Garmin Ltd.: The Art of Specialization and the Great Tech Pivot

I. Introduction & The Garmin Phenomenon

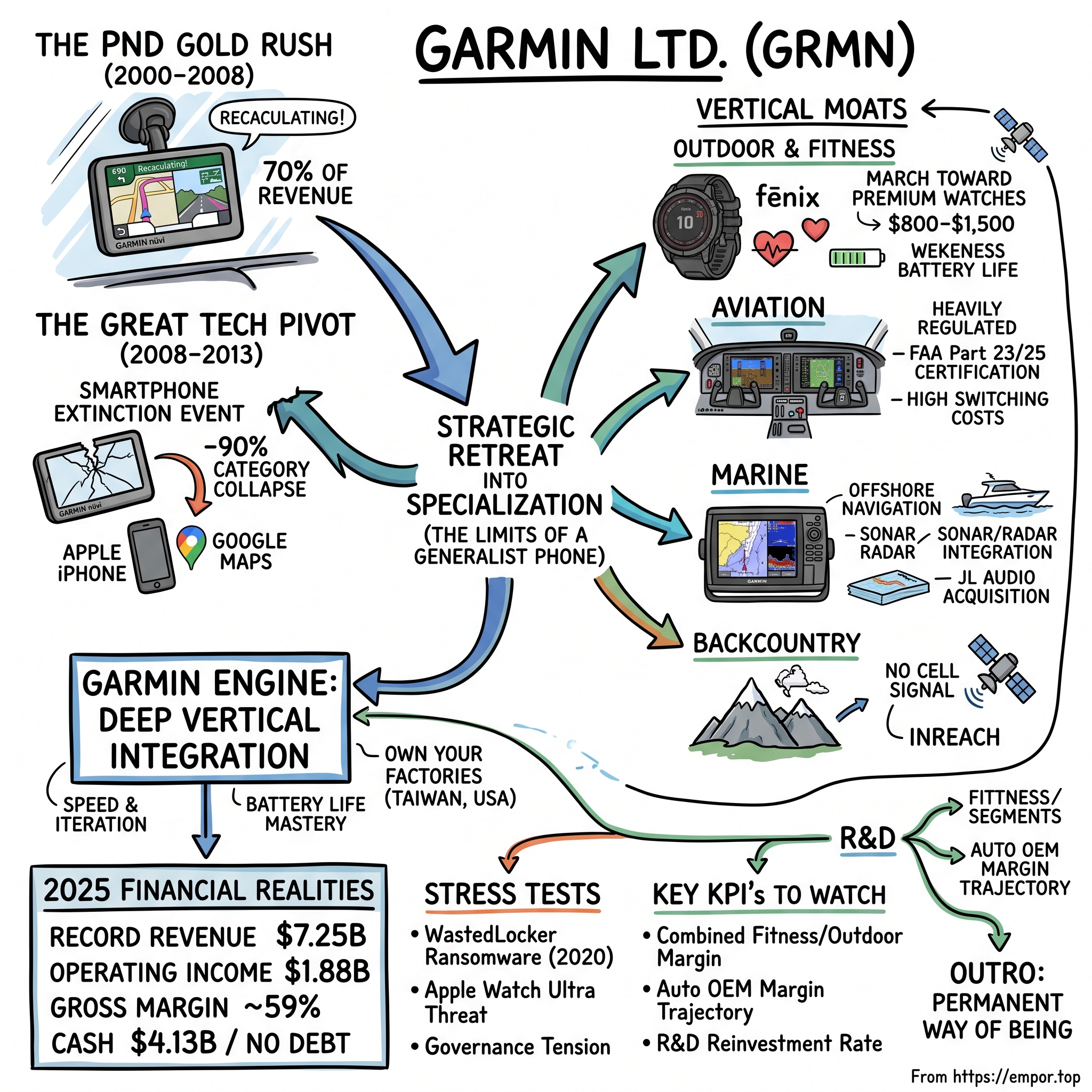

Rewind to the summer of 2008. A Garmin nüvi is stuck to the windshield of what feels like every third car in America, suction-cupped to the glass, chirping "recalculating" at drivers who missed their exit. The company behind it is on top of the world: revenue is barreling toward $3.5 billion, roughly seventy percent of it flowing from a single product category — the portable dashboard GPS unit — and Wall Street is treating Garmin like a growth stock that will own navigation forever. Then, one year earlier and largely unnoticed on the P&L, a man in a black turtleneck had walked onto a stage in San Francisco and held up a phone. Within five years, the category that made Garmin famous would collapse by roughly ninety percent, and the smartphone would give away, for free, the exact product Garmin sold for two hundred dollars.

Here is the part that should not have happened. A hardware company whose flagship business was annihilated by Apple and Google did not die. It did not become a cautionary case study alongside TomTom, Magellan, and Palm. Instead, by fiscal 2025 Garmin posted record consolidated revenue of $7.25 billion, up fifteen percent, and record operating income of $1.88 billion, up eighteen percent, on a gross margin near 59 percent.1 The balance sheet is almost comical in its conservatism: roughly $4.13 billion in cash and marketable securities, zero debt, and about $1.36 billion of free cash flow in a single year.1 This is a consumer-hardware company — the exact business model that every venture capitalist and strategist insists is a low-margin commodity trap — printing software-like margins with no leverage at all.

How? The thesis of this story is deceptively simple, and it runs against the grain of two decades of "the smartphone eats everything" conventional wisdom. Garmin survived because its leadership understood the limits of the general-purpose computer in your pocket. A phone is a magnificent generalist. But it has an eighteen-hour battery, a screen you cannot read in direct sunlight, and an owner who does not want to drop it in the ocean, strap it to a bush plane's instrument panel, or take it forty meters underwater. So instead of fighting Apple and Samsung on the smartphone's home turf — the generalist arena where scale and app ecosystems crush everyone — Garmin retreated into terrain where the phone is weak or absent altogether: elite endurance sport, general aviation cockpits, offshore marine navigation, and the backcountry where there is no cell signal at all. It built a hyper-specialized, deeply vertical moat one niche at a time.

This is a story about the counterintuitive economics of not trying to win the mass market. It is also, uncomfortably for the tidy version, a story with a loss-making segment, a genuine Apple threat at the high end, a ten-million-dollar ransom paid to a sanctioned Russian criminal group, and a governance structure that a certain kind of activist investor would love to pry open. We will get to all of it. But it begins, as these things do, with two engineers who met building avionics and became convinced that a cluster of American military satellites was about to change the world.

II. The Origins of GPS & The Founders' Genesis (1989–1999)

Picture a cubicle farm at AlliedSignal in the mid-1980s, deep inside the Bendix/King avionics division, where a soft-spoken Taiwanese-born electrical engineer named Min Kao sat designing navigation systems for aircraft. Kao had come to the United States for graduate school, earned a PhD in electrical engineering at the University of Tennessee, and drifted into the unglamorous, safety-obsessed world of avionics — a field where a single failed component can kill people, and where "good enough" is not a phrase anyone uses. Down the hall was Gary Burrell, an older, plain-spoken Kansas engineer with decades in the aerospace instrument business. The two men shared a conviction that most of their colleagues thought was premature bordering on crazy: the U.S. government's Navstar Global Positioning System — a constellation of satellites still being launched, still incomplete, still deliberately scrambled for civilian users — was going to become the backbone of all navigation, for everyone, everywhere.

The problem was that no established employer wanted to bet the business on it yet. So in 1989, Burrell and Kao did the thing engineers with a conviction and a mortgage do: they left, and they founded their own company in Lenexa, Kansas. They called it ProNav. When a trademark conflict forced a rename, they built one out of their own first names — Gary and Min — and Garmin was born. It is a useful early tell about the company's personality that its very name is an engineering economy: two inputs, no marketing agency, minimal fuss.

Their first real validation arrived courtesy of a war. In 1991, as the company shipped early GPS receivers, Operation Desert Storm sent American troops into a featureless Iraqi and Kuwaiti desert where conventional maps were useless. Civilian GPS was still degraded by "Selective Availability" — the Pentagon deliberately dithered the public signal so it was accurate only to roughly a football field — but even a rough fix was miraculous in an ocean of sand. The military bought commercial handheld receivers in bulk because it did not have enough of its own, and GPS earned a battlefield reputation for keeping soldiers alive. For a young company selling reliability, there is no better advertisement than "it works when your life depends on it."

Notice what Garmin did not do next. It did not chase the largest, cheapest, most obvious consumer market. It went where failure was unthinkable and standards were brutal: general aviation flight decks and deep-sea marine navigation. These were tiny markets by unit volume, dominated by regulation and certification, where customers would pay real money and switching was painful. That was precisely the point. By cutting its teeth in zero-failure environments, Garmin built two things that would prove far more durable than any single product: a genuine engineering culture obsessed with ruggedness and reliability, and a brand that serious professionals trusted with their lives. Both would matter enormously when the easy money arrived — and the easy money was coming fast, because GPS was about to go mainstream.

III. The PND Gold Rush & The Smartphone Extinction Event (2000–2010)

On December 8, 2000, Garmin went public on the Nasdaq under the ticker GRMN, and the timing could hardly have been better. Selective Availability had been switched off earlier that year, instantly making civilian GPS ten times more accurate, and the cost of GPS chips was falling off a cliff. What followed was one of the great consumer-hardware gold rushes of the 2000s. Garmin's nüvi — a slim, friendly touchscreen box that suction-cupped to your windshield and spoke turn-by-turn directions — became a genuine cultural artifact. "Recalculating," delivered in that patient robotic voice when you blew past a turn, entered the vernacular as a running joke. At the peak in 2008, portable navigation devices drove roughly seventy percent of Garmin's revenue, which had swelled past $3.5 billion, and the company was minting cash.

A quick note on corporate plumbing, because it matters later. Garmin's legal structure migrated over these years — the holding company reincorporated in Switzerland (Cayman Islands first, then a redomestication to Schaffhausen, Switzerland, in 2010) for tax efficiency, while the operational nerve center stayed resolutely in Olathe, Kansas. The result is a company that is Swiss on paper, Kansan in culture, and Taiwanese in manufacturing — a structural quirk that lowers its tax rate and occasionally confuses people about what Garmin actually is.

Then came the comet. In January 2007, Steve Jobs unveiled the iPhone. In 2008 and 2009, Google bundled free turn-by-turn Google Maps Navigation into Android. Overnight, the value proposition of a standalone two-hundred-dollar GPS box evaporated: why buy a single-purpose device when the supercomputer already in your pocket did the same job for free, with live traffic and a map that updated itself? The standalone PND market collapsed by roughly ninety percent over five years. It was an extinction-level event for the category, and how Garmin survived it while rivals did not became a case study in its own right.10 TomTom cratered. Magellan effectively vanished as a serious force. Garmin's stock, which had briefly touched the stratosphere, lost more than eighty percent of its value from peak to trough. Every bear thesis about consumer hardware — that it is a commodity waiting to be disrupted by software — was being proven in real time, on Garmin's own income statement.

Garmin's first instinct was to fight fire with fire, and it produced the company's most instructive failure. In 2009, Garmin partnered with Taiwan's Asus to launch the nüvifone — a GPS-centric smartphone meant to out-navigate the iPhone. It was a disaster. Building a competitive smartphone in the late 2000s was not fundamentally a hardware problem; it was an ecosystem problem — operating systems, app stores, developer relations, carrier deals, the whole modern mobile stack — and a rugged-instrument company from Kansas had no realistic path to matching Apple and Google there. The nüvifone flopped, quietly and expensively. The lesson Garmin's leadership took from it would define the next fifteen years and is worth stating plainly: do not fight a generalist platform on its own ground. The interesting question was where, exactly, to fight instead.

IV. The Great Pivot to Specialization (2010–2020)

The most important thing about Garmin's pivot is that it was engineered by insiders who had lived through the near-death experience, not by a turnaround CEO parachuted in with a slide deck. In 2013, Cliff Pemble became chief executive. Pemble was not a celebrity hire; he was employee number six, hired in 1989 in the company's earliest days, an engineer who had spent his entire career inside Garmin. Co-founder Min Kao stepped up to executive chairman. This is executive continuity of an almost eerie degree, and it produced something rare in a company that had just watched its core business implode: zero strategy drift, no scapegoating, no lurching reinvention. The people who built the ruggedness-and-reliability culture were the same people deciding where to point it next.

The core insight was a mirror image of the nüvifone mistake. If Garmin could not beat the smartphone in the smartphone's world, it would put GPS and sensors where smartphones could not survive — physically, environmentally, and by battery life. That single idea got refracted across four rebuilt businesses.

In the Outdoor and Fitness categories, Garmin essentially invented and then owned the premium multisport watch. The Forerunner line pioneered the GPS running watch and layered on heart-rate and physiological data; the fēnix line, launched in 2012, created a category that barely existed before — the rugged, expensive, weeks-of-battery-life adventure watch aimed not at the casual step-counter but at the ultramarathoner, the mountaineer, the person who is genuinely off-grid. Crucially, Garmin deliberately walked away from the cheap fitness-tracker fight (the Fitbit end of the market that Google would eventually absorb) and toward hardware that sells for $800 to $1,500. It chose margin over volume, enthusiast over mass — the exact opposite of the PND playbook, and a direct response to what the PND collapse had taught them.

In Aviation, Garmin did something a consumer-electronics company almost never manages: it climbed up the value chain into heavily regulated cockpits. Its integrated glass flight decks — the G1000 in general-aviation aircraft, the larger G5000 in business jets — became the systems that aircraft are literally built around. Here the moat is regulatory and physical at once. Certifying avionics under the FAA's Part 23 and Part 25 rules takes years and enormous cost, and ripping a Garmin suite out of a certified airframe to install a competitor's is a six-figure, retraining-intensive ordeal. Switching costs do not get much higher than "requires re-certifying the airplane."

In Marine, Garmin assembled chartplotters, high-definition sonar, radar, and increasingly high-margin integrated systems for leisure boats, buying and building its way to breadth.

The emotional peak of the decade came in 2020, and it was in aviation. Garmin won the Robert J. Collier Trophy — American aviation's most prestigious annual award, whose past recipients include Orville Wright, the crew of Apollo 11, and the designers of the jet engine — for Autoland.5 Autoland is genuinely remarkable technology: if a pilot of a small aircraft becomes incapacitated, a passenger (or the system itself) can press a single button, and the airplane will autonomously pick an airport, navigate to it, communicate its intentions, descend, flare, land, and stop, entirely on its own. For a company that the market had written off a decade earlier as a maker of soon-to-be-obsolete car gadgets, standing in the company of the Wright brothers was a vivid statement of just how far the pivot had carried it — and a hint that the real machine underneath was not any single product, but how Garmin builds things.

V. The Garmin Engine: Deep Vertical Integration

To understand why Garmin's margins look more like a software company's than a gadget maker's, walk (in your imagination) through a factory floor in Taiwan. This is 台灣航電 Garmin Taiwan, the manufacturing heart of the consumer business, and it is the thing that makes Garmin structurally different from almost every consumer-electronics brand you can name. Apple designs in Cupertino and outsources assembly to Foxconn; Fitbit designed and outsourced; the standard modern playbook is to be "asset-light," to own the brand and the software and let someone else run the factories. Garmin does the opposite. It owns its plants. It manufactures its own devices. The regulated avionics, meanwhile, are assembled onshore in the United States — in Kansas and Oregon — precisely because FAA certification demands tight, auditable control over the production line. Garmin is deliberately, unfashionably, vertically integrated — a strategy long-time industry observers have credited as a core, underappreciated source of its manufacturing and margin advantage.11

Why does this matter to an investor rather than an operations nerd? Three concrete reasons, and they compound.

First, speed and iteration. When you design the chip, write the firmware, and run the assembly line under one roof, you can prototype and revise far faster than a company negotiating across a contract manufacturer's wall. New sensors, new watch models, and new sonar units move from idea to shelf on a cadence that outsourced competitors struggle to match.

Second, margin capture. Every contract manufacturer builds in a markup; owning the factory means Garmin keeps that margin instead of paying it out. This is a meaningful part of how the company sustains gross margins near 59 percent and operating margins in the mid-twenties — numbers that are extraordinary for physical hardware and that an outsourced model structurally leaks away.1 It is worth being precise here rather than taking the claim on faith: vertical integration is not automatically superior — it ties up capital in plants and inventory, and it can become a liability if volumes fall. Garmin's version works because its products are high-value and its balance sheet can carry the assets without strain.

Third — and this is the one consumers actually feel — battery life mastery. Because Garmin controls the entire hardware-software stack, it can ruthlessly optimize for endurance. It eschews a heavy general-purpose mobile OS in favor of proprietary, lightweight firmware, and it pairs that with transflective Memory-in-Pixel (MIP) displays. The simple analogy: a normal smartwatch screen is like a television, lit from behind and gulping power; a MIP display is more like an old digital calculator screen — it uses ambient light and sips power, actually getting more readable in bright sun rather than less. Add solar charging lenses on the premium models, and the practical result is a watch measured in weeks of battery life against an Apple Watch's roughly eighteen hours. For the offshore sailor, the multi-day ultramarathoner, or the backcountry hunter, that is not a spec-sheet bragging point; it is the entire reason to buy. Vertical integration, in other words, is not an abstract virtue here — it is the mechanism that produces the specific customer benefit the phone cannot copy, which is exactly what a durable moat is supposed to do.

VI. Hamilton Helmer's 7 Powers & Porter's Five Forces

If you want to know why Garmin's profits have proven so hard to compete away, it helps to run the business through two classic frameworks and ask, at each step, is this real or is it a story management tells itself?

Start with Hamilton Helmer's 7 Powers. The most convincing power Garmin holds is switching costs, and it is concentrated in aviation and marine. Retrofitting a certified cockpit away from Garmin can run well into six figures and requires pilots to retrain on unfamiliar systems; a boat builder who standardizes on Garmin's networked helm faces similar friction. This is not a marketing moat — it is a physical and regulatory one, and it is the reason the aviation and marine cash flows are so defensible.

Next, a partial cornered resource: Garmin's proprietary GPS chip designs, its transflective display and solar-lens technology, and, we will see shortly, the physiological algorithms it bought outright. These are genuinely differentiated, though "cornered" overstates it — competitors have their own sensors and chips; Garmin's edge is integration and refinement, not a resource nobody else can obtain.

Then scale economies, which for Garmin take an unusual shape. The company spends well over a billion dollars a year on R&D and spreads it across five segments that are different on the surface but share deep technological plumbing — GPS, sensors, low-power firmware, mapping, connectivity. A running watch and a chartplotter and a flight deck have more in common under the hood than a customer would ever guess, so a dollar of sensor or battery research pays off in four places at once. That is a real, if medium-strength, advantage.

Finally, brand — high power, and specifically an enthusiast brand. Among triathletes, ultrarunners, private pilots, and boat captains, "Garmin" carries the kind of trust that lets the company charge what enthusiasts half-jokingly call "the Garmin tax" and have it paid willingly. But notice the boundary: this brand power is strong precisely at the hardcore end and thins out toward the casual, mass consumer, where Apple's brand is far stronger. Garmin's brand is a fortress, not an empire.

Now Porter's Five Forces, quickly. Threat of new entrants: near-zero in aviation and marine (regulation, certification, decades of trust) and low-to-moderate in premium wearables (real R&D and proprietary health IP required, but not impossible). Bargaining power of buyers: low, because Garmin sells to highly fragmented customers — millions of individual retail consumers, plus boat and aircraft builders — none of whom can dictate terms. Competitive rivalry: this is the honest split in the whole business. In general aviation, rivalry is muted — it is effectively a duopoly with Honeywell, and Garmin is the aggressor. In consumer wearables, rivalry is intense and rising: Apple's Watch Ultra, plus scrappy specialists like Coros and Suunto, are all pushing directly at Garmin's premium sport franchise. So the frameworks converge on a clear reading: Garmin's moat is deepest where the market is smallest and most regulated, and shallowest where the market is largest and most visible. That tension — defensible niches versus contested consumer growth — is the axis every other section of this story turns on, and it shows up nowhere more clearly than in how Garmin spends its money.

VII. The M&A and Capital Allocation Playbook

There is a certain personality type that a debt-free balance sheet with $4.13 billion of cash reveals, and Garmin's is on full display in how it buys things.1 This is not a company that does transformational, bet-the-farm acquisitions financed with debt and hope. It does small, strategic, cash-funded bolt-ons — and it is unusually disciplined about it. Three deals tell the story.

The most strategically elegant was Firstbeat Analytics, acquired in 2020.6 Firstbeat is a Finnish company whose physiological algorithms — the math that turns raw heart-rate data into "training status," recovery time, stress, and heart-rate-variability insights — were quietly the industry standard, licensed by many of Garmin's own competitors, including Suunto and Polar. By buying Firstbeat outright, Garmin did two things at once: it brought a core piece of its wearables' intelligence in-house (saving licensing fees and controlling the roadmap), and it kicked away the ladder behind it, denying rivals guaranteed future access to the same innovations. That is a textbook example of a small deal with outsized strategic leverage — buying the toll booth your competitors also had to drive through.

Tacx, the Dutch indoor bike-trainer maker, acquired in 2019, is a more cautionary tale — and a more honest one about cyclicality.7 The timing looked inspired when the COVID-19 pandemic sent the entire world indoors and demand for connected bike trainers exploded. But what booms in a lockdown busts afterward: the "indoor bike hangover" of overcapacity and slumping demand followed, and Garmin had to manage the down-cycle without letting it damage corporate margins. It is a useful reminder that even a disciplined acquirer inherits the cyclical demand of the thing it buys, and that a good deal at one point in the cycle can look expensive at another.

The JL Audio acquisition in 2023 rounds out the marine ecosystem, bringing premium audio into Garmin's boats.8 Garmin did not publicly disclose the financial terms, stating only that they would not be released — a reminder that even a transparent company keeps some cards close. The FY2023 statement of cash flows implied cash consideration of roughly $150 million for the year's acquisitions, and market observers attributed the bulk of it to JL Audio; regardless of the precise figure, the pattern is the point. Garmin paid cash off its own balance sheet, issued no dilutive stock, and folded a respected brand into a segment where it already had distribution. Across all three deals the discipline rhymes: buy capability or a strategic chokepoint, pay in cash, avoid leverage, and keep every acquisition small enough that a mistake is survivable. The result of that conservatism is a segment-level portfolio worth examining one business at a time — because the aggregate numbers hide as much as they reveal.

VIII. Segment-Level Deep Dive & 2025 Financial Realities

Underneath the tidy $7.25 billion headline are five very different businesses, and 2025 was the year the internal center of gravity visibly shifted. For years the story was "Outdoor is the cash machine." In 2025, the running watch business quietly took the crown.

Fitness became Garmin's largest segment, posting roughly $2.36 billion in net sales — up a striking 33 percent — with operating income around $726 million at about a 31 percent margin, and operating profit growing roughly fifty percent year over year.13 The driver is the "everyday smartwatch" pushing beyond the hardcore athlete: the Venu line and accessible running trackers pulling in mainstream buyers who want Garmin's health data without a $1,000 fēnix. The analytical read is that Garmin has found genuine demand below its enthusiast core without cannibalizing it — a rare feat, and the single most important growth engine in the company right now.

Outdoor — the former king — generated about $2.05 billion in net sales, up 5 percent, with operating income near $690 million at roughly a 34 percent margin: the highest-margin business in the portfolio.13 These are the premium adventure watches (fēnix, epix, tactix) at $800–$1,500 price points, and their profitability is the clearest proof that the "sell margin, not volume" strategy works. The slower growth versus Fitness also tells you something: the enthusiast market is maturing, and future upside depends more on defending price than on adding customers.

Aviation delivered roughly $987 million in net sales, up 13 percent, with operating income around $257 million at about a 26 percent margin.13 This is secular, defensible growth — general-aviation upgrades, Autoland adoption, and the switching-cost moat doing exactly what it is supposed to. It is the segment that anchors the whole enterprise in a downturn.

Marine came in near $1.18 billion, up 10 percent, with operating income around $251 million at roughly a 21 percent margin — the lowest margin of the four profitable segments, and no accident.13 Marine is an ecosystem play (chartplotters, radar, the Force trolling motors, now JL Audio audio) with high customer stickiness, but it is also directly exposed to the economics of leisure boating, which swings hard with consumer confidence and interest rates.

And then there is Auto OEM, the segment that would give an activist heartburn. It posted about $665 million in net sales, up 9 percent — but an operating loss of roughly $49 million, a negative 7 percent margin.13 Every other segment funds this one. Management's framing, delivered on the Q4 2025 earnings call, is that Auto OEM is an investment phase, not a broken business: the segment is absorbing heavy upfront R&D and engineering to build embedded systems — domain controllers and infotainment — for automakers.2 The near-term revenue is driven by BMW domain-controller programs that management expects to peak in 2026, and the real prize is a large next-generation infotainment program with Mercedes-Benz slated to launch in 2027, which the company argues will finally carry the segment to profitability.2 An investor should treat that as a claim to be tested, not a fact. The bull reading is optionality: a foothold in automotive compute that could become a major franchise. The bear reading is that this is a structurally low-margin, capital-hungry business selling to powerful buyers (automakers, who have enormous bargaining leverage — the exact opposite of Garmin's fragmented consumer base), and that "profitable in 2027" is precisely the kind of receding horizon that deserves skepticism until the Mercedes revenue actually shows up. Which segment you weight more tells you a lot about how you'd underwrite the whole company — and it sets up the harder questions about what could break the case.

IX. Stress Test: Cybersecurity, Apple's Threat, & Governance

On July 23, 2020, Garmin's world went dark. Garmin Connect — the cloud service syncing millions of watches — went offline. So did aviation services like flight-plan filing, call centers, and even production lines. The culprit was WastedLocker, a strain of ransomware attributed to the Russian criminal group Evil Corp, which had encrypted Garmin's systems and demanded payment for the decryption key.9 For roughly five days, one of the world's premier navigation companies could not navigate its own operations.

What happened next is where the story gets uncomfortable. Multiple reports indicated Garmin ultimately obtained a decryptor after a ransom in the neighborhood of $10 million was paid, reportedly routed through a third party.9 This was not merely a large check; it was a legal and ethical minefield, because the U.S. Treasury had sanctioned Evil Corp, and paying a sanctioned entity can itself violate the law. Garmin has been characteristically tight-lipped about the specifics. The strategic lesson the company appears to have absorbed is architectural: a hardware ecosystem that depends on a central cloud is only as reliable as that cloud, and since then Garmin has leaned harder into robust offline on-device mapping and functionality, reducing the systemic risk of a single point of failure. For investors, the episode is a permanent reminder that a connected-device business carries connected-device risk, and that Garmin's disclosure instinct is to say as little as legally possible.

The second stress test is competitive, and it wears an Apple logo. The Apple Watch Ultra is a direct assault on Garmin's premium Outdoor turf — a rugged, expensive, adventure-positioned watch from the most powerful consumer brand on earth. Can it erode Garmin's franchise? The honest answer is: at the edges, yes; at the core, not easily. Garmin's defenses are concrete rather than rhetorical — multi-week battery life against Apple's single day, a specialized developer ecosystem in Connect IQ, solar charging, genuine ruggedness, and decades of trust among people whose hobbies can kill them. Apple wins the mainstream "smartwatch that also does fitness" buyer handily. Garmin wins the person for whom the watch is a piece of safety equipment. The strategic vulnerability is the seam between them: the aspirational enthusiast who could go either way, and whom Apple can subsidize into its ecosystem. Garmin cannot get complacent about the high end, because that is the one place a trillion-dollar competitor is actually pointed at it.

The third stress test is governance, and it is the one a real activist would fixate on. Look at the setup through a skeptical long/short lens: a company with a loss-making Auto OEM segment that could be spun off, and $4.13 billion of idle cash that could be levered up and returned to shareholders far more aggressively. Why has no activist forced the issue? The answer is ownership structure. Executive Chairman Min Kao personally controls roughly 9–10 percent of the company — on the order of 18 to 19 million shares — a stake large enough to make a hostile campaign extraordinarily difficult, and it aligns his personal fortune with long-term outcomes rather than quarterly ones.4 CEO Cliff Pemble is a deeply aligned lifer. The board is, in effect, structurally insulated from short-term pressure. The bull case for this insulation is that it is exactly what let Garmin make patient, decade-long R&D bets and survive the PND collapse without being forced into value-destroying panic moves. The bear case is that the same insulation lets management keep funding a money-losing segment and sitting on a mountain of low-returning cash without ever having to answer a determined outside challenge. Both are true at once. That unresolved tension — patient stewardship or unaccountable comfort? — is the real governance question, and it leads directly to what an investor should actually watch.

X. The Investor Playbook & Key KPIs to Watch

Strip away the narrative and the question for a long-term investor becomes concrete: what handful of numbers actually tells you whether the Garmin thesis is intact or breaking? Not the twenty metrics in the earnings deck — three.

The first is the combined Fitness and Outdoor operating margin. Together these two segments are the profit engine and the front line against Apple, Coros, and Suunto. As long as their blended operating margin holds above roughly thirty percent, it signals that Garmin still has pricing power at the premium end and that competition has not forced it into a discounting war. A sustained downward drift would be the earliest, clearest sign that the "Garmin tax" is eroding — that the enthusiast moat is being commoditized. This is the vital sign to watch above all others.

The second is the Auto OEM margin trajectory. This is the "show me" metric. Management has staked credibility on the segment turning profitable as BMW peaks in 2026 and Mercedes-Benz launches in 2027.2 An investor does not need to forecast it — just track it quarter by quarter and see whether the loss narrows on schedule. If it does, the optionality was real and the market gets a new growth franchise roughly for free. If the losses persist past the promised inflection, it becomes evidence that management's guidance discipline has slipped, and the spin-off/activist conversation gets a lot louder.

The third is the R&D reinvestment rate — R&D as a percentage of sales, historically running in the mid-teens. This is the lifeblood of a company whose entire strategy is out-engineering generalists in specialized niches. If that ratio quietly falls, it may flatter near-term margins, but it would be management borrowing from the future — starving the innovation pipeline that is the whole point of the business. Watching it is how you check that Garmin is still playing the long game it claims to play.

Behind those three numbers sit three durable lessons this story leaves for investors, worth stating plainly. First, the power of the niche: you do not have to win the mass market to build a great business — under-the-radar niches can be larger, stickier, and far more profitable than anyone expects, and being unglamorous is a feature, not a bug. Second, vertical integration is not dead: in the right hands, owning your factories delivers speed, quality, and margin protection that the asset-light orthodoxy simply cannot replicate — though it demands a balance sheet strong enough to carry the assets through a downturn. Third, cash is a strategic weapon: staying debt-free with billions in reserve is what let Garmin survive a category extinction and buy strategic assets like Firstbeat on its own terms — the same conservatism that frustrates activists is what bought the company its second life.

XI. Outro

The tidy version of the Garmin story — company gets disrupted, pivots brilliantly, prints cash forever — is true enough to be inspiring and incomplete enough to be dangerous. The fuller version is more interesting. Two avionics engineers built a culture obsessed with reliability, rode a GPS gold rush to the top, watched their core business get vaporized by the smartphone, made one instructive failure trying to fight on the disruptor's turf, and then executed one of the great strategic retreats in modern corporate history — not by finding a bigger market, but by finding the terrain where the world's most powerful generalist computer is weak. They did it with the same people, the same balance-sheet conservatism, and the same engineering-first temperament they started with.

What makes Garmin worth studying is not that the pivot is finished, but that the same forces are still in tension today. The enthusiast moat is deep but bordered by a trillion-dollar competitor. The vertically integrated engine throws off extraordinary margins but ties up capital that a raider would rather see returned. The founder-aligned governance that enabled patient, contrarian bets is the same structure that lets a loss-making segment and a cash mountain sit unchallenged. Garmin has earned the benefit of the doubt through two decades of doing what it said it would do — but the whole point of an independent read is that credibility is a reason to watch closely, not a reason to stop watching. The next chapters — whether Auto OEM ever earns its keep, whether the Garmin tax survives the Apple onslaught, whether all that cash gets deployed as shrewdly as it was hoarded — are the ones that will decide whether the great pivot was a one-time escape or a permanent way of being.

References

-

Garmin announces fourth quarter and fiscal year 2025 results — Garmin Newsroom, 2026-02-18 ↩↩↩↩↩↩↩↩↩

-

Garmin Ltd. Q4 2025 Earnings Call Transcript — Garmin Investor Relations, 2026-02-18 ↩↩↩

-

Garmin announces fourth quarter and fiscal year 2025 results — PR Newswire, 2026-02-18 ↩↩↩↩↩

-

Garmin Ltd. Notice and Proxy Statement 2026 — Garmin Ltd., 2026-04-22 ↩

-

Garmin Wins Prestigious Robert J. Collier Trophy for Autoland — National Aeronautic Association, 2021-06-03 ↩

-

Garmin Acquires Firstbeat Analytics, a Leading Provider of Physiological Analytics — Garmin Press Room, 2020-06-30 ↩

-

Garmin Acquires Indoor Cycling Specialist Tacx — Garmin Press Room, 2019-02-12 ↩

-

Garmin Completes Acquisition of JL Audio — Garmin Newsroom, 2023-09-20 ↩

-

Inside Garmin's 2020 Ransomware Attack and WastedLocker Ransom — Reuters, 2020-07-27 ↩↩

-

How Garmin Navigated the Smartphone Disruption — Bloomberg, 2021-08-12 ↩

-

Garmin's Vertical Integration Moat and Manufacturing Strategy — DC Rainmaker, 2022-04-15 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube