GameStop: The Ultimate Power-Up

The morning of January 28, 2021, marked one of the most extraordinary moments in Wall Street history. GameStop's stock reached a pre-market value of over $500 per share ($125 split-adjusted), nearly 30 times the $17.25 valuation at the beginning of the month. Hedge funds were hemorrhaging billions. Reddit users were becoming millionaires. Trading apps were crashing under unprecedented volume. At the center of it all stood a struggling video game retailer that many had written off as the next Blockbuster.

How did a brick-and-mortar chain selling physical game discs become the David that nearly toppled Wall Street's Goliaths? The answer involves Harvard Business School classmates with a vision, a chess-playing CEO who refuses a salary, and an army of retail investors who turned "diamond hands" into a battle cry. This is the story of GameStop—a company that survived the digital apocalypse not through brilliant strategy, but through becoming something far stranger: a symbol.

Origins: The Babbage's Beginning

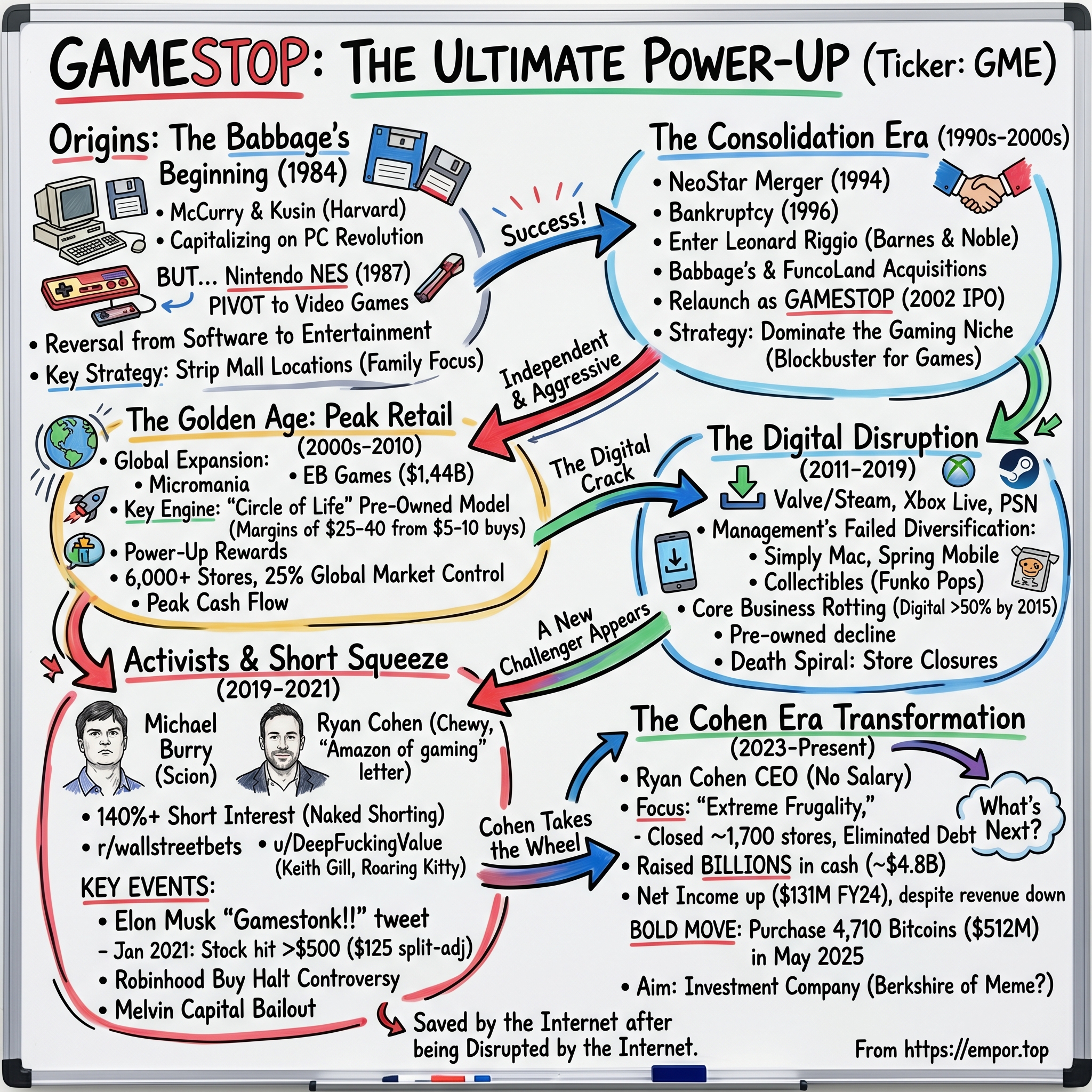

The year was 1984. While Apple was launching the Macintosh and telling the world to "Think Different," two Harvard Business School classmates were thinking about something more specific: how to capitalize on the nascent personal computer revolution. James McCurry and Gary M. Kusin founded Babbage's, naming their venture after Charles Babbage, the 19th-century mathematician who conceptualized the first mechanical computer. The choice was deliberate—they saw themselves as pioneers in a new digital frontier.

Their timing seemed perfect. Personal computers were transitioning from hobbyist curiosities to household necessities. But McCurry and Kusin quickly discovered that software, not hardware, held the real opportunity. By 1987, they had made a crucial pivot that would define the company's future: Nintendo had just launched the NES in America, and Babbage's began stocking video games alongside productivity software.

The transformation was swift and decisive. Babbage's went public in 1988, riding the wave of Nintendo-mania that was sweeping suburban America. By 1991, video games accounted for two-thirds of sales—a complete reversal from their original business plan. The Harvard MBAs had stumbled into something far more lucrative than spreadsheet software: they had discovered that America's children (and increasingly, adults) would pay premium prices for digital entertainment.

What made Babbage's special wasn't just timing—it was location strategy. While competitors fought for real estate in urban centers, Babbage's focused on strip malls in suburbs where families with disposable income lived. Each store became a destination, a place where kids dragged their parents on weekends, where the latest gaming magazines were devoured, where employees actually knew the difference between a JRPG and a platformer. This wasn't just retail; it was community building, decades before anyone would use that term in a business context.

The Consolidation Era: Building an Empire

The 1990s brought both opportunity and crisis. In 1994, Babbage's merged with Software Etc. to form NeoStar Retail Group, creating a gaming retail powerhouse. But the consolidation came with overleveraged balance sheets and operational chaos. By 1996, NeoStar was bankrupt—killed not by digital distribution (that threat was still years away) but by old-fashioned financial mismanagement.

Enter Leonard Riggio, the Barnes & Noble founder who understood something fundamental about specialty retail: success came from dominating a niche, not diversifying away from it. Riggio purchased NeoStar's assets for just $58.5 million in 1996—a fraction of what the company had been worth just two years earlier. Under Barnes & Noble's ownership, the pieces started coming together. The acquisition of Babbage's Etc. for $215 million in 1999 was followed by the $160 million purchase of FuncoLand in 2000.

The masterstroke came with the rebrand. "GameStop" wasn't just a new name—it was a statement of intent. This would be the definitive destination for gaming. The 2002 IPO raised the capital needed for aggressive expansion. Barnes & Noble retained control but gave management the autonomy to pursue an audacious goal: become to video games what Blockbuster was to movies.

By the time Barnes & Noble spun off GameStop in 2004, making it fully independent, the foundation for an empire was complete. The company had over 1,500 stores, a recognized brand, and most importantly, a business model that seemed unassailable. Physical game sales were growing double-digits annually. The PlayStation 2 was the fastest-selling console in history. Gaming was going mainstream, and GameStop was perfectly positioned to capture the profits.

The Golden Age: Peak Physical Retail

Independence unleashed GameStop's ambitions. The 2005 acquisition of Electronics Boutique (EB Games) for $1.44 billion wasn't just about adding 4,250 stores across Australia, Canada, Europe, and New Zealand—it was about achieving global scale before anyone else could. Management understood that in retail, there would be one dominant player per region, and GameStop intended to be that player everywhere.

The international expansion continued with surgical precision. The 2007 acquisition of Rhino Video Games' 70 stores from a struggling Blockbuster provided entry into new markets at fire-sale prices. The crown jewel came in 2008: French retailer Micromania for $700 million, establishing GameStop as the dominant force in European gaming retail.

But what truly drove profits wasn't new game sales—it was the ingenious pre-owned business model. GameStop would buy used games for $5-10 and resell them for $25-40, achieving margins that made other retailers envious. The "Circle of Life" program pushed employees to convert every new game purchase into a future trade-in. Power-Up Rewards members got extra trade-in credit, ensuring customer loyalty. Publishers hated it (they saw no revenue from secondary sales), but customers loved the value proposition.

At its 2008 peak, GameStop operated over 6,000 stores globally. Same-store sales grew consistently. The company generated over $1 billion in operating cash flow. J. Paul Raines, who became CEO in June 2010, inherited what seemed like an unstoppable retail machine. Wall Street loved the story—a specialty retailer with 30%+ margins, subscription revenue from warranties and memberships, and a moat that seemed impregnable.

The numbers were staggering: GameStop controlled an estimated 25% of the global video game retail market. On major game releases, publishers had no choice but to work with GameStop for midnight launches and exclusive pre-order bonuses. The company's buyers could make or break smaller titles just by deciding how much shelf space to allocate. This was power—real, tangible market power that translated into exceptional financial returns.

The Digital Disruption: Beginning of the End?

The first cracks appeared around 2011. Steam, Valve's digital distribution platform, had quietly grown to 30 million users. Microsoft and Sony began selling full games directly through Xbox Live and PlayStation Network. The threat wasn't immediate—digital downloads still required hours with typical internet speeds—but the writing was on the wall.

Management's response revealed a troubling lack of vision. Instead of embracing digital transformation, GameStop tried to diversify away from it. The acquisition of Simply Mac stores attempted to leverage retail expertise into Apple products. Spring Mobile aimed to capitalize on the smartphone boom. The push into collectibles—everything from Funko Pops to gaming t-shirts—tried to find products that couldn't be digitized.

Each pivot failed for the same reason: GameStop was trying to be something it wasn't. The Simply Mac stores couldn't compete with Apple's own retail experience. The mobile phone business was already dominated by carrier stores. Collectibles, while showing promise, could never generate the volume needed to offset declining game sales. Meanwhile, the core business was rotting. Digital game sales grew from 20% of the market in 2010 to 50% by 2015. Pre-owned game revenue, the company's profit engine, began declining as players kept their digital libraries forever.

Store closures began slowly—a few dozen in 2012, accelerating to hundreds per year by 2015. Management insisted these were "optimization" efforts, closing only underperforming locations. But employees knew better. District managers were being laid off. Store hours were being cut. The generous trade-in values that drove the pre-owned business were being reduced to preserve margins. The death spiral had begun.

Enter the Activist: Ryan Cohen's Arrival

The GameStop story might have ended like so many other retail casualties—a quiet bankruptcy, some private equity vultures picking at the corpse, a few nostalgic news articles. But in mid-2019, something unexpected happened. Michael Burry's Scion Asset Management purchased over 3% of GameStop, arguing the company was undervalued even accounting for its challenges. Burry, famous for predicting the 2008 financial crisis, saw something others missed: GameStop's real estate, cash flow, and brand still had value.

The real catalyst came in September 2020. Ryan Cohen disclosed a near 10% stake in GameStop, later increased to 12.9% through an amended 13D filing with the SEC. Cohen wasn't just any activist investor—he had built Chewy from nothing into a $3.35 billion exit to PetSmart. More importantly, he understood how to compete with Amazon in the digital age.

Cohen's activist letter to the board in November 2020 was scathing. He criticized the company's "lackadaisical approach to customer service," its failure to build meaningful digital capabilities, and its bloated cost structure. But unlike most activists who simply demand cost cuts and dividends, Cohen presented a vision: transform GameStop into the "Amazon of gaming." Focus on e-commerce, competitive pricing, faster delivery, and expanded product selection. Become a technology company, not a retailer.

On January 11, 2021, Cohen joined the board along with Alan Attal and Jim Grube, two former Chewy executives. The market's reaction was immediate—the stock jumped from $20 to $35. But this was just the appetizer for what was about to unfold.

The Short Squeeze Saga: WallStreetBets vs. Wall Street

To understand what happened next, you need to understand the setup. By July 2019, over 63% of GameStop's shares were sold short—traders betting the stock would fall. By January 2021, approximately 140 percent of GameStop's public float had been sold short, a dangerous situation called "naked shorting" where more shares are shorted than actually exist.

Enter Keith Gill, a Massachusetts financial analyst who'd been studying GameStop since 2019. Under the username "u/DeepFuckingValue" on Reddit, Gill posted a screenshot of a roughly $53,000 long position in GameStop consisting of 50,000 shares and 500 call options. Gill started sharing his investment thesis through YouTube videos as "Roaring Kitty" in July 2020.

Gill's argument was simple but compelling: GameStop wasn't going bankrupt. It had enough cash to survive, new console releases would drive sales, and Cohen's involvement could transform the company. The stock, trading at $4-5, was priced for bankruptcy. Any positive development could trigger a short squeeze—forcing short sellers to buy shares to cover their positions, driving the price higher.

The r/wallstreetbets community, a Reddit forum of retail traders known for high-risk options trading, embraced Gill's thesis. Through late 2020 and early January 2021, more retail investors piled in. On January 26, business magnate Elon Musk tweeted "Gamestonk!!"—a reference to the "stonks" meme—along with a link to the r/wallstreetbets subreddit. A brief, sharp rise in the share price to over $200 followed Musk's tweet.

The squeeze accelerated beyond anyone's imagination. On January 28, 2021, the all-time highest intraday stock price for GameStop was $483.00. In pre-market trading hours the same day, it briefly hit over $500, up from $17.25 at the start of the month. Trading volume exploded—over 175 million shares traded on January 25 alone.

Then came the controversy that would define the episode. On January 28, Robinhood and several other popular brokerages halted buying of GameStop, citing liquidity requirements from clearinghouses. Users could sell but not buy—a restriction many saw as protecting hedge funds at the expense of retail traders. The backlash was immediate and fierce. Politicians from Alexandria Ocasio-Cortez to Ted Cruz condemned the restrictions. Class-action lawsuits were filed. Congressional hearings were demanded.

The casualties were severe. Melvin Capital had lost 53 percent of its investments by the end of January. Citadel LLC and Point72 Asset Management invested $2.75 billion to bail out Melvin. Other hedge funds reportedly lost billions. Meanwhile, Keith Gill's original investment was worth nearly $48 million by January 27, though he lost $15 million in one day as the stock fluctuated wildly.

The Cohen Era: Transformation or Speculation?

The short squeeze grabbed headlines, but the real story was just beginning. On September 28, 2023, Cohen took over as Chief Executive Officer of GameStop, receiving no salary for his roles as CEO and chairman. His first email to employees set the tone: "Extreme frugality is required. Every expense at the company must be scrutinized under a microscope and all waste eliminated".

Cohen's transformation was ruthless in its efficiency. Since joining the board in 2021, the company closed 1,700 underperforming stores—nearly a third of its footprint. Layers of management were eliminated. Unprofitable ventures were shut down. The European operations were largely wound down, with the company exiting Italy entirely and closing German stores.

The financial engineering was equally dramatic. GameStop eliminated its long-term debt completely. Multiple share offerings during price spikes raised billions in cash. By early 2025, the company held approximately $4.775 billion in cash and marketable securities—a war chest that gave it flexibility most retailers could only dream of.

The results spoke for themselves. For fiscal year 2024, net sales were $3.823 billion compared to $5.273 billion in fiscal 2023, but net income was $131.3 million compared to just $6.7 million the prior year. Revenue was down, but profitability was up—Cohen had successfully transformed GameStop from a growth story to a value play.

But the boldest move came in May 2025. GameStop purchased 4,710 bitcoins worth $512.6 million at Bitcoin's price of $108,837. The purchase signaled a dramatic shift—GameStop was no longer just a retailer but was positioning itself as an investment company, following the playbook of MicroStrategy (now called Strategy) which had seen its stock soar by accumulating Bitcoin.

The market's reaction was mixed. Some saw it as a desperate attempt to remain relevant. Others viewed it as brilliant capital allocation—using the inflated stock price to raise cash, then deploying that cash into appreciating assets. Cohen himself remained characteristically cryptic, refusing interviews and communicating primarily through meme-filled tweets.

Porter's Five Forces Analysis

Michael Porter's framework reveals why GameStop's traditional business model was doomed from the start:

Supplier Power: Absolute dominance. Sony, Microsoft, and Nintendo hold all the cards. They control product allocation, pricing, and increasingly, distribution through their own digital stores. GameStop needs them far more than they need GameStop. The console makers can—and have—cut retailers out entirely through digital sales.

Buyer Power: Infinite alternatives. Gamers can purchase from Amazon (often cheaper and delivered same-day), directly from PlayStation Store or Xbox Marketplace (instantly), or from big-box retailers like Walmart and Best Buy. GameStop offers no unique value proposition beyond nostalgia.

Threat of Substitutes: Existential. Digital downloads aren't just a substitute—they're a superior product for most consumers. No physical storage needed, instant access, can't be lost or damaged, often cheaper during sales. Game Pass and PlayStation Plus offer hundreds of games for a monthly fee, destroying the value proposition of both new and used game sales.

New Entrants: Low barriers, declining market. Anyone can sell video games—it requires no special expertise or infrastructure. But more importantly, why would anyone enter a declining market? The physical game retail space is shrinking rapidly, discouraging new competition.

Competitive Rivalry: Intense but irrelevant. Best Buy, Walmart, Target, and Amazon all sell games, often as loss leaders to drive traffic. They can afford to undercut GameStop because games are a tiny portion of their business. GameStop, meanwhile, has nowhere else to go.

The Five Forces analysis makes clear: GameStop operates in an structurally unattractive industry getting worse every year. No amount of operational excellence can overcome these fundamental challenges.

Hamilton's 7 Powers Framework

Hamilton Helmer's 7 Powers framework is even more damning:

Scale Economies: Lost forever. Digital platforms like Steam have true scale economies—near-zero marginal cost for each additional sale. GameStop's physical stores have negative scale economies as sales decline.

Network Effects: None. Unlike platforms like Xbox Live or Steam where more users attract more developers which attract more users, GameStop has no network effects. One customer shopping there doesn't make it more valuable for another.

Counter-Positioning: Failed attempts. The push into collectibles and mobile phones weren't true counter-positioning—they were desperate diversification. Real counter-positioning would require doing something incumbents couldn't copy without hurting their existing business. GameStop has found no such strategy.

Switching Costs: Zero. A customer can buy their next game from Amazon or download it digitally with no penalty. There's no lock-in, no accumulated benefits, no reason to stay loyal to GameStop.

Branding: Damaged but oddly powerful. The GameStop brand means different things to different people. To traditional gamers, it's increasingly irrelevant. But to meme stock investors, it's become a symbol of retail trader rebellion. This bizarre brand value is perhaps GameStop's only remaining moat.

Cornered Resource: Eroding rapidly. The pre-owned games market was GameStop's cornered resource—they had the scale and systems to make it profitable. But digital games can't be resold, and newer physical games often require online activation, limiting the secondary market.

Process Power: None evident. GameStop has no unique processes or capabilities that competitors can't replicate. Their store operations, inventory management, and customer service are competent but not exceptional.

The 7 Powers analysis reaches an inescapable conclusion: GameStop has no sustainable competitive advantages in its core business. Its survival depends entirely on financial engineering and the bizarre dynamics of meme stock trading.

The Investment Lens: Bear vs. Bull

The bear case writes itself. GameStop is a melting ice cube, a retailer whose core market is disappearing. Physical game sales will eventually approach zero as internet speeds improve and digital natives become the primary gaming demographic. The company's attempts at transformation—into collectibles, cryptocurrency, NFTs—smack of desperation rather than strategy. Even with Cohen's cost cuts, the company generated only $131 million in profit on $3.8 billion in sales—a measly 3.4% margin. The Bitcoin purchase looks like gambling with shareholder money. At current valuations, you're paying a premium for a dying business.

The bull case requires more imagination but isn't without merit. GameStop has $4.5+ billion in cash with zero debt—remarkable for a "dying" retailer. The company is profitable despite revenue declines, showing management's cost discipline. Ryan Cohen has a proven track record; he built Chewy from nothing and competed successfully against Amazon. The retail investor base provides a floor under the stock price that traditional analysis can't explain. The Bitcoin position could appreciate significantly. Most intriguingly, Cohen seems to be transforming GameStop from an operating company into an investment vehicle—a gaming-focused Berkshire Hathaway for the meme stock generation.

The reality likely lies somewhere in between. GameStop's traditional business will continue declining, but perhaps more slowly than bears expect. Console makers still need physical retailers for hardware sales and market presence. The company's cash hoard provides years of runway for transformation attempts. The meme stock phenomenon has fundamentally changed the rules—traditional valuation metrics don't apply when millions of retail investors treat holding the stock as a form of protest against Wall Street.

Playbook: Lessons from the GameStop Saga

The GameStop phenomenon offers several crucial lessons for investors, regulators, and companies:

The power of retail coordination is real and lasting. Social media has enabled retail investors to coordinate in ways previously impossible. The GameStop squeeze wasn't a one-off event—it fundamentally changed how markets work. Any heavily shorted stock with a compelling narrative is now vulnerable to squeeze dynamics.

Short selling has become exponentially more dangerous. The asymmetry was always there—limited upside, unlimited downside—but social media has weaponized it. Hedge funds must now factor in the risk of becoming targets for retail trader rebellion. The days of safely shorting struggling retailers into bankruptcy are over.

Digital disruption is usually irreversible but not always immediate. GameStop's core business has been dying for over a decade, yet the company survives. Betting on the timing of disruption is nearly as dangerous as betting against it entirely.

Meme value can exceed fundamental value for extended periods. Traditional finance assumes prices eventually reflect intrinsic value. GameStop proves that in the age of social media, narrative value can sustain prices far above fundamental value for years, not just days or weeks.

Financial engineering can extend corporate life indefinitely. With access to capital markets, a dying business can transform into something entirely different. GameStop raised billions by selling shares at inflated prices, then used that cash to ensure survival regardless of operating performance.

Regulatory frameworks are outdated for the social media age. The trading restrictions during the squeeze exposed how ill-equipped current regulations are for handling coordinated retail trading. The definition of market manipulation needs updating for an era where a single tweet can move billions in market cap.

Epilogue: What's Next?

GameStop in 2025 is a company without precedent. It's simultaneously a dying retailer and a cash-rich investment vehicle. Its shareholders aren't owners in the traditional sense—they're members of a movement. Its CEO doesn't take a salary because he's playing a different game entirely, one where traditional corporate metrics matter less than meme momentum and community loyalty.

The transformation into a Bitcoin holder signals Cohen's ultimate strategy: GameStop is becoming a permanent capital vehicle for the retail investment revolution. Like Berkshire Hathaway evolved from a failing textile manufacturer into Buffett's investment platform, GameStop is evolving from a failing game retailer into... something else. What exactly remains to be seen.

Can Cohen engineer a Berkshire-style transformation? The challenges are immense. Berkshire had Warren Buffett's investing genius and decades of compound returns. GameStop has Reddit threads and diamond hand emojis. Yet stranger things have happened—like a video game retailer nearly bankrupting Wall Street's smartest hedge funds.

The ultimate irony is perfect: a company saved by the internet that was being killed by the internet. GameStop was disrupted by digital distribution, then saved by digital communities. It's a cautionary tale about the death of physical retail that became an inspirational story about the power of retail investors.

Final Thoughts

GameStop's place in financial history is already secure. It will be studied in business schools not for operational excellence or strategic brilliance, but as the moment when the rules changed. When retail investors realized they could move markets. When social media became a financial weapon. When memes became valuable.

For fundamental investors, GameStop presents a paradox: a company whose value cannot be determined by traditional analysis. Its worth lies not in cash flows or assets but in its symbolism. It's a $5 billion bet that the retail investment revolution is just beginning, that Cohen can find productive uses for capital, that community and narrative matter more than spreadsheets and models.

The GameStop saga isn't really about GameStop at all. It's about power—who has it, who's losing it, and how technology redistributes it. The hedge funds that shorted GameStop weren't just betting against a struggling retailer; they were betting against the idea that retail investors matter. They lost that bet catastrophically.

As we look toward the future, GameStop stands as a monument to market disruption—not the kind taught in business school, but the kind that happens when millions of people decide that the rules of the game need changing. Whether GameStop survives another decade or disappears tomorrow, its impact is permanent. The Power to the Players tagline has taken on new meaning: the players aren't just gaming anymore—they're trading, and they're winning.

The game has stopped being predictable. And perhaps that's the most valuable lesson of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube