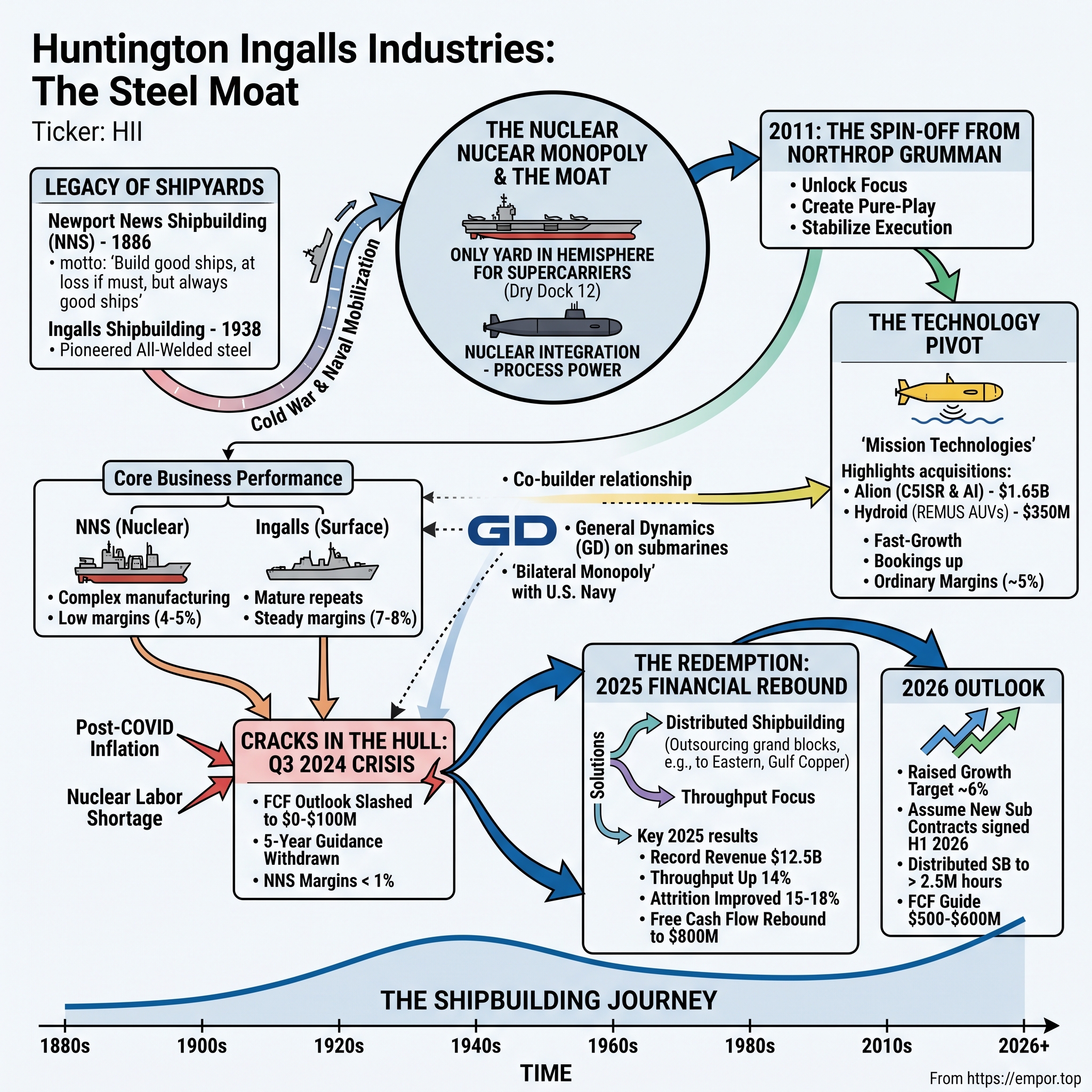

Huntington Ingalls Industries: The Steel Moat of American Sea Power

There is a dry dock in Virginia that is, quite literally, one of one. Dry Dock 12 at Newport News Shipbuilding is the only graving dock in the Western Hemisphere large enough to assemble a Gerald R. Ford-class nuclear aircraft carrier — 100,000 tons of steel, a floating city with two reactors, launching and recovering aircraft in the middle of an ocean. If that dock and the workforce around it disappeared, the United States would not be able to build another supercarrier. Not next year, not for a decade, not without spending a sum of money that begins to rival the cost of the ships themselves.

That single fact contains the whole strange story of Huntington Ingalls Industries. This is a company whose product is so complex, so capital-intensive, and so strategically essential that it has effectively no competitors for its most important work — and yet whose returns, for long stretches, have looked more like those of a struggling industrial contractor than a monopolist. It is a business built on the most durable moat in American industry and, simultaneously, one of its most punishing cost structures. Understanding how both things are true at once is the point of this episode.

I. Introduction & Episode Roadmap

How does a company that makes its living bending heavy steel and welding nuclear reactor compartments come to hold an absolute monopoly over the ultimate instrument of global power projection — the nuclear-powered aircraft carrier? And why, if that monopoly is so complete, did its stock lose more than a quarter of its value in a single trading day?

Huntington Ingalls Industries, Inc. — ticker HII, listed on the NYSE — is the largest military shipbuilder in the United States. In fiscal year 2025 it generated $12.5 billion in revenue, an 8.2% increase over the prior year, and reported full-year diluted earnings of $15.39 per share.1 Behind that revenue sits a backlog of roughly $48 billion in contracted work — years of guaranteed demand from a single, overwhelming customer.1

To grasp the scale, hold a few concrete facts in mind. HII employs roughly 44,000 people, the overwhelming majority of them in two shipyards and their surrounding communities.3 It is not a diversified industrial with a shipbuilding arm; it is American military shipbuilding, plus a growing technology-services business bolted on the side. When you buy a share of HII, you are buying a claim on the earnings of two irreplaceable industrial facilities and the skilled workforce inside them — and on the multi-decade stream of contracts the U.S. government will place through them.

That customer is the United States Navy, and the relationship between the two is the analytical heart of this story. It is a bilateral monopoly: essentially one buyer of strategic hulls and, for the most critical of them, one supplier capable of building them. The Navy cannot let HII fail, because HII's yards are the industrial base for carriers and a large share of the submarine fleet. But HII cannot walk away from the Navy either, because there is no other customer on Earth for a $13 billion aircraft carrier. Each side has enormous power over the other, and neither can leave the table. Most of what looks strange about HII's financials — the thin margins, the lumpy cash flow, the recurring contract disputes — flows from that structural fact.

Here is the roadmap for the next two hours. We will trace HII's arc from a neglected division inside an aerospace-and-electronics conglomerate to a focused, publicly traded pure-play shipbuilder. We will dig into the brutal unit economics of nuclear shipbuilding — the capital intensity, the fixed-price contract traps, and the post-pandemic skilled-labor crisis that nearly broke the model. We will benchmark the company's digital pivot, including its $1.65 billion acquisition of Alion Science and Technology and the rise of its high-tech Mission Technologies division. We will relive the Q3 2024 cash-flow crisis, when free cash flow collapsed and the stock cratered 26% in a day, and then the 2025 rebound that followed. And we will examine the operational bet management is now making — a strategy it calls "distributed shipbuilding" — to route around a labor shortage it cannot simply hire its way out of.

Throughout, we will keep the investor's central question in front of us: does HII win from here because it owns an unassailable industrial monopoly, or is that monopoly a gilded trap — 100% market share in a market whose only buyer sets the price? Let's start where the steel does, on two riverbanks more than a century apart.

II. The Legacy of the Shipyards: Huntington, Ingalls, and the Nation-Building Era

Picture the James River in Virginia in the 1880s. A railroad baron named Collis Potter Huntington had already pushed the Chesapeake and Ohio Railway eastward to a sleepy tidewater spot called Newport News, so that Appalachian coal could reach deep water and be loaded onto ships. But Huntington was not a man who liked to hand the last, most profitable link in a chain to someone else. If ships were going to carry his coal, he reasoned, he might as well build the ships. In 1886 he founded the Newport News Shipbuilding and Dry Dock Company, and he chose a motto that still hangs over the yard: "We shall build good ships here — at a profit if we can, at a loss if we must, but always good ships."6

That last clause — at a loss if we must — turns out to be uncannily prophetic. More than a century later, it reads less like a founder's boast than a description of the company's actual cost accounting.

Newport News grew up alongside American naval ambition itself. When Theodore Roosevelt wanted to announce to the world that the United States had arrived as an industrial and naval power, he sent the Great White Fleet steaming around the globe — and several of those battleships had been built on the James. The yard became a place where national ambition was translated directly into tonnage. If Washington wanted to project power, Newport News was where the projection got welded together.

Six hundred miles to the southwest, on the Gulf Coast, a second story began in 1938. Robert Ingersoll Ingalls Sr. founded Ingalls Shipbuilding on the east bank of the Pascagoula River in Mississippi, and he did something quietly radical: he bet on all-welded steel construction. For decades ships had been built by overlapping steel plates and hammering them together with rivets — slow, heavy, labor-intensive. Ingalls's first ship, delivered in 1940, was among the first with a hull whose plates were welded end to end.6 Welding was faster, lighter, and cheaper, and it arrived just in time: within a few years the United States would need to build ships at industrial scale for a world war. The technique that Ingalls pioneered helped make that possible.

Both yards were forged in the same crucible — the Second World War and then the Cold War — and both became primary engines of American sea power. The Second World War turned them into arsenals. Yards like Newport News and Ingalls churned out warships and cargo hulls at a tempo that is almost impossible to imagine today, part of the industrial mobilization that let the United States out-build every adversary at sea. That wartime experience left a permanent imprint: these were not job shops but institutions, with their own training pipelines, their own trade cultures, and a workforce that passed skills from one generation to the next on the deck plate. That intergenerational transfer of tacit knowledge — the kind of thing that lives in a veteran welder's hands, not in a manual — is precisely the asset that would fray decades later, and its erosion sits at the center of the modern story.

But it was Newport News that took the decisive technological leap. In 1960 the yard launched the USS Enterprise (CVN 65), the world's first nuclear-powered aircraft carrier, and in 1972 it delivered the USS Nimitz (CVN 68), lead ship of the class that would define the American carrier fleet for half a century.6 Nuclear propulsion changed everything. A conventionally powered ship is tethered to fuel and to the tankers and ports that supply it; a nuclear carrier can steam for roughly two decades between refuelings, turning it into a mobile sovereign airfield that can loiter anywhere in the world for months without asking anyone's permission. That is the entire strategic proposition of American sea power in one hull.

Mastering reactor integration — building a controlled nuclear power plant inside a warship and getting it certified to standards set by the Navy's famously exacting nuclear-propulsion establishment — was the moat-deepening act. Consider what it actually requires: a workforce cleared and qualified to handle nuclear components, facilities built and certified for reactor work, decades of accumulated process knowledge about how to weld, inspect, and integrate systems where a defect is not a warranty claim but a catastrophe, and a regulatory relationship that cannot be replicated by writing a check. This is why no one else in the hemisphere can do this work, and why the moat is measured not in market share but in the sheer impossibility of anyone else standing up the capability. It is also, as we will see, why the returns are so hard-won: the same complexity that keeps competitors out keeps costs stubbornly high.

Here is the tension worth carrying forward. HII's physical plant — the enormous graving docks, the gantry cranes, the concentrated workforce — was purpose-built for a 20th-century model of mobilization: vast, physical, blue-collar, and permanent. It was a triumph of an industrial age. But the products the Navy now demands are increasingly software-defined, sensor-laden, and iterative, and the skilled workforce that once filled those yards has thinned. Modern management is, in effect, trying to run a 21st-century enterprise inside a 20th-century footprint. How that legacy asset base became both HII's greatest strength and its heaviest constraint is the thread that runs through everything that follows — including the corporate decision, decades later, to cut these yards loose entirely.

III. The Northrop Grumman Era & The 2011 Spin-Off: Releasing the Drag

By the turn of the millennium, the two historic shipyards had been swept up in the great defense-industry consolidation that followed the Cold War. In 2001, aerospace-and-electronics giant Northrop Grumman acquired Litton Industries — which owned Ingalls — and then Newport News Shipbuilding, folding both into a new unit called Northrop Grumman Shipbuilding.5 On paper, it looked like empire-building: one company that could build the Navy's electronics, its aircraft, and its ships. In practice, it was a marriage of businesses that did not belong under the same roof.

The mismatch was financial before it was cultural. Northrop's aerospace and defense-electronics businesses threw off double-digit operating margins on comparatively modest capital. Shipbuilding was the opposite animal. Its margins ran in the mid-single digits in a good year. It demanded relentless, heavy capital expenditure — dry docks, cranes, nuclear-qualified facilities that cost hundreds of millions and paid back over decades. And its cash conversion cycle was measured not in quarters but in years: a submarine or carrier takes the better part of a decade to build, with cash tied up in work-in-progress the entire time. For a conglomerate whose investors prized capital-light, high-return electronics, shipbuilding was a persistent drag on blended returns — a business that consumed cash and reported losses on exactly the kind of fixed-price development programs that could blow a hole in a quarter.

There is a general lesson here that recurs across corporate history: when you bolt together two businesses with fundamentally different margin profiles, capital intensities, and risk characteristics, the market does not average them — it discounts the whole. The high-return business gets dragged down in the valuation, and the low-return business never gets the focused management attention it needs. Northrop's leadership eventually saw it clearly.

So on March 31, 2011, Northrop Grumman spun off its shipbuilding operations as an independent, publicly traded company: Huntington Ingalls Industries. The separation was structured as a tax-free pro-rata distribution — Northrop shareholders simply received shares of the new entity — and it was championed by Northrop CEO Wes Bush as a way to sharpen the returns of the remaining aerospace-and-electronics company.5 In one motion, the two riverbank shipyards that had built American sea power for a century were set free to sink or swim on their own.

The timing of the 2011 separation is worth pausing on, because it tells you something about how the parent viewed the asset. Northrop cut shipbuilding loose during a period of defense-budget uncertainty, not at a market top — this was a portfolio-cleanup decision, a deliberate choice to hand shareholders a business the parent no longer wanted to carry rather than a celebrated growth story being set free to soar. HII began public life, in effect, as a spun-off orphan: an unglamorous, capital-heavy industrial with a fortress franchise but a reputation for lumpy execution. Early on, the market treated it accordingly, valuing it well below the aerospace-and-electronics multiples that its former parent commanded. In one sense, that discount was the whole opportunity — a durable monopoly trading like a troubled contractor. In another, it was the market pricing in exactly the risk that would eventually materialize in 2024: that the returns on this business are structurally thin and periodically fragile.

The early post-spin playbook was not glamorous, and it was not supposed to be. Freed from corporate overhead and from competing for capital against higher-return sibling divisions, HII's first job was blocking and tackling: stabilize shipyard throughput, lock in multi-year procurement contracts that gave the yards predictable work, and impose basic operational discipline on programs that had a history of overruns. For a while, it worked. As a focused pure-play, HII could tell investors a clean story — a fortress backlog, an irreplaceable industrial position, and steadily improving execution. The question the spin-off left unanswered, and that the next fifteen years would test, is whether focus alone can fix a business whose core economics are dictated by a single customer. To see why that question is so hard, we have to go inside the business itself.

IV. The Core Business: Inside the Nuclear Monopoly and the Surface Duopoly

Walk the two yards and you are really looking at two different companies stapled together, plus a third that barely touches steel at all.

The larger of the two shipbuilding engines is Newport News Shipbuilding (NNS), which generated $6.5 billion of revenue in FY2025 — roughly 52% of the company — at a 5.1% operating margin, itself an improvement from a depressed 4.1% the year before.2 This is the crown-jewel business and, paradoxically, the lower-margin one. Newport News builds and refuels nuclear aircraft carriers and builds a large share of the nuclear submarine fleet. It is the most complex manufacturing in the HII portfolio, and complexity, as we will see, is exactly what compresses its margins.

The second engine is Ingalls Shipbuilding, which contributed $3.1 billion of revenue in FY2025 — about a quarter of the total — at a 7.6% operating margin.2 Ingalls builds surface combatants and amphibious warships: Arleigh Burke-class destroyers, the Navy's big-deck amphibious assault ships and their smaller amphibious transport docks, and the Coast Guard's National Security Cutters. Its work is conventionally powered — no reactors — and its programs are more mature and repeatable. That combination is why Ingalls has been the steadier, higher-margin cash generator, the quiet workhorse that funds the drama up in Virginia.

The third leg, Mission Technologies, we will hold for the next section, because it is a different business entirely.

The flagship programs: what the yards are actually building

To make the economics concrete, it helps to know what is physically on the ways. At Newport News, the carrier franchise is anchored by the Gerald R. Ford class. The lead ship delivered years ago; the second, CVN 79 John F. Kennedy, spent 2025 completing dock trials and moving into sea trials on the path to delivery. Behind it, the two-carrier contract for CVN 80 Enterprise and CVN 81 Doris Miller is in construction — CVN 80 reached 50% erected in the dry dock during 2025 — and Congress authorized a block buy for the next pair, CVN 82 and CVN 83, in the FY2026 defense bill.12 A carrier is a decade-long build and, when refuelings and inactivations are added, Newport News effectively has a carrier relationship with the Navy that never ends. The yard also performs the mid-life refueling and complex overhaul (RCOH) of Nimitz-class carriers — a multi-year, multi-billion-dollar job of defueling and re-fueling a reactor and modernizing the ship — including the USS John C. Stennis, whose overhaul was one of the programs that generated a negative charge in the 2024 crisis.3

On the submarine side, Newport News builds portions of every Virginia-class boat and delivered SSN 798 Massachusetts in 2025 while launching SSN 800 Arkansas.2 The strategic prize is Columbia, and the fact that Newport News delivered the bow of the first boat — District of Columbia — rather than the whole submarine is a reminder of the co-builder structure that caps its share of the program.2 At Ingalls, meanwhile, the destroyer line runs on the Arleigh Burke Flight III (DDG 128 Ted Stevens delivered, DDG 129 launched, DDG 135 Thad Cochran's keel laid in 2025), alongside the amphibious ships and the exotic three-ship Zumwalt class, which Ingalls has been modifying to carry hypersonic missiles.2

The reason this inventory matters to an investor is that each program is at a different point on its cost curve, and HII's blended margin is simply the weighted average of ships priced in very different eras. A lead ship or a first-of-class is where money is lost; a mature repeat build is where it is made. Much of what looks like management drama is really the mix of the portfolio shifting under the accounting.

The structure of the industry: a duopoly with one referee

To understand HII's competitive position, you have to understand that in major U.S. naval shipbuilding there is really only one peer: General Dynamics (GD), through its Marine Systems group. GD owns Electric Boat, the submarine builder; Bath Iron Works, which builds destroyers; and NASSCO, which builds auxiliary and support ships.12 Between them, HII and GD are the American naval shipbuilding industry. That is the whole market.

But here is the twist that makes this less of a cage match than it sounds. The two companies are not only rivals — on the most important programs, they are co-builders. Building nuclear submarines is so complex, and the required throughput so high, that the Navy has deliberately structured the work so that neither company can do it alone. On the Virginia-class fast-attack submarines, HII's Newport News and GD's Electric Boat split the construction and then alternate final assembly and delivery, teaming rather than competing on each hull. On the Columbia-class ballistic-missile submarine — the single most important program in the Navy's shipbuilding plan, since it carries the sea-based leg of the nuclear deterrent — Newport News builds major sections (including the bow, and it delivered the first Columbia bow in 2025) as a subcontractor to Electric Boat, which serves as prime.2 The economics of that arrangement matter: on parts of these programs HII is effectively a supplier to its own competitor, which caps both its pricing leverage and its margin.

On surface ships, the "competition" is really a managed split. For the newest Arleigh Burke (DDG 51) Flight III destroyers, the Navy deliberately divides awards between HII's Ingalls and GD's Bath Iron Works — not to drive a hard price war, but to keep two destroyer yards alive so that the industrial base has redundancy. The buyer is protecting its suppliers from each other.

Around the edges sit the fringe players. Austal USA builds aluminum and steel littoral and auxiliary ships, and Fincantieri Marinette Marine — the U.S. arm of Italy's Fincantieri — is building the Navy's new Constellation-class frigates. These are real companies doing real work, but they compete in niches that don't touch HII's nuclear franchise. No one is entering the carrier or nuclear-submarine business.

There is a cautionary tale for HII watchers buried in that frigate program, and it is worth a moment of second-layer diligence. The Constellation class was supposed to be a low-risk buy based on a proven European parent design — and it has been beset by design churn, weight growth, and multi-year schedule slips. The lesson is not that Fincantieri is uniquely troubled; it is that every modern naval program, even one billed as low-risk, runs into the same immovable constraints — skilled labor, design maturity, and supply chain — that mauled HII in 2024. It is a reminder that the difficulties at Newport News are not a company-specific failing so much as the physics of the industry, which cuts both ways: it excuses some of HII's stumbles, and it warns that the new frigate and "battleship" franchises HII is now chasing will not be easy money either.

Seven Powers and Five Forces: anatomy of the moat

It is worth being precise about why the moat is so deep, using Hamilton Helmer's 7 Powers framework, because the sources of durable advantage here are unusually clean.

Scale economies, taken to an extreme. Dry Dock 12 at Newport News is the only dock in the Western Hemisphere capable of building a Ford-class carrier. That is not a figure of speech — it is a physical asset that exists in exactly one place, and duplicating it would be a national-scale infrastructure project. The minimum efficient scale for building a supercarrier is, essentially, "be Newport News."

Switching costs that approach infinity. The Navy cannot simply take its carrier program to another builder. There is no other builder. Standing up a rival nuclear-qualified yard — the facilities, the reactor-handling certifications, the trained workforce, the regulatory approvals — would cost a staggering sum and take the better part of a generation. For the customer, the cost of switching is measured in decades and in strategic risk it cannot accept.

A cornered resource in human form. The moat is not only concrete and steel; it is people. The concentrated pools of nuclear-qualified welders, pipefitters, and engineers in the Newport News region of Virginia and around Pascagoula, Mississippi are themselves a scarce, hard-to-replicate asset. You cannot conjure a nuclear-certified welder overnight; the training pipeline runs for years. As we will see, this cornered resource is also the company's single greatest vulnerability — because a cornered resource you are struggling to retain stops being a moat and starts being a bottleneck.

Process power through systemic complexity. Coordinating millions of individual parts, integrating a nuclear reactor, and satisfying exacting military and regulatory standards across a seven-to-ten-year build cycle is an organizational capability that cannot be bought off a shelf. It is embedded in the routines, the tooling, and the institutional memory of the yards.

Now run it through Porter's Five Forces and the picture sharpens further — with one critical qualification.

Threat of new entrants: essentially zero. The capital and regulatory hurdles are, for practical purposes, insurmountable. No private actor is going to build a competing nuclear shipyard on spec.

Threat of substitutes: low, but not nil. Some defense theorists argue the future belongs to swarms of cheap, uncrewed surface and undersea vessels rather than a handful of exquisite, expensive capital ships — and the Navy is genuinely experimenting with a "hybrid fleet." That is a real long-term debate. But for now, nuclear carriers and submarines remain the core of American power projection, and the demand signal points up, not down.

Bargaining power of buyers: this is where the moat inverts. Yes, HII faces every one of the classic protections — but it faces exactly one customer, and that customer is a monopsonist with the full power of the U.S. government behind it. The Navy sets the requirements, controls the appropriations, writes the contract terms, and audits the costs. It can — and does — push hard on price. The saving grace, and it is a real one, is that the Navy's monopsony power is checked by its own dependence: it needs HII solvent and building, so it frequently subsidizes the company's capital improvements and workforce training, including through submarine industrial-base funding tied to national-security priorities.9

The strange economics of a buyer that subsidizes its supplier

Here is a dynamic you almost never see in a normal industry, and it is essential to understanding HII: the monopsony buyer routinely puts money into its supplier's factories. Because the Navy's demand for submarines has run ahead of the industrial base's capacity to build them, Congress has appropriated billions in "submarine industrial base" funding to expand and stabilize the supply chain — money that flows largely to HII's and Electric Boat's suppliers but also benefits the prime yards directly, funding tooling, facilities, and workforce development.9 During the 2024 crisis, management repeatedly referenced an initiative it called the SAWS plan — a Navy proposal to reallocate funding toward higher wages and infrastructure at the yards right now, before later boats begin construction. Kastner endorsed it on the Q3 2024 call as "an excellent idea" precisely because, in his words, it unlocked investment "without needing any more funding."3

The same episode surfaced a startling number: a bipartisan group of senators warned of a potential $17 billion funding shortfall on the Virginia-class program over roughly six years — a measure of just how far the cost of building submarines had outrun the budgets set for them years earlier.3 Kastner declined to endorse that specific figure, but he did not dispute the underlying reality: the budgets written for these boats predated the inflation and labor disruption that followed, and the whole multi-year negotiation with the Navy was, at bottom, an argument about who absorbs that gap.

This is the monopsony relationship in its full strangeness. The Navy has immense power to dictate price — and simultaneously a national-security interest in keeping HII healthy enough to keep building. It squeezes with one hand and subsidizes with the other. For investors, the practical implication is that HII's returns are not set by a market clearing price at all; they are the negotiated output of a bargaining process between a company that cannot be allowed to fail and a customer that cannot be replaced. That is a more stable arrangement than a competitive market in some ways, and a more constrained one in others.

That is the paradox in a sentence: HII has a 100% share of a market whose single buyer sets its prices. The moat guarantees the demand. It does not guarantee the returns. Everything about HII as an investment turns on that distinction — and the company's response has been to try to build a second business where the pricing dynamics might be kinder.

V. The Technology Pivot: Mission Technologies and the Alion Acquisition

If you were running a company whose core business had an impregnable moat but structurally capped returns, what would you do? You would go looking for growth and margin somewhere the government buys differently — where the product is software and services rather than steel, where contracts turn over in months rather than decades, and where you are not the only bidder but also not competing against your own reactor-handling costs.

That is the logic behind HII's third division, now called Mission Technologies. The pitch is straightforward: heavy shipbuilding is a mature, slow-growth business, so build out a higher-velocity operation that captures defense budgets for software, artificial intelligence, C5ISR (the military's shorthand for command, control, communications, computers, cyber, intelligence, surveillance, and reconnaissance), electronic warfare, cyber, and uncrewed systems. In FY2025, Mission Technologies crossed $3.0 billion of revenue for the first time — about 24% of HII — at a 5.0% operating margin, up from 3.9% the prior year.2

The division was assembled substantially by acquisition, and two deals define it.

The larger was Alion Science and Technology, which HII agreed in July 2021 to buy from private-equity firm Veritas Capital for $1.65 billion in cash, closing that August.[^8] Alion brought digital, AI, and defense-engineering capabilities — precisely the C5ISR and technical-services work HII wanted. On the numbers management disclosed, HII expected Alion to contribute roughly $1.6 billion of revenue and about $135 million of adjusted EBITDA in 2022, which put the purchase at roughly 12.2 times expected 2022 adjusted EBITDA.7 That multiple sat comfortably inside the 10x–19x band that premium government-services businesses were fetching in that cycle — HII was paying a full but not obviously reckless price for scale in a hot market.

The deal had a financial hangover, though, and it is worth naming plainly. HII funded the purchase with debt, and the added leverage prompted S&P Global Ratings to revise its outlook on the company to negative — an analytical judgment that the acquisition had, at least temporarily, weakened the balance sheet in exchange for a lower-margin services business.8 That is the skeptic's framing of the whole Mission Technologies project: HII took on debt to buy revenue that carries margins lower than its own shipyards, then asked investors to believe the mix would improve over time.

The smaller but strategically pointed deal came a year earlier. In March 2020, HII completed its $350 million acquisition of Hydroid, the maker of the REMUS line of autonomous underwater vehicles.[^10] REMUS — think of a torpedo-shaped robot submarine that can map the seafloor, hunt mines, or conduct surveillance without a crew — gave HII a genuine foothold in uncrewed undersea systems, a capability the Navy increasingly wants. On the disclosed economics, the price represented a high-teens multiple of the business's near-term EBITDA, or a somewhat lower effective multiple after tax benefits — a rich number, but a small check for a strategic option on the future of undersea warfare.

The bookings tell a better story than the margins

If you want to see why management remains bullish on the division despite its ordinary margins, look at the order flow rather than the income statement. In the third quarter of 2024 alone — the same quarter the shipyards were melting down — Mission Technologies booked roughly $11 billion of potential contract value, a record for the division, headlined by a $6.7 billion single-award contract to provide electronic-warfare engineering and technical services to the U.S. Air Force, the largest award in the division's history.3 It also grew revenue at a double-digit clip that year while the shipyards shrank. In other words, the fast-growth thesis for Mission Technologies is real on the top line even where it disappoints on the bottom line.

Management has also been reshaping the division for efficiency, consolidating it from six business units down to four to concentrate on higher-growth areas — C5ISR, electronic warfare, cyber, and uncrewed systems — and to lower its bid cost structure.3 And it has been pushing the aperture wider: the division sees international openings tied to allied programs, including work adjacent to the AUKUS submarine partnership among Australia, the United Kingdom, and the United States, and it develops the Navy's Minotaur mission-system software that ties sensors and platforms together. The strategic logic is coherent — sit at the intersection of manned and unmanned, own the autonomy software, and ride budgets that grow faster than steel.

So how should an independent observer grade Mission Technologies today? The honest answer is: promising at the edges, ordinary in the middle. On the Q4 2025 earnings call in February 2026, management pointed to real momentum in the crown-jewel product lines — the delivery of HII's 750th REMUS vehicle, the debut of a new family of uncrewed surface vessels called Romulus running on the company's own Odyssey autonomy software, and delivery of small uncrewed undersea vehicles to the Navy.2 These uncrewed systems provide genuine optionality, and they map directly onto the Navy's hybrid-fleet strategy; CEO Chris Kastner called autonomy the division's single largest source of internal R&D spending. That is the bull's exhibit A.

But the reality check is that the bulk of Mission Technologies is still lower-margin IT services and systems integration, much of it on cost-type contracts where fees are capped by design. The 5.0% operating margin tells the story: this is not the software-like, high-margin business some investors hoped HII was buying. On the same call, the CFO conceded that roughly 80–85% of the division's work is cost-type, and that lifting margins depends on shifting the mix toward products over studies — a slow, unfinished project.3 Mission Technologies has diversified HII's customer base and given it exposure to faster-growing budgets. It has not yet transformed the company's return profile. And whatever optionality it adds sits atop a shipbuilding core that, in the autumn of 2024, suddenly looked like it might be broken.

VI. The Cracks in the Hull: The Q3 2024 Crisis and the Labor Bottleneck

On the morning of October 31, 2024, HII reported its third-quarter results, and the market's reaction was violent. The stock fell roughly 26% in a single session — shedding more than $65 a share — one of the worst days in the company's history as a public company.4 For a business whose entire investment thesis rests on the predictability of a fortress backlog, the speed of the collapse was itself the message: something in the model was not as reliable as advertised.

Peel back the release and the anatomy of the miss was ugly on three fronts.

First, the earnings crater. Third-quarter earnings came in at $2.56 per share, down sharply from $3.70 a year earlier, and well below what analysts had modeled.3 Operating income for the quarter fell more than 50% year over year, and consolidated operating margin compressed to 3.0% from 6.1%.3 The engine room of the problem was Newport News, where operating margin collapsed to just 1.1% from 6.2% — the nuclear crown jewel briefly earning almost nothing.3

Second, and more alarming, the cash-flow bomb. Coming into 2024, management had guided full-year free cash flow to $600–$700 million. On this call they slashed it to a range of zero to $100 million — and it would ultimately land at just $40 million for the year.3 For a company that had built its investor reputation on meeting or beating its cash targets year after year, a roughly $600 million evaporation of forecast cash was a credibility event, not just an earnings event.

Third, and most telling, management withdrew its five-year (2024–2028) cumulative free-cash-flow outlook entirely.3 CFO Tom Stiehle framed it almost apologetically on the call, noting that the company held its guidance "near and dear" and had met or exceeded it every year since 2019 — and that pulling a multi-year target was an admission that, right now, they could not credibly forecast the out-years.3 When a management team stops giving you a number rather than give you a worse one, that is a signal worth taking seriously.

What actually broke

Kastner and Stiehle attributed the damage to two intertwined causes, and the distinction between them matters for whether you believe the problem is temporary or structural.

The first was a fixed-price legacy trap. As Kastner put it bluntly on the call, "nearly all the ships currently under construction were negotiated prior to COVID."3 Those contracts — priced years earlier — baked in cost assumptions and risk-sharing clauses that never contemplated the post-pandemic reality: 9%-plus inflation on materials and wages for a stretch, a fragile supply chain, and a workforce that had lost a generation of experience to early retirements. Under a fixed-price incentive contract, that inflation is HII's problem to absorb, not the Navy's. The company was, in effect, still delivering ships at yesterday's prices using today's costs.

The second was the nuclear labor crisis, and it is the one that should keep investors up at night because it is a physical constraint, not an accounting one. A severe shortage of experienced skilled tradespeople — welders, pipefitters, nuclear technicians — combined with an influx of inexperienced "green" labor, produced inefficiency and, worse, rework. On the Virginia-class Block IV submarines, the yard hit rework it had not anticipated as boats neared critical test milestones, forcing schedule slips. Newport News booked $78 million of net unfavorable cumulative adjustments in the quarter, including $34 million tied to the Block IV submarines, $16 million on the two-carrier CVN 80/81 contract, and $14 million on a carrier refueling overhaul.3 Layered on top was a separately disclosed welding-procedure issue involving, in the company's words, fewer than two dozen welders — small in scope but corrosive to confidence.3

There was also a strategic overhang looming behind the numbers: a long-awaited "17-ship" omnibus submarine agreement — covering Virginia-class Block V and Block VI and Columbia Build 2 — that HII had expected to sign in the second half of 2024, and that would have unlocked investment and reset the portfolio to current-cost terms. The timing and structure of that deal had gone uncertain, and management had risk-adjusted its guidance to reflect a world in which it did not arrive on schedule.3 Kastner was careful not to let analysts split the damage cleanly between "performance" and "the missing contract," insisting the two were entangled — but that refusal to parse was itself telling, because it meant investors could not easily isolate how much of the miss was HII's own execution versus an external negotiating delay.

The plumbing: why the cash actually vanished

It is worth dwelling on the mechanism of the cash-flow collapse, because it is the single most important thing to understand about how this business breathes. HII does not get paid a lump sum when it hands over a finished ship. It collects cash by hitting contractual milestones and incentives along the multi-year build, and in between those collections its cash is trapped on the balance sheet as work-in-progress — steel bought, labor paid, but not yet billed. When schedules slip and milestones move to the right, two things happen at once: less margin is recognized, and the associated cash simply does not get collected on time. Working capital, which had been climbing all year, ballooned. Stiehle described a working-capital ratio in the "upper 8s" percent of sales that he wanted back near a normalized 5%, and conceded it could take twelve to eighteen months to grind through the pre-COVID ships and collect the cash sitting behind them.3 The lesson for anyone modeling HII: the income statement tells you how the ships are performing, but the balance sheet tells you whether the cash is coming — and in a milestone business, cash and earnings can diverge violently for years.

Management's capital-allocation response revealed how seriously it took the squeeze. It throttled share repurchases for the balance of 2024 — after buying back 608,000 shares for $162 million year-to-date — and cut planned capital expenditure from a targeted 5.3% of sales down to 3.4%, deferring investment in the very throughput improvements it said it needed.3 Yet it still raised the dividend, to $1.35 per share, a roughly 3.8% increase.3 That combination — cut buybacks and capex, protect the dividend — is the classic defensive crouch of a company signaling to income investors that the payout is safe even as everything else is being rationed.

The Q&A: where the story got stress-tested

The prepared remarks blamed macro labor markets and legacy contracts. The analyst Q&A is where you find out whether management can defend the story — and this one got pointed. Bank of America's Ron Epstein asked the question everyone was thinking: given the rosy picture painted at the prior investor day, "how could you not see this coming?" Kastner's answer was a partial mea culpa — the company's assumptions about how quickly it would work through the pre-COVID ships had simply been "a little bit too optimistic."3

Wolfe Research's Myles Walton and Goldman's Noah Poponak pressed on the most important question of all: was the five-year cash-flow withdrawal a timing problem or a sign the shipbuilding business model was structurally broken? Management insisted it was timing and performance, not a broken model, and reaffirmed a mid-to-long-term shipbuilding margin target of 9–10% — but conceded cash would be "choppy for a couple of years."3 Others, including Citi's Jason Gursky, probed whether HII was quietly conceding to the Navy's aggressive pricing on the delayed submarine contracts, and whether it might make sense to simply slow down to let green labor season. Kastner's response there was revealing: the company would pivot to hiring fewer entry-level workers and more experienced ones, and lean harder on outsourcing over 1 million hours of fabrication in 2024 with plans to grow that by more than 30% in 2025.3

That last point is the hinge of the whole story. Buried in a brutal quarter was the seed of the strategy that would define HII's recovery. The company could not hire its way out of a nuclear-labor shortage fast enough — so it would start sending the work to where the workers were. Whether that bet paid off is the subject of the next chapter.

VII. The Redemption: 2025 Financial Rebound and the 2026 Outlook

If October 2024 was the crisis, February 5, 2026 was the vindication lap — or at least management's attempt at one. On its Q4 2025 call, HII reported a full year that, on the headline numbers, looked like a different company from the one that had cratered fifteen months earlier.

Consolidated revenue rose 8.2% to a record $12.5 billion, with all three divisions setting revenue records.1 Shipbuilding revenue alone grew 9.7% year over year — Ingalls up 11.2% and Newport News up 9% — a reassuring sign that the top-line problem had never really been demand.2 The more important number was cash: free cash flow rebounded to $800 million, above the guidance range the company had set, from a mere $40 million the year before.1 Management credited a very strong working-capital finish to the year — roughly $170 million of working-capital tailwind — as milestone payments came in and the balance sheet unwound.2 Net earnings reached $605 million, and the company generated $1.196 billion of operating cash flow while investing $396 million, or 3.2% of sales, back into the yards.12

The evidence tells a specific story here, and it is worth stating plainly rather than cheering. The 2025 recovery was driven far more by throughput and cash timing than by margin expansion. Shipbuilding operating margin improved to 5.9% for the year from 5.2% in 2024 — real progress, but still a long way from the 9–10% target, and management explicitly declined to promise when that target would be reached.2 Newport News margin recovered to 5.1% but was still held down by continued negative cumulative adjustments on the CVN 80 and CVN 81 carriers; net cumulative adjustments for the year were still negative $64 million at Newport News.2 In other words, the crisis's core wound — thin, pre-COVID-priced nuclear work — had scabbed over, not healed. What had genuinely improved was volume: throughput rose 14% in 2025, and the yards hired more than 6,600 shipbuilders while attrition improved by an estimated 15–18%.2

The 2026 outlook

For 2026, management guided shipbuilding revenue to $9.7–$9.9 billion, shipbuilding margin to 5.5%–6.5%, Mission Technologies revenue to $3.0–$3.2 billion, and free cash flow to $500–$600 million.211 At the midpoint, that implies combined 2025–2026 free cash flow of about $1.35 billion — an increase from the roughly $1.2 billion two-year figure management had floated a quarter earlier, and a deliberate signal that it was rebuilding the multi-year credibility it had torched in 2024.2 Notably, management raised its medium-term shipbuilding revenue growth target from roughly 4% to roughly 6%, citing unprecedented demand and pending awards — and pointedly said even that excluded upside from two newly announced programs, a new frigate and a "battleship."2 The guidance carries an explicit condition, though: it assumes HII reaches agreement on the next Virginia and Columbia submarine contracts in the first half of 2026, the very deals whose delay helped trigger the 2024 crisis. As of this recording, those contracts had not yet been signed — a live risk sitting underneath the whole outlook.2

A few pieces of financial plumbing sit behind those headline numbers and reward attention. The 2025 free-cash-flow beat was flattered by roughly $170 million of working-capital tailwind and by beneficial cash-tax effects from 2025 tax legislation that management expects to continue helping in 2026.2 Investors should therefore discount the quality of the 2025 cash beat somewhat — some of it was timing and tax, not durable operating improvement. Management was also candid that cash arrives in a brutally uneven cadence: it guided first-quarter 2026 free cash flow to negative roughly $600 million as the fourth-quarter working-capital benefit unwinds.2 That is normal for this business, but it means any single quarter's cash figure is close to meaningless; only the full-year and multi-year numbers tell you anything. Capital expenditure, meanwhile, is guided back up to 4–5% of sales — $500–$600 million — reversing the crisis-era throttling and signaling that management now feels confident enough to invest into the capacity constraint again.2 The pension, once a swing factor, has become a relatively minor cash item, with contributions of $54 million in 2025.2

The management question

Who is steering this? Christopher Kastner has served as president and CEO since March 2022, and he is a deep operational insider rather than a visionary hired from outside. He came up through the finance and operations spine of the company — executive vice president and CFO from 2016 to 2021, then COO — which means he understands contract structure, risk clauses, and the mechanics of where cash gets trapped on the balance sheet better than almost anyone. That is either exactly what a company grinding through legacy fixed-price contracts needs, or a sign of a management culture that optimizes rather than transforms; reasonable investors can disagree.

On alignment: Kastner held roughly 70,500 shares as of late 2025, worth on the order of $15–$23 million depending on the day's price — meaningful money, but a small ownership stake in absolute terms, which is typical for defense primes run by career executives rather than founders.10 His total 2025 compensation was reported at about $13.8 million, heavily weighted toward performance-share units tied to return on invested capital and relative total shareholder return.10 The structure is defensible — ROIC-linked pay is exactly what you want in a capital-intensive business — but it is worth watching whether the metrics get reset softer after a hard year, a common way boards quietly cushion executives through a downturn.

On credibility, the record across the last several calls is genuinely mixed, and an honest assessment has to hold both halves. On the debit side: management came into 2024 with an optimistic investor-day framing, missed badly, and then withdrew a multi-year target rather than defend a revised one — the classic pattern of a team that had over-promised on a business it did not fully control. It also leaned on a consistent external narrative — "pre-COVID contracts," "macro labor markets" — that, while largely true, conveniently located the cause of the miss outside the company's own execution, and it declined repeatedly to quantify how much of the damage was self-inflicted. On the credit side: management did not paper over the 2024 miss, laid out a specific and concrete recovery plan (throughput targets, hiring numbers, outsourcing goals, a $250 million cost-reduction target), and then largely delivered against it in 2025 — beating its own rebuilt free-cash-flow guidance and hitting most of its milestone ship deliveries. Crucially, the language has stayed consistent across calls: the same throughput-and-transition framework Kastner used to explain the 2024 collapse is the one he used to explain the 2025 recovery, which is what you want to see. A management team that tells the same causal story on the way down and the way up is more believable than one that reinvents its narrative each quarter. The unfinished business — the reason the jury is still out — is that the headline promise, 9–10% shipbuilding margins, remains undated and undelivered.

Capital allocation and the new optionality

The recovered cash did not go to shareholders in 2025. HII repurchased no shares during the year and paid $213 million in dividends, ending the year with $774 million of cash and about $2.5 billion of liquidity.2 Management was explicit about the priority order on the Q4 call: reinvest in the shipyards first. Asked directly by JPMorgan's Seth Seifman whether excess cash might flow to buybacks, Kastner deflected with a line he attributed to a predecessor — "cash can be pretty lumpy" — and argued the highest-return use of capital was still pouring money into the yards to lift throughput.2 For a business whose whole problem is a capacity constraint, that is a defensible answer; it is also a reminder that HII is not, and for the foreseeable future will not be, a capital-return story.

What genuinely changed the demand picture in late 2025 was politics. Congress passed the FY2026 National Defense Authorization Act on a bipartisan basis in December, and it was about as good as HII could have scripted: incremental funding and block-buy authorization for carriers CVN 82 and CVN 83, procurement authorization for up to five Columbia-class submarines, and continuous-production authority for a range of Virginia-class components to smooth the supply chain.2 On top of that, the Navy signaled two entirely new franchises — a new frigate and what management referred to as a "battleship" program, part of a broader fleet-expansion push — and HII expects to build the first ships of the new frigate class leveraging the proven design of its Ingalls-built National Security Cutter.2 Management explicitly excluded both new programs from its raised medium-term growth target, framing them as upside — which is the right posture, since neither has a defined acquisition strategy yet, and management could not put revenue figures on them.

HII also signed a memorandum of agreement with South Korea's HD Hyundai Heavy Industries to explore future collaboration — a notable move given that foreign shipbuilders with spare capacity have become part of Washington's conversation about expanding the U.S. industrial base.2 On the Q4 call, an analyst floated whether a Korean or Japanese yard might even fund capital in a joint venture; Kastner kept "the aperture open" without committing to anything.2 It is optionality, not a plan — but it signals that even the most closed of industries is being pried open by the sheer scale of the Navy's ambitions.

The "distributed shipbuilding" bet

The operational centerpiece of the recovery is the strategy that first surfaced in the depths of the 2024 crisis: distributed shipbuilding. The idea is to stop treating the two yards as the only place work can happen. Instead of trying to cram every hour of fabrication into labor-constrained Virginia and Mississippi, HII outsources chunks of the work — fabricating "grand blocks," large pre-assembled ship sections — to a network of smaller shipyards and fabricators around the country, then brings the finished modules in for final integration. Think of it as the difference between a restaurant where one kitchen cooks every dish from scratch and one that has trusted regional partners prep components that get assembled on site.

The scale-up has been rapid. HII doubled its outsourced hours in 2025 and targeted a further 30% increase in 2026, working with a network of more than 23 established outside vendors.2 Industry reporting in July 2026 put the 2026 goal at over 2.5 million hours of outsourced fabrication routed to partners such as Eastern Shipbuilding, Gulf Copper, and Trident Maritime Systems.[^13] As a proof of concept, in early July 2026 Ingalls integrated its first offsite-built grand blocks into the destroyer USS Thad Cochran (DDG 135), part of the company's push toward a targeted 15% throughput increase in 2026.[^13]2

Here is the independent read. Distributed shipbuilding is a genuinely clever response to a genuinely hard problem: if your cornered resource — nuclear-region skilled labor — is the binding constraint, you relax the constraint by geographically dispersing the work to other labor pools. But it is not free. Management has been candid that outsourcing carries a premium and that first-time builds at new suppliers add cost, which is part of why 2026 margin guidance stays capped in the 5.5%–6.5% zone even as revenue grows.2 The strategy trades margin for throughput and schedule. Whether that is a good trade depends entirely on the thing we turn to next: whether the new contracts, priced for today's world, eventually deliver the margin expansion the whole bull case is riding on.

VIII. The Investor's Dilemma: Bull vs. Bear and Risk Radar

Strip away the narrative and HII presents one of the cleaner bull/bear debates in the industrial universe, because both sides are arguing about the same fact — the monopoly — and simply disagree about what it's worth.

The current risk radar

Three material risks drive the economics, and each operates through a specific mechanism worth naming.

Labor scarcity is the physical limit on revenue. This is not a soft ESG risk; it is the hard ceiling on the business. If HII cannot hire and — more importantly — retain nuclear-qualified technicians, ships cannot be built on schedule, cash-flow milestones get missed, and negative cumulative adjustments flow straight through the income statement. The 2024 crisis was, at bottom, a labor-productivity crisis. The 2025 recovery was, at bottom, a labor-retention recovery. Watch this above all else. On the Q4 2025 call, Deutsche Bank's Scott Deuschle even asked whether the boom in data-center construction around Virginia was poaching electricians and pipefitters; management said it hadn't seen an impact yet but was watching — a reminder that HII competes for skilled trades against the entire regional economy, not just other shipyards.2

Inflation on fixed-price contracts remains a drag, though a fading one. Newer contracts increasingly feature inflation indexation and economic-price-adjustment clauses that shift some cost risk back to the Navy. But the legacy pre-COVID fixed-price blocks still in the yards continue to weigh on Newport News margins, and management has said the portfolio won't tip to majority post-COVID work until around 2027.3 Until then, every quarter carries the risk of another negative adjustment on an old ship.

The Navy budget cycle is an exogenous timing risk. HII lives and dies by congressional appropriations. Continuing resolutions, budget delays, or a failure to authorize a specific block buy can push multi-billion-dollar awards to the right and disrupt milestone timing. The offset in the current cycle is unusually strong political support: the FY2026 National Defense Authorization Act, passed on a bipartisan basis in December 2025, backed block-buy procurement for carriers CVN 82 and CVN 83 and authorized up to five Columbia-class submarines — about as supportive a demand backdrop as a defense prime could ask for.2

Execution risk in the transformation itself. Distributed shipbuilding is unproven at scale, and it introduces new failure modes: quality control across two dozen outside vendors, the logistics of moving giant grand blocks and mating them precisely, and the first-time-build inefficiencies management has openly acknowledged. If an outsourced block arrives late or out of tolerance, it can stall an entire ship — trading one bottleneck for another. The strategy is a reasonable response to the labor constraint, but it is a bet, not a guarantee.

Supply-chain fragility and, increasingly, cyber. The 2024 crisis was in part a supply-chain story — late deliveries of critical material rippling into labor inefficiency and rework — and that fragility has not fully healed. Layered on top is the reality that a builder of nuclear warships is a prime target for state-sponsored cyber intrusion; a serious breach of design data or production systems would be both a security and a financial event. These are lower-probability risks than labor, but they are tail risks with outsized consequences.

The activist's stress test

What would a skeptical activist actually push on here? Not the balance sheet — HII runs modest leverage and an investment-grade profile. The sharper lines of attack are three. First, capital discipline: management funded the Alion acquisition with debt to buy a lower-margin services business, took an S&P outlook cut for it, and years later still runs Mission Technologies at a 5% margin — a fair prompt to ask whether the diversification created value or merely bought revenue. Second, disclosure and accountability: withdrawing a five-year cash-flow target and then declining to cleanly separate execution misses from contract-timing delays makes it genuinely hard for outsiders to hold management to account for what it controls versus what it doesn't. Third, the margin target itself: management has defended a 9–10% shipbuilding margin as "not just aspirational" while pointedly refusing to date it — a posture that lets a distant goal float indefinitely as the portfolio "transitions." None of these is a smoking gun. Together they define the burden of proof HII carries: it must show, in the numbers and not the narrative, that the new contracts convert into structurally higher returns.

The bear case

A skeptical long/short investor would frame it like this: shipbuilding is structurally a low-return capital trap dressed up as a monopoly. HII has essentially zero pricing power against a monopsony buyer that controls its revenue, its contract terms, and its regulatory environment. Operating margins are capped in the 5–7% range, and because the business is so operationally leveraged, a modest slip in labor productivity — a few points of rework — can wipe out a meaningful chunk of a year's earnings, as 2024 proved in vivid color. The capital intensity is relentless: HII must plow hundreds of millions back into the yards every year just to stay in place, and much of that capex is effectively directed by the customer. And the diversification story — Mission Technologies — mostly added lower-margin services revenue and acquisition debt without transforming returns. In this reading, the $48 billion backlog is not a treasure chest; it is a two-decade obligation to build ships at prices someone else sets, at returns that barely clear the cost of capital.

The bull case

The bull turns every one of those facts on its head. HII owns the single most durable industrial monopoly in America — a position no amount of capital or ambition can replicate on any relevant time horizon. The backlog guarantees demand for two decades regardless of the economic cycle. The margin compression is a transitional phenomenon tied to a specific, identifiable cohort of pre-COVID contracts; as those clear the yards and the portfolio tips to newer, higher-priced, inflation-indexed contracts — Virginia Block V and VI, Columbia Build 2, the next carriers — margins should expand back toward the 9–10% target management still defends. Meanwhile, distributed shipbuilding attacks the one variable — labor — that actually constrains growth. And the geopolitical backdrop, with great-power competition driving the most supportive naval-procurement environment in a generation, means the demand isn't just durable, it's accelerating.

Myth versus reality

A few consensus narratives about HII deserve fact-checking, because the popular story and the operating reality diverge in instructive ways.

Myth: "HII is a monopoly, so it must have great pricing power." Reality: it has monopoly supply and near-zero pricing power, because its single buyer sets terms and audits costs. The two are not the same thing, and conflating them is the most common error in the bull case.

Myth: "The $48 billion backlog means guaranteed profits." Reality: the backlog guarantees revenue, not margin. A large share of it is priced under older contracts, and revenue booked at a thin or negative margin is not a profit engine — it is an obligation to build at yesterday's prices. Backlog quality matters more than backlog size.

Myth: "The 2024 crash proved the business is broken." Reality: the 2024 collapse was overwhelmingly a working-capital and legacy-contract event, not a demand or franchise event. Demand was never the problem; the moat never cracked. What cracked was the ability to convert milestones to cash on schedule — a serious but different, and more fixable, problem, as the 2025 rebound partly demonstrated.

Myth: "Mission Technologies makes HII a high-margin tech company." Reality: it is mostly cost-plus services at a 5% margin. The uncrewed-systems franchise is genuinely valuable optionality, but the division has not re-rated the company's return profile, and pretending otherwise misreads the mix.

The referee's view

Both cases are internally coherent, which is why the stock is volatile. The honest synthesis is that the bull case is not wrong — it is unproven, and it hinges on a single question that the numbers have not yet answered: can HII translate the newer, better-priced contracts into sustained margin expansion, or will labor and inflation keep clawing it back? The 2025 results were encouraging on throughput and cash but ambiguous on margin, which sat almost exactly where it did before adjusting for the recovery. Management has earned some credibility back by beating its rebuilt cash guidance, but it has not yet demonstrated the structural margin lift the thesis requires — and it wisely refuses to put a date on it.

The three KPIs that actually matter

For a long-term owner tracking this company, most of the noise can be ignored in favor of three signals:

- Shipyard throughput and labor retention. This is the primary operational bottleneck and the leading indicator of everything else. Rising throughput and improving attrition mean the labor engine is working; deterioration here shows up as missed milestones and negative adjustments a few quarters later.

- The milestone-to-cash conversion cycle. Because HII's cash is trapped in years-long work-in-progress, the pace at which contract milestones convert to collected cash — visible in the quarterly swings in contract assets and liabilities and working capital — is the truest measure of financial health. The 2024 crisis and 2025 recovery were both, fundamentally, working-capital stories.

- New-contract pricing structure. Whether the next carrier (CVN 82/83) and submarine awards embed robust inflation protection and fair incentive fees will determine whether the margin-expansion thesis is real or a mirage. This is the single variable that separates the bull and bear cases.

Track those three and you are tracking the actual business. Everything else — the quarterly EPS beats and misses, the stock's daily gyrations — is derivative of them. Which brings us to what this whole saga can teach investors far beyond the shipyard gates.

IX. Playbook: Business & Investing Lessons

Lesson 1: A 100% market share can be a trap, not a treasure. HII builds every American nuclear aircraft carrier, and that fact has not made it a high-return business. The reason is that market share means nothing without pricing power, and pricing power evaporates when you have a single buyer who also controls your regulatory environment, your appropriations, and your contract terms. Monopoly over supply is worthless if the demand side is an even more powerful monopsony. When you evaluate any business that boasts of dominant share, the sharper question is always: dominant share of a market with how many buyers, and who sets the price?

Lesson 2: When labor is the binding constraint, deconstruct the process. The instinctive response to a labor shortage is to pay up and hire — and HII does that too. But the more durable lesson of distributed shipbuilding is that even the heaviest, most stubbornly localized industrial process can be modularized and dispersed to where the workers actually are. HII took a manufacturing process everyone assumed had to happen in two specific places and began breaking it into pieces that could be built across a national network. It is an expensive answer, and it trades margin for throughput — but it demonstrates that "we can't find enough people here" is often a problem of process design, not just of hiring.

Lesson 3: Beware conglomerate drag — and respect the power of focus. Northrop Grumman's decision to spin off its shipyards illustrates a recurring truth of corporate finance: when you house businesses with fundamentally divergent margins, capital intensities, and risk profiles under one roof, the market discounts the combination and management attention gets misallocated. Separating high-margin, capital-light electronics from low-margin, capital-heavy shipbuilding unlocked focus and operational discipline for both. The flip side, which HII's own history since the spin-off proves, is that focus is necessary but not sufficient: it let management concentrate on the shipbuilding problem, but it did not — and could not — change the underlying economics dictated by having one customer.

X. Epilogue & Outro

Stand at the edge of Dry Dock 12 and the scale is almost incomprehensible. A hull the size of a skyscraper laid on its side, cranes that can lift a thousand tons, tens of thousands of workers moving across a footprint measured in acres — an industrial cathedral for building the largest warships ever made. Six hundred miles away on the Pascagoula River, the same drama plays out on a different scale, destroyers and amphibs taking shape section by section. There is nothing else quite like it in the private economy of the United States.

And here is the enduring paradox the whole story circles back to. The most technologically advanced military the world has ever seen — with its hypersonic missiles, its AI-enabled sensors, its uncrewed swarms — ultimately rests its global strategic dominance on the shoulders of skilled blue-collar workers welding steel and pulling cable in two shipyards in Virginia and Mississippi. A superpower's ability to project force across every ocean depends, in the end, on whether Huntington Ingalls can find, train, and keep enough people who know how to build a ship.

That is the moat, and that is the vulnerability, and they are the same thing. HII owns an industrial position no competitor can touch and no customer can abandon. It also owns a cost structure and a labor dependency that turn its guaranteed demand into merely adequate, hard-won returns. Whether the coming decade rewards its owners will come down to the least glamorous variables imaginable — throughput, retention, and the fine print of a submarine contract. For a company that builds the instruments of the sublime, the fate of the investment rests on the resolutely mundane. That tension, more than any single number, is the story of the steel moat of American sea power.

References

-

HII Reports Fourth Quarter and Full Year 2025 Results — Huntington Ingalls Industries (SEC Form 8-K), 2026-02-05 ↩↩↩↩↩↩

-

Huntington Ingalls Industries Q4 2025 Earnings Call Transcript — Investing.com, 2026-02-05 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Huntington Ingalls Industries (HII) Q3 2024 Earnings Call Transcript — Seeking Alpha, 2024-10-31 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

HII Shares Crater on Slashed Cash Flow Forecast, Submarine Delays — Bloomberg, 2024-10-31 ↩

-

Northrop Grumman Form 10-12B/A, HII Spin-Off Registration Statement — SEC, 2011 ↩↩

-

History — 140+ Years of Shipbuilding Heritage — Huntington Ingalls Industries ↩↩↩

-

Huntington Ingalls to Buy Alion Science and Technology for $1.65 Billion — Defense News, 2021-07-06 ↩

-

S&P Global Ratings — Introduction to Credit Ratings (HII outlook revision context), 2021 ↩

-

Navy, HII Reach Agreements on Submarine Industrial Base Support — USNI News, 2024-11-04 ↩↩

-

Huntington Ingalls Industries Form DEF 14A Proxy Statement — SEC, 2026-03-20 ↩↩

-

Huntington Ingalls Q4 2025 Earnings Presentation and 2026 Outlook — Investing.com, 2026-02-05 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube