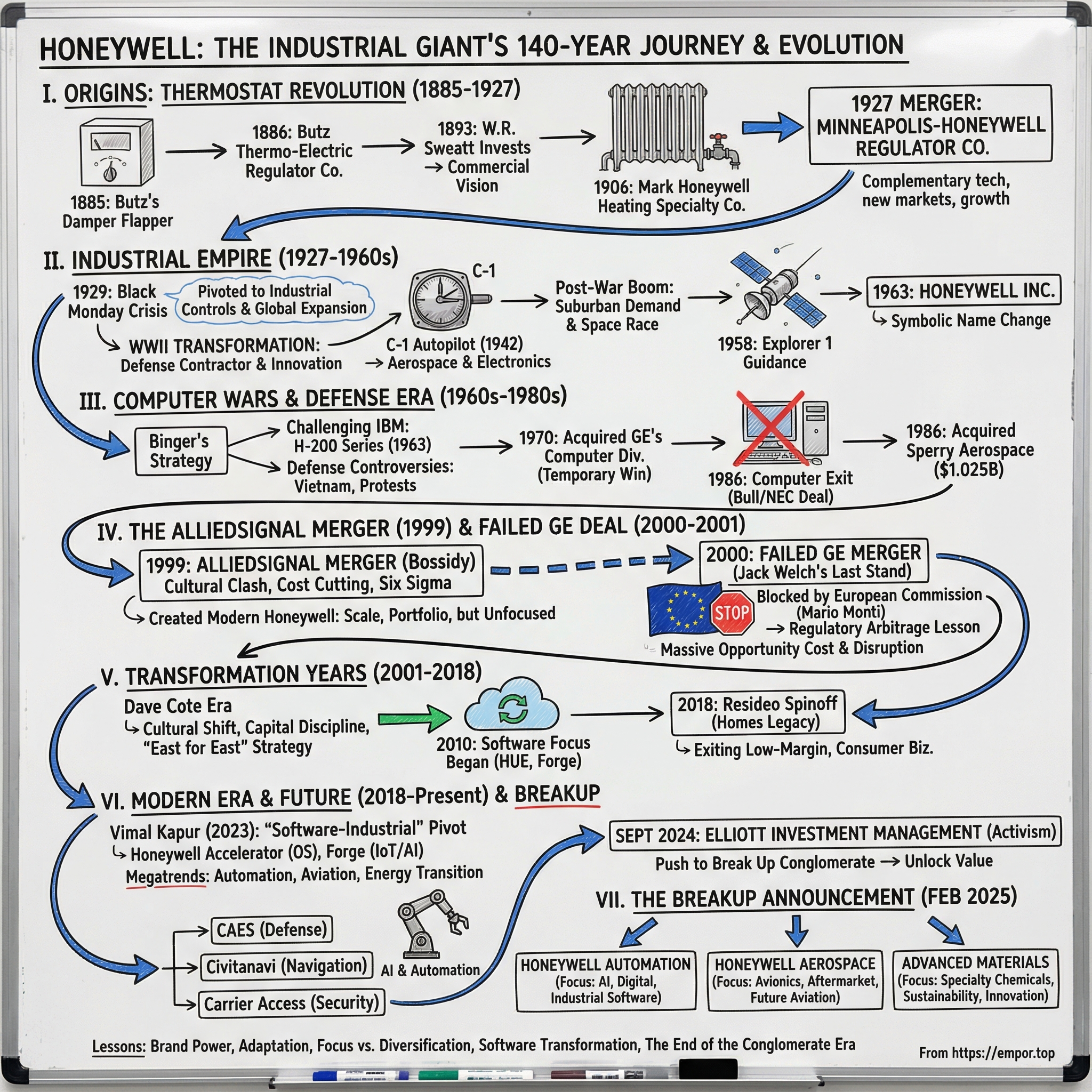

Honeywell International: The Story of America's Industrial Automation and Aerospace Giant

I. Introduction & Episode Roadmap

Picture this: It's December 2024, and Elliott Investment Management, the activist hedge fund with over $70 billion under management, has just taken a $5 billion-plus stake in a 140-year-old industrial conglomerate. Their demand? Break it up. The target? Honeywell International—a company that started with a simple invention to keep Minnesota homes from freezing and somehow ended up building the guidance systems that took Apollo astronauts to the moon.

Today's Honeywell is a $145 billion market cap behemoth generating $36.7 billion in annual revenue across four seemingly disconnected segments: aerospace systems that power everything from commercial jets to military drones, building automation that controls the climate in your office tower, industrial automation software running factories worldwide, and specialty materials creating everything from refrigerants to bulletproof vests. The company touches nearly every aspect of modern life—from the moment your plane takes off to the temperature of your office to the chips in your smartphone.

But here's the question that keeps coming up in boardrooms and trading floors: How did a thermostat company become a defense contractor, then a computer manufacturer, then pivot to become what CEO Vimal Kapur calls a "software-industrial" powerhouse? And more importantly, why is this industrial giant now planning to split itself into three separate companies—Honeywell Automation, Honeywell Aerospace, and Solstice Advanced Materials—after spending decades assembling itself through over 100 acquisitions?

The answer lies in one of American business's most remarkable stories of reinvention. It's a tale that spans three centuries, involves forgotten computer wars with IBM, a dramatic failed merger with General Electric that came down to European regulators' fears about aircraft engine monopolies, and a company that has somehow managed to be simultaneously everywhere and invisible. While names like GE and IBM dominated headlines, Honeywell quietly built an empire by mastering the unglamorous but essential: keeping buildings comfortable, planes flying safely, and factories running efficiently.

This is also a story about timing—both good and catastrophically bad. About a company that entered the computer business just as IBM was establishing dominance, tried to merge with GE just as antitrust sentiment was shifting globally, and is now breaking itself apart just as industrial conglomerates are coming back into fashion. It's about leadership dynasties that provided 75 years of stability, followed by decades of musical chairs in the C-suite. And it's about a fundamental tension that has defined Honeywell for a century: Should you be a focused specialist or a diversified conglomerate?

What we'll explore today is how Honeywell became the ultimate industrial survivor—a company that has outlasted most of its original competitors, pivoted through multiple technological revolutions, and somehow emerged as one of the few American industrials that hasn't been disrupted by Silicon Valley or decimated by Asian competition. We'll examine the playbook they've developed for acquiring and integrating businesses, their unique approach to industrial software, and why breaking up might actually be the smartest strategic move they've made in decades.

We'll start in 1885 Minneapolis, where a Swiss immigrant's solution to waking up in a freezing house would launch an industrial empire. We'll witness the birth of modern building automation, the transformation into a defense contractor during World War II, and the computer wars that almost destroyed the company. We'll dissect the AlliedSignal merger that created the modern Honeywell, the failed GE deal that would have created an industrial monopoly, and the current three-way split that promises to unlock $20 billion in market value.

Along the way, we'll extract lessons about brand power, regulatory arbitrage, the challenges of running a conglomerate in the age of specialized investing, and what happens when financial engineering meets industrial engineering. We'll examine why Honeywell trades at a discount to pure-play competitors despite superior execution, how they've managed to maintain 30-40% software gross margins in traditionally hardware businesses, and whether the upcoming split is admission of failure or strategic brilliance.

This isn't just a corporate history—it's a masterclass in adaptation, a cautionary tale about the limits of scale, and potentially, the blueprint for how century-old industrial companies can compete in the software age. Whether you're an investor trying to understand industrial technology, an executive managing a complex portfolio, or simply curious about the hidden giants that make modern life possible, Honeywell's story offers insights that transcend any single industry.

So buckle up as we trace the unlikely journey from a Minneapolis basement workshop to a global industrial software empire, and explore why three smaller Honeywells might be worth more than one giant one. The thermostat that started it all was designed to maintain perfect temperature balance—ironically, it took 140 years for the company itself to find its own equilibrium.

II. Origins: The Thermostat Revolution (1885–1927)

The winter of 1885 in Minneapolis was particularly brutal, even by Minnesota standards. Temperatures plunged to minus 30 degrees Fahrenheit, and keeping a home warm meant one thing: someone had to wake up every few hours throughout the night to shovel coal into the furnace. Miss a feeding, and you'd wake to frozen pipes and frost on the inside of your windows. It was in this environment that Albert Butz, a Swiss immigrant and inventor, had an idea that would seem obvious in retrospect but was revolutionary at the time: What if the furnace could regulate itself?

Working in his workshop, Butz created what he called the "damper flapper"—a thermostat that could automatically regulate furnace dampers using a motor wound by a clock mechanism. When the temperature dropped below a set point, the device would open the furnace damper, allowing more air to stoke the fire. When it got too warm, it would close the damper, banking the flames. The implications were immediate and profound: for the first time in human history, you could maintain a consistent indoor temperature without constant human intervention. You could sleep through the night without fearing frozen pipes. You could leave your house for days without returning to an arctic interior.

On April 23, 1886, Butz received a patent for his invention and formed the Butz Thermo-Electric Regulator Company in Minneapolis. But like many inventors, Butz was better at creating than commercializing. The company struggled to find customers—the device was expensive, complicated to install, and required educating a market that didn't yet know it needed automatic temperature control. By 1888, facing mounting debts and limited sales, Butz was forced to sell his patents to the Consolidated Temperature Controlling Company, which itself was teetering on bankruptcy.

Enter William R. Sweatt, a character who would prove to be one of the most important yet underappreciated figures in American industrial history. Sweatt wasn't an inventor or an engineer—he was a businessman who understood something Butz didn't: the value wasn't in the technology itself but in creating a market for it. When Sweatt bought into the struggling company in 1893 for a modest investment, he didn't just acquire patents; he acquired a vision of the future where automatic control would transform not just homes but entire industries.

Sweatt's first insight was that the residential market, while eventually massive, was the wrong place to start. Homeowners were conservative, skeptical of new technology, and scattered across a vast geography. But commercial buildings—hotels, offices, schools—they had professional maintenance staff, larger budgets, and more acute problems with temperature control. A hotel that could advertise "automatic temperature control in every room" had a competitive advantage. A school that didn't need a janitor to tend furnaces all night could reduce costs.

By 1900, Sweatt had completed his buyout of the other investors and reorganized the company as the Minneapolis Heat Regulator Company. He was now sole owner of a business generating about $15,000 annually—modest, but growing. Sweatt's masterstroke was recognizing that selling hardware was just the beginning. The real money was in installation, maintenance, and ongoing service contracts. He built a network of trained technicians who could not only install systems but maintain them, creating recurring revenue streams that would become the backbone of the business model.

Meanwhile, 500 miles away in Wabash, Indiana, another inventor was tackling a different but related problem. Mark Honeywell, a plumbing and heating contractor, was frustrated with the inefficiency of hot water heating systems. The problem was that water, when heated, would expand and create air bubbles that would get trapped in radiators, preventing proper circulation. The solution required manually bleeding each radiator—a time-consuming and imperfect process.

In 1906, Honeywell invented what he called the "mercury seal generator"—a device that could automatically remove air from hot water heating systems. It was an elegant solution: using mercury's unique properties to create a seal that would allow air to escape while keeping water in. That same year, he founded the Honeywell Heating Specialty Company with an initial investment of $5,000. Unlike Butz, Honeywell was both inventor and businessman. He quickly built a network of distributors and positioned his product as essential for any modern hot water heating system.

The two companies were natural competitors, but they were also natural complements. Minneapolis Heat Regulator controlled temperature through furnace dampers; Honeywell Heating Specialty ensured efficient heat distribution through radiators. Both were selling into the same market—the rapidly growing commercial building sector of early 20th century America. Cities were building skyward, and every new office building, hotel, and department store needed heating systems.

By the mid-1920s, both companies had grown substantially. Minneapolis Heat Regulator, under Sweatt's leadership, had expanded internationally with offices in Canada and Europe. Annual revenues exceeded $3 million. Honeywell Heating Specialty had similarly grown, with Mark Honeywell's aggressive marketing and superior technology capturing significant market share. But both faced a common challenge: larger competitors were emerging, and the cost of R&D and market expansion was growing exponentially.

The merger discussions began in 1926, initiated by investment bankers who saw the obvious synergies. But this wasn't just a financial transaction—it was a merger of two very different corporate cultures and personalities. Sweatt was the careful strategist, focused on steady growth and financial discipline. Mark Honeywell was the showman-inventor, passionate about technology and prone to bold bets. The negotiations were complex, involving not just valuation but governance structure, headquarters location, and whose name would go on the door.

On April 5, 1927, the merger was completed, creating the Minneapolis-Honeywell Regulator Company. The combined entity had assets of $3.5 million, 1,000 employees, and a dominant position in the American heating controls market. In a compromise that reflected both egos and practical considerations, Mark Honeywell became president while W.R. Sweatt served as chairman. The Honeywell name was chosen for the combined company—Mark Honeywell had insisted on it, arguing his name had better brand recognition.

The timing seemed perfect. The Roaring Twenties were in full swing, construction was booming, and demand for building controls was insatiable. The newly merged company immediately embarked on an ambitious expansion plan, opening new factories, hiring engineers, and developing next-generation products. They introduced the "Chronotherm," the first clock-controlled thermostat, which could automatically adjust temperature based on time of day—revolutionary for reducing heating costs in commercial buildings.

But storm clouds were gathering. Within 18 months of the merger, Black Monday would strike, the Great Depression would begin, and the combined company would face its first existential crisis. The merger that had seemed so promising in the optimism of 1927 would soon be tested by the harshest economic conditions in American history. Yet it was precisely this trial by fire that would forge Minneapolis-Honeywell into something more than just a heating controls company—it would force them to diversify, innovate, and ultimately transform into the industrial conglomerate we know today.

The foundation was set: two complementary technologies, two strong brands, and two very different leaders now united in a single company. What happened next would determine whether Minneapolis-Honeywell would remain a niche player in building controls or evolve into something far greater. The answer would come from an unexpected source: global war and the birth of the military-industrial complex.

III. Building an Industrial Empire (1927–1960s)

October 28, 1929. As Wall Street traders leaped from windows and fortunes evaporated in minutes, the executives at Minneapolis-Honeywell Regulator Company gathered in their wood-paneled boardroom overlooking the Mississippi River. The combined company, barely two years old, had just reported assets valued at over $3.5 million. By the close of Black Monday, paper wealth across America had vanished, construction projects were being cancelled en masse, and their primary market—new commercial buildings—was about to disappear almost entirely.

W.R. Sweatt, now firmly in control as chairman after Mark Honeywell's death in 1929, faced a stark choice: retrench and try to survive on maintenance contracts for existing systems, or use the crisis to transform the company entirely. Sweatt chose transformation, but not in the way anyone expected. Instead of cutting costs, he increased research spending. Instead of focusing on their core market, he began acquiring competitors at fire-sale prices. It was a contrarian bet that would establish the Sweatt dynasty's approach to crisis management: when others retreat, advance.

The first major pivot came from necessity. With new construction virtually halted, Minneapolis-Honeywell needed new markets. Sweatt noticed something interesting in their service data: industrial facilities—factories, refineries, power plants—were still operating, and they needed increasingly sophisticated control systems. A petroleum refinery couldn't simply shut down because of economic conditions; if anything, they needed better controls to operate more efficiently during tough times. This insight led to the creation of the Industrial Division in 1931, marking the company's first major expansion beyond building controls.

The development of the "Brown Instrument" line of industrial controls in 1934 was the breakthrough. These devices could measure and control temperature, pressure, and flow in industrial processes with unprecedented precision. A petroleum refinery using Brown Instruments could increase yield by 2-3% simply through better process control—worth millions in an era of razor-thin margins. The sales pitch was compelling: the controls would pay for themselves within months through improved efficiency.

But Sweatt's real genius was recognizing that Minneapolis-Honeywell's future lay beyond American borders. In 1934, while most American companies were still reeling from the Depression, he orchestrated a partnership with Yamatake Company in Japan. The Japanese were embarking on rapid industrialization, and they needed control systems. The deal was structured brilliantly: Yamatake would manufacture Minneapolis-Honeywell designs under license, paying royalties while adapting products for Asian markets. Similar deals followed in Europe, creating a global network of partnerships that generated revenue without requiring capital investment.

The Sweatt dynasty—first W.R., then his son Harold who took over in 1934—would provide an astounding 75 years of uninterrupted family leadership. This continuity gave Minneapolis-Honeywell something rare in American business: the ability to think in decades rather than quarters. Harold Sweatt, who would lead the company until 1953, inherited his father's contrarian instincts but added his own innovation: he believed the company should be at the forefront of every major technological shift, even if it meant cannibalizing existing products.

December 7, 1941, changed everything. Within days of Pearl Harbor, Harold Sweatt was in Washington, meeting with War Department officials. The military needed precision control systems for everything from tank engines to bomber cabins to munitions factories. Minneapolis-Honeywell's experience with industrial controls made them an ideal contractor. But the military wanted more than just suppliers—they wanted partners in developing entirely new technologies.

The company's transformation into a defense contractor was swift and total. Employment jumped from 3,000 in 1940 to 12,000 by 1943. Factories that had been making thermostats were converted to produce artillery shell fuses. Engineers who had designed building controls were now working on classified projects. Revenue quintupled. But the most important development wasn't the money—it was the technology transfer. Working on military projects exposed Minneapolis-Honeywell to cutting-edge research in electronics, precision manufacturing, and systems integration.

The crown jewel of their wartime work was the C-1 autopilot, completed in 1942. This wasn't just an incremental improvement on existing technology—it was a fundamental breakthrough in control systems. The C-1 could maintain level flight, execute precise turns, and even perform complex maneuvers, all through an intricate system of gyroscopes, servomotors, and feedback loops. The psychological impact on bomber crews was immense: they could fly longer missions with less fatigue, improving both survival rates and bombing accuracy.

The success of the C-1 established Minneapolis-Honeywell as a serious player in aerospace, a position they would never relinquish. By war's end, they had produced over 30,000 autopilot systems and countless other military controls. The company that had entered the war as a building controls manufacturer emerged as a diversified industrial giant with deep expertise in aerospace, electronics, and precision manufacturing.

The post-war period presented new challenges. Military contracts dried up, but consumer demand exploded as returning GIs started families and moved to suburbs. Minneapolis-Honeywell faced a choice: try to maintain their wartime scale by entering consumer markets, or focus on their industrial and commercial strengths. They chose a middle path that would define their strategy for decades: they would remain primarily B2B but would continuously expand into adjacent technical markets.

The 1950s saw explosive growth through both organic expansion and strategic acquisitions. The development of the T-86 "Round" thermostat in 1953—that iconic circular design that became ubiquitous in American homes—showed they hadn't forgotten their roots. But the real action was in aerospace and industrial controls. The company was selected to provide controls for the Minuteman missile program, the B-52 bomber, and virtually every major military aircraft program.

The space race provided the next catalyst. On January 31, 1958, Minneapolis-Honeywell's stabilization system helped guide Explorer 1, America's first satellite, into orbit. The technical challenge was immense: creating control systems that could function in the vacuum of space, withstand massive temperature variations, and operate with absolute reliability. There was no possibility of maintenance calls in orbit. This forced a level of quality and redundancy that would become hallmarks of Honeywell's aerospace division.

By 1960, the company had been transformed beyond recognition. Revenue exceeded $370 million, up from $3.5 million at the 1927 merger. They employed 30,000 people across dozens of facilities worldwide. The product line had expanded from simple thermostats to include industrial process controls, aerospace systems, and even early computers. The international network established in the 1930s had grown into a major source of revenue and technological innovation.

But success brought new challenges. The company was becoming unwieldy, with divisions that barely communicated with each other. The aerospace division operated like a completely different company from building controls. Industrial automation had its own culture, customers, and competitive dynamics. The question facing leadership was whether this diversification was a source of strength or a distraction from core competencies.

In 1963, recognizing both the company's transformation and the need for a clearer identity, the board voted to simplify the name to Honeywell Inc. The "Minneapolis" was dropped, signaling that this was no longer a regional company. The "Regulator" was removed, acknowledging that they did far more than just regulate temperature. It was a symbolic change that reflected a fundamental reality: the heating controls company founded in 1886 had evolved into something entirely different—a technology conglomerate competing on the frontiers of aerospace, computing, and automation.

Yet even as Honeywell celebrated its success, storm clouds were gathering. A company called International Business Machines was dominating the emerging computer industry. General Electric and Siemens were becoming industrial giants that dwarfed Honeywell. The comfortable position they had carved out in the 1950s was about to be challenged by larger, better-capitalized competitors. The next phase of Honeywell's evolution would require not just growth but transformation—a willingness to bet the company on new technologies and markets that didn't yet exist.

IV. The Computer Wars & Defense Era (1960s–1980s)

James Binger stepped into the CEO role at Honeywell in 1961 with the confidence of a former Navy fighter pilot and the strategic mind of a Yale-trained lawyer. At his first board meeting, he laid out a vision that seemed almost delusional: Honeywell would challenge IBM in computers, expand aggressively in defense contracting, and become a global industrial powerhouse. Board members exchanged glances—IBM controlled 70% of the computer market, and Honeywell had less than 3%. But Binger had done his homework. He knew something the board didn't: the Pentagon was desperate for an alternative to IBM, and they were willing to pay for it.

The computer division's origins actually dated back to 1955, when Honeywell had formed a joint venture with Raytheon called Datamatic Corporation. Their first product, the D-1000, was a disaster—a room-sized behemoth that cost $2 million and found exactly three customers. But Binger saw potential where others saw failure. In 1957, Honeywell bought out Raytheon's share and went all-in on computers. The H-800, launched in 1959, was their first real competitor to IBM's mainframes—faster, cheaper, and crucially, compatible enough with IBM systems that customers could switch without rewriting all their software.

Binger's strategy was guerrilla warfare against Big Blue. While IBM focused on large corporate accounts, Honeywell targeted government agencies, universities, and international markets where IBM was weak. They pioneered the concept of "liberator" programs—software tools that could convert IBM programs to run on Honeywell machines. The marketing was aggressive, almost personal. One famous ad showed a David-versus-Goliath scene with the tagline: "The Other Computer Company." They were positioning themselves as the scrappy alternative to IBM's monopolistic dominance.

The breakthrough came in 1963 with the H-200 series. Priced 30% below comparable IBM systems but offering superior performance, it was the first serious threat to IBM's dominance. Orders poured in from customers tired of IBM's high prices and legendary arrogance. By 1964, Honeywell had captured 8% of the global computer market—small, but growing fast. The computer division's revenue jumped from $27 million in 1960 to over $250 million by 1965. Wall Street took notice, and Honeywell's stock price doubled.

But even as Binger celebrated success in computers, a darker chapter was unfolding. The Vietnam War was escalating, and Honeywell's defense contracts were becoming increasingly controversial. The company had always made military equipment, but Vietnam was different. This wasn't producing autopilots for defensive aircraft or controls for missile silos—this was creating weapons designed to kill in particularly gruesome ways.

The BLU-26 cluster bomb, which Honeywell began producing in 1964, became a symbol of the war's brutality. Each bomb contained hundreds of steel ball-bearing bomblets that would scatter over an area the size of several football fields, shredding anything in their path. Honeywell also manufactured components for napalm delivery systems and guidance systems for missiles targeting North Vietnam. Most controversially, they produced land mines—devices that would continue killing long after the war ended.

By 1968, Honeywell had become a lightning rod for anti-war protests. The "Honeywell Project," organized by activist Marv Davidov, staged dramatic protests at the company's Minneapolis headquarters. Protesters would chain themselves to doors, disrupt shareholder meetings, and organize boycotts. One infamous incident in 1970 saw hundreds of protesters attempting to shut down Honeywell's annual meeting, leading to 90 arrests. The company's recruiting efforts on college campuses were regularly disrupted by students who saw Honeywell as complicit in war crimes.

Binger's response was tone-deaf at best. In one shareholder meeting, he defended the cluster bomb production by arguing that Honeywell was "helping to defend freedom." When pressed about civilian casualties, he claimed the company couldn't be responsible for how the military used their products. This legalistic argument satisfied no one. Talented engineers refused job offers, customers faced boycott pressures, and employee morale plummeted. The company that had built its reputation on making life more comfortable was now associated with death and destruction.

The financial performance during this period was paradoxical. Defense contracts were incredibly lucrative—by 1969, military sales accounted for nearly 20% of Honeywell's $1.2 billion in revenue, with profit margins far exceeding civilian products. The computer division was finally profitable, capturing 10% of the mainframe market. The stock price had tripled during Binger's tenure. By any financial metric, his strategy was working brilliantly.

But the human cost was mounting. Internal documents later revealed that many Honeywell engineers were deeply uncomfortable with their work. One engineer's diary, discovered years later, described the moral anguish of designing systems that would inevitably kill civilians. The company tried to compartmentalize—keeping defense work separate from civilian divisions—but the taint was spreading. Some of their best computer scientists left for competitors, unwilling to work for a "death merchant."

The 1970s brought new challenges and opportunities. In 1970, Honeywell pulled off a stunning coup by acquiring GE's computer division for $234 million. GE, frustrated by years of losses competing with IBM, was exiting the computer business entirely. Overnight, Honeywell's computer market share jumped to 15%, making them the clear number-two player behind IBM. They inherited GE's customer base, technology portfolio, and most importantly, their GECOS operating system, which would evolve into GCOS—a system still in use today in some legacy applications.

But the victory was temporary. IBM struck back with the System/370 series in 1970, a new architecture that leapfrogged everyone else's technology. Honeywell found itself in an arms race it couldn't win. Development costs were exploding—a new mainframe line cost hundreds of millions to develop. IBM could amortize these costs across a huge customer base; Honeywell couldn't. By 1975, despite having technically superior products in many cases, Honeywell was losing money on every computer sold.

The defense controversy reached its peak in 1975 when the Vietnam War ended, but the damage to Honeywell's reputation lingered. The company faced lawsuits from veterans exposed to Agent Orange (Honeywell had produced components for the spraying systems), protests from international human rights groups about land mines, and continued boycotts from activist organizations. Binger, who retired in 1978, left a company that was financially successful but morally compromised in the eyes of many.

Edson Spencer, who succeeded Binger as CEO, faced an impossible situation. The computer division was bleeding cash—losses exceeded $100 million in 1980 alone. The defense business was profitable but toxic to the company's reputation. Meanwhile, competitors like Siemens and ABB were attacking Honeywell's core industrial and building controls markets. Spencer made the difficult decision: Honeywell would gradually exit both computers and controversial defense contracts.

The computer exit was engineered through a complex transaction with France's Compagnie des Machines Bull and Japan's NEC in 1986. Honeywell retained a minority stake but effectively ended its 30-year war with IBM. The final insult came when industry analysts barely noticed—Honeywell had become such a marginal player that their exit didn't even impact market dynamics.

The defense pivot was more subtle. Instead of making weapons, Honeywell would focus on defensive systems—aircraft navigation, satellite controls, and communications equipment. They would still be a defense contractor, but one focused on keeping American forces safe rather than creating offensive weapons. It was a distinction that mattered more in marketing than reality, but it helped rehabilitate the company's image.

By 1986, when Honeywell acquired Sperry Aerospace from Unisys for $1.025 billion, the transformation was complete. The company that had tried to be everything—a computer giant, a weapons manufacturer, an industrial conglomerate—was refocusing on what it did best: aerospace systems, industrial controls, and building automation. The lessons were expensive but clear: competing with entrenched monopolies like IBM was futile, and controversial products could destroy decades of reputation building.

The Binger era officially ended with his retirement, but its impact lasted decades. He had transformed Honeywell from a modest controls company into a diversified technology giant, but at tremendous cost. The computer division alone had consumed over $2 billion in investment for minimal return. The defense controversies had tainted the brand for a generation. Yet he had also built capabilities in aerospace and electronics that would become the foundation for future growth.

As the 1980s drew to a close, Honeywell faced an existential question: What kind of company did it want to be? The answer would come from an unexpected source—not from Minneapolis headquarters, but from a aggressive competitor-turned-suitor that would completely reimagine what Honeywell could become. The age of financial engineering was about to collide with industrial engineering, and Honeywell would never be the same.

V. The AlliedSignal Merger: Creating a Giant (1999)

Larry Bossidy sat in his Morristown, New Jersey office on a gray March morning in 1999, staring at a spreadsheet that would reshape American industrial history. The CEO of AlliedSignal, a former Jack Welch protégé who had transformed a struggling conglomerate into a Wall Street darling, was contemplating the biggest gamble of his career: acquiring Honeywell, a company with nearly twice as many employees but barely half the profit margins. His CFO had just left after delivering a stark assessment: "Larry, they have a better brand, but we have better operations. If we can't fix their operations, this will be remembered as one of the worst deals in industrial history."

The origins of the merger actually traced back to a chance encounter at an industry conference in 1998. Bossidy and Honeywell CEO Michael Bonsignore were sharing complaints about competing with United Technologies and General Electric when Bossidy made an offhand comment: "You know, Mike, together we'd be bigger than UTC." Bonsignore laughed it off, but Bossidy wasn't joking. He had already run the numbers.

AlliedSignal itself was a product of mergers—formed in 1985 from the combination of Allied Corporation and Signal Companies. Under Bossidy's leadership since 1991, the company had been transformed through ruthless cost-cutting, Six Sigma implementation, and strategic acquisitions. Revenue had grown from $12 billion to $15.1 billion, but more importantly, operating margins had nearly doubled. Bossidy had learned from his mentor Jack Welch that in industrial businesses, operational excellence mattered more than strategy.

Honeywell, by contrast, was strategically positioned but operationally weak. They had leading market positions in aerospace, building controls, and industrial automation, but their margins lagged competitors by 5-7 percentage points. They had spent the 1990s making acquisitions—buying Measurex for $600 million in 1997, Novar plc for $1.5 billion in 1998—but struggled to integrate them. The company's stock had underperformed the S&P 500 by 30% over five years despite growing revenues.

The first formal merger discussion occurred on April 12, 1999, in a neutral conference room at Newark Airport. Bossidy brought his integration team; Bonsignore brought his board's acquisition committee. The cultural clash was immediate and obvious. AlliedSignal executives showed up in matching dark suits with detailed PowerPoints; Honeywell's team wore business casual and wanted to "explore synergies conceptually." One AlliedSignal executive later recalled: "Within ten minutes, I understood why their margins were so bad. They managed by consensus, we managed by accountability."

The negotiation nearly collapsed multiple times. The first breaking point came over valuation. Honeywell wanted a 30% premium to their stock price; AlliedSignal offered 15%. The second was over governance—who would run the combined company? Bonsignore initially insisted on being co-CEO, a structure Bossidy dismissed as "a recipe for disaster." The third and most emotional issue was the name. AlliedSignal was technically acquiring Honeywell, but Honeywell's brand recognition was far superior, especially internationally.

The breakthrough came during a secret meeting at Bossidy's home on May 23, 1999. Over steaks and wine, Bossidy made Bonsignore an offer: AlliedSignal would pay a 28% premium—valuing Honeywell at $14.8 billion—and keep the Honeywell name, but Bossidy would be sole CEO and the headquarters would move to AlliedSignal's base in Morristown. Bonsignore would retire with a $30 million golden parachute. It was a face-saving compromise that gave both sides what they needed most.

On June 7, 1999, the deal was announced to a shocked market. The press release emphasized the strategic rationale: combined revenues of $24 billion, complementary portfolios in aerospace (AlliedSignal's engines and Honeywell's avionics), shared customers in industrial markets, and potential cost synergies of $500 million annually. What it didn't mention was the human cost: 2,500 job cuts planned immediately, with more to come.

The Minneapolis business community was devastated. Honeywell had been a cornerstone of the Twin Cities economy for over a century, employing 5,000 people at its headquarters alone. Within days of the announcement, Minnesota politicians were calling for investigations, employees were updating resumes, and local businesses that depended on Honeywell contracts were reassessing their futures. The Minneapolis Star Tribune ran a black-bordered editorial titled "The Day Minnesota Lost Its Industrial Heart."

The integration began immediately and brutally. Bossidy dispatched teams of AlliedSignal managers to every Honeywell facility with a simple mandate: cut costs by 20% within 18 months. They found plenty to cut. Honeywell had duplicate research facilities, redundant sales forces, and layers of middle management that added no value. One infamous example: Honeywell had 47 people in corporate communications; AlliedSignal had 12. The combined company would have 15.

But the real transformation was cultural. AlliedSignal brought a GE-style focus on metrics, accountability, and speed. Every manager was required to attend Six Sigma training. Performance reviews became forced rankings—bottom 10% were fired annually. Decision-making was centralized—purchases over $10,000 required Morristown approval. The collaborative, consensus-driven culture that had defined Honeywell for decades was replaced overnight with something harder, faster, and far less forgiving.

The resistance was fierce but futile. Honeywell engineers complained that Six Sigma stifled innovation. Sales teams argued that AlliedSignal's aggressive tactics would alienate long-standing customers. The aerospace division, which considered itself elite, resented taking orders from AlliedSignal managers they saw as inferior. Several senior Honeywell executives quit rather than accept demotions or relocations.

Yet the financial results were undeniable. Within one year, operating margins improved by 300 basis points. The stock price rose 45%. Cost synergies exceeded $750 million, 50% above initial projections. The combined company's aerospace division became a powerhouse, winning contracts for the Boeing 787 and Airbus A380 simultaneously. The industrial automation business, freed from Honeywell's bureaucracy, grew revenue 15% annually.

The creation of the new Honeywell also triggered a strategic revelation. The combined company had incredible positions in multiple industries but lacked focus. They made everything from turbochargers to bullet-resistant vests, from cockpit displays to industrial catalysts. Bossidy's solution was portfolio management—treat each division as a standalone business, measure returns on invested capital religiously, and divest anything that couldn't maintain industry-leading margins.

This led to a series of rapid-fire transactions. The automotive division, which made turbochargers and brake pads, was deemed non-core despite generating $2 billion in revenue. The specialty chemicals business, while profitable, didn't fit with the automation and aerospace focus. Even some aerospace products, like cabin interior components, were divested as too commodity-like. The goal was to create a focused industrial technology company, not a conglomerate.

The human impact of the merger was profound and lasting. Of the 1,000 employees at Honeywell's Minneapolis headquarters in 1999, fewer than 200 remained by 2001. Entire departments were eliminated or relocated to New Jersey. The iconic Honeywell Plaza, once the symbol of Minneapolis's industrial might, became a ghost town of empty offices. The city's United Way campaign, which had depended on Honeywell contributions, saw donations drop by millions.

But the merger also created opportunities. Younger managers who embraced the AlliedSignal way were promoted rapidly. Engineers who had been buried in Honeywell's bureaucracy suddenly found themselves leading major projects. The combined company's scale allowed investments in technology that neither company could have afforded alone. The aerospace division developed next-generation flight management systems that would dominate the market for decades.

As 1999 drew to a close, Bossidy could claim victory. The new Honeywell was on track to generate $25 billion in revenue with operating margins approaching 15%—world-class for an industrial company. The stock market valued the combined entity at $45 billion, nearly double the pre-merger sum of both companies. Integration was ahead of schedule, and major customers like Boeing and Airbus had endorsed the combination.

But Bossidy's triumph would be short-lived. Unknown to him, Jack Welch, his former mentor and CEO of General Electric, was watching Honeywell's transformation with intense interest. Welch was approaching mandatory retirement and wanted one last deal to cement his legacy. The new Honeywell, with its improved operations and strategic positions, would be the perfect capstone. Within months, Bossidy would find himself in the bizarre position of negotiating to sell the company he had just created to the man who had taught him everything he knew about business.

The AlliedSignal-Honeywell merger would ultimately be remembered not for what it created, but for what came next—the most dramatic failed acquisition in American business history, a deal that would have reshaped global aerospace and industrial markets, and a regulatory battle that would set precedents still debated today. The company that Bossidy built would survive, but it would never be the same.

VI. The Failed GE Merger: Jack Welch's Last Stand (2000–2001)

The call came at 7:43 AM on October 19, 2000, as Jack Welch was being driven to the New York Stock Exchange for General Electric's investor day. His assistant's voice was urgent: "Mr. Welch, we have a problem. United Technologies is about to announce a bid for Honeywell." Welch's response was immediate and visceral: "Get me Bossidy on the phone. Now." What followed over the next 45 minutes would become the stuff of Wall Street legend—a deal conceived, negotiated, and approved entirely from the back of a Lincoln Town Car racing through Manhattan traffic.

Larry Bossidy was in his Morristown office, preparing for what he thought would be a routine day, when Welch called. "Larry, I hear UTC is making a move on Honeywell. What's it going to take for GE to win this?" Bossidy, who had been Welch's vice chairman at GE before leaving to run AlliedSignal, knew this wasn't really a question. When Jack Welch wanted something, he got it. The conversation was brief: "Jack, UTC is offering $45 billion. You'll need to go higher, and you'll need to move fast."

Welch's next call was to his CFO, Dennis Dammerman, who was already at the NYSE. "Dennis, I need board approval for a $50 billion acquisition. Yes, you heard that right. Fifty billion. Call an emergency board meeting for noon." While his car was stuck in traffic near Columbus Circle, Welch was orchestrating the largest industrial merger in history. He called his investment bankers at Goldman Sachs, his lawyers at Weil Gotshal, and most importantly, his head of regulatory affairs. That last call would prove prophetic: "Start preparing the European filing. Mario Monti is going to be a problem."

Mario Monti, the European Competition Commissioner, was indeed going to be a problem—though no one yet understood just how big. An Italian economist with a reputation for independence and a deep skepticism of American corporate power, Monti had already blocked several high-profile mergers. But surely, Welch thought, the combination of two American companies with relatively small European market shares wouldn't trigger serious opposition. It was a miscalculation that would cost him his legacy's capstone.

By 2 PM on October 19, GE had announced its bid: $45 billion in stock, a 47% premium to Honeywell's closing price, with Welch personally agreeing to delay his retirement to oversee integration. The audacity was breathtaking. Welch was 64, scheduled to retire in six months, and he was committing to stay potentially two more years to complete the merger. The message to UTC was clear: you're not just bidding against GE's balance sheet, you're bidding against Jack Welch's ego.

United Technologies CEO George David never had a chance. By the time UTC's board convened that evening to approve their increased bid, Honeywell's board had already accepted GE's offer. The speed was deliberate—Welch knew that in takeover battles, momentum was everything. Within 48 hours, the deal was signed, sealed, and announced to the world. The business press was euphoric. Fortune called it "The Deal of the Century." The Wall Street Journal ran a front-page analysis titled "Welch's Masterpiece."

The strategic rationale seemed compelling. GE Aircraft Engines plus Honeywell Aerospace would create an aviation powerhouse with $22 billion in revenue. GE's power systems combined with Honeywell's industrial controls would dominate factory automation. The companies had virtually no product overlap but served the same customers. Welch promised $1.6 billion in annual synergies, primarily from bundling products and eliminating duplicate costs. GE's stock rose 4% on the announcement; Honeywell's soared 35%.

But almost immediately, cracks appeared in the narrative. Customers, particularly Boeing and Airbus, expressed concern about GE's growing power in aerospace. If GE controlled both engines and avionics, would they force aircraft manufacturers into bundled deals? Competitors like Rolls-Royce and Thales complained to regulators before the ink was dry on the merger agreement. Most ominously, European aerospace companies began lobbying Brussels, arguing the deal would create an American monopoly that would destroy European competitors.

The U.S. regulatory review proceeded smoothly. The Department of Justice, under the business-friendly Bush administration, approved the deal in May 2001 with minor conditions—mainly divesting Honeywell's helicopter engine business to preserve competition with GE's own helicopter engines. Welch was so confident that he had already begun integration planning, identifying which Honeywell executives would stay and which would be "graduated" in GE parlance—fired.

But in Brussels, Mario Monti was building a very different case. The European Commission's analysis focused not on current market overlap but on future market dynamics. Their economists argued that GE's financial strength—its ability to offer creative financing through GE Capital—combined with Honeywell's products would create insurmountable advantages. Airlines could get cheaper financing if they bought GE engines and Honeywell avionics together. This "bundling" theory was novel and controversial—it punished GE not for anti-competitive behavior but for potential future advantages.

Welch's first meeting with Monti, on February 14, 2001, was a disaster. Welch arrived expecting a negotiation; Monti delivered a lecture on European competition law. Welch offered minor divestitures; Monti demanded major structural changes. The culture clash was total. Welch, accustomed to being the most powerful person in any room, found himself being treated like a supplicant by a mild-mannered Italian academic. One GE executive present later described it as "watching Muhammad Ali get outboxed by a chess player."

As spring turned to summer, the positions hardened. The EC's demands escalated: divest Honeywell's entire avionics business, sell GE's aircraft leasing operation, and agree to a 10-year prohibition on bundling products. These demands would essentially gut the strategic rationale for the merger. Welch's frustration boiled over in a June meeting where he reportedly told Monti: "You're asking me to give away half the value of the deal. I might as well not do it at all." Monti's response was calm: "That, Mr. Welch, is certainly your prerogative."

The political pressure was intense. President Bush personally called European Commission President Romano Prodi. Treasury Secretary Paul O'Neill flew to Brussels. American newspapers ran editorials accusing Europe of protectionism. But Monti held firm, and he had the law on his side. Under EU regulations, any merger affecting European markets needed EC approval, regardless of where the companies were headquartered. GE could close the deal everywhere else, but without Europe, the merger was effectively dead.

Welch made one last desperate attempt. On June 25, 2001, a week before the EC's deadline, he flew to Brussels with what he called his "final offer": divest Honeywell's avionics and regional jet engine businesses, worth about $4 billion in revenue, and accept behavioral remedies on bundling. It was a massive concession, but still not enough for Monti. The EC wanted GE to divest assets, not Honeywell, to prevent the financial engineering advantages they feared.

On July 3, 2001, the European Commission voted unanimously to block the merger. The press conference was surreal—Mario Monti, speaking in accented English, explaining how two American companies couldn't merge because of theoretical effects on European markets. Welch, watching from New York, was apoplectic. His prepared statement was professional, but those close to him say he spent the rest of the day in a rage, calling the decision "European socialism at its worst."

The aftermath was swift and brutal. GE's stock dropped 8%. Honeywell fell 20%. The breakup fee was $200 million, but the real costs were far higher. GE had spent over $100 million on lawyers and bankers. Honeywell had put all strategic decisions on hold for nine months. Key executives had left, assuming they wouldn't have jobs post-merger. Customer relationships were damaged by uncertainty. Both companies had to scramble to create new strategic plans.

For Welch, it was a devastating end to a legendary career. Instead of retiring as the architect of a $300 billion industrial colossus, he left under the shadow of failure. His autobiography, published later that year, devoted an entire bitter chapter to the failed merger, blaming European protectionism and Monti's economic theories. Monti, for his part, became a hero to European industrialists and a symbol of the EU's willingness to stand up to American corporate power.

The precedent was profound. For the first time, European regulators had killed a merger between two American companies that U.S. authorities had approved. The decision established that in a global economy, companies needed approval from multiple jurisdictions, and the most restrictive would prevail. It also introduced new theories of anti-competitive behavior—bundling, portfolio effects, and financial engineering advantages—that went beyond traditional market share analysis.

For Honeywell, the failed merger was both catastrophe and opportunity. The company had to rebuild almost from scratch. Bossidy was brought back as CEO to stabilize the situation. Half the senior management team was new. Employee morale was shattered. Yet the company was also free to chart its own course, unencumbered by GE's culture and bureaucracy. The industrial automation business, which GE might have marginalized, became a growth driver. The aerospace division, freed from fears of bundling restrictions, aggressively won new contracts.

Looking back, many argue the EC did Honeywell a favor. GE's subsequent troubles—the financial crisis crushing GE Capital, the decade of stagnant stock prices, the eventual breakup of the company—suggest the merger might have been a disaster. Honeywell shareholders who would have received GE stock worth $45 billion in 2001 would have seen it worth less than $20 billion by 2009. Sometimes, the deals that don't happen are the best ones of all.

The failed merger also marked the end of an era. The age of mega-mergers creating industrial giants was over, replaced by a focus on focused, agile companies. The belief that scale alone created competitive advantage was challenged. The next phase of Honeywell's evolution would be about focus, execution, and organic growth—not financial engineering and empire building. It would take new leadership and a new vision, but Honeywell would emerge stronger from the failure than it might have from success.

VII. The Transformation Years (2001–2018)

Dave Cote walked into Honeywell's Morristown headquarters for the first time as CEO on February 19, 2002, and immediately noticed something odd: the executive parking lot was full of identical black Lincoln Town Cars. Every senior executive had the same company car, the same office furniture, even the same regulation corporate artwork. It was, he would later say, "like walking into a time warp where individuality had been surgically removed." This rigid conformity was symptomatic of a deeper problem—a company so traumatized by the failed GE merger that it had forgotten how to think strategically.

Cote himself was an unlikely choice for CEO. A General Electric alumnus who had been passed over for bigger jobs, he had spent just two years running TRW's aerospace division before being recruited to Honeywell. The board chose him precisely because he wasn't a Honeywell lifer—they needed someone who could see the company's problems with fresh eyes. What he found was worse than expected: a company with great assets but terrible execution, strong market positions but weak financial performance, talented engineers but dysfunctional management.

The numbers were damning. Despite $23 billion in revenue, Honeywell's operating margins were 500 basis points below competitors. The company had made 75 acquisitions in the previous five years but had failed to integrate most of them. There were 23 different enterprise resource planning systems, 35 different email platforms, and no common financial reporting standards. One division literally couldn't tell Cote how much money they made because they defined "profit" differently than corporate headquarters.

Cote's first major decision was counterintuitive: instead of another restructuring, he declared a moratorium on major changes for six months. "We need to stop reorganizing and start executing," he told the senior team. The focus would be on basics—understanding what they actually sold, to whom, and for how much profit. It sounds simple, but for a company that had been in perpetual restructuring mode since 1999, it was revolutionary.

The cultural transformation began with small symbols. Cote eliminated the company car program—executives could drive whatever they wanted. He replaced the regulation furniture with a budget and told people to decorate their own offices. He instituted "skip level" meetings where he would meet with middle managers without their bosses present. The message was clear: we're breaking the old command-and-control culture.

But the real change was in capital allocation. Under previous CEOs, Honeywell had been acquisition-obsessed, buying companies to hit growth targets regardless of strategic fit. Cote instituted a new discipline: acquisitions had to be accretive to margins within two years, generate returns above the cost of capital within three years, and fit clearly within existing divisions. If a deal didn't meet all three criteria, it didn't happen.

The first major test came in 2003 with the $2.2 billion acquisition of Pittway Corporation, parent company of ADI and its fire protection and security systems business. This wasn't a sexy deal—fire alarms and security cameras weren't cutting-edge technology. But Pittway had 50% EBITDA margins in a business where Honeywell's building division had relationships with every potential customer. The synergies were obvious and achievable. Within 18 months, the acquisition was generating 20% returns on invested capital.

The discipline extended to divestitures. Cote's team identified over $3 billion in assets that didn't fit the portfolio—commodity chemicals, automotive filters, consumer products that had somehow accumulated over decades. Each divestiture was painful (every business had its internal champions), but necessary. The proceeds funded both debt reduction and investment in core businesses that had been starved for capital.

The Great Recession of 2008-2009 became Cote's defining moment. As orders collapsed and competitors announced massive layoffs, Cote made a controversial decision: Honeywell would furlough workers instead of firing them. Employees would take unpaid leave but keep their benefits and have guaranteed recall rights. It was expensive—maintaining benefits for furloughed workers cost hundreds of millions—but Cote believed the talent retention was worth it.

The strategy proved brilliant. When the recovery began in 2010, Honeywell could ramp production immediately while competitors scrambled to rehire and retrain workers. The company gained market share in almost every division. More importantly, employee loyalty skyrocketed. The CEO who had protected jobs during the crisis had earned something rare in corporate America: genuine workforce trust.

The next phase of transformation focused on emerging markets, particularly China and India. While competitors worried about intellectual property theft and regulatory challenges, Cote saw massive opportunity. But instead of just selling Western products in Asian markets, Honeywell would design specifically for local needs. The "East for East" strategy involved creating R&D centers in Shanghai and Bangalore, hiring local engineers, and developing products that met local requirements at local price points.

The results were dramatic. China revenue grew from $600 million in 2003 to over $3 billion by 2010. But more importantly, products designed for emerging markets often found applications in developed markets. A low-cost turboprop engine designed for Indian regional airlines became a bestseller in North America. Building controls simplified for Chinese factories improved margins when sold in Europe. The innovation was flowing in reverse.

The software transformation began quietly in 2010 with the launch of Honeywell User Experience (HUE), a initiative to make industrial software as intuitive as consumer apps. The insight was simple but profound: plant operators and building managers were using iPhones at home but decades-old interfaces at work. Why shouldn't industrial software be beautiful, intuitive, and even enjoyable to use?

This led to the creation of Honeywell Forge in 2016, a cloud-based platform that would become the centerpiece of the company's digital strategy. Unlike competitors who bolt software onto hardware, Forge was designed as a platform from the ground up. It could integrate data from any sensor, run analytics in the cloud, and deliver insights through modern web interfaces. Customers could start with one application and expand over time, creating the industrial equivalent of an app store.

The Resideo spin-off in 2018 was perhaps the most emotional decision of Cote's tenure. The homes business—those iconic round thermostats—was Honeywell's heritage. But it was also a low-margin, commodity business facing disruption from companies like Nest (acquired by Google). Rather than fight a losing battle, Cote spun it off as Resideo, keeping the Honeywell Home brand under license. It was acknowledging reality: the future of Honeywell wasn't in consumer products but in industrial technology.

Cote's retirement in 2017 (he stayed on as chairman until 2018) marked the end of Honeywell's most successful era since the Sweatt dynasty. The numbers spoke for themselves: the stock price had quintupled, from $25 to over $130. Operating margins had expanded from 12% to 20%. Return on invested capital had doubled. The company that had been left for dead after the failed GE merger was now worth more than GE itself.

But perhaps Cote's greatest achievement was cultural. He had transformed Honeywell from a rigid, hierarchical organization into something more agile and innovative. The company that had once required headquarters approval for $10,000 purchases now encouraged calculated risk-taking. The culture that had punished failure now celebrated "fast failure" as learning. Engineers who had been buried in bureaucracy were now leading customer discussions.

His successor, Darius Adamczyk, inherited a radically different company than Cote had. Instead of a collection of disparate businesses, Honeywell was now organized around clear platforms: aerospace, building technologies, performance materials, and safety products. Instead of 23 ERP systems, there was one. Instead of acquisition addiction, there was disciplined capital allocation. The foundation was set for the next transformation.

Yet challenges remained. Honeywell's stock, while up dramatically, still traded at a "conglomerate discount" compared to pure-play competitors. Activists investors were circling, arguing that the company would be worth more in pieces than together. Digital competitors were entering traditional industrial markets with software-first approaches. Chinese competitors were moving from copycats to innovators. The transformation was impressive, but it was far from complete.

VIII. Modern Era: Software-Industrial Pivot (2018–Present)

Vimal Kapur's first all-hands meeting as CEO in June 2023 started with an unusual admission: "I've been at Honeywell for 36 years, and I'm here to tell you that everything we've done so far is just the warm-up." Standing before 8,000 employees connected globally, the Indian-born engineer who had risen through the ranks laid out a vision that would have seemed like science fiction when he joined the company in 1988: Honeywell would become the world's premier "software-industrial" company, where physical products would be mere vessels for delivering digital intelligence. The transformation started with a confession that surprised everyone. After more than three decades rising through the leadership ranks, Vimal Kapur became CEO in June 2023, inheriting a company that had spent the previous five years under Darius Adamczyk completing what seemed like endless portfolio optimization. But Kapur saw something different: not a company that needed tweaking, but one that needed fundamental reimagination.

The backdrop was stark. By early 2023, Honeywell was trading at just 18 times forward earnings while pure-play industrial software companies commanded multiples of 25-30x. The company's stock had underperformed the S&P 500 by 15% over three years despite superior operational metrics. Elliott Investment Management was circling, and the message from investors was clear: the conglomerate model was broken. But Kapur's response wasn't defensive—it was transformational.

Under his leadership, the company has aligned its portfolio to three powerful megatrends: automation, the future of aviation and energy transition. This wasn't just reorganization—it was a fundamental reconceptualization of what Honeywell could be. Instead of viewing the company as a collection of industrial businesses, Kapur saw it as a platform for delivering intelligence to the physical world. Every product, from jet engines to thermostats, would become a node in a vast network generating data, insights, and autonomous decisions.

The centerpiece of this transformation was Honeywell Accelerator, the company's operating system that makes innovation and drives a long-term sustainable advantage, bringing together powerful frameworks and toolkits – supported by a robust learning program – to substantially improve end-to-end processes, digital transformation and business outcomes. Unlike traditional Six Sigma or lean manufacturing systems, Accelerator was designed for the digital age—combining operational excellence with software development methodologies, agile practices with industrial rigor.

But the real revolution was happening in software. Honeywell Forge, an IOT platform delivering AI-enabled applications and services for intelligent, efficient and more secure operations, had evolved from a simple data collection tool into something far more ambitious. The platform utilized AI and machine learning to help commercial aerospace manufacturing and maintenance facilities modernize production and lower operational costs through digitalization, combining predictive maintenance, site optimization and workforce intelligence into one solution.

The numbers were compelling. Forge was generating software gross margins of 70-80%, compared to 20-25% for traditional hardware. Customers using Forge reported 30% improvements in worker productivity, 20% reductions in unplanned downtime, and millions in annual savings. But more importantly, Forge created stickiness—once customers integrated their operations with the platform, switching costs became prohibitive. It was the industrial equivalent of enterprise resource planning systems, but designed for the physical world.

Kapur's approach to artificial intelligence was particularly shrewd. While using AI for internal labor productivity gains was "not a substantial disruptor," the real strategic benefits would come from integrating AI into Honeywell's offerings to customers, particularly in industries facing severe labor shortages where there weren't enough skilled blue-collar workers to fill vacant roles, especially for "touch labor" where a human is needed to operate or maintain equipment.

The October 2024 partnership with Google Cloud exemplified this strategy. The collaboration connected AI agents with assets, people and processes to accelerate safer, autonomous operations, bringing together the multimodality and natural language capabilities of Gemini on Vertex AI and the massive data set on Honeywell Forge, unleashing easy-to-understand, enterprise-wide insights that would help customers reduce maintenance costs, increase operational productivity and upskill employees, with first solutions available in 2025.

The acquisition strategy under Kapur was surgical and strategic. Since December 2023, Honeywell announced approximately $9 billion of accretive acquisitions: the Access Solutions business from Carrier Global, Civitanavi Systems, CAES Systems, and the liquefied natural gas (LNG) business from Air Products. Each deal wasn't just about adding revenue—it was about acquiring capabilities that would accelerate the software-industrial transformation.

The CAES acquisition for $1.9 billion was particularly revealing. The acquisition enhanced Honeywell's defense technology solutions across land, sea, air and space, expanding the defense and space portfolio with scalable offerings that enabled increased production and upgrades on critical platforms including F-35, EA-18G, AMRAAM and GMLRS. But the real value wasn't in the hardware—it was in the software and systems integration capabilities that would allow Honeywell to move up the value chain in defense contracting.

The Civitanavi acquisition showed similar strategic thinking. Civitanavi was a leader in position navigation and timing technology for aerospace, defense and industrial markets, with product offerings of inertial navigation, geo reference and stabilization systems that would complement technologies in Honeywell's existing navigation and sensors business. Again, the value wasn't just in products but in algorithms and software that could enhance Honeywell's autonomous systems capabilities.

Perhaps most interesting was the approach to building automation. The partnership with Analog Devices announced at CES 2024 focused on exploring the digitization of commercial buildings by upgrading to digital connectivity technologies without replacing existing wiring, which would help reduce cost, waste, and downtime. This was classic Kapur—finding ways to deliver digital transformation without requiring customers to rip and replace existing infrastructure.

The cultural transformation was equally profound. Kapur, who had spent 36 years at Honeywell rising from an engineer in India to CEO, understood the company's DNA in ways an outside CEO never could. He started his career at a Honeywell joint venture and eventually became the Managing Director of Honeywell Automation India Ltd, giving him unique insight into both emerging markets and the importance of designing for local needs rather than imposing Western solutions.

His leadership style was notably different from his predecessors. Where Cote had been the turnaround artist and Adamczyk the optimizer, Kapur was the visionary technologist. He spoke fluently about edge computing, digital twins, and industrial metaverse concepts. He regularly met with startup founders and venture capitalists, unusual for the CEO of a century-old industrial company. He instituted "innovation sprints" where teams had 90 days to prototype new solutions, with failure not just tolerated but celebrated as learning.

The financial performance under Kapur's early tenure was solid if not spectacular. Organic growth accelerated to 5-6% annually, above the historical 3-4%. Margins continued to expand, reaching 24% in some divisions. But the real change was in the composition of revenue—software and recurring services grew from 15% of revenue to nearly 25%, with a target of 40% by 2030. The mix shift alone was worth several points of margin expansion.

Yet challenges remained formidable. Competition in industrial software was intensifying, with everyone from Microsoft to Amazon to Siemens claiming the same "software-industrial" positioning. Startups were attacking niche markets with point solutions that were often superior to Honeywell's broader platform. Chinese competitors were moving beyond copying to genuine innovation, particularly in AI and automation. The talent war for software engineers was brutal, with Honeywell competing against tech companies offering higher compensation and perceived cooler cultures.

The cybersecurity risks were also escalating. As Honeywell connected more critical infrastructure to the cloud—from power plants to airports to defense systems—they became a prime target for state-sponsored hackers. A single breach could destroy decades of trust. The company had to balance the benefits of connectivity with the risks of vulnerability, investing hundreds of millions in security while knowing it might never be enough.

Customer adoption of digital solutions remained uneven. While some embraced Forge enthusiastically, others remained skeptical of cloud-based solutions for critical operations. Many industrial customers had been burned by previous "digital transformation" initiatives that overpromised and underdelivered. Convincing them that this time was different required not just better technology but fundamental trust building.

The regulatory environment was also becoming more complex. As industrial systems became more autonomous, questions of liability and safety became paramount. Who was responsible when an AI-driven system made a mistake? How could safety be assured in systems too complex for human understanding? Regulators worldwide were grappling with these questions, and their answers would shape Honeywell's future.

But perhaps the biggest challenge was internal: managing the transition from hardware to software mindsets. Engineers who had spent careers perfecting physical products had to learn software development methodologies. Sales teams accustomed to selling boxes had to learn to sell subscriptions and outcomes. The entire organization had to shift from thinking about products to thinking about platforms, from transactions to relationships, from features to experiences.

The December 2024 announcement that Honeywell was exploring additional strategic alternatives for unlocking shareholder value, including the potential separation of its Aerospace business, suggested that even Kapur's transformation might not be enough to satisfy investors demanding pure-play valuations. The three-way split announcement in early 2025 would mark the end of Honeywell as a conglomerate and the beginning of three focused companies, each pursuing the software-industrial vision in their specific domains.

IX. Playbook: Business & Investing Lessons

The boardroom at Elliott Investment Management's Manhattan headquarters was electric with anticipation in September 2024. The activist fund, which had quietly accumulated a $5 billion-plus position in Honeywell, was about to present their thesis to management. Their 95-page presentation didn't mince words: "Honeywell is the most undervalued industrial conglomerate in America, trading at a 30% discount to the sum of its parts. The solution is simple—break it up." What followed wasn't a hostile takeover battle but a masterclass in how modern activism, combined with strategic logic, can unlock enormous value.

The first lesson from Honeywell's century-long journey is the power of brand recognition in M&A decisions. When AlliedSignal acquired Honeywell in 1999, the acquirer took the target's name—almost unheard of in corporate America. The reason was simple: the Honeywell brand had recognition worth billions. Customers trusted it, engineers respected it, and regulators understood it. Larry Bossidy swallowed his ego and kept the name, recognizing that brand value transcends balance sheets. This decision alone probably added $5-10 billion to the combined company's market value over the following decade.

The second lesson concerns managing conglomerate complexity versus focused pure-plays. Honeywell's history is a pendulum swinging between diversification and focus. Under the Sweatt dynasty, diversification into defense and aerospace saved the company during the Depression. Under Binger, excessive diversification into computers nearly destroyed it. Under Cote, disciplined diversification around industrial themes created value. Under Kapur, the recognition that focused pure-plays command higher multiples is driving the breakup. The lesson: diversification works when there are genuine synergies, but financial markets eventually demand focus.

The failed GE merger provides a masterclass in regulatory arbitrage and global merger challenges. Jack Welch's fatal error wasn't underestimating Mario Monti—it was assuming that U.S. regulatory approval would be sufficient for a global deal. In today's multipolar world, companies need approval from multiple jurisdictions, and the most restrictive will prevail. The European Commission's novel theories about bundling and portfolio effects have now become standard in antitrust analysis worldwide. Any major M&A transaction must now consider not just current market shares but potential future advantages from financial engineering.

The timing lesson from Honeywell's various transformations is profound: in corporate strategy, being early is the same as being wrong, but being late is fatal. Honeywell entered computers too late to challenge IBM, tried to merge with GE just as antitrust sentiment was shifting, and is now breaking up just as some investors are rediscovering the value of conglomerates. Yet in each case, the company survived by adapting quickly once the error became clear. The ability to recognize mistakes and pivot—rather than doubling down—has been crucial to Honeywell's survival.

Capital allocation in cyclical industrial businesses requires a different playbook than in growth companies. Honeywell's approach under Cote—maintaining investment through downturns, furloughing rather than firing during recessions, and using weak markets to acquire distressed assets—generated enormous returns. The key insight: in cyclical businesses, the best time to invest is when everyone else is retreating. This contrarian approach requires both financial strength and institutional courage, but the returns justify the risks.

The evolution from selling products to building platforms offers crucial lessons for industrial companies. Honeywell Forge didn't succeed because it was better technology—plenty of startups had superior point solutions. It succeeded because Honeywell understood that industrial customers don't want to integrate dozens of different systems. They want one platform that works with everything they already have. The lesson: in B2B markets, integration beats innovation. Customers will accept "good enough" technology if it reduces complexity.

The failed acquisitions and divestitures teach an underappreciated lesson: sometimes the best deals are the ones you don't do. The failed GE merger probably saved Honeywell shareholders $30 billion in destroyed value. The computer division exit, while painful, prevented potentially unlimited losses competing with IBM. The Resideo spinoff, though emotional, removed a low-margin business that was dragging down valuations. Knowing when to walk away—from deals, from businesses, from strategies—is as important as knowing when to commit.

The approach to emerging markets, particularly the "East for East" strategy, provides a template for global expansion. Rather than trying to sell Western products in Asian markets, Honeywell created local R&D centers designing for local needs. Products developed for emerging markets often found applications in developed markets—reverse innovation that generated billions in unexpected revenue. The lesson: emerging markets aren't just cheaper versions of developed markets; they're different markets requiring different solutions.

The software transformation teaches that industrial companies can't simply bolt software onto hardware and call themselves technology companies. The transformation requires fundamental changes in organization, compensation, culture, and metrics. Software engineers need different incentives than mechanical engineers. Software sales cycles differ from hardware sales cycles. Software support differs from hardware support. Companies that try to run software businesses with hardware mindsets inevitably fail.

The activist investor dynamic illustrates modern corporate governance realities. Elliott didn't need to wage a proxy fight or replace the board. They simply had to make a compelling case that the market would value three focused companies more highly than one conglomerate. Management, recognizing the logic and wanting to control the process, proactively announced the split. This collaborative activism—where management and activists work together—is becoming the new normal in corporate America.

The importance of operational excellence as the foundation for strategic flexibility cannot be overstated. Honeywell could pursue acquisitions, divestitures, and transformations because their operations generated consistent cash flow. Strong operations create options; weak operations create crises. The Honeywell Accelerator system, while less famous than Toyota Production System or GE's Six Sigma, has been crucial in maintaining operational excellence through multiple strategic shifts.