Goldman Sachs: The Vampire Squid's Evolution

I. Introduction & Episode Roadmap

Picture this: December 2008. Lloyd Blankfein sits in his corner office at 200 West Street, staring at the Manhattan skyline as snow begins to fall. Three months earlier, Goldman Sachs—the firm that had survived the Great Depression, two world wars, and countless market crashes—had admitted it was "toast" without government intervention. The mighty vampire squid, as Rolling Stone would soon call it, had nearly suffocated in the financial crisis it helped create. Yet here was Blankfein, not just surviving but calculating how to emerge stronger, richer, more powerful than ever.

How does a company go from being one coal chute away from obscurity in 1869 to becoming the most influential financial institution on Earth? How does it place alumni in seemingly every corner of government—from Treasury Secretaries to central bank governors—while maintaining its mystique as Wall Street's most selective club? And perhaps most intriguingly: how does it repeatedly dance on the edge of destruction, only to emerge with even greater market share? Today, Goldman Sachs is the second-largest investment bank in the world by revenue and is ranked 55th on the Fortune 500 list, with headquarters still anchored in Lower Manhattan and regional offices stretching from London to Hong Kong. But this is not a story of steady, linear progress. It's a tale of immigrant ambition, family feuds, catastrophic gambles, near-death experiences, and the ultimate prize: becoming so essential to global capitalism that failure itself becomes impossible.

Over the next several hours, we'll trace this evolution from Marcus Goldman's humble commercial paper operation to David Solomon's modern colossus generating $53.5 billion in revenue in 2024. We'll examine how Goldman built its legendary partnership culture, why it abandoned that structure after 130 years, how it survived—and profited from—the 2008 financial crisis while competitors collapsed, and what its dominance tells us about American capitalism itself.

The themes that emerge are as complex as they are controversial: the tension between serving clients and trading against them, the revolving door between 200 West Street and Washington D.C., the price of being "too big to fail," and the eternal question—is Goldman Sachs the smartest firm on Wall Street or simply the most ruthless?

What makes this story particularly fascinating is not just Goldman's survival but its ability to transform crisis into opportunity. Every existential threat—from the 1929 crash to Penn Central to 2008—somehow left the firm stronger. As we'll see, this isn't luck. It's a playbook refined over 155 years, one that values information over everything, treats risk as religion, and understands that in finance, proximity to power is power itself.

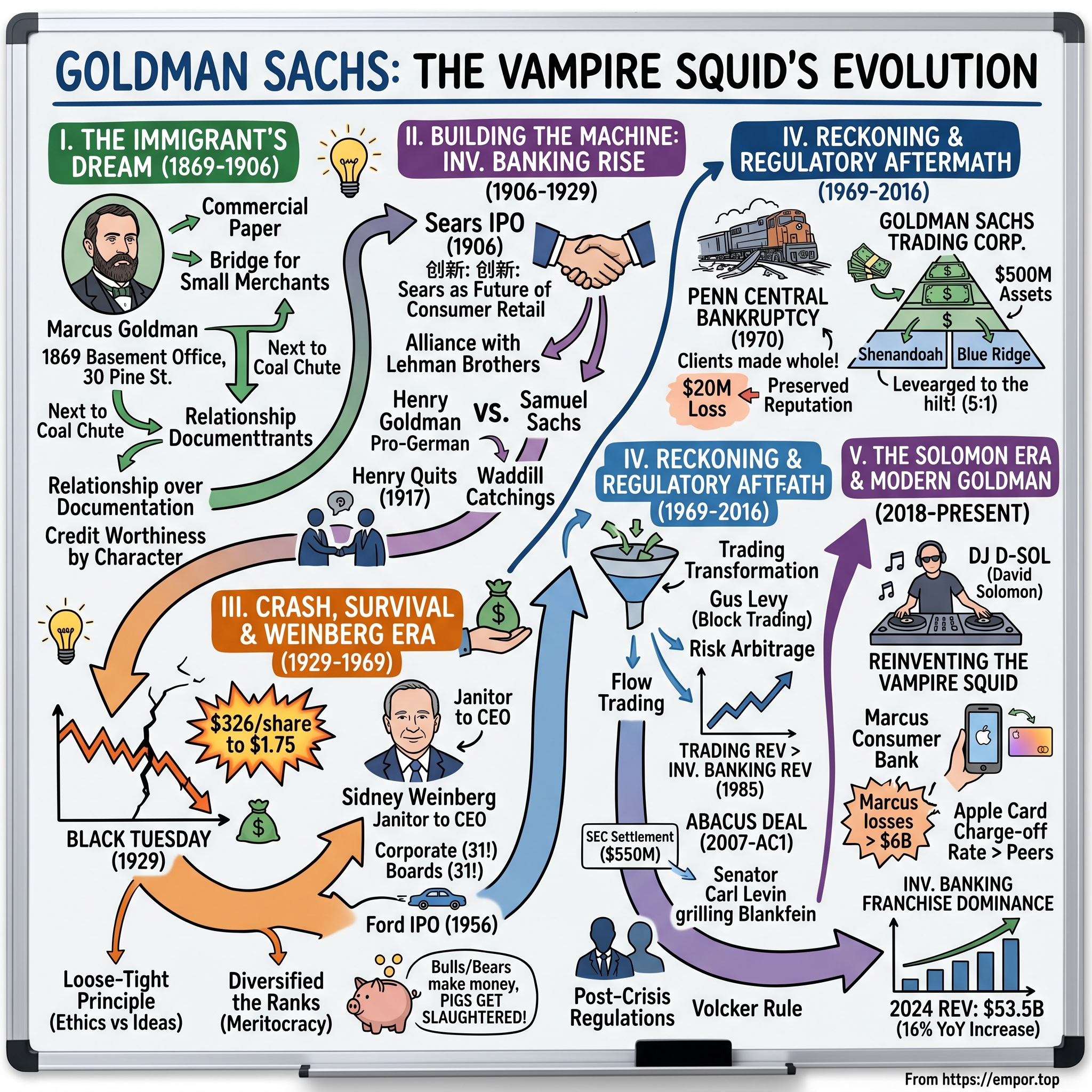

II. The Immigrant's Dream: Marcus Goldman & Early Years (1869–1906)

The year is 1848. Revolution sweeps across Europe like wildfire—monarchies topple, barricades rise in Paris, Vienna erupts in violence. In the small Bavarian town of Trappstadt, a 27-year-old Jewish cattle drover named Marcus Goldman watches his world collapse. The failed revolutions bring not freedom but intensified antisemitism. Jewish communities face pogroms, economic restrictions tighten, and the dream of equality dies in the streets. Goldman makes a decision that will reshape American finance: he boards a ship to America.

Marcus Goldman wasn't supposed to become a titan of Wall Street. Born in 1821 to Mark Goldmann (the family would later anglicize the name) and his wife Ella, Marcus grew up in rural Bavaria where Jews faced strict limitations on employment, movement, and even marriage. His father traded cattle—one of the few professions permitted to Jews—and Marcus learned early that success meant reading people as carefully as balance sheets. When he arrived in Philadelphia in 1848, he carried little more than determination and an understanding that in America, unlike Bavaria, a Jew could build something lasting.

Philadelphia in the 1850s teemed with opportunity and chaos. Marcus started as an itinerant peddler, carrying goods on his back through Pennsylvania Dutch country. The work was brutal—walking twenty miles a day, sleeping in barns, facing suspicious farmers who'd never seen a Jew before. But Marcus possessed an unusual gift: he could evaluate character instantly, sensing who would pay their debts and who would disappear into the night. This skill—reading creditworthiness through handshakes and conversations rather than financial statements—would become the foundation of an empire.

In 1850, Marcus married Bertha Goldman (coincidentally sharing his surname), whose family had established themselves in Philadelphia's growing Jewish community. Bertha brought not just a dowry but connections—her relatives ran successful businesses, attended synagogue with other German-Jewish immigrants, and understood that in America, community meant capital. Together they had five children, including daughters Rosa, Louisa, and Rebecca, whose marriages would prove as strategically important as any IPO.

By 1869, Marcus had saved enough to make his next move. New York was becoming the nation's financial capital, and Marcus sensed opportunity in the chaos following the Civil War. He rented a one-room basement office at 30 Pine Street, next to a coal chute, and hung a simple shingle: "Marcus Goldman, Banker and Broker."

The innovation that built Goldman Sachs wasn't complex—it was brilliant in its simplicity. Marcus discovered a gap in the market: small merchants and entrepreneurs needed short-term capital but couldn't access bank loans. Meanwhile, commercial banks sat on idle cash seeking safe, short-term investments. Marcus became the bridge. He would visit hat makers, leather goods dealers, and textile merchants in lower Manhattan, buying their promissory notes at a steep discount—sometimes 8-9% for 30-90 day paper. Then he'd walk uptown to the commercial banks and sell the notes at a smaller discount, pocketing the spread.

What made Marcus different wasn't just the business model—it was his method. While established bankers demanded extensive documentation and collateral, Marcus relied on relationships. He'd sit in a merchant's shop, observe their customers, examine their inventory, gauge their character through conversation. A firm handshake might be worth more than a financial statement. His Bavarian cattle-trading heritage served him well—he could smell desperation or dishonesty instantly.

The numbers tell the story of his success. By 1882, Marcus was turning over $30 million in commercial paper annually—roughly $950 million in today's dollars. His reputation grew: if Marcus Goldman bought your paper, banks would too. He became a one-man credit rating agency, his judgment trusted from Wall Street to Washington Street.

But Marcus understood that family businesses needed family. In 1882, his daughter Louisa had married Samuel Sachs, a young man from a prominent Bavarian-Jewish family who'd established themselves in Boston's financial circles. Samuel was everything Marcus wasn't—refined, educated, cautious where Marcus was bold. When Marcus invited his son-in-law to join the firm as a partner, it wasn't nepotism—it was strategy. The firm became Goldman, Sachs & Co., though locals still called it "Goldman's."

The 1880s brought more family into the fold. Marcus's son Henry Goldman joined in 1885, bringing an aggressive ambition that sometimes worried his father. Henry had grown up watching Marcus build the business note by note, but he dreamed bigger—why just trade commercial paper when you could underwrite entire companies? Ludwig Dreyfuss, husband of Marcus's daughter Rebecca, also joined, creating a family firm that controlled both ownership and management.

By 1896, Goldman Sachs had grown large enough to seek a seat on the New York Stock Exchange. The membership cost $150,000—a fortune at the time—but it represented arrival. Goldman Sachs was no longer a scrappy commercial paper dealer but a legitimate Wall Street firm. The boy from Bavaria who'd fled pogroms now controlled one of New York's rising financial houses.

The real breakthrough came in 1906, though Marcus was already stepping back from daily operations. Henry Goldman had befriended Julius Rosenwald, a fellow German-Jew who'd built Sears, Roebuck & Company into America's largest retailer through mail-order catalogs. Sears needed capital to expand, but traditional investment banks like J.P. Morgan wouldn't touch it—retail was considered too risky, too common, beneath the dignity of white-shoe firms that financed railroads and steel.

Henry saw opportunity where others saw risk. He convinced his father and uncle that Sears represented the future—a new kind of company selling directly to America's growing middle class. The initial public offering in 1906 raised $30 million, with Goldman Sachs as lead underwriter. The stock soared. Suddenly, Goldman Sachs wasn't just successful—it was innovative, willing to back entrepreneurs that established firms ignored.

Marcus Goldman lived to see this triumph but not much longer. He died in 1909, leaving an estate worth $5 million (roughly $160 million today) and a firm bearing his name that had grown far beyond his immigrant dreams. His obituary in the New York Times called him "one of the builders of Wall Street," but that understates his achievement. Marcus didn't just build a firm—he created a model. Trust over documentation. Relationships over rigid rules. And most importantly: find value where others see only risk.

The commercial paper innovation seems quaint now, but it revolutionized American small business finance. Before Marcus, entrepreneurs faced impossible choices—predatory lenders or no credit at all. Marcus created a market, turning individual promises to pay into tradeable securities. Every time a small business today factors receivables or issues commercial paper, they're using Marcus Goldman's innovation.

But perhaps his greatest legacy was cultural. The firm he founded would always carry the DNA of the immigrant outsider—hungrier than established competitors, willing to challenge conventions, understanding that in America, merit could triumph over birthright. That basement office next to the coal chute wasn't just where Goldman Sachs began—it was where modern investment banking discovered that fortune favors the bold. The question that would haunt his successors: how bold is too bold?

III. Building the Machine: Investment Banking Rise (1906–1929)

The morning of July 28, 1914, Henry Goldman sat in his corner office at 43 Exchange Place, reading cables from London. Austria-Hungary had just declared war on Serbia. Within days, the dominoes would fall—Russia, Germany, France, Britain—until all of Europe was aflame. But Henry wasn't thinking about geopolitics. He was thinking about his friend, Philip Lehman of Lehman Brothers, and the alliance they'd built to challenge J.P. Morgan's stranglehold on American finance. That partnership was about to shatter over something as distant as the Kaiser's ambitions and as intimate as family loyalty.

After Marcus Goldman's death in 1909, control of Goldman Sachs passed to an unlikely duo: Samuel Sachs, the cautious son-in-law who preferred steady commercial paper profits, and Henry Goldman, Marcus's son who dreamed of turning Goldman Sachs into a powerhouse rivaling Morgan and Kuhn, Loeb. Their contrasting styles created a dynamic tension—Samuel's conservatism checking Henry's ambition, Henry's vision pushing Samuel's boundaries. Together, they'd grown the firm from $5 million in capital to over $20 million by 1914.

The key to their expansion was an unlikely alliance. In 1906, Henry had approached Philip Lehman with a proposal: Goldman Sachs had the retail and consumer goods expertise; Lehman Brothers understood commodities and Southern markets. Why not combine forces to compete with the Morgan monopoly? The partnership worked brilliantly. Together they underwrote Studebaker, F.W. Woolworth, Continental Can, and dozens of other companies that traditional Wall Street ignored. By 1912, the Goldman-Sachs-Lehman alliance was underwriting over $75 million in securities annually.

Henry's genius lay in seeing value where others saw vulgarity. While J.P. Morgan financed railroads and U.S. Steel—the commanding heights of industrial capitalism—Henry backed department stores, retailers, and consumer goods companies. His logic was simple: America was becoming a consumer society. The average American would never buy steel ingots, but they'd shop at Sears, Woolworth's, and May Department Stores. "The mines and mills and railroads will always need bankers," Henry told his partners, "but the future belongs to whoever serves the American consumer."

The firm's culture reflected this democratic capitalism. In 1912, Henry made a radical decision: he promoted Henry S. Bowers to partner, the first non-family member to achieve that status. Bowers wasn't Jewish, didn't marry into the family, had no connection to the German-Jewish aristocracy that dominated Wall Street's Jewish firms. He was simply brilliant at evaluating retail companies. The message was clear—at Goldman Sachs, talent trumped bloodlines.

But as Europe descended into war, the partnership began to fracture. Henry Goldman was passionately pro-German. He'd studied in Germany, spoke fluent German, believed German culture represented the apex of civilization. When the war began, he refused to buy Liberty Bonds, telling anyone who'd listen that Germany was fighting for survival against British imperialism. At one partners' meeting in 1915, he declared, "The Kaiser is no different from King George—they're both fighting for empire."

Samuel Sachs was horrified. He had two sons who would soon be eligible for the draft. The firm's clients were American companies selling to American consumers. Supporting Germany—even rhetorically—was business suicide. The arguments grew vicious. Samuel accused Henry of putting philosophy over profits. Henry shot back that Samuel was a coward, bowing to mob sentiment.

The breaking point came at a partners' dinner in early 1917. America was weeks from entering the war. Henry raised his glass and toasted "the fatherland." Samuel walked out. Philip Lehman followed. The room sat in stunned silence as Henry finished his champagne alone. Within weeks, Henry Goldman resigned from the firm his father had founded, selling his stake back to the remaining partners for $5 million. He never set foot in 43 Exchange Place again.

Samuel Sachs now controlled Goldman Sachs, but he'd lost his greatest dealmaker. The Lehman alliance was dead—Philip couldn't forgive Henry's German sympathies or Samuel's inability to control his partner. The firm that had challenged Morgan suddenly found itself isolated, its deal flow evaporating. Samuel needed new blood, new vision, someone who could restore Goldman's reputation and momentum.

He found it in Waddill Catchings, a Mississippi native with a Harvard Law degree and connections throughout corporate America. Catchings joined in 1918, bringing a radically different vision. Why just underwrite securities for companies? Why not create securities, package them, trade them, turn Goldman Sachs from a service provider into a principal investor? Samuel, exhausted from the Henry Goldman civil war, gave Catchings unprecedented freedom.

The 1920s roared, and Goldman Sachs roared louder. Under Catchings' leadership, the firm underwrote $1.5 billion in securities between 1925 and 1929. But Catchings' masterpiece—or catastrophe, depending on your perspective—was the Goldman Sachs Trading Corporation, launched in December 1928.

The Trading Corporation was financial engineering at its most creative and dangerous. Goldman Sachs created a publicly traded investment trust, essentially a closed-end fund that would invest in other companies. The initial offering raised $100 million, with Goldman Sachs retaining a 40% stake. The stock price doubled within weeks. Catchings then performed financial alchemy: the Trading Corporation created another trust, the Shenandoah Corporation, which created another trust, the Blue Ridge Corporation. Each trust issued stock and bonds, using the proceeds to buy stakes in the others, creating a pyramid of leverage that would make modern derivatives traders blanch.

By summer 1929, the Trading Corporation controlled over $500 million in assets with only $100 million in actual capital—a 5:1 leverage ratio that seemed conservative by the standards of the day but would prove catastrophic. The original $100 million investment was valued at $500 million on paper. Goldman Sachs partners were worth fortunes they'd never dreamed possible. Catchings was hailed as a genius who'd discovered how to manufacture wealth from thin air.

The numbers from 1929 capture the insanity. Trading Corporation stock hit $326 per share in early 1929. Blue Ridge reached $117. Shenandoah touched $141. Goldman Sachs itself, still a private partnership, was valued by partners at over $100 million—twenty times its book value just a decade earlier. The firm opened new offices in Chicago, Boston, Philadelphia, even Berlin. It hired hundreds of salesmen, analysts, traders. The basement office next to the coal chute was now a marble-clad temple to capitalism.

But hidden in the prosperity were warning signs. Eddie Cantor, the comedian who'd invested his life savings in Trading Corporation on Goldman's recommendation, joked to audiences: "They told me to buy Goldman Sachs stock for my old age. It worked—I feel like I'm ninety years old!" The laughter was nervous. Everyone sensed the music would stop; nobody wanted to be caught without a chair.

The partnership structure during this period deserves examination. Unlike corporations with shareholders and boards, Goldman Sachs operated as a pure partnership. Partners had unlimited liability—if the firm failed, creditors could seize their personal assets, their homes, everything. This should have encouraged conservatism. Instead, it created a gambling mentality: if you're betting everything anyway, why not bet big?

The international expansion during the 1920s established patterns that persist today. Goldman opened its London office in 1925, not to serve British companies but to access European capital for American deals. The relationship with Kleinwort Sons, established in 1887, deepened into a full alliance. Goldman partners shuttled between New York and London on luxury liners, living like the aristocrats they'd once envied.

Cultural changes accompanied the growth. The firm that Marcus Goldman had run like a family store now employed over 600 people. Harvard MBAs replaced City College graduates. The partners' dining room served four-course lunches with wine. The firm bought a box at the Metropolitan Opera, a table at the Union Club, all the accouterments of establishment respectability.

Yet underneath the polish, Goldman retained its outsider edge. While Morgan partners summered in Newport, Goldman partners worked through August. While Kuhn, Loeb maintained banker's hours, Goldman traders arrived before dawn. The firm pioneered statistical analysis of securities, hiring mathematicians to build models predicting stock movements. They called it "scientific investing"—others called it gambling with equations.

As 1929 drew to a close, Waddill Catchings gave a speech to Goldman employees. "We have built something magnificent," he declared. "The Trading Corporation represents the democratization of investment, allowing ordinary Americans to participate in the prosperity of our greatest companies." He was right about one thing—ordinary Americans would indeed participate in what came next. But it wouldn't be prosperity they'd be sharing.

The partnership that had survived family feuds and world war was about to face its greatest test. The machine Henry Goldman and Waddill Catchings built had grown beyond anyone's comprehension or control. The question wasn't whether it would crash, but whether anything would survive the wreckage. Samuel Sachs, now in his seventies, would watch his life's work evaporate in weeks. But from that destruction would rise an unlikely savior—a Brooklyn-born janitor's son who'd started at Goldman as an assistant, carrying messages between partners who barely knew his name.

IV. Crash, Survival & The Weinberg Era (1929–1969)

October 29, 1929. Black Tuesday. Sidney Weinberg stood at the trading desk at 43 Exchange Place, watching numbers that defied comprehension. Goldman Sachs Trading Corporation, which had touched $326 per share months earlier, traded at $32. By day's end, it would be worth $20. The pyramid of trusts Waddill Catchings had constructed—Shenandoah, Blue Ridge—collapsed like a house of cards in a hurricane. Partners who'd been worth millions on paper that morning were effectively bankrupt by lunch. One trader turned to Weinberg and said, "We've destroyed everything Marcus Goldman built in a single morning."

But Weinberg, all five-foot-four of him, just smiled grimly. "Then we'll build it again," he said. "Better."

The scale of the catastrophe defied belief. The Trading Corporation, which had controlled $500 million in assets, saw its value shrink to under $20 million within weeks. By 1932, shares that had peaked at $326 traded for $1.75. The original $100 million that Goldman Sachs had raised from public investors had evaporated almost entirely. Eddie Cantor's joke turned bitter: "The only thing that's holding Goldman Sachs up is the paint on the walls."

Lawsuits flooded in. Investors who'd bought Trading Corporation shares on Goldman's recommendation demanded restitution. The firm faced over $50 million in legal claims—ten times its remaining capital. Waddill Catchings, the architect of the disaster, resigned in disgrace, retreating to Mississippi where he would spend his remaining years writing economic treatises nobody would read. Samuel Sachs, broken by the catastrophe, died in 1935, having watched his brother-in-law's firm nearly disappear.

Enter Sidney Weinberg—the most unlikely savior in Wall Street history. Born in 1891 in Brooklyn's Red Hook section to Polish-Jewish immigrants, Sidney was the third of eleven children. His father was a liquor wholesaler who barely spoke English. His mother took in sewing to make ends meet. Sidney dropped out of P.S. 13 at age thirteen, not because he wasn't bright but because the family needed every dollar.

His first job at Goldman Sachs, in 1907, was as assistant to the janitor, earning $3 a week. His duties: delivering messages, cleaning spittoons, polishing the brass railings. But Sidney possessed something rare—an ability to remember everything he heard and everyone he met. Partners would discuss deals while he swept; Sidney absorbed every detail. When a partner couldn't remember a client's name, Sidney would whisper it as he passed. Soon, partners started asking the janitor's assistant for his opinion on deals.

By 1925, Sidney had worked his way from janitor's assistant to the trading desk to partnership—a fifteen-year ascent that would be impossible at any other Wall Street firm. He hadn't attended Harvard or Yale; his education came from night school at Brooklyn's Browne's Business College. But Sidney understood something his Ivy League colleagues didn't: business was about relationships, not pedigrees.

When the crash came, Sidney was one of the few partners with little personal wealth at risk—he'd been too junior to participate fully in the Trading Corporation bonanza. This poverty became his power. While other partners were paralyzed by personal catastrophe, Sidney could think clearly. He engineered a brilliant strategy: instead of declaring bankruptcy, Goldman would slowly, methodically repay every creditor, restore every relationship, rebuild trust dollar by dollar.

The numbers from the 1930s tell a story of grinding persistence. In 1930, Goldman Sachs revenues fell to $2.1 million—less than the firm earned in 1910. The partnership capital, which had exceeded $100 million in 1929, shrank to under $5 million. Of the twenty partners in 1929, only six remained by 1935. The firm survived on commercial paper trading—Marcus Goldman's original business—and the occasional small underwriting.

But Sidney saw opportunity in catastrophe. While competitors retreated, he expanded Goldman's relationships. He joined corporate boards—starting with McKesson & Robbins, then General Foods, Continental Can, eventually serving on thirty-one boards simultaneously. Each board seat brought business back to Goldman. CEOs who wouldn't return Goldman's calls would chat with Sidney at board meetings. Slowly, the deal flow returned.

Sidney's style was unique on Wall Street. He called everyone from CEO to janitor by their first name. His office door was always open. He'd show up at a client's factory floor, talking to workers about production problems. When Ford Motor Company considered going public in the 1950s, Henry Ford II asked Sidney to handle it not because Goldman was the biggest firm—it wasn't—but because Sidney was the only banker who understood manufacturing.

The Ford IPO in 1956 represented Goldman's resurrection. The offering was the largest in history—$657 million, valuing Ford at $3.2 billion. Goldman Sachs, written off as dead after 1929, was lead underwriter. The fee—$9 million—exceeded the firm's total capital. Sidney had engineered the impossible: Goldman Sachs was not just alive but thriving, handling the most prestigious deal of the decade.

Sidney's management philosophy transformed Goldman's culture. He instituted what he called "the loose-tight principle"—loose on ideas, tight on ethics. Partners had freedom to pursue deals, take risks, innovate. But any hint of impropriety meant immediate expulsion. "Our assets are our people, capital and reputation," he'd tell new hires. "If any of these are ever diminished, the last is the most difficult to restore." These words would become Goldman's motto, carved into conference rooms and, supposedly, consciences.

The Weinberg era also saw Goldman pioneer new business lines. Gus Levy, who joined in 1933 and became Sidney's protégé, revolutionized block trading in the 1950s. The concept was simple but radical: when institutions wanted to sell large blocks of stock, instead of dribbling shares into the market and depressing prices, Goldman would buy the entire block at a negotiated discount, then resell gradually for profit.

The first major block trade, in 1953, involved 100,000 shares of Studebaker. Levy bought the block at $18.25, resold at an average of $18.75, netting $50,000 profit in two days. By 1960, Goldman was executing over $1 billion in block trades annually, dominating a business that barely existed a decade earlier. Levy's traders, known as "Levy's boys," became Wall Street legends—aggressive, innovative, willing to commit massive capital on instinct.

The numbers from the Weinberg era document an extraordinary transformation. Partnership capital grew from $5 million in 1935 to $50 million in 1969. Revenues increased from $2 million to over $200 million. The firm that had six partners in 1935 had forty-three by 1969. Goldman Sachs, nearly destroyed by speculation, had become Wall Street's most conservative firm—and paradoxically, its most innovative.

Sidney's relationship with government deserves special attention. During World War II, he served as vice-chairman of the War Production Board, essentially running American industrial mobilization while refusing any salary. This dollar-a-year man coordinated the production of everything from bombers to boots, earning the nickname "the body snatcher" for his ability to recruit executives for government service. The connections he built—with generals, admirals, future presidents—would benefit Goldman for decades.

The cultural transformation under Sidney was profound. The firm that had been dominated by German-Jewish aristocracy became a meritocracy. Sidney hired Catholics, Irish-Americans, Italian-Americans—anyone with talent and hunger. He promoted women to senior positions decades before other Wall Street firms. When asked about diversity, Sidney's answer was simple: "I was a janitor's assistant. Who am I to discriminate?"

Yet Sidney wasn't soft. Partners who underperformed were ruthlessly culled. The "up or out" system—produce or leave—became Goldman gospel. Every December, partners would gather for what they called "the bloodbath"—compensation decisions that could make careers or destroy them. Sidney would sit at the head of the table, cigar smoke curling around his head, dispensing verdicts with biblical finality.

The international expansion accelerated under Sidney. The London office, shuttered during the war, reopened in 1953. Tokyo followed in 1969. But unlike the 1920s expansion, which chased quick profits, Sidney's international strategy focused on relationships. Goldman partners would spend years in foreign capitals, learning languages, understanding cultures, building trust. The firm that had been insular became genuinely global.

Sidney's personal quirks became Goldman lore. He collected ceramic pigs—hundreds of them, filling his office shelves. When asked why, he'd grin: "To remind me that bulls make money, bears make money, but pigs get slaughtered." He'd take the subway to work, standing in packed cars reading the Wall Street Journal, fellow commuters never knowing the rumpled little man beside them ran one of Wall Street's most powerful firms.

By 1969, when Sidney stepped down as senior partner at age seventy-seven, Goldman Sachs had been completely transformed. The firm that nearly disappeared in 1929 was now among Wall Street's elite. Revenue per partner exceeded $5 million. The client list read like a Fortune 500 index. The Trading Corporation disaster was ancient history, replaced by a reputation for conservative excellence.

But Sidney's greatest achievement wasn't financial—it was cultural. He'd taken a family firm dominated by nepotism and transformed it into a meritocracy. He'd replaced speculation with service, arrogance with hustle. Most importantly, he'd proven that on Wall Street, resurrection was possible. You could lose everything and rebuild, stronger than before.

Sidney died in 1969, still coming to the office until weeks before his death. His funeral at Temple Emanu-El brought together presidents and janitors, CEOs and secretaries. Henry Ford II gave the eulogy, calling Sidney "the most remarkable man I ever met—and I've met them all." The New York Times obituary ran on the front page, calling him "Mr. Wall Street"—the Brooklyn dropout who'd saved American capitalism's most Jewish firm and made it indispensable to American capitalism itself.

His successor, Gus Levy, inherited a firm that was profitable, prestigious, and about to face its next existential crisis. The lessons of 1929 had been learned, but the 1970s would bring new challenges—a commercial paper crisis that would echo Marcus Goldman's original business, testing whether Sidney's cultural transformation could survive without Sidney himself.

V. Penn Central Crisis & Trading Transformation (1969–1990s)

June 21, 1970. Sunday afternoon. Gus Levy sat in his Park Avenue apartment, telephone pressed to his ear, sweat beading on his forehead despite the air conditioning. On the other end, Federal Reserve Chairman Arthur Burns delivered news that would determine Goldman Sachs's survival: Penn Central Transportation Company, the nation's largest railroad, would file for bankruptcy within hours. Goldman Sachs had sold nearly $100 million of Penn Central's commercial paper to clients. Paper that was now worthless.

"Gus," Burns said quietly, "this could destroy your firm."

Levy's response would define Goldman's next era: "Then we'll make our clients whole, Art. Every penny."

The Penn Central disaster was particularly cruel because it struck at Goldman's oldest, most trusted business—commercial paper, the very foundation Marcus Goldman had laid a century earlier. Throughout 1969, Goldman had aggressively marketed Penn Central's short-term debt to institutional clients, assuring them it was safe as government bonds. The railroad was too big to fail, Goldman's salesmen promised. American commerce depended on it.

But Penn Central was a financial Frankenstein, created from the 1968 merger of the Pennsylvania and New York Central railroads—two dying giants whose union created not strength but accelerated decay. Management had hidden losses through creative accounting, paying dividends with borrowed money while basic infrastructure crumbled. Trains derailed daily. Freight rotted in yards. The company burned through $1 million in cash every day just to keep running.

Goldman should have known. Warning signs were everywhere—delayed financial statements, management turnover, desperate requests for larger credit facilities. But the firm had grown complacent, assuming its hundred-year reputation for evaluating creditworthiness meant something. The commercial paper department, generating steady fees with minimal capital commitment, had become a cash cow nobody questioned.

When Penn Central filed the largest corporate bankruptcy in American history—$7 billion in assets—Goldman faced $100 million in lawsuits from clients who'd bought the worthless paper. The firm's capital was only $50 million. Simple math suggested Goldman Sachs would follow Penn Central into bankruptcy.

But Gus Levy understood something his predecessors hadn't: reputation was worth more than any single profit or loss. He made a decision that stunned Wall Street—Goldman would use its own capital to buy back the worthless Penn Central paper from clients, absorbing losses that could destroy the firm to preserve relationships that might save it.

The buyback cost Goldman $20 million—40% of its capital—and took three years to complete. Partners who'd expected million-dollar bonuses received IOUs. The firm borrowed against everything—its Exchange seat, its building, even partners' personal assets. John Whitehead, who'd become co-senior partner with Levy, later recalled: "We were technically insolvent for eighteen months. If clients had demanded immediate payment, we couldn't have met it."

Yet the strategy worked. Clients who might have sued were stunned by Goldman's willingness to absorb losses it wasn't legally obligated to take. Institutional investors who'd written off their Penn Central losses found Goldman checks in the mail. The firm that should have been destroyed by Penn Central became the only Wall Street house to emerge with its reputation enhanced.

The crisis forced a fundamental restructuring. Goldman created its first real risk management department, with power to override business heads. The commercial paper business was completely reorganized, with multiple levels of credit approval required for any issuer over $10 million. Most importantly, the firm adopted what became known as the "14 principles"—Sidney Weinberg's philosophy codified into corporate commandments, beginning with "Our clients' interests always come first."

With disaster averted, Levy and Whitehead could focus on transformation. They recognized that Goldman's partnership structure, while fostering loyalty, limited growth. Competitors like Morgan Stanley and Merrill Lynch were expanding rapidly, fueled by external capital Goldman couldn't match. The solution: grow through innovation rather than capital, pioneering businesses that required brains over balance sheets.

The international expansion accelerated dramatically. London, reopened in 1970, grew from five employees to fifty within three years. Tokyo, opened in 1974, immediately became profitable by focusing on Japanese institutions seeking U.S. investments. Zurich followed in 1974, capturing Swiss banking relationships. But unlike American competitors who tried to transport Wall Street wholesale overseas, Goldman adapted to local cultures. London partners wore Savile Row suits and joined gentlemen's clubs. Tokyo partners learned Japanese, attended tea ceremonies, built relationships over decades not quarters.

The true transformation came in trading. Levy's block trading operation, successful in the 1960s, exploded in the 1970s. The concept evolved from simple stock blocks to complex risk arbitrage, merger arbitrage, and eventually proprietary trading. Goldman would commit its own capital, betting on market movements, merger completions, interest rate changes. The firm that had nearly died from speculation was becoming a speculation machine—but with a difference.

The key innovation was what Goldman called "flow trading"—using client orders to inform proprietary bets. When Fidelity wanted to sell a million shares of IBM, Goldman would buy the block, but traders would also position the firm's own capital to profit from the likely market impact. When merger talks leaked, Goldman's arbitrage desk would accumulate positions before announcements. The ethical lines were blurry, but the profits were clear: trading revenues grew from $10 million in 1970 to over $500 million by 1985.

New divisions sprouted like mushrooms after rain. Fixed Income, created in 1972, grew from trading government bonds to creating complex derivatives. The mortgage desk, launched in 1978, pioneered the securitization of home loans—bundling mortgages into tradeable securities that would later play a starring role in the 2008 crisis. The commodities division, J. Aron & Company, acquired in 1981, brought Goldman into oil, gold, and currency trading. Each division operated like a separate firm, with its own culture, compensation, and risk limits.

The numbers tell the story of explosive growth. Partnership capital increased from $50 million in 1970 to $500 million by 1985. Revenues grew from $200 million to $2 billion. The firm that had forty-three partners in 1969 had seventy-five by 1985. But most tellingly, trading revenues surpassed investment banking revenues for the first time in 1985—Goldman Sachs was no longer primarily an advisory firm but a trading house.

The cultural implications were profound. Investment bankers, who'd dominated Goldman since Sidney Weinberg, suddenly found traders earning multiples of their compensation. A successful M&A partner might earn $2 million; a star trader could make $10 million. The old Goldman—relationship-focused, client-centric, conservative—was being eaten alive by a new breed: mathematicians, physicists, computer scientists who viewed markets as puzzles to solve rather than relationships to nurture.

Robert Rubin, who joined in 1966 and ran risk arbitrage, embodied this new Goldman. Yale and Harvard Law educated but with a gambler's instinct, Rubin built a trading empire within Goldman. His arbitrage desk would take massive positions—$500 million, $1 billion—betting on merger completions. When deals succeeded, profits were enormous. When they failed, losses could cripple the firm. Rubin's solution: hedge everything, diversify positions, never bet the firm on a single trade.

The technology revolution transformed Goldman's capabilities. The firm spent $100 million on computer systems in the 1980s—more than its total capital in 1970. Traders could execute thousands of transactions daily, positions updated in real-time, risk calculated continuously. The firm that had used paper ledgers now had more computing power than most universities.

Goldman Sachs Asset Management, created in 1988, represented another evolution. Why just advise clients on investments when you could manage their money directly? Starting with $1 billion under management, GSAM grew to $10 billion within five years. The fees were steady, predictable, everything trading revenues weren't. It also created conflicts—was Goldman recommending investments because they were best for clients or because Goldman earned management fees?

The compensation culture evolved dramatically. The old partnership model—where partners shared profits according to seniority—gave way to "eat what you kill" systems where producers kept percentages of their revenues. A twenty-eight-year-old trader could out-earn senior partners if his desk was profitable enough. This created a mercenary culture—producers jumped between firms for better packages, loyalty evaporated, the partnership ethos Sidney Weinberg had cultivated seemed quaint.

Yet the partnership structure itself survived, creating a unique dynamic. While competitors went public, Goldman remained private, its capital base limited to what partners could contribute. This forced discipline—the firm couldn't take massive risks because partners' personal wealth was at stake. But it also created pressure. Partners who wanted to cash out had to sell their stakes back to the firm at book value, not market value. As Goldman's franchises became more valuable, the gap between book and market value widened, creating internal tensions.

The personalities of this era were as colorful as their profits. John Weinberg, Sidney's son, maintained his father's client focus while trading exploded around him. Stephen Friedman, cerebral and cautious, tried to balance trading aggression with banking tradition. Jon Corzine, who started in fixed income, built a trading empire that would eventually consume the firm's culture—and nearly the firm itself.

By the 1990s, Goldman faced a paradox. It was simultaneously the most successful and most stressed firm on Wall Street. Revenues exceeded $5 billion, profits topped $1 billion, the partnership was worth over $5 billion at book value—probably $20 billion at market. But competitors with public currency were acquiring assets, expanding globally, taking risks Goldman couldn't match. The firm that had survived Penn Central through partnership solidarity was being strangled by partnership limitations.

The debate over going public, simmering since the 1980s, reached boiling point. Younger partners wanted liquidity, older partners feared losing culture. Traders argued public capital was essential for competing; bankers worried about quarterly earnings pressure. The firm that had transformed itself from advisory to trading faced another transformation—from partnership to corporation.

The decision would split the partnership, nearly destroy the firm in 1994, and ultimately create the modern Goldman Sachs—publicly traded, massively capitalized, and powerful beyond Marcus Goldman's wildest dreams. But first, it would have to survive one more near-death experience, this time self-inflicted. The lessons of Penn Central—never bet the firm, always protect the franchise—would be forgotten in the pursuit of profits that seemed too good to refuse.

VI. Going Public & Peak Power (1999–2006)

December 3, 1998. Jon Corzine stood before 221 Goldman Sachs partners in the Windows on the World restaurant atop the World Trade Center. Outside, Manhattan glittered in winter twilight. Inside, history was being made. After 129 years as a private partnership—the last major investment bank to maintain that structure—Goldman Sachs would go public. The vote had been close, bitter, personal. Partners who'd worked together for decades no longer spoke. But the die was cast. The firm Marcus Goldman founded in a basement would soon trade on the exchange he'd joined in 1896.

"This isn't the end of Goldman Sachs," Corzine declared, his voice catching slightly. "It's the beginning of something greater."

Within six months, he'd be forced out in a coup that would shock Wall Street. The man who'd engineered Goldman's IPO wouldn't be there to ring the opening bell.

The road to that moment had been paved with near-catastrophe. In 1994, Goldman had attempted its first IPO, pulling back at the last moment when the bond market crashed, erasing $1.5 billion in trading profits. Partners who'd already made plans for their newfound wealth—houses in the Hamptons, yachts, art collections—watched it evaporate. The firm that prided itself on reading markets had misread the biggest decision in its history.

But 1998 was different. The Asian financial crisis and Russian default had created chaos, but also opportunity. Long-Term Capital Management, the hedge fund that had nearly destroyed the global financial system, had been rescued with Goldman's participation—and Goldman had profited from the chaos, earning $2.6 billion that year. The partnership was worth an estimated $20 billion. The only question was how to unlock that value.

Corzine, who'd become senior partner in 1994, championed the IPO with evangelical fervor. A trader at heart, he understood that Goldman needed capital to compete. Morgan Stanley had gone public in 1986, Lehman in 1994, Bear Stearns in 1985. They were using public money to build trading operations that dwarfed Goldman's. The firm that had pioneered block trading was being out-traded by competitors with deeper pockets.

The opposition was led by John Whitehead and John Weinberg—the "two Johns" who'd run Goldman through the 1980s. They argued that public ownership would destroy Goldman's culture. Quarterly earnings pressure would force short-term thinking. The partnership ethos—where everyone's money was at risk—would vanish. Goldman would become just another public company, its soul sold for stock options. The internal battle was vicious. Partners meetings devolved into shouting matches. Lifetime friendships ended. One partner reportedly threw a coffee mug at another. The final vote, in June 1998, was 221 in favor, 21 against—overwhelming on paper but representing deep divisions that would never fully heal.

The coup against Corzine came swiftly and ruthlessly. In January 1999, just months before the IPO, Hank Paulson orchestrated a palace revolt. Paulson, who'd run investment banking with military precision, believed Corzine was too undisciplined, too willing to bet the firm on his trading instincts. The Executive Committee voted to strip Corzine of his sole leadership, forcing him to share power with Paulson. Corzine, seeing the writing on the wall, negotiated his exit—a $400 million payout that would fund his political career as New Jersey senator and governor.

On May 4, 1999, Goldman Sachs offered 69 million shares at $53, raising $3.657 billion. The stock opened at $76 and closed at $70.375, a 33% first-day gain. The market valued Goldman at $33 billion—more than Merrill Lynch, nearly as much as Morgan Stanley. Partners who'd been worth millions on paper were suddenly worth tens of millions in tradeable stock. The janitor's assistant's firm had become one of the world's most valuable financial institutions.

Hank Paulson became Chairman and CEO immediately after the IPO, succeeding Corzine. A Christian Scientist who didn't drink, didn't smoke, and ran five miles every morning, Paulson represented a radical departure from Goldman's trading cowboys. He'd built the investment banking division into a powerhouse, competing head-to-head with Morgan Stanley for the most prestigious deals. Now he had the entire firm.

Paulson's Goldman was a study in contradictions. Publicly, he preached the old values—clients first, long-term thinking, reputation above profits. Privately, he unleashed the trading desks, allowing them to take positions that would have horrified Sidney Weinberg. The firm that had nearly died from leverage in 1929 was leveraging itself 25:1, 30:1, sometimes 35:1. But now it wasn't partnership capital at risk—it was shareholder money, other people's money, nobody's money.

The trading transformation was dramatic. Lloyd Blankfein, who'd joined Goldman in 1982 after Harvard Law, had built the commodities division from a backwater into a profit machine. Starting at J. Aron, the precious metals dealer Goldman acquired in 1981, Blankfein turned commodity trading into financial engineering. Oil wasn't just oil—it was futures, options, swaps, structured products that could be sliced, diced, and sold to anyone who'd buy them.

The firm's expansion continued with landmark deals like underwriting Microsoft's IPO and advising General Electric on its RCA acquisition. By 2000, Goldman was everywhere—advising on the AOL-Time Warner merger, the largest in history; underwriting IPOs for every dot-com with a business plan; trading billions in currencies, commodities, and derivatives daily.

The mortgage machine deserves special attention. Goldman's mortgage desk, led by Dan Sparks and later Josh Birnbaum, transformed home loans into trading instruments. They didn't just securitize mortgages—they created synthetic CDOs, CDO-squareds, instruments so complex their own creators couldn't fully explain them. By 2006, Goldman was originating, packaging, and trading over $100 billion in mortgage securities annually.

The numbers from this era are staggering. Revenues grew from $5.4 billion in 1999 to $37.7 billion in 2006. Net income increased from $2.7 billion to $9.4 billion. The stock price rose from $53 to over $200. Return on equity exceeded 30%. Goldman partners who'd kept their stock from the IPO were worth hundreds of millions. Lloyd Blankfein, who'd become president and COO in 2004, was earning over $50 million annually.

The government connections during this period created the "Government Sachs" mythology. Robert Rubin had become Treasury Secretary under Clinton. Jon Corzine was elected senator. Joshua Bolten became White House Chief of Staff. Stephen Friedman chaired the National Economic Council. But the ultimate revolving door moment came in 2006: Hank Paulson left Goldman to become Treasury Secretary, selling his $700 million in Goldman stock tax-free thanks to government ethics rules.

The culture had transformed completely. The old Goldman—partners eating lunch together, working late but going home to families—was replaced by a 24/7 trading floor where analysts slept under desks and vice presidents divorced at twice the national average. The firm that had hired from City College now recruited exclusively from Harvard, Princeton, Wharton. Starting salaries for twenty-two-year-old analysts exceeded $100,000; bonuses could double that.

Technology became Goldman's secret weapon. The firm spent over $2 billion annually on technology by 2006, building trading systems that could execute millions of trades in microseconds. The legendary "secret sauce" was actually thousands of programmers building algorithms that could spot arbitrage opportunities faster than competitors. When Sergey Aleynikov, a Goldman programmer, left for a competitor in 2009 and allegedly stole code, the FBI arrested him within days—the code was that valuable.

Risk management, supposedly Goldman's strength, became increasingly fictional. Value at Risk models showed maximum daily losses of $100-200 million, but positions were so complex, so interrelated, that nobody really knew the exposure. The firm that had survived 1929 by understanding its risks was now too complex for anyone to fully comprehend.

Goldman was later accused of deliberately underpricing IPOs to generate profits for favored clients, who would return these profits through increased business—a practice that defrauded both issuing companies and retail investors.

By 2006, at the peak of its power, Goldman Sachs seemed invincible. It dominated investment banking, led in trading, was building a massive asset management business. Alumni ran the Treasury, the New York Stock Exchange, the New York Fed. The firm Marcus Goldman started with $500 was worth $100 billion. Goldman executives owned apartments in 15 Central Park West, houses in the Hamptons, jets that shuttled between offices in London, Hong Kong, and New York.

But within the mortgage trading desk, something was shifting. Michael Swenson, a trader who'd joined from Morgan Stanley, was looking at the numbers and not liking what he saw. Default rates were rising. Housing prices were stalling. The mortgages Goldman was packaging and selling were increasingly toxic. In December 2006, David Viniar, Goldman's CFO, called a meeting that would save the firm and destroy its reputation: it was time to get short the housing market.

What happened next would make Goldman Sachs either the smartest firm on Wall Street or the most cynical, depending on your perspective. The firm that had spent years building the mortgage machine was about to bet billions on its destruction. And when the edifice collapsed, Goldman would be standing in the rubble, not only surviving but profiting from the catastrophe that destroyed its competitors and nearly destroyed capitalism itself.

VII. The Financial Crisis: Survival & Controversy (2007–2009)

December 14, 2006. Conference Room 30B at 85 Broad Street. David Viniar, Goldman's CFO, stared at the spreadsheet showing the firm's mortgage positions. The firm had just lost $100 million in a single day on subprime positions. For a firm that routinely made or lost that much before lunch, it shouldn't have mattered. But something in the pattern disturbed him. He turned to the dozen traders and risk managers assembled around the table and said ten words that would save Goldman Sachs: "Let's be aggressive distributing things because there'll be very good opportunities."

Translation: Get the hell out. Now.

What followed was one of the most profitable trades in Wall Street history—and one of the most controversial. While Goldman was privately "getting short" the housing market, it was simultaneously selling mortgage securities to clients, sometimes the very instruments it was betting against. The firm that preached "clients' interests always come first" was about to test that principle like never before.

The architect of Goldman's survival was not Lloyd Blankfein, who'd become CEO in June 2006, but a collection of traders who saw what others missed. Michael Swenson, Josh Birnbaum, and Dan Sparks of the mortgage desk had been tracking deterioration in subprime mortgages since 2004. They noticed borrowers defaulting not after years but after months. They saw mortgage brokers openly discussing fraud. They watched as lending standards disappeared entirely—NINJA loans (No Income, No Job, No Assets) were being packaged into AAA-rated securities.

By February 2007, Goldman had not just reduced its mortgage exposure but had gone massively short through a variety of instruments. The firm bought credit default swaps on mortgage securities—essentially insurance that paid off when mortgages failed. It shorted the ABX index, a benchmark for subprime mortgages. Most controversially, it created synthetic CDOs like ABACUS 2007-AC1, which were designed to fail, sold them to clients, then bet against them.

The ABACUS deal would become infamous. Goldman allowed hedge fund manager John Paulson (no relation to Hank), who was betting against housing, to help select the mortgages in the CDO, ensuring they were likely to default. Goldman then sold the CDO to institutional clients, including German bank IKB and Dutch bank ABN AMRO, without disclosing Paulson's role. When the mortgages predictably failed, Paulson made $1 billion. The clients lost everything.

By summer 2007, as Bear Stearns hedge funds collapsed and credit markets froze, Goldman was perfectly positioned. The firm reported record earnings of $3.2 billion in the third quarter of 2007, while competitors were writing down billions in mortgage losses. Blankfein's compensation for 2007: $68 million, the highest ever for a Wall Street CEO. The firm that had nearly died in 1929 from bad bets was now profiting from everyone else's bad bets.

But Goldman had one massive exposure it couldn't hedge: AIG. The insurance giant had sold credit default swaps on mortgage securities to every major bank, including $20 billion to Goldman. If AIG failed, Goldman's hedges were worthless. Throughout 2007 and 2008, Goldman aggressively demanded collateral from AIG, draining the insurer's cash reserves. By September 2008, Goldman had collected $7.5 billion in collateral, but AIG owed much more.

September 15, 2008. Lehman Brothers collapsed. Merrill Lynch sold itself to Bank of America. AIG teetered on bankruptcy. That afternoon, Lloyd Blankfein attended an emergency meeting at the Federal Reserve Bank of New York. Around the table sat the CEOs of every major bank, the Treasury Secretary (former Goldman CEO Hank Paulson), and the New York Fed President Timothy Geithner. The topic: saving American capitalism.

Blankfein would later admit what he said that day: "We were toast." Despite all of Goldman's hedges, preparations, and profits, the firm couldn't survive a complete market collapse. If AIG failed, if credit markets stayed frozen, if depositors panicked, Goldman Sachs—the firm that had survived everything—would disappear within days. The solution came on September 21, 2008. Goldman Sachs and Morgan Stanley converted to bank holding companies, placing themselves under Federal Reserve regulation. The move was both humiliating—investment banks had prided themselves on being unregulated—and essential. As bank holding companies, they could access the Fed's discount window, borrow unlimited funds, and most importantly, receive TARP bailout money.

Two days later came the masterstroke. On September 23, 2008—two days after Goldman Sachs became a bank holding company—the firm announced a private offering to Berkshire Hathaway whereby Berkshire Hathaway would purchase $5 billion in special preferred shares that would pay a 10 percent annual dividend. Warren Buffett, the Oracle of Omaha, was investing in Goldman at its darkest hour. The message to markets was unmistakable: if Buffett believed in Goldman, everyone should.

The Buffett deal was expensive—Goldman had the option of buying back the shares for $5 billion plus a one-time dividend of $500 million, and Berkshire Hathaway would also acquire warrants to buy an additional $5 billion of common stock at $115 per share. But it achieved its purpose. The day after the announcement, Goldman Sachs completed a public offering of 46.7 million shares of common stock at $123 per share for proceeds of $5.75 billion in an offering that was well-received and oversubscribed.

The government bailout followed swiftly. In October 2008, Goldman received $10 billion from TARP, the Troubled Asset Relief Program. Blankfein didn't want it—Goldman insisted it didn't need the money—but Paulson forced all major banks to take TARP funds to avoid stigmatizing the weak ones. Goldman would repay the TARP money in June 2009, with interest, eager to escape government restrictions on compensation.

But the real controversy centered on AIG. When the government bailed out the insurance giant with $180 billion, it paid out credit default swaps at 100 cents on the dollar. Goldman received $12.9 billion from this backdoor bailout—money it claimed it didn't need because its positions were hedged. Critics argued this was impossible; if AIG had failed, Goldman's hedges with other counterparties would have been worthless as those counterparties would have failed too.

The phone records would become toxic. During the week of the AIG bailout, Hank Paulson spoke to Lloyd Blankfein twenty-four times. The Treasury Secretary, who'd run Goldman two years earlier, was in constant contact with his successor while deciding whether to save AIG—and by extension, Goldman itself. Paulson claimed he'd recused himself from Goldman-specific decisions, but the calls suggested otherwise.

Meanwhile, Goldman's trading desks were printing money from the chaos. The firm made over $100 million in trading revenues on ninety-eight separate days in 2009. Its traders, understanding that the Fed would pump unlimited liquidity into markets, positioned accordingly. While unemployment soared and foreclosures mounted, Goldman earned $13.4 billion in 2009, paying out $16.2 billion in compensation. The average Goldman employee earned $498,000 that year.

The public relations disaster was immediate and lasting. Matt Taibbi's Rolling Stone article calling Goldman "a great vampire squid wrapped around the face of humanity" became the defining image. Protesters occupied Zuccotti Park, blocks from Goldman's headquarters. "Government Sachs" became shorthand for crony capitalism. The firm that had survived the crisis through foresight, hedging, and perhaps a bit of insider knowledge had become the symbol of everything wrong with Wall Street.

The profits from the crisis were extraordinary. Goldman's "Big Short" netted approximately $4 billion. The firm earned billions more from trading in the volatile markets of 2008-2009. The Buffett investment, while expensive, provided crucial confidence when Goldman needed it most. By 2010, Goldman's stock had recovered to pre-crisis levels.

But the damage to Goldman's reputation was permanent. The firm that had prided itself on client service was exposed as betting against the very products it sold to clients. The ABACUS scandal led to a $550 million SEC settlement in 2010—the largest penalty ever paid by a Wall Street firm at that time. Goldman neither admitted nor denied wrongdoing, but the details that emerged in congressional testimony were devastating.

The most damaging moment came in April 2010 when Goldman executives testified before the Senate Permanent Subcommittee on Investigations. Senator Carl Levin grilled Lloyd Blankfein about selling "shitty deals" to clients—using Goldman's own internal emails as evidence. Fabrice Tourre, the Goldman vice president who'd structured ABACUS, had written about selling "these complex, highly leveraged, exotic trades" to "widows and orphans."

Blankfein's defense was technically accurate but morally bankrupt: Goldman was a market maker, not a fiduciary. The firm had no obligation to act in clients' best interests. It could sell securities while simultaneously betting against them. This was how markets worked. But to the public watching on television, it sounded like an admission that Goldman's business model was built on deception.

The internal culture during the crisis revealed Goldman at its best and worst. The firm's risk management had been superb—it had seen the crisis coming and positioned accordingly. Its traders had been brilliant, making money in the most chaotic markets in history. Its government connections had proven invaluable, ensuring survival when pure market forces might have meant destruction.

But the crisis also exposed the contradictions at Goldman's core. The firm that proclaimed "our clients' interests always come first" had profited from client losses. The company that claimed to be about long-term relationships had embraced short-term trading profits. The partnership ethos that Sidney Weinberg had cultivated had been replaced by a bonus culture where individual profit trumped collective reputation.

The numbers tell the story of survival and profit. Goldman's stock, which had fallen to $47 in November 2008, recovered to $170 by April 2010. The firm that had admitted it was "toast" without government help had not just survived but thrived. Return on equity in 2009 exceeded 20%. Compensation per employee remained the highest on Wall Street.

But something fundamental had changed. Pre-crisis, Goldman had been respected, even admired—the smartest firm on Wall Street, the place every MBA wanted to work. Post-crisis, it became a symbol of greed, exploitation, and the revolving door between Wall Street and Washington. The firm had won the financial game but lost the reputation war.

Lloyd Blankfein would later reflect on this period with characteristic ambiguity. Asked if Goldman had done anything wrong, he said, "We participated in things that were clearly wrong and have reason to regret. We were a participant in the market, but we survived the crisis better than others." It was the perfect Goldman answer—acknowledging error without admitting guilt, expressing regret without accepting responsibility.

The survival of Goldman Sachs through the financial crisis was a masterclass in risk management, political connections, and ruthless self-preservation. The firm had seen the crisis coming, positioned itself to profit, and when threatened with extinction, leveraged every relationship and rule to ensure survival. It had done exactly what it was designed to do—make money and survive.

But the cost was enormous. The firm that Marcus Goldman had built on trust, that Sidney Weinberg had rebuilt on relationships, that had once represented the best of American capitalism, had become its villain. The vampire squid had survived, even prospered, but at the price of its soul. The question that would define Goldman's next decade was whether that soul could be recovered—or whether, in modern finance, having a soul was simply a luxury Goldman could no longer afford.

VIII. Reckoning & Regulatory Aftermath (2010–2016)

April 27, 2010. Senate Hearing Room 106. Lloyd Blankfein adjusted his microphone, staring at the panel of senators who would spend the next eleven hours dissecting Goldman Sachs's role in the financial crisis. Behind him sat rows of protesters holding signs: "JAIL THE BANKSTERS." Senator Carl Levin held up a stack of internal Goldman emails, his voice dripping with disgust: "You sold your clients a deal you internally described as 'shitty.' How do you explain that?"

Blankfein's response would become infamous: "In our market-making function, we are not acting as an investment advisor. We are acting as a principal."

Levin exploded: "You're trying to sell a shitty deal—your words—and you're saying that's consistent with your values?"

The hearing was political theater, but the damage was real. Every American with a television watched Wall Street's most powerful CEO essentially admit that Goldman had no obligation to protect clients from bad investments—even ones Goldman itself was betting against. The firm that had survived the financial crisis financially intact was being destroyed reputationally in real-time.

The SEC settlement had been announced just eleven days earlier. Goldman agreed to pay $550 million to settle charges that it misled investors in the ABACUS CDO—Companies selling undervalued stock and their initial consumer stockholders were both defrauded by this practice. The firm neither admitted nor denied wrongdoing, but the facts spoke for themselves. Goldman had let John Paulson help design a CDO destined to fail, sold it to clients without disclosure, and profited when it collapsed.

The congressional testimony revealed a cultural rot that went beyond ABACUS. Internal emails showed Goldman salespeople referring to CDOs as "junk," "dogs," "big old pig," and most memorably, "shitty deals." Thomas Montag, who ran Goldman's securities business, had written in June 2007: "Boy, that timberworld deal is a shitty deal. Just don't tell [the client] that, of course."

But the most damaging revelation came from Fabrice Tourre, the Goldman vice president who'd structured ABACUS. His emails, read aloud in the Senate, painted a picture of Wall Street at its most cynical. He'd written to his girlfriend: "The whole building is about to collapse anytime now... Only potential survivor, the fabulous Fab... standing in the middle of all these complex, highly leveraged, exotic trades he created without necessarily understanding all of the implications of those monstrosities!!!"

Blankfein's defense—that market-making was different from advising, that Goldman had no fiduciary duty to clients—was legally accurate but morally catastrophic. Senator Susan Collins asked the question that cut to the heart: "Do you have a duty to act in the best interests of your clients?"

Blankfein's response was a masterpiece of evasion: "I believe we have a duty to serve our clients well."

The public heard something different: Goldman Sachs would screw you if it could profit from it.

The regulatory response was swift and severe. The Dodd-Frank Act, passed in July 2010, included the Volcker Rule, which limited banks' ability to trade for their own accounts—a direct attack on Goldman's business model. The firm that had made billions from proprietary trading would have to find new ways to generate profits.

Goldman created the Business Standards Committee in January 2010, a direct response to public outrage. The committee, chaired by board member and former Fannie Mae CEO James Johnson, was tasked with reviewing every aspect of Goldman's business practices. The resulting report, released in January 2011, contained 39 recommendations, including enhanced disclosure, client suitability standards, and structured product reviews.

But the legal settlements kept coming. In 2014, Goldman paid $3.15 billion to the Federal Housing Finance Agency to resolve claims related to mortgage securities sold to Fannie Mae and Freddie Mac. The firm didn't admit wrongdoing but acknowledged that it had provided "incomplete information" about the mortgages underlying the securities.

The biggest settlement came in 2016. Goldman agreed to pay $5.06 billion to resolve federal and state claims related to its mortgage business: $2.39 billion in civil penalties, $1.8 billion in relief to underwater homeowners and distressed borrowers, and $875 million to settle claims from other entities. It was the last major bank to settle mortgage crisis charges, having fought longer and harder than competitors.

The statement of facts accompanying the settlement was devastating. Goldman had known the mortgages it was securitizing were trash. One Goldman mortgage trader had written in 2006: "Loan performance is GRIM... we should close this dog." Another had said: "Real bad feeling across the board about how we mark our positions." Yet Goldman had continued packaging and selling these securities to clients.

The cultural transformation during this period was profound and painful. Goldman instituted mandatory training on conflicts of interest, client responsibilities, and reputational risk. Every email was monitored, every trade scrutinized. The freewheeling culture that had generated massive profits was replaced by compliance paranoia.

Compensation became a battleground. Public outrage over banker bonuses forced Goldman to restructure pay. In 2009, the firm had set aside $16.2 billion for compensation—$498,000 per employee—while unemployment hit 10%. The backlash was fierce. Goldman responded by paying senior executives in stock that couldn't be sold for five years, implementing clawback provisions, and capping cash bonuses.

The partner election process, once Goldman's most sacred ritual, became contentious. The firm that had 483 partners in 2000 had shrunk to 375 by 2010. Being "tapped" as a partner had meant lifetime security; now partners were regularly "de-partnered" if they didn't generate sufficient revenue. The partnership that Sidney Weinberg had nurtured was becoming just another corporate title.

Internal dissent grew louder. Greg Smith's March 2012 New York Times op-ed "Why I Am Leaving Goldman Sachs" became a sensation. Smith, a Goldman executive director, wrote: "The environment now is as toxic and destructive as I have ever seen it... It makes me ill how callously people talk about ripping their clients off."

Smith described a culture where making money trumped everything: "It astounds me how little senior management gets a basic truth: If clients don't trust you they will eventually stop doing business with you. It doesn't matter how smart you are."

Goldman's response was swift and dismissive, calling Smith a "disgruntled employee" whose views didn't reflect the firm's culture. But privately, the op-ed terrified management. If a mid-level employee felt this way, what did clients think?

The numbers during this period tell a story of resilience despite reputational damage. Revenues remained robust: $39.2 billion in 2010, $28.8 billion in 2011, $34.2 billion in 2012. Return on equity, while lower than pre-crisis peaks, stayed respectable: 11.5% in 2010, 5.8% in 2011, 10.7% in 2012. The firm that everyone loved to hate was still printing money.

But the business mix was changing. Trading revenues, once Goldman's engine, were declining due to Volcker Rule restrictions and reduced risk appetite. Investment banking was resurging, with Goldman regularly topping league tables for M&A and equity underwriting. Asset management was growing steadily, reaching $1.18 trillion in assets under supervision by 2014.

The international expansion accelerated as Goldman sought growth beyond toxic American politics. The firm deepened its presence in Asia, particularly China, where Goldman had been operating since 1994. European operations expanded despite the sovereign debt crisis. By 2015, nearly 40% of Goldman's revenues came from outside the Americas.

Technology became both an opportunity and threat. Goldman invested heavily in electronic trading platforms, algorithmic trading systems, and digital infrastructure. But technology also meant fewer traders were needed. The firm that had employed 30,000 people in 2007 had roughly the same headcount in 2015 despite significantly higher revenues.

The leadership during this period reflected Goldman's challenges. Lloyd Blankfein, once celebrated as the trader who'd saved Goldman, became a liability. His tone-deaf comments—like doing "God's work" by providing liquidity to markets—reinforced Goldman's image as arrogant and out-of-touch. Yet he survived, partly because he'd made partners rich, partly because no obvious successor existed.

Gary Cohn, Goldman's president and COO, represented the firm's future—or so it seemed. Dyslexic, from a middle-class Cleveland family, Cohn had started in commodities and worked his way up through sheer determination. He was everything Blankfein wasn't: tall, charismatic, comfortable with media. Many assumed he'd succeed Blankfein.

But the most significant change was invisible to outsiders: Goldman's risk appetite had fundamentally shifted. The firm that had bet billions against housing wouldn't take similar risks again. Value at Risk limits were reduced. Proprietary trading was eliminated. The wild cowboys who'd generated massive profits (and losses) were replaced by steady executives focused on client service.

By 2016, Goldman had paid over $9 billion in mortgage-related settlements. The legal bills exceeded the profits from the "Big Short." The reputational damage was incalculable. The firm that had been Wall Street's gold standard was now its symbol of greed.

Yet Goldman survived, even thrived in some ways. The settlements, while massive, were manageable given Goldman's earnings power. The regulatory restrictions, while limiting, forced Goldman to focus on sustainable businesses. The reputational damage, while severe, didn't stop clients from hiring Goldman for the biggest deals.

The paradox of post-crisis Goldman was that everyone hated the firm but still needed it. Corporations hired Goldman for IPOs because Goldman could still command the highest prices. Governments hired Goldman to manage bond offerings because Goldman had the best distribution. Even clients who'd been burned in the crisis came back because, simply put, Goldman was still the best at what it did.

As 2016 drew to a close, Goldman faced a new challenge: the election of Donald Trump as president. The populist who'd campaigned against Wall Street immediately began filling his administration with Goldman alumni. Steve Mnuchin, Goldman partner from 1994 to 2002, became Treasury Secretary. Gary Cohn left Goldman to become Director of the National Economic Council. Steve Bannon, who'd worked at Goldman in M&A, became chief strategist.

The revolving door that had been Goldman's strength was becoming its weakness. Every Goldman appointment reinforced the narrative that the firm controlled government. The vampire squid mythology, which Goldman had hoped would fade, was reinforced by Trump's Goldman-heavy administration.

Lloyd Blankfein, who'd survived the financial crisis, the congressional hearings, the settlements, and the cultural revolution, now faced his biggest challenge: finding a successor who could lead Goldman into a new era. The firm needed someone who could generate profits without generating headlines, who could serve clients without seeming to screw them, who could be powerful without appearing evil.

That person would turn out to be David Solomon, a investment banker who moonlighted as a DJ. His appointment would signal Goldman's attempt to reinvent itself once again—from trading powerhouse to technology-enabled financial services company. Whether that transformation would succeed, whether Goldman could escape its vampire squid reputation, remained to be seen.

But one thing was certain: the Goldman Sachs that emerged from the regulatory reckoning was fundamentally different from the firm that had entered the financial crisis. More regulated, less profitable, more careful, less aggressive. The question was whether this new Goldman could maintain its position as Wall Street's premier firm, or whether in trying to be less evil, it would become merely ordinary.

IX. The Solomon Era & Modern Goldman (2018–Present)

The Hamptons, July 2017. David Solomon, Goldman's co-head of investment banking, stood behind the DJ booth at a charity event, electronic dance music pulsing through the speakers. The crowd—hedge fund managers, tech entrepreneurs, society fixtures—danced to his set. Someone filmed it on their phone. Within hours, the video was viral: a Goldman Sachs executive spinning records as "DJ D-Sol."

Harvey Schwartz, Solomon's internal rival for the CEO position, watched the video from his office at 200 West Street. He turned to an aide: "I'm competing against a DJ?"

Six months later, Schwartz abruptly resigned, clearing Solomon's path to the throne. The man who'd spent his nights mixing beats would spend his days mixing Goldman's business model, attempting the most radical transformation in the firm's history.

Solomon officially became CEO on October 1, 2018, inheriting a firm that was profitable but strategically adrift. In 2024, Goldman increased net revenues by 16 percent year-over-year to $53.5 billion; grew earnings per share by 77 percent to $40.54; improved return on equity by over 500 basis points to 12.7 percent; improved efficiency ratio by 11.5 percentage points to 63.1 percent; and generated total shareholder return of 52 percent. But in 2018, the numbers were less impressive. Trading revenues were stagnant. Investment banking faced fierce competition. The stock price had barely moved in five years.