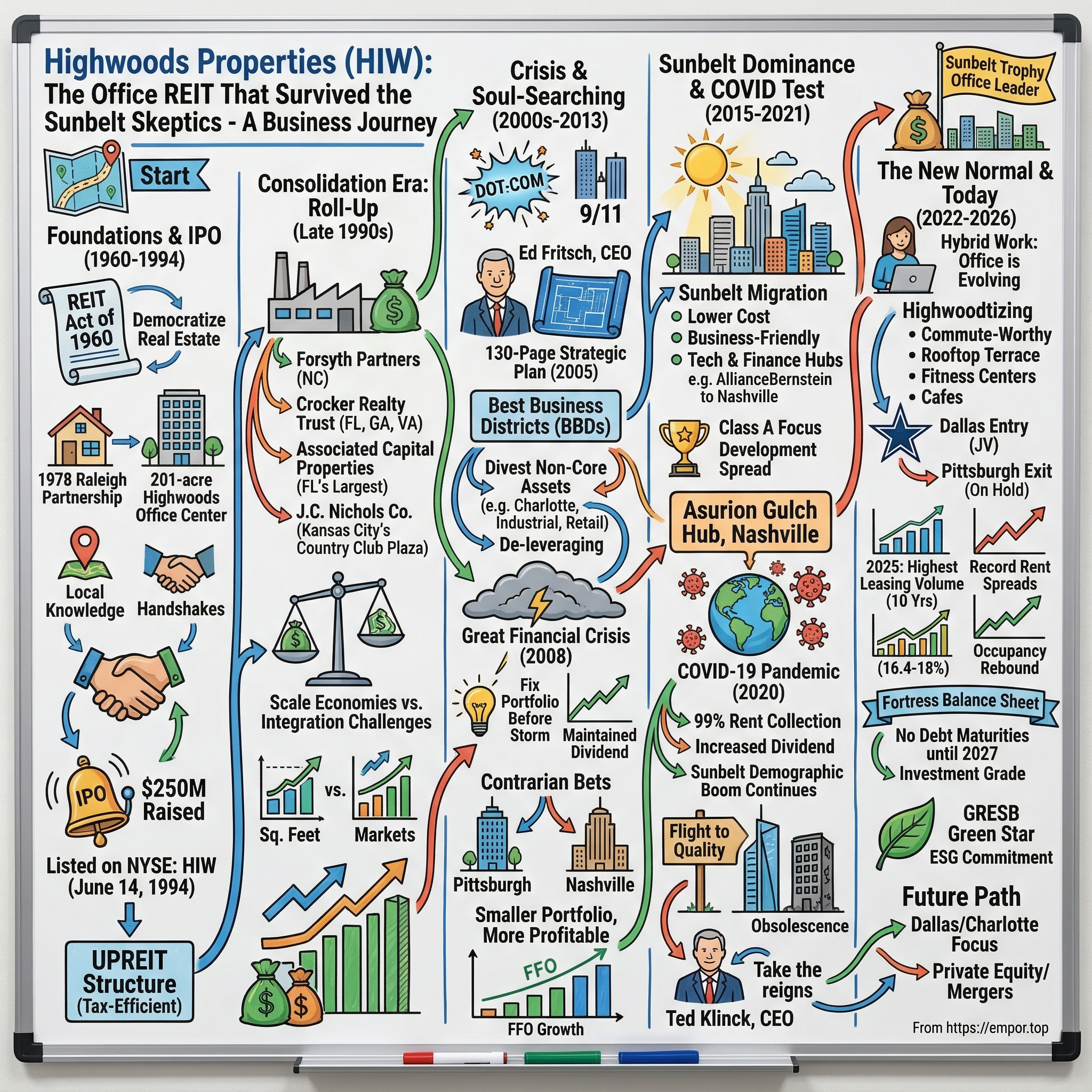

Highwoods Properties: The Office REIT That Survived the Sunbelt Skeptics

Introduction and Episode Roadmap

Picture this: It is March 2020, and every office building in America has gone dark. Employees are Zooming from spare bedrooms. Pundits are declaring the death of the office with the same certainty they once declared the death of the shopping mall. Office REIT stocks are cratering. One company, Highwoods Properties, watches its stock price plummet from an all-time high of $36.14 on Valentine's Day to something far less romantic within weeks.

And yet, the company's tenants keep paying rent. Not most of them. Nearly all of them: 96 percent in April, 99 percent by May. Highwoods does not cut its dividend. It raises it.

How did a Raleigh, North Carolina real estate company, born from a private partnership in the late 1970s, become the largest pure-play office REIT in the American Sunbelt? How did it survive two generational crises, a pandemic that emptied its entire product category, and emerge as perhaps the most interesting test case for whether the office has a future in post-pandemic America?

The central tension is as stark as it gets in commercial real estate: Is Sunbelt office dead, or is it the single best bet left standing?

To answer that question, the story starts well before anyone had heard of COVID-19, before the Sunbelt migration became a cable news talking point, and before the phrase "return to office" entered the lexicon. It starts with a decision by the United States Congress in 1960 to fundamentally change how Americans could invest in real estate, and with a group of North Carolina developers who saw something in the Research Triangle that the rest of Wall Street missed entirely.

The arc follows a familiar pattern for students of business history: founding vision, explosive growth, crisis, painful restructuring, vindication, another crisis, and now the great open question. Along the way, Highwoods Properties offers a masterclass in capital allocation, market selection, and the power of knowing exactly what you are and, more importantly, what you are not. This is a story about real estate, but it is also a story about focus, about discipline, and about betting on America's geography when others were betting against it.

Why does this matter now? Because the office sector sits at a crossroads unlike anything in its history. Billions of square feet of American office space face uncertain futures. REITs that once traded at premiums now trade at deep discounts to the replacement cost of their buildings. And yet, in certain markets, in certain neighborhoods, in certain buildings, tenants are lining up, rents are rising, and the fundamentals look better than they have in years. Highwoods Properties is the clearest lens through which to understand this bifurcation, and the lessons it offers apply far beyond commercial real estate.

The REIT Revolution and Founding Context

Before there were REITs, investing in commercial real estate was a rich person's game. Think of it this way: if you wanted to own a piece of a skyscraper or an office park, you either had the capital to buy one yourself, or you were out of luck. There was no equivalent of buying a share of stock to get a slice of a shopping center in Dallas or an apartment complex in Atlanta.

The Real Estate Investment Trust Act of 1960 changed the equation permanently. Congress created a vehicle that would allow ordinary investors to pool their money into professionally managed real estate portfolios, much as mutual funds had done for stocks. The catch, and it was a deliberate one, was that REITs had to distribute at least 90 percent of their taxable income to shareholders each year. In exchange, they paid no corporate income tax.

The structure was elegant in its simplicity: democratize real estate ownership, force regular cash returns to investors, and create liquidity in a historically illiquid asset class. Think of it as a bargain between real estate operators and the government: you get favorable tax treatment, but you cannot hoard cash. You must share the profits.

For three decades after the 1960 Act, REITs existed but never quite caught fire. They were a niche product, mostly small, mostly equity-light, and mostly ignored by institutional investors. The 1980s real estate crisis changed everything, though not in the way anyone planned.

The Savings and Loan debacle, one of the worst financial catastrophes in American history, left a trail of overbuilt properties, failed banks, and distressed assets across the country. Hundreds of savings institutions had poured money into speculative real estate development during the early 1980s, fueled by deregulation and generous tax incentives. When the Tax Reform Act of 1986 removed those incentives and the economy softened, the bubble burst spectacularly. Over a thousand S&Ls failed. The Resolution Trust Corporation was created to liquidate their assets, dumping enormous quantities of commercial real estate onto the market at fire-sale prices.

When the dust settled in the early 1990s, a strange and potent confluence emerged. There was an enormous supply of real estate available at bargain prices. A newly cautious banking system had tightened lending standards, making traditional bank financing harder to obtain. And a generation of institutional investors, pension funds and insurance companies and endowments, were hungry for yield in a declining interest rate environment.

The REIT IPO boom of 1993 and 1994 was the result, as dozens of private real estate operators rushed to go public, accessing capital markets that were suddenly wide open and eager for real estate exposure.

Simultaneously, a geographic thesis was crystallizing that would shape the next three decades of American commercial real estate. The Sunbelt, that broad swath of states stretching from the Carolinas through Georgia, Tennessee, Florida, and Texas, was pulling population and corporate investment away from the Rust Belt and the expensive coastal cities. Lower costs of living, business-friendly tax environments, expanding universities, and growing technology corridors made cities like Atlanta, Charlotte, Raleigh, Nashville, and Tampa magnets for corporate expansion.

The Research Triangle in North Carolina was a microcosm of the trend: a cluster of three major research universities, Duke, UNC Chapel Hill, and NC State, surrounded by pharmaceutical companies, technology firms, and government contractors, all generating demand for high-quality office space in a region where land was plentiful and construction costs were a fraction of what they were in Manhattan or San Francisco.

It is worth pausing here to appreciate just how dramatic this IPO wave was. In 1991, the entire publicly traded REIT market was worth roughly $9 billion. By the end of 1994, it had ballooned to over $44 billion. More than 100 REIT IPOs came to market in those three years. It was the largest transfer of real estate ownership from private to public hands in American history, and it created the industry structure that exists today.

This was the environment, the REIT boom, the Sunbelt migration, the knowledge economy's emergence, in which a group of Raleigh developers decided their private partnership was ready for the public stage.

The Origins and IPO

Highwoods Properties traces its roots to 1978, when a private real estate partnership was formed in Raleigh, North Carolina to develop, lease, and manage the 201-acre Highwoods Office Center on the city's northeast side. The founding team included Ronald P. Gibson, who would serve as managing partner and eventually CEO; H. Pope Shuford, who focused on office development in the Research Triangle; and O. Temple Sloan Jr., a prominent North Carolina businessman and chairman of General Parts International, with deep ties to the state's business community, who became Chairman of the Board.

These were not coastal financiers parachuting into North Carolina with institutional capital. These were local operators who knew every road, every submarket, every corporate decision-maker in the Triangle. They had been doing deals on handshakes and local knowledge for years before anyone on Wall Street cared about Raleigh.

Sloan, in particular, brought a network that extended across North Carolina's business establishment. As chairman of General Parts International, which grew to become one of the largest auto parts distributors in North America, he understood how to build businesses in mid-sized Southern cities where relationships mattered as much as capital. That sensibility, the belief that being deeply embedded in a community was itself a competitive advantage, would define Highwoods' approach for decades.

For sixteen years, the predecessor firm built and managed office properties in the Raleigh area, developing the kind of granular local market expertise and tenant relationships that would become the company's calling card. They learned which intersections attracted tenants and which ones did not. They built relationships with the mid-sized professional services firms, the regional banks, the technology companies spinning out of university research labs. It was not glamorous. It was not going to make the front page of the Wall Street Journal. But it was building something that would prove remarkably durable: deep local knowledge in a market that the rest of America was about to discover.

The decision to go public came in 1994, squarely in the middle of the REIT IPO wave. On June 14, 1994, Highwoods Properties listed on the New York Stock Exchange under the ticker HIW, raising approximately $250 million.

The company structured itself as an UPREIT, which stands for Umbrella Partnership REIT. To explain this in plain terms: the founding sponsors contributed their properties into an operating partnership in exchange for partnership units, which could later be converted to common shares. The benefit was tax deferral: instead of selling their properties and paying capital gains taxes, they rolled their equity into the public vehicle and deferred those taxes indefinitely. It was a smart, tax-efficient way to bring a portfolio of Raleigh-area office properties onto a public platform with access to growth capital.

The initial portfolio was modest by national standards: a collection of office properties concentrated in the Research Triangle, some warehouse and industrial space, 94 acres of development land, and the management and leasing business. But the vision was ambitious in its own, distinctly Southern way.

Highwoods was not trying to compete with the Brookfields and Boston Properties of the world for trophy towers in gateway cities. Instead, the thesis was straightforward: build and own the best office properties in the best secondary Sunbelt cities, markets where the company could be, as management liked to say, "a big dog on a medium-sized porch." While the big REITs fought over Manhattan and San Francisco, Highwoods would quietly dominate Raleigh and its future target markets.

The early strategy emphasized conservative leverage, a focus on Funds From Operations (the REIT equivalent of earnings, which strips out non-cash items like depreciation to give a cleaner picture of cash-generating ability), and building deep relationships with mid-sized corporate tenants. If you think about what makes a great landlord, it is not just the building itself but the relationship with the tenant: understanding their growth plans, their space needs, their timeline for expansion. For those unfamiliar with REIT accounting, FFO deserves a brief explanation because it is the single most important metric for evaluating a REIT. Traditional earnings per share includes depreciation expense, which in real estate can be enormous because buildings are depreciated over 39 years. But a well-maintained office building does not actually lose value the way a factory machine does; in many cases, it appreciates. FFO adds back depreciation to net income, giving investors a much cleaner picture of the actual cash the business generates. When you hear REIT investors talk about "multiple of FFO," think of it like a price-to-earnings ratio but more reflective of economic reality.

These were not the flashiest principles in 1994, but they would prove remarkably durable through the storms that lay ahead.

The IPO coincided with something else important: the early career of a young employee who would eventually reshape the company entirely. Ed Fritsch had joined the predecessor firm in 1982, fresh from the University of North Carolina at Chapel Hill, at the age of 23. Over the next twelve years before the IPO, he had done virtually every job in the company: property management, asset management, development, operations. He was being groomed, whether anyone called it that or not, for something much bigger. But in 1994, the company was focused on growth, not succession, and the growth was about to be staggering.

The Consolidation Era: Roll-Up Strategy

If the IPO was the opening act, the late 1990s were the main event. The REIT playbook of the era was simple and intoxicating: use cheap equity from enthusiastic public markets to acquire portfolios of properties, expand your platform, and grow earnings through scale. Every REIT was doing it. Highwoods did it bigger and faster than almost anyone in the Sunbelt.

The first move came in February 1995 with the Forsyth Partners merger, which expanded the company's North Carolina footprint into the Greensboro and Winston-Salem markets. John L. Turner, who had co-founded Forsyth Partners' predecessor in 1975, joined Highwoods through the transaction, bringing two decades of Triad-area relationships. It was a logical adjacency: one more North Carolina market, one more set of local relationships, one more step toward dominating the state.

Then came the deal that changed Highwoods' trajectory entirely. In 1996, the company merged with Crocker Realty Trust, adding approximately 5.7 million square feet to the portfolio and, critically, establishing Highwoods in Florida, Atlanta, and Virginia for the first time. Overnight, the company went from a North Carolina developer to a multi-state operator. The Crocker deal was the kind of transformational acquisition that separates a regional player from a platform company.

In October 1997, the company executed its largest deal yet: the merger with Associated Capital Properties, valued at $622 million. ACP was the largest private owner of office properties in Florida, with 85 office buildings totaling 6.5 million square feet scattered across Tampa, Orlando, and other Florida markets. Jim Heistand, the founder of ACP who would later become CEO of Parkway Properties, joined Highwoods as a senior vice president. The ACP merger brought the total portfolio to approximately 28 million square feet, a nearly five-fold increase from the IPO just three years earlier.

That pace of growth was breathtaking. And it was not over.

The following year brought perhaps the most distinctive acquisition in Highwoods' history: the J.C. Nichols Company in Kansas City for $544 million. The crown jewel was Country Club Plaza, a historic, upscale open-air lifestyle center spanning 15 blocks with roughly a million square feet of retail, another million of office, and 462 apartment units. The Plaza was a landmark, one of the first planned shopping centers in America, designed in a Spanish architectural style in the 1920s. It ended more than 90 years of local Nichols family ownership and represented Highwoods' most significant foray outside the Sunbelt. Whether it belonged in the portfolio was a question that would take years to answer.

By the end of 2004, Highwoods had assembled a portfolio of 33.9 million rentable square feet across 444 properties, diversified across office, industrial, retail, and apartments. The tenant roster read like a cross-section of Sunbelt commerce: financial services firms, healthcare companies, government contractors, professional services operations, technology companies. The roll-up strategy had succeeded spectacularly in building scale.

But scale had a cost. The company was now operating in more than a dozen markets, managing multiple property types, running separate leasing teams and management offices across the Southeast and Midwest. Integration challenges mounted. The dot-com bust in 2000 and 2001 and the economic aftermath of September 11 tested Sunbelt office demand for the first time. Occupancy wobbled. The broader demographic trend held, companies continued to move operations to the Southeast, but the question of whether Highwoods, now sprawling across so many markets and property types, was positioned to capture that demand efficiently had a growing urgency.

The tension between growth and focus is one of the oldest in business strategy, and by 2004, Highwoods was living it acutely. The company had the footprint of a national operator but the DNA of a regional developer. The roll-up had created geographic breadth, but it had also diluted the local market intimacy that had made the original Raleigh business work so well. In Kansas City, Highwoods was competing against landlords who had been there for decades. In Memphis, it was managing commodity office parks that could have been owned by anyone.

The answer required a new CEO with a very different vision of what the company should be.

The Great Financial Crisis: Survival and Soul-Searching

Ed Fritsch had been patient. After joining the company in 1982 as a 23-year-old, he rose methodically through the organization: Vice President of Operations during the IPO era, Chief Operating Officer in 1998 during the acquisition spree, President in late 2003. When he finally assumed the CEO role in July 2004, succeeding co-founder Ronald Gibson, he had spent 22 years learning every corner of the business. Few CEOs in American commercial real estate have ever had a longer apprenticeship.

Fritsch inherited a company at a crossroads that most outsiders did not yet see. The portfolio was large and diversified, which sounded impressive in investor presentations. But Fritsch, who had been in the trenches managing individual properties for two decades, knew the reality was more complicated. Some markets were winners. Some were treadmills. And a few were slowly dying, propped up by inertia and the reluctance to admit that an acquisition that looked brilliant in 1998 was a drag on returns by 2004.

In January 2005, just six months into his tenure, Fritsch and the board implemented a 130-page strategic plan that would define the company for the next fifteen years. The plan introduced a concept that would become central to Highwoods' identity: "Best Business Districts," or BBDs.

The thesis was deceptively simple but radical in its implications: only the premier locations within the best Sunbelt cities would generate durable demand from high-quality tenants over the long term. Everything else, every commodity office park in a secondary submarket, every industrial warehouse that did not fit the thesis, every property in a market where Highwoods could not be the dominant local player, was a candidate for disposal.

The mantra was ruthlessly clear. Fritsch told his team: "No person, no process, and no property was sacred. We popped the hood and questioned everything."

The results of the strategic reset were dramatic even before the financial crisis hit. Between early 2005 and late 2007, Highwoods divested approximately $741 million in non-core office and industrial properties plus $96 million in land. The company exited Charlotte and Columbia, South Carolina. It began trimming industrial and retail holdings. Headcount started to decline. This was not an optimization exercise; it was a transformation. The company was deliberately getting smaller to get better, a strategy that runs counter to every empire-building instinct in corporate America.

The timing proved fortuitous in a way no one could have planned. When the Great Financial Crisis struck in 2008, Highwoods was in a stronger position than most office REITs precisely because it had spent the preceding three years de-leveraging and simplifying. The crisis was still brutal. Office vacancies spiked nationally. Rents collapsed. Refinancing became nearly impossible for the most leveraged players. Several office REITs slashed or eliminated their dividends, sending their stocks into freefall and destroying investor confidence.

Highwoods weathered the storm. The company maintained its dividend through the crisis, a critical signal to income-oriented REIT investors who treat dividend cuts as near-terminal events. Leverage, which had been reduced from 51 percent of gross assets to around 42 percent through the strategic plan's early execution, provided a cushion that many peers lacked. Fritsch later described having "a quality balance sheet" that provided "significant flexibility" when credit markets froze.

The flexibility was not theoretical. It was the difference between survival and distress.

But the crisis also reinforced a harder truth that would shape the next decade of strategy: not all Sunbelt markets were created equal. Some, like Memphis and the weaker parts of Kansas City, behaved like commodity office markets: highly cyclical, vulnerable to oversupply, and difficult to differentiate. Tenants in these markets leased on price, and when the economy weakened, they left. Others, like Raleigh and Nashville, showed genuine resilience because they were anchored by knowledge economy employers, research universities, and healthcare systems that generated demand even in downturns.

The financial crisis did not just test the balance sheet. It provided the data to prove which markets actually worked. And for investors, it offered a lesson that applies far beyond real estate: the time to fix your portfolio is before the storm, not during it. Highwoods' pre-crisis divestitures were not prescient timing; Fritsch did not know a financial crisis was coming. But the discipline of asking "where can we actually win?" and acting on honest answers created a margin of safety that saved the company when the cycle turned.

The post-crisis period also offered opportunities for those with capital and courage. In 2011, Highwoods acquired PPG Place in Pittsburgh for $214 million, purchased at less than half its replacement cost when few investors were looking at the Steel City. The following year, EQT Plaza, a 32-story Class A tower also in Pittsburgh, was added for $99 million. In 2013, the Pinnacle at Symphony Place in Nashville was acquired for $153 million. These were contrarian bets made with recycled capital from non-core dispositions, and they illustrated the Highwoods playbook in its purest form: sell the mediocre, buy the excellent, and do it when others are too scared to write checks.

The Refocusing: BBDs and the Best Buildings Thesis

By 2013, the results of Fritsch's strategic plan were impossible to ignore, even for skeptics. Since the plan's implementation in 2005, Highwoods had sold over $1.4 billion in buildings and $113 million in land. The company had reduced its headcount by 24 percent and its building count by 40 percent.

On the surface, this looked like a company in retreat. The reality was the opposite.

Annual revenues had increased 19 percent. Net operating income had risen 29 percent on an annualized basis. The stock had gained over 124 percent on a cumulative total-returns basis. Portfolio occupancy had improved from 85 percent to 90 percent. Office properties had gone from 85 percent to 92 percent of annual rental revenues, reflecting the exit from non-office property types.

The math told a story that every capital allocator should study: Highwoods got smaller in terms of square footage and building count, but more profitable in terms of income per square foot and returns on invested capital. The company was earning more by owning less.

This counterintuitive result flowed directly from the BBD thesis. But what exactly does "Best Business District" mean in practice? It is more nuanced than simply owning office buildings in good cities.

It is about identifying the specific submarkets within each metropolitan area that will attract the most talent, corporate investment, and tenant demand over the next decade. These are walkable, amenity-rich, mixed-use districts where Class A office space sits alongside restaurants, fitness centers, retail, and green space. They are the neighborhoods where a 28-year-old software engineer or financial analyst actually wants to spend their workday, not because their employer mandates it, but because the experience is genuinely appealing.

In Raleigh, the BBD was the Research Triangle Park corridor and the emerging downtown. In Nashville, it was the Gulch district and Cool Springs in the southern suburbs. In Tampa, it was the Westshore submarket evolving into Midtown Tampa. In Atlanta, it was Buckhead and the Perimeter Center. Each market had its own geography, its own tenant dynamics, its own supply constraints. The magic was not a formula; it was local knowledge applied with strategic discipline.

The "flight to quality" trend was already emerging before anyone called it that. Corporate tenants were becoming more sophisticated about using office space as a recruiting and retention tool. They increasingly demanded buildings with modern amenities, energy efficiency, natural light, and locations their employees actually wanted to visit.

Class B and C office buildings, the kind Highwoods was actively disposing of, the buildings with low ceilings, poor ventilation, and suburban parking lots surrounded by nothing, began their long decline into structural obsolescence. Class A buildings in the right locations commanded premium rents and attracted the credit-quality tenants that made landlords sleep well at night.

Development became a key pillar of the strategy during this period. Rather than simply acquiring existing buildings at market prices, Highwoods invested in ground-up development in its BBDs. Building a new office tower from scratch costs more upfront and takes longer than buying an existing building. But the returns are significantly higher, because the developer captures the spread between construction cost and the stabilized value of the completed, leased building. This "development spread" typically runs 150 to 250 basis points above the yield on comparable acquisitions. For a company willing to take the construction and leasing risk, development is the single best way to create value in commercial real estate.

The capital recycling machine was relentless: sell non-core assets at one cap rate, develop or acquire trophy assets at a higher yield, harvest the spread as FFO growth. The tenant mix evolved accordingly, shifting toward technology companies, life sciences firms, financial services operations, and healthcare systems, the knowledge economy anchors that were growing fastest in the Sunbelt.

By 2015, Highwoods had completed its transformation from a sprawling multi-property-type conglomerate into a focused, pure-play office REIT owning the best buildings in the best districts of the best Sunbelt cities. A useful way to think about what Highwoods accomplished during this period is to compare it to a stock portfolio. Imagine you own 30 stocks, and you discover that 10 of them are generating most of your returns while 20 are treading water or losing money. The disciplined investor sells the 20, concentrates into the winners, and watches the portfolio's return on capital improve dramatically. That is essentially what Fritsch did with the real estate portfolio, except instead of selling stocks with a click, he was selling buildings, exiting markets, laying off employees, and restructuring an entire organization. The difficulty of execution makes the results all the more impressive.

The question was whether the Sunbelt would continue to deliver the growth needed to justify the concentration.

The Sun Keeps Rising: Sunbelt Migration Accelerates

Between 2015 and 2019, everything Highwoods had bet on for twenty years started paying off in accelerating fashion. The narrative around coastal cities shifted from aspiration to anxiety. San Francisco housing costs became a national punchline. A studio apartment in the Mission District cost more than a three-bedroom house in Raleigh. New York's combined state and local tax burden drove headlines about millionaire departures. Corporate leaders began openly questioning whether their headquarters needed to be in gateway cities at all.

The corporate relocations became a steady drumbeat. Financial services firms expanded operations in Charlotte, where Bank of America was already headquartered and where a deep talent pool of banking professionals lived at a fraction of coastal living costs. Technology companies discovered the Research Triangle, drawn by Duke, UNC, and NC State graduates who preferred staying in the region rather than competing for $3,500-a-month apartments in the Bay Area.

Nashville evolved from a music city stereotype into a genuine corporate hub, anchored by healthcare companies like HCA Healthcare and supplemented by a wave of firms drawn to Tennessee's zero state income tax. AllianceBernstein moved its headquarters from New York to Nashville. Amazon chose Nashville for a major operations hub. Asurion, the technology services giant, committed to a massive new campus in the city's central business district.

Highwoods rode the wave from a position of strength. Occupancy rates climbed into the 91 to 92 percent range, among the best in the office REIT sector nationally. To put that in context, the national office vacancy rate hovered around 12 to 13 percent during this period, meaning Highwoods' portfolio was outperforming the broader market by a wide margin. The outperformance was not accidental. It was the direct result of the BBD strategy: by concentrating in the best submarkets where demand exceeded supply, Highwoods avoided the commodity trap that plagued office owners in weaker locations.

Rent growth accelerated as demand outpaced supply in the company's BBDs. The development pipeline hit its stride, with build-to-suit deals and speculative developments delivering strong returns.

The algorithm was elegant in its simplicity: acquire land in Best Business Districts, develop Class A buildings, lease them to creditworthy tenants on long-term leases, and harvest the FFO. Rinse and repeat. The beauty of the model was that each development created a tangible, income-producing asset that appreciated over time, unlike a technology company where growth requires constant reinvestment just to maintain the installed base.

The balance sheet improved steadily during this period. Investment-grade credit ratings gave Highwoods access to the corporate bond market at attractive rates, and debt-to-EBITDA ratios declined as NOI grew faster than borrowings. The company was also actively deleveraging by using proceeds from non-core asset sales to pay down debt rather than fund new acquisitions, a discipline that ran counter to the industry's typical instinct to reinvest every dollar into new deals.

For context, debt-to-EBITDA is the most widely followed leverage metric for REITs. It measures how many years of earnings it would take to pay off all debt. A ratio below 6x is generally considered conservative for an office REIT. Highwoods managed to bring this ratio down through a combination of debt reduction and NOI growth, creating financial flexibility that would prove invaluable when the next crisis arrived.

Perhaps the most significant development of this era was the announcement in July 2018 of the Asurion Gulch Hub in Nashville's CBD, a $285 million build-to-suit headquarters campus for the technology services company Asurion. The project consisted of two mid-rise buildings on a six-level parking podium totaling 551,000 square feet. It created 400 IT jobs and consolidated four separate Asurion offices into a single campus. This was the BBD strategy made manifest: a major corporate tenant choosing a Highwoods-developed building in a premier Nashville district because the location, the building quality, and the neighborhood all made it the obvious choice.

The competitive landscape was not without challenges. Cousins Properties, headquartered in Atlanta, was running a similar Sunbelt playbook with significant market overlap in Atlanta, Charlotte, and Nashville. Cousins had roughly double Highwoods' market capitalization and a portfolio tilted toward the highest-end trophy assets, but the two companies were fishing in the same pond for tenants and development sites. Piedmont Office Realty Trust was also focused on Sunbelt office markets, though its portfolio included more suburban locations that would prove vulnerable in the post-pandemic world.

The differentiation came down to execution: market selection, development expertise, tenant relationships, and the willingness to be disciplined about what you would not own. Highwoods' advantage was its BBD framework, which gave the organization a clear decision-making filter for capital allocation. When a deal did not fit a BBD, the answer was no, regardless of how attractive the cap rate looked on a spreadsheet.

Highwoods had become a pure play on Sunbelt office, which was either a stroke of genius or a dangerous concentration bet. When the market was running in your direction, concentration felt like conviction. The question was what would happen when the market turned.

By February 2020, the stock hit its all-time high of $36.14. Ed Fritsch had retired the previous September after 37 years with the company, handing the CEO role to Ted Klinck. Klinck had joined Highwoods in 2012 as Chief Investment Officer after sixteen years at Morgan Stanley Real Estate, where he oversaw more than $15 billion in transactions. He held an MBA from the University of Georgia and a BBA from SMU, bringing institutional-grade capital markets sophistication to complement the local market expertise that Fritsch had cultivated.

Klinck had been promoted to President in November 2018, ensuring a smooth succession that had been planned years in advance. The balance sheet was clean, the development pipeline was full, and the Sunbelt thesis had never been more popular. Then the world changed.

COVID-19 and The Remote Work Earthquake

On March 11, 2020, the World Health Organization declared COVID-19 a global pandemic. Within days, office buildings across America emptied. The emptying was not gradual; it was instantaneous. One week, 50 million Americans commuted to offices. The next week, those offices were ghost towns. Lobby security guards scanned empty halls. Elevators sat motionless. The hum of HVAC systems provided the only sound in buildings designed for hundreds of workers.

For an office REIT, this was not merely a cyclical downturn of the kind the industry had survived before. It was an existential challenge to the fundamental premise of the business: that companies need physical space where employees gather to work. If remote work proved just as productive, if Zoom and Slack and cloud computing made the office obsolete, then owning 30 million square feet of office buildings was not a business. It was a liability.

The stock market rendered its judgment swiftly and mercilessly. Office REITs were brutalized, hit harder than nearly any other sector in the REIT universe. Industrial REITs, which owned warehouses and logistics centers, soared as e-commerce boomed. Data center REITs surged as the world moved online. Office REITs cratered. The market was pricing in permanent demand destruction.

But the early operating data told a more nuanced story than the stock price suggested.

In April 2020, the first full month of the shutdown, Highwoods collected 96 percent of contractually required rents. By May, the figure was 99 percent. By the third quarter, rent collections were running at 99.7 percent. Total rent deferrals granted represented barely one percent of annualized rental revenues. These numbers stunned industry observers, because they contradicted the narrative that office was dead. Tenants were not breaking leases. They were paying rent for buildings they were not physically using, largely because those tenants were creditworthy companies with long-term lease obligations they had no intention of abandoning.

The Sunbelt demographic story held up too, and in fact it accelerated. Population growth in Highwoods' markets did not reverse during the pandemic. Nashville, Raleigh, Charlotte, Tampa, and Atlanta all saw net in-migration during 2020 and 2021 as remote workers fled high-cost coastal cities for lower-cost Southern cities. The irony was thick: remote work, the very thing threatening office demand, was actually boosting population growth in Highwoods' markets.

Occupancy dipped, but modestly. From pre-pandemic levels around 91.4 percent, in-service occupancy fell to approximately 90.2 percent by the third quarter of 2020, a decline of only 120 basis points. Compare that to coastal gateway markets where vacancy rates surged by 500 to 1,000 basis points, with Manhattan and San Francisco seeing vacancies climb above 20 percent, and the Sunbelt resilience was striking.

Most remarkably, Highwoods increased its dividend. While peers were cutting payouts to conserve cash, and some, like Piedmont Office, would eventually halt dividends entirely, Highwoods raised its quarterly distribution. The message to the market was unmistakable: this company's cash flows were durable enough to not only maintain but grow shareholder returns during the worst crisis the office sector had ever faced.

But the easy part was collecting rent on existing leases. The hard part was the leasing environment going forward. New leasing velocity slowed dramatically as tenants deferred decisions, waited for clarity on return-to-office plans, and debated how much space they would need in a hybrid world.

The "return to office" versus "hybrid work" tug-of-war consumed corporate America for the next two years, with CEOs issuing edicts, employees pushing back, and the workplace strategy industry having its moment in the sun.

What emerged from this tug-of-war was a bifurcation that played directly into Highwoods' hand. The "flight to quality" trend that had been building for a decade went into overdrive. Companies that did bring employees back wanted those offices to be exceptional: Class A buildings in walkable, amenity-rich locations with modern ventilation systems, outdoor space, fitness facilities, and collaboration areas.

Class B and C buildings, the type Highwoods had spent a decade selling, saw vacancies spike and rents crater. Industry research suggested that a quarter of existing office space in America could be functionally obsolete by 2030, and roughly 60 percent would be at risk without significant capital investment.

Highwoods prudently hit the brakes on speculative development during 2020 and 2021, avoiding the trap of building into uncertain demand. But the company did not stop investing entirely. Capital expenditures shifted toward upgrading existing buildings, adding amenities, and making the portfolio what management called "commute-worthy." If employees had a choice about coming in, the building had better be worth the commute.

The pandemic revealed something fundamental about the office market that few had appreciated before: it is not one market but two. There is a market for high-quality, well-located, amenity-rich Class A space in the best neighborhoods, and there is a market for everything else. The first market contracted during COVID but proved resilient. The second market may never fully recover. The bifurcation was not new, but the pandemic accelerated it by a decade.

The pandemic did not kill the office. But it killed a certain kind of office. And Highwoods, by a combination of strategic foresight and a decade of portfolio pruning, had already gotten rid of exactly the kind of office that the pandemic rendered obsolete.

The New Normal: Repositioning for Hybrid Work

By 2022, a new consensus was forming across corporate America. Hybrid work was not a temporary experiment; it was permanent. But so was the office. Companies still needed physical space for collaboration, culture-building, client meetings, compliance activities, and the kind of spontaneous interaction that Zoom could not replicate. The question was how much space, what kind, and where.

The shift in tenant behavior was measurable. Fewer square feet per employee became the new standard. A company that once leased 200 square feet per worker might now target 150 or even 125. But the space that remained had to be dramatically better than what came before. The office had to compete with the home, and that meant gyms, outdoor terraces, food and beverage options, collaboration zones, quiet rooms, and a general atmosphere that made employees feel like they were gaining something by commuting rather than losing an hour of their day.

Highwoods' response was to lean into making its workplaces "commute-worthy" with a strategy they branded "Highwoodtizing." This meant upgrading lobbies, adding fitness centers, building rooftop terraces, installing customer lounges, and creating food and beverage options within properties.

In Nashville's Cool Springs submarket, Highwoods built a Central Park featuring food, beverage, a playground, and live music, an investment that helped backfill substantially all of a major 2023 lease expiration at the Ovation properties. The concept was straightforward: if an employee can get a great cup of coffee, eat lunch outdoors, and use a modern gym without leaving the office campus, the commute starts to feel less like a burden and more like a benefit.

Making an office park feel like a destination rather than an obligation was the new competitive battlefield, and Highwoods was investing accordingly. The company estimated that these amenitization investments typically generated returns well in excess of their cost by driving higher occupancy and better lease renewal rates.

The most significant strategic move of 2022 was the entry into the Dallas market through a joint venture with Granite Properties. The flagship investment was 23Springs, a 26-story, 626,000-square-foot Class AA office tower in Uptown Dallas, plus Granite Park Six, a 19-story building in Plano. Dallas offered the same Sunbelt characteristics Highwoods prized: population growth, corporate relocations, a business-friendly environment, and limited new supply in the best submarkets. The Dallas entry was an acknowledgment that even a focused company needed to expand its addressable market when the right opportunity appeared.

To fund the Dallas entry, Highwoods announced its intention to exit Pittsburgh, where it owned PPG Place and EQT Plaza. The company had purchased these properties at deep discounts during the post-financial-crisis period, and they had served their purpose. But Pittsburgh's office fundamentals had deteriorated, and the city no longer fit the Sunbelt BBD profile.

The sale process proved more challenging than expected. By early 2024, Highwoods put the Pittsburgh exit on hold due to unfavorable market conditions, handing property management to JLL while retaining ownership and waiting for better pricing.

The episode illustrated a reality of real estate investing that balance sheet models can obscure: you can only sell when someone is willing to buy, and in the post-pandemic office market, willing buyers for non-Sunbelt assets were scarce. Transaction volumes in the office sector had fallen to their lowest levels in over a decade. Lenders were cautious, appraisals were uncertain, and buyers were demanding discounts that sellers were not willing to accept. Pittsburgh became a reminder that even the best strategic plans are subject to market timing.

The financial headwinds of 2022 and 2023 were significant for the entire REIT sector. The Federal Reserve's aggressive rate-hiking campaign drove interest expense sharply higher for leveraged real estate companies. Inflation pushed up operating costs. And occupancy, which had been remarkably resilient during the initial pandemic phase, began to erode as pandemic-era leases expired and tenants right-sized their footprints for the hybrid era. Occupancy troughed at approximately 85 to 86 percent in 2024, well below pre-pandemic levels.

FFO told a mixed story. After reaching $4.03 per share in 2022, FFO declined to $3.61 in 2024 and $3.48 in 2025, reflecting the combined impact of higher interest costs, occupancy pressure, and the capital recycling program that temporarily reduced NOI from sold properties before replacement income came online from new developments.

Market-by-market performance divergence intensified during this period. Raleigh led with over 6 percent revenue growth and nearly 9 percent NOI growth, vindicating the company's home-market concentration. Charlotte also outperformed. Nashville continued to attract corporate investment. Meanwhile, Richmond lagged, and Highwoods began exiting that market in 2025, selling properties and transitioning management to Cushman and Wakefield. The company was still editing its portfolio, still pruning the weaker branches to feed the stronger ones.

Ted Klinck's four strategic tenets guided the company through this turbulent stretch: own well-differentiated office assets in the BBDs of its markets, maintain a fortress balance sheet, attract top talent, and communicate transparently.

The fortress balance sheet proved especially critical. Highwoods extended a $200 million term loan from 2026 to 2031, ensuring no consolidated debt maturities until 2027. Available liquidity stood at $625 million. The company also established a $300 million equity distribution agreement for future capital needs. In a sector where several peers faced debt walls and covenant risks, Highwoods' conservative financial management was not just prudent. It was a competitive advantage that allowed the company to play offense while others were scrambling to survive.

The leadership continuity through this period was notable. Unlike many REITs that cycled through management teams during the post-COVID turmoil, Highwoods had the benefit of a CEO who had been at the company since 2012 and understood both the capital markets side (from his Morgan Stanley years) and the operational side (from his CIO and President roles). Klinck did not panic. He did not make dramatic strategic pivots. He executed the same BBD-focused playbook that Fritsch had established, adapted for the new reality of hybrid work and higher interest rates. In a sector where investors crave stability, this consistency mattered.

Today and the Path Forward

As of early 2026, Highwoods Properties operates a portfolio of approximately 26.7 million square feet across eight markets: Atlanta, Charlotte, Dallas, Nashville, Orlando, Raleigh, Richmond (exiting), and Tampa. The portfolio carries a gross asset value north of $6.7 billion. The stock trades at roughly $21.90, giving the company a market capitalization of approximately $2.57 billion.

That gap between gross asset value and market cap reflects the persistent and deep discount that the public market applies to office real estate, a discount that either represents justified skepticism or a generational buying opportunity, depending on one's view of the office's future.

But the operating fundamentals paint a picture of a company accelerating out of a trough, and the gap between operating performance and stock price may be the most interesting tension in the entire office REIT sector today.

In 2025, Highwoods signed 3.2 million square feet of leases, the highest volume in ten years. GAAP rent spreads reached 16.4 percent overall, with new lease rent spreads hitting 18 percent, both record levels. Net effective rents ran approximately 20 percent higher than 2024 levels. The portfolio ended 2025 at over 89 percent leased, up from the trough, and management projects occupancy rising another 200 basis points by the end of 2026.

The development pipeline stands at $474 million, with 78 percent pre-leased, up from 56 percent a year earlier. The potential NOI growth from eight development buildings as they stabilize is estimated at $50 to $60 million, a meaningful increment on a company generating roughly $500 million in annual NOI. That represents 10 to 12 percent growth from development alone, before any contribution from acquisitions or same-property rent increases.

Management sees potential for up to $200 million of new development announcements in 2026, signaling confidence that the worst of the post-pandemic leasing drought is over.

The 2026 FFO guidance of $3.40 to $3.68 per share, with a midpoint of $3.54, represents a 5.7 percent increase over the initial 2025 outlook, the first meaningful growth trajectory in three years.

Recent capital allocation has been decisive. In November 2025, Highwoods acquired 6Hundred at Legacy Union in Charlotte for a total expected investment of $223 million. This is a 24-story Class AA tower with 411,000 square feet, 84 percent leased with a 12-year weighted average lease term. Class AA is not a standard industry designation; it represents the absolute top tier of office quality, the kind of building that tenants choose as a statement about their brand and their commitment to employee experience.

In January 2026, the company closed on the Bloc83 joint venture in Raleigh, a 492,000-square-foot complex at 97 percent leased, along with The Terraces in Dallas's Preston Center, 173,000 square feet at 98 percent leased. These were exactly the kind of trophy, near-fully-occupied assets in BBDs that the strategy prescribes.

On the most recent earnings call, Klinck cited "limited to no new supply" across core Sunbelt BBDs, describing a "convergence of occupancy gains, rental rate growth, and stabilization" of the development pipeline supporting "outsized NOI and earnings growth" over the next few years. With only $96 million remaining to fund the existing development pipeline, the balance sheet has capacity for both opportunistic acquisitions and new development starts.

On the ESG front, Highwoods has achieved a GRESB Green Star rating for four consecutive years, reached 100 ENERGY STAR certifications, and secured LEED and Fitwel certifications for all new wholly owned developments. The company met its 20 percent energy and greenhouse gas reduction goals three years ahead of schedule. These credentials increasingly matter to the corporate tenants Highwoods targets, particularly life sciences and technology firms with their own sustainability commitments. In a world where tenants are choosing between buildings, environmental certifications have become table stakes rather than differentiators.

Playbook: Business and Investing Lessons

The Highwoods story offers a wealth of lessons that extend well beyond commercial real estate and into the broader domains of capital allocation, strategic management, and long-term investing.

The first and most important lesson is the power of focus. Under Ed Fritsch, Highwoods deliberately shrank its portfolio, exiting markets, selling property types, and reducing headcount, all while growing revenues and NOI. The company sold over $1.4 billion in non-core buildings and still grew earnings. This runs counter to the empire-building instinct that dominates most corporate boardrooms. Capital allocation discipline, the willingness to sell assets that are merely good to concentrate on assets that are great, is a genuine source of competitive advantage. For investors, this is a pattern worth watching in any capital-intensive business. When management starts talking about "focus" and "core competencies" and actually follows through with divestitures, pay attention.

The second lesson is that real estate is profoundly local. Highwoods' BBD strategy was not about owning office buildings in the Sunbelt generically; it was about owning the best buildings in the best neighborhoods in specific cities. The difference between a trophy office tower in Nashville's Gulch and a commodity office park in suburban Memphis is not incremental; it is existential. One commands premium rents from blue-chip tenants who sign ten-year leases. The other competes on price, attracts tenants who leave at the first sign of a downturn, and generates returns that barely cover the cost of capital. Market selection matters more than property count. Submarket selection matters more than market selection. And building quality within a submarket matters most of all.

The third lesson concerns the value of riding secular trends with patience. The Sunbelt migration thesis that underpinned Highwoods' strategy played out over thirty years. Population growth, corporate relocations, and knowledge economy expansion in the Southeast were not short-term trades but multi-decade structural shifts. Highwoods bet on this thesis in 1994 and is still benefiting from it in 2026. The patience required to hold a geographic conviction through two recessions, a pandemic, and an interest rate cycle is something few investors possess, but the payoff for those who do can be substantial.

Balance sheet conservatism is the fourth lesson, and it is the one that separates survivors from casualties in every real estate cycle. Highwoods maintained its dividend through both the 2008 financial crisis and the 2020 pandemic. Multiple peers did not. The difference was leverage. Companies that stretched their balance sheets during the good times to juice returns found themselves unable to refinance, forced to sell assets at the worst possible moment, or compelled to slash dividends and destroy investor trust. In real estate, the single most important financial metric is not return on equity or FFO growth. It is whether you survive the next downturn with your dividend, your credit rating, and your strategic flexibility intact.

The REIT structure itself offers a unique lesson in the tension between discipline and constraint. The requirement to distribute 90 percent of taxable income means REITs cannot hoard cash the way a technology company can. This forces discipline: there is no cash pile to paper over bad capital allocation decisions. But it also limits strategic flexibility. When Highwoods needs capital for development or acquisitions, it must either sell assets, issue equity, or take on debt. The interplay between these levers is the art of REIT management.

Development as a source of returns deserves special mention. Ground-up development generates higher returns than acquisitions because the developer captures the spread between construction cost and stabilized value. But it requires execution: entitlements, construction management, leasing, and the willingness to take vacancy risk on speculative projects. Highwoods' development of the Asurion headquarters in Nashville, Bloc83 in Raleigh, and the Midtown Tampa projects illustrate how development can create irreplaceable assets that acquisitions cannot replicate.

Management quality is the final lesson. Ed Fritsch's 37-year tenure at Highwoods, including fifteen years as CEO, provided strategic clarity and institutional memory that is rare in any industry. He arrived before the company went public, lived through every market cycle, and had the conviction to implement a strategic plan that required the company to shrink before it could grow. Ted Klinck's succession was planned years in advance, ensuring continuity rather than disruption. The contrast with companies that change CEOs every five years, each bringing a new strategy that contradicts the last, could not be sharper.

Porter's Five Forces and Hamilton's Seven Powers

Understanding Highwoods' competitive position requires examining both the industry structure and the sources of durable advantage. These frameworks reveal where the company is strong, where it is vulnerable, and what its moat really looks like in a sector that does not produce moats the way Silicon Valley does.

Starting with Porter's framework, the threat of new entrants in Sunbelt office real estate is low but not zero. Building a Class A office tower requires hundreds of millions of dollars, years of development time, deep local relationships with tenants and brokers, and land in the right locations, land that is often already controlled by incumbents. A private equity firm with a checkbook cannot simply show up in Raleigh's BBD and replicate what Highwoods built over three decades. But capital can enter through acquisitions of existing buildings, particularly when distressed assets become available.

The bargaining power of suppliers is moderate and cyclical. Construction costs have been volatile, rising significantly during the post-pandemic period due to supply chain disruptions and labor shortages. A building that cost $200 per square foot to develop in 2018 might cost $280 in 2024. Capital markets access is the more critical supplier relationship: when credit is tight, the cost and availability of debt can constrain growth dramatically. Highwoods' investment-grade rating mitigates this risk but does not eliminate it.

Tenant bargaining power is the most consequential force in the post-pandemic office market. In submarkets with oversupply, tenants have significant leverage: they can demand free rent periods, tenant improvement allowances, shorter lease terms, or simply downsize. But in Highwoods' BBDs, where supply is constrained and demand from relocating companies remains robust, the landlord retains meaningful pricing power. The company's record 18 percent new lease rent spreads demonstrate that in the right submarkets, the flight to quality has shifted bargaining power back toward the owners of the best buildings.

The threat of substitutes is the elephant in the room. Remote work is the most powerful substitute for office space in history. It costs nothing, requires no commute, and for many knowledge workers, is at least as productive as in-office work for individual tasks. Coworking spaces and flexible office providers offer additional alternatives. However, the substitute threat has compressed demand per employee without eliminating demand altogether. Collaborative work, corporate culture, compliance requirements, and client-facing activities still require physical space. The net effect is that tenants want less space, but dramatically higher-quality space, a trend that benefits Highwoods at the expense of commodity office owners.

Industry rivalry is intense and structural. Highwoods competes with Cousins Properties, the most direct competitor with significant market overlap, as well as Piedmont Office, Brandywine, and numerous private landlords and institutional investors including pension funds and sovereign wealth funds that own office buildings directly. In weaker submarkets, one office building is interchangeable with another, and competition devolves into a price war that erodes margins for everyone. Highwoods differentiates through its BBD focus, development capabilities, and deep local relationships, but maintaining that differentiation requires constant reinvestment and operational excellence.

Turning to Hamilton Helmer's Seven Powers, Highwoods' moat is real but different from what you would find at a technology company. Scale economies are limited; office real estate does not benefit from network effects the way a software platform does. Branding power is moderate, recognized among regional tenants and brokers but not a consumer brand.

The three most relevant powers are cornered resource, switching costs, and process power.

Cornered resource is Highwoods' strongest competitive advantage: owning premier office buildings and development land in supply-constrained BBDs. Land in Raleigh's Research Triangle Park, Nashville's Gulch, or Midtown Tampa is scarce, and existing ownership confers an advantage that new entrants cannot easily replicate. You cannot build another Bloc83 or another 23Springs in the same location; those sites are taken. And in many of Highwoods' BBDs, zoning restrictions, infrastructure limitations, and community opposition to new development further constrain supply, creating a natural moat around existing assets.

Switching costs are moderate to high. Relocating a corporate office is expensive, disruptive, and involves long lead times. A typical office relocation costs $150 to $250 per square foot in moving expenses, furniture, IT infrastructure, and productivity loss. That creates significant inertia working in the landlord's favor when lease renewal time arrives.

Process power comes from decades of accumulated local market knowledge, development expertise, tenant relationships, and operational efficiency that cannot be acquired overnight. Knowing which Raleigh submarkets will attract the next wave of tech tenants, or which Nashville neighborhoods will draw the next corporate relocation, is knowledge that takes decades to build and is nearly impossible to replicate.

Counter-positioning played a historical role worth noting. When the large coastal REITs like Boston Properties, Vornado, and SL Green were focused on gateway cities and competing for trophy towers in Manhattan and San Francisco, Highwoods' exclusive Sunbelt focus was contrarian, even dismissed by some institutional investors who viewed secondary cities as lacking the prestige and liquidity of gateway markets. That positioning has been vindicated over time as Sunbelt office fundamentals have outperformed coastal markets, but the counter-positioning advantage has diminished as the Sunbelt thesis has become consensus and attracted more competition.

In sum, Highwoods' competitive position rests on three pillars: owning irreplaceable real estate in the right locations, locking in tenants with long-term leases that create recurring revenue, and leveraging deep local expertise that takes decades to build.

It is not a tech-company moat. There are no network effects compounding with each new user, no zero-marginal-cost scaling, no winner-take-all dynamics. But in the context of commercial real estate, where advantages are always local and always temporal, it is among the strongest competitive positions in the sector.

Bull vs. Bear Case and Investment Framework

The bull case for Highwoods starts with a simple observation: the stock is pricing in disaster while the operating fundamentals are improving. Trading below net asset value with a roughly 9 percent dividend yield, the market is either expecting significant further deterioration in office demand or a balance sheet event, and neither appears imminent given improving occupancy, record leasing spreads, a fortress balance sheet, and no debt maturities until 2027.

The Sunbelt migration is not a fad; it is a multi-decade structural shift driven by demographics, tax policy, cost of living, and employer preferences that shows no sign of reversing. Highwoods owns the physical infrastructure that corporate tenants need when they expand or relocate to the Southeast.

The flight to quality within office is accelerating, and Highwoods' Class A and Class AA buildings in BBDs are precisely the kind of space gaining market share from commodity office. There is a credible argument that the total addressable market for the specific type of office space Highwoods owns is actually growing, even as the broader office market contracts. When obsolete buildings are removed from supply and demand concentrates in the best remaining assets, the owners of those assets gain pricing power.

The development pipeline offers meaningful earnings growth potential. With $474 million of projects that are 78 percent pre-leased, the potential for $50 to $60 million of incremental NOI represents significant growth on a roughly $500 million base, and that is before considering up to $200 million in new development starts expected in 2026.

The dividend, at $2.00 per share annually, provides a substantial income stream while investors wait for the market to recognize improving fundamentals. Highwoods has paid dividends continuously since its 1994 IPO and increased the payout during the pandemic, a track record that speaks to management's confidence in cash flow durability. In a sector where income reliability is paramount, that unbroken dividend history carries real weight with institutional investors who allocate to REITs specifically for predictable cash yields.

The bear case centers on structural questions that improving lease spreads alone may not resolve.

Hybrid work has permanently reduced demand for office space per employee. Even as companies bring workers back, most are using less total space. Some studies estimate that average space per employee has declined 15 to 20 percent from pre-pandemic levels, and the trend shows no sign of reversing. This structural compression means that even in growing Sunbelt markets, net absorption may not return to pre-pandemic levels for years, if ever. If total office demand plateaus, even the best buildings face a ceiling on rent growth.

Geographic concentration is a real risk that merits serious attention. Highwoods is effectively a bet on eight Sunbelt markets.

A regional economic downturn concentrated in the Southeast, a major hurricane devastating Tampa or Orlando, or a reversal in corporate relocation patterns could disproportionately impact the portfolio in ways that a nationally diversified REIT would absorb more easily.

Interest rates remain a persistent headwind for the entire REIT sector, and office REITs in particular. Higher rates directly increase borrowing costs, reduce the present value of future cash flows in discounted cash flow models, and make dividend yields less attractive relative to risk-free alternatives like Treasury bonds. When a 10-year Treasury yields 4.5 percent, a 9 percent REIT yield needs to compensate for significantly more risk. If rates stay elevated longer than expected, REIT valuations may remain compressed regardless of how well the underlying properties perform.

The cautionary tale is visible in the peer group. Piedmont Office completely halted its dividend, an extraordinary step that illustrates what can happen when office fundamentals deteriorate faster than portfolio repositioning can keep pace.

Piedmont and Highwoods both operated in Sunbelt office markets, but the quality and location of their respective portfolios diverged significantly. The contrast between the two companies underscores the lesson that being in the right sector is not enough; you must be in the right buildings in the right submarkets within that sector. Highwoods is in a far stronger position, but the comparison serves as a sobering reminder of the genuine structural pressure facing the broader office REIT sector.

Technology disruption also deserves careful consideration. AI could reduce the need for certain categories of knowledge workers, particularly in back-office functions like data entry, basic analysis, and routine legal or financial work, and by extension reduce the office space they occupy. Conversely, AI could increase the value of in-person collaboration for the creative, strategic, and relationship-driven work that machines cannot replicate, potentially benefiting high-quality office environments designed for human interaction rather than individual screen time.

For investors tracking Highwoods' ongoing performance, two key performance indicators stand above the rest.

First, same-property cash NOI growth: this metric strips out the noise from acquisitions, dispositions, and development to reveal whether the existing portfolio is generating more or less income over time. Persistent positive same-property NOI growth indicates pricing power and tenant demand.

Second, leasing spreads on new and renewal leases: the difference between rents on new leases versus expiring leases indicates whether market rents are rising and the portfolio is marking to market at higher rates. This is a leading indicator of future revenue growth. The record 18 percent new lease spreads achieved in 2025 represent the single most bullish data point in the current Highwoods story and will be worth monitoring closely for durability.

The Future of Office and Highwoods

The office is evolving, not dying. The office of 2030 will look different from the office of 2019: smaller per capita, higher quality, more amenitized, and more intentionally designed for collaboration and culture rather than individual heads-down work. The buildings that meet this description will command premium rents and attract premium tenants who view physical workspace as a strategic asset rather than a cost center. The buildings that do not will join the growing roster of functionally obsolete properties being converted to residential, demolished, or simply sitting vacant.

Industry observers estimate that between 20 and 30 percent of America's existing office stock could face obsolescence over the coming decade, a shakeout that paradoxically benefits the owners of the best remaining assets by tightening supply in the most desirable locations. Think of it like the retail apocalypse of the late 2010s: when weaker malls and shopping centers closed, the surviving Class A malls saw foot traffic and rents increase because there was less competition for the same consumer base. The same dynamic may be playing out in office, with obsolescent buildings being removed from supply and demand concentrating in the best remaining properties.

Highwoods' next chapter may involve a smaller but more valuable portfolio. The Richmond exit, the Pittsburgh disposition effort (even if delayed), and the continued capital recycling suggest a company still refining its geographic footprint even after two decades of strategic pruning. The addition of Dallas and the deepening investment in Charlotte through the Legacy Union acquisition point toward a portfolio concentrating in the markets with the strongest multi-decade growth trajectories.

Management has not signaled any such expansion, but the optionality exists, and the development capabilities could transfer.

Strategic options on the corporate side also remain on the table. A merger with a peer like Cousins Properties, which shares significant market overlap in Atlanta, Charlotte, and Nashville, has been speculated about by analysts for years. Such a combination would create meaningful scale in the most attractive Sunbelt BBDs and generate cost synergies. A take-private transaction by a private equity firm looking to acquire Sunbelt office below replacement cost is another possibility, particularly given the current valuation discount. Highwoods could also expand into adjacent property types like life sciences, medical office, or lab space, leveraging its development capabilities into sectors with stronger growth profiles than traditional office.

The Sunbelt itself faces emerging challenges that will shape the next decade. Climate change is increasing hurricane, flood, and heat risks across the Southeast, with insurance costs rising sharply in Florida and coastal markets. Water scarcity and energy grid reliability are growing concerns, particularly in Texas where grid failures during extreme weather events have raised questions about infrastructure resilience. Infrastructure investment needs are mounting as population growth strains existing roads, transit systems, and utilities, with traffic congestion in Atlanta and Nashville reaching levels that rival the coastal cities many transplants fled.

Political dynamics could shift as formerly business-friendly states grapple with the consequences of rapid growth. Housing affordability, once a key advantage of Sunbelt cities over coastal alternatives, is eroding in markets like Nashville, Charlotte, and Raleigh as demand outpaces supply. Whether the Sunbelt can maintain its cost advantage over the next decade is an open question that directly affects Highwoods' thesis.

Technology will continue to reshape the landlord-tenant relationship in ways that are still emerging. Smart building systems that optimize energy use, monitor air quality, and track space utilization are becoming expected features in Class A office. Workplace analytics that help tenants understand how their employees actually use space can inform lease renewals. Flexible space configurations that can be reconfigured quickly for different team sizes are replacing the fixed cubicle layouts of the past. Landlords who invest in these capabilities will retain tenants. Those who do not will find their buildings competing on price alone.

Perhaps the biggest surprise in the Highwoods story is the one hiding in plain sight: that Sunbelt office actually worked after the pandemic. In a world that declared the office dead, a Raleigh-based REIT kept collecting rent, kept developing buildings, kept signing leases at record rents, and kept paying dividends. It did so not because it was lucky, but because it had spent fifteen years preparing for a crisis it could not have predicted by owning the best buildings in the best locations and maintaining the financial strength to weather any storm.

For founders and investors, the lesson transcends commercial real estate. Long-term thinking, the courage to focus when others are diversifying, contrarian positioning in markets the consensus has abandoned, and the discipline to allocate capital to the highest-returning opportunities rather than the most comfortable ones: these are the principles that built Highwoods from a 201-acre office park in Raleigh into a multi-billion-dollar portfolio of Sunbelt trophy assets. Whether the public market recognizes that value at the current stock price is the open question. The operating fundamentals continue to build the case. And in the meantime, the dividend keeps getting paid, the leases keep getting signed, and the buildings keep getting built, one BBD at a time, in the cities where America's workers are choosing to live.

Further Reading and References

For those looking to go deeper on the Highwoods story and the broader Sunbelt office thesis, the following resources are recommended:

Highwoods Properties Annual Reports from 2008, 2015, 2020, and 2024 provide the most direct window into management's strategic thinking at each inflection point, available on the company's investor relations site. The Brookings Institution's research on "The Rise of the Sunbelt" offers rigorous demographic and economic analysis of the migration trends that underpin Highwoods' markets. Green Street Advisors' research reports, particularly those arguing that "The Death of Office is Greatly Exaggerated," provide the most sophisticated analytical counter-narrative to the office-is-dead consensus.

NAREIT's office REIT research and white papers offer industry structure and trends data, while Ralph Block's "REITs and Real Estate Investing" remains the definitive guide to understanding REIT business models and valuation. Enrico Moretti's "The New Geography of Jobs" explains why certain cities win in the knowledge economy, a thesis that maps directly onto Highwoods' market selection. Harvard Business Review's post-COVID workplace research provides the academic foundation for understanding hybrid work's impact on office demand.

CoStar Group's market reports for Raleigh, Charlotte, Atlanta, Nashville, Dallas, and Tampa offer the granular submarket data that serious office REIT investors need. Bloomberg and Wall Street Journal coverage of the office REIT sector from 2020 through 2025 captures the real-time market sentiment shifts that created the current valuation disconnect. Finally, Ed Fritsch's interviews and investor presentations, available on the Highwoods investor relations site, articulate the BBD strategy in management's own words, providing strategic rationale from the architect who built the modern company over more than three decades.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube