HealthStream Inc.: Building Healthcare's Essential Infrastructure — One Learner at a Time

I. Introduction & Episode Roadmap

There is a company in Nashville, Tennessee, that most investors have never heard of, yet it quietly touches the professional lives of over five million healthcare workers across the United States. Every time a nurse completes a mandatory compliance module, every time a hospital credentials a new surgeon, every time a shift schedule gets published at a medical center — there is a reasonable chance that HealthStream's software is somewhere in the loop.

The company generated approximately $304 million in revenue in 2025, growing steadily if unspectacularly, while maintaining gross margins north of sixty percent and carrying zero long-term debt.

The central question of this deep dive is deceptively simple: how did a Nashville startup, founded in 1990 before the commercial internet even existed, become the backbone of healthcare workforce training in America? And more provocatively — is the most interesting chapter of the HealthStream story still ahead?

This is a company built on three interlocking themes.

First, platform effects: HealthStream has spent three decades assembling a suite of products that are individually useful but collectively create an ecosystem that becomes very difficult for customers to leave.

Second, founder-led vision: Bobby Frist has been CEO for thirty-five years, a tenure that would be remarkable in any industry but is almost unheard of in technology.

Third, navigating healthcare's complexity: this is a sector where regulatory requirements create mandatory demand, where sales cycles are measured in quarters not weeks, and where switching costs are embedded not just in contracts but in deeply integrated workflows.

What makes HealthStream fascinating from an investor's perspective is that it sits at the intersection of several powerful secular trends — the chronic nursing shortage, the digitization of healthcare operations, the regulatory intensification of the post-pandemic era — while operating in a business that most people would describe as "unsexy."

Compliance training. Credentialing software. Shift scheduling.

These are not the categories that generate breathless coverage on CNBC. But they are the categories that generate durable, recurring revenue with high switching costs and genuine mission criticality. Hospitals cannot operate without trained, credentialed, and scheduled staff. Full stop.

The story that follows covers thirty-five years of patient capital allocation, a near-death experience during the dot-com bust, a decade-long acquisition spree that transformed the company's product footprint, and a current strategic pivot toward becoming a true platform company — a transition that, if executed successfully, could fundamentally change HealthStream's growth trajectory and competitive moat.

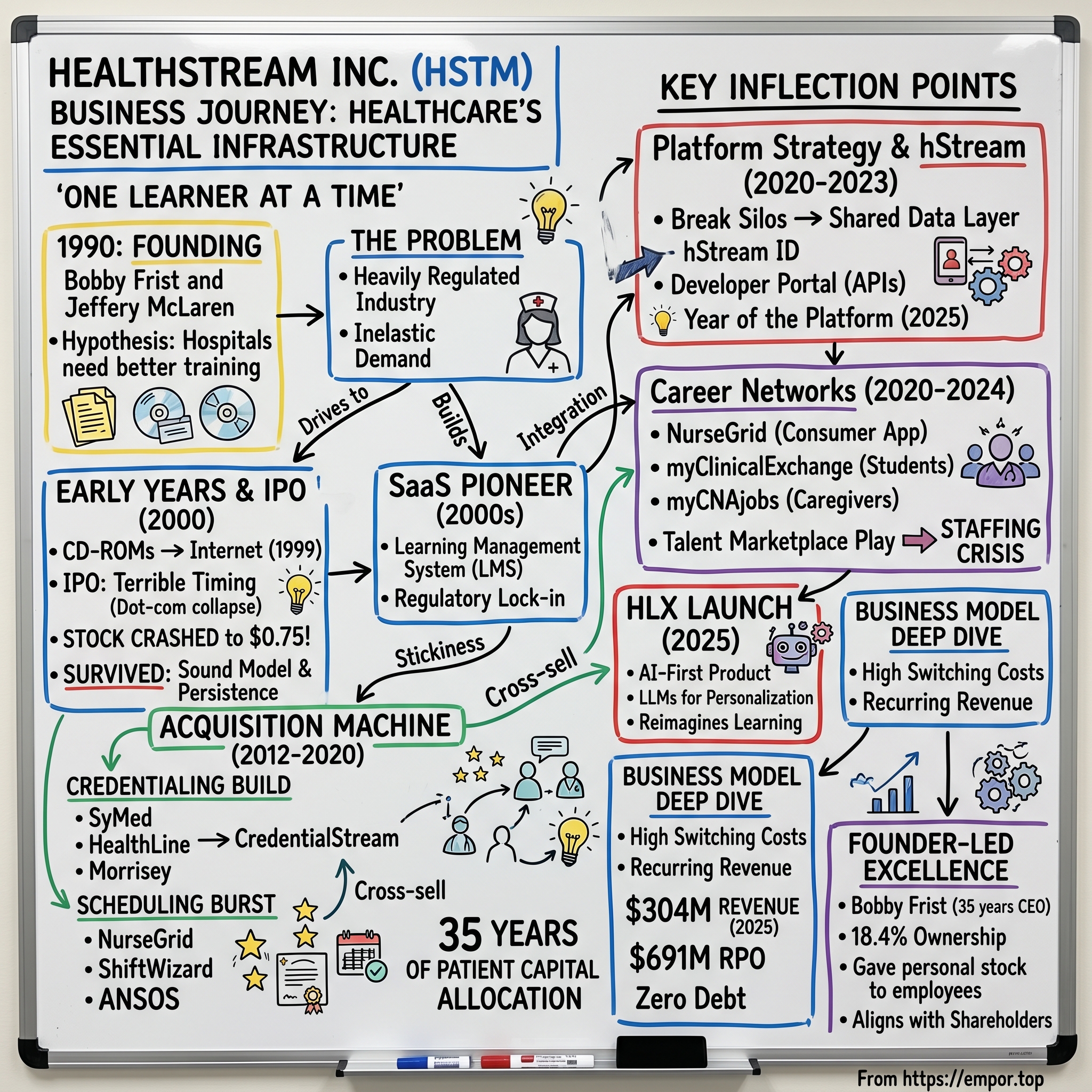

II. Founding Story & Healthcare Context (1990)

Picture Nashville in 1990. Walk down Commerce Street and you will pass a dozen office buildings whose tenants read like a roster of American healthcare: HCA Healthcare, the largest for-profit hospital chain in the world. Hospital Alliance. PhyAmerica. Envision Healthcare. Nashville is not just a city with a healthcare sector — it is a city that was built by healthcare, starting in 1968 when Dr. Thomas Frist Sr., a Nashville internist, partnered with his surgeon son Thomas Frist Jr. and businessman Jack Massey to found Hospital Corporation of America. By 1990, HCA's gravitational pull had attracted hundreds of healthcare companies to Middle Tennessee, creating an ecosystem where "healthcare" was not just an industry but a culture, a social network, and — for one family in particular — a dynasty.

The Frist family tree reads like a map of American power in healthcare and politics. Dr. Thomas Frist Sr. co-founded HCA. His son, Thomas Frist Jr., built it into a colossus — a company that today operates roughly 180 hospitals across the United States and United Kingdom, generating over sixty billion dollars in annual revenue. Thomas Jr. became Tennessee's wealthiest citizen, with a net worth exceeding twenty billion dollars.

His brother, Bill Frist, became a heart-lung transplant surgeon and then served as the United States Senate Majority Leader from 2003 to 2007. Into this family of hospital operators and statesmen, Robert A. Frist Jr. — Bobby, as everyone in Nashville calls him — carved a different path entirely.

Bobby Frist could have walked into any corner office in Nashville healthcare. The family name alone would have opened every door in the industry. Instead, in 1990, he co-founded a startup — a company that would not operate hospitals or perform surgeries but would build software to help the people who did those things get better at their jobs.

Together with Jeffery L. McLaren, a Trinity University graduate with degrees in both business and philosophy, Bobby Frist incorporated HealthStream in 1990 with a hypothesis that was ahead of its time: hospitals needed a better way to train their people.

The problem was not abstract. Healthcare is among the most heavily regulated industries in America. The Joint Commission, OSHA, CMS, and individual state boards all mandate continuous training and competency verification for healthcare workers. A single hospital might face hundreds of distinct training requirements covering everything from bloodborne pathogen safety to patient privacy under HIPAA to fire extinguisher operation.

In 1990, virtually all of this training was delivered through in-person sessions, paper sign-off sheets, and filing cabinets full of compliance records.

The insight that animated HealthStream's founding was that this was not just an inconvenience — it was a structural opportunity.

Consider the scale of the problem. A typical mid-size hospital employs two to three thousand people, each of whom must complete dozens of distinct training requirements annually. Multiply that across roughly six thousand hospitals in the United States, add in long-term care facilities, ambulatory surgery centers, and physician practices, and the total training burden runs into hundreds of millions of individual course completions per year.

And the penalties for non-compliance were severe: failed Joint Commission surveys, Medicare decertification, malpractice liability, and potentially catastrophic legal exposure. This was not discretionary spending that could be cut in a recession. It was as close to inelastic demand as exists in enterprise software.

But in 1990, there was no internet to deliver this training digitally. HealthStream's earliest solutions involved CD-ROMs, proprietary networks, and on-site technology installations — clunky, expensive, and difficult to scale. The company spent nearly a decade building relationships, developing content, and waiting for technology to catch up with the vision. McLaren served as president from 1990 to 2000, leading the product development effort, before later stepping back to a board seat and founding Medaxion, a company in the anesthesia information space.

One of HealthStream's earliest wins was a contract with Columbia/HCA — the entity that HCA had become after its merger with Columbia Hospital Corporation. The Frist family connection unquestionably opened doors, but it would be a mistake to reduce HealthStream's origin to nepotism. Bobby Frist chose to build a technology company in an era when healthcare technology was barely a recognized category. He chose to focus on a problem — workforce training — that most hospital executives considered a cost center, not a strategic asset. And he chose to stay the course through nearly a decade of pre-internet obscurity, building content libraries and hospital relationships that would become invaluable once the web arrived.

There is a telling detail about the early years that reveals Frist's temperament. While the late 1990s dot-com bubble was minting overnight millionaires from consumer internet companies with no revenue, HealthStream was doing something deeply unglamorous: building courseware about bloodborne pathogens, fire safety, and patient restraint protocols. The company was constructing, one module at a time, a library of healthcare-specific training content that would take years to produce and that no venture-backed startup could replicate quickly. It was the kind of work that required both conviction and a high tolerance for boredom — two qualities that would prove more valuable than any algorithm.

By March 1999, when HealthStream finally began marketing its internet-based solutions, the company had already built something that pure internet startups lacked: deep domain expertise, a library of healthcare-specific content, and a base of hospital customers who trusted the company to keep their workforces compliant. That combination of digital ambition and healthcare credibility would prove decisive in the years to come.

III. The Long Build: From Startup to SaaS Pioneer (1990s–2000s)

HealthStream's IPO on April 14, 2000, was a masterclass in terrible timing.

The company priced its offering at nine dollars per share on the NASDAQ exchange, raising roughly forty-two million dollars. The original pricing range had been eleven to thirteen dollars, but the late stages of the dot-com collapse forced a last-minute markdown.

On opening day, shares opened at $9.03, briefly touched $9.63, then fell to $7.94 before closing at $8.50 — already fifty cents below the offering price. By December 2000, just eight months later, HealthStream's stock had cratered to seventy-five cents per share. The company's market capitalization, which had stood at approximately $165 million at the IPO, had been nearly obliterated.

This was the crucible. To understand how dire the situation was, consider the context: the NASDAQ Composite, which had peaked at 5,048 in March 2000, would eventually fall to 1,114 by October 2002 — a decline of seventy-eight percent. Hundreds of healthcare technology companies that went public in the same era — companies with more funding, more employees, more press coverage — went bankrupt between 2000 and 2003. The graveyard of healthcare dot-coms from that period includes names like drkoop.com, Healtheon (absorbed into WebMD), and dozens of others that promised to digitize medicine but ran out of cash before achieving sustainable revenue. HealthStream survived, and the reasons are instructive for understanding everything the company has done since.

First, the business model was fundamentally sound even if the valuation was not. Hospitals still needed compliance training. Regulations did not disappear because the NASDAQ crashed. HealthStream's revenue was small but recurring, and the customers who had adopted the platform had no incentive to leave.

Second, Bobby Frist did not panic. He did not sell the company, did not pivot away from healthcare, did not lay off the core team and try to become something else. Nashville business press from the period described him simply as "persistent" — a word that, in retrospect, might be the most important adjective in the HealthStream story.

The company used the post-bubble years to do something unsexy but transformative: it built a software-as-a-service business before the term SaaS was widely used.

HealthStream's transition to subscription-based delivery happened organically. Hospitals paid annual fees per user for access to the learning management system and its content library. Revenue was predictable. Contracts were multi-year. Customer acquisition costs were high — hospital sales cycles could stretch for months — but once a hospital adopted HealthStream, it tended to stay.

The compliance records, training histories, and workflow integrations created switching costs that were less about contractual lock-in and more about operational dependency. Ripping out HealthStream meant rebuilding years of training documentation and finding an alternative that could satisfy the same regulatory requirements.

By the mid-2000s, HealthStream had established itself as the category leader in healthcare learning management. Its platform — the HealthStream Learning Center — became the system of record for mandatory training at thousands of healthcare organizations. To appreciate the density of the compliance web that creates demand for this product, consider a single example: a registered nurse at a Joint Commission-accredited hospital must complete annual training on topics including infection prevention, patient safety, workplace violence prevention, hazardous materials handling, emergency preparedness, cultural competency, age-specific care, medication administration, pain management, restraint and seclusion, HIPAA privacy, information security, fraud and abuse awareness, and sexual harassment prevention — among others. Each topic has its own regulatory origin, its own content requirements, and its own documentation standards. HealthStream's software handled the entire workflow for all of them: assigning courses, tracking completion, generating compliance reports, and alerting administrators to gaps.

The stickiness of this product cannot be overstated. When a hospital adopts HealthStream's learning management system, it is not buying a piece of software — it is delegating a regulatory obligation to a platform.

The training records stored in HealthStream become the hospital's proof of compliance during Joint Commission surveys and regulatory audits. Migrating away from HealthStream means migrating those records, revalidating compliance status, and retraining administrators on a new system.

For a hospital administrator already juggling a hundred priorities, the switching cost is not measured in dollars but in risk. The risk of a gap in compliance documentation during a transition is, in many cases, simply unacceptable.

This dynamic — regulatory lock-in combined with operational dependency — is the foundation of HealthStream's business moat. It does not produce the kind of explosive growth that excites momentum investors, but it produces something arguably more valuable: durability.

By the end of the 2000s, HealthStream had grown from a dot-com-era near-casualty into a profitable, publicly traded SaaS company with a dominant position in its niche. The stock price had recovered from its seventy-five-cent nadir to trade consistently above ten dollars. Revenues were growing steadily.

And Bobby Frist, still at the helm, was beginning to think about the next phase of expansion — one that would require not just organic growth but acquisitions.

IV. The Acquisition Machine: Build vs. Buy Strategy (2000s–2010s)

Sometime around 2012, Bobby Frist made a strategic decision that would reshape HealthStream's identity: the company would expand beyond learning management into adjacent categories through acquisition.

The logic was straightforward. HealthStream had built deep relationships with hospital administrators and a strong brand in healthcare IT. But its revenue was concentrated in a single product category — learning — and growth in that category was constrained by the pace at which new hospitals adopted the platform.

The adjacent categories — credentialing, scheduling, competency management — served the same customer, faced the same regulatory dynamics, and offered the same recurring revenue characteristics. The question was whether to build these capabilities from scratch or to buy companies that had already built them.

Frist chose to buy, and the acquisition spree that followed between 2012 and 2020 fundamentally transformed HealthStream from a learning management company into a comprehensive healthcare workforce platform.

The credentialing buildout came first and was executed with methodical precision. SyMed Development, acquired in 2012, added medical staff management and credentialing software. HealthLine Systems, acquired in March 2015, brought Echo — a SaaS credentialing solution used by over a thousand healthcare facilities. In October 2015, HealthStream formally merged these assets into Echo Inc., a dedicated subsidiary focused on credentialing. Then came Morrisey Associates in August 2016 for approximately forty-eight million dollars — a Chicago firm founded in 1987 that had built web-based software for practitioner credentialing and privileging. Morrisey had generated nearly thirteen million in revenue the prior year and came with deep relationships in the hospital credentialing workflow. By January 2018, HealthStream consolidated all of these assets under a new brand: Verity, later evolving into what is now CredentialStream.

The strategic logic of the credentialing play was elegant. A hospital's credentialing office and its education department serve the same population — the clinical workforce — and face the same regulatory framework.

When a surgeon applies for privileges at a hospital, the credentialing office must verify their medical education, board certifications, malpractice history, and competency. Many of those competency requirements overlap directly with the training tracked in HealthStream's learning management system. By owning both the learning and credentialing workflows, HealthStream could offer hospitals a unified view of their workforce's qualifications — a "single source of truth" that reduced administrative burden and compliance risk.

The scheduling buildout followed a similar pattern, compressed into a remarkable eighteen-month burst in 2020. In March 2020, HealthStream acquired NurseGrid for twenty-five million dollars — a Portland, Oregon startup that had built the most popular mobile app for nurses, with over 260,000 monthly active users. In October 2020, ShiftWizard was added for approximately thirty-two million dollars — a cloud-based scheduling solution that KLAS had named its Category Leader with a ninety-seven percent customer retention rate. And in December 2020, HealthStream made its largest acquisition to date: ANSOS Staff Scheduling from Change Healthcare for approximately $67.5 million. ANSOS was an enterprise-grade scheduling system used by over three hundred hospitals, and the deal came with related tools for patient tracking and capacity planning, plus approximately ninety Change Healthcare employees.

In total, HealthStream spent roughly $125 million in 2020 alone to build a comprehensive scheduling capability — from the enterprise level (ANSOS) to the nurse-manager level (ShiftWizard) to the individual nurse's phone (NurseGrid). The logic mirrored the credentialing play: scheduling is another workflow that touches every healthcare worker, is subject to regulatory requirements around staffing ratios and rest periods, and generates data that connects naturally to learning and credentialing records.

The speed and scale of the scheduling buildout deserves particular attention. In the span of nine months — from March to December 2020 — HealthStream spent approximately $125 million to acquire three scheduling companies, each serving a different layer of the market. NurseGrid operated at the individual nurse level — a personal productivity app. ShiftWizard operated at the nurse manager level — a departmental scheduling tool. ANSOS operated at the enterprise level — a hospital-wide staffing and capacity planning system. Together, they formed a complete scheduling stack from the individual nurse's phone to the hospital's command center. The timing was notable: HealthStream executed these acquisitions during the first year of the COVID-19 pandemic, when hospital staffing had become the single most urgent operational challenge in American healthcare. Whether by design or serendipity, the company was assembling the tools to address the most pressing workforce problem its customers had ever faced.

These acquisitions were not without risk. Integration is difficult in any context, and HealthStream was absorbing companies with different technology stacks, different cultures, and different customer bases. Bringing ninety Change Healthcare employees into the organization — a full team with its own established processes and culture — required careful change management. The company's revenue growth remained modest even as it added new product lines, suggesting that cross-selling was proving harder than the strategy implied. Public market investors, accustomed to SaaS companies growing at thirty or forty percent annually, were unimpressed by HealthStream's mid-single-digit growth rates. The stock traded sideways for extended periods.

But Frist was playing a longer game. Each acquisition added another strand to the web of workflows connecting HealthStream to its hospital customers. A hospital using HealthStream for learning, credentialing, and scheduling would find it exponentially more difficult to switch away than a hospital using HealthStream for learning alone. The land-and-expand playbook — start with one product, then cross-sell adjacent solutions — required patience, but the compounding effect of multiple integrated products was the strategic moat that Frist was building brick by brick. By the early 2020s, the pieces were in place. What remained was connecting them.

V. Key Inflection Point No. 1: The Platform Strategy & hStream Launch (2020–2023)

In November 2022, HealthStream launched the hStream Developer Portal, and what might have looked like a routine product announcement was actually the most consequential strategic move in the company's history. To understand why, consider the difference between a software company and a platform company.

A software company sells applications. Customers buy them, use them, and the vendor earns revenue from subscriptions or licenses. The relationship is transactional: the customer pays, the vendor delivers functionality.

A platform company does something different. It creates an ecosystem — a set of shared services, data standards, and integration points — on which both the vendor and third parties can build.

The classic examples are Salesforce (which transformed from a CRM application into a platform for business applications), Apple (which created iOS as a platform for developers), and Amazon Web Services (which turned infrastructure into a platform). In each case, the platform created network effects: the more developers and partners built on the platform, the more valuable it became for customers, which attracted more developers and partners.

For a thirty-two-year-old healthcare training company to attempt this same transition was audacious. But the logic was sound. Through its acquisitions, HealthStream had assembled three core application suites — Learning, Credentialing, and Scheduling — each serving the same customer base of healthcare organizations. The problem was that these applications, built or acquired at different times on different technology architectures, did not naturally talk to each other. A nurse's training records in the Learning Center were disconnected from her credentialing status in CredentialStream, which was disconnected from her shift schedule in ShiftWizard. The data existed in silos.

The hStream platform was designed to break those silos. At its core, hStream is a shared data layer and identity system.

The hStream ID serves as a universal identifier for healthcare professionals across all three domains. When a nurse completes a training module, that completion is recorded against her hStream ID. When her credentials are verified, that verification is linked to the same ID. When she is scheduled for a shift, the scheduling system can check — via the platform — whether her training is current and her credentials are valid.

This integration sounds simple, but in a world where hospitals typically run dozens of disconnected software systems, it is genuinely transformative.

The Developer Portal extended this logic to third parties. By publishing APIs for Learning and Credentialing, HealthStream invited customers and partners to build integrations that pulled data into or out of the hStream platform. The inaugural partner — CAE Healthcare, which builds resuscitation training manikins — demonstrated the concept: a training simulation device could automatically record completion data directly into a nurse's hStream profile through the API. By the second quarter of 2025, over 460 developers from 194 customer accounts were accessing the platform APIs.

Bobby Frist designated 2025 as the "Year of the Platform," a declaration that was equal parts strategic roadmap and internal rallying cry. On earnings calls, he was explicit: "We're in this transition of trying to move from SaaS applications to a PaaS — a platform as a service — architecture." The distinction matters for investors because PaaS businesses tend to have stronger competitive moats (switching costs increase as customers build on the platform), higher lifetime values (more integration means more stickiness), and greater potential for network effects (each additional participant makes the platform more valuable for all participants).

Think about what this means in practical terms. Imagine you are a hospital CIO evaluating whether to consolidate your learning, credentialing, and scheduling systems onto a single platform. Today, your learning data lives in HealthStream, your credentialing data lives in a separate system from symplr, and your scheduling data lives in UKG. When a nurse changes units, three separate systems need to be updated. When a Joint Commission surveyor asks whether a particular nurse is current on her competency requirements for the ICU, someone has to manually cross-reference training records with credentialing status and scheduling assignments. The hStream pitch is: put all three on our platform, and we will connect them automatically through a single identity and data layer. The surveyor's question can be answered with one click instead of three phone calls. That is a compelling value proposition — not because it is technically revolutionary, but because it eliminates real operational pain.

The early evidence was encouraging. HealthStream's Remaining Performance Obligations — the total value of contracted revenue not yet recognized — reached $691 million by the end of 2025, up 11.2 percent from $621 million a year earlier. This is a forward-looking metric that suggests customers were signing longer-term, larger contracts as they deepened their commitment to the hStream ecosystem. Management noted that approximately thirty-nine percent of RPO would convert to revenue within the next twelve months and sixty-seven percent within twenty-four months, reflecting the multi-year nature of platform commitments.

By the end of 2023, HealthStream had approximately 5.79 million contracted subscriptions to hStream — a number that represents not individual users but individual human-product relationships across the platform. A single nurse might have subscriptions for Learning, Credentialing, and Scheduling, each counting separately. The growth of this metric reflects the land-and-expand dynamic at work: as hospitals adopt more of the hStream suite, the number of subscriptions per user increases, deepening the relationship and raising the switching cost with each additional product.

The platform strategy also created a new growth vector that HealthStream had never previously had: the ability for customers to consolidate third-party learning records into HealthStream. Hospitals use dozens of training systems beyond HealthStream — vendor-specific device training, university continuing education, professional association courses — and the records from those systems historically lived in separate databases. The Learning API within hStream allows hospitals to push those external records into HealthStream, making it the single repository for all workforce education data. Every hospital that does this becomes more dependent on HealthStream, not because of a contractual obligation, but because HealthStream has become the institutional memory of their workforce's qualifications.

VI. Key Inflection Point No. 2: Building Career Networks — The Talent Marketplace Play (2020–2024)

The most counterintuitive move in HealthStream's recent history was its decision to build a consumer-facing business. For thirty years, HealthStream had been a pure B2B enterprise software company. Its customers were hospitals and health systems, its users were employees of those hospitals, and its revenue came exclusively from institutional subscriptions. Then, starting in 2020, Bobby Frist began assembling something different: a network of direct relationships with individual healthcare workers.

The centerpiece of this strategy was NurseGrid, the Portland startup acquired in March 2020 for twenty-five million dollars. To understand why this deal mattered, consider what a typical nurse's work life looks like. Nurses rarely work Monday through Friday, nine to five. They work twelve-hour shifts — days, nights, weekends — on rotating schedules that change every few weeks. They swap shifts with colleagues constantly. They juggle commitments across multiple units, sometimes multiple hospitals. Managing this complexity on paper calendars or basic smartphone calendars is a persistent source of stress in a profession already defined by stress.

NurseGrid solved this problem elegantly. At the time of acquisition, it had over 260,000 monthly active nurses using its mobile app to manage schedules, swap shifts, and communicate with colleagues. What made NurseGrid unusual was that it was a consumer app adopted by nurses individually, not deployed by hospital IT departments. Nurses downloaded it from the App Store because it solved a personal problem, and they continued using it because it worked. The app maintained a 4.9 out of 5 rating with over 130,000 reviews, making it one of the highest-rated professional apps in the healthcare category. For context, a 4.9 rating at that volume of reviews is exceptionally rare — most professional productivity apps struggle to maintain ratings above 4.0.

By the fourth quarter of 2025, NurseGrid had grown to over 670,000 monthly active users, with approximately 2,000 new nurses signing up each week. Bobby Frist claimed on earnings calls that NurseGrid now reached roughly one in five nurses working in the United States — a penetration rate that, if accurate, gives HealthStream a direct relationship with the nursing workforce that no purely B2B competitor can replicate. Think about what that means: HealthStream can reach twenty percent of American nurses not through their employers but through an app the nurses chose to install on their personal phones. That is a fundamentally different kind of market access.

The same year it acquired NurseGrid, HealthStream purchased myClinicalExchange, a Denver-based company that managed clinical rotation placements for nursing students. If NurseGrid captured nurses at the point of active employment, myClinicalExchange captured them even earlier — at the student stage, when they were arranging the clinical rotations required for their nursing degrees. The strategic insight was powerful: if HealthStream could establish a relationship with a nurse while she was still a student, and then maintain that relationship through NurseGrid as she entered the workforce, and then deepen it through the institutional products (Learning Center, CredentialStream) used by her employer, the company would effectively own the entire lifecycle of a healthcare career.

In November 2024, HealthStream doubled down on this student pipeline by acquiring TCPS (Total Clinical Placement System) and The Clinical Hub — two additional companies in the clinical rotation management space. These were small deals — TCPS for up to $1.65 million, The Clinical Hub for up to $600,000 — but they expanded the coverage of HealthStream's nursing student network, connecting more schools with more hospitals for clinical placement coordination.

Then came the most recent and perhaps most strategically significant piece of the career network puzzle. In December 2025, HealthStream acquired MissionCare Collective for up to forty million dollars — twenty-six million in cash at closing, approximately four million in HealthStream common stock, and up to ten million in earnout payments. MissionCare's flagship product, myCNAjobs.com, describes itself as the nation's largest caregiver network, with 5.2 million caregivers on its platform and relationships with over eight thousand healthcare providers.

With MissionCare, HealthStream now operates three distinct Career Networks: NurseGrid for licensed nurses, myClinicalExchange for nursing and allied health students, and myCNAjobs for certified nursing assistants and non-medical caregivers. Together, these networks span the entire breadth of the healthcare workforce, from CNA training programs through nursing school clinical rotations to active nursing careers. The vision is unmistakable: HealthStream wants to be the professional network for healthcare workers — the LinkedIn meets Indeed of the healthcare labor market.

This ambition sits against the backdrop of the worst healthcare staffing crisis in American history. The numbers are staggering in both scale and implication. Over 138,000 nurses exited the workforce since 2022, driven by burnout, pandemic trauma, and dissatisfaction with working conditions. Nearly forty percent of active nurses have indicated they intend to leave by 2029 — a figure that, if it materializes, would constitute an existential threat to the American healthcare system. The average hospital spends over sixty thousand dollars to replace a single registered nurse when accounting for recruitment, onboarding, training, and the productivity loss during the transition period. U.S. hospitals collectively spent roughly $1.7 billion on travel nurses in 2024, a stopgap measure that is financially unsustainable for most institutions.

Perhaps most telling is the supply-side constraint: more than 65,000 qualified nursing applicants are denied entry to U.S. nursing schools annually — not because they are unqualified, but because schools lack sufficient faculty and clinical placement capacity. This is the bottleneck that myClinicalExchange directly addresses. By streamlining the coordination of clinical rotations between nursing schools and hospitals, HealthStream is working to widen the pipeline at its narrowest point.

Bobby Frist cited Bureau of Labor Statistics projections on the fourth-quarter 2025 earnings call, noting that healthcare accounted for approximately 82,000 of the 130,000 new jobs added to the U.S. economy in January 2026 alone. He projected that roughly one-quarter of all new jobs in the country over the next decade will be in healthcare. For HealthStream, the math is simple: every new healthcare worker needs to be trained, credentialed, and scheduled. Every one of these data points is a tailwind for the career network strategy.

For investors, the career network strategy represents a potential step-change in HealthStream's business model. Enterprise software revenue is linear — you sign a hospital, you earn a subscription fee. Network revenue can be exponential — each additional participant makes the network more valuable for all other participants. If HealthStream can build genuine two-sided marketplace dynamics between healthcare workers and healthcare employers, the economic characteristics of the business could improve dramatically. That is a big "if," and the execution risk is real, but the strategic logic is compelling.

VII. Key Inflection Point No. 3: AI-First Product Innovation — The HLX Launch (2025)

On January 27, 2025, HealthStream launched the HealthStream Learning Experience — HLX — and in doing so made a bet that the future of healthcare workforce development looks nothing like its past. The launch represented something more than a product release. It was a philosophical statement about what healthcare learning could become when freed from the constraints of pure compliance.

To understand why HLX matters, consider how healthcare training has worked for the past three decades — including the decades during which HealthStream has been the dominant platform for delivering it. A hospital's education department creates an annual training calendar. Mandatory courses are assigned to every employee based on their role: OSHA blood-borne pathogens for everyone, medication administration for nurses, restraint and seclusion for behavioral health staff. Employees receive notifications. They log in, click through the modules, answer the quiz questions at the end, and receive a completion certificate. The education department generates a report showing ninety-eight percent compliance. Everyone moves on with their lives.

It is necessary, it is valuable, and it is profoundly uninspiring. Ask a nurse how she feels about her annual compliance training modules and the answer will typically involve an eye roll. The content is consumed because it must be, not because it engages. In survey after survey, healthcare workers rank mandatory training among their least satisfying professional activities — below documentation, below meetings, sometimes even below dealing with difficult patients. The irony is that the system designed to develop healthcare professionals has, in practice, become an exercise in checking boxes.

HLX represents a deliberate attempt to break this pattern. Built natively on the hStream platform — making it the first application designed from the ground up on HealthStream's new architecture — HLX reimagines healthcare learning as a personalized, self-directed experience rather than a compliance checkbox. The application uses large language models to analyze a healthcare worker's personal portfolio of accomplishments, competencies, and career goals, then recommends learning pathways tailored to their individual development. Think of it as the difference between a mandatory fire safety video and a personalized career development coach.

For non-technical readers, the term "AI-first" deserves explanation. It does not mean that artificial intelligence runs the product autonomously. It means that from the earliest design stages, the product team asked of every feature: "How could an AI model make this better?" The result is a system where AI is embedded in the workflow rather than bolted on as an afterthought. LLMs — the same category of technology that powers tools like ChatGPT — assist managers in creating learning content, reducing the time and expertise required to develop new training materials. Rather than spending hours writing course descriptions and learning objectives, a manager can input the topic and learning goals, and the LLM generates a draft that the manager can refine. Recommendation engines surface relevant courses, articles, podcasts, and videos based on a learner's profile and career trajectory — the same concept that Netflix uses to suggest movies, applied to professional development. Social and mentoring features connect healthcare workers with peers and mentors — addressing one of the most commonly cited drivers of nurse burnout: professional isolation and lack of career development support.

The competitive positioning is deliberate. Bobby Frist has described HLX as combining a Netflix-like user experience — personalized recommendations, engaging interface, self-directed discovery — with LinkedIn Learning-like career development capabilities, all built for the specific requirements of healthcare. The emphasis on "healthcare-specific" is important because it differentiates HLX from general-purpose learning experience platforms like Degreed, Cornerstone, or LinkedIn Learning, none of which understand healthcare regulatory requirements, clinical competency frameworks, or the specific career pathways of nurses, physicians, and allied health professionals.

One particular use case illustrates why HLX could be genuinely transformative rather than merely incremental. Hospitals facing nursing shortages frequently need to cross-train nurses — taking a medical-surgical nurse and upskilling her to work in critical care, for example. This is a complex process involving didactic education, simulation training, supervised clinical hours, and competency verification. Today, most hospitals manage this with a combination of spreadsheets, paper checklists, and manual coordination. HLX could orchestrate the entire pathway: identifying which competencies the nurse already holds, generating a personalized learning plan for the gaps, tracking progress through each milestone, and verifying completion through integration with the credentialing system. That turns a months-long administrative headache into an automated workflow — and it is exactly the kind of capability that hospitals will pay a premium for during a staffing crisis.

At launch, three large healthcare organizations selected HLX, with two serving as formal launch partners. The early traction, while modest in scale, validates that the market is ready for this kind of product evolution. For investors watching HealthStream's growth rate — which has been stuck in the mid-single digits for years — HLX represents the most plausible catalyst for acceleration. A product that moves HealthStream from compliance necessity to career development platform could justify higher per-user pricing, increase engagement metrics, and drive adoption in departments and use cases that the legacy Learning Center never reached.

VIII. The Business Model Deep Dive

HealthStream's financial profile is a study in the tradeoffs inherent in building durable, subscription-based businesses in complex, regulated industries.

The company reports through two segments: Workforce Solutions and Provider Solutions.

Workforce Solutions encompasses the learning, scheduling, and talent management products — essentially everything that touches a healthcare organization's employees. Provider Solutions covers credentialing and privileging — the products that verify and manage the qualifications of physicians, advanced practice providers, and other credentialed clinicians.

In 2025, total revenue reached $304.1 million, up 4.3 percent from the prior year. The fourth quarter of 2025 was particularly strong, with revenue of $79.7 million — the company's highest-ever quarterly figure — growing 7.4 percent year over year, powered by subscription revenue growth of 8.2 percent.

Gross margins have remained relatively stable in the sixty-three to sixty-five percent range, reflecting the fundamental scalability of a SaaS model where content development and platform maintenance costs are amortized across millions of users.

The margins are not at the eighty-plus percent levels of the highest-margin SaaS companies, partly because HealthStream invests heavily in content development (much of it proprietary and healthcare-specific), maintains a significant professional services team for implementation and customer success, and bears meaningful hosting and infrastructure costs as it migrates more customers to cloud-based delivery.

The unit economics tell a clear story about why hospitals do not leave. The cost to acquire a hospital customer is substantial — the sales process involves demonstrations, compliance reviews, IT security assessments, integration planning, and multi-stakeholder committee decisions. Sales cycles can stretch six to twelve months.

But once a hospital is on the platform, the retention dynamics are extraordinarily favorable. HealthStream's training records become the hospital's compliance documentation. The credentialing data becomes the medical staff office's system of record. The scheduling system becomes the operational backbone of nurse staffing. Each additional product deepens the integration and raises the cost of departure.

This creates a powerful land-and-expand dynamic that is the engine of HealthStream's growth. A hospital might initially adopt HealthStream for compliance training — the entry-level product that addresses a universal pain point. Over time, the same hospital adds credentialing, then scheduling, then competency management. Each addition increases the per-user revenue and the total contract value. The Remaining Performance Obligations figure of $691 million — representing contracted but not yet recognized revenue — is the financial expression of this dynamic. It means that even if HealthStream signed zero new customers tomorrow, it has nearly two and a half years of revenue visibility already locked in.

The content strategy adds another layer of defensibility. HealthStream maintains a library of proprietary courses covering healthcare compliance, clinical competencies, and professional development. It also partners with third-party content providers — including medical device manufacturers, professional associations, and academic institutions — to offer a broad catalog through its platform. The combination of proprietary and partnered content creates a library effect: the more content available on the platform, the more valuable it becomes for customers, and the harder it is for competitors to replicate.

Revenue growth in the mid-single digits is the characteristic that most frustrates growth-oriented investors. HealthStream is not a hypergrowth story and probably never will be.

Healthcare sales cycles are long. Hospital budgets are constrained. Decision-making is diffuse. A single product implementation can take months. These structural realities cap the pace of growth regardless of the quality of the product or the size of the market.

What they do not cap is the durability of the revenue once captured. For investors who prioritize compounding over velocity, HealthStream's business model — with its high retention, embedded switching costs, and regulatory tailwinds — offers something rare: genuine predictability in an uncertain world.

In 2025, adjusted EBITDA reached $71.8 million, representing a margin of approximately twenty-four percent, with the company generating sufficient free cash flow to fund thirty million dollars in share repurchases while maintaining its debt-free balance sheet.

The twelve-percent increase in dividends — to $0.035 per share per quarter — signals management confidence in the sustainability of cash flows. For a company with no debt and fifty-seven million dollars in cash, the capital allocation is conservative but deliberate: fund acquisitions from operating cash flow, return excess capital through buybacks and dividends, and never lever up the balance sheet.

IX. Founder-Led Excellence: The Bobby Frist Story

In December 2025, Bobby Frist did something unusual for the CEO of a publicly traded technology company. He took 146,286 shares of HealthStream common stock — worth approximately $3.8 million — from his personal holdings and distributed them to over seven hundred non-executive employees. No strings attached. Immediate vesting. No conditions on tenure or performance. This was not the first time. He had done the same thing in 2015, giving $1.5 million in shares to over six hundred employees, and again in December 2021, giving $2.25 million to over a thousand employees during the depths of the COVID-19 pandemic.

The 2025 gift was large enough to reduce HealthStream's reported earnings per share by nine cents in the fourth quarter — a non-trivial impact that required management to introduce a specific non-GAAP adjustment on the earnings call to help investors understand the underlying operational performance. In other words, Frist's personal generosity was material to the financial statements. When asked about the practice, he framed it as recognition: "I am humbled by our employees' visionary drive and hard work to make a difference in healthcare." The statement itself is typically understated. The action is not.

What makes these gifts distinctive is their consistency and their structure. They come from Frist's personal holdings, not from the company's equity compensation pool. The company bears only administrative costs and payroll taxes, which Frist also reimburses through additional share contributions.

The recipients are exclusively non-executive employees — front-line and mid-level staff who are not already participating in executive equity programs. In an era when CEO compensation packages dominate headlines and the ratio of executive-to-median-worker pay has become a cultural flashpoint, Frist's repeated personal transfers of wealth to his employees are genuinely anomalous.

Bobby Frist's thirty-five-year tenure as CEO is itself a defining feature of the HealthStream story. He has led the company through the pre-internet era, the dot-com bust, the recovery, the acquisition era, and now the platform transition. His ownership stake — approximately 18.4 percent of shares outstanding as of 2025 — gives him an alignment with shareholders that few professional managers can match. When Bobby Frist makes a strategic decision, he is betting his own wealth on the outcome.

His leadership philosophy is codified in a document that HealthStream employees call "the Constitution" — a physically distinctive twenty-two-page booklet with a vivid red cover, printed on heavy cardstock in an oversized format. The document articulates HealthStream's vision, mission, values, and business principles, and it is treated as a living operational guide rather than a dusty corporate artifact. Over 230 employees completed formal certification courses on its contents. New employees study it during orientation. An internal recognition program — "RAVE Reviews" — celebrates employees who exemplify its values. The physical heft of the booklet is deliberate: it is designed to sit on a desk, to be referenced, to carry weight both literal and metaphorical.

The culture Frist has built emphasizes a philosophy he articulates as "improving patient outcomes through people development." The belief is that every product HealthStream builds should ultimately connect to patient care — not directly, through clinical devices or treatments, but indirectly, by making the people who deliver care more competent, more compliant, and more engaged. It is a long-term, systems-level perspective on healthcare improvement, and it permeates the company's strategic decisions. When HealthStream acquires a scheduling company, the framing is not "we are diversifying revenue" but "we are helping hospitals staff their units more effectively so patients receive better care." Whether one views this as genuine conviction or savvy positioning, the consistency is remarkable.

Frist has been recognized externally as Ernst and Young's Entrepreneur of the Year for the southeastern United States and as Lipscomb University's Entrepreneur of the Year. He co-founded Nashville's Entrepreneur Center and served as its Chairman of the Board. He has chaired the Nashville Health Care Council, the influential industry group that represents the concentration of healthcare companies headquartered in the city. In a town defined by healthcare dynasties, Bobby Frist has built his own — not by joining the family hospital empire, but by creating the infrastructure that helps every hospital in America develop its workforce.

X. Strategic Framework Analysis: Porter's Five Forces & Hamilton's Seven Powers

Understanding HealthStream's competitive position requires looking beyond financial metrics to the structural dynamics that determine whether the company's advantages are durable.

Starting with the threat of new entrants: it is low, and getting lower.

Building a competitive healthcare learning management system requires not just software engineering talent but deep regulatory expertise — understanding Joint Commission standards, OSHA requirements, CMS Conditions of Participation, state-specific nursing board mandates, and the constantly evolving compliance landscape. It requires a content library that covers hundreds of mandatory training topics, validated by subject matter experts and updated continuously as regulations change.

It requires established relationships with hospital chief nursing officers, compliance directors, and IT departments who are notoriously risk-averse when selecting new vendors. And it requires the kind of track record — years of successful Joint Commission surveys, zero compliance failures attributable to training gaps — that a startup simply cannot demonstrate. A well-funded new entrant could theoretically build all of this, but the time and capital required creates a natural barrier that protects incumbents.

The bargaining power of suppliers is moderate. HealthStream's most important "suppliers" are the content creators and subject matter experts who develop its training materials, and the cloud infrastructure providers (primarily Amazon Web Services and Microsoft Azure) that host its platform. Content partnerships are important but diversified — no single content provider represents a critical dependency. Infrastructure costs have been rising, contributing to some margin pressure, but HealthStream has been managing this through scale efficiencies and platform consolidation.

The bargaining power of buyers is moderate to high on paper, but moderated in practice by the nature of the demand. Large hospital systems — HCA Healthcare, CommonSpirit Health, Ascension — command significant negotiating leverage and can extract volume discounts.

But the demand for compliance training is not discretionary. A hospital cannot decide to skip OSHA training this year because the budget is tight. The mandatory nature of the training creates inelastic demand that limits buyers' ability to use their leverage to compress pricing below a certain floor. The result is that HealthStream's pricing power is constrained at the top end but protected at the bottom — a dynamic that produces stable rather than volatile revenue.

The threat of substitutes is low to moderate. The most obvious substitutes are general-purpose learning management systems — platforms like Cornerstone OnDemand, SAP SuccessFactors, or Workday Learning — that serve all industries rather than healthcare specifically.

These platforms are capable and well-funded, but they lack the healthcare-specific content, regulatory mapping, and compliance reporting that HealthStream has built over three decades. A hospital could theoretically adopt Workday for its learning management, but it would then need to source all of its healthcare compliance content separately, map it to regulatory requirements manually, and build custom compliance reporting — a project that would consume IT resources and introduce compliance risk.

The alternative of building training in-house is even less attractive: the cost of developing, maintaining, and updating hundreds of compliance courses exceeds the cost of a HealthStream subscription by an order of magnitude.

Competitive rivalry is moderate. HealthStream's most direct competitor is Relias, a Bertelsmann-owned company that also specializes in healthcare learning. Relias competes aggressively on pricing and includes certain compliance tools in its base subscription that HealthStream charges for separately.

Symplr competes in credentialing. UKG competes in scheduling. But no single competitor matches HealthStream's breadth across all three domains, and the integration of these domains through the hStream platform is creating a competitive advantage that becomes more pronounced as customers adopt multiple products.

Turning to Hamilton Helmer's Seven Powers framework, HealthStream's competitive advantages come into sharper focus. Scale economies are strong — the cost of developing a compliance training course is fixed regardless of whether it is consumed by ten thousand or five million healthcare workers. HealthStream's user base of over five million learners allows it to amortize content development costs across a scale that no competitor can match, enabling it to invest more in content quality while maintaining competitive pricing.

Network effects are emerging rather than established — this is the promise of the Career Networks strategy. NurseGrid, myClinicalExchange, and myCNAjobs each create two-sided marketplace dynamics: more nurses on the platform make it more valuable for hospitals, and more hospital participation makes it more valuable for nurses. If these network effects reach critical mass, they could become self-reinforcing in a way that subscription software alone cannot.

Switching costs are HealthStream's single strongest power. Training records, credentialing data, compliance documentation, scheduling histories — all of this accumulates in HealthStream's systems over years, and migrating it to a competitor involves not just technical complexity but regulatory risk.

A hospital in the middle of a Joint Commission survey cycle cannot afford a gap in its compliance documentation. This creates a form of lock-in that is not contractual but operational, and it is arguably more durable than any contractual commitment.

Process power — the accumulated operational knowledge from thirty-five years of serving healthcare organizations — is strong but difficult to quantify. HealthStream understands hospital purchasing dynamics, regulatory timelines, clinical workflow patterns, and the specific pain points of chief nursing officers in a way that comes only from decades of focused experience. This institutional knowledge infuses product development, sales processes, and customer success operations.

Branding and cornered resources offer moderate advantages. HealthStream is the recognized category leader in healthcare learning — its Learning Center ranked first in G2's Best Healthcare Software in 2025 — but brand alone is not a decisive competitive weapon in enterprise software. Its regulatory expertise and content library are valuable cornered resources, but they are maintainable rather than unreplicable.

Counter-positioning — the power that comes from a business model innovation that incumbents cannot adopt without damaging their existing business — is limited. HealthStream is not disrupting anyone's business model. It is competing within an established category with a better product and deeper expertise.

The overall picture is of a company whose competitive position rests primarily on switching costs and scale economies, with emerging network effects that could become the third pillar of its moat if the Career Networks strategy succeeds. For investors, the key question is whether the platform transition and career network buildout can convert HealthStream's existing advantages — which produce stable but slow growth — into a position that also generates accelerating growth.

XI. Bull vs. Bear Case & Key Risks

The bull case for HealthStream begins with a simple observation: the demand for healthcare workforce training, credentialing, and scheduling is not cyclical — it is structural. Regulatory requirements do not disappear during recessions. Hospitals cannot defer compliance training because the economy is soft. The Joint Commission does not pause its survey schedule because hospital margins are under pressure. This creates a floor under HealthStream's revenue that few technology companies enjoy.

Building on that foundation, the bulls point to several catalysts.

The platform strategy, if executed successfully, should unlock margin expansion by consolidating customers onto a unified architecture and reducing the cost of maintaining multiple legacy systems. The emerging network effects from NurseGrid (670,000 monthly active nurses), myClinicalExchange (nursing student pipeline), and myCNAjobs (5.2 million caregivers) could create two-sided marketplace dynamics that accelerate growth beyond the traditional enterprise software sales cycle.

The nursing shortage — projected to worsen throughout the decade — drives demand for every product in HealthStream's portfolio: training tools to onboard new hires faster, credentialing software to verify qualifications efficiently, scheduling systems to optimize staffing, and career networks to attract and retain scarce talent.

AI-powered products like HLX increase engagement and could justify premium pricing.

The company's 2025 financial performance demonstrated momentum: CredentialStream grew approximately twenty-one percent, ShiftWizard grew approximately thirty-one percent, and the Competency Suite grew approximately twenty-seven percent in the fourth quarter. These are not the growth rates of a tired legacy business — they are the growth rates of products gaining traction in a market with real demand.

Adjusted EBITDA of $71.8 million and 2026 guidance calling for revenue of $323 million to $330 million suggest management sees continued acceleration. The debt-free balance sheet with fifty-seven million in cash provides both defensive resilience and offensive optionality for further acquisitions.

The bear case is equally grounded, and intellectually honest investors must wrestle with it. Revenue growth of four to six percent annually is modest for any company that wants to be valued as a technology business. To put this in perspective, the median SaaS company in public markets grows revenue at roughly fifteen to twenty percent annually. HealthStream's growth rate is closer to that of a utility than a technology platform. The market has historically valued the company accordingly, assigning it a revenue multiple well below the SaaS median.

Large hospital consolidation — driven by mergers among health systems seeking scale — could reduce the total number of addressable accounts, concentrating buying power in fewer hands and increasing pricing pressure. When two hospital systems merge, they typically standardize on a single vendor for each software category. If HealthStream serves one system and a competitor serves the other, the outcome is a coin flip. The platform transition carries meaningful execution risk: migrating legacy customers to the hStream architecture is a multi-year project, and every migration carries the risk of disruption, dissatisfaction, and customer loss. The financial statements already reflect this transition in microcosm — legacy application revenue declined approximately twenty-seven percent in the fourth quarter of 2025, as older products are sunset in favor of modern replacements. The question is whether the new products grow fast enough to more than offset the legacy decline.

General-purpose human capital management platforms — particularly Workday, UKG, and Cornerstone OnDemand — represent a competitive threat that should not be dismissed. These companies have billions of dollars in resources, established positions in hospital HR departments, and a strategic interest in expanding into healthcare-specific workflows.

If Workday decided to build a healthcare compliance learning module, it could leverage existing customer relationships and a massive distribution advantage. HealthStream's defense — domain expertise, regulatory specificity, content depth — is real, but it is not invulnerable against a well-funded, determined competitor.

Cloud infrastructure costs have been a source of margin pressure, and the trend line is not obviously favorable. As HealthStream migrates more workloads to the cloud and more customers demand cloud-based delivery, hosting costs as a percentage of revenue could increase. Amazon Web Services and Microsoft Azure — the dominant cloud providers — have pricing power that HealthStream cannot easily counterbalance. This is a structural challenge facing the entire SaaS industry, but it is particularly relevant for a company whose gross margins are already in the mid-sixties rather than the high seventies.

Customer bankruptcy is flagged as a recurring risk in HealthStream's filings — an acknowledgment that some of its smaller hospital and skilled nursing facility customers operate on thin financial margins and could become insolvent during periods of economic stress. The skilled nursing facility sector, in particular, has experienced significant financial distress in recent years, with dozens of operators filing for bankruptcy protection. While HealthStream's exposure to any single customer is limited, a systemic downturn in the post-acute care sector could create a headwind.

There is also a regulatory risk that receives insufficient attention: the possibility that mandatory training requirements could be reduced rather than expanded. While the long-term trend has been toward more regulation, political movements toward deregulation — particularly at the state level — could erode the compliance-driven demand that forms the bedrock of HealthStream's business. This is a low-probability scenario but a high-impact one, and it deserves monitoring.

For investors monitoring HealthStream's trajectory, three KPIs deserve particular attention.

First, the growth rate of Remaining Performance Obligations — the $691 million figure reported in the fourth quarter of 2025 — because it reflects the pace at which customers are committing to multi-year, multi-product contracts on the hStream platform. Accelerating RPO growth would signal that the platform strategy is working; decelerating growth would raise questions about customer adoption.

Second, the trajectory of NurseGrid's monthly active users, currently at 670,000-plus. This metric captures the health of HealthStream's most ambitious strategic bet — the career network play — and its ability to build consumer-scale relationships with the healthcare workforce.

Third, subscription revenue growth — which hit 8.2 percent in the fourth quarter of 2025 — is the cleanest indicator of underlying business momentum, stripping out the noise of professional services, one-time fees, and accounting adjustments.

XII. The Road Ahead: What's Next for HealthStream?

In February 2026, Bobby Frist stood before analysts on HealthStream's fourth-quarter earnings call and laid out the numbers that defined his company's thirty-fifth year: record quarterly revenue, double-digit growth in credentialing and scheduling, the largest Remaining Performance Obligations backlog in company history. For a company that has spent most of its public life being described as "steady" and "boring," the acceleration was notable. HealthStream enters 2026 with more strategic clarity than at any point in its history. The product portfolio is built. The platform architecture is live. The career networks are assembling. The question is whether the next five years will look like a continuation of the steady, mid-single-digit growth that has characterized the company for a decade — or whether the platform transition and network effects will catalyze a step-change in the growth trajectory.

The 2026 guidance provides a starting point for the analysis. Management expects revenue of $323 million to $330 million, representing growth of six to eight and a half percent — an acceleration from the 4.3 percent growth delivered in 2025. Approximately thirteen million dollars of the expected growth comes from inorganic contributions by the Virsys12 and MissionCare Collective acquisitions, meaning organic growth is expected in the three to five percent range. Adjusted EBITDA guidance of $73 million to $77 million implies margins holding steady or expanding slightly.

The platform strategy payoff remains the biggest open question. The hStream architecture is live, HLX is in market, the Developer Portal is gaining traction with 460-plus developers, and RPO is growing at eleven percent. But converting platform adoption into revenue acceleration requires customers to deepen their usage — buying more modules, integrating more data, building on the APIs — and that process takes time in healthcare. The hospitals that adopt HLX in 2026 will not generate full-year revenue contributions until 2027 or 2028. The Career Networks need to achieve sufficient scale to create genuine marketplace dynamics, which may take several more years. Patient capital, indeed.

International expansion represents an intriguing but unaddressed opportunity. HealthStream's products are designed for the U.S. healthcare regulatory environment, which limits their applicability overseas without significant adaptation. The regulatory frameworks in the UK (governed by the Care Quality Commission), Europe (with its patchwork of national health systems), and Asia (where healthcare delivery models vary dramatically by country) are different enough to require substantial content development and workflow customization. Whether the addressable market justifies that investment is an open question that management has not publicly addressed in detail. The October 2025 acquisition of Virsys12 — a Salesforce-based credentialing platform serving payer and health plan enterprises — suggests that Frist sees more opportunity in expanding across the U.S. healthcare value chain (from hospitals to insurers) than in expanding geographically. This is a reasonable prioritization for a company with limited resources relative to the size of the domestic opportunity.

The role of AI is likely to evolve from a product feature to a strategic imperative. HLX's AI-first design — using large language models for content recommendation, learning pathway personalization, and manager assistance — positions HealthStream at the leading edge of healthcare workforce development technology. But AI in healthcare is a double-edged sword: the potential for efficiency gains is enormous, but the regulatory scrutiny and liability implications of AI-driven decisions in clinical contexts are equally significant. HealthStream will need to navigate this terrain carefully, balancing innovation with the conservative risk tolerance of its hospital customers.

The ownership structure raises a question that every long-term investor must consider: succession. Bobby Frist is a founder-CEO with thirty-five years of tenure and an 18.4 percent ownership stake. His strategic vision has guided every major decision the company has made. What happens when he steps back — whether by choice or by time — is a risk that the market has not yet had to price.

This is not an idle concern. The healthcare technology sector has seen a wave of private equity acquisitions in recent years, with firms like Thoma Bravo, Vista Equity Partners, and Veritas Capital aggressively consolidating healthcare IT companies. HealthStream's combination of recurring revenue, high switching costs, a debt-free balance sheet, and a category-leading market position makes it a textbook PE candidate. A private equity firm could acquire HealthStream, lever up the balance sheet, accelerate the platform migration through investment, cross-sell aggressively, and harvest the recurring revenue stream over a five-to-seven-year hold period. Whether Frist would entertain such a transaction is unknown — his 18.4 percent stake gives him significant blocking power, and his personal attachment to the company suggests he would be a reluctant seller. But investors should be aware that the question exists, and that the stock price might someday reflect a control premium.

The long-term vision Bobby Frist has articulated is ambitious: owning the entire healthcare workforce lifecycle, from student to retiree, across learning, credentialing, scheduling, and career management. If the hStream platform becomes the operating system for healthcare workforce management — the single pane of glass through which hospitals manage their most valuable and most expensive resource — then HealthStream's current valuation may prove to be a fraction of its eventual worth. If the platform transition stalls, if the career networks fail to achieve escape velocity, if a well-funded competitor builds a comparable offering — then HealthStream remains what it has been: a durable, profitable, slow-growing niche leader. Both outcomes are plausible, and the tension between them is what makes the story worth watching.

XIII. Lessons for Founders & Investors

HealthStream's thirty-five-year journey from Nashville startup to healthcare infrastructure company offers several lessons that extend well beyond its specific industry.

Boring is beautiful. The most durable businesses are often the least exciting to describe. Compliance training, credentialing verification, shift scheduling — none of these categories will ever generate the kind of enthusiasm reserved for artificial intelligence, electric vehicles, or social media. But they generate something more valuable: predictable, recurring revenue with high switching costs and regulatory-driven demand. The companies that build essential infrastructure for regulated industries may never achieve viral fame, but they compound wealth over decades with a consistency that glamorous growth stories rarely match.

Regulatory moats are real and underappreciated. Investors often focus on technological innovation as the primary source of competitive advantage, but in healthcare, regulation creates a form of structural demand that no amount of innovation can replicate. Hospitals must train their staff on OSHA requirements. They must verify their physicians' credentials. They must comply with Joint Commission standards. These are not preferences — they are legal obligations backed by the threat of Medicare decertification, malpractice liability, and loss of operating licenses. Any company that embeds itself in the compliance workflow of a regulated industry benefits from demand that is not discretionary, not cyclical, and not subject to the whims of buyer preference.

Founder patience is a competitive advantage. Bobby Frist has led HealthStream for thirty-five years. He survived the dot-com bust, navigated years of operating losses, executed a decade of acquisitions, and is now orchestrating a platform transition — all while maintaining an ownership stake that ensures he eats his own cooking. This kind of long-term orientation is rare in public markets, where CEO tenure averages less than seven years and activist investors push for quarterly optimization. The companies that build the most durable advantages are often led by founders who think in decades, not quarters — who are willing to sacrifice short-term growth for long-term positioning.

Platform transitions are multi-year endeavors. HealthStream spent years building the hStream architecture, and the "Year of the Platform" designation in 2025 marks not a completion but an inflection point. Transforming a collection of SaaS applications into a unified platform ecosystem requires re-architecting technology, re-educating customers, re-training sales teams, and re-orienting an entire organization around a new set of strategic priorities. There are no shortcuts, and the results take time to appear in financial statements.

Network effects do not happen overnight. The Career Networks strategy — NurseGrid, myClinicalExchange, myCNAjobs — is HealthStream's most ambitious bet, and it will take years to determine whether genuine two-sided marketplace dynamics emerge. Building a network requires achieving critical mass on both sides — enough healthcare workers to attract employers, enough employers to attract healthcare workers — and that chicken-and-egg problem is the hardest challenge in platform businesses.

Deep vertical focus beats horizontal expansion. HealthStream has resisted the temptation to become a general-purpose learning management system serving all industries. By staying focused exclusively on healthcare, it has built domain expertise, content libraries, and customer relationships that horizontal competitors cannot easily replicate. The lesson is counterintuitive: in a world that rewards scale, going narrow can be more powerful than going broad, provided the vertical is large enough and defensible enough to sustain a significant business. Healthcare alone employs over twenty million Americans — a vertical that is larger than the entire economy of many countries.

There is one more lesson that may be the most important of all: the value of thinking in decades rather than quarters. Bobby Frist founded HealthStream in 1990 and is still running it in 2026. He survived a stock price of seventy-five cents. He survived years of single-digit growth. He survived the skepticism of investors who wanted faster returns and analysts who questioned whether the company could ever become more than a niche player. Through all of it, he kept building — acquiring capabilities, developing content, deepening customer relationships, constructing a platform — with the patience of someone who understood that the most valuable infrastructure is the kind that takes decades to construct and proves impossible to displace once built.

XIV. Epilogue

In December 2025, HealthStream completed the acquisition of MissionCare Collective — adding 5.2 million caregivers to its network for up to forty million dollars. It was the kind of deal that perfectly encapsulates the company Bobby Frist has built: strategically coherent, financially disciplined, and almost entirely ignored by the broader market.

HealthStream's stock trades at a valuation that reflects the market's ambivalence about companies that grow steadily rather than explosively. The ownership structure tells its own story: institutional investors hold approximately seventy percent of shares, insiders hold about twenty percent — with Frist himself accounting for the lion's share — and the public float is a relatively thin ten percent. This concentrated ownership means the stock is less liquid than most NASDAQ-listed companies of similar market capitalization, which can amplify price movements in both directions. The company bought back thirty million dollars of its own shares in 2025 and increased its dividend by nearly thirteen percent — capital returns that, combined with the thin float, signal a management team that is quietly but consistently returning value to shareholders who stick around.

There is a category of public company that rarely makes headlines, never trends on social media, and would not be recognized by ninety-nine percent of individual investors — yet quietly powers the essential operations of an entire industry. HealthStream is one of these companies. It does not deliver drugs or manufacture medical devices or operate hospitals. It does something arguably more fundamental: it ensures that the five million people who do those things are trained, credentialed, and scheduled to do them properly.

In healthcare, the most valuable companies are not always the most famous. Sometimes they are the ones keeping the lights on — one learner at a time.

XV. Further Reading & Resources

Primary Sources: HealthStream Investor Relations (ir.healthstream.com); HealthStream 10-K Annual Reports (2020–2025); Quarterly Earnings Transcripts; CEO Bobby Frist interviews and conference presentations.