Hologic: The Science of Sure in Women's Health

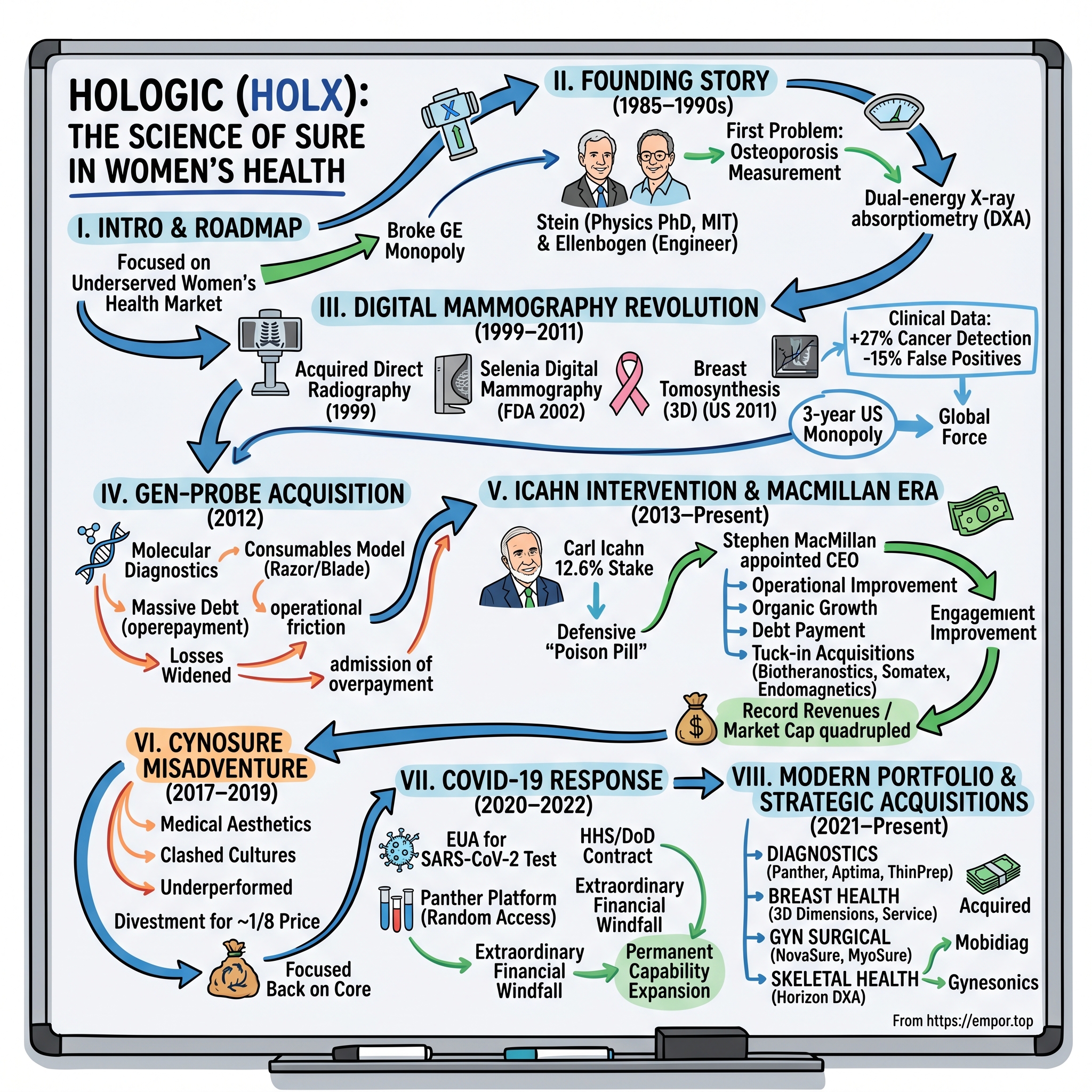

I. Introduction & Episode Roadmap

Picture this: A small Massachusetts startup in 1985, twelve employees huddled around X-ray equipment, trying to solve a problem that most of the medical establishment ignored—how to accurately measure bone density in aging women. Fast forward to today, and that same company commands a $20 billion market capitalization, holds the number one position in breast cancer screening globally, and processes millions of molecular diagnostic tests annually. This is the story of Hologic—a company that built an empire by focusing relentlessly on a market that Big Med Tech consistently underserved: women's health.

The journey from bone densitometry pioneer to women's health powerhouse wasn't linear. It's a tale of technical breakthroughs that changed cancer detection forever, of billion-dollar acquisitions that nearly sank the company, of activist investors storming the boardroom, and of a COVID-19 response that generated windfall profits which management actually deployed wisely—a rarity in corporate America.

What makes Hologic particularly fascinating for students of business strategy is how it turned a perceived limitation—focusing "only" on women's health—into its greatest competitive advantage. While giants like GE Healthcare and Siemens Healthineers spread themselves across every medical specialty, Hologic went deep. They didn't just make mammography machines; they revolutionized how breast cancer is detected. They didn't just enter diagnostics; they built the most automated molecular testing platform in the industry.

This deep dive will explore how a physics PhD and an engineering graduate built a company around "doing good," how they broke GE's monopoly in digital mammography, why Carl Icahn's intervention might have saved the company, and what the Cynosure disaster teaches us about the perils of adjacency moves. We'll examine the operational playbook that quadrupled the stock price, dissect the company's four business segments, and evaluate whether Hologic's focused strategy can continue delivering alpha in an increasingly consolidated med tech landscape.

II. Founding Story & Early Vision (1985–1990s)

The conference room at 350 Campus Drive in Somerset, New Jersey, wasn't much to look at in September 1985. Jay Stein, fresh from completing his physics PhD at MIT, sat across from S. David Ellenbogen, a Newark College of Engineering graduate with a knack for medical device engineering. Between them lay blueprints for an X-ray densitometer—a machine that could peer through skin and muscle to measure the density of bones. It wasn't sexy technology. It wasn't going to make headlines. But Stein saw something others missed: millions of women suffering from osteoporosis had no reliable way to know their bones were weakening until they fractured. "Hologic started with an act of doing good … and it has continued by doing good for so many employees and so many customers and patients around the world," Stein would later reflect. "And I truly hope that the act of doing good for people, which was the core foundation of the company, continues into the far future."

The founding philosophy wasn't just feel-good rhetoric. Stein co-founded Hologic with a dozen employees, bringing together his Ph.D. in Physics from MIT and Ellenbogen's engineering expertise to tackle a massive unmet medical need. At the time, osteoporosis affected millions of postmenopausal women, yet diagnosis typically came only after a fracture occurred—by which point significant bone loss had already happened.

The technical challenge was formidable. Traditional X-ray technology couldn't provide the precision needed to detect subtle changes in bone density. Stein became the principal author of numerous patents involving X-ray technology, developing dual-energy X-ray absorptiometry (DXA) systems that could measure bone mineral density with unprecedented accuracy. These weren't just incremental improvements—they represented a fundamental leap in diagnostic capability.

By the late 1980s, Hologic's bone densitometers were gaining traction in hospitals and clinics. The market opportunity was enormous: the aging Baby Boomer generation meant millions of women would soon enter the high-risk years for osteoporosis. But what set Hologic apart wasn't just the technology—it was the company's singular focus on understanding and serving the specific needs of women's healthcare providers.

The company evolved from "a small bone density scanning company to being one of the largest women's healthcare companies in the United States", but that transformation would take decades and multiple strategic pivots. In those early years, Hologic established two principles that would guide every major decision: technical excellence and an unwavering commitment to women's health.

The bone density business provided steady cash flow and established Hologic's reputation for reliability in the medical device world. During Stein's tenure, he grew the company from a small startup to a major player in medical technology with close to $0.5B in revenue. But the real breakthrough—the one that would transform Hologic from a niche player into a global force—was still a decade away.

As the 1990s dawned, Stein and his team began looking beyond bone density. They saw an opportunity in another area where women's health was underserved: breast cancer screening. The mammography market was dominated by film-based systems that hadn't fundamentally changed in decades. What if, they wondered, they could apply digital imaging technology to mammography the way they had revolutionized bone density measurement?

III. Digital Mammography Revolution (1999–2011)

The acquisition seemed modest at the time. In 1999, when Hologic purchased Direct Radiography Corp. from Sterling Diagnostic Imaging, industry observers saw it as a logical bolt-on—a bone density company adding some digital X-ray capabilities. What they missed was that Hologic had just acquired the foundation for a revolution in breast cancer detection.

Direct Radiography brought more than just assets; it brought a team that had been pioneering flat-panel digital detectors. Through this acquisition, Hologic added DirectRay flat-panel digital X-ray, EPEX, and Radex general radiography systems to its product line. But the real prize was the expertise in digital imaging that would soon be applied to mammography.

The mammography market in 2000 was a study in technological stagnation. Film-based mammography had been the standard for decades, with GE Healthcare holding a near-monopolistic position. Radiologists would hold film sheets up to light boxes, squinting to detect tiny calcifications or masses. The process was slow, subjective, and limited by the inherent constraints of film. Storage rooms overflowed with film archives. Second opinions required physically shipping films between facilities.

Hologic's engineers saw digital mammography not as an incremental improvement but as a fundamental reimagining of breast cancer screening. In 2002, after years of development and clinical trials, the FDA approved Hologic's Selenia digital mammography system. This wasn't just digitizing the old process—it was transforming it. Digital detectors could capture a wider range of tissue densities in a single exposure. Images could be manipulated, zoomed, and enhanced. Computer-aided detection could flag potential areas of concern.

But breaking into a market dominated by GE was like attacking a fortress. GE had relationships with virtually every major hospital system. Their sales force outnumbered Hologic's entire employee base. The conventional wisdom was that Hologic would capture a small niche and GE would continue its dominance.

What happened next became a case study in focused execution beating diversified incumbency. While GE treated mammography as one product line among hundreds, for Hologic it was existential. Every engineer, every salesperson, every executive was laser-focused on mammography. They didn't just sell machines; they partnered with radiologists, understood workflow challenges, and continuously refined their technology based on clinical feedback.

The real game-changer came in 2008 when Hologic introduced breast tomosynthesis in many countries recognizing the CE mark. In 2011 Hologic got FDA approval and introduced tomosynthesis in the US. Hologic was the only provider of tomosynthesis systems allowed to sell in the US for the next three years.

Tomosynthesis—or 3D mammography—was to traditional mammography what a CT scan is to a standard X-ray. Instead of capturing a single flat image, the system took multiple images from different angles and reconstructed them into a three-dimensional view of the breast. Radiologists could now scroll through tissue layers, dramatically reducing the problem of overlapping structures that could hide cancers or create false positives.

The clinical data was stunning. Studies showed that 3D mammography increased cancer detection rates by 27% while simultaneously reducing false-positive callbacks by 15%. For the millions of women who had experienced the anxiety of a callback for additional imaging, this was transformative. For healthcare systems dealing with the costs and inefficiencies of false positives, it was economically compelling.

The three-year monopoly on 3D mammography in the U.S. market from 2011 to 2014 allowed Hologic to establish itself as the undisputed leader in breast imaging. By the time competitors received FDA approval for their own tomosynthesis systems, Hologic had already installed thousands of units and built deep relationships with radiologists who had experienced the clinical benefits firsthand.

The education campaign around 3D mammography revealed Hologic's sophistication in market development. Rather than just selling to hospitals, they launched consumer awareness campaigns. They worked with advocacy groups. They published clinical studies. They turned "3D mammography" into a term that patients began requesting by name. This pull-through demand from patients created pressure on imaging centers to upgrade their technology.

By 2011, Hologic had not only broken GE's monopoly—they had redefined the entire mammography market. The company that had started with bone density measurement was now the global leader in breast cancer screening. But this success brought its own challenges. With a market cap approaching $5 billion and ambitions for further growth, Hologic's board began looking for the next big leap. They found it in molecular diagnostics, setting the stage for the company's most ambitious—and problematic—acquisition yet.

IV. The Gen-Probe Acquisition: Building a Diagnostics Powerhouse (2012)

The boardroom at Hologic's Marlborough headquarters was tense in April 2012. The company was about to make the biggest bet in its history: $3.8 billion for Gen-Probe, a San Diego-based molecular diagnostics company. To put this in perspective, Hologic's entire market cap was roughly $5 billion. They were essentially betting the company. The strategic rationale was compelling on paper. Gen-Probe brought automated molecular diagnostic platforms—the Tigris and Panther systems—that could run high-volume tests for sexually transmitted infections, blood screening, and other applications. For Hologic, this meant moving beyond capital equipment sales into the recurring revenue model of diagnostic consumables. It was the classic "razor and blade" strategy that Wall Street loved.

Rob Cascella, Hologic's CEO at the time, painted a vision of synergy: "This transaction combines best-in-class technology with strong market presence and global distribution to target the rapidly growing molecular diagnostics market". The combined company would derive 50% of revenue from diagnostics, transforming Hologic from primarily an imaging company into a balanced diagnostics and imaging powerhouse.

But the financing structure would haunt Hologic for years. To fund the $3.8 billion purchase price, the company took on massive debt, leveraging itself to dangerous levels. The integration proved more challenging than anticipated. Gen-Probe had its own culture, its own systems, its own way of doing business. Merging a San Diego molecular diagnostics company with a Massachusetts imaging company created operational friction that the optimistic synergy projections hadn't fully accounted for. The financial results told the story: Losses widened by 1332.4% in Q4 and by 1492.8% in 2013. Hologic posted losses of $1.11 billion, or $4.11 per share, on sales of $622.1 million during the 3 months ended September 28. That compared with losses of $77.8 million, or 29¢ per share, on sales of $588.6 million during the same period last year. For the full year, Hologic posted losses of $1.17 billion, or $4.36 per share, on sales of $2.51 billion. That compared with losses of $73.6 million, or 28¢ per share, on sales of $2.01 billion in 2012. The billion-dollar loss was driven by a massive goodwill impairment charge on the diagnostics business—essentially an admission that they had overpaid for Gen-Probe.

The company was drowning in debt, struggling with integration, and facing increasingly restless shareholders. The stock price, which had been above $20 when the Gen-Probe deal was announced, sank toward $15. Something had to change, and change came in the form of one of Wall Street's most feared corporate raiders.

V. The Icahn Intervention & MacMillan Era (2013–Present)

The letter arrived at Hologic's headquarters on a cold November morning in 2013. Carl Icahn, the octogenarian activist investor who had built a fortune on corporate raids and hostile takeovers, had acquired a 12.6% stake in the company. His message was blunt: management had destroyed shareholder value with the Gen-Probe acquisition, the board was asleep at the wheel, and dramatic change was needed immediately.

In Nov 2013, Carl Icahn, the activist investor, acquired a 12.6% stake in Hologic, demanding board representation, management changes, and a new CEO. Shortly after Hologic initiated a "poison pill", to avoid a potential hostile takeover. However, by Dec 2013, Hologic agreed to add two Icahn representatives to its board and brought in MacMillan, the former CEO of Stryker, as its new CEO.

The poison pill—technically a shareholder rights plan—was Hologic's initial defensive move, designed to prevent Icahn from accumulating more shares and launching a full takeover. But Icahn had leverage, and he knew it. The stock was trading at multi-year lows, the debt burden from Gen-Probe was crushing, and institutional investors were losing patience.

Within weeks, a settlement was reached. Two Icahn nominees would join the board, and more importantly, Hologic would bring in new leadership. The choice was inspired: Stephen MacMillan, the former CEO of Stryker who had transformed that company into one of the most efficient operators in med tech.

MacMillan walked into Hologic in December 2013 with a reputation as a turnaround artist. At Stryker, he had driven operating margins from the mid-teens to the mid-20s through relentless focus on operational excellence. His philosophy was simple but powerful: fix the basics before chasing growth, eliminate complexity, and focus on what you do best.

Stephen MacMillan was appointed CEO in Dec 2013. He embarked on a strategy of organic growth and global expansion, particularly through the development and commercialization of diagnostic products. He also put a lot of focus on profitability and debt payment.

The transformation began immediately. MacMillan instituted what he called "The Hologic Way"—a comprehensive operational improvement program that touched every aspect of the business. Manufacturing processes were streamlined. The product portfolio was rationalized, with underperforming products discontinued. The sales force was restructured to focus on the highest-value opportunities.

But perhaps most importantly, MacMillan changed the narrative around the Gen-Probe acquisition. Rather than viewing it as a disaster to be unwound, he saw it as a diamond in the rough that needed polishing. The Panther platform, Gen-Probe's flagship molecular diagnostics system, was technically superior to competing platforms. It just needed better commercial execution.

The results were dramatic. MacMillan drove the company to record revenues. During his tenure, Hologic's revenue surpassed $4B and its market cap quadrupled reaching nearly $20B. Operating margins expanded from the low teens to over 20%. The debt that had seemed insurmountable was steadily paid down, with the company returning to investment-grade credit ratings.

MacMillan's approach to M&A was radically different from his predecessors. During his time Hologic shifted to smaller and more strategic acquisitions such as Biotheranostics, Somatex, and Endomagnetics. These were bolt-on acquisitions that enhanced existing product lines rather than transformative deals that bet the company. Each acquisition was thoroughly vetted for cultural fit and integration complexity, not just strategic rationale.

The cultural transformation was equally important. MacMillan instituted quarterly business reviews where every division had to present their results and plans in excruciating detail. Accountability became paramount. The company moved from a culture of consensus to one of performance. Underperformers were managed out; high performers were richly rewarded.

By 2016, even Icahn was impressed. Carl remained involved with Hologic till May 2016 when he exited his position, making over 40% profit, stating "The new CEO of Hologic [MacMillan] did an excellent job". Had Carl kept his stake, his profit would have been over 200% today.

The MacMillan era proved that sometimes activist investors, despite their reputation as corporate raiders, can catalyze necessary change. The combination of Icahn's pressure and MacMillan's execution created one of the great turnaround stories in med tech. But even master operators make mistakes, as Hologic would soon learn with an ill-fated venture into medical aesthetics.

VI. The Cynosure Misadventure (2017–2019)

The conference call on March 7, 2017, was upbeat. MacMillan announced that Hologic was acquiring Cynosure, a Westford, Massachusetts-based medical aesthetics company, for $1.65 billion. "This acquisition represents an exciting growth opportunity in an attractive adjacency," he told analysts. The aesthetics market was growing at double digits, driven by millennials' embrace of cosmetic procedures and the rise of med spas. It seemed like the perfect complement to Hologic's women's health focus. Cynosure manufactured laser and energy-based systems for procedures like body contouring, skin revitalization, and hair removal. The company had pioneered SculpSure, a non-invasive body contouring device that competed with CoolSculpting. Approximately 60 percent of Cynosure's business was derived from physicians outside the traditional areas of plastic surgery and dermatology, with a significant focus on the OB/GYN channel. The logic was that Hologic's strong relationships with OB/GYNs could accelerate Cynosure's growth.

But from day one, the cultures clashed. Cynosure sold to plastic surgeons and dermatologists who operated cash-pay aesthetic practices. Hologic sold to hospitals and health systems focused on insurance-reimbursed procedures. The sales processes were completely different. The customer decision-making criteria were different. Even the regulatory environments were different—aesthetics faced less stringent FDA oversight but dealt with complex direct-to-consumer marketing regulations.

The operational challenges mounted quickly. Cynosure's direct sales model, with reps earning high commissions on capital equipment sales, didn't mesh with Hologic's more consultative, relationship-based approach. Integration efforts stalled as it became clear that synergies between selling mammography systems to hospitals and laser hair removal devices to med spas were essentially nonexistent.

The financial performance was disastrous. Since acquiring Cynosure in 2017, it had significantly underperformed expectations. While other segments within Hologic performed well, it was the aesthetics unit that nearly always underperformed and in one earnings quarter caused the firm to drop revenue guidance. The aesthetics market itself was becoming more competitive, with new entrants and aggressive pricing pressure. Cynosure was losing market share.

By 2019, MacMillan had seen enough. On November 20, 2019, Hologic announced the divestment of Cynosure to Clayton, Dubilier & Rice for $205 million; this was completed on December 30, 2019. The company that Hologic had purchased for $1.65 billion was sold for roughly one-eighth of that price—a staggering destruction of shareholder value.

"Divesting our medical aesthetics business will enable us to focus on what we do best — helping women and their families live healthier lives through early detection of disease," MacMillan said in the release. "We believe this transaction will unlock value for Hologic shareholders, and at the same time provide Cynosure and its employees the best opportunity to succeed in the medical aesthetics marketplace. Moving forward, our business development strategy remains focused on the smaller, tuck-in deals that have been performing well for us and strengthening our core franchises."

The Cynosure debacle offered several critical lessons. First, adjacency isn't just about overlapping customer bases—it's about aligned business models, sales processes, and cultures. Second, even great operators like MacMillan can make strategic errors when they venture outside their circle of competence. Third, the discipline to admit a mistake and cut losses—even at a massive loss—can be more value-creating than doubling down on a failed strategy.

The write-down was painful, but the market rewarded the decision. Shares of Hologic (NASDAQ: HOLX) were up 3.4% upon news of it divesting Cynosure. Investors recognized that Hologic was returning to its core strength: focused innovation in women's health. Little did anyone know that within months, that focus would be tested by a global pandemic that would transform Hologic's diagnostics business overnight.

VII. COVID-19 Response & Molecular Diagnostics Leadership (2020–2022)

The email arrived at 2:47 AM on a Saturday in early March 2020. Kevin Thornal, president of Hologic's diagnostics division, was being summoned to an emergency call with the FDA. The agency needed diagnostic companies to develop COVID-19 tests—immediately. Within 72 hours, Hologic's molecular diagnostics team had pivoted from developing tests for sexually transmitted infections to creating what would become one of the most widely used COVID-19 assays in America.

In March 2020, Hologic received emergency use authorization from the FDA for a test for SARS-CoV-2 to help mitigate the COVID-19 pandemic. The speed of development was unprecedented. Leveraging the Panther platform—the same system from the Gen-Probe acquisition that had once seemed overpriced—Hologic could run up to 1,000 COVID tests in 24 hours with minimal hands-on time.

The technical advantages of the Panther system suddenly became mission-critical. Unlike many competing platforms that required batch processing, Panther allowed random access—labs could load samples continuously and get results in about three hours. This meant hospitals could process emergency room patients, surgical candidates, and routine screenings all on the same system without waiting to accumulate a full batch.

Production scaled at a pace that would have seemed impossible in normal times. Hologic's manufacturing facilities in San Diego, which had been producing thousands of STI tests per week, shifted to producing millions of COVID tests. The company hired hundreds of workers, ran facilities 24/7, and even chartered planes to ensure raw material supplies wouldn't be interrupted.

In November 2020, Hologic won a $119 million contract from the U.S. Department of Health and Human Services and the Department of Defense to help expand production facilities in three states, Wisconsin, Maine, and California, with the goal to provide 13 million COVID tests per month by January 2022.

The financial windfall was extraordinary. COVID testing generated over $1 billion in revenue in fiscal 2021 alone. Operating margins in the diagnostics division exceeded 40%. The company generated more free cash flow in 18 months than it had in the previous five years combined. But unlike many companies that saw COVID windfalls evaporate as quickly as they arrived, MacMillan had a plan.

Rather than returning all the COVID profits to shareholders or making another large acquisition, Hologic invested in permanent capability expansion. The company upgraded its entire Panther installed base, expanded its menu of non-COVID molecular tests, and built out international distribution. The message to the market was clear: COVID was a catalyst, not a crutch.

The company also used the pandemic to deepen customer relationships. Hospitals that had never used Hologic's diagnostic systems suddenly depended on them for COVID testing. Once the Panther systems were installed, Hologic could introduce its full menu of women's health diagnostics—STI panels, HPV tests, and viral load monitoring. It was the classic land-and-expand strategy, accelerated by a global crisis.

The strategic reinvestment extended beyond just diagnostics. Hologic accelerated R&D across all divisions, upgraded manufacturing facilities, and even enhanced its digital infrastructure. The company that had struggled with debt just seven years earlier was now deploying capital from a position of strength.

By late 2021, as COVID testing volumes began to normalize, Hologic's diagnostics business had been transformed. The division that had been a question mark after the Gen-Probe acquisition was now generating over $2 billion in annual revenue with industry-leading margins. The Panther installed base had nearly doubled. International revenues had grown by 40%.

More importantly, Hologic had proven the value of its focused strategy. While larger competitors had struggled to balance COVID response with their other business lines, Hologic's concentrated expertise in molecular diagnostics allowed it to move faster and capture more share. The company that had started 2020 as a well-regarded but niche player in molecular diagnostics ended 2022 as one of the clear leaders in the space.

The COVID windfall also provided the financial flexibility for Hologic to return to strategic acquisitions—but this time, following the disciplined, tuck-in approach that MacMillan had promised after the Cynosure disaster.

VIII. Modern Portfolio & Strategic Acquisitions (2021–Present)

The acquisition announcement on January 11, 2021, barely made headlines. Hologic was buying Biotheranostics, a breast cancer diagnostics company, for $230 million. On the same day, they announced the acquisition of SOMATEX, a German medical device company, for $64 million. These weren't transformational deals that would reshape the company. They were precisely targeted additions to strengthen existing franchises—exactly the strategy MacMillan had promised after Cynosure.

In 2025, Hologic acquired Gynesonics for $350 million, which developed the Sonata System, an ultrasound imaging device for uterine fibroids. Each acquisition followed the same pattern: bolt-on technologies that enhanced Hologic's existing platforms, required minimal integration risk, and could be immediately leveraged through Hologic's established commercial channels.

The Biotheranostics acquisition brought the Breast Cancer Index test, a genomic test that helps determine which patients would benefit from extended endocrine therapy. This fit perfectly with Hologic's breast health franchise—the same radiologists detecting cancers with Hologic's 3D mammography systems could now also order precision medicine tests to guide treatment decisions. In April 2021, the company announced it will acquire Mobidiag, a molecular diagnostics firm with multiplex technology, for $795 million. The acquisition completed in June 2021. The acquisition marks the fourth such deal for Hologic in calendar 2021. In January, Hologic bought Somatex for $64 million, followed by the $230 million purchase of Biotheranostics in February and the $159 million buy of Diagenode in March.

The acquisition of Mobidiag extended Hologic's portfolio into the large, fast growing acute care segment. It also strengthened Hologic's global footprint and accelerated regional time-to-market. Mobidiag provides near-patient, molecular diagnostic instruments and tests for acute care conditions including gastrointestinal and respiratory infections, antimicrobial resistance management,and healthcare associated infections (HAIs). Its Amplidiag and Novodiag testing platforms deliver results in 50 minutes to two hours. The Novodiag platform combines real-time PCR and microarray capabilities to provide high-level multiplexing.

In April 2024, Hologic agreed to acquire British medical device manufacturer Endomag for $310 million. The acquisition completed in July that year. Endomag's magnetic seed localization technology for breast cancer surgery perfectly complemented Hologic's breast imaging business. Rather than using wires to mark tumors for surgical removal—a decades-old technique that was uncomfortable for patients—Endomag's technology used tiny magnetic seeds that could be placed days or weeks before surgery. The company operates through four segments: Diagnostics, Breast Health, GYN Surgical, and Skeletal Health. Each segment reflects Hologic's focused approach to women's health, with interconnected products that create a comprehensive ecosystem.

The Diagnostics segment, now representing nearly half of total revenue, offers molecular diagnostic assays including the Aptima family for STDs and respiratory infections, the ThinPrep cytology system for cervical cancer screening, and the Rapid Fetal Fibronectin Test for assessing pre-term birth risk. The molecular diagnostics business has been a consistent growth driver, powered by an installed base of more than 3,300 high-throughput Panther systems worldwide.

The Breast Health segment provides comprehensive breast cancer care solutions, including the Selenia 3D Dimensions mammography systems, image analytics software, minimally invasive biopsy guidance systems, and breast conserving surgery products. Service revenues now account for 40% of Breast Health sales, providing stable recurring revenue that smooths the volatility of capital equipment sales.

The GYN Surgical segment includes minimally invasive surgical products, such as the NovaSure endometrial ablation system and the MyoSure tissue removal devices. These products are designed to improve patient outcomes while reducing procedural complexity and recovery times. The international Surgical business has been particularly strong, with nearly 20% growth driven by successful execution of a go-direct strategy in Europe.

The Skeletal Health segment, the smallest division, offers the Horizon DXA system for bone density evaluation—a direct descendant of the technology that founded the company nearly 40 years ago. While comparatively smaller, it maintains Hologic's presence in the osteoporosis market where the company began.

The integrated nature of these segments creates powerful synergies. A patient might receive a 3D mammography screening (Breast Health), have suspicious cells analyzed with ThinPrep (Diagnostics), undergo a biopsy with Hologic's guidance systems (Breast Health), and if needed, have tissue removed with minimally invasive surgical tools (GYN Surgical). This comprehensive approach to women's health creates customer stickiness and cross-selling opportunities that broader competitors struggle to match.

Looking ahead, Hologic's acquisition strategy remains disciplined and focused. The company continues to evaluate tuck-in acquisitions that enhance its core franchises, with a particular emphasis on technologies that can be immediately leveraged through its existing commercial channels. The disasters of Gen-Probe's integration challenges and Cynosure's complete failure have been replaced by a methodical approach that prioritizes cultural fit and operational synergies over transformational ambitions.

IX. Playbook: Business & Investing Lessons

The Hologic story offers a masterclass in both strategic triumphs and cautionary tales. After nearly four decades of evolution, several key lessons emerge that transcend the medical device industry.

The Power of Focus: Women's Health as a Defensible Niche

While competitors like GE Healthcare and Siemens Healthineers pursue breadth across all medical specialties, Hologic's laser focus on women's health created unexpected advantages. This isn't just about market segmentation—it's about developing deep, specialized expertise that broader competitors can't match. When a hospital evaluates mammography systems, they're not just buying a machine; they're buying into Hologic's decades of specialized knowledge in breast tissue imaging. This focus creates a moat that's difficult for diversified competitors to cross, even with superior resources.

The focus strategy also enables faster innovation cycles. While a company like GE must allocate R&D across dozens of product lines, Hologic can concentrate its entire development budget on a narrow set of interrelated problems. This concentration of resources explains how a company with a fraction of GE's R&D budget could pioneer breakthrough technologies like 3D mammography.

Activist Investors as Catalysts for Change

The Icahn intervention demonstrates that activist investors, despite their reputation as short-term profit seekers, can catalyze necessary transformations. Icahn didn't just demand cost cuts or asset sales—he forced a CEO change that brought in MacMillan, whose operational excellence transformed the company. The lesson isn't that activists are always right, but that external pressure can break organizational inertia when management becomes complacent.

Carl's 40% profit when he exited in 2016 looks modest compared to the 200% returns he would have earned by holding through 2021. This reveals another truth about activist investing: the changes they catalyze often create value that extends far beyond their investment horizon.

Turnaround Playbook: Operational Excellence Before Growth

MacMillan's transformation of Hologic follows a reproducible pattern. First, fix the basics—manufacturing efficiency, sales force productivity, product rationalization. Only after establishing operational excellence did he pursue growth through acquisitions. This sequencing matters because growth without operational discipline leads to complexity that destroys value, as the Gen-Probe acquisition initially demonstrated.

The emphasis on debt reduction before expansion also proved crucial. By strengthening the balance sheet first, Hologic could make acquisitions from a position of strength rather than desperation. This patient approach to capital allocation distinguishes sustainable turnarounds from temporary recoveries.

M&A Discipline: Learning from Gen-Probe and Cynosure

The contrast between the Gen-Probe and Cynosure acquisitions offers a framework for evaluating M&A success. Gen-Probe, despite its initial challenges, was strategically sound—it moved Hologic into the recurring revenue model of diagnostics and provided technology platforms that became invaluable during COVID. The integration was painful, but the strategic logic held.

Cynosure, by contrast, failed on multiple dimensions. The customer bases didn't overlap meaningfully. The sales processes were incompatible. The business models—insurance-reimbursed procedures versus cash-pay aesthetics—created operational friction. The lesson: adjacency in customer demographics (women) doesn't equal adjacency in business model or operations.

The subsequent shift to smaller, tuck-in acquisitions like Biotheranostics and Endomag shows organizational learning. These deals enhanced existing franchises rather than creating new ones, could be integrated quickly, and carried minimal cultural risk.

Regulatory Moats in Medical Devices

Hologic's three-year monopoly on 3D mammography in the U.S. illustrates the power of regulatory barriers. Unlike software or consumer products where competitors can quickly copy innovations, medical devices face years of clinical trials and regulatory approval. First-mover advantage in medical devices isn't just about market share—it's about establishing clinical evidence, training radiologists, and becoming the standard of care before competitors can even enter the market.

This regulatory moat becomes self-reinforcing. Once hospitals invest in Hologic systems and train staff on the technology, switching costs become prohibitive. The installed base becomes an annuity of service contracts and upgrade revenues that competitors can't access.

Razor/Blade Model in Diagnostics

The Panther platform exemplifies the razor/blade model in diagnostics. The initial system placement might break even or even lose money, but each installed system generates recurring revenue through test cartridges for years. During COVID, this model proved its value—Hologic could rapidly scale test production for its installed base while competitors struggled to place new systems.

The model also creates predictable revenue streams that smooth the volatility of capital equipment cycles. While mammography system sales might fluctuate with hospital capital budgets, diagnostic test volumes grow steadily with patient volume. This mix of capital and consumable revenue provides both growth and stability.

The Platform Advantage

Hologic's evolution from product company to platform company represents a fundamental strategic shift. Instead of selling individual products, they provide integrated platforms—the Panther for diagnostics, the Genius 3D mammography ecosystem for breast health, the MyoSure system for gynecological surgery. Platforms create customer lock-in, enable rapid introduction of new products, and generate network effects as more users adopt the system.

The platform strategy also changes the competitive dynamics. Competitors must match not just individual products but entire ecosystems. This raises barriers to entry and increases customer switching costs, creating sustainable competitive advantages that pure product innovation cannot provide.

X. Analysis & Bear vs. Bull Case

Competitive Landscape

Hologic operates in highly competitive markets with formidable rivals. In diagnostics, Abbott, Roche, and BD dominate with broader product portfolios and global reach. In imaging, GE Healthcare and Siemens Healthineers leverage their scale across multiple imaging modalities. Yet Hologic's focused strategy creates defensible positions even against these giants.

In mammography, Hologic maintains approximately 70% market share in the U.S. and growing share internationally. The company's #1 position in 3D mammography isn't just about market share—it's about setting the standard of care. Clinical studies using Hologic systems become the evidence base that competitors must match or exceed.

In molecular diagnostics, while Roche and Abbott have broader menus, Hologic's Panther platform excels in workflow automation and ease of use. The system's random access capability—allowing continuous sample loading rather than batch processing—provides operational advantages that broader platforms struggle to match.

Market Position Strengths

Three structural advantages underpin Hologic's market position. First, the installed base creates recurring revenue streams and high switching costs. With over 3,300 Panther systems and thousands of mammography systems globally, Hologic has built an annuity-like business model.

Second, the integrated portfolio creates cross-selling opportunities. A hospital using Hologic's mammography systems is more likely to adopt their biopsy guidance systems and surgical tools. This ecosystem approach increases wallet share and customer retention.

Third, the focus on women's health creates specialization advantages. While competitors treat women's health as one vertical among many, for Hologic it's the entire business. This focus drives faster innovation, deeper customer relationships, and better clinical outcomes.

Growth Drivers

Several secular trends support long-term growth. Aging demographics in developed markets increase demand for mammography screening and osteoporosis testing. Rising healthcare access in emerging markets expands the addressable patient population. The shift toward precision medicine favors companies with integrated diagnostic and treatment solutions.

International expansion represents a particular opportunity. International sales currently represent about 26% of revenue, suggesting significant headroom for growth. The company's direct sales strategy in Europe has driven 20% growth in surgical products, demonstrating the potential for geographic expansion.

New product cycles also drive growth. The recent FDA clearance for AI-enhanced mammography reading, the expanding menu on the Panther platform, and the integration of acquired technologies create multiple growth vectors beyond market expansion.

Risks and Challenges

Reimbursement pressures pose the most significant near-term risk. Healthcare systems globally face budget constraints, potentially limiting capital equipment purchases and pressuring test pricing. The shift toward value-based care could pressure margins if Hologic can't demonstrate clear clinical value.

Competition continues to intensify. Chinese manufacturers offer lower-cost alternatives in emerging markets. Tech giants like Google and Amazon eye healthcare opportunities. New entrants with novel technologies could disrupt established markets.

Regulatory changes create uncertainty. More stringent FDA requirements could slow product approvals and increase development costs. International regulatory harmonization remains elusive, complicating global expansion.

Technological disruption lurks as a long-term threat. Liquid biopsies could reduce demand for tissue-based diagnostics. AI could commoditize image interpretation. Point-of-care testing could bypass central lab platforms.

Financial Metrics Analysis

Hologic's financial performance reflects both its operational improvements and strategic focus. Operating margins have expanded from the low teens to over 20% under MacMillan's leadership. Return on invested capital exceeds 10%, demonstrating efficient capital allocation. Free cash flow generation remains robust, funding both acquisitions and shareholder returns.

The balance sheet has strengthened considerably since the Gen-Probe acquisition. Net debt to EBITDA has declined to manageable levels. The company maintains investment-grade credit ratings, providing financial flexibility for opportunistic acquisitions.

Valuation metrics suggest reasonable pricing relative to peers. Trading at approximately 15-20x forward earnings, Hologic commands a premium to diversified med tech but a discount to pure-play diagnostics companies. This positioning reflects both the quality of the business and the market's assessment of growth potential.

Bull Case

The bull thesis rests on Hologic's unique position in women's health, operational excellence, and multiple growth drivers. The company's focused strategy creates competitive advantages that broader competitors can't replicate. International expansion, new product introductions, and demographic tailwinds support sustained mid-single-digit organic growth.

The acquisition strategy, now disciplined and focused on tuck-ins, can accelerate growth without the integration risks of transformational deals. The platform business model generates predictable recurring revenues with expanding margins. Management has demonstrated the ability to execute operationally while maintaining strategic discipline.

Bulls see Hologic as a defensive growth story—resilient demand for women's health services, recession-resistant diagnostic testing, and mission-critical screening programs. The company's market leadership positions and high switching costs create a wide moat that protects market share and pricing power.

Bear Case

Bears worry about market maturation in core segments. U.S. mammography screening rates have plateaued. Competition in molecular diagnostics intensifies as patents expire and technologies commoditize. Growth increasingly depends on international expansion, which carries execution risk and lower margins.

The capital equipment exposure creates cyclical vulnerability. Hospital capital budgets fluctuate with economic conditions and regulatory changes. The shift toward value-based care could pressure both equipment pricing and test reimbursement. Competition from lower-cost alternatives could force price concessions.

Bears also point to technological disruption risks. AI could reduce the need for specialized imaging equipment. Direct-to-consumer testing could bypass traditional diagnostic channels. Novel screening technologies could obsolete current approaches. The focused strategy that creates advantages today could become a liability if women's health approaches fundamentally change.

XI. Epilogue & Future Outlook

The women's health market stands at an inflection point. After decades of underinvestment relative to other medical specialties, women's health is finally receiving the attention—and capital—it deserves. Venture funding for women's health startups has exploded. Major pharmaceutical companies are expanding their women's health portfolios. Digital health platforms are reimagining care delivery models. For Hologic, this represents both opportunity and challenge.

The opportunity lies in market expansion. As awareness grows and access improves, more women globally will receive regular screening and preventive care. The total addressable market for women's health products could double over the next decade. Hologic's established positions and clinical credibility position it to capture disproportionate share of this growth.

Yet the challenge comes from new entrants unburdened by legacy infrastructure. Digital-first companies offer at-home testing and telehealth consultations. AI startups promise to democratize image interpretation. Consumer health companies target younger women with preventive health platforms. Hologic must balance defending its core franchises while adapting to new care delivery models.

AI and Machine Learning in Diagnostics

Artificial intelligence represents both Hologic's greatest opportunity and most significant threat. The company has embraced AI as an enhancement to its existing platforms—AI-assisted mammography reading improves radiologist productivity and accuracy. Machine learning algorithms optimize the Panther platform's workflow. Predictive analytics identify high-risk patients for enhanced screening.

But AI could also disrupt Hologic's business model. If AI can accurately interpret mammograms, does the imaging equipment manufacturer capture the value, or does it shift to the software provider? If point-of-care devices with AI can match central lab accuracy, does the high-throughput platform model remain viable? Hologic must navigate the transition from hardware-centric to software-enhanced solutions without cannibalizing its core business.

Liquid Biopsy and Precision Medicine Trends

The emergence of liquid biopsy—detecting cancer through blood tests rather than tissue samples—could fundamentally reshape cancer screening. Early detection through circulating tumor DNA could identify cancers before imaging can visualize them. This technology could complement or potentially replace traditional screening methods.

Hologic's response has been measured but strategic. Rather than rushing into liquid biopsy, the company has focused on enhancing its tissue-based diagnostics with molecular markers. The Breast Cancer Index test from Biotheranostics exemplifies this approach—using genomic analysis to guide treatment decisions. This positions Hologic to participate in precision medicine without abandoning its core competencies.

Building a Platform vs. Product Company

The strategic question facing Hologic is whether to remain a specialized medical device company or evolve into a broader women's health platform. The product company model—selling equipment and consumables—generates predictable returns but faces commoditization pressure. The platform model—connecting patients, providers, and payers—offers higher growth potential but requires new capabilities.

MacMillan's approach has been pragmatic: strengthen the product portfolio while selectively building platform capabilities. The Genius digital diagnostics system integrates AI into workflow management. The company's sponsorship of the WTA Tour builds consumer brand awareness. These initiatives suggest a gradual evolution rather than radical transformation.

Final Reflections

Hologic's journey from a twelve-person startup to a $20 billion market leader offers enduring lessons about focus, execution, and resilience. The company that nearly collapsed under debt from the Gen-Probe acquisition emerged stronger and more focused. The operational discipline instilled by MacMillan created a culture of accountability and continuous improvement.

Perhaps most importantly, Hologic demonstrates that specialization can triumph over diversification in healthcare. While giants spread resources across every medical specialty, Hologic's singular focus on women's health created deeper expertise, stronger customer relationships, and better clinical outcomes. In an industry often criticized for treating women's health as an afterthought, Hologic made it the entire thought.

The challenges ahead are real—technological disruption, competitive pressure, regulatory uncertainty. But Hologic has proven its ability to adapt and evolve. From bone density to digital mammography to molecular diagnostics, the company has repeatedly transformed itself while maintaining its core mission.

As Jay Stein hoped in his retirement message, the act of doing good for people remains the core foundation of the company. In healthcare, where patient outcomes ultimately determine success, this purpose-driven approach creates value that transcends quarterly earnings. For investors evaluating Hologic, the question isn't just about financial returns—it's about backing a company whose success directly correlates with improving women's health globally.

The science of sure—Hologic's tagline—captures both the company's technical rigor and its essential promise: bringing certainty to the uncertain, clarity to the complex, and hope to millions of women facing health challenges. In that mission lies both Hologic's past achievements and its future potential.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube