Genuine Parts Company: The NAPA Empire That Built America's Aftermarket

I. Introduction & Cold Open

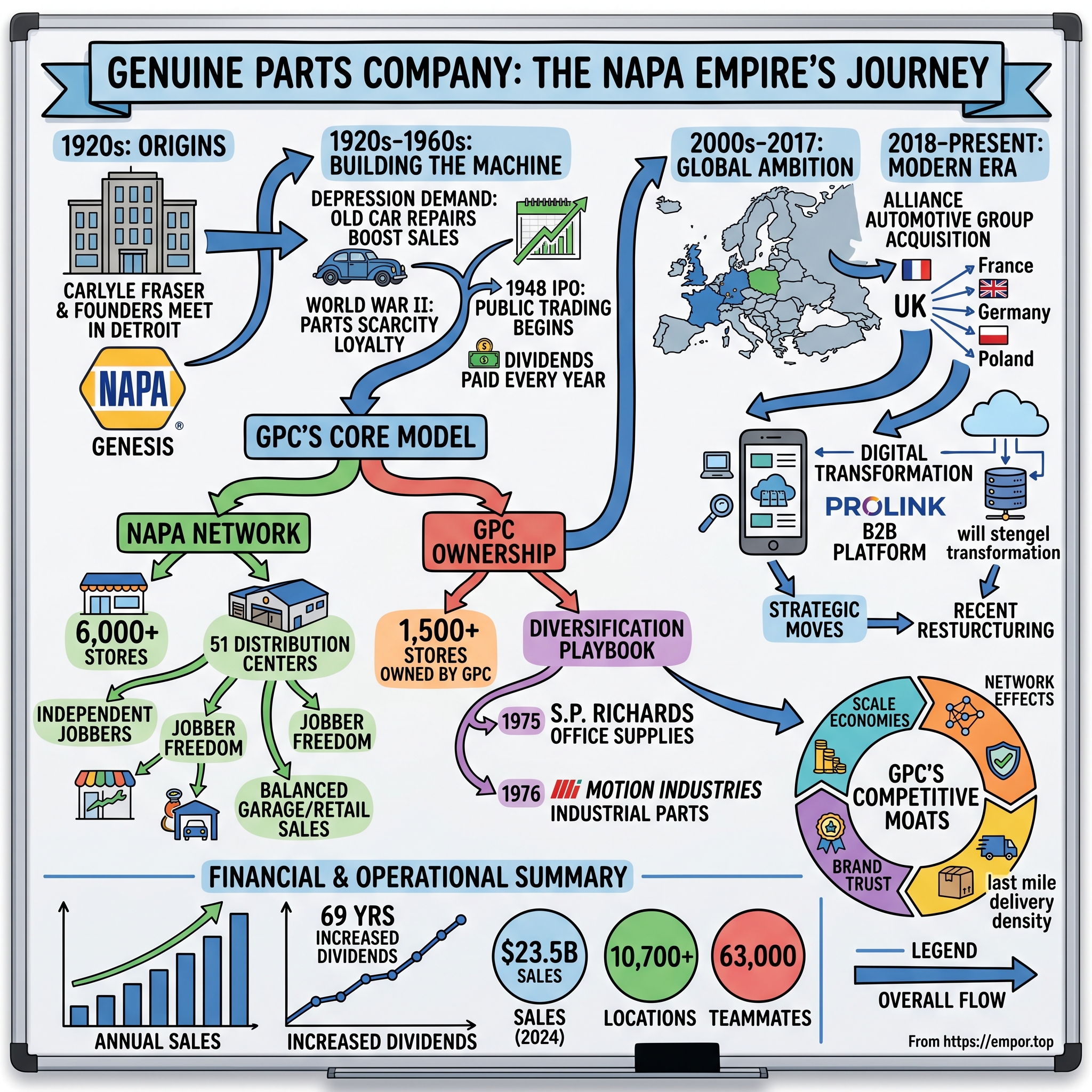

Picture this: Atlanta, 1928. The city still rebuilding from Sherman's march, now emerging as the South's commercial hub. In a modest storefront on Marietta Street, six men gather around a wooden desk, sorting through boxes of spark plugs, fan belts, and brake shoes. Their leader, a 36-year-old entrepreneur named Carlyle Fraser, counts out the day's receipts—$205.48. Not bad, but not enough. The company has $40,000 in capital, six employees, and a dream that seems almost laughable: to build a parts distribution network that could serve every garage in America.

Fast forward to 2024. That six-person operation has morphed into Genuine Parts Company, a $16.94 billion colossus with 63,000 teammates across 10,700 locations in 17 countries. Annual sales? $23.5 billion. The company has paid dividends for 76 consecutive years, increased them for 69 straight years—a feat matched by fewer than 50 companies in America. How does a business selling unglamorous replacement parts—windshield wipers, oil filters, alternators—become one of the most consistent wealth creators in American capitalism?

The answer lies in understanding a fundamental truth about American mobility: cars break. They always have, they always will. And when they do, someone needs to supply the parts—fast, reliably, at scale. This is the story of how Genuine Parts Company built the infrastructure that keeps America moving, created the NAPA brand that became synonymous with automotive reliability, and constructed competitive moats so deep that even Amazon struggles to cross them.

This isn't just a business story—it's a masterclass in patient capital allocation, network effects, and the power of being boring in exactly the right way. It's about recognizing that in business, as in life, the unsexy essentials often generate the most enduring returns. Welcome to the untold empire of automotive aftermarket distribution.

II. Origins: The Fraser Brothers & NAPA's Genesis (1925-1928)

The Detroit winter of 1925 cut through wool overcoats like a knife. Inside the Book-Cadillac Hotel, radiators hissed and clanged as sixty-eight independent auto parts sellers gathered in a smoke-filled conference room. The automobile industry was barely twenty years old, but already these men could see the future: millions of cars would need millions of parts, and whoever controlled distribution would control an empire.

In 1925, a group of independent auto parts sellers met in Detroit to form the National Automotive Parts Association. Their mission was simple: Improve the distribution of auto parts to serve the people and businesses who increasingly relied on cars and trucks for their transportation needs. Among the founding members sat Carlyle Fraser, a 33-year-old parts man from Pittsburgh with sharp eyes and an accountant's mind for detail. As a founder, Carlyle Fraser was on the front lines.

Fraser understood something fundamental that others missed. While Detroit's titans—Ford, Chrysler, Durant—fought over who could build cars fastest and cheapest, Fraser saw opportunity in what happened after the sale. Cars broke down. Parts wore out. And unlike new car purchases, replacement parts couldn't wait. When a delivery truck's water pump failed, when a taxi's brake shoes wore thin, speed mattered more than price. Distribution was destiny.

Three years after that Detroit meeting, Fraser made his move. Fraser launched his own company in 1928 with business partner William "Bill" Martin, purchasing Motor Parts Depot in Atlanta, Georgia for $40,000. The seller, watching Fraser sign the papers, offered unsolicited advice: "The automobile business has reached its peak." Fraser smiled politely and kept signing.

Atlanta in 1928 was no Detroit. The city had 270,000 residents, unpaved roads beyond downtown, and a business culture still recovering from Reconstruction. But Fraser saw advantages: central location for Southeast distribution, lower operating costs than Northern cities, and distance from Detroit's gravitational pull. He renamed the business Genuine Parts Company—a name suggesting authenticity in an era rife with counterfeit parts.

In its first year, the store, renamed the Genuine Parts Company, had annual sales of $75,000 and six employees. The company lost money—about $2,500—on those sales. Fraser's six employees must have wondered if they'd joined a sinking ship. But Fraser had a theory about the replacement parts business that would prove prophetic: it was countercyclical. When the economy boomed, people bought new cars and needed parts for maintenance. When it crashed, they fixed old cars and needed even more parts for repairs.

Genuine Parts (GPC) pushed swift, reliable service as a way to outflank the competition. While competitors took days to fill orders, Fraser instituted same-day delivery for local garages. He stocked deeper inventory than anyone thought prudent—20,000 different parts when most distributors carried 5,000. His mantra: "The sale you lose today from lacking inventory is a customer you lose forever."

Fraser's relationship with the National Auto Parts Association (NAPA) became a perfect match. Through NAPA, Fraser accessed a network of manufacturers and distributors across the country. He could source parts no one else in Atlanta could find, cementing relationships with repair shops that would last decades. The NAPA connection gave him something money couldn't buy: trust. In an industry plagued by fly-by-night operators selling substandard parts, the NAPA name meant quality.

By late 1929, Fraser had grown sales to $152,000 and turned his first profit: $3,100. He hired four more employees, bringing the total to ten. On October 24, 1929—Black Thursday—the stock market began its historic crash. Fraser, reviewing inventory reports in his Marietta Street office, had no idea that the coming catastrophe would transform his struggling parts store into the foundation of a distribution empire. The Great Depression was about to make Genuine Parts Company's fortune.

III. Building the Machine: Depression Through Post-War Boom (1930s-1960s)

The winter of 1931 hit Atlanta hard. Banks failed weekly. Breadlines stretched around Five Points. In the basement of Genuine Parts Company's distribution center, Carlyle Fraser stood watching mechanics rebuild connecting rods—taking broken parts and making them serviceable again. The Great Depression had become his laboratory for a radical thesis: economic catastrophe was good for the parts business.

The stock market crash of 1929 and economic instability of the Great Depression also increased demand for auto parts because more people and businesses were repairing older vehicles rather than buying new ones. Fraser's counterintuitive insight proved devastatingly correct. While Ford and General Motors shuttered plants and laid off thousands, Genuine Parts hired. In 1931, GPC started refurbishing used parts to help customers in need of quality products at affordable rates. The rebuilding operation—connecting rods, water pumps, generators—offered parts at 40% less than new. For Depression-era Americans clutching their wallets, it was salvation.

During the 1930s, company sales went from $339,000 to $3.18 million. Think about that: a ten-fold increase during America's worst economic decade. How? Fraser understood that cars had become essential infrastructure. People couldn't afford new vehicles, but they absolutely couldn't afford not to have transportation. The average car age stretched from 4.5 years in 1929 to nearly 8 years by 1935. Every additional year meant more repairs, more parts, more business for Genuine.

Fraser's distribution philosophy during this period was revolutionary for its simplicity: be everywhere, stock everything, deliver immediately. By 1935, GPC operated seven distribution centers across the Southeast. Each center carried 25,000 different parts—an inventory depth competitors considered insane. But when a mechanic in rural Georgia needed a specific water pump for a 1927 Buick, GPC had it. That mechanic became a customer for life.

World War II transformed the business again, but not how you'd expect. Consumers again held onto their older cars, sometimes having little choice because automakers were devoting much of their capacity to the war effort. By the same token, the War Production Board only allocated resources to parts manufacturers to build "functional" parts for cars. This restriction meant, for instance, no fenders or door hardware were available to sell to those needing them. With auto sales slacking, the average vehicle was 7.28 years old in 1946, compared with 4.77 years old in 1941 before the United States entered the war. As a result, $19 in parts were bought for the average car in 1945.

The war years taught Fraser another lesson: scarcity creates loyalty. When you're the only distributor who can find that impossible-to-source part, price becomes secondary to availability. GPC's vast network and deep relationships with manufacturers meant they could source parts others couldn't. They became the distributor of last resort—and first choice.

By 1948, twenty years after that $40,000 beginning, the transformation was complete. In the year of its 20th anniversary in 1948, the company had $20 million in sales. That same year the company went public, selling 150,000 shares of common stock at $11 per share. The IPO wasn't just about raising capital—though the $1.65 million certainly helped. It was Fraser's declaration that Genuine Parts had graduated from regional player to national force.

The company has paid a cash dividend to shareholders every year since going public in 1948. That first dividend in 1948—25 cents per share—began what would become one of the longest dividend streaks in American capitalism. Fraser insisted on it, even when board members suggested reinvesting everything for growth. "A business that can't pay its owners," he said, "isn't much of a business."

A successful businessman, Fraser was elected President of NAPA, serving from 1941-1942. This wasn't honorary—Fraser used the position to reshape NAPA's strategy, pushing for standardization of parts numbering systems and coordinated purchasing that would give members better pricing power against manufacturers.

The post-war boom of the 1950s presented a different challenge: abundance. Americans were buying cars at unprecedented rates. By 1955, 67% of American families owned at least one car. The two-car garage became suburban architecture's defining feature. Economic prosperity in the post-war years meant more and more Americans owned cars, with many families owning two. An increased number of cars on the roads meant a growing demand for auto parts.

1966 marked a pivotal strategic shift. GPC introduced the first NAPA-branded parts—oil filters, spark plugs, and fan belts manufactured to GPC specifications. This wasn't just private labeling; it was vertical integration of the supply chain. By controlling the brand, GPC captured manufacturer margins while ensuring quality standards. The NAPA shield logo began appearing in garages across America, becoming as trusted as the mechanics who installed the parts.

Fraser developed Genuine Parts into the largest auto parts distribution business in the world, generating $82 million in sales by 1961. But size alone didn't capture what Fraser had built. He'd created a network effect before Silicon Valley coined the term. Every new distribution center made the network more valuable to manufacturers (broader reach) and to repair shops (better availability). Every new repair shop customer made GPC more attractive to manufacturers. The virtuous cycle accelerated with each turn.

Fraser's management philosophy during this explosive growth remained remarkably consistent: hire good people, give them autonomy, hold them accountable. Distribution center managers ran their operations like independent businesses, with P&L responsibility and broad decision-making authority. This decentralized structure—unusual for the era—allowed GPC to maintain entrepreneurial energy even as it scaled.

By 1968, forty years after Fraser bought that first Atlanta store, Genuine Parts Company operated 35 distribution centers, served over 5,000 jobber stores, and generated $185 million in annual sales. Fraser, now 76, stepped back from daily operations but remained chairman. At the retirement dinner, someone asked him the secret to GPC's success. His answer was characteristically understated: "We just tried to have the right part at the right place at the right time. Turns out that's harder than it sounds."

IV. The Diversification Playbook (1970s-1990s)

Calgary, 1972. Oil money flowed through Alberta like crude through pipelines. In a boardroom overlooking the Bow River, Wilton Looney—GPC's CEO since Carlyle Fraser's death in 1961—shook hands with the owners of Corbetts Ltd. It was Genuine Parts' first international acquisition, modest in size but revolutionary in implication. The American parts distributor was going global.

Elected Chairman and CEO of Genuine Parts Company in 1961, serving in that position until his retirement in 1990. Wilton D. Looney guided GPC's growth from $34 million to more than $3.4 billion in sales during his tenure as CEO. But Looney wasn't interested in growth for growth's sake. He had a philosophy he called "Looney's Law": "we're not just interested in making a sale; we're interested in making our customers profitable and happy."

Looney came from different stock than Fraser. He didn't want to continue working on his parent's one-mule farm in Vanna, Georgia. He traveled to Elberton, Georgia and found a job at Western Auto Supply Company where he worked for $10 per week, six days a week until he was recruited to work for Genuine Parts Company in Charlotte, North Carolina. He served in the US Army during World War II as a vehicle maintenance and construction supervisor on the Burma Road project. The Burma Road taught him logistics at scale—keeping supply lines open across impossible terrain. He'd apply those lessons to GPC's expansion.

The 1970s brought economic chaos: oil embargoes, stagflation, Detroit's quality crisis. Yet Looney saw opportunity in disruption. His first major diversification came in 1975. In 1975, GPC acquired S.P. Richards, which was described by Industrial Distribution as "a distributor of general office products, technology products and accessories, office furniture, JanSan and safety supplies". Office supplies? Wall Street was baffled. But Looney understood: offices needed supplies like cars needed parts—constantly, reliably, without fail.

Then came the masterstroke. In 1976, under the leadership of CEO Wilton Looney, GPC expanded into the industrial parts business with the acquisition of Motion Industries, Inc. Looney believed that industrial parts would be recession-proof in the same way that auto parts were: during recessions industrial firms would buy replacement parts for existing machinery rather than purchasing new equipment. Motion Industries, based in Birmingham, Alabama, distributed bearings, power transmission components, and industrial supplies to factories across the South.

The logic was elegant: factories are just cars at scale. Both have moving parts that wear out. Both need immediate replacement when something breaks. Both value reliability over price when production is on the line. Motion started as a distributor of bearings and industrial supplies, and expanded to offer products related to automation, conveyance, hydraulics, fluid power, and robotics. What NAPA was to garages, Motion would become to factories.

In 1978 Genuine installed a computerized point-of-sale system for billing customers, tracking inventories, and automatically ordering replacements for parts that were sold. The system, developed with Data General Corp., cost $24,000 to $30,000 per complete system, and grew to include 900 jobbers by 1982. This system gave Genuine an important advantage over competitors, because no other independent distributor could match the services Genuine could offer.

The technology investment was vintage Looney: expensive upfront, transformative long-term. While competitors still called in orders and tracked inventory on index cards, GPC jobbers could see real-time availability across the entire network. A mechanic in Memphis could know instantly if a part was available in Nashville. The network effect, already powerful, became exponential.

1982 brought the recession everyone feared—except Looney. Acquired Dallas-based General Automotive Parts Corp. for $250 million, GPC's largest acquisition to date. General Automotive operated 29 distribution centers serving 900 NAPA stores across Texas and surrounding states. The deal doubled GPC's presence in the Southwest overnight. While competitors retrenched, GPC expanded. Genuine's sales reached $1.6 billion in 1981, of which 63 percent came from the distribution of parts, 22 percent came from industrial replacement parts, and 8 percent from office-supply products. The firm had 55 U.S. distribution centers for auto parts and four in western Canada, selling to about 5,200 jobbers, of which it owned about 350.

The recession validated Looney's diversification thesis perfectly. New car sales cratered—down 35% from 1979 to 1982. But GPC's sales grew. Automotive parts sales increased as Americans kept older cars running. Industrial parts boomed as factories repaired rather than replaced equipment. Even office supplies held steady—businesses still needed paper and pens. The three-legged stool Looney built wouldn't topple.

By 1990, when Looney retired after 51 years with the company, the transformation was complete. Leading the company's growth from $34 million to more than $3.4 billion in sales. But the numbers only told part of the story. Looney had evolved GPC from a regional auto parts distributor into a diversified distribution powerhouse with global reach.

The 1990s acceleration began with new leadership. Larry Prince, Looney's handpicked successor, brought a financier's precision to GPC's sprawling empire. His mantra: "Grow where we're strong, exit where we're not." The international expansion intensified.

In December 1998, GPC spent about £231 million to buy the remaining 80% of Montreal-based UAP Inc. that it did not already own. UAP wasn't just another acquisition—it was Canada's leading automotive parts distributor with deep French-Canadian roots dating to 1926. UAP has peddled the right parts since 1926. The Genuine Parts Canadian subsidiary rebuilds and distributes replacement parts for cars, trucks, and other heavy-duty vehicles. It operates via a network of 12 distribution centers in Canada that supply some 600 NAPA Auto Parts stores (about a third of which are company-owned, or JVs, and the remainder independently owned).

The same year, GPC made another strategic move: The July 1998 acquisition of EIS, Inc., a distributor of electrical and electronic materials, in a deal valued at about $180 million. EIS distributed wire, cable, and electrical components to industrial OEMs and motor repair shops. It was another leg on the stool—complementary to Motion but serving different customers with different needs.

In January 1999, GPC further expanded its auto parts group by acquiring yet another Atlanta-based firm, Johnson Industries, Inc. The 1990s closed with GPC generating over $8 billion in annual sales, operating in multiple countries, serving multiple industries, yet maintaining the disciplined distribution focus Fraser and Looney had instilled. The foundation was set for the 21st century's greatest challenge: going truly global.

V. The Global Ambition: Alliance Automotive & European Conquest (2000s-2017)

London, September 2017. The rain drummed against the windows of Alliance Automotive Group's headquarters as Jean-Jacques Lafont, AAG's co-founder and CEO, reviewed the final terms. Across the table sat Paul Donahue, who'd become Genuine Parts Company's CEO just the year before. Between them lay documents that would reshape the global automotive aftermarket: a $2 billion acquisition agreement that would give an American company instant dominance in European parts distribution.

Genuine Parts Company announced today that it has completed the purchase of Alliance Automotive Group (AAG) for a total purchase price of approximately $2 billion (US$), including the repayment of AAG's outstanding debt, effective today. The price tag made headlines, but the strategic implications ran deeper. This wasn't just GPC's largest acquisition ever—it was a declaration that the future of parts distribution would be global.

The road to this London boardroom began years earlier. The 2008 financial crisis had reshuffled the European automotive aftermarket like a deck of cards. National champions weakened. Private equity circled. Blackstone, the private equity giant, had assembled Alliance Automotive Group through serial acquisitions across France, Germany, and the UK, creating Europe's second-largest parts distribution platform.

AAG is the second largest parts distribution platform in Europe, with a focus on light vehicle and commercial vehicle replacement parts. Headquartered in London, AAG has approximately 8,000 employees and 2,100 company-owned stores and affiliated outlets across France, the U.K., Germany and Poland. But size alone didn't capture AAG's strategic value. The company had cracked the code of European distribution—a market where national preferences, regulatory differences, and language barriers had stymied American companies for decades.

Jean-Jacques Lafont had built AAG with a philosophy that mirrored GPC's own history. Jean-Jacques Lafont, Chairman, Chief Executive Officer and co-founder of Alliance Automotive Group, said, "The AAG team has tremendous respect for Genuine Parts Company and its well-deserved reputation as a long-standing leader in the automotive parts industry." Like Carlyle Fraser in 1920s Atlanta, Lafont understood that distribution was about relationships, not just logistics. AAG's network included both company-owned stores and affiliated independent operators—a hybrid model that balanced control with local expertise.

The European market presented unique challenges that made AAG's expertise invaluable. Unlike America's relatively homogeneous automotive landscape, Europe was a patchwork. French mechanics preferred different brands than German ones. UK garages operated on different business models than Polish ones. AAG serves approximately 40,000 garages with over 100,000 different parts for repair and maintenance from a network of more than 300 company-owned stores and approximately 1,800 affiliated outlets. Each market required deep local knowledge that couldn't be replicated from Atlanta.

Paul Donahue, who'd spent his career climbing GPC's ranks, understood the transformative potential. Paul Donahue, Genuine Parts Company's President and Chief Executive Officer, stated, "We are excited to combine with AAG and enter the European markets with critical scale and a leading market position in the automotive aftermarket." This wasn't toe-dipping into Europe—it was a cannonball dive.

The financing structure revealed GPC's confidence. The Company financed the purchase, including the pay-off of AAG's existing debt arrangements, with approximately $2 billion of debt financing. For a company that had historically been conservative with leverage, taking on $2 billion in debt was unprecedented. But the math was compelling: For 2018, incremental diluted earnings per share is estimated at $0.45 to $0.50 and adjusted earnings per share is estimated at $0.65 to $0.70, which excludes the amortization of acquisition-related intangibles.

The strategic rationale went beyond immediate accretion. Europe's automotive aftermarket was consolidating rapidly. Independent garages were being rolled up into chains. Parts distributors were merging to gain scale against manufacturers. E-commerce threats loomed. AAG gave GPC a platform to participate in—and shape—this consolidation.

AAG has a consistent track record of organic revenue and earnings growth supported by strategic investments based on a proven M&A strategy to gain scale, efficiencies and geographic coverage. AAG wasn't just a collection of assets; it was a proven acquisition machine. The company had completed dozens of bolt-on acquisitions, integrating local distributors into its network while maintaining their entrepreneurial energy.

The cultural fit proved surprisingly strong. AAG has a strong management team and a deep bench of talent, and our similar cultures and histories make this acquisition an excellent strategic fit. Both companies shared DNA: family-founded businesses that had professionalized without losing their entrepreneurial spirit, distributors who saw themselves as partners to independent garages, companies that valued long-term relationships over short-term profits.

November 2, 2017, the deal closed. GPC shares initially dropped—investors worried about integration risk, European exposure, debt levels. But Donahue and his team had a different timeline in mind. They weren't buying AAG for next quarter's earnings. They were buying it for the next quarter-century of global growth.

The integration proceeded with surgical precision. Rather than imposing American methods on European operations, GPC took a "reverse integration" approach—learning from AAG's best practices and applying them globally. AAG's digital capabilities, particularly in B2B e-commerce, were more advanced than GPC's. Their garage loyalty programs showed higher engagement. Their private label penetration exceeded NAPA's.

By 2019, the thesis was validated. AAG contributed over $3 billion in revenue. More importantly, it provided a platform for further European expansion. GPC acquired operations in Poland, the Netherlands, and Belgium. The NAPA brand began appearing in European garages—not replacing local brands but complementing them.

The AAG acquisition marked GPC's transformation from an American company with international operations to a truly global enterprise. AAG is poised to contribute significant sales growth and earnings accretion to Genuine Parts Company and also serves to enhance the GPC platform for long-term, sustainable expansion across the global automotive parts industry. It proved that GPC's distribution model—patient capital, local relationships, operational excellence—could translate across oceans and cultures.

As 2017 closed, Genuine Parts Company stood transformed. From Carlyle Fraser's six-person Atlanta shop to a global distribution powerhouse operating on four continents. The company that had mastered American distribution now possessed the keys to European markets. The foundation was set for an even more ambitious transformation: becoming the world's indispensable automotive parts distributor in the digital age.

VI. Modern Era: Digital Transformation & Market Leadership (2018-Present)

Atlanta, June 3, 2024. The morning sun glinted off the glass towers of Genuine Parts Company's Wildwood headquarters as employees gathered in the auditorium. After 96 years and only five CEOs, the company was witnessing another historic transition. Paul D. Donahue will transition from chairman and CEO to executive chairman, effective June 3, 2024. Standing at the podium, Will Stengel—43 years old, architect of GPC's digital transformation—prepared to address the company as its sixth CEO.

The path to this moment began in 2019, when GPC made an unusual hire. He joined the company as GPC's first chief transformation officer in 2019, became president in 2021, and became chief operating officer in 2023. Stengel came from HD Supply, where he'd digitized a traditional distribution business. GPC didn't need a parts expert—they had thousands of those. They needed someone who understood how Amazon, technology, and changing customer expectations were reshaping distribution.

Stengel's arrival coincided with a moment of reckoning. E-commerce was no longer a future threat—it was present reality. Professional mechanics ordered parts on their phones between jobs. DIY customers expected same-day delivery. Amazon Business was targeting B2B distribution with algorithmic pricing and two-hour delivery windows. The old advantages—relationships, inventory depth, local presence—still mattered, but they weren't enough.

As Chief Transformation Officer, Will has led the effective and disciplined management of our transformation initiatives while also taking on various operational and strategic responsibilities. His first move was counterintuitive: instead of building new technology, he studied what already worked. GPC's European operations, through AAG, had more advanced digital capabilities than the U.S. business. Motion Industries had developed sophisticated predictive maintenance algorithms. Even some independent NAPA jobbers had innovative local delivery models.

The transformation strategy that emerged was distinctly GPC: evolutionary, not revolutionary. Rather than disrupting the existing network, Stengel enhanced it. Digital catalogs didn't replace counter relationships—they supplemented them. Predictive analytics didn't eliminate inventory expertise—they amplified it. Mobile apps didn't disintermediate jobbers—they empowered them.

By 2023, the results were tangible. NAPA's ProLink digital catalog processed millions of queries daily, using AI to recommend parts based on repair history. Motion's automation solutions helped factories predict equipment failures before they happened. The company's logistics network, enhanced by machine learning, could route parts more efficiently than ever—often beating Amazon's delivery times in served markets.

The strategic focus also sharpened. Under his leadership, the company simplified its business mix, expanded its global footprint and delivered significant shareholder value. The office products business, S.P. Richards, was divested in 2020. The electrical materials division followed. GPC returned to its core: automotive and industrial parts distribution, but now on a global scale with digital capabilities.

April 30, 2024 marked another milestone. Effective April 30, 2024, the company acquired Motor Parts & Equipment Corporation (MPEC). It is the largest independent owner of NAPA Auto Parts stores in the U.S., operating 181 locations across Illinois, Indiana, Iowa, Michigan, Minnesota and Wisconsin. The MPEC acquisition wasn't just about adding stores—it was about density. In distribution, density is destiny. More stores in a market means better delivery economics, deeper inventory, stronger technician relationships.

"We are pleased to announce the completion of this strategic acquisition, which aligns with our initiative to own more NAPA stores in priority markets," said Will Stengel, President & CEO-elect of GPC. The strategy represented a subtle but important shift. Historically, GPC had been content to supply independent NAPA owners. Now, they were selectively acquiring the best operators, bringing more stores under direct control.

The financials told a story of resilience amid transformation. 2024 revenue reached $23.487 billion, with steady if unspectacular growth. More importantly, return on equity remained robust at 19.13%, proof that GPC could invest in transformation while maintaining profitability. The dividend, that sacred commitment dating to 1948, not only continued but increased for the 69th consecutive year.

"As I transition from the CEO role, I am pleased to welcome Will as only the sixth CEO in our company's 96-year history," said Mr. Donahue. The generational handoff was deliberate and smooth—Donahue remaining as executive chairman to provide continuity while Stengel drove transformation.

The challenges ahead were formidable. Electric vehicles, with fewer moving parts, threatened long-term parts demand. Direct-to-consumer models were evolving rapidly. Industrial automation could reduce the need for replacement parts. But Stengel's GPC had advantages previous generations lacked: global scale, digital capabilities, and the irreplaceable asset of 63,000 employees who understood that distribution was ultimately about solving customer problems, not just moving boxes.

"I am humbled and honored for the opportunity to lead Genuine Parts Company and especially grateful for my GPC teammates and the support of Paul and the board of directors," said Mr. Stengel. "We will continue to build on the strong foundation laid over many years as we work to deliver solutions for our customers, invest in talent and capabilities and create value for our shareholders."

The modern GPC stands as a bridge between eras. It maintains the patient, relationship-driven culture that Carlyle Fraser instilled in 1928 while embracing the digital transformation necessary for 2024. It operates NAPA stores that look like they did decades ago, while running sophisticated algorithms that predict part failures before they happen. It serves mechanics who've bought from the same counter person for thirty years, while also fulfilling orders placed by AI-powered procurement systems.

What makes GPC different in the digital age isn't technology—anyone can buy software. It's the combination of technology with irreplaceable physical assets: 10,700 locations, millions of SKUs in inventory, relationships with hundreds of thousands of repair shops. Amazon can deliver a part tomorrow. GPC can deliver the right part, with the right advice, in the right quantity, often within hours. In the end, when a delivery truck is broken down on the highway or a factory line has stopped, that difference matters more than price.

VII. The NAPA Network Effect

Birmingham, Alabama, 7:00 AM. Before the first customer arrives, Tony Martinez unlocks his NAPA Auto Parts store, flips on the lights, and boots up the computer system that connects him to a $23 billion distribution network. Tony owns this store—one of approximately 4,500 independently owned NAPA locations across America. But ownership here means something different than a typical franchise. NAPA owners enjoy great freedom to operate their businesses as they see fit because NAPA is not a franchise. Owners pay no franchise, licensing, or royalty fees.

This distinction—no franchise fees, no royalties—represents one of business history's most underappreciated strategic masterstrokes. While McDonald's, Subway, and countless others built empires on franchise fees, GPC built something arguably more powerful: a network effect so strong that independent businesspeople pay for the privilege of joining through their purchases, not their fees.

The NAPA Network stretches nationwide across 6,000 store locations and 51 strategically placed distribution centers. There are over 6,000 NAPA Auto Parts stores in the United States, approximately 1,500 of which are owned by Genuine Parts Company. The math is revealing: GPC directly owns about 25% of NAPA stores, while independent operators own the rest. This hybrid model combines the control of corporate ownership with the entrepreneurial energy of independent operators.

Tony's store exemplifies the genius of the model. He invested between $75,000 and $150,000 to open his store—capital for inventory, fixtures, working capital. Do you have access to $75,000–$150,000 of financial funding? But unlike a franchise, he pays no ongoing fees to GPC. Instead, he buys parts from GPC's distribution centers. Every spark plug, every brake pad, every windshield wiper generates margin for both Tony and GPC. Their interests align perfectly: the more Tony sells, the more both parties profit.

The economics are compelling. The average gross sales for a NAPA Auto Parts franchise are approximately $2.0 million per location. Assuming a 15% operating profit margin, $2.0 million yearly revenue can result in $300,000 operating profit annually. For a small business owner, those numbers represent genuine wealth creation. For GPC, 4,500 stores generating $2 million each in purchases creates a $9 billion revenue stream with minimal capital investment.

But the network effect transcends simple economics. Every NAPA store strengthens every other NAPA store. When a mechanic in Birmingham needs a part that Tony doesn't stock, Tony can check inventory at nearby NAPA stores or order from the distribution center for same-day delivery. The mechanic gets the part, Tony keeps the customer, and the sale stays within the NAPA network.

Instead, NAPA provides a proven system with a large framework of options and lets owners decide how they wish to run their businesses. This flexibility proves crucial. Tony knows his market—the local fleet operators, the DIY customers who come in every Saturday, the professional mechanics who need delivery before 10 AM. He sets his hours, chooses his inventory mix, hires his staff. GPC provides the infrastructure; Tony provides the local expertise.

The support system resembles a franchise without the constraints. Take advantage of the strong NAPA brand, as well as effective national marketing and local advertising assistance. From tech support to store signage, The NAPA Network delivers support, incentives and discounts that guarantee success. GPC funds national advertising—those NASCAR sponsorships, the "NAPA Know How" campaigns. They provide training programs, inventory management systems, and marketing materials. But Tony decides how to use these tools.

The commercial side of the business—sales to repair shops—demonstrates the network's true power. There are 6600 NAPA stores,over 6000 are independent. They dont have access to NAPA online sales records.NAPA stores have a more balanced garage/retail ratio on sales than a lot of chains. Where a PEP Boys is probably almost 100% retail,and an AutoZone maybe 80/20 retail,and the old VIP almost 100% retail,I am told that O'Reilly is pushing hard to increase its garage/fleet penetration This balanced customer mix—professional and retail—provides resilience. When DIY sales slump, commercial sales often compensate.

The jobber delivery model, refined over decades, creates switching costs that protect market share. Tony's delivery driver knows every shop's quirks: who needs delivery before 8 AM, who pays cash, who always orders the wrong part number. These relationships, built over years, can't be replicated by an algorithm or undercut by a website. When Amazon offers a part for 5% less, the shop manager sticks with Tony because Tony's driver will deliver it in an hour, not tomorrow.

Technology amplifies rather than threatens these relationships. NAPA's ProLink system gives professional technicians access to millions of parts across the network. But the order still flows through Tony's store, preserving his customer relationship and margin. The system makes Tony more valuable to his customers, not less.

The brand itself carries weight that transcends marketing. NAPA Auto Parts was established in 1925 in Atlanta. Some NAPA Auto Parts stores are owned and operated by GPC, but most are independently owned and operated. Nearly a century of "NAPA Know How" has created trust that new entrants can't quickly replicate. When a customer sees the NAPA shield, they expect quality parts, knowledgeable counter staff, and standing behind the product.

Recent strategic moves reveal GPC's evolving approach to the network. It is the largest independent owner of NAPA Auto Parts stores in the U.S., operating 181 locations across Illinois, Indiana, Iowa, Michigan, Minnesota and Wisconsin. "We are pleased to announce the completion of this strategic acquisition, which aligns with our initiative to own more NAPA stores in priority markets," said Will Stengel, President & CEO-elect of GPC. The MPEC acquisition shows GPC selectively increasing direct ownership in key markets—not to eliminate independents but to ensure critical mass in strategic geographies.

The international expansion follows the same playbook. As of 2020, the NAPA brand includes 12 stores operating in Australia. Seven other businesses owned by General Parts Company, including Ashdown-Ingram and Covs, have been rebranded under the NAPA name. Rather than imposing the model wholesale, GPC adapts it to local markets while maintaining the core network principles.

For investors, the NAPA network represents a moat that's nearly impossible to replicate. A competitor can't simply throw money at the problem. Building 6,000 stores would cost billions. Convincing independent operators to switch would require massive incentives. Creating the brand trust would take decades. The network effect means that even if a competitor built 3,000 stores, they'd still be at a disadvantage—the value of a network grows exponentially with its size.

The model's resilience shows in the numbers. Through recessions, technological disruption, and changing consumer behavior, the NAPA network has not just survived but thrived. Those 6,000 stores process millions of transactions daily, each one reinforcing the network's value, each one making it harder for competitors to break in. It's distribution as destiny, network effects as competitive advantage, and proof that in business, sometimes the best franchises aren't franchises at all.

VIII. Playbook: What Makes GPC Different

The conference room in Atlanta has witnessed 76 years of board meetings. On the wall hangs a simple plaque: "Dividend paid every year since 1948." Below it, another: "Dividend increased 69 consecutive years." These aren't just corporate achievements—they're a philosophy carved in brass. When executives propose acquisitions, new initiatives, or strategic pivots, someone inevitably asks: "Will this let us keep raising the dividend?"

This discipline shapes everything. The company has paid a cash dividend to shareholders every year since going public in 1948. Think about what that means: through the Korean War, Vietnam, oil crises, stagflation, dot-com bubbles, financial meltdowns, and global pandemics, GPC has written a check to shareholders every single quarter. Not many companies can make that claim—fewer than 50 in America.

The dividend commitment forces a different kind of thinking. You can't make reckless acquisitions when you need cash for dividends. You can't chase fads when you're committed to 30-year shareholders. You can't leverage to the hilt when you've promised steady, growing payments. The dividend becomes a governor on corporate excess, a north star for capital allocation.

But GPC's playbook goes deeper than financial discipline. At its core lies a model they've perfected: "distribution as a service." They don't just move boxes from manufacturers to end users. They provide credit to customers, inventory management, technical expertise, warranty handling, marketing support, and logistics optimization. The parts are almost incidental—what GPC really sells is the entire infrastructure that keeps cars and factories running.

Consider the acquisition integration machine GPC has built. Since 1972, they've completed over 100 acquisitions, from tiny regional jobbers to the $2 billion Alliance Automotive deal. The playbook never varies: preserve what works, improve what doesn't, integrate what adds value. They don't slap the GPC logo on everything and call it done. Instead, they study the acquired company's best practices and often adopt them across the network.

The AAG acquisition exemplified this approach. Rather than imposing American methods on European operations, GPC learned from AAG's superior digital capabilities and customer engagement programs. AAG's B2B e-commerce platform was more advanced than NAPA's—so GPC adapted AAG's technology for North American markets. This intellectual humility—rare in acquisitions—explains why GPC's deals generally work while 70% of M&A destroys value.

The balance between company-owned and franchise operations represents another strategic masterstroke. Unlike pure franchisors (who lack operational control) or pure corporate chains (who lack entrepreneurial energy), GPC operates both models simultaneously. Company-owned stores in critical markets ensure standards and provide testing grounds for new initiatives. Independent stores bring local market knowledge and entrepreneurial drive. Each model strengthens the other.

Counter-cyclical resilience isn't luck—it's designed into the business model. When new car sales boom, people drive more, wearing out parts faster. When new car sales crash, people keep older cars longer, requiring more repairs. When the economy strengthens, commercial vehicle usage increases, driving industrial parts demand. When it weakens, companies repair equipment rather than replacing it. GPC wins either way.

The capital allocation framework resembles a decision tree refined over decades. First priority: maintain and grow the dividend. Second: invest in organic growth—new distribution centers, technology, inventory. Third: acquisitions that strengthen the network or enter adjacent markets. Fourth: share buybacks when the stock trades below intrinsic value. This hierarchy never changes. Fashion doesn't influence it. Activist investors can't shake it.

Geographic and product diversification follows a specific logic. GPC doesn't diversify for its own sake—each new market must leverage existing capabilities. When they entered Europe, they bought established distributors who understood local markets. When they expanded into industrial parts, they applied automotive distribution principles to a new customer base. When they added office products (later divested), they used the same logistics infrastructure. Every diversification builds on existing strengths.

The company's approach to technology investment reveals sophisticated thinking about disruption. Rather than viewing digital as a threat, GPC sees it as an amplifier of existing advantages. Their 10,700 physical locations become fulfillment centers for online orders. Their technical expertise becomes content for digital platforms. Their inventory depth enables same-day delivery that pure e-commerce players can't match. Technology doesn't replace the traditional model—it enhances it.

Consider how GPC handles market cycles. During downturns, weaker competitors cut inventory, reduce service, and retrench. GPC does the opposite—maintaining inventory levels, preserving customer service, and often acquiring distressed competitors. When recovery comes, GPC has gained market share and customer loyalty. This patient approach requires financial strength and long-term thinking that quarterly-focused companies can't match.

The management philosophy emphasizes continuity over disruption. As I transition from the CEO role, I am pleased to welcome Will as only the sixth CEO in our company's 96-year history," said Mr. Donahue. Six CEOs in 96 years—that's not corporate instability, it's institutional knowledge preservation. Each CEO serves for decades, learns from their predecessor, and grooms their successor. This continuity creates a corporate culture that transcends individuals.

The "distribution as a service" model creates switching costs that protect margins. When GPC serves a repair shop, they don't just deliver parts. They provide credit terms, handle warranty claims, offer technical support, manage returns, and provide inventory financing. Switching suppliers means replacing all these services, not just finding another parts source. The deeper the service relationship, the higher the switching cost.

Margin preservation in a competitive industry requires discipline. GPC doesn't win on price—they win on availability, reliability, and service. When competitors cut prices, GPC emphasizes their value proposition: the part you need, when you need it, with expertise included. This positioning requires confidence and patience. It means walking away from low-margin business. It means investing in service when others cut costs.

The international expansion strategy follows a specific template: enter through acquisition of established players, maintain local management and brands, gradually introduce best practices, and only then consider brand harmonization. This patient approach takes longer than aggressive standardization but produces better results. Local expertise remains while global scale advantages accumulate.

What makes GPC different isn't any single factor—it's the accumulation of small advantages compounded over decades. The dividend discipline that ensures financial conservatism. The network effects that create competitive moats. The service orientation that generates switching costs. The patient capital that enables counter-cyclical investment. The cultural continuity that preserves institutional knowledge. Together, these elements create a business model that's remarkably simple to understand but nearly impossible to replicate. It's not glamorous. It's not disruptive. It just works, year after year, dividend after dividend.

IX. Power Analysis & Competitive Position

The parking lot at a NAPA distribution center tells you everything about competitive advantage. At 5 AM, delivery trucks are already loading—drivers who know every pothole between here and their delivery routes, carrying parts ordered last night that mechanics need this morning. Down the street, an AutoZone sits empty, waiting for retail customers. This time advantage—the hours before competitors open—represents just one layer of GPC's competitive moat.

Scale economies in distribution follow power laws, not linear progressions. The difference between 100 locations and 1,000 isn't ten times the advantage—it's exponentially greater. With 10,700 locations globally, GPC operates at a scale where unit economics transform. They can stock parts that turn once a year because across their network, that part sells weekly. They can justify distribution centers in secondary markets because route density makes delivery profitable. They can negotiate with suppliers from a position where GPC represents 10%, 20%, sometimes 30% of a manufacturer's total volume.

The network effects compound these scale advantages. Every additional NAPA store makes the entire network more valuable. More stores mean more inventory turns, better parts availability, faster delivery, stronger supplier terms. A mechanic in Montana can access parts sitting in Minnesota through the NAPA network faster than Amazon can ship them. This isn't theoretical—it happens thousands of times daily.

Switching costs embed themselves at multiple levels. For repair shops, changing parts suppliers means new account setups, different part numbers, revised ordering processes, retrained staff, and lost warranty history. The shop's mechanics know NAPA part numbers by heart. The shop management software integrates with NAPA's systems. The delivery driver knows to leave parts in the third bay if no one's at the counter. These micro-frictions aggregate into macro-advantages.

The brand power of NAPA transcends marketing. When a customer says, "Get me a NAPA battery," they're not just requesting a product—they're expressing trust built over decades. NAPA means the part won't fail prematurely, the warranty will be honored, and if something goes wrong, there's a store nearby to make it right. This trust took 99 years to build. Competitors can't purchase it, can't replicate it quickly, and can't undermine it easily.

The competitive landscape reveals GPC's positioning. O'Reilly Automotive (ORLY), with a $70 billion market cap, focuses primarily on retail customers. AutoZone (AZO), valued at $55 billion, pioneered the DIY superstore model. Advance Auto Parts (AAP), struggling at $2 billion market cap, illustrates what happens when execution falters. Each competitor chose a different strategy. GPC chose not to choose—they serve everyone, but with clear priorities.

The commercial business—sales to repair shops—represents GPC's fortress. While competitors fight for price-conscious DIY customers, GPC dominates the professional market where relationships, reliability, and technical support matter more than saving fifty cents. A professional mechanic can't wait two days for Amazon delivery when a customer's car is on the lift. This immediacy requirement creates GPC's competitive space.

Amazon's entry into automotive parts sparked fear across the industry. The everything store would surely disrupt sleepy parts distributors. Reality proved different. Amazon excels at shipping predictable orders to patient customers. They struggle with urgent needs, technical questions, warranty handling, and commercial credit terms. A DIYer ordering floor mats? Amazon wins. A shop needing four brake calipers by noon with net-30 terms? That's GPC territory.

Digital threats require nuanced analysis. Can Uber-style delivery services disintermediate parts distribution? Can AI-powered procurement systems bypass traditional distributors? Can direct-to-consumer manufacturers eliminate the middleman? The answer to each is "partially." But partial disruption often strengthens incumbents who adapt. GPC's digital investments don't aim to become Amazon—they aim to become Amazon-proof.

The international expansion provides competitive insulation. While U.S. competitors remain largely domestic, GPC operates across North America, Europe, and Australasia. This geographic diversity reduces dependence on any single market. When U.S. automotive sales slowed in 2024, European operations provided stability. When Brexit disrupted UK operations, U.S. strength compensated. Diversification isn't just risk management—it's opportunity multiplication.

Industrial distribution through Motion Industries creates a second competitive arena with different dynamics. Competitors like W.W. Grainger (GWW) and Fastenal (FAST) focus on MRO supplies. Motion specializes in power transmission, bearings, and industrial automation—technical products requiring expertise. This specialization in complexity creates barriers. Anyone can sell toilet paper to factories. Fewer can specify the right bearing for a critical production application.

The strategic position reveals three sustainable advantages. First, route density in core markets makes last-mile delivery economically superior to any alternative. Second, technical expertise in complex parts creates value beyond simple fulfillment. Third, embedded relationships with professional customers generate switching costs that price competition can't overcome.

Market share data illustrates GPC's position. In U.S. automotive aftermarket distribution, GPC holds approximately 8% share—largest among distributors but fragmented enough for growth. In industrial distribution, Motion holds about 3% share in a $150 billion market. These shares seem modest until you realize the markets are so fragmented that 8% makes you the giant.

Competitive responses reveal respect for GPC's position. O'Reilly and AutoZone rarely attack GPC's commercial stronghold directly. Instead, they focus on retail expansion. Amazon partnered with repair shops rather than trying to replace distributors. Industrial competitors segment around Motion rather than through it. When competitors avoid direct confrontation, it signals strength.

The capital intensity of distribution creates barriers to new entrants. Building a distribution network requires billions in inventory, real estate, and working capital. But capital alone isn't enough—you also need relationships, systems, and expertise that only develop over time. A private equity firm can't simply buy their way into GPC's position. The Chinese can't export a competing model. Silicon Valley can't code around it.

Regulatory and environmental changes potentially strengthen GPC's position. Electric vehicles require fewer parts but more technical expertise. Environmental regulations increase parts complexity. Right-to-repair legislation protects independent repair shops—GPC's core customers. Each regulatory shift creates disruption that established players navigate better than upstarts.

The competitive analysis yields a paradox: GPC's greatest strength is that they're boring. They don't make headlines. Venture capitalists don't target them. Disruptors focus on sexier opportunities. This invisibility becomes armor. While everyone watches Amazon battle Walmart, GPC quietly compounds value, raises dividends, and strengthens their network. Sometimes the best competitive position is the one nobody notices until it's too late to challenge.

X. Bear vs. Bull Case

The bear case starts with a number that keeps automotive executives awake: 30. That's roughly how many moving parts in an electric vehicle drivetrain, compared to 2,000+ in a traditional internal combustion engine. Fewer parts mean fewer failures, fewer replacements, fewer trips to NAPA. If EVs achieve 50% market penetration by 2035, as some predict, GPC's addressable market could shrink dramatically.

The math is sobering. No oil changes, no transmission fluid, no spark plugs, no fuel filters, no exhaust systems. Regenerative braking extends brake pad life by 2-3x. Electric motors last 300,000+ miles versus 150,000 for combustion engines. Yes, EVs need tires, suspension components, and cabin filters. But the total parts content per vehicle lifecycle could drop 40-50%. For a business built on replacement parts, that's existential.

Direct-to-consumer threats multiply daily. Manufacturers increasingly sell parts directly online, bypassing distributors. Tesla services its vehicles through company-owned centers, cutting traditional distributors entirely from the value chain. Rock Auto ships parts directly from warehouses to consumers. Amazon Business targets commercial customers with algorithmic pricing and one-day delivery. Each channel shift strips away a piece of GPC's market.

The stock performance reflects these concerns: net income of $317 million, or $2.26 per diluted share in the prior year period. down 23.93% over 52 weeks while the S&P 500 hit record highs. The market clearly worries about GPC's future. When a dividend aristocrat trades at a discount, investors are pricing in problems.

Macro headwinds compound structural challenges. Industrial production slowed throughout 2024. Automotive sales remain below pre-pandemic peaks. Interest rates pressure consumer spending. Inflation squeezes margins. The company's own CEO acknowledged these challenges, focusing on "controlling what we could" rather than promising growth. When management emphasizes defense over offense, concerns are legitimate.

Debt levels from acquisitions constrain flexibility. The $2 billion Alliance Automotive acquisition added significant leverage. While manageable at current interest rates, this debt limits future acquisition capacity and reduces financial flexibility. If operations deteriorate, dividend sustainability could come into question—breaking a 69-year streak would devastate the stock.

But the bull case starts with reality, not projection. The company has paid a cash dividend every year since going public in 1948, and 2025 marks the 69th consecutive yea of dividend increases. Companies don't achieve such streaks by accident. They do it through business models resilient enough to survive everything from world wars to global pandemics.

The aging vehicle fleet provides immediate opportunity. Average U.S. vehicle age reached 12.5 years in 2024, the highest ever recorded. Vehicles aged 6-11 years—prime repair age—represent the fastest-growing segment. These vehicles need parts, regardless of economic conditions. An aging fleet is GPC's sweet spot: too old for warranties, too valuable to scrap, requiring constant maintenance.

EV disruption timeline remains uncertain. Despite headlines, EVs represent only 7.6% of U.S. sales in 2024. Full fleet turnover takes 20+ years. Charging infrastructure remains inadequate. Battery replacement costs shock consumers. Cold weather performance disappoints. The combustion engine's death, to paraphrase Mark Twain, has been greatly exaggerated.

Moreover, EVs create new opportunities. Battery thermal management systems require sophisticated cooling components. High-voltage systems need specialized safety equipment. Software updates create service opportunities. Electric vehicles still need tires, brakes, suspension—often specialized versions costing more than traditional equivalents. The parts mix changes, but demand continues.

Consolidation opportunities abound globally. The automotive aftermarket remains highly fragmented, especially internationally. Thousands of small distributors lack scale to compete effectively. GPC can acquire these businesses at reasonable multiples, integrate them into the network, and extract synergies. The AAG acquisition playbook can repeat across Europe, Asia, and Latin America.

The fundamentals remain strong: 19.13% return on equity demonstrates efficient capital utilization. 3.51% dividend yield attracts income investors in a low-rate environment. The balance sheet, while leveraged from acquisitions, remains investment-grade. Cash flow generation continues robustly. These aren't the metrics of a dying business.

The recession-resistant model provides downside protection. History shows that economic downturns often help GPC. When unemployment rises, people repair rather than replace vehicles. When corporate profits fall, companies extend equipment life. The worse the economy, the better the parts business. Few companies can claim countercyclical dynamics this strong.

The irreplaceable distribution network represents the ultimate moat. Rebuilding GPC's infrastructure would cost tens of billions and take decades. The relationship network can't be replicated digitally. The technical expertise requires human knowledge. Same-day delivery demands physical proximity. These advantages don't disappear because Tesla sells cars online.

International expansion provides growth runway. Europe's aftermarket is consolidating rapidly. Asia's vehicle fleet is aging. Latin America lacks organized distribution. GPC has proven it can export its model successfully. With only 17 countries currently served, geographic expansion could drive decades of growth.

Management quality inspires confidence. "I am humbled and honored for the opportunity to lead Genuine Parts Company and especially grateful for my GPC teammates and the support of Paul and the board of directors," said Mr. Stengel. "We will continue to build on the strong foundation laid over many years as we work to deliver solutions for our customers, invest in talent and capabilities and create value for our shareholders." Will Stengel brings digital expertise while respecting GPC's culture. The leadership transition proceeded smoothly. The company adapts without abandoning core principles.

The valuation argument is compelling. At $119 per share, GPC trades at 14x earnings versus historical averages near 18x. The 3.51% dividend yield exceeds 10-year Treasury rates. If EVs destroy the business slowly, you collect dividends while waiting. If fears prove overblown, multiple expansion provides upside. Heads you win, tails you don't lose much.

The bear-bull debate ultimately comes down to timeframe and temperament. Bears see disruption accelerating, margins compressing, and growth stalling. Bulls see adaptation continuing, moats holding, and dividends growing. Both sides have merit. But history suggests betting against companies that have survived 96 years and raised dividends for 69 consecutive years requires compelling evidence of imminent collapse. That evidence, despite real challenges, doesn't yet exist.

The stock may frustrate growth investors and worry technology enthusiasts. But for patient investors seeking defensive growth and reliable income, GPC offers something increasingly rare: a business model that has proven its resilience across economic cycles, technological changes, and competitive threats. Sometimes boring is beautiful, especially when boring pays dividends every quarter for seven decades running.

XI. Recent News

The boardroom at GPC's Atlanta headquarters buzzed with controlled tension in February 2025. The company's Board of Directors approved a 3% increase in its regular quarterly cash dividend for 2025. This increased the cash dividend payable to an annual rate of $4.12 per share from $4.00 per share in 2024. The quarterly cash dividend of $1.03 per share is payable April 2, 2025 to shareholders of record March 7, 2025. The company has paid a cash dividend every year since going public in 1948, and 2025 marks the 69th consecutive year of increased dividends paid to shareholders. The streak continues, but beneath the celebration lay complex realities.

Sales for the twelve months ended December 31, 2024 were $23.5 billion, up 1.7% from the same period in 2023. Net income for the twelve months was $904 million, or $6.47 per diluted share, compared to $9.33 per diluted share in 2023. Adjusted net income for 2024 was $1.1 billion, or $8.16 per diluted share, a decrease of 12.5% compared to $9.33 per diluted share in 2023. Revenue growth barely exceeded inflation while earnings declined materially—not the headlines you want when announcing a dividend increase.

The restructuring announcement revealed management's response to margin pressure. In 2024, the company announced a global restructuring designed to better align the company's assets and further improve the efficiency of the business. Throughout 2024, the efforts progressed as planned, delivering cost savings at the high end of the company's expectations. During 2025, the company will expand its restructuring efforts and take additional cost actions. It expects to incur additional costs of approximately $150 million to $180 million in 2025, which will continue to be reported as a non-recurring expense. Through these efforts, the company expects to realize approximately $100 million to $125 million of additional savings in 2025. When fully annualized in 2026, the company expects 2024 and 2025 restructuring efforts and cost actions will deliver approximately $200 million of cost savings.

The restructuring scale—$200 million in annualized savings—represents nearly 20% of current net income. This isn't trimming fat; it's fundamental reorganization. Distribution center consolidations, headcount reductions, process automation—the playbook for a mature business facing margin compression.

Will Stengel's first full year as CEO brought immediate challenges. "We had a solid start to 2025, despite the tariffs and trade dynamics that are impacting the operating landscape," said Will Stengel, President and Chief Executive Officer. "We remain focused on what we can control—excellent customer service and our strategic initiatives to improve the business. I am proud of our teammates across the globe and want to thank them for their dedication to serving our customers."

The tariff mention deserves attention. changes in general economic conditions, including unemployment, inflation (including the direct and indirect impact of tariffs and other similar measures, as well as the potential impact of retaliatory tariffs and other similar actions) Trade policy uncertainty creates inventory management challenges, margin pressure from cost increases, and potential supply chain disruptions—complications GPC hasn't faced at this scale before.

Q1 2025 results showed mixed signals. Sales were $5.9 billion, a 1.4% increase compared to $5.8 billion in the same period of the prior year. The improvement is attributable to a 3.0% benefit from acquisitions, partially offset by a 0.8% decrease in comparable sales and a 0.8% net unfavorable impact of foreign currency and other. Acquisitions drive growth while organic sales decline—a concerning trend for a business model built on same-store sales growth.

The automotive-industrial divergence intensified. Global Automotive sales were $3.7 billion, up 2.5% from the same period in 2024. The improvement is attributable to a 4.1% benefit from acquisitions, partially offset by 0.8% decrease in comparable sales and a 0.8% net unfavorable impact of foreign currency and other. The one less selling day in the U.S. compared to the prior year period negatively impacted Global Automotive sales growth and comparable sales growth by approximately 0.9%. Segment EBITDA of $286 million decreased 10.7%, with segment EBITDA margin of 7.8%, down 110 basis points from the same period of the prior year.

Industrial weakness persisted. Industrial sales were $2.2 billion, down 0.4% from the same period in 2024, with a 1.3% benefit from acquisitions, offset by a 0.7% decrease in comparable sales and 1.0% unfavorable impact of foreign currency. The one less selling day in the U.S. compared to the prior year period negatively impacted Global Industrial sales growth and comparable sales growth by approximately 1.5%. Manufacturing slowdown hits Motion Industries directly—when factories reduce production, industrial parts demand falls immediately.

By Q2 2025, management revised expectations downward. "Our results for the quarter were in line with our expectations and reflect the execution of our strategic initiatives and cost restructuring actions against continued challenging market conditions," said Will Stengel, President and Chief Executive Officer. "As we turn to the second half of the year, we remain focused on what we can control as we proactively manage through an evolving external environment. I want to thank our teammates across the globe for their relentless dedication and commitment to serving our customers."

Cash flow deterioration raised concerns. The company generated cash flow from operations of $169 million for the first six months of 2025. The reduction in the company's operating cash flows year-over-year is driven by lower net income, accelerated tax payments versus 2024 and changes in working capital. Free cash flow was a deficit of $80 million for the first six months of 2025 after giving effect to $249 million in capital expenditures. Negative free cash flow in H1—while investing for the future—pressures the dividend aristocrat status.

Debt levels reflect acquisition appetite. You can click the graphic below for the historical numbers, but it shows that as of June 2025 Genuine Parts had US$4.81b of debt, an increase on US$3.88b, over one year. Nearly $1 billion in additional debt year-over-year funds acquisitions but reduces financial flexibility.

The competitive landscape shifted dramatically with Advance Auto Parts' struggles. While AAP closes stores and restructures, GPC gains market share—illustrating that execution matters more than market conditions. O'Reilly and AutoZone continue aggressive expansion, but their focus on retail DIY leaves GPC's commercial stronghold relatively protected.

International operations face unique pressures. European markets, particularly through AAG, confront economic slowdown and competitive intensity. The strong dollar creates translation headwinds. Yet international diversification provides portfolio balance when U.S. markets weaken.

The dividend aristocrat analysis group highlights GPC's position. GPC, a Dividend King with 69 consecutive years of dividend increases, faces challenges like market competition and the rise of electric vehicles (EVs). As a Dividend King, GPC has increased its dividend for 69 consecutive years, a testament to its financial stability. The company recently raised its annual payout to $4.12 per share. According to Monexa AI, GPC's dividend yield is approximately 3.29%, making it attractive for income-seeking investors.

Looking ahead, management's 2025 guidance suggests cautious optimism. Revenue growth of 2-4%, adjusted EPS of $7.75-$8.25, and operating cash flow between $1.2-$1.4 billion—solid but unspectacular targets reflecting current realities. The restructuring benefits should materialize in 2026, potentially restoring margin expansion.

The recent news narrative reveals a company in transition: navigating near-term headwinds while investing for long-term positioning, maintaining dividend aristocrat status despite earnings pressure, executing strategic restructuring while serving customers daily, and adapting to technological change while preserving cultural continuity. These aren't contradictions—they're the complexities of managing a 96-year-old business in rapidly changing markets.

XII. Links & Resources

For investors and analysts seeking deeper understanding of Genuine Parts Company, the following resources provide essential information:

Official Company Resources: - Investor Relations: https://www.genpt.com/investors - Annual Reports & SEC Filings: Available through investor relations portal - Earnings Calls & Presentations: Quarterly webcasts archived on company website - NAPA Auto Parts: https://www.napaonline.com - Motion Industries: https://www.motionindustries.com

Financial Data & Analysis: - NYSE: GPC - Real-time stock quotes and historical data - EDGAR Database: SEC filings including 10-K, 10-Q, and proxy statements - Dividend History: 76 consecutive years of payments, 69 years of increases

Industry Resources: - Automotive Aftermarket Suppliers Association (AASA) - Auto Care Association - Industry statistics and trends - Industrial Distribution Magazine - Motion Industries coverage

Historical & Background: - Automotive Hall of Fame - Carlyle Fraser and Wilton Looney profiles - NAPA History & Heritage - Company museum and archives - Atlanta History Center - GPC corporate archives

Competitive Intelligence:

- O'Reilly Automotive (ORLY) investor relations

- AutoZone (AZO) investor materials

- Advance Auto Parts (AAP) financial reports

- W.W. Grainger (GWW) - Industrial distribution comparison

Key Company Metrics: - Founded: 1928 - Headquarters: Atlanta, Georgia - Employees: ~63,000 globally - Locations: 10,700+ across 17 countries - Stock Symbol: NYSE: GPC - Market Cap: ~$16.94 billion (as of late 2024) - Annual Revenue: $23.5 billion (2024)

Subsidiary & Brand Websites: - Alliance Automotive Group (Europe): https://allianceautomotivegroup.eu - UAP Inc. (Canada): https://www.uapinc.com - GPC Asia Pacific: https://gpcasiapac.com

For those interested in the broader themes explored in this analysis—patient capital allocation, distribution economics, network effects in traditional industries—GPC represents a masterclass in building enduring competitive advantages through operational excellence rather than technological disruption.

The company's investor relations team can be reached at (678) 934-5000 for specific inquiries. Quarterly earnings calls typically occur within 30 days of quarter-end, with materials posted to the investor relations website prior to market open.

This analysis draws from public sources and represents independent research. As with all investment decisions, readers should conduct their own due diligence and consider their individual financial objectives and risk tolerance. Past performance, including GPC's remarkable dividend history, does not guarantee future results.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube