Hormel Foods: From Minnesota Meatpacker to Modern Food Empire

I. Introduction & Episode Roadmap

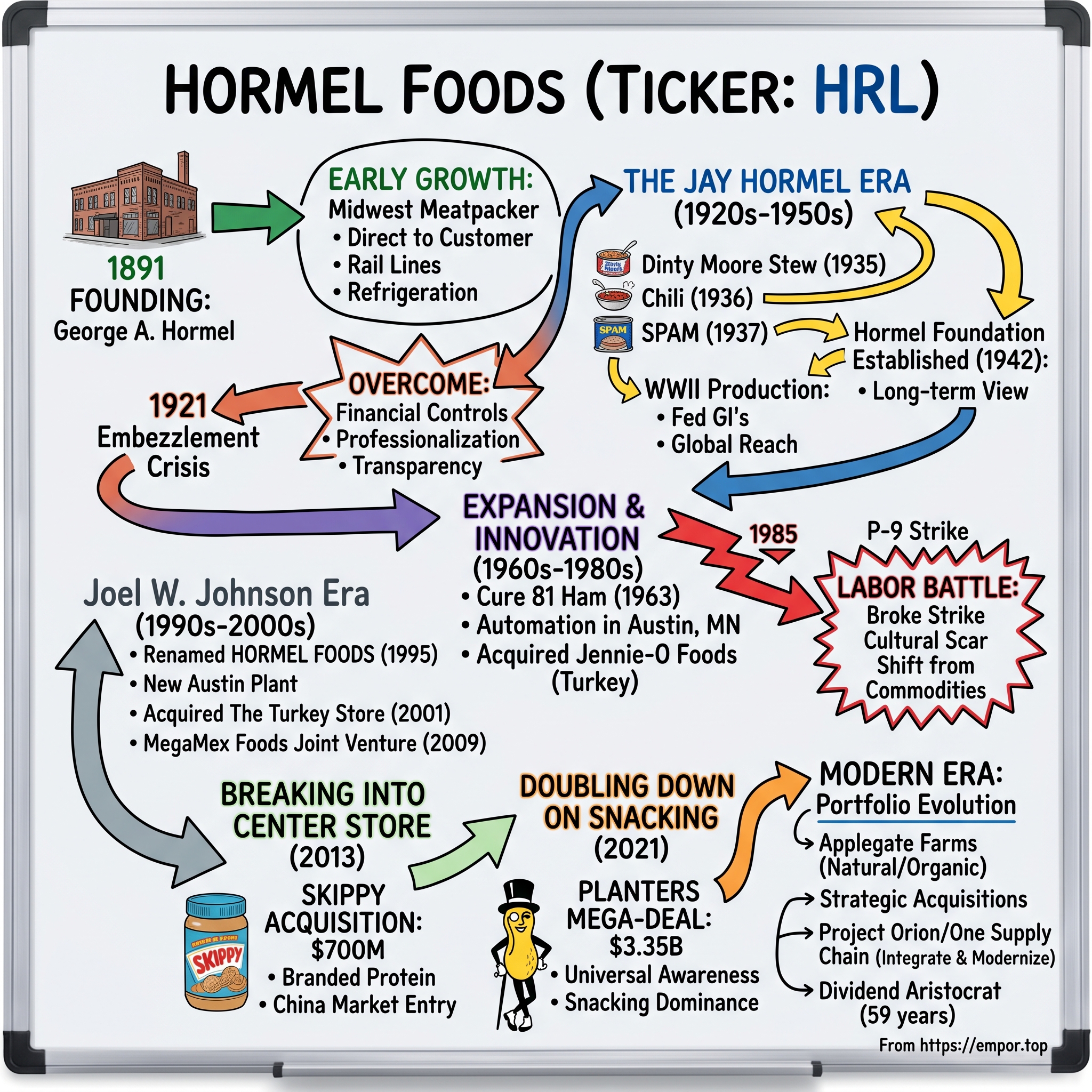

Picture this: It's 1891 in Austin, Minnesota—a small meatpacking town where the smell of smoke and cured ham permeates the cold Midwest air. George A. Hormel, a former tannery worker turned butcher, has just dissolved his partnership and is about to embark on what seems like an impossibly ambitious venture: building his own meatpacking empire from a borrowed creamery building on the Cedar River. Fast forward 130 years, and that scrappy startup has morphed into something George could never have imagined—a $12 billion Fortune 500 company that sells everything from SPAM to Skippy peanut butter to Planters peanuts across 80 countries.

The paradox of Hormel Foods is fascinating: How does a company founded in the era of horse-drawn carriages and ice houses remain not just relevant but dominant in the age of plant-based proteins and direct-to-consumer brands? How does a Midwest meatpacker transform itself into a global snacking powerhouse while maintaining its Minnesota roots and family foundation ownership structure?

Today, Hormel Foods employs more than 20,000 people globally and boasts over 40 brands that rank first or second in their categories. The company that once focused solely on processing hogs in rural Minnesota now generates billions from peanut butter in China, turkey in California, and guacamole in Mexico. It's a transformation story that rivals any Silicon Valley narrative—except this one took 13 decades and involved considerably more pork.

What we're going to explore is a masterclass in corporate evolution: from the early days of George Hormel's direct-to-consumer innovation (yes, even in 1891), through the creation of SPAM—arguably one of the most culturally significant food products of the 20th century—to the modern era's aggressive M&A strategy that brought Skippy and Planters into the fold. We'll examine how the company navigated existential crises: a million-dollar embezzlement that nearly destroyed it in 1921, one of the most brutal labor strikes of the 1980s that tore apart its hometown, and the constant pressure to evolve beyond its meatpacking roots.

The key themes that emerge from Hormel's story read like a business school curriculum: the power of brand building over generations, the delicate art of strategic acquisitions, the complexity of supply chain innovation, and perhaps most uniquely, how a foundation-controlled ownership structure has enabled long-term thinking in an era of quarterly capitalism. This isn't just a story about processed meat—it's about how American food culture evolved, how global supply chains developed, and how a company can reinvent itself while honoring its heritage.

Our journey will take us from ham to SPAM to Skippy to Planters, tracing how each era's leadership responded to its unique challenges while building toward something larger. We'll see how the Hormel family's vision evolved from feeding local communities to feeding the world, and how modern leadership has had to balance the weight of that legacy with the demands of contemporary markets.

II. Founding & Early Years: Building a Meatpacking Foundation (1891–1920s)

The story begins not with grand ambition but with betrayal. In 1891, George A. Hormel discovered his business partner had been skimming profits from their Hormel & Friedrich meat market. Rather than fight it out in court, George made a decision that would define his character and company culture for the next century: he simply walked away and started fresh. With $500 in savings and a fierce determination to control his own destiny, he rented an abandoned creamery building in northeast Austin, right on the Cedar River—location chosen deliberately for its water access and ice harvesting potential.

George Hormel wasn't your typical 19th-century entrepreneur. Born in Buffalo, New York, in 1860, he'd worked in Chicago's notorious meatpacking plants and Toledo tanneries, absorbing lessons about industrial-scale food processing while developing a visceral understanding of what not to do. Where Chicago's packers prioritized volume and efficiency at any cost, George envisioned something different: quality products, fair dealing, and—revolutionary for the time—direct relationships with both farmers and retailers.

The early operation was almost comically small. George personally slaughtered and processed hogs in the morning, delivered products to customers in the afternoon, and kept the books at night. His first employee was his 11-year-old son Jay, who helped after school. But George had timing on his side: Austin sat at the intersection of major rail lines, the local farming community was expanding rapidly, and refrigeration technology was just beginning to make year-round meat processing feasible.

By 1899, George had accumulated enough capital and credibility to make his first major bet: a $40,000 facilities upgrade that would have seemed insane to his competitors. This wasn't just expansion—it was transformation. The new refrigeration facility allowed year-round operations (previously, meatpacking was seasonal work), while electric elevators, modern pumps, and expanded smokehouses quintupled capacity. Most importantly, George installed something radical: a quality control system that tracked products from farm to table, allowing him to guarantee freshness in an era when spoiled meat regularly killed customers.

The company incorporated in 1901 as Geo. A. Hormel & Company, with George holding the majority stake but distributing shares to key employees—an early form of equity compensation that would become a Hormel hallmark. The incorporation coincided with George's most audacious move yet: establishing an export division in 1905. While his competitors fought for domestic market share, George looked overseas, particularly to Europe and South America where American meat products commanded premium prices. The genius of George's export strategy became clear during World War I. By the end of World War I, exports accounted for about 33 percent of the company's yearly sales, a staggering percentage for a company barely two decades old. The war transformed Hormel from a regional player into an international supplier, with government contracts driving unprecedented expansion. The company employed women for the first time in its history as men went off to fight, and production lines ran around the clock to meet military demand.

But success brought vulnerability. In 1921, the company faced its first existential crisis—one that came not from competition or market forces, but from within. When George's son Jay Hormel returned from service in World War I, he uncovered that assistant controller Cy Thomson had embezzled $1,187,000 from the company over the previous ten years. The scale of the theft was catastrophic: the company had borrowed $3 million for operating expenses that year, expecting to repay it from profits that Thomson had been systematically stealing.

George Hormel's response to the crisis revealed the steel beneath his mild Midwestern manner. Rather than panic or pursue vengeance, he treated it as a business problem to solve. He personally confronted his bankers, laid out the situation with complete transparency, and convinced them to extend the loans. Then he implemented financial controls that would become industry standards: multiple signature requirements, regular audits, and—most importantly—a corporate culture that rewarded honesty over results. His mantra during the recovery became "Originate, don't imitate", pushing the company to innovate its way out of crisis rather than cut its way to survival.

The embezzlement scandal, paradoxically, strengthened Hormel. It forced professionalization of operations, attracted better management talent (who saw opportunity in a wounded but fundamentally sound company), and most importantly, accelerated product development. By 1926, the company had recovered sufficiently to launch what would become a signature innovation: Hormel Flavor-Sealed Ham, America's first canned ham. This wasn't just a new product—it was a category creator that would define American convenience food for the next century.

III. The Jay Hormel Era: Innovation & Labor Revolution (1920s–1950s)

Jay C. Hormel returned from World War I a changed man. Where his father George was methodical and conservative, Jay was visionary and restless. He'd seen mass production at military scale, understood emerging consumer psychology, and most importantly, believed that labor and management could be partners rather than adversaries. When he became president in 1929, with George stepping back to chairman, Jay didn't just inherit a company—he inherited an opportunity to reimagine what American business could be.

The timing seemed catastrophic. The stock market crashed months after Jay took control, and the Great Depression threatened to destroy everything his father had built. But Jay saw opportunity where others saw disaster. While competitors slashed wages and fired workers, Jay introduced something radical: profit sharing. In 1938, Jay C. Hormel introduced the "Joint Savings Plan" which allowed employees to share in the profits of the company. This wasn't charity—it was calculated strategy. Jay believed that workers who thought like owners would work like owners, and the results proved him right.

But Jay's true genius lay in product development. He understood that the Depression had fundamentally changed American eating habits: families needed affordable protein that could be stored without refrigeration, prepared quickly, and—crucially—that children would actually eat. His response was a trio of products that would define Hormel for generations: Dinty Moore beef stew (1935), Hormel Chili (1936), and most famously, SPAM (1937).

The SPAM story deserves its own examination. The name itself remains shrouded in corporate mythology—Shoulder of Pork and hAM? Spiced hAM? Special Processed American Meat? Jay never definitively answered, understanding that mystery breeds interest. What mattered was the product: a shelf-stable, versatile protein that could be fried, baked, or eaten cold, priced at 25 cents a can when fresh meat cost three times as much.

Initially, SPAM was a modest success. Then came Pearl Harbor. Hormel's production increased to aid in World War II and 65% of its products were purchased by the U.S. government by 1945. The scale was staggering: in 1941 Hormel was producing 15 million cans a week, and the government was distributing it under the lend-lease program. SPAM fed American GIs from Normandy to Iwo Jima, sustained British families through rationing, and even reached Soviet troops on the Eastern Front. Nikita Khrushchev later credited SPAM with helping the Red Army survive: "Without SPAM, we wouldn't have been able to feed our army."

The wartime success created an unexpected problem: overexposure. Returning veterans were so sick of SPAM that it became a punchline, synonymous with monotony and military life. Jay's response was brilliant: he embraced the joke. The "Hormel Girls," a 60-woman orchestra and dance troupe, toured the country from 1946 to 1953, turning SPAM from wartime necessity into peacetime novelty. By 1959, Hormel had sold more than one billion cans of SPAM—proof that sometimes the best marketing strategy is to laugh along with your critics.

Jay's vision extended beyond products to corporate structure. By 1942, George and Jay established the Hormel Foundation to act as trustees of the family trusts, creating a unique ownership structure that would protect the company from hostile takeovers while funding charitable and educational initiatives. The Hormel Institute, established the following year at the University of Minnesota, began groundbreaking research on nutrition and food science, giving the company a scientific edge that competitors couldn't match.

The foundation structure proved prescient when founder George Hormel died in March 1946 at age 85. Rather than family squabbles or succession battles, the transition was seamless. Jay became chairman, and the company continued its innovation streak. In 1959, Hormel achieved another first that reflected Jay's progressive values: Hormel was the first meatpacker to receive the Seal of Approval of the American Humane Society for its practice of anesthetizing animals before slaughter. This wasn't just ethics—it was smart business, as humane treatment resulted in better meat quality and differentiated Hormel in an industry notorious for its brutal practices.

IV. Expansion & Product Innovation Era (1960s–1980s)

The 1960s opened with Hormel at a crossroads. Jay Hormel's death in 1954 had ended the direct family leadership, and the company faced new challenges: suburbanization was changing shopping patterns, television was revolutionizing marketing, and consumers increasingly demanded convenience over tradition. The response came in 1963 with a product that would redefine the company: the Hormel Cure 81 Ham, a skinless, boneless, cured ham with the shank removed. The name itself—Cure 81—suggested scientific precision, while the product delivered foolproof preparation. It was ham for the Space Age: consistent, convenient, and impossible to ruin.

Hormel added several more slaughtering, processing, and packing facilities throughout the country, and in 1965 it added a new 75,000-square-foot, automated sausage manufacturing building to its Austin plant. This wasn't just expansion—it was transformation. The new facilities incorporated automation that reduced labor costs while improving consistency, positioning Hormel for the coming battle over margins that would define the industry in the 1980s.

That battle arrived with devastating force in 1985. The meatpacking industry was undergoing brutal consolidation, with new competitors using non-union labor to undercut established players. Hormel, facing pressure to remain competitive, asked its Austin workers to accept a 23% wage cut. The workers, many of them second and third-generation Hormel employees who considered the company family, felt betrayed. The resulting strike would tear apart not just the company but the entire town of Austin.

The P-9 strike, as it became known (after Local P-9 of the United Food and Commercial Workers), wasn't just a labor dispute—it was a cultural war. The strikers, led by the charismatic Jim Guyette, drew support from across the country. Jesse Jackson came to Austin. Documentary filmmakers arrived. The strike became a symbol of American labor's last stand against corporate power. For 13 months, the battle raged, with replacement workers crossing picket lines protected by National Guard troops, families split between strikers and "scabs," and violence erupting regularly.

Hormel's response was ruthless but effective. The company hired permanent replacements, obtained injunctions against picketing, and simply waited out the strikers. By January 1986, the strike was broken. The union was decertified, hundreds of workers never returned, and Austin itself was permanently scarred—relationships destroyed, trust shattered. But from a business perspective, Hormel had won. Labor costs were reduced, productivity increased, and the company proved it could weather even the most severe crisis.

The post-strike era saw Hormel accelerate its transformation from meatpacker to food company. Management, led by CEO Richard Knowlton, understood that the strike had been a symptom of a larger problem: the commodity meat business was dying, and only value-added products could sustain margins. In an 18-month period in the late 1980s, Hormel introduced 134 new products, including Top Shelf vacuum-packed unrefrigerated meals with a shelf life of 18 months. This explosion of innovation wasn't random—it was strategic, targeting emerging consumer segments with specific solutions.

The decade closed with two transformative acquisitions. In 1986, Hormel Foods acquired Jennie-O Foods, instantly becoming a major player in the turkey industry just as Americans were shifting from red meat to poultry. The company also began an exclusive licensing arrangement to produce Chi-Chi's brand products, recognizing the growing Hispanic population and Americans' increasing appetite for Mexican food. These moves signaled a new Hormel: opportunistic, diverse, and willing to move beyond its pork-centric heritage.

V. Strategic Transformation: From Meatpacker to Food Company (1990s–2000s)

The company began trading on the New York Stock Exchange in 1990, a symbolic moment that marked Hormel's arrival as a national player. But the real transformation came with leadership. In 1992, Joel W. Johnson became president, the first president not to have risen through the Hormel ranks, having been hired away from rival Kraft General Foods. Johnson brought an outsider's perspective and a consumer packaged goods mentality that would fundamentally reshape the company.

Johnson's first major decision was radical: change the name. George A. Hormel & Company changed its name to Hormel Foods Corporation in January 1995. This wasn't just rebranding—it was repositioning. "Hormel Foods" signaled that the company was no longer just about meat but about feeding America across every daypart and occasion. The timing was perfect: consumers were fragmenting into countless niches, each demanding specialized products, and Hormel intended to serve them all. The physical manifestation of this transformation was breathtaking. A new 1,089,000-square-foot plant – equivalent to approximately 23 football fields – opened in Austin, Minn. The $100 million building featured state-of-the-art processing equipment and represented the largest investment in company history. This wasn't just a plant—it was a statement. While competitors outsourced and offshored, Hormel doubled down on American manufacturing, betting that operational excellence could overcome labor cost disadvantages. But the truly transformative acquisition came in 2001. Hormel's acquisition of The Turkey Store Company for $334.4 million in cash created Jennie-O Turkey Store with sales exceeding $1 billion, 70 percent from the old Jennie-O operations, and an 18 percent share of the $5.5 billion turkey market. This wasn't just adding scale—it was category domination. The merged JOTS operation became the largest turkey processor in the world, processing more than 1.2 billion pounds of turkey annually.

The strategic logic was compelling: The merger was a nice fit; The Turkey Store had specialized in fresh boneless and ground turkey, while Jennie-O concentrated on processed products. Hormel could now offer customers everything from commodity turkey to highly processed convenience products, controlling the entire value chain from hatchery to retail shelf. The acquisition also brought Jeff Ettinger into Hormel's leadership ranks as president of the combined turkey operations—a move that would prove prescient when he later became CEO of the entire company. The decade also saw Hormel make another strategic bet that would pay dividends: Mexican food. In 2009 Hormel and Herdez del Fuerte created the joint venture MegaMex Foods to market and distribute Mexican food in the United States. The venture significantly expanded the existing agreement between the two companies and produced a portfolio with initial revenue of about $200 million. The comprehensive portfolio included brands such as CHI-CHI'S®, HERDEZ®, LA VICTORIA®, EMBASA® and DOÑA MARÍA®, positioning Hormel to capitalize on the growing Hispanic population and Americans' increasing appetite for Mexican cuisine.

This wasn't just opportunism—it was demographic destiny. Hormel understood that America's palate was changing, driven by immigration, travel, and generational shifts. By partnering with Herdez rather than trying to build Mexican authenticity from scratch, Hormel gained instant credibility in a category where heritage matters. The joint venture structure also allowed both companies to maintain focus while sharing risks and rewards—a model that would inform future partnerships.

VI. The Skippy Acquisition: Breaking Into Center Store (2013)

The boardroom at Hormel headquarters was tense on that January morning in 2013. CEO Jeffrey Ettinger was about to propose the largest acquisition in the company's 122-year history—and it wasn't for a meat company. The target was Skippy peanut butter, a brand that Unilever had decided no longer fit its portfolio strategy. The price tag: $700 million, more than double any previous Hormel acquisition. For a company that had built its reputation on pork and poultry, buying a peanut butter brand seemed either brilliant or insane.

Ettinger's pitch was simple but compelling: "The acquisition of the Skippy® peanut butter business represents a significant opportunity for Hormel Foods. It allows us to grow our branded presence in the center of the store with a non-meat protein product and it reinforces our balanced portfolio". What he didn't say but everyone understood: Hormel needed to break out of the meat aisle if it wanted to continue growing.

The strategic logic was multifaceted. First, peanut butter represented a $2 billion category with 74 percent household penetration—second only to ham as America's most popular sandwich. Unlike meat products that required refrigeration and had limited shelf life, peanut butter was shelf-stable, high-margin, and traveled well. The Skippy domestic line consisted of 11 varieties of shelf-stable products, holding the No. 2 share in the category and leading in the faster-growing natural peanut butter subcategory.

But the real prize was international, particularly China. Skippy® peanut butter is the leading brand in China and is sold in more than 30 other countries on five continents. For Hormel, which had been trying to expand SPAM's presence in Asia, Skippy provided instant distribution channels and brand recognition. The acquisition included manufacturing facilities in both Little Rock, Arkansas, and crucially, Weifang, China—giving Hormel its first significant production footprint in the world's largest consumer market.

The financial engineering was equally clever. Total annual sales are expected to be approximately $370 million, with nearly $100 million of those sales outside the United States. The purchase price is approximately $700 million. Hormel Foods expects this acquisition to be modestly accretive in fiscal 2013. Full year accretion in fiscal 2014 is expected to be between 13 and 17 cents per share. The multiple seemed high at first glance—nearly 2x sales—but the international growth potential and category dynamics justified the premium.

There was another, less discussed benefit: commodity diversification. Hormel's margins were constantly squeezed by volatile meat prices, particularly during droughts that spiked feed costs. Peanut prices moved on entirely different cycles. As CFO Jody Feragen explained to skeptical analysts, when corn prices rose (hurting turkey and pork margins), peanut prices often fell, providing a natural hedge. This wasn't just product diversification—it was risk management disguised as M&A.

The integration proved smoother than expected. Rather than trying to "Hormel-ize" Skippy, the company let it run relatively independently while leveraging Hormel's supply chain expertise and retail relationships. Innovation followed quickly: new flavors, better packaging, expansion into adjacent categories like peanut butter spreads and snack products. Within five years, Skippy's sales had grown by over 30%, validating the acquisition price that initially seemed steep.

VII. The Planters Mega-Deal: Doubling Down on Snacking (2021)

The phone call came on a Sunday evening in January 2021. Jim Snee, Hormel's CEO since 2016, was at home when his head of corporate development called with urgent news: Kraft Heinz was finally ready to sell Planters. The iconic nuts brand had been shopped around quietly for months, with ConAgra, B&G Foods, and Pinnacle all kicking the tires. But Hormel had been preparing for this moment since Skippy proved the power of acquiring century-old brands. This time, they wouldn't be outbid.

The numbers were staggering: Hormel Foods will acquire the business for $3.35 billion in cash in a transaction that provides a tax benefit valued at approximately $560 million, equating to an effective purchase price of $2.79 billion. This was more than four times what Hormel paid for Skippy, making it the largest acquisition in our company's history. The business, which includes most Planters products and the Corn Nuts brand, contributed about $1.1 billion to Kraft Heinz's 2020 sales.

Wall Street initially balked. At 3x sales, the multiple seemed rich for a mature brand in a commoditized category. But Snee saw what the skeptics missed. "Planters® is an iconic leading snack brand with universal consumer awareness," said Jim Snee, chairman of the board, president and chief executive officer of Hormel Foods. "The acquisition of the Planters® business adds another $1 billion brand to our portfolio and significantly expands our presence in the growing snacking space.

The strategic rationale went deeper than just adding another brand. Hormel had watched as snacking overtook traditional meals in American eating habits. COVID-19 accelerated this trend—people working from home didn't want three square meals; they wanted convenient, portion-controlled protein throughout the day. Planters gave Hormel instant dominance in a category perfectly aligned with these changing consumption patterns.

There was also beautiful portfolio synergy. The Planters® brand enhances our portfolio built for individual and social snacking occasions, and perfectly complements our snacking brands such as Hormel Gatherings®, Columbus®, Justin's®, SKIPPY®, Herdez® and Wholly®. Skippy and Planters together created a snacking powerhouse—peanut butter and peanuts, sold through the same channels, appealing to the same consumers, but at different occasions. Hormel could now offer retailers a complete nut-based protein portfolio from premium (Justin's) to mainstream (Skippy) to snacking (Planters).

The operational synergies were equally compelling. "Our competencies in brand stewardship, revenue growth management, e-commerce, innovation and consumer insights will be key to driving growth for the Planters® brand and for our customers," Snee said. "We also expect significant synergies as we integrate this business into our One Supply Chain and Project Orion system". Hormel projected $50-60 million in cost synergies by 2024, primarily from supply chain optimization and overhead reduction.

But perhaps the most important aspect was what Planters represented for Hormel's transformation. This wasn't a company buying adjacent meat products anymore—this was a global food company acquiring iconic brands regardless of category. The acquisition included three production facilities and established Hormel as a legitimate player in snacking, a $150 billion category growing at 5% annually.

"This is an important day for Hormel Foods as we close the largest acquisition in our company's history. As a global branded food company, we have been making a purposeful and strategic shift in our portfolio of brands and products, which includes enhancing our snacking offerings. The Planters® snacking business is an important cornerstone to this strategy, and now joins our leading brands such as SKIPPY®, SPAM®, Hormel® Natural Choice®, Applegate®, Justin's®, Columbus® and Wholly® Guacamole".

VIII. Modern Era: Portfolio Evolution & Strategic Focus (2010s–Present)

The decade beginning in 2010 marked Hormel's most dramatic transformation yet. Under the leadership of Jeff Ettinger, the company made more than 10 acquisitions, including SKIPPY® peanut butter; CytoSport, Inc., maker of Muscle Milk® products; and Applegate Farms, LLC., maker of natural and organic meats. This wasn't random dealmaking—it was systematic portfolio construction designed to position Hormel for a radically different food future.

Ettinger, who became CEO in 2005, understood something fundamental: the American diet was fragmenting into countless niches, each demanding specialized solutions. The mass market was dying, replaced by a mosaic of consumer tribes—paleo enthusiasts, clean label devotees, protein maximizers, convenience seekers. Hormel couldn't serve them all with SPAM and bacon. It needed a portfolio as diverse as America itself.

The CytoSport acquisition in 2014 exemplified this strategy. The purchase price is approximately $450 million for a business with Total 2014 annual sales expected to be approximately $370 million. To traditional food industry observers, buying a sports nutrition company seemed bizarre for a meat processor. But Ettinger saw the connection: "Muscle Milk® products will serve as a growth catalyst for our Specialty Foods segment, providing this division with a leading brand in the high-growth sports nutrition category. The acquisition of CytoSport expands our offerings of portable, immediate, protein-rich foods, and broadens our appeal with younger consumers".

The relationship wasn't entirely new—Hormel's Century Foods subsidiary had been CytoSport's largest supplier for 15 years, giving Hormel intimate knowledge of the business. This pattern would repeat: Hormel often dated before marrying, using supplier relationships to understand businesses before acquiring them.

But the most audacious acquisition of the Ettinger era was Applegate Farms in 2015 for $775 million. Applegate has about 100 employees in New Jersey and about $340 million in annual revenue, making it the largest U.S. organic and natural meat purveyor. This deal raised eyebrows for different reasons—Applegate's customers viewed Hormel as "Big Meat," the antithesis of everything Applegate stood for.

The backlash was immediate and fierce. Applegate's Facebook page filled with angry customers accusing the company of selling out. But Ettinger had anticipated this. "We expect the team in New Jersey to run the business," he said. "They are the ones who have developed this great bond with their customers". Applegate would remain a standalone subsidiary, maintaining its commitment to antibiotic-free agriculture and humane animal treatment. Hormel was essentially buying credibility in the natural and organic space, understanding that any attempt to "Hormel-ize" Applegate would destroy the very value they were acquiring. The transition to Jim Snee as CEO in October 2016 marked another evolution in Hormel's transformation. Snee, who joined Hormel in 1989 and worked his way up through the foodservice division, brought a different perspective than his predecessors. Where Ettinger had been the dealmaker, Snee would be the integrator, focused on making Hormel's increasingly complex portfolio work as a coherent whole.

Snee inherited a company that had grown through acquisition but hadn't fully integrated its operations. Each business unit operated somewhat independently, with separate supply chains, IT systems, and go-to-market strategies. This worked when Hormel was smaller, but with revenues approaching $10 billion, the inefficiencies were becoming unsustainable. Snee's response was Project Orion and the One Supply Chain initiative—ambitious programs to unify Hormel's operations under common systems and processes.

The company adopted a three-year plan in 2023 to "transform and modernize." Former group vice president Steve Lykken called it "the most significant undertaking" in company history. This wasn't just operational improvement—it was preparing Hormel for a future where scale and efficiency would determine survival. The company reorganized into three clear segments: Retail, Foodservice, and International, each with distinct strategies but sharing common infrastructure.

Under Snee's leadership, Hormel also confronted challenges that would have destroyed lesser companies. The COVID-19 pandemic hit food processors particularly hard, with plant workers unable to socially distance and demand patterns shifting overnight as restaurants closed and grocery sales exploded. Snee's handling of the crisis exemplified his leadership style: "In Jim's mind, it was, 'How do we keep food on people's tables, that we're delivering product to our customers?' 'How do we make sure we are paying our people? And most importantly, how do we keep everybody safe?' ".

The acquisition of the PLANTERS® snacking portfolio in 2021 was the capstone of Snee's tenure, but it also represented something larger: Hormel's complete transformation from regional meatpacker to global food company. The company now generated approximately $12 billion in annual revenue across more than 80 countries worldwide with brands including PLANTERS®, SKIPPY®, SPAM®, HORMEL® NATURAL CHOICE®, APPLEGATE®, JUSTIN'S®, WHOLLY®, HORMEL® BLACK LABEL®, COLUMBUS®, JENNIE-O® and more than 30 other beloved brands.

IX. Playbook: Business & Investing Lessons

The Hormel story offers a masterclass in corporate evolution, but the lessons extend far beyond food processing. What emerges from 130+ years of history is a playbook for building enduring value in any industry facing disruption.

The Power of Brand Building Over Generations

SPAM teaches perhaps the most important lesson: brands can transcend their original purpose and even overcome negative associations if managed correctly. By 1959, Hormel had sold more than one billion cans of SPAM despite—or perhaps because of—its status as a cultural punchline. Rather than defending the product or trying to make it "cool," Hormel embraced its kitsch factor while quietly improving quality and expanding varieties. Today, SPAM sells in over 44 countries with dozens of flavors tailored to local tastes. The lesson: authenticity beats aspiration in brand building.

Strategic M&A: Discipline Over Deal-Making

Hormel's acquisition strategy reveals a pattern: they buy brands, not businesses. Whether Skippy, Applegate, or Planters, each acquisition brought established consumer equity that Hormel could amplify through superior operations and distribution. They also show remarkable discipline in walking away from deals—Hormel was reportedly interested in multiple targets over the years but refused to overpay. The Planters deal, while expensive at $3.35 billion, came with $560 million in tax benefits, reducing the effective price to $2.79 billion—financial engineering that turned a good deal into a great one.

Managing Through Crisis: The 1985 Strike as Case Study

The P-9 strike could have destroyed Hormel. Instead, it became a turning point. The company's handling—ruthless but legal, firm but not vindictive—established a template for managing existential threats. Key lessons: maintain operational flexibility (the ability to hire replacements), control the narrative (Hormel never publicly demonized strikers), and use crisis to drive transformation (post-strike productivity improvements funded the move into value-added products). Most importantly, Hormel understood that winning the battle wasn't enough—they needed to win the peace, which they did by gradually improving wages and benefits once the immediate threat passed.

The Hormel Foundation: Patient Capital as Competitive Advantage

The foundation structure, established by George and Jay Hormel in 1942, provides Hormel with a unique advantage: immunity from hostile takeovers and freedom from quarterly earnings pressure. The foundation controls 48% of Hormel's shares, ensuring management can pursue long-term strategies without activist interference. This structure enabled Hormel to invest in R&D during downturns, make acquisitions others deemed too expensive, and maintain manufacturing in Austin when pure economics suggested otherwise. The lesson: ownership structure determines strategic options.

Supply Chain as Differentiator

Hormel's supply chain innovations—from George's early refrigeration investments to modern Project Orion—consistently provided competitive advantages. The company's ability to process everything from live animals to finished products gives it margin flexibility competitors lack. When input costs rise, Hormel can adjust its product mix; when they fall, it can capture the spread. The One Supply Chain initiative takes this further, allowing Hormel to manufacture any product at any facility, dramatically improving capital efficiency.

Balancing Legacy with Innovation

Hormel demonstrates how to honor heritage while embracing change. SPAM remains central to the company's identity, but it represents less than 3% of revenues. The company maintains its Austin headquarters and manufacturing despite economics favoring relocation. These aren't sentimental decisions—they're strategic ones. Legacy provides authenticity that startups can't replicate, while innovation ensures relevance. The balance creates a moat: competitors can copy products but not provenance.

International Expansion Through Partnership

Rather than trying to force American products on foreign markets, Hormel partners with local players who understand consumer preferences. The MegaMex joint venture with Herdez del Fuerte gave Hormel instant credibility in Mexican food. In China, Skippy was already the leading peanut butter brand when Hormel acquired it, providing distribution infrastructure for other products. The lesson: in international expansion, distribution matters more than production.

X. Analysis & Bear vs. Bull Case

Bull Case: The Transformation Is Working

The bullish thesis rests on Hormel's successful pivot from commodity meatpacker to branded food company. With over 40 brands ranking first or second in their categories, Hormel has pricing power that commodity players lack. The snacking portfolio—anchored by Planters and Skippy—positions Hormel in a $150 billion global category growing at 5% annually. International expansion, particularly in Asia where protein consumption is rising rapidly, provides a decades-long growth runway.

The company's balance sheet remains fortress-like despite recent acquisitions, with moderate leverage and consistent free cash flow generation exceeding $500 million annually. The dividend aristocrat status—59 consecutive years of increases—attracts income investors who provide a stable shareholder base. Management has proven adept at acquisition integration, with Skippy and Jennie-O demonstrating successful value creation post-purchase.

Demographically, Hormel benefits from multiple tailwinds: the convenience trend favors ready-to-eat products, protein's health halo supports core offerings, and Hispanic population growth drives MegaMex products. The company's diverse portfolio provides natural hedges—when turkey prices spike, peanut butter margins expand; when consumers trade down, SPAM sales increase.

Bear Case: Mature Categories and Margin Pressure

The bearish view starts with category maturity. Despite acquisitions, organic growth remains anemic—low single digits in good years, flat to negative in bad ones. The U.S. packaged food industry faces structural headwinds: declining birth rates reduce household formation, health concerns pressure processed foods, and private label gains share in every category Hormel competes.

Integration risks loom large with Planters. At $3.35 billion, the acquisition must deliver promised synergies to justify its price. Previous large CPG integrations (think Kraft-Heinz) demonstrate how difficult capturing synergies can be. Cultural integration poses additional challenges—Planters employees from Kraft Heinz may clash with Hormel's Midwest culture.

Commodity volatility threatens margins across the portfolio. Turkey, pork, and peanut prices move independently but all face climate-related supply risks. Labor costs continue rising, particularly in meatpacking where Hormel competes for workers with Amazon warehouses offering similar wages but better conditions. Transportation costs, representing 10% of revenues, show no signs of moderating.

Competition intensifies from every angle. Traditional competitors like Tyson and Smithfield match Hormel's moves while private equity-backed challengers cherry-pick profitable niches. Plant-based alternatives, while still small, capture a disproportionate share of growth and marketing attention. Direct-to-consumer brands bypass traditional retail entirely, threatening Hormel's distribution advantages.

Valuation Analysis

At current levels, Hormel trades at approximately 20x forward earnings, a premium to food producer peers but a discount to branded food companies. The valuation implies modest growth expectations—perhaps appropriate given category dynamics. The dividend yield around 3% provides support but limits capital allocation flexibility.

Peer comparison reveals Hormel's unique position: more diversified than pure-play meat companies (Tyson), less leveraged than recent PE rollups (Smithfield), better growth profile than traditional CPG (Campbell Soup), but lacking the pure-play exposure of trending categories (Beyond Meat). This complexity makes Hormel difficult to value—it's neither fish nor fowl, which may explain the perpetual "show me" discount.

Capital Allocation Framework

Management's capital allocation priorities appear clear: 1. Maintain dividend aristocrat status (first priority, non-negotiable) 2. Invest in operations (Project Orion, capacity expansion) 3. Strategic M&A (brands over businesses) 4. Opportunistic buybacks (minimal recently given acquisition spending)

This framework suggests continued acquisitions in snacking and international markets, limited buybacks until leverage decreases, and steady dividend growth matching earnings expansion. The foundation's ownership provides stability but also limits financial engineering options available to peers.

XI. Epilogue & "If We Were CEOs"

Standing in Hormel's Austin headquarters, surrounded by 130 years of history, the weight of legacy is palpable. Photos of every CEO line the walls—just ten in total, an average tenure of 13 years that speaks to continuity rare in corporate America. The question facing the next CEO isn't whether to change but how fast and how far.

If we were running Hormel, the temptation would be to accelerate everything: double down on snacking, expand aggressively internationally, perhaps even divest legacy meat operations to become a pure-play branded food company. The market would reward such "bold" moves with multiple expansion and acclaim.

But Hormel's history suggests patience beats pivots. The company's greatest successes—SPAM, Skippy, Planters—came from steady execution rather than strategic revolution. The next big acquisition shouldn't be rushed; better to wait for the right asset at the right price than overpay for growth. International expansion should follow the established playbook: partnership over pioneering, distribution before production.

The real opportunity lies in operational excellence. One Supply Chain and Project Orion are still being implemented—full benefits won't appear for years. These unsexy initiatives could generate more value than any acquisition by improving margins across the entire portfolio. Similarly, digital transformation remains nascent. Hormel's e-commerce presence lags peers, but catching up doesn't require massive investment, just focused execution.

Plant-based proteins present a fascinating dilemma. Hormel can't ignore the trend but shouldn't overreact. The answer might be treating alternative proteins like any other category: acquire established brands rather than developing internally. Let entrepreneurs take the R&D risk; Hormel can provide scale and distribution once winners emerge.

Sustainability represents both obligation and opportunity. Consumers increasingly demand transparency about sourcing, animal welfare, and environmental impact. Hormel's foundation ownership provides cover for investments that public companies might avoid. Leading on sustainability could differentiate Hormel in commodity categories where products are otherwise interchangeable.

The international strategy needs refinement but not revolution. China remains the prize—rising incomes, protein adoption, and established Skippy presence provide a platform for expansion. But success requires patience. Building brands in China takes decades, not quarters. The MegaMex model—joint ventures with local partners—should be replicated in other markets.

The most contrarian move would be doing nothing dramatic. In a world of activist investors and quarterly capitalism, Hormel's ability to think in decades rather than quarters is its greatest advantage. The foundation structure ensures this patience can persist. Sometimes the best strategy is to tend the garden you have rather than constantly seeking new fields to plow.

XII. Recent News**

Latest Financial Performance**

Hormel Foods reported fiscal 2024 results showing the complexity of managing a diversified food portfolio in challenging times. Hormel Foods Corporation (NYSE: HRL), a Fortune 500 global branded food company, today reported fourth quarter and full-year fiscal 2024 results. All comparisons are to the fourth quarter of fiscal 2023 unless otherwise noted.

For the full year, Revenue: US$11.9b (down 1.6% from FY 2023), reflecting ongoing challenges in certain categories offset by strength in value-added products. The company's Transform & Modernize (T&M) initiative delivered meaningful results, with the Company made meaningful progress delivering value through the T&M initiative, generating $75 million in operating income benefit.

CEO Jim Snee emphasized the portfolio's resilience: "Fiscal 2024 demonstrated solid execution of our strategy, the power of our portfolio and the resilience of our team," said Jim Snee, chairman of the board, president and chief executive officer. "Across our business segments, we reinvested in our brands, expanded our market presence and introduced innovative solutions to drive impactful results," Snee said. "In Retail, our flagship and rising brands, such as HORMEL® BLACK LABEL®, JENNIE-O®, SPAM®, and APPLEGATE®, delivered strong growth and expanded households".

Dividend Aristocrat Status Maintained

Demonstrating financial stability, "We recently announced a 3% increase in our dividend, raising the annual rate to $1.16 per share. This marks the 59th consecutive year of annual dividend growth at Hormel Foods." Effective Nov. 15, 2024, the Company paid its 385th consecutive quarterly dividend at the annual rate of $1.13 per share.

Leadership Transition

In a significant development, Hormel Foods Corporation (NYSE: HRL), a Fortune 500 global branded food company, today announced that James P. Snee, chairman of the board, president and chief executive officer, will retire at the end of fiscal 2025, following a distinguished 36-year career with the company. Under Snee's leadership, the company grew its roster of protein-centric brands with acquisitions in its Retail, Foodservice and International segments: the PLANTERS® snacking portfolio, the FONTANINI® branded foodservice business and the South America-focused CERATTI® brand.

Product Innovation and Market Performance

The company continues to show strength in key categories. We grew volume and dollar sales for many products during the quarter, including Skippy® peanut butter, Jennie-O® lean ground turkey, Applegate® natural and organic meats, Wholly® and Herdez® guacamole, Lloyd's® barbecue items and Corn Nuts® corn kernels. Hormel® Black Label® bacon achieved strong results during the quarter, growing volume, dollar sales, and household penetration.

Innovation remains a priority, with Two of our most exciting innovation items – Hormel® Flash 180™ sous vide-style chicken breast and Hormel® ribbon pepperoni – have already exceeded our sales projections for fiscal 2024. We delivered excellent growth during the quarter in the convenience channel, led by Planters® flavored cashews and Corn Nuts® corn kernels.

XIII. Links & Resources

Company Resources: - Hormel Foods Investor Relations: https://investor.hormelfoods.com - Annual Reports & SEC Filings: https://investor.hormelfoods.com/financials/sec-filings - Corporate History Archive: https://www.hormelfoods.com/about/our-history/ - Hormel Foundation: https://www.hormelfoundation.com

Key Brands: - SPAM Museum: https://www.spam.com/museum - Planters: https://www.planters.com - Skippy: https://www.peanutbutter.com - Jennie-O Turkey Store: https://www.jennieo.com - MegaMex Foods: https://www.megamexfoods.com

Industry Analysis: - Meat Institute: https://www.meatinstitute.org - National Turkey Federation: https://www.eatturkey.org - American Peanut Council: https://www.peanutsusa.com - Snack Food Association: https://www.snacintl.org

Historical Resources: - "SPAM: A Biography" by Carolyn Wyman (Harvest Books, 1999) - "The Hormel Strike: A Study in Industrial Conflict" by Hardy Green (Temple University Press, 1990) - Austin Daily Herald Archives (local coverage of Hormel history) - Minnesota Historical Society Hormel Collection

Academic Studies: - Harvard Business School Case: "Hormel Foods Corporation" (2018) - University of Minnesota Hormel Institute Publications - Cornell University Industrial and Labor Relations Archive (P-9 Strike Collection)

Financial Analysis: - Morningstar Equity Research Reports - S&P Capital IQ Industry Reports - Value Line Investment Survey Coverage

Trade Publications: - The National Provisioner - Meat+Poultry Magazine - Food Business News - Progressive Grocer

Documentary & Media: - "American Dream" (1990) - Documentary on the 1985-86 Hormel Strike - Acquired Podcast episodes on food industry consolidation - Various CNBC and Bloomberg interviews with Hormel executives

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube