HNI Corporation: The Office Furniture Powerhouse You've Never Heard Of

I. Introduction and Episode Roadmap

Walk into any mid-size corporate office in America. Look around.

Sit in the conference room chair. Open a filing cabinet. Lean back at your desk. Run your hand along the edge of the workstation.

There is a remarkably good chance that the furniture surrounding you was manufactured by a company headquartered in a small Iowa river town of thirty thousand people. A company that just became the largest office furniture maker on the planet, with nearly six billion dollars in pro forma revenue. A company that most people, even seasoned investors, could not name.

That company is HNI Corporation.

Most people have never heard the name. That is by design.

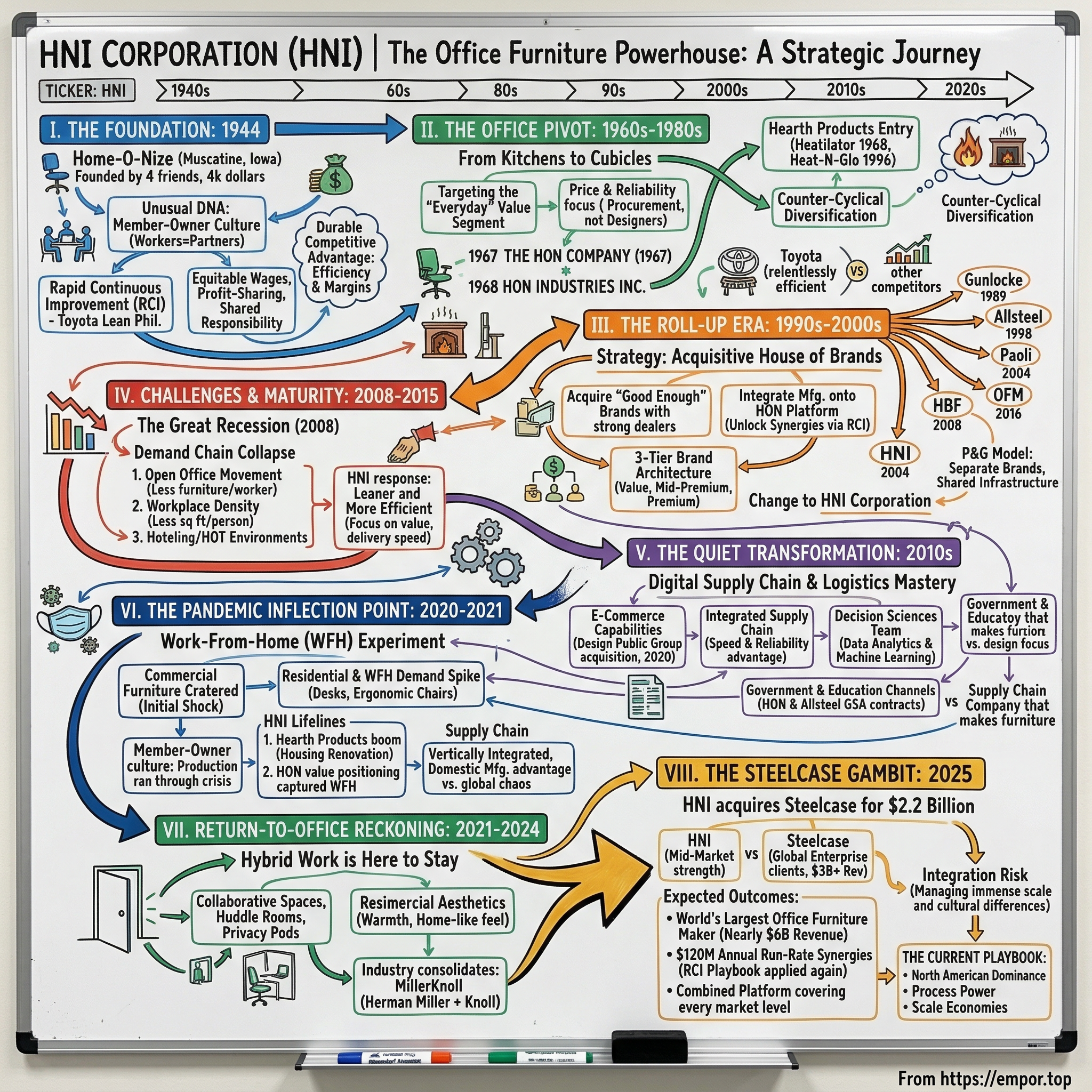

Here is the central mystery of this story: How did a scrappy manufacturer of steel kitchen cabinets, founded in 1944 by four friends pooling four thousand dollars, become the backbone of corporate America's offices? How did it swallow competitors three times its historical size? And why, despite its enormous footprint, does nobody outside the furniture industry know its name?

The answer involves a set of strategic choices that sound almost quaint in today's era of hyper-growth startups and quarterly earnings obsession. Vertical integration in an age of outsourcing. Employee ownership in an age of activist shareholders. Patient capital allocation in an age of SPAC deals and meme stocks. A relentless, almost boring focus on operational efficiency in an age that worships disruption. And then, just when the narrative seemed settled, two massive acquisitions that fundamentally reshaped the competitive landscape of an entire industry.

This is a story about the power of quiet competence. It is also a story about whether quiet competence is enough when the world of work is being reinvented in real time. The pandemic emptied offices. Hybrid work redefined how corporations think about physical space. Return-to-office mandates created a new wave of demand, but for different kinds of furniture than what came before. Through all of this, HNI made its biggest bets ever, acquiring Kimball International for $485 million in 2023 and then Steelcase for $2.2 billion in 2025. The Iowa furniture maker that grew up in the shadow of Herman Miller and Steelcase now stands above them all.

The question every investor should be asking is whether this is the beginning of a new era of dominance or the peak of a consolidation cycle in a structurally challenged industry.

This is a story that spans eight decades, four CEOs, dozens of acquisitions, a pandemic, and a fundamental rethinking of the relationship between work and physical space. To understand where HNI is going, we need to understand where it came from. And that means going back to the beginning, to a small town on the Mississippi River where four friends with four thousand dollars decided to build something lasting.

II. The Member-Owned Foundation: Understanding HNI's Unusual DNA

Before we dive into HNI's strategic evolution, a quick note on what makes this company unusual at the DNA level, because if you do not understand the member-owner culture, you will not understand any of the strategic decisions that follow.

It started, as many great American business stories do, with a Sunday afternoon conversation between friends who wanted to do something meaningful after the war.

In June 1943, in the middle of the biggest war the world had ever seen, engineer C. Maxwell Stanley and advertising executive Clement T. "Clem" Hanson sat together and hatched a plan. The war would end eventually. Soldiers would come home. They would need jobs. Stanley and Hanson envisioned a manufacturing enterprise in their corner of Iowa that would employ returning veterans and build something lasting. They recruited industrial designer H. Wood Miller and sheet metal manufacturer Albert F. Uchtorff. On January 6, 1944, the four men signed Articles of Incorporation for a company called Home-O-Nize. Each contributed one thousand dollars for ten shares of stock. Total starting capital: four thousand dollars.

The name was Clem Hanson's idea, and it tells you everything about the era. "Home" suggested the destination of their products. The suffix lent itself to advertising slogans like "Economize with Home-O-Nize" and "Modernize with Home-O-Nize." They set up their plant in Muscatine, Iowa, a town on the Mississippi River that had previously been known as the pearl button capital of the world, and waited for the war to end.

The first product rolled off the line in April 1947, and it was not what anyone expected. Rather than the kitchen cabinets and home freezers they had initially planned, the first manufactured item was an aluminum hood for installing commercial gas at farms and residences. They eventually did produce home freezers and steel kitchen cabinets, but what matters here is the instinct that was already present in the founding team: pragmatism over ideology. They built what the market needed, not what their original business plan said.

But the truly distinctive feature of Home-O-Nize was not its products. It was its philosophy about people. From the very beginning, Stanley, Hanson, and Miller believed that employees should be treated as partners, not hired hands. They instituted equitable wages, benefit programs, and profit-sharing arrangements that were unusual for a small Iowa manufacturer in the 1940s. This was not corporate altruism. It was a strategic conviction that workers who felt ownership in the enterprise would build better products, waste less material, and stay longer.

This conviction evolved into what HNI today calls its "member-owner" culture. Every employee at HNI is called a "member," a deliberate linguistic choice that signals shared responsibility and shared reward. Members participate in profit-sharing programs tied to individual and collective performance. They receive stock through the company's compensation plans. They are expected to think like owners because, in a meaningful sense, they are owners.

The cultural backbone of this system is something HNI calls Rapid Continuous Improvement, or RCI. Think of it as Toyota's lean manufacturing philosophy transplanted to the Mississippi River Valley. RCI operates on four principles: creating value, starting with the customer, engaging employees, and viewing problems as opportunities. Every member, from the factory floor to the executive suite, is expected to scrutinize processes, identify waste, and continuously refine operations. Under Stanley M. Howe, who joined Home-O-Nize in 1948 and rose to become president in 1964, this philosophy became almost fanatical. At its peak efficiency, the company could produce a desk every minute, a file cabinet every forty seconds, and a chair every twenty seconds.

Why does this matter for investors? Because it explains how HNI has consistently generated free cash flow and expanded margins in an industry that most analysts dismiss as commoditized. When your entire workforce is culturally programmed to find and eliminate waste, your cost structure becomes a durable competitive advantage, not just a line item to be cut during downturns. It also explains why HNI has been able to integrate acquisitions effectively. When you buy a company and overlay the RCI system onto its operations, you unlock efficiencies that the acquired company never achieved on its own.

Consider the contrast with how most publicly traded companies operate. The typical Fortune 500 company manages to a quarterly earnings cadence, making decisions that optimize for the next ninety days. Investments that take three years to pay off are hard to justify to Wall Street. Long-term manufacturing improvements that sacrifice near-term margins get punished by analysts. But at HNI, the member-owner philosophy creates a constituency, the workforce itself, that benefits from long-term value creation rather than short-term stock price movements. When HNI invested in the Mexico manufacturing facility in 2021, knowing it would take years to reach full efficiency, or when it maintained R&D spending through the pandemic downturn, these were decisions that a more short-term-oriented company might not have made. The culture does not make HNI immune to market pressures. It is still a publicly traded company that reports quarterly results. But it provides a degree of strategic patience that is genuinely rare among industrial companies of this size.

This playbook of cultural integration would prove decisive in every acquisition that followed, from the early brand additions of the 1990s all the way through to the transformational Steelcase deal. Understanding the member-owner culture is the key to understanding why HNI can buy companies and make them better. Without it, the rest of this story is just a list of transactions.

III. From Kitchens to Cubicles: The Office Furniture Pivot (1960s-1980s)

To understand the pivot that made Home-O-Nize into a furniture powerhouse, you have to understand what was happening in America in the 1950s.

Picture the landscape. The postwar economic boom was creating something the country had never seen at this scale: the modern corporate office. White-collar employment was exploding. Companies like IBM, General Electric, and the emerging conglomerates needed desks, chairs, filing cabinets, and storage systems for hundreds of thousands of new office workers. The firms that had dominated office furniture since the early twentieth century, companies like Steelcase in Grand Rapids, Michigan, and Herman Miller, also in Michigan, were thriving. But they focused on the premium end of the market, on design and innovation. Someone needed to serve the vast middle: the regional banks, the insurance companies, the government agencies, the school districts, and the thousands of small and mid-size businesses that needed functional, durable, affordable furniture without the design pedigree.

The leadership at Home-O-Nize saw this opportunity and made the pivotal strategic decision that would define the next seventy years. They shifted the company's focus from home products to standardized office furniture. The office products division became "The H-O-N Division," and by the early 1960s, it was growing fast. Annual sales passed five million dollars in 1961 and ten million by 1965. The company served about seventy-five wholesalers across the United States and even sold HON products through Sears, Roebuck and Co. for small businesses and home offices.

The naming conventions evolved to match the transformation. In 1967, the H-O-N Division officially became The HON Company. In 1968, Home-O-Nize changed its corporate name to HON INDUSTRIES Inc.

The kitchen cabinet maker from Iowa was gone. In its place stood a focused office furniture manufacturer with a clear strategic identity: be the low-cost, high-quality producer for the value segment of the market. This was not a timid strategic choice. It was a deliberate bet that the largest segment of the office furniture market, the everyday chairs and desks and filing cabinets that every business needs, would always be driven by price and reliability rather than design awards and magazine covers.

This was not a glamorous position. Herman Miller had Charles and Ray Eames designing iconic chairs. Steelcase was winning contracts with Fortune 500 companies for massive office buildouts. HON INDUSTRIES was making filing cabinets and basic desks for regional businesses and government offices. But Stanley Howe, who ran the company from 1964 through the late 1980s, understood something that the design-forward competitors did not fully appreciate: in office furniture, the vast majority of purchases are made by procurement departments, not designers. These buyers care about price, durability, lead times, and warranty coverage. They do not care about winning design awards. HON did not just accept this reality. It built its entire operational model around serving it.

Simultaneously, the company made a move that seemed tangential at the time but would prove strategically important for decades: it entered the hearth products business. The 1968 acquisition of Heatilator, a maker of prefabricated fireplaces, gave HON a second revenue stream in a completely different market. This diversification was deliberate. Office furniture demand is tied to commercial real estate cycles, which are notoriously volatile. Hearth products are tied to residential construction and renovation, which follows a different cycle. By straddling both, HON could smooth out the booms and busts that plagued pure-play office furniture companies. The hearth business would later be strengthened by the 1996 acquisition of Heat-N-Glo, forming what became Hearth Technologies, and eventually today's Hearth and Home Technologies division.

There is a useful analogy here. Think of the office furniture industry in the 1960s through 1980s as having the same structure as the automobile industry. Herman Miller was the BMW: design-forward, premium-priced, beloved by architects and tastemakers. Steelcase was the General Motors: dominant through scale and relationships with big corporate clients. HON was the Toyota: not as flashy, not as prestigious, but relentlessly efficient, fanatically focused on quality at a competitive price, and quietly gaining share year after year. Just as Toyota's manufacturing philosophy eventually reshaped the entire auto industry, HON's operational discipline would eventually give it the platform to transform office furniture through acquisition.

By the late 1980s, HON INDUSTRIES had established its identity. It was not the most innovative, the most prestigious, or the most talked-about company in office furniture. It was the most efficient. It could produce more furniture, faster and cheaper, than any competitor. It had a diversified revenue base. It had a culture of ownership and continuous improvement. And it was about to enter the most aggressive growth phase in its history.

IV. The Roll-Up Era: Acquiring the "Good Enough" Brands (1990s-2000s)

In March 1990, HON INDUSTRIES brought in Jack D. Michaels as president. Michaels came from Hussmann Corporation, a manufacturer of commercial refrigeration systems, and the choice was telling. The board did not hire a furniture industry insider or a design visionary. They hired a manufacturing executive who understood how to scale operations, manage acquisitions, and extract efficiency from industrial businesses. It was a signal of what HON INDUSTRIES intended to become: not a furniture company that occasionally acquired competitors, but an acquisition-driven industrial conglomerate that happened to make furniture. Michaels brought an acquisitor's instinct that would transform the company. Over his fourteen-year tenure as CEO, Michaels more than tripled revenues while increasing profits by more than four times and earnings per share by more than five times. His strategic insight was deceptively simple: the office furniture industry was fragmented, full of respected regional brands with strong dealer relationships but subscale manufacturing operations. If you could buy those brands, keep them intact to preserve their dealer networks and customer loyalty, and then overlay HON's manufacturing efficiency onto their operations, you could create a house of brands that covered every segment of the market.

The company had gone public on the New York Stock Exchange around 1971, giving it access to capital markets for acquisitions. But Michaels brought discipline to the process. He was not buying for revenue growth alone. He was buying for strategic positioning. Each acquisition had to meet specific criteria: the target needed a strong brand reputation in its segment, an established dealer network that complemented rather than duplicated HON's existing relationships, and a manufacturing operation that could be improved through the application of HON's operational methods. If a target met those criteria, the price was almost secondary, because Michaels knew that the operational improvements HON could deliver would generate returns that justified a fair premium. If a target did not meet those criteria, no price was low enough to justify the integration headaches.

The 1989 acquisition of The Gunlocke Company was an early signal of this strategy, and it illustrates the logic beautifully.

Gunlocke, based in Wayland, New York, had been making premium wood office furniture for over a century. The company held the extraordinary distinction of having supplied furniture to the Oval Office for over 124 years. This was not HON's traditional value market. Gunlocke gave the company a foothold in the premium segment, a way to serve the executive suites while HON served the cubicle farms. The two brands could share dealer networks without cannibalizing each other because they targeted completely different buyers.

The 1998 acquisition of Allsteel was even more significant. Allsteel, originally founded in 1912 as All-Steel Equipment Company, occupied the critical middle ground between HON's value positioning and Gunlocke's premium market. It had a strong reputation in commercial interiors, particularly for systems furniture and architectural products. With Allsteel, HON INDUSTRIES now had a three-tier brand architecture: HON for value, Allsteel for mid-premium, and Gunlocke for premium. Each brand maintained its own identity, its own sales force, and its own dealer relationships, but all shared manufacturing infrastructure and operational processes.

Meanwhile, Michaels doubled down on the hearth products diversification. The 1996 acquisition of Heat-N-Glo Fireplace Products was merged with the existing Heatilator operation to form Hearth Technologies, creating the nation's leading manufacturer of hearth products. Heat-N-Glo had pioneered direct-vent gas fireplace technology, which allowed homeowners to install fireplaces without traditional chimneys, dramatically expanding the addressable market for hearth products. The combination with Heatilator, which had been the market leader in prefabricated wood-burning fireplaces since 1927, created a powerhouse that covered every fuel type and installation method in the hearth industry. This was counter-cyclical diversification at its finest. When corporate real estate slumped, people were still buying homes and renovating their fireplaces.

By the early 2000s, the company had outgrown its original identity. In May 2004, it acknowledged the transformation that had already occurred by changing its name from HON INDUSTRIES to HNI Corporation. The old name created confusion between the parent company and The HON Company subsidiary, and the Honeywell ticker symbol was already "HON" on the NYSE. The new name, HNI, was clean and corporate, reflecting a portfolio company rather than a single-brand manufacturer.

The leadership succession at HNI is itself a notable feature of the company. Unlike many corporations where the CEO position attracts outsiders with transformational agendas, HNI has consistently promoted from within, choosing leaders who have spent decades absorbing the company's culture and operational philosophy.

Stan A. Askren succeeded Michaels as CEO in November 2004 and continued the acquisition strategy with his own emphasis on lean manufacturing. He had joined HNI in 1990 and spent over a decade absorbing the RCI culture before taking the top job. Under Askren, HNI acquired Paoli Inc. in 2004, adding wood case goods and seating, and HBF (Hickory Business Furniture) in 2008 for $75 million, adding premium upholstered seating and textiles. Later, OFM was acquired in 2016 for $34 million, adding another value-oriented brand.

The playbook was remarkably consistent across every acquisition: buy a respected brand with established dealer relationships, preserve the brand identity, integrate the manufacturing onto HNI's platform, and extract efficiency gains through RCI. It was not flashy. It was not disruptive. But over two decades, it built a portfolio of brands that collectively covered nearly every price point and product category in the North American office furniture market.

Think of it as a Procter and Gamble model applied to office furniture. P&G does not sell "P&G shampoo." It sells Head and Shoulders, Pantene, and Herbal Essences, each targeting a different customer segment with a distinct brand identity, all manufactured on the same production platforms and distributed through the same retail channels. HNI does the same thing with office furniture. The HON brand sits in the same relationship to Gunlocke that Tide sits to Downy: same parent, same operational infrastructure, completely different customer proposition.

This house-of-brands approach is exactly why most people have never heard of HNI Corporation. They know HON. They know Allsteel. They may know Gunlocke or HBF. But the company behind all of them stays in the background, which is precisely how HNI wants it. The parent brand is invisible because its visibility would add no value to the customer relationship. Procurement officers buying HON filing cabinets do not care who owns HON. Architects specifying HBF textiles do not care that the same company makes Heatilator fireplaces. The brand separation is not just organizational convention. It is a strategic choice that preserves the integrity of each brand's positioning while allowing the parent to extract operational synergies behind the scenes.

V. The Great Recession and Structural Challenges (2008-2015)

The financial crisis of 2008 hit the office furniture industry like a wrecking ball. To understand why, you need to understand the demand chain. Office furniture purchases are what economists call a "derivative demand." Nobody buys a desk because they want a desk. They buy a desk because they are hiring an employee who needs a place to work, or because they are leasing new office space, or because they are renovating an existing space. Each of those decisions is itself driven by broader economic conditions: employment growth, corporate profitability, commercial construction activity, and business confidence. When all of those drivers reverse simultaneously, as they did in 2008, furniture demand does not just decline. It evaporates.

Commercial real estate, the ultimate driver of furniture demand, experienced its worst downturn since the Great Depression. Companies froze capital spending. New office construction halted. Renovation projects were shelved indefinitely. The entire demand curve collapsed in a matter of months.

HNI was not immune. No office furniture company was.

Revenue dropped sharply, and the company responded with the playbook it had refined over decades: cost cuts, plant consolidations, and a relentless focus on protecting the core. But what made the Great Recession different from previous downturns was what happened during the recovery. Office furniture demand did not bounce back the way it had after previous recessions. Something structural was changing.

The first structural shift was the open office movement. Inspired by tech company campuses in Silicon Valley, corporate America began ripping out private offices and cubicle walls in favor of open floor plans with benching systems and shared workstations. This had a direct, measurable impact on furniture demand: open offices use significantly less furniture per employee. Fewer panels, fewer desks, fewer filing cabinets. The very trend that was reshaping how Americans worked was shrinking the addressable market for traditional office furniture.

The second structural shift was workplace density. Companies discovered they could fit more employees into less square footage. The metric that real estate departments began optimizing was square footage per employee, and it was going in one direction: down. From an average of 225 square feet per worker in the early 2000s, corporate America pushed toward 150 square feet and below. Less space per person meant less furniture per person.

The third shift, still nascent but gaining momentum, was the emergence of HOT (Hotel/Office/Touchdown) environments. These were flexible workspaces where employees did not have assigned desks. Instead, they checked in to whatever workstation was available, hotel-style. Think of it as the Airbnb model applied to office desks: no permanent assignment, just shared access to a pool of resources. The furniture implications were negative: if three employees share one desk across different days, that is two fewer desks to sell. Multiply that across a five-hundred-person office, and the furniture requirement drops by a third or more.

These three shifts, taken together, represented a genuine structural headwind for the industry. The office furniture market was not just experiencing a cyclical downturn. It was being reshaped by fundamental changes in how companies thought about workspace. The question for HNI and its competitors was how to respond: adapt the product line to the new reality, or hope that the pendulum would swing back.

For HNI, these structural headwinds paradoxically reinforced the value of its strategic positioning. In a market where buyers were more price-sensitive than ever, where procurement departments were squeezing every dollar out of furniture budgets, being the low-cost producer was the right place to be. The design-premium competitors, Herman Miller and Steelcase, had margins to protect and brand positioning that prevented them from competing aggressively on price. HNI could win deals on total cost of ownership, delivery speed, and operational reliability, the boring virtues that procurement departments actually care about.

The period from 2008 to 2015 was not a growth story. It was a survival-and-positioning story. HNI used the downturn to rationalize its manufacturing footprint, close underperforming plants, invest in automation, and deepen its cost advantages. The company emerged from this period leaner and more operationally efficient than ever.

There is a myth in the investment community that the Great Recession permanently impaired office furniture companies. The reality is more nuanced. The recession did not kill demand for office furniture. It accelerated a shift in what kind of furniture companies needed. The companies that suffered most were those locked into legacy product lines, selling the same cubicle systems and executive desk suites they had sold for decades. The companies that adapted, redesigning their product lines for open offices, smaller footprints, and collaborative work, found that the new demand, while different in character, was still substantial.

HNI was better positioned for this transition than its reputation suggested. Because it had always competed on value rather than design prestige, its customers were already the pragmatic buyers who cared most about functionality, durability, and price, exactly the attributes that mattered in the new austerity-driven office environment. The prestigious design competitions went to Herman Miller and Steelcase. The actual purchase orders went, in disproportionate numbers, to HNI.

But the strategic question that hung over the entire industry remained unresolved: Was the decline in furniture demand per employee cyclical, or was it the new normal? The answer would come from an unexpected direction.

VI. The Quiet Transformation: E-Commerce and Supply Chain Mastery (2010s)

While the headline story of office furniture in the 2010s was about shrinking demand and open office trends, something less visible but equally important was happening behind the scenes. The way office furniture was bought and sold was being fundamentally rewired. And this transformation would prove to be just as consequential for HNI's competitive position as the product and demand shifts that dominated industry headlines.

Traditionally, office furniture was a relationship business. A company needed new furniture, so it called its dealer. The dealer came to the office, measured the space, presented options from the manufacturers it represented, handled the order, coordinated delivery, and managed installation. This model worked beautifully for large projects, new office buildouts and major renovations, but it was cumbersome and expensive for smaller purchases. If a company needed twenty chairs or ten desks, the traditional dealer model was overkill.

The Amazon effect was transforming buyer expectations across every B2B category, including furniture. Corporate procurement departments wanted transparency on pricing, online configurators that let them spec products without a sales call, and delivery timelines measured in days, not weeks. Government buyers purchasing through GSA contracts wanted simplified ordering processes. Small businesses wanted to buy office furniture the same way they bought everything else: online.

HNI recognized this shift earlier than most of its competitors and invested accordingly. The company built dealer portal technology that streamlined the ordering process, allowing dealers to check inventory, configure products, and place orders through a single digital interface rather than through phone calls and faxes. It invested in digital configurators that allowed end customers to customize products online, choosing materials, finishes, and configurations through visual tools that rendered the finished product in three dimensions. It developed e-commerce capabilities, including the strategic acquisition of Design Public Group at the end of 2020, which brought a digitally native organization to accelerate HNI's online distribution. Design Public Group operated consumer-facing websites including designpublic.com and danishdesignstore.com, along with commercial and architecture-and-design channel capabilities. The acquisition was funded from cash on hand, a typical HNI move, and it signaled the company's recognition that e-commerce was not a threat to be feared but a channel to be mastered. HON products were already among the most widely available office furniture brands through office product distributors and online resellers, and the Design Public Group acquisition deepened that digital presence.

But the more consequential transformation was happening in the supply chain. HNI's vertical integration, its ability to control manufacturing rather than just assembly, became a decisive advantage in an era when speed and reliability mattered more than ever. When a customer ordered a product, HNI could manufacture it, configure it, and ship it from its own facilities. Competitors who relied on third-party manufacturers and component suppliers were at the mercy of longer, less predictable supply chains.

The company manages approximately four hundred suppliers and procures four hundred thousand different parts. To put that in perspective, a typical automobile has about thirty thousand parts. HNI's supply chain manages more than thirteen times that level of component diversity across its product portfolio. That level of complexity requires sophisticated logistics orchestration, and HNI invested in the systems to manage it. The company deployed inventory optimization software to reduce working capital tied up in raw materials and finished goods. It adopted Microsoft Azure cloud services for its technology infrastructure, enabling faster data processing and more agile application development. And it built an internal decision sciences team that used data analytics and machine learning to continuously improve operations, applying quantitative methods to everything from production scheduling to demand forecasting.

The company also invested in its government and education channels during this period. The HON Company and Allsteel both maintained GSA schedule contracts, making them approved vendors for federal furniture procurement. Fewer than nine hundred companies held GSA Multiple Award Schedule contracts for furniture and furnishings, making HON and Allsteel part of a relatively exclusive club. This was not high-growth work, but it was steady and predictable, providing a revenue floor that smoothed out the volatility of the commercial cycle.

HNI's Sagus division, encompassing Artco Bell Corporation for K-12 education furniture, Midwest Folding Products for cafeteria and folding tables, and LSI Corporation for laminate casework, became the second-largest source of educational furniture in North America, generating annual sales exceeding ninety million dollars. Schools and government agencies do not stop buying furniture during recessions. They may delay, but the institutional replacement cycle eventually catches up. This was the kind of boring, steady business that suited HNI's temperament perfectly.

The strategic clarity of the 2010s can be summarized in a single choice: HNI decided to be the supply chain company that happens to make furniture, rather than a furniture company that happens to have a supply chain. The industry was bifurcating into two lanes. In one lane, Herman Miller and Steelcase competed on design innovation, workplace research, and brand prestige, commanding premium prices from customers who valued aesthetics and wanted to make a statement with their office environment. In the other lane, HNI competed on operational excellence, cost efficiency, delivery speed, and reliability, serving the vast middle market that needed good furniture fast and at a fair price. Both lanes were viable. But HNI's lane was the bigger one, measured by unit volume and number of customers served.

VII. The Pandemic Inflection Point: COVID-19 and Work-From-Home (2020-2021)

March 2020.

Offices across America go dark. The lights are still on, but nobody is there.

Within weeks, the largest involuntary work-from-home experiment in history was underway, and every assumption about office furniture demand was suddenly up for debate.

For HNI, the initial shock was severe. Jeff Lorenger had been Chairman and CEO for less than a month when the pandemic hit. Imagine the scenario: you have just been given the top leadership role at a company that has been growing steadily for decades, and within weeks, the entire demand environment collapses. Every corporate customer freezes spending. Your products sit in warehouses. Your factories, which are calibrated for steady throughput, have no orders to fill.

First-quarter 2020 sales fell to $468.7 million, and the company recorded $32.7 million in goodwill and intangible asset impairment charges plus $3.4 million in direct COVID-related costs. The quarter ended with a net loss of $23.9 million, a stark reversal for a company accustomed to steady profitability. Management responded with crisis-mode discipline: suspended share repurchases, cut operating costs, reduced capital expenditures. But crucially, they did not panic. This is where the member-owner culture showed its value in crisis. At many companies, the first response to a demand collapse is mass layoffs, a move that destroys institutional knowledge and cripples the company's ability to respond when demand returns. HNI cut costs, but it preserved its workforce to the greatest extent possible, betting that the disruption was temporary and that the people and capabilities it retained would be needed when the market recovered. HNI entered the pandemic with low debt and liquidity equivalent to more than two years of free cash flow. The balance sheet had been built for exactly this kind of moment.

The pandemic created a strange bifurcation in furniture demand that nobody had anticipated. Residential furniture boomed as Americans trapped at home invested in their living spaces. Wayfair's stock price quadrupled. Restoration Hardware reported its best quarters ever. But commercial furniture cratered as corporations froze spending on offices that nobody was using. The two segments of the furniture market moved in opposite directions with a violence that had never been seen before.

HNI was primarily a commercial furniture company, which put it on the wrong side of this divide. But two factors partially offset the damage.

First, the hearth products division became a genuine lifeline. As Americans poured money into their homes, fireplace and stove sales surged. The housing renovation boom of 2020 and 2021 was a direct tailwind for Hearth and Home Technologies, validating decades of diversification strategy. The division that some analysts had dismissed as a strategic distraction was suddenly the star performer.

Second, and more unexpectedly, home office furniture demand spiked.

Millions of people working from home for the first time discovered that their kitchen tables and living room couches were not adequate substitutes for proper office furniture. After weeks of back pain and neck strain, they went shopping. They needed desks, ergonomic chairs, and storage solutions. HNI's HON brand, with its value positioning and wide availability through online retailers, was well positioned to capture this demand. The company pivoted portions of its production capacity to meet residential delivery requirements.

As the initial shock subsided and the economy began to reopen, HNI's supply chain advantages became starkly visible. The global supply chain chaos of 2020 and 2021 is well documented, but its impact on the furniture industry was particularly severe. Office furniture is a surprisingly complex product to manufacture. A single office chair might contain steel, aluminum, foam, textiles, plastic, and dozens of fasteners and mechanisms, all sourced from different suppliers, often in different countries. When shipping containers from Asia were delayed by months, when foam suppliers declared force majeure, when steel prices doubled, the entire manufacturing process ground to a halt for companies that depended on just-in-time global supply chains.

HNI's vertically integrated, predominantly domestic manufacturing base gave it a decisive edge. The company controlled more of its manufacturing processes in-house than its competitors. It sourced more of its materials domestically. It maintained higher inventory levels of critical components, a practice that would have been criticized as inefficient in normal times but proved invaluable during the crisis. The company could deliver products when competitors could not. By the third quarter of 2021, HNI's workplace furnishings delivery backlog had nearly doubled, growing ninety-nine percent year-over-year. Revenue grew twenty-six percent in that quarter. The company was not just recovering; it was gaining market share.

The pandemic also stress-tested the member-owner culture in a way that nothing else had. Manufacturing employees could not work from home. They were showing up to factories during a global health crisis, making chairs and desks and fireplaces while their counterparts at tech companies worked safely from their living rooms. HNI's profit-sharing model and ownership culture created a level of trust and commitment that kept production lines running when competitors faced walkouts and labor shortages. This is not a quantifiable advantage that appears on a balance sheet. But it was real, and it mattered.

One of the most underappreciated aspects of HNI's pandemic performance was its balance sheet discipline. The company entered the crisis with low debt and liquidity equivalent to more than two years of free cash flow. This was not an accident. It was the result of decades of conservative financial management rooted in the member-owner philosophy. When you view your employees as owners, you do not lever up the balance sheet to boost short-term returns at the expense of long-term stability. You maintain a fortress balance sheet so that you can survive downturns without devastating the people who depend on the company. This conservative posture, which may have cost HNI some returns during the bull market of the 2010s, proved invaluable when the crisis hit.

But the deeper question, the one that would define the company's next strategic chapter, was still unanswered. Was the pandemic a temporary disruption after which office life would return to normal? Or had it permanently altered the relationship between work and physical space? Jeff Lorenger, who had become CEO in 2018 and Chairman in February 2020, just weeks before the pandemic hit, had to make strategic decisions without knowing the answer. Lorenger's background was instructive: he had served as President of Allsteel from 2008 to 2014, then President of Contract Furniture, then President of Office Furniture, before ascending to the CEO role. He had spent his entire career inside HNI, absorbing the RCI culture and understanding the dealer network from the ground level. He was not an outsider brought in to shake things up. He was a product of the system, and he would use that system to make the most aggressive strategic moves in the company's history.

VIII. The Return-to-Office Reckoning (2021-2024)

The return-to-office story did not unfold the way anyone predicted. The narrative in 2021 was simple: vaccines roll out, offices reopen, demand recovers. CEOs across corporate America declared that the great work-from-home experiment was over and that productivity required physical presence. Jamie Dimon at JPMorgan, David Solomon at Goldman Sachs, and Elon Musk at Tesla all made high-profile demands for full-time office attendance. The furniture industry braced for a surge of demand that would mark the definitive post-pandemic recovery. Reality was much messier.

First came the false dawns.

Companies announced return-to-office dates, then postponed them as new COVID variants emerged. Corporate CEOs made bold declarations about everyone coming back five days a week, then quietly walked them back when employees resisted. By 2022, it was clear that the pre-pandemic world of universal five-day office attendance was not coming back. What replaced it was the hybrid work model, a compromise where employees came to the office two to four days per week and worked from home the rest.

For the office furniture industry, hybrid work created a paradox that confounded the simple narratives on both sides of the debate. The bears said offices were dying and furniture demand would never recover. The bulls said everyone would return to the office and demand would surge. Both were wrong. The reality was more interesting and more complex.

On one hand, companies were downsizing their real estate footprints. Smaller offices meant less total furniture. On the other hand, the furniture they did need was fundamentally different from what they had before. The old model of rows of identical cubicles with assigned seating was obsolete. The new model required collaborative spaces for team meetings and brainstorming. It needed huddle rooms for small group discussions. It demanded privacy pods for video calls, which had become the default mode of communication even for people in the same building. It required flexible furniture that could be reconfigured for different uses throughout the day.

And perhaps most importantly, it demanded "resimercial" aesthetics, a term coined by the industry to describe furniture that looked and felt more like a living room than a corporate office. The logic was simple: if the office had to compete with the comfort and convenience of working from home, it needed to feel more like home. Harsh fluorescent lighting gave way to warm ambient lighting. Utilitarian plastic chairs gave way to upholstered lounge seating. Laminate desks gave way to wood-topped tables with organic shapes. The office was being redesigned as a destination, a place that people wanted to come to rather than a place they were forced to attend.

This product evolution played directly to HNI's strengths in several ways. The company's multi-brand architecture meant it could offer solutions across the entire spectrum of needs. HON provided the value-oriented basics. Allsteel offered mid-premium collaborative furniture and architectural products. Beyond, another HNI brand, specialized in open-plan benching systems. HBF brought high-design upholstered seating and textiles. And the Kimball International brands, acquired in June 2023, added ancillary and hospitality-style furniture that was perfect for the resimercial trend.

Meanwhile, the industry was consolidating in response to these pressures. In 2021, Herman Miller acquired Knoll in a $1.8 billion deal, forming MillerKnoll with approximately $3.6 billion in combined annual sales. This was a seismic event. Two of the most prestigious names in American design furniture merged to create a design-forward powerhouse. It also sent a signal: the era of the standalone mid-size furniture company was ending. Scale was becoming essential for survival.

The Kimball International acquisition deserves particular attention because of what it reveals about Lorenger's strategic thinking. Announced on March 8, 2023, and closed on June 1, the deal valued Kimball at approximately $485 million in cash and stock. Kimball shareholders received nine dollars in cash plus 0.1301 shares of HNI stock per share, an eighty-one percent premium over Kimball's thirty-day volume-weighted average price. The pro forma combined company would generate approximately three billion dollars in revenue and three hundred five million dollars in EBITDA, including twenty-five million dollars of expected annual synergies.

What made the deal smart was not just the financial engineering. Kimball's brands filled specific gaps in HNI's portfolio. Kimball's strength in hospitality furniture aligned with the resimercial trend. Its healthcare furniture offering opened a relatively recession-resistant end market. And Kimball had been burdened by an unprofitable acquisition of its own, a company called Poppin, which made stylish but money-losing office supplies and furniture. HNI divested Poppin in the third quarter of 2023, a move estimated to increase annual operating profit by twenty million dollars while reducing revenue by only fifty-six million. Buying a company, stripping out the unprofitable part, and integrating the profitable core onto your own operational platform: this was the HNI acquisition playbook executed with surgical precision. It was also a signal to the market that Lorenger's team had the analytical rigor to distinguish between a company's structural value and its temporary problems, a skill that would prove essential when evaluating much larger targets.

The technology integration trend also shaped HNI's product development. Furniture was no longer just furniture. It was infrastructure. Desks needed integrated power and data connectivity. Conference tables required built-in charging stations and cable management. Collaborative spaces needed acoustic properties and booking system integration. This convergence of furniture and technology raised the bar for product development and manufacturing, favoring larger companies with the R&D budgets and engineering capabilities to deliver integrated solutions.

Activity-based working, known as ABW, became the dominant design philosophy for new office buildouts. Under ABW, an office is divided into zones designed for specific activities: focus work, collaboration, social interaction, learning, and rejuvenation. Each zone requires different furniture. The focus zone needs privacy screens and acoustic panels. The collaboration zone needs modular tables and writable surfaces. The social zone needs lounge seating and cafe-style furniture. The result is that a single office now requires a more diverse range of furniture products than ever before, playing directly to HNI's multi-brand portfolio strategy.

By 2024, the return-to-office trend was finally gaining real momentum. Calendar year 2025 brought the highest net absorption of office space since 2019. U.S. office leasing established a new post-pandemic high in the fourth quarter of 2025, with annual leasing activity up more than five percent for the full year. The smaller players were struggling with the capital requirements of product transitions and supply chain investments. HNI was gaining share in a market that was, at last, growing again. Legacy workplace furnishings organic net sales rose six percent in fiscal 2025, driven by strong performance across the contract furniture brands. Management described return-to-office as a "positive driver of activity," and the accelerating order trends and rising backlog levels suggested the momentum was building rather than fading.

IX. Portfolio Strategy and Brand Architecture Today

The question that every conglomerate must answer is whether the whole is worth more than the sum of its parts. For HNI, the answer depends on understanding why it keeps its brands separate rather than consolidating under a single umbrella.

The post-Steelcase brand portfolio is worth cataloging, because its sheer breadth is itself a competitive advantage. HON serves the value and volume channel. Allsteel targets mid-market contract furniture with a strength in architectural products. Beyond specializes in open-plan benching systems. Gunlocke serves the premium traditional wood furniture market. HBF and HBF Textiles provide high-end seating and textile solutions. Kimball covers ancillary and hospitality furniture. National serves multi-use and collaborative environments. And Steelcase, the crown jewel of the acquisition strategy, brings premium workplace solutions including architecture, furniture, and technology integration. In the hearth segment, Heatilator, Heat and Glo, Harman, Quadra-Fire, and Majestic cover every price point and fuel type in the fireplace market.

Consider this portfolio through the lens of a furniture dealer. A dealer in Dallas serves a dozen different customers: a regional bank needs value-oriented desks and filing, a law firm wants premium wood furniture for partner offices, a tech startup demands modern collaborative pieces with residential aesthetics, a hospital needs durable healthcare-grade seating. Under the old model, this dealer would need relationships with four or five different manufacturers. Under HNI's house-of-brands model, one parent company can serve all of these needs through distinct brand identities. HON handles the bank. Gunlocke serves the law firm. Kimball or Allsteel equips the tech startup. The dealer gets the efficiency of a single relationship with the breadth of multiple brands.

The efficiency gains are substantial. A dealer can attend one training program, access one ordering system, and manage one relationship while offering products across a dozen market segments.

This architecture also prevents the brand dilution that plagues companies that try to stretch a single name across too many market segments. A corporate procurement officer who knows HON as a reliable, affordable brand would be confused to see it on premium executive furniture. A designer who specifies HBF textiles for a flagship lobby would not want the same brand on commodity seating. The separation is not organizational vanity. It is strategic discipline.

Now, what about the other half of the business?

The Residential Building Products segment, operating as Hearth and Home Technologies, remains a meaningful component of HNI despite the company's dramatic expansion in workplace furnishings. The segment generates approximately six hundred million dollars in annual revenue, roughly a quarter of the legacy company's total, but its importance extends well beyond its revenue contribution. Hearth and Home Technologies operates at an eighteen-percent non-GAAP operating margin, significantly higher than the workplace furnishings segment's ten-and-a-half percent. It generates more than its proportional share of operating profits. And it continues to operate on a different cycle than office furniture, providing stability when commercial real estate weakens.

A distinctive feature of the hearth business is its own vertical integration. About one quarter of the segment's revenue comes from products and services sold through owned installing distributors under the Fireside Hearth and Home brand. This captive distribution channel gives HNI direct access to end consumers, control over the installation experience, and the ability to quickly adjust to material cost changes, a level of vertical integration that most furniture companies have never attempted.

The strategic debate within HNI about whether to keep or divest the hearth business has simmered for years among analysts and investors. The argument for divestiture is that the two businesses have nothing in common operationally and that a pure-play office furniture company would command a higher valuation multiple. The argument for keeping it is simpler but more compelling: it generates disproportionate profits at high margins, it operates on a different cycle, and it provides strategic optionality. In a world where office furniture demand can evaporate overnight, as the pandemic demonstrated, having a profitable, cash-generative business tied to the housing market is a genuine strategic asset. So far, management has sided with keeping it, and the hearth division's performance has validated that decision.

On the question of international presence, HNI has made a deliberate and somewhat contrarian choice: it has been systematically pulling back from international operations. The company sold its Lamex office furniture business in China and Hong Kong to Kokuyo Co. Ltd. for seventy-five million dollars in July 2022, recording a fifty-million-dollar pretax gain. It then sold HNI India to the same buyer, with the deal closing in April 2025. Rather than trying to compete globally, HNI has concentrated its resources on the North American market where its operational advantages, dealer relationships, and brand recognition are strongest. The one international expansion has been strategic: a 160,000-square-foot seating manufacturing facility in Saltillo, Mexico, opened in 2022, which provides cost-advantaged production capacity and tariff mitigation for the domestic market, not international sales.

This is not the strategy of a company trying to conquer the world. It is the strategy of a company trying to dominate its home market with ruthless efficiency. Whether that is wise depends on whether you believe North America remains a large enough opportunity to justify the focus. The Steelcase acquisition complicated this narrative somewhat, because Steelcase had global operations that HNI has now inherited. How HNI manages these international assets, whether it invests in them, maintains them, or eventually divests them as it did with its own China and India businesses, will reveal much about the company's evolving strategic vision. For now, the North American focus remains the core of the thesis.

X. The Current Playbook: How HNI Competes Today

Understanding how HNI competes today requires getting past the abstraction of "operational excellence" and into the concrete details of what that actually means on the factory floor and in the supply chain.

Start with a number: four hundred thousand. That is how many different parts HNI procures from approximately four hundred suppliers to manufacture its products. Managing that level of complexity, turning four hundred thousand parts into chairs, desks, filing systems, fireplaces, and dozens of other product categories while maintaining industry-leading margins, is not something you can replicate with a PowerPoint strategy deck. It is the accumulated result of decades of operational discipline, technology investment, and cultural commitment to continuous improvement.

The manufacturing footprint tells the operational story in physical terms.

Pre-Steelcase, HNI operated roughly forty locations across the United States and Asia. The company has continuously rationalized this footprint, closing underperforming facilities and consolidating production into its most efficient plants. The Hickory, North Carolina plant, inherited from the Kimball International acquisition, was announced for closure in 2024 with expected annual savings of approximately eleven million dollars. The Gunlocke plant in Wayland, New York, which had manufactured premium wood furniture for over 124 years, was announced for closure in January 2026, with production to be consolidated into other North American facilities. These are painful decisions, a 130-plus-year-old factory closing is not just an operational event but a community one, yet they reflect the relentless optimization that defines HNI's culture.

The pattern of rationalization deserves emphasis because it illustrates a broader principle. Many conglomerates acquire companies and leave their manufacturing footprints largely intact, either out of inertia or because the political cost of closing facilities is too high. HNI has consistently demonstrated the willingness to make painful decisions, closing inherited facilities and consolidating production into its most efficient plants. This is not asset-stripping. It is manufacturing optimization, and it is one of the primary mechanisms through which HNI delivers the synergies it promises when making acquisitions.

The Mexico facility deserves attention as a case study in strategic manufacturing. Announced in September 2021 and opened in early 2022, the Saltillo plant was HNI's first manufacturing operation in Mexico. With approximately 250 workers producing seating in a 160,000-square-foot facility, it was initially modest. But the economics are compelling: management expects the facility to yield twenty to twenty-five million dollars in net savings by the end of 2026, adding more than seventy cents to annual earnings per share. A subsequent $106 million expansion of an Arteaga plant demonstrated that Mexico would be a growing part of HNI's manufacturing strategy, providing cost advantages that supplement the domestic manufacturing base without abandoning it.

The member-owner culture continues to function as a competitive moat in ways that are difficult for outsiders to fully appreciate. In an industry where skilled manufacturing labor is scarce and turnover is expensive, HNI's profit-sharing programs, stock ownership opportunities, and cultural emphasis on member engagement create workforce stability that competitors struggle to match. This is not the kind of advantage that shows up in a quarterly earnings release. It shows up in lower training costs, higher productivity, better quality control, and the institutional knowledge that accumulates when people stay at a company for decades rather than cycling through every few years.

Technology investments have accelerated under Lorenger. HNI has deployed digital configurators that allow customers to spec products online, logistics software that optimizes delivery routes and timing, and data analytics platforms that continuously improve manufacturing processes. The company uses Ascend.io data pipelines and an internal decision sciences team to drive what it calls manufacturing digital transformation. The goal is not technology for its own sake but technology in service of the core competitive advantages: speed, cost, and reliability.

Speed to market has become an increasingly important competitive dimension. In the pre-pandemic era, long lead times for custom office furniture were accepted as normal. Companies planned office buildouts months in advance and tolerated delivery windows measured in weeks. The pandemic compressed these timelines. Companies making return-to-office decisions wanted furniture quickly. The rise of flexible work arrangements meant that office configurations changed more frequently, requiring faster furniture procurement cycles. HNI's manufacturing efficiency and domestic production base give it a structural speed advantage over competitors reliant on overseas manufacturing or complex supply chains.

On sustainability, HNI has made genuine progress. The company has achieved a seventy-nine-percent reduction in absolute combined Scope 1 and Scope 2 greenhouse gas emissions. Ten sites have achieved zero waste to landfill status, with two earning third-party TRUE certification. The company has eliminated expanded polystyrene foam packaging across Kimball International and Residential Building Products divisions and is actively identifying and eliminating PFAS from its products. In an era when corporate customers increasingly require sustainability certifications from their furniture suppliers, these are not feel-good metrics. They are table-stakes requirements for winning bids.

The dealer relationship model remains central to HNI's go-to-market strategy. With 247 authorized dealerships across North America, HNI sells through partners rather than going direct to end customers. This is a strategic choice, not a limitation. Dealers provide local market knowledge, installation services, ongoing customer relationships, and the consultative selling that large furniture projects require. By supporting dealers rather than competing with them, HNI maintains a distribution network that would cost billions to replicate and decades to build from scratch.

The financial trajectory tells the story of what all these competitive elements produce when combined. HNI achieved four consecutive years of double-digit non-GAAP earnings-per-share growth from fiscal 2022 through fiscal 2025. Non-GAAP operating margins expanded nearly nine hundred basis points over the same period. Fiscal 2025 revenue reached $2.8 billion, up over twelve percent year-over-year, with nearly six percent coming from organic growth. Even excluding the Steelcase acquisition, which closed in December 2025 and added $187.5 million in fourth-quarter revenue, the legacy business was performing at its highest level in years. The Steelcase contribution was modest for now, just one quarter of consolidated results, but the combined platform is positioned to generate approximately $5.8 billion in annual revenue going forward. Management has guided for combined adjusted EBITDA near $750 million and annual free cash flow of approximately $350 million when synergies are fully realized.

XI. The Steelcase Gambit and Porter's Five Forces

No analysis of HNI can be complete without addressing the single largest bet the company has ever made: the acquisition of Steelcase Inc. To appreciate the magnitude of this move, consider that Steelcase was not some struggling competitor that HNI picked up at a discount. Founded in 1912 in Grand Rapids, Michigan, Steelcase was one of the most storied names in American manufacturing, with 113 years of history, more than three billion dollars in annual revenue, and a global footprint spanning dozens of countries. It was, by most measures, a larger and more recognized company than HNI itself. The Iowa manufacturer was effectively acquiring the Michigan giant.

The deal came together quickly by the standards of a transaction this size.

Announced on August 3, 2025, and completed on December 10, 2025, the $2.2 billion cash-and-stock deal was transformational by any measure. Steelcase shareholders received $7.20 in cash plus 0.2192 shares of HNI stock per share. Post-deal, HNI shareholders owned approximately sixty-four percent of the combined company and Steelcase shareholders owned approximately thirty-six percent. The combined entity had pro forma revenue of $5.8 billion, pro forma adjusted EBITDA of approximately $745 million, and expected annual run-rate cost synergies of $120 million when fully mature.

To put this in context: HNI acquired a company with a 113-year history and more than three billion dollars in revenue, a company that had been one of its primary competitors for decades. The deal consolidated the "Big Three" of North American office furniture, Steelcase, Herman Miller (now MillerKnoll), and HNI, into a "Big Two," with HNI now the largest office furniture maker in the world. At approximately 5.8 times Steelcase's trailing twelve-month adjusted EBITDA, inclusive of the $120 million in expected synergies, the transaction valued Steelcase at a modest premium that HNI believed would be more than justified by the operational improvements it planned to deliver.

The strategic logic was compelling on multiple levels.

Steelcase's strength was in top-tier global enterprise clients, the Fortune 500 companies that buy furniture at massive scale. Legacy HNI's strength was in mid-tier contracts, the regional and mid-size companies that represent the bulk of the market. The combination created a full-spectrum platform capable of serving customers at every level. And the $120 million in expected synergies, projected to add $1.20 to non-GAAP diluted earnings per share when fully mature, represented the familiar HNI playbook of overlaying operational efficiency onto an acquired company's cost structure.

HNI's management emphasized that brand identities and dealer partnerships would be preserved, a commitment consistent with the house-of-brands strategy that had worked across every previous acquisition. Steelcase would remain Steelcase. Its brand, its dealer relationships, and its Grand Rapids heritage would be maintained. But behind the scenes, manufacturing, procurement, logistics, and back-office functions would be consolidated under HNI's operational platform. Steelcase's CEO and other senior executives departed post-acquisition, a typical pattern in deals of this scale.

The deal's timing was arguably as important as its structure. By acquiring Steelcase during an accelerating return-to-office cycle, HNI was positioning itself to ride the demand recovery with a dramatically larger platform. The $120 million in expected synergies, derived from overlapping functions in manufacturing, procurement, and corporate overhead, represented the straightforward cost savings that HNI's RCI culture excels at extracting. But the revenue synergies, while harder to quantify, were potentially even more significant. Steelcase's relationships with global enterprise clients could be cross-pollinated with HNI's mid-market brands. A Fortune 500 company that bought Steelcase for its headquarters could now source HON or Allsteel for its regional offices through the same parent relationship.

The risk, of course, is integration complexity. Absorbing a $3 billion company while still digesting the Kimball International acquisition is operationally demanding. The combined company now manages an enormous number of brands, manufacturing facilities across multiple countries, thousands of dealer relationships, and tens of thousands of employees. Cultural integration between Steelcase's more design-oriented, globally minded organization and HNI's operationally focused, North America-centric culture will require years of careful management. This is the risk that the market appears to be pricing in, with the stock trading well below analyst price targets.

This backdrop sets the stage for understanding HNI's competitive position through two essential strategic frameworks: Michael Porter's Five Forces, which analyzes the structural attractiveness of the industry, and Hamilton Helmer's Seven Powers, which identifies the specific sources of durable competitive advantage that individual companies possess.

Starting with Porter's Five Forces:

The threat of new entrants is low. Office furniture manufacturing is capital intensive, requiring significant investment in production facilities, tooling, and technology. Building a dealer network takes years. Establishing brand credibility with corporate procurement departments takes even longer. The barriers to entry are formidable, and the Steelcase acquisition raised them further by consolidating industry capacity.

Supplier bargaining power is moderate. HNI procures steel, textiles, wood, components, and hundreds of other materials from approximately four hundred suppliers. The company's scale, amplified by the Steelcase acquisition, provides meaningful purchasing leverage. But commodity price volatility, particularly in steel, remains a margin headwind that even scale cannot fully eliminate.

Buyer bargaining power is high, and this is the force that most shapes HNI's strategic decisions. Corporate procurement departments are sophisticated, price-sensitive negotiators. They use competitive bidding processes, demand volume discounts, and increasingly require sustainability certifications. Government buyers purchasing through GSA contracts operate under strict pricing frameworks. This buyer power is why HNI's cost leadership position is so valuable: in a market where buyers have significant negotiating leverage, the low-cost producer has the most room to compete on price while maintaining margins.

The threat of substitutes is moderate-to-high and rising. Remote work, coworking spaces, and alternative work arrangements all reduce the need for traditional office furniture. Smaller office footprints mean less furniture per company. Standing desks, convertible workstations, and modular systems can replace larger, more expensive traditional furniture. This is the structural risk that investors must weigh most carefully.

Competitive rivalry is high. Even after the Steelcase acquisition, HNI faces intense competition from MillerKnoll, the privately held Haworth, and numerous smaller domestic and international competitors, including imports from China and other low-cost manufacturing countries. The MillerKnoll combination, formed from Herman Miller's $1.8 billion acquisition of Knoll in 2021, generates approximately $3.6 billion in annual sales and remains a formidable competitor, particularly in the premium and design-forward segments. Haworth, as a private family-owned company headquartered in Holland, Michigan, competes aggressively in the mid-market without the quarterly earnings pressure that affects publicly traded competitors. And Chinese imports, while not yet dominant in the contract furniture segment due to the importance of local dealer relationships and customization, continue to exert pricing pressure on commodity products like basic seating and storage.

Hamilton Helmer's Seven Powers framework provides a complementary lens to Porter's forces, focusing on the specific sources of durable competitive advantage that a company possesses. Through this framework, HNI's competitive position reveals both strengths and limitations. The company's scale economies are strong, with manufacturing scale, distribution reach, and purchasing power creating genuine cost advantages. Process power is arguably its most important advantage, with the RCI culture, supply chain efficiency, vertical integration expertise, and decades of accumulated operational knowledge creating capabilities that competitors cannot easily replicate. Switching costs are moderate, driven by dealer relationships, product compatibility within existing installations, and the cost of qualifying new suppliers.

But network effects are essentially absent, as furniture is not a network business. Branding power is limited in the traditional consumer sense, as HNI's brands are well-known within the industry but invisible to end users. This is the "stealth brand" paradox: HNI's brands are trusted by the people who buy furniture but unknown to the people who sit in it. And counter-positioning is not applicable since HNI is the incumbent, not the challenger.

The absence of strong branding power in the consumer sense is notable. Nobody walks into a furniture store and asks for an HNI product. The individual brands have industry recognition, but none commands the kind of consumer premium that, say, Apple commands in consumer electronics or Nike commands in athletic wear. In the office furniture world, the closest equivalent to genuine brand power belongs to Herman Miller, whose Aeron chair became a cultural icon. HNI has no equivalent product, and the Steelcase brand, while highly respected among architects and facility managers, does not carry the same cultural cachet.

The key takeaway for investors is that HNI's competitive advantage is rooted in operational execution and cost leadership, not in brand prestige or network effects. In Helmer's framework, this makes HNI a "good business" built on process power and scale economies rather than a "great business" with winner-take-all dynamics. But here is the nuance that Helmer's framework can miss: in a commoditizing industry where most participants are "good businesses" at best, the company with the strongest process power wins the war of attrition. HNI does not need to be a great business in the abstract. It needs to be the best operator in its industry. And by that measure, eighty-two years of evidence suggests it is.

XII. Bull vs. Bear Case

The investment debate around HNI comes down to a single, deceptively simple question: what does the future of work look like?

If offices remain central to how knowledge work gets done, HNI's operational excellence can generate attractive returns in a growing market. If offices continue to shrink in importance, then even the best operator in the industry will struggle to deliver growth.

Start with the bull case, which centers on three pillars: the return-to-office cycle, the integration thesis, and the valuation gap.

The case begins with the return-to-office momentum that has built since 2023. Corporate America has moved decisively toward enforcing in-office attendance, with major employers mandating three to five days per week in the office. Calendar year 2025 saw the highest net absorption of office space since 2019. U.S. office leasing activity hit a new post-pandemic high. This is not a tentative recovery. It is a genuine demand cycle, and HNI, as the largest office furniture manufacturer in the world, is positioned to capture a disproportionate share.

The hybrid work thesis actually strengthens the bull case when examined closely. Hybrid work does not mean fewer offices. It means different offices. Companies are redesigning their workspaces to support collaboration, creativity, and employee experience, because the office must now justify its existence by offering something that working from home cannot. This office redesign cycle is a massive furniture replacement opportunity. Out go the rows of identical cubicles. In come collaborative zones, privacy pods, lounge seating, bookable conference rooms, and reconfigurable furniture systems. Every redesigned office is a new furniture order.

HNI's supply chain and cost advantages position it to gain market share during this cycle. Competitors who lack HNI's manufacturing scale, vertical integration, and operational efficiency will struggle to match its pricing and delivery speed. The Kimball International integration is delivering synergies on track. The Steelcase integration is underway with $120 million in annual run-rate synergies expected. Management targets workplace furnishings operating margins near twelve percent, a meaningful expansion from current levels.

The hearth products diversification provides ballast against cyclicality. Despite weakness in new home construction, the division grew six percent in fiscal 2025 and generated eighteen-percent operating margins. This business alone would be a respectable standalone company.

The member-owner culture represents patient capital in an impatient market. While competitors face pressure from activist investors to maximize short-term returns, HNI's member-ownership philosophy supports the kind of long-term investment in manufacturing capabilities, technology, and people that generates compounding advantages over time.

ESG trends favor domestic manufacturing. As corporate customers face increasing pressure to demonstrate supply chain sustainability and reduce carbon footprints, HNI's predominantly North American manufacturing base and documented environmental progress become competitive advantages. Buying from a domestic manufacturer with verified emissions reductions is easier to justify to an ESG committee than importing from overseas facilities with less transparent environmental practices.

The company's free cash flow generation has been consistently strong, with fiscal 2024 generating $173.8 million and fiscal 2025 operating cash flow reaching $276.3 million. Post-Steelcase, management targets combined annual free cash flow of approximately $350 million. This level of cash generation supports ongoing debt reduction from the acquisitions while funding continued investment in manufacturing capabilities and technology.

And the valuation appears attractive. With a forward price-to-earnings ratio around thirteen times and analyst price targets in the mid-sixty to mid-seventy dollar range, representing significant upside from the current stock price of approximately forty dollars, the market seems to be discounting the earnings power of the post-Steelcase combined entity. The company also pays a quarterly dividend of thirty-four cents per share, yielding approximately three and a third percent, providing income while investors wait for the integration thesis to play out.

The bear case is equally substantive and must be taken seriously. In the spirit of rigorous analysis, the bear arguments deserve the same depth as the bull case, because the risks are real and the stakes, given the leverage from two major acquisitions, are higher than at any point in HNI's history.

The structural decline thesis argues that the pandemic permanently reduced the demand for traditional office furniture. Remote work is not going away. Even with return-to-office mandates, the pre-pandemic world of five-day, assigned-desk office work is over. Companies are maintaining smaller office footprints. Square footage per employee continues to compress. The net effect is a smaller addressable market for office furniture.

Commoditization risk is real and arguably intensifying. In the value segment where HNI has historically competed, furniture is increasingly treated as a commodity by procurement departments. The differentiation that justifies premium pricing exists at the design end of the market, Herman Miller chairs, Knoll tables, but not in the filing cabinets and basic desks that represent a significant portion of HNI's volume. Import competition, particularly from China and other low-cost manufacturing countries, adds further pricing pressure.

The integration risk of two major acquisitions in rapid succession should not be underestimated. Kimball International was absorbed in 2023 and its synergies are still being realized. Steelcase, a company roughly the same size as legacy HNI, was absorbed in December 2025. Integrating two large acquisitions simultaneously while maintaining service quality, preserving dealer relationships, and managing cultural differences is extraordinarily difficult. The company has never attempted anything of this scale.