Huntington Bancshares: Building a Midwestern Banking Powerhouse

I. Introduction & Episode Framework

Picture downtown Columbus, Ohio, on a crisp autumn morning in 2021. Two banking executives—one from Detroit, one from Columbus—stand in the gleaming headquarters of what would become a $175 billion financial giant. The merger papers between Huntington Bancshares and TCF Financial had just been signed, creating the nation's 10th largest regional bank. But this moment wasn't just about size—it was the culmination of 155 years of calculated expansion, survival through multiple financial crises, and a bet that the American Midwest still matters in an increasingly coastal economy.

Huntington Bancshares Incorporated (Nasdaq: HBAN) today stands as a $208 billion regional banking powerhouse, commanding significant market share across twelve states with nearly 1,000 branches. Yet its story begins far humbler—in the back office of a Columbus grain merchant who decided, in the chaotic aftermath of the Civil War, that his city needed a different kind of bank.

What makes Huntington fascinating isn't just its longevity—plenty of banks have survived 150 years. It's how this institution repeatedly reinvented itself at crucial junctures: becoming one of the first bank holding companies in 1966, pioneering 24-hour automated banking in 1972, navigating the treacherous waters of interstate deregulation, and most recently, executing one of the pandemic era's boldest regional bank mergers. Each transformation required not just financial engineering but cultural evolution—maintaining the community bank ethos while building institutional scale.

The themes we'll explore resonate far beyond banking: How do you preserve local relationships while pursuing economies of scale? Can a Midwest-focused strategy thrive when coastal markets dominate headlines? And perhaps most intriguingly—in an era of digital disruption and fintech insurgents, what's the endgame for American regional banking?

This is the story of how P.W. Huntington's conservative private bank evolved into a serial acquirer that would execute over 50 acquisitions, survive multiple existential crises, and emerge as the dominant financial institution across America's industrial heartland. It's about calculated risks, costly missteps (hello, Florida), and ultimately, a lesson in strategic patience that would make Warren Buffett smile.

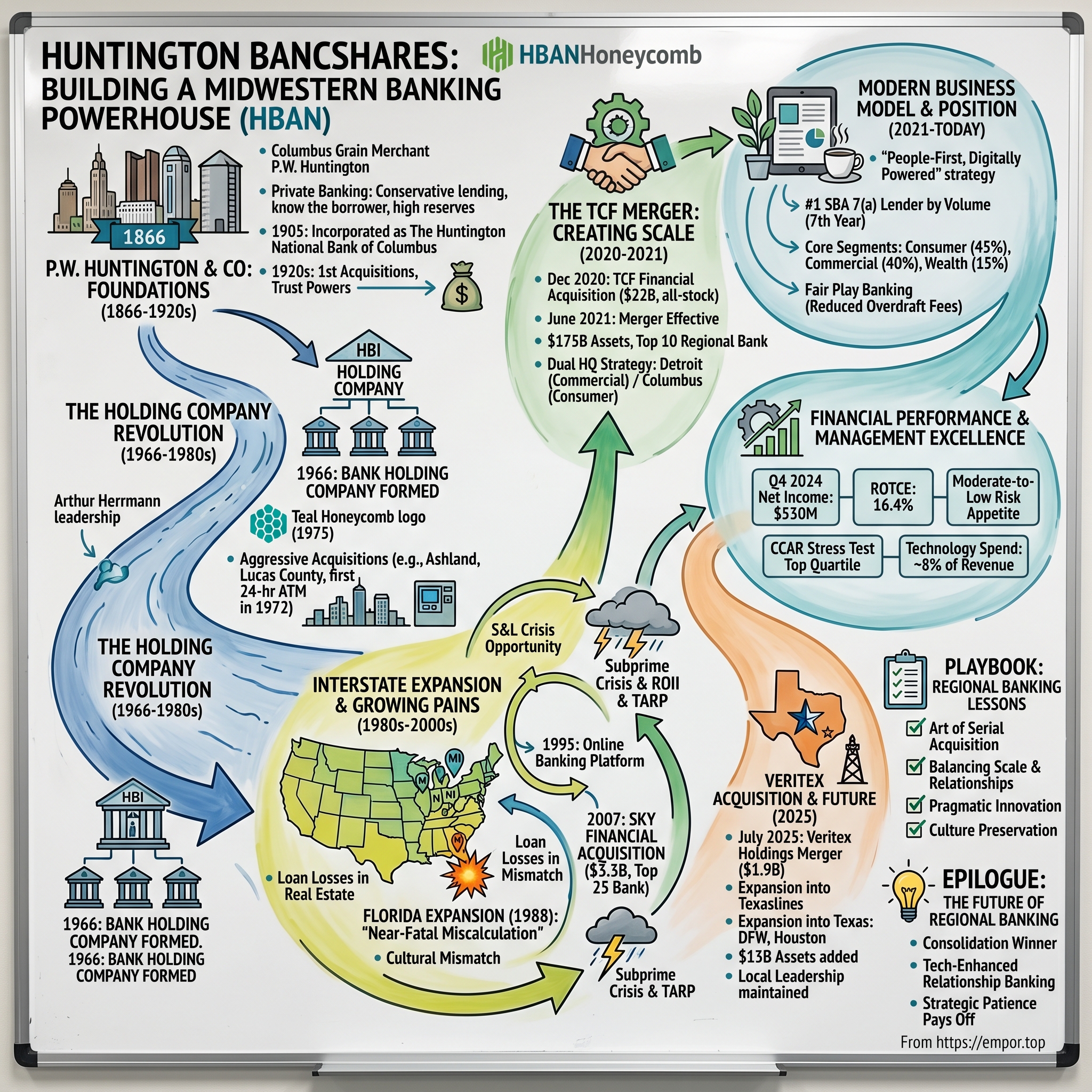

II. P.W. Huntington & The Foundation Era (1866–1920s)

The year 1866 saw Columbus, Ohio, transforming from a wartime supply depot into an industrial boomtown. Railroad lines converged like spokes on a wheel, bringing coal from Appalachia and grain from the plains. Into this economic crucible stepped Pelatiah Webster Huntington—P.W. to his associates—a grain merchant who had noticed something troubling: local businesses were being strangled by Eastern banks that neither understood nor cared about Ohio's unique economy.

P.W. didn't start with a grand vision of interstate banking empires. He opened what was essentially a counting house—P.W. Huntington & Company—offering private banking services to fellow merchants who needed working capital between harvest seasons. His philosophy was radically conservative even by 19th-century standards: know your borrower personally, keep reserves high, and never chase yields into unfamiliar territory. He famously kept a ledger where he recorded not just loan amounts but personal observations about borrowers' character, family situations, and business acumen.

The operation formalized in 1905 when it incorporated as The Huntington National Bank of Columbus, with P.W. bringing four of his five sons into the partnership during the 1890s and early 1900s. This wasn't nepotism—it was succession planning, Victorian-style. Each son learned a different aspect of banking, from credit analysis to operations, creating what would become a multi-generational leadership pipeline.

When P.W. died in 1918, shortly after formally handing control to his sons, the bank held $11 million in assets—substantial for a single-city institution but hardly remarkable nationally. Francis Huntington, assuming the presidency, inherited not just a bank but a philosophy: conservative lending, deep local knowledge, and patient capital accumulation. Under Francis's 14-year tenure, two critical developments emerged that would shape Huntington's next century.

First came trust powers—limited in 1915, then full powers from the Federal Reserve System in 1922. This might seem like bureaucratic minutiae, but it fundamentally changed the bank's relationship with wealthy Ohio families. Suddenly, Huntington wasn't just lending money; it was managing estates, administering trusts, and becoming embedded in the intergenerational wealth transfer of Columbus's industrial elite. This created sticky, profitable relationships that would fund future expansion. Second, and more dramatically, came the initiation of an acquisition program in 1923, when Huntington purchased the State Savings Bank & Trust Company and the Hayden-Clinton National Bank of Columbus, swelling its capital base. This wasn't opportunistic dealmaking—it was strategic consolidation. The Hayden-Clinton merger alone, completed on March 14, 1923, would give Huntington National nearly $11,000,000 in additional resources for a total of about $30,000,000, arranged by Francis R. Huntington himself.

The genius wasn't just in the numbers but in what these acquisitions brought: talent and trust relationships. As a result of its acquisitions, Huntington became active in the trust business—by 1930 the bank's trust assets totaled more than all its other banking assets combined. Think about that transformation: in seven years, a traditional lending bank had become primarily a wealth management institution, all while maintaining its commercial banking core.

This foundation era established three principles that would echo through Huntington's next century: conservative underwriting paired with aggressive acquisition, deep local relationships balanced with institutional scale, and most critically, the ability to transform strategically while appearing operationally stable. As the Roaring Twenties gave way to the Great Depression, these principles would be tested like never before.

III. The Holding Company Revolution (1966–1980s)

The conference room at Huntington's Columbus headquarters hummed with nervous energy in early 1966. Around the polished table sat lawyers, executives, and regulators discussing something that seemed almost subversive: reorganizing a 100-year-old bank into something called a "holding company." The Bank Holding Company Act had been amended, creating a loophole wide enough to drive a stagecoach through—and Huntington was about to become one of the first traditional banks to exploit it.

In 1966, Huntington Bancshares Incorporated was established as a bank holding company, fundamentally altering what had been a single-bank institution into what would become a multi-state acquisition machine. This wasn't just corporate restructuring—it was preparation for war. Interstate banking was still technically illegal, but holding companies could own banks in multiple states as long as they kept them legally separate. It was regulatory arbitrage at its finest.

The transformation accelerated when Arthur Herrmann took leadership in 1975, bringing a diversification mindset that would have horrified old P.W. Huntington. But Herrmann understood something fundamental: Ohio's industrial economy was changing, and banks that didn't adapt would become acquisition targets themselves. In 1975, the company changed its logo to its current "honeycomb" logo—a visual signal of interconnected strength rather than monolithic power.

The acquisition spree that followed was breathtaking in scope and surgical in execution. In 1967, Huntington Bancshares acquired the Washington Court House-based The Washington Savings Bank. In 1969, it acquired the Ashland-based Farmers Bank. In 1970, it also acquired the Bowling Green-based Bank of Wood County Company, the Toledo-based Lucas County State Bank, and Lagonda National Bank of Springfield. Each target was chosen not just for deposits but for geographic positioning—creating a hub-and-spoke model across Ohio's secondary cities.

The pace intensified in 1971-1972, with acquisitions including First National Bank & Trust Company of Lima, The Woodville State Bank, Portage National Bank of Kent, The First National Bank of Wadsworth, and The First National Bank of Kenton. But here's where Huntington distinguished itself from peers: while others were buying banks, Huntington was simultaneously revolutionizing banking operations. In 1972, it established the first 24-hour, fully automated banking office—a move that seems quaint now but was revolutionary then, essentially creating the prototype for modern ATM networks.

The numbers tell the story of transformation: assets grew from just $400 million in 1966 to nearly $2.5 billion by 1979, while the institution expanded from a handful of Columbus offices to 97 locations through 15 affiliated banks. But the real achievement was cultural. Huntington had figured out how to maintain local bank relationships while achieving holding company scale—each acquired bank kept its local management and community connections while tapping into Huntington's growing technological and capital resources.

This period also saw the emergence of what would become Huntington's signature management style: promote from within, maintain operational autonomy at the local level, but centralize technology and risk management. It was federalism applied to banking—strong local governance with powerful central coordination on matters of systemic importance.

The regulatory environment was shifting beneath everyone's feet. The McFadden Act's restrictions on interstate banking were being undermined by creative legal structures, technology was beginning to blur geographic boundaries, and the savings and loan industry was starting its slow-motion collapse. Huntington, with its new holding company structure and proven acquisition integration capabilities, was perfectly positioned for what would come next: the great deregulation wave of the 1980s.

IV. Interstate Expansion & Growing Pains (1980s–2000s)

Frank Wobst stood before a wall-sized map of the United States in 1985, colored pins marking Huntington's branches clustered tightly in Ohio. "Gentlemen," he said to his executive team, "by decade's end, we'll need pins in at least five states, or we'll be someone else's acquisition." The Interstate Banking and Branching Efficiency Act was still nine years away, but Wobst could read the regulatory tea leaves. Regional banking compacts were forming, creating a narrow window for expansion before the money center banks could swoop in.

The push beyond Ohio started cautiously—Michigan in 1982, Indiana in 1985, Kentucky in 1986. Each expansion required navigating different state regulations, political environments, and competitive dynamics. Michigan proved particularly challenging; dominated by Detroit's big three banks, Huntington had to build presence through small acquisitions in secondary markets like Lansing and Grand Rapids, slowly working toward Detroit's suburbs.

But then came Florida—Huntington's bold bet and near-fatal miscalculation. The Sunshine State seemed irresistible in the late 1980s: explosive population growth, wealthy retirees, booming real estate. Huntington poured resources into building a 126-branch network, acquiring everything from small community banks to troubled S&Ls. By the end of 1998, Huntington ranked as the 31st largest bank in the United States with assets of $28.3 billion and 529 branches in six states, including 187 in Ohio, 135 in Michigan, and 126 in Florida.

The Florida expansion looked brilliant on paper—until it didn't. The state's real estate market, always volatile, crashed harder than anyone anticipated in the early 1990s. Huntington's loan losses mounted, particularly in commercial real estate and construction lending. The cultural mismatch became apparent too: Ohio's conservative lending culture clashed with Florida's aggressive, relationship-light banking style. By 2002, Huntington would sell its Florida operations to SunTrust, taking a painful write-down but preserving capital for Midwest opportunities.

The S&L crisis of the late 1980s and early 1990s provided both challenge and opportunity. While Huntington had to navigate its own credit issues, particularly from Florida exposure, it also picked up failed thrift branches at fire-sale prices from the Resolution Trust Corporation. The key was maintaining capital strength while competitors struggled—Huntington's conservative Midwest portfolio provided ballast against Florida losses.

Technology emerged as the great differentiator during this period. While other regionals focused purely on branch expansion, Huntington invested heavily in digital infrastructure. By 1995, it launched one of the industry's first fully functional online banking platforms. The bank created telephone banking centers that operated 24/7, pioneering what would later be called "omnichannel" banking. These weren't just efficiency plays—they were customer acquisition tools that worked across state lines without requiring physical branches. The 2007 Sky Financial acquisition marked a pivotal moment. The merger, completed on July 1, 2007, saw Sky Financial shareholders receive 1.098 shares of Huntington common stock and $3.023 in cash for each Sky share, valuing the transaction at $3.3 billion. This wasn't just another regional consolidation—it was a bet that the Midwest economy would weather whatever storm was brewing in the mortgage markets. The deal made Huntington the 24th largest U.S.-based bank, with assets over $50 billion.

Timing, as they say, is everything. The Sky deal closed just as the subprime crisis was metastasizing into a full-blown financial meltdown. Within months, Huntington faced a double whammy: integration costs from Sky plus deteriorating credit conditions across all portfolios. The bank participated in TARP, taking $1.4 billion in government capital—a necessary but humbling acknowledgment that even conservative Midwest banks weren't immune to systemic crises. Yet here's what separates survivors from casualties: Huntington used the crisis as cover to fix structural problems. While receiving TARP funds, it aggressively wrote down bad loans, restructured operations, and most importantly, invested countercyclically in technology and talent when competitors were retreating. Huntington repaid the funds ahead of schedule, emerging from the crisis with renewed strength. The crisis, painful as it was, forced the discipline that Florida's boom times had eroded.

V. The TCF Merger: Creating Scale (2020–2021)

December 13, 2020. As COVID-19 ravaged the economy and banks braced for a wave of defaults that would rival 2008, Stephen Steinour made a contrarian bet. Standing before virtual cameras—the pandemic had made in-person announcements impossible—he announced that Huntington would acquire Detroit-based TCF Financial Corporation. The timing seemed either brilliant or insane. Huntington Bancshares and TCF Financial Corporation announced the signing of a definitive agreement on December 13, 2020, under which the companies would combine in an all-stock merger valued at approximately $22 billion. TCF brought $49 billion in total assets and a top 10 deposit market share in the Midwest. At the effective time of the merger on June 9, 2021, each share of TCF common stock was converted into the right to receive 3.0028 shares of Huntington common stock.

The strategic logic was compelling. The combination marks Huntington's entrance into attractive markets in Minnesota and Colorado, as well as new businesses, including inventory finance lending. The headquarters for the Commercial Bank is in Detroit; Columbus remains the headquarters for the holding company and the Consumer Bank. This wasn't just geographic expansion—it was capability acquisition. TCF's inventory finance business filled a gap in Huntington's commercial offerings, while their Minnesota franchise provided entry into a market Huntington had long coveted.

But what made this deal different from typical bank mergers was the integration philosophy. Rather than the usual slash-and-burn approach, Huntington committed to keeping dual headquarters—Commercial in Detroit, Consumer and holding company in Columbus. This distributed leadership model recognized a fundamental truth: in regional banking, local relationships still matter. You can't run Michigan banking from Ohio any more than you can understand Minnesota credit culture from Detroit.

Estimated cost savings of the combined company are approximately $490 million, or 37% of TCF's noninterest expense—aggressive but achievable through back-office consolidation while maintaining front-office presence. The regulatory process proved surprisingly smooth, though the Department of Justice required the divestiture of 13 TCF branches in Michigan, a relatively minor concession for a deal of this magnitude.

The numbers told the story: The combined company, with headquarters in Detroit and Columbus, Ohio, has about $175 billion in assets and $142 billion in deposits. But the real achievement was cultural—merging during a pandemic, integrating two different banking philosophies, and emerging stronger. By year-end 2021, with systems conversion complete, Huntington had proven that scale could be achieved without sacrificing the local touch that defines successful regional banking.

VI. Modern Business Model & Competitive Position (2021–Today)

Walk into any Huntington branch today and you'll notice something different. There's no rope line corralling customers toward tellers behind bulletproof glass. Instead, universal bankers with tablets greet customers in an open floor plan that feels more Apple Store than traditional bank. This physical manifestation of Huntington's "People-First, Digitally Powered" strategy represents a $3 billion bet that the future of regional banking isn't choosing between digital and physical—it's seamlessly blending both. The geographic footprint now spans 12 states with 978 branches, serving primarily the Midwest region. But what distinguishes Huntington isn't just physical presence—it's dominance in specific niches. For the seventh consecutive year, the Huntington National Bank is the nation's largest originator, by volume, of Small Business Administration (SBA) 7(a) loans, surpassing $1.5 billion in SBA 7(a) loans and supporting more than 7,500 small businesses. This isn't accident or subsidy—it's strategic focus. While mega-banks chase corporate lending and fintechs target consumer payments, Huntington owns the sweet spot of American capitalism: small business formation.

The business model breaks into three core segments. Consumer banking contributes roughly 45% of revenues through traditional deposit gathering, mortgages, and credit cards—but with a twist. Huntington's "Fair Play Banking" philosophy eliminates most overdraft fees, extends grace periods, and provides 24-hour cushions for deposits to clear. It sounds like leaving money on the table, but it's actually customer acquisition strategy: build trust, reduce churn, capture lifetime value.

Commercial banking, now headquartered in Detroit following the TCF merger, generates about 40% of revenues through middle-market lending, treasury management, and specialized verticals like healthcare, technology, and energy. The remaining 15% comes from wealth management and capital markets—businesses that barely existed twenty years ago but now provide critical fee income diversification.

The technology stack underwent complete modernization between 2019-2023, with over $1 billion invested in digital capabilities. Mobile deposit capture, real-time payments, API-based treasury services—table stakes for any bank today, but Huntington's implementation focuses on simplicity over feature bloat. Their mobile app consistently ranks in the top quartile for user satisfaction, not because it does everything, but because it does essential things exceptionally well.

But here's the strategic insight that most miss: Huntington isn't trying to be a universal bank. The program is part of Huntington's $40 billion Strategic Community Plan, which includes a $2 billion focus on lending to minority-owned businesses or businesses operating in largely minority communities. Lift Local Business is just another way Huntington is reinforcing its commitment to strengthening small businesses and the communities they call home. They're building a fortress in middle America, serving customers that coastal banks ignore and fintechs can't properly underwrite.

The inventory finance business acquired from TCF exemplifies this approach. Floor plan financing for auto dealers isn't sexy, but it's sticky, profitable, and requires deep industry knowledge that Silicon Valley startups can't replicate with algorithms alone. Similarly, their agricultural lending practice leverages 150 years of Midwest relationships—you can't underwrite a grain elevator from a WeWork in San Francisco.

VII. Financial Performance & Management Excellence

Stephen Steinour's corner office overlooks downtown Columbus, but the view that matters is on his computer screen: real-time dashboards tracking deposit flows, loan originations, and credit metrics across twelve states. When he took over as CEO in 2009, Huntington was bleeding from bad loans and investor confidence had evaporated. Today, the bank consistently delivers returns that place it in the top quartile of regional banks—a transformation that required not just strategic vision but operational discipline. The 2024 numbers tell a compelling story. Net income for the 2024 fourth quarter was $530 million, or $0.34 per common share, with return on average assets at 1.05%, return on average common equity at 11.0%, and return on average tangible common equity (ROTCE) at 16.4%. These aren't just respectable numbers—they're top-quartile performance for regional banks in a challenging rate environment.

What's particularly impressive is the consistency. Steinour's management team has delivered positive operating leverage—revenues growing faster than expenses—for 28 of the last 32 quarters. That's not luck; it's operational excellence. The bank maintains an efficiency ratio around 56%, meaning it spends 56 cents to generate a dollar of revenue—well below the regional bank average of 62%.

Credit quality tells another story of disciplined management. "Our credit continues to perform well, consistent with our aggregate moderate-to-low risk appetite. Our credit results for the quarter, including net charge-offs, reflect stability, supported by a positive economic environment." Net charge-offs remain at just 30 basis points, remarkable given the bank's significant exposure to commercial real estate and middle-market lending.

The capital position provides both defense and offense. Common Equity Tier 1 ratio stands at 10.5%, comfortably above regulatory minimums and peer averages. This isn't hoarding capital—it's maintaining dry powder for opportunistic acquisitions while ensuring fortress-like stability. Huntington has consistently passed Federal Reserve stress tests in the top quartile, a testament to conservative underwriting even during expansion phases.

Fee income diversification has accelerated under Steinour's leadership. Noninterest income increased $36 million, or 7%, from the prior quarter, to $559 million. From the year-ago quarter, noninterest income increased $154 million, or 38%. Capital markets revenues, wealth management fees, and payment processing income now contribute meaningfully to the bottom line—revenue streams that barely existed a decade ago.

The management philosophy combines aggressive growth with conservative risk management—seemingly contradictory but actually complementary. Steinour, who joined Huntington after running regional banking at CrossHarbour Capital and Citizens Financial, brought Wall Street sophistication to Main Street banking. His leadership team blends Huntington lifers who understand the culture with outside hires who bring fresh perspectives.

CCAR (Comprehensive Capital Analysis and Review) stress test performance deserves special mention. For nearly a decade, Huntington has not just passed but excelled, typically showing less severe losses under stress scenarios than peer banks. This isn't about gaming the tests—it's about genuinely conservative underwriting, diversified revenue streams, and maintaining significant capital buffers.

The bank's approach to technology spending—roughly 8% of revenues—strikes a balance between innovation and prudence. Rather than chasing every fintech trend, Huntington focuses on technologies that directly improve customer experience or reduce operational costs. Their recent implementation of AI-driven fraud detection reduced false positives by 40% while catching 15% more actual fraud—tangible ROI on technology investment.

VIII. The Veritex Acquisition & Future Growth (2025)

July 14, 2025. The announcement came on a Monday morning that would reshape the geography of American regional banking. Huntington Bancshares and Veritex Holdings, Inc. announced entry into a definitive merger agreement—a $1.9 billion all-stock transaction that would finally give Huntington meaningful presence in Texas, the nation's second-largest economy.

The strategic logic was undeniable. As of March 31, 2025, Veritex reported approximately $13 billion in assets, $9 billion in loans, and $11 billion in deposits. But this wasn't just about adding assets—it was about planting a flag in America's most dynamic growth markets. This strategic acquisition accelerates Huntington's strong organic growth in Texas by expanding its presence in Dallas/Fort Worth and Houston.

Under the terms of the agreement, Huntington will issue 1.95 shares for each outstanding share of Veritex in a 100% stock transaction. Based on Huntington's closing price of $17.39 as of July 11, 2025, the consideration implies $33.91 per Veritex share or an aggregate transaction value of $1.9 billion. The premium—about 23%—was generous but not excessive, reflecting both the quality of Veritex's franchise and the competitive dynamics of Texas banking where everyone from JPMorgan to regional players was hunting for scale.

Steve Steinour framed the deal in strategic terms: "This combination supports our ambitions and reflects our long-term commitment to the state of Texas, one of the most dynamic and fastest-growing economies in the country." But the subtext was clear—after years of organic growth attempts, Huntington needed critical mass in Texas to compete effectively.

The integration playbook borrowed heavily from the TCF success. Holland will stay on at Huntington in a nonexecutive capacity as chairman of its Texas operations. This wasn't just ceremonial—keeping local leadership was crucial in Texas, where banking relationships are intensely personal and outsiders are viewed with suspicion.

As an initial step, Huntington is funding $10 million toward philanthropic investments in Texas. This might seem like corporate virtue signaling, but it's actually shrewd relationship building. Texas banking is as much about community presence as balance sheet strength—you need to be seen at the rodeo, the symphony gala, and the United Way campaign.

The timing reflected both opportunity and necessity. Texas's economy, valued at close to $3 trillion, was attracting corporate relocations at unprecedented rates. Tesla, Oracle, HP—the list of companies moving operations to Texas kept growing. Each relocation meant new banking relationships, treasury management needs, commercial real estate financing. Without scale in Texas, Huntington was missing the biggest economic story in America.

The combination is expected to close early in the fourth quarter of 2025, subject to regulatory approvals and customary closing conditions. The regulatory path should be smoother than the TCF deal—no significant market overlap means fewer required divestitures. But the real challenge will be cultural integration. Texas banking has its own rhythm, its own relationship dynamics. Huntington will need to be a Texas bank that happens to be owned by an Ohio company, not an Ohio bank operating in Texas.

IX. Playbook: Regional Banking Lessons

Step into any business school classroom discussing banking strategy, and Huntington's playbook offers a masterclass in regional bank evolution. The lessons aren't just about M&A execution or technology adoption—they're about threading the needle between scale and intimacy, between standardization and local customization.

The Art of Serial Acquisition and Integration: Huntington has completed over 50 acquisitions since 1966, but here's what's remarkable—they've never had a major integration failure. The secret isn't complex: keep the best people from both sides, maintain local branding during transition periods, and integrate back-office functions first while preserving front-office relationships. The TCF merger exemplified this approach—systems integration took 18 months, but customer-facing changes were gradual and telegraphed well in advance.

Balancing Local Relationships with Scale Economics: The distributed leadership model—commercial banking in Detroit, consumer in Columbus, Texas operations maintaining local leadership—isn't organizational sprawl. It's recognition that regional banking requires regional expertise. You can centralize risk management, technology, and treasury, but lending decisions and relationship management must stay local. A real estate developer in Houston doesn't want to explain Texas property dynamics to a credit officer in Columbus.

Managing Through Rate Cycles: Huntington's asset-liability management through multiple rate cycles reveals disciplined thinking. They've consistently maintained a relatively neutral rate position—not betting heavily on rate directions but focusing on net interest margin stability. During the 2022-2024 rate hiking cycle, while some banks got caught with duration mismatches, Huntington's careful hedging and diverse funding sources kept margins stable.

Technology Investment Philosophy: Rather than trying to out-tech the fintechs, Huntington focuses on "appropriate technology"—solutions that genuinely improve customer experience or reduce costs. Their mobile app doesn't have every bell and whistle, but check deposit works flawlessly. Their commercial banking platform might not match JPMorgan's capabilities, but it handles what middle-market clients actually need. It's pragmatic innovation over innovation theater.

Regulatory Management Excellence: In the post-Dodd-Frank world, regulatory management is a core competency. Huntington's approach—over-communicate with regulators, maintain capital well above minimums, fix problems before they become enforcement actions—might seem overly conservative. But it provides strategic flexibility. While peers wrestle with consent orders, Huntington can pursue acquisitions and new market entry.

Culture Preservation Through Growth: From $400 million in assets to $208 billion, Huntington has maintained remarkable cultural consistency. The "Welcome" philosophy isn't just marketing—it permeates hiring, training, and performance management. They've institutionalized culture through specific practices: promoting from within for key roles, maintaining profit-sharing programs that align employee and shareholder interests, and keeping decision-making distributed rather than centralized.

The deeper lesson is about strategic patience. Huntington didn't chase every trend—they passed on investment banking in the 1990s, avoided subprime lending in the 2000s, didn't rush into cryptocurrency in the 2020s. They picked their spots: small business lending, middle-market banking, wealth management for mass affluent clients. It's not about being everything to everyone but being essential to someone.

X. Bull vs. Bear Case Analysis

The investment case for Huntington splits dramatically depending on your view of American regional banking's future. Bulls see a consolidation winner with sustainable competitive advantages; bears see a melting ice cube in a warming competitive environment.

The Bull Case:

Scale advantages in Midwest markets represent a formidable moat. With top-five deposit share in 70% of its markets, Huntington enjoys pricing power and customer acquisition costs that new entrants can't match. The network effects are real—being the primary bank for local businesses means you get their owners' personal accounts, their employees' mortgages, their suppliers' credit lines. It's an ecosystem, not just a customer list.

The proven M&A execution capability sets Huntington apart. While other regionals stumble through integrations, Huntington has a repeatable playbook. The TCF integration delivered $490 million in cost synergies—37% of TCF's expense base—while retaining key revenue producers. The Veritex deal follows the same template. In a consolidating industry, being the best acquirer is like being the best poker player at the table—eventually, you end up with all the chips.

The strong deposit franchise provides sustainable funding advantages. Core deposits represent 92% of total deposits, with average costs well below market rates. This isn't just about loyal customers—it's about primary banking relationships that are expensive and difficult for competitors to dislodge. In a digital world where money moves in milliseconds, relationship deposits are gold.

Fee income diversification reduces dependence on rate spreads. Capital markets, wealth management, and payments now generate meaningful revenue independent of interest rate cycles. The SBA lending dominance—seven consecutive years as the nation's #1 originator—creates both fee income and deep small business relationships that generate multiple revenue streams.

The Bear Case:

Regional banking faces structural headwinds that no amount of execution excellence can overcome. The cost of compliance keeps rising—regulatory burden consumes 10-15% of operating expenses versus 3-5% pre-2008. Technology investment requirements keep escalating—customers expect Chase-quality digital experiences from regional bank balance sheets. The math gets harder every year.

Integration execution risks multiply with each acquisition. The TCF integration succeeded, but it consumed enormous management attention for two years. The Veritex deal adds complexity in unfamiliar markets. At some point, organizational capacity gets stretched, cultures clash, and integration synergies disappoint. The law of large numbers suggests Huntington's M&A magic can't last forever.

Commercial real estate exposure lurks as a potential time bomb. While current credit metrics look benign, CRE represents 24% of the loan portfolio. With office vacancies at historic highs and retail facing structural challenges, the next downturn could hit harder than expected. Regional banks always look smart in good times—it's the bad times that reveal true risk management.

Net interest margin pressure won't abate. The flat yield curve, deposit competition, and regulatory liquidity requirements create a vice squeezing profitability. Even with perfect execution, it's hard to see margins expanding meaningfully from current levels. The golden age of 4% NIMs is over—permanently.

Competition from both larger banks and fintechs intensifies daily. JPMorgan is aggressively expanding branches in Huntington's markets. Fintechs are unbundling profitable products—payments, lending, wealth management—leaving traditional banks with expensive infrastructure and commoditized offerings. Being stuck in the middle—too small for scale, too big for agility—is a dangerous position.

The Verdict:

The bull and bear cases aren't mutually exclusive—they're both probably right, just on different timelines. Near-term (1-3 years), Huntington's execution excellence, market position, and acquisition pipeline should drive outperformance. The Veritex integration will likely succeed, Texas expansion will gain traction, and consistent earnings growth seems probable.

Long-term (5-10 years), the structural challenges facing regional banking are real and possibly insurmountable. The end game might be further consolidation—Huntington as acquirer becomes Huntington as acquired. But that's not necessarily bearish for shareholders. Being an attractive acquisition target in a consolidating industry can be highly profitable—ask TCF shareholders who received a 30% premium.

XI. Epilogue: The Future of Regional Banking

The conference room on the 30th floor of Huntington's Columbus headquarters offers a panoramic view of the Midwest's economic transformation. Where factories once belched smoke, medical centers and tech campuses now sprawl. Where grain elevators dominated skylines, wind turbines spin lazily. The economy Huntington was built to serve no longer exists—yet the bank thrives. This paradox illuminates regional banking's future.

The consolidation endgame seems inevitable. America doesn't need 4,500 banks when technology eliminates geographic constraints on banking services. The efficient number is probably closer to 50-100 banks: a handful of nationals, couple dozen super-regionals, and specialized players serving specific niches. Huntington, approaching $250 billion in assets post-Veritex, positions itself firmly in that surviving cohort.

But survival requires transformation. The community banking value proposition—knowing your customers, understanding local dynamics, providing relationship-based credit—remains valid but insufficient. Regional banks must layer technological sophistication onto relationship banking, achieving the seemingly impossible: Amazon's efficiency with Main Street's empathy.

Digital transformation for regionals isn't about competing with fintechs on their terms—it's about using technology to enhance what makes regional banking special. AI that helps relationship managers anticipate client needs. Mobile apps that combine functionality with human support. Digital lending platforms that speed decisions without sacrificing underwriting quality. Technology as enhancer, not replacer, of human judgment.

The regulatory evolution will determine much. If regulators continue treating $250 billion banks like systemically important financial institutions, the compliance burden will force further consolidation. But if regulations recognize the difference between regional and money-center banks, a sustainable middle ground might emerge. The political economy suggests some accommodation—America likes the idea of local banks, even if it increasingly banks with national institutions.

What might Huntington's next decade look like? The growth algorithm seems clear: continue consolidating attractive Midwest franchises, build critical mass in Texas and Southeast markets, develop fee businesses that leverage the commercial banking platform. The bank could reasonably reach $400-500 billion in assets through organic growth and strategic acquisitions.

But the more interesting question is strategic optionality. Does Huntington remain an independent super-regional, competing through superior execution and local market knowledge? Does it become a serial acquirer, rolling up smaller regionals into a new model of distributed banking? Or does it eventually sell to a money-center bank seeking Midwest market share?

The answer likely depends on factors beyond Huntington's control: regulatory philosophy, technology evolution, economic cycles, competitive dynamics. But what Huntington does control—execution excellence, credit discipline, cultural consistency—positions it to thrive regardless of scenario.

The lesson of Huntington's 158-year history isn't about predicting the future—it's about building institutions resilient enough to adapt to unpredictable change. From P.W. Huntington's grain-dealer loans to Stephen Steinour's digital transformation, the constant has been pragmatic adaptation rather than strategic revolution.

As regional banking faces existential questions, Huntington offers a possible answer: you don't have to choose between scale and service, between technology and tradition, between shareholders and stakeholders. With skilled management, patient capital, and strategic discipline, you can serve all masters—at least for a while longer.

The view from that 30th floor conference room will undoubtedly change over the next decade. But whether Huntington watches that transformation as an independent company or as part of something larger, it will have proven something important: regional banking, done right, creates value that transcends financial metrics. It builds businesses, strengthens communities, and provides the circulatory system for economic vitality.

That's not a bad legacy for a grain dealer's bank that decided to dream bigger.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube