Home Depot: Building an Empire in Orange

I. Introduction & Episode Preview

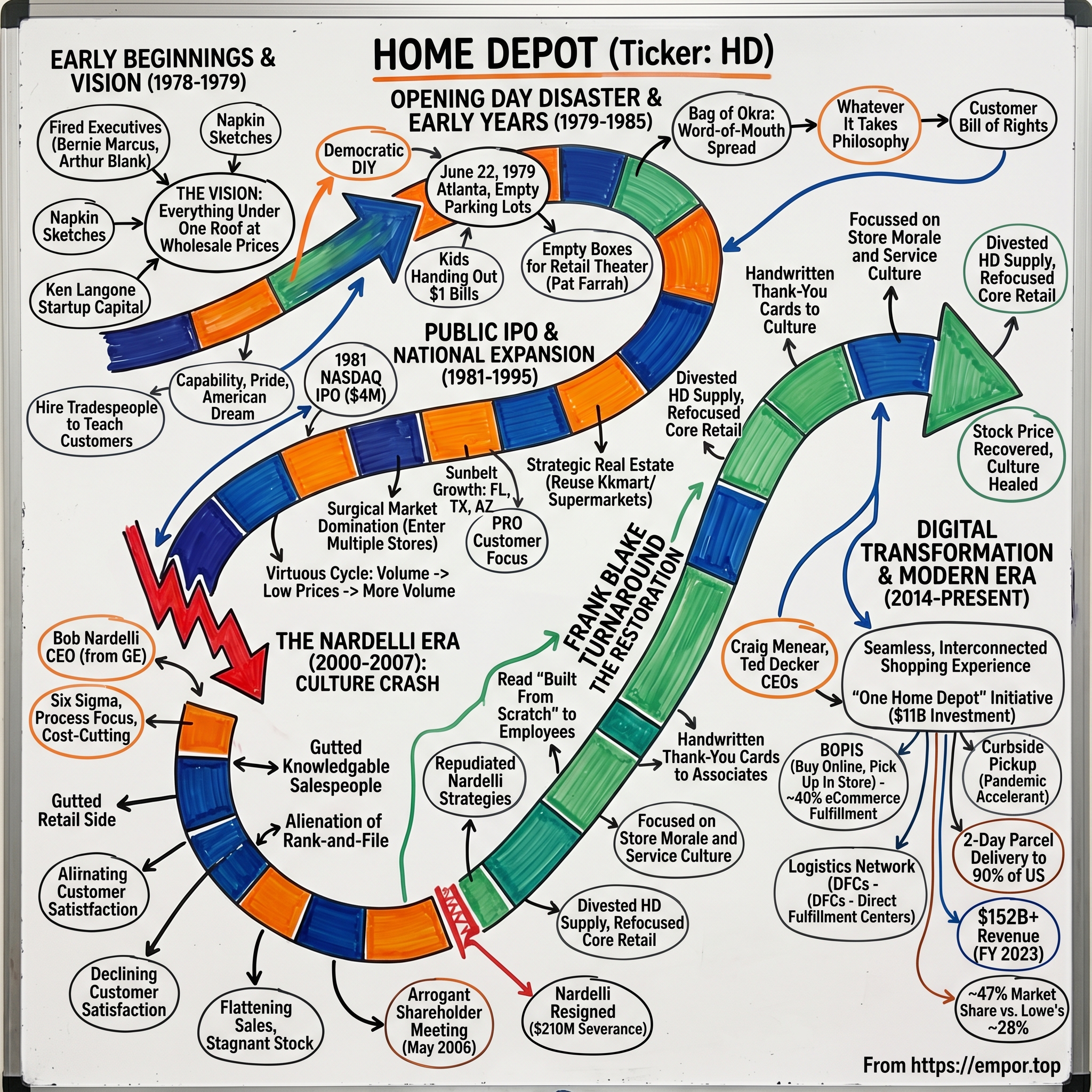

Picture this: Two middle-aged executives, freshly fired from their jobs, sitting in a Los Angeles coffee shop in 1978, sketching out plans on napkins. Bernie Marcus, 49, and Arthur Blank, 35, had just been unceremoniously dumped by their corporate parent. Most people would be updating their resumes. These two? They were dreaming up what would become the largest home improvement retailer in the world.

The question at the heart of today's story isn't just how they did it—it's how they did it their way. How did a parking lot disaster on opening day transform into a $400 billion market cap juggernaut? How did a company built on the radical idea of teaching customers to put competitors out of business actually work? And perhaps most intriguingly, how did Home Depot survive—and ultimately thrive—after nearly destroying its own culture in pursuit of operational efficiency?

Today, Home Depot stands as an American retail colossus. With over 490,000 employees and $152 billion in revenue, it commands roughly 43% of the U.S. home improvement market. Its orange-aproned associates have become as iconic as the stores themselves. But the path from that coffee shop to retail dominance was anything but smooth.

We'll trace the journey from the Handy Dan years through the watershed firing that created the company, explore the opening day disaster that nearly killed it in the crib, examine the cultural civil war of the Nardelli era, and understand how Frank Blake brought the company back to its roots. Along the way, we'll uncover the strategic moats, operational innovations, and leadership lessons that transformed a simple idea—everything under one roof at wholesale prices—into an empire that has fundamentally reshaped how Americans think about their homes.

The real story of Home Depot isn't just about lumber and power tools. It's about the delicate balance between entrepreneurial culture and operational excellence, the power of treating employees like owners, and why sometimes the best business strategy is teaching your customers to do it themselves. Let's dive into how Bernie Marcus and Arthur Blank built their orange empire, lost their way, and found it again.

II. The Handy Dan Years & Getting Fired

By 1972, Bernie Marcus had climbed his way to the top of the retail hardware world—or so he thought. As Chairman and President of Handy Dan Improvement Centers, a home improvement chain nestled within the Daylin Corporation conglomerate, Marcus was running a respectable operation with dozens of stores across the western United States. It was here, in the fluorescent-lit aisles of Handy Dan, that he met a young financial executive named Arthur Blank who would become not just his business partner, but his lifelong friend.

Marcus and Blank made an odd pair. Bernie was the quintessential New York retailer—loud, passionate, with a salesman's gift for reading people and a merchant's eye for what would sell. Blank was his opposite: methodical, numbers-driven, the kind of guy who found poetry in perfectly balanced spreadsheets. Yet something clicked between them. They shared an obsession with customer service and a growing frustration with corporate bureaucracy.

Their eureka moment came almost by accident. Near the end of their Handy Dan tenure, they started experimenting with discount pricing at one location—a radical idea in the hardware business where margins were gospel. The results were counterintuitive and thrilling: when they marked down items, volume exploded and costs as a percentage of sales actually decreased. They were onto something big, but they'd never get the chance to pursue it at Handy Dan.

Enter Sanford Sigoloff, the corporate turnaround artist who would inadvertently launch Home Depot. Known as "Ming the Merciless" for his slash-and-burn approach to restructuring, Sigoloff took control of Daylin Corporation in 1978 with a mandate to clean house. Marcus and Blank had been pushing for expansion, for investment, for pursuing their discount vision. Sigoloff saw expensive executives with expensive ideas.

The axe fell on April 14, 1978. Marcus got the call on a Friday afternoon—he was out, effective immediately. Blank and their colleague Ron Brill got similar calls. No severance package worth mentioning, no golden parachute. Just a pink slip and a escort to the parking lot. Marcus was 49 years old, at what should have been the apex of his career, and suddenly unemployed.

Most people would have been devastated. Marcus was furious—and energized. "I was too young to retire and too old to start over in another corporate hierarchy," he'd later recall. Within hours of being fired, he was on the phone with Blank: "Arthur, this is our chance. Let's build the store we've been dreaming about."

The timing seemed impossible. They had no money, no stores, no suppliers, and they'd just been very publicly fired. But they had something more valuable: a vision that had been percolating for years and the burning desire to prove Sigoloff wrong.

That's when Ken Langone entered the picture. A Wall Street investment banker with a reputation for backing mavericks, Langone had made his fortune taking Ross Perot's EDS public. He met Marcus through a mutual friend just weeks after the firing. Marcus pitched him the vision: massive warehouse stores, wholesale prices, expert advice, everything under one roof. Langone was intrigued enough to commit to raising $2 million in startup capital.

"Bernie, you're going to be the richest man in America," Langone told him after hearing the pitch. Marcus thought he was crazy. But Langone saw what others missed: the American DIY revolution was about to explode, and these fired executives had the perfect formula to capture it. The firing that was meant to end their careers had instead freed them to build something extraordinary.

III. The Vision: Building a New Kind of Store

Bernie Marcus didn't just want to build another hardware store—he wanted to democratize home improvement itself. Standing in those empty warehouses in Atlanta in early 1979, he could see it all: 60,000 square feet of retail space, ceiling heights that seemed to scrape the sky, and row after row of everything a homeowner could ever need. This wasn't going to be your father's corner hardware store with creaky floors and dusty shelves. This was retail revolution.

The vision was deceptively simple yet radically ambitious: create a one-stop shop for do-it-yourselfers that didn't exist anywhere in America. At the time, if you wanted to renovate your kitchen, you'd visit maybe six different stores—the lumber yard, the hardware store, the plumbing supply house, the electrical supplier. Each had different hours, different pricing schemes, and most treated retail customers like annoying interruptions to their contractor business.

Marcus and Blank wanted to blow that model apart. Their warehouse concept would put everything under one massive roof at wholesale prices. But here's where they zagged when everyone else would have zigged: they didn't want to just stack products high and let customers fend for themselves like a traditional warehouse store. They wanted to teach America how to use those products.

"We're not just selling hammers and nails," Marcus would tell early employees. "We're selling capability. We're selling pride. We're selling the American dream of homeownership and the satisfaction of building something with your own hands."

The cultural timing was perfect. This was 1979—inflation was eating away at middle-class budgets, contractors were expensive and often unreliable, and a new generation of homeowners was emerging who actually wanted to get their hands dirty. The DIY movement wasn't just about saving money; it was becoming a lifestyle, a weekend identity, almost a religion for suburban America.

But Marcus and Blank's masterstroke was recognizing that desire alone wasn't enough. Most people wanted to fix their own leaky faucet or build their own deck, but they were terrified of screwing it up. That's where the radical part of their vision came in: hire experienced tradespeople—plumbers, electricians, carpenters—pay them well, and have them teach customers how to do projects themselves.

Think about the insanity of that for a moment. They were going to pay premium wages to employees who would literally teach customers how to avoid hiring professionals. It was like a restaurant teaching you to cook so you'd never eat out again. Traditional retailers thought they were nuts.

The early business plan, sketched out with Langone's help, called for stores that would carry 25,000 different products—an unheard-of selection at the time. They'd buy direct from manufacturers, cutting out distributors. They'd mark everything up just 30%, compared to the traditional 50-70% in hardware retail. Volume would make up for margins.

Blank, ever the numbers guy, had worked out the math obsessively. If they could hit $9 million in sales per store annually, they'd be profitable. The average hardware store did maybe $1 million. They were betting on a 9x improvement through selection, price, and service.

They even had a name picked out—well, almost. Marcus originally wanted to call it "Bad Bernie's Buildall," playing off the discount electronics chain Crazy Eddie's. Thankfully, cooler heads prevailed. They settled on The Home Depot, with the deliberately folksy "The" suggesting a destination, not just another store.

The orange theme came from a Canadian hardware chain Marcus had studied. Orange was bright, optimistic, impossible to ignore—everything their stores would be. Those orange aprons that would become iconic? That was about democratization too. No suits, no ties, no hierarchy visible on the floor. Everyone from the CEO to the newest cashier would wear the same orange apron.

As they prepared to open those first two Atlanta stores, Marcus and Blank had crystallized their vision into what would become their customer bill of rights: the best selection, the best prices, the best service. But more than that, they were selling empowerment. They were betting that Americans didn't just want to own homes—they wanted to improve them, customize them, make them their own.

"We're not in the hardware business," Blank would say. "We're in the American dream business." That dream was about to face its first test in a nearly empty parking lot.

IV. Opening Day Disaster & Early Years (1979–1985)

June 22, 1979. Atlanta, Georgia. Two massive warehouses—former Treasure Island stores—sit waiting with 60,000-square-foot spaces stocked with up to 50,000 products. Bernie Marcus and Arthur Blank had bet everything on this day. They'd hired staff, trained them extensively, stocked shelves (sort of), and prepared to revolutionize American retail. There was just one problem: nobody showed up.

Marcus and Blank had positioned their children at the entrance, handing out one-dollar bills as tokens of gratitude. The plan was simple—create some buzz, get people through the doors, let the prices and selection do the rest. They thought they'd run out of dollar bills by noon, but reality had a different plan in store.

"By 5 or 6 in the evening, our kids were out in the parking lot, stopping people and giving them money to come into the store. It was a crushing disappointment," Blank would later acknowledge. Imagine the scene: the founders' children literally chasing down cars in the parking lot, pressing dollar bills into confused drivers' hands, begging them to just come look inside. "By dinner time they still had plenty of cash," Marcus wrote in his memoir. "We were devastated."

The warehouse concept that seemed so brilliant in theory looked like a disaster in practice. These weren't your cozy corner hardware stores with creaky wood floors and the smell of sawdust. These were cavernous spaces with concrete floors and industrial shelving reaching toward 16-foot ceilings. To customers accustomed to intimate neighborhood shops, it must have looked more like a wholesale depot than a retail store—which was exactly the point, but nobody understood that yet.

But Marcus and Blank weren't about to fold. They had a secret weapon, though they didn't know it yet: Pat Farrah, their merchandising guru, had convinced suppliers to give them empty boxes with labels when they couldn't afford actual merchandise. "OK, you won't give us any more merchandise because you're afraid we won't be able to pay you. Give us empty boxes with your labels on," Farrah had told skeptical vendors. Those towering shelves that looked so impressively stocked? Many of the boxes up high were empty—retail theater at its finest.

The third day marked a turning point. A satisfied customer arrived at the store, not with cash, but with a bag of okra as a token of gratitude for a fantastic shopping experience. It sounds absurd—payment in vegetables—but that bag of okra represented something profound: word was starting to spread. This wasn't just another hardware store. This was something different.

What made it different wasn't just the prices, though marking everything up just 30% instead of the industry standard 50-70% certainly helped. It was the radical commitment to customer service that seemed to contradict the warehouse model itself. Marcus and Blank implemented a customer "bill of rights," stating that customers should always expect the best assortment, quantity and price, as well as the help of a trained sales associate. These commitments were an extension of the company's "whatever it takes" philosophy.

The "whatever it takes" mentality played out in ways that would become legendary. Associates would spend hours with a single customer, teaching them how to tile a bathroom or install a ceiling fan. They'd make phone calls to track down obscure parts. They'd even visit customers' homes to help diagnose problems. This wasn't just customer service—it was customer education, customer empowerment, customer partnership.

Early on, Bernie would stand outside with a fist of single dollar bills and give people a dollar if they'd go in and see what was in the store. But before too long, the founders knew they were onto something, "because we began to see the enthusiasm of the customers as they were coming in the stores".

The transformation was remarkable. While the initial sales projection per store was set at $9 million, the reality exceeded expectations, with each store making over $17 million. Those empty parking lots of June 1979 gave way to packed weekends where the challenge wasn't getting customers in—it was managing the crowds.

By 1981, just two years after that disastrous opening day, Home Depot was ready to go public. They went public on NASDAQ, raising over $4 million. This infusion of capital boosted investments and profits. The IPO valued the company at roughly $12 million—not bad for a business that had started with children handing out dollar bills in an empty parking lot.

The expansion that followed was methodical but aggressive. In 1981, Home Depot expanded to Miami with a total of four new locations. Each new market was carefully chosen, each store location meticulously scouted. They weren't just opening stores; they were establishing beachheads in a retail revolution.

In less than eight years, Home Depot reached a significant milestone by opening its 100th store. The company that couldn't attract customers on day one was now drawing millions of weekend warriors, professional contractors, and everyone in between. The orange apron had become a symbol not just of expertise, but of a democratized approach to home improvement.

What's remarkable about these early years is how many of the company's core principles were established in crisis. The commitment to customer service came from watching customers struggle in those first empty stores. The focus on education emerged from the reality that most Americans wanted to do projects themselves but didn't know how. The "whatever it takes" philosophy was born from desperation—when you're giving away dollar bills to get people in the door, you'll do whatever it takes to keep them coming back.

The founders also learned the power of strategic theater. Those empty boxes on high shelves? They created an impression of abundance that became reality. The massive scale of the stores? It signaled serious business, wholesale prices, professional-grade supplies. Even the orange color scheme—bright, optimistic, impossible to ignore—was carefully chosen to project energy and accessibility.

But perhaps the most important lesson of those early years was about resilience and vision. Marcus and Blank could have panicked after that first day. They could have downsized, gone traditional, played it safe. Instead, they doubled down on their vision. They kept those massive stores, kept those low margins, kept investing in employee training and customer service. They bet that Americans were ready for a new way to improve their homes, and they were right.

After The Home Depot went public in 1981, Marcus and Blank made a commitment to give back to the communities where their stores were located. Following through on that commitment, legions of Team Depot volunteers work tirelessly to help veterans and communities. This wasn't just corporate PR—it was an extension of the same philosophy that had associates teaching customers how to use a drill. Home Depot wasn't just selling products; it was investing in communities, one project at a time.

By 1985, Home Depot had grown from those two Atlanta stores to a regional powerhouse with dozens of locations and hundreds of millions in revenue. The company that started with a parking lot disaster was well on its way to dominance. But this was just the beginning—the real expansion was yet to come.

V. Going Public & National Expansion (1981–1995)

The numbers from Home Depot's 1981 IPO seem quaint now: raising over $4 million to fuel expansion. But for Bernie Marcus and Arthur Blank, going public represented more than capital—it was validation that their warehouse concept could scale beyond Atlanta. Wall Street was betting on orange aprons and weekend warriors, and the founders were about to prove that bet spectacularly right.

The expansion strategy was surgical in its precision. Rather than scattered growth, Home Depot concentrated on market domination. They'd enter a metropolitan area with multiple stores simultaneously, creating instant critical mass. This wasn't just about convenience—it was about changing consumer behavior. When you had three or four Home Depots in a market, weekend projects stopped being something you planned around hardware store hours and became something you could tackle on impulse.

The formula was deceptively simple but ruthlessly executed: massive selection (25,000+ SKUs when competitors carried maybe 5,000), wholesale pricing (those 30% markups when others charged 50-70%), and expert advice from well-paid associates who actually knew how to use a compound miter saw. But the secret sauce was the combination—any competitor could copy one element, but copying all three while maintaining profitability required scale that took years to build.

From those first stores in 1979, Bernie and his fellow founders grew a business that eventually employed more than 500,000 associates. Each new market brought the same playbook: hire experienced tradespeople, pay them well above retail average, and unleash them on customers hungry for knowledge. A master plumber making $20 an hour at Home Depot in 1985 might seem expensive until you realized he was creating ten new customers a day who'd never attempt their own repairs anywhere else.

The geographic expansion followed the sunbelt initially—Florida, Texas, Arizona. These markets had growing populations, new construction, and a DIY culture fostered by suburban sprawl. But Marcus and Blank's genius was recognizing that every market had untapped DIY potential. The question wasn't whether Milwaukee or Phoenix was more naturally suited to home improvement—it was about teaching each market to see their homes differently.

Competition during this period was fragmented and unprepared. Lowe's, founded in 1946, was still primarily a regional player in the Carolinas. Local hardware stores couldn't match the selection or prices. The big-box revolution that would eventually bring Walmart into every sector hadn't yet focused on home improvement. Home Depot had a window—maybe five years, maybe ten—to establish itself as the category killer before serious competition emerged.

The cultural timing was perfect. This was Reagan's America, where self-reliance was virtue and homeownership was gospel. The same demographic that had bought suburban homes in the 1970s now had equity to tap for improvements. Cable TV was bringing This Old House and Bob Vila into living rooms, making home improvement aspirational rather than just functional. Home Depot wasn't just riding these trends—it was amplifying them.

The company's approach to real estate was particularly clever. While competitors built stores, Home Depot often leased abandoned supermarkets or discount stores, retrofitting them at a fraction of new construction costs. These locations had proven traffic patterns, ample parking, and the kind of no-frills aesthetic that reinforced the warehouse pricing message. A former Treasure Island or Kmart transformed into Home Depot sent a clear signal: this is where you come for deals, not decor.

By the late 1980s, Home Depot had crossed the 50-store threshold and was generating over $1 billion in revenue. The company that had started the decade as a three-store Atlanta curiosity was now a force that suppliers couldn't ignore. This scale created a virtuous cycle: better purchasing power meant lower prices, which drove more volume, which justified more stores, which increased purchasing power further.

The relationship with suppliers evolved dramatically during this period. Initially, vendors were skeptical—remember those empty boxes Pat Farrah had to beg for? By 1990, Home Depot was the largest single customer for many manufacturers. The company could demand exclusive products, special pricing, and customized delivery schedules. Some suppliers essentially became Home Depot subsidiaries in all but name, with 50% or more of their production going to those orange-signed warehouses.

By 2003 the company had grown to more than 1,700 stores employing 300,000 people. The Home Depot's growth was unparalleled. It was the youngest company to reach $30 billion, $40 billion, $50 billion, and then $60 billion in sales—though we're getting ahead of ourselves. The foundations for that explosive growth were laid in these expansion years.

The Pro customer—contractors and professional builders—became increasingly important during this period. While the DIY customer got the marketing attention, Pros provided consistent, high-volume sales. A single contractor might spend $50,000 annually, equivalent to hundreds of weekend warriors. Home Depot's ability to serve both segments in the same store was unique—Lowe's explicitly targeted DIY, while traditional building supply companies ignored retail customers.

Employee culture during the expansion years remained remarkably consistent with the founding vision. Despite growing from hundreds to tens of thousands of employees, the orange apron maintained its meaning. Stock options were distributed broadly, creating thousands of employee millionaires by the 1990s. The company's inverted pyramid organizational chart—customers on top, CEO on bottom—wasn't just corporate speak. Associates were empowered to make decisions, accept returns without hassle, and spend whatever time necessary with customers.

The technology investments of this era, primitive by today's standards, were revolutionary for retail. Computerized inventory management allowed stores to track exactly what was selling and reorder automatically. This seems basic now, but in 1988, knowing you had seventeen Milwaukee drills in stock across three stores and fourteen more arriving Tuesday was competitive advantage.

Marketing evolved from those desperate dollar bill handouts to sophisticated campaigns that sold capability rather than products. "You can do it. We can help" wasn't just a slogan—it was a promise that turned intimidated homeowners into confident project tacklers. TV commercials showed real customers completing real projects, not actors pretending to shop. The message was consistent: you're more capable than you think, and we're here to prove it.

The international question loomed throughout this period. Should Home Depot export its model to Canada? Mexico? Europe? The decision to focus exclusively on U.S. expansion until the mid-1990s was deliberate. Marcus believed that America alone offered enough growth for decades, and that international expansion would distract from the core mission. This focus allowed Home Depot to achieve density and dominance that would prove crucial when competition intensified.

By 1995, Home Depot operated over 400 stores and was approaching $20 billion in sales. The company that couldn't get customers through the door in 1979 was now reshaping how Americans thought about their homes. Sunday morning meant coffee and a trip to Home Depot. Kitchen renovations went from five-figure contractor projects to weekend adventures. The orange apron had become as much a part of American retail culture as the golden arches.

But success brought scrutiny. Critics contended that Home Depot's aggressive expansion unfairly drove smaller competitors out of business and created a monopoly in some markets. The mom-and-pop hardware store, that Norman Rockwell fixture of Main Street America, was disappearing. Communities debated whether the jobs and tax revenue Home Depot brought justified the loss of local businesses.

These concerns would intensify in the coming years, but in 1995, Home Depot seemed unstoppable. Marcus was preparing to step back from day-to-day operations, confident that the company's culture and model were unassailable. The board was beginning to think about succession, about taking Home Depot from founder-led entrepreneurship to professional management.

Nobody could have predicted that the next phase would nearly destroy everything Marcus and Blank had built—not through external competition or market changes, but through a fundamental misunderstanding of what made Home Depot work. The stage was set for the Nardelli era.

VI. The Nardelli Era: Six Sigma Meets Retail (2000–2007)

The scene at General Electric headquarters in November 2000 was corporate theater at its finest. Jack Welch, the legendary CEO who'd turned GE into America's most valuable company, was about to announce his successor. Three executives had been groomed for years, subjected to every test Welch could devise. Jeffrey Immelt got the nod. In an intense three-way competition to become CEO of GE, Welch chose Jeffrey Immelt. Nardelli was devastated.

Within minutes of the announcement, Nardelli was offered the presidency of Home Depot. He demanded the CEO's job. The Home Depot board was convinced that the company needed a sophisticated leader from the outside. In December 2000, after 27 years at GE, Nardelli moved to Atlanta with a compensation package amounting to $24 million in 2001.

Ken Langone, still on Home Depot's board after helping found the company, had made the call personally. About ten minutes after Welch let him go, Nardelli received a job offer from Ken Langone, who at the time was on the board of directors of both GE and The Home Depot. Nardelli became CEO of The Home Depot in December 2000 despite having no retail experience.

The hiring seemed inspired at first. Home Depot had grown to over 1,100 stores with $46 billion in revenue, but the entrepreneurial chaos that had fueled its rise was becoming a liability. Same-store sales were flattening. Inventory management was haphazard. Each store operated like its own fiefdom. The board believed they needed a "sophisticated leader"—someone who could bring the operational discipline that had made GE the envy of corporate America.

Bob Nardelli was that sophistication personified. At GE Power Systems, he'd grown sales from $5 billion to $20 billion. He was a Six Sigma black belt, a devotee of Jack Welch's management philosophy that used statistical methods to eliminate defects and variation. At GE he was known as "Little Jack." He would bring order to Home Depot's orange chaos.

Using the Six Sigma management strategy used at GE, he dramatically overhauled the company and replaced its entrepreneurial culture of innovative product design with one focused on relentless cost-cutting. Nardelli was credited with doubling the sales of the chain and improving its competitive position. Revenue increased from $45.74 billion in 2000 to $81.51 billion in 2005, while net earnings after tax rose from $2.58 billion to $5.84 billion.

The numbers were undeniable. Under Nardelli, Home Depot became a financial powerhouse. He centralized purchasing, saving billions. He upgraded technology infrastructure, spending $400 million on inventory and tracking systems. He consolidated 157 different employee evaluation forms into two. Everything became measurable, quantifiable, optimizable.

But something was dying in those aisles. Nardelli was notably criticized for cutting back on knowledgeable full-time employees with experience in the trades and replacing them with part-time help with little relevant experience. This move reduced costs, but hurt customer service at a time when Lowe's was making inroads nationwide.

The cultural transformation was jarring. He hired dozens of command-and-control military guys to manage. He shifted Home Depot away from retail to a new contracting business that could more easily be controlled and measured. He was comfortable with this low-margin, wholesale business because it fit into his managerial style. When you live by measurement and numbers, that's what you build--things you can easily measure--such as whole contracting operations. Nardelli gutted the retail side by cutting the great, knowledgeable salespeople who were so helpful to customers.

Although Home Depot cofounders Bernie Marcus and Arthur Blank continued on as cochairmen, Nardelli and the board soon asked Blank to leave, and Marcus later retired. The founders watched from the sidelines as their customer-obsessed culture was systematically dismantled and replaced with GE-style process optimization.

Employees who'd once spent hours teaching customers how to install tile were now measured on transaction speed. The inverted pyramid—customers on top, CEO on bottom—was flipped. Store managers who'd run their locations like small businesses were replaced with ex-military officers who understood command structures. The orange apron, once a symbol of expertise and empowerment, became just a uniform.

According to Barry Henderson, an equities analyst at T. Rowe Price, the Baltimore, Md.-based mutual fund company, Nardelli made "two big mistakes" at Home Depot: He alienated employees and angered stockholders. Henderson says the alienation of the rank-and-file at the home improvement retailer has been largely overlooked by the business press in analyses of Nardelli's departure. Nardelli concentrated on overhauling Home Depot's business processes, which did need to be addressed, but he "overfocused" on the processes and swept aside the elements that made Home Depot special. For one thing, Nardelli angered people by firing long-time Home Depot executives and bringing in GE alumni

Customer complaints soared. The American Consumer Satisfaction Index showed Home Depot's scores declining year after year under Nardelli's tenure. Meanwhile, Lowe's—which had explicitly positioned itself as the friendly alternative—saw its satisfaction scores rise. The weekend warriors who'd made Home Depot their second home started shopping elsewhere.

The stock market rendered its verdict coldly. During Nardelli's tenure, The Home Depot stock was essentially steady while competitor Lowe's stock doubled, which along with his $240 million compensation eventually earned the ire of investors. While Nardelli was doubling revenues, shareholders watched their investment stagnate as the rest of the market boomed.

The May 2006 annual shareholder meeting became Nardelli's Waterloo. He limited shareholder questions to one minute. Board members didn't even show up. When investors tried to question his compensation—which would total over $240 million for six years of flat stock performance—Nardelli cut them off. The meeting lasted 30 minutes. It was corporate arrogance at its worst.

Seth Godin gets it right when he says that consumer complaints about Home Depot soared under Nardelli. He alienated his customers, his employees and ultimately, his shareholders, who were infuriated at Nardelli's huge compensation while the stock languished. Nardelli's arrogant behavior at the last annual meeting seemed to seal his fate. His compliant board which gave him so much money despite that lagging stock price, finally bought him out with an outrageous package.

Nardelli and the board reached a mutual agreement for Nardelli to resign on January 3, 2007; his severance package was estimated at $210 million. The severance wasn't a golden parachute for failure—it was the price negotiated in 2000 to lure him from GE, an insurance policy against exactly this scenario. But to employees and shareholders, it felt like a final insult.

The Nardelli era revealed a fundamental truth about Home Depot: its competitive advantage wasn't operational efficiency or inventory management systems. It was culture. The passion of associates who loved teaching customers. The entrepreneurial energy of store managers. The sense that everyone, from CEO to cashier, was in the business of empowering Americans to improve their homes.

Nardelli had taken a company built on relationships and tried to run it on processes. He'd replaced expertise with efficiency, passion with procedures. In trying to turn Home Depot into GE, he'd nearly destroyed what made it Home Depot. The company he left behind was financially larger but culturally hollowed out. The question now was whether anyone could bring back the soul of the orange apron.

VII. The Frank Blake Turnaround (2007–2014)

The boardroom was silent as Frank Blake walked in on January 3, 2007. Nobody expected this. The executive vice president who'd worked quietly under Nardelli for five years was suddenly the CEO. Wall Street was skeptical—Blake had never run anything close to this scale. Employees were wary—was this just Nardelli 2.0? But Blake had something nobody anticipated: humility and a deep reverence for what Home Depot used to be.

Soon after becoming the top executive at Home Depot in 2007, Frank Blake read to employees on a live TV broadcast from a copy of "Built from Scratch," the company biography written by founders Bernie Marcus and Arthur Blank. It was theater, but meaningful theater. Here was the new CEO literally reading from the founders' playbook, signaling that the Nardelli era's obsession with Six Sigma and operational metrics was over.

After Nardelli resigned as chairman and CEO on January 3, 2007, amid controversy over the company's stagnating stock price, poor customer service and Nardelli's salary, Blake was elevated to these positions. The irony wasn't lost on anyone—Blake had been Nardelli's longtime protégé at GE, then his right hand at Home Depot. Indeed, Blake repudiated many of his predecessor's strategies, and it has been reported that the two men have not spoken since Nardelli departed Home Depot.

Blake's first moves were symbolic but powerful. He brought back Home Depot's inverted pyramid, on which "CEO" is at the bottom and "customers" are at the top. He brought back Homer badges to award store employees for great service. In 2007, he began granting restricted stock to assistant store managers. These weren't just gestures—they were signals that the company was returning to its roots.

The operational challenges Blake inherited were staggering. The housing market was beginning its historic collapse. Blake took over as chairman and CEO of the U.S.'s fourth-largest retailer in January 2007, just as the financial crisis was starting to fester. Home values were plummeting, credit was tightening, and Americans were about to stop spending on everything, especially home improvement.

Blake's response was counterintuitive. While he could have doubled down on cost-cutting, he instead focused on culture. To this day he still taps Blank and Marcus for advice on how to improve customer service and stay true to the original values of the company they launched in 1978. He regularly walked stores with them, had them speak at manager rallies, made it clear that the founders' vision still mattered.

Blake's strategy has revolved around reinvigorating the stores and its service culture (engaging employees, making products readily available and exciting to customers, improving the store environment, and dominating the professional contracting business, an area in which Home Depot's closest rivals trail far behind), as he recognized that employee morale is a more sensitive issue in retail compared to other industry sectors like manufacturing. Blake was given credit for returning to the "Orange Apron Cult — the nearly religious zeal for knowledgeable employees and high levels of customer service that was the secret of the company's original success"

The Sunday ritual became legendary. Every Sunday he hand-writes dozens of thank-you cards, most of them to store employees who helped customers solve problems. Think about that—the CEO of a $70 billion company spending hours each week handwriting notes to floor associates. It was both touching and strategic, showing employees that customer service wasn't just corporate speak.

He has a monthly live call-in TV show, called InBox Live, broadcast internally to Home Depot stores. Any associate in any store can ask him questions, and they do. The questions, and his answers, are unscripted. This wasn't staged corporate communication—associates asked tough questions about layoffs, strategy, competition. Blake answered honestly, sometimes admitting he didn't know.

But Blake wasn't just a culture warrior—he made brutal business decisions when necessary. Seeing that the home improvement chain itself needed major repairs, he laid off 11,000 staff, sold HD Supply in 2007 and closed the Expo Design Center division in 2009. The HD Supply sale for $8.5 billion was particularly symbolic—this was Nardelli's baby, his attempt to move beyond retail. Blake sold it without sentiment, using the proceeds to shore up the balance sheet.

Blake rebuilt Atlanta-based Home Depot's supply chain and rethought its retail strategy. But unlike Nardelli's top-down transformation, Blake's changes came from listening to stores, to customers, to the market. He didn't impose solutions; he discovered them.

Navigating the 2008 financial crisis required every ounce of Blake's diplomatic skills. Housing starts collapsed from 2.3 million in 2005 to under 600,000 in 2009. Home Depot's same-store sales turned negative for the first time in decades. The company that had never known anything but growth was suddenly shrinking.

Blake's response was measured but decisive. Rather than panic, he focused on market share. If the pie was shrinking, Home Depot would take a bigger slice. He invested in training when competitors were cutting. He improved inventory systems so stores never ran out of key items. He focused relentlessly on the Pro customer, who still had work even in a downturn.

Today things are turning around for Home Depot, which had sales of $68 billion and earnings from continuing operations of $3.3 billion in 2010. Thanks to Blake's renovations, it's performed well during this year's weak housing and job market. Net earnings in Q2 2011 were $1.4 billion, or $0.86 per share, beating analyst expectations.

The employee morale transformation was measurable. Home Depot said a 2009 survey showed associates' morale improved over 2007. Customers are happier too, according to Home Depot's weekly customer surveys. About 100,000 shoppers per week responded to online surveys, consistently showing improvement in service scores.

Yet challenges remained. J.D. Power and Associate results ranked Home Depot last in both home-improvement and appliance sales for customer satisfaction. Even though Home Depot has shown progress in the home-improvement category, the study said, it remained at the bottom due to "weak customer service relative to other retailers." The Nardelli damage ran deep; culture doesn't rebuild overnight.

Blake's leadership style was the antithesis of command-and-control. He asked questions rather than gave orders. In his first three years, he sat down annually with direct reports asking, "What should a new CEO do? What should someone in my job be doing?" He wanted honest feedback, not validation.

He's proud of his tradition of hand-writing thank-you cards to employees on Sundays. His inspiration for this gesture: then–Vice President George H. W. Bush, for whom the onetime lawyer served as deputy general counsel from 1981 to 1983. "He'd spend an hour every morning writing notes to people," recalls Boston native Blake, who has a JD from Columbia Law School. "As a staff member, I remember the feeling of getting a note from the vice president of the United States saying 'nice job' on something.

Divesting HD Supply and refocusing on core retail wasn't just financial engineering—it was philosophical realignment. Home Depot wasn't going to be a conglomerate. It wasn't going to chase every adjacent market. It was going to be the best home improvement retailer in the world, period.

The Pro customer focus intensified under Blake, but with a crucial difference from Nardelli's approach. Where Nardelli saw Pro as a separate business requiring different systems, Blake saw it as an extension of the DIY promise. Pros were just customers who bought more. Serve them well in the same stores, with the same associates, and they'd reward you with loyalty.

By 2014, when Blake handed over the CEO role to Craig Menear, Home Depot had not just survived the housing crisis—it had emerged stronger. Stock price had recovered and surpassed pre-crisis highs. More importantly, the culture had healed. Associates again felt proud to wear the orange apron. Customers again saw Home Depot as a place to learn, not just transact.

Blake's legacy wasn't in the numbers, though those were impressive. It was in proving that culture and performance weren't opposing forces. That you could be operationally excellent without being soulless. That sometimes the best strategy is remembering who you used to be. The company Blake left behind was recognizably the same one Bernie Marcus and Arthur Blank had founded—just 2,000 stores larger.

VIII. The Digital Transformation & Modern Era (2014–Present)

Craig Menear didn't look like a revolutionary when he took over from Frank Blake in November 2014. A 20-year Home Depot veteran who'd worked his way up through merchandising, Menear seemed like the safe, internal choice. But beneath that mild-mannered exterior was someone who understood a fundamental truth: retail was about to be completely reimagined, and Home Depot could either lead that transformation or become its victim.

Craig Menear has served as CEO and President of The Home Depot since November 2014 and Chairman since February 2015. Craig brings decades of retail experience from mass, home center, specialty and big box retailing to his role during a time when the retail landscape is rapidly changing. Unlike his predecessors who'd focused on either operations (Nardelli) or culture (Blake), Menear saw that the future required both—plus something entirely new: digital transformation at massive scale.

Succeeding Frank Blake in these roles, Menear has served as its chief executive officer since November 2014, and as its chairman since February 2015. But Menear's vision went beyond just adding e-commerce capabilities. Under his leadership, the company continues to focus on providing a seamless, interconnected shopping experience that blends the physical and digital worlds – leveraging the convenience of its stores, digital experiences, innovative product offerings and reliable delivery options for Pro and DIY customers.

The numbers told a stark story. Amazon was growing its home improvement category by double digits annually. Younger customers expected to research online, compare prices instantly, watch how-to videos, and choose between delivery, pickup, or shopping in-store—all seamlessly. Meanwhile, Home Depot's website was essentially a digital catalog, and its mobile app was an afterthought.

Building on Blake's success, Menear led Home Depot's continued innovation into integrated digital retail with acquisitions of tech-focused firms like Interline Brands to complement physical stores. He also oversaw further expansion of distribution centers to grow online order fulfillment capabilities. But the real transformation wasn't in acquisitions—it was in reimagining what a store could be.

Menear shared that the leadership team understood that there was no use in fighting the inevitable. Instead, they started to look deeply at the trends that were beginning to unfold and evaluated their entire business against the backdrop of these changes. They embraced the changing world, rebuilt their strategy, and started making headway into the market that they were fairly certain would emerge.

The omnichannel revolution that Menear championed wasn't just about having a website and stores. It was about making them work together in ways nobody had imagined. Buy Online, Pick Up In Store (BOPIS): Nearly 40% of The Home Depot's eCommerce orders are fulfilled through BOPIS. This allows customers to conveniently shop online and pick up their purchases in-store, combining the speed of online shopping with the immediacy of in-store pick-up.

But BOPIS was just the beginning. In 2016, Home Depot also plans to roll out a further BODFS (buy online deliver from store) option, which will enable the retailer to fulfill online orders directly from stores – a strategy that also enables next day delivery within a two-hour window. Stores weren't just places to shop anymore—they were distribution nodes in a vast logistics network.

The transformation required massive investment. Starting in 2018, the company began what would become an $11 billion "One Home Depot" initiative. This wasn't just IT spending—it was a complete reimagining of how the company operated. The strategy is a multi-year, $11 billion modernization effort that it launched in 2018. That investment has transformed how the retailer integrates its physical and digital operations, allowing it to meet rising customer expectations and maintain a competitive edge against both traditional rivals and online-first disruptors.

Pro customer focus and B2B expansion became central to Menear's strategy. While DIY customers got the headlines, Pro customers—contractors, builders, property managers—drove consistent, high-volume sales. A single Pro might spend $100,000 annually, and they valued different things: speed, reliability, credit terms, bulk delivery. Menear invested heavily in Pro-specific services: dedicated checkout, job site delivery, volume pricing programs.

Supply chain investments transformed Home Depot's ability to compete. Furthermore, the company has invested in three direct fulfillment centers (DFCs) – one in California, another in Georgia, and a third in Ohio – to enhance shipping speeds. According to Market Retailer, Home Depot is now able to guarantee two-day parcel delivery to 90% of the US population.

The pandemic that began in 2020 became an unexpected accelerant for Menear's digital strategy. At Home Depot, 60 percent of online orders were completed by curbside pickup. The online growth is supporting new customer acquisition. What might have taken five years to implement was rolled out in months. Curbside pickup, which barely existed before COVID, became a major sales channel almost overnight.

Home Depot has reported a 25% increase in online orders with curbside pickup since launching the service, demonstrating its popularity with customers. The company that had started with Bernie Marcus handing out dollar bills in parking lots was now having customers wait in those same parking lots for associates to load their trunks with online orders.

The digital transformation wasn't without challenges. CEO Craig Minear said that those "investments are significant and long-term in nature." But Home Depot remains optimistic that profits will increase as the user experience improves. Margins came under pressure as the company invested billions in technology while maintaining competitive pricing.

When Craig stepped to the front of the class he reminded us; "We're in the business of delivering great product. That means we need to care deeply about and invest in innovation in our product." Among other things, he explained that the reason customers go to a Home Depot is for quality products, great advice, and a delightful in-store experience. The company needed to invest to deliver best-in-class experiences around the things that made it great because those were going to be the things that enabled its move into the digital age.

In January 2022, The Home Depot announced Craig Menear would be stepping down as the CEO and president effective March 1, 2022, while continuing to serve as the chairman of the board. He was replaced by former executive vice president Ted Decker. The Home Depot®, the world's largest home improvement retailer, today announced that Edward "Ted" Decker has been named CEO and president, and has been elected to the company's board of directors, all effective March 1, 2022. Craig Menear, currently chairman and CEO, will continue to serve as Chair of the Board.

Decker joined The Home Depot in 2000 and was named president and chief operating officer (COO) in October 2020, where he was responsible for global store operations, global supply chain, outside sales and service, real estate, as well as merchandising, marketing and online strategy, serving Pro and DIY customers in stores and online. The transition was seamless—Decker had been groomed for the role and shared Menear's vision of interconnected retail.

The pandemic boom in home improvement created both opportunity and complexity. Home Depot has seen tremendous growth during the pandemic, as nesting trends and a strong housing market inspired Americans to invest in their homes or move to bigger places. That growth has continued, including in the most recent fiscal quarter, even as some consumers hired home professionals in lieu of do-it-yourself projects.

International expansion successes and failures taught important lessons. While Home Depot had largely focused on North America, understanding global markets became crucial for supply chain management and sourcing. The company learned that its model didn't translate directly to every market, but the operational excellence it developed domestically gave it advantages in procurement and logistics globally.

By 2024, the transformation was undeniable. In fiscal 2024, Home Depot online sales surpassed $21 billion. Home Depot fulfilled half of those orders through stores, illustrating the growing importance of a seamless online-to-offline experience. The company that had once been dismissed as a digital laggard was now showing traditional retailers and pure-play e-commerce companies how to blend physical and digital retail.

The modern Home Depot operates as a logistics company that happens to sell home improvement products. Stores function as showrooms, fulfillment centers, pickup locations, and traditional retail spaces simultaneously. Associates armed with mobile devices can check inventory across the network, place orders for delivery, or arrange installation services. The orange apron now comes with as much digital savvy as product knowledge.

Yet challenges remain. Amazon continues to expand its home improvement presence. New digitally-native brands bypass traditional retail entirely. Labor shortages make it harder to maintain the expert service that differentiates Home Depot. But the foundation Menear and now Decker have built—combining Bernie Marcus's customer obsession, Frank Blake's cultural focus, and cutting-edge digital capabilities—positions Home Depot to compete in any retail environment.

The digital transformation story of Home Depot proves that even 40-year-old retailers can reinvent themselves. It's not about choosing between stores or digital, tradition or innovation, service or efficiency. It's about integrating everything into something greater than the sum of its parts. The company that started with two empty warehouses in Atlanta has become a model for how traditional retailers can thrive in the digital age.

IX. Competition & Market Dynamics

The numbers are stark and unforgiving: Home Depot holds the lead with a market share of approximately 47%, whereas Lowe's commands around 28%. In fiscal 2023, HD reported revenues of $152.7 billion compared with Lowe's $86.4 billion. Yet beneath these headline figures lies a more complex competitive landscape, one where two giants have spent decades locked in a battle that has reshaped American retail and forced both companies to constantly reinvent themselves.

Together, they held an impressive 81% of the home improvement retail market share in 2017. These giants have consistently controlled at least 60% of web sales in this category for the past five years, a testament to their market dominance. While Home Depot has maintained a steady market share of around 43%, Lowe's has gained ground, increasing its share from 17% in 2019 to 21% in 2024.

The David and Goliath narrative doesn't quite fit here—Lowe's is no scrappy underdog. Founded in 1946, thirty-three years before Home Depot opened its first store, Lowe's had the first-mover advantage but somehow became the perpetual second place. The story of this rivalry isn't just about who's bigger; it's about fundamentally different approaches to the same market, and how those differences have created distinct competitive moats.

Home Depot's dominance starts with the Pro customer—contractors, builders, property managers who drive consistent, high-volume business. Home Depot has established itself as the industry leader through its consistent focus on innovation, supply-chain efficiency and its deep integration with Pro contractor services. The brand is widely recognized for its reliability among Pros, supported by a robust infrastructure that enables fast, efficient product delivery and service. This alignment with the Pro segment drives higher transaction values and fosters long-term customer loyalty, giving HD a strong competitive edge.

This Pro focus isn't just about having the right products—it's about building an entire ecosystem. Job site delivery within tight windows. Net 30-day payment terms. Dedicated Pro desks with experienced staff who speak contractor language. Volume pricing that actually makes sense for someone buying fifty sheets of drywall. Home Depot understood early that winning the Pro meant winning the most valuable customers in home improvement.

In contrast, Lowe's positions itself as a more consumer-centric brand, focusing on aesthetically curated in-store experiences, stylish product displays and strength in categories like appliances, lighting and home décor. While this appeals strongly to the DIY demographic, Lowe's continues to lag behind Home Depot in the Pro segment, wherein factors like bulk availability, inventory consistency and rapid fulfillment are key.

The appliance wars illustrate this perfectly. Market Share: Lowe's leads the major appliances market with 40.2% share, staying ahead of Home Depot, which holds 36.2%. Lowe's has made appliances a cornerstone, with beautiful showrooms and exclusive brands. But appliances are largely a one-time purchase for homeowners. Home Depot's Pro customers buy lumber, fasteners, and tools weekly—creating stickier, more profitable relationships.

In fiscal 2024, Home Depot reported revenues of around $152 billion, nearly double of Lowe's $87 billion. Home Depot's net income of $15 billion underscores its superior profitability and operational efficiency compared with Lowe's $7.7 billion, highlighting its financial strength. When comparing market share and key financial statistics, Home Depot maintains a clear and commanding lead over Lowe's in the U.S. home improvement landscape.

The digital battlefield has become increasingly important. Home Depot is projected to reach $23.6 billion in web sales in 2024, while Lowe's is projected to reach $11.3 billion according to Digital Commerce 360's Top 2000 Database. Home Depot expanded its physical footprint in the past seven years by adding 56 new stores, while Lowe's closed 406 locations.

Yet Lowe's strategy of consolidation shows promise. When comparing web sales per store on a five-year CAGR basis, Lowe's outperforms Home Depot (26.5% vs. 21.0%). Lowe's has demonstrated stronger recent growth, outpacing Home Depot by 2.0 basis points in online penetration (ecommerce sales/total sales) since 2018. By focusing on fewer, more productive stores, Lowe's is extracting more value per location even as its overall footprint shrinks.

Amazon looms as the existential threat both companies face. The e-commerce giant's infinite shelf space, algorithmic recommendations, and logistics prowess pose challenges that neither Home Depot nor Lowe's faced from traditional competitors. Amazon is becoming a notable player in the power tools space, with only 1 ppt less share than Lowe's. For categories that don't require expertise or immediate availability—basic tools, hardware, lighting—Amazon is steadily gaining share.

But Amazon's threat has limitations. You can't touch and feel tile samples online. You can't get expert advice on matching paint colors through an app. You can't pick up 20 bags of mulch for a weekend project with two-day shipping. The physicality of home improvement—both in terms of products and expertise—creates a moat that pure e-commerce struggles to cross.

The international expansion story offers lessons in humility for both companies. Home Depot's ventures into China and other markets largely failed, teaching expensive lessons about the cultural specificity of DIY culture. Lowe's similarly struggled internationally, ultimately retreating to focus on North America. The American home improvement model, it turns out, doesn't translate universally.

E-commerce threats continue evolving beyond Amazon. Direct-to-consumer brands now bypass traditional retail entirely for everything from smart home devices to designer fixtures. Specialty e-tailers offer deeper selection in narrow categories. Online marketplaces connect contractors directly with suppliers. Each nibbles at the margins of the home improvement giants' dominance.

From a strategic and operational standpoint, Home Depot has adopted a more aggressive approach by heavily investing in logistics, omnichannel integration and supply-chain automation. Its "One Home Depot" strategy has successfully unified digital and physical shopping experiences, providing seamless access for retail consumers and professional contractors.

Lowe's has been undergoing a multi-year transformation plan aimed at simplifying operations, modernizing its technology infrastructure and enhancing overall store productivity to boost efficiency and competitiveness. Under CEO Marvin Ellison, who joined from Home Depot in 2018, Lowe's has been playing catch-up, but with increasing effectiveness.

The contractor/Pro moat that Home Depot has built represents perhaps the most defensible competitive advantage in the sector. Market Share: Home Depot leads with 46.2%, coming in above all other retailers, including Lowe's who won 37.3% dollar share. Notably, Walmart and Amazon are making a name for themselves in this space at 7.9% and 7.7% respectively.

Why does the Pro moat matter so much? Professional customers are less price-sensitive—they care more about availability and reliability. They're less likely to switch retailers once they've established relationships and credit accounts. They buy in volume and with frequency that dwarfs consumer purchases. Most importantly, they're largely immune to e-commerce disruption—when you need materials today for a job site, Amazon's two-day delivery is two days too slow.

The market dynamics reveal a mature industry with entrenched positions but continuing evolution. This industry has experienced substantial growth, surging from $24.0 billion in web sales pre-pandemic (2019) to a projected $54.3 billion by the end of 2024. The pandemic accelerated digital adoption, but it also reinforced the value of physical stores as fulfillment nodes.

International expansion successes and failures have taught both companies to focus on their core North American markets. The complexity of adapting to different building codes, construction methods, and cultural attitudes toward DIY proved more challenging than anticipated. The lesson: sometimes the best growth strategy is deepening dominance in markets you understand rather than chasing geographic expansion.

Looking ahead, the competitive landscape will likely be shaped by several factors. Housing stock in America continues to age, creating steady demand for repair and renovation. Millennials entering prime homeowning years bring different expectations—more digital engagement, more DIY confidence from YouTube University, but also less hands-on experience than previous generations.

The rise of the "Pro-sumer"—sophisticated DIYers who tackle professional-grade projects—blurs traditional customer segments. These customers want Pro-quality products with DIY-friendly guidance, creating opportunities for whoever can best serve this hybrid need.

Climate change and sustainability concerns are reshaping product mix and customer priorities. Energy-efficient appliances, sustainable materials, and resilience-focused home improvements represent growing categories that both retailers must navigate carefully.

The talent war for knowledgeable associates intensifies as both companies compete not just with each other but with every other retailer for workers who can provide expert advice. The orange apron and blue vest represent more than just uniforms—they're symbols of expertise that e-commerce can't replicate.

Ultimately, the Home Depot-Lowe's rivalry has been good for consumers, driving innovation, keeping prices competitive, and maintaining service standards. The market is big enough for both to thrive, but their different strategies—Home Depot's Pro focus versus Lowe's DIY emphasis, operational efficiency versus customer experience—ensure the competition remains dynamic. Neither can afford complacency, and that competitive tension continues to push both companies forward.

X. Playbook: Business & Leadership Lessons

The Home Depot story offers a masterclass in business building, destruction, and resurrection. From Bernie Marcus's parking lot humiliation to Frank Blake's handwritten notes, from Bob Nardelli's Six Sigma sledgehammer to Craig Menear's digital transformation, the company's journey illuminates timeless truths about culture, strategy, and the delicate art of scaling values.

The Power of Culture: From Founders to Frank Blake's Restoration

Culture isn't what you say—it's what you celebrate, punish, and perpetuate when nobody's watching. Bernie Marcus and Arthur Blank didn't just build a culture; they architected a belief system. The orange apron wasn't a uniform; it was a statement that everyone, from CEO to cashier, served the customer. The inverted pyramid wasn't corporate poetry; it was organizational physics that determined how decisions flowed.

The Nardelli era proved culture's fragility. In just six years, he transformed Home Depot from a missionary organization to a mercenary one. Associates became employees. Mentors became metrics. The entrepreneurial chaos that had built the company was replaced with process precision that nearly killed it. Nardelli doubled revenues but destroyed the soul—a Faustian bargain that ultimately cost him his job and the company its identity.

Blake's restoration demonstrated culture's resilience—if you're intentional about resurrection. Reading from "Built from Scratch" wasn't nostalgia; it was archaeology, carefully excavating buried values. Those Sunday thank-you notes weren't just nice gestures; they were cultural signals that rippled through 400,000 associates. Culture, Blake proved, can be rebuilt, but only through deliberate, consistent, humble action.

The lesson: Culture is your only sustainable competitive advantage. Products can be copied, prices can be matched, but a genuine culture of service, ownership, and expertise takes decades to build and can't be replicated by competitors who don't share your DNA.

Customer Service as Competitive Advantage in Commoditized Retail

In a world where everyone sells the same hammers and lumber, why does Home Depot win? The answer lies in a paradox: they taught customers to need them less, which made customers need them more. By empowering DIYers with knowledge, Home Depot created emotional bonds that transcended transactional relationships.

This wasn't altruism—it was strategy. A customer who successfully installs their first toilet thanks to an associate's patient guidance doesn't just buy a toilet. They buy confidence. They buy identity. They buy into a relationship that Amazon, for all its algorithmic sophistication, can't match. The margin on that toilet might be 30%, but the lifetime value of that empowered customer approaches infinity.

The Pro customer strategy extends this logic to its ultimate conclusion. By treating contractors not as customers but as partners—offering credit terms, job site delivery, dedicated service—Home Depot embedded itself into their business operations. Switching costs became not just financial but operational and relational. This is moat-building at its finest.

Scale Economics and Supplier Relationships

Scale in retail isn't just about buying power—it's about ecosystem control. When Home Depot became the largest customer for hundreds of suppliers, the relationship fundamentally changed. Suppliers started designing products specifically for Home Depot's specifications and price points. Exclusive products proliferated. Manufacturing capacity was allocated based on Home Depot's forecasts.

This created a virtuous cycle: scale begat selection, selection begat traffic, traffic begat scale. But it also created responsibility. When you control 40% of a supplier's business, their survival depends on your success. This mutual dependency, properly managed, becomes strategic partnership. Improperly managed, it becomes destructive codependency.

The lesson: Scale advantages compound, but only if you use scale to benefit all stakeholders—customers through lower prices, suppliers through volume guarantees, associates through stable employment. Extractive use of scale, squeezing every stakeholder for maximum profit, ultimately destroys the ecosystem you depend on.

The Danger of Bringing the Wrong Playbook

Nardelli's failure wasn't personal—it was philosophical. He brought GE's playbook to Home Depot, like a classical musician trying to lead a jazz ensemble. Six Sigma works brilliantly for manufacturing, where variation is the enemy. But retail thrives on variation—every customer interaction is unique, every project different, every problem requiring creative solutions.

The metrics Nardelli loved—transaction times, inventory turns, labor efficiency—improved dramatically. But the metrics that mattered—customer satisfaction, employee engagement, cultural health—cratered. He optimized everything that could be measured and destroyed everything that couldn't. It's a cautionary tale for any leader: the playbook that made you successful in one context might be poison in another.

Frank Blake understood this. Despite coming from the same GE tree, he recognized that Home Depot needed its own playbook, not imported wisdom. His legal background—trained to ask questions, not impose solutions—served him better than any operational expertise would have. Sometimes the best leaders are those humble enough to learn the business rather than those confident enough to transform it.

Building an Ecosystem

Home Depot didn't just sell products; they built an entire ecosystem around home improvement. DIY workshops taught skills. Pro services provided expertise. Tool rental offered access without ownership. Installation services bridged the gap between DIY ambition and reality. Each element reinforced the others, creating network effects that competitors struggled to replicate.

The ecosystem strategy recognizes that customers don't just want products—they want outcomes. A beautiful kitchen, a sturdy deck, a problem solved. By providing every element needed for that outcome—products, knowledge, services, financing—Home Depot became indispensable to the entire journey, not just the purchase transaction.

This ecosystem thinking extends to digital transformation. Buy online, pick up in store isn't just a fulfillment option—it's ecosystem integration. The app that shows inventory across nearby stores, the YouTube videos teaching techniques, the Pro Xtra loyalty program—each element strengthens the web of connections between Home Depot and its customers.

Capital Allocation: The Unsung Hero

Through different eras and CEOs, Home Depot has consistently excelled at capital allocation—the CEO's most important job that nobody talks about. Share buybacks when the stock was undervalued. Dividends that grew consistently. Strategic acquisitions that filled capability gaps. Disciplined expansion that prioritized market density over geographic coverage.

The decision to sell HD Supply for $8.5 billion wasn't just portfolio optimization—it was philosophical clarity. Home Depot was a retailer, not a conglomerate. The capital from that sale funded digital transformation and supply chain investments that strengthened the core business rather than chasing adjacent opportunities.

The contrast with failed retailers is stark. While others chased fads, loaded up on debt, or diversified into unrelated businesses, Home Depot maintained disciplined focus. Every dollar of capital was evaluated against a simple question: does this strengthen our ability to serve customers in our stores? This discipline, compounded over decades, created enormous shareholder value.

The Innovation Paradox

Home Depot's relationship with innovation is paradoxical. The company that revolutionized retail has been notably conservative about change. They were late to e-commerce, slow to embrace mobile, and resistant to marketplace models. Yet this conservatism might be wisdom in disguise.

By letting others pioneer and make mistakes, Home Depot could adopt proven innovations rather than experimental ones. They didn't need to be first to e-commerce—they needed to be best at integrating digital and physical retail. They didn't need to create a marketplace—they needed to perfect their supply chain. Sometimes fast following beats first moving, especially when you have structural advantages that transcend any single innovation.

The key is distinguishing between core innovations that threaten your model and peripheral innovations that enhance it. E-commerce threatened if seen as replacement for stores, but enhanced if seen as extending store capabilities. Home Depot eventually got this distinction right, though the journey was painful.

Leadership Transitions and Institutional Memory

The progression from Marcus to Blank to Nardelli to Blake to Menear to Decker tells a larger story about leadership evolution. Founders bring vision and passion but often struggle with scale. Professional managers bring process and efficiency but can destroy culture. Servant leaders can restore culture but might lack strategic boldness. The ideal leader combines all three, but they're unicorns.

Home Depot's solution has been to maintain institutional memory through board continuity, founder involvement, and cultural artifacts. "Built from Scratch" isn't just a book—it's organizational scripture. The orange apron isn't just uniform—it's identity. These elements provide continuity through leadership transitions, ensuring that even dramatic changes in strategy don't destroy core values.

The Measurement Challenge

What gets measured gets managed, but what gets managed isn't always what matters. Home Depot's journey illustrates the perpetual challenge of balancing quantifiable metrics with qualitative health. Customer satisfaction scores matter, but not as much as customer lifetime value. Same-store sales matter, but not as much as market share. Stock price matters, but not as much as competitive position.

The best leaders, like Blake and Menear, understood that metrics are tools, not masters. They tracked everything but obsessed over few things. They distinguished between leading indicators (customer satisfaction, employee engagement) and lagging indicators (financial results). Most importantly, they remembered that some of the most important things—culture, morale, reputation—resist quantification entirely.

The Ultimate Lesson

If Home Depot teaches one overarching lesson, it's this: sustainable competitive advantage comes from alignment between strategy, culture, and execution. When all three align—as they did under the founders and again under Blake—magic happens. When they diverge—as under Nardelli—disaster follows.

Strategy without culture is mechanical. Culture without strategy is aimless. Execution without both is pointless. Home Depot's greatest periods combined a clear strategy (serve DIYers and Pros better than anyone), a strong culture (the orange apron service ethos), and excellent execution (supply chain, merchandising, store operations). When any element weakened, performance suffered.

The company that started with children handing out dollar bills in an empty parking lot has become a case study in American business. Not because it's perfect—the scars from the Nardelli era prove otherwise—but because it demonstrates both the heights that aligned organizations can reach and the depths that misaligned ones can plumb. The orange apron endures not as corporate kitsch but as a reminder that in retail, as in life, genuine service to others remains the most sustainable path to success.

XI. Bear vs. Bull Case & Valuation

The investment case for Home Depot splits along a fundamental question: Is this a mature retailer facing secular headwinds, or a dominant platform with decades of growth ahead? The answer determines whether the stock's premium valuation represents dangerous complacency or justified confidence.

Bull Case: The Fortress of Orange

Start with the moat—it's not just wide, it's getting wider. Home Depot's dominant market position isn't merely about being biggest; it's about network effects that compound with scale. Every new Pro customer makes the Pro desk more valuable. Every distribution center makes next-day delivery more economical. Every exclusive product deepens supplier dependencies. This isn't market share that can be competed away—it's structural advantage that reinforces itself.

The Pro customer moat deserves special attention. These customers generate 45% of sales with higher margins, lower price sensitivity, and switching costs that border on prohibitive. Once a contractor establishes credit terms, delivery schedules, and relationships with Pro desk associates, moving to Lowe's isn't just inconvenient—it's operationally disruptive. Amazon can't serve these customers effectively; local suppliers lack the selection. This is as close to customer captivity as retail allows.

Housing stock aging represents a multi-decade tailwind that's often underappreciated. The median U.S. home is now 40 years old. These homes require constant maintenance, periodic updates, and increasingly, major systems replacement. Unlike new construction, which cycles with the economy, repair and maintenance spending is remarkably stable. An aging house doesn't care about recession—the roof still leaks, the furnace still breaks, the kitchen still looks dated.

The digital transformation, far from complete, offers substantial runway. While e-commerce penetration in home improvement lags other retail categories, this is feature, not bug. It means Home Depot can capture digital growth while maintaining store relevance. Their interconnected retail model—where stores become fulfillment nodes—turns the physical footprint from burden to advantage. Every competitor trying to build similar capabilities starts decades behind.

Demographics favor continued growth. Millennials, despite stereotypes about avocado toast and rental preferences, are entering prime homebuying years with surprising enthusiasm for DIY projects. They learned from YouTube, not fathers, but they're equally eager to tackle projects. Meanwhile, aging Boomers increasingly hire Pros for projects they once did themselves—good for Home Depot either way.

The balance sheet provides enormous flexibility. With consistent free cash flow generation exceeding $15 billion annually, Home Depot can simultaneously invest in growth, return cash to shareholders, and maintain financial fortress status. This isn't a retailer scrambling to fund transformation—it's a cash machine with options.

Technology investments are finally paying dividends. The $11 billion "One Home Depot" initiative seemed expensive, but it's creating capabilities competitors can't match. Predictive inventory management reduces stockouts. Computer vision enables visual search. Augmented reality helps customers visualize projects. These aren't gimmicks—they're moats being digitized.

Bear Case: Storm Clouds Gathering

Yet the bear case carries weight. Start with Amazon—not today's Amazon, but tomorrow's. As drone delivery matures, as same-day delivery expands, as AR/VR shopping improves, Amazon's structural disadvantages in home improvement erode. Yes, you can't drone-deliver lumber, but you can deliver everything else. And "everything else" is where margins live.