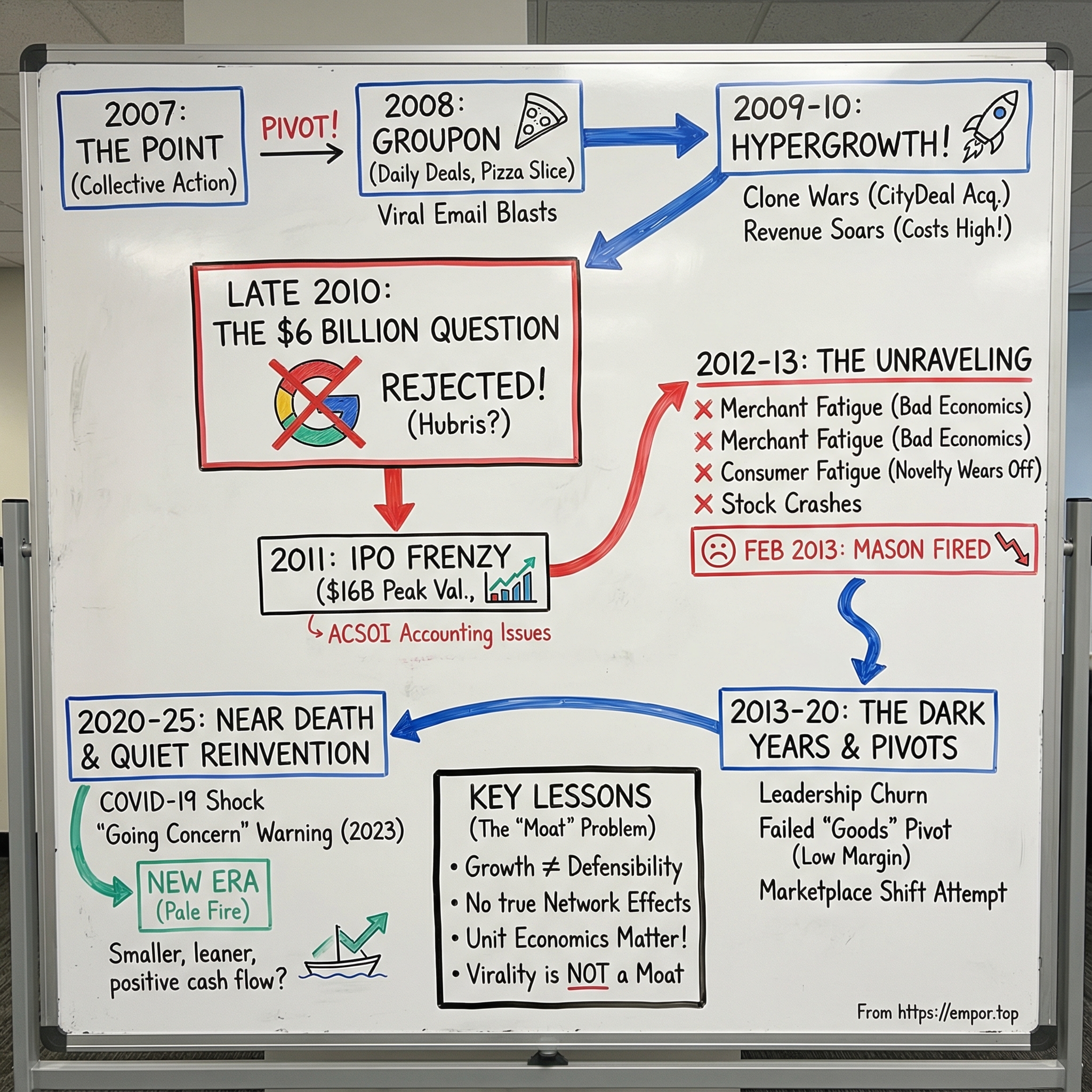

Groupon: The Rise, Fall, and Quiet Reinvention of the Daily Deal Empire

I. Introduction & Episode Roadmap

Picture this: it’s December 2010. A two-year-old startup out of Chicago—one that kicked off with a two-for-one pizza deal sold to people in an office building lobby—has a decision in front of it that most founders only daydream about.

Google wants to buy them. For $6 billion.

This is the Google that already owned search, was sitting on more than $30 billion in cash, and had never written a check anywhere near that size for an acquisition. And Groupon’s board, led by a 29-year-old former music major named Andrew Mason, looks at the offer and says no.

Not “let’s negotiate.” Not “maybe later.” Just: no thanks. We’re going to be bigger.

At the time, that confidence didn’t feel crazy. A December 2010 report said Groupon was projecting it would hit $1 billion in sales faster than any business ever. Forbes put it on the cover and called it the fastest-growing company in history. Consumers refreshed their inboxes for daily blasts: half-off massages, cheap dinners, cut-rate laser hair removal. Local merchants, battered by the Great Recession, lined up for access to Groupon’s millions of subscribers. “I’ve got a Groupon” became a real phrase people said out loud—cultural shorthand for being smart, thrifty, in-the-know.

A year after turning down Google, Groupon went public. The IPO priced at $20 a share, raised $700 million, and briefly became the biggest U.S. tech offering since Google’s in 2004. By the end of its first trading day, Groupon was valued at $16.6 billion.

And then came the part nobody wanted to put on the cover.

Over the following years, the daily-deal empire that seemed unstoppable started to look… fragile. In the decade that followed, Groupon’s financial trajectory was mostly a long, grinding decline. The company says it has about 14 million active users today, but the cultural moment vanished, competitors swarmed, merchants soured, and Wall Street lost patience.

So here’s the question that makes Groupon more than just a nostalgia story: how did a company turn down Google’s $6 billion offer, IPO at more than $16 billion, then lose over 95% of its value—and somehow still exist today?

This is a cautionary tale about growth-at-all-costs, about unit economics, and about what happens when virality gets mistaken for defensibility. But it’s also, strangely, a story of endurance. Billings hit a low of $1.56 billion. Revenue fell to $492 million in 2024. And now, both are ticking up again, with projected billings of $1.6 billion and about $500 million in revenue. Groupon has reached positive free cash flow for the first time in years, and the turnaround—quietly—is starting to stick.

The Groupon saga matters because it captures a very specific kind of startup tragedy: a company that grows faster than anyone thought possible, becomes a verb, attracts unlimited capital—and then realizes that none of it automatically becomes a moat. If you want a case study in the difference between a real platform and a dressed-up growth machine, Groupon is required reading.

II. The Origin Story: From The Point to Groupon (2008–2009)

The Groupon story starts, oddly enough, with a guy trying to break up with his cell phone company.

Andrew Mason was born on October 22, 1980, in Pittsburgh and grew up in the suburb of Mount Lebanon. His parents were entrepreneurs—his father sold diamonds, his mother ran a photography business—and that “make your own thing” instinct rubbed off early. At 15, Mason launched a weekend bagel-delivery hustle called Bagel Express.

He didn’t follow the classic startup-founder script after that, either. Mason graduated from Northwestern in 2003 with a bachelor’s degree in music. When that didn’t translate into a job, he taught himself to code and landed at InnerWorkings, a Chicago company where he met the founder: Eric Lefkofsky.

That introduction mattered. Lefkofsky was already deep into the Chicago venture world, a serial entrepreneur who’d built multiple businesses with his longtime partner Brad Keywell. And he had a talent for spotting raw potential. Mason had it.

In 2006, Mason earned a scholarship to the University of Chicago’s Harris School of Public Policy after creating Policy Tree, a tool for visualizing policy debates. But his attention kept snapping back to a different kind of problem—one that felt small and personal, but also universal: companies that could say “no” to customers because customers were alone.

Mason’s failed attempt to cancel a cell phone contract became the seed of an idea: what if people could act together, and only commit once enough others committed too?

That became The Point, launched in November 2007. It was an online platform for organizing collective action—boycotts, scholarships, charitable projects—built around a simple mechanism. People could pledge money or participation, but they wouldn’t be charged unless the campaign hit a pre-set threshold: the “tipping point.” The name was a nod to Malcolm Gladwell’s The Tipping Point, and the concept was genuinely elegant—use collective leverage to do what individuals can’t.

Lefkofsky put $1 million behind it. Mason dropped out of school after just three months to build it full-time.

But The Point struggled to find its footing. Some of its campaigns were big and weird—like Mason’s proposal to build a dome over Chicago to protect it from snow. It drew a meaningful amount of pledges, but it also highlighted the problem: attention wasn’t the same as a business model. The platform was powerful in theory, but too abstract in practice, and monetizing it was hard.

Still, inside The Point was the insight that would become Groupon.

The campaigns that worked best weren’t political or philanthropic. They were commercial. People used the tipping-point mechanic to band together and negotiate group discounts from local businesses. And that’s when Mason and Lefkofsky noticed the thing that would define the next decade of local commerce: commerce worked where activism didn’t.

So in late 2008, with the financial crisis crushing small businesses and consumers suddenly obsessed with saving money, Mason pivoted. He took The Point’s core mechanic—commit together, tip together—and aimed it at local merchants desperate for foot traffic.

On October 22, 2008, Groupon ran its first deal: a two-for-one pizza offer at Motel Bar, a Chicago restaurant in the same building. It sold out quickly and created the kind of buzz you can’t buy with ads.

The name was perfect, too: “group” plus “coupon.” Backed by Lefkofsky and Keywell, Mason launched Groupon—initially through getyourgroupon.com—and the idea snapped into place. The Point might not have generated enough traffic to survive, but Groupon was a near-instant hit. Within months, it was already profitable.

It worked because the timing was brutal and therefore ideal. Merchants needed customers right now. Consumers needed deals right now. Groupon stitched those two urgencies together with daily email, a clear discount, and a clock that made the choice feel immediate: buy today, or it’s gone.

Once it proved itself in Chicago, Groupon expanded fast—New York, Boston, Washington, D.C., all within its first six months.

The playbook was simple enough to explain in a sentence, which is always dangerous. Cut a deal with a local merchant, offer a steep discount (often half off or more), blast it to an email list, keep roughly half the revenue, then repeat in the next city. Layer in the “tipping” mechanic, add the 24-hour expiration window, and you get a powerful cocktail of social proof and scarcity—two forces that email marketing almost never gets to wield.

And then there was the voice.

Mason insisted that the deals had to be fun to read, not just transactional. Groupon hired Brandon Copple, the former managing editor of Crain’s Chicago Business, as managing editor, and he ran a staff of copywriters armed with a massive style manual. The goal wasn’t just to inform—it was to entertain. If people lingered on the pitch and enjoyed it, they were more likely to buy. Groupon didn’t just sell discounts; it sold a little story every day.

If you’re looking for the seed of both Groupon’s genius and its eventual undoing, it’s here in the origin.

The pivot from The Point to Groupon showed real instinct for product-market fit. But the business that emerged was also built on recession-era dynamics—merchants willing to sacrifice margins for survival, consumers hungry for bargains—and that’s a kind of fuel that burns hot, fast, and unpredictably.

III. The Rocketship: Hypergrowth & The Clone Wars (2009–2010)

From a single pizza deal in a Chicago building lobby, Groupon turned into something the startup world hadn’t really seen before: hypergrowth that felt less like a curve and more like a wall. The numbers were so loud they became their own marketing. And they were about to draw two things like magnets: imitators, and the most powerful acquirer in tech.

From January 2010 to January 2011, Groupon’s U.S. monthly revenue jumped from $11 million to $89 million. A few years later, consolidated annual revenue would crest near $3.2 billion.

The engine behind it was brutally simple. Groupon’s standard pitch to merchants was a roughly 50/50 split. A restaurant might sell a $40 voucher that promised $80 worth of food, and Groupon would keep about $20. The merchant was betting those bargain-hunters would come back at full price. Groupon was betting it could sign up enough merchants and enough customers before anyone stopped to ask whether that bet actually worked.

Then came the land grab.

By October 2010, Groupon was live in about 150 cities across North America and another 100 cities across Europe, Asia, and South America. It had roughly 35 million registered users. The operating system was city-by-city conquest: parachute into a new market, hire a sales team, build an email list with aggressive marketing, and sign up local merchants as fast as possible. The deal itself doubled as the ad, and the product had virality baked in. A half-off massage wasn’t just a purchase—it was something you forwarded.

Inside the company, headcount ballooned just as quickly. Groupon went from about 125 people to more than 3,000 in a year, including around 1,000 at its famously wacky Chicago headquarters. The vibe was loud, young, and fast. That wasn’t an accident—it was the culture of a company trying to outrun competition by sheer velocity.

Because the competition was coming.

The most threatening clone wasn’t in the U.S. at first—it was overseas. CityDeal, incubated by Rocket Internet (the Samwer brothers’ startup factory), was widely regarded as a straight Groupon replica. Rocket’s playbook was controversial but effective: spot a proven American model, clone it internationally before the original could expand, then either sell it back or dominate locally.

CityDeal spread quickly, operating in dozens of cities across Europe. It even threatened to lean on Groupon’s identity itself, with country-specific sites that pushed right up against Groupon’s branding.

Groupon’s response was as aggressive as its growth: buy the clone before the clone becomes the incumbent.

In May 2010, Groupon acquired CityDeal, effectively doubling its international footprint. By August 2010, Groupon’s valuation had climbed to around $1.5 billion. The CityDeal deal was both brilliant and desperate. It instantly gave Groupon a presence “across the pond,” expanding reach to roughly 18 countries and 140 cities. It also meant absorbing a fast-moving organization and scaling operations even further, with reports describing the price as a “three-digit-million figure”—implying something like $100 million for a company that had only existed for months.

Mason later singled out Oliver Samwer, one of CityDeal’s co-founders, as a big reason the clone was so dangerous: CityDeal had hit number one in every country it served in just five months. Samwer had done this before, helping build European versions of American hits like eBay, eHarmony, and Zappos. He knew the game. And he played it relentlessly.

But CityDeal wasn’t an outlier. It was a signal.

By 2010, Forbes noted there were more than 700 Groupon copycats—most of them overseas. In the U.S., LivingSocial became Groupon’s primary rival, backed by major funding and running the same race with the same rules. LivingSocial, founded in 2007 in Washington, D.C., would grow to nearly 70 million members worldwide by 2013. Years later, in 2016, Groupon acquired LivingSocial.

The clone wars exposed the truth underneath Groupon’s meteoric rise: there were essentially no barriers to entry. If you could hire sales reps, build an email list, and stand up a website, you could be in business. The tech was almost comically simple—Groupon itself had started on a WordPress blog with hand-made PDFs. What mattered wasn’t proprietary technology. It was execution speed.

So Groupon kept sprinting. It expanded to more than 300 markets across 35 countries, up from just 28 U.S. markets the year before. The company said it had saved customers more than $800 million in that year—up from around $50 million the prior year. Everything about the story screamed momentum.

And at headquarters, that momentum became identity. Mason’s leadership was irreverent and deliberately unconventional, and it attracted exactly the kind of young salespeople and writers who could thrive in a high-energy, high-chaos environment. By 2011, Groupon had moved into its new home in the former Montgomery Ward catalog warehouse—thousands of millennials pouring into a company that felt like the center of the internet, even though its business was selling discounted massages.

But even at the peak of the euphoria, the warning lights were there if you looked.

The metrics that dazzled everyone—subscriber growth, city launches, gross merchandise value—didn’t answer the harder questions. Customer acquisition costs were enormous. Many merchants didn’t renew after running a deal, arguing that bargain-hunters didn’t come back at full price. And the 50/50 split often meant small businesses were effectively selling at a loss, hoping “volume” would make up for it.

Groupon’s hypergrowth era is the cleanest illustration of a brutal lesson: revenue growth alone tells you nothing about whether a business is healthy. You can scale unbelievably fast while quietly losing money on every transaction. The clone wars didn’t just create competition—they revealed that Groupon’s “moat” was mostly a head start.

And head starts don’t last forever.

IV. The $6 Billion Question: Turning Down Google (Late 2010)

On December 3, 2010, Groupon made the decision that would define its legacy.

Google offered to buy the company for $6 billion, and Groupon walked away.

In Chicago’s tech scene, it landed like a sonic boom. Groupon was barely two years old, still in the middle of its city-by-city blitz, and already being courted by the most powerful acquirer on the planet. This would have been Google’s biggest acquisition ever, dwarfing its $3.1 billion purchase of DoubleClick just a few years earlier.

To understand why the “no” felt plausible in the moment—and why it reads like a disaster in hindsight—you have to look at what Google thought it was buying, and what Groupon’s leadership thought they were becoming.

Google’s problem was offline commerce. It owned online intent through search and owned online ads. What it didn’t have was a reliable bridge from “I’m interested” to “I walked into the store and bought something.” Groupon, meanwhile, had built something that looked like that bridge: tens of millions of email subscribers, plus a rapidly growing web of relationships with small businesses—powered by a very human machine of sales reps and account managers.

Google wasn’t just buying a deals website. It was buying distribution, and a nationwide merchant pipeline, at the exact moment local digital advertising was starting to matter.

But the $6 billion headline wasn’t a simple $6 billion check. Reports suggested a large chunk of the price would be paid over time, contingent on Groupon hitting aggressive revenue targets. And hovering over everything was the strong likelihood of an antitrust review that could drag the deal out for more than a year—an eternity for a company moving as fast as Groupon was.

Inside Groupon, the board wrestled with it: Andrew Mason, Eric Lefkofsky, Brad Keywell, and investors including New Enterprise Associates and Digital Sky Technologies. Google had expressed interest the prior month. Then came the offer. And then, to the shock of pretty much everyone watching, Groupon decided to stay independent.

On paper, the logic was easy to sell. Groupon’s growth curve was the kind that makes rational people start talking like gamblers. If you believed the company could keep compounding—keep launching cities, keep stacking subscribers, keep owning the category—then $6 billion didn’t look like a peak. It looked like an early bid.

Founders love to tell stories about the companies that sold too soon. In late 2010, Groupon could tell itself it was avoiding the fate of the next Facebook-that-sold-to-Yahoo, or the next Google-that-took-a-small-check early and regretted it forever. The market was euphoric, and Groupon was the main character.

There was also a real cultural fear. Groupon was, at its core, a people business: sales on the ground, copywriters in the trenches, relationship management at scale. Google was an engineering-first company that preferred systems over armies. If you believed Groupon’s edge lived in that messy, high-velocity, human machine, then being absorbed into Google looked less like a win and more like a slow suffocation.

Still, the simplest explanation is often the truest one: Groupon thought it was worth more. An IPO promised not just validation, but liquidity at an even bigger number—and the chance to keep playing the game on their terms.

The counterfactual makes the moment famous. Groupon didn’t sell. Google built its own competitor, Google Offers, and later shut it down in 2014. The grand vision of daily deals as the gateway to local commerce never became the durable platform Google wanted—and, as it turned out, neither did Groupon’s version.

And for Groupon, the timeline is brutal. Just a couple years after rejecting Google, its market value fell below the offer. Soon after, Andrew Mason was out as CEO.

The rejection is now one of tech history’s great “what ifs.” Not because selling is always the right answer—but because certainty has a value that founders routinely underestimate. Growth curves feel infinite when you’re inside them. They almost never are.

V. The IPO Spectacle & Red Flags (2011)

With Google’s billions off the table, Groupon sprinted toward the other obvious exit: the public markets. In June 2011, Andrew Mason announced the plan. What followed wasn’t just a fast IPO—it was one of the most controversial IPO processes of the era, and it put a spotlight on problems the hype had been papering over.

On June 2, 2011, Groupon filed its S-1 to go public under the ticker GRPN. The deal was led by Morgan Stanley, Goldman Sachs, and Credit Suisse. When Groupon finally hit the Nasdaq on November 4, 2011, it was the biggest internet IPO since Google in 2004.

The filing instantly became famous—not for its financial rigor, but for its tone. Mason’s shareholder letter read like it had wandered in from a comedy blog. It talked about dancing classes, gorilla suits, and a “Grouspawn” program the company described as “a foundation we created that awards college scholarships to babies whose parents used a Groupon on their first date.” Silicon Valley found it charming. Securities lawyers found it… less charming.

But the real trouble wasn’t the jokes. It was the accounting.

Groupon’s S-1 leaned hard on a metric called Adjusted Consolidated Segment Operating Income—ACSOI. The pitch was that GAAP didn’t capture the “real” economics of the business, and that ACSOI did. The problem, and what immediately got the SEC’s attention, was how ACSOI got there: it ignored big costs associated with acquiring customers.

Under GAAP, Groupon acknowledged it was losing money. Under ACSOI, those losses turned into profits—because ACSOI included all the revenue, but only some of the expenses. In the initial S-1, Groupon reported a GAAP loss of $413.4 million for 2010 and a loss of $113.9 million for the first three months of 2011. Under ACSOI, those same periods flipped to positive $60.6 million and $81.6 million.

The SEC wasn’t impressed. Groupon took heat from investors and regulators for spotlighting the metric. After regulators raised questions—questions the Wall Street Journal described as calling out “financial voodoo”—Groupon downplayed ACSOI in amended IPO documents, pushing it into the background as just an internal measure.

Then came another blow. In late September, Groupon revised its reported revenue to “correct for an error”: it had been counting the money it owed merchants—the merchants’ share of each coupon—as Groupon revenue. Once it fixed that, Groupon’s reported sales for the first half of 2011 dropped sharply, from $1.5 billion to $688 million. The headline wasn’t subtle: the company had, effectively, cut its own topline in half during the roadshow.

And Mason added fuel to the fire. In the middle of the pre-IPO quiet period, he wrote a lengthy, profanity-laced internal memo that leaked to the press—touting Groupon’s prospects and attacking the financial press for negative coverage. The SEC ultimately required Groupon to include the memo in its IPO filing.

None of it stopped the train. Investor demand for tech in 2011 was still running hot. Groupon’s underwriters bumped the price at the last minute, above the earlier $16 to $18 target range, and added another 5 million shares. The IPO raised $700 million for the company, and by the end of the first day Groupon carried a valuation north of $16 billion—bigger than household-name retailers like Whole Foods, Best Buy, and Bed, Bath & Beyond.

The euphoria didn’t last. Within about two weeks, the stock started sliding, and the ride turned bumpy fast.

In hindsight, the warnings were almost too clean. When a company needs a custom profit metric that conveniently excludes the expenses required to operate—especially marketing and customer acquisition—that’s not just aggressive presentation. It’s a signal that the core engine may not work on normal terms. And when leadership treats the IPO rulebook like a nuisance rather than a boundary, it’s another kind of signal: not about the business model, but about how the business will behave once public markets start asking harder questions.

VI. The Unraveling: When The Model Breaks (2011–2013)

Within eighteen months of its triumphant IPO, Groupon’s stock had cratered, the company was drowning in bad headlines, and the cracks that had always been there were now running straight through the foundation.

This wasn’t a temporary slump or a post-IPO hangover. The problems were structural. The model depended on two leaps of faith happening at the same time: customers would get a great experience at a steep discount, and merchants would convert those one-time bargain hunters into full-price regulars. In practice, too many customers walked away with a mediocre service, and too many merchants walked away with a list of coupon users who never came back.

The merchant side deteriorated first, and fast. A survey from Susquehanna Financial Group and daily deal aggregator Yipit looked at 400 businesses that had run discounts through Groupon, LivingSocial, and other deal platforms. A majority—52%—said they would not run another deal in the next six months. The comments were blunt: “It is for desperate businesses.” “The financials just can’t work out.” “Groupon is the worst marketing ever.”

Because once you actually did the math, “marketing” started to look a lot like selling at a loss.

A restaurant owner might offer a 40€ dinner for two at a 50% discount—20€ instead of 40€. Even that is already a huge haircut. Then Groupon takes its cut, often around half, leaving the restaurant with about 10€ per voucher. The salesperson’s pitch was that the restaurant would make it up on volume, on upsells, and especially on repeat business—customers who’d return later and pay full price, bringing friends.

But one analysis found only about 20% of Groupon buyers returned for full-price purchases. The conversion story—the idea that discount customers would turn into loyal customers—proved mostly wishful thinking. Groupon was exceptionally good at attracting deal hunters. And deal hunters are, by definition, not loyal. They jump to the next inbox special.

Then the consumer side started to sour too. “Groupon fatigue” set in. The daily emails that once felt like a fun surprise began to feel like noise—too many offers, too little quality control, and too many deals that sounded better than they actually were. Even the most enthusiastic subscribers eventually hit their limit.

Public-market investors didn’t need to read the tea leaves. They could read the earnings.

In its first earnings release as a public company, Groupon reported a fourth-quarter 2011 loss of $9.8 million on an adjusted basis, which spooked investors who’d been sold a story of leverage and momentum. In March 2012, additional concerns flared when the company restated 2011 revenues downward. By August 2012, the stock was down about 75%.

And the accounting headaches kept piling up. Just weeks before the IPO, under pressure from the SEC, Groupon changed how it recognized revenue—slashing its reported 2010 revenue by half. Then, in April 2012, Groupon restated earnings again after its auditor flagged a “material weakness in its internal controls,” which is a polite way of saying the company’s financial plumbing wasn’t reliable.

All of this was happening while the daily-deals gold rush was cooling off. Competition stayed fierce—LivingSocial, Amazon, and others kept pushing in—at the exact moment consumers and merchants were losing interest in the category itself. Merchants complained about deep discounts, delayed payments, and fulfillment issues. And Groupon’s expensive international expansion, especially in recession-hit Europe, started biting into margins and slowing growth by late 2012.

Inside the company, the board’s patience with Andrew Mason thinned as Groupon missed projections quarter after quarter. Rumors swirled late in 2012 that the board was looking to replace him after terrible third-quarter results. His exit would come right after another dismal quarter—an ending that felt less like a surprise than an inevitability.

The public embarrassment was already baked in. On December 18, 2012, CNBC named Mason “Worst CEO of the Year,” writing in part: “Mason’s goofball antics, which can come off more like a big kid than company leader, almost make a mockery of corporate leadership—especially for a company with a market value of more than $3 billion. It would be excusable, even endearing, if the company were doing well but it’s not. Sales growth is through the floor.”

But beneath the stock chart and the snark was the deeper strategic issue: Groupon looked like a two-sided marketplace, but it didn’t behave like one.

In a true platform, each new user on one side makes the product more valuable for the other side, and that feedback loop creates defensibility. Groupon’s loop didn’t compound. Merchants wanted new customers—not the same discount seekers cycling through. Customers wanted new deals—not the same merchants running promotions again and again. As Groupon scaled, neither side became meaningfully stickier. The engine kept running, but it never turned into a moat.

And once growth stopped masking that reality, the unraveling wasn’t just possible. It was baked in.

VII. The Mason Exit & The Dark Years (2013–2015)

On February 28, 2013, Groupon’s board finally pulled the lever. Andrew Mason was fired as CEO the day after the company missed analysts’ expectations on sales and came up painfully short on profit.

Mason’s goodbye was pure Mason: blunt, self-aware, and impossible to PR-polish.

"After four and a half intense and wonderful years as CEO of Groupon, I've decided that I'd like to spend more time with my family. Just kidding—I was fired today. If you're wondering why... you haven't been paying attention. From controversial metrics in our S1 to our material weakness to two quarters of missing our own expectations and a stock price that's hovering around one quarter of our listing price, the events of the last year and a half speak for themselves. As CEO, I am accountable."

The email ricocheted across the internet, mostly because it said the quiet part out loud. Fired CEOs don’t usually admit they were fired. Mason did. He even joked about needing a “fat camp” to lose his “Groupon 40,” then ended with the closest thing to a founder’s benediction: “have the courage to start with the customer.” His biggest regrets, he wrote, were the times he let “a lack of data override my intuition on what’s best for our customers.”

Even his exit package carried the same oddball signature. Reports estimated his severance at just $378.36—six months of salary—because Mason had famously cut his pay to $756.72 a year in 2011. The real wealth, and the real stakes, were in his stock.

With Mason out, Groupon went into triage mode. Executive chairman Eric Lefkofsky stepped into a newly created “office of the chief executive” alongside vice chairman Ted Leonsis. By August 2013, Lefkofsky formally became CEO.

It was a stabilizing move, but not a magical one. By the time Lefkofsky stepped down in 2015, Groupon’s value had fallen to about $2.6 billion. The company wasn’t just fighting competitors anymore; it was fighting the slow realization that the daily-deals engine wasn’t a durable business on its own.

So Groupon started searching for a way out—anything that could turn the brand’s massive reach into something more defensible than tomorrow’s discount email.

That’s where the pivots came in. Groupon rolled out new initiatives, including a physical product business called Groupon Goods and a credit card payments processing service. It experimented with events and ticketing through GrouponLive. Goods was the biggest swing: a bid to become a broader marketplace where other sellers could move physical products, more Amazon or eBay than “half off a massage.”

But going toe-to-toe with Amazon in physical goods was a brutal place to learn humility. The category was crowded, the products didn’t stand out, and customer demand didn’t scale the way the company needed. Years later, in February 2020, Groupon announced it would be “exiting goods.”

Leadership churn kept going, too. In 2015, Rich Williams took over as CEO and set out to remake Groupon from a daily-deals blast into a local marketplace. Over the next decade, the company repeatedly restructured—cutting employees, changing priorities, and swinging focus between the original local-deals DNA and the merchandise experiment.

Groupon also pulled back hard internationally. By March 31, 2017, the company had completed the dispositions of operations in 11 countries, and those results were presented as discontinued operations.

For anyone watching from the outside, the post-Mason stretch delivered an uncomfortable lesson: swapping CEOs and launching new product lines can buy time, but it can’t fix a model that doesn’t work. Groupon could change leadership, cut costs, and rebrand the offering—but the core challenge remained the same: creating sustainable value for both merchants and consumers, at the same time.

VIII. The Quiet Reinvention: From Deals to Marketplace (2015–2020)

While the outside world kept writing Groupon’s obituary, the company was trying to do something much harder than “cut costs and wait it out.” It was trying to change what Groupon actually was. Under Rich Williams, the ambition shifted from a one-day-at-a-time discount machine to something closer to an always-on local marketplace.

The groundwork for that change had started earlier. In November 2013—just before Groupon’s fifth anniversary—the company rebuilt its website and shipped a set of new features. The SVP of product management put it plainly: the old Groupon was “designed for a deal of the day,” and the new Groupon was “designed for a marketplace.”

That sentence captures the entire pivot. Daily deals are a sugar rush: one big blast, one big spike, then you start over tomorrow. A marketplace, in theory, is the opposite. Inventory sticks around. Merchants can adjust offers based on demand instead of gambling on a single, make-or-break promotion. And consumers don’t have to wait for an email to tell them what today’s “one thing” is.

So Groupon started rebuilding the experience around browsing and personalization. Instead of mass email blasts being the product, algorithms tried to match offers to individual preferences. And instead of urgency doing all the work, Groupon introduced “Pull,” where customers could search through thousands of deals and buy what they wanted, when they wanted it.

That change went hand-in-hand with the mobile shift. Groupon moved a large chunk of its North American users to mobile—nearly 40%—and reduced its dependence on email, which fell to under half of transactions. The bet was clear: if Groupon could become something you opened like an app, not something that yelled at you like a newsletter, it might finally have a more durable relationship with customers.

Mobile wasn’t a new idea at the company. Back in 2011, Groupon built Groupon Now, an early attempt to make deals feel immediate on a smartphone. The interface was famously simple: two buttons, “I’m Hungry” and “I’m Bored.” Tap one, and the app used geolocation to surface nearby food or entertainment deals.

At the same time, Groupon had to fix the merchant side of the equation. The take rate—Groupon’s cut of each sale—evolved downward. Lower commissions were meant to attract better merchants, not just the ones in survival mode. And more self-service tools meant Groupon didn’t need to rely on an army of salespeople to keep supply flowing, which was essential if unit economics were ever going to improve.

On the surface, the company still looked big. Groupon hit its highest global revenue in 2016, at just over $3 billion. But that “peak” masked an uncomfortable truth: a meaningful chunk of that revenue was coming from Groupon Goods, and Goods came with terrible margins.

Eventually, Groupon said the quiet part out loud. In February 2020, the company announced it would be exiting goods, calling it a business that had “outlived its role as a business driver” and had become “a significant drag” on profitability. The goal was to phase out Groupon Goods by the end of the year and refocus on what the company originally had: helping people discover local things to do.

The problem was that Goods had been doing a lot of the heavy lifting. With the Goods division responsible for around half of Groupon’s $1.12 billion revenue in 2019, walking away meant accepting that the company would get smaller before it could get healthier.

Then came COVID-19.

The pandemic didn’t just slow Groupon down. It erased the demand for its core product overnight. Restaurants closed. Spas shut down. Local experiences—the very thing Groupon was leaning into—became impossible to deliver. For the first nine months of 2020, Groupon lost more than $300 million, compared with $91 million in the year-ago period.

The company laid off about 2,800 employees—around 44% of its workforce. The board also adopted a shareholder rights plan, commonly called a “poison pill,” to defend against any attempts to take control of the company.

If you’re looking for the lesson in the 2015–2020 stretch, it’s this: the marketplace pivot made sense on paper, but execution risk is real—and timing can be cruel. Groupon wasn’t just fighting its business model; it was fighting its own brand. It had trained customers to think of it as a place for deep discounts, not a trusted way to discover great local experiences. And changing what you mean to people takes time—exactly what Groupon didn’t have when the world shut down.

IX. Recent History & Current State (2020–2025)

By late 2025, Groupon existed in a form that would have been almost unrecognizable to the team that turned down Google’s billions. Smaller. Quieter. And, surprisingly, showing signs of real operational health.

But the path here ran straight through a near-death experience.

In 2023, Groupon was teetering on the edge of insolvency. The once-iconic unicorn—celebrated for rejecting Google’s $6 billion offer and later commanding a peak valuation often cited around $25 billion—had shrunk dramatically after years of revenue declines and downsizing. In May 2023, Groupon issued a “going concern” warning, telling investors the company could be out of business within a year.

Into that crisis stepped Dusan Senkypl, a Czech investor and Groupon’s largest shareholder. Senkypl is a co-founder of Pale Fire Capital, a private equity firm based in Prague. Pale Fire didn’t just buy and watch from the sidelines. The relationship turned into an activist fight that ended with the firm winning two board seats—one held by Senkypl himself—and, eventually, real influence over the turnaround plan.

“It was not a great situation for the business,” said Rana Kashyap, a New York-based former hedge fund investor who joined Groupon in January 2023 under Senkypl’s leadership. “Things were pretty grim.”

The turnaround playbook started with the unglamorous stuff: costs, focus, and survival. Groupon cut expenses and even unwound pieces of its old identity, including its physical footprint. It broke the lease on its massive River North headquarters at 600 W. Chicago Ave., a building that once held thousands of employees at the height of the daily-deals era. In January 2024, Groupon moved downtown, subleasing a single 25,000-square-foot floor.

The customer story was just as stark. Active customers had been in steady decline for years, falling from over 50 million at a peak in the fourth quarter of 2014 to about 18 million by the first quarter of 2023.

And yet, after the bottom came something Groupon hadn’t delivered in a long time: stabilization.

Billings hit a low of $1.56 billion. Revenue fell to $492 million in 2024. But in 2025, both began ticking up again, with projected billings of $1.6 billion and about $500 million in revenue. Kashyap said the company reached positive free cash flow for the first time in years—and that the turnaround was finally taking hold, with Chicago leading the way.

In the third quarter, billings growth across North America was up 18%, and Chicago—Groupon’s largest and fastest-growing market—nearly doubled the national rate. Groupon, a supply-driven business at its core, found momentum by expanding local third-party deals that performed well online.

Strategically, the company leaned harder into what still worked: local. Groupon moved further away from goods—ceding that battlefield to a crowded universe of e-commerce competitors—and doubled down on higher-value local offerings. “Things To Do” became its largest category, anchored by experiences like boat tours, museums, and activities with a clear value proposition.

The leadership team changed with the business. As of November 2025, Senkypl served as CEO, a role he held permanently after being appointed in May 2024. Kashyap became CFO on September 1, 2025. Jiri Ponrt moved into the COO role on September 1, 2025, after serving as CFO.

Financially, Groupon guided to full-year 2025 Adjusted EBITDA of $70 million to $75 million. In Q3 2025, the company reported global billings growth of 11% year over year, with the core local category up 18% and representing 89% of total billings. Adjusted EBITDA came in at $18 million, and Groupon reported $60 million in trailing twelve-month free cash flow. Customer acquisition also showed momentum, with nearly 300,000 net new active customers added quarter over quarter and more than 1 million over the last four quarters.

Zooming out, the competitive landscape that once made daily deals feel inevitable has largely collapsed. Google walked away from its deals ambitions. Amazon Local shut down. LivingSocial—once said to be worth as much as $4.5 billion in the private markets—ended up inside Groupon for what was described as a “non-material” price.

So Groupon, improbably, is still here. For investors, it’s an unusual setup: a much smaller company with drastically reduced expectations that might actually be sustainable. The open question is whether there’s any real path to growth from this base—or whether Groupon has simply found a size at which it can exist without imploding.

X. Inflection Points Deep Dive

Groupon’s story looks like a straight line on the way up and a messy collapse on the way down. In reality, it hinged on a handful of moments—each one narrowing the set of options until the company was boxed into a model that couldn’t live up to the expectations it had created.

Here are the six inflection points that mattered most:

1. The Google Rejection (December 2010) This was the sliding-doors moment. Taking Google’s $6 billion would have crystallized a win that early investors and employees could only dream about. Walking away meant betting that Groupon could become a durable, independent business—and that Google, of all companies, couldn’t just build its own version. In hindsight, the decision reads less like conviction and more like hubris: the belief that a growth curve would stay infinite, and that a head start was the same thing as a moat.

2. The IPO (November 2011) Going public put Groupon on a clock. Quarterly expectations became the scoreboard before the model had proved it could be sustainably profitable. The IPO also created a different set of incentives: liquidity for insiders and constant pressure to defend the narrative. The accounting controversies weren’t just a sideshow—they were an early signal that storytelling was outpacing fundamentals.

3. The Merchant Revolt (2012) When surveys showed more than half of merchants saying they wouldn’t run another deal, the marketplace started to break from the supply side. And once merchants pull back, everything else follows. Fewer compelling offers means less consumer excitement. Less consumer excitement means even fewer merchants willing to take the risk. That negative loop is the inverse of what a healthy platform is supposed to do—and once it starts, it’s brutally hard to stop.

4. The Mason Firing (February 2013) Firing Andrew Mason was an admission that the original playbook wasn’t working. But replacing the CEO didn’t replace the economics. The years that followed—Lefkofsky, Williams, and a rotating cast of leaders—weren’t just about governance. They reflected a company searching for a management fix to what was, at root, a structural problem.

5. The Marketplace Pivot (2015-2016) Moving from “deal of the day” to an always-on marketplace was strategically logical. It made Groupon feel less like an email stunt and more like a shopping destination. But it ran headfirst into reputation. Consumers had learned to associate Groupon with desperation discounts, not quality experiences. Merchants had learned to associate Groupon with one-time bargain hunters, not lasting demand. The pivot was necessary. It just wasn’t enough on its own.

6. COVID-19 and the Going Concern (2020-2023) The pandemic was the gut punch that nearly finished the company, wiping out local experiences overnight. By 2023, Groupon was issuing a going concern warning—basically telling the world it might not survive the next year. The restructuring and turnaround push led by Senkypl and Pale Fire Capital became the last, best attempt at finding a sustainable version of Groupon: smaller than the original ambition, but potentially real.

For investors, the takeaway isn’t just that Groupon made a few bad calls. It’s that decisions compound. Each moment above didn’t just change the quarter—it narrowed the future. And eventually, Groupon found itself trying to support a public-company valuation with a business model that couldn’t generate the kind of returns that valuation demanded.

XI. Strategic Analysis: Porter's 5 Forces

If you step back from the drama—Google, the IPO, the fall—and just look at the game Groupon chose to play, Porter’s 5 Forces explains why the outcome was almost prewritten. The industry structure made sustained profitability feel less like a challenge and more like a contradiction.

Threat of New Entrants: HIGH

Starting a daily deals competitor took almost nothing: a basic website, an email list, and a handful of salespeople. Groupon was operating in a market with effectively no barriers to entry. The tech wasn’t special. The merchant “relationships” weren’t exclusive. And any company with enough marketing muscle could copy the playbook. The flood of more than 700 clones in the first couple of years didn’t just create noise—it proved the model was easy to replicate.

Bargaining Power of Suppliers (Merchants): HIGH

On the supply side, merchants had options. They could buy Google ads, run Facebook campaigns, advertise on Yelp, lean into Instagram, or just do their own promotions. And the merchants Groupon wanted most—the successful ones with real demand—were the least likely to agree to deep discounts and big revenue splits. The ones willing to say yes often did it out of desperation, which tended to mean weaker offerings and worse customer experiences. Over time, frustration grew: slim or negative profitability on deals, delayed payouts, and the operational pain of handling a surge of coupon customers.

Bargaining Power of Buyers (Consumers): HIGH

On the customer side, Groupon trained people to behave like mercenaries. Deal-seekers are disloyal by nature, and switching costs were basically zero. If the emails got annoying, one click and you were gone. If another platform had a better offer, you didn’t “churn”—you just bought there instead. Groupon’s audience was huge, but it was the exact audience least likely to become long-term, full-price customers for merchants.

Threat of Substitutes: VERY HIGH

Groupon’s real product was “customer acquisition for local businesses,” and substitutes were everywhere. Google Search and Maps, Facebook and Instagram ads, Yelp listings, credit card reward programs, and direct-to-consumer promotions all competed for the same marketing dollars. And as digital advertising got more targeted and measurable, Groupon’s mass email discount blasts started to look like a blunt instrument from an earlier internet era.

Competitive Rivalry: EXTREME

At the peak of daily-deals mania, the space was a brawl. Hundreds of competitors fought for the same merchants and the same attention. Some offered merchants better economics just to win deals. Marketing spending escalated. With little differentiation, competition collapsed into a race to the bottom—on price, on take rate, and often on quality.

Conclusion: Groupon was stuck in one of the worst industry setups imaginable for building a durable profit machine. Every force pushed against it at once. The only theoretical escape hatch would’ve been to become so dominant that network effects kicked in—but daily deals never had strong enough network effects for that dominance to be either achievable or defensible.

XII. Strategic Analysis: Hamilton's 7 Powers

Hamilton Helmer’s framework is all about what makes a business durable. Not “popular,” not “fast-growing,” but protected. Run Groupon through the 7 Powers and you can see why a company could explode into the culture and still end up with almost nothing standing between it and the next clone.

Scale Economies: INITIALLY PRESENT, NOT DEFENSIBLE

At first, Groupon did get some benefits from size. A bigger email list in a city made each deal easier to sell, and a larger sales force got more efficient as teams learned what worked. But scale never turned into leverage. A merchant didn’t pay more because Groupon had 100,000 subscribers instead of 50,000. Consumers didn’t get meaningfully better deals because the list was bigger. Groupon grew, but it didn’t gain pricing power.

Network Effects: WEAK TO NON-EXISTENT

This was the fatal flaw. In a true two-sided marketplace, more buyers attract more sellers, which attracts more buyers, and the flywheel gets stronger over time. Groupon didn’t work that way. The platform was built on deep discounts, which attracted deal-seekers—but those customers rarely turned into long-term regulars for merchants. Merchants wanted new customers; adding more of the same bargain-hunters didn’t make the platform more valuable. Consumers wanted new deals; adding more merchants offering the same kind of discount didn’t compound value either. Groupon had a growth loop early on, but not a durable network effect.

Counter-Positioning: NO

Nothing about Groupon’s model made it hard for incumbents to respond. Google launched Google Offers. Amazon launched Amazon Local. Yelp added deals. If you already had local relationships or consumer traffic, adding “discount offers” wasn’t a self-destructive move. Groupon didn’t force competitors into an uncomfortable tradeoff. It just gave them a feature to copy.

Switching Costs: NONE

On both sides, switching was frictionless. Consumers could subscribe to multiple deal emails at once and click whichever looked best. Merchants could run promotions with multiple platforms without any real penalty. Neither side got locked in, and Groupon didn’t accumulate the kind of dependency that makes a marketplace resilient.

Branding: INITIALLY STRONG, BECAME LIABILITY

Groupon’s brand started as an asset: instant recognition, a sense of fun, a shared cultural reference point. But the model carried a built-in trap. Too many customers had inconsistent experiences, and too many businesses ended up with one-time visitors who never returned at full price. As competition flooded the market and deal quality got noisier, “Groupon” increasingly meant deep discounts and desperation pricing. Great for awareness. Terrible if your endgame is a trusted marketplace for high-quality local experiences.

Cornered Resource: NO

Groupon didn’t have proprietary tech competitors couldn’t replicate. Its consumer and merchant data wasn’t uniquely defensible. Merchant relationships were transactional, not exclusive. There was no scarce input—no locked-up supply, no special distribution channel—that others couldn’t chase too.

Process Power: NO

The machine that powered Groupon was labor-heavy: salespeople signing merchants, writers crafting deal copy, support teams handling the fallout. It scaled through headcount, not through a hard-to-copy process advantage. Competitors could hire similar teams and run the same playbook. And over time, that operational footprint became a burden: constant effort just to keep the inventory flowing.

Conclusion: Groupon ended up with effectively none of the 7 powers in a durable way. That’s the answer to the central puzzle of its history. Groupon had unprecedented growth, billions in revenue, and massive brand awareness—but growth without defensibility is just scale without protection. When the growth slowed, there was no moat to hold the business together.

XIII. Playbook: Business & Investing Lessons

Groupon’s rise and fall is a masterclass in how a company can win the internet and still lose the business. For founders building marketplaces—and investors underwriting them—the lessons aren’t subtle. They’re foundational.

For Founders & Operators:

Growth ≠ defensibility. Groupon grew at a pace that made people suspend disbelief. And it still didn’t have a moat. Virality is distribution, not protection. Every “we’re growing fast” chart needs a second chart right next to it: why can’t someone else do the same thing?

Unit economics matter from day one. Groupon often lost money on the transaction and told itself scale would fix it later. That story is intoxicating in a bull market—and lethal in real life. If a customer never pays you back in contribution margin, growth doesn’t save you. It just makes you fail faster.

Two-sided marketplaces are hard. Calling something a marketplace doesn’t make network effects appear. Groupon connected buyers and merchants, but the relationship didn’t compound. As the platform grew, neither side became meaningfully stickier. If your “marketplace” is really just a series of one-off, discount-driven transactions, you don’t have a flywheel—you have a treadmill.

Beware one-time customer behavior. Groupon was unbelievably good at finding deal-seekers. And deal-seekers are, by definition, not loyal. If your customer base is selected for price sensitivity, you bake margin pressure into the model forever. The easiest customers to acquire are often the least valuable customers to keep.

Merchant lifetime value is everything. On the supply side, the whole game is repeatability. If merchants don’t come back after one campaign, you’re not building a marketplace—you’re burning through a finite list. Groupon’s churn meant it had to keep feeding the machine with new merchants, until “new” stopped being available at scale.

Culture of discipline vs. culture of growth. Mason’s culture was perfect for hypergrowth: loud, fast, quirky, and optimized for momentum. But profitability requires a different muscle: control, consistency, and operational rigor. Making that cultural shift is one of the hardest transitions a startup can face—especially when the company has already trained itself to worship growth.

For Investors:

Question the metrics. Gross merchandise value isn’t revenue. ACSOI wasn’t profit. When a company leans on custom metrics, ask what the standard ones are saying—and why management doesn’t want to lead with them. In Groupon’s case, the adjustment worked largely by counting all the revenue while conveniently ignoring major expenses, turning losses into “profits” on paper.

Watch the lockup. Insider selling isn’t always a red flag—people diversify, taxes are real—but aggressive selling should change your posture. If early investors and executives are rushing to cash out, it’s worth asking what risks they see up close that the market hasn’t priced in yet.

Study the cohorts. Are early customers coming back? Are merchants renewing? Cohorts tell you whether growth is product-driven or marketing-driven. Groupon’s topline momentum masked shaky retention on both sides.

Industry structure matters more than execution. Groupon wasn’t just mismanaged; it was playing in a brutal structure. When entry is easy, switching costs are near zero, and rivals are everywhere, even excellent execution only gets you so far. Great operators can optimize inside the box. They usually can’t change the box.

The acquisition offer is information. Google’s $6 billion bid wasn’t charity; it was a highly informed valuation from one of the best analyzers in tech. Groupon turning it down is famous—but the bigger lesson is that credible offers often reveal the ceiling more accurately than founder ambition does.

XIV. Bull vs. Bear Case

The Bull Case:

Groupon has survived multiple near-death experiences and still generates around $500 million in revenue. For a company that went from “fastest-growing in history” headlines to being written off as a tech cautionary tale, just being here is already a kind of win.

And the turnaround case isn’t just vibes. Groupon’s CFO has pointed to a business doing about $1.6 billion in billings, roughly $500 million in revenue, around $70 million in EBITDA, and about $60 million in free cash flow, with roughly 16 million active customers. Management frames this as a strategic transformation: local billings growth of 18% in Q3 and about 1 million net new active customers over the last four quarters.

The other tailwind is that the battlefield has emptied out. Most daily deal competitors have faded, been shut down, or been absorbed. Groupon still owns the default consumer association for discounted local experiences, and the bet is that this brand recognition is an asset again—especially in “Things To Do,” where museums, tours, and activities offer a clearer value proposition than the bargain-basement service deals that hurt Groupon’s reputation in the first place.

Layer on top the valuation argument: if the stock trades at a fraction of revenue, the upside can look meaningful if growth stabilizes and cash flow holds. And Pale Fire Capital’s influence offers a narrative Groupon rarely had in the past—disciplined capital allocation and operational focus instead of growth-at-all-costs improvisation.

The Bear Case:

Groupon could also still be a fundamentally declining business with no durable growth path. After peaking around $3 billion in revenue in 2016, it fell to about $500 million by 2023. That kind of drop isn’t a dip. It’s a decade-long erosion of relevance.

The hardest part to fix may be memory. For many consumers, “Groupon” still means a mediocre experience, awkward redemption rules, or merchants that felt like they were on the platform because they had to be. Repositioning as a higher-quality local marketplace isn’t just a product change—it’s a reputation rebuild, and those can take years.

Meanwhile, the world moved on. Local discovery now happens through Google Maps, Instagram, Yelp, and social media. Merchants have their own loyalty programs, better targeting tools, and more ways to reach customers without taking a deep discount and splitting revenue. The problem Groupon originally solved still exists, but it now has dozens of alternatives that feel more modern and more integrated into daily life.

And structurally, the old critique still bites: there’s no obvious technological moat. Years of leadership turnover and strategic drift have burned time and trust. In this view, the stock isn’t cheap—it’s a value trap, priced low because the business is still fighting gravity.

The Realistic Case:

The most likely outcome sits between the extremes. Groupon survives as a smaller, potentially profitable niche business for price-conscious consumers who actively seek discounts on local experiences. It doesn’t return to its former cultural status, and it doesn’t need to—because the company is no longer trying to justify a peak-era narrative.

In that world, the current valuation may be roughly fair: not a screaming bargain, not wildly overpriced, just a reflection of a business that can generate cash but probably won’t become a growth story again.

A modest acquisition is plausible—by a larger platform like Yelp or TripAdvisor, or by a private equity firm that specializes in distressed and turnaround assets. Not thrilling, not glamorous. But potentially a steady cash generator for the right owner.

XV. What To Watch: Key Metrics & Indicators

If you want to know whether Groupon’s latest comeback is real—or just a temporary bounce—there are three signals that matter more than everything else.

1. North America Local Billings Growth

This is the heartbeat of the turnaround. In Q3 2025, Groupon reported global billings up 11% year over year, with its core local category up 18% and making up 89% of total billings. The key now is whether North America Local can keep growing at a healthy clip. If that growth holds, it suggests the marketplace is attracting demand and, crucially, enough supply to meet it. If billings flatten or slide, it’s a sign Groupon may have stabilized—but not found a path back to growth.

2. Active Customer Trends

Groupon’s model only works if it can keep pulling people back in a world where local discovery is everywhere. In Q3 2025, the company added nearly 300,000 net new active customers quarter over quarter, and more than 1 million over the last four quarters. That’s the kind of momentum you can build a narrative on—but it has to continue. Watch the quarter-to-quarter trend: steady gains suggest the product is getting stickier; a return to sequential declines suggests the old churn problem is creeping back.

3. Free Cash Flow

At the end of the day, the most honest metric is cash. Groupon posted adjusted EBITDA of $18 million and about $60 million in trailing twelve-month free cash flow. Positive free cash flow means the company can fund itself and operate without constantly reaching for outside capital. If free cash flow grows, it’s evidence the business is getting stronger, not just smaller. If it turns negative again, the survival questions come rushing back.

Beyond those headline indicators, the supporting cast still matters: merchant retention (rarely disclosed, but occasionally hinted at), take rate changes, marketing efficiency (customer acquisition cost relative to lifetime value), and how dependent the business is on North America versus weaker international operations.

XVI. Epilogue: The Groupon Legacy

What did Groupon prove? That consumers love deals—obvious in hindsight, but Groupon demonstrated it at unprecedented scale. That local merchants desperately need digital customer acquisition, a truth that helped spark an entire ecosystem of tools and platforms built to bring customers through the door. And that email, used the right way, could drive real commerce. For a while, Groupon’s daily emails achieved the kind of engagement that felt almost impossible.

What did Groupon get wrong? Most of what makes a business durable. The model was optimized for virality and speed, not for healthy unit economics or long-term merchant satisfaction. The culture celebrated momentum more than discipline. Leadership treated early traction like proof of an enduring advantage.

And the model’s flaws weren’t subtle once the hype wore off. Groupon’s decline wasn’t the result of one bad quarter or one competitor. It was the collision of a difficult-to-sustain business model, persistent profitability challenges, and intense competition from other coupon, rebate, and local discovery products.

The key players moved on. Andrew Mason—the music major who built, then lost, a multi-billion-dollar company before 35—went looking for a different kind of product-market fit. After Groupon, he launched Detour, an app for GPS-guided city tours, and later founded Descript, a collaborative content creation tool for audio and video that incorporates advanced AI features. Descript became a real success in its category, a sign that Mason absorbed hard lessons from Groupon and applied them to a business with very different economics.

Eric Lefkofsky’s post-Groupon chapter was even more dramatic. In 2015, he founded Tempus AI, a company focused on enabling physicians to deliver personalized cancer care, and he became its CEO. Lefkofsky is also a co-founder of Echo Global Logistics, InnerWorkings, and Mediaocean. As of September 2025, his net worth was estimated at about $6 billion.

That arc is one of the strangest contrasts in modern business: from discount coupons for pedicures to potentially life-saving cancer care powered by artificial intelligence. Tempus, an AI-powered health care technology company, is publicly traded, has around 4,000 employees, offices and labs across the country, and a market cap of more than $13 billion. The irony is hard to miss: the company Lefkofsky built to fight cancer is now worth more than Groupon ever was at its peak.

Groupon also left behind a permanent scar—and a permanent lesson—for investors. It changed how people evaluate “platform” claims. The company became a go-to cautionary reference point: does this marketplace have real network effects, or is it simply taking a cut of transactions? Is growth compounding, or is it being purchased at negative unit economics? A lot of the tougher questions sophisticated investors now ask about fast-growing companies trace back to watching Groupon’s story unfold in public.

And unlike other cautionary tales—Pets.com’s instant implosion, Webvan’s logistical overreach, WeWork’s governance meltdown—Groupon’s is distinctive because it didn’t end with a single crater. The company didn’t die; it shrank. The meteor didn’t crash into the earth; it burned for years until only a small ember remained.

Today, that quirky e-commerce startup once dubbed the fastest-growing company ever—the one that ran Super Bowl ads and dominated the media cycle—is still here, smaller and quieter, trying to execute a turnaround after years of downsizing and red ink.

Whether the second act becomes something meaningful is still an open question. But the first act—the breathtaking ascent and humbling descent—has already earned its place as one of the defining business stories of the digital era, and a reminder that growth without a moat is usually just the prologue to decline.

XVII. Further Reading & Resources

Primary Sources: - Groupon SEC filings (S-1, 10-Ks, proxy statements) on SEC.gov - Groupon Investor Relations presentations and earnings call transcripts

Key Historical Documents: - Andrew Mason’s S-1 letter to shareholders - Andrew Mason’s February 2013 farewell email (“I was fired today”) - SEC correspondence and filings related to ACSOI

Academic Analysis: - Harvard Business Review case studies on Groupon and merchant economics - Marketing Letters study on Groupon deal structures (2016) - Stanford and Kellogg business school case studies on Groupon’s model and incentives

Journalistic Coverage: - Chicago Tribune reporting on Groupon and its Chicago headquarters - Wall Street Journal coverage of the accounting controversies - Forbes coverage of Groupon’s “fastest-growing company” era

Strategic Frameworks: - Bill Gurley’s writing on marketplace economics and sustainability - Hamilton Helmer’s 7 Powers framework for competitive advantage - Michael Porter’s Five Forces framework, applied to platform businesses

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube