Canada Goose: The Masterclass in Extreme-Weather Luxury

I. Introduction & The $1,500 Parka Phenomenon

Walk down a January sidewalk in Manhattan, Yorkville, or 静安区 Jing'an in Shanghai and you will see it before you see the person wearing it: a small circular patch on the left sleeve, a stylized map of the Arctic ringed in red, white, and blue, stitched onto a jacket that costs more than most people's monthly rent. The patch does not advertise a logo in the way a Louis Vuitton monogram does. It advertises something stranger — the idea that the wearer is dressed for a scientific expedition to the South Pole, even though the wearer is, in fact, waiting for an Uber.

This is the central magic trick of Canada Goose Holdings Inc. A company that began as a cramped garment shop above a Toronto street, stitching wool vests and snowmobile suits for tradesmen, turned a piece of genuinely technical survival equipment into one of the most recognizable luxury status symbols on earth. The flagship Expedition Parka retails well north of $1,500, and for years people lined up in the cold to buy one. How does a working-class utility brand become a global fashion object without losing the authenticity that made it desirable in the first place? And what happens when the thing that fueled the ascent — scarcity, cold-weather mystique, "Made in Canada" pride — collides with the unglamorous arithmetic of running eighty-eight retail stores across three continents?

Consider the sheer improbability of the transformation. Down-filled parkas are, at the level of raw materials, a commodity. Goose down is goose down; nylon shell is nylon shell; a zipper is a zipper. There is no patented molecule inside a Canada Goose jacket, no proprietary chip, no line of code that a competitor cannot replicate. And yet the company persuaded millions of affluent consumers around the world to pay two, three, sometimes four times what a functionally similar coat costs, and to feel good about doing it. That is the essence of a luxury business — the ability to sell meaning at a premium to materials — and it is also its Achilles' heel, because meaning is fragile in a way that a factory or a patent is not. A brand can be red-hot for a decade and cold within two seasons, and the graveyard of once-coveted fashion labels is deep. The entire investment question with Canada Goose reduces, in the end, to a single wager: is the meaning it has manufactured durable, or is it a moment?

That collision is the story of the modern company. In fiscal 2026, the year ended March 29, 2026, Canada Goose generated CA$1,528.2 million in revenue, up 13.3% year over year, with a gross margin of 69.7% that would make most luxury houses envious.1 And yet operating income in that same year fell from CA$164.1 million to CA$88.8 million — nearly cut in half — as the cost of running a global retail and marketing machine swallowed the brand's extraordinary gross profit.1 The paradox of Canada Goose today is that the product has never been more profitable to make, and the business has rarely looked harder to run.

This is the arc we will trace. First, the improbable journey from a private-label contract manufacturer to a premium direct-to-consumer juggernaut. Second, the defining strategic bet of third-generation leader Dani Reiss — the refusal to move manufacturing offshore, a decision that looked like stubbornness and turned out to be a marketing masterstroke. Third, the Bain Capital era, which re-engineered the company from a low-margin wholesaler into a high-margin retailer and took it public in 2017. And finally, the present chapter of friction: bloated overhead, a corporate restructuring, a heavy dependence on China, and the swirl of take-private speculation that in August 2025 put a roughly US$1.4 billion price tag on the company's head.2 The Arctic patch still commands a premium. The question for investors is whether the business underneath it does.

Keep two facts in mind as the story unfolds, because they frame everything. The first is that the company's peak public valuation, reached in 2018, was roughly US$7.7 billion — and the take-private interest that surfaced in 2025 valued it at less than a fifth of that.2 Something went wrong between the euphoria and the present, and it was not the product, which still sells at full price. The second is the margin paradox already noted: a business that keeps nearly seventy cents of gross profit on every revenue dollar somehow lets most of that profit evaporate before it reaches the operating line. Hold those two facts together — a collapsed valuation and a leaking income statement despite an intact brand — and you have the tension that animates this entire episode. This is not a story about whether people want the jackets. It is a story about whether a wonderful brand can be turned into a wonderful business, and about the very specific ways that translation has, so far, proven harder than anyone at the 2017 IPO would have guessed.

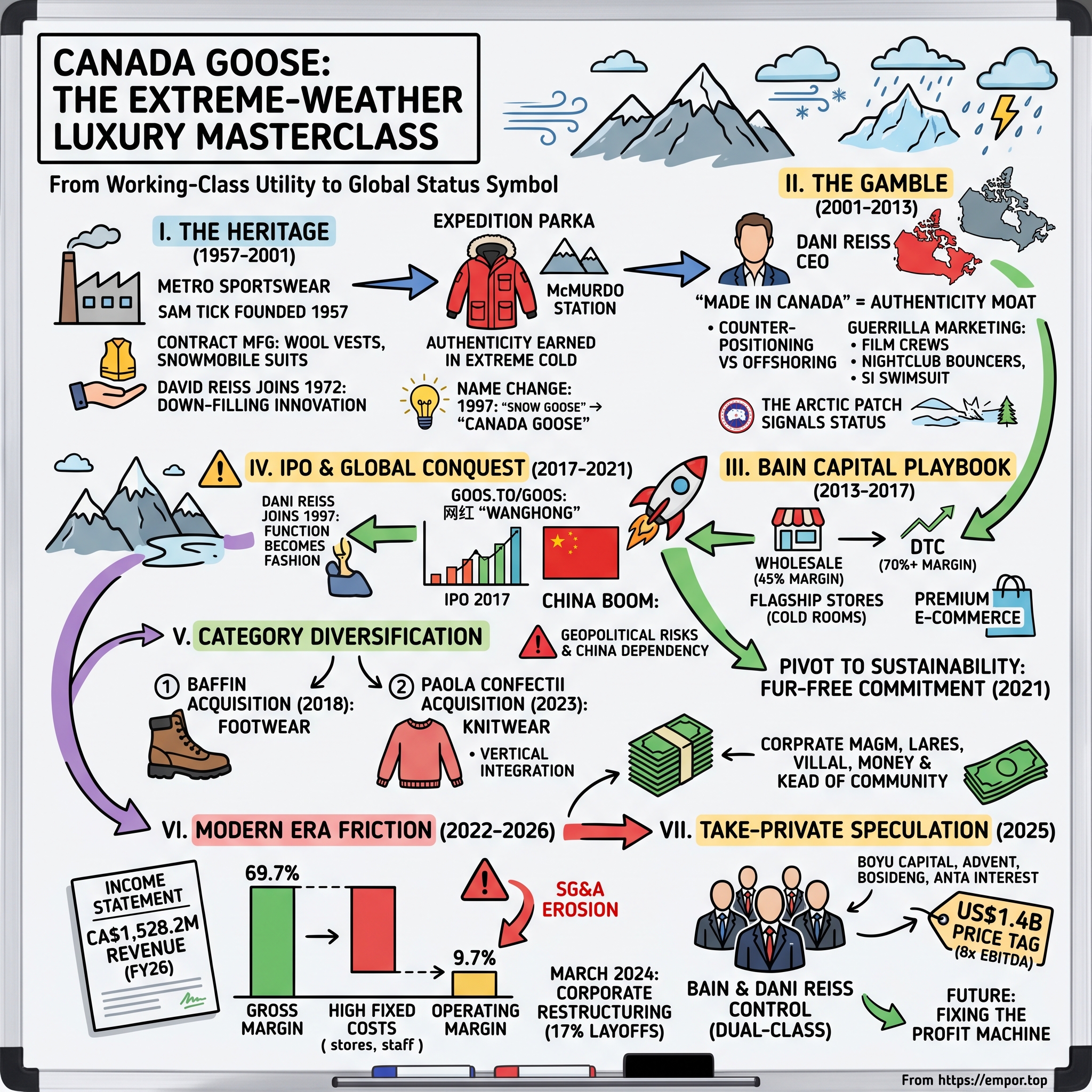

II. The Heritage of Metro Sportswear: From Working-Class Utility to Arctic Royalty (1957–2001)

The origin story does not begin with luxury. It begins with a Polish immigrant named Sam Tick, who in 1957 founded a small outerwear manufacturer called Metro Sportswear Ltd. in Toronto. The customers were not fashion editors; they were the people who had to work outside in a Canadian winter. Metro made wool vests, raincoats, snowmobile suits, and heavy-duty coats — utilitarian gear sold, for the most part, under other companies' labels. This was the unglamorous business of contract manufacturing, where a factory's competitive edge is measured in stitch quality and cost per unit, not brand desire.

The first inflection came in 1972, when Tick's son-in-law, David Reiss, joined the company. Reiss was a builder and a tinkerer, and his signature contribution was mechanical rather than fashionable: he developed a volume-based down-filling machine, a way to inject goose down into garments consistently and at scale. That single innovation shifted the factory's center of gravity from generic outerwear toward high-performance, down-filled jackets — the product category that would eventually define the brand. It is worth pausing on the significance: the company's identity as a maker of serious cold-weather insulation was rooted in a manufacturing capability, not a design aesthetic. The warmth came first; the cool came much later.

Through the 1970s and 1980s, Metro built its reputation the hard way, by outfitting people whose lives depended on staying warm. It made coats for police forces, for municipal workers, for forest rangers. Its most storied product, the Expedition Parka, was developed for scientists stationed at Antarctica's McMurdo Station, where the garment had to perform in temperatures that kill. This was authenticity you could not manufacture in a marketing department — the brand earned its extreme-weather credibility in the actual extreme, decades before anyone thought to wear the parka to a nightclub.

It is worth dwelling on why this matters, because it is the load-bearing wall of everything Canada Goose would later become. Luxury brands spend fortunes trying to invent heritage — to conjure a story of craft, purpose, and provenance that justifies a premium. Canada Goose acquired its heritage the only way that is truly unfakeable: by decades of making functional gear for people in genuinely hostile conditions, with no thought whatsoever of glamour. The rangers, the researchers, the workers on Arctic oil rigs — they were not a marketing campaign. They were the actual customer base, and the demanding customer base at that. A jacket that fails in downtown Toronto is an inconvenience; a jacket that fails at McMurdo is a medical emergency. That is a very different design discipline, and the brand equity it produced later was, in a real sense, earned before it was ever monetized. When the fashion world eventually discovered Canada Goose, it discovered a company that already had the one thing money genuinely cannot buy: a credible reason to exist.

Then came the accident that named a legend. David Reiss launched a consumer-facing brand called "Snow Goose." When the company began pushing into Europe in the 1990s, it discovered the name was already trademarked there. Forced to improvise, Reiss coined a replacement: "Canada Goose." It was a workaround, born of a legal conflict, and it turned out to be the single most valuable asset the company would ever create — a name that fused the country's rugged image with the migratory bird built for cold. Half a moat is sometimes an accident you were smart enough not to undo.

The final piece of the pre-modern story is a person. In 1997, David's son Dani Reiss joined the family business. He was not an obvious heir — a short-story writer by temperament, he had little initial interest in outerwear and reportedly intended only a brief stint before pursuing a literary life. What changed his mind was a pattern he noticed at European trade shows: adventurers and buyers were drawn to these jackets not merely because they worked, but because they looked like the real thing. Function was becoming fashion in front of his eyes.[^3]

There is a family-business archetype worth naming here, because Reiss would spend his career defying it. The old proverb holds that the first generation builds, the second maintains, and the third destroys — the "third-generation curse," in which heirs inherit wealth they did not create and squander an empire they do not understand. Dani Reiss was, by any literal reading, the third generation: grandson of the founder Sam Tick, son of the operator David Reiss. A writer with no burning desire to run a coat factory is precisely the profile that fulfills the curse. Instead, he became the person who saw the latent luxury brand hiding inside the industrial manufacturer — arguably a clearer view than either of his predecessors had, precisely because he came at it as an outsider who understood story rather than as a lifer who understood stitching. In 2001, Dani Reiss became chief executive, inheriting a profitable but small manufacturer with a great name and an untold story.[^3] The raw materials of a luxury brand were all there. What they lacked was someone willing to bet the company on them — and to do it, contrarily, by keeping the factory at home.

III. The Dani Reiss Revolution: The Gamble on "Made in Canada" (2001–2013)

Picture the early 2000s in the North American apparel industry. The offshoring wave was not a trend; it was gospel. Nearly every outerwear brand — including technical rivals like Arc'teryx — was moving production to Asia to slash labor costs, and Wall Street rewarded the ones that did. Against that consensus, a young CEO running a modest Toronto manufacturer made a decision that his own advisors and much of the industry considered close to irrational: Canada Goose would keep making its jackets in Canada.

The economics of that choice were, on paper, terrible. Domestic labor was expensive, which compressed margins. Domestic capacity was finite, which capped growth — you cannot simply order another million units when your factories and skilled sewers are the bottleneck. In a purely spreadsheet-driven analysis, "Made in Canada" was a self-imposed handicap. But Reiss understood something the spreadsheet missed. The manufacturing location was not a cost line; it was the proof of authenticity that could justify a luxury price. His analogy became a company mantra: making Canada Goose jackets in Asia would be like making Swiss watches in China. The origin was the product. Strip it away and you are left with an expensive coat that anyone could copy.

This is the strategic heart of the early Reiss era, and it deserves an honest, two-sided reading. "Made in Canada" was a genuine differentiator and a brilliant piece of positioning — a story competitors literally could not tell. But it was also a constraint that would later shape the company's biggest tensions, from capacity limits to the eventual acquisition of overseas facilities. The bet worked because Reiss paired it with something equally important: he built brand heat almost for free.

There is a deeper strategic principle buried in the "Made in Canada" decision, and it is one Hamilton Helmer would recognize as counter-positioning. Reiss was not merely choosing a marketing angle; he was choosing a business model his larger, offshored competitors could not copy without cannibalizing themselves. A rival that had spent a decade moving production to Asia to please cost-focused buyers could not credibly reverse course and claim domestic authenticity — its whole cost structure and supply chain were built the other way. The incumbent's greatest strength, cheap offshore production, became the very thing that locked it out of the premium-authenticity position Canada Goose was staking. For a window of years, that was a real and defensible edge. The catch, which we will return to, is that counter-positioning is only a moat while the incumbent refuses to follow. As the whole industry drifted toward "gorpcore" — technical outdoor gear as high fashion — the position Canada Goose pioneered became crowded with imitators who learned to tell heritage stories of their own.

With no traditional advertising budget to speak of, Reiss ran a guerrilla seeding strategy that reads today like a case study in earned cultural relevance. The genius of it was that it never looked like marketing, because in a sense it wasn't — it started with a genuine functional need. Film crews shooting in freezing conditions were given jackets to keep their people warm on set, and warmth on a frozen location shoot is not a favor, it is a necessity. Directors and actors started keeping the coats, wearing them off-camera between takes, and then the parkas began drifting on-screen — appearing in cold-weather productions where the wardrobe department reached for the real thing because it was already there and it actually worked. A disaster epic set in a freezing New York, an adventure film in a wintry landscape: the jacket showed up not as a paid placement but as the authentic choice of people who needed to stay warm while pretending to freeze. That distinction matters enormously, because audiences are exquisitely sensitive to the difference between a product placed and a product genuinely worn.

The brand extended the same logic outward in every direction. It rode high-visibility cultural moments, including a memorable Sports Illustrated Swimsuit shoot in Antarctica, where a model in a bikini and a Canada Goose parka fused two forms of aspiration in a single unforgettable image. And in a move that captured the brand's knowing relationship with exclusivity, jackets were gifted to the bouncers outside elite London and New York nightclubs — the literal gatekeepers of cool, standing in the cold all night, now wrapped in the warmest and most conspicuous coat on the sidewalk. Think about the semiotics of that placement: the person who decides who gets in is wearing your coat, which makes your coat the uniform of the in-crowd's border guard. None of this was mass advertising. All of it signaled the same message through a hundred small channels — that the people who really knew, the ones who worked in the cold and the ones who partied past it, wore Canada Goose. It was a masterclass in building desire through association rather than assertion, and it cost a fraction of what a conventional luxury advertising campaign would have.

Underneath the marketing sat a deliberately technical spine. The company promoted a Thermal Experience Index, a simple warmth-rating scale that told a customer which jacket suited which conditions. It was, in one sense, a merchandising tool. But it also reinforced the essential positioning: this is a piece of equipment engineered for a purpose, not a fashion item chasing a season.

That distinction is subtle but strategically enormous, and it is worth making explicit because it explains the pricing power. A pure fashion item is priced against taste, which is fickle and comparative — a consumer asks whether this coat is worth more than that coat this season. A piece of technical equipment is priced against performance and consequence — a consumer asks whether it will keep them warm at minus forty, and once convinced, becomes far less price-sensitive, because who negotiates on survival gear? By insisting on the utilitarian frame even as it sold to fashion buyers, Canada Goose got to have it both ways: the emotional desire of fashion married to the price-insensitivity of function. The warmth rating, the extreme-condition testing, the expedition heritage — these were not just storytelling flourishes. They were the mechanism that let the company hold a price that a fashion-only brand could never defend for a product with no proprietary technology inside it. That framing — utility first, status as a byproduct — let Canada Goose charge fashion-luxury prices while claiming the credibility of a technical outfitter. By 2013, the brand had heat, pricing power, and a story money could not buy. What it did not yet have was the capital and operating machine to turn that heat into a global company. That is precisely what arrived next, wearing a private-equity suit.

IV. The Bain Capital Playbook: Shifting from Wholesale to DTC (2013–2017)

In 2013, Bain Capital acquired a majority stake — roughly 70% — in Canada Goose, in a deal that reportedly valued the company at around US$250 million.2 For Dani Reiss, the appeal was not a cash-out but an accelerant: Bain brought the capital and the operational playbook to take a beloved Canadian brand global. For Bain, the appeal was a business with a rare combination — a product people loved, a story competitors couldn't replicate, and a margin structure that was being quietly given away to third parties.

That last point was the crux of the Bain thesis, and it is worth explaining in plain terms because it drove everything that followed. When Canada Goose sold a jacket through a wholesale partner — a Nordstrom, a Holt Renfrew, a sporting-goods chain — it captured a wholesale gross margin, historically in the neighborhood of 45–50%. The retailer pocketed the rest of the markup to the consumer. When Canada Goose sold that same jacket directly, through its own store or its own website, it captured the full retail spread, and gross margins on direct sales ran well above 70%. The product was identical. The difference in economics was entirely about who owned the customer relationship. Bain looked at that gap and saw the whole investment thesis: shift the mix from wholesale to direct-to-consumer, and you don't just grow revenue — you fundamentally re-rate the profitability of every jacket sold.

Executing that shift meant building a company Canada Goose had never been. It opened high-concept flagship stores in the cities that mattered — Toronto, New York, London, Tokyo — designed as brand temples as much as points of sale, some featuring cold rooms where shoppers could test a parka in sub-zero air. It built a localized, premium e-commerce platform so the online experience matched the price point. Each of these was a deliberate move up the value chain, trading the capital-light simplicity of wholesale for the capital-intensive control of owning distribution.

The trade-off embedded in that shift is one of the most important things to understand about the modern company, so it is worth spelling out in operational terms rather than abstract ones. A wholesale-led model is asset-light and risk-shifted: a retail partner takes the inventory, staffs the store, pays the rent, and absorbs the markdown risk if the season is warm. Canada Goose simply ships product and books a lower but reliable margin. A DTC model inverts every one of those relationships. Now Canada Goose signs the lease, hires and trains the sales associates, carries the inventory, builds and runs the website, and eats the loss if the coats do not sell. In exchange, it captures the full retail margin and — the part Bain prized most — it owns the customer relationship and the data that comes with it. This is a classic operating-leverage bet: you convert variable costs into fixed costs to capture more margin per sale, and it is spectacular when volumes are high and rising, and punishing when they flatten. The upside was margin and brand control. The cost — as the company would learn painfully a decade later — was a fixed overhead base that has to be fed whether or not the winter is cold and the shoppers show up. Bain and Reiss built the machine on the assumption that the demand would keep climbing fast enough to keep the machine full. For years it did.

The strategy culminated on March 16, 2017, when Canada Goose listed simultaneously on the Toronto Stock Exchange and the New York Stock Exchange under the ticker GOOS, pricing its initial public offering at CA$17.00 per share and raising roughly CA$340 million.[^3] The debut was a hit; the stock jumped on its first day, and the market embraced the story of a heritage Canadian brand with luxury margins and a long runway of global growth. Crucially, the offering locked in a dual-class share structure that concentrated voting control with Bain and Reiss — a governance choice whose consequences would echo through every future question about the company's ownership. Public investors were buying into the growth story; they were not buying the ability to steer it.

That governance choice deserves a moment of scrutiny rather than a passing mention, because it is the kind of structural detail that looks harmless in a boom and decisive in a crisis. A dual-class structure is a bargain offered to public markets: give the founders and their backers permanent control, and in return you get access to a company they would otherwise keep private. Investors accepted the bargain in 2017 because the growth was intoxicating and the alignment looked perfect — why worry about voting rights when the stock only goes up? The problem with permanent control is that it is permanent through the bad times too. When performance faltered and the shares fell, ordinary shareholders had no lever to pull: no ability to force a board refresh, no path to invite an activist, no vote that could compel a strategic change. They could sell, or they could wait. With fresh capital, a public currency, and a DTC engine just beginning to spin, Canada Goose entered its most euphoric phase — the years when the brand seemed to conquer everything it touched, and when the fine print of its governance seemed like someone else's problem.

V. The Public Markets and Global Conquest: Peak Brand Heat (2017–2021)

For a stretch after the IPO, Canada Goose looked unstoppable, and the market treated it that way — the company's value climbed to a peak of roughly US$7.7 billion in 2018, about a year after going public.2 The engine of that euphoria had a clear geographic center of gravity: China. When Canada Goose entered mainland China in 2018, it walked into a luxury market that was expanding faster than almost any in the world, and the brand's cold-weather mystique translated with startling ease. Store openings in Beijing and Shanghai drew hours-long queues, and the parkas earned the coveted label of 网红 wanghong — "internet-famous" — products that Chinese consumers photographed, shared, and desired as social currency. Greater China rapidly became the fastest-growing and one of the most profitable regions in the company, a high-margin retail engine bolted onto a Canadian heritage brand.

The China boom validated Bain's DTC thesis on a global scale, but it also planted a dependency the company is still managing today. When more than a third of your sales come from one region, that region's economy, real-estate sentiment, and consumer confidence become your economy too — a vulnerability that would move from theoretical to painfully concrete in the 2020s.

There was also a geopolitical dimension that the queues in Beijing obscured. Selling a Western luxury brand into China means operating at the mercy of forces entirely outside a company's control: currency swings, tariff regimes, and — most dangerously for a national-identity brand like this one — the risk of becoming a target in a diplomatic dispute. Canada Goose learned this early. When Canada-China relations soured in late 2018 following the arrest of a Chinese technology executive on a U.S. warrant, the brand found itself caught in the crossfire of nationalist sentiment online, its Beijing flagship opening delayed amid the tension. The episode was a preview of a structural truth: a brand whose very name invokes a foreign nation is uniquely exposed when that nation's relationship with China curdles. The China engine was, and remains, both the company's greatest growth story and its most concentrated political risk — a single market that can be turned against it by events on the evening news rather than anything happening in the stores.

The same period brought a reputational reckoning. Animal-rights activists, led by PETA, pressured the company for years over two natural materials at the core of its product: the coyote fur used on parka hoods and the down harvested for insulation. The campaigns were relentless, and they threatened the brand precisely where luxury brands are most exposed — in their public image. Canada Goose's response was a strategic pivot dressed as an ethical one. In 2021, the company committed to stop purchasing all fur, with the transition to be completed by the end of 2022. The move satisfied ESG-focused public investors and defused a persistent PR liability. But it is worth being clear-eyed about the trade-off: it also alienated some traditionalists who genuinely valued fur's performance against Arctic wind, and it quietly conceded that the brand's future lay more in the fashion-luxury tier than in the extreme-expedition niche where it was born. When a survival-gear company decides which of its features are negotiable, it is telling you what business it now believes it is in.

The fur decision also illustrates a recurring pattern in how Canada Goose manages reputational risk: it tends to convert a defensive necessity into an offensive narrative. Phasing out fur was, at root, a response to years of activist pressure and shifting consumer values — a cost of doing business in the modern luxury market. But the company packaged it as forward-looking leadership on sustainability, and layered on further commitments around responsible down sourcing and reclaimed materials. Whether one reads this as genuine values or savvy repositioning, the strategic effect is the same: it kept the brand acceptable to the ESG-minded institutional investors and younger consumers who increasingly drive luxury demand. The risk in the maneuver is authenticity dilution. A brand built on uncompromising extreme-weather function invites skepticism every time it subordinates performance to image, and the traditionalist who prized fur's real-world advantage in Arctic wind is a small but symbolically important constituency to lose.

Then came the pandemic, which by rights should have crushed a brand built on going outside and being seen. Instead, Canada Goose proved resilient. High-net-worth consumers, grounded from travel and flush with unspent discretionary income, redirected spending toward localized luxury, and the company's digital channel absorbed demand that would otherwise have flowed through stores. The premium aura held. But the pandemic's real lesson was about fragility as much as strength: it showed how much the model now depended on discretionary luxury spending and on a handful of affluent markets. As the world reopened, those dependencies — China, discretionary demand, a heavy fixed-cost retail base — would stop being tailwinds and start being the plot. Before we get there, though, the company was busy trying to become something more than a one-jacket, one-season business.

VI. Category Diversification and Vertically Integrated M&A: Baffin and Paola Confectii

Every seasonal business eventually confronts the same uncomfortable truth: it makes almost all of its money in a few cold months and spends the rest of the year waiting. For Canada Goose, the strategic answer was to extend the brand across more of the calendar and more of the body — and, characteristically, to do it by buying capability rather than borrowing prestige. Two acquisitions, five years apart, reveal how the company thinks about growth when it is being disciplined.

The first was footwear. In November 2018, Canada Goose acquired Baffin Inc., a Canadian maker of cold-weather boots, for CA$32.5 million.3 The logic was intuitive: if the brand defends people against extreme weather from the neck up, footwear was the natural extension downward. But the more telling detail is what kind of asset Canada Goose chose to buy. This was not a splashy fashion label acquired at a nosebleed multiple to buy relevance — the trap that ensnares so many luxury conglomerates. It was an industrial, utilitarian, cold-weather manufacturer bought for a modest sum. The capital allocation was conservative and on-brand. The results, however, have been patient at best: Canada Goose-branded footwear did not launch until 2021, was slow to scale, and by the mid-2020s had not become a material revenue driver. The lesson is a useful corrective to the brand's own mythology — extending a powerful brand into a new category is far harder and slower than it looks, even when the strategic fit is obvious and the price is right.

The second acquisition, in November 2023, was subtler and arguably smarter. Canada Goose acquired Paola Confectii, its long-time Romanian manufacturing partner, in a move that gave the company its first manufacturing facility in Europe.4 The strategic target here was margin and control, not category. By bringing a trusted knitwear producer in-house, Canada Goose deepened its vertical integration precisely in a high-margin, non-outerwear category — knitwear such as its HyBridge Knit line — and established a European production footprint from which to expand its spring, summer, and shoulder-season assortment. This is the "Made in Canada" philosophy adapted for a global reality: own the making, control the quality, capture the margin, but do it where it makes strategic sense rather than as dogma.

Note the intellectual honesty required to appreciate the Paola deal, because it complicates the founding myth. For two decades, "Made in Canada" was the brand's sacred proof point, the reason a jacket made offshore was supposedly unthinkable. Yet here the company was, buying a factory in Romania and openly planning to produce knitwear in Europe. Is that hypocrisy? Not quite — knitwear was never the heritage-defining category, and Canada Goose has been careful to keep its flagship down-filled parkas anchored to Canadian production while extending non-core categories elsewhere. But it does reveal that the "Made in Canada" principle was always more marketing asset than iron law, applied where it created pricing power and quietly relaxed where it did not. That is pragmatic management, not dogma, and investors should read it as such: the company will honor the heritage story exactly as far as it pays to, and no further. The vertical integration itself is sound industrial logic — owning a trusted supplier removes margin leakage and secures capacity — but it also adds fixed assets and manufacturing complexity to a company already struggling to control its cost base, a tension that runs quietly beneath the growth narrative.

Together, these deals sketch the diversification strategy and its central tension. The non-outerwear categories — knitwear, rainwear, lightweight down, apparel, footwear — are the company's answer to its brutal seasonality, and management has made expanding them a stated priority. But there is a delicate balance to strike, and it cuts against easy optimism. The heavyweight parkas still generate the overwhelming majority of cash flow and carry the brand equity that lets everything else command a premium. Diversification that dilutes the core, or that chases revenue into lower-margin, less-differentiated categories, would be a cure worse than the disease. The strategic prize is a genuine year-round brand; the strategic risk is becoming a mediocre generalist apparel company that happens to make a famous coat. Which of those Canada Goose is becoming is, more than anything, what the recent financials are trying to tell us.

VII. The Modern Era: Operational Friction, Restructuring, and the Chinese Power Dynamics (2022–2026)

On the morning of May 14, 2026, Dani Reiss framed the just-completed fiscal year as "a year of meaningful progress and execution against our goals," pointing to revenue growth that was "broad-based across regions and channels."1 Read the numbers underneath the quote, however, and a more complicated picture emerges — one where a spectacular product-margin story is being steadily eroded by the cost of the machine built to sell it.

Start with what is genuinely strong. Fiscal 2026 revenue reached CA$1,528.2 million, up 13.3%, with direct-to-consumer sales climbing 15.9% to CA$1,157.4 million — now roughly three-quarters of the business.1 Wholesale, the channel Bain spent a decade de-emphasizing, grew a more modest 11.7% to CA$291.2 million, while the small "Other" segment slipped to CA$79.6 million.1 DTC comparable sales grew 8.4% for the year and 10% in the fourth quarter — the fifth consecutive quarter of positive comparable growth.1 Gross margin held at an elite 69.7%, essentially flat versus 69.9% a year earlier.1 On the top line and at the product level, the brand's pricing power looks intact. This is not a company with a demand problem at the gross-profit line.

The fourth quarter, in particular, carried a note of momentum that management was eager to amplify. Revenue in the quarter jumped 17.9% to CA$453.3 million, with wholesale revenue surging 54.4% to CA$49.1 million as the company shipped its spring/summer 2026 order book earlier and its wholesale partners placed heavier in-season orders — a tentative sign that the wholesale channel, long treated as the poor cousin to DTC, may be stabilizing rather than shrinking.1 But the same quarter carries a cautionary lesson in reading Canada Goose's numbers: that early wholesale shipment timing flatters the quarter's growth while pulling forward sales that would otherwise have landed later, and the quarter's gross margin actually slipped to 69.6% from 71.3% a year earlier precisely because of that heavier wholesale mix and higher freight and duty costs.1 It is a small but instructive reminder that channel mix and shipment timing can make any single period look better or worse than the underlying trend, which is why the full-year figures — and the multi-year direction of margins — tell the truer story than any one quarter's headline.

The problem lives below it. Selling, general and administrative expenses ballooned to CA$976.7 million in fiscal 2026, from CA$779.0 million the prior year — a 25% jump that overwhelmed the CA$122 million of incremental gross profit and dragged operating income down from CA$164.1 million to CA$88.8 million.1 Management attributes the rise to "strategic investments in brand and marketing, product design and development, and our retail network," alongside discrete, non-recurring charges that included an arbitration payment to a former supplier and a bad-debt provision tied to a U.S. wholesale partner.1 Some of that spending is genuine investment; some is one-time noise. The cleaner read comes from adjusted EBIT, which strips out the discrete items: it fell from CA$171.4 million to CA$148.0 million, and adjusted EBIT margin compressed from 12.7% to 9.7%.1 Even on the company's own preferred, flattering metric, the profitability of the business went down in a year revenue went up. Reported net income attributable to shareholders fell to CA$22.5 million, or CA$0.23 per diluted share, from CA$94.8 million a year earlier.1 For a brand that sells the definition of pricing power, single-digit operating margins are the number that should keep management awake.

To see the mismatch in the sharpest relief, hold the two ends of the income statement side by side. Every incremental dollar of fiscal 2026 revenue arrived carrying roughly seventy cents of gross profit — elite economics by any standard. And yet, by the time the year's costs were paid, only about six cents of every revenue dollar survived to the operating line. That gap is the entire modern predicament of Canada Goose in a single sentence. It is not that the jackets are unprofitable; it is that the apparatus assembled to sell them — the stores, the marketing, the corporate headcount, the product-development pipeline — consumes so much of the gross profit that the shareholder is left with a sliver. A skeptical investor looks at that and asks the obvious question: if a 70%-gross-margin brand cannot convert that into a healthy operating margin, is the problem the market, or is it management's cost discipline? The company's own fiscal 2027 plan, promising SG&A to decline as a share of revenue, is a tacit acknowledgment that the honest answer is at least partly the latter.1

The balance sheet, at least, is not the source of anxiety. Canada Goose ended fiscal 2026 with inventory of CA$386.3 million — essentially flat year over year, which management pointed to as evidence of proactive stock control — and it reduced net debt by 6% to CA$383.2 million, keeping leverage at a manageable 1.3 times EBITDA.1 This matters because it removes the most acute form of pressure: the company is not fighting a solvency or refinancing crisis, and it is not being forced into fire-sale discounting by a mountain of unsold coats. That relative financial stability is what gives management the room to attempt an operational turnaround on its own timeline rather than under duress — and it is also, not incidentally, what makes the company an attractive and financeable take-private target. The problem to be fixed is a profitability problem, not a survival problem, which is a considerably better position to argue from.

The overhead did not appear from nowhere. It is the accumulated weight of the DTC land-grab — a store network that reached 88 permanent locations globally at year-end fiscal 2026, up nine net new stores in the year, each carrying rent, staff, and depreciation that must be paid in July as surely as in January.1 That structural mismatch — fixed costs spread evenly across a year, revenue crammed into a few cold months — is the mechanical reason a 70%-gross-margin business can post a sub-10% operating margin. It is also why, in March 2024, management was forced into a blunt corrective: a restructuring that eliminated roughly 17% of the company's global corporate workforce in an effort to rein in overhead.[^6] That layoffs came at all is the most honest admission available that the cost base had outrun the business.

Geographically, the center of gravity has shifted decisively east. Asia Pacific — overwhelmingly Greater China — has grown into one of the company's two largest regions alongside North America, with each contributing on the order of CA$0.6 billion in fiscal 2026, and Greater China standing as the single largest and fastest-growing market.1 That is a triumph of the 2018 China entry and a concentration risk in equal measure. When a slowing Chinese economy, a wobbly property market, or a bout of luxury-spending caution arrives, it lands directly on Canada Goose's revenue line with little to offset it. Diversification of geography, like diversification of product, remains a work in progress rather than an accomplished fact.

Layered on top of that concentration is a trade-policy exposure that has moved from background noise to boardroom priority. A company that deliberately manufactures in high-cost Canada and sells a large share of its output into the United States and China is, by construction, exposed to tariffs and shifting trade rules in a way an offshored competitor spreading production across many countries is not. The "Made in Canada" identity that generates the brand's pricing power is also a geographic bet on the stability of North American and cross-Pacific trade — a bet that looks far less comfortable in an era of rising protectionism. Management's own fiscal 2027 outlook is explicit that it assumes the tariff environment stays "unchanged" from fiscal 2026, an assumption that is really a disclosed risk in disguise: if trade barriers escalate, the concentrated, home-country manufacturing base that is the brand's greatest romantic asset becomes a very real margin liability.1 It is a striking illustration of how the same strategic choice can be a moat and a vulnerability depending on which way the political wind blows.

The most revealing part of the modern story is the gap between the prepared remarks and the analyst Q&A. In scripted comments, Reiss reliably emphasizes "brand momentum," store expansion, and "deliberate lifestyle product diversification" into knitwear and eyewear — the language of a brand in control of its narrative. On the fiscal 2026 results, he framed the year as "meaningful progress," citing "stronger conversion in DTC, improved wholesale performance, and continued momentum across our expanded product offering," and told investors that entering fiscal 2027 the focus is "to convert brand momentum and a stronger operating foundation into sustainable EBIT margin expansion, starting this year."1 It is confident, forward-leaning language — the vocabulary of a leader asking to be judged on the coming turnaround rather than the just-finished compression.

The pushback from Bay Street and Wall Street runs in the other direction. Analysts press on SG&A efficiency, on the CA$8.4 million store-impairment charge taken in the fourth quarter after a review of underperforming locations — a charge that, however small in absolute terms, is management's own admission that some of the DTC build-out was overbuilt — on inventory turns, and on why operating margins are compressing so sharply when gross margins sit near seventy percent.1 The healthy way to weigh management credibility here is behaviorally, over time. On one hand, the fact that leadership executed a painful 17% corporate layoff in 2024, took visible impairments, and then published a specific, numeric fiscal 2027 margin target rather than a vague aspiration counts in its favor — these are the actions of a team confronting the cost problem rather than talking past it.[^6] On the other, the very need for those corrective actions is evidence that the cost base was allowed to run well ahead of the business in the first place, and a target is a promise, not a result. Management's fiscal 2027 outlook — low-single-digit revenue growth and an adjusted EBIT margin of 11–12%, explicitly assuming softer consumer demand and reduced travel while pricing actions and operational efficiencies drive the margin recovery — is, in effect, a commitment to begin fixing exactly this.1 It is a credible-sounding plan built on levers the company genuinely controls. Whether it is a delivered one is the open question, and it is being asked against the backdrop of a far larger question about who will own the company at all.

VIII. The Take-Private Speculation & Governance Under Dual-Class Control

Private equity firms are not known for their patience, which is what made the summer of 2025 so remarkable. Bain Capital had by then held its controlling position in Canada Goose for roughly twelve years — an extraordinarily long hold for a buyout fund, which typically aims to enter and exit within five to seven. The long hold was itself a signal: the easy, fast money had not materialized the way it might have looked destined to in 2018. And so Bain began, quietly and then not so quietly, to look for the exit.

On August 27, 2025, the search became public. Reports emerged that Bain had drawn take-private interest valuing Canada Goose at roughly US$1.4 billion — about eight times the company's trailing twelve-month average EBITDA.2 The bidders were a revealing mix of financial and strategic players. On the private-equity side, 博裕资本 Boyu Capital had made a verbal offer and Advent International had entered discussions.2 On the strategic side, the interested parties reportedly included Chinese down-apparel champion 波司登 Bosideng International and a consortium pairing Hong Kong-listed sportswear giant 安踏体育 Anta Sports Products with 方源资本 FountainVest.2 The stock jumped on the news.2 The composition of that bidder list tells its own story: the most natural strategic buyers for this Canadian icon are Chinese apparel and sportswear conglomerates — a reflection of both where Canada Goose's growth now lives and where the deepest strategic logic for owning it resides.

It is important to be precise about what this was and was not. These were verbal, early-stage offers, not firm bids, and Bain was reported to be holding off on any decision to see whether more suitors emerged.2 A US$1.4 billion valuation, while a strong return on Bain's reported US$250 million entry in 2013, sits far below the roughly US$7.7 billion the public market briefly ascribed to the company at its 2018 peak.2 The bids are best read not as vindication but as a floor — evidence that sophisticated buyers see enduring value in the brand even after years of margin compression, and a reminder of how far the equity has fallen from its euphoric high.

The eight-times-EBITDA multiple embedded in those offers is itself a piece of analysis worth decoding, because it tells you how the smart money is pricing this asset. Eight times trailing EBITDA is a workmanlike, unglamorous multiple — the kind of number you pay for a solid but challenged consumer business, not the rich double-digit multiples that genuine luxury compounders like a Hermès or even a Moncler command.5 In other words, the bidders are not paying for a pristine luxury brand firing on all cylinders; they are paying for a good brand with a broken cost structure, on the thesis that a patient private owner — free from the quarterly scrutiny of public markets — can do the unglamorous work of rationalizing the store fleet, cutting overhead, and rebuilding the margin without a live audience. That is a classic private-equity value-creation playbook, and the fact that the natural buyers are financial engineers and Chinese strategics rather than Western luxury houses is quietly telling. It suggests the market sees the value here as a turnaround-and-consolidation story, or a bet on Chinese distribution, rather than as a trophy asset to be collected at any price. For public shareholders, the practical implication is a valuation anchored more to fixable operations than to unbounded brand dreams.

None of it can happen, however, without passing through the wall that Bain and Reiss built into the company at the IPO. Canada Goose's dual-class structure divides ownership into multiple voting shares, held by Bain and Reiss and carrying ten votes each, and subordinate voting shares, held by the public and carrying one vote each. The arithmetic of control is stark: together, Bain and Reiss command roughly nine-tenths of the total voting power, split between Bain's controlling block and Reiss's substantial personal stake.[^3] No hostile takeover, no activist raid, and no take-private transaction can occur without their explicit, coordinated consent. For public shareholders, this is a double-edged inheritance. It protects the brand's heritage and long-term stewardship from short-term raiders. It also means that if a deal happens, its terms will be shaped first by what suits the two insiders — and Reiss's personal incentive is not merely price but finding a long-term owner who will protect the brand he spent a career building. As of mid-2026, no transaction has been announced, and the company remains public, its future ownership an open and consequential question. What is not in question is the strategic frame through which to judge it, which is where we turn next.

IX. Playbook & Strategic Analysis: Porter's 5 Forces, 7 Powers, and the Bull vs. Bear Case

Strip away the parka mythology and the take-private drama, and you are left with a durable question: does Canada Goose actually possess a defensible competitive advantage, or is it a very good brand in a brutally competitive industry? The honest answer requires running the business through two frameworks and refusing to grade generously.

Before doing that, it is worth confronting the consensus narratives head-on, because a few myths cloud clear thinking about this company. Myth one: Canada Goose is a broken brand. The financials say otherwise — a ~70% gross margin sustained through a turbulent period is not the signature of a brand losing its pricing power, and the take-private bidders would not be circling a genuinely broken name.1 The brand is intact; the cost structure is the problem, and conflating the two leads to the wrong conclusion. Myth two: the company is a pure luxury play that deserves a luxury multiple. The eight-times-EBITDA valuation implied by the 2025 bids says the smart money disagrees, pricing it as a challenged consumer business with a turnaround option rather than a serene compounder.2 Myth three: diversification has already de-risked the seasonality. The persistence of the seasonal problem — and the very existence of a strategic push to fix it — is the tell that this remains, for now, a business that lives and dies by winter. Holding these corrected views in mind is the prerequisite for an honest framework analysis, rather than one anchored to either the bull's romance or the bear's dismissal.

Start with Hamilton Helmer's 7 Powers, which asks where a company's advantage genuinely comes from. The clearest power Canada Goose holds is Brand — and it is real. The Arctic Program patch and the "Made in Canada" pedigree constitute a durable signal of both luxury and utility that lets the company charge a large premium and hold a ~70% gross margin, which is the single most persuasive piece of evidence that the brand power is intact.1 After that, the powers thin out quickly. Cornered Resource is moderate at best: vertical integration of Canadian manufacturing and the Romanian Paola Confectii facility gives some control over quality and margin, but skilled sewing and down-filling are not truly scarce inputs.4 Scale Economies are low-to-moderate — grouped purchasing of down and centralized marketing help, but Canada Goose is a fraction of the size of its largest rivals. Counter-Positioning, once a genuine strength when the brand offered rugged extreme-performance gear against delicate fashion-first European houses, has largely faded now that Canada Goose competes squarely in the fashion-luxury tier where those same houses live. And crucially, three of the seven powers are simply absent: Switching Costs (a consumer can buy a different coat tomorrow with zero friction), Network Effects (owning a parka makes no one else's parka more valuable), and meaningful Process Power (this is high-end manufacturing, not a proprietary process rivals cannot copy). The uncomfortable conclusion is that Canada Goose rests on essentially one power — brand — and brand, unlike a network effect or a switching cost, has to be re-earned every single season.

Porter's Five Forces sharpens the same point from the outside in. Rivalry is high and getting harder, and the competitive set is worth examining because each rival attacks Canada Goose from a different direction. Italian luxury outerwear leader Moncler is the aspirational benchmark — a larger, more diversified luxury house that has successfully positioned down jackets as pure fashion objects and commands the premium valuation multiple Canada Goose can only envy.5 Chinese down-apparel giant 波司登 Bosideng attacks from the other end of the map: a home-market champion of enormous scale whose revenue dwarfs Canada Goose's, it owns the mainstream Chinese consumer that Canada Goose is trying to court from abroad, and it does so with the advantages of local manufacturing, local distribution, and freedom from the geopolitical vulnerability of a foreign national brand.[^8] And premium technical-crossover labels like Arc'teryx — themselves riding the same gorpcore wave — attack the authenticity flank, offering serious performance credibility to the exact urban consumer who once had to buy a Canada Goose to signal outdoorsy competence. Squeezed between an aspirational luxury benchmark above, a scale champion in its most important growth market, and technical purists on its flank, Canada Goose occupies a contested middle that is harder to defend than it looks. Bargaining power of buyers is moderate: consumers have unlimited alternatives but have shown a willingness to pay up for the brand — pricing power that holds only as long as the brand stays hot, which is precisely the variable no management team can guarantee. The threat of substitutes is real and structural, and it is the most under-appreciated risk in the entire story: warmer winters driven by climate change directly reduce the functional need for a CA$1,500 expedition parka. A company whose core product is insurance against extreme cold has a genuine, non-cyclical problem if extreme cold becomes rarer — a slow-motion erosion of the addressable market that no amount of brand heat can fully offset. The remaining forces are milder: the threat of new entrants into genuine luxury is limited by the years it takes to build brand credibility, and the bargaining power of suppliers is modest given the commodity nature of down and nylon, a position vertical integration has strengthened further.

Which brings us to the explicit investment spine — the "why win" and "why lose" cases, held in tension rather than resolved.

The bull case rests on four pillars. First, pricing power that has not cracked: a ~70% gross margin through a period of margin turmoil says the premium is intact.1 Second, a DTC network that, run well, produces highly productive stores in cold-weather metropolitan hubs. Third, a credible path to becoming a year-round lifestyle brand through knitwear, footwear, and lightweight apparel, reducing the seasonal chokehold. Fourth, a valuation floor established by the US$1.4 billion take-private interest, which offers both downside support and the possibility of a premium exit.2

The bear case attacks each pillar with the company's own numbers. SG&A bloat is not a rounding error but the central problem — overhead consumed enough gross profit to nearly halve operating income, and an adjusted EBIT margin of 9.7% is simply low for a brand that claims luxury economics.1 Severe seasonality persists despite years of diversification effort; this remains, at its core, a business that earns its living in a few cold months, which strands expensive fixed costs across three quarters of thin demand. Geographic concentration in Greater China exposes the company to a single economy's confidence, to property-market fragility, and to the ever-present risk of nationalist backlash against a Western brand.1 And climate change quietly shrinks the addressable need over time.

The activist-style stress test writes itself, and it is more than a rhetorical exercise given the take-private interest already circling. A skeptical long/short investor would challenge the cost discipline directly: why did SG&A grow 25% in a year revenue grew 13%, and what specifically will reverse it beyond a promised target? They would probe the retail footprint — an CA$8.4 million impairment on underperforming stores raises the question of how many of the eighty-eight locations are genuinely productive versus vanity real estate that flatters the brand while diluting returns.1 They would attack the dual-class governance as the structural reason management has faced so little accountability for years of margin erosion — public shareholders cannot vote for change, only exit. And they would highlight the widening gap between a management narrative of "brand momentum" and a profit-and-loss statement showing the opposite at the operating line, arguing that the very existence of serious take-private bids is the market's verdict that the company is worth more in private hands, free from public scrutiny, than it has managed to be as a public company.2

The bull and bear cases do not cancel out — they describe a genuinely undecided business, where a strong brand and a weak cost structure are pulling in opposite directions, and where the outcome depends less on desire for the product than on discipline in running the company. The pivotal insight for an investor is that Canada Goose's fate is unusually within its own control. This is not a company whose product has been disrupted or whose demand has collapsed; the top line is growing and the gross margin is intact. What is broken is the machine between revenue and profit, and machines can be fixed by management that chooses to fix them. That is simultaneously the most hopeful and the most damning thing one can say about it. That is exactly why the metrics to watch are operational, not aspirational.

X. Epilogue & The 3 Critical KPIs to Watch

The temptation with a brand like Canada Goose is to watch the wrong things — the celebrity sightings, the store queues, the cultural cachet. Those made the company famous. They will not determine whether it is a good business from here. For that, three numbers matter more than the rest, and none of them requires believing or disbelieving management's narrative — they simply keep score.

The first is the SG&A-to-revenue ratio, and the store productivity underneath it. This is the crux of the entire modern story. Canada Goose has already proven it can generate luxury gross margins; what it has not proven is that it can carry a global store-and-marketing base without giving those margins back. The fiscal 2027 promise of an 11–12% adjusted EBIT margin, up from 9.7%, is a specific, falsifiable target.1 Whether overhead falls as a share of revenue — restoring the operating leverage a 70%-margin brand ought to enjoy — is the single most important thing to track, and it is where management's credibility will be won or lost.

The second is inventory turnover and weeks of supply. For a seasonal luxury brand, inventory discipline is existential. Overbuild ahead of a warm winter and you face the one thing that can destroy the premium faster than any competitor: discounting. Canada Goose ended fiscal 2026 with inventory roughly flat year over year at CA$386.3 million, which management framed as proactive control.1 Tight stock management protects the brand's pricing integrity; loose management invites the margin-diluting markdown cycle that has humbled many a luxury name. Watch the turns.

The third is the non-outerwear revenue mix — the share of sales coming from knitwear, footwear, and lightweight apparel. This is the truest single gauge of whether the strategic project of the last decade is actually working: the transition from a three-month parka business into a year-round brand. If that mix climbs meaningfully and profitably, the seasonality and climate risks ease and the diversification thesis earns its keep. If it stalls, Canada Goose remains what it has always been — a magnificent maker of winter coats, hostage to the weather and to a few cold cities. The subtle trap to watch for is diversification that grows the top line while diluting the economics: expanding into lower-margin, less-differentiated categories can boost revenue and mask the seasonality problem while quietly eroding the very premium positioning that makes the company special. The right question is not just whether non-outerwear grows, but whether it grows without dragging down the blended margin.

A brief word on what deliberately did not make this list. It is tempting to obsess over the take-private saga, over quarterly comparable-sales prints, or over the celebrity-and-culture signals that first made the brand famous. But comparable sales are already captured inside the store-productivity lens, ownership changes are binary events rather than ongoing performance measures, and cultural buzz is a lagging, unquantifiable indicator that the financials will reveal soon enough. The three metrics above are chosen because each one directly tests a specific pillar of the investment case — cost discipline, inventory and pricing integrity, and the year-round transition — and because, unlike the brand's mystique, each can actually be measured quarter after quarter.

Canada Goose is, in the end, a masterclass in a specific kind of alchemy: turning utility-focused craftsmanship into a global luxury status symbol, and doing it largely without a traditional marketing budget. That achievement is real and rare. But the next chapter is being written not in the design studio or the seeding strategy, but in the far less romantic arithmetic of fixed costs, store productivity, Chinese consumer confidence, and private-equity ownership. The patch still signals the Arctic. Whether the business beneath it can generate Arctic-grade returns is a question the brand's history cannot answer — only its discipline can.

References

-

Canada Goose Reports Fourth Quarter and Full Year Fiscal 2026 Results — Canada Goose Holdings Inc., 2026-05-14 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Bain Capital Waits On More Bidders In $1.4 Billion Canada Goose Sale — Forbes, 2025-08-27 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Canada Goose acquires cold-weather footwear brand Baffin — Fashion United, 2018-11-05 ↩

-

Canada Goose Announces the Acquisition of Romanian Manufacturing Partner Paola Confectii — Canada Goose IR, 2023-11-28 ↩↩

-

Moncler Group FY2025 Financial Results — Moncler Group Investor Relations, 2026-02-28 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube