H&R Block: Reinventing the Green Square

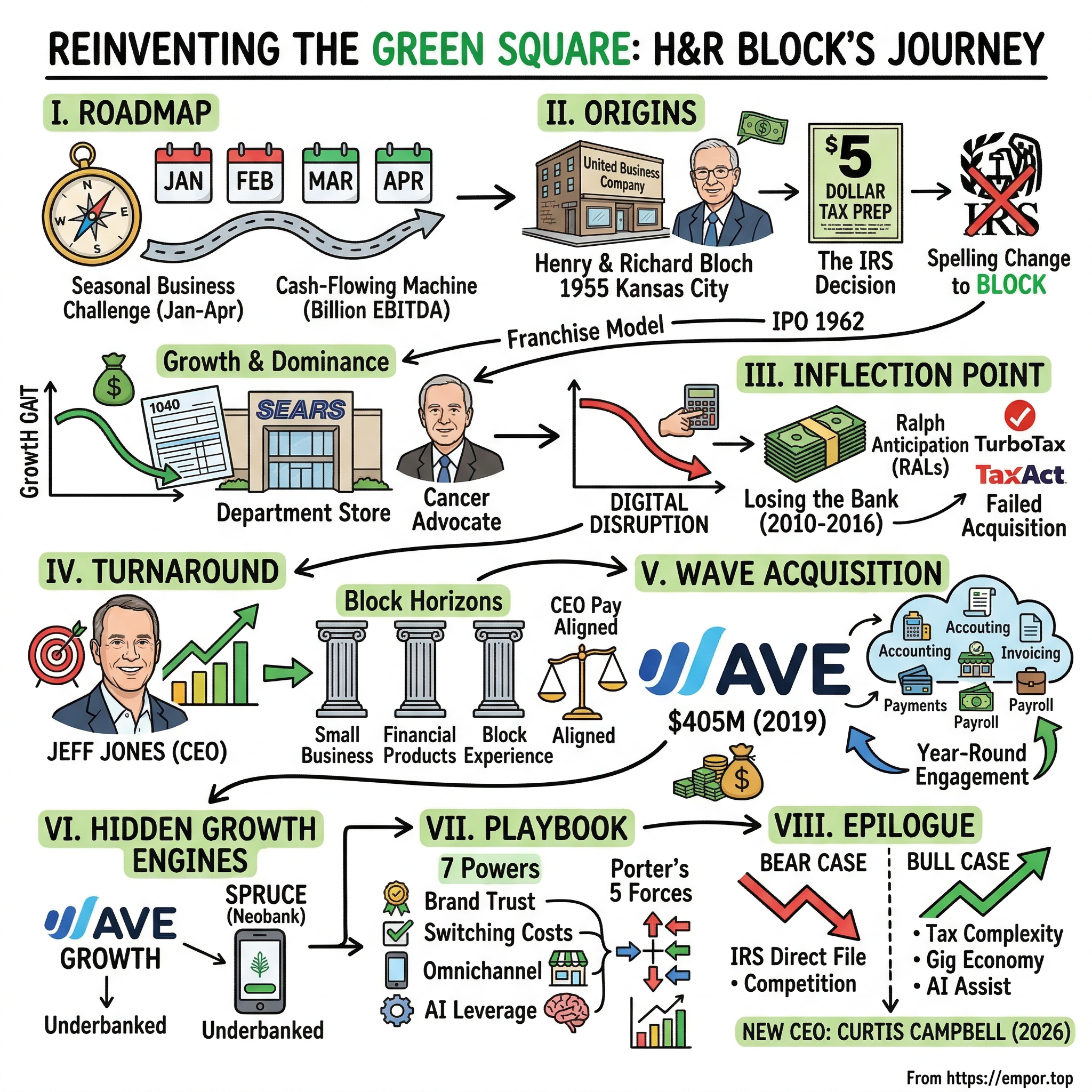

I. Introduction & Episode Roadmap

Here is a question that should keep every business strategist up at night: how does a company whose entire business model depends on a four-month window—January through April, the grinding months of American tax season—survive in a world that moves twenty-four hours a day, seven days a week, three hundred sixty-five days a year?

H&R Block is not what most people think it is. The popular image is a strip-mall storefront with fluorescent lights, a friendly tax preparer behind a desk, and a stack of W-2 forms. Your parents went there. Maybe your grandparents, too.

And that image is not wrong—but it is dangerously incomplete.

Because behind that familiar Green Square logo sits a cash-flowing machine that generates roughly a billion dollars of EBITDA annually, survived the most ferocious digital disruption in consumer financial services (the rise of Intuit's TurboTax), weathered the 2008 financial crisis by surrendering a bank charter it probably never should have had, and is now quietly incubating a fintech startup and a neobank inside a seventy-year-old brand.

The thesis of this deep dive is straightforward: H&R Block is one of the most misunderstood companies in the S&P 400. It is not a melting ice cube. It is not a legacy dinosaur waiting for the asteroid.

It is a business that stared down the innovator's dilemma, lost a decade to it, brought in an outsider CEO from the consumer-tech world, and rebuilt itself around three growth pillars—small business financial services, mobile banking for the underbanked, and an AI-enhanced omnichannel tax experience—while returning more than four and a half billion dollars to shareholders through buybacks and dividends since 2016.

The roadmap for what follows: a quick origin story of the Bloch brothers and their accidental invention of an industry, then the bulk of our time on the last fifteen years. The near-death digital disruption. The forced retreat from banking. The Jeff Jones turnaround and the Block Horizons strategy. The $405 million bet on a Toronto fintech called Wave. The hidden growth engines that are slowly converting this seasonal business into a year-round financial ecosystem. And finally, the strategic frameworks—Hamilton Helmer's 7 Powers, Porter's Five Forces—that help explain why this business might be far more durable than the market's current seven-times-earnings multiple suggests. Or why it might not be.

II. Origins: The Bloch Brothers & The Invention of Tax Prep

Kansas City, Missouri. 1955. Henry Bloch, a thirty-two-year-old World War II veteran who had flown thirty-two combat missions as a B-17 navigator over Europe, sat in a cramped downtown office on Main Street running a bookkeeping firm called United Business Company. His younger brother Richard, a Wharton-educated economist, worked alongside him. The business was, by Henry's own cheerful admission, terrible. "We would get one new client and then we would lose one," he later recalled. "Some of our accounts struggled to keep their doors open from one month to the next." They prepared tax returns on the side—a free add-on to keep bookkeeping clients happy.

Then the IRS made a decision that would accidentally create a billion-dollar industry. Facing complaints about errors in its free tax preparation assistance program, the agency began pulling the service from cities across America. Kansas City was among the first to lose it. Suddenly, hundreds of thousands of ordinary taxpayers had nowhere to turn.

A newspaper advertising salesman named John White walked into the Bloch brothers' office and pitched an idea: run an ad in the Kansas City Star promoting their five-dollar tax preparation service. Henry and Richard scraped together about a hundred dollars for the ad. The next morning, their office was flooded. Within weeks, that single advertisement had generated over twenty thousand dollars in revenue—nearly a third of what their entire bookkeeping operation brought in over the course of a year. Henry recalled the moment with characteristic understatement: "I can distinctly remember thinking, 'This tax thing is tremendous.'"

The brothers made two decisions that would define the next seven decades. First, they divested the bookkeeping business to their employees and reincorporated on July 1, 1955 as a dedicated tax preparation firm. Second, they changed the spelling of their surname from Bloch to Block—a purely practical choice to prevent customers from mispronouncing it as "blotch." A hundred-dollar ad and a phonetic spelling change: the founding acts of what would become the largest retail tax preparation company in the world.

The scaling mechanism was the franchise, and like so many great business innovations, it happened by accident. In 1956, the brothers noticed that the IRS was about to discontinue its free assistance in New York City. They opened seven storefront offices in Manhattan and generated sixty-seven thousand dollars in their first season. But neither Henry nor Richard wanted to relocate from Kansas City. When two local CPAs expressed interest in buying the New York operation but could not afford the full price, the brothers improvised: they took ten thousand dollars upfront plus a royalty percentage of future revenues. "When we first franchised," Henry admitted years later, "we didn't even know what the word meant."

That accidental arrangement became the template. Franchise offices opened in Columbia, Topeka, Des Moines, Oklahoma City, Little Rock—and then everywhere. The early terms were extraordinarily generous. Initial royalties were set at just two percent of gross receipts. Henry described it in characteristically self-effacing fashion: "We didn't sell franchises; we gave them away. An employee would come in and ask us to help him open an H&R Block office in Chicago or Detroit or someplace. We gave him a little spending money and loaned him enough to rent a store and buy some desks." Almost all of those early franchisees became wealthy.

By 1962, with 206 offices generating nearly eight hundred thousand dollars in revenue, H&R Block went public with a $300,000 IPO—75,000 shares priced at four dollars each. It was a modest debut for a company that would eventually touch the financial lives of hundreds of millions of Americans. By 1967, the network had swelled to nearly 1,700 offices in over a thousand cities across forty-four states, preparing two and a half million returns a year. The company also built its own internal tax preparer training program that was enrolling over ten thousand students per year by 1967, though fewer than half ultimately became H&R Block employees. This was the beginning of a process advantage that persists to this day: the institutional capability to train, deploy, and manage a massive seasonal workforce.

By 1970, there were more than 4,300 offices stretching across the United States, Canada, and Puerto Rico. Then the IRS inadvertently handed H&R Block its greatest competitive gift.

In 1972, IRS Commissioner Johnnie Walters launched a public relations campaign against commercial tax preparers, declaring the 1040 form "so simple a fifth-grader could complete it." The Wall Street Journal responded by running a test: it sent reporters to both IRS-run preparation centers and commercial services, and found that IRS preparers were no more reliable than their private-sector counterparts. The campaign backfired spectacularly.

It did not drive customers away from paid preparation—it drove them away from H&R Block's smaller, weaker competitors who could not absorb the reputational hit. H&R Block emerged as the only profitable commercial tax preparation firm of consequential national scale, a survivorship dynamic that cemented its dominance for the next three decades. That same year, the company shrewdly expanded into 147 Sears department stores—a natural fit for a brand that Richard Bloch once described as "the Sears, Roebuck of taxes."

The personal story of Richard Bloch deserves its own moment. In 1978, at the height of H&R Block's success, Richard was diagnosed with stage four lung cancer and given three months to live. He rejected the prognosis with the same stubbornness that had built the company. He sought aggressive treatment, fought through it, and two years later was declared cancer-free. The experience transformed him. He co-founded the Cancer Hotline in 1980 with his wife Annette, authored several books on cancer treatment that were distributed free of charge to hundreds of thousands of patients, and established the R.A. Bloch Cancer Foundation. He spent the remainder of his life as one of America's most visible cancer advocates, dying of heart failure on July 21, 2004, at age seventy-eight—twenty-six years after the death sentence that was supposed to end him in three months.

Henry, meanwhile, channeled his energies into both the company and Kansas City itself. He served on more than fifty corporate and nonprofit boards, endowed the Henry W. Bloch School of Management at the University of Missouri-Kansas City, and with his wife Marion established the Marion and Henry Bloch Family Foundation in 2011. "Kansas City saw my company through the lean years," he said, "and I'm grateful for the opportunity to give back." He died on April 23, 2019, at age ninety-six, in the city where a hundred-dollar newspaper ad had changed his life sixty-four years earlier.

The company made forays into adjacent businesses through the 1980s and 1990s—some brilliant, some disastrous.

The brilliant one was CompuServe, the pioneering online information service acquired in 1980 for twenty-three million dollars. Under H&R Block's ownership, CompuServe pivoted from corporate computer time-sharing into consumer online services—bulletin boards, email, software forums, and early internet access. Its earnings tripled between 1983 and 1985, and the subscriber base quadrupled.

Here is the ironic footnote: H&R Block used CompuServe's existing communications infrastructure to pioneer electronic tax filing with the IRS in 1986, processing twenty-two thousand returns in initial test markets. The company that would later be blindsided by digital disruption had actually been one of the first companies in America to file taxes electronically. When H&R Block sold its remaining CompuServe stake to WorldCom in January 1998, the price was approximately 1.3 billion dollars—a fifty-six-fold return on the original twenty-three-million-dollar investment. It remains one of the most successful acquisitions in the history of American consumer finance, and one of the least discussed.

The disasters, however, were equally instructive. A legal services joint venture with attorney Joel Hyatt flopped and was sold in 1987. A business seminar company called Path Management Industries, acquired for thirty-five million dollars, was gutted by a postal rate increase and a recession, and sold for twenty million—a fifteen-million-dollar loss.

More consequentially, in 1997, H&R Block acquired Option One Mortgage Corporation, a California-based firm controlling over five thousand mortgage brokers. This was the beginning of a financial services diversification strategy that also included the purchase of Olde Discount Stockbrokers in 1999, relaunched as H&R Block Financial Advisors. The mortgage business, in particular, would prove catastrophic—Option One was a subprime lender, and its exposure would nearly sink the parent company when the housing bubble burst in 2007-2008.

But through the diversification missteps, the core tax business hummed. By the turn of the millennium, H&R Block was preparing more than twenty million returns annually, operating roughly twelve thousand offices globally, and commanding approximately a quarter of the entire retail tax preparation market.

They had built something genuinely remarkable: a mass-market financial services brand trusted by tens of millions of Americans with their most sensitive financial information. Richard called it "the Sears, Roebuck of taxes"—high volume, standardized service, accessible price point. But as the internet age dawned, that Sears comparison would prove more prophetic than he intended, and not in a flattering way. The very things that made H&R Block dominant—ubiquitous physical storefronts, armies of seasonal tax preparers, a model built on face-to-face interaction—were about to become the company's greatest vulnerabilities.

III. The Inflection Point: Digital Disruption & Losing the Bank (2010–2016)

Imagine you are running H&R Block in 2010. You sit atop a kingdom of twelve thousand offices, staffed by tens of thousands of seasonal tax preparers, processing north of twenty million returns a year. Your brand is one of the most recognized in American consumer finance. And then you look at the data and realize that the ground beneath you is shifting in a way that no amount of storefront signage can stop.

The numbers told the story with brutal clarity. In 2008, the split between assisted tax preparation (someone prepares your return for you) and do-it-yourself filing (you do it with software) stood at roughly seventy to thirty. That ratio had been stable for years, the bedrock assumption upon which H&R Block's entire business model rested.

Then TurboTax arrived at scale.

By 2012, Intuit's flagship product held nearly sixty percent of all self-prepared returns filed online—a commanding lead that made it the undisputed king of DIY. H&R Block's digital product, through various rebrandings (TaxCut, then H&R Block At Home, then simply H&R Block), clung to about fifteen percent. The constant rebranding itself told a story of organizational indecision—three names in six years for a product competing against a rival with one of the most recognizable brand names in consumer software. TaxAct, a scrappy third competitor, held about eighteen percent. Between them, these three firms controlled over ninety percent of the digital tax market.

By 2016, the assisted-versus-DIY split had tightened to roughly fifty-five to forty-five. Fifteen percentage points of market share had migrated from storefronts to screens in just eight years. For a company whose cost structure was built around physical offices and human preparers, this was an existential trend.

Meanwhile, Intuit was not standing still. In 2010, it had introduced SnapTax on the iPhone—an app that let users photograph their W-2 and file a simple return entirely from their phone. It was a mobile-first strategy years before most financial services companies were even thinking about mobile. The message to consumers was unmistakable: tax filing can be as easy as taking a picture. For H&R Block, still investing primarily in storefront real estate and seasonal hiring, the technological gap was widening.

The fundamental problem was elegantly simple: the overwhelming majority of individual tax returns in America are straightforward. A W-2 employee with a standard deduction, maybe a mortgage interest write-off—for these filers, paying H&R Block a hundred fifty to three hundred dollars for what TurboTax could handle for free or near-free seemed increasingly irrational. The internet had made the simplicity of most returns obvious, and consumer behavior followed the logic. Online DIY filing was growing at eleven percent year-over-year by 2012. And it was not just a shift in channel—it was a shift in consumer psychology. People who had always assumed they needed professional help were discovering they did not, and the ones they were losing first were the easiest, most profitable returns: the simple W-2 filers who required minimal preparer time but still paid the standard fee.

H&R Block's initial response was to try to buy its way to competitiveness. In October 2010, the company announced a $287.5 million deal to acquire 2SS Holdings, the maker of TaxAct—the number-three DIY tax software behind TurboTax and H&R Block's own product. The logic was straightforward: combine the number-two and number-three digital products to mount a credible challenge to TurboTax's sixty-percent share. If you cannot beat the monopolist with one product, maybe you can do it with two. The Department of Justice saw it differently. Arguing that three firms already controlled ninety percent of the digital tax market and a merger would reduce that to two, the DOJ filed a civil antitrust lawsuit to block the deal. Judge Beryl Howell ruled against H&R Block, and in November 2011, the company abandoned the acquisition without appeal. TurboTax's digital dominance remained unchallenged, and H&R Block's most ambitious attempt to solve its digital problem had been killed by regulators. The irony would deepen years later when Curtis Campbell—who would become H&R Block's CEO in 2026—spent five years running TaxAct and driving double-digit revenue growth at the very company H&R Block had tried to acquire.

The leadership during this period was, charitably, unstable. Between 2007 and 2011, H&R Block cycled through four CEOs:

Mark Ernst was forced out by activist shareholders in November 2007. Alan Bennett, the former Aetna CFO, stepped in as interim CEO—twice. Russ Smyth, a former McDonald's Europe president brought in as a permanent solution in August 2008, resigned after less than two years to take a private-company CEO role in Chicago. Bennett returned again to hold the fort.

Four leaders in four years. The revolving door consumed the organization's strategic bandwidth at precisely the moment when coherent digital strategy was most desperately needed. No CEO stayed long enough to implement a multi-year transformation plan—and meanwhile, TurboTax was compounding its advantages every single tax season.

Behind the CEO chaos stood an activist investor who had reshaped the board: Richard Breeden, the former SEC chairman, who won a proxy fight in 2007 with over eighty-five percent of the shareholder vote. Breeden's diagnosis was correct—H&R Block had dangerously diversified into subprime mortgage lending through Option One, securities brokerage through H&R Block Financial Advisors, and banking through H&R Block Bank, all while losing focus on its tax core.

He directed the exit from mortgages and brokerage, freeing up roughly 1.4 billion dollars to pay down debt. The surgery was necessary—Option One's subprime exposure was a ticking bomb in 2007-2008—but it consumed the company's attention during the critical years when digital investment would have mattered most. The stock underperformed the S&P 500 during Breeden's watch. He stepped down in March 2011, leaving a leaner but still strategically adrift company behind.

When William "Bill" Cobb finally took the CEO seat in May 2011—the former president of eBay Marketplaces, where he had led a division trading twenty-five billion dollars in goods and services, hired specifically for his digital commerce experience—the company was already in retreat. His first major restructuring, in April 2012, cut 350 full-time jobs and shuttered 200 underperforming offices, with expected annualized savings of eighty-five to one hundred million dollars. The company united its previously separate digital and retail store tax businesses under a unified structure—a belated recognition that the artificial wall between "online" and "in-person" was hampering both channels. Cobb's digital credentials were genuine, but the core structural challenge—the cost model of physical assisted preparation versus cheap DIY software—resisted the fixes available to him.

The decline continued in grinding, year-by-year fashion. Fiscal 2013: 25.4 million worldwide returns, with U.S. assisted returns declining 2.7 percent. Fiscal 2014: 24.2 million worldwide, down another 2.6 percent. Fiscal 2015: essentially flat at 24.2 million, but U.S. assisted returns fell 4.4 percent, driven by a drop in returns containing the Earned Income Tax Credit—meaning H&R Block was losing its lower-income clientele to cheaper alternatives. Then fiscal 2016 delivered the worst results yet: U.S. returns fell to 19.59 million from 20.52 million the prior year—a decline of nearly five percent. The company announced 250 corporate layoffs, roughly thirteen percent of its full-time workforce. Full-time headcount dropped from 2,200 to 1,735. Another 200 offices were closed. Total revenues came in just over three billion dollars, down forty million. The legacy business was bleeding, and the pace was accelerating.

Compounding the digital crisis was a parallel drama that consumed enormous management attention: the saga of H&R Block Bank.

To understand the bank story, you need to understand a product that most middle-class Americans have never heard of: the refund anticipation loan, or RAL. Here is how it worked. A lower-income taxpayer walks into H&R Block in January. Their return shows a refund of, say, two thousand dollars—often the single largest lump sum they will receive all year. But the IRS takes weeks to process refunds. The taxpayer needs the money now. So H&R Block, through its bank, would advance the full refund amount immediately—minus a fee, typically fifty to a hundred dollars or more, plus interest. When the IRS refund arrived weeks later, it went directly to the bank to repay the loan. For the taxpayer, it was fast cash. For H&R Block, it was extraordinarily profitable.

The company had chartered H&R Block Bank in 2006—an FDIC-insured federal savings bank specifically designed to facilitate these loans and related financial products. By 2014, the bank's Emerald Prepaid MasterCard alone had 2.4 million users loading over nine billion dollars annually. The bank was not a side business. It was deeply embedded in H&R Block's value proposition to its most loyal customer base.

Then the regulatory walls closed in, and the sequence is worth understanding in detail because it illustrates how quickly a profitable financial product can collapse when the regulatory environment shifts. For years, H&R Block had contracted with HSBC to fund its refund anticipation loans—the arrangement dated to 2005. The economics were straightforward: HSBC put up the capital, H&R Block provided the customers, and both parties shared the substantial fees. The key underwriting tool was the IRS "debt indicator"—a single code embedded in the electronic filing system that told lenders whether a taxpayer owed back taxes, child support, or other federally collected obligations. Think of it as a one-letter credit check, provided free by the government.

In August 2010, the IRS announced it would eliminate the debt indicator for the 2011 filing season. Without that signal, lenders could not assess whether a refund would actually be paid or intercepted by the government. The FDIC warned that making RALs without the indicator would be "unsafe and unsound." Then, in December 2010, the Office of the Comptroller of the Currency issued a directive ordering HSBC to immediately cease offering any form of RAL. HSBC notified H&R Block that it was terminating RAL funding effective immediately. In a matter of weeks, H&R Block's entire external RAL partnership collapsed. The company could not offer RALs through its own bank either—regulatory pressure made it untenable. By November 2011, H&R Block announced it would not offer RALs at all in the 2012 tax season. Consumer advocacy groups praised the decision. The company's lower-income customers, who had relied on those loans to bridge the gap between filing and refund receipt, were left to find alternatives.

But losing the RAL business was only the first domino. The Dodd-Frank Wall Street Reform and Consumer Protection Act had abolished the Office of Thrift Supervision on July 21, 2011, transferring its supervisory functions to the OCC and other federal banking agencies. H&R Block Bank, originally chartered under the more permissive OTS framework, now fell under stricter oversight. The new regulatory framework proposed capital requirements that were wildly disproportionate to H&R Block's capital-light business model—the bank was already required to maintain a twelve percent minimum leverage ratio, versus the typical four to five percent for commercial banks. The company's CFO put it bluntly: "The proposed rules would require us to hold significant levels of additional capital, which does not properly align with our capital-light business model." Being a savings and loan holding company had become an anchor dragging down the entire enterprise.

The exit took years and multiple false starts. In July 2013, H&R Block signed a definitive agreement with Republic Bank and Trust Company to sell the bank's assets and transfer approximately $470 million in customer deposits. Three months later, Republic withdrew its regulatory conversion application after concerns emerged about mixing banking and tax-refund processing. The deal collapsed. Finally, in April 2014, H&R Block signed a purchase and assumption agreement with BofI Federal Bank (now Axos Financial), a San Diego-based online bank. After an amendment in August 2015, the transaction closed on August 31, 2015: BofI received $419 million in cash and assumed an equal amount of deposit liabilities. H&R Block Bank merged into its parent entity, Block Financial LLC, and formally surrendered its federal savings bank charter to the OCC. Nine years as a banking institution—2006 to 2015—ended with a signature on a regulatory form.

The strategic implications were profound. H&R Block had been forced to give up direct control over the financial products that served its most loyal—and most vulnerable—customers. Going forward, branded products like the Emerald Card and Emerald Advance lines of credit would still exist, but the bank behind them would be a third party under a Program Management Agreement.

The company would need to figure out how to offer financial products without actually being a bank.

This is the kind of constraint that can either kill a company or liberate it. In H&R Block's case, it would prove unexpectedly generative—seeding the ideas that eventually became Spruce and the broader financial services strategy. The lesson the company internalized: you do not need to own the banking infrastructure to capture the banking relationship. You just need to be the brand the customer trusts. But in the moment, in the autumn of 2015, it felt like a forced retreat.

By the end of 2016, H&R Block was a company in genuine crisis. Digital market share was a fraction of TurboTax's. Client volumes were declining. Hundreds of offices were shuttered. The bank was gone. The brand still resonated, but the business model was fraying. What the company needed was not another incremental operator—it needed someone who could reimagine the entire enterprise from the customer experience backward. Someone who understood both retail and technology. Someone, ideally, who had seen what happens when a company fails to adapt to disruption, and had the scars to prove it.

IV. The Turnaround: Jeff Jones & "Block Horizons"

Jeff Jones had one of the strangest career arcs in modern corporate America before he ever set foot in Kansas City. A communications major from the University of Dayton who started as an advertising account manager at Leo Burnett, Jones had climbed through the ranks of brand-centric companies—Coca-Cola, Gap, and ultimately Target, where he served as executive vice president and chief marketing officer. At Target, he was the architect of the brand's recovery after the devastating 2013 data breach, launched the Cartwheel savings app, and earned recognition as one of the Wall Street Journal's "5 CMOs to Watch." The man understood retail brands, digital transformation, and the emotional dynamics of consumer trust.

Then came the Uber detour. In August 2016, Jones left Target to become president of Uber's ridesharing business. Six months later, he resigned. His public explanation was unusually candid for a corporate executive: "The beliefs and approach to leadership that have guided my career are inconsistent with what I saw and experienced at Uber, and I can no longer continue as president of the ride sharing business." The departure, which coincided with a cascade of scandals at the company—sexual harassment allegations, a leaked video of CEO Travis Kalanick berating a driver, revelations about a tool used to track journalists—made Jones something rare in the corporate world: an executive who had walked away from a hot company on principle, and was willing to say so publicly.

On August 22, 2017, H&R Block announced Jones as its new president and CEO, effective October 9. He was forty-nine years old. It was his first chief executive role, and the company he was inheriting was, by any honest assessment, in trouble: declining client volumes, a shrinking footprint, a digital product that was a distant also-ran to TurboTax, and a brand that—while still trusted—was increasingly associated with an outdated way of doing business.

Jones brought something H&R Block had lacked for over a decade: a coherent strategic vision rooted in consumer experience rather than accounting operations.

His first major move, announced in October 2018, was deceptively simple—upfront transparent pricing for all tax preparation services, effective the following January. This sounds like a minor operational change. It was not. It was a statement of values that fundamentally altered the customer relationship.

Jones had studied the consumer research and found that price opacity was a primary source of anxiety for tax filers. Customers walked into H&R Block offices not knowing what they would owe until the return was complete. The experience was akin to dining at a restaurant where the menu has no prices—by the time you see the bill, it is too late to choose differently. By publishing prices in advance and guaranteeing no surprises, Jones was importing the consumer-tech playbook—where transparency builds trust—into an industry that had long profited from opacity.

He also shuttered another 400 underperforming offices in 2018 following the Tax Cuts and Jobs Act, which simplified filing for millions by increasing the standard deduction. Rather than fighting the trend, Jones leaned into it—closing the weakest locations while investing in digital capabilities and the remaining storefronts.

The compensation structure the board designed for Jones tells its own story about alignment. His base salary of $995,000 was deliberately modest by Fortune 500 CEO standards—it represented just nine percent of his total target compensation. The remaining ninety-one percent was variable: fourteen percent in short-term annual bonuses, and a dominant seventy-seven percent in long-term equity incentives, primarily Performance Share Units.

The message was clear: Jones would get rich only if shareholders did.

The PSU structure was rigorous. Each three-year cycle measured cumulative EBITDA from continuing operations, with a modifier based on Total Shareholder Return relative to the S&P 400 Index, adjustable by plus or minus twenty-five percent. Payouts could range from zero (if performance was below threshold) to two hundred percent of target (if performance was exceptional). This is worth pausing on: a CEO whose equity compensation can go to zero is a CEO with a very different risk calculus than one collecting guaranteed restricted stock grants. Jones's compensation structure meant that in a bad scenario—declining EBITDA, underperforming stock—he would receive less than a million dollars a year for running a three-billion-dollar company.

Additionally, Jones was required to hold H&R Block stock valued at six times his base salary—roughly six million dollars—and was strictly prohibited from hedging or pledging those shares. This was not a CEO who could extract value while the stock languished. His fortune was welded to the company's performance.

The early results under Jones were encouraging. In his first full operating year, fiscal 2018, revenue climbed to $3.2 billion—up four percent year-over-year. U.S. returns prepared rose to approximately twenty million, a 2.5 percent increase. More importantly, the rate of decline in U.S. assisted clients moderated dramatically, from negative 2.5 percent the prior year to negative 0.6 percent—still declining, but the bleeding had slowed to a trickle. Online DIY returns grew 10.3 percent, outpacing the industry for the first time in years. Pretax income hit $669 million, up 6.3 percent. Jones had stabilized the patient. Now he needed to cure it.

The COVID-19 pandemic in 2020 threw a wrench into the turnaround momentum. The IRS extended the federal tax filing deadline, disrupting H&R Block's carefully orchestrated seasonal operations. Management noted the company had been "on track to deliver on its financial outlook" before the pandemic struck. But the crisis also demonstrated something important: H&R Block's physical offices and human preparers were not just a legacy cost—they were a service that millions of Americans genuinely valued and were willing to wait for. When offices reopened, customers came back. The resilience of assisted demand through the pandemic was, in retrospect, the strongest evidence yet that H&R Block's core business model had a floor.

The compensation results over the full Jones tenure validated the alignment structure the board had designed. The FY2023-2025 PSU cycle delivered an EBITDA performance of 94.9 percent of target, which sounds modest until you apply the TSR modifier: H&R Block's total shareholder return placed it at the seventy-second percentile of the S&P 400, triggering a 118.2 percent multiplier. The final payout was 112.2 percent of target—Jones received 101,228 shares (including dividend equivalents), vesting on August 13, 2025. In that fiscal year alone, Jones realized over twenty-one million dollars in total vested equity value across 339,033 shares. Over his full tenure, the stock rose 123 percent, the company returned more than four and a half billion dollars to shareholders, the quarterly dividend increased approximately seventy percent, and H&R Block's market capitalization grew from $5.5 billion to $7.4 billion at its peak.

The strategic blueprint came together under the banner of "Block Horizons 2025," formally launched in June 2021. The name itself was revealing—it set a specific time horizon (five years) with measurable goals, rather than the vague aspirational language that often passes for corporate strategy.

The plan rested on three pillars.

First, Small Business: leveraging the recently acquired Wave platform and the Block Advisors brand to serve the millions of self-employed and micro-business owners who needed year-round financial services, not just a once-a-year tax filing. The gig economy was exploding—Uber drivers, Etsy sellers, DoorDash couriers—and every one of them needed help with quarterly estimated taxes, expense tracking, and end-of-year filing.

Second, Financial Products: building Spruce, a mobile banking platform targeting the underbanked and low-to-moderate income Americans who were already H&R Block tax clients. This was a direct response to the forced bank charter exit—if you cannot be a bank, become the front door to one.

Third, Block Experience: reimagining the core tax preparation business as an omnichannel offering where customers could start a return on their phone, continue it on a laptop, and walk into a physical office to have a human finish it—or any combination thereof. The vision was to turn "omnichannel" from a buzzword into a genuine competitive moat.

The organizational restructuring that accompanied Block Horizons was surgical rather than sweeping: approximately ninety new promotions and expanded roles, with fewer than ninety positions eliminated. Jones was building, not just cutting. The 2021 tax season delivered the largest market share gains in more than a decade, validating the approach.

In November 2021, the board rewarded Jones with a second five-year employment contract, running through November 2026. But Jones did not stay for the full term. On August 11, 2025, H&R Block announced that Jones would retire as CEO effective December 31, 2025. His successor, Curtis Campbell, had joined the company in May 2024 as president of Global Consumer Tax and chief product officer. Campbell's resume read like a deliberate synthesis of every capability H&R Block needed: five years as president and CEO of TaxAct (where he drove double-digit revenue growth), a vice presidency at Intuit (direct competitor intelligence), a general manager role at Amazon Web Services (technology depth), and senior positions at Capital One (financial services acumen).

The transition was notable for what it lacked.

There was no golden parachute for Jones—no multi-million-dollar severance package, no accelerated equity vesting beyond what he had already earned. He transitioned to a strategic advisor role through September 2026 on base salary alone—no equity kicker, no special bonus. In an era of eye-popping executive exit packages, this was refreshingly clean.

Campbell assumed the CEO title and a board seat on January 1, 2026, with the same $995,000 base salary Jones had carried. His total target compensation package mirrors Jones's structure—heavily weighted toward long-term equity incentives tied to EBITDA and TSR performance. The board clearly intends to replicate the alignment model that worked during the Jones era.

Looking back, the Jones era accomplished something that looked nearly impossible in 2017: it stabilized and then grew a legacy tax preparation business while simultaneously building new revenue streams in small business services and financial products, all while returning extraordinary amounts of capital to shareholders.

Revenue grew from roughly three billion to 3.76 billion. EBITDA approached a billion dollars. The share count shrank by over forty percent through aggressive buybacks. The brand was revitalized. And perhaps most importantly, Jones changed the narrative: H&R Block was no longer described as a legacy company in decline, but as a turnaround story with optionality.

Whether the next chapter—under Campbell, in an era of generative AI and political uncertainty about tax policy—can sustain that trajectory is the central question facing investors today. And to understand the answer, we need to look at the two hidden growth engines that Jones's strategy planted and that Campbell now inherits: Wave and Spruce.

V. M&A & Capital Deployment: The Wave Acquisition

H&R Block has a problem that most companies would kill for: it generates an enormous amount of free cash flow—nearly six hundred million dollars in fiscal 2025 alone—from a business that requires relatively little capital investment to maintain. The storefronts are leased, the tax preparers are seasonal, and the technology platform, once built, scales cheaply across twenty million returns. The question that has defined H&R Block's capital allocation for the past decade is simple: what do you do with all that cash?

The historical answer was overwhelmingly: give it back to shareholders. Since 2016, H&R Block has returned more than four and a half billion dollars through dividends and share repurchases. The company has bought back over forty-three percent of its shares outstanding during that period—an extraordinary level of financial engineering that mechanically supports earnings-per-share growth even in years when the top line barely moves. The current dividend stands at $1.68 per share annually, representing eight consecutive years of increases including a twelve percent bump in fiscal 2026 and a seventeen percent increase the year before. At recent prices around thirty-two dollars, the yield approaches five percent.

But aggressive capital return creates its own tension. A company that returns virtually all of its free cash flow is implicitly saying that it does not see sufficiently attractive reinvestment opportunities within its own business. For a company facing secular headwinds from digital disruption, that message can become self-fulfilling: if you do not invest in the future, you may not have one.

Which brings us to Wave—the deal that broke the pattern and signaled a new era of strategic ambition.

In June 2019, H&R Block announced it would acquire Wave Financial, a Toronto-based fintech startup, for $405 million in cash. The deal closed on July 1, 2019.

At the time, four hundred and five million dollars seemed like a steep price for a company whose primary product—cloud-based accounting, invoicing, and receipt-tracking software for small businesses—was entirely free. Wave did not charge a dime for its core tools.

Revenue came exclusively from paid add-on services: payment processing (card transaction fees when customers paid invoices via card), payroll subscriptions (a monthly fee for processing employee paychecks), and bookkeeping assistance. The company was serving over four hundred thousand small businesses globally every month, but the revenue base was modest—H&R Block estimated Wave would contribute forty to forty-five million dollars of revenue in its first partial fiscal year.

The strategic logic, however, was compelling on multiple levels. Start with the "build versus buy" question. H&R Block's leadership had concluded—correctly, by most accounts—that the company simply could not build a modern, cloud-native SaaS product internally. Its core technology competency was in tax preparation software, a highly specialized domain with entirely different architecture, user experience expectations, and development rhythms than general-purpose small business financial software. Building a QuickBooks competitor from scratch inside H&R Block would have been like asking a Formula 1 team to design a minivan. The DNA was wrong.

Wave, by contrast, had been purpose-built for the exact market H&R Block coveted. Co-founded in 2009 in Toronto by Kirk Simpson and James Lochrie, Wave's free pricing strategy was a deliberate wedge to acquire cost-sensitive micro-business owners—freelancers, gig workers, sole proprietors—who would never pay thirty to seventy dollars a month for QuickBooks. Once those users were on the platform, Wave monetized them through transactions: processing their invoice payments, running their payroll, handling their bookkeeping. It was a classic "land and expand" SaaS model, but with the unusual twist of a genuinely free core product rather than a time-limited free trial.

Was $405 million too much? In isolation, paying roughly ten times Wave's estimated first-year revenue contribution looked expensive. The financial press was skeptical. Why would a tax preparation company pay four hundred million dollars for free accounting software?

But context matters enormously. Two years later, in September 2021, Intuit paid approximately twelve billion dollars to acquire Mailchimp—a bootstrapped email marketing platform with about eight hundred million in annual revenue. The strategic rationale was strikingly similar: expand the small business footprint, build year-round customer relationships, cross-sell financial products. Intuit paid roughly fifteen times revenue.

Meanwhile, Xero, the New Zealand-listed cloud accounting competitor to QuickBooks that dominates in Australia and the UK, carried a market capitalization of thirteen to eighteen billion dollars on three million subscribers. Against those benchmarks, paying $405 million for Wave's four hundred thousand active users and growing revenue base looks less like a splurge and more like a strategic steal. H&R Block acquired a cloud-native SaaS business with a proven monetization model for roughly three percent of what Intuit later paid for Mailchimp—and Wave was arguably a better strategic fit for its acquirer.

The acquisition also gave H&R Block something it desperately needed: year-round customer engagement. The fundamental business problem has always been seasonality—the overwhelming majority of revenue compressed into the January-through-April tax filing window. Small businesses, by contrast, need accounting software every day. They send invoices in July. They run payroll in October. They reconcile receipts in December. Wave's platform, integrated into H&R Block's ecosystem, created a continuous relationship with customers who had previously disappeared after April 15 and reappeared the following January.

Kirk Simpson, Wave's co-founder and CEO, remained in place after the acquisition and ran the business independently from Toronto for three years before stepping down in June 2022. He was succeeded by Zahir Khoja, a former Mastercard and Afterpay executive—a signal that H&R Block intended to accelerate Wave's payments and financial services capabilities rather than simply milk the existing user base.

The Wave deal also resolved an uncomfortable truth about H&R Block's capital return strategy. A company trading at seven times earnings with a five percent dividend yield is cheap by almost any measure. But if the business is genuinely in secular decline, cheap can always get cheaper. Wave represented a bet—the first significant one in years—that H&R Block could grow into new markets rather than simply manage its existing business for cash. The four hundred and five million dollar purchase price, funded entirely from cash on hand without any new debt, was large enough to be meaningful but small enough that failure would not be existential.

For long-term investors, the key question about Wave is not whether the acquisition was good value in 2019—it almost certainly was. The question is whether H&R Block can execute on the cross-selling opportunity: converting its twenty million annual tax clients into year-round Wave users, and converting Wave's hundreds of thousands of small business users into H&R Block tax clients. If the flywheel works, Wave transforms HRB's economics from seasonal to perennial. If it doesn't, it remains a nice but modest growth kicker on the margin of a still-seasonal business.

VI. The "Hidden" Growth Engines: Wave & Spruce

Inside the hulking, seventy-year-old body of H&R Block, two businesses are growing at rates that would be respectable for a venture-backed startup—and they are doing it largely unnoticed by the market.

Start with Wave.

In fiscal 2025, Wave generated approximately thirty million dollars per quarter in revenue, growing at over thirteen percent year-over-year—its third consecutive year of double-digit growth. By the second quarter of fiscal 2026, reported in February 2026, the growth had accelerated further, with management citing "strong growth in Wave subscription revenue and payments volume" as a primary driver of the quarter's 11.1 percent revenue increase.

The company does not break Wave out as a standalone segment in its public filings, which means most equity analysts model it as a rounding error within the consolidated numbers. This is a mistake—and potentially an opportunity for investors paying closer attention.

Here is why Wave matters more than its current revenue suggests. The product solves H&R Block's most fundamental strategic problem: the empty months between May and December when the core tax business generates virtually nothing. Wave's small business customers do not disappear after April 15. They send invoices in the summer. They process payments in the fall. They run payroll every two weeks, all year long. Every dollar of Wave revenue is inherently non-seasonal, which means it directly addresses the structural weakness that has depressed H&R Block's valuation for decades.

The business model is also structurally attractive from a margin perspective. Wave's free core product (accounting, invoicing, receipt tracking) acts as a customer acquisition engine with near-zero marginal cost—users find the software through search, sign up, and begin using it without any sales interaction. Monetization happens through high-margin add-on services: payment processing fees (a percentage of each card transaction), payroll subscriptions, and bookkeeping services. This is a transaction-revenue model layered on top of a SaaS distribution mechanism, which means revenue scales with customer activity rather than requiring proportional headcount growth.

The integration between Wave and the broader H&R Block ecosystem is where the real strategic leverage lies. A gig worker who uses Wave to invoice clients and track expenses throughout the year already has their financial data organized when tax season arrives. The natural next step is to file their tax return through H&R Block, where that data can be imported directly. Conversely, a small business owner who files taxes through Block Advisors (H&R Block's premium small business advisory brand) can be cross-sold on Wave for year-round bookkeeping and payments. This creates a two-way customer acquisition flywheel that neither product could power on its own.

Then there is Spruce—H&R Block's neobank play, and perhaps the most creative strategic move the company has made in the post-bank-charter era.

Launched on January 20, 2022, Spruce is a mobile banking platform offering a spending account, debit card, and connected savings account—all with no monthly fees, no sign-up fees, and no minimum balance requirements. The banking infrastructure is provided by Pathward, N.A. (formerly MetaBank), an FDIC-insured partner bank.

H&R Block is not a bank. It learned that lesson the hard way. But through Spruce, it can offer banking products without the regulatory burden of holding a charter—the same model that Chime, Cash App, and other neobanks use.

The target market is not the mass affluent. It is not the tech-forward millennial who already has three fintech apps on their phone. Spruce is aimed at the underbanked—Americans who have some banking relationship but still rely on expensive alternative financial services like payday loans and check-cashing outlets. H&R Block identified approximately eight million of its existing tax clients as fitting this profile. These are the people who walk into H&R Block offices every January, hand over their W-2, and wait for their refund to arrive—often the single largest cash infusion of their entire year.

The strategic insight was elegant: if those refund dollars could be deposited into a Spruce account instead of a traditional bank or prepaid card, H&R Block could keep that capital within its own ecosystem.

The customer gets a no-fee banking product with useful features—early direct deposit, overdraft protection up to twenty dollars, retailer rewards. H&R Block gets year-round deposit balances and transaction data that deepen the customer relationship far beyond the four-month tax window. It is a classic two-sided value exchange, and it leverages H&R Block's unique advantage: it already knows these customers intimately from their tax returns.

The growth trajectory tells the story of a product finding its market. By December 2022—less than a year after launch—Spruce had 171,000 sign-ups and $117 million in customer deposits. A year later, sign-ups had climbed to 316,000 and deposits had nearly quadrupled to $456 million. By fiscal year-end 2024 in April, the platform reached 476,000 sign-ups and approximately one billion dollars in deposits. By the end of fiscal 2025, sign-ups had reached 700,000. In March 2023, H&R Block deepened the integration by enabling customers to open a Spruce account directly while sitting with a tax professional in an office—turning the tax appointment itself into a banking customer acquisition moment.

Two statistics reveal the depth of engagement. First, ninety percent of new Spruce users also filed a tax return with H&R Block, confirming that the cross-sell between banking and tax preparation works in both directions. Second, roughly fifty percent of Spruce deposits were non-tax-related—meaning customers were not just dumping their refund into the account and withdrawing it. They were using Spruce as their primary banking relationship, receiving paychecks via direct deposit, spending through the debit card, and accumulating savings. This is the difference between a promotional gimmick and a genuine financial product with retention dynamics.

Spruce competes in a crowded neobank landscape alongside Chime, Green Dot, and Cash App—all of which target similar demographics. But H&R Block has a distribution advantage that none of those competitors can match: roughly twelve thousand physical offices where trained professionals can explain the product face-to-face to customers who may distrust purely digital financial services. For the underbanked population—many of whom have had negative experiences with traditional banks and are wary of app-only solutions—the ability to walk into a local H&R Block office and talk to a human about their banking account is a meaningful differentiator.

A brief but entertaining aside: in December 2021, the same month Spruce was taking shape internally, Jack Dorsey's Square, Inc. rebranded itself as Block, Inc. and rolled out a green square-shaped logo while simultaneously launching Cash App Taxes—a direct competitor to H&R Block's core business. H&R Block filed a trademark infringement lawsuit in the Western District of Missouri, and the district court initially sided with them, finding that consumers would likely confuse the two brands. But the Eighth Circuit Court of Appeals reversed the preliminary injunction in January 2023 in a two-to-one ruling, concluding that H&R Block had not demonstrated sufficient consumer confusion or irreparable harm. The two companies settled amicably in April 2023, dismissing the case with prejudice. The legal battle was lost, but the PR battle was arguably won: the lawsuit reminded every financial journalist in America that when you think of a green square and financial services, you think of H&R Block.

Taken together, Wave and Spruce represent something genuinely new for H&R Block: revenue streams that do not depend on tax season.

They are still modest relative to the roughly 3.8-billion-dollar consolidated business—Wave is approaching a hundred-twenty-million-dollar annual run rate and Financial Services is a steady eight-figure quarterly contributor. In absolute terms, these are not the numbers that move the needle on a company this size. Not yet.

But they are growing at double-digit rates in a company whose core tax business grows at low-to-mid single digits. Over time, these businesses have the potential to fundamentally alter H&R Block's revenue profile, its valuation multiple, and the market's perception of what this company actually is.

The critical question is the rate of compounding. If Wave maintains thirteen-plus-percent growth for another five years, it becomes a roughly $250 million annual revenue business—material even within a four-billion-dollar enterprise. If Spruce reaches two million users and captures a meaningful share of their year-round banking activity, the Financial Services segment could generate revenue that is larger than what many standalone neobanks produce. The math of compounding favors patience, but the competitive clock does not stand still.

Which raises the question: how defensible are these businesses, and the tax core that funds them? For that, we need a framework.

VII. Playbook: Hamilton's 7 Powers Analysis

Hamilton Helmer's framework—outlined in his book 7 Powers: The Foundations of Business Strategy—defines seven conditions that create persistent differential returns through some combination of a benefit to the incumbent and a barrier to challengers.

Applied to H&R Block, the framework reveals a company with multiple overlapping but individually moderate powers, creating a competitive position that is more durable than any single moat would suggest on its own.

Brand. This is H&R Block's most potent power, and it operates in a domain where brand trust is not merely a preference but a near-necessity. Consider the psychology: when an American sits down to file their taxes, they are engaging with the Internal Revenue Service—the most powerful collection agency on earth. The consequences of error range from audit anxiety to financial penalties to, in extreme cases, criminal prosecution. In this emotional landscape, the Green Square does not represent a tax preparation service. It represents peace of mind. It represents audit defense. It represents the assurance that a seventy-year-old institution with more than eight hundred million returns prepared stands behind your filing. That emotional weight is extraordinarily difficult for a new entrant to replicate. TurboTax has built its own powerful brand around simplicity and self-empowerment, but it occupies a fundamentally different psychological niche: "you can do this yourself" versus "we will protect you." Both are powerful, but they serve different emotional needs. The barrier in Helmer's framework is time: it took H&R Block seven decades to build this brand equity, and no amount of venture capital can compress that timeline.

Switching Costs. Once H&R Block has a customer's complete tax history—prior-year returns, depreciation schedules, carryforward amounts, basis calculations for investments and real estate, W-2 and 1099 records—switching to a new provider creates genuine friction. The data must be reconstructed or transferred. The new preparer must learn the customer's situation from scratch. For a W-2 employee with a simple return, this friction is low, which is why the DIY migration happened so easily. But for anyone with self-employment income, rental properties, investment portfolios, or a small business running payroll on Wave, the switching costs are substantial. In January 2024, H&R Block actually launched a "Direct Import" feature that pulls prior-year data from TurboTax into H&R Block's platform—an acknowledgment that switching costs are a two-way barrier, and that reducing inbound friction is a customer acquisition tool. The company reported that more than five million people switched to H&R Block in 2023, suggesting the friction of switching away from competitors can be weaponized as effectively as the friction of leaving.

Scale Economies. H&R Block processes over twenty million returns annually. This scale creates cost advantages that operate across multiple dimensions. The Tax Institute—a proprietary internal research division staffed by CPAs, tax attorneys, and enrolled agents—develops training materials and compliance guidance that are amortized across the entire filing base. The AI Tax Assist system, built on Microsoft's Azure OpenAI platform, is trained on seventy years of tax return data and the accumulated expertise of approximately sixty thousand tax professionals. No independent CPA, no regional tax firm, and no startup can assemble a training dataset of this depth. The roughly twelve thousand retail offices, while a cost burden when empty, represent a distribution network that would cost billions to replicate. Technology investments—the MyBlock digital platform, the virtual appointment system, the mobile-first tax preparation experience—are amortized across a user base that is simply inaccessible to smaller competitors.

Counter-Positioning (The Omnichannel Advantage). Here is where H&R Block turned its biggest historical liability into what may be its most distinctive strategic asset. The physical storefront network that nearly killed the company during the digital disruption has been reimagined as the anchor of an omnichannel experience that pure digital players cannot replicate. A customer can begin a tax return on their phone at midnight, realize they do not understand how to handle their freelance 1099-K income, and walk into an H&R Block office the next morning to have a human professional finish the return—seamlessly, with all data preserved in the shared MyBlock platform. TurboTax cannot offer this. It has no storefronts. It cannot put a human being across the desk from a confused taxpayer who needs to look someone in the eye and hear "this is going to be fine." Conversely, an independent CPA cannot offer the digital sophistication, the AI-powered guidance, or the brand-backed guarantees that H&R Block wraps around its technology platform. The omnichannel model occupies a strategic position that is structurally difficult for either type of competitor to attack.

Process Power. Seventy years of training tax preparers, managing a seasonal workforce that scales from a few thousand to sixty thousand and back again, maintaining quality control across twelve thousand locations, and processing regulatory changes (the tax code changes every year) has created deeply embedded organizational processes.

Consider the sheer operational complexity: every January, H&R Block must stand up what is essentially a temporary army of sixty thousand tax professionals, equip them with updated software reflecting the latest tax code changes, deploy them to twelve thousand locations, ensure consistent service quality, and then scale back down by May. Doing this reliably, year after year, across every state and many countries, is a process capability that has been refined over seven decades.

The average H&R Block tax professional has ten years of experience. The training programs, quality assurance protocols, and compliance systems represent institutional knowledge that cannot be purchased or quickly replicated.

Network Effects and Cornered Resources. These are H&R Block's weakest powers. Tax preparation does not exhibit strong network effects—the product is not more valuable to one user because another user also uses it. There are minor effects: more tax professional hires improve staffing flexibility, and Wave's payment processing has modest network dynamics.

As for cornered resources, the Tax Institute and the exclusive Microsoft Azure AI 100 partnership offer some proprietary advantage, but these are not the kind of irreplaceable assets—like a patent or a regulatory license—that Helmer's framework describes at its strongest. H&R Block does not own a resource that competitors literally cannot access. It owns resources that would be very expensive and time-consuming to replicate, which is a meaningful but lesser form of competitive protection.

Now layer Porter's Five Forces on top to stress-test this competitive position from a different angle.

Rivalry among existing competitors: High. Intuit's TurboTax dominates DIY with roughly sixty percent share, and price competition on simple returns has compressed margins. The Free File Alliance—an agreement between the IRS and major tax software companies to offer free filing for lower-income taxpayers—has further squeezed pricing power at the bottom of the market. Jackson Hewitt, Liberty Tax, and tens of thousands of independent CPAs compete for the assisted market. This is not a cozy oligopoly—it is a genuinely competitive industry.

Threat of new entrants: Low to moderate. Brand trust and regulatory complexity create meaningful barriers—you cannot just launch a tax preparation service without deep expertise in tax law, IRS compliance, data security, and state-by-state filing requirements. However, the IRS Direct File program represented a novel government-backed entrant that could bypass all commercial players entirely. And Cash App Taxes (formerly Credit Karma Tax, acquired by Square's Block, Inc.) demonstrated that well-funded tech companies can enter the market by offering free filing as a loss leader to acquire financial services customers.

Threat of substitutes: Moderate. The ultimate substitute for professional tax preparation is self-preparation, and the evidence from the past fifteen years is clear: a significant percentage of Americans have decided they can do it themselves. Free alternatives exist and work well for simple returns. The question is whether the complexity ceiling—the point at which a return becomes too difficult for DIY—continues to capture enough of the population to sustain H&R Block's assisted business.

Buyer power: Asymmetric. For simple returns, buyer power is high—there are many free or low-cost options, and switching costs are minimal. But for complex returns—small business owners, investors, gig workers with multiple 1099s, homeowners with rental properties—buyer power decreases meaningfully. These filers need expertise, and they will pay for it. H&R Block's strategic challenge is to push its business mix toward higher-complexity, lower-buyer-power segments.

Supplier power: Low to moderate, with one critical exception. Most of H&R Block's inputs—office leases, technology infrastructure, marketing—are commoditized. But credentialed tax professionals (CPAs and enrolled agents) are in genuine short supply nationally, and the accounting profession has been struggling with a pipeline problem for years. Fewer accounting graduates, combined with more retirements, could constrain H&R Block's ability to staff its offices—or force wage increases that compress margins.

The overall picture is a company with no single dominant moat but a constellation of reinforcing advantages—brand, switching costs, scale, and an omnichannel position that is structurally difficult to attack from either the pure-digital or pure-physical side. The market's current seven-times-earnings valuation implies either that these advantages are eroding faster than the financials suggest, or that the market is mispricing the durability of the business. Reasonable people can disagree on which interpretation is correct.

VIII. Epilogue: Bear vs. Bull Case

Every investment thesis lives in the tension between what could go wrong and what could go right. For H&R Block, both sides of that tension are unusually vivid.

The Bear Case: Government, Competition, and Secular Decline

The most existential threat to H&R Block has never been Intuit. It has been the United States government.

The IRS Direct File pilot program, launched for the 2024 tax season and expanded to twenty-five states in 2025, represented something genuinely new: a free, government-built tax filing tool that could theoretically eliminate the need for commercial tax preparation for millions of Americans with simple returns. Ninety percent of pilot users rated their experience as excellent or above average. The program saved users an estimated $5.6 million in preparation fees in its first year. If scaled nationally—to all fifty states, covering all return types—Direct File could have represented a structural threat that no amount of brand equity or omnichannel innovation could fully counter.

Then politics intervened. Under the current administration, the IRS Direct File program was terminated in late 2025 as part of broader government efficiency initiatives. For now, the threat is neutralized.

But the bear case argues that this reprieve is temporary. A future administration could revive and expand the program, and technological advances make it increasingly feasible for the government to offer comprehensive free filing. The structural logic has not changed: millions of American tax returns are simple enough that a competent government system could handle them, and the political appeal of "free tax filing" is enduring on both sides of the aisle. Other developed nations—Australia, the United Kingdom, Japan—already offer some form of government-facilitated filing. The United States is the outlier, and that outlier status may not last forever.

Beyond government, Intuit remains a relentless and extremely well-capitalized competitor. TurboTax holds roughly sixty percent of the DIY market and continues to invest aggressively in AI-powered guidance that narrows the experience gap between DIY software and human-assisted preparation. Every year that AI gets better at answering tax questions, the value proposition of paying a human preparer erodes slightly for another slice of the market. Intuit's market capitalization of approximately $175 billion dwarfs H&R Block's roughly four billion—the competitive resource asymmetry is enormous.

The bear also points to the structural reality of seasonality. Despite Wave and Spruce, the overwhelming majority of H&R Block's revenue still arrives between January and April. The Q2 fiscal 2026 results—$198.9 million in revenue against a seasonal operating loss of $241.6 million—illustrate how stark the off-season economics remain.

Think about what that means operationally: for roughly eight months of the year, H&R Block burns cash. The company's annual profitability depends entirely on one explosive quarter (the fiscal Q4, January through April). Until year-round revenue streams grow to a scale that meaningfully changes the quarterly cadence, H&R Block remains vulnerable to any disruption that affects the tax season window: government shutdowns, pandemic-related filing extensions, or sudden changes in tax policy.

And then there is the stock's recent decline. Trading near its fifty-two-week low of around thirty-two dollars—down roughly fifty percent from the fifty-two-week high of $64.62—the market is clearly pricing in meaningful risk. Whether that risk reflects concern about the CEO transition, the competitive landscape, or broader market rotation away from value stocks, the magnitude of the decline suggests this is not just a routine pullback. For a company that has been buying back its own shares aggressively, a sustained stock decline means the buyback program is destroying less value per dollar—but it also means the remaining authorization has more shares to retire.

The Bull Case: Complexity, the Gig Economy, and AI Leverage

The bull case begins with a simple observation: the American tax code only gets more complex, not less.

Every new piece of legislation—from the Tax Cuts and Jobs Act to the Inflation Reduction Act to whatever emerges next—adds layers of rules, phase-outs, credits, and deductions that make self-preparation more daunting for an increasing number of taxpayers. The "One Big Beautiful Bill" legislation currently under discussion could further shift share from DIY to assisted preparation—H&R Block's management expects it to capture roughly twenty basis points of share from DIY—because complexity is the friend of professional tax preparers.

This is the counter-intuitive insight at the heart of the bull thesis: the very same forces that the bear case points to as threats—legislative change, gig economy growth, new financial products—actually increase the demand for professional tax help. When Congress adds a new clean energy credit with eight pages of qualifying criteria and three phase-out schedules, a TurboTax user stares at a screen and wonders if they are leaving money on the table. An H&R Block client hands the forms to a professional who has been trained on exactly those provisions.

The gig economy supercharges this dynamic. There are tens of millions of Americans earning income through ride-sharing, food delivery, freelance platforms, and side businesses. Every one of them is a potential 1099-K filer with messy, multi-source income—the exact demographic that finds self-preparation overwhelming and gravitates toward either Wave's small business tools or Block Advisors' professional services.

A January 2025 study by H&R Block and Morning Consult found that nearly half of gig workers and side hustlers were unaware of the 1099-K reporting changes—an education gap that represents both a marketing opportunity and a genuine service need. H&R Block estimates the total addressable market for small business services exceeds one hundred billion dollars. Even capturing a single-digit percentage of that market would dwarf Wave's current revenue contribution.

The AI angle is perhaps the most underappreciated element of the bull case.

The consensus narrative is that generative AI is a threat to H&R Block because it will enable consumers to prepare their own taxes without professional help. Ask ChatGPT about your tax situation, get a perfect answer, file yourself—no preparer needed. This narrative sounds compelling until you think about liability. When ChatGPT gives you bad tax advice and the IRS comes calling, who pays the penalty? Not OpenAI. When H&R Block gives you bad advice, they have a guarantee program that covers the cost of errors. The liability gap between "AI chatbot" and "licensed tax professional backed by a seventy-year-old institution" is not a gap—it is a chasm.

The counter-narrative—which H&R Block is betting on—is that AI does not replace human tax professionals but makes them dramatically more efficient. Through the AI Tax Assist partnership with Microsoft, built on Azure OpenAI, H&R Block's sixty thousand tax professionals have access to an AI system trained on seventy years of institutional knowledge. This does not eliminate the human; it amplifies them.

A tax professional who can answer complex questions faster, identify overlooked deductions more reliably, and process returns more efficiently creates more value per hour—which improves margins in the assisted business without reducing headcount. Think of it as giving every tax preparer a genius research assistant who has memorized the entire Internal Revenue Code and every prior-year return H&R Block has ever filed.

H&R Block is the only company in the tax industry selected for Microsoft's "AI 100" program, giving it preferred access to enterprise AI development resources. The competitive advantage is the combination of AI capability with proprietary training data and human expertise—a tripartite asset that no pure-tech competitor or independent CPA can replicate.

The capital return story reinforces the bull case at current valuations.

At roughly seven times earnings with a five percent dividend yield, investors are being paid handsomely to wait. The $1.5 billion share repurchase authorization (with approximately $700 million remaining) means the company can retire a meaningful percentage of its current market capitalization at depressed prices.

Eight consecutive years of dividend increases, with recent raises of twelve to seventeen percent, suggest management confidence in the sustainability of cash flows. Since 2016, H&R Block has bought back over forty-three percent of its outstanding shares—a level of capital return that mechanically supports EPS growth and signals management's view that the stock is undervalued.

The KPIs That Matter

For investors tracking H&R Block's ongoing performance, three metrics matter above all others:

First, total U.S. tax returns prepared—the single most important volume indicator for the core business. This number captures both assisted and DIY filings and reflects H&R Block's share of the overall tax preparation market. If this number is declining, no amount of pricing optimization or cost-cutting will save the business.

Second, Wave revenue growth rate—the barometer of whether the year-round strategy is working. Sustained double-digit growth signals successful cross-selling and market expansion. A deceleration to single digits would suggest the small business opportunity is more limited than management believes.

Third, net client growth in the assisted channel—the specific metric that determines whether H&R Block is winning or losing the battle for high-value, complex-return customers who generate the best economics. The DIY business is important, but the assisted business is where brand, switching costs, and omnichannel positioning create the most durable competitive advantage.

Looking Ahead

Curtis Campbell took the CEO seat on January 1, 2026, inheriting a business that Jeff Jones transformed from a declining legacy brand into a growing, multi-platform financial services company.

Campbell's first earnings call, in February 2026, emphasized AI-enabled tax professional assistance, workflow automation, and the omnichannel "start online, finish with a pro" experience as his strategic priorities—a continuation, not a disruption, of the Jones playbook.

The fiscal 2026 guidance calls for revenue of $3.875 to $3.895 billion and EBITDA of $1.015 to $1.035 billion, both representing growth over the prior year. These are not explosive numbers, but they represent steady, profitable growth from a business generating roughly a billion dollars of annual EBITDA—a cash engine that funds both capital return and investment in the future.

The open questions are consequential.

Will Campbell maintain the aggressive dividend-and-buyback capital return strategy, or will he hunt for another Wave-style acquisition to accelerate growth? His background at Capital One and AWS suggests a leader comfortable with both financial discipline and technology investment—but capital allocation is always a question of emphasis, and the balance between returning cash and investing for growth defines the character of a company's next chapter.

Can Wave continue to grow at double-digit rates as it scales, or will competition from QuickBooks and FreshBooks intensify? Intuit's QuickBooks has roughly six million subscribers and is investing aggressively in AI-powered features. FreshBooks, Zoho, and a constellation of vertical SaaS tools are all competing for the same micro-business customer. Wave's free-tier advantage is real, but it may face pressure as competitors experiment with their own freemium models.

Will Spruce convert its 700,000 sign-ups into a meaningful, scaled financial services business, or will it remain a niche product? The neobank space has been brutal to many startups—even well-funded ones like Dave, MoneyLion, and Varo have struggled to reach profitability. Spruce's advantage is that it does not need to acquire customers from scratch—it inherits them from the tax business—but converting inherited users into engaged daily banking customers is a different kind of challenge.

And most importantly: in a world where AI is making self-preparation easier every year, can the assisted tax business—the beating heart of H&R Block's economics—continue to hold its ground?

These are the questions that will determine whether the Green Square, seventy years after a hundred-dollar newspaper ad in Kansas City, remains one of the most durable consumer franchises in American financial services—or becomes, like the Sears, Roebuck comparison Richard Bloch once made with pride, a cautionary tale about the limits of scale in a digital world.

IX. Further Reading & Resources

-

H&R Block FY2025 Annual Report & 10-K — SEC filing with complete financials, segment detail, and risk factors. Available at investors.hrblock.com.

-

H&R Block FY2025 Proxy Statement (DEF 14A) — Detailed executive compensation disclosure including Jeff Jones' PSU structure, stock ownership requirements, and Curtis Campbell's employment agreement. SEC EDGAR.

-

"H&R Block: A Taxing Fall from Grace" — Harvard Business School Technology and Operations Management case study on the 2010-2016 digital disruption period.

-