Hilton Worldwide: The Architecture of Hospitality Empire

I. Introduction & Episode Overview

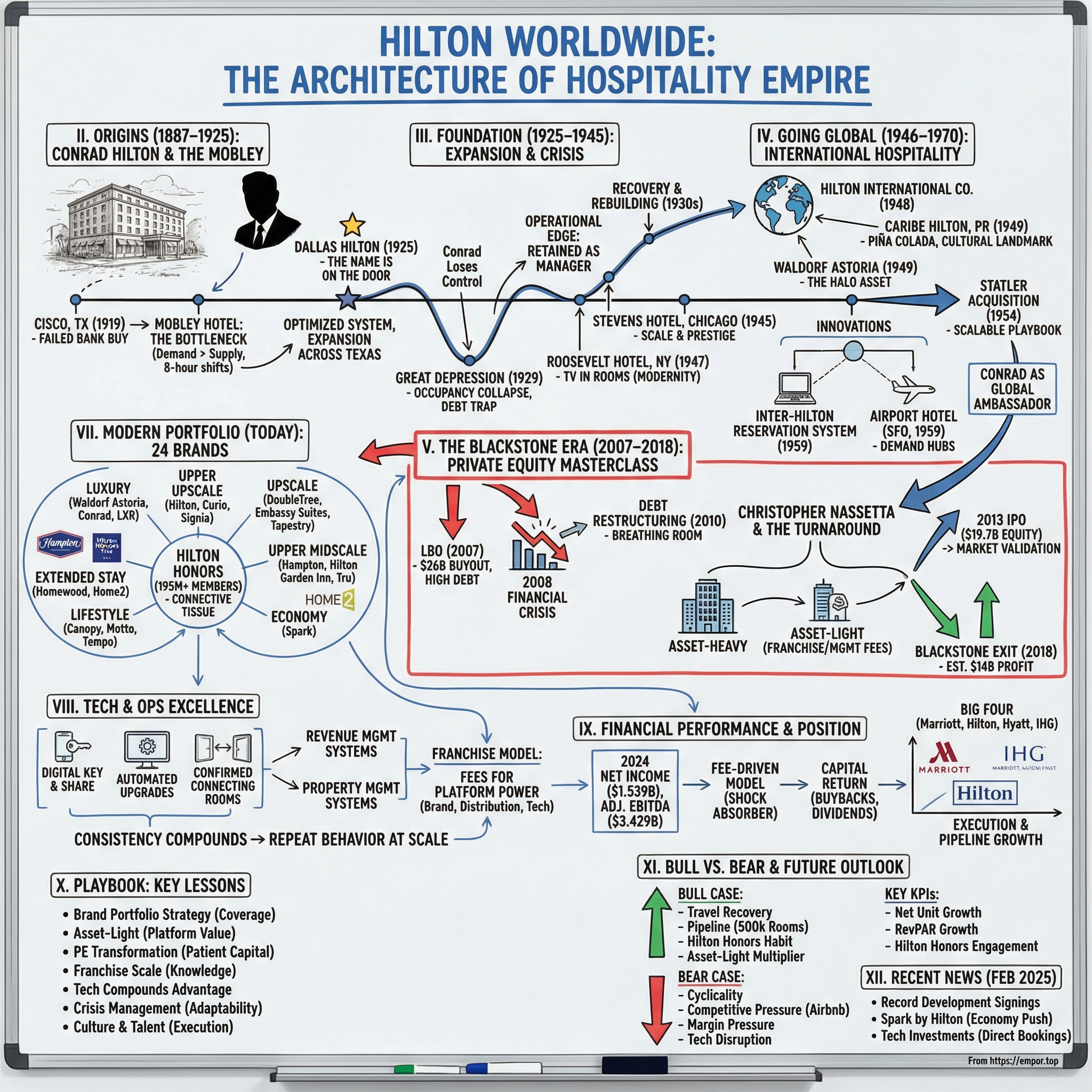

Picture this: It's 2018, and Stephen Schwarzman stands at a podium in Manhattan, announcing that Blackstone has just completed the sale of its final stake in Hilton Worldwide. The private equity firm has netted $14 billion in profit—the most lucrative private equity deal in history. Not bad for a company they nearly wrote off as dead during the 2008 financial crisis.

But here's what makes this story truly remarkable: The empire that generated those billions began a century earlier with a failed attempt to buy a bank in dusty Cisco, Texas. One man's pivot from banking to hospitality would create the blueprint for how the modern world travels, sleeps, and conducts business away from home. Today, Hilton stands as a leading global hospitality company with a portfolio of 24 world-class brands comprising more than 8,800 properties and nearly 1.3 million rooms, in 139 countries and territories. The 2024 numbers tell a story of remarkable scale: Net income was $1,539 million for the full year, with Adjusted EBITDA of $3,429 million, while revenue reached US$11.2 billion. But these numbers only hint at the deeper transformation.

The central question we're exploring isn't just how a company scales—plenty of businesses grow large. It's how Conrad Hilton's original insight about standardized hospitality excellence became the template that every major hotel company would eventually copy, how private equity engineering created billions in value from what seemed like a dying asset, and why, in an age of Airbnb and alternative lodging, the traditional hotel model keeps winning.

This is a story told in three acts: the creation of an industry standard, the financial engineering that unlocked hidden value, and the technology platform that powers modern travel. Along the way, we'll discover how buying distressed assets in Texas oil towns led to inventing the modern franchise model, how a nearly bankrupt company during the 2008 crisis became history's greatest private equity success, and why owning hotels turned out to be the worst way to run a hotel business.

II. Origins: Conrad Hilton & The Mobley Hotel (1887–1925)

The snow was falling hard on Christmas Day, 1887, when Mary Genevieve Laufersweiler gave birth to her second son in a small adobe house in San Antonio, Socorro County, New Mexico. She named him Conrad—Conrad Nicholson Hilton. His father, Augustus Halvorsen Hilton, a Norwegian immigrant who'd arrived in America as a child, ran the local general store and would later try his hand at everything from banking to politics. Young Conrad grew up watching his father's restless ambition, absorbing lessons about risk, leverage, and the art of the deal that would define his entire life. From 1912 to 1916, Hilton was a Republican representative in the first New Mexico Legislature, but became disillusioned with the "inside deals" of politics. It was a pattern that would repeat throughout his life: enter a field with grand ambitions, discover its limitations, then pivot to something bigger. At twenty-four, the youngest member of the newly formed state legislature, Conrad championed bills for better roads and schools, served on eight committees, and gave earnest speeches about progress. He soon grew frustrated with the bureaucracy, slowness, cheating, lying, and inside deals of politics.

But the real education was happening at home. Augustus had converted part of the family's general store into a makeshift hotel during hard times—a ten-room operation where Conrad and his siblings would greet trains, haul luggage, and learn the fundamental equation of hospitality: beds plus service equals profit. When Augustus died in a car accident in 1919 while Conrad was serving in France during World War I, the son returned home with a $5,000 inheritance and a burning ambition to become a banker. The pivotal moment came in 1919. Conrad Hilton enters the hotel business in Cisco, Texas. On his way to buy a bank, Hilton purchases The Mobley, a local hotel, instead. The story has been told a thousand times, but the details matter: Conrad had arrived in the dusty oil boomtown with $5,000 and dreams of empire-building through banking. The seller of the bank he'd targeted sent him a telegram at the last minute, raising the price from $75,000 to $80,000. Conrad's response? "He can keep his bank!"

Striding across from the train station, he encountered a two-story red brick building with a lobby packed with oil field workers waiting in line for rooms. Mobley rented the hotel's 40 beds in eight-hour blocks corresponding to shifts. The owner, Henry Mobley, was making money hand over fist but had caught oil fever himself—he wanted out of the "glorified boarding house" business to try his luck in the fields.

Conrad watched the chaos in that lobby—roughnecks sleeping in shifts, money changing hands every eight hours, a business that essentially operated at 300% occupancy—and saw something Henry Mobley couldn't: a system waiting to be born. Before long, they closed a $40,000 deal and Conrad Hilton had his first hotel. Within a year, he'd paid back his investors and discovered two principles that would guide his entire empire.

First was "digging for gold"—the relentless optimization of space. At the Mobley, he converted the dining room into additional guest rooms (there were plenty of restaurants in town), cut down the front desk to add a newsstand, and subdivided larger rooms. His 40-room hotel became 46 rooms without adding a single square foot.

Second was what he called "esprit de corps"—making every employee feel personally responsible for guest satisfaction. This wasn't just management philosophy; it was revolutionary thinking in an era when hotel workers were treated as interchangeable laborers. By 1925, Conrad was ready for his coming-out party. When Conrad Hilton opened the first hotel to bear the Hilton name in 1925, he aimed to operate the best hotel in Texas. For the building site Hilton chose the highest point in downtown Dallas. Ground was broken on July 25, 1924 and the building was completed just over one year later for a total cost of $1.36 million—Hilton's second most costly Texas highrise. The hotel officially opened on Thursday, August 6, 1925.

The Dallas Hilton wasn't just a hotel; it was a statement of intent. Hilton retained the prominent architectural firm of Lang and Witchell, one of the two most respected firms in Dallas, to design the new hotel. They designed the hotel as a 14-story, reinforced concrete and masonry structure in a simplified Sullivanesque style with symmetrical facades and Beaux Arts detailing. This was Conrad saying: I'm not just another hotelier. I'm building something permanent, something that will outlast us all.

III. Building the Foundation: Expansion & Innovation (1925–1945)

The roaring twenties were kind to Conrad Hilton. Hilton opened a new Texas hotel every year between 1925 and 1930 and by the onset of the Great Depression owned a total of eight. Each property was a laboratory for his evolving science of hospitality. In Abilene, he pioneered the idea of converting unused mezzanine space into revenue-generating shops. In Waco, he experimented with room configurations that would become industry standard. In El Paso, he built what locals called "the castle in the sky"—a towering testament to ambition that would nearly destroy him.

Then came October 29, 1929. Black Tuesday. The stock market collapsed, taking with it the dreams of millions—including, it seemed, Conrad Hilton's empire.

Despite efforts to advertise in national magazines, however, he was close to bankruptcy by 1931. Economic hardship lessened nationwide travel and forced him to close his El Paso hotel in 1933. He recovered, with the help of Shearn and William L. Moody, Jr., of Galveston and a number of other investors, and subsequently merged his hotels with the Moodys' operations to form the National Hotel Company, of which he was one-third owner and general manager.

The Depression years revealed Conrad's true genius: not in building hotels, but in saving them. He negotiated with creditors, convinced investors to hold on, and most importantly, maintained the fiction that everything was fine. Guests checking into a Hilton hotel in 1932 would never know the owner was borrowing money from bellhops to buy meals. Conrad later called these his "leather soup" years—when things got so tough, you'd boil leather and call it dinner. But Conrad's genius wasn't in surviving—it was in positioning for the recovery he knew would come. In 1943, he bought the Roosevelt Hotel in New York City. Then came his masterstrokes. In 1945, the great hotelier Conrad Hilton purchased The Stevens Hotel and renamed it as "The Conrad Hilton Hotel" a few years later, along with the Palmer House. At the time, the Stevens was the largest hotel in the world. The Stevens acquisition was particularly audacious—Conrad bought what had been the world's most expensive hotel failure for $7.35 million, a fraction of its $30 million construction cost. The 1947 Roosevelt Hotel: first hotel in the world to have televisions in its rooms. In 1947, The Roosevelt Hilton in New York City became the first hotel in the world to install televisions in guest rooms. This wasn't just about luxury—it was Conrad recognizing that the post-war traveler wanted connection, entertainment, and a window to the wider world from their room. The Roosevelt's general manager initially introduced televisions to 40 of the rooms, charging guests $3 per day extra for the service—a fortune at the time, but guests gladly paid.

Meanwhile, Conrad was quietly assembling something unprecedented. He formed the Hilton Hotels Corporation in 1946, and Hilton International Company in 1948. By creating two entities—one domestic, one international—he was laying the groundwork for what would become the first truly global hotel empire. This structural innovation would prove crucial: it allowed him to partner with local investors abroad while maintaining control of the domestic operation, a model every major hotel chain would eventually copy.

The culmination of this era was his boldest acquisition yet. Over the next decade, he expanded west to California and east to Chicago and New York, crowning his expansions with such acquisitions as the Stevens Hotel in Chicago (then the world's largest hotel; it was renamed the Conrad Hilton), and the fabled Waldorf-Astoria in New York City. The Stevens deal, in particular, showcased Conrad's evolution from hotel operator to financial engineer. He'd spent years buying the hotel's bonds at 20 cents on the dollar, positioning himself for the eventual purchase.

IV. Going Global: The Birth of International Hospitality (1946–1970)

In May 1949, something extraordinary happened at the Caribe Hilton in Puerto Rico. A bartender named Ramon "Monchito" Marrero was experimenting with local ingredients—fresh pineapple juice, coconut cream, and the island's famous rum. After three months of refinement, he created what would become one of the world's most famous cocktails: the Piña Colada. It was the perfect metaphor for what Hilton International was becoming—taking local culture and packaging it for global consumption while maintaining authentic flavor.

Hilton International is born, with the opening of the Caribe Hilton in Puerto Rico. Legendary barman Ramon "Monchito" Marrero creates the Pina Colada later in 1954. But the Caribe Hilton represented something far more significant than a new drink recipe. It was the beginning of Conrad's vision to export American hospitality standards worldwide while respecting local customs—a delicate balance that would define international business for the next century.

Conrad's international ambitions weren't purely commercial. During the Cold War, he saw his hotels as "little Americas"—beacons of capitalism and democracy in contested territories. When the Soviets started building hotels in non-aligned nations, Conrad accelerated his expansion, believing American hospitality could win hearts and minds better than any propaganda. The Istanbul Hilton, opened in 1955, became the social center of Turkey's modernization. The Cairo Hilton hosted diplomatic negotiations that shaped the Middle East. Conrad Hilton purchases "The Greatest of Them All," the original Waldorf Astoria in New York, NY. On October 12, 1949, The Waldorf became a Hilton hotel. Conrad had kept a photograph of the Waldorf-Astoria under the glass on his desk since 1931, with "The Greatest of Them All" scrawled across it. The purchase price was never fully disclosed, but industry insiders estimated it at around $3 million—for a property that had cost $42 million to build. The acquisition made Conrad the first hotelier to appear on the cover of Time magazine. Conrad Hilton buys Statler Hotel for $111 million, which at the time was the largest real estate deal ever. In 1954, Conrad Hilton made a $111 million deal, which at the time represented the greatest merger in hotel history and the largest real estate transaction the world had ever known. The acquisition of Hotels Statler Company brought eight hotels in operation and two more in construction. This wasn't just about size—Statler had pioneered standardization in hotel operations, something Conrad deeply admired. The Statler hotels had been the first to offer "a room with a bath for a dollar and a half," democratizing comfort for the traveling middle class. Hilton becomes the first hotel company to introduce a multi-hotel reservations system, the Inter-Hilton Hotel Reservation System, August 15. This is the beginning of the modern day reservation system. But the true innovation came in 1954 when Hilton created the world's first central reservations office, titled "HILCRON". The reservations team in 1955 consisted of eight members on staff booking reservations for any of Hilton's then 28 hotels. The chalkboard measured 30 feet by 6 feet and allowed HILCRON to make over 6,000 reservations in 1955.

This seems quaint now, but consider what it meant: a traveler could call one number and book a room in any Hilton property worldwide. No other chain could offer this. It was the hospitality equivalent of the telephone network—suddenly, all nodes were connected. Hilton pioneers the airport-hotel concept by opening the 380-room San Francisco Airport Hilton. In 1959, Hilton opened its first airport hotel (380-room San Francisco Airport Hilton) and pioneered the airport hotel concept. This wasn't just about location—it was about recognizing that air travel was transforming business. The jet age had arrived, and Conrad saw that the modern business traveler needed seamless connections between flights and meetings. The airport hotel would become one of the industry's most profitable segments, but in 1959, everyone thought Conrad was crazy to build a hotel next to runway noise.

During the 1950s and 1960s, Hilton Hotels' worldwide expansion facilitated both American tourism and overseas business by American corporations. This wasn't just business expansion—it was soft power diplomacy. Every Hilton that opened in Cairo, Istanbul, or Hong Kong became a little piece of America, a safe harbor for Western business travelers, and crucially, a training ground for local hospitality workers who would go on to transform their own countries' tourism industries.

The international division's crown jewel was the Istanbul Hilton, opened in 1955. It wasn't just a hotel—it was Turkey's declaration that it belonged to the modern world. The building itself, a gleaming modernist tower overlooking the Bosphorus, became the symbol of Turkey's Western orientation during the Cold War.

V. The Blackstone Era: Private Equity's Masterclass (2007–2018)

On July 3, 2007, the fax machines at Hilton's headquarters started humming with what would become the most audacious bet in hospitality history. Under the terms of the agreement, Blackstone will acquire all the outstanding common stock of Hilton for $47.50 per share. The price represents a premium of 40% over yesterday's closing stock price. The total transaction value: $26 billion, making it one of the largest leveraged buyouts ever attempted.

The timing couldn't have been worse—or so it seemed.

The Hilton buyout marks one of the most leveraged transactions in history, financing the $26bn deal using $20.8bn debt. Jonathan Gray, then head of real estate at Blackstone, had structured the deal with layers of debt that would make a Jenga tower look stable: senior debt, mezzanine debt, and just enough equity to keep the regulators happy. The plan was simple: buy Hilton, optimize operations, expand internationally, and ride the global travel boom.

Then Lehman Brothers collapsed fourteen months later.

By early 2009, Hilton's debt was trading at 30 cents on the dollar. Blackstone had to write down its investment by 71%. The firm's limited partners were furious. The financial press declared it the worst LBO in history. Stephen Schwarzman later admitted they were "looking over the precipice into the abyss."

But here's where the story turns from disaster to masterclass. Blackstone negotiated a debt restructuring deal in 2010; repurchasing $1.8bn of Mezzanine debt at a 54% discount and converting junior mezzanine loans into preferred equity, helping to remove significant debt (~$3.5bn) from Hilton's balance sheets. Hilton also benefited from the fall in rates, saving $700m annually. They essentially bought back their own debt at fire-sale prices, using the crisis as an opportunity to restructure the entire capital stack.

The real genius, though, was in the operational transformation led by Christopher Nassetta, the CEO Blackstone brought in. Nassetta had run Host Hotels and understood something fundamental: owning real estate is a terrible way to run a hotel company. Arguably the most significant contribution to Hilton's value creation was the shift from a large real-estate portfolio, with a capital-intense model to implementing an 'asset-light' strategy, putting emphasis on franchise agreements and licensing its brands to other hotel owners in exchange for fees... by 2013, ~92% of Hilton's hotels were operating under franchise or contract agreements.

This wasn't just financial engineering—it was a complete reimagining of what a hotel company should be. Instead of a real estate company that happened to operate hotels, Hilton became a brand and management company that collected fees from property owners. The capital requirements plummeted while margins soared. Every dollar of revenue from management and franchise fees was worth multiples more than a dollar from owned hotels.

Nassetta also drove operational excellence with an intensity that would make Six Sigma consultants weep with joy. He standardized everything from towel folding to check-in scripts across thousands of properties. He renegotiated supplier contracts globally, saving hundreds of millions. He launched Hilton's first new brands in years, targeting underserved segments like extended stay and lifestyle hotels.

By 2013, the transformation was complete. What had looked like the worst private equity deal in history was about to become the best.

VI. The 2013 IPO & Public Market Return

After Blackstone's success in transforming Hilton into an asset-light, global and high-growth company they took it public on the New York Stock Exchange on the 11th December, 2013. The IPO valued Hilton with an equity value of $19.7bn and with an enterprise value of $33.6bn, up from $26bn when Blackstone made an acquisition. Approximately 117.6m shares were sold at $20 per share, marking it the largest-ever hotel IPO at the time.

The roadshow had been a masterpiece of storytelling. Nassetta and the Blackstone team didn't just sell a turnaround story—they sold a platform story. Hilton wasn't competing with Marriott or Hyatt anymore; it was competing with Visa and Mastercard as a global fee-collection machine. The pitch was simple: every time someone traveled for business or pleasure, Hilton got paid, whether they owned the building or not.

Blackstone decided to retain a 76.2% ownership to maintain control. Throughout the next 5 years, Blackstone steadily sold its stake through a series of secondary offerings until May 2018, where they completely sold off their position. The discipline of this exit strategy was remarkable. Rather than dumping shares and depressing the price, Blackstone methodically reduced its position in tranches, often timing sales with positive earnings announcements or new development deals.

Each secondary offering told a story of continued growth. In 2014, they sold $2.9 billion worth. In 2015, another $3.6 billion. By 2016, the stock had nearly doubled from its IPO price. Wall Street, initially skeptical of a recovered LBO, became true believers in the Hilton story.

In total from 2007-2018, it is estimated Blackstone generated $14bn profit from this acquisition, marking it one of the most lucrative deals seen in private equity. But the numbers only tell part of the story. Blackstone had fundamentally transformed how the hospitality industry thought about itself. Every major chain would eventually adopt Hilton's asset-light model. The idea that a hotel company should own hotels became as outdated as the idea that Netflix should own movie theaters.

The market's reception validated everything. By the time Blackstone fully exited in May 2018, Hilton's stock was trading at $81 per share, more than four times the IPO price. The company that nearly died in 2009 was now worth more than Ford Motor Company.

VII. The Modern Portfolio: 24 Brands & Strategic Positioning

Walk into any major city today and you'll likely see multiple Hilton properties within blocks of each other—but they're not competing. They're capturing different segments of the same market with surgical precision. Hilton has 22 brands across different market segments, including Conrad Hotels & Resorts, Canopy by Hilton, Curio, Hilton Hotels & Resorts, DoubleTree by Hilton, Embassy Suites by Hilton, Hilton Garden Inn, Hampton by Hilton, Homewood Suites by Hilton, Home2 Suites by Hilton... Waldorf Astoria Hotels & Resorts, Signia by Hilton, Tru by Hilton, Tapestry Collection by Hilton, Tempo by Hilton, Motto by Hilton, and Spark by Hilton.

This isn't brand proliferation for its own sake—it's a sophisticated market segmentation strategy that would make Procter & Gamble jealous. Each brand targets a specific price point, traveler type, and occasion. The genius is in the overlapping coverage: lose a customer from Waldorf Astoria due to budget constraints? Capture them at Conrad. Business traveler becomes a leisure traveler? Move them from Hilton to DoubleTree.

The luxury tier showcases this strategy perfectly. Waldorf Astoria represents "unforgettable experiences"—the $2,000-a-night suite market. Conrad targets the "smart luxury" segment—executives who want quality without ostentation. LXR provides unique, independent-style hotels for travelers who claim they'd never stay at a chain. Each brand has distinct design standards, service protocols, and marketing strategies, but they all feed the same loyalty program.

The mass market dominance comes from Hampton Inn, with over 2,500 properties globally. Hampton is Hilton's cash cow, generating predictable franchise fees from franchisees who can build and operate these limited-service hotels at relatively low cost. The brand promise is brilliantly simple: clean, comfortable, consistent. No surprises. The free hot breakfast became so iconic that removing it would be brand suicide.

DoubleTree is infamous for its warm chocolate chip cookies at check-in. This might seem like a trivial detail, but it represents something profound about brand differentiation. In a world where hotel rooms are increasingly commoditized, that warm cookie creates an emotional connection worth millions in marketing. DoubleTree gives out over 30 million cookies annually—each one a small investment in customer loyalty.

The lifestyle and boutique plays—Curio, Tapestry, Canopy—represent Hilton's answer to the boutique hotel revolution. These aren't cookie-cutter properties; each maintains local character while benefiting from Hilton's distribution and operational systems. It's Hilton's way of saying: you can have your Instagram-worthy boutique hotel experience and still earn Hilton Honors points.

Speaking of which, Hilton Honors (formerly Hilton HHonors) is Hilton's guest loyalty program, through which frequent guests can accumulate points and airline miles by staying within the Hilton portfolio. The program is one of the largest of its type, with approximately 195 million members. But the real genius of Hilton Honors isn't its size—it's its integration across all brands and its partnership ecosystem. Members can earn and burn points not just at hotels but through credit cards, car rentals, and dozens of other partners. It's a currency system that locks in high-value customers across their entire travel lifecycle.

VIII. Technology & Operations Excellence

In 2016, Hilton did something that seemed insane: they let guests use their phones as room keys. Not just at one property—across the entire portfolio. Hilton has introduced industry-leading technology enhancements to improve the guest experience, including Digital Key Share, automated complimentary room upgrades and the ability to book confirmed connecting rooms. The Digital Key technology alone required coordinating with thousands of property owners, upgrading locks, training staff, and convincing skeptical guests to trust their phone with their room security.

But this is where Hilton's franchise model shows its teeth. When you control the brand standards, you can mandate technology adoption. Franchisees might grumble about upgrade costs, but they can't risk losing the Hilton flag. This gives Hilton unprecedented ability to roll out innovations at scale—something independent hotels or loose affiliations could never match.

The franchise model itself has been perfected to an art form. New franchisees receive 2,000-page brand standards manuals that specify everything from thread count to shower pressure. They get access to Hilton's global supply chain, negotiated rates with vendors, and most importantly, the reservation system that drives 60% of their bookings. In exchange, Hilton collects 4-6% of room revenue as franchise fees, plus another 4% for marketing—pure margin revenue with zero capital investment.

Our business model is fee-based, capital efficient, and highly resilient with tremendous growth potential around the world. This isn't just corporate speak. The beauty of the model is its scalability. Adding a new hotel to the network costs Hilton virtually nothing—the franchisee bears all the capital costs. Yet each new property strengthens the network effect, making the brand more valuable to all participants.

Development velocity tells the growth story. Approved 34,200 new rooms for development during the fourth quarter, bringing our development pipeline to 498,600 rooms as of December 31, 2024, representing growth of 8 percent from December 31, 2023. That's nearly half a million rooms in development—equivalent to adding another entire Hyatt to Hilton's portfolio. The pipeline is heavily weighted toward Asia and limited-service brands, reflecting where the growth and margins are.

The operational metrics reveal the machine's efficiency. Revenue per available room (RevPAR) consistently outperforms the industry average. But the real magic is in the margin structure. When revenue comes from franchise and management fees rather than operating hotels, EBITDA margins can exceed 40%. Compare that to the 15-20% margins of owned hotels, and you understand why Blackstone's asset-light transformation was so valuable.

Hilton's technology stack goes far beyond digital keys. Their revenue management system uses machine learning to optimize pricing across millions of room nights in real-time. The Hilton Honors app has become a digital concierge, handling everything from check-in to room service orders. They're experimenting with voice-activated room controls, robot deliveries, and even cryptocurrency payments in certain markets.

IX. Financial Performance & Market Position

The 2024 numbers tell a story of remarkable resilience and growth. Net income was $505 million for the fourth quarter and $1,539 million for the full year... Adjusted EBITDA was $858 million for the fourth quarter and $3,429 million for the full year. But these headline numbers mask the real story: the quality of earnings.

Nearly 70% of Hilton's EBITDA comes from franchise and management fees—highly recurring, capital-light revenue streams that weather economic storms far better than owned hotel operations. When occupancy drops 10%, an owned hotel might see profits evaporate. A franchise fee drops 10%, but profits remain robust because there's no associated cost structure.

Revenue: US$11.2b (up 154% from FY 2020) shows the post-pandemic recovery has been extraordinary. But more impressive is the margin expansion. Despite labor shortages, inflation, and supply chain chaos, Hilton has actually improved its margins through operational efficiency and mix shift toward higher-margin fee business.

Capital allocation tells another story of discipline. Repurchased 3.1 million shares of Hilton common stock during the fourth quarter; bringing total capital return, including dividends, to $781 million for the quarter and $3.0 billion for the full year. This isn't financial engineering—it's a recognition that the business generates far more cash than it can efficiently redeploy into growth. The development pipeline is entirely funded by franchisees, leaving Hilton flush with cash.

Competitive positioning versus Marriott, Hyatt, and IHG reveals interesting dynamics. Marriott is larger (8,785 properties vs. Hilton's 8,800, but with 1.6 million rooms vs. Hilton's 1.3 million), but Hilton generates higher RevPAR in most markets. Hyatt focuses on luxury and has higher average daily rates but lacks Hilton's scale in limited service. IHG has strong international presence but weaker brand recognition in the crucial U.S. market.

Wall Street's perspective has evolved dramatically. The stock trades at roughly 25x forward EBITDA, a premium multiple that reflects the quality of the business model. Analysts consistently praise the visibility of earnings, the strength of the development pipeline, and the resilience of the fee model. The company that nearly collapsed in 2009 is now seen as one of the most defensive plays in the consumer discretionary sector.

The balance sheet transformation is complete. Net debt stands at roughly 3x EBITDA, a conservative level for such a stable business. The company maintains investment-grade credit ratings, a far cry from the junk-rated debt of the Blackstone era. This financial flexibility allows Hilton to weather downturns, fund technology investments, and return capital to shareholders without stress.

X. Playbook: Key Business Lessons

The Hilton story offers a masterclass in business transformation, but the lessons extend far beyond hospitality. The power of brand portfolio strategy shows that owning the entire price spectrum isn't about cannibalizing your premium brands—it's about capturing value wherever customers want to transact. Procter & Gamble learned this with detergent, General Motors with cars, and Hilton perfected it in hospitality.

The asset-light versus asset-heavy debate was definitively settled by Hilton's transformation. Real estate might be valuable, but it's a different business than hospitality. By separating property ownership from hotel operations, Hilton unlocked value that had been hidden for decades. This same principle has revolutionized industries from telecommunications (tower companies) to retail (sale-leasebacks). The lesson: own what differentiates you, outsource what doesn't.

Private equity value creation, when it actually works, follows a predictable pattern that Blackstone executed flawlessly. Buy a good business with a bad balance sheet. Fix the operations. Optimize the capital structure. Exit into a strong market. But the Hilton deal added another dimension: fundamental business model transformation. This wasn't just leverage and cost-cutting—it was reimagining what the company could be.

Building a global franchise system requires a delicate balance of standardization and flexibility. Hilton learned that brand standards must be non-negotiable (that Hampton breakfast better be consistent from Toledo to Tokyo), but local adaptation is essential (that Tokyo Hampton better have rice at breakfast). The franchise model only works when franchisees make money, creating aligned incentives that pure ownership could never achieve.

Technology as competitive advantage in hospitality isn't about having the latest gadgets—it's about using technology to create network effects. Every hotel added to Hilton's system makes the reservation platform more valuable. Every Hilton Honors member makes the loyalty program more attractive to hotels. Every technological innovation that requires scale to implement becomes a moat against smaller competitors.

The importance of crisis management and patient capital cannot be overstated. Blackstone could have panicked in 2009, sold assets at fire-sale prices, and locked in massive losses. Instead, they played the long game, restructured methodically, and turned disaster into triumph. Conrad Hilton did the same during the Great Depression. The lesson: in crisis, cash and courage are the only currencies that matter.

Culture and talent, from Conrad to Nassetta, reveal an interesting paradox. The founder's vision must be strong enough to survive generations but flexible enough to evolve. Conrad's obsession with standardization and "digging for gold" remains, but modern Hilton would be unrecognizable to him. Nassetta understood this balance—honor the heritage while transforming the business. The best leaders are translators between past and future.

XI. Bear vs. Bull Case & Future Outlook

The bull case for Hilton rests on several powerful pillars. Global travel continues its inexorable growth, driven by rising middle classes in Asia, increased business connectivity, and the human desire for experiences over possessions. Hilton's development pipeline of nearly 500,000 rooms provides visible growth for years. The loyalty program moat deepens with every member added, creating switching costs that protect market share. The asset-light model means growth requires minimal capital, leaving cash for shareholders.

Full year 2025 system-wide RevPAR is projected to increase between 2.0 percent and 3.0 percent on a comparable and currency neutral basis compared to 2024; full year Adjusted EBITDA is projected to be between $3,700 million and $3,740 million. These projections might seem modest, but they reflect the maturity and stability of the business. This isn't a startup promising hockey-stick growth—it's a profit machine with visible, predictable expansion.

The bear case cannot be ignored. Economic sensitivity remains Hilton's Achilles heel. When businesses cut travel budgets or consumers postpone vacations, Hilton feels it immediately. Unlike true consumer staples, travel is discretionary, making Hilton vulnerable to recession. Competition from alternative lodging, particularly Airbnb, continues to capture share in certain segments. Young travelers often prefer the "authentic" experience of staying in someone's apartment over the standardized comfort of a hotel.

Margin pressure lurks everywhere. Labor costs are rising globally as hospitality workers demand better wages and conditions. Technology investments, while necessary, require constant capital. Franchisees push back on fee increases, limiting pricing power. Online travel agencies like Booking and Expedia control increasing share of distribution, demanding higher commissions.

Technology disruption risks extend beyond Airbnb. What happens when virtual reality makes business travel less necessary? When autonomous vehicles make road trips more appealing than flying and staying in hotels? When digital nomads choose monthly rentals over nightly rates? Hilton must evolve its model for a world where traditional travel patterns might fundamentally change.

The next frontier—what does Hilton look like at 200 years?—likely involves transcending traditional hospitality. Hilton could become a broader travel and experience platform, organizing not just where you stay but what you do. The brand permission extends far beyond beds—it encompasses trust, consistency, and global reach. Hilton-branded residences, co-working spaces, or even virtual experiences could extend the ecosystem.

Environmental and social governance increasingly matters. Hotels are resource-intensive operations in an increasingly climate-conscious world. Hilton's commitment to cut its environmental footprint in half by 2030 isn't just corporate rhetoric—it's essential for maintaining social license to operate. The company that masters sustainable hospitality will win the next generation of travelers.

XII. Recent News

The latest developments at Hilton represent a dramatic acceleration of its portfolio expansion and strategic positioning. In 2024, Hilton added 973 hotels and nearly 100,000 rooms, the single biggest increase in rooms in Hilton's more than 100-year history, achieving net unit growth of 7.3%. This unprecedented growth was fueled by strategic acquisitions and partnerships that fundamentally reshape the company's competitive position.

Strategic Acquisitions Reshape Portfolio

Hilton paid $210 million to acquire all rights to the Graduate Hotels brand worldwide, entering into franchise agreements for all existing and signed pipeline Graduate Hotels. The Graduate acquisition brings more than 35 operating and pipeline properties focused on university towns—a niche market with tremendous growth potential. Nassetta noted "with thousands of colleges and universities around the world, we believe the addressable market for the Graduate brand is 400-500 hotels globally".

The NoMad acquisition represents Hilton's entry into the fast-growing luxury lifestyle hotel market with a meticulously designed brand defined by exceptional food and beverage, interior design and service. While financial terms weren't disclosed, Hilton acquired a majority controlling interest in Sydell Group to expand the NoMad Hotels brand from its existing London flagship location to high-end markets around the world. Sydell will be responsible for design, branding and management of the NoMad brand while Hilton will lead all development.

Lifestyle Portfolio Doubles Down

With nearly 350 existing lifestyle hotels and another 350 expected to join the portfolio by 2028, Hilton is set to double its presence in the fast-growing lifestyle category in the next four years. This aggressive expansion reflects changing traveler preferences, with Hilton's 2024 Trends Report identifying that nearly a quarter of global travelers are planning getaways for concerts, sporting events and other one-of-a-kind, local experiences this year.

Partnership Revolution

Beyond acquisitions, Hilton has revolutionized its growth strategy through strategic partnerships. The exclusive partnership with Small Luxury Hotels of the World instantly added hundreds of properties to Hilton's luxury portfolio. The AutoCamp partnership extends Hilton into outdoor hospitality, allowing the brand to capture the glamping trend without capital investment.

Record Financial Performance Continues

The latest earnings confirm the strategy is working. Net income was $505 million for the fourth quarter and $1,539 million for the full year, with Adjusted EBITDA of $858 million for the fourth quarter and $3,429 million for the full year, exceeding the high end of guidance. Full year 2025 system-wide RevPAR is projected to increase between 2.0 percent and 3.0 percent on a comparable and currency neutral basis compared to 2024; full year Adjusted EBITDA is projected to be between $3,700 million and $3,740 million.

Development Pipeline Reaches New Heights

Hilton signed more than 1,430 hotels representing 154,000 rooms in 2024, demonstrating unprecedented developer interest. The pipeline momentum continues, with approximately half a million rooms in the development pipeline providing visibility for years of growth ahead.

Board Confidence in Capital Returns

The Board of Directors authorized the repurchase of an additional $3.5 billion of common stock under the Company's existing stock repurchase program, bringing the total amount currently authorized for future repurchases to approximately $4.8 billion. This massive authorization reflects confidence in the business model's cash generation capabilities and commitment to shareholder returns.

XIII. Links & Resources

SEC Filings & Investor Materials

- Hilton Investor Relations: https://ir.hilton.com/

- 2024 Annual Report (10-K): https://ir.hilton.com/financial-reporting/sec-filings

- Quarterly Earnings Presentations: https://ir.hilton.com/events-and-presentations

- Proxy Statements: https://ir.hilton.com/financial-reporting/sec-filings

Industry Reports & Analysis

- STR Global Hotel Performance Data: https://str.com/

- Lodging Magazine Industry Reports: https://lodgingmagazine.com/

- Hotel News Now Analytics: https://www.hotelnewsnow.com/

- Skift Research Hotel Reports: https://research.skift.com/

Historical Books & Biographies

- "Be My Guest" by Conrad Hilton (1957) - Founder's autobiography

- "The Hiltons: The True Story of an American Dynasty" by J. Randy Taraborrelli (2014)

- "From the Ground Up: A Journey to Reimagine the Promise of America" by Howard Schultz (references Hilton's influence on hospitality)

Academic Case Studies

- Harvard Business School: "Hilton Hotels: Brand Differentiation through Customer Relationship Management" (2019)

- Stanford Graduate School of Business: "The Blackstone Group and Hilton Hotels" (2015)

- Wharton: "Private Equity and the Transformation of Hilton Worldwide" (2018)

- Cornell Hotel School Publications: Multiple studies on Hilton's franchise model

Podcast Episodes & Interviews

- Masters of Scale: "Chris Nassetta on Building a Global Hospitality Platform" (2023)

- How I Built This: Historical episode on Conrad Hilton's empire building

- Skift Podcast: Regular coverage of Hilton's quarterly earnings and strategy

- Hotel Business Podcast: Deep dives on Hilton's brand strategy

Trade Publication Deep Dives

- Hotel Management Magazine: "The Evolution of Hilton's Brand Architecture" (2023)

- Hospitality Net: Research papers on asset-light transformation

- Hotel News Resource: Coverage of major Hilton developments

- HOTELS Magazine: Annual rankings and Hilton analysis

Financial Analysis Resources

- Morningstar Equity Research Reports on HLT

- S&P Capital IQ Hotel Industry Reports

- Credit Suisse Lodging Sector Analysis

- Morgan Stanley Research on Global Lodging REITs and C-Corps

Technology & Innovation Resources

- Hospitality Technology Magazine: Coverage of Hilton's digital initiatives

- PhocusWire: Analysis of Hilton's distribution strategy

- Hotel Tech Report: Reviews of Hilton's technology stack

Competitor Resources

- Marriott International Investor Relations: https://marriott.gcs-web.com/

- Hyatt Hotels Corporation: https://investors.hyatt.com/

- IHG Hotels & Resorts: https://www.ihgplc.com/investors

- Accor Investor Relations: https://group.accor.com/en/investors

Conclusion: The Architecture Endures

The Hilton story, spanning over a century from a dusty Texas oil town to a global hospitality empire worth tens of billions, offers profound lessons about business transformation, resilience, and the power of systematic thinking. What began as Conrad Hilton's $40,000 purchase of the Mobley Hotel has evolved into a platform that processes over 220 million guest stays annually across nearly 1.3 million rooms worldwide.

The genius of Hilton isn't in any single innovation but in the relentless application of a few core principles across decades and through multiple ownership structures. Conrad's original insights—standardize excellence, optimize every square foot, treat employees as partners in hospitality—remain embedded in the company's DNA even as it has transformed from a real estate owner to a brand and management platform.

The Blackstone era proved that even mature businesses can be fundamentally reimagined. The shift to an asset-light model wasn't just financial engineering; it was a recognition that in the 21st century, intellectual property and network effects matter more than physical assets. By owning the brands, technology, and customer relationships while letting others own the real estate, Hilton achieved the holy grail of business: scalability without capital intensity.

Today's Hilton operates at the intersection of several powerful trends. The global middle class continues to expand, particularly in Asia where Hilton's development pipeline is concentrated. Business travel, despite predictions of its demise, has proven remarkably resilient as human connection remains irreplaceable. The lifestyle hotel revolution, rather than disrupting Hilton, has been co-opted through acquisitions and new brand launches. Even the threat from alternative lodging has been partially neutralized through partnerships and brand diversification.

The numbers tell a story of remarkable execution. From near-bankruptcy in 2009 to generating $3.4 billion in EBITDA in 2024, from 8 struggling hotels during the Depression to 8,800 properties today, from a Texas-centric operation to a presence in 139 countries—each transformation built upon the last, creating compound value that few companies achieve.

Yet challenges remain. The democratization of travel through platforms like Airbnb continues to evolve. Climate concerns increasingly influence travel patterns and regulatory environments. Technology threatens to disintermediate traditional booking channels. Economic cycles remain an ever-present risk to discretionary travel spending. The next generation of travelers may have fundamentally different expectations about hospitality.

But if history is any guide, Hilton will adapt. The company that survived the Great Depression, transformed through private equity ownership, and emerged stronger from a global pandemic has proven its resilience. The development pipeline of nearly 500,000 rooms provides growth visibility for years. The loyalty program with 226 million members creates powerful network effects. The brand portfolio from Spark to Waldorf Astoria captures value across every price point and travel occasion.

The real moat, however, may be something less tangible: the accumulated knowledge of how to deliver hospitality at scale. Every process refined over decades, every relationship with developers and franchisees, every data point about guest preferences—these create barriers that capital alone cannot overcome. When Conrad Hilton said he wanted to "fill the earth with the light and warmth of hospitality," he was articulating a mission that transcends business cycles and ownership changes.

As Hilton approaches its second century, the fundamental question isn't whether people will continue to travel—human curiosity and commerce guarantee that. It's whether the traditional hotel model, even transformed into an asset-light platform, remains the optimal way to serve those travelers. The aggressive moves into lifestyle brands, luxury partnerships, and alternative lodging suggest Hilton's leadership understands that standing still means falling behind.

The architecture Conrad Hilton built—not the physical hotels but the systematic approach to hospitality—has proven remarkably durable. It survived family ownership, public markets, private equity transformation, and return to public markets. It adapted from American expansion to global dominance, from owning assets to licensing brands, from analog to digital, from standardization to personalization while maintaining standardized excellence.

For investors, Hilton represents a rare combination: a century-old company with startup-like growth characteristics, a cyclical business with remarkably stable fee streams, a capital-intensive industry played with an asset-light model. The stock market's premium valuation reflects this unique positioning. For the hospitality industry, Hilton remains the template others copy, the standard against which performance is measured.

The journey from the Mobley Hotel to a global platform managing $11 billion in revenue teaches us that great businesses aren't built on single insights but on systems that compound advantages over time. Conrad Hilton's original vision—that travelers everywhere deserved consistent, quality accommodation—seems obvious now only because he made it so. The next century will bring challenges we cannot imagine, but if the past is prologue, Hilton will meet them by returning to first principles: dig for gold in every opportunity, treat every stakeholder as a partner, and never forget that hospitality, at its core, is about human connection.

The architecture endures not because it's perfect, but because it's perfectible—always evolving, always improving, always building on what came before. That may be Conrad Hilton's greatest legacy: not the hotels that bear his name, but the idea that systematic excellence, applied consistently over time, can transform not just a company but an entire industry's conception of what's possible.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube