W.W. Grainger: The Unglamorous $50 Billion Empire That Keeps America Working

I. Introduction & Episode Roadmap

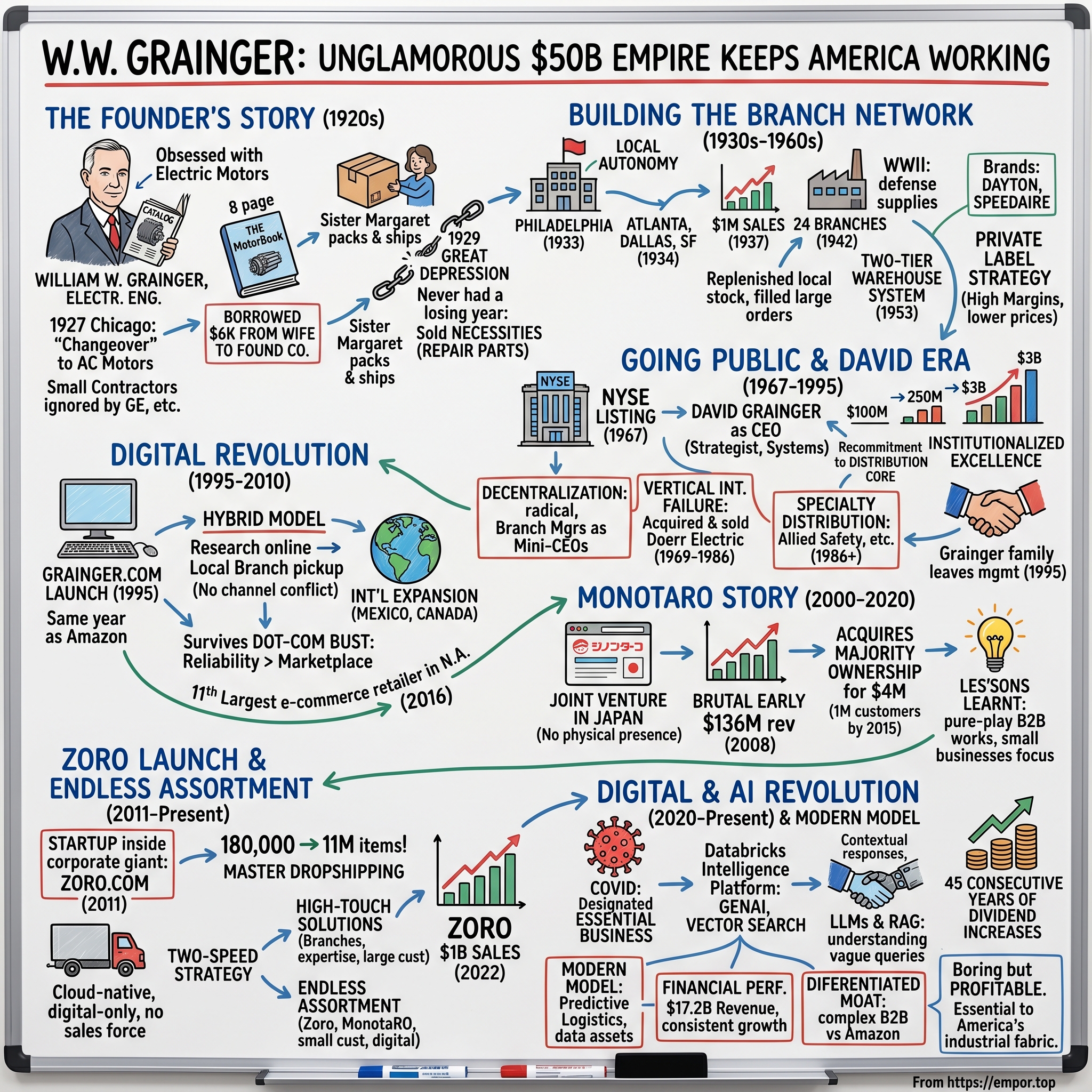

Picture this: It's 1927 Chicago. The city hums with the electric buzz of the Roaring Twenties—jazz clubs, speakeasies, and the intoxicating promise of endless prosperity. But while most entrepreneurs chase glamorous fortunes in stocks or real estate, a 34-year-old electrical engineer named William Wallace Grainger obsesses over something decidedly unsexy: electric motors.

More specifically, he obsesses over why small contractors can't get them.

In 1927, William Wallace Grainger, a 34-year-old electrical motor salesman, recognized a need for a wholesale supply source. He established the company to provide customers with a reliable means of obtaining electric motors. It's a problem so boring, so utterly devoid of jazz-age glamour, that nobody else bothers to solve it. And that's precisely why it becomes the foundation of what is today a company with 2024 revenue reaching $17.2 billion, serving over 4.5 million customers worldwide.

This is the paradox of W.W. Grainger: How an eight-page motor catalog—literally a photocopied price list—evolved into North America's MRO (Maintenance, Repair, and Operations) distribution backbone. "For the ones who get it done"—that's their tagline today, and it perfectly captures the unglamorous truth about their empire. While Silicon Valley obsesses over disrupting everything, Grainger quietly ensures that factories keep running, hospitals stay operational, and the physical infrastructure of civilization doesn't grind to a halt.

Think about it: Every Amazon warehouse, every Tesla factory, every data center powering your Netflix binge—they all need mundane supplies. Safety goggles. Industrial lubricants. Replacement motors. The stuff nobody thinks about until it breaks at 2 AM on a Sunday. That's Grainger's domain, and they've turned this boring necessity into a financial juggernaut that's increased dividends for 45 consecutive years.

The themes we'll explore aren't sexy, but they're profound: How distribution becomes infrastructure. Why boring businesses often build the best moats. And perhaps most fascinating—how a company founded on paper catalogs transformed itself into one of North America's largest e-commerce operations, with $17.2 billion in 2024 revenue flowing through digital channels that would make many tech startups jealous.

II. The Founder's Story & Great Depression Origins

The year is 1927, and something revolutionary is happening to American industry—though almost nobody realizes it yet. As AC transmission and distribution techniques improved around 1900, and a variety of types and sizes of AC motors became available, a gradual swing toward AC began. By 1920 most utility companies were finding the cost of substations excessive and a conversion of systems (called "changeover") was underway.

This technical shift created a massive, fragmented market. As alternating current became standard in the United States, Grainger's market changed. Suddenly, instead of massive DC motors powering entire factory floors through elaborate belt-and-pulley systems, manufacturers could place individual AC motors at each workstation. The demand for small, specialized motors exploded. But here's the problem: manufacturers like General Electric and Westinghouse only cared about volume orders. If you were a small contractor who needed three motors, not three hundred, you were out of luck.

Enter William W. Grainger. Mr. Grainger first worked as a designer of electric motors, and early in his career he recognized the need for the independent distribution of electric motors at the wholesale level in the United States. He wasn't just any salesman—he was an electrical engineer who graduated from the University of Illinois in 1919, someone who understood both the technical specifications and the business opportunity hiding in plain sight.

In the late 1920s, William W. Grainger--motor designer, salesman, and electrical engineer--sought to tap a segment of the market for wholesale electrical equipment sales. He set up an office in Chicago in 1927 and incorporated his business one year later. The company sold goods primarily through MotorBook, an eight-page catalog, which would become the backbone of the company's name recognition.

The MotorBook wasn't fancy. It was literally eight photocopied pages listing motors and prices. Along with his sister Margaret, Grainger built a business based on mail-order catalog sales. Margaret handled the books while William packed boxes. No venture capital, no grand vision statements—just a brother and sister shipping motors from a Chicago storefront.

Then came the market crash of 1929. Two years into building his business, Grainger faced the economic apocalypse that would destroy countless companies. But here's where the story gets interesting: In 1929 he borrowed $6,000 from his wife to found the company that he named for himself, and it has never had a losing year. Think about that—borrowing from your spouse just as the Great Depression begins. That's either insanity or conviction.

The Depression tested everything. Sales in 1932 fell below the previous year's, to $163,000--the first of only four years where sales would not increase. But Grainger survived by doing what would become the company's signature move: being boringly essential. When factories couldn't afford new equipment, they needed parts to repair what they had. When businesses cut to the bone, they still needed basic supplies to function. Grainger wasn't selling luxuries—he was selling necessities.

The genius wasn't just in what Grainger sold, but how he sold it. While competitors required minimum orders or only dealt with established accounts, Grainger would sell to anyone. One motor or one hundred—if you could pay, he would ship. This democratization of industrial supply seems obvious now, but in 1932, it was revolutionary.

By 1933, with the country still mired in depression, Grainger made his next counterintuitive move: expansion.

III. Building the Branch Network: Geographic Expansion (1930s–1960s)

Most Depression-era businesses retrenched, hoarded cash, and prayed for survival. William Grainger looked at the economic wasteland of 1933 America and saw opportunity. Grainger established its first branch in Philadelphia in 1933. Atlanta, Dallas, and San Francisco branches opened in 1934.

The logic was brilliant in its simplicity: As the economy cratered, real estate became cheap, talented workers became available, and competitors disappeared. While others retreated, Grainger advanced. By 1937, when annual sales hit $1 million, the company had sales offices around the country. In just three years of the worst economic conditions in American history, he'd built a national presence.

But physical expansion was just one dimension of Grainger's strategy. The real innovation was organizational. Each branch operated with remarkable autonomy—local managers knew their customers, understood regional needs, and could make inventory decisions without waiting for Chicago's approval. This wasn't the command-and-control structure typical of the era; it was almost federation-like, with each branch functioning as a semi-independent business united by the Grainger catalog and supply chain.

World War II accelerated everything. Branches opened around the country at a brisk pace, with 24 operating by 1942. The war effort created insatiable demand for industrial supplies, and Grainger's distributed network meant they could serve defense contractors from coast to coast. Unlike companies that had to build infrastructure during the war boom, Grainger had spent the Depression years laying groundwork.

The post-war era brought new challenges. Sales more than doubled from 1948 to 1952, calling for organizational adjustments. A single sales representative could no longer serve an entire branch, and in 1948 Grainger expanded the sales force for the first time. The company was evolving from a catalog operation to something more complex—a hybrid of distribution, sales, and service.

In 1953 the company created a regional warehousing system that replenished branch stock and filled larger orders. This two-tier structure—local branches for immediate needs, regional warehouses for bulk orders—would become the template for modern distribution networks. Amazon's fulfillment centers? Home Depot's distribution model? They're all variations on what Grainger pioneered in 1953.

By 1962, with sales at $43.5 million, Grainger had quietly built one of America's most sophisticated distribution networks. But the real competitive advantage wasn't the branches or warehouses—it was the private label strategy that would define the company's next phase.

Brands exclusive to Grainger--Dayton, Teel, Demco, Dem-Kote, and Speedaire—counted for about 65 percent of the company's 1975 sales. These weren't just rebranded generics. Grainger worked directly with manufacturers to create products that met specific customer needs, often with better specifications than name brands but at lower prices. The Dayton motor became legendary among contractors—reliable, affordable, and only available through Grainger.

This private label strategy created a beautiful business dynamic: higher margins for Grainger, lower prices for customers, and zero channel conflict since nobody else could sell these products. It transformed Grainger from a middleman into something more powerful—a curator and creator of industrial solutions.

The branch network also enabled something crucial: relationships. In an era before CRM software, Grainger's local sales representatives knew their customers personally. They knew that the factory on Oak Street ordered replacement belts every third Tuesday, that the hospital preferred overnight delivery, that the contractor doing the airport renovation needed specialty fasteners. This institutional knowledge, distributed across hundreds of branches, became an unassailable moat.

By the mid-1960s, Grainger had built something remarkable: a business that was simultaneously local and national, high-touch and high-scale, specialized and comprehensive. They'd proven that distribution wasn't just about moving boxes—it was about creating infrastructure so reliable that American industry could depend on it absolutely.

The company was ready for its next transformation: going public and scaling beyond what even William Grainger had imagined.

IV. Going Public & The David Grainger Era (1967–1995)

In 1967, forty years after William Grainger started shipping motors from a Chicago storefront, the company took its next evolutionary leap: Grainger was listed on the New York Stock Exchange (NYSE). The timing was deliberate. The founder was 73 years old, his health declining, and succession planning had become critical. But rather than sell to a competitor or private equity (had it existed), Grainger chose the public markets—a decision that would fundamentally reshape the company's trajectory.

In 1968, as sales passed $100 million and the company began to sell stock to the public, William Grainger retired and was succeeded as company chief by his son David. The transition from founder to heir is where most family businesses stumble, but David Grainger was no nepotism hire. David joined the company in 1952 and became a director of it the next year. He'd spent sixteen years learning every aspect of the business, from warehouse operations to customer relationships.

The difference between father and son was stark. William was an engineer who solved problems; David was a strategist who saw systems. William built a distribution network; David would transform it into a diversified industrial powerhouse. "Going from $100 million to $250 million (in 1973) really changed our lives," said David Grainger, "When you reach that level, corporate officers start losing specific control. The top two or three officers no longer can know everything going on everywhere."

This acknowledgment—that scale required fundamental organizational change—drove David's most important decisions. Rather than trying to maintain centralized control, he embraced radical decentralization. Branch managers became mini-CEOs, regional directors gained profit-and-loss responsibility, and the corporate office shifted from commanding to supporting.

David's boldest move came in 1969: Grainger acquired Doerr Electric Corporation, a manufacturer of electric motors. This wasn't just buying a supplier—it was a philosophical shift. For forty years, Grainger had been purely a distributor. Now they were vertically integrating, becoming a manufacturer. The logic seemed compelling: control your supply chain, capture manufacturing margins, ensure product quality.

But by 1986, David reversed course, selling Doerr to Emerson Electric for $24.3 million. The experiment had taught a crucial lesson: Grainger's competitive advantage wasn't in making products but in the distribution ecosystem they'd built. Manufacturing required different skills, different capital allocation, different management focus. The sale of Doerr marked the end of Grainger's manufacturing ambitions and a recommitment to their core competency: being the best distributor in industrial America.

Starting in 1986, David launched a different kind of expansion: specialty distribution. Rather than making products, Grainger would acquire specialized distributors that served niche markets. In 1990, they entered the safety-products distribution business through the acquisition of Allied Safety, Inc. These weren't random acquisitions—each targeted a specific customer need that complemented Grainger's existing offerings. A contractor buying motors might also need safety equipment. A factory ordering lubricants probably needed spill kits.

The David Grainger era established patterns that would define the company for decades: disciplined capital allocation, strategic focus on distribution, and the courage to admit and correct mistakes. When he retired as CEO in 1995, leadership of the company left the hands of the Grainger family for the first time when David Grainger, son of the founder, retired as chief executive officer in 1995. He remained as chair of the board and was succeeded as CEO by Richard Keyser.

The numbers tell the story of David's tenure: from $100 million in sales when he took over in 1968 to over $3 billion when he stepped down as CEO in 1995. But the real achievement wasn't growth—it was institutionalizing excellence. David transformed his father's entrepreneurial creation into a professional organization capable of thriving without any Grainger at the helm.

The company that Richard Keyser inherited in 1995 was radically different from William Grainger's motor catalog business, yet somehow exactly the same: boringly essential, relentlessly reliable, and sitting at the intersection of American industry's most basic needs. But Keyser faced a challenge neither Grainger had confronted: the internet was coming, and it threatened to make physical distribution networks obsolete.

V. The Digital Revolution: From Catalog to E-Commerce Giant (1995–2010)

Richard Keyser's first day as CEO in 1995 coincided with one of business history's most important inflection points. That same year, Amazon sold its first book online, eBay launched as AuctionWeb, and the Netscape IPO ignited the dot-com boom. The conventional wisdom was stark: brick-and-mortar was dead, middlemen would be disintermediated, and any company dependent on physical catalogs and branch networks was doomed.

Grainger's response was extraordinary in its speed and decisiveness. In 1995 the grainger.com website was launched with an electronic catalog, later evolving to an eCommerce platform. Think about that timing—the same year Keyser took over, before most Americans had even heard of the World Wide Web, Grainger was already online. This wasn't a panicked reaction to competitive pressure; it was proactive transformation.

But here's what made Grainger's digital strategy different from the dot-com era's "pure play" fantasies: they didn't see digital and physical as either/or. While competitors were either doubling down on branches or pivoting entirely online, Grainger pursued a hybrid model that seems obvious now but was revolutionary then. The website wasn't meant to replace branches—it was meant to strengthen them.

A customer could research products online at 2 AM, place an order at 6 AM, and pick it up from their local branch by 8 AM. Or they could walk into a branch, have a sales rep help them find an obscure part online, and have it shipped directly to their job site. The digital catalog didn't replace the paper one—it supplemented it with search functions, technical specifications, and real-time inventory data that no printed book could match.

The late 1990s also marked Grainger's first serious international expansion. In the late 1990s, Grainger established operations outside the United States for the first time. In 1996 the company opened a branch in Monterrey, Mexico. The same year, Grainger purchased a division of Acklands, Ltd., a Canadian manufacturer of industrial safety and automotive aftermarket products. These weren't vanity projects or growth-for-growth's-sake moves. Mexico represented the NAFTA opportunity—American factories moving production south still needed MRO supplies. Canada offered a familiar market with similar customer needs but different enough to test Grainger's adaptability.

The dot-com bubble of 1999-2000 created a fascinating dynamic for Grainger. While pure-play B2B marketplaces raised billions and promised to revolutionize industrial procurement, Grainger quietly built actual infrastructure. They integrated their inventory systems across channels, developed sophisticated search algorithms for industrial products, and created customer-specific pricing engines that could handle the complexity of B2B transactions.

When the bubble burst in 2001, the contrast was stark. Ventures like Ventro and VerticalNet—which had raised hundreds of millions to create online industrial marketplaces—evaporated. Grainger not only survived but thrived. Why? Because they understood something the dot-com evangelists missed: B2B purchasing isn't just about price discovery and transaction efficiency. It's about reliability, technical support, credit terms, and the peace of mind that comes from knowing your supplier will still exist tomorrow.

By 2005, Grainger's digital transformation was accelerating in ways that would have seemed like science fiction a decade earlier. They introduced automated inventory management systems that could predict when customers would need reorders. They created punchout catalogs that integrated directly with customers' procurement software. They built APIs before most people knew what APIs were.

The real masterstroke came in how Grainger handled channel conflict—or rather, how they avoided it entirely. Rather than having digital compete with branches, they aligned incentives. Branch managers got credit for online sales in their territory. Sales reps earned commissions whether customers bought in-person, online, or over the phone. This seems obvious now, but in the early 2000s, most traditional companies were tearing themselves apart with internal channel wars.

In 2016, Grainger was named the 11th largest eCommerce retailer in North America by Internet Retailer. Let that sink in. A company founded in 1927 to distribute electric motors via mail-order catalog had become one of the continent's largest e-commerce operations—bigger than many pure-play internet retailers that launched decades later.

By 2010, Grainger had achieved something remarkable: they'd successfully navigated one of business history's most disruptive technological shifts without abandoning their core identity. They were still the boring, reliable, essential supplier to American industry. They just happened to also be a digital powerhouse.

But Keyser and his team weren't satisfied with successfully defending the core business. They saw an opportunity to go on offense, to build entirely new growth engines that leveraged their digital capabilities. The first major move would come through an unlikely source: a joint venture in Japan that would teach Grainger lessons they'd apply globally.

VI. The MonotaRO Story & Asian Expansion (2000–2020)

The year 2000 marked a curious experiment for Grainger. While American dot-coms were imploding and the NASDAQ crashed 78% from its peak, Grainger quietly launched a joint venture 6,000 miles away in Osaka, Japan. Established in 2000 in Osaka, MonotaRO started as a joint venture company between Grainger and Sumitomo Corporation supplying MRO products in Japan.

The name itself tells a story: MonotaRO is both an acronym for Maintenance, Repair & Operations and a play on Momotarō, a legendary Japanese folk hero. It also means "to have sufficient products" in Japanese—a triple-layered meaning that signaled serious intent to localize, not just translate.

Japan's MRO market was the second-largest in the world, but it operated nothing like America's. Distribution was controlled by massive trading houses with centuries-old relationships. Small businesses were served by local suppliers who'd been embedded in communities for generations. The idea that customers would buy industrial supplies online, from a company with no physical presence, seemed absurd.

But MonotaRO's founders spotted an inefficiency hiding in plain sight: Japan's small businesses were dramatically underserved. While large corporations had dedicated procurement departments and negotiated supply contracts, a small machine shop or repair service paid retail prices for everything. The market was huge—hundreds of thousands of small businesses—but so fragmented that traditional distributors ignored it.

MonotaRO's model was radical for Japan: no sales force, no branches, just a website and next-day delivery. MonotaRO has successfully innovated in the Japanese MRO market, the second largest industrial market in the world, offering more than 110,000 products to more than 320,000 customers. They priced everything transparently—no haggling, no relationship-based discounts, just consistent prices visible to anyone with an internet connection.

The early years were brutal. In 2008, eight years after launch, MonotaRO had revenues of $136M and operating earnings of $11 million. Decent numbers, but hardly revolutionary for nearly a decade of effort. Many companies would have written off the experiment. Grainger doubled down.

In 2009, Grainger made a pivotal decision: Grainger plans to become a 53% majority owner of MonotaRO. Grainger expects to invest approximately $4M through a tender offer bid process. The amount seems comically small now—$4 million for majority control of what would become their most successful international venture. Grainger has completed its tender offer bid in Japan for 380,000 shares of MonotaRO Co., Ltd., at a price of 1,010 Yen ($11.11) per common share. As a result of the completion of the transaction, Grainger has achieved a 53% majority ownership in MonotaRO.

What happened next validated everything. MonotaRO's growth exploded. The company went from serving 320,000 customers in 2009 to over 1 million by 2015. They expanded beyond Japan into other Asian markets. Most remarkably, they achieved margins that made Grainger's U.S. business look pedestrian. In 2013, MonotaRO was named to Forbes Asia "Best Under A Billion" list.

But the real value of MonotaRO wasn't the financial returns—it was the education. MonotaRO taught Grainger that pure-play e-commerce could work in B2B. That you didn't need branches if you had the right digital experience. That small businesses, traditionally ignored by industrial distributors, represented massive untapped demand. Most importantly, that the Grainger model wasn't the only model.

These lessons would prove invaluable when Grainger launched their next experiment: Zoro. But MonotaRO also revealed a tension that would define Grainger's next decade. The company now had two successful but fundamentally different models: the high-touch, full-service Grainger approach in North America, and the low-touch, pure-digital MonotaRO model in Asia. Could these coexist? Should they compete? And most importantly, what did this mean for Grainger's future?

The answer would come in 2011, with the launch of a startup inside the corporate giant—a digital-native business built to compete with both Amazon and Grainger itself.

VII. The Zoro Launch & Endless Assortment Strategy (2011–Present)

In May 2011, while Grainger's traditional business hummed along generating billions in revenue, a team of 20 people gathered in Mundelein, Illinois, with a seemingly suicidal mission: build a competitor to Grainger. A subsidiary of W.W. Grainger, Inc. (NYSE: GWW), Zoro.com launched in May 2011 with 20 team members and 180,000 items.

The name "Zoro" had no meaning—it was chosen precisely because it meant nothing, carried no baggage, set no expectations. When the wholly-owned subsidiary of powerhouse MRO supplier Grainger opened its doors in 2011, its workforce was about 20 people. Zoro.com launched its website with 180,000 items from Grainger's assortment and everyone pitched in to help pack and ship. Picture that: executives packing boxes, engineers working customer service, everyone doing everything because there was no other choice.

The strategic logic was both brilliant and terrifying. Grainger's research showed a massive market they weren't reaching: small businesses that found Grainger intimidating, expensive, or simply irrelevant. These weren't factories needing sophisticated procurement solutions—they were auto repair shops needing shop towels, small contractors needing safety glasses, mom-and-pop operations needing basic supplies. Zoro, says Weadick, is focused more on small businesses, and especially those looking for a very simple and efficient transaction.

Amazon Business was coming—everyone knew it. Rather than wait to be disrupted, Grainger decided to disrupt itself. But Zoro wasn't just Grainger-dot-com with a different logo. It was built from scratch as a cloud-native, digital-only business with radically different economics. No branches. No sales force. No catalog. Just a website, great search, and fast shipping.

The execution philosophy was pure Silicon Valley startup, bizarre for a company owned by an 84-year-old industrial distributor. As a cloud-native business, Zoro's technology infrastructure is inherently scalable. They used modern web frameworks, deployed continuously, ran A/B tests on everything. While Grainger's main website had to support legacy systems and enterprise customers with complex needs, Zoro could build fresh, optimize for conversion, and move fast.

Within the first year, Zoro.com offered more than 200,000 products. By 2016, Zoro.com reached a major milestone of 1 million unique products and now offers nearly 7 million products and counting. This growth rate was insane—from 180,000 to 7 million products in a decade. How? They became masters of dropshipping before most people knew the term. Rather than stock everything, they connected directly to hundreds of suppliers' warehouses. Customer orders trigger automatic purchase orders to suppliers who ship directly in Zoro-branded boxes.

The business model was elegantly simple: one price for everyone (no negotiation), free shipping over $50 (later $35), easy returns, and an "endless aisle" of products. Its slick website, transparent one-price-for-all and "endless aisle"-type assortment brings customers in need of a quick, hassle-free solution minus the bells and whistles.

By 2022, Zoro hit a remarkable milestone: A subsidiary of W.W. Grainger, Inc. (NYSE: GWW), Zoro.com launched in May 2011 with 20 team members and 180,000 items. Now, with more than 600 team members, Zoro.com continues to expand and rapidly grow by offering 11 million unique products. They'd reached $1 billion in annual sales—a unicorn by any measure, built inside a 95-year-old company.

But the real innovation wasn't Zoro itself—it was Grainger's two-speed strategy. They now explicitly operated two models: High-Touch Solutions (the traditional Grainger business) and Endless Assortment (Zoro and MonotaRO). It operates through two segments, High-Touch Solutions North America and Endless Assortment.

High-Touch serves large customers who need expertise, credit terms, custom pricing, and someone to call when things go wrong. Endless Assortment serves everyone else—customers who just want to buy stuff quickly and cheaply online. The models have different economics, different capabilities, different cultures. But they share Grainger's supply chain, purchasing power, and institutional knowledge.

The numbers validate the strategy. In Q4 2023, Zoro's Q4 sales rose 2.3% year over year to $264 million. MonotaRO's Q4 sales increased 7.8% to $438 million. Combined Endless Assortment Q4 sales increased 6.0% to over $700 million. The Endless Assortment segment is growing faster than the traditional business and at higher margins.

But perhaps the most important outcome is strategic optionality. If Amazon Business crushes traditional distribution, Grainger has Zoro. If customers demand high-touch service, Grainger's branch network is ready. If everything moves online, they're prepared. If physical presence remains valuable, they're covered. They've built a portfolio of models, each optimized for different customer segments and future scenarios.

The question now isn't whether Grainger can compete in the digital age—they've proven they can. The question is whether they can maintain this portfolio approach as artificial intelligence transforms not just how products are sold, but how industrial knowledge itself is packaged and delivered.

VIII. Digital Transformation & AI Revolution (2020–Present)

March 2020. The world shuts down. Supply chains shatter. And suddenly, W.W. Grainger—a 93-year-old motor distributor—finds itself on the front lines of a global pandemic. Grainger was designated as an essential business during the early days of the coronavirus pandemic.

The pandemic created a perfect storm of challenges that would have destroyed a less adaptable company. Demand for personal protective equipment exploded 10,000%. Manufacturing customers shut down while healthcare customers couldn't buy fast enough. International supply chains froze while domestic demand spiked. Branches had to operate with social distancing while e-commerce orders overwhelmed distribution centers.

Then came the controversy. In March 2020, Grainger was sent a letter from the Wisconsin Department of Agriculture, Trade and Consumer Protection accusing them of price gouging. Grainger had increased its prices for surgical masks from $0.17 to $1.00 per mask. The optics were terrible—a billion-dollar corporation seemingly profiteering from a crisis. The reality was more complex: Grainger's own costs had skyrocketed as suppliers raised prices and air freight replaced ocean shipping. But nuance doesn't travel well on social media.

Yet the pandemic also validated Grainger's digital transformation. In 2019, more than 70 percent of Grainger orders in the U.S. originated via a digital channel (including Grainger.com, inventory management systems, and eProcurement). When physical interactions became impossible, Grainger was ready. Customers could order online, use punchout catalogs, or leverage automated inventory systems without human contact.

But Grainger's leadership saw beyond pandemic response to a more fundamental transformation: artificial intelligence was about to revolutionize how businesses discover and purchase industrial products. The challenge was daunting. Grainger offered millions of products with complex technical specifications. A customer might search for a "thing that stops water" when they need a ball valve, or "the spinning thing" when they need a bearing. Traditional search would fail; AI might succeed.

Databricks provided Grainger with a data intelligence platform that transformed the approach to managing their vast product catalog. With Databricks Vector Search, Grainger had secure access to comprehensive data engineering and management features specifically designed to support RAG applications within a data intelligence platform. "We chose to work with Databricks Mosaic AI because it gave us flexibility in how we do vectorization and embedding."

The technical architecture was sophisticated: Retrieval Augmented Generation (RAG) that could understand context, interpret vague queries, and return accurate results. But the real innovation was making this invisible to users. A maintenance worker searching for parts doesn't care about vector embeddings or large language models—they just want to find the right valve quickly.

By integrating contextually relevant data into the model outputs, Grainger's RAG application leverages LLMs to ensure that customer inquiries are met with precise, contextually appropriate responses. The GenAI capabilities of the Databricks Platform also enabled Grainger to enhance product discovery even further through conversational interfaces. Even while supporting multiple search modalities and thousands of real-time queries, Grainger's GenAI models provided accurate and near-instantaneous results.

The impact was immediate and profound. The impact of this integration has been profound, with significant advancements in search recall and discoverability across the company's 2.5 million products. The solution further empowered sales teams and call center agents with faster and more accurate product retrieval capabilities, which saves time, reduces errors and lets employees assist customers more efficiently.

Think about what this means: A sales rep talking to a customer who can't quite describe what they need can now find it instantly. A maintenance worker at 3 AM can use natural language to find obscure parts. The institutional knowledge that once lived only in the heads of experienced employees is now embedded in AI systems accessible to everyone.

But Grainger's AI transformation goes beyond search. They're using machine learning for demand prediction, optimizing inventory across their network. They're deploying computer vision to identify parts from photos. They're building recommendation engines that understand not just what customers bought, but what they'll need next.

The numbers tell the story of successful transformation. For the full year, sales of $17.2 billion increased 4.2%, or 4.7% on a daily, organic constant currency basis compared to the prior year. In an era when traditional distributors are struggling, Grainger continues growing. More impressively, they're doing it profitably, with margins expanding even as they invest heavily in technology.

Raghunathan emphasized the capabilities of the Databricks Data Intelligence Platform, noting, "Grainger's website is high traffic since we are a go-to for many companies. Even with our strong sales force of 4,000 professionals, e-commerce is a main pillar for our business, and that means we have to continuously improve. Updating our tech stack is a must and aligns us with modern methodologies — that's where Databricks helped us the most."

The AI revolution at Grainger isn't just about technology—it's about preserving and scaling institutional knowledge. Every customer interaction, every product query, every transaction feeds back into the system, making it smarter. The company that started with William Grainger personally knowing what motors his customers needed has evolved into an AI-powered platform that knows what millions of customers need before they ask.

IX. Modern Business Model & Financial Performance

Let's talk about the money—because ultimately, all these strategic pivots and digital transformations mean nothing if they don't translate to financial performance. And here's where Grainger's story gets genuinely remarkable: Grainger is a profitable corporation and has increased dividends to its shareholders for forty five consecutive years.

Forty-five consecutive years of dividend increases. That puts Grainger in the elite "Dividend Aristocrat" club—companies that have raised dividends for at least 25 straight years. Through recessions, oil crises, dot-com busts, financial crises, and pandemics, Grainger has never cut its dividend. That's not just financial strength; that's institutional permanence.

The 2024 numbers are staggering: sales of $17.2 billion increased 4.2%, or 4.7% on a daily, organic constant currency basis compared to the prior year. But the headline number obscures the elegance of the underlying model. Grainger now operates as two distinct businesses under one corporate umbrella, each with different economics and strategies.

High-Touch Solutions North America is the traditional Grainger business—331 branches, 4,000 sales professionals, deep customer relationships. This segment serves large customers who value expertise over price. They're buying solutions, not products. When a factory's production line goes down, they don't want the cheapest bearing; they want the right bearing delivered immediately by someone who understands their operation.

The unit economics are compelling: average order size around $260, gross margins north of 38%, customer retention rates above 90%. These aren't transactions; they're relationships. Many customers have been buying from Grainger for decades, their procurement systems integrated with Grainger's, their maintenance schedules synchronized with Grainger's inventory.

Endless Assortment (Zoro and MonotaRO) operates on completely different physics. No branches, minimal human interaction, millions of SKUs, transparent pricing. The endless assortment business model targets customers with less complex needs with a broad range of products sold online. Average orders are smaller, but the cost to serve is dramatically lower. No sales commissions, no branch overhead, just technology and logistics.

The growth rates tell the story: While High-Touch grows at GDP-plus rates (3-5% annually), Endless Assortment grows at 10-15%. More importantly, Endless Assortment operates at higher incremental margins—each additional dollar of revenue drops more to the bottom line because the infrastructure is already built.

The geographic footprint has become increasingly sophisticated. Beyond the 331 North American branches, Grainger operates massive distribution centers that are marvels of automation. The newest facility in Houston, announced for 2026, will span 1.2 million square feet—roughly 21 football fields of industrial supplies, robots, and conveyor systems.

But physical infrastructure is just the visible part. The invisible infrastructure—the data, algorithms, and relationships—might be more valuable. Grainger knows what every customer bought, when they bought it, and when they'll likely need more. They can predict demand spikes, optimize inventory placement, and route orders efficiently. This isn't just distribution; it's predictive logistics.

The competitive moat keeps widening. Amazon Business, despite its resources, struggles with the complexity of B2B. Industrial customers need approved vendor lists, purchase orders, net payment terms, safety certifications, and technical support. They need someone to call when the wrong part arrives. They need consistency across thousands of locations. Amazon excels at B2C convenience; Grainger excels at B2B complexity.

Meanwhile, traditional competitors like Fastenal and MSC Industrial face a different challenge. They're stuck in the middle—lacking Grainger's scale and digital capabilities but also lacking the focus and agility of specialists. Fastenal has tried vending machines; MSC has tried acquisitions. Neither has matched Grainger's two-speed model.

The financial resilience is remarkable. Full Year 2023 Highlights: Grew sales to $16.5 billion, up 8.2%, or 9.5% on a daily, organic constant currency basis. Realized reported operating margin of 15.6%, up 110 basis points. In an inflationary environment where many distributors saw margins compress, Grainger expanded margins while growing revenue. That's pricing power—the ultimate sign of competitive advantage.

Looking forward, the company has been explicit about its ambitions: outperform market growth by 400-500 basis points annually in High-Touch, while scaling Endless Assortment to become a multi-billion dollar segment. They're not choosing between models; they're optimizing both for their respective markets.

X. Playbook: Business & Investing Lessons

After nearly a century of operation, Grainger has inadvertently written one of business history's most valuable playbooks. Not for building the next unicorn or disrupting industries, but for something harder: building a company that becomes infrastructure, that grows steadily for decades, that survives technological upheaval while maintaining its core identity.

Lesson 1: The Power of Boring, Essential Businesses

Grainger sells mundane products to unglamorous customers for routine applications. No consumer brand cache, no viral marketing campaigns, no charismatic founder on magazine covers (William Grainger gave barely any interviews in his lifetime). Yet this boring business has created more lasting wealth than most "exciting" companies ever will.

The insight: Boring businesses have sustainable moats precisely because they're boring. Venture capitalists don't fund competitors. MBAs don't dream of running them. The media doesn't cover them. This lack of attention creates space for patient compound growth. While everyone else chases the next big thing, boring businesses quietly become systemically important.

Lesson 2: Distribution as Defensible Infrastructure

Software companies talk about network effects; Grainger built physical network effects. Every branch makes nearby branches more valuable through inventory sharing. Every customer relationship makes supplier relationships stronger through volume. Every product added makes the catalog more comprehensive. These aren't winner-take-all dynamics, but they're winner-take-most.

The modern parallel is Amazon's fulfillment network, but Grainger did it first and arguably better for B2B. The difference: Amazon optimized for consumer convenience, Grainger optimized for business reliability. Different games, different rules, different moats.

Lesson 3: The Catalog-to-Digital Transformation Playbook

Most traditional companies failed the digital transition because they saw it as replacement rather than enhancement. Sears killed its catalog to focus on stores, then killed its stores to focus on digital, and ended up killing itself. Grainger kept everything—catalog, branches, sales force, website—and made them work together.

The key insight: Customer don't care about your channels; they care about their problems. Some problems are solved best online, others in-person, most through a combination. Companies that force customers to choose channels lose to companies that let customers use all channels seamlessly.

Lesson 4: Two-Speed Innovation

The Zoro launch demonstrated something profound: Large companies can innovate like startups if they're willing to truly separate the new from the old. Not innovation labs or corporate venture arms—actual separate businesses with different brands, cultures, and economics.

But separation isn't abandonment. Zoro leverages Grainger's supplier relationships and logistics infrastructure while maintaining startup agility. MonotaRO uses Grainger's knowledge while operating independently in Japan. This portfolio approach—multiple models for multiple futures—provides both growth and resilience.

Lesson 5: Building Moats Through Service and Availability

Grainger's real product isn't motors or safety equipment—it's availability. The confidence that whatever you need, whenever you need it, Grainger has it or can get it. This requires massive working capital, sophisticated logistics, and deep supplier relationships. It's expensive, capital-intensive, and takes decades to build. Which is exactly why it's defensible.

The modern tech equivalent is AWS. Amazon doesn't just rent servers; they provide the confidence that computing power will always be available when needed. Same model, different product, same moat dynamics.

Lesson 6: Private Label as Strategic Control

Those Dayton motors and Speedaire compressors weren't just higher-margin products—they were strategic assets. Customers who preferred Grainger's private label brands couldn't switch suppliers without switching products. Suppliers who manufactured these products couldn't sell directly without violating agreements.

This seems obvious now—every retailer has private label—but Grainger pioneered it in B2B distribution when conventional wisdom said business buyers only wanted name brands. They proved that business buyers, like consumers, care more about value and reliability than logos.

Lesson 7: International Expansion Through Joint Ventures

Rather than imposing the American model globally, Grainger partnered with local companies who understood local markets. MonotaRO succeeded because Sumitomo knew Japan. The Mexican operation worked because they adapted to local business practices. This humility—acknowledging that different markets require different approaches—enabled successful international expansion where others failed.

Lesson 8: Managing Through Economic Cycles

Grainger has survived every recession since 1927. The pattern is consistent: maintain inventory when others cut, hire talent when others fire, expand footprint when others contract. This countercyclical approach requires financial strength and institutional confidence—the belief that downturns are temporary but competitive advantages are permanent.

The 2008 financial crisis exemplified this. While competitors pulled back, Grainger invested in e-commerce capabilities and emerged stronger. COVID-19 was the same story—massive investment in digital capabilities while others retrenched.

The meta-lesson across all of these: Competitive advantage comes not from any single decision but from the accumulation of thousands of correct small decisions over decades. Grainger's moat isn't one thing—it's everything, integrated and reinforced over 97 years.

XI. Analysis & Bear vs. Bull Case

Bull Case: The Industrial Economy's Infinite Game

The optimistic case for Grainger starts with a simple observation: The physical economy isn't disappearing. Every Tesla Gigafactory, every Amazon fulfillment center, every data center powering the cloud—they all need maintenance, repair, and operating supplies. The more we digitize, paradoxically, the more physical infrastructure we need to support that digitization.

Grainger's position as North America's MRO leader becomes more valuable, not less, as complexity increases. Modern facilities require more sophisticated supplies, more technical expertise, more reliable delivery. A factory running just-in-time production can't wait three days for a critical part. A hospital can't risk equipment failure. A data center can't tolerate downtime. These customers need what Grainger provides: certainty.

The digital transformation story is compelling. In 2016, Grainger was named the 11th largest eCommerce retailer in North America. This isn't a legacy company bolting on digital capabilities—it's a digital leader that happens to have physical infrastructure. The AI investments through Databricks position them at the forefront of B2B e-commerce innovation. They're not just digitizing the catalog; they're using AI to fundamentally improve how businesses discover and procure supplies.

The Endless Assortment strategy provides optionality. If the market moves toward self-service and price transparency, Zoro and MonotaRO are ready. If it values expertise and relationships, High-Touch Solutions dominates. This isn't hedging—it's playing multiple games simultaneously and winning all of them.

Financially, the bull case is straightforward: GDP-plus growth, expanding margins, and consistent capital returns. Forty-five consecutive years of dividend increases suggests this isn't changing. The company generates enormous free cash flow, has minimal capital requirements for growth, and returns excess capital to shareholders religiously.

The competitive position keeps strengthening. Amazon Business, despite unlimited resources, hasn't dented Grainger's growth. Traditional competitors lack the scale and technology to compete effectively. New entrants face the chicken-and-egg problem: you need inventory to attract customers, but you need customers to justify inventory. Grainger has both, at scale.

Bear Case: The Slow-Motion Disruption Risk

The pessimistic view starts with Amazon Business, which launched in 2015 and now generates over $35 billion in annual revenue. That's twice Grainger's total revenue, achieved in less than a decade. If Amazon decides to seriously focus on B2B—building business-specific features, offering credit terms, providing technical support—Grainger's moat might not be wide enough.

The margin structure is concerning. Grainger operates at 15%+ operating margins in a business where Amazon accepts 1-3% margins. If Amazon or other tech giants decide to trade profits for market share, Grainger faces an impossible choice: match prices and destroy profitability, or maintain margins and lose customers. The stock market values Grainger on earnings; Amazon doesn't care about earnings.

Technology disruption could accelerate beyond Grainger's adaptation speed. What if AI enables customers to bypass distributors entirely, connecting directly with manufacturers? What if 3D printing makes inventory obsolete for certain parts? What if autonomous procurement systems optimize purchasing across multiple suppliers, eliminating distributor loyalty? Grainger's advantages—inventory, expertise, relationships—might become less relevant.

The customer concentration risk is real. Large enterprise customers generate disproportionate profits. If a few major accounts switch to Amazon Business or direct procurement, the impact would be severe. These customers have procurement departments sophisticated enough to manage multiple suppliers and capture savings.

Economic sensitivity remains high. Despite diversification, Grainger is fundamentally tied to industrial production. A manufacturing recession, sustained inflation, or supply chain disruption hits directly. The company performed well through COVID, but the next crisis might be different. Climate change, geopolitical instability, or technological disruption could impact industrial demand in unpredictable ways.

Valuation multiples are demanding. Grainger trades at premium multiples relative to distribution peers, pricing in continued execution and growth. Any disappointment—a quarter of weak sales, margin compression, or loss of a major customer—could trigger multiple compression beyond the fundamental impact.

The international growth story is mixed. While MonotaRO succeeds in Japan, expansion elsewhere has been fitful. The company divested operations in China and Europe. The global opportunity might be more limited than bulls believe, constraining long-term growth potential.

The Balanced View

The truth, as always, lies between extremes. Grainger faces real disruption risks but has proven remarkably adaptable. They're expensive but not overvalued if execution continues. Amazon is a threat but not an existential one—the B2B market is enormous and complex enough for multiple winners.

The key question isn't whether Grainger survives—they will. It's whether they can maintain premium returns in an increasingly competitive environment. The answer likely depends on execution: continuing to innovate digitally, maintaining service superiority, and adapting to changing customer needs.

For investors, Grainger represents a fascinating study in resilience and adaptation. It's neither a pure value play nor a growth story, but something rarer: a competitively advantaged business in slow transformation, generating substantial cash flows while investing for the future.

XII. Epilogue & "What Would We Do?"

If we were running Grainger today, the strategic priorities would be clear but the execution would be complex.

First, we'd accelerate the AI transformation beyond search into prediction. Grainger has millions of customers buying billions of products—that's a data asset no competitor can replicate. Build AI that doesn't just help customers find products but predicts what they'll need before equipment fails. Offer "reliability-as-a-service"—using IoT sensors and predictive analytics to prevent downtime rather than just supplying parts after breakdown.

Second, we'd expand internationally through the Endless Assortment model, not High-Touch. MonotaRO proved that digital-first works in markets without established branch networks. India, Southeast Asia, and Latin America are massive, fragmented, underserved markets perfect for the Zoro model. Build or acquire local digital leaders, apply Grainger's supply chain expertise, and scale rapidly.

Third, we'd pursue strategic acquisitions in specialized verticals. Healthcare, renewable energy, and electric vehicle infrastructure all need specialized MRO supplies and expertise. Rather than building expertise internally, acquire the leading distributors in these verticals and integrate them into the Grainger ecosystem.

Fourth, we'd create a true platform business. Grainger has relationships with thousands of suppliers and millions of customers but mostly acts as a middleman. Build a marketplace where suppliers can sell directly to customers with Grainger providing fulfillment, financing, and trust. Take a percentage of transactions rather than marking up inventory. This transforms Grainger from a distributor to an infrastructure provider.

Fifth, we'd separate and potentially spin off the Endless Assortment business. Zoro and MonotaRO operate so differently from High-Touch that managing them together creates inefficiency. As independent companies, they could move faster, access different capital pools, and pursue strategies that might conflict with the core business. Grainger shareholders would own both but each could optimize independently.

The future of B2B distribution isn't about choosing between digital and physical, or between service and price. It's about building infrastructure so essential that it becomes embedded in how business operates. Grainger has done this once with physical distribution. The opportunity now is to do it again with digital intelligence.

The company that William Grainger founded to solve a simple problem—small contractors couldn't buy motors—has evolved into something he couldn't have imagined: an AI-powered platform supporting millions of businesses with billions of products. But the core mission remains unchanged: helping the people who keep the world working do their jobs better.

That's not a glamorous mission. It won't generate headlines or inspire Hollywood movies. But for nearly a century, it's created tremendous value for customers, employees, and shareholders. In a business world obsessed with disruption and transformation, there's something profound about a company that simply executes, adapts, and endures.

The next century will bring challenges William Grainger couldn't imagine: artificial general intelligence, climate adaptation, technologies we haven't invented yet. But if history is any guide, Grainger will adapt to these changes the same way they always have: slowly, carefully, and successfully. They'll be boring, essential, and profitable.

For investors, entrepreneurs, and business students, Grainger offers a different model of success. Not the hockey-stick growth of venture-backed startups or the glamour of consumer brands, but the compound power of being indispensable. Of solving real problems for real customers with real products, year after year, decade after decade.

That's the Grainger story: boring, essential, and ultimately, one of American business history's great successes. A company that keeps the world working, one motor, one safety glove, one industrial widget at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube