Host Hotels & Resorts: The Empire Behind the Brands

I. Introduction & Episode Roadmap

Walk into the New York Marriott Marquis on a Tuesday in Times Square. Ride the glass elevators up through the atrium, past the revolving rooftop restaurant, into a ballroom the size of a football field where a pharmaceutical company is holding its annual sales meeting. Every guest in that building believes they are staying with Marriott. The logo is on the pens, the robes, the app that let them skip the front desk. Not one of them is thinking about who actually owns the 1,966 rooms above their heads, the steel, the land, the elevators, the roof.

The answer is a company almost none of them have ever heard of: Host Hotels & Resorts, the largest lodging real estate investment trust in the world. Host owns the New York Marriott Marquis. It owns the Orlando World Center Marriott. In 2024 it bought The Ritz-Carlton Oʻahu, Turtle Bay on the North Shore of Oʻahu. It owns roughly 41,839 rooms across 76 consolidated hotels, and in fiscal 2025 those hotels generated $6.11 billion of revenue and $1.757 billion of Adjusted EBITDAre.1 And yet Host has no consumer brand, no loyalty program, no reservation system, and no employees checking you in. It is a landlord that owns some of the most famous hotels on earth and lets other companies put their names on the door.

That is the central paradox worth sitting with. In an era obsessed with brands, platforms, and asset-light software margins, how does a company that owns nothing but heavy physical real estate — buildings that require constant, expensive renovation just to stand still — remain relevant, let alone valuable? To answer that, you have to understand a divorce.

The hospitality industry underwent one of the great strategic separations in American corporate history: the severing of owning hotels from operating them. Marriott, Hilton, Hyatt, and IHG spun the bricks out and kept the brands. They became fee-collecting management and franchise machines with almost no real estate on the balance sheet. Someone, though, still had to own the buildings. Host is what happens when you become the professional, institutional owner of the buildings the brand companies no longer wanted to hold.

This is the story of how Host was born — not out of ambition, but as a corporate landfill for Marriott's toxic 1990s debt. It is the story of how that landfill reorganized itself into a tax-advantaged REIT, went on a pre-crisis buying spree that bought it the Starwood portfolio and a new name, and then, under a former deal lawyer named James Risoleo, reinvented itself again as a disciplined capital-recycling machine that sells slow assets high and buys irreplaceable ones.

Three themes run through everything. The first is the asset-heavy versus asset-light split — why the industry divorced ownership from operation, and who really got the better end. The second is what we will call the treadmill CapEx battle — the permanent, structural friction between the owner (Host, which wants net operating income) and the brand manager (Marriott or Hyatt, which wants gross revenue and pristine brand standards) over who pays for renovations and how much. The third is capital recycling — Risoleo's rejection of buy-and-hold real estate dogma in favor of constant portfolio rotation. Whether that rotation actually creates value, or merely creates activity, is one of the questions a skeptical investor should keep asking as this story unfolds.

One more framing before the history, because it sets the analytical posture for everything that follows. It is tempting, with a company this large and this successful at surviving, to narrate it as a triumph — to accept management's telling that discipline and irreplaceable real estate add up to an unbeatable machine. That is not the job here. Host is also, unavoidably, a bet on a single deeply cyclical industry, dependent on brands it does not control, filling rooms through loyalty programs it does not own, and spending a rising share of its cash flow just to keep its buildings from aging out of relevance. A useful reading holds both truths at once: a genuinely advantaged owner of scarce assets, and a business with structural leaks and cyclical exposure that no balance sheet fully seals. The point of the sections ahead is to test the bull case against evidence rather than to recite it — to ask, at each turn, what the numbers and the behavior actually prove. Let's start where it started: with a company drowning in debt.

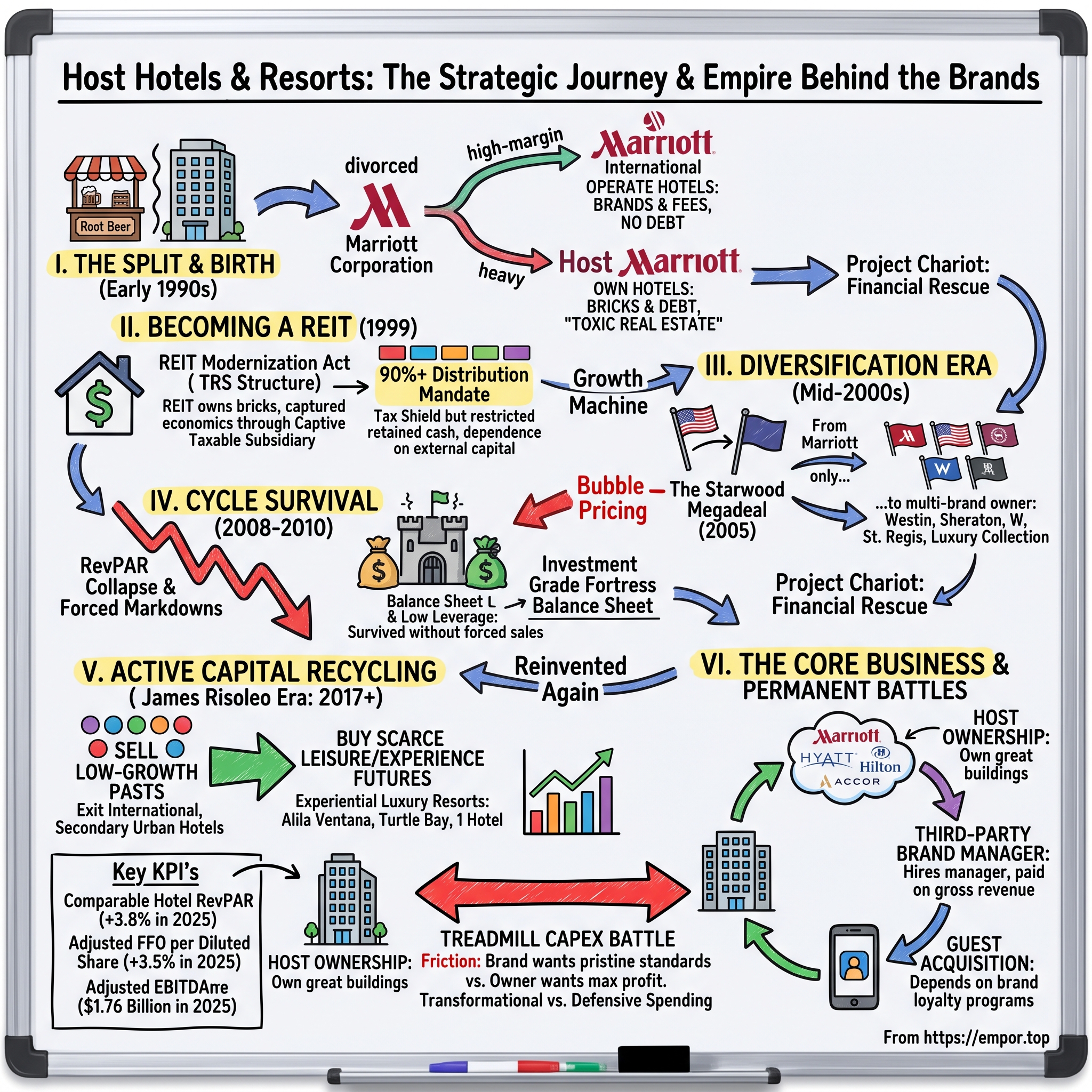

II. Project Chariot: The Split that Saved Marriott

In early 1992, J.W. "Bill" Marriott Jr. had a problem that could have ended the company his father founded from a nine-stool root beer stand in 1927. Marriott Corporation had spent the late 1980s building hotels at a furious pace, on a specific and, in hindsight, fragile assumption: that it would develop hotels, then sell them to limited partnerships and syndicators and outside investors, while keeping the lucrative long-term contracts to manage them. Build, sell, manage, repeat. It was an elegant machine — right up until the early-1990s real estate crash and the 1986 tax reforms vaporized the market for exactly the kind of syndicated real estate Marriott was manufacturing.[^4]

The result was a balance sheet buried under roughly $2.9 billion of debt and a warehouse full of hotels the company had built to sell and now could not.[^4] The stock was punished. Bankruptcy was not an abstract fear. Into this walked one of the most inventive financial minds of his generation.

Stephen F. Bollenbach was a corporate finance specialist with a résumé for exactly this moment — he had restructured Donald Trump's over-levered casino empire and would later become CFO of The Walt Disney Company, where he engineered the acquisition of Capital Cities/ABC, before running Hilton Hotels as CEO. Marriott hired him as chief financial officer in 1992 for one reason: his talent for corporate restructuring.[^4] What he proposed became known internally by a code name — Project Chariot — and it was audacious enough that when it leaked in October 1992, it detonated.

The idea was to split Marriott Corporation into two publicly traded companies along the industry's deepest fault line: the split between the brand and the bricks.

On one side would sit Marriott International — the crown jewel. It would keep the brand names, the management and franchise contracts, the reservation system, the loyalty program, the software, the reputation, and the growth. Crucially, it would carry almost none of the debt. This was the high-margin, capital-light, fee-collecting business, and it went to Bill Marriott. On the other side would sit Host Marriott — the bricks. It would hold the physical hotels, the airport and toll-road concessions, the low-growth operating assets, and nearly all of the parent company's long-term debt.[^4] Richard Marriott, Bill's brother, would chair it. In plain terms: one twin got the family jewelry, the other got the family mortgage.

It is worth pausing on the human stakes, because this was a family business, not an abstraction. Bill Marriott had spent his life building the operating company his father, J. Willard Marriott, had started with a root beer stand; the brand carried the family name and the family's identity. To hand the good company to Bill and the debt to Richard was not a neutral engineering choice — it was a decision about which brother would steward the legacy and which would manage the liability. Bollenbach, an outsider brought in precisely because he had no sentimental attachment to any of it, could see the two businesses clearly as separate financial animals in a way the family, understandably, could not. His detachment was the point. A restructuring specialist's job is to look at a beloved institution and ask the cold question: which parts of this are actually worth more apart than together?

You can imagine how the people holding that mortgage reacted. Marriott's bondholders — institutions who had lent money to what they believed was a single, integrated, investment-grade company, some of whom had bought a fresh $400 million bond offering just months earlier — watched the announcement wipe value off their holdings as they realized their claims were about to be marooned inside the debt-laden real estate entity. A group led by PPM America sued, and the litigation, argument, and public fury that followed cast Host Marriott, in the memorable framing of the era, as a "toxic real estate trash can" into which the good company was dumping its problems.[^4] Bollenbach ultimately defused the revolt by restructuring the debt terms, sweetening the arrangement, and letting the passage of time do the rest — as the economy recovered, the split companies' equity soared and the bonds recovered toward par.

Here is the part worth pausing on, because it is the intellectual seed of the entire modern industry. Project Chariot was not just a balance-sheet trick. It was a philosophical declaration: that operating a hotel and owning a hotel are two fundamentally different businesses, with different economics, different risk profiles, different investors, and different ideal capital structures. Managing hotels is a people-and-brand business that throws off high-margin fees and needs almost no capital. Owning hotels is a real estate business that is capital-intensive, cyclical, and leveraged. Bolting them together, Bollenbach argued, mispriced both.

Every major lodging company eventually followed, and the logic compounded on itself. Once one brand demonstrated that shedding real estate and living on management and franchise fees produced higher margins, cleaner balance sheets, and richer stock-market valuations, the rest could not afford not to. Hilton, IHG, and later Marriott itself pushed toward near-total asset-light models, selling real estate and keeping fees; the industry reorganized around the principle that the brand is the durable, high-return asset and the building is the low-return commodity someone else should finance. The asset-light hotel management model that is now industry gospel was, in effect, pioneered in this act of financial desperation. And notice the quiet irony buried in the celebration of asset-light: it only works if someone, somewhere, is willing to be asset-heavy — to own the buildings the brands walked away from. The entire elegant, capital-light superstructure of modern hospitality rests on the existence of professional owners willing to carry the bricks. Host is the largest of them. But the split also created an orphan. Somebody still had to own the buildings. That orphan, handed the debt and the bricks and told to survive, is the company this story is about — and its next move was to escape the very tax structure that was strangling it.

III. The Reconstitution: Becoming a REIT

Host Marriott spent the mid-1990s doing something unglamorous and essential: not dying. It sold assets, refinanced the debt it had been saddled with, and slowly rebuilt a balance sheet that had been engineered to be somebody else's problem. But even as it stabilized, a structural flaw sat at the heart of its design. Host owned cash-generating real estate, yet it was organized as an ordinary "C" corporation. That meant its profits were taxed twice — once at the corporate level, and again when distributed to shareholders. For a company whose entire reason to exist was owning income-producing property, this was like running a marathon in a lead vest.

There was a well-worn escape hatch in the U.S. tax code, built precisely for companies like this: the real estate investment trust. Created by Congress in 1960 to let ordinary investors own income-producing real estate the way they own stocks, a REIT pays essentially no corporate income tax — provided it distributes at least 90% of its taxable income to shareholders each year and meets strict tests on what it owns and how it earns.[^5] For Host, converting to a REIT meant it could keep the cash the taxman had been taking and redirect it to paying down debt, funding renovations, and paying dividends.

So on the cusp of 1999 — effective at the very end of the 1998 tax year — Host Marriott reorganized itself as a REIT.[^5] On paper, it was an elegant fix. In practice, it collided immediately with an awkward rule.

Under the tax law as it stood in 1998, a REIT was forbidden from operating its own hotels. It could own the building and collect rent, but it could not itself run the front desk, employ the housekeepers, or book the rooms — because the income a hotel earns from actually selling rooms and meals was considered "active" business income, not the "passive" rental income a REIT is designed to collect. This is the catch at the center of every hotel REIT's existence: a hotel is not like an office tower where you sign a tenant to a 10-year lease and collect a check. A hotel re-rents every room every single night. Its income is inherently operational.

Host's first workaround was clumsy. To comply, it spun off its hotel-operating and senior-living businesses into a separate company, Crestline Capital Corporation, and then leased its hotels to Crestline, which operated them and paid Host rent.[^5] Host became a landlord to a tenant it had just created — a structure that satisfied the letter of the law but leaked economics at every seam, since the profit from running the hotels now accrued to Crestline's shareholders rather than Host's.

The fix arrived almost immediately, and it reshaped the entire industry. In December 1999, Congress passed the REIT Modernization Act, which, effective in 2001, allowed a REIT to lease its hotels to a wholly owned "Taxable REIT Subsidiary," or TRS.[^5] The elegance is worth appreciating. The TRS is a taxable corporation that the REIT owns. The REIT leases its hotels to itself — to its own TRS — and the TRS in turn hires an independent brand manager like Marriott to actually run the hotel. The TRS pays a modest layer of corporate tax on the operating profit, but Host now captured the economics of running its hotels while keeping the REIT's tax shield on the rent. Host promptly brought the tenant function back in-house and unwound the Crestline arrangement.

There is a subtler consequence of the REIT structure that shapes everything Host does, and investors should hold it firmly in mind. The 90%-distribution mandate is a double-edged sword. On one edge, it is a discipline: management cannot quietly hoard cash to build an empire, because most of the taxable income has to go out the door to shareholders each year. On the other edge, it is a constraint: a REIT retains relatively little of its own cash flow, which means that to grow — to buy Turtle Bay, to fund a transformational renovation — it must repeatedly return to the capital markets, issuing debt or new equity. That dependence on external capital is precisely why a hotel REIT's cost of capital and balance-sheet quality are not accounting trivia but the core competitive variable. A REIT that must issue equity when its own stock is cheap dilutes its shareholders; one that can fund itself with cheap debt and self-help dispositions grows without punishing them. Everything downstream — the fortress balance sheet, the capital recycling, the obsession with per-share metrics — flows from this structural reality that the REIT gives up its own retained earnings in exchange for its tax shield.

This is the corporate DNA of every modern lodging REIT: own the building through the REIT, operate it through a captive taxable subsidiary, and hire a third-party brand to manage it. It looks like bureaucratic plumbing, and it is — but that plumbing is what makes the whole thing legal and tax-efficient. With the structure finally rationalized, Host had a machine that could grow. And in 2005, it decided to grow all at once, with the biggest bet in its history.

IV. The Starwood Megadeal & Changing of the Flag

By the mid-2000s, the world was awash in cheap money, and real estate was the party everyone wanted to attend. Private equity firms were raising record funds. Cap rates — the yield a buyer accepts on a property, which moves inversely to price — were compressing to levels that made every asset look expensive and every seller look smart. Host, now a healthy REIT with a rehabilitated balance sheet, had a strategic itch it wanted to scratch. It was, essentially, a one-brand company. Its portfolio was overwhelmingly Marriott-flagged, a legacy of its birth. If Marriott's brand or fortunes ever wobbled, Host's entire portfolio wobbled with it.

The cure appeared in the form of a complex, multi-party transaction with Starwood Hotels & Resorts Worldwide, a company then racing to shed real estate and become asset-light itself. In November 2005, Host Marriott announced it would acquire a portfolio of 38 luxury and upper-upscale hotels from Starwood for consideration of roughly $4 billion, in a cash-and-stock deal that would vault Host into a genuinely diversified multi-brand owner.4

In one stroke, Host broke its dependence on the Marriott flag. The portfolio brought Westin, Sheraton, W, St. Regis, and Luxury Collection properties into the fold — brands Host had never owned. It brought an international footprint in Europe and Asia (a footprint Host would, tellingly, later dismantle to refocus on North America). And it brought scale: the combined company vaulted to the top of the U.S. lodging industry, and to reflect its new identity as a landlord to many brands rather than a captive of one, the company changed its name in 2006 from Host Marriott Corporation to Host Hotels & Resorts, Inc.4 The old name announced servitude to a single brand. The new name announced independence from all of them.

There is a temptation to tell this as a triumph, and the outline hands us that framing. A neutral read is more textured. Host bought this portfolio at what turned out to be very near the top of the pre-Global Financial Crisis real estate bubble. Within roughly two years, the crash would arrive, hotel demand would collapse, and every asset bought at 2005–2006 prices would look, on a mark-to-market basis, like a mistake. Timing is not a footnote in real estate; it is often the whole game. Anyone assessing management's acquisition instincts should hold both facts in mind at once: the Starwood deal was strategically correct — diversification, scale, a new identity — and it was executed at a cyclically brutal price.

And the crash, when it came, was not gentle. Between 2008 and 2010, business and group travel evaporated, RevPAR across the industry fell off a cliff, and the value of every hotel bought at bubble prices was marked down hard. A more leveraged owner would have been forced to sell its best assets at the worst possible moment — the classic way real estate fortunes are destroyed. Host's international ambitions, too, aged poorly: the European and Asian footprint the Starwood deal delivered added complexity, currency exposure, and management distraction far from Host's home market, and over the following decade Host would methodically unwind most of it, exiting joint ventures and refocusing the portfolio squarely on North America. The lesson the company appears to have internalized is that geographic sprawl looks like diversification on a map and feels like fragility on a balance sheet.

What redeemed it was duration. Host did not have to sell into the crash. As a REIT with permanent capital and a portfolio of buildings on land that cannot be replicated, it could hold irreplaceable assets — the Westin sitting on prime downtown blocks, the resorts on coastlines that will never be re-zoned — through a full cycle and out the other side. The land-grab logic proved durable even though the entry multiple was punishing. And in the process, Host established something less tangible but more valuable than any single hotel: it became the institutional owner of choice for the world's leading brands, the counterparty a Marriott or a Hyatt or a Westin wanted holding its flagship real estate. It is worth being concrete about what that reputation actually buys, because "partner of choice" can sound like a platitude. When a brand wants to seed a new hotel or convert an existing one, it needs an owner who can write a large check, close reliably, fund the required capital, and be a sophisticated counterparty across a 20-to-30-year management agreement rather than a distressed seller three years later. Host offers exactly that profile — scale, permanence, and creditworthiness — which is why brands are willing to sweeten deals with "key money," the cash a manager pays an owner to win or keep a management contract, as Marriott did on Turtle Bay. Key money is the tell that the relationship runs both ways: the brand needs great owners as much as owners need great brands, and Host's size makes it one of the few counterparties that can play at the top of that market. That reputation, more than the buildings, is what the next CEO would spend a decade monetizing — by learning when not to hold.

V. The James Risoleo Era: Active Capital Recycling

In January 2017, Host handed the corner office to a man who had spent two decades on the other side of its deals. James F. Risoleo was not a hotelier who had come up through front-desk operations. He was a lawyer and a dealmaker — a longtime head of Host's acquisitions and investments function — who had personally lived through the Starwood purchase, the crash, and the recovery.10 He took over from W. Edward Walter, and he brought with him a conviction forged by watching the company buy high in 2006: that the sacred real estate commandment of buy and hold forever was, for a hotel REIT, a trap.

Risoleo's counter-doctrine is the through-line of the modern company, and it has a name: capital recycling. The thesis is deceptively simple. A hotel is not a bond you clip coupons on for thirty years. It is a wasting, capital-hungry asset whose competitive position and cash flow drift over time. So instead of holding everything, Host should behave like an active portfolio manager — continuously selling assets whose future growth looks tired or whose renovation bills loom large, and redeploying the proceeds into assets with better growth, higher room rates, and more defensible locations. Sell the past, buy the future, and let the spread between the two multiples be the value creation.

In practice that meant an unsentimental cleanup. Host exited its international joint ventures in Europe and Asia. It sold slower-growth, capital-intensive urban hotels in secondary markets. And it pushed the portfolio toward what Risoleo believes the affluent traveler increasingly wants: experiential, high-average-daily-rate luxury resorts in places that are hard to build near. Then came the event that stress-tested every word of Risoleo's doctrine at once: the COVID-19 pandemic. In the spring of 2020, hotel demand did not decline — it vanished. Occupancy at full-service and group hotels collapsed toward single digits as conventions cancelled, borders closed, and business travel stopped cold. For a lodging owner, it was the closest thing to a controlled experiment in existential risk: revenue near zero, fixed costs stubbornly high, and no visibility on when guests would return. Companies that had spent the prior decade loading up on debt to juice returns suddenly faced a brutal arithmetic, and several hotel owners were pushed to the brink.

This is where the unglamorous discipline paid off. Because Risoleo had insisted on running low leverage and hoarding liquidity in the good years — a posture that had looked conservative, even dull, to investors chasing higher-octane peers — Host entered the pandemic with the financial oxygen to survive it. The company suspended its dividend to preserve cash, drew down and rebuilt liquidity, and, crucially, avoided the forced sales that hollowed out weaker owners. When demand began to recover, Host was not repairing its balance sheet; it was going shopping. The affluent-leisure resorts that boomed as pent-up travelers sought experiences were exactly the assets Host wanted more of, and it had the capacity to buy while others were still bandaging wounds. The pandemic, in other words, was the moment the fortress-balance-sheet philosophy stopped being a talking point and became a demonstrated survival advantage — the single most important piece of evidence in the entire management-credibility file, because it was tested by reality rather than asserted on a slide.

The clearest early expression of the buying that followed was the 2021 purchase of the Alila Ventana Big Sur, a small, ultra-luxury resort perched on the California coast, for roughly $150 million — a deal that bought not rooms but scarcity, on cliffs no competitor can replicate.10

The doctrine's boldest test came in 2024, when Host deployed roughly $1.5 billion across four properties. The centerpiece was The Ritz-Carlton Oʻahu, Turtle Bay on Oʻahu's North Shore, acquired for a total deal value of approximately $725 million — about $680 million net of key money paid by Marriott — including 450 rooms and, critically, a 49-acre parcel entitled for development.5 The mechanics here reveal the whole playbook. Host bought the asset, immediately transitioned management to Marriott, converted the flag to Ritz-Carlton, and took control of developable land. The initial purchase multiple looked rich — a premium price for a premium view. But the value engine is not the price paid on day one; it is the repositioning: a better brand drives higher rates, the key money from Marriott lowers the effective basis, and the land parcel is free optionality. Host argues the deal becomes accretive on a forward basis as those levers pull. That is the bull framing, and it is management's; the bear note is that it depends on execution the market cannot yet verify.

The same year brought 1 Hotel Central Park, a 234-room luxury property acquired for $265 million — a rare high-yield luxury footprint in Manhattan bought at a more attractive entry multiple than Turtle Bay — and, in Nashville, the 215-room 1 Hotel Nashville together with the 506-room Embassy Suites by Hilton Nashville Downtown for a combined $530 million, adding high-margin group and leisure exposure in one of the country's fastest-growing metros.6

The multiples tell the strategic story in shorthand, and they are not all flattering. By external analysis of the 2024 spree, Turtle Bay was bought at roughly 16 times its trailing EBITDA — a full price, a low-single-digit cap rate, exactly the kind of premium a disciplined buyer is supposed to avoid — while 1 Hotel Central Park was bought closer to 11 times, a far more attractive entry.10 The bull argument for paying up on Turtle Bay rests entirely on the forward math: transition the flag to Ritz-Carlton, capture Marriott's key money to cut the effective basis, and unlock the 49-acre development parcel, and the multiple is supposed to compress toward the low-teens as EBITDA grows into the price.510 This is the crux of the "changing of the flag" concept — the deliberate re-branding of an asset to reset its earning power. It can work spectacularly; it can also be the story a buyer tells to justify overpaying. The honest position is that on Turtle Bay the verdict is genuinely unproven, and a diligent investor should track whether that asset's EBITDA actually climbs toward the pro-forma promise or stalls, leaving Host having paid a trophy price for a trophy view.

Does the recycling actually work, or is it expensive motion? Here the 2025 evidence is more concrete than management rhetoric. On the sell side, Host sold the Four Seasons Resort Orlando and a Jackson Hole resort for a combined $1.1 billion at a 14.9x EBITDA multiple, a price CFO Sourav Ghosh's team pegged at roughly an 11% unlevered internal rate of return over the hold.2 Selling stabilized luxury at nearly 15 times cash flow and redeploying toward assets bought at lower multiples is, mechanically, the arbitrage the strategy promises. On the Q4 2025 call, Risoleo was blunt about the posture: the company was "testing the market with dispositions," and "everything is for sale at the right price."2 That is either admirable discipline or a warning that nothing is truly core — a skeptic can read it both ways.

The financial framing that makes this credible is governance. CEO Risoleo and CFO Ghosh are compensated heavily through long-term equity tied to relative total shareholder return against the MSCI US REIT Index and to Adjusted FFO-per-share growth, a structure explicitly designed to discourage empire-building through dilutive, scale-for-scale's-sake acquisitions.7 And the balance sheet is the enabler: Host runs at investment-grade leverage — 2.6x net-debt-to-EBITDA at the end of 2025, against a stated low-leverage target — with $2.4 billion of liquidity.2 That fortress is not defensive vanity. It is a strategic weapon: when over-levered private-equity owners hit refinancing walls in a higher-rate world, the buyer with cash and investment-grade access gets to set the price.

The partnership at the top reinforces the point. Sourav Ghosh, who rose through Host's own ranks in strategy and finance before taking the CFO seat, is the disciplinarian half of a deliberate pairing: Risoleo the dealmaker who sees the asset, Ghosh the capital allocator who polices the price and guards the balance sheet. On the earnings calls, the division of labor is audible — Risoleo narrates strategy and demand, Ghosh walks the numbers, the leverage, and the guidance with an almost stubborn precision. It is a healthy tension for a company whose greatest historical danger has always been overpaying at the top of a cycle, because the dealmaker's instinct to buy needs a counterweight whose job is to say no. Whether Host consistently deploys that advantage well, rather than merely possessing it, is the question the operating business answers next.

VI. The Core Business: Operations & The "Treadmill CapEx" Battle

Strip away the M&A drama and ask the plainest question: how does Host actually make money on a random Wednesday? The answer is almost boringly focused. Host operates in a single reportable segment — hotel ownership — and the model is to own great buildings, hire great brands to run them, and keep the difference.3 There is no diversification into office, no data-center pivot, no fee-management arm. It is a pure-play bet on premium U.S. lodging real estate.

Look inside the revenue and you see two things. First, the operator mix is concentrated. Hotels managed or franchised by Marriott drove roughly 64% of Host's 2025 hotel revenues, with Hyatt-managed properties representing about 17%; the remainder is split among Hilton, Accor, and independent managers.3 Host paid Marriott alone $187 million of management fees plus about $7.6 million of franchise fees in 2025 — a figure that quantifies exactly how central that single relationship is, and exactly how much leverage the counterparty holds.3 Second, the revenue is high-touch. Roughly 60% comes from selling rooms; the other 40% comes from food and beverage, conferences, spa, golf, and the amenities that define a resort or a big-box convention hotel.3 That F&B-heavy mix is a tell: these are not roadside select-service boxes. They are complex, staff-intensive, experience-driven properties where a wedding, a sales conference, or a Michelin-tier restaurant can matter as much as room occupancy.

The demand feeding those rooms comes in two flavors, and the balance between them is a strategic lever. Transient demand is the individual traveler — the leisure guest, the lone business traveler — who books close-in and pays whatever the rate is that night; it is high-margin and, in a boom, highly profitable, but it is also the first to disappear in a shock. Group demand is the convention, the corporate meeting, the association gathering booked a year or more in advance; it fills large blocks of rooms and drives the banquet, catering, and audiovisual spend that powers the F&B line. Group is less profitable per room than peak transient but far more predictable, because it is contracted ahead. Host's tilt toward massive convention and resort hotels is a deliberate bet on owning the assets where group and high-end transient both want to be — the properties a citywide convention cannot route around. When management on recent calls emphasized recovering group booking pace and a 2026 World Cup tailwind, it was pointing at exactly this: the return of the pre-booked, high-visibility demand that de-risks a full-service portfolio.2

To see why the brand relationship matters so much, follow a single guest to the door. A traveler can book a Host hotel three ways, and each costs the owner a wildly different amount. If she books directly through the Marriott app because she is chasing Bonvoy points, the cost of acquiring her is essentially the brand fee Host already pays — cheap. If she books through an online travel agency like Expedia or Booking.com, that intermediary takes a commission that can run into the mid-teens as a percentage of the room rate — a toll extracted on every such booking. And if the hotel has to discount to fill the room at all, the rate itself erodes. The entire economic case for staying inside a brand's ecosystem is that the loyalty program is a customer-acquisition machine that fills rooms at low cost — think of Bonvoy as a river that continuously flows guests toward Host's doors, guests Host would otherwise have to buy one by one from the OTA toll-collectors. This is the mechanism beneath the abstract phrase "brand dependence": Host does not merely license a name, it rents access to the cheapest source of demand in the industry, and it pays for that access with fees and with the loss of the direct customer relationship.

Now the friction. Host owns the building but does not run it, and that separation — the very split Project Chariot created — plants a structural misalignment at the heart of every hotel. The brand manager is paid a base fee, typically 1.5% to 3.0% of total revenue, plus an incentive fee tied to operating profit. Read that carefully: the base fee rewards the manager for maximizing gross revenue, while Host, the owner, is trying to maximize net operating income. Those are not the same goal. A manager can chase top-line growth and brand prestige with the owner's money — staffing lavishly, discounting to fill rooms, protecting the flag's reputation — in ways that grow the fee while thinning the owner's margin. The owner and the operator are partners on the same asset with subtly opposed incentives, and the entire relationship is a negotiation over who captures the value the hotel produces.

Nowhere is that negotiation sharper than over capital. Brands protect their names by mandating renovations — Property Improvement Plans, or PIPs — on a schedule: soft goods like carpets, drapes, and linens every six to ten years, hard goods like furniture and bathrooms every ten to fifteen.8 If Host refuses to fund a required PIP, it risks the ultimate sanction: losing the flag. And losing the Marriott flag on a hotel is not cosmetic. It severs the property from Marriott Bonvoy — the loyalty engine that funnels guests to the door — and turning a Marriott into an unbranded independent overnight would gut its booking base. So the owner pays.

This is the treadmill. A large share of Host's capital spending is defensive — money laid out not to grow cash flow but merely to maintain brand standards, market share, and RevPAR. It is the cost of standing still, and in an era of high construction and labor inflation, it is a rising cost. This is the single most important structural knock on the hotel-REIT model, and an honest telling has to foreground it: some meaningful portion of the cash Host generates is quietly recycled straight back into the buildings just to keep them from decaying, before a dollar reaches shareholders.

Host's answer is twofold, and here the evidence is genuinely interesting. First, scale as leverage: as Marriott's largest owner, Host negotiates down PIP scopes that a small owner would simply have to accept — using the concentration that looks like a risk as a source of bargaining power. Second, it tries to convert defensive spending into offensive spending. Rather than merely replacing carpets, Host runs "transformational" renovations that reposition an asset — sometimes re-flagging a tired property to a higher luxury brand — to drive a permanent step-change in room rate. Management claims these transformational projects delivered average RevPAR index gains of 8.7 points against a 3-to-5-point target, at mid-teens cash-on-cash returns.2 Picture the difference concretely. A defensive PIP replaces the carpet and drapes in 400 rooms so the hotel keeps looking like a current-standard Marriott — the guest barely notices, the rate does not move, and Host has simply paid to stay in place. A transformational renovation gut-renovates the same hotel into a higher tier, adds a destination restaurant and a reimagined lobby, and re-flags it to a luxury brand — now the property commands a structurally higher average daily rate, and the return is measured not against "we kept the flag" but against a permanent step-up in earning power. The RevPAR index — a measure of how a hotel performs against its direct competitive set — is the scoreboard for whether the repositioning actually took share, and management's claimed 8.7-point average gain, if durable, means these projects are pulling business away from competitors rather than merely refreshing the wallpaper.2 If those numbers hold up across a cycle, they are the best rebuttal to the treadmill critique: proof that Host can occasionally turn the maintenance tax into a growth investment. If they don't, the treadmill wins. That tension — defensive cost versus accretive reinvestment — is the operational heart of the whole enterprise, and it sets up the question of whether Host has any durable competitive advantage at all.

VII. Porter's 5 Forces & Hamilton Helmer's 7 Powers

To decide whether Host is a genuinely advantaged business or merely a large one, it helps to war-game it through two classic frameworks. Start with Michael Porter's five forces, which map where the profit pools leak.

Threat of new entrants is very low, and this is Host's deepest structural protection. You cannot conjure a new 2,000-room hotel into the center of Times Square, or a new beachfront resort onto the North Shore of Oʻahu. Zoning restrictions, soaring construction costs, environmental review, and raw land scarcity make replicating Host's best assets nearly impossible. The barrier is not a patent or a brand — it is physics and municipal law. New supply is the thing that kills hotel returns, and in Host's premium, high-barrier markets, new supply is structurally throttled.

Bargaining power of buyers is mixed. An individual leisure traveler has almost no leverage — they pay the posted rate or they stay elsewhere. But corporate and association group-meeting planners, who book hundreds of room-nights and huge banquet spends at once, have real negotiating power. Host blunts this by owning "must-have" convention and group hotels so large and so well-located that a major citywide event has few substitutes. Scale of box becomes a defense against buyer power.

Bargaining power of suppliers — and here the key supplier is the brand — is high, and it is Host's most uncomfortable force. Marriott and Hyatt control the guest relationship through their loyalty programs; Marriott Bonvoy alone counts well over 200 million members. Host depends on those platforms to fill rooms cheaply, because the alternative — buying guests from online travel agencies like Expedia and Booking.com — carries steep commissions. The brand can mandate spending, collect fees on gross revenue, and threaten the flag. This is the tax Host pays for not owning a consumer brand of its own, and it is permanent.

Threat of substitutes is low to moderate. Airbnb and short-term rentals genuinely disrupted economy and midscale lodging, but they cannot replicate a 100,000-square-foot ballroom, a convention hotel's group infrastructure, or a full-service luxury resort with restaurants, spa, and golf. Host's deliberate tilt toward large group hotels and experiential resorts is, in part, a bet on the segment least exposed to substitution.

Rivalry among competitors is moderate, and worth war-gaming property by property rather than in the abstract. Host's publicly traded peers each occupy a slightly different corner of the same industry. Park Hotels & Resorts, spun out of Hilton, is the closest analogue in scale and in its big-box, group-heavy DNA — a mirror image of Host on the Hilton side of the brand divide. Pebblebrook tilts toward independent and lifestyle hotels in urban and resort markets and runs with more operational hands-on-ness and, historically, more leverage. Sunstone, RLJ, and DiamondRock round out the field with their own mixes of urban, resort, and select-service exposure. What separates Host is not that it owns better hotels in every case — several peers own trophy assets too — but that it owns the largest collection of them with the lowest cost of capital, and that combination is the actual weapon. In a bidding war for a trophy resort, the buyer who can finance most cheaply and close most reliably wins, and Host's investment-grade rating and balance-sheet liquidity make it that buyer more often than not. The more dangerous competitors, though, are the private-equity sponsors — Blackstone chief among them, and the seller of Turtle Bay — because they play a different game: they buy with leverage, renovate, and flip on a three-to-five-year clock, and in a frothy market they will outbid a disciplined REIT that refuses to overpay. Host's edge shows up not when money is cheap and everyone is bidding, but when credit tightens and the leveraged flippers become forced sellers. Cost of capital is a weapon that fires hardest in a downturn.

Now overlay Hamilton Helmer's 7 Powers, which asks not where profit leaks but where durable advantage actually lives. For Host, three of the seven apply, and only loosely.

The primary power is Cornered Resource: irreplaceable real estate. The land under the New York Marriott Marquis and the coastline under Turtle Bay are legally and geographically cornered assets — you cannot build another. This is Host's realest moat, and notably it is the one thing the brand companies don't have. Marriott owns brands anyone can, in theory, out-market; Host owns dirt no one can out-build.

The second is Scale Economies, expressed mainly through cost of capital and procurement. As the largest lodging REIT, Host accesses debt and equity markets at rates smaller peers and private sponsors cannot match, and it buys furniture, fixtures, and equipment in bulk. This is a real but relative advantage — it makes Host a lower-cost owner, not an un-competable one.

The third, Network Effects, is the most important thing to get right, because Host does not own it. The network effects belong to Marriott Bonvoy and World of Hyatt. Host merely piggybacks: every new loyalty member lowers the customer-acquisition cost of filling Host's rooms. That is a benefit Host rents, not a moat Host owns — and it can be repriced against Host at every management-contract renewal. It is just as revealing which of Helmer's powers Host lacks. It has no Branding power — that belongs entirely to Marriott and Hyatt, which is the whole point of the arrangement. It has little Switching Cost leverage over its own guests, who are loyal to Bonvoy, not to Host. It has no Counter-Positioning — Host is not doing something incumbents cannot copy; it is doing the same thing as every other lodging REIT, only bigger and cheaper-funded. And its Process Power is thin, since the day-to-day operating excellence lives with the brand managers. Strip it down and Host has essentially one-and-a-half durable powers: a genuine Cornered Resource in its irreplaceable dirt, and a partial Scale Economy in its cost of capital. That is a narrower moat than the company's size might suggest, and an investor should size the thesis accordingly rather than assume that "largest lodging REIT" automatically means "widest moat."

The honest conclusion from both frameworks is the same: Host's advantage is real but concentrated in one place — the irreplaceability of its physical assets — while the most powerful economic engine in the industry, the loyalty network, sits on the other side of the table. That asymmetry is exactly what the bull and bear cases fight over.

VIII. The Investment-Story Spine: Why Win vs. Why Not

Every real investment debate can be compressed into a single question asked twice: why does this company win from here, and what breaks the case? Host's spine is unusually clean, because the bull and bear arguments are often the same fact viewed from opposite ends.

Start with the bull case. The first pillar is experiential premiumization. Post-pandemic consumer spending shifted structurally toward luxury leisure and high-end experiences, and Host's resort-heavy, premium portfolio sits directly in that current. On the Q4 2025 call, Risoleo attributed the company's demand strength to "the strength of the affluent consumer," and the numbers cooperated — comparable RevPAR growth of 3.8% for the year, roughly 200 basis points ahead of the upper-tier industry.2 Outperforming your own segment is the kind of evidence, not assertion, that a credible edge requires. The second pillar is group and international recovery: corporate group demand and inbound travel filling urban convention hotels in New York, San Francisco, and Chicago, with a specific 2026 tailwind management flagged from the World Cup. The third is the capital-recycling arbitrage already examined — the demonstrated ability to sell stabilized assets near 15x and redeploy at lower multiples.2

Now flip each one over, because the bear case lives on the back of the same coins. Against premiumization stands the capital-intensity treadmill: if labor, construction, and insurance inflation keep rising, defensive PIP spending consumes an ever-larger slice of operating cash flow, leaving less for dividends and growth — and the affluent-consumer tailwind is itself cyclical, the first thing to fade in a downturn. Against the recovery thesis stands cost-of-capital shock: hotels are valued on cap rates, and if interest rates stay structurally higher, cap rates rise, which mathematically pushes portfolio values down even if the hotels themselves perform. A landlord's asset value is hostage to the discount rate. And against the recycling arbitrage stands climate and insurance risk, the most physical threat of all: Host owns coastal luxury resorts in exactly the places extreme weather is intensifying. The 2023 Maui wildfires, which we will examine next, were not a hypothetical — they hit real Host assets and real cash flow.

An activist or a short-seller would press three specific points. First, portfolio and disclosure: Host's single-segment reporting and constant buy-sell churn make it genuinely hard for an outsider to judge whether recycling creates value or just generates transaction fees and narrative — "everything is for sale at the right price" is a philosophy that resists accountability. Second, the fee drag: paying a single manager $187 million a year, on gross revenue, while that manager owns the loyalty relationship, is a permanent structural leak that no amount of scale fully closes.3 Third, capital returns versus reinvestment: Host returned about $860 million to shareholders in 2025 through $205 million of buybacks and $0.95 per share of dividends, plus an expected special dividend of roughly $0.72 per share tied to a $500 million taxable gain on dispositions.2 A bull sees disciplined capital return; a bear asks whether buying back stock and paying special dividends is the best use of cash for a company that also complains about a rising renovation treadmill. Pull the two sides together and the verdict is deliberately unfinished, which is the honest place to leave it. Host wins from here if — and only if — three things hold: the affluent-leisure and group demand that lifted 2025 proves structural rather than a post-pandemic sugar high; the transformational-CapEx engine keeps converting a maintenance tax into genuine rate growth faster than inflation raises the tax; and the recycling machine keeps buying at spreads wide enough to justify the transaction friction. Host loses, or merely treads water, if rates stay high enough to grind down asset values regardless of operations, if the treadmill outruns the repositioning, or if the "everything is for sale" posture turns out to be motion mistaken for progress. Notice that none of these hinge on whether Host owns good hotels — it plainly does. They hinge on execution, cost of capital, and the discipline of a management team that has, so far, earned more trust than it has spent. The resolution of that debate does not live in rhetoric. It lives in a small number of hard operating metrics, and in a risk radar dominated by fire and water.

IX. Strategic Position: Key KPIs & Risk Radar

On the morning of February 18, 2026, Host released its full-year results, and the following day management sat for the earnings call that would frame the story for the year ahead.12 For an analyst dialing in, the temptation is to drown in the supplemental package — dozens of pages of property-level statistics, reconciliations, and non-GAAP tables that a lodging REIT produces every quarter. The discipline is to ignore almost all of it. A company this large moves on a handful of variables, and the skill is knowing which dials tell you whether the machine is actually working and which are noise dressed up as precision.

If an investor could watch only a handful of dials on this company, which ones actually matter? For a lodging REIT, three cut through the noise — and the discipline is to track them over time, not to prize any single quarter's print.

The first is comparable hotel RevPAR — revenue per available room, the product of how full the hotels are and what they charge. It is the purest read on organic room-revenue health because "comparable" strips out the distortion of hotels bought and sold, isolating same-store demand. In fiscal 2025, comparable RevPAR reached $229.24, up 3.8% year over year, with the gains driven more by rate than by occupancy — a healthier mix, because rate flows to the bottom line far more efficiently than filling rooms with discounts.1 The tell to watch going forward is the composition of RevPAR growth: rate-led is strong, occupancy-led is soft, discount-led is a warning.

The second is Adjusted FFO per diluted share — funds from operations, the REIT world's substitute for earnings per share. FFO adds back real estate depreciation (a huge non-cash charge that makes GAAP net income misleading for property companies) to approximate the distributable cash a REIT actually generates. Host delivered Adjusted FFO of $2.07 per share in 2025, up 3.5%, comfortably covering its dividend.1 Per-share is the operative word: it is the metric that exposes whether growth is real or merely bought by issuing equity, which is exactly why management's incentive comp is tied to it.7

The third is Adjusted EBITDAre — a real-estate-specific cash-flow measure used to judge both operating performance and leverage. Host reported $1.757 billion of Adjusted EBITDAre on $6.114 billion of revenue in 2025, and it is the denominator in the 2.6x leverage ratio that anchors the whole balance-sheet story.12 For 2026, management guided to Adjusted EBITDAre of $1.74–1.80 billion and Adjusted FFO of $2.03–2.11 per share — a modest, un-heroic range whose credibility is enhanced by the fact that 2025's results exceeded the company's initial guidance, EBITDAre by 8.5%.1 Beating your own guidance is one of the few clean tests of management honesty about the business, and Host passed it this cycle.

A word on the dividend, because it is where REIT investors most often fool themselves. Host's regular dividend of $0.95 per share in 2025 is not the whole return, and reading it in isolation misleads.1 Because the company is required to distribute realized taxable gains, a big disposition year throws off a special dividend — management flagged roughly $0.72 per share tied to a $500 million taxable gain on 2025 sales.2 That special payout is real cash, but it is a return of capital from selling assets, not recurring income from operating them; a naïve investor who annualizes it as if it were the run-rate yield will badly overestimate the sustainable payout. The disciplined way to read Host is on total return and on Adjusted FFO per share through a cycle — treating buybacks, regular dividends, and lumpy special dividends as different tools the company uses to hand cash back, rather than as a single stable coupon. This is also where the capital-allocation debate sharpens: every dollar paid out as a special dividend or spent on the $205 million of 2025 buybacks is a dollar not reinvested into the portfolio, and whether that is prudent discipline or a company quietly shrinking itself depends entirely on whether it can find assets to buy at better returns than its own shares offer.2

Then there is the risk radar, and for Host it is unusually physical. Climate and catastrophe risk is not an abstraction. The August 2023 Maui wildfires struck three of Host's major Hawaiian properties — the Hyatt Regency Maui, the Andaz Maui, and the Fairmont Kea Lani — and the demand shock imposed roughly a 160-basis-point drag on 2024 comparable RevPAR.9 The recovery has been real: Maui delivered $111 million of EBITDA in 2025 against an initial $90 million expectation, with management guiding toward $120 million in 2026.2 But the episode is a permanent reminder that a portfolio of irreplaceable coastal assets is also a portfolio of assets exposed to fire, storm, and rising seas.

That feeds directly into insurance-premium inflation, a margin headwind almost entirely outside management's control. Property and casualty coverage in Hawaii, Florida, and California has been repricing brutally, and every dollar of premium is a dollar off net operating income. The third radar item is labor scarcity and wage pressure: hospitality is intensely labor-dependent, and a full-service hotel is one of the most labor-heavy assets in real estate — housekeepers, banquet staff, restaurant workers, front desk, engineering. Rising union wages and structural staffing shortages compress margins directly, and because Host does not run the hotels, it must work through its brand managers to bend the cost curve, pushing them toward labor-saving practices like mobile check-in and opt-in housekeeping. This is a subtle governance point worth noticing: on the most important cost line in the business, Host is a passenger, not the driver — it can influence but not dictate how its own hotels are staffed. Comparable hotel EBITDA margin of 28.9% in 2025 slipped 40 basis points year over year — a small figure, and management attributed part of it to the roll-off of one-time Maui business-interruption proceeds received in 2024 rather than to underlying deterioration.1 But the direction is the one the bears watch, because margin is where the treadmill, insurance inflation, and wage pressure all ultimately show up. None of these risks is thesis-ending on its own. Together they define the terrain on which the capital-recycling machine must keep running.

X. Epilogue & Playbook Lessons

Stand back from three decades of this story and the arc is almost novelistic. A company born in 1993 as a debt-laden orphan — the twin who got the mortgage while his brother got the jewelry — clawed its way to a 2026 in which it sits on a fortress balance sheet, owns some of the most valuable hotel real estate on earth, and beats its own guidance in a choppy market.1 The transformation is real. The lesson it teaches is not the one management would put on a slide.

The first lesson is about matching asset duration to capital structure. Host nearly died in the early 1990s not because it owned bad hotels but because it owned long-duration real estate financed with a capital structure that assumed it could sell those hotels quickly. When the exit closed, the mismatch became a crisis. The REIT conversion, the deleveraging, and Risoleo's obsession with investment-grade leverage are all, at bottom, one lesson learned the hard way: own permanent assets with permanent capital, and never again let the financing be more fragile than the thing it finances.

The second lesson is the quiet vindication of the asset-heavy side of the split. The conventional story of Project Chariot is that Marriott International, going asset-light, became the stock-market darling — all those high-margin fees, no capital, endless compounding. That story is true. But it is incomplete. Host proves that the unglamorous twin — the owner of the physical buildings, saddled with the treadmill of renovation and the tyranny of the cap rate — could also build a durable, cash-generative machine, provided it owned the right buildings: the cornered, irreplaceable ones. The asset-light revolution had an unsung winner on the asset-heavy side.

There is a lesson between those two about management credibility measured by behavior, not narrative, and it is the one investors should weigh most heavily because it is the hardest to fake. The most persuasive thing in Host's file is not any single acquisition or any quarter's RevPAR; it is the consistency between what management said it would do and what it actually did when tested. It promised a fortress balance sheet in the good years and was mocked as dull — then the pandemic arrived and the dullness was survival. It set guidance for 2025 and beat it, EBITDAre by 8.5%, rather than the more common pattern of setting a number and quietly missing it.1 It ties its own pay to relative total shareholder return and per-share FFO, structurally discouraging the empire-building that destroys REIT investors.7 None of this proves the future, and a skeptic will rightly note that a rising travel cycle flatters everyone. But target-setting discipline, guidance you can trust, and a stated strategy that survives contact with a crisis are exactly the behavioral evidence that separates a credible management team from a promotional one — and on that scorecard, Host has spent this cycle building trust rather than burning it.

And the third lesson, the one Risoleo would want emphasized and the one a neutral observer should hold most skeptically, is the power of capital recycling — the idea that value in real estate is not merely built and held but continuously rotated out of the low-growth past and into the high-moat future. The 2025 evidence for it is genuine: selling luxury at nearly 15x, redeploying at lower multiples, beating guidance, running low leverage into a market where over-levered rivals may be forced sellers. But the same philosophy that produces discipline — "everything is for sale at the right price" — is also a philosophy that can never quite prove it is creating value rather than manufacturing activity, because there is always another trade to point to.2 The honest verdict is that Host has earned the benefit of the doubt on execution while leaving the ultimate question open: whether a great collection of buildings, run by other people's brands, filled through other people's loyalty programs, and endlessly traded, compounds wealth or merely preserves it. That is the story worth watching from here — one RevPAR print, one PIP negotiation, and one disposition multiple at a time.

References

-

Host Hotels & Resorts, Inc. Reports Results for 2025 — GlobeNewswire, 2026-02-18 ↩↩↩↩↩↩↩↩↩↩

-

Host Hotels (HST) Q4 2025 Earnings Call Transcript — The Motley Fool, 2026-02-19 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Host Hotels & Resorts Form 10-K for the Fiscal Year Ended December 31, 2025 — SEC ↩↩↩↩↩

-

Host Marriott Corporation Announces Acquisition of a Portfolio of 38 Luxury and Upper Upscale Hotels From Starwood; Company to Change Name to Host Hotels & Resorts — Host Hotels & Resorts, 2005-11-14 ↩↩

-

Host Hotels & Resorts to Acquire The Ritz-Carlton Oʻahu, Turtle Bay — Host Hotels & Resorts, 2024-05-29 ↩↩

-

Host Hotels & Resorts Form 10-K for the Fiscal Year Ended December 31, 2024 — SEC ↩

-

Host Hotels & Resorts Definitive Proxy Statement (Form DEF 14A) — SEC, April 2025 ↩↩↩

-

Hotel REITs Face the "PIPs Treadmill" of Property Improvement Plans — CoStar, 2024-03-12 ↩

-

Host Hotels & Resorts Maui Operations Rebound Post-Wildfires — CoStar, 2024-11-06 ↩

-

Host Hotels & Resorts: The Capital Recycling Compounder — Seeking Alpha, 2025-06-18 ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube