Honeywell Aerospace Inc: The $70B Conglomerate Breakup and the Battle for the Skies

I. Introduction & The $70 Billion Pure-Play

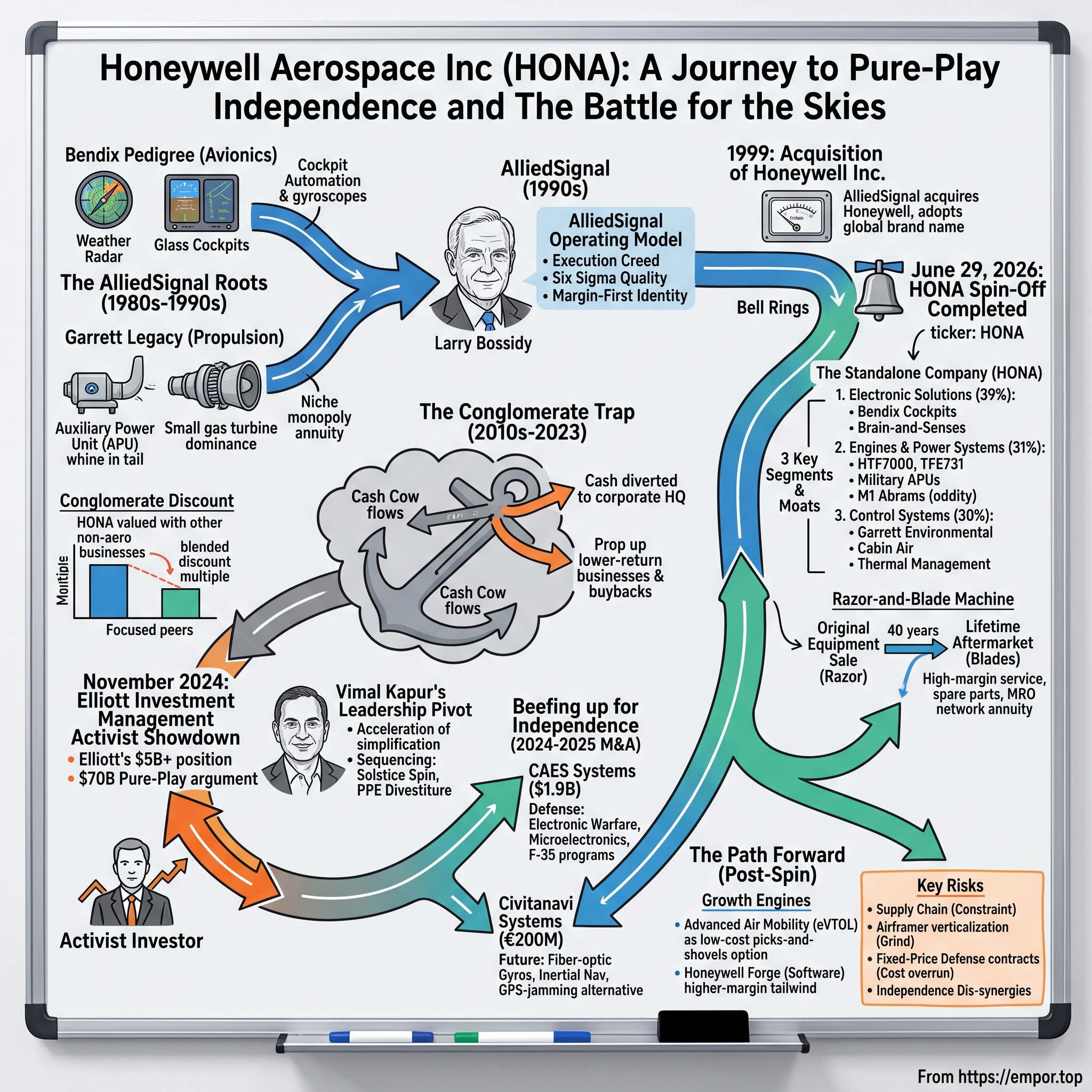

On June 29, 2026, a company that had technically existed inside a larger company for twenty-seven years walked out onto the Nasdaq for the first time under its own name. The ticker was HONA. The company was Honeywell Aerospace Inc., and the moment it began trading, one of the most valuable, least-understood industrial franchises in the world stopped being a line item inside a diversified conglomerate and became a standalone public equity that investors could finally price on its own merits.1

The mechanics of the divorce were almost anticlimactic for something twenty-seven years in the making. Shareholders of the parent — now renamed Honeywell Technologies, still trading under the old HON ticker after a one-for-two reverse split that roughly halved its share count — received one share of Honeywell Aerospace for every two Honeywell shares they held as of the June 15 record date. Honeywell Aerospace stepped into the public markets carrying roughly 36,000 employees and more than 10,000 customers, and immediately took its place among the largest pure-play aerospace suppliers on Earth.1

The numbers underneath the spin-off explain why Wall Street cared. In fiscal 2025, Honeywell Aerospace generated about $17.4 billion in net sales, threw off roughly $4.3 billion in adjusted operating profit — a margin in the mid-24% range on a reported basis and around 26% on an adjusted segment basis — and in the first quarter of 2026, as a business already being run for independence, expanded its segment margin to 26.5%.[^2]2 Those are not the economics of an industrial-parts supplier scraping for pennies against a purchasing department. Those are the economics of a business that, once designed into an airframe, essentially cannot be dislodged for the thirty-to-forty-year service life of the aircraft.

Which raises the central puzzle of this story. If Honeywell Aerospace was this good — this dominant in cockpits and cabin air and auxiliary power, this sticky, this profitable — why did it spend nearly three decades trapped inside a multi-industry conglomerate, its cash flows quietly diverted to prop up lower-return businesses and fund corporate buybacks? And what finally broke it loose? The answer arrived in November 2024 in the form of Elliott Investment Management, which disclosed a stake exceeding $5 billion — one of the largest activist positions in the firm's history — and made a blunt, public argument: conglomerates are dead, and this one is worth far more in pieces.3

Consider what the market was being asked to price. Honeywell Aerospace is not a supplier of one thing; it is a supplier of nearly everything that is not the primary engine or the fuselage. Walk through a modern airliner or a business jet and the Honeywell content is everywhere and mostly invisible: the flight-management computer plotting the route, the inertial reference system that knows the aircraft's exact attitude, the weather radar in the nose, the auxiliary power unit whining in the tail, the environmental-control system pumping conditioned air into the cabin, the wheels and brakes on some airframes, the connectivity hardware beaming data to the ground. Each of these is a certified, safety-critical system with its own decades-long service tail. Bundle thousands of such systems across tens of thousands of aircraft, and you have assembled one of the great recurring-revenue machines in industrial history — a machine that happened to spend a generation hidden behind a fire-alarm business and a warehouse-scanner business.

This is the story of how that machine came to trade under its own ticker. But it is also a story that starts a hundred years earlier, with a self-made inventor in South Bend, Indiana, a pilot obsessed with breathing at 30,000 feet, and a series of mergers so tangled that the company flying the "Honeywell" flag today was originally named after a nineteenth-century thermostat it acquired almost as an afterthought. To understand why HONA is one of the great franchises in modern aviation, you have to understand the razor-and-blade economics of jet engines and avionics, the activist showdown that freed it, the acquisitions that armored it for independence, and — most importantly — the honest case for why it wins from here and what could still break it. A word on posture before we begin: Honeywell tells a confident story about its own moat, and much of it holds up. But "management says it will win" is a claim, not evidence. The work of this piece is to separate the two. Let us start where the DNA was written.

II. The Deep DNA: Bendix, Garrett, and the AlliedSignal Roots

Vincent Bendix was the kind of self-invented American striver the 1920s manufactured in bulk. Born Vincent Bendix in Moline, Illinois, he ran away to New York as a teenager, sold literature door to door, and taught himself engineering on the side. His first fortune came from the automobile: the Bendix drive, the clever little mechanism that let an electric starter motor engage a car's flywheel and then disengage once the engine caught. Before Bendix, you cranked a car by hand and occasionally broke your arm doing it. After Bendix, you turned a key. He founded the Bendix Corporation in 1924, and from starters he pushed into brakes, and from brakes — as aviation exploded in the 1930s — into the instruments that let pilots fly when they could not see the ground.10

This is the part of the Bendix legacy that survives inside HONA today. Bendix became a name synonymous with the flight deck: weather radar that let a crew see a storm cell a hundred miles out, automatic flight controls, navigation instruments, landing gear. When Bendix absorbed the marine and flight-control assets of Sperry, it folded in another century of gyroscope and automation know-how. The through-line from Vincent Bendix's radar sets to the glass cockpits Honeywell sells today is direct: this is the company that helped teach airplanes to fly themselves, and that pedigree in cockpit automation is one of the two founding rivers that feed the modern business.

The other river started in a one-room office in Los Angeles in 1936, opened by a man named John Clifford Garrett.11 Garrett's obsession was altitude. In the 1930s, flying high meant flying above the weather and the turbulence — but the higher you climbed, the thinner and colder the air, until the crew and passengers simply could not breathe. Garrett's company, later called AiResearch, went to work on the unglamorous but existential problem of keeping humans alive in the flight levels: cabin pressurization, cooling, and the intercoolers that let engines gulp thin high-altitude air. When Boeing built the B-29 Superfortress, the pressurized bomber that could cross oceans at 30,000 feet, Garrett's pressurization and environmental systems were part of what made the crew's survival possible.

But Garrett's most durable invention was a small turbine engine that most airline passengers have heard without ever seeing. Listen to the whine in the tail of a parked airliner before the main engines light — that is the Auxiliary Power Unit, or APU, a compact gas turbine that provides electrical power and air conditioning on the ground and can restart the engines in flight. Garrett pioneered the small gas-turbine APU, and Honeywell rode that head start to a position of extraordinary dominance. On several commercial aircraft families, a Honeywell APU is effectively the only APU — a near-monopoly on a component every one of those jets must carry and must service for decades. The exact market-share figure is not something the company breaks out in its filings, but the strategic point survives without a precise number: the APU is a small box that generates a very long, very high-margin aftermarket annuity, and Honeywell owns the franchise.

To grasp why the APU franchise is so valuable, picture the economics from the airline's side. An airline that operates a fleet of a given aircraft type has, on each of those jets, one APU — and if that aircraft family came from the factory with a Honeywell APU, then for the entire operational life of every one of those airplanes, the airline is buying Honeywell overhauls, Honeywell spare parts, and Honeywell service. There is no realistic substitution: you cannot bolt a different manufacturer's APU into the tail without a costly, years-long re-certification that no airline would undertake to save a few points on a maintenance bill. So Honeywell captures a near-total share not just of the original sale but of a thirty-year service relationship, on a component the aircraft cannot legally dispatch without. Multiply that across the global fleets where Honeywell APUs are the standard fit, and you have a franchise that generates dependable, high-margin cash almost regardless of the economic weather — the textbook definition of a niche monopoly with a long tail. This single product line is a microcosm of the entire company's model.

How did a cabin-air company and a cockpit-instruments company end up under one roof? Through the great conglomerate-building of the 1980s. In 1985, Allied Corporation — a chemicals and oil company — merged with The Signal Companies, a diversified industrial group, to create Allied-Signal.12 Garrett had come into the family through Signal, and now sat alongside Bendix's avionics, which Allied had absorbed earlier in the decade. In one corporate entity you suddenly had propulsion, environmental control, and avionics — the three pillars of an aircraft supplier — bolted together almost by accident of dealmaking.

What turned that accident into a machine was a man. In 1991, Allied-Signal recruited Larry Bossidy, a thirty-four-year General Electric veteran and one of Jack Welch's most trusted lieutenants, to run the sprawling, underperforming company.12 Bossidy brought the GE operating religion with him: relentless cost discipline, Six Sigma quality obsession, and a conviction that execution — not strategy decks — was where value was made or lost. He dropped the hyphen (AlliedSignal became the brand), tightened the factories, and leaned hard into aerospace as the crown jewel. Under Bossidy, the aerospace division became the disciplined, high-margin engine of the whole enterprise — a template of operational intensity that, thirty years later, the standalone HONA still invokes.

It is worth dwelling on Bossidy for a moment, because his fingerprints are still on the standalone company's culture. Bossidy had spent decades inside General Electric under Jack Welch, absorbing a management philosophy that treated operational rigor as a competitive weapon in its own right. He co-authored, after his AlliedSignal years, a business book titled Execution — a word that doubled as his entire creed. Where many CEOs of the era chased splashy acquisitions and visionary strategy, Bossidy preached the unglamorous gospel of hitting numbers, running lean factories, and holding managers personally accountable for results. When he arrived at Allied-Signal in 1991, he found a company that had drifted, and he attacked it with a mixture of quality programs, working-capital discipline, and a willingness to fire businesses and people that did not perform. The aerospace division thrived under that treatment precisely because aerospace rewards obsessive process control — a single defective turbine blade can down an aircraft — and Bossidy's insistence on Six Sigma quality mapped perfectly onto a business where quality is not a slogan but a certification requirement. The margin-first, execution-first identity that Honeywell Aerospace carries into independence is, in a real sense, Bossidy's inheritance.

Bossidy's final act rewrote the company's identity. In 1999, AlliedSignal acquired Honeywell Inc. for roughly $14.8 billion.12 Honeywell Inc. was itself an ancient name — it traced to the Butz Thermo-Electric Regulator Company, founded in 1885 around Albert Butz's automatic furnace damper, an early thermostat.13 Here is the twist that confuses people to this day: AlliedSignal was the acquirer and the survivor, but it took the Honeywell name, because "Honeywell" was the far more recognizable global household brand, and moved into a headquarters in Morristown, New Jersey. The company that emerged from the 2020s conglomerate under the Honeywell flag was, in corporate DNA, AlliedSignal — which was Bendix plus Garrett plus a century of mergers. All of that history is what walked onto the Nasdaq in 2026. The question is what makes it worth so much. For that, we have to understand how the business actually makes money.

III. The Razor-and-Blade Machine: Honeywell's Tri-Segment Moat

Here is a fact that sounds like a mistake and is actually the whole strategy: Honeywell is often happy to sell a jet engine or a cockpit to an airframer at a razor-thin margin, sometimes at a loss. If that sounds like a terrible way to run a business, you are thinking about it the way a manufacturer of toasters would. Aerospace does not work like toasters. Aerospace works like razors and blades — and the blades run for forty years.

To see why, follow what happens after Boeing or Gulfstream or Bombardier chooses a supplier for a new aircraft. That choice is not a purchase order; it is a certification event. The engine, the flight-management computer, the environmental-control system — each has to be tested, qualified, and certified by the FAA and its global equivalents as airworthy on that specific airframe. That process costs hundreds of millions of dollars and takes years. Once it is done, the supplier is designed in. Every one of those aircraft that rolls off the line for the next two decades carries that supplier's box, and every one of those boxes has to be inspected, repaired, and overhauled on a rigid schedule for the thirty-to-forty-year life of the airframe — using the supplier's parts, the supplier's manuals, and often the supplier's own maintenance, repair, and overhaul (MRO) network. The engine is the razor, sold cheap to win the platform. The decades of mandatory, high-margin aftermarket service are the blades. Winning the razor is expensive and brutally competitive. Losing the blades, once you have the razor, is almost impossible.

That single dynamic explains the shape of the standalone company, which reports through three segments. Electronic Solutions is the largest, at roughly $6.8 billion of fiscal 2025 sales — about 39% of the total.2 This is the direct heir to the Bendix flight deck: integrated cockpit avionics like the Primus Epic system, flight-management computers, inertial navigation, and — bolstered by recent acquisitions we will come to — electromagnetic defense electronics and space-grade components. It is the brain-and-senses business of the airplane.

Engines & Power Systems, at about $5.4 billion (roughly 31% of sales), is the propulsion and power business.2 It houses the HTF7000 family that powers super-midsize business jets, the venerable TFE731 that has been on the wing of business aircraft since the early 1970s and has logged well over 100 million flight hours across thousands of engines, the commercial and military APUs descended from Garrett, and — a genuine oddity in an aviation portfolio — the AGT1500 gas turbine that is the sole powerplant of the U.S. Army's M1 Abrams main battle tank, a program in service since 1980.1415 A jet-engine company that also powers America's tanks is a reminder of how deep and idiosyncratic this installed base runs.

A quick note on why the split across three roughly equal-sized segments is itself a strength rather than a sign of a company that lacks focus. Because each segment sells a different category of certified system into the same set of airframes, Honeywell captures multiple, independent annuity streams from every aircraft it is on — avionics and propulsion and environmental control — which diversifies the aftermarket base across product cycles and technology shifts. A competitor trying to displace Honeywell would have to win not one certification battle but three, on three unrelated technology fronts. That breadth-within-focus is the difference between a diversified conglomerate (a grab-bag of unrelated businesses) and a diversified franchise (many defensible positions serving one deeply understood customer and mission). The former destroys value; the latter compounds it.

Control Systems, at roughly $5.2 billion (about 30%), is the descendant of Garrett's altitude obsession: the environmental-control systems that pressurize and cool the cabin, thermal-management systems that keep electronics and engines from cooking themselves, and the actuation that moves flight surfaces.2 It is the least glamorous of the three and one of the most defensible, because cabin air and thermal management are exactly the kind of unglamorous, safety-critical, certified systems that no airframer wants to re-qualify on a whim.

The best way to feel the switching cost is by analogy. Imagine a hospital that has wired its entire building around one manufacturer's monitoring system — every sensor, every cable, every trained technician, every regulatory approval built around that one vendor. Ripping it out to save money on a competitor's cheaper boxes would mean re-wiring the building, re-training the staff, and re-certifying the whole system with the regulator, at a cost that dwarfs any savings. Aerospace is that dynamic on steroids, because the "building" is a flying machine that kills people if it fails, and the regulator is the FAA. Once a flight deck, an engine, or an environmental-control system is certified on a Boeing 737 or a Gulfstream G650, displacing it means a competitor must fund hundreds of millions of dollars of re-engineering and re-certification, wait years for approval, and persuade a risk-averse airframer to accept the disruption — all to unseat an incumbent that works fine. It almost never happens mid-program. The incumbent's position is, for practical purposes, locked for the life of the airframe, which can run half a century from first flight to final retirement.

Now layer on the frameworks that professional investors use to test whether a moat is real. In the language of Hamilton Helmer's 7 Powers, Honeywell holds at least three. The first is switching costs, already described — the certification lock-in that makes a designed-in supplier nearly permanent. The second is scale economies: a global web of MRO centers and a spare-parts logistics network that a new entrant could not replicate without decades and billions, and that lets Honeywell service an aircraft anywhere in the world faster and cheaper than a subscale rival. The third, more arguable, is a cornered resource in specific know-how — turbine-blade coatings that survive combustion temperatures, thermal-management designs, decades of certified engineering data — the kind of tacit knowledge that does not walk out the door easily.

Run the same business through Porter's Five Forces and the picture holds. The threat of new entrants is close to nil: the capital, the certification, and the installed base are impassable barriers. Rivalry exists at the OEM design-win stage — Honeywell fights hard against Collins Aerospace, Thales, GE, and others to get designed into a new platform — but evaporates in the aftermarket, where the incumbent effectively owns the plane. The real pressure comes from two directions, and honest analysis has to name them: buyer power and the aftermarket grab. The airframers — Boeing and Airbus above all — are enormous, sophisticated customers who would very much like to capture the lucrative service revenue themselves, and they push constantly to verticalize component aftermarkets and squeeze tier-one suppliers. That tension is not hypothetical; it is the central competitive war of the coming decade, and we will return to it in the bear case.

It helps to put concrete arithmetic behind the razor-and-blade metaphor, because the ratios are what make aerospace unusual. Across a typical program life, the original-equipment sale of an engine or an avionics suite is often the smaller half of the lifetime revenue; the aftermarket — spare parts, scheduled overhauls, repairs, upgrades — frequently exceeds the original hardware value several times over, and it does so at margins that can be double or triple those on the original sale. A commercial engine sold at a loss to win a Boeing platform can, over thirty years of mandatory overhauls, become one of the most profitable single relationships in the company. This is why aerospace suppliers obsess over "shipset content" and "installed base" the way software companies obsess over seats and net revenue retention: each design win is an annuity contract dressed up as a product sale. And because the FAA and its counterparts mandate the maintenance intervals, the demand is not a marketing achievement but a regulatory certainty — the airline cannot skip the overhaul and keep flying legally.

The MRO network that captures this annuity is itself a moat that compounds with scale. Honeywell operates and authorizes a global web of maintenance, repair, and overhaul facilities, and the value of that network grows non-linearly: the more aircraft in the field carrying Honeywell content, the denser the service network can be, the faster and cheaper an airline anywhere in the world can get a part or an overhaul, and the harder it becomes for a subscale competitor to offer comparable turnaround. An airline grounded by a missing component is losing hundreds of thousands of dollars a day, so speed of service is not a convenience — it is the product. A new entrant would need not just the certified part but a worldwide logistics and repair footprint to match, which is a decade-and-billions problem, not a quarter-and-millions one.

There is a second-order dynamic in the OEM relationship that rewards attention, because it is where the model is most often misread. When Honeywell sells a flight deck or an APU to Gulfstream or Bombardier at a thin margin, the low price is not a concession extracted by a powerful buyer — it is a deliberate investment in an annuity, priced almost like a customer-acquisition cost. The airframer captures the upfront discount; Honeywell captures the twenty-to-forty-year service stream that follows, plus the pricing latitude that comes from being the sole certified source of spare parts once the aircraft is in service. The subtlety is that this only works if the aftermarket actually stays with the original manufacturer, which is precisely what the airframers and a growing ecosystem of independent "parts manufacturer approval" competitors and third-party MRO shops are trying to erode. So the loss-leader logic is genuinely powerful, but it is also conditional: it holds exactly as long as Honeywell can defend its grip on the parts and overhauls that follow the sale. Read that way, the low OEM margin is not a weakness in the numbers but the entry fee to the real business — and the durability of the whole model rests on winning the fight for the blades, not the razors.

The analytical takeaway is this: Honeywell Aerospace is not a great business because it makes clever hardware, though it does. It is a great business because the structure of aviation — certification, safety regulation, and multi-decade service life — converts each hardware win into a locked, recurring, high-margin annuity that is remarkably insulated from the economy, because planes must fly and flying planes must be serviced. Which makes the next question almost unbearable: how does a business this good end up undervalued? The answer is that it was wearing a costume.

IV. The Conglomerate Trap & The Elliott Activist Showdown

For most of the 2010s and early 2020s, if you wanted to own Honeywell Aerospace, you had no choice but to also own a fire-alarm business, a warehouse-automation business, a chemicals-and-refrigerants business, and a building-controls business — all bundled inside Honeywell International, a classic multi-industry conglomerate. And the market did to that bundle exactly what it does to most conglomerates in the modern era: it applied a discount.

The mechanism of the conglomerate discount is worth spelling out, because it is the financial heart of this story. When a superb, high-multiple business like aerospace is stapled to slower-growing, lower-margin segments, the whole entity tends to trade at a blended multiple that sits below what the crown jewel would command alone. Investors who want pure aerospace exposure — and who would pay a premium for it — cannot get it cleanly, so they either stay away or demand a discount for the complexity. On top of that sits a subtler cost: capital allocation. Under the long reign of Dave Cote and then Darius Adamczyk, Honeywell International ran aerospace as a cash cow — a treasury that generated dependable free cash flow which corporate headquarters could redeploy wherever it liked. Sometimes that meant cross-subsidizing weaker segments; often it meant funding conglomerate-level share buybacks. What it frequently did not mean was letting aerospace keep and reinvest its own cash into aerospace-specific M&A or next-generation propulsion at the scale a focused competitor would. The division was, in effect, capital-starved relative to pure-play rivals like GE Aerospace, TransDigm, and RTX, and the market noticed — pricing Honeywell at a persistent discount that observers put in the range of 20% to 30% relative to those focused peers.

To understand how the trap was built, you have to understand the two men who ran Honeywell before Kapur. Dave Cote took over what was then Honeywell International in 2002, inheriting a company reeling from a collapsed merger with General Electric that European regulators had blocked, and spent a celebrated fifteen-year tenure rebuilding it into a disciplined, high-multiple industrial. Cote was, by most measures, an excellent operator — he professionalized the culture, expanded margins, and made Honeywell a Wall Street favorite. But his model was fundamentally a conglomerate model: a portfolio of good businesses, centrally managed, with aerospace as the dependable engine funding the whole. Darius Adamczyk, who succeeded Cote as CEO in 2017, largely continued the approach, pruning at the edges but keeping the diversified structure intact. Neither man was a villain in this story; both ran the playbook their era rewarded. The problem was that the era changed underneath them.

What changed was the market's verdict on diversification itself. Through the 2010s, investors watched a parade of conglomerates trade at persistent discounts to the sum of their parts, and they watched focused pure-plays — companies that did one thing and did it superbly — command premium multiples. The intellectual case for the conglomerate, which had held since the 1960s, quietly collapsed. By the early 2020s the message from capital markets was unambiguous: complexity was being taxed, and focus was being rewarded. Aerospace, the best asset Honeywell owned, was the one paying the highest price for being trapped, because the gap between what it would fetch alone and what it fetched inside the bundle was the widest.

Enter the most feared name in shareholder activism. On November 12, 2024, Elliott Investment Management disclosed that it had built a position in Honeywell exceeding $5 billion — among the largest single bets in the firm's history — and published a letter making the case for a clean breakup into two independent companies: Aerospace and Automation.3 Elliott's argument was not subtle, and it did not need to be, because the evidence was all around it. The conglomerate, Elliott argued, was an obsolete structure that the best industrial managements had already abandoned. General Electric — the very cathedral of the conglomerate faith, the church where Larry Bossidy had trained — had just broken itself into three, and the aerospace piece, GE Aerospace, had been rewarded by the market with a soaring multiple. United Technologies had split into RTX, Carrier, and Otis. Even Honeywell's building-controls cousin, Johnson Controls, had spent a decade shedding businesses to become a pure play. The pattern was unmistakable: focus was being rewarded, and breadth was being punished. Elliott put concrete numbers on the prize, arguing the separated entities could deliver substantial upside — on the order of a stock that could rise roughly 50% or more over two years — as the pieces re-rated toward their focused peers.3

Now, activist arithmetic always deserves skepticism; a firm that has just bought $5 billion of stock has every incentive to paint the sunniest possible picture. But Elliott's structural claim was hard to refute, because it rested not on optimism about Honeywell's operations but on a simple observation about how the market prices focus versus complexity. And crucially, the person on the other side of the table did not spend eighteen months fighting it.

That person was Vimal Kapur, who had become CEO of Honeywell International on June 1, 2023, and added the chairman's title in 2024.6 Kapur, a Honeywell lifer who had run the automation businesses, could have dug in and defended the empire. Instead he pivoted — and here is where management credibility becomes an analytical fact worth weighing. Rather than treating Elliott as a threat to be repelled, Kapur accelerated a portfolio simplification that, in fairness, had begun before Elliott arrived, and turned it into a full breakup. Over roughly eighteen months he executed a sequence: Honeywell committed publicly to separating Aerospace and Automation into independent companies;[^5] it completed the sale of its personal protective equipment business to Protective Industrial Products for about $1.325 billion in May 2025; it spun off its advanced materials business as Solstice Advanced Materials, which began trading on the Nasdaq as SOLS on October 30, 2025; and it finished the marquee act — the aerospace spin-off — on June 29, 2026.6161

There is a subtle point in the sequencing that rewards attention. The advanced-materials spin-off and the PPE divestiture came first, before the aerospace separation, and they were not incidental — they were the warm-up acts that proved the company could execute clean separations and simplify the portfolio methodically rather than in one chaotic lurch. By the time the aerospace spin closed, Honeywell had already demonstrated the operational muscle to carve a business out cleanly, stand up its systems, and float it. That staging also let management argue it was pursuing a coherent strategy of its own rather than simply capitulating to an activist — a distinction that matters for how boards and long-term shareholders judge a management team's independence and credibility. Whether the strategy would have moved this fast without Elliott's $5 billion pressing on the scale is unknowable, and the honest reading is that the activist accelerated a direction management had already, if more slowly, chosen.

Whether you read Kapur's pivot as principled conviction or pragmatic surrender, the behavior is the tell: presented with a credible external challenge, management chose to dismantle its own conglomerate rather than defend it, and executed the sequence on schedule. That is a form of accountability that investors reward. But a breakup is not just a legal event; it is also a chance to reshape the asset before it leaves home. In the two years before the spin, Honeywell went shopping — and what it bought tells you a great deal about the company it wanted HONA to be.

V. Beefing Up for Independence: Capital Deployment & 2024-2025 M&A

If you are going to send a business out into the world as an independent public company, you want it to leave home strong — with the right capabilities, the right growth vectors, and a defensible margin profile. In 2024, Honeywell went on an aerospace shopping spree that was, in hindsight, a deliberate pre-spin fortification. Two deals stand out, and they point in the same strategic direction: deeper into high-barrier defense and autonomy.

The larger of the two was CAES Systems. In June 2024, Honeywell agreed to acquire CAES — a maker of high-reliability radio-frequency electronics, microelectronics, and electromagnetic electronic-warfare systems — from private-equity owner Advent International for about $1.9 billion in cash, closing the deal on September 4, 2024.[^7]4 Strategically, CAES plugged directly into the Electronic Solutions segment and pushed it into some of the most defensible real estate in defense: the RF and microelectronics that sit inside programs like the F-35 fighter, the EA-18G Growler electronic-attack aircraft, and precision munitions. These are not commoditized components; they are qualified onto specific weapons systems, which means CAES came with its own version of the certification lock-in that makes the whole aerospace model work, plus a defense backlog with very high barriers to entry.

Did Honeywell overpay? The honest answer is: possibly a little, and probably worth it. At a purchase price around $1.9 billion, the deal reportedly valued CAES at roughly 14 times estimated 2024 EBITDA on a tax-adjusted basis. That is a full price by industrial standards — but it sits below where prime defense pure-plays were trading at the time, in the mid-to-high-teens multiple range, and for a business that lifts HONA's defense margin mix and hardens its exposure to long-cycle, funded government programs, paying a defense multiple for a defense asset is defensible logic rather than empire-building. The more skeptical read is that any 14-times-EBITDA cash acquisition raises the bar for execution: the synergies and margin accretion have to actually show up, and a spun-off company carrying freshly acquired goodwill has less room for integration missteps.

There is a deeper strategic logic to loading up on defense specifically ahead of a spin. Commercial aerospace is cyclical — it rises and falls with airline profitability, travel demand, and the OEM production rate, which itself gyrates with Boeing's and Airbus's ability to deliver. Defense, by contrast, moves to a different and largely counter-cyclical drummer: government budgets, geopolitical tension, and multi-year procurement programs that do not care whether business-travel demand is up or down this quarter. A standalone aerospace company weighted more heavily toward defense is a steadier, more predictable cash generator — exactly the profile that supports a premium, stable multiple and reassures investors nervous about the airline cycle. Buying CAES was therefore not only about adding capability; it was about tuning the shape of the earnings stream HONA would present to the market on day one, tilting it toward the funded, backlog-rich, less cyclical end of the spectrum. In a world of rising defense budgets across the United States, Europe, and Asia, that tilt looked well-timed.

The second deal was smaller but pointed at the future. In March 2024, Honeywell agreed to acquire Civitanavi Systems, an Italian specialist in fiber-optic gyroscopes and inertial navigation, in a tender offer valuing the company at roughly €200 million, or about $215 million, and completed the acquisition later in 2024.5 Inertial navigation is the technology that lets an aircraft, a missile, or an autonomous vehicle know precisely where it is and how it is moving without relying on GPS — which matters enormously in a world where GPS can be jammed or spoofed. Civitanavi bridges Honeywell's legacy in high-end defense navigation toward the lower-cost, higher-volume sensing that autonomous and unmanned platforms will require, and it deepened the company's European footprint. It is a small bet on a large trend: the proliferation of things that need to navigate themselves.

Just as important as the assets was the leadership installed to run the independent company, because incentives reveal intent. The CEO of Honeywell Aerospace is Jim Currier, a veteran operator who had led the aerospace business since 2023 from its Phoenix base.8 The Form 10 filing laid out his standalone package: a base salary of $1,400,000 and a target annual cash incentive of 175% of that base, with the bulk of his potential wealth loaded into equity — stock options and performance share units whose value is tied directly to how HONA performs as an independent stock.7 The design is textbook post-spin alignment: pay the CEO modestly in cash and heavily in equity so that his personal fortune rises and falls with the shares public investors are buying. Whether it produces the intended discipline depends entirely on how the performance targets are set — the detail where such plans are made rigorous or made hollow — but the structural intent is clear. A skeptical governance analyst would want to see the specific performance metrics attached to those share units before applauding: options reward any rise in the stock, including a re-rating the market hands over for free on the first day of trading, while performance share units tied to relative total shareholder return or hard operating targets reward genuine outperformance. The gap between those two designs is the gap between paying for luck and paying for skill, and it is exactly the kind of detail that separates alignment on paper from alignment in fact.

Currier himself is worth a closer look, because the character of a spun-off company's first CEO shapes its early identity. He is an operator rather than a financier or a celebrity executive — a career aerospace man who rose through the business and took the helm of the aerospace division in 2023, running it from Phoenix, the historic heart of the old Garrett propulsion operations. That profile matters: a spin-off in its fragile early years needs someone who knows where the bodies are buried in the factories and the MRO shops, who can wring out the dis-synergies of separation, and who can defend margins contract by contract against sophisticated airframe customers. It is a less glamorous mandate than a growth-story CEO's, but it is the right one for a business whose value proposition is durability and profitability rather than reinvention. The risk in an operator-CEO is the mirror image: a leader steeped in the existing business may be slower to make the bold, uncomfortable bets — in autonomy, in software, in next-generation propulsion — that could matter a decade out. Which tendency wins will be visible in how HONA allocates capital over its first few years as a public company.

Sitting above Currier is a chairman chosen to set a tone. Craig Arnold, the former chairman and CEO of Eaton Corporation, was named non-executive independent chair of the HONA board.8 Arnold's résumé is a signal in itself: at Eaton he was known as a disciplined, margin-focused operator who took a sprawling electrical-and-industrial company and drove its profitability and multiple steadily higher. Installing him as the independent chair of a newly free aerospace company telegraphs the boardroom priority — operational discipline and margin expansion, not empire-building. The governance package, in other words, was assembled to answer the exact critique that freed the company in the first place. With the asset fortified and the leadership in place, the question turns to growth: where does a mature, cash-rich aerospace franchise find its next act?

VI. Hidden Growth Engines & Speculative Optionality

Every mature cash cow needs a story about the future, and Honeywell has two — one genuinely exciting, one genuinely useful, and both requiring a clear-eyed sense of proportion so that neither is oversold.

The exciting one is Advanced Air Mobility, the industry's term for the electric vertical-takeoff-and-landing aircraft — eVTOLs — that a fleet of well-funded startups is racing to build. Think of them as large, piloted (and eventually autonomous) electric air taxis meant to hop across congested cities. Here is the quietly clever part of Honeywell's position: in a gold rush, the reliable money is often in selling picks and shovels rather than digging for gold yourself. Honeywell is not trying to build its own air taxi. Instead it supplies the critical systems that these aircraft cannot fly without — flight-control computers, electric actuators and motors, and compact power units — to a roster of the leading developers, names like Archer, Joby, Lilium, and Hyundai's Supernal. If even a fraction of these companies reach commercial scale, Honeywell is designed into their aircraft the same way it is designed into a Gulfstream, with the same long aftermarket tail.

The number Honeywell attaches to this — a potential lifetime program backlog exceeding $10 billion — is the kind of figure that deserves to be read with both excitement and suspicion. It is a lifetime and potential number, dependent on aircraft that are, in many cases, not yet certified and startups that are, in many cases, not yet profitable and burning cash at alarming rates. Advanced Air Mobility accounts for less than 3% of Honeywell's revenue today. The correct way to hold it is as an option, not a forecast: a genuine, high-upside call on the future of urban transport that costs relatively little to maintain and could pay off large — but that must not be allowed to distract management or investors from the turbine business that actually pays the bills. If eVTOLs become a real industry, Honeywell is positioned to win a meaningful slice. If they do not, the core is unharmed. That asymmetry is the point.

The useful growth engine is software. Honeywell Forge for Aerospace is the company's push to move up the value chain from selling hardware to selling connected-aircraft services — real-time maintenance diagnostics, fuel-burn and flight-path optimization, and predictive analytics delivered as software-as-a-service. The logic is compelling: Honeywell already sits inside the airplane, already generates torrents of operating data from its own sensors and systems, and software attached to that installed base carries gross margins north of 70% — dramatically higher than hardware, and recurring in a way that smooths the cyclicality of OEM deliveries. The honest caveat is that it remains a small contributor to the overall Electronic Solutions mix, and that "industrial company pivots to high-margin SaaS" is one of the most frequently promised and least frequently delivered transformations in the sector. The prize is real; the execution is unproven at scale. Investors should treat connected-aircraft software as a margin-mix tailwind to watch, not a re-rating catalyst to assume.

Behind both of these sits a longer-horizon question that the whole industry is wrestling with: the decarbonization of flight. Aviation is one of the hardest sectors to decarbonize because jet fuel's energy density is extraordinarily difficult to match with batteries, and Honeywell's exposure here is characteristically indirect and picks-and-shovels. It is not betting the company on a single propulsion breakthrough; instead it is developing hybrid-electric propulsion components, sustainable-aviation-fuel-related technologies (a legacy of its chemicals heritage, some of which departed with the Solstice spin), and the electrical and thermal systems that any future greener aircraft will need regardless of which architecture wins. The honest framing is that this is a multi-decade R&D commitment with uncertain payoff timing, not a near-term earnings driver, and management's job is to fund enough of it to stay relevant without letting it consume the returns the core generates today. For an investor, the relevant test is capital discipline: is R&D spending on these frontier programs sized as a sensible option premium, or is it creeping toward the kind of open-ended "diworsification" that destroys returns in the name of the future?

Neither of these engines changes what Honeywell Aerospace fundamentally is today — a mature, dominant, cash-generative franchise built on turbines and cockpits and cabin air. What they add is optionality: two credible, low-cost ways the story could get bigger, layered on top of a core that does not need them to justify the investment. That distinction — core cash machine versus speculative upside — is exactly the discipline the whole investment case requires, which brings us to the spine of the argument: why HONA wins from here, and what could break it.

VII. The "Why Win / Why Not" Investment Spine & Risk Radar

Strip away the century of history and the corporate theater of the breakup, and an investor is left with a single question: is Honeywell Aerospace, standing on its own, a business that compounds value from here — and at what price is that already assumed? The honest answer requires holding the bull and bear cases in the same hand.

The case for winning rests on three pillars, each grounded in something more concrete than management rhetoric. The first is the installed base. Tens of thousands of active commercial and defense aircraft fly today with Honeywell engines, APUs, cockpits, or environmental systems aboard, and every one of them generates a stream of mandatory, high-margin aftermarket revenue for decades. This is the single most durable feature of the business, and its durability is structural rather than cyclical: a recession may delay a new aircraft order, but it does not stop existing planes from flying and requiring service. The aftermarket is the ballast that keeps the whole enterprise steady when the OEM cycle turns down.

It is worth war-gaming the competitive set to see where HONA actually sits, because "aerospace pure-play" hides real differences. GE Aerospace is the gold standard — but it is fundamentally a large commercial-engine company, and large engines are the single most valuable razor-and-blade franchise in aviation, with aftermarkets that dwarf almost anything else. Honeywell does not make the primary large engines for widebody and narrowbody airliners; it makes almost everything else, plus business-jet engines and APUs. That is a different, more diversified, arguably lower-ceiling franchise than GE's, and an investor betting on multiple convergence should be honest that HONA's content is broader but individually less dominant than a big-engine maker's. TransDigm, at the other extreme, is a collection of highly proprietary, sole-source niche components run with ferocious pricing power and financial engineering, commanding one of the richest multiples in all of industrials. Honeywell shares some of TransDigm's proprietary-content DNA but is far larger, more OEM-exposed, and more constrained by big customers. RTX and its Collins Aerospace unit are the closest true peer — a diversified systems supplier competing head-to-head with Honeywell in cockpits and more. The realistic read is that HONA deserves a premium multiple, but calibrating it to GE Aerospace's may be optimistic; its natural home is likely a strong pure-play multiple that reflects a diversified, sticky, but not big-engine-anchored franchise.

The second pillar is the re-rating thesis — the entire financial logic of the spin-off. As a segment buried inside a conglomerate, aerospace was priced at a blended, discounted multiple. As a standalone stock, HONA can be valued against its true comparables — GE Aerospace and TransDigm, franchises that command some of the richest multiples in all of industrials precisely because of the aftermarket economics described earlier. If HONA converges even partway toward those multiples, the value creation comes from the change in structure, not from any operational heroics. This is the most reliable part of the bull case because it depends least on the future and most on the simple mechanics of how markets price focus. The caveat, and it is a real one, is that a re-rating can be partly or wholly priced in on day one; buying a pure play after the market has already awarded it a pure-play multiple leaves less on the table than buying the conglomerate before the spin.

The third pillar is capital-allocation liberation. Free at last from the corporate treasury that swept its cash to other uses, HONA can reinvest its own free cash flow into aerospace R&D — hybrid-electric propulsion, next-generation flight decks — and into targeted aerospace M&A, while returning the rest to its own shareholders. The management incentives and the choice of a margin-focused chairman are designed to make that discipline stick. This pillar is the most dependent on execution, and therefore the one where a skeptic should demand proof over several years rather than trust the org chart.

The case against is not a rebuttal of the moat — the moat is real — but a catalog of the specific ways this specific business can disappoint. Four risks stand out. The first is the supply chain, which has been the aerospace sector's persistent affliction: shortages of castings, forgings, and aerospace-grade semiconductors that delay engine and cockpit deliveries, trigger late-delivery penalties, and strain relationships with Boeing and Airbus. Honeywell does not control its own inputs end to end, and in a constrained supply environment even a company with a perfect order book cannot ship what it cannot build.

The second is the aftermarket grab already flagged — the structural tension with the airframers. Boeing and Airbus are not passive customers; they are sophisticated giants who understand exactly how profitable the tier-one aftermarket is, and both have strategic ambitions to verticalize component services and capture that margin for themselves. This is the slow, grinding competitive threat that could erode the franchise not in a single blow but over a decade of contract-by-contract pressure. An investor should watch aftermarket margins as closely as any headline number.

The third is the defense-contract structure. With defense representing a large slice of sales — on the order of 40% — HONA carries exposure to fixed-price development programs, the contract type where a supplier agrees to a price before it fully knows its costs. In an era of input-cost and labor inflation, fixed-price development work has been where defense contractors across the industry have taken painful charges, because a cost overrun on a fixed price comes straight out of profit. The CAES acquisition deepened defense exposure, which cuts both ways: more high-barrier, funded backlog, but also more of exactly this contract risk.

Beyond these four, a full risk radar has to flag two items that scale with exactly the strategy management is pursuing. The first is cybersecurity, the shadow side of the connected-aircraft ambition. The more Honeywell turns aircraft into networked data platforms — beaming diagnostics and flight information to and from the ground — the larger the attack surface it creates, and a supplier whose systems sit inside thousands of commercial and military aircraft is an obvious, high-value target. A serious breach of avionics or aircraft-data systems would be both an operational and a reputational event, and the obligation to secure that infrastructure grows with every dollar of connectivity revenue. The second is geopolitical and supply-chain exposure of a specific aerospace flavor: the industry depends on a narrow global base of foundries and specialty-metal suppliers for castings, forgings, and semiconductors, and a company selling defense electronics into a fracturing world of export controls and technology blocs is exposed to both the physical scarcity of inputs and the political friction of who is allowed to buy what. Neither risk is acute today, but both grow in lockstep with the connected-aircraft and defense-heavy strategy the company has chosen.

The fourth is the mundane but real cost of independence itself. A business that lived for decades inside a parent shared a great deal of invisible infrastructure — corporate IT, legal, tax, treasury, compliance, back-office systems. Standing alone means rebuilding all of it, which introduces duplicated overhead and "dis-synergies" that can weigh on margins in the early years before the standalone organization is optimized. This is the standard tax of every spin-off, and the honest question is not whether it exists but whether management can absorb it faster than it erodes the very margin story that justified the separation.

There is a useful myth-versus-reality check embedded in the whole spin-off narrative. The myth, repeated in every celebratory account of a breakup, is that separation creates value — that the act of unbundling conjures wealth out of thin air. The reality is more disciplined: separation reveals value that was always there but obscured, and it enables value by improving capital allocation and focus. Those are real, but they are not magic, and they are partly self-limiting, because the moment the market can see the crown jewel clearly, it prices the jewel — often before or on the first day of trading. The investor who profited most from Honeywell's simplification may well have been the one who bought the discounted conglomerate in 2023 or early 2024, not the one buying the clean pure-play in July 2026. The second myth worth puncturing is that a pure-play automatically operates better than a division. It can — focus removes distraction and aligns incentives — but it also strips away the shared services, the corporate balance-sheet strength, and the diversification cushion that a big parent provided. Whether HONA operates better alone is a hypothesis to be tested against the margin line over the next several years, not a law of nature.

An activist or short-seller stress-testing HONA would press on precisely these seams: the fixed-price defense tail, the dis-synergy drag, the sustainability of aftermarket margins under airframer pressure, and the risk that a full pure-play multiple is already baked into the price so that the easy re-rating money has been made. None of these breaks the franchise; all of them could compress the returns.

Management gave investors its first real standalone pitch at an aerospace investor day on June 3, 2026, weeks before the spin closed, and the framing there is the baseline against which future credibility should be judged. The headline commitments were a 6% to 8% organic sales growth rate compounding through the end of the decade, continued margin expansion from the mid-26% level, and free cash flow growing faster than earnings — the last a signal that management wants to be judged on cash conversion, not just accounting profit.9 The value of an investor-day target is that it becomes a promise on the record: the discipline of a management team is revealed over time by whether it hits the numbers it sets, explains the misses candidly when it doesn't, and keeps its story consistent from one presentation to the next rather than quietly moving the goalposts. HONA has no track record as a standalone yet — its entire history of promises begins now — which means the early quarters carry outsized weight in establishing whether this team sets targets it can beat or targets it will have to walk back. Skeptical investors should treat the first two or three earnings calls less as data points on the business and more as data points on management's honesty.

Which is why, cutting through the noise, three KPIs matter most for tracking whether the thesis is working. The first is organic sales growth: management has framed a target of roughly 6% to 8% organic growth per year, driven by the commercial aftermarket recovery and a defense ramp, and this number is the cleanest readout on whether the installed-base flywheel and backlog are actually compounding.9 The second is segment operating margin, which ran at 26.5% in the first quarter of 2026; watching that figure hold and climb over multiple years — not one flattering quarter — is how an investor separates a genuine standalone efficiency story from a cyclical sugar high and a dis-synergy stumble.[^2] The third is free-cash-flow conversion — how much of operating profit turns into actual cash — because a capital-intensive, long-cycle business lives or dies on cash generation, and disciplined conversion is the ultimate proof that the capital-allocation liberation is producing real, deployable money rather than accounting profit. Watch those three, and you are watching the actual argument rather than the press release.

VIII. Epilogue & Outro

Step back the full hundred years, and the arc has a strange symmetry to it. Two founders — Vincent Bendix teaching airplanes to fly by instrument, John Garrett keeping their occupants alive at altitude — built businesses that were merged, re-merged, renamed, and buried inside ever-larger corporate structures until the original names survived only as engineering legacies. The company that emerged wearing the "Honeywell" badge was really AlliedSignal, which was really Bendix plus Garrett, disciplined by a GE-trained operator and rebranded after the thermostat company it acquired. For twenty-seven years that inheritance sat inside a conglomerate, its cash quietly financing other people's priorities, its true value obscured by a discount the market applies to complexity. It took a $5 billion activist bet and a CEO willing to dismantle his own empire to set it free.

The activist chapter deserves a clear-eyed epitaph, because it is easy to draw the wrong lesson from it. The tidy version says Elliott showed up, demanded a breakup, and unlocked billions — activism as heroism. The more accurate version is that Elliott's real contribution was timing and pressure, not insight: the case for separating aerospace was visible to anyone who could read a sum-of-the-parts model, and management was already drifting toward simplification. What the $5 billion stake did was compress a multi-year drift into an eighteen-month execution and remove management's option to stall. That is genuinely valuable — capital that forces good decisions to happen faster is doing real work — but it is a reminder that the underlying value was created a century ago by Bendix and Garrett and compounded by decades of certified installed base, not conjured by a hedge fund's letter. Activists harvest value; they rarely create it.

There are lessons in that for anyone who studies how value is created and hidden. The first is the power of activist-driven simplification — the recurring modern discovery that a superb business trapped inside a mediocre structure is worth more once it is cut loose, and that sometimes the most value-additive corporate act is subtraction. The second is the enduring strength of switching costs and installed-base economics: the reason aerospace commands premium multiples is not glamour but the certification lock-in and multi-decade service annuity that make a designed-in supplier nearly permanent. The third is that some of the best businesses in the world hide in plain sight, their quality masked by the company they are forced to keep.

There is a fourth lesson, quieter than the others, about the relationship between structure and time. Honeywell Aerospace was a superb business in 2010 and 2015 and 2020, just as it is in 2026; nothing about the underlying franchise changed on June 29. What changed was the wrapper — and the wrapper turned out to be worth twenty or thirty percent of the value. For long-term investors, that is a reminder that the same assets can be worth materially different amounts depending on how they are held, who controls the capital, and what the market can see. The patient money is often made not by finding a better business but by finding a great business in the wrong wrapper and waiting for the wrapper to come off. The harder question — always — is whether you are early enough that the market has not already figured it out, and here the timeline is unforgiving: by the time a spin-off is a headline, the discount it was meant to cure is usually well on its way to closing.

But the neutral posture this story opened with has to close it too. Freedom is an opportunity, not an outcome. HONA now has to prove, on its own income statement and its own cash-flow statement, that the margin it inherited can be defended against the airframers, that the fixed-price defense work will not spring leaks, that the dis-synergies of independence will be absorbed rather than allowed to fester, and that the re-rating the whole exercise was built to capture has not already been paid away in the opening price. The conglomerate discount is gone. What replaces it — a durable pure-play premium earned through execution, or a fresh set of standalone disappointments — is a question that only the next several years of results can answer. The airplane has left the hangar. Whether it climbs is now, finally, in the hands of a company that has no one left to blame but itself.

References

-

Honeywell Technologies Launches As Independent, Pure-Play Automation Company Following Completion of Honeywell Aerospace Spin-Off — PR Newswire, 2026-06-29 ↩↩↩

-

Honeywell Aerospace Inc. Form 10-12B/A Registration Statement (FY2025 financials and segments) — SEC EDGAR, 2026 ↩↩↩↩

-

Activist investor Elliott Management has $5 billion Honeywell stake, seeks breakup — CNBC, 2024-11-12 ↩↩↩

-

Honeywell Completes Acquisition of CAES — Honeywell, 2024-09-04 ↩

-

Honeywell to Acquire Civitanavi Systems to Strengthen Autonomous Operations Offerings — PR Newswire, 2024-03-28 ↩

-

Honeywell Completes Sale of Personal Protective Equipment Business to Protective Industrial Products — Honeywell, 2025-05-22 ↩↩

-

Honeywell Aerospace Inc. Form 10-12B, Exhibit 10.8 (James Currier offer letter) — SEC EDGAR, 2026-02-17 ↩

-

Honeywell Announces CEO and Board Chair for Aerospace Spin-off — PR Newswire, 2025 ↩↩

-

Honeywell Aerospace targets 6-8% organic sales CAGR to 2030 (Investor Day) — TheFly via TipRanks, 2026-06 ↩↩

-

John Clifford Garrett — Pima Air & Space Museum Hall of Fame ↩

-

15 Surprising Facts About Honeywell's 1,500 Horsepower Turbine Tank Engine — Honeywell Aerospace ↩

-

TFE731 Engine Still Going Strong at 50 — Honeywell Aerospace ↩

-

Solstice Advanced Materials Completion of Spin-Off, Form 8-K — SEC EDGAR, 2025-10-30 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube