HIVE Digital Technologies: Weaponizing Power from Bitcoin to AI

I. Introduction & The "Dual-Engine" Thesis

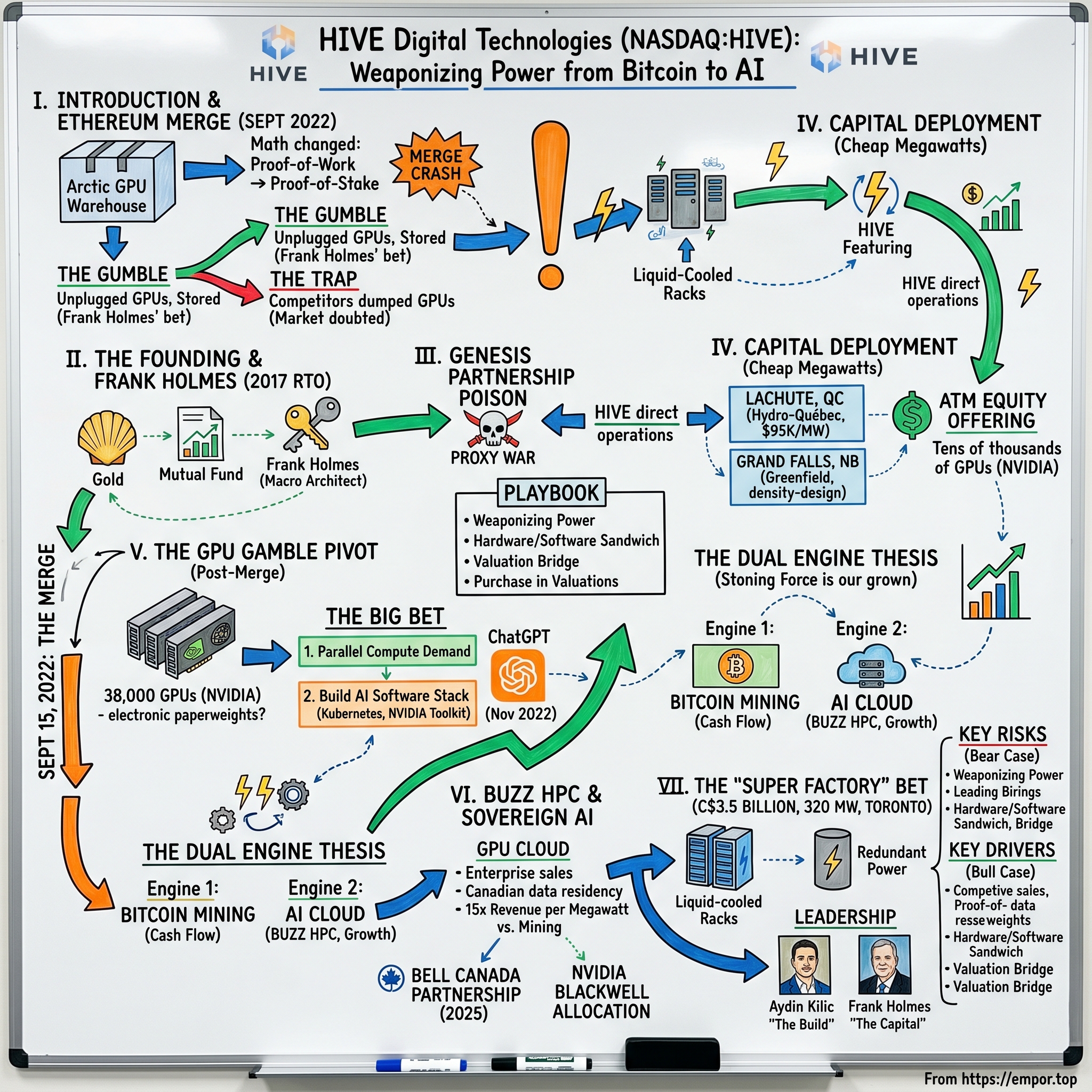

Picture a windowless warehouse in Boden, in northern Sverige (Sweden), in the autumn of 2022. The Arctic air is doing what nature designed it to do: it is pulling waste heat off thousands of stacked graphics cards through aluminum coils, allowing each chip to keep running at full clock speed without melting itself. For five years, those cards had performed a single, simple task. They guessed numbers. Specifically, they guessed cryptographic nonces in the Ethereum proof-of-work algorithm, racing other machines around the world to win a block reward roughly every thirteen seconds. The math behind that race was the only thing standing between HIVE Blockchain Technologies and bankruptcy.

Then, on September 15, 2022, the math changed. Ethereum's developers executed what cryptographers called "The Merge," migrating the world's second-largest blockchain from proof-of-work to proof-of-stake.1 Overnight, the 38,000 NVIDIA GPUs HIVE had spent four years acquiring became, in the eyes of the market, electronic paperweights. Competitors began dumping their RTX cards on eBay at twenty cents on the dollar.

HIVE did the opposite. The company unplugged the cards, wrapped them in anti-static covers, and stored them. Frank Holmes, the executive chairman, kept telling anyone who would listen that the GPUs would be worth more in twelve months than they were the day Ethereum forked. Almost no one believed him. Eighteen months later, after ChatGPT detonated global demand for parallel computing, those same cards were not just operating again — they were earning roughly fifteen times more revenue per megawatt than they ever had mining Ether.

That is the central trick of HIVE Digital Technologies: a Canadian crypto miner that quietly converted itself into one of the more interesting AI infrastructure plays on the NASDAQ. The company you are about to meet operates two engines. Engine one is Bitcoin mining, the cash-flow business that nobody loves and nobody fully prices. Engine two is BUZZ HPC, the GPU-cloud subsidiary that rents NVIDIA H100s and now H200s to enterprises, research labs, and a partnership with Bell Canada that is being explicitly branded as "sovereign AI."[^2]

The rebrand from HIVE Blockchain to HIVE Digital Technologies in July 2023 was not cosmetic.2 It was a deliberate attempt to bridge the valuation chasm between "cyclical commodity miner trading at 4x EBITDA" and "AI infrastructure pure-play trading at 30x revenue." Whether that bridge holds depends on a thesis we will return to repeatedly in this article: that owning the power, the building, and the silicon — what the team internally calls the "hardware/software sandwich" — is structurally more defensible than buying compute wholesale from a hyperscaler.

This story has all the Acquired hallmarks. A reverse takeover of a dormant gold shell company. A proxy war with the largest cloud-mining brand of the 2017 cycle. A near-death pivot triggered by an exogenous protocol change. And, in May 2026, the announcement of a C$3.5 billion, 320-megawatt AI campus on the edge of Toronto that, if completed, would make HIVE one of the largest privately developed compute campuses in Canada.3

The question we want to answer is simple. Did HIVE get lucky, or did it build something durable? To find out, we have to start where every great Canadian financial story tends to start: with a mining promoter, a shell company, and a phone call from Reykjavík.

II. The Founding & The Frank Holmes Factor

The man at the center of HIVE's origin story does not look like a crypto founder. Frank Holmes is in his late sixties, wears double-breasted suits to mining conferences, and has spent the bulk of his career running U.S. Global Investors — a San Antonio-based mutual fund company best known for its gold and precious-metals funds. Holmes is a CFA charterholder. He was born in Toronto, made his name in resource investing during the 1990s commodity supercycle, and developed an almost theological belief in two things: the macro power of monetary debasement, and the underappreciated arbitrage of stranded energy in northern latitudes.

In 2017, Bitcoin was racing toward $20,000 and Ethereum had just crossed $1,000 for the first time. A Hong Kong–based cloud-mining company called Genesis Mining, run by an Icelandic-German entrepreneur named Marco Streng, was sitting on a problem. Genesis had built an enormous mining footprint in Ísland (Iceland), drawn by geothermal and hydro power that ran around 4 cents per kilowatt-hour. But Genesis was a private company, and its investors — many of whom had bought "lifetime mining contracts" — wanted liquidity. The cleanest way to provide that liquidity, in the Canadian small-cap playbook, was a reverse takeover of a listed shell.

The shell they found was a dormant British Columbia company called Leeta Gold Corp. The transaction, completed in September 2017, vended Genesis's first-generation mining facilities into the public vehicle, rebranded it HIVE Blockchain Technologies, and listed it on the TSX Venture Exchange. Frank Holmes was installed as executive chairman. U.S. Global Investors took an investment stake. From day one, the pitch was specific: HIVE would be the first publicly traded crypto miner of meaningful scale, and it would be structured as institutional-grade — meaning audited financials, NI 43-101–style disclosure habits imported from mining, and a board with adults on it.

Holmes's contribution to the story is worth dwelling on because it explains why HIVE survived multiple crypto winters that vaporized peers. He understood three things instinctively that most crypto operators had to learn the hard way. First, in any capital-intensive commodity business, the lowest-cost producer wins, and your cost is dominated by the price of your input — in this case, electricity. Second, equity capital in a bull market is the cheapest capital you will ever access, and you should issue it aggressively when the window is open. Third, the equity itself is a marketing product; quarterly disclosures, conference appearances, and a steady drumbeat of "macro" framing are how you keep the multiple from collapsing.

So HIVE built where the power was cheap and the climate was cold. Iceland gave the company access to 100 percent renewable geothermal-and-hydro power. Sweden — specifically the northern industrial corridor near Boden, on the same grid that historically powered aluminum smelters and SCA paper mills — offered hydro power in the 3-to-4-cent range and ambient air cooling roughly nine months of the year. These were not exotic choices. They were the same logic that drove Alcoa to build smelters in Iceland in the 1960s: when you cannot move the electrons cheaply, you move the workload to where the electrons live.

The early bet was not on Bitcoin. It was on Ethereum. Bitcoin mining by late 2017 had already industrialized around ASIC chips — application-specific integrated circuits manufactured by Bitmain in Shenzhen, which were essentially impossible to source at scale unless you were on Jihan Wu's personal allocation list. Ethereum, by contrast, was still GPU-mineable, which meant HIVE could buy NVIDIA and AMD consumer cards through normal distributors. That created a vastly easier procurement story for a public-market vehicle that needed to deploy capital fast and show shareholders something happening on the ground.

It also created a dependency. Because Genesis had built the Iceland and Sweden facilities, Genesis still operated them. HIVE owned the boxes; Genesis kept the keys. That arrangement worked beautifully when crypto prices were rising. It was about to work catastrophically when they fell.

III. The Genesis Mining Era: A Partnership Turned Poison

By early 2019, the Bitcoin price had fallen from $19,000 to below $4,000, Ethereum was down 90 percent from its peak, and the entire industry was experiencing what insiders called the "long crypto winter." Every miner in the world was losing money. Every operator was cutting corners. And inside HIVE, a slow-burning conflict with Genesis Mining had reached the point of legal warfare.

The structure of the original 2017 deal had given Genesis two things at once: a large equity stake in HIVE, and a master services agreement under which Genesis ran HIVE's facilities for a fee. In a bull market, that alignment looked fine. In a bear market, the incentives split apart. Genesis was being paid to operate, regardless of whether the facilities were profitable. HIVE was being asked to fund operating losses and capex upgrades. The board began asking pointed questions about whether Genesis was meeting its service-level commitments, particularly on uptime and hashrate at the Swedish sites.

In March 2019, HIVE went public with its concerns. The company alleged "material breaches" of the operating agreement, accused Genesis of failing to deliver promised hashrate, and refused to make further payments under the contract. Genesis fired back almost immediately, attempting what the financial press generously called a "hostile board takeover." Because Genesis still held a significant equity block, it was able to requisition a special shareholder meeting and propose a slate of directors that would have effectively returned operational control to Genesis. The Canadian small-cap world watched in real time as a proxy war erupted inside one of the most-followed crypto names on the TSX-V.

The fight was resolved on June 28, 2019, when HIVE and Genesis announced a landmark settlement.[^5] The terms were not cheap. HIVE took ownership of the Swedish facilities outright, terminated the master services agreement, and assumed direct responsibility for operations. Genesis exited its operating role and significantly reduced its ownership over the subsequent quarters. In exchange, HIVE released its claims and avoided what would have been a long, distracting legal battle just as it needed to focus on surviving the winter.

The deeper story is what happened on the ground over the next twelve months. HIVE had to learn, very quickly, how to operate a facility it had never run. That meant hiring electricians, network engineers, firmware specialists, and most importantly, people who knew how to keep tens of thousands of GPUs from cooking themselves under load. The company brought in operators from the Nordic industrial sector — engineers who had worked at smelters, paper mills, and traditional data centers — and grafted them onto the existing crypto-native team. The cultural friction was real. But it produced the foundational capability that would matter most later: HIVE became one of the very few crypto miners that genuinely understood facility operations as a discipline, not as a service to be outsourced.

The most consequential hire of this era was Aydin Kilic. Kilic joined HIVE in 2021 from BitDigital, where he had run mining operations through the 2020 halving. He came in initially as president and chief operating officer, with a clear mandate: turn HIVE from a holding company that owned mining assets into an operating company that ran them. Kilic is a soft-spoken, technical operator — an electrical engineer by training, fluent in the physics of cooling and power distribution, and obsessed with operational KPIs that most crypto executives could not have defined. He would eventually be elevated to chief executive officer in 2023, completing what insiders described as the company's transition from "promoter-led" to "engineer-led."

The Genesis split, in retrospect, was the best thing that ever happened to HIVE. It forced the company to develop the operational muscle it would need for the next pivot. Independence was expensive, and it was uncomfortable, but it built the engineering culture that would later allow HIVE to do something almost no other crypto miner managed: rewrite its own software stack in eighteen months to support enterprise AI workloads.

But before that pivot, HIVE had to do something even more fundamental. It had to figure out how to grow without diluting itself into oblivion.

IV. Capital Deployment: The Art of the Cheap Megawatt

The single most important number in a crypto-mining business is not hashrate, market cap, or even Bitcoin price. It is the all-in cost per megawatt of installed capacity. Every other metric is downstream of that one. If you can build or buy a megawatt of power-connected, racked, cooled, and energized data center capacity for $100,000, you are competing in a different sport than the operator who is paying $300,000. Over a five-year horizon, that delta dwarfs almost any optimization on the operating side.

In April 2020, in the middle of the COVID lockdown, HIVE made what looked at the time like an opportunistic small acquisition. The company bought a 30-megawatt data center facility in Lachute, Québec, from a distressed seller for roughly US$4 million in cash plus assumed liabilities.4 That works out to a build-equivalent cost of around US$95,000 per megawatt — at a moment when industry consensus pegged greenfield construction at $250,000 per megawatt or more for comparable facilities. The Lachute deal was textbook distressed-asset arbitrage. Someone had spent the capex; COVID had wrecked their financing; HIVE arrived with cash and walked away with infrastructure at a discount that would have been impossible eighteen months earlier.

The Lachute facility also gave HIVE its first major foothold in Canada itself, which mattered for reasons beyond cost. Québec runs on Hydro-Québec power — overwhelmingly hydroelectric, priced for industrial users in the 4-to-5-cent range, and politically stable in ways that crypto-friendly jurisdictions like Kazakhstan, Iran, or even parts of the United States simply are not. For a company increasingly being asked by ESG-conscious institutional investors how it justified its energy footprint, being able to point at hydro power on the Canadian Shield was the difference between getting a meeting and getting hung up on.

The following year, in 2021, HIVE doubled down on the green-power thesis. The company committed approximately C$25 million to acquire and build out a 50-megawatt facility in Grand Falls, New Brunswick, leveraging the province's mix of hydro, nuclear, and wind generation. The Grand Falls site was different from Lachute in one critical respect: it was a greenfield project rather than a distressed acquisition. HIVE was signaling that it had developed enough operational confidence to build, not just buy. The cost-per-megawatt was higher than Lachute, but still well below industry benchmarks, and the site was designed from day one with the higher-density power distribution that GPUs require — a detail that would matter enormously when the AI pivot arrived.

Underwriting all of this expansion was a financing tool that crypto skeptics often deride and crypto operators quietly worship: the At-the-Market equity offering. An ATM is exactly what it sounds like. The company files a shelf prospectus, appoints a broker, and is then permitted to drip-issue new shares directly into the open market at prevailing prices, day after day, in modest volumes. It is the equity equivalent of dollar-cost averaging in reverse. In a bull market, when the stock is being bid up by retail enthusiasm for crypto exposure, an ATM functions as a controlled printing press — letting the company convert its own paper into hardware at attractive blended prices, without the discount-and-warrant package that a traditional bought deal would require.

HIVE used its ATM aggressively during the 2020-2021 bull cycle. The company issued hundreds of millions of dollars of equity at prices that, in retrospect, were lifetime highs. Critics called this dilutive. They were not wrong in arithmetic — the share count grew substantially. But the more useful question is what HIVE got in exchange. The answer was hardware. Specifically, tens of thousands of NVIDIA GPUs purchased through 2021, when the supply chain was constrained, lead times were six months, and the only way to get cards at all was to be a known buyer with cash in hand.

Did HIVE overpay for those GPUs? On the day of purchase, yes — almost every miner did, because the secondary market for cards had been distorted by gaming demand and the broader crypto bid. But there is a more interesting question lurking here: was the Bitcoin "HODL" strategy that HIVE pursued — holding mined Bitcoin on the balance sheet rather than selling it monthly to cover opex — the right call? In hindsight, partially. The Bitcoin that HIVE held through the 2022 crash was painful to mark down at the time but rebuilt dramatically as Bitcoin recovered toward and beyond $100,000 in 2024 and 2025. The lesson is less about timing and more about treasury philosophy: a Bitcoin miner that does not believe in Bitcoin's long-term thesis probably should not be a Bitcoin miner at all.

By the end of 2021, HIVE owned roughly 100 megawatts of power-connected capacity across four jurisdictions, a Bitcoin treasury that ran into the hundreds of millions of dollars at peak, and a fleet of ASIC and GPU hardware that put it in the top tier of publicly listed miners by hashrate. The thesis was working. And then, on September 15, 2022, the thesis broke.

V. The Inflection Point: "The Merge" & The GPU Gamble

Crypto people had been talking about The Merge for years. Ethereum's developers had publicly committed to migrating the network from proof-of-work to proof-of-stake since at least 2016. The migration kept slipping. Every six months there would be a new target date; every six months the date would move. By 2022, even seasoned Ethereum operators had begun to assume The Merge might never actually happen — or that if it did, it would happen in some far-off future after they had already depreciated their GPUs to zero.

It happened on September 15, 2022, at exactly 06:42:42 UTC, when the Ethereum mainnet transitioned to its new consensus algorithm.1 Within seconds, the global hashrate of Ethereum's proof-of-work chain — built up over seven years to a peak of roughly 1,000 terahashes per second — dropped to zero. Every GPU in the world that had been mining Ether woke up the next morning with nothing economically rational to do.

For HIVE, this was an existential moment. The company had built much of its 2020-2022 narrative around being the largest publicly traded Ethereum miner. Roughly 38,000 NVIDIA GPUs sat in its Swedish and Canadian facilities, accounting for a meaningful share of revenue and a much larger share of growth optionality. The market response was brutal. HIVE's share price, which had peaked above $30 in late 2021, was trading in the low single digits by October 2022. Every other publicly listed Ethereum miner — names like Hut 8, Hut 8's competitors, and a long tail of smaller operators — faced the same problem.

What most of them did was the rational thing. They liquidated. NVIDIA RTX 3080s, 3090s, and A4000s flooded the secondary market in the fall of 2022. Used-card prices on resellers like ePay collapsed to 25-30 cents on the dollar of original retail. Miners with debt-financed GPU fleets found themselves in technical default on equipment loans. Several smaller operators simply wound down.

HIVE did something different. The company's leadership — Frank Holmes from the macro chair, Aydin Kilic from the operations chair — made a bet that the GPUs were not garbage but rather under-employed. The argument, internally, was that NVIDIA had spent the previous decade quietly turning its graphics cards into the world's de facto parallel computing platform via CUDA, the proprietary software layer that lets developers run general-purpose code on GPUs. Anything that benefited from massive parallelism — scientific simulation, video rendering, and, increasingly, machine learning model training — could run on the same silicon that had been hashing Ethash.

The bet required two things to come true. First, demand for parallel compute outside of crypto had to grow fast enough to absorb the supply. Second, HIVE had to be able to actually deliver that compute to customers, which meant rebuilding its software stack from "miner" to "cloud provider." Neither was guaranteed.

So HIVE stored the GPUs. The company kept them powered down, racked in the Swedish facility, and began the laborious work of standing up a cloud platform. They hired developers fluent in Kubernetes, NVIDIA Container Toolkit, and SLURM — the workload management system that high-performance computing centers had used for decades. They built network plumbing capable of saturating 100-gigabit Ethernet links to neighboring racks, because machine learning training jobs require GPUs to talk to each other constantly. They began bidding on small academic and research workloads to prove that the platform could deliver SLA-grade uptime.

And then, on November 30, 2022, OpenAI released ChatGPT. Within sixty days, the global demand curve for GPU compute went vertical. By mid-2023, NVIDIA's data center revenue had more than doubled year-on-year, and the market price for renting an H100 GPU hour had climbed from around $2 to nearly $8 in some venues. The 38,000 cards that HIVE had refused to sell were suddenly the most strategically valuable inventory the company owned.

This is the moment the "dual engine" strategy was born — not as a marketing tagline, but as a description of what the business had actually become. Bitcoin mining was Engine One: the cash-generating, energy-arbitrage business that paid the bills and gave the company a defensible reason to control megawatts of cheap, clean power. AI cloud was Engine Two: the high-multiple growth business that could potentially re-rate the entire enterprise to a different valuation peer group. Neither engine, alone, would have justified the path. Together, they created an internal hedge: when Bitcoin was strong, the miners paid for AI capex; when AI was strong, the GPU cloud subsidized the miners.

But for the AI side to scale beyond opportunistic capacity, HIVE needed to give it a name, a brand, and eventually a separate operational identity. That subsidiary was BUZZ HPC.

VI. The Hidden Business: BUZZ HPC & Sovereign AI

If you visit hivedigitaltechnologies.com today, you will find references to BUZZ HPC scattered throughout the investor materials, but the brand is rarely featured front-and-center. There is a reason for that. BUZZ HPC was structured deliberately to operate as a distinct commercial entity — with its own go-to-market motion, its own enterprise sales team, and its own customer relationships — so that it could be valued separately by the market and, eventually, potentially spun out or partially monetized if conditions warranted.

The basic unit economics of BUZZ are what make the story interesting. A megawatt of Bitcoin mining capacity, under reasonable assumptions about hashprice and network difficulty, generates somewhere in the range of $1 million of annual revenue. That number bounces with Bitcoin's price and the global hashrate, but the order of magnitude is stable. A megawatt of GPU cloud capacity, by contrast — particularly one packed with modern H100 or H200 silicon, sold to enterprise customers at market rates — can generate $15 million of annual revenue or more. The leverage is staggering. Not 50 percent more, not 2x — more like 15x revenue per megawatt of identical electrical infrastructure.

The gross margins are different too. Bitcoin mining gross margins, after power costs but before depreciation, typically run somewhere in the 35-to-55 percent range depending on hashprice. AI cloud gross margins, after power and amortized hardware, can run in the 60-to-75 percent range for high-end GPUs on long-term contracts. The depreciation profile is faster — NVIDIA H100s arguably have a three-to-four-year useful economic life before they are displaced by next-generation parts — but the gross dollars per megawatt are so much higher that the math still works decisively in AI's favor.

The watershed moment for BUZZ as a commercial entity came in August 2025, when HIVE announced a partnership with Bell Canada to build out what the press release explicitly called "sovereign AI infrastructure."[^2] The word "sovereign" is doing a lot of work in that sentence. It signals that the compute is located in Canada, owned by Canadian shareholders, operated under Canadian data residency rules, and available to Canadian enterprises and government agencies that — for regulatory, security, or competitive-intelligence reasons — would prefer not to have their training data sitting on AWS in Virginia or on Azure in Iowa.

The sovereign AI thesis is bigger than HIVE and bigger than Canada. Across Europe, the Middle East, India, and increasingly Southeast Asia, governments and large enterprises have begun to view dependency on US-hyperscaler compute as a strategic vulnerability. The European Union's AI Act, India's data localization rules, and various national security reviews of AI workloads have all pushed in the same direction. There is a real, measurable willingness-to-pay premium for compute that is provably "in jurisdiction." Bell Canada brings to the partnership precisely what HIVE lacks: relationships with Canadian banks, telcos, hospital networks, and government departments that buy infrastructure based on procurement frameworks rather than crypto cycles. HIVE brings to the partnership what Bell lacks: actual installed GPU capacity, operational know-how, and a credible NVIDIA allocation.

That NVIDIA relationship deserves its own paragraph. By 2024, NVIDIA's product allocation had become arguably the most rationed scarce resource in technology. Hyperscalers, sovereign wealth funds, and well-capitalized AI labs were all competing for the same finite supply of H100s, H200s, and the forthcoming B200 "Blackwell" generation. NVIDIA's CEO Jensen Huang and his sales organization decided who got chips and in what order. HIVE, by virtue of being a long-standing NVIDIA customer through its mining era and having credible enterprise demand via the Bell partnership, was admitted to NVIDIA's Cloud Partner Program, which placed it in the institutional allocation queue for Blackwell-generation parts. For a company that had been written off as a "GPU dinosaur" in late 2022, being on the Blackwell allocation list in 2025 represented a remarkable reversal of fortune.

BUZZ HPC's customer mix, as best as can be assembled from public commentary, leans toward AI startups, academic and research institutions, and a growing pipeline of mid-market enterprise customers running everything from drug-discovery models to financial risk simulations. The platform is not trying to compete with AWS on every workload. It is trying to win the workloads where customers care most about Canadian data residency, predictable pricing on long-duration training jobs, and direct access to specific GPU SKUs without the multi-quarter waitlists that hyperscalers impose.

The hidden business is becoming the visible one. And the next thing HIVE planned to make visible was the largest single piece of greenfield infrastructure it had ever attempted.

VII. The "Super Factory" Bet: C$3.5 Billion in Toronto

On May 14, 2026 — less than a week before this article is being written — HIVE Digital Technologies announced what it described as the largest AI infrastructure commitment in Canadian history: a C$3.5 billion, 320-megawatt AI campus on a site in the Greater Toronto Area.3 The company branded it the "Super Factory," a term borrowed deliberately from the language Elon Musk has used to describe Tesla's gigafactories and which is now being widely repurposed across the AI infrastructure world.

The numbers, on first read, are arresting. C$3.5 billion across 320 megawatts works out to roughly C$10.9 million per megawatt of fully built-out, GPU-ready capacity. Compare that to the C$83,000 per megawatt that HIVE paid in Lachute six years earlier and the scale of the shift becomes obvious. The Lachute facility was Bitcoin mining infrastructure — concrete floor, basic ventilation, ASICs in open-air shelves. The Toronto Super Factory is something else entirely: liquid-cooled racks designed for NVIDIA B200 and beyond, redundant power feeds, Tier-3 mechanical and electrical reliability, low-latency fiber connectivity to the major Canadian financial and research networks, and physical security at a level that enterprise and government customers will actually accept.

The capex jump tells you something important about the company. HIVE is no longer playing the cheap-megawatt arbitrage game it perfected from 2020 to 2022. It is now playing a fundamentally different game: greenfield development of AI-grade data center capacity at industry-standard build costs, financed by a combination of project debt, equity issuance, and what is rumored to be significant strategic capital from infrastructure investors. The asset-light model — buy distressed crypto sites, retrofit them cheaply — has been replaced by an asset-heavy model in which HIVE is itself the developer, the operator, and ultimately the credit. This is a higher-risk, higher-reward profile, and it requires a different kind of competence than the one that built the original business.

The strategic logic, however, is internally consistent with everything that came before. HIVE's competitive position rests on owning the entire stack — the power permit, the building, the chip, the software layer, and the customer relationship. At the Lachute scale of US$4 million for 30 megawatts, you could prove the model. At the Toronto scale of C$3.5 billion for 320 megawatts, you can actually compete for hyperscale-adjacent workloads and, more importantly, lock in customers like Bell who need genuinely large blocks of dedicated compute. There is no middle path. You either stay small and accept that you are a niche provider, or you scale to the point where the hyperscalers consider you a viable alternative.

The execution risk is real, and any serious analyst should be honest about it. Building a 320-megawatt liquid-cooled AI campus is not the same as building a 30-megawatt Bitcoin mine. The supply chain is tighter — transformers, switchgear, and cooling equipment have multi-year lead times in the current AI buildout cycle. The labor market for data center construction is the tightest it has been in twenty years, with hyperscalers, telcos, and dozens of new AI infrastructure startups all bidding for the same contractors. Permitting in Ontario has improved under recent provincial policy changes, but the politics of large industrial electricity loads remain delicate, particularly as Ontario continues to wrestle with its long-term generation mix.

The role of leadership in navigating all of this becomes critical, and it reveals the elegant division of labor inside HIVE's executive office. Frank Holmes, the executive chairman, owns the capital story. He is the one who has spent two decades cultivating relationships with institutional investors, retail brokers, and the equity capital markets desks who will be syndicating the financing for the Super Factory. He is the one who appears on BNN Bloomberg making the case for "weaponizing power" — a phrase he has used with increasing frequency since 2024 — and who has the credibility to ask for billions in a market that is, justifiably, skeptical of crypto-adjacent issuers.[^7]

Aydin Kilic, the chief executive, owns the build. He is the one who has to deliver the megawatts on time, on budget, and at the technical specification that enterprise customers will actually pay premium prices for. Kilic's elevation to CEO in 2023 was a deliberate signal that the company's center of gravity had shifted from financial engineering to operational execution. If the Super Factory comes in on schedule by the planned phasing, Kilic will have validated a thesis that has been building for three years: that a former crypto miner can become a credible enterprise infrastructure operator.

If the Super Factory slips materially, every multiple HIVE has built in the public market will compress, and the bear case will write itself.

VIII. Management & Incentives

There is a useful exercise to do with any public company you are studying: read the proxy circular before you read the annual report. The proxy tells you who actually runs the place, how they get paid, what they get paid for, and how much of their own wealth is tied up in the outcome. With HIVE, that exercise is particularly illuminating because the two key executives sit on opposite ends of the operator-versus-financier spectrum and yet seem to function as a tight unit.

Frank Holmes, as we have established, is the macro architect. His day job remains running U.S. Global Investors, the San Antonio mutual fund company he has led for over thirty years. His HIVE role as executive chairman is, in practice, a part-time but very high-leverage one: he sets the capital allocation framework, leads investor communications, and serves as the public-facing voice on questions of strategy and crypto markets. Holmes's compensation at HIVE is structured to reflect the chairman role rather than full executive responsibility, but he has been a meaningful equity holder since the 2017 founding, which aligns his interests with long-term shareholders.

Aydin Kilic is the operator-in-chief. An electrical engineer by training with deep operational experience across multiple mining cycles, he brings to the CEO chair the rare combination of technical fluency and managerial discipline that the company will need to execute on the Toronto buildout. According to the management proxy circular, Kilic's directly-held stake represents approximately 0.28 percent of outstanding shares — a small percentage in absolute terms, but a meaningful dollar amount, and one that grows in importance as the company adds restricted share unit and option grants over time.[^8] The company maintains a 10 percent equity dilution cap for RSU and option pool issuance, which is roughly in line with US tech-industry norms and tighter than some Canadian small-cap peers.

What is most interesting about HIVE's incentive structure is what it now measures. In the company's earliest years, executive bonuses and milestones were tied principally to hashrate — the raw mining capacity HIVE had online, denominated in exahashes per second for Bitcoin and terahashes per second for Ethereum. Hashrate was the metric the company reported in monthly production updates, and it was the metric retail investors anchored to.

Hashrate is, however, a deeply imperfect proxy for actual economic value creation. A miner can have enormous hashrate and lose money every quarter if its power costs are too high or if it has bought hardware at the wrong point in the cycle. As the AI pivot took hold, HIVE began re-orienting both its public reporting and its internal compensation framework toward metrics that better capture the dual-engine reality: GPU utilization rates (what percentage of the cloud fleet is actually rented out), HPC revenue per available megawatt-hour, and customer contract duration. These are the metrics enterprise infrastructure investors actually care about. They are the metrics that will, over time, drive HIVE toward a different valuation peer group.

The shift in incentives is doing more than just changing the bonus pool math. It is changing who the company hires. The 2024 and 2025 senior engineering hires at HIVE and BUZZ HPC have come not from the crypto-miner world but from enterprise infrastructure, cloud operations, and traditional high-performance computing. The cultural transformation is incomplete, but it is real, and it is being driven from the top.

The skin-in-the-game story is, for a CEO of a publicly listed company at this stage of growth, reasonable. It is not the kind of founder-controlled, 30-percent-insider structure that would make a Buffett-style investor weep with joy. But it is not the kind of professional-management, zero-skin structure that should send anyone running, either. Kilic and Holmes own enough of the company that they are personally exposed to the outcome of the Super Factory bet, and they have repeatedly demonstrated through behavior — particularly the decision to hold the GPUs through The Merge rather than liquidate — that they are willing to make uncomfortable long-term bets rather than chase short-term optics.

That orientation matters more than any single line in the proxy. It is what makes the next few years actually investable, rather than merely interesting.

IX. Playbook: Business & Investing Lessons

Step back from the chronology for a moment and HIVE's story compresses into three transferable lessons that apply far beyond crypto or AI.

The first is what Frank Holmes calls "weaponizing power." In a world where energy is increasingly the binding constraint on economic activity — whether for AI training, electric vehicle charging, industrial reshoring, or simple residential demand growth — a long-dated power permit is an option on the most profitable use of an electron at any given point in the future. The asset itself, the megawatts connected to the grid, is durable. What runs on top of those megawatts can change. HIVE has now demonstrated, over a five-year window, that the same megawatts can be Ethereum mining, then Bitcoin mining, then AI training, then potentially something else again. The permit is the moat. The chips on top of it are the rotating cast.

This insight generalizes. Companies that own irreplaceable infrastructure rights — water permits in arid regions, port concessions, rail rights-of-way, frequency spectrum, grid interconnection queue positions — are increasingly being re-rated in public markets because investors are starting to understand that the underlying option value is durable across many possible end-state uses. HIVE's specific contribution to this thinking is the speed and visibility of the demonstration. Few companies have so cleanly proven that the same physical asset can produce two entirely different revenue streams from two entirely different industries within a five-year window.

The second lesson is what we will call the hardware/software sandwich. The most defensible position in any compute business is not just owning the chip, and not just renting it out. It is owning the entire stack: the power permit at the bottom, the building, the chip, the software layer that schedules workloads onto the chip, and the customer relationship at the top. Each layer of the sandwich provides a small piece of margin protection. Owning all of them simultaneously creates compounding defensibility. A pure-play GPU reseller competes on price every quarter. A hyperscaler buries the chip in a black-box service and competes on platform features. HIVE's positioning — control the facility, control the chip, control the cloud layer — is a middle path that offers both transparency to enterprise customers and structurally better margins than a pure reseller.

The hyperscaler comparison is worth dwelling on because it frames the competitive question correctly. AWS, Azure, and Google Cloud will win the majority of generic enterprise AI workloads. That is not in dispute. What they will not necessarily win is the segment of customers who care about specific data residency, who want predictable long-term pricing on dedicated capacity, who need access to specific GPU SKUs without multi-quarter waitlists, and who would prefer to deal with a counterparty whose entire business is GPU compute rather than one for whom GPUs are a small slice of a sprawling cloud catalog. That segment is real, it is growing, and it is exactly where BUZZ is positioned.

The third lesson is the valuation bridge. HIVE has been engaged, since the 2023 rebrand, in a deliberate attempt to migrate from one valuation peer group to another. Public-market valuations for cyclical commodity miners typically range from 3x to 6x EBITDA. Public-market valuations for AI infrastructure pure-plays range from 15x to 40x EBITDA or higher, depending on growth and contract visibility. The difference between those two ranges, applied to even a modest base of cash flows, can change the equity value of a business by a factor of five or more.

The bridge cannot be built by press releases alone. It is built by demonstrating, quarter after quarter, that an increasing share of revenue and EBITDA comes from the higher-multiple business. As BUZZ HPC's contribution to total revenue grows — first to 25 percent, then to 40 percent, then potentially above 50 percent as the Toronto Super Factory comes online — the weighted-average multiple investors will assign to HIVE should compress upward toward the AI infrastructure end of the spectrum. The risk, of course, is that the bridge does not get built fast enough, or that AI infrastructure multiples themselves compress before HIVE can complete the transition.

This valuation arbitrage is not unique to HIVE. Companies as different as IBM (re-rating around AI and hybrid cloud), Schlumberger (re-rating around energy transition services), and many smaller industrials have attempted the same playbook. What makes HIVE's version distinctive is the speed and the cleanliness. The pivot did not require entering a new geography, acquiring a new business, or building a new sales channel. It required only repurposing existing electrons and existing silicon for a new workload. When the pivot works, it works fast.

The playbook, in summary, is power plus stack plus narrative. Power gives you optionality, stack gives you margin, and narrative gives you the equity capital to compound. Miss any one of the three and the model breaks. Get all three right and you produce, in HIVE's specific case, the chance to transition from a $500-million-market-cap cyclical curiosity to a multi-billion-dollar infrastructure name.

X. Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Frameworks are most useful when they constrain how you think about a business rather than when they decorate a slide. With HIVE, three of Hamilton Helmer's 7 Powers map cleanly onto the actual competitive dynamics. The other four either do not apply or apply weakly enough that they are not worth dwelling on.

The clearest of the three is Scale Economies. The economics of AI data centers favor large operators in ways that compound over time. NVIDIA's product allocation system, in particular, rewards customers who can take large volumes — a 10,000-GPU order goes to the front of the line, a 100-GPU order waits. The Toronto Super Factory, at 320 megawatts, is large enough to credibly request Blackwell allocations in volume that smaller operators simply cannot match. The same scale advantage shows up in power procurement (large industrial loads negotiate better tariffs), in construction (large general contractors will work with you), and in customer acquisition (enterprise customers care about counterparty size).

The second is Switching Costs, applied to the AI cloud business rather than the mining business. Once a customer has trained a model on BUZZ HPC's infrastructure, the data, the trained weights, and the operational tooling all live on or near that infrastructure. Moving to a competing cloud is technically possible but expensive — terabytes of model weights have to be physically transferred, retraining pipelines have to be reconfigured, and any custom integration with BUZZ's scheduling layer has to be rebuilt. This data-gravity effect is the same dynamic that has made it so hard for enterprises to leave AWS even when cheaper alternatives appear. It is a real moat, though one that takes years to build at scale.

The third is Cornered Resource, and it is arguably the most underappreciated. Licensed power allocations in Canada have become structurally scarce. Ontario's grid interconnection queue, Québec's industrial tariff allocations, and New Brunswick's provincial power agreements all face multi-year waitlists for new large industrial loads. A company that already holds those allocations — as HIVE does, across its existing footprint — possesses something that genuinely cannot be replicated by a competitor with unlimited capital. The Super Factory's Ontario allocation, in particular, is the kind of resource that took years to secure and would take a new entrant years to match. This is a different kind of moat from technology or brand. It is a physical-world scarcity that the market is just beginning to price.

The other Helmer powers — Network Economies, Counter-Positioning, Branding, and Process Power — apply weakly or not at all in HIVE's case. The business does not benefit from network effects in the way a marketplace does. Counter-positioning would require the hyperscalers to be structurally unable to copy what HIVE does, which is not really true. Branding is genuine but limited. Process Power, the kind of proprietary operational know-how that takes decades to develop, is something HIVE is building but cannot yet claim.

Now turn the lens around with Porter's Five Forces.

The threat of new entrants is moderate-to-high. Building a 30-megawatt crypto mine is something anyone with capital can do. Building a 300-megawatt AI campus is materially harder — power allocations, supply chain access, and customer trust take years to assemble. The scale-economy and cornered-resource dynamics described above push this force down over time.

The threat of substitutes is real and worth taking seriously. Customers who need GPU compute can buy it from AWS, Azure, Google Cloud, Oracle, CoreWeave, Lambda Labs, Crusoe, Nebius, or any number of newer AI cloud entrants. On generic workloads, the hyperscalers are the substitute, and they have effectively unlimited capital. HIVE's defense is the sovereign / specialized AI niche, which is genuine but is also being targeted by every other Tier-2 cloud provider in the market.

The bargaining power of suppliers is currently enormous. NVIDIA effectively dictates timing, pricing, and product mix for the entire industry, with allocation rationed at the CEO level. Until competitive silicon — from AMD, from custom ASIC efforts like AWS's Trainium and Google's TPUs, or from emerging players — meaningfully erodes NVIDIA's position, every cloud provider faces the same supplier-power dynamic. There is no special weakness here for HIVE versus peers.

The bargaining power of buyers is moderate. Large enterprise customers can negotiate hard on multi-year contracts, but the current undersupply of AI compute gives infrastructure providers the upper hand for as long as the shortage persists. The interesting question is what happens when, eventually, supply catches up to demand and pricing normalizes. The defensibility built up during the shortage — switching costs, customer integration, brand — will determine who survives the normalization.

The intensity of rivalry is the trickiest force to assess. Among Tier-2 AI cloud providers — CoreWeave, Lambda, Crusoe, Nebius, and others — rivalry is high and getting higher, with each player attempting to lock down customers, GPU allocations, and power infrastructure simultaneously. HIVE's positioning in Canada, with its sovereign AI partnership with Bell, gives it a degree of geographic differentiation that pure-play US competitors do not have. But the rivalry is real, and it will likely intensify as more capital floods into the space.

The framework analysis lands on a single thesis. HIVE's moat is not yet wide, but it is identifiable, defensible, and growing. The combination of scale economies (chips and power), switching costs (data gravity), and cornered resources (Canadian power permits) gives the company a plausible path to durable competitive advantage. None of those moats is unique to HIVE, but the combination, at the scale and in the jurisdiction in which HIVE is operating, is rare.

XI. Conclusion & The Bear/Bull Case

Every investable story has a bull case and a bear case worth taking seriously. With HIVE, both are unusually specific, which is itself a good sign — businesses with vague narratives in both directions are usually businesses to avoid.

The bull case starts with the Super Factory delivering on schedule. If the Toronto campus comes online in phases through 2027 and 2028, and if BUZZ HPC's enterprise pipeline converts at anything close to the rate the Bell partnership suggests, the AI revenue line could overtake Bitcoin mining revenue within twenty-four months of first power at the new site. At that point, the question of valuation peer group becomes settled: HIVE trades as an AI infrastructure name, with the multiple compression toward 20x to 30x EBITDA that comes with that classification. Layer on top a continued Bitcoin bull market, a stabilized hashprice environment, and the existing Bitcoin treasury — and the equity story compounds from multiple directions simultaneously. In the most optimistic scenario, HIVE becomes what some Canadian analysts have begun calling the "Digital Utility" of Canada — a regulated-feeling infrastructure provider with growth optionality attached.

The bear case is equally specific and worth respecting. The first failure mode is GPU oversupply. If the global AI infrastructure buildout outruns end-customer demand — and there are credible voices in the industry warning of exactly this — rental rates for H100 and B200 capacity could fall faster than HIVE's economic models assume. A 30 percent compression in GPU-hour pricing could turn the Toronto Super Factory from an obvious win into a marginal investment, particularly if the build-out cost runs over.

The second failure mode is Bitcoin price collapse. The Toronto project is large enough that HIVE will need to fund a meaningful portion of it through a combination of project debt, ATM issuance, and operating cash flow. If Bitcoin enters a deep and sustained drawdown during the build-out window, both the operating cash flow and the equity capital markets access could dry up simultaneously. The company would face an unhappy choice between slowing the project (and ceding the AI infrastructure window to faster-moving competitors) or pushing through with worse financing terms.

The third failure mode is execution risk. Building Tier-3 AI data centers at the 320-megawatt scale is something that hyperscalers have learned to do well over fifteen years. HIVE has done it at the 30- and 50-megawatt scale, on legacy infrastructure, retrofitted for crypto mining. The leap to greenfield, hyperscale-adjacent enterprise infrastructure is real, and there is genuine schedule risk in every major piece — power energization, cooling commissioning, network buildout, customer migration. A six-month slip is recoverable. An eighteen-month slip would be deeply damaging to the equity story.

A myth-vs-reality fact-check is worth running here, because the consensus narratives in both directions get parts of the story wrong. The myth on the bull side is that HIVE has already become an AI company. The reality is that, on a trailing-twelve-month basis, Bitcoin mining still produces the majority of revenue and substantially all of the operating cash flow. The AI transition is genuine and accelerating, but it is not yet complete, and any analyst who treats HIVE as a pure AI play is mispricing the cyclical risk. Conversely, the myth on the bear side is that HIVE is just another crypto miner riding the AI hype train. The reality is that the company has built genuine operational capabilities — engineering depth, NVIDIA allocation, enterprise customer relationships through Bell — that materially differentiate it from peers who issued AI press releases without doing the underlying work.

For investors who want to track the story over the next several years, the KPIs that actually matter narrow down to a short list. The most important is the share of total revenue and gross profit coming from HPC and AI cloud services — the higher this number, the more the multiple should re-rate. The second is utilization of installed GPU capacity at BUZZ HPC, which tells you whether the infrastructure is actually being rented out at premium prices or sitting idle. The third is build-cost-per-megawatt at the Toronto Super Factory as it phases in, which will reveal whether HIVE can deliver on the asset-heavy buildout at the budget it has publicly committed to. Watch those three numbers; everything else is secondary.

A brief second-layer note worth flagging: HIVE operates in an environment of layered regulatory and ESG scrutiny that should be on every investor's radar. Bitcoin mining remains politically contested in multiple jurisdictions, with periodic proposals in Canadian provinces and US states to restrict industrial crypto loads or impose surcharge tariffs. AI data centers are starting to face similar scrutiny over water consumption, grid impact, and embodied carbon. The "green energy" framing that HIVE has cultivated for nearly a decade — hydro in Canada, geothermal in Iceland — is a real ESG asset, but it is not a permanent shield. Investors should also watch for any disclosure changes around segment reporting as BUZZ HPC becomes more material; a clean breakout of HPC revenue, contract duration, and unit economics would be one of the strongest possible signals that management is preparing for a re-rating event, possibly even a partial spinout of the subsidiary.

There is something deeply Canadian about this entire story. A reverse takeover of a gold mining shell. A proxy fight that gets settled rather than litigated to death. A bet on cheap hydroelectric power in the provinces. A pivot that requires not flashy reinvention but quiet, disciplined operational work. Frank Holmes, a Toronto-born CFA running a mutual fund in San Antonio, partnered with Aydin Kilic, an electrical engineer building data centers in Lachute and Boden, executing a plan to compete with Silicon Valley's AI giants from a 320-megawatt campus outside Toronto.

The market will decide whether the dual engine is a coherent business or a marketing construct holding two incompatible halves together. The next twenty-four months — first power at Toronto, the next leg of the Bitcoin cycle, and the trajectory of NVIDIA's product roadmap — will provide the answer. For now, what can be said with confidence is this: a company that, in 2022, had every reason to liquidate its GPUs and quietly fade away instead chose to store them, retrain its own people, and bet that the world would eventually need every parallel computing cycle it could find. So far, the bet has paid. The harder bet is the one being placed in Toronto right now.

References

-

The Ethereum Merge and its Impact on Miners — Reuters, 2022-09-15 ↩↩

-

HIVE Rebrands to HIVE Digital Technologies to Reflect AI Pivot — Nasdaq, 2023-07-12 ↩

-

HIVE Announces Massive C$3.5 Billion AI Super Factory in Toronto — News Release, 2026-05-14 ↩↩

-

HIVE Acquires 30 MW Quebec Data Center for US$4 Million — HIVE Digital, 2020-04-08 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube