Grab Holdings: Southeast Asia's Super App Empire

I. Introduction & Episode Roadmap

Picture this: It's 2011, and two MBA students at Harvard Business School are watching a classmate struggle to find a safe taxi in Cambridge. The classmate, frustrated, turns to Anthony Tan and says, "You guys are from Malaysia—why is your taxi system so terrible?" That moment of embarrassment would spark the creation of what would become Southeast Asia's first decacorn and the biggest technology startup in the region.

The story of Grab isn't just another Silicon Valley-style disruption narrative transplanted to Asia. It's a masterclass in hyperlocal adaptation, a tale of how two unlikely co-founders—one from automotive royalty, the other from a middle-class engineering background—built a $40 billion empire by solving a deeply personal problem: making transportation safer in Southeast Asia.

Today, Grab Holdings Inc. is a multinational technology company headquartered in One-North, Singapore, operating a super-app for ride-hailing, food delivery, and digital payment services on mobile devices. But to understand how a Harvard Business School project became the operating system for daily life across eight countries and 500 cities, we need to start at the beginning—with monsoon rains, family legacies, and a profound sense of duty to solve real problems for real people.

The themes that will emerge throughout this story are profound: How do you beat Uber at its own game in its most ambitious international market? Can you build a profitable super app in emerging markets where credit card penetration is below 10%? And perhaps most importantly—what happens when your closest competitor is also your best friend?

II. Origins & The Harvard Business School Genesis (2009-2012)

The origin story of Grab begins not in a Silicon Valley garage, but in the legacy-laden boardrooms of Malaysian automotive royalty. Anthony Tan was born in Kuala Lumpur, Malaysia, his father Tan Heng Chew serving as president of Tan Chong Motor, a Malaysian manufacturing company that assembles and distributes Nissan vehicles in Southeast Asia. His great-grandfather was a taxi driver and his grandfather pioneered the Japanese automotive industry in Malaysia.

Growing up, Anthony wasn't sheltered from the family business. He worked on the assembly line at his father's company and attended meetings with union bosses at a young age. This early exposure to both the executive suite and the factory floor would prove invaluable—he understood transportation not as an abstract market opportunity, but as a visceral, physical business that touched millions of lives daily.

Meanwhile, across town in Petaling Jaya, Tan Hooi Ling grew up in a middle-class household in a semi-detached house, her father a civil engineer and mother a remisier. Her path to Harvard was more conventional—showing early aptitude for mathematics and science, she pursued a degree in mechanical engineering from the University of Bath—but her motivations for revolutionizing transportation were deeply personal.

"I felt constrained and I could never really go where I wanted to because I was afraid of taxi drivers—I really was, and even when I wasn't, my parents were [for me]," she recalled. Her mother's fears over her safety on late night journeys prompted her to update her with taxis' licence plate numbers and distance from home. This was before the proliferation of GPS-enabled smartphones—Hooi Ling was essentially running a manual tracking system with her mother as the operations center.

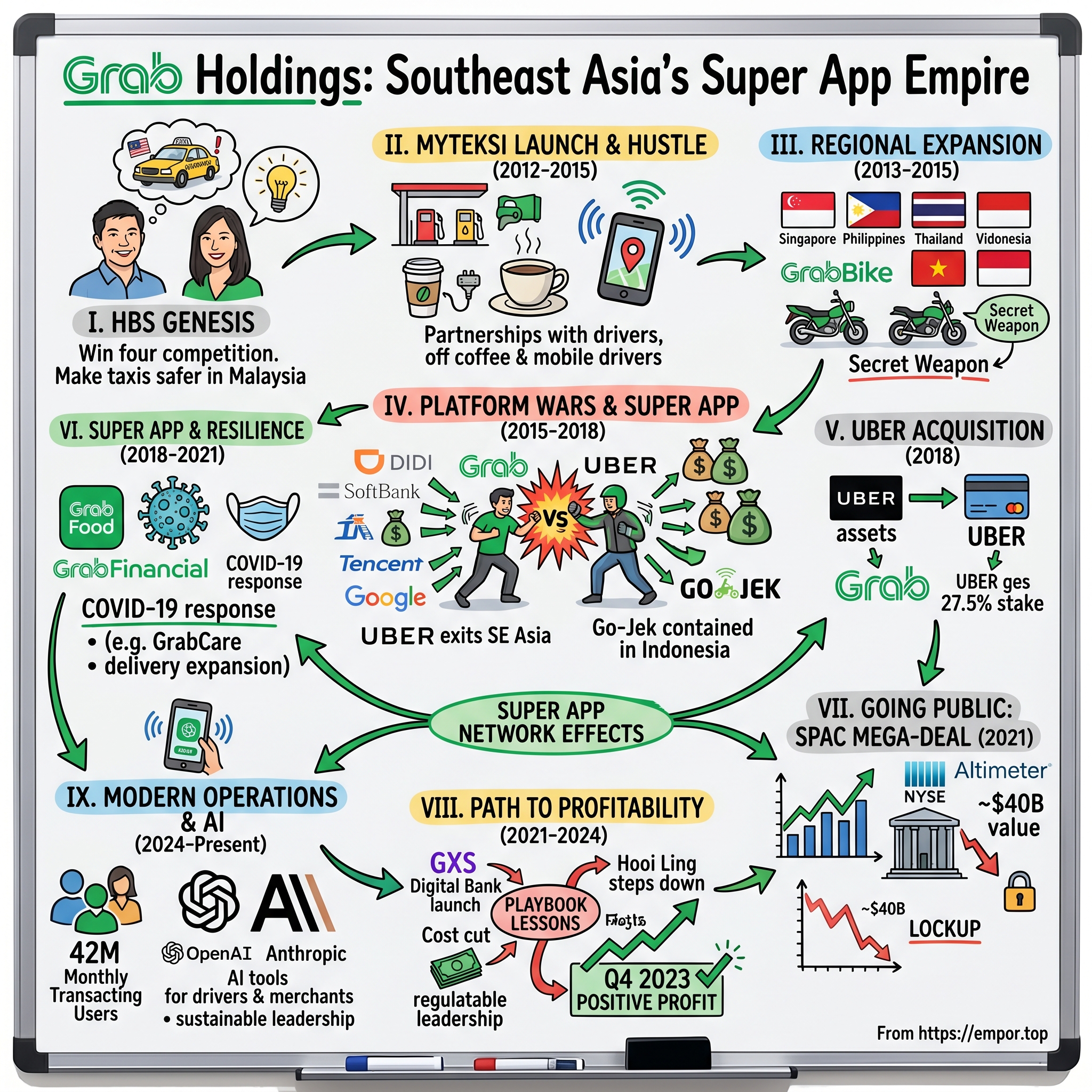

The two Tans (no relation, despite the shared surname) met at Harvard Business School in 2009, where fate—or perhaps the alphabetical seating arrangement—brought them together. While attending Harvard Business School, Tan partnered with classmate Tan Hooi Ling on making taxis safer in Malaysia, partly due to its ranking as having the worst cab service in the world. They wrote a business plan for a taxi booking app, which won second prize at the HBS New Venture Competition in 2011.

The business plan was born from that moment of shame when their classmate criticized Malaysian taxis, but it addressed a real crisis. In Malaysia, stories of taxi-related robberies and assaults were common. The lack of accountability—no tracking, no digital records, cash-only transactions—created an environment where both passengers and reputable drivers suffered.

Using the $25,000 of prize money from the competition, their own personal funds and an investment from Anthony's mother, the duo launched MyTeksi in June 2012 with headquarters in Kuala Lumpur. But launching was just the beginning of their challenges.

Anthony faced a choice that would define not just his career, but the company's culture: join the family business or pursue this uncertain startup. The expectations were immense—he was groomed from childhood to take over Tan Chong Motor. Yet he chose the harder path, driven by a belief that technology could solve problems his family's traditional business couldn't touch.

Hooi Ling faced her own crossroads. Although the pair had started the company, Tan had to return to McKinsey after graduation to serve out her bond with the consulting firm as a condition of sponsoring her education. She later moved to San Francisco-based software company Salesforce, while taking time out of her schedule to help Anthony with Grab in Southeast Asia. She returned to work full-time on Grab in 2015.

This geographic and professional separation in the early years would prove both a challenge and an unexpected advantage—it forced Anthony to build a leadership team and operational discipline from day one, while Hooi Ling's continued involvement from afar brought Silicon Valley perspectives and networks that would prove crucial when the global ride-hailing wars began.

III. Early Years: Building MyTeksi & Regional Expansion (2012-2015)

The early days of MyTeksi were defined by pure hustle and a deep understanding that Southeast Asia wasn't Silicon Valley. Anthony Tan would spend his days going from gas station to gas station, buying coffee for taxi drivers, sitting with them for hours to understand their concerns. "Manual GPS system" became "digital accountability"—but the human touch remained paramount.

The company's first major innovation wasn't technological—it was social. Instead of trying to disrupt taxi drivers (Uber's approach), MyTeksi partnered with them. They positioned the app not as a threat to traditional taxis but as a tool to help honest drivers get more business while avoiding dangerous passengers. Safety was a two-way street.

GrabTaxi expanded to the Philippines in August 2013, and to Singapore and Thailand in October of the same year. Each market required careful recalibration. In the Philippines, they had to navigate complex regulations and a fragmented taxi ecosystem. In Singapore, they faced a sophisticated market with high service expectations. In Thailand, they encountered initial regulatory resistance but massive consumer demand.

In 2014, GrabTaxi further continued its growth and expansion to new countries: first launching in Sai Gon, Vietnam, in February, and Jakarta in Indonesia in June. Vietnam would prove to be a crucial testing ground for what would become one of Grab's most important innovations.

In November 2014, GrabTaxi launched its first GrabBike service in Sai Gon as a trial service. By 2015, GrabBike's motorcycle service rides had spread throughout Vietnam and Indonesia. This wasn't just adding another vehicle type—it was recognizing a fundamental reality of Southeast Asian transportation. In cities like Jakarta and Ho Chi Minh City, motorcycles weren't just convenient; they were essential. Traffic moved differently, commerce operated differently, and Grab adapted accordingly.

The motorcycle services would become Grab's secret weapon against Uber. While Uber struggled to adapt its four-wheel-focused model to Southeast Asian realities, Grab was building a multi-modal transportation platform that matched how people actually moved through these cities. A Bangkok office worker might take GrabBike to avoid morning traffic, GrabCar for a client meeting, and GrabTaxi for a family dinner—all through one app, one wallet, one account.

During this period, while Anthony was building operations across Southeast Asia, Hooi Ling maintained her unique position—officially employed elsewhere but deeply involved in strategic decisions. She played a crucial role in establishing Grab's operations in these countries, leveraging her consulting background to navigate complex regulatory and logistical challenges. Her McKinsey training proved invaluable in structuring expansion plans, analyzing market entry strategies, and building the financial models that would attract serious venture capital.

By the end of 2015, Grab (having dropped "Taxi" from its name to reflect broader ambitions) was operating in six countries with thousands of drivers. But this was just the pre-game warm-up. The real battle was about to begin, as Uber, flush with billions in venture funding, set its sights on conquering Southeast Asia.

IV. The Platform Wars: Grab vs Uber vs Go-Jek (2015-2018)

By 2016, it was rebranded as Grab with an expansion of partnerships in Southeast Asia that coincided with the development of products for couriers. The name change signaled something profound: this was no longer about taxis or even transportation—it was about building the operating system for Southeast Asian commerce.

The platform wars that erupted from 2015 to 2018 were unlike anything the tech world had seen. This wasn't just competition—it was total war, with billions of dollars in subsidies, aggressive recruitment tactics, and a winner-take-all mentality that would leave only one regional champion standing.

Uber entered Southeast Asia with its standard playbook: premium service, credit card payments, and massive subsidies to gain market share. They had conquered markets from New York to London with this approach. Southeast Asia, they assumed, would be no different.

But Grab understood what Uber didn't—or perhaps, what Uber was too rigid to adapt to. While Uber insisted on credit card payments, Grab accepted cash, recognizing that in markets where banking penetration was below 30%, cash was still king. While Uber paid drivers bi-weekly, Grab paid daily, understanding that many drivers lived paycheck to paycheck. These weren't just features—they were fundamental recognitions of local economic realities.

The competition with Go-Jek added another dimension. Started as a motorcycle taxi call center in Indonesia in 2010, Go-Jek had transformed into a super app by 2015, offering everything from ride-hailing to food delivery to massage services. The rivalry between Anthony Tan and Go-Jek's founder Nadiem Makarim became personal—they had once been friends, bonding over their shared vision of solving Southeast Asian problems. Now they were locked in an existential battle for regional dominance.

The capital arms race was staggering. SoftBank, recognizing the strategic importance of Southeast Asia, invested in both Grab and Uber globally, essentially betting on all horses. Didi Chuxing, fresh from defeating Uber in China, invested in Grab as a proxy war against their former opponent. Google backed Go-Jek, while Tencent supported both Go-Jek and Grab. It was a complex web of alliances and competitions that would make Game of Thrones look straightforward.

The human cost was real. Drivers played platforms against each other for better incentives. Consumers enjoyed artificially low prices subsidized by venture capital. But underneath, all three companies were burning cash at unsustainable rates. Something had to give.

By early 2018, Uber was reportedly losing $2 million per day in Southeast Asia. Despite having 25% market share regionally, they were a distant third in crucial markets like Indonesia. The new Uber CEO, Dara Khosrowshahi, faced pressure to stem losses ahead of an eventual IPO. For Grab, the war was existential—Southeast Asia was their only market. For Uber, it was one of many fronts in a global campaign.

V. The Uber Acquisition: Southeast Asia's Biggest Deal (2018)

In March 2018, Grab merged with Uber's Southeast Asian operations. As part of the acquisition, Grab took over Uber's assets and operations, including Uber Eats in Malaysia, Singapore and Thailand. The announcement on March 26, 2018, sent shockwaves through the tech world.

In exchange, Uber will get a 27.5 percent stake in Singapore-based Grab while Uber CEO Dara Khosrowshahi will join Grab's board. For Uber, the 27.5% stake in Grab, worth close to $1.6 billion, represented a strong return on Uber's $700 million investment in Southeast Asia.

The deal's structure revealed sophisticated financial engineering. As part of the deal, Grab has to go public by 2023 or pay Uber $2 billion—a clever mechanism ensuring Uber would eventually liquidate its stake at a favorable valuation.

Around 500 Uber employees in Southeast Asia would move over to Grab, bringing valuable operational expertise but also integration challenges. The cultural differences between Uber's Silicon Valley approach and Grab's Southeast Asian ethos would require careful management.

Grab said that Uber's ride-sharing app would be available for a further two weeks, while Uber Eats would close down and migrate to GrabFood at the end of May. The rapid transition demonstrated Grab's operational readiness—they had been preparing for this moment.

The regulatory response was swift and varied. Singapore and Philippines competition authorities extended Uber app operations to ensure market stability. Indonesia, Thailand, and Vietnam launched investigations into potential anti-competitive behavior. But the deal's strategic logic was compelling—ending a destructive subsidy war that benefited no one long-term.

In May 2018, Grab launched GrabFood food delivery service. In October 2018, Grab launched GrabExpress courier service. The Uber acquisition had given Grab the market dominance and operational bandwidth to rapidly expand beyond ride-hailing. The super app vision was becoming reality.

For Anthony Tan and Hooi Ling Tan (who had finally returned full-time in 2015), this was vindication of their localization strategy. They had defeated the world's most valuable startup not through superior technology or more capital, but through deeper understanding of their markets. As Anthony would later say, "We didn't win because we were better at being Uber. We won because we were better at being Southeast Asian."

VI. Building the Super App: Beyond Ride-Hailing (2018-2021)

With Uber vanquished and Go-Jek contained primarily to Indonesia, Grab embarked on its most ambitious phase: building a true super app that would be indispensable to Southeast Asian daily life.

In 2018, Grab also launched Grab Financial, a financial arm of the company. This wasn't just about adding payment features—it was about banking the unbanked, providing financial services to millions who had never had a credit card or formal bank account.

The expansion into new verticals came rapidly. In February 2019, the company launched GrabPet in Singapore for pet transportation. GrabKitchen cloud kitchens launched across six countries, reaching 50 locations within a year. Each new service strengthened the ecosystem—more reasons to open the app, more transactions, more data, deeper engagement.

Then came COVID-19.

The pandemic could have destroyed Grab. Mobility demand collapsed overnight as lockdowns swept across Southeast Asia. But crisis revealed character, and Grab's response showed how deeply embedded it had become in the region's infrastructure.

In April 2020, top management salaries were cut by 20 percent and employees encouraged to take voluntary no-pay leave. In June 2020, Grab retrenched 360 employees, just under 5 percent of total headcount. These were painful but necessary decisions to preserve cash and protect the company's long-term viability.

But Grab also innovated through the crisis. In February 2020, Grab launched GrabCare for healthcare workers in Singapore, providing 24-hour services to Tan Tock Seng Hospital and National Centre for Infectious Diseases. Grab expanded GrabMart and GrabAssistant services to more cities to meet increased demand for online food and grocery deliveries.

The pandemic accelerated digital adoption by years. Consumers who had never ordered food online became regular GrabFood users. Small businesses that had resisted digital payments were forced to adapt. Grab, positioned at the center of this digital transformation, saw its relevance increase even as its ride-hailing business suffered.

By late 2020, there were signs of recovery and renewed ambition. In December 2020, Grab was granted a digital bank licence from Singapore together with Singtel, winning one of only two digital full bank licenses from the Monetary Authority of Singapore. This wasn't just another vertical—it was the foundation for Grab's next decade of growth.

VII. Going Public: The SPAC Mega-Deal (2021)

On April 13, 2021, Grab announced it intended to go public in the U.S. through a partnership with Altimeter Growth Corp. The combined company was expected to have an equity value on a pro-forma basis of approximately $39.6 billion. That's more than twice the roughly $16 billion the firm was last privately valued at, and would mark the biggest-ever deal with a SPAC.

The SPAC structure was unconventional for a Southeast Asian company but strategically brilliant. It provided certainty on valuation, faster time to market, and the ability to make forward-looking statements about growth—crucial for a company whose story was about future potential rather than current profitability.

At closing, the combined company expected to receive approximately $4.5 billion in cash proceeds, including more than $4.0 billion from a fully committed PIPE offering. The investor roster read like a who's who of global finance: BlackRock, Fidelity, T. Rowe Price, Abu Dhabi sovereign wealth fund Mubadala, and Singapore investment arm Temasek.

But Grab's SPAC had a crucial difference: The shares acquired by Altimeter would be subject to a three-year lockup period, significantly longer than typical SPAC transactions. This signaled long-term confidence and alignment—Altimeter wasn't looking for a quick flip.

December 2, 2021, should have been a day of celebration. Instead, it turned into a sobering reminder of public market realities. Grab's shares fell 21% on the first day of trading, closing at $8.67, well below the $10 SPAC reference price. The broader SPAC market had soured, tech valuations were under pressure, and investors were increasingly focused on profitability over growth.

The founder wealth creation was still substantial—Anthony Tan's stake was worth $829 million, Hooi Ling's $256 million—but the poor debut highlighted the challenges ahead. Grab was now playing by public market rules: quarterly earnings calls, analyst scrutiny, and the relentless pressure for profitability.

VIII. The Path to Profitability & Digital Banking (2021-2024)

The public market debut's disappointment catalyzed a fundamental shift in Grab's strategy. Growth at all costs was out; sustainable, profitable growth was in.

GXS Bank launched in August 2022 after securing the digital full bank license from MAS in 2020. GXS owns one of the two Digital Full Bank licenses issued by MAS, backed by a consortium consisting of Grab Holdings. This wasn't just another product launch—it was the culmination of Grab's financial services ambitions.

The path to profitability required difficult decisions. In June 2023, Grab announced an 11 percent reduction of its workforce. In May 2023, Hooi Ling Tan announced she would step down as COO by the end of 2023—a significant transition as one of the co-founders stepped back from daily operations.

But beneath the cost-cutting, fundamental improvements were taking shape. Take rates were increasing as Grab reduced subsidies. Driver and merchant retention remained strong despite lower incentives. The super app ecosystem was generating network effects—users who used multiple services had higher retention and lifetime value.

Then came the historic moment: Q4 2023 Profit for the period was positive at $11 million, with Revenue growing 30% year-over-year to $653 million and Adjusted EBITDA improving to $35 million. After years of losses, Grab had finally turned profitable.

"2023 was a pivotal year for us. We generated over $11 billion of earnings for our partners, achieved strong top-line growth as we exited the year with Mobility GMV above pre-COVID levels and Deliveries GMV growth re-accelerating, while also reaching Adjusted EBITDA profitability," said Anthony Tan.

The momentum continued. In February 2024, Grab announced a $500 million share buyback program—a signal of confidence and financial strength. The company also announced it would repay its Term Loan B facility, reducing interest expenses and improving future profitability.

Through 2024, profitability gains accelerated. In Q3 2024, the company achieved a profit of $15 million and record Adjusted EBITDA of $90 million, marking its eleventh consecutive quarter of improvement. Monthly Transacting Users reached 42 million, demonstrating that Grab could grow users while maintaining profitability.

IX. Modern Operations & AI Integration (2024-Present)

As Grab entered 2025, it was no longer a startup fighting for survival but an established platform exploring new frontiers of growth and efficiency.

GrabCab received a 10-year street-hail operator licence from Singapore's Land Transport Authority in 2025, becoming the sixth taxi operator in the country. This full-circle moment—from disrupting taxis to becoming a licensed taxi operator—demonstrated Grab's evolution from disruptor to incumbent.

In April 2025, Grab released AI Merchant Assistant and AI Driver Companion, two AI-based tools developed with OpenAI and Anthropic. The former offers business insights to merchants while the latter provides predictive analytics for high-demand areas and voice reporting to drivers. These weren't just tech experiments but practical tools addressing real pain points—helping merchants optimize inventory and pricing, enabling drivers to maximize earnings through better positioning.

The scale of Grab's operations by 2025 was staggering. With 42 million Monthly Transacting Users, Grab was processing millions of transactions daily across eight countries, generating vast amounts of data that could be leveraged for better matching algorithms, fraud detection, and service optimization.

The competitive landscape had also evolved. Go-Jek, now merged with Tokopedia to form GoTo, remained formidable in Indonesia but hadn't successfully expanded regionally. Sea Limited's Shopee competed in e-commerce and digital payments but lacked Grab's transportation network. Regional players like Foodpanda (owned by Delivery Hero) competed in food delivery but lacked Grab's ecosystem breadth.

Grab's focus shifted to what Anthony Tan called "sustainable leadership"—maintaining market position while improving unit economics. This meant fewer flashy announcements and more operational excellence: reducing driver wait times by seconds, improving delivery accuracy by percentage points, increasing loan approval rates while maintaining credit quality.

X. Playbook: Business & Investing Lessons

The Grab story offers profound lessons for entrepreneurs and investors navigating emerging markets:

Localization Beats Standardization Grab's victory over Uber demonstrated that in diverse, complex markets, deep local understanding trumps global scale. Every market in Southeast Asia required different approaches—motorcycles in Vietnam, regulatory partnerships in Singapore, cash payments in the Philippines. Grab's willingness to build different products for different markets, while maintaining a unified platform, proved decisive.

The Super App Paradox Super apps work in markets with specific characteristics: large unbanked populations, mobile-first internet adoption, and regulatory environments that allow cross-vertical expansion. Grab succeeded because Southeast Asia had all three. The same strategy would likely fail in the US or Europe, where specialized apps dominate and regulatory boundaries are stricter.

Network Effects in Multi-Sided Marketplaces Grab built reinforcing network effects across multiple dimensions. More drivers attracted more riders, which attracted more drivers. But crucially, food delivery drivers could also do package delivery, ride-hailing customers became food ordering customers, and payment users became lending customers. Each new service strengthened existing ones.

Capital Intensity and Path to Profitability Grab burned through billions before achieving profitability—a luxury few startups have. But they used that capital strategically: to build market dominance before focusing on unit economics. The key insight: in winner-take-all markets, achieving dominant position first, then optimizing for profitability, can be the right sequence—if you have patient capital.

Managing Regulatory Complexity Operating across eight countries meant navigating eight different regulatory regimes, each with unique requirements and political considerations. Grab's approach—partnering rather than disrupting, employing local government relations teams, adapting to rather than fighting regulations—proved more sustainable than Uber's more confrontational approach.

XI. Analysis & Bear vs Bull Case

Bull Case: The Platform Powerhouse The optimists see Grab as Southeast Asia's answer to Amazon—an indispensable platform that touches every aspect of digital life. With profitability achieved and record Adjusted EBITDA of $90 million in Q3 2024, the financial trajectory is compelling. The digital banking opportunity could be transformative—Southeast Asia has 400 million unbanked or underbanked adults, and Grab's data advantage in underwriting could unlock massive value.

The ecosystem is self-reinforcing. GrabFood and GrabMart active users have 5x more order frequency and 2x retention rate than single service users. As Grab adds more services, user stickiness increases, customer acquisition costs per service decline, and lifetime value expands. The platform has reached critical mass where network effects create a deep competitive moat.

Demographic tailwinds are powerful. Southeast Asia's 650 million population is young, increasingly urban, and rapidly adopting digital services. GDP per capita is growing, smartphone penetration is increasing, and digital payment adoption is accelerating. Grab is perfectly positioned to capture this secular growth.

Bear Case: The Profitability Puzzle Skeptics point to harsh realities. Despite achieving profitability, margins remain thin. The $15 million profit in Q3 2024 on revenue of $716 million represents barely 2% margins. Any increase in competition or need for renewed subsidies could quickly return Grab to losses.

Competition remains intense. GoTo dominates Indonesia, Southeast Asia's largest market. Regional players like Foodpanda compete aggressively in food delivery. Traditional banks are launching digital services. Chinese tech giants like Alibaba and Tencent continue to invest in the region. Grab's market leadership is real but not unassailable.

Regulatory risks loom large. Digital banking comes with stringent capital requirements and regulatory oversight. Governments increasingly scrutinize platform monopolies. Labor regulations around gig workers are evolving. Data privacy laws are tightening. Any major regulatory shift could significantly impact Grab's business model.

The super app model's scalability is questionable. While successful in Southeast Asia, expansion beyond the region seems unlikely. This caps Grab's total addressable market at Southeast Asia's $180 billion digital economy—large, but not infinite.

Valuation Reality Check From the $39.6 billion SPAC valuation, Grab's market cap has fluctuated significantly, trading between $10-15 billion for much of 2024. This represents a sobering recalibration of expectations. While the business has improved operationally, public markets have been skeptical about the long-term margin potential and growth trajectory.

Compared to global peers, the picture is mixed. Uber trades at higher multiples but has better margins and operates in wealthier markets. DoorDash has similar challenges with profitability but benefits from a more homogeneous market. Sea Limited offers perhaps the best comparison—another Southeast Asian platform company that has struggled with profitability while building ecosystem breadth.

XII. Epilogue & Reflections

What would have happened if Uber had won Southeast Asia? The region's digital economy might look very different—more standardized perhaps, but less adapted to local needs. Motorcycle taxis might not have been digitized. Cash payments might not have been accepted. The hundreds of thousands of drivers who rely on daily payments might have been excluded.

Grab's victory wasn't predetermined. It required extraordinary execution, massive capital, and some fortunate timing. If Uber hadn't been distracted by internal turmoil in 2017, if SoftBank hadn't pushed for consolidation, if Go-Jek had expanded more aggressively—the outcome could have been different.

The Grab story also challenges Silicon Valley orthodoxy. The "blitzscaling" playbook worked, but only after significant localization. The "winner-take-all" dynamics played out, but with regional rather than global winners. The path to profitability took longer than expected but was ultimately achieved through operational excellence rather than financial engineering.

For Southeast Asian entrepreneurs, Grab provides both inspiration and caution. It proves that regional champions can emerge and compete with global giants. But it also shows the enormous capital requirements and execution challenges of building platform businesses in emerging markets.

Looking forward, Grab faces existential questions. Can it maintain growth while preserving profitability? Will the super app model continue to resonate as Southeast Asian consumers become more sophisticated? Can it expand beyond transportation and delivery into true financial services? How will it compete with the next generation of AI-native startups?

Perhaps most importantly, Grab must navigate its evolution from insurgent to incumbent. The company that once disrupted taxis is now a licensed taxi operator. The startup that fought regulations now works closely with governments. The challenger that offered drivers better terms now must balance driver welfare with shareholder returns.

Grab's investors include Japan's SoftBank Group and MUFG, Booking Holdings, Toyota and Microsoft—a testament to its strategic importance. But public market investors remain skeptical, as evidenced by the stock's performance. The next chapter will determine whether Grab becomes Southeast Asia's defining technology company or merely its first.

The story of Anthony Tan and Tan Hooi Ling—two Harvard students who saw a problem and decided to solve it—has become Southeast Asian tech legend. From gas station coffee runs to a $40 billion valuation, from MyTeksi to super app, from burning billions to achieving profitability, Grab's journey encapsulates the challenges and opportunities of building technology businesses in emerging markets.

As we close this analysis, one thing is clear: Grab has fundamentally changed how Southeast Asia moves, eats, and pays. Whether it can maintain that position while delivering sustainable returns to shareholders remains the billion-dollar question. But for millions of users across Southeast Asia, Grab has already succeeded in its original mission—making life safer, easier, and more convenient, one ride at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube