Horizon Bancorp Inc.: From Small-Town Banking to Regional Powerhouse

I. Introduction & Episode Roadmap

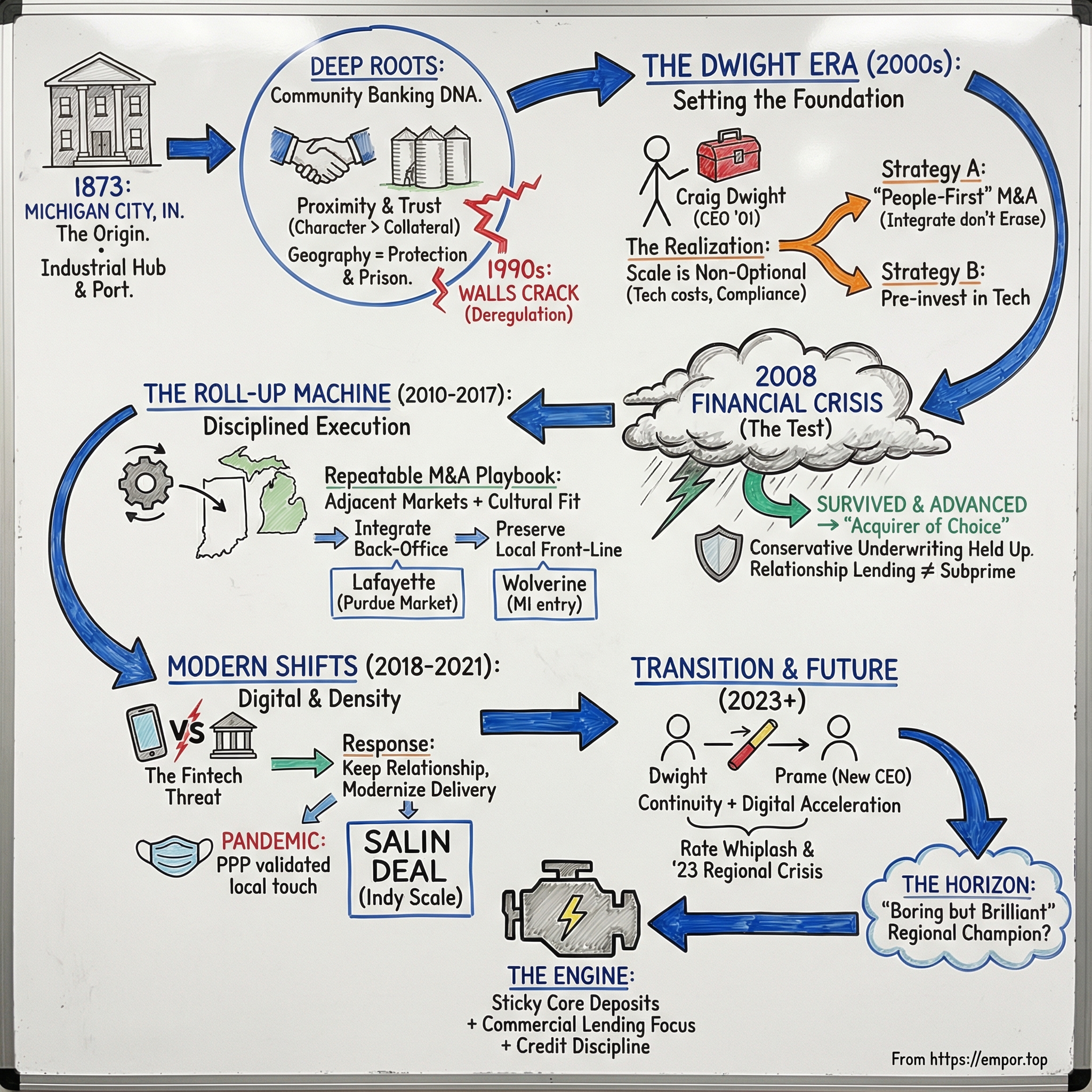

Picture Michigan City, Indiana in the early 1870s. The Civil War is over. Industrialization is accelerating. Great Lakes commerce is surging. Ships move lumber, grain, and iron ore through a busy port town, and behind all that motion is a simple need: working capital for entrepreneurs, and a safe place for families to keep their savings.

Horizon Bancorp was founded in 1873 and is still headquartered in Michigan City.

Fast-forward 152 years. That same institution—now Horizon Bank—has become the commercial bank holding company for a bank with $7.8 billion in assets, serving customers across a set of Midwestern markets it describes as diverse and economically attractive. The journey from a single-town bank to a scaled regional operator isn’t just a growth story. It’s a case study in how “boring” businesses survive long enough to become powerful.

So here’s the deceptively simple framing question: how does a 150-year-old bank from Michigan City become a regional powerhouse, while so many institutions around it either collapsed, got absorbed, or slowly lost their identities to national giants?

The answer is a very Midwestern cocktail: pragmatism, disciplined execution, and a roll-up strategy that—done well—compounds. And it’s also about leadership. Over more than two decades, Craig Dwight helped build an organization that refused to be average. During his tenure, the company grew from roughly $400 million in assets to about $7.7 billion—close to 20x growth in an industry not exactly known for moonshots.

This story matters because community banking is at an existential moment. Consolidation has been reshaping the industry for more than four decades, driven primarily by mergers, with failures and a lack of new entrants adding to the squeeze. The number of banks in America has fallen from over 18,000 in the 1980s to fewer than 5,000 today. In that world, Horizon didn’t just survive. It positioned itself as the consolidator, not the consolidated.

At its core, Horizon is still a community bank serving northern and central Indiana, and southern, central, and the Great Lakes Bay regions of Michigan. Its stated mission is straightforward: anticipate and fulfill customer needs with exceptional service and sensible advice—and it credits that philosophy with keeping it strong since 1873. The interesting part is how you keep saying that, meaning it, and scaling anyway.

Along the way, we’ll keep coming back to a few questions that show up in almost every great business story: How do you scale without losing your identity? How do you buy other companies without destroying what you paid for? What do you do when technology threatens to commoditize your advantage—especially when that advantage is human relationships? And maybe most importantly: can a company be both boring and brilliant at the same time?

II. The Deep Roots: Community Banking in the Midwest (1873–1990s)

To understand Horizon, you first have to understand what “community banking” meant in 19th-century America—and why the Midwest, in particular, turned out to be perfect terrain for it.

Horizon began life in Michigan City, Indiana, in 1873. And Michigan City wasn’t some sleepy outpost. Sitting at the southern tip of Lake Michigan, it was an economic crossroads where trade routes and port traffic connected towns like Chicago and Detroit. Lumber from Michigan, grain from Indiana farms, and the early output of Midwestern factories moved through the region. Money had to move, too—and someone had to be trusted to hold it, lend it, and manage the risk.

That’s where the community bank came in. And it ran on something that’s hard to model and even harder to replicate: proximity. In a place like Michigan City, bankers didn’t just review applications. They knew the people behind them. They saw borrowers at church, in local businesses, and on civic boards. Credit decisions weren’t kicked to a faceless committee in a faraway headquarters. They were made by people who could judge character as naturally as they could judge collateral.

This is the heart of what economists now call relationship lending: the idea that local knowledge creates information you can’t capture in a credit score. A farmer might have a bad year, but if the banker knew he’d survived droughts before and always made good eventually, that context mattered. The model depends on hiring from the community, empowering local decision-makers, and treating trust as an asset on the balance sheet—even if it never shows up in the accounting.

For more than a century, that approach served banks like Horizon well. But it came with a built-in constraint: geography. Regulation—shaped by Glass-Steagall and strict limits on branching—kept most community banks tied to their home turf. Geography was both protection and prison.

Indiana made that especially real. Until July 1, 1985, the state didn’t even allow banks to branch across county lines. A bank in Michigan City couldn’t simply open a branch down the road in another county, much less scale into bigger cities like Fort Wayne or Indianapolis. The result was a patchwork of small, insulated banking empires—great for incumbents with little competition, less great for customers with limited choice, and inefficient for an economy that increasingly needed capital to move faster.

And insulation tends to create bad habits. When customers can’t easily leave, there’s less urgency to modernize. Plenty of community banks of that era operated like comfortable family businesses: conservative, steady, and unprepared for a world where competition could suddenly show up from across the state—or across the country.

Horizon, though, showed hints early on that it didn’t want to just coast. The bank says that in 1974 it became the first bank in Indiana to open an ATM. That’s not just a fun trivia fact. It’s a signal: even in an era when regulation protected the franchise, someone inside Horizon was still asking, “How do we serve customers better?” That instinct—adopt technology without losing the relationship—becomes a recurring theme later.

By the early 1990s, the walls that kept banks local were starting to crack. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 would soon make it far easier for banks to operate across state lines, and consolidation would accelerate. Community banks were heading toward a forced choice: get bigger, get acquired, or get left behind.

For investors, this history isn’t just scene-setting. It’s the origin story of Horizon’s operating DNA: relationship-first lending, conservative underwriting, local authority, and a willingness to embrace new delivery channels without turning the business into something impersonal. Those aren’t just slogans. They’re habits built over 150 years—habits that, as we’ll see, made all the difference once the industry stopped being protected.

III. The Craig Dwight Era Begins: Setting the Foundation (1990s–2000s)

Every long-lived institution eventually hits a moment where “the way we’ve always done it” stops working. For Horizon, that moment arrived in the 1990s—and the person who helped turn it into an advantage was Craig Dwight.

Dwight became Horizon’s CEO in 2001 and its Chairman in 2013. Before that, he served as President and Chief Administrative Officer of Horizon, and beginning in 1998 he was the CEO and Chair of Horizon Bank. In other words: by the time he took the top job, he wasn’t parachuting in. He’d already been in the engine room, watching the industry’s guardrails come off in real time.

And he didn’t need a dramatic reinvention story to see what was happening. The regulatory walls that had protected small banks for generations were weakening. Competition was no longer just the bank across town—it was the bank across the state, and soon, across the country. In that environment, a small community bank could keep doing what it had always done… right up until the day it couldn’t.

The big realization that solidified during this era was simple and slightly brutal: scale was becoming non-optional. Technology spending, compliance obligations, and the fight for experienced talent were rising faster than the economics of a tiny balance sheet could support. A lot of banks were headed for the same fork in the road: merge, sell, or slowly fall behind.

But Dwight also understood the trap inside consolidation. Done poorly, acquisitions don’t create a stronger bank—they create a larger one that’s weaker. When big banks bought community banks, they often did the obvious things: cut costs, centralize decision-making, standardize products. And in the process, they broke the very thing they’d bought. Customers didn’t stay loyal to a logo; they stayed loyal to people and relationships. Remove the people, and the deposits and loans tend to walk out the door.

Horizon’s bet was that it could be the rare acquirer that didn’t commit that sin. Over more than 25 years, Dwight drove Horizon’s success by building a culture centered on putting client needs first, strengthening the communities Horizon serves, and delivering value for shareholders. The strategy wasn’t just “buy banks.” It was: integrate without erasing what made those banks work. Find scale economies where they’re real—systems, operations, duplicative back office—while keeping the relationship model intact.

That meant the early deals weren’t just growth; they were apprenticeships. Horizon began assembling what would eventually look like an acquisition machine: due diligence that cared about culture as much as credit quality, integration playbooks designed to preserve local knowledge, and retention plans to keep the bankers who actually owned the relationships.

The “people-first” culture mattered here in a very practical way. In a world where every seller worries they’re about to be absorbed and stripped for parts, Horizon could credibly say: your team will still matter, and local decision-making won’t disappear overnight. And because they could point to prior deals where they followed through, that promise became a competitive advantage—especially against national acquirers with reputations for centralizing everything.

Under Dwight, Horizon also made a set of technology decisions that look obvious in hindsight and uncomfortable in the moment. Many community banks treated tech as a necessary evil—spend as little as possible and move on. Horizon leaned the other way, upgrading core banking systems, digital platforms, and operational infrastructure to support a much larger organization than it was at the time. It was spending for the bank they intended to become, not the bank they happened to be that year.

By the time the 2008 financial crisis arrived, those choices had quietly shaped a very different kind of institution: conservative underwriting, strong capital ratios, and a growing confidence that it could evaluate and integrate acquisitions with discipline. The playbook was written. Now it was about to be stress-tested in the harshest environment banking had seen in generations.

For anyone trying to understand Horizon today, this is where the patterns were set. Disciplined M&A with an emphasis on cultural fit and geographic adjacency. Technology investment ahead of immediate need. And a culture that treated people as strategy, not as a cost line. None of that is easy to copy quickly—because it wasn’t built quickly.

IV. Surviving the Financial Crisis: The Ultimate Test (2007–2010)

September 2008. Lehman Brothers collapses. Credit markets seize up. And suddenly the panic isn’t confined to Wall Street—it’s everywhere. Banks start failing across America, including the local and community institutions where ordinary families keep their savings and small businesses run payroll.

Lehman—then the fourth-largest U.S. investment bank—filed for bankruptcy on September 15 in what became the largest bankruptcy in U.S. history. The next day, the Fed stepped in to bail out American International Group, the country’s largest insurer. And by September 25, Washington Mutual was seized in what became the largest bank failure in U.S. history. In less than two weeks, confidence—the real currency of banking—was ripped out from under the system.

The crisis did what every crisis does: it separated culture from slogans. Banks that had chased yield by piling into subprime mortgages or complex securities watched their balance sheets detonate. Banks that had loosened underwriting standards to grow faster discovered that growth built on weak credit isn’t growth at all—it’s a time bomb.

Horizon came into the storm with a different posture. Under Dwight, the bank had built a reputation for conservative underwriting, and in this moment that conservatism mattered. Horizon had largely avoided the kinds of products that were destroying competitors—option ARMs, negative amortization mortgages, and no-doc loans. Just as important, the relationship-lending model meant decisions weren’t made purely by spreadsheet. Horizon’s bankers actually knew their borrowers, and credit was extended on the basis of real-world judgment and creditworthiness—not just a FICO score and a model.

“Craig successfully guided Horizon through remarkable growth, as well as periods of economic turmoil, including the Great Recession and the COVID-19 pandemic,” Magnuson said.

And while the crisis was terrifying, it also created a rare, counter-cyclical opening for banks that had stayed healthy. Troubled institutions were suddenly available at distressed prices. Regulators, trying to prevent more outright failures, were motivated to steer weaker banks toward stronger partners. Even the labor market shifted: talented bankers at struggling institutions—people with deep customer relationships but the wrong corporate parent—were suddenly willing to move.

By the time the worst of it passed, Horizon didn’t just survive. It came out stronger than it went in. Competitors failed or pulled back, and Horizon gained share. It attracted talent. And it proved, under the harshest conditions imaginable, that its acquisition and integration instincts weren’t theoretical. This is where the “acquirer of choice” reputation—so valuable in the decade that followed—was forged.

The crisis also validated the broader thesis Dwight had been building toward: consolidation wasn’t a side effect of modern banking. It was becoming the business model. Compliance burdens were rising. Technology costs were climbing. And the economics were increasingly favoring institutions with enough scale to invest, adapt, and still keep the lights on. For banks that preserved capital and competence through 2008, the next decade wasn’t just survivable—it was an opportunity runway.

For anyone evaluating Horizon’s risk management, this period is the clearest proof point. The conservative culture wasn’t marketing copy. It was institutional DNA that protected the franchise when it mattered most—and it set up the next act of the story, when Horizon would start turning disciplined M&A into a repeatable machine.

V. The Roll-Up Machine: Disciplined M&A as Strategy (2010–2016)

Once the dust settled after the financial crisis, the next phase of community banking began: consolidation at speed. Thousands of small banks were bruised from the recession, and now they faced a new reality—higher compliance costs, rising technology expectations, and thinner margins that made staying independent feel less like pride and more like peril. For well-capitalized buyers, it was open season.

Horizon was ready for that moment. And it didn’t approach it like a one-off growth spurt—it approached it like an operating system. You can see the cadence in a line the company would use later, around a Michigan branch transaction: it would be Horizon Bank’s 15th acquisition since 2002 and the fifth in the previous five years, a way of “productively deploying excess capital and cash” at the holding company. The point wasn’t that one deal. The point was the steady drumbeat behind it.

During these years, Horizon’s acquisition playbook hardened into something repeatable. The targets tended to sit in a sweet spot—roughly $200 million to $1 billion in assets. Big enough to matter, small enough to absorb. And the geography wasn’t random. Horizon focused on adjacent markets, building density instead of scattering branches across a map. In banking, proximity isn’t just convenience—it’s efficiency, brand recognition, and an easier integration path.

What made the playbook more than finance was how much effort Horizon put into cultural fit. Due diligence wasn’t only about credit quality and numbers. The team studied how a bank treated its employees, how lending decisions got made, and how deeply the institution was woven into local civic life. Dwight framed it bluntly: “We have a demonstrated history of integrating cultures, prioritizing community involvement and retaining seasoned local bankers, which continue to be key components to our future success.”

Integration followed the same philosophy: centralize what customers don’t see, preserve what they do. Back-office functions like HR, compliance, and technology could be consolidated—there’s no reason to duplicate those in every acquired institution. But on the front lines, Horizon aimed to keep the human machinery intact. Customer-facing operations retained a local feel, branch leaders kept authority, and community ties weren’t treated like dead weight to cut.

And every time they did it, the organization got better at doing it again. Systems conversions became smoother. Retention improved as Horizon built a reputation as a buyer that didn’t automatically gut the acquired bank. The time from close to “this feels normal” kept shrinking.

One of the clearest examples came in 2015, when Horizon acquired Peoples Bancorp of Auburn, Indiana. The $73 million deal gave Horizon entry into Northeast Indiana—its first major push into the Fort Wayne area, one of the state’s largest metropolitan markets. Peoples Bancorp wasn’t a flimsy bolt-on, either. It was a 90-year-old bank with 16 branches across Northeast Indiana and Southwest Michigan.

By then, the geographic intent was hard to miss. Horizon was stitching together a corridor—Michigan City to South Bend to Fort Wayne—stacking market knowledge, local talent, and customer relationships in a way that would be expensive for competitors to dislodge.

The market noticed. In an era when many banks couldn’t grow without taking uncomfortable risks, Horizon was growing by doing something deceptively hard: buying well, integrating well, and repeating it without blowing up the culture. For investors looking back today, this stretch is where Horizon earned the reputation that still defines it—the bank that could consolidate with discipline, pull out real efficiencies, and still protect the relationship value that makes community banking work.

VI. The Transformational Deal: Lafayette Community Bank (2017)

Not all acquisitions are created equal. Some deals simply fill in a few gaps on the map. Others change what a bank can be, where it can compete, and how seriously the market takes it. For Horizon, 2017 was the year it proved it could do the second kind.

On September 1, 2017, Horizon completed its acquisition of Lafayette Community Bancorp and its wholly-owned subsidiary, Lafayette Community Bank.

On paper, it wasn’t the biggest deal. The purchase price was about $32 million. Lafayette reported roughly $172 million in assets and about $20 million in equity as of March 31, while Horizon sat at about $3.2 billion in assets at the same point in time. This wasn’t a “bet the bank” swing.

But strategically, it mattered far more than the headline size. Lafayette Community Bank had been founded in 2000 and built its business in Lafayette and West Lafayette—squarely inside the Purdue University orbit. That market isn’t just another dot in Indiana. It’s a research-university economy with a steady churn of new businesses, student housing demand, and a deeper talent pipeline than most Midwestern towns can claim.

The deal also expanded Horizon’s physical presence: four new branches, bringing the network to 60 offices across northern and central Indiana and southern Michigan and Ohio.

Then came the part that tells you how mature Horizon’s acquisition machine had become: the integration plan. The systems integration and sign change were scheduled for the weekend of September 23—just a few weeks after close. Customers didn’t have to do anything. Accounts would convert automatically, while checks, direct deposits, payments, and even account numbers would stay the same. That kind of “you barely notice it happened” transition doesn’t come from optimism. It comes from reps.

And Horizon didn’t stop there. Just weeks later, on October 17, 2017, it closed another acquisition: Wolverine Bancorp, Inc. and its wholly-owned subsidiary, Wolverine Bank, in Michigan.

Wolverine was no startup. It was originally chartered in 1933 and headquartered in Midland, serving the Great Lakes Bay Region through three full-service banking offices. The acquisition added to Horizon’s Michigan buildout—and it also shaped the company’s governance. Immediately after closing, Horizon appointed Eric P. Blackhurst of Midland to its board. Blackhurst, who had spent much of his career at Dow Chemical, would later become independent chairman of Horizon’s board—an unusually clear line from M&A to long-term leadership evolution.

Together, Horizon’s acquisitions of Lafayette Community Bancorp in Indiana and Wolverine Bancorp in Michigan increased total loans by $445 million.

The results showed up in performance. Horizon earned $33.1 million for the year, up 38 percent from $23.9 million the year before.

More important than any single metric was what 2017 signaled: Horizon could close and integrate multiple deals in rapid succession without losing control of the wheel. The playbook wasn’t just working—it was scaling. And that’s the moment a community bank stops looking like a local operator with ambition and starts looking like a disciplined regional consolidator with real institutional capability.

VII. The Modern Era: Strategic Repositioning (2018–2021)

By 2018, Horizon had done something many community banks never pull off: it had turned itself into a credible regional player. But the ground under the industry was shifting again. A new wave of competitors—fintechs like Chime and SoFi, plus digital-first banks built around clean interfaces and instant onboarding—was unbundling the customer relationship from the branch. They weren’t trying to win with better credit judgment. They were trying to win with convenience.

Horizon’s response wasn’t to abandon relationship banking. That would have been like ripping out the engine to install a nicer stereo. Instead, the strategy was to keep the relationship model—and modernize the delivery layer. Invest in digital so customers could do the basics quickly, while keeping local bankers and decision-making as the difference-maker when the stakes were real: a business loan, a line of credit, a family buying a home.

That same “modernize without losing yourself” mindset showed up in M&A, too.

In 2019, Horizon made its biggest move in years with Salin Bank. Indianapolis-based Salin Bancshares Inc.—the third-largest privately held bank in Indiana—agreed to be acquired by Michigan City, Indiana-based Horizon Bancorp Inc. in a deal worth about $135.3 million.

The logic was straightforward and ambitious: the merger would strengthen Horizon’s core deposit base, expand its presence across central and northeast Indiana, add offices in growth markets like Fort Wayne and Columbus, and deepen its foothold in Indianapolis and Lafayette.

The acquisition closed on March 26, 2019. Salin Bancshares and Salin Bank and Trust Company were merged into Horizon and Horizon Bank immediately.

What made the Salin deal so important wasn’t just the scale—though it had plenty. Salin, a family-owned bank tracing its roots back 116 years to the Farmers & Merchants State Bank of Logansport, had $918.4 million in total assets as of Sept. 30. This wasn’t a couple of branches and a logo. It was a real platform—and it gave Horizon meaningful credibility in Indianapolis, the state’s largest metro area and a market where larger commercial relationships live and die on reputation.

Then came 2020, and the script changed overnight.

The COVID-19 pandemic didn’t just disrupt banking; it rewired customer behavior. Branch lobbies emptied. Remote work became standard. Digital adoption surged—years of incremental change compressed into months.

But in the middle of all that, community banking had a strange moment of resurgence. The Paycheck Protection Program demanded speed, judgment, and local knowledge. Many large banks, built around centralized processes and scale efficiencies, struggled to move quickly. Community banks that knew their customers—who could pick up the phone, verify the story, and make a decision—became critical partners for small businesses fighting to survive.

In September 2021, Horizon pushed its Michigan strategy forward with a different kind of transaction: it acquired 14 branches from TCF National Bank, now The Huntington National Bank after the TCF-Huntington merger. The deal brought 14 branches across 11 Michigan counties, adding density in the Midland market and extending Horizon’s footprint into northern and central parts of Michigan’s Lower Peninsula.

Horizon agreed to pay a 1.75% premium on deposits acquired at closing, or $17.1 million based on deposits of approximately $976 million at March 31, 2021.

And management wasn’t shy about the expected impact: Horizon said it expected the transaction to be in excess of 17% accretive to 2022 earnings per share, excluding non-recurring transaction-related expenses.

Craig Dwight framed it the way a relationship bank would: “I’ve been so proud of our entire team as they remain focused on a well-executed integration of these new branches, which include more than 50,000 primarily retail and small business customers accounts.”

This was Horizon’s opportunism, but the disciplined kind. When big banks merge, they often shed branches for regulatory or strategic reasons. For a well-prepared acquirer, those divestitures can be a shortcut to scale: real customers, real deposits, and a running start in markets you already understand—without the complexity of absorbing an entire institution.

Stepping back, the 2018–2021 stretch showed what Horizon was becoming: not just a serial acquirer, and not just a community bank with a nice story. It was an operator that could absorb meaningful scale, keep investing in digital, and still prove—during a crisis that tested the whole system—that relationships weren’t a nostalgic advantage. They were a practical one.

VIII. The CEO Transition & New Chapter (2021–Present)

Every institution that lasts long enough eventually faces the handoff: can the strategy survive the founder-of-the-modern-era stepping aside? For Horizon, that moment arrived in 2023, when Craig Dwight—after more than two decades shaping the bank’s direction—passed the CEO role to Thomas Prame.

Horizon Bancorp and Horizon Bank announced that Thomas M. Prame would be appointed Chief Executive Officer of both organizations effective June 1, 2023. Craig M. Dwight would retain the Chief Executive Officer title until June 1 and then retire as an employee effective July 3, 2023.

It closed a long chapter. Dwight had served as CEO since 2001 and Chairman since 2013. Before that, he had been President and Chief Administrative Officer of Horizon, and beginning in 1998 he was CEO and Chair of Horizon Bank. He wasn’t just the leader during the roll-up years—he was the architect who helped Horizon become the kind of bank that could do them at all.

The baton pass wasn’t abrupt, either. Horizon announced it had named Prame as President of the Company and its wholly owned subsidiary, Horizon Bank, effective August 15, 2022—an explicit step in expanding the leadership team and setting up an orderly succession.

Prame’s profile was intentionally different from Dwight’s. He came from Chicago-based First Midwest Bank, where he spent about a decade in leadership roles, according to his LinkedIn account. Earlier, he was an executive vice president at Colonial Bank in Montgomery, Alabama, and a national director for several CitiMortgage loan programs.

In Horizon’s own words, Prame joined following a successful run at First Midwest Bancorp, where he held executive officer positions of increasing responsibility after joining in 2012. Most recently he served as Executive Vice President and CEO of Community Banking, where he created and executed strategic plans that increased digital technology, lifted sales productivity, and improved efficiency.

He also brought the kind of Midwest credibility that matters in this business: an MBA from the University of Notre Dame’s Mendoza College of Business, and a Bachelor of Science in economics from the University of Rochester.

If Dwight’s era was defined by building an acquisition machine without breaking community-banking DNA, Prame’s mandate was clear from the start: keep that DNA, but push harder on technology. Prame has been particularly interested in expanding Horizon’s technological capabilities—because the competitive battlefield isn’t just branches and lenders anymore. It’s onboarding flows, mobile experiences, fraud tools, and the ability to serve customers who may never set foot in a lobby.

The transition also balanced continuity with evolution at the board level. Dwight stayed on as Chairman into 2025, providing institutional memory and oversight while Prame ran day-to-day execution. Horizon Bancorp later announced that Craig Dwight, Chairman of the Board, would retire from the Board of Directors effective at the expiration of his current term on May 1, 2025.

At the same time, the Board elected Eric Blackhurst to serve as Independent Chairperson effective upon Dwight’s retirement. Blackhurst had been a director for more than seven years, and his influence had been felt most directly as Chair of Corporate Governance and as a member of the Compensation Committee. In a company that has grown through acquisition, that kind of governance continuity matters—because integrating banks is hard, but integrating leadership is its own kind of risk.

Then, as if to underline why succession planning isn’t a luxury in banking, the macro environment turned volatile.

The 2022–2024 interest rate whiplash created a new set of challenges. After years of near-zero rates compressing margins, the Federal Reserve’s aggressive hiking cycle flipped the pressure points. Securities portfolios that looked safe on day one suddenly carried meaningful unrealized losses once marked to market. Deposit competition intensified as customers could finally earn real yield elsewhere—and they started acting like it.

Horizon responded with balance sheet moves designed to reset profitability and reduce complexity. In December, the Company announced a repositioning that included the sale of $382.7 million in lower-yielding securities and the surrender of $112.8 million of bank owned life insurance (BOLI) policies.

In the fourth quarter of 2024, Horizon announced additional strategic actions designed to simplify the business, strengthen the balance sheet, and improve long-term structural profitability. In October, the Company completed the repositioning of about $325 million of available-for-sale securities.

Operationally, management pointed to improving profitability metrics. The company delivered its sixth consecutive quarter of margin expansion, with margin now above 3%. That was driven by strong organic growth in commercial loans, even as total assets and loans held for investment declined—primarily due to the sale of its mortgage warehouse business.

And looming over all of it was the 2023 regional banking crisis. The failures of Silicon Valley Bank, Signature Bank, and First Republic didn’t just rattle depositors; they rewired what investors and regulators cared about overnight. Suddenly, “stable funding” wasn’t a boring footnote—it was the story. Banks with concentrated, rate-sensitive deposits got punished. Banks with diversified, relationship-based franchises were rewarded.

Horizon argued it fell into the second category. Its conservative culture—the same one that had protected it in 2008—again looked like an asset. The bank’s deposit base remained stable while other institutions saw outflows, and the relationship-driven franchise Horizon had built over decades was exactly the kind of “sticky” funding profile the market revalued in real time.

Credit quality also remained solid. The company reported annualized net charge-offs of 0.03% of average loans during the third quarter, and non-performing assets to total assets of 0.32%, with no material change in the loss outlook. Provision for loan losses of $1.0 million reflected continued positive credit performance.

As of the most recent quarter, the company described its results as being highlighted by a sixth consecutive quarter of margin expansion above 3%, strong loan growth with exceptional credit metrics, and a core funding base that continues to deliver value even in an uncertain economic environment.

For investors, the CEO transition is the most significant governance event of the past decade. The board’s decision to elevate Prame—someone with large-bank experience and a track record in digital and efficiency initiatives—signals where Horizon wants to go next. The open question is the one that hangs over every community bank trying to scale: can Horizon keep what made it special, while adapting to competitive pressures that increasingly reward technological scale?

IX. The Business Model Deep Dive

To really judge Horizon’s strategy—and its odds in a world of fintechs and mega-banks—we need to slow down and explain what a community bank actually is. Not culturally. Economically. Where does the money come from, what can go wrong, and what makes one bank meaningfully better than another?

At the simplest level, banks make a spread. They take in deposits (a liability) and turn that funding into loans and other earning assets (an asset) at higher rates than they pay depositors. That difference flows through as net interest income—the engine that keeps most banks running.

For Horizon, net interest income was $52.3 million in the first quarter of 2025, compared to $53.1 million in the fourth quarter of 2024. The quarter-to-quarter dip wasn’t a collapse in economics so much as a mix issue: average earning assets were lower, and the first quarter had two fewer days. Meanwhile, the thing management actually cares about—the spread—kept improving. Horizon’s net FTE interest margin was 3.04% in the first quarter of 2025, up from 2.97% in the fourth quarter of 2024.

That metric, the net interest margin—or NIM—is the scoreboard. It’s the difference between what the bank earns on loans and securities and what it pays to fund them. In community banking, getting above 3% is generally a sign of a healthy, well-priced balance sheet. Horizon has been trying to expand that margin with disciplined pricing and balance sheet optimization, and in early 2025 it was showing up in the numbers.

Next, look at what Horizon chooses to lend on, because loan mix is strategy in disguise. As of March 31, the loan portfolio was roughly 60% commercial, 17% residential, and 22% consumer—largely unchanged from the prior quarter.

That heavy tilt toward commercial lending matters. Commercial loans—commercial real estate (CRE), commercial and industrial (C&I), and other business lending—tend to carry better yields than vanilla consumer credit, and they fit Horizon’s relationship-banking identity. This is the bank showing you, in portfolio form, what it wants to be: a business bank with deep local ties, not just a branch network that happens to offer mortgages.

Horizon Bancorp operates as the holding company for Horizon Bank, and it runs a full-service menu: checking, savings, money market accounts, certificates of deposit, and both interest-bearing and non-interest-bearing demand deposits. On the lending side, it provides commercial loans, residential real estate, mortgage warehouse loans, consumer loans, land and home equity, auto, and agriculture loans. Beyond that, there’s a whole layer of fee-based services: corporate and individual trust and agency work, investment management, real estate investment trust services, debit and credit cards, treasury management, trust and wealth management, retirement plans, and insurance products.

Which brings us to what might be Horizon’s most valuable asset: deposits.

In banking, deposits aren’t just something you report. They’re a competitive moat—especially the “core” kind, like checking and savings accounts from real households and operating accounts from local businesses. Those balances tend to be stickier and cheaper than wholesale funding. In the first quarter, Horizon reported deposit growth of 1.7% to $5.7 billion, with stable non-interest-bearing balances and growth in core relationship consumer and commercial portfolios.

Then there’s the other lever banks pull when the rate environment gets weird: fee income. Wealth management, treasury services, mortgage banking, and card-related fees help smooth out the fact that net interest income rises and falls with rates and competition. It’s not always the biggest line item, but it matters because it makes the business less one-dimensional.

Of course, none of this works if the cost structure gets out of hand. That’s where the efficiency ratio comes in: non-interest expense divided by revenue. It’s basically a measure of how much the bank has to spend to generate a dollar of income. Community banks often aim for something in the mid-to-high 50s, and scale from M&A is one of the few reliable ways to improve it.

Dwight pointed to this directly as Horizon was integrating acquisitions and pushing technology investments: “Horizon’s strategy to build mass and scale in order to maximize operational leverage is working as we continue to experience lower costs as a percent of average assets,” he said. “Excluding merger expenses, we reduced total non-interest expenses by $10,000 and $217,000 when comparing the first quarter of 2019 to the fourth and first quarters of 2018. This decrease in expenses is the result of focus by our entire team to pursue operational efficiencies and leverage new technologies.”

But the real test—always—is credit.

A bank can look brilliant in a benign environment and still be quietly writing tomorrow’s losses. Horizon’s underwriting discipline has been a recurring theme in this story, and the credit metrics here back it up: net charge-offs were 0.02% of average loans for the quarter, delinquent loans were 0.38% of total loans at period end, and non-performing loans were 0.44% of total loans at period end.

Pulling it all together, the model is clear: Horizon is built around commercial lending, funded by a relationship-driven deposit base, supported by fee businesses that diversify revenue, and protected—so far—by strong credit quality. The tension going forward is just as clear, too. The bank needs to keep these advantages while spending enough on technology to meet modern customer expectations, all while competing against larger banks with more scale and fintechs with cleaner, faster user experiences.

X. Strategic Frameworks Analysis

Porter's Five Forces

Threat of New Entrants: Moderate-High

For most of modern history, banking’s defenses were obvious: you needed capital, a charter, regulatory approval, and a branch network. Those barriers still exist—but fintech found the side door. Through partnerships with licensed banks and Banking-as-a-Service models, new brands can launch fast, reach customers nationally, and compete on what many people experience most: the app.

That’s why digital-first players like Chime and SoFi can feel like “new banks” without actually being banks in the traditional sense.

Horizon’s defense is the stuff that doesn’t fit neatly into a user interface: embedded commercial relationships, a full-service offering that can cover a customer’s financial life, and local decision-making speed that big institutions often can’t match.

Bargaining Power of Suppliers: Low-Moderate

In banking, your suppliers are your depositors—the source of the raw material: funds. When rates rise, those suppliers get choosier. Customers rate-shop. Money moves faster. What used to be sleepy checking balances suddenly turns into a bidding war.

On top of that, banks rely on a small set of core technology providers—FIS, Fiserv, Jack Henry—vendors with real pricing power because switching is expensive, risky, and operationally painful.

Horizon’s position is solid but not immune: it benefits from a relationship-driven deposit base, yet that advantage can weaken during periods when pricing competition gets intense.

Bargaining Power of Buyers: Moderate-High

Borrowers have options. Commercial clients can shop among banks, credit unions, alternative lenders, and, for larger businesses, the capital markets. Retail customers can compare rates instantly and move their money with fewer headaches than ever. The main thing keeping people in place is friction—and digital tools keep sanding that friction down.

Horizon’s edge shows up when speed and flexibility matter: quick answers for business owners, relationship lending that can bend during tough stretches, and full-service capabilities that make switching more painful once treasury services and credit facilities are embedded.

Threat of Substitutes: High

This is the long-term pressure point. Direct lenders can take pieces of small business credit. Cash management fintechs can own treasury functions. Robo-advisors compete for investment accounts. Peer-to-peer payments reduce the centrality of a traditional checking relationship. And crypto, while currently diminished as a mainstream threat, still represents a possible future path to disintermediation.

Horizon’s response is essentially a two-front strategy: improve digital experience so the bank is easy to use day-to-day, while leaning into what tech can’t fully replace—advice, trust, and human judgment.

Competitive Rivalry: High

Horizon competes in a crowded neighborhood. First Merchants is a major Central Indiana player headquartered in Muncie. Old National is another heavyweight, now larger after absorbing First Midwest. Lakeland Financial is a strong regional competitor. And national banks like PNC and JPMorgan can outspend almost everyone on technology and marketing. Then there are credit unions, which operate with tax advantages and a member-first narrative that resonates with many consumers.

Horizon’s differentiation is its attempt to live in the middle ground: enough scale to invest and integrate, enough community DNA to keep relationships and local decisioning real. And, importantly, a track record of executing M&A without constant self-inflicted wounds.

Hamilton's 7 Powers

Scale Economies: Moderate

At nearly $8 billion in assets, Horizon has real scale compared to the sub-$1 billion banks that still populate the Midwest. That scale matters in the unglamorous places: compliance, technology, and back-office operations. But it’s still small next to money-center banks, where scale becomes a superpower measured in orders of magnitude.

Network Effects: Weak

Traditional banking doesn’t get much stronger as more people join, the way a social platform or payments network does. There may be light network effects in business ecosystems—companies that use Horizon for treasury and payments may prefer counterparties who do the same—but that’s incremental, not foundational.

Counter-Positioning: Historically Strong, Now Challenged

For decades, community banks had a clean advantage: big banks weren’t structurally built to profitably serve small towns and small businesses with high-touch service. Standardization was their strength, and it made relationship banking look inefficient.

Digital has changed the math. Fintech can serve customers anywhere with low marginal cost. National banks can offer increasingly personalized digital experiences that mimic parts of what “relationship” used to mean. The geographic moat that once protected banks like Horizon has been shrinking.

Switching Costs: Strong

This is one of Horizon’s most durable advantages. Commercial relationships aren’t just accounts—they’re integrations: ACH setups, credit facilities, treasury workflows, and operating routines. Moving all of that is disruptive and risky, which makes those relationships sticky. Even on the consumer side, people underestimate how much friction is embedded in changing primary banks—though that friction is slowly declining.

Branding: Moderate-Strong (Regional)

In Indiana and Michigan, the Horizon name carries real weight: trust, community presence, and familiarity. But it’s not a national brand, and building one would be expensive and slow. The strategic question isn’t whether Horizon can become a household name everywhere—it’s whether a strong regional brand is enough in a world where banking is increasingly location-agnostic.

Cornered Resource: Weak

Horizon doesn’t own an unassailable asset. Its deposit franchises in specific markets are valuable, but not exclusive. Its relationship bankers are an advantage, but talented people can be recruited away. These are strengths, not true cornered resources.

Process Power: Moderate-Strong

This is where Horizon really differentiates itself. The M&A machine—finding deals, diligencing them, integrating systems, retaining talent, blending cultures—is hard-earned know-how. It compounds with every acquisition. Pair that with underwriting discipline that’s held up across cycles, and you get a set of institutional processes that are difficult for competitors to copy quickly.

Overall Assessment: Horizon’s most durable power comes from Process Power (M&A execution) and Switching Costs (embedded commercial relationships). But it’s operating under real pressure from technology-driven Counter-Positioning. The way forward is keeping the acquisition and risk-management machine humming, while building digital capabilities strong enough that customers don’t get peeled away by better interfaces and faster onboarding.

XI. Bull vs. Bear Case & Investment Perspective

The Bull Case

The bull case for Horizon is less about a single catalyst and more about a set of advantages that reinforce each other over time.

Proven M&A execution, with a long runway still ahead

Community banking is still consolidating. Over the past decade, there have been a little more than 1,700 completed community bank mergers. And with more than 4,000 community banks still operating in the U.S., there’s no shortage of potential sellers. Horizon’s edge isn’t just that it can buy banks—it’s that it has shown it can integrate them, keep the relationships, and make the combined organization stronger. That capability compounds with every deal.

Regional economic tailwinds

Horizon’s footprint sits in parts of Indiana and Michigan that benefit from real economic momentum: manufacturing reshoring, logistics investment as the Midwest becomes more central to distribution, and the commercialization engine around research universities like Purdue. The bet here is that Horizon is anchored in markets with enough churn—new businesses, new projects, new demand—to keep the loan and deposit franchise growing, not just surviving.

A deposit franchise that may be underappreciated

The 2023 banking crisis reminded everyone what’s actually scarce in banking: stable, relationship-based deposits. Horizon argues its deposit base held up during that period, and the bull view is that the market still may not be fully pricing the long-term value of that kind of funding advantage.

Continuity in leadership, without losing momentum

The CEO transition from Craig Dwight to Thomas Prame was structured to preserve the institutional muscle memory that made Horizon successful, while adding new emphasis—especially around digital capability and efficiency. As Horizon’s Lead Director Michele M. Magnuson put it: “The Board is extremely grateful for the dedication and leadership Craig has provided Horizon over the last several decades. During his tenure as Chairman and CEO of Horizon and Horizon Bank, the Company grew from approximately $400 million in total assets to $7.7 billion.”

Optionality: a takeout premium

If Horizon ever becomes the target rather than the buyer, shareholders would likely see a meaningful premium. A buyer wouldn’t just be purchasing loans and branches; it would be buying established markets, a deposit franchise, a seasoned integration machine, and a credit culture that’s proven it can survive stress.

The Bear Case

The bear case is what happens if the industry’s structural pressures overpower Horizon’s strengths.

Scale disadvantage: stuck in the middle

At close to $8 billion in assets, Horizon can be seen as too large to be a pure community bank that wins on intimacy alone, but still far too small to match the technology budgets and operating leverage of truly large regional banks. That “in-between” position can be dangerous: you inherit the complexity without all the benefits of scale.

The technology arms race doesn’t slow down

Customer expectations are set by apps and platforms outside of banking, and that bar keeps rising. The concern is that the level of ongoing investment required to keep up with digital-first challengers—and with national banks that can spend at a different magnitude—could pressure profitability over time.

Commercial real estate risk

Horizon has meaningful exposure to commercial real estate, an area facing multiple headwinds: e-commerce reshaping retail, hybrid work pressuring office demand, and higher rates weighing on valuations and refinancing. Even well-underwritten CRE can become uncomfortable when the macro environment turns.

Midwest demographics

Even if specific pockets of Indiana and Michigan are growing, the broader region still faces population stagnation and talent migration to faster-growing metros. That can cap organic growth and make it harder to expand without continued acquisitions.

Regulatory burden rises with size

As banks grow past certain thresholds, scrutiny increases and compliance obligations expand. The risk isn’t that Horizon can’t comply—it’s that the cost of compliance can rise faster than revenue, especially for banks that are big enough to be watched closely but not big enough to absorb costs effortlessly.

Higher acquisition prices make the math harder

As competition for bank deals increases, it gets harder to buy at prices that are clearly accretive. Credit unions are becoming more active buyers, which can push valuations up. Over the past decade, about 8% of completed community bank mergers involved a credit union or thrift as the buyer. In 2024, seven of the 60 completed community bank mergers included a credit union buyer. That pricing pressure shrinks the margin for error in Horizon’s favorite playbook.

Key Metrics to Watch

If you’re tracking whether Horizon is executing—or drifting—three metrics do most of the telling.

1. Net Interest Margin (NIM)

This is the core earnings engine. Horizon has pushed NIM back above 3%. The key question is whether that can hold as deposit competition remains intense and customers continue to demand higher rates on their money.

2. Commercial loan growth

Commercial lending is where Horizon’s relationship model shows up most clearly—and where it tends to earn the best spreads. Consistent organic growth here signals the franchise can win business without needing M&A to do all the work.

3. Efficiency ratio

Scale is supposed to make the bank more efficient over time. If the efficiency ratio improves, it suggests integrations are working and costs are being controlled. If it worsens, that’s often an early warning sign: integration friction, rising operating costs, or competitive pressure forcing higher spend just to stand still.

XII. Epilogue: The Future of Community Banking

As we wrap this deep dive, Horizon sits at an inflection point—not just as a company, but as a representative example of what community banking is becoming.

Management has been explicit about what it believes is working: six consecutive quarters of margin expansion, with margin now above 3%; strong loan growth paired with exceptional credit metrics; and a core funding base that continues to matter even when the macro picture is murky. The company also pointed to a more efficient expense base entering 2025, plus added flexibility in its capital position after selling its mortgage warehouse business.

That sale, in particular, is a good snapshot of the new era: simplify, sharpen, and redeploy. Horizon completed the sale of its mortgage warehouse business and recorded a pre-tax gain of $7.0 million.

Zoom out, and the strategic pattern of recent quarters is hard to miss. Horizon has been willing to exit lower-margin activities, reposition securities portfolios, and lean harder into core commercial lending. It’s the behavior of a management team that doesn’t believe stability is something you’re granted—it’s something you constantly earn.

Which leads to the big, unavoidable question: can community banks survive long-term?

There are three plausible futures.

1. Continued consolidation into super-regionals

This is the most straightforward path. Consolidation keeps rolling. Strong operators absorb weaker or smaller neighbors. Over time, the winners become regional champions—and then, as history tends to rhyme, those champions either merge with each other or get bought by national banks looking for deposits, density, and local relationships.

2. Niche survival through specialization

Some banks will stay alive by being the best at one thing: agriculture lending, medical practice financing, or serving particular communities where trust and local knowledge aren’t marketing—they’re real barriers to entry. Horizon’s commercial focus could deepen into specific industry verticals where it can build repeatable expertise.

3. A technology-enabled renaissance

This is the optimistic version: community banks pair their human advantage with modern distribution. Banking-as-a-Service partnerships, embedded finance, and AI-driven personalization make it possible to offer digital convenience without giving up relationship intimacy. But it’s also the hardest path, because it demands real investment and cultural change, not just a new app and a press release.

For Horizon, the “regional champion” strategy appears most aligned with where it’s already headed: keep building density across Indiana and Michigan, get to enough scale to fund modern technology expectations, and preserve the relationship culture that differentiates it from national players.

And of course, there are wildcards. Regulation can either speed up consolidation or slow it down. Credit cycles have a way of humbling even well-run banks. And a large national bank could decide Horizon’s franchise—markets, deposits, and operating discipline—is worth acquiring.

So what does “winning” look like five or ten years from now? There are several realistic endings. Maybe Horizon becomes a much larger institution dominating community banking across Indiana and Michigan, with technology that feels closer to a national bank while keeping local decision-making intact. Maybe the endgame is a sale to a larger regional at a healthy premium, rewarding shareholders for decades of disciplined execution. Or maybe it stays independent—one of the few remaining consolidators still capable of buying and integrating without breaking what it acquires.

The lessons, though, are surprisingly timeless.

Process power and execution discipline compound. Horizon’s acquisition capability wasn’t built overnight. It accumulated deal by deal, integration by integration, until it became a durable institutional advantage.

M&A is a skill, not just a strategy. Plenty of companies can announce a deal. Far fewer can integrate consistently, retain key people, and actually realize the benefits.

Sometimes the best moat is just doing boring things well, consistently. There’s nothing flashy about relationship lending or conservative underwriting. But doing them well through multiple cycles builds something rare in banking: trust that holds up under pressure.

Community and relationships still matter—but must digitize. Trust, advice, and local knowledge still win business. The difference now is that customers also expect modern digital experiences, and they won’t wait patiently for a bank to catch up.

“This philosophy is what has kept us growing stronger than ever since 1873.”

In an age of algorithmic lending and digital disruption, Horizon offers a different thesis: that small-town values and sophisticated execution can coexist, that relationship and scale aren’t mutually exclusive, and that boring—done brilliantly—can still win.

XIII. Further Reading & Resources

Top Long-Form References

- HBNC 10-K and Proxy Statements (SEC EDGAR) - The primary source material: how Horizon describes its business, its risks, its strategy, and the governance choices behind the numbers

- FDIC Community Banking Studies - The best macro-level context for why consolidation keeps happening, what “community bank” really means in practice, and how the economics are changing

- Federal Reserve Bank of Kansas City Research - Particularly useful for Midwestern economic and banking analysis, with research that helps explain the environment Horizon operates in

- S&P Global Market Intelligence Regional Banking Reports - Strong for competitive landscape work, deal comps, and transaction data across the regional and community banking sector

- Conference call transcripts - Where you hear the strategy in management’s own voice: what they’re emphasizing, what they’re worried about, and what they believe they can execute

Key Industry Reports

- FDIC Quarterly Banking Profile - A steady baseline for how the industry is performing and what “normal” looks like across cycles

- CSBS Annual Survey of Community Banks - A grounded look at what community bankers say is actually driving their decision-making year to year

- Federal Reserve research on deposit competition and digital transformation - Essential reading for understanding the modern fight for funding and the race to meet rising customer expectations

The community banking story is far from over. And if there’s a takeaway worth sitting with, it’s this: the most interesting advantages in banking are rarely the loud ones. They’re built in process, discipline, and trust—compounded quietly over decades.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube