Hallador Energy Company: The Last Coal Miner Standing

I. Introduction & Episode Roadmap

How does a company survive, and even thrive, in America's most hated industry?

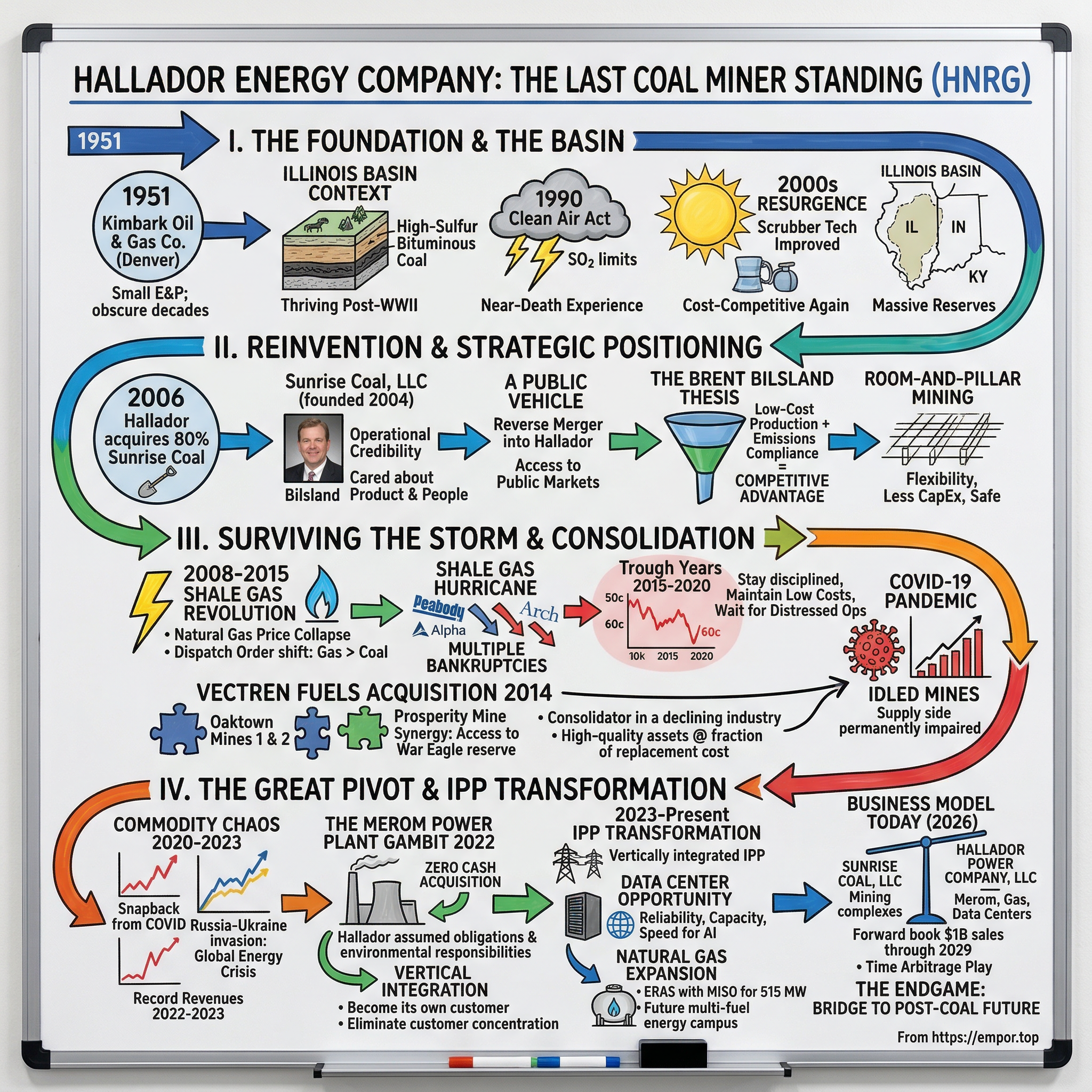

That is the central question of Hallador Energy's story. In an era when coal companies have been bankrupted, shamed, divested, and legislated into oblivion, this small Indiana-based operation has not only endured but has pulled off one of the most audacious strategic pivots in American energy. It has gone from a tiny regional coal miner to a vertically integrated independent power producer with nearly a billion-dollar market capitalization. And it has done it while sitting atop what most investors consider to be a stranded asset: high-sulfur Illinois Basin coal.

Hallador Energy, trading on the NASDAQ under the ticker HNRG, is one of the last pure-play Illinois Basin coal producers in the United States. The company operates underground and surface mines in southwestern Indiana, and since 2022, it also owns and operates a 1,080-megawatt coal-fired power plant. It has gone from a sixty-cent stock during the depths of the COVID pandemic to trading in the twenties, a run that would make even the most enthusiastic growth investor do a double take.

But this is not a growth story. This is an endgame story. And endgame stories, when executed well, can be just as compelling as any Silicon Valley rocket ship.

The paradox at the heart of Hallador is straightforward: coal is in terminal decline in the United States, and everyone knows it. U.S. coal consumption has fallen by more than half since its peak in 2007. Utilities are closing coal plants at an accelerating pace. ESG mandates have made the industry virtually uninvestable for institutional capital. And yet, here is Hallador, generating record cash flows, signing deals with data center developers, and filing applications for natural gas power expansion. The company is not denying the end of coal. It is playing the endgame better than anyone else.

The themes that run through this story are universal: consolidation as a survival strategy, contrarian bets that look insane until they don't, the power of vertical integration, and the delicate art of managing a business for cash extraction rather than growth. Whether you care about coal or not, the capital allocation lessons embedded in Hallador's journey are relevant to any investor thinking about declining industries, activist management teams, or the value of being the last one standing when everyone else has left the room.

So let's dig in. Literally.

II. The Illinois Basin & Coal's Golden Age Context

Picture a map of the American Midwest. Draw a rough triangle from Springfield, Illinois, down to Evansville, Indiana, and across to Paducah, Kentucky. Underneath that triangle lies one of the most consequential geological formations in American energy history: the Illinois Basin.

To understand Hallador, you first need to understand this basin, because the geology beneath southern Illinois, southwestern Indiana, and western Kentucky is the entire reason this company exists.

The Illinois Basin is one of the great geological curiosities of American energy. Stretching across three states, it contains the largest bituminous coal reserve base in the United States, with an estimated 200 billion tons of coal underground, of which roughly 38 billion tons in Illinois alone are considered economically recoverable. These are staggering numbers. For context, at current U.S. consumption rates, the Illinois Basin alone could theoretically supply the nation's coal needs for centuries.

But there is a catch, and it is a big one. Illinois Basin coal is what geologists call "high-sulfur" coal, containing roughly three to five percent sulfur by weight. When burned, that sulfur converts to sulfur dioxide, the primary precursor to acid rain. For decades, this chemical reality made Illinois Basin coal the black sheep of the American coal family. While low-sulfur coal from the Powder River Basin in Wyoming and the Central Appalachian fields of West Virginia could be burned relatively cleanly, Illinois Basin coal required expensive pollution control equipment to meet federal air quality standards.

Before the regulatory revolution, coal was simply America's energy backbone. In the decades following World War II, coal-fired power plants mushroomed across the Midwest, the South, and the Ohio Valley. Utilities loved coal because it was cheap, abundant, domestically sourced, and could be stockpiled on-site for months, providing energy security that no other fuel could match. By the late 1980s, coal accounted for more than half of all electricity generated in the United States. It was the foundation upon which the world's largest economy ran.

Then came the Clean Air Act Amendments of 1990. This landmark legislation imposed strict limits on sulfur dioxide emissions from power plants, creating a cap-and-trade system that fundamentally reshaped the economics of coal. Overnight, utilities that had been happily burning high-sulfur Illinois Basin coal faced a choice: install expensive scrubbers, which are technically known as flue-gas desulfurization systems, to remove sulfur from their smokestacks, or switch to low-sulfur coal from the Powder River Basin, which could be burned with minimal SO2 emissions.

Most chose to switch. The result was a near-death experience for the Illinois Basin.

Production collapsed as utilities signed long-term contracts with Wyoming coal producers instead. Mines closed. Towns hollowed out. Communities that had depended on coal for generations watched their economic foundation crumble. The Illinois Basin, which had been a thriving coal province, became something of a ghost region in the energy landscape.

But the obituaries were premature. Two developments gave the Illinois Basin a second life. First, Powder River Basin coal, while low in sulfur, is also low in energy density, meaning you need to burn significantly more of it to generate the same amount of electricity. When you factor in the rail transportation costs of shipping coal from Wyoming to power plants in Indiana or Illinois, the economic advantage narrows considerably. Second, and more importantly, scrubber technology improved dramatically and costs came down. By the mid-2000s, utilities were installing modern scrubbers that could remove more than ninety-five percent of sulfur dioxide from exhaust gases. Once a plant had a scrubber, there was no longer a compelling reason to pay a premium for low-sulfur coal. Illinois Basin coal, with its high energy density and proximity to Midwestern utilities, suddenly became competitive again.

This was the window that Hallador walked through. Understanding the timeline is important: Illinois Basin coal production bottomed out in the mid-1990s, then began a steady recovery that would eventually see the basin recapture significant market share from both the Powder River Basin and Appalachia. By 2008, the Illinois Basin was producing approximately 99 million short tons per year, roughly equally divided between Illinois, Indiana, and western Kentucky. The basin had gone from near-death to resurgence in less than fifteen years.

The cast of characters in the Illinois Basin during this resurgence included giants like Peabody Energy, the world's largest private coal company, which operated massive surface mines across multiple basins; Alliance Resource Partners, the dominant pure-play producer in the basin with production approaching 28 million tons; Foresight Energy, which built some of the most productive longwall mines in the country, capable of producing up to 25 million tons annually; and Murray Energy, the largest private coal company in America run by the irrepressible Bob Murray, who famously refused to acknowledge climate change while expanding his coal empire across multiple states.

Against these titans, Hallador was a rounding error. Indiana's third-largest coal producer, it barely registered on the national production rankings. But being small, it turned out, was exactly the advantage it needed. The big players were weighed down by corporate bureaucracy, public market expectations, and debt loads that assumed the boom times would last forever. Hallador, under Bilsland's leadership, had none of those encumbrances. It could move fast, keep costs low, and make opportunistic decisions without needing approval from a board full of outside directors or a syndicate of investment bankers.

III. Hallador's Founding & Early Wilderness Years (1951-2000s)

The origin story of Hallador Energy is not the typical founder-in-a-garage tale. It is something far stranger: a Denver-based oil and gas exploration company that spent decades in obscurity before reinventing itself entirely as an Indiana coal miner.

In July 1951, a small group of geologists and business professionals in Denver, Colorado, incorporated The Kimbark Company, Ltd., later known as Kimbark Oil and Gas Company. The company was a classic small-cap exploration outfit, the kind of operation that populated the Denver energy scene by the hundreds during the postwar oil boom. For nearly four decades, Kimbark operated in relative anonymity, drilling wells and exploring acreage without ever achieving the scale or the strike that would catapult it into prominence.

The first pivotal moment came in December 1989, when Kimbark merged with Hallador Exploration Company, a California-based entity founded in 1985. The shareholders approved a name change, and the combined entity became Hallador Petroleum Company, eventually evolving into Hallador Energy Company. The name "Hallador" loosely translates from Portuguese as "one who leads the way," a name that would prove either prophetic or ironic depending on which decade you're examining.

For the next fifteen years, Hallador existed in what can only be described as corporate limbo. It was publicly traded but barely noticed, an oil and gas company without the production scale to matter and without the exploration budget to swing for the fences. The company was essentially a shell with a NASDAQ listing, the kind of entity that might get used as a vehicle for a reverse merger or might simply wither away as its remaining assets depleted.

What changed everything was a group of coal men in Indiana who saw an opportunity and needed a public vehicle to pursue it. In the early 2000s, the Bilsland family and their partners, the Laswell brothers, were watching the Illinois Basin coal market with growing excitement. The Laswells and Hank Bilsland, the patriarch, had a history together. They had been three of the four principal owners of Catlin Coal, Inc., which had developed the Riola Mine in Catlin, Illinois. That mine was sold in 2000 to Black Beauty Coal Company, giving the group both capital and the conviction that there was money to be made in Illinois Basin coal, particularly as scrubber installations were making high-sulfur coal marketable again.

In 2004, they founded Sunrise Coal, LLC, with the vision of building a modern, efficient coal mining operation in southwestern Indiana. Among the founding investors was Hank Bilsland's son, Brent, who would eventually become the central figure in Hallador's transformation.

The question was how to access public markets to fund their ambitions. Starting from scratch with an IPO would have been expensive, time-consuming, and uncertain. The answer was sitting in Denver, gathering dust: Hallador Energy, with its NASDAQ listing and minimal operations.

In 2006, Hallador acquired eighty percent of Sunrise Coal, effectively becoming a coal company overnight. The old oil and gas shell had found its purpose. Three years later, in 2009, Hallador purchased the remaining twenty percent, making Sunrise Coal a wholly owned subsidiary. The transformation was complete. What had been a dormant Denver exploration company was now a pure-play Indiana coal producer.

This kind of corporate metamorphosis is not uncommon in the small-cap world, but it is rarely executed with the strategic clarity that the Bilsland team brought to the table. They were not financial engineers looking to flip a shell company. They were coal operators who understood the geology, the customers, and the regulatory environment of the Illinois Basin better than almost anyone. They just needed a public listing to pursue their vision, and Hallador gave them one.

The Bilsland-Laswell partnership is worth lingering on because it reveals how the coal business actually works at the ground level. This is not an industry where you recruit a management team from McKinsey. The people who run successful coal mines are the people who grew up around coal mines, who understand the specific characteristics of Indiana V seam coal, who know which county officials to call when a permit needs expediting, and who have the trust of miners' unions and utility procurement officers alike. The Catlin Coal experience had given the Bilsland-Laswell team something that no amount of financial engineering could replicate: the operational credibility to build a mining company from scratch in a community that was deeply skeptical of outsiders.

There is a parallel here to the craft brewing revolution or the resurgence of independent bookstores: sometimes the biggest competitive advantage in a declining industry is simply caring about the product and the people more than the corporate behemoths do. The Bilslands were not managing coal from a Denver headquarters. They were living in Indiana, walking the mine faces, and eating lunch with the same people who operated the continuous mining machines. That personal proximity created a culture of operational excellence that would prove decisive in the years ahead.

IV. The Brent Bilsland Era Begins: Going Public & Strategic Positioning (2005-2014)

Brent Bilsland is not the kind of CEO you find profiled in glossy business magazines. He does not give TED talks or tweet about corporate purpose. He is a coal man from Indiana, the son of a coal man, who grew up understanding that the energy business is fundamentally about two things: moving dirt and managing contracts. Before entering the coal industry, he spent seven years at Knapper Corporation, an agricultural company he co-founded. That agricultural background, with its emphasis on commodity cycles, weather risk, and thin margins, proved to be remarkably good preparation for running a coal company in a declining market.

When Bilsland took the reins at Sunrise Coal as president in 2006, he brought a thesis that ran counter to prevailing industry wisdom. Most coal executives in the mid-2000s were focused on the Powder River Basin or the export market. The smart money was fleeing the Illinois Basin, viewing its high-sulfur coal as a long-term liability. Bilsland saw something different. He saw that scrubber installations were accelerating across the Midwest, that transportation costs from Wyoming were rising, and that Illinois Basin coal's high energy density gave it a structural cost advantage over its low-sulfur competitors. His thesis was deceptively simple: low-cost production plus emissions compliance technology equals competitive advantage.

The key to executing this thesis was securing long-term contracts with the Midwestern utilities that were the natural customers for Illinois Basin coal. These were not glamorous relationships. They were the product of years of handshake deals, mine tours, and reliability demonstrations. Bilsland cultivated relationships with thirteen utilities across the region, an extraordinary customer base for a company of Hallador's size. In an industry where trust matters, where a utility needs to know that its coal supplier will deliver the right tonnage of the right quality on the right schedule, week after week, year after year, these relationships were worth more than any balance sheet asset.

The early Sunrise Coal operations were modest by industry standards. The company developed mining operations in Knox County, Indiana, using room-and-pillar mining methods. For those unfamiliar with underground coal mining, the difference between room-and-pillar and longwall mining is worth understanding because it says a lot about Hallador's strategic philosophy.

In room-and-pillar mining, miners cut a network of rooms into the coal seam, leaving pillars of coal standing to support the roof. Think of it like carving a checkerboard pattern into a block of cheese: you eat the squares and leave the grid structure standing. It is slower than longwall mining but requires less capital equipment, is safer, and offers more flexibility to adjust production up or down in response to market conditions.

Longwall mining, by contrast, uses a massive shearer that moves back and forth across a long coal face, supported by hydraulic roof supports that advance as the coal is extracted. Longwall mines can produce enormous volumes, sometimes five to ten million tons per year from a single panel, but the equipment costs tens of millions of dollars and the mine layout must be designed years in advance.

Foresight Energy was deploying longwall mining to spectacular production numbers in Illinois, building mines that rivaled the most productive operations in the world. Sunrise Coal's room-and-pillar approach was conservative by comparison, but it was deliberately so. The lower capital intensity meant less debt. The flexibility meant the company could scale production to match actual orders rather than running flat-out to cover fixed costs. And the safety record was better, which mattered both for the miners and for the company's regulatory standing.

This conservatism extended to the balance sheet. While peers were leveraging up to fund acquisitions and production expansion, Hallador maintained a discipline that would later prove to be its greatest competitive advantage. The company did not chase growth for growth's sake. It did not borrow heavily to buy distressed assets at inflated prices. It waited. And in the coal industry of the late 2000s and early 2010s, patience was perhaps the rarest commodity of all.

In January 2014, Bilsland was promoted to CEO of the parent company, Hallador Energy, with Victor Stabio moving to chairman. It was a succession that had been years in the making. Stabio, who had guided the company through its transition from oil and gas to coal, recognized that the next phase of Hallador's evolution required a leader with deep operational roots in the coal business rather than a corporate generalist. Bilsland was that leader. By 2018, he would assume the chairmanship as well, making him the undisputed captain of the ship: chairman, president, and CEO.

Beyond his formal titles, Bilsland also became active in industry advocacy, holding leadership positions with the Reliable Energy Association, America's Power, the National Mining Association, and the Indiana Coal Council. These roles gave him visibility into the policy decisions that would shape coal's future and access to the utility executives who would determine whether Hallador's coal had a market. But it was the deal he engineered in 2014, just months after his promotion to CEO, that truly put Hallador on the map.

The contrast between Bilsland's approach and the rest of the coal industry during this period is stark. While Arch Coal, Alpha Natural Resources, and Patriot Coal were loading up on debt to acquire metallurgical coal assets in Appalachia, betting on a permanent commodity supercycle driven by Chinese demand, Bilsland was doing the unglamorous work of building relationships with Indiana utilities and keeping his cost structure lean. When the supercycle ended, the difference in outcomes was devastating. The overleveraged players went bankrupt. Hallador survived. That was not luck. That was strategic discipline.

V. The Shale Gas Revolution & Coal's Existential Crisis (2008-2015)

The shale gas revolution arrived like a category five hurricane, and it hit the coal industry hardest of all.

To understand the magnitude of what happened, consider this: in 2008, natural gas prices in the United States averaged around nine dollars per million BTU. By 2012, they had collapsed to under two dollars. This was not a normal commodity cycle. This was a fundamental restructuring of the American energy landscape, driven by the twin technologies of hydraulic fracturing and horizontal drilling, which unlocked vast reserves of natural gas trapped in shale formations across the country. The Marcellus Shale in Pennsylvania, the Barnett Shale in Texas, the Haynesville in Louisiana, all of them began producing gas in quantities that no one had predicted even five years earlier.

For coal, the impact was immediate and brutal. Natural gas and coal compete directly for the same market: baseload electricity generation. Think of it this way: a utility executive sitting in Indianapolis looking at their generation portfolio is essentially asking one question every day: which of my plants should I run right now to generate electricity at the lowest cost? When gas prices were high, the answer was coal. When gas prices collapsed below two dollars, the answer was almost always gas. The technical term for this is "dispatch order," and when natural gas jumped ahead of coal in the dispatch order, entire mines lost their reason for existing.

The efficiency gap made it worse. A modern combined-cycle gas turbine can convert natural gas to electricity at a thermal efficiency north of sixty percent, meaning more than half of the energy in the fuel becomes electricity. The best coal plants operate at maybe thirty-five to forty percent efficiency. When gas prices collapsed, coal plants that had operated profitably for decades suddenly found themselves underwater. Utilities were not making ideological choices. They were making economic ones, and the economics had shifted decisively.

The bankruptcies started slowly, then cascaded. Patriot Coal, a company that had been spun off from Peabody Energy and later absorbed assets from Arch Coal, filed for bankruptcy in 2012, then again in 2015. James River Coal went down in 2014. In August 2015, Alpha Natural Resources, one of the largest coal producers in the country, filed for Chapter 11. Walter Energy, a major metallurgical coal producer, went under the same year. Then came the two body blows that shook the entire industry: Arch Coal filed in January 2016, and Peabody Energy, the world's largest private coal company, filed in April 2016. By the time Peabody entered bankruptcy, nearly half of all coal produced in the United States came from a company that was, or had been, in bankruptcy proceedings.

The carnage was concentrated in Appalachia, where production costs were highest and coal seams were becoming thinner and harder to reach. But the Illinois Basin was not immune. Foresight Energy, which had built enormous longwall mines in southern Illinois, struggled under the weight of its debt. Murray Energy, which had expanded aggressively across multiple coal basins, would eventually file for bankruptcy in 2019.

So how did Hallador survive? The answer lies in a combination of structural advantages and deliberate strategic choices.

First, Illinois Basin coal had real cost advantages over Appalachian coal. The seams were thicker, the overburden was thinner, and the mining methods were more efficient. Indiana and Illinois mines could produce coal for meaningfully less per ton than their Appalachian counterparts. When utilities needed to buy coal, even in a depressed market, Illinois Basin producers were among the last to be priced out.

Second, Hallador's utility customers were, by and large, plants that had invested in scrubbers and were committed to burning coal for the foreseeable future. These were not marginal plants on the verge of retirement. They were large, efficient units with years of remaining useful life. The contracts Hallador had in place provided a floor of demand that insulated the company from the worst of the market downturn.

Third, and most critically, Hallador had not overlevered itself. The companies that went bankrupt during this period almost universally shared one characteristic: they had taken on enormous debt to fund acquisitions at the top of the cycle. Alpha Natural Resources had paid four billion dollars for Massey Energy in 2011, just as coal prices were peaking. Arch Coal had paid three and a half billion for International Coal Group. These were bets that coal prices would stay high forever. When prices collapsed, the debt remained but the cash flows to service it did not. Hallador, by contrast, had maintained a conservative balance sheet. The company was not trying to be the biggest. It was trying to be the last.

Bilsland's playbook during this period was almost monastic in its simplicity: stay disciplined, maintain low costs, honor your contracts, keep debt manageable, and wait for distressed opportunities. It was not a strategy that would get you on the cover of Forbes. But it was a strategy that kept you alive when the companies on the cover of Forbes were filing for Chapter 11.

VI. The Great Consolidation Play: Acquiring Vectren Fuels (2014)

On July 1, 2014, Sunrise Coal, Hallador's operating subsidiary, announced that it had reached an agreement to purchase Vectren Fuels, the wholly owned coal mining subsidiary of Vectren Corporation, a publicly traded utility holding company based in Evansville, Indiana. The deal closed on August 29, 2014, and it transformed Hallador overnight from a small regional operator into a significant force in the Illinois Basin.

The backstory of the deal reveals much about how Hallador's strategy worked in practice. Vectren Corporation was primarily a natural gas and electric utility, and its coal mining subsidiary, Vectren Fuels, was increasingly an awkward fit within the parent company's portfolio. Utilities that owned captive coal mines were facing growing scrutiny from regulators, investors, and environmental groups. The trend in the utility industry was toward clean energy, or at least the appearance of clean energy, and owning coal mines sent exactly the wrong signal. Vectren wanted out. Hallador wanted in.

The purchase price was 296 million dollars, with working capital adjustments that could push the total to 325 million dollars. To finance the deal, Hallador secured a 425-million-dollar credit facility led by PNC Bank. This was, by any measure, a transformative bet for a company of Hallador's size. The acquisition was, proportionally speaking, one of the largest in the company's history, the kind of deal that would either make the company or break it.

What Hallador got for its money was extraordinary. The acquisition included three underground coal mines in southwestern Indiana: Oaktown Mine 1 and Oaktown Mine 2 in Knox County, and the Prosperity Mine near Petersburg in Pike County. The deal also came with two wash plants and two rail loading facilities, critical infrastructure for getting coal from the mine face to the customer. But the real prize was not the operating assets. It was the reserves.

The combined operation, including Sunrise Coal's existing reserves and the Vectren Fuels properties, created a complex with approximately 230 million tons of identified reserves, of which 161 million tons were controlled by Hallador. To put that in perspective, at production rates of six to seven million tons per year, these reserves represented decades of mining life. In an industry where competitors were going bankrupt, Hallador had just secured a reserve base that could sustain operations well into the 2040s.

There was a beautiful operational synergy embedded in the deal that most observers missed. The Vectren Fuels acquisition gave Hallador access to the Oaktown 2 mine portal, which was geographically adjacent to Sunrise Coal's War Eagle reserve. Without the acquisition, developing War Eagle independently would have required approximately 150 million dollars in capital expenditures for a new mine entrance, new infrastructure, and new permitting. With the acquisition, Hallador could access War Eagle through the existing Oaktown 2 portal, eliminating that entire capital burden. It was the kind of operational insight that only a mine operator would recognize, and it dramatically improved the economics of the combined enterprise.

The integration was not without challenges. Combining two coal mining operations involves harmonizing safety protocols, equipment maintenance schedules, labor practices, and customer relationships. Hallador had to absorb hundreds of new employees and blend corporate cultures that, while both rooted in Indiana coal mining, had developed different operating philosophies under different ownership. The Oaktown mines had been run as a utility subsidiary, with a cost structure and management philosophy shaped by regulated utility economics rather than competitive commodity markets. Sunrise Coal, by contrast, had been built from scratch by entrepreneurs who watched every dollar.

But the Bilsland team had credibility with the workforce. These were coal men managing coal men, not private equity operators or financial engineers imposing spreadsheet solutions from a corner office in Manhattan. Bilsland personally visited each mine in the weeks following the acquisition, meeting with shift supervisors, equipment operators, and safety officers. The message was consistent: we are keeping these mines open, we are keeping you employed, and we are going to run this operation more efficiently than it has ever been run before. In an industry where miners had watched one corporate owner after another abandon them, that message carried real weight.

The timing of the acquisition was significant. Hallador bought Vectren Fuels in 2014, just as the coal industry was entering its darkest chapter. Within eighteen months of the deal closing, Arch Coal and Peabody Energy would file for bankruptcy. Other coal companies were desperately trying to sell assets, and buyers were nowhere to be found. Hallador had executed its consolidation play at precisely the moment when the seller had maximum motivation to deal and the buyer faced minimal competition. Whether this timing was strategic genius or fortunate coincidence, the result was the same: Hallador had become a consolidator in an industry defined by consolidation, acquiring high-quality assets at a fraction of their replacement cost.

The deal also revealed something important about Bilsland's strategic philosophy. In a dying industry, there are two paths: you can be the consolidator or the consolidated. The companies that get consolidated are the ones that overleverage, lose customers, or simply run out of cash. The consolidators are the ones with patient capital, strong relationships, and the willingness to buy when everyone else is selling. Hallador had chosen its path, and the Vectren Fuels acquisition was the proof point.

VII. Navigating the Trough: Strategic Discipline in Coal's Dark Ages (2015-2020)

The years between 2015 and 2020 represent a period of quiet determination for Hallador Energy. There were no headline-grabbing deals, no dramatic pivots, and precious little attention from Wall Street. This was the coal industry's dark ages, and Hallador's primary strategic objective was simple: survive with the balance sheet intact.

While many coal companies during this period attempted diversification strategies, pivoting into natural gas, real estate, or other ventures in an effort to escape the stigma and declining economics of coal, Hallador largely stayed in its lane. The company focused on what it knew best: mining coal efficiently, maintaining its utility relationships, and keeping its cost structure competitive. It was a period defined not by bold moves but by the absence of mistakes.

The operational reality during these years was grinding. Natural gas prices, while no longer at the extreme lows of 2012, remained depressed enough to keep coal under intense competitive pressure. Utility customers were beginning to announce coal plant retirements with increasing frequency. Environmental regulations, particularly under the Obama administration's Clean Power Plan proposals, created additional uncertainty. Every quarter brought new questions about coal's future, and every earnings call required Hallador's management to explain why the company was not pivoting away from a fuel source that the market had largely written off.

Bilsland's response to these pressures was characteristically blunt. He argued, consistently and publicly, that coal was being prematurely dismissed. His thesis rested on several pillars: grid reliability required dispatchable baseload power that renewables and gas could not always provide; the installed base of coal plants represented hundreds of billions of dollars in infrastructure that utilities could not walk away from overnight; and the Illinois Basin's cost advantages meant that its coal would be among the last to be displaced, even in a declining market.

This was not a popular position. ESG-focused investors were divesting from coal. Banks were cutting off lending to coal companies. Even some of Hallador's competitors were publicly acknowledging that the industry's future was limited. But Bilsland's contrarian stance was rooted in operational reality, not wishful thinking. He knew his customers' plants, he knew their contracts, and he knew that many of them had no viable alternative to coal for the next decade or more.

The company's financial discipline during this period was notable. Hallador paid a modest quarterly dividend of four cents per share through 2019, which represented a signal to shareholders that the company remained cash-generative even in the worst market conditions. But in early 2020, as COVID-19 sent electricity demand plummeting and created existential uncertainty for coal producers, Hallador suspended its dividend. The decision was prudent. Many companies in similar positions waited too long to conserve cash and paid the price. Hallador's willingness to cut the dividend early, while painful for income-oriented shareholders, preserved the balance sheet flexibility that would prove essential in the years ahead.

Then came the pandemic.

The COVID-19 crisis of spring 2020 marked the absolute nadir. Electricity demand collapsed as the economy shut down. Factories went dark. Office buildings emptied. Industrial production halted. Mines were idled across the country.

Hallador's stock, which had been trading in the low single digits, fell to sixty cents per share in June 2020. Sixty cents. For a company with hundreds of millions of tons of coal reserves, multiple operating mines, and long-term utility contracts. The market was pricing Hallador for liquidation. It was the kind of price that implied not just that coal was dead but that Hallador specifically would not survive to see the other side of the crisis.

But within the misery of the COVID crash lay the seeds of what came next. The demand destruction of spring 2020 led to underinvestment in coal production capacity across the industry. Mines that were idled never reopened. Workers who were furloughed found jobs elsewhere and never came back. Equipment that was parked in storage began to rust. Rail contracts lapsed. Supply chains atrophied. The supply side of the coal market was permanently impaired, and when demand eventually recovered, there would be far less coal available to meet it.

This is a pattern that commodity investors recognize: the bust creates the conditions for the next boom. In oil, the dynamic is well understood. In coal, it was even more pronounced because the bust was not cyclical but structural. Investors were not just waiting out a price downturn; they were abandoning the industry permanently. No one was going to build a new coal mine when the market recovered. No one was going to train a new generation of coal miners. The capacity that was lost during COVID was gone forever. The stage was being set for a supply-demand imbalance that would generate extraordinary profits for the survivors.

VIII. Commodity Chaos & The Perfect Storm (2020-2023)

What happened to energy markets between 2020 and 2023 was so extreme, so unprecedented in its velocity and magnitude, that even seasoned commodity traders struggled to make sense of it. For Hallador Energy, it was the moment when years of patient survival transformed into something approaching vindication.

The snapback from COVID's demand destruction came faster than anyone expected. By the second half of 2020, electricity consumption was already recovering, driven by a combination of economic reopening, stimulus-fueled activity, and the growing electrification of heating, transportation, and industrial processes. But the supply side could not keep up. Coal mines that had been shut down during the pandemic could not simply be switched back on. Rehiring miners, restarting equipment, securing permits, rebuilding supply chains, all of it took time. And time was something the market did not have.

Then came 2021, and with it a series of events that turbocharged coal's unexpected resurgence. Natural gas prices, which had been depressed for the better part of a decade, began to rise sharply. A cold snap in February 2021 exposed the fragility of the Texas power grid and reminded utilities across the country that fuel diversity was not a luxury but a necessity. Suddenly, the coal plants that had been scheduled for retirement were being called back into service. The utilities that had been reducing their coal purchases were placing urgent orders.

And then, in February 2022, Russia invaded Ukraine. The geopolitical shock sent global energy markets into chaos. European natural gas prices exploded to levels that would have been considered impossible just two years earlier. Germany, which had bet heavily on Russian pipeline gas while simultaneously shutting down its nuclear plants, found itself scrambling for any available energy source. The Dutch TTF natural gas benchmark, Europe's primary gas pricing reference, spiked to the equivalent of more than fifty dollars per million BTU, a level roughly twenty-five times higher than U.S. gas prices had been just two years earlier.

While the United States was largely insulated from the direct impact of European gas prices, the ripple effects were profound. American LNG exports surged as European buyers bid aggressively for every available cargo, tightening domestic natural gas supply and pushing U.S. prices to their highest levels since the shale boom. Henry Hub natural gas prices more than tripled from their 2020 lows. Coal, which had been the fuel of last resort, suddenly became the fuel of necessity. Utilities that had been planning to close coal plants postponed retirements. Utilities that had reduced coal procurement were placing emergency orders.

For Hallador, the impact was transformative. Coal prices, which had been languishing in the low thirties per ton, surged. By 2022, the company's average realized coal price had risen to approximately forty-five dollars per ton. By 2023, it reached nearly fifty-nine dollars per ton, a level not seen in years. Revenue followed: the company generated roughly 362 million dollars in 2022 and then an extraordinary 635 million dollars in 2023, a record year that validated every contrarian bet Bilsland had made over the prior decade.

The cash generation was stunning. In 2023, Hallador reported record net income of 44.8 million dollars, or a dollar thirty-five per share, and adjusted EBITDA of 107 million dollars. For a company whose stock had been at sixty cents just three years earlier, these were almost surreal numbers. Operating cash flow reached 59.4 million dollars, providing the capital to reduce debt, invest in operations, and prepare for the next phase of the company's evolution.

But Bilsland, characteristically, did not get carried away. Rather than using the windfall to chase growth or reward shareholders with special dividends, Hallador's primary use of the cash was debt paydown. The company aggressively deleveraged, reducing its bank debt by more than fifty percent to 44 million dollars by the end of 2024. This was a conscious choice: in an industry where high leverage had killed company after company, Bilsland was determined to enter the next phase of Hallador's life with a clean balance sheet.

The commodity chaos of 2020 to 2023 also exposed a structural reality that had been obscured by years of cheap gas and coal pessimism: the American power grid needed more generation capacity than it had, and coal was one of the few sources that could provide reliable, dispatchable power at scale. Data centers, electric vehicles, reshoring of manufacturing, electrification of heating, all of these trends were driving electricity demand higher at a rate that renewable energy and gas alone could not meet. The narrative around coal was beginning to shift, if only slightly, from "how quickly will it die" to "how long do we actually need it."

The momentum continued into 2025. Hallador's third-quarter results showed revenue up forty percent year-over-year to 146.8 million dollars, with coal sales surging sixty-two percent and electric sales climbing twenty-nine percent. Net income for the quarter reached 23.9 million dollars. The company was demonstrating that its vertically integrated model could generate meaningful profits even as it transitioned away from pure coal mining.

Perhaps most significantly, the period saw Hallador secure approximately one billion dollars in forward energy, capacity, and coal sales through 2029. That forward book provided the kind of revenue visibility that coal companies rarely enjoy, and it gave Bilsland the confidence to pursue ambitious expansion plans. The company had gone from fighting for survival to planning for growth, a transition that few in the coal industry had managed to make.

For a company positioned as one of the last efficient coal producers in the Illinois Basin, the shift in both narrative and financial results was worth its weight in, well, coal.

IX. The Merom Power Plant Gambit (2022)

If the Vectren Fuels acquisition in 2014 was Hallador's coming-out party, the Merom Generating Station deal in 2022 was its masterpiece. It was the kind of transaction that makes business school case studies, not because of its complexity but because of its audacity and its strategic clarity.

The Merom Generating Station is a two-unit, 1,080-megawatt coal-fired power plant located in Sullivan County, Indiana, about fifty miles from Hallador's mining operations. Built in 1982, the plant had been owned and operated by Hoosier Energy Rural Electric Cooperative, which supplied power to eighteen member cooperatives across central and southern Indiana. For decades, Merom had been a reliable workhorse, providing baseload electricity to rural communities. But by the early 2020s, Hoosier Energy was under growing pressure to transition away from coal, both from its members, who increasingly wanted clean energy, and from regulators and environmental groups.

Hoosier Energy's dilemma was acute. Continuing to operate Merom was becoming politically and economically untenable. Several of its member cooperatives were pushing for cleaner energy sources, and the cooperative had already signed a power purchase agreement in May 2021 for 150 megawatts of solar capacity and 50 megawatts of battery storage, signaling its intention to transition away from coal. But simply shutting Merom down was enormously expensive: the decommissioning costs, environmental remediation, and lost generation capacity would have imposed a heavy burden on the cooperative's member utilities. And the plant still had years of useful life left. The asset retirement obligations alone were estimated at approximately 5.6 million dollars.

Hoosier needed someone to take Merom off its hands, and the universe of potential buyers for a coal-fired power plant in 2022 was, to put it charitably, thin. No utility wanted to add coal generation to its portfolio. Private equity firms were under pressure from their limited partners to avoid fossil fuel investments. Infrastructure funds were focused on renewables and transmission. The number of entities in the United States that would willingly acquire a coal-fired power plant in 2022 could probably be counted on one hand.

Enter Brent Bilsland with a proposition that was elegant in its simplicity. Hallador would acquire Merom for essentially zero cash. In return, Hallador would assume the decommissioning obligations and environmental responsibilities associated with the plant. The deal also included a three-and-a-half-year power purchase agreement with Hoosier Energy, under which the cooperative would purchase all of Merom's output through May 2023, then transition to buying twenty-two percent of energy output and thirty-two percent of capacity through 2025.

The announcement came on February 15, 2022, and the transaction was finalized on October 21 of the same year. Hallador valued the total arrangement at approximately 184.5 million dollars, though most of that figure reflected the present value of the power purchase agreement rather than a traditional purchase price.

Think about that deal structure for a moment. Hallador acquired over a gigawatt of generation capacity for zero cash. In an industry where building a new power plant of comparable size would cost well over a billion dollars, Hallador got one for free, albeit with environmental obligations attached. It was like getting a house for free because the previous owner did not want to pay property taxes. Except this house generated hundreds of millions of dollars in revenue.

The strategic logic was profound. By acquiring Merom, Hallador accomplished something that no other Illinois Basin coal producer had done: it became its own customer. The coal that Sunrise Coal mined in Knox County could be shipped to Merom in Sullivan County and converted into electricity, which could then be sold into the MISO market or through bilateral contracts with other utilities. In one transaction, Hallador had transformed from a company that sold a commodity into a company that sold a product. The margin captured in converting coal to electricity was dramatically higher than the margin on selling raw coal, and it gave Hallador control over its own destiny in a way that pure coal producers could only envy.

There was an additional dimension to the deal that often gets overlooked. By owning both the mine and the power plant, Hallador eliminated one of the most significant risks in the coal business: customer concentration. A coal company is only as strong as the utility contracts it holds. If a utility decides to retire a plant, switch fuels, or renegotiate terms, the coal supplier has very little leverage. But when you own the plant that burns your coal, the customer cannot walk away. You are, in a very literal sense, selling to yourself.

The operational challenges of running a power plant were not trivial. Hallador had no prior experience in power generation. Running a coal mine and running a power plant are fundamentally different businesses, even though they involve the same commodity. A coal mine is essentially a logistics and excavation operation: you dig rock out of the ground, process it, and put it on a train or a truck. A power plant is a precision engineering operation: you must maintain steam pressure, turbine speeds, emissions controls, and grid synchronization within tight tolerances, twenty-four hours a day, seven days a week. A mistake at a mine costs you production. A mistake at a power plant can cost lives.

Hallador needed to hire or retain specialized personnel, manage a complex regulatory environment involving both the EPA and FERC, maintain a 1,600-acre cooling reservoir called Turtle Creek, and navigate the intricacies of MISO's wholesale electricity market. MISO, the Midcontinent Independent System Operator, is the entity that manages the electrical grid across fifteen U.S. states and one Canadian province. Selling power into MISO requires understanding capacity auctions, energy pricing, transmission constraints, and reliability requirements that are a world away from the straightforward tonnage-and-price dynamics of coal sales.

But Bilsland approached the transition with the same methodical discipline that had characterized his coal operations. The company created a new subsidiary, Hallador Power Company, LLC, to house the generation assets, and retained experienced plant operators to manage day-to-day operations. The Merom workforce, many of whom had spent their entire careers at the plant, stayed on under the new ownership, providing the operational continuity that was essential to keeping a forty-year-old power plant running safely and efficiently.

The Merom deal also said something profound about end-game strategy in the coal industry. In a market where coal's share of electricity generation is shrinking, the companies that survive will be the ones that control as much of the value chain as possible. Owning the mine gives you control over production costs. Owning the plant gives you control over revenue. Owning both gives you the ability to optimize across the entire chain, adjusting production levels, maintenance schedules, and market timing to maximize cash flow. It is the difference between being a price-taker and being a business owner.

There is an analogy from another struggling industry that helps illustrate the logic. When movie theater chains were facing extinction from streaming, the smartest operators did not just run theaters. They started producing their own content, operating their own concession supply chains, and building premium experiences that streaming could not replicate. They went from being distribution endpoints to vertically integrated entertainment companies. Hallador did the same thing in coal: it went from being a commodity supplier at the mercy of its customers to a vertically integrated energy company that controls every link in the chain from the coal face to the electrical grid.

For investors watching from the sidelines, the Merom acquisition was either a stroke of genius or the last act of a company going down with the ship. But the numbers that followed strongly suggested the former. The company's stock, which had been languishing in the single digits, began a sustained climb that would eventually take it above twenty dollars per share, a validation that the market was beginning to see Hallador not as a coal miner headed for oblivion but as a power company with a viable strategy for the next decade.

X. The IPP Transformation & Capital Strategy (2023-Present)

The years following the Merom acquisition marked Hallador's most consequential transformation. The company was no longer a coal miner that happened to own a power plant. It was becoming a vertically integrated independent power producer that happened to mine its own fuel.

This distinction matters enormously. Coal mining companies trade at terminal value multiples. Investors look at a coal miner and see a depleting asset base, environmental liabilities, and a customer base that is shrinking by the year. Independent power producers, by contrast, trade at multiples that reflect their contracted cash flows, their capacity value to the grid, and their optionality to add new generation sources. By repositioning itself as an IPP, Hallador was inviting the market to revalue the same assets through a fundamentally different lens.

In 2024, the company made a deliberate decision that crystallized this transformation. Hallador reduced coal production by approximately forty percent, pulling back from higher-cost reserves and focusing mining activity on the lowest-cost, most accessible seams. This was counterintuitive: at a time when coal prices were still strong, why would you produce less? The answer was that Hallador was optimizing not for coal revenue but for power generation margins. The coal it mined was increasingly consumed internally at Merom, where it generated higher-value electricity rather than being sold on the open market at commodity prices.

Revenue predictably dropped in 2024 to 404 million dollars, down from the record 635 million the prior year. But this decline was by design, not distress. The company used the year to reduce bank debt by more than half and to invest in the infrastructure needed for the next phase of its evolution.

That next phase arrived with remarkable speed. In January 2025, Hallador announced that it had signed an exclusive commitment agreement with a global data center developer for long-term energy supply. The deal included up to five million dollars in payments to Hallador during the negotiation period alone. Data centers, driven by the insatiable electricity demands of artificial intelligence training and cloud computing, had become the hottest growth market in the power generation sector. Here was Hallador, a coal company from Indiana, signing deals with the same kinds of technology customers that were lining up to buy power from nuclear plants and solar farms.

The data center connection was not as improbable as it might seem. Data centers need three things from their power source: reliability, capacity, and speed. They need power that is available twenty-four hours a day, seven days a week, regardless of weather conditions. A single modern AI training cluster can consume as much electricity as a small city, and even a brief power interruption can destroy millions of dollars worth of computation. They need lots of capacity, often hundreds of megawatts for a single facility. And they need it fast, because the race to build AI infrastructure was creating a capacity crunch that existing clean energy sources could not resolve quickly enough.

Consider the math: a large language model training run might require 50 to 100 megawatts of continuous power for months at a time. The major hyperscalers, companies like Microsoft, Google, Amazon, and Meta, were collectively seeking gigawatts of new power capacity. Solar and wind could provide some of this, but their intermittency was a problem for facilities that needed power around the clock. Nuclear was attractive but took a decade to build. Natural gas was the obvious bridge fuel, but permitting and pipeline constraints were creating bottlenecks. In this environment, any existing power plant with significant dispatchable capacity, available grid interconnection, and room for expansion became immensely valuable. Merom's 1,080 megawatts of dispatchable capacity, located in a region with available land, water resources from the Turtle Creek Reservoir, and existing high-voltage transmission infrastructure, was exactly the kind of asset that data center developers were seeking.

Then in December 2025, Hallador filed an Expedited Resource Addition Study application, known as an ERAS, with MISO, accompanied by a thirteen-million-dollar deposit, for the development of up to 515 megawatts of natural gas generation capacity adjacent to the Merom site. This was the clearest signal yet that Hallador was planning for a future beyond coal. The natural gas expansion would allow the company to continue serving its power customers even as coal generation eventually wound down, transforming Merom from a coal-only site into a multi-fuel energy campus.

In January 2026, the company priced a fifty-million-dollar public offering of common stock at eighteen dollars per share. For a stock that had been at sixty cents less than six years earlier, this was a stunning validation of the transformation strategy. The proceeds were earmarked for general corporate purposes, including funding the natural gas generation expansion. Hallador had also utilized an at-the-market equity program to raise up to 100 million dollars, which was ended without penalties when the public offering was completed. The company's market capitalization approached 880 million dollars by early 2026.

The capital allocation strategy has evolved significantly from Hallador's earlier years. Instead of paying dividends, which were suspended in 2020 and have not been reinstated, the company has prioritized debt reduction, operational investment, and growth capital for the natural gas expansion. This represents a conscious bet that the value created by the IPP transformation will ultimately deliver greater returns to shareholders than dividend payments from a declining coal business.

Whether this bet proves correct depends on execution. Hallador must successfully navigate the MISO interconnection process, secure the permits and financing for gas generation, and convert its data center negotiations into binding long-term contracts. The company is essentially asking shareholders to trust that a coal management team can become a power generation management team. The track record of the Merom integration suggests this is plausible, but the scale of the natural gas expansion represents a meaningful step up in complexity.

XI. The Business Model & Competitive Position Today

As of early 2026, Hallador Energy operates a business model that is unique in the American energy landscape: a vertically integrated coal-to-power operation that is actively diversifying into natural gas generation while pursuing data center customers.

The company's operational footprint consists of two core businesses housed under a single corporate umbrella. Sunrise Coal, LLC, operates the mining side, with active underground mines at the Oaktown 1 and Oaktown 2 complexes in Knox County, Indiana, along with the Freelandville and Prosperity surface mining operations. The combined complex sits atop reserves that provide decades of mining life at current production rates. Hallador Power Company, LLC, operates the Merom Generating Station, converting Sunrise Coal's output into electricity that is sold into the MISO wholesale market and through bilateral contracts.

The customer base has undergone a fundamental shift since the Merom acquisition. Whereas Hallador once sold coal to a portfolio of thirteen utility customers, the company now sells an increasing share of its output to itself, consuming it at Merom to generate electricity. The remaining coal sales go to external utility customers under contracts that typically span multiple years. The company announced in late 2025 that it had secured approximately one billion dollars in forward energy, capacity, and coal sales through 2029. This forward book provides significant revenue visibility, a rarity in the coal industry where spot market exposure can create enormous earnings volatility.

The cost structure advantages that have defined Hallador since its earliest days remain intact. Room-and-pillar mining, while less productive per unit than longwall mining, requires lower capital investment and offers greater flexibility to adjust production levels in response to market conditions. The proximity of the Oaktown complex to the Merom plant reduces transportation costs, one of the most significant variable expenses in the coal business. And the decades of reserve life mean that Hallador is not facing the mine depletion issues that have plagued Appalachian producers.

The regulatory compliance story is worth dwelling on because it functions as a genuine competitive advantage. The Merom plant is equipped with modern emissions control equipment, including scrubbers for sulfur dioxide and selective catalytic reduction systems for nitrogen oxide. These environmental controls represent hundreds of millions of dollars in sunk capital that would be prohibitively expensive for a new entrant to replicate. The fact that these systems are already installed and operational means that Hallador can burn high-sulfur Illinois Basin coal while meeting all current federal and state emissions standards. New coal plants are essentially impossible to build in the United States today, which means that Merom's existing permits and compliance infrastructure represent a form of irreplaceable strategic asset.

The cash generation model has become more predictable with the shift to power generation. Coal mining revenues are inherently volatile, driven by commodity prices, contract resets, and production variability. Power generation revenues, by contrast, include capacity payments from MISO that provide a baseline of income regardless of how much electricity is actually generated. Energy sales into the MISO market add variable revenue that correlates with electricity prices, and bilateral contracts provide additional stability. The blended revenue stream from coal sales and power generation is smoother and more predictable than coal alone, which supports a higher-quality earnings profile.

For investors tracking Hallador's ongoing performance, two key performance indicators stand out above all others. First, the realized price per megawatt-hour of electricity sold from Merom, which captures the company's ability to monetize its vertical integration through power generation margins. Second, the contracted forward revenue book, which indicates the visibility and durability of future cash flows. These two metrics, more than any headline production number or coal price, will determine whether Hallador's transformation succeeds or whether the company reverts to being valued as a terminal coal asset.

XII. Porter's Five Forces Analysis

Looking at Hallador through Michael Porter's competitive framework reveals an industry that is, by most conventional measures, terrible, but one in which Hallador has positioned itself in the least-worst spot available.

The threat of new entrants is effectively zero. Building a new coal mine in the United States today requires navigating a thicket of federal and state environmental permits that can take years to obtain, assuming they can be obtained at all. The capital costs are enormous, the political environment is hostile, and the long-term demand trajectory is declining. No rational investor is going to build a new coal mine in 2026. For Hallador, this means that every competitor who exits the industry permanently reduces supply without any offsetting new entry. The installed base is the installed base. It only shrinks.

The bargaining power of suppliers is relatively low. Coal mining requires labor, equipment, and materials, all of which are reasonably commoditized. While skilled miners are becoming harder to find as the workforce ages and younger workers choose other industries, Hallador's Indiana operations benefit from a legacy mining community where knowledge and skills are passed through generations. Equipment comes from a handful of major manufacturers, Joy Global now Komatsu Mining being the most prominent, but the market for used mining equipment is deep enough that Hallador has alternatives.

The bargaining power of buyers represents the most nuanced force in this analysis. Historically, coal producers have been at the mercy of their utility customers, who could play suppliers against each other and threaten to switch to natural gas if coal prices were not competitive. But Hallador's acquisition of Merom fundamentally changed this dynamic. When you are your own primary customer, buyer power becomes less relevant. For the remaining external coal sales, Hallador still faces negotiating pressure from utilities, but the dwindling number of Illinois Basin suppliers means that the balance has shifted somewhat. The utilities that still need coal have fewer places to buy it.

The threat of substitutes is, undeniably, very high. Natural gas, solar, wind, and battery storage all compete with coal for electricity generation. Over any ten-year horizon, the trend favors these alternatives. But there is an important caveat: these substitutes are not perfect replacements for coal's specific attributes. Gas requires pipeline infrastructure that does not exist everywhere. Solar and wind are intermittent and require backup. Battery storage is still expensive at grid scale. For utilities that need dispatchable baseload power in the near term, coal remains a viable option, particularly when the coal plant is already built and paid for.

Competitive rivalry within the Illinois Basin is low in terms of the number of players but intense in terms of the stakes. Alliance Resource Partners is the dominant producer, with significantly larger scale than Hallador. Peabody Energy maintains its massive Bear Run surface mine in Sullivan County. Beyond these two, the field has thinned dramatically. Foresight Energy and Murray Energy are shadows of their former selves. The remaining competitors are fighting over a shrinking pie, but the pace of the shrinkage is slow enough that multiple players can coexist profitably, at least for the next decade.

Comparing Hallador to its closest peer, Alliance Resource Partners, is instructive. Alliance is the Illinois Basin's eight-hundred-pound gorilla, a master limited partnership with production capacity that dwarfs Hallador's. Alliance has opted for a different strategic path: remaining a pure coal producer and miner, returning cash to unitholders through distributions rather than pursuing vertical integration into power generation. Both strategies have merit. Alliance's approach generates higher current yields but leaves the company exposed to the same customer dependency risks that have always plagued coal miners. Hallador's approach sacrifices current income for strategic control and long-term optionality. In essence, Alliance is playing the dividend extraction game while Hallador is playing the transformation game. Time will tell which approach proves wiser, but the fact that both are generating positive cash flows in an industry that was supposed to be dead by now says something about the resilience of well-run operations in the Illinois Basin.

The conclusion from Porter's framework is clear: this is a structurally unattractive industry by almost every measure. But within that structure, Hallador has done everything possible to insulate itself from the worst forces. Its vertical integration reduces buyer power. The absence of new entrants protects pricing. And its cost position ensures it will be among the last to be forced out.

XIII. Hamilton's 7 Powers Framework Analysis

Hamilton Helmer's 7 Powers framework, designed to identify the sources of durable competitive advantage, yields some surprising insights when applied to a coal company.

Scale economies are moderate but meaningful. As one of the largest Illinois Basin producers, Hallador can spread its fixed costs, mine development expenses, equipment purchases, and administrative overhead, across a larger production base than smaller competitors. The Vectren Fuels acquisition in 2014 was explicitly designed to capture this advantage, roughly doubling production capacity and creating the scale needed to achieve lower per-ton costs. However, Alliance Resource Partners operates at a significantly larger scale, which limits how much advantage Hallador can claim from scale alone.

Network effects, as expected, are nonexistent in the coal business. Coal is a commodity. No one downloads an app because their friends are using it. No producer benefits from having more customers in the way that a platform business does. This is simply not a relevant source of power for Hallador, and never will be.

Counter-positioning is where Hallador's story gets interesting, and it may be the most important power the company possesses. Counter-positioning describes a situation where an entrant's business model is superior to the incumbent's, but the incumbent cannot adopt it because doing so would damage their existing business. In Hallador's case, the counter-positioning is inverted: the company stayed in coal while the rest of the investment world and much of the industry itself fled. Its willingness to remain committed to coal, to buy coal assets when others were selling, and to acquire a coal-fired power plant when utilities were desperate to divest, created an asymmetric opportunity. The incumbents, which in this context means the ESG-conscious utilities, institutional investors, and diversified energy companies, could not rationally hold onto coal assets because of the reputational and regulatory costs. Hallador faced no such constraints. It was already the coal company. There was no additional stigma to absorb.

Switching costs are medium and underappreciated. A utility that has configured its plant to burn a specific grade of coal, has rail infrastructure connecting it to a specific mine, and has trained its workforce on the specific handling characteristics of that coal does not switch suppliers casually. The testing, transportation reconfiguration, and operational adjustments involved in changing coal sources create friction that benefits incumbents like Hallador. The Merom vertical integration further strengthens this power: the plant is literally designed to burn Sunrise Coal's output.

Branding power is zero. Coal is a commodity. No one pays a premium for coal from a particular producer. This is, again, simply not a relevant source of competitive advantage in this industry.

Cornered resource is a genuine source of power for Hallador. The company controls some of the most accessible, lowest-cost coal reserves in the Illinois Basin, with geological characteristics, seam thickness, overburden depth, and proximity to transportation infrastructure, that cannot be replicated. These reserves are located near both the mining workforce and the Merom plant, creating a geographic clustering of assets that would be nearly impossible for a new entrant to assemble. Additionally, the Merom plant itself, with its existing permits, emissions control equipment, and grid interconnection, is a cornered resource. You cannot build another one.

Process power is moderate. Hallador has developed operational expertise in Illinois Basin coal mining over two decades, knowledge of local geology, safety practices, labor management, and cost optimization, that constitutes institutional knowledge. This is not the kind of dramatic process advantage that a Toyota or a TSMC possesses, but in an industry where small differences in cost per ton can determine profitability, it matters.

The key insight from the 7 Powers analysis is that Hallador's durable advantages come primarily from counter-positioning and cornered resource. The company's willingness to be the last one standing in a despised industry, combined with its control over geological assets and generation infrastructure that cannot be replicated, creates a defensible position that is far more robust than the typical coal company's.

This is fundamentally a time arbitrage play: Hallador is betting that coal will be needed for longer than the market expects, and it has positioned itself to capture the value from that gap between perception and reality. The concept of time arbitrage is worth emphasizing because it applies far beyond coal. In any industry undergoing structural decline, there is a difference between the pace at which the market prices the decline and the pace at which the decline actually occurs. When the market prices the decline faster than reality, the gap creates opportunity. When the market prices it slower, the gap creates risk. Hallador's entire strategy is predicated on the belief that the market has consistently overestimated how quickly coal would disappear from the American energy mix. So far, that belief has been vindicated. The question is whether the gap between market perception and reality will persist long enough for Hallador to complete its transformation into a gas-fired power producer.

XIV. The Bull Case & Bear Case

The investment case for Hallador Energy is genuinely polarized, with thoughtful arguments on both sides that reflect fundamental disagreements about energy policy, grid reliability, and the pace of the energy transition.

The bull case begins with scarcity, and it is a powerful one. Hallador is one of a shrinking number of pure-play coal producers with meaningful production capacity. As competitors exit the industry, either through bankruptcy, retirement, or strategic pivots, the remaining supply becomes increasingly valuable. This is the "last man standing" thesis, and it has historical precedent in other declining industries. When the number of domestic steel producers shrank in the 1990s and 2000s, the survivors, companies like Nucor and Steel Dynamics, enjoyed years of pricing power and outsized returns precisely because they were the last ones left. Basic economics dictates that in a market with declining but nonzero demand and rapidly declining supply, the last producers enjoy pricing power that is disproportionate to their market position.

The vertical integration with Merom adds a layer of margin stability that few coal companies have ever achieved. By converting coal to electricity, Hallador captures value at multiple points in the supply chain and insulates itself from the worst of coal commodity price volatility. The company effectively sets its own coal transfer price, optimizing across the mine and plant to maximize consolidated cash flow.

The data center opportunity represents genuine upside that is not fully reflected in current valuations. If Hallador can convert its commitment agreement into a binding long-term power purchase agreement with a major data center developer, the resulting contracted cash flows could fundamentally alter the company's risk profile. Data centers need reliable, dispatchable power, and Merom's 1,080 megawatts of capacity is exactly the kind of asset they are competing for.

The natural gas expansion, if successfully executed, provides a bridge to a post-coal future. The 515 megawatts of gas generation capacity that Hallador has applied for would transform the Merom site into a multi-fuel energy campus, allowing the company to continue serving its power customers even as coal generation eventually winds down. This optionality is valuable and often underappreciated by analysts who view Hallador through a coal-only lens.

Finally, the balance sheet is clean. With bank debt reduced to 44 million dollars and a recent fifty-million-dollar equity raise, Hallador has the financial flexibility to pursue its strategic plan without the leverage constraints that have historically destroyed coal companies.

Now for the other side of the ledger.

The bear case is equally compelling and begins with the most fundamental objection: coal is a terminal decline industry. The question is not whether coal will eventually be phased out of U.S. electricity generation but when. Every year, the share of coal in the generation mix declines. Every year, more coal plants are retired. The trajectory is clear, and no amount of contrarian positioning changes the underlying trend.

Regulatory risk looms large and is perhaps the most unpredictable variable in the entire analysis. While the current administration has signaled a more favorable stance toward coal, federal energy policy is subject to reversal with every election cycle. The EPA under the Biden administration had proposed rules requiring carbon capture and storage for coal plants operating beyond 2039, technology that would need to run at ninety percent efficiency, with compliance beginning in 2032. While the current administration has moved to roll back or delay these rules, no investor should assume that future administrations will maintain the same posture. The regulatory pendulum swings with every election, and a coal plant with a forty-year operating life will see many administrations come and go. State-level renewable energy mandates and regional greenhouse gas regulations add additional layers of risk that exist independently of federal policy.

Customer concentration is a structural vulnerability. The Merom plant sells power into the MISO market and through bilateral contracts, but the economics depend heavily on capacity payments and energy prices that are ultimately determined by factors outside Hallador's control. A prolonged period of low electricity prices, driven by renewable energy buildout or reduced demand growth, could compress margins significantly.

Stranded asset risk is real for both the coal reserves and the Merom plant. If coal generation is retired faster than expected, Hallador's reserves become worthless and the Merom decommissioning obligations become a pure liability with no offsetting revenue. The company's entire strategy is a bet on the timing of the energy transition, and bets on timing are inherently risky.

ESG stigma continues to limit Hallador's investor base and capital market access. Many institutional investors are prohibited by mandate from holding coal stocks. Lending institutions are reducing their exposure to fossil fuels. This constrained capital market access increases the company's cost of capital and limits its strategic options.

And natural gas and renewables are becoming structurally cheaper. Solar-plus-storage, in particular, is approaching cost parity with coal generation in many markets. As battery technology improves and costs decline, the economic case for maintaining coal generation weakens year by year. Each price decline in renewables and storage shortens the runway that Hallador's bull case depends on.

There is also execution risk in the transformation itself. Hallador is attempting to simultaneously operate coal mines, run a power plant, develop natural gas generation capacity, and negotiate data center deals. Each of these activities requires different expertise, different regulatory relationships, and different capital allocation frameworks. The management team, while deeply experienced in coal, has limited track record in gas-fired generation and none in serving hyperscale data center customers. The gap between announcing a commitment agreement and signing a binding long-term power purchase agreement is wide, and many such negotiations have ended without a deal.

Finally, the company's equity dilution deserves attention. The January 2026 stock offering and the prior at-the-market program increased the share count at a time when the business model is still in transition. If the natural gas expansion takes longer or costs more than anticipated, shareholders who bought at eighteen dollars per share could find themselves in a position where the transformation premium evaporates before the transformation is complete.

XV. Lessons for Founders, Operators & Investors

Hallador Energy's two-decade journey offers a surprisingly rich set of lessons that extend far beyond the coal industry.

The lessons fall into five categories, each applicable far beyond the coal sector.