strongly with a generation that grew up managing their finances on their phones. Regulatory burden continues to disproportionately affect smaller banks, creating a structural incentive toward consolidation.

There is a myth versus reality dimension to the bear case that is worth addressing directly. The popular narrative in banking is that community banks are a dying breed, inevitably destined to be absorbed into larger institutions or rendered obsolete by fintech disruption. The reality, as Heritage's story demonstrates, is more nuanced. Community banks that serve specific geographic and industry niches with genuine expertise and relationship depth continue to generate attractive returns and maintain loyal customer bases. The question is not whether community banking has value, it clearly does, but whether that value can be captured efficiently enough to justify the overhead of a standalone public company. Heritage's decision to merge suggests its board concluded that the answer, for a bank of its specific size and market position, was no.

The deposit growth trajectory deserves particular scrutiny. Heritage grew deposits ten percent year-over-year in 2024, a remarkable pace for a community bank in a competitive market. Total deposits reached $4.90 billion at year-end 2025, up from $4.38 billion at year-end 2023. But the composition of those deposits has changed meaningfully. Noninterest-bearing deposits, which are free funding for the bank, declined from approximately thirty-nine percent of total deposits at year-end 2022 to approximately twenty-seven percent at year-end 2025, reflecting the industry-wide migration into interest-bearing accounts. The growth of ICS and CDARS deposits to over one billion dollars has provided insurance stability but at a higher cost than traditional deposits. The net interest margin, while expanding recently, remains sensitive to the rate environment and the ongoing competition for deposits.

For investors evaluating Heritage, particularly in the context of the pending CVB merger, the critical KPIs to monitor are: the net interest margin trend, which is the core profitability driver that tells you whether the bank can earn an adequate spread between lending and funding costs; and nonperforming assets as a percentage of total assets, the early warning system for credit quality deterioration where Heritage has been exceptional. These two metrics, tracked over the coming quarters, will tell the story of whether boring banking can thrive at a larger scale, or whether the magic was specific to Heritage's independent, community-focused model.

XIII. Epilogue and Reflections

The story of Heritage Commerce Corp is, at its core, a story about the power of knowing what not to do. In a market that celebrates disruption, that rewards speed and scale and audacity, Heritage built a forty-year franchise by being deliberate, by being conservative, and by being deeply, almost stubbornly, committed to relationships over transactions.

The leadership succession tells its own story about institutional resilience. From William Del Biaggio Jr.'s founding vision through Jack Conner's nearly two decades as chairman, from Walter Kaczmarek's steady hand through the financial crisis to Clay Jones's leadership through the SVB collapse and the CVB merger, Heritage has benefited from leaders who understood the institution's DNA and protected it, even when the market was rewarding different choices.

The resilience through multiple crises is perhaps the most remarkable aspect of the Heritage story. The S&L crisis aftermath. The dot-com bust. A fraud scandal involving the founder's own son. The worst financial meltdown since the Depression. A global pandemic. The collapse of the most iconic bank in Silicon Valley. Heritage survived them all, not through luck or government largesse (though TARP certainly helped during the darkest days), but through a consistent set of principles: know your customers, manage your risks, maintain adequate capital, and resist the temptation to be something you are not.

The community bank paradox is alive and well at Heritage. This is a deeply human business operating in an increasingly digital world, and the tension between those two realities is real and unresolved. The relationship model creates extraordinary credit quality and deposit stickiness. But it is expensive, it is difficult to scale, and it relies on a declining resource: experienced bankers who have the skill and the patience to build genuine relationships with business owners.

The decision to merge with CVB Financial represents Heritage's answer to that paradox: scale up, combine the relationship model with a larger platform, and try to preserve the culture that made Heritage special while gaining the resources and reach that independence could not provide. Whether that proves to be the right call will depend on execution, on whether the combined entity can retain the Heritage bankers and the Heritage clients who made the franchise valuable in the first place.

For founders and operators, the Heritage story offers a powerful lesson in strategic patience. In a world of blitzscaling and growth-at-all-costs, Heritage built a durable franchise by compounding relationships and reputation over four decades. The returns were not spectacular in any single year, but the cumulative effect was extraordinary: a bank that was ranked number one in America for credit quality, that survived every crisis thrown at it, and that ultimately commanded an eight-hundred-million-dollar valuation from a buyer who recognized the value of what Heritage had built.

For investors, the lesson is equally clear. Sometimes boring is beautiful. The sexiest investments in banking during the 2010s were the high-growth disruptors: the SVBs, the First Republics, the fintechs. Most of those stories ended in tears. Heritage, the boring little community bank that nobody wrote breathless articles about, survived them all. There is a kind of crisis alpha that comes not from brilliant trades or innovative products, but simply from avoiding blow-ups. Heritage mastered that art.

The unanswered question, the one that the CVB merger will not fully resolve, is whether community banking is a dying business model or an enduring one that simply looks different in the digital age. Heritage's story suggests the latter, but with a caveat: the scale required to deliver relationship banking profitably keeps going up, and the competitive threats keep multiplying. The community bank of 2026 looks very different from the one William Del Biaggio Jr. founded in downtown San Jose in 1994, and the one that exists in 2036 will look different still.

What will not change, if Heritage's story is any guide, is the fundamental insight at the heart of the model: that businesses need banks that understand them, and that understanding cannot be automated, outsourced, or disrupted. It can only be earned, one relationship at a time.

XIV. Links and References

Top 10 Long-Form Resources:

- Heritage Commerce Corp Investor Relations (heritagecommercecorp.com) - 10-Ks, proxy statements, earnings transcripts, and press releases going back decades

- FDIC Bank Data and Statistics - Heritage's call reports, peer comparisons, and historical industry data

- Federal Reserve Report on the March 2023 Banking Crisis - The definitive analysis of SVB's failure and its systemic implications

- FDIC Community Banking Study - Long-term trends, challenges, and the evolving role of community banks in the American financial system

- S&P Global Market Intelligence - Regional bank sector analysis, Heritage Commerce coverage, and peer comparison tools

- American Banker archives - Decades of coverage of Bay Area banking, Heritage's acquisitions, and leadership transitions

- Federal Reserve Bank of San Francisco Economic Research - Bay Area economy, banking sector dynamics, and regional economic analysis

- ProPublica Eye on the Bailout - Comprehensive TARP tracking database with Heritage's complete government aid and repayment history

- Heritage Commerce Corp SEC Filings (SEC EDGAR) - Proxy statements, 8-Ks, governance documents, and material event disclosures

- Seeking Alpha and earnings call transcripts - Management's own words on strategy, competitive positioning, and forward outlook

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube