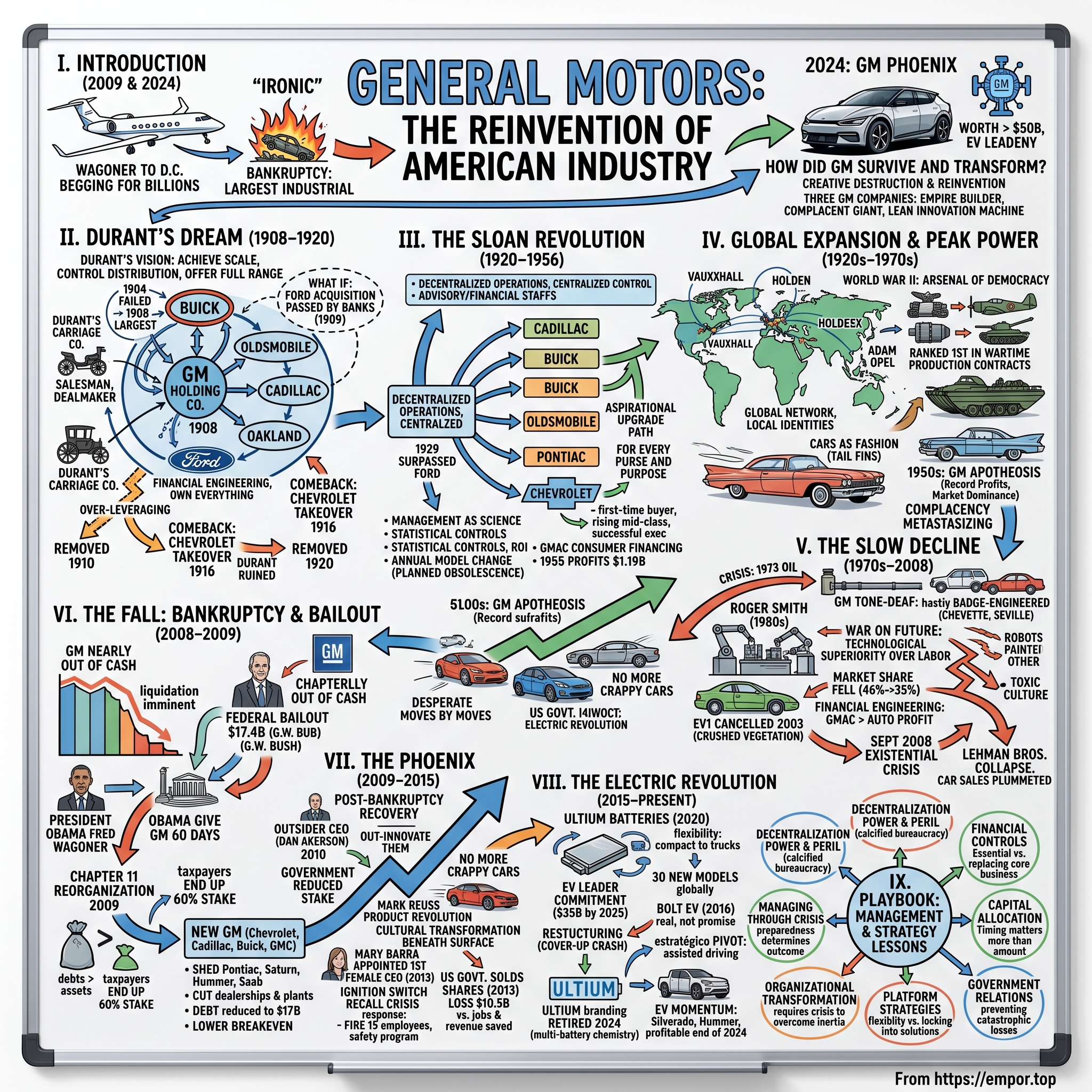

General Motors: The Reinvention of American Industry

I. Introduction & Episode Thesis

The year is 2009. Rick Wagoner, CEO of General Motors, boards a corporate jet in Detroit, bound for Washington D.C. He's about to beg Congress for billions in taxpayer money to save what was once the mightiest corporation on Earth. The irony isn't lost on anyone—arriving in a private jet to plead poverty. Within months, Wagoner would be fired by the President of the United States, and GM would file the largest industrial bankruptcy in American history. The company that had once commanded over half the U.S. auto market, that had literally helped win World War II, that had defined American capitalism itself, was effectively dead.

Fast forward to 2024. General Motors is worth over $50 billion, leads Detroit's charge into electric vehicles, operates one of the most valuable autonomous driving companies in the world, and has completely reimagined what a 116-year-old industrial giant can become. This is a story of destruction and rebirth, of hubris and redemption, of how the very DNA of American industry was rewritten not once, but multiple times. The central question isn't whether GM survived—it did. The question is how a company can lose everything and still emerge as a credible competitor to Tesla, how it can transform from the epitome of corporate bloat to a lean innovation machine, and what this metamorphosis reveals about the nature of American capitalism itself. This is the story of three distinct General Motors companies: the empire builder that created modern management, the complacent giant that nearly destroyed itself, and the phoenix that today commands a market capitalization of $53.61 billion.

What makes GM's story particularly compelling for investors is that it's not just corporate history—it's a living case study in transformation. The company that once epitomized everything wrong with American manufacturing now pioneers electric vehicle platforms that rival anything from Silicon Valley. The bureaucracy that couldn't compete with Toyota now moves with startup-like agility in autonomous driving. The financial engineering that led to bankruptcy has given way to disciplined capital allocation that would make Warren Buffett proud.

Over the next several hours, we'll trace this extraordinary arc through three major transformations. First, how William Durant assembled the pieces that would become the world's largest corporation, only to lose control twice. Second, how Alfred Sloan invented modern management and built an empire that seemed invincible for half a century. And finally, how hubris, competition, and changing markets brought that empire crashing down—only for a new generation of leaders to rebuild it into something entirely different.

This isn't just GM's story. It's the story of American industry writ large, of creative destruction and reinvention, of how even the mightiest institutions must evolve or die. As we'll see, the company that emerges from each crisis is fundamentally different from what came before, yet somehow still recognizably General Motors. That paradox—continuity through radical change—may be the most important lesson for any investor trying to understand not just where GM is headed, but where American capitalism itself is going.

II. Durant's Dream: The Birth of General Motors (1908–1920)

Picture Flint, Michigan, September 16, 1908. While Henry Ford was tinkering with his Model T in nearby Detroit, William Crapo Durant was orchestrating something far more audacious—not building a car company, but assembling an empire. That morning, Durant signed the papers incorporating General Motors as a holding company in New Jersey, with authorized capital of $12.5 million. Within 24 hours, he would wire $4.5 million to purchase Buick Motor Company. Within two years, he would control over twenty automotive companies. This wasn't manufacturing; it was financial engineering before the term existed.

Durant understood something his contemporaries didn't: the automobile industry's future wouldn't belong to the best engineer or even the best car. It would belong to whoever could achieve scale, control distribution, and offer a full range of products. Where Ford saw efficiency through standardization—"any color as long as it's black"—Durant saw opportunity in variety. His vision was breathtakingly simple and impossibly complex: own everything, offer everything, dominate everything.

The man himself was a study in contradictions. Before automobiles, Durant had built Durant-Dort Carriage Company into the largest manufacturer of horse-drawn vehicles in the United States, selling 150,000 units annually by 1900. He wasn't an engineer—he was a super-salesman, a dealmaker, a financial wizard who could see patterns others missed. When he first encountered David Buick's struggling motor company in 1904, he saw not a failing business but the cornerstone of an empire. By 1908, under Durant's leadership, Buick was the largest car manufacturer in America, outselling Ford and Cadillac combined.

The acquisition spree that followed was legendary in its audacity. Oldsmobile came first, purchased for $3 million despite having only $2 million in assets—Durant paid the premium for its dealer network and brand recognition. Then came Cadillac, the "Standard of the World," acquired for $4.5 million in cash. Oakland Motor Car Company (later Pontiac), dozens of parts suppliers, and even companies making everything from trucks to tractors. Durant's philosophy was integration at any cost: if you needed it to build a car, GM should own it. The most tantalizing "what if" in automotive history came in October 1909. Henry Ford agreed to sell his company to General Motors for $8 million, with terms of $2 million in cash, $2 million in stock, and the remaining $4 million paid during the next three years at 5% interest. The loan committee of the bank, however, passed on this deal. If Durant had had the cash, Ford would have become a division of GM. Think about that: no Ford vs. Chevy rivalry, no Mustang vs. Camaro, no F-150 vs. Silverado. The entire structure of American automotive competition would have been fundamentally different. The banks' refusal to lend Durant that $2 million down payment may have been the most consequential "no" in industrial history.

But Durant's over-leveraging finally caught up with him. The Panic of 1910-1911 exposed the fragility of his empire. Durant over-leveraged GM in making acquisitions, and was removed by the board of directors in 1910 at the order of the bankers who backed the loans to keep GM in business. The bankers took control, installing their own management team. Durant, the empire builder, was out of his own empire.

What happened next was pure Durant: audacious, brilliant, and slightly insane. In November 1911, Durant co-founded Chevrolet with race car driver Louis Chevrolet, who left the company in 1915 after a disagreement with Durant. But Durant wasn't building Chevrolet to compete with GM—he was building it to buy GM. Over the next five years, he secretly accumulated GM stock, using Chevrolet as his vehicle (literally and figuratively) for the takeover.

At a GM board meeting in 1916, Durant announced that Chevrolet now had controlling interest of GM. Durant was again elected president of GM. It was one of the greatest comebacks in business history—a deposed founder using a startup to recapture his empire. With backing from Pierre S. du Pont, whose family would play a crucial role in GM's future, Durant was back in charge.

But Durant's second act would be even shorter than his first. In 1920, the post-World War I boom ended, stocks lost 25% of their value, and 100,000 businesses went bankrupt. Durant, ever the gambler, had personally borrowed millions to prop up GM's stock price. When the market crashed, he was ruined. Pierre du Pont orchestrated Durant's removal and took control of the company. Durant would never return to GM, dying nearly penniless in 1947, managing a bowling alley in Flint.

Yet Durant's vision—a multi-brand automotive conglomerate offering "a car for every purse and purpose"—would become the foundation of GM's century-long dominance. He didn't just build a car company; he invented the modern automotive industry's structure. Every multi-brand strategy, every automotive holding company, every attempt at vertical integration traces back to that September morning in 1908 when Billy Durant decided to buy everything.

III. The Sloan Revolution: Building the Modern Corporation (1920–1956)

Alfred Pritchard Sloan Jr. arrived at General Motors in 1918 when Durant acquired United Motors, the parts conglomerate Sloan had been running. Where Durant was all passion and instinct, Sloan was pure rationality—an MIT-trained engineer who saw business as a system to be optimized. When he assumed the presidency in 1923, GM was still a chaotic collection of fiefdoms, each division operating as its own kingdom. Sloan would transform this chaos into the most sophisticated industrial organization the world had ever seen.

In 1920, du Pont orchestrated the removal of Durant once again and replaced him with Sloan. Actually, Pierre du Pont himself served as president from 1920 to 1923, with Sloan working as his vice president and operations chief. When du Pont stepped aside in 1923, Sloan was ready. He had spent three years studying GM's dysfunction and designing his solution: decentralized operations with centralized control.

The concept sounds simple but was revolutionary. Sloan reorganized GM from a sprawling, uncoordinated collection of business units into a single enterprise consisting of five main automotive divisions—Cadillac, Buick, Pontiac, Oldsmobile, and Chevrolet—the activities of which were coordinated by a central corporate office equipped with large advisory and financial staffs. Each division head ran their business like a CEO, with full profit-and-loss responsibility. But they operated within strict financial controls and strategic guidelines set by headquarters. It was federalism applied to business. Sloan's masterstroke was the "ladder of success"—five brands positioned precisely to avoid internal competition while offering a clear upgrade path. Chevrolet for the first-time buyer, Pontiac for the rising middle class, Oldsmobile for the established professional, Buick for the successful executive, and Cadillac for those who had truly arrived. Each brand had its own identity, its own price point, its own customer. A young family might start with a Chevrolet and, over decades, work their way up to a Cadillac, never leaving the GM family. Ford offered one car in one color; GM offered aspiration itself.

In 1922, the year before Sloan took charge, General Motors made a net profit of $53 million on sales of $464 million. Those profits were less than half the $120 million earned by arch-rival Ford. In Sloan's last full year serving as Chairman of General Motors, 1955, company profits were $1.19 billion on sales of $12.4 billion. That 1955 sales figure, having grown at over 10 percent per year for thirty-three years, was double the next largest company on earth.

The transformation was staggering. Under Sloan's stewardship, GM didn't just grow—it redefined what a corporation could be. The annual model change, introduced by Sloan, turned automobiles from durable goods into fashion statements. Why keep a car for a decade when next year's model would make yours look dated? This "planned obsolescence" was controversial but brilliant, creating perpetual demand in what could have been a saturated market.

Sloan also greatly strengthened GM's sales organization and pioneered innovations in consumer financing. The creation of General Motors Acceptance Corporation (GMAC) in 1919 had preceded Sloan, but he weaponized it. While Ford demanded cash, GM offered credit. While Ford sold transportation, GM sold dreams on the installment plan. By 1929 General Motors had surpassed the Ford Motor Company to become the leading American passenger-car manufacturer.

But perhaps Sloan's greatest innovation was invisible to consumers: the professionalization of management itself. He introduced statistical controls, return on investment calculations, and market research as standard practice. Every decision was backed by data. Every division's performance was measured against precise metrics. This wasn't entrepreneurial gut instinct; it was management as science.

The man himself was as precise as his systems. Where Durant was warm and impulsive, Sloan was cold and calculating. He arrived at the office at exactly the same time each day, ate the same lunch (often from a brown bag even as CEO), and approached every problem with the detachment of an engineer examining a blueprint. When asked about his management philosophy, he once said, "Take my assets—but leave me my organization, and in five years I'll have it all back."

Sloan's GM also pioneered the modern relationship between management and labor, though not always smoothly. When workers organized the massive Flint sit-down strike in 1936—occupying factories and refusing to leave—Sloan initially refused to negotiate. The successful strike legitimized the United Auto Workers as the exclusive bargaining representative for GM workers, establishing a pattern of labor relations that would define American manufacturing for decades.

By the 1950s, GM wasn't just a car company—it was an institution. Profits in 1955 were 50% higher than those at each of the next largest companies, Standard Oil of New Jersey (now ExxonMobil), Royal Dutch Shell, and American Telephone and Telegraph (AT&T). Sloan had built something unprecedented: a corporation so vast, so profitable, so dominant that it seemed immune to competition. The company that Durant had assembled from parts, Sloan had transformed into the machine that ran America.

When Sloan finally stepped down as chairman in 1956, he left behind not just a company but a template. The "GM way"—decentralized operations with centralized control, multiple brands targeting different market segments, annual model changes, consumer financing, professional management—became the American way of business. Every MBA program taught Sloan's methods. Every large corporation studied his organizational charts. For the next quarter-century, to understand GM was to understand American capitalism itself.

IV. Global Expansion & Peak Power (1920s–1970s)

The morning of December 7, 1941, found GM president Charles Wilson in his Detroit office, despite it being a Sunday. By afternoon, news of Pearl Harbor had reached him. Within hours, Wilson was on the phone with Washington, offering GM's entire production capacity to the war effort. "This is a war of production," he would later say, and no one could produce like General Motors. What followed was the most extraordinary transformation in industrial history—in less than two months, GM would cease all civilian car production and become, quite literally, the Arsenal of Democracy.

But GM's global ambitions had begun long before the war. The company had been methodically building an empire since the 1920s. It added overseas operations, including Vauxhall of England in 1925, Adam Opel of Germany in 1929, and Holden of Australia in 1931. These weren't just export operations or licensing deals—GM was buying established manufacturers, integrating them into its global network while maintaining their local identities. Vauxhall kept its British character, Opel remained distinctly German, Holden stayed Australian. It was the Sloan philosophy applied globally: centralized control with decentralized operations.

The Opel acquisition was particularly significant. For $33.3 million, GM acquired Germany's largest automaker, gaining not just production capacity but access to European engineering expertise and a distribution network across the continent. By 1940, Opel was the largest car manufacturer in Europe. The moral complexities of this would haunt GM—their German subsidiary continued operating through the Nazi era, though GM executives would later claim they had lost control of these operations once war broke out. When war came, the transformation was total. General Motors ranked first among United States corporations in the value of wartime production contracts. William S. Knudsen, GM's president, left to serve as head of U.S. wartime production for President Franklin Roosevelt—working for a dollar a year. Between February 10, 1942 and September 9, 1945, not a single passenger car for civilian use left any GM assembly line. Instead, the numbers tell an almost incomprehensible story: 119,562,000 artillery shells; 39,181,000 cartridge cases; 206,000 aircraft engines; 13,000 Navy fighter planes and torpedo bombers; 97,000 aircraft propellers; 301,000 aircraft gyrocompasses; 38,000 tanks and tank destroyers; 854,000 trucks; 190,000 canons; 1.9 million machine guns and submachine guns; 3.1 million carbines; 3.8 million electric motors; 11 million fuses; 360 million ball and roller bearings; 198,000 diesel engines.

No other corporation, anywhere on earth, at any time in history, ever did more to win a war. The famous "Duck"—the DUKW amphibious vehicle—was a GM creation. GM built over 21,000 of them, at a cost to the government of $10,800 each. At 31 feet long, the Duck could carry a payload of well over 5,000 pounds. Between D-Day on June 6, 1944 and May 8, 1945, Ducks moved 5.05 million tons of cargo onto the continent of Europe.

By 1941 GM was making 44 percent of all the cars in the United States and had become one of the largest industrial corporations in the world. But the war years weren't just about production—they fundamentally changed American society. Women entered factories in unprecedented numbers. African Americans, previously excluded from most industrial jobs, found new opportunities. The social transformations that would reshape America in the 1960s had their roots in GM's wartime factories.

The post-war era saw GM's apotheosis. Pent-up consumer demand, suburban expansion, and the interstate highway system created perfect conditions for automotive dominance. GM didn't just ride this wave—it helped create it. The company's styling studios, led by Harley Earl, turned cars into rolling sculptures. The 1948 Cadillac introduced tail fins inspired by the P-38 Lightning fighter plane. The 1953 Corvette created an entirely new category: the American sports car. The 1955 Chevrolet Bel Air became an icon of American optimism.

The numbers were staggering. By the mid-1950s, GM employed over 500,000 people directly and millions more indirectly. The company's market capitalization exceeded that of the next three automakers combined. "What's good for General Motors is good for America," supposedly said CEO Charles Wilson (though the actual quote was more nuanced). The statement became infamous, but at the time, it seemed self-evidently true.

GM's international expansion accelerated. The company became Brazil's largest automaker, dominated Australia through Holden, maintained its European presence through Opel and Vauxhall, and even attempted to crack the Japanese market. By the 1960s, GM was building cars on every inhabited continent. The sun never set on the GM empire.

The 1960s brought new challenges and new triumphs. Ralph Nader's "Unsafe at Any Speed" attacked the Corvair, launching the consumer safety movement. GM's response—hiring private detectives to investigate Nader—became a public relations disaster when exposed. Yet the company continued to prosper. The muscle car era—Pontiac GTO, Chevrolet Camaro, Oldsmobile 442—showed GM could still capture the zeitgeist.

Labor relations remained complex. The company had learned to live with the UAW, and the pattern bargaining system they established—where UAW contracts with one of the Big Three set the pattern for the others—created predictability. But it also created rigidity. Health benefits, pensions, and job banks—payments to laid-off workers—seemed affordable when GM controlled half the market. They would prove crushing when that dominance ended.

By 1970, GM was unquestionably the most powerful industrial corporation in world history. It sold more than half the cars in America, employed more people than many countries' entire manufacturing sectors, and generated profits that dwarfed those of any competitor. The company that Billy Durant had cobbled together from parts, that Alfred Sloan had organized into a machine, had become something beyond either man's imagination: not just a company but an institution, not just a business but a way of life.

Yet signs of trouble were emerging. A new competitor had appeared in the rearview mirror—small, distant, easy to dismiss. Toyota sold just 257 cars in America in 1958. By 1970, Japanese automakers had captured 4% of the U.S. market. GM executives, surveying their empire from the fourteenth floor of the headquarters building in Detroit, weren't particularly worried. After all, they were General Motors. They had survived the Depression, won the war, and dominated the peace. What could possibly go wrong?

V. The Slow Decline: Competition & Complacency (1970s–2008)

Roger Smith stood before a packed auditorium in 1981, his first day as GM's CEO, and declared war on the future. "We're going to spend our way to success," he announced, outlining plans to invest $40 billion—more than the GDP of many countries—to transform GM into a high-tech powerhouse. Robots would replace workers. Computers would design cars. Saturn would revolutionize how cars were built and sold. GM would leapfrog the Japanese through sheer technological superiority. Seven years later, Michael Moore's documentary "Roger & Me" would savage Smith as the CEO who destroyed Flint while pursuing his techno-utopian dreams. Both narratives were true. Both missed the deeper story: GM wasn't dying from any single disease but from a syndrome of interconnected failures that had been metastasizing for decades.

The 1973 oil crisis should have been GM's wake-up call. Gas lines stretched for blocks. American consumers suddenly cared about fuel economy. Honda Civics and Toyota Corollas flew off dealer lots while GM's land yachts—Buick Electras, Cadillac Eldorados, Oldsmobile 98s—sat unsold. GM's response? The Chevrolet Chevette, a hastily badge-engineered version of an Opel design, and the Cadillac Seville, essentially a glorified Chevy Nova priced like a Mercedes. The message to consumers was clear: GM either didn't understand the crisis or didn't care. The truth was more complex and more damning. Under the leadership of Roger B. Smith in the 1980s, GM began to experience a decline. Foreign automakers, led by Toyota and Honda, were capturing some of GM's market share and the unwieldy GM bureaucracy was often slow to respond to changes in consumer demands. Over the decade of the 1980s, GM spent upwards of $90 billion attempting to remake itself, including a 1981 joint venture with the Japanese robot manufacturer, Fujitsu-Fanuc. With the resulting venture, GMF Robotics, GM became the largest manufacturer of robots in the world.

The robots famously painted each other instead of the cars—a perfect metaphor for GM's dysfunction. Smith's vision of "lights-out factories" that could run without workers crashed into reality. The technology wasn't ready, the execution was botched, and the culture was toxic. GM's market share fell from 46% to 35% during Smith's tenure. Meanwhile, Toyota and Honda weren't just building better cars; they were building them with less automation and more respect for workers' intelligence.

The Saturn experiment epitomized both GM's ambition and its confusion. Launched in 1985 as "a different kind of car company," Saturn was supposed to prove GM could beat the Japanese at their own game. Separate factories, separate dealer networks, separate culture—essentially, GM admitting its core business was so broken it needed to start over from scratch. Saturn initially succeeded, building a loyal customer base and innovative labor agreements. But it was never properly funded, never fully integrated, and eventually became just another division producing badge-engineered mediocrity. The EV1 story perfectly encapsulates GM's dysfunction. On December 5, 1996, General Motors introduced the EV1, its first production electric car. The EV1 was available through lease only and represented a significant milestone in electric vehicle development. It had zippy acceleration, aerodynamic bodywork, and pioneering regenerative braking technology that would later become standard in all electric vehicles. GM built 1,117 EV1s between 1996 and 1999, leasing them to customers who loved them passionately.

However, due to limited range, high production costs, and scant infrastructure, GM discontinued the EV1 program by 2003. But here's where GM's tone-deafness reached its apex: instead of selling the cars to the devoted customers who wanted to keep them, GM recalled every single EV1 and crushed them. The sight of these innovative vehicles being destroyed while customers literally held candlelight vigils became a public relations disaster, immortalized in the documentary "Who Killed the Electric Car?" GM had spent over a billion dollars developing cutting-edge technology, then destroyed it all rather than support a small fleet of vehicles. It was corporate stupidity elevated to performance art.

Quality problems plagued every division. The notorious diesel engines of the late 1970s—converted gasoline engines that couldn't handle diesel's compression—turned "diesel" into a dirty word for American consumers. The Chevrolet Citation, GM's first front-wheel-drive compact, was recalled so many times that Consumer Reports called it one of the worst cars ever tested. Badge engineering reached absurd levels: by the mid-1980s, a Chevrolet Celebrity, Pontiac 6000, Oldsmobile Cutlass Ciera, and Buick Century were essentially the same car with different grilles.

In 2004, GM discontinued the Oldsmobile brand—a division that had existed since 1897, that had pioneered the automatic transmission, that had once epitomized American middle-class aspiration. The brand that had introduced the Rocket V8 engine died not with a bang but with a whimper, its last models indistinguishable from their Chevrolet siblings.

The financial engineering that had once been GM's strength became its weakness. Rather than investing in better cars, GM invested in financing. General Motors Acceptance Corporation (GMAC) became more profitable than the automotive operations. GM was essentially a bank that happened to make cars. When you're making more money from loans than from products, you've lost the plot.

Meanwhile, Toyota methodically improved quality, efficiency, and customer satisfaction. The Toyota Production System—lean manufacturing, just-in-time inventory, continuous improvement—became the gold standard. While GM was spending billions on robots that didn't work, Toyota was empowering workers to stop the production line if they spotted a defect. While GM was fighting its unions, Toyota was building a collaborative culture at its American plants. The student had become the master.

The 2000s brought more desperate moves. Bob Lutz, the legendary product guru, was brought back to improve vehicles, and he did—the Cadillac CTS, Chevrolet Malibu, and Pontiac Solstice showed GM could still build compelling cars. But it was too little, too late. Legacy costs—pensions and healthcare for hundreds of thousands of retirees—added $2,000 to the cost of every car GM built. Market share continued its inexorable decline.

By 2007, warning lights were flashing red. GM posted a loss of $38.7 billion, the largest annual loss in automotive history. The company that had once controlled over half the U.S. market now held less than 24%. In 2008, Toyota Motor Corporation surpassed GM as the world's largest automaker, ending a 77-year reign. The king was dead, even if it didn't know it yet.

Then came September 2008. Lehman Brothers collapsed. Credit markets froze. Car sales plummeted. GM, which had been burning through cash for years, suddenly faced an existential crisis. In December 2008, CEO Rick Wagoner, along with his counterparts from Ford and Chrysler, drove to Washington in hybrid vehicles (they had learned from the private jet fiasco) to beg for government loans. GM stated that it was nearly out of cash and may not survive past 2009.

The empire that Billy Durant built, that Alfred Sloan organized, that had won the war and defined American prosperity, was weeks away from liquidation. Everything that had made GM great—its size, its scope, its integration, its legacy—had become liabilities. The slow decline was over. The fall was about to begin.

VI. The Fall: Bankruptcy & Government Bailout (2008–2009)

Rick Wagoner sat in the Treasury Building on March 27, 2009, waiting to meet with Steven Rattner, the Obama administration's "car czar." He thought they would discuss GM's restructuring plan. Instead, Rattner delivered a message from the President of the United States: Wagoner was fired, effective immediately. After 32 years with the company, eight as CEO, Wagoner was out. No American president had ever fired the chief executive of a private company before. But then, no American company like GM had ever fallen so far, so fast.

The numbers were apocalyptic. In the fourth quarter of 2008, GM burned through $9.6 billion in cash—about $100 million per day. Vehicle sales had dropped 45% from their peak. The company's stock, which had traded above $40 in October 2007, fell below $2. GM's market capitalization, once larger than the GDP of most countries, had shrunk to less than $1 billion—making it worth less than Hasbro, the toy company.

On December 19, George W. Bush announced that he had approved the bailout plan, which would give loans of $17.4 billion to U.S. automakers GM and Chrysler. Bush provided $13.4 billion immediately, with another $4 billion available in February 2009. It was unprecedented: a Republican president, in his final days in office, essentially nationalizing two of America's largest corporations. "If we were to allow the free market to take its course now, it would almost certainly lead to disorderly bankruptcy," Bush explained, adding that such a collapse would send the economy into a deeper and longer recession.

But the Bush loans were just life support. The real reckoning came with the Obama administration. President Barack Obama announced that he would give GM 60 additional days to try and restructure their company and prove their viability. If they succeeded, Washington would provide General Motors with additional bridge loans. However, if GM could not meet the requirements set by the White House, a prepackaged bankruptcy was probable.

The government's automotive task force, led by Rattner and Ron Bloom, discovered a company even more dysfunctional than they had imagined. GM had 92 different IT systems that couldn't talk to each other. The company was still organized around Alfred Sloan's brand hierarchy, even though the brands had lost all distinctiveness. Pontiac, once the excitement division, was selling rebadged Chevrolets. Saturn, created to be different, had become just another outlet for generic GM products. Hummer, acquired during the SUV boom, was now a liability in an era of $4 gasoline.GM filed for Chapter 11 reorganization in the Manhattan New York federal bankruptcy court on June 1, 2009. The numbers were staggering: $172.81 billion in debts and $82.29 billion in assets, making it the fourth-largest bankruptcy in U.S. history. The government will pour another $30 billion into GM to fund operations during its reorganization. Taxpayers will end up with a 60% stake in GM, with the union, its creditors and federal and provincial governments in Canada owning the remainder of the company.

The restructuring was brutal and necessary. GM will shed its Pontiac, Saturn, Hummer and Saab brands and cut loose more than 2,000 of its 6,000 U.S. dealerships by next year. That could result in more than 100,000 additional job losses if those dealerships are forced to close. The company that once operated over 150 plants in North America would emerge with just 34. Employment would fall from 91,000 to 64,000. Salaried retirees would lose dental and life insurance benefits. The old GM's $54.4 billion in debt would be reduced to $17 billion in the new company.

The speed was breathtaking. Through the bankruptcy process, the "good" assets were sold to a new company—creatively named "New GM"—while the toxic assets remained with "Old GM," later renamed Motors Liquidation Company. The entire process took just 40 days, making it one of the fastest major bankruptcies in American history. On July 10, 2009, the new General Motors Company emerged from bankruptcy.

The ownership structure told the story: the U.S. government owned 60.8%, the Canadian and Ontario governments owned 11.7%, the UAW's healthcare trust owned 17.5%, and unsecured creditors got the remaining 10%. The United States of America had become the majority owner of General Motors. The company founded by a capitalist wheeler-dealer, built by the ultimate corporate manager, was now controlled by politicians and bureaucrats.

President Obama tried to reassure markets: "What I am not doing—what I have no interest in doing—is running GM." The administration established clear principles: the government would not interfere in day-to-day operations, would not use its ownership stake to protect plants or dealers, and would exit as soon as practicable. As a result of this restructuring, GM will lower its breakeven point to a 10 million annual car sales environment. Before the restructuring, GM's breakeven point was in excess of 16 million annual car sales.

The human cost was immeasurable. Families that had worked for GM for generations suddenly found themselves without jobs or benefits. Communities built around GM plants became ghost towns. Dealers who had invested their life savings in GM franchises were wiped out with 72 hours' notice. The psychological impact on Detroit was devastating—the city that had put the world on wheels was now the symbol of American decline.

But there was also clarity. For the first time in decades, GM knew exactly what it was: four brands (Chevrolet, Cadillac, Buick, GMC), focused on North America and China, with a cost structure that could actually compete. The sprawling empire was gone. The bureaucratic maze was simplified. The legacy costs that had been slowly strangling the company were largely eliminated.

Ed Whitacre, the former AT&T CEO brought in to chair the new GM, captured the moment perfectly: "This is not the old GM. The old GM is dead. This is the new GM." He was right in ways he probably didn't fully understand. The company that emerged from bankruptcy wasn't just financially restructured—it was culturally transformed. The arrogance was gone, replaced by a hunger to prove the skeptics wrong. The complacency was gone, replaced by an urgency that comes from near-death experiences.

The bailout would remain controversial for years. Critics on the right saw it as socialism, government picking winners and losers, a dangerous precedent for state intervention in private enterprise. Critics on the left saw it as corporate welfare, saving shareholders and executives while workers bore the pain. The $10.3 billion loss taxpayers ultimately took when the government sold its last shares in 2013 became a political talking point for years.

Yet without the bailout, the consequences would have been catastrophic. The Center for Automotive Research estimated that the government rescue saved 1.2 million jobs and preserved $34.9 billion in tax revenue. The collapse of GM would have taken down much of the supplier base, potentially destroying Ford and devastating what remained of American manufacturing. Sometimes the unthinkable—government ownership of General Motors—is preferable to the alternative.

VII. The Phoenix: Post-Bankruptcy Recovery (2009–2015)

Dan Akerson stood before a room full of skeptical Wall Street analysts in August 2010, his first major presentation as GM's new CEO. A former Navy officer and telecom executive, Akerson was an outsider in the insular world of Detroit automotive culture. His message was blunt: "We're not going to out-Japan the Japanese. We need to out-innovate them." Behind him, a slide showed GM's North American market share: 18.8%, less than half what it had been when Akerson joined the Navy in 1970. The analysts weren't buying it. GM stock was trading at $29, well below the $33 IPO price from nine months earlier. One analyst asked pointedly: "Why should anyone believe this time is different?"

It was a fair question. The "new" GM looked suspiciously like the old one. The same headquarters building in Detroit's Renaissance Center. Many of the same executives. The same union contracts, albeit modified. The same dealer body, albeit smaller. Most importantly, the same product portfolio that had failed to excite consumers for decades. The Chevrolet Malibu was still boring. The Buick LaCrosse still looked like something your grandfather would drive. Cadillac was still chasing the Germans with cars that weren't quite good enough.

But beneath the surface, something fundamental had changed. The bankruptcy had done more than clean up the balance sheet—it had shattered the cultural inertia that had paralyzed GM for decades. Akerson, precisely because he was an outsider, could ask questions that had been verboten under the old regime. Why does it take four years to develop a new car? Why do we have 26 different types of cup holders? Why are there seven layers of management between the factory floor and the CEO?The IPO itself was a masterpiece of financial engineering and political theater. On November 17, 2010, General Motors made a successful return to the stock market with an initial public offering (IPO) that raised $20.1 billion at $33 per share. It was the largest IPO in U.S. history at the time. The government reduced its stake from 61% to 33%, recovering $13.5 billion. The symbolism was powerful: just 17 months after bankruptcy, GM was back on the New York Stock Exchange.

But symbols don't sell cars. The real work happened in the factories and design studios. Mark Reuss, who would later become president, led a product revolution. The philosophy was simple but radical for GM: no more mediocrity. Every vehicle had to be best-in-class or at least competitive. The Chevrolet Cruze, GM's new compact car, actually handled well. The Cadillac ATS could genuinely compete with a BMW 3 Series. The Chevrolet Silverado remained a profit machine but now had the quality to justify its price. On December 10, 2013, GM became the first automaker to appoint a female CEO. Mary Barra, a 33-year GM veteran who had started as an 18-year-old co-op student inspecting hood and fender panels at Pontiac, became CEO on January 15, 2014. The daughter of a GM die-maker, Barra was the anti-Roger Smith: an engineer who actually understood cars, a consensus builder who listened before deciding, a leader who famously declared "no more crappy cars" as her north star.

Barra's first test came immediately. Just weeks into her tenure, GM began recalling vehicles for faulty ignition switches that could turn off while driving, disabling airbags. The problem had killed at least 13 people. Internal documents showed GM had known about the issue for over a decade but hadn't acted. It was the company's darkest hour since bankruptcy—proof that the cultural problems ran deeper than any financial restructuring could fix.

Barra's response was transformative. She fired 15 employees, including senior executives. She created a "Speak Up for Safety" program encouraging employees to report problems without fear of retaliation. She testified before Congress with a combination of contrition and determination that won grudging respect. Most importantly, she used the crisis to complete the cultural transformation that bankruptcy had begun. The old GM—bureaucratic, insular, in denial—was finally, truly dead. On December 9, 2013 the U.S. government sold its remaining shares of GM stock. The Treasury recovered $39 billion of the $49.5 billion it invested, resulting in a loss of $10.5 billion to taxpayers. Critics called it corporate welfare. Defenders pointed to the Center for Automotive Research study showing the bailout saved 1.2 million jobs and preserved $34.9 billion in tax revenue. The "Government Motors" era was officially over.

With government ownership behind it, GM could finally focus on the future. The company posted record profits: $9.7 billion in 2011, its best year ever. New products were actually competitive. The Chevrolet Impala, once a rental car special, was named Consumer Reports' top sedan. The Cadillac CTS could legitimately compete with BMW. The Corvette Stingray proved GM could still build world-class performance cars.

But Barra understood that success in traditional vehicles wasn't enough. The industry was changing more fundamentally than at any time since Durant assembled his empire. Tesla was showing that electric vehicles could be desirable. Google was developing self-driving cars. Uber was reimagining transportation itself. The next decade wouldn't be about better cars—it would be about reimagining mobility.

The recovery numbers told only part of the story. Yes, GM was profitable again. Yes, quality had improved dramatically. Yes, market share had stabilized around 17-18%. But the deeper transformation was cultural. The company that had once epitomized bureaucratic inertia was becoming nimble. The company that had once dismissed innovation was embracing it. The company that had nearly died from arrogance was learning humility.

By 2015, six years after bankruptcy, GM was unrecognizable from the bloated giant that had collapsed in 2009. It was leaner—34 U.S. plants versus over 100 at its peak. It was more focused—four brands versus eight. It was more global—making more money in China than in North America. Most importantly, it was hungrier. Near-death experiences have a way of clarifying priorities.

The phoenix had risen. But the question now wasn't whether GM had recovered from its past. It was whether it could invent its future. The company that had defined the 20th century's transportation model would have to help create the 21st century's. Electric vehicles. Autonomous driving. Mobility as a service. The old GM would have dismissed these as fads. The new GM would bet its existence on them.

VIII. The Electric Revolution: GM's Second Act (2015–Present)

Mary Barra stood before a packed audience at the Consumer Electronics Show in Las Vegas on January 6, 2016—not the Detroit Auto Show, but CES, the technology industry's premier event. Behind her, a sleek electric concept car rotated slowly on a platform. "This is the Chevrolet Bolt EV," she announced, "200 miles of range for $30,000 after federal tax credits. It goes on sale this year." The audience erupted. Tesla's Model 3 was still a promise; GM's Bolt was real. For the first time in decades, General Motors had beaten Silicon Valley at its own game.

The moment was more significant than anyone in that audience realized. GM—the company that had killed the EV1, that had been synonymous with gas-guzzling SUVs, that environmentalists loved to hate—was going all-in on electric vehicles. Not as a compliance play or a science experiment, but as the core of its future strategy. The company that had invented planned obsolescence was planning its own obsolescence, deliberately cannibalizing its immensely profitable internal combustion business for an uncertain electric future.

The decision to abandon the EV1 had come from fear, not vision. Now, in 2016, GM was choosing hope over fear. Barra stated "GM is committed to delivering the best driving experiences to our customers in a disciplined and capital efficient manner", though this commitment would evolve dramatically in the coming years.

The transformation began with a simple acknowledgment: Tesla had proven electric vehicles could be desirable, not just dutiful. But where Tesla targeted the luxury market with the Model S and Model X, GM saw an opening in the mass market. The Bolt represented something radical—not in its technology, though that was impressive, but in its positioning. This wasn't a compliance car built to satisfy California regulators. This was GM saying, definitively, that electric vehicles were the future.

Behind the scenes, the real revolution was happening in GM's research labs and boardrooms. The heart of GM's strategy became a modular propulsion system and a highly flexible, third-generation global EV platform powered by proprietary Ultium batteries, which would allow the company to compete for nearly every customer in the market today, whether they were looking for affordable transportation, a luxury experience, work trucks or a high-performance machine.

The Ultium platform, unveiled in March 2020, represented the biggest bet in GM's history. The Ultium battery used large (23.0-by-4.0-by-0.4-inch) pouch-type cells that packaged energy more densely than cylinders could, weighing about 3 pounds each, holding 0.37 kWh of energy, and could be arranged vertically or horizontally to suit space requirements. GM would be first to monitor battery cells wirelessly using the Bluetooth-like 2.4-GHz spectrum, reducing cost, weight, complexity, warranty problems, and space required to solder all those wired connections. It constantly monitored battery health, sharing info with the cloud to detect potential issues with certain battery batches, and enabled flash reprogramming when retrofitting newer battery chemistries or when repurposing a pack for its second life.

On January 25, 2022, General Motors outlined its plans to become a leading electric vehicle maker, committing $35 billion towards electric and autonomous vehicles through 2025. This investment marks a significant pivot towards sustainability and aims to produce 30 new EV models globally by 2025, with a goal of transitioning to a fully electric lineup by 2035. The numbers were staggering—more than Ford and Stellantis combined were spending on EVs. This wasn't hedging; this was transformation.

But the journey to electric leadership would prove more challenging than any PowerPoint presentation suggested. GM's battery assembly plants had persistent problems with the automation that packs battery cells into modules, which delayed the launch of the Hummer EV and kept other vehicles from getting into mass production. Building Ultium batteries had been problematic, making it difficult for GM to sell more than 70,000 EVs in the early part of the year.

The Cruise autonomous vehicle bet represented another massive gamble. In the 2010s, a resurgent GM made big moves into electric vehicles, autonomous driving technology and ride-sharing via its Cruise subsidiary. Since GM bought a controlling stake in Cruise for $581 million in 2016, the robotaxi service piled up more than $10 billion in operating losses while bringing in less than $500 million in revenue.

The vision was compelling: a world where autonomous electric vehicles would revolutionize transportation, where GM would operate fleets of robotaxis, where car ownership itself might become obsolete. Cruise represented GM's attempt to own not just the vehicle but the entire mobility ecosystem. The Origin, a vehicle with no steering wheel or pedals, designed purely for autonomous ride-sharing, embodied this future.

Reality proved messier. After one of its autonomous Chevrolet Bolts dragged a San Francisco pedestrian who was hit by another vehicle in 2023, the California Public Utilities Commission alleged Cruise then covered up details of the crash for more than two weeks. The incident became a crisis that forced a complete restructuring of the unit.

By December 2024, GM made a stunning reversal. GM would no longer fund Cruise's robotaxi development work given the considerable time and resources that would be needed to scale the business, along with an increasingly competitive robotaxi market. GM expected the restructuring to lower spending by more than $1 billion annually after the proposed plan was completed, expected in the first half of 2025.

Instead, GM intended to combine the majority-owned Cruise LLC and GM technical teams into a single effort to advance autonomous and assisted driving. The focus shifted to Super Cruise, GM's hands-free driving technology. Super Cruise was offered on more than 20 GM vehicle models and currently logging over 10 million miles per month. This represented a fundamental strategic pivot—from revolutionary robotaxis to evolutionary driver assistance, from moonshot to pragmatism.

The Ultium strategy itself underwent dramatic revision. In October 2024, GM announced the retirement of the Ultium brand, marking a significant shift. Introduced with great fanfare just four years ago, the modular battery platform was initially presented as a "one-size-fits-all" solution for a wide range of EVs. GM's decision to move away from Ultium stemmed from the need to optimize its battery approach for different vehicles, exploring various battery chemistries to better match power and performance demands, shifting from a single-chemistry solution—nickel manganese cobalt cells developed in partnership with LG Energy Solution—towards a more flexible approach that included prismatic cells produced with Samsung SDI.

Despite these pivots, GM's EV momentum continued building. GM was on track to produce and wholesale 200,000 EVs in North America in 2024, with the company expecting to reach a key profitability milestone by the end of the year, with its EV business becoming profitable on a contribution-margin basis. The Chevrolet Equinox EV, starting at $35,000, proved GM could build compelling mass-market electric vehicles. The Cadillac Lyriq showed the company could compete in the luxury EV space. The GMC Hummer EV and Silverado EV demonstrated that even the most traditional truck buyers could be converted to electric.

The company's global restructuring reflected this new focus. It exited or sold less profitable brands like Opel, Vauxhall and Holden to refocus on core markets where it could win. China, once seen as the future of GM's growth, became a profitable joint venture rather than a corporate obsession. The strategy was clear: dominate in North America, compete selectively globally, and lead the transition to electric vehicles.

Yet challenges remained formidable. Tesla's market capitalization still dwarfed GM's despite selling a fraction of the vehicles. Chinese automakers like BYD were growing rapidly, threatening to enter the U.S. market with low-cost EVs. The charging infrastructure remained inadequate. Consumer adoption, while growing, lagged behind the industry's massive investments. And the political landscape around EVs remained volatile, with potential changes in federal incentives threatening to upend carefully laid plans.

IX. Playbook: Management & Strategy Lessons

The transformation of General Motors from Durant's holding company to Sloan's machine to today's technology company offers a masterclass in both management excellence and organizational failure. The lessons aren't just historical curiosities—they're living principles that explain why some companies survive existential crises while others disappear.

The Power and Peril of Decentralization

Alfred Sloan's greatest innovation wasn't a car—it was an organizational structure. His decentralized model with centralized control became the template for every large corporation in America. Division heads ran their businesses like CEOs, with full profit-and-loss responsibility, but within strict financial guidelines set by headquarters. The beauty was its balance: autonomy to innovate, controls to prevent chaos.

But what made GM great also made it rigid. By the 1980s, the decentralized divisions had become isolated kingdoms, each protecting their turf rather than collaborating. The Pontiac division wouldn't share innovations with Chevrolet. Cadillac insisted on developing its own engines even when corporate platforms were superior. The structure designed to promote entrepreneurship had calcified into bureaucracy. The lesson: organizational structures must evolve with strategic needs. What works in one era becomes a straitjacket in the next.

Market Segmentation as Competitive Advantage

Sloan's "ladder of success"—Chevrolet to Pontiac to Oldsmobile to Buick to Cadillac—was brilliant marketing psychology. It wasn't just about having different products; it was about creating an aspirational journey. A young family starting with a Chevrolet could envision their future Cadillac. Each step up the ladder reinforced brand loyalty while maximizing lifetime customer value.

The failure came when the distinctions blurred. By the 1980s, a Chevrolet Celebrity, Pontiac 6000, Oldsmobile Cutlass Ciera, and Buick Century were essentially the same car. Badge engineering destroyed brand identity. Customers paying Buick prices for Chevrolet quality felt betrayed. The lesson: market segmentation only works when the segments offer genuinely different value propositions. Cosmetic differentiation is worse than no differentiation.

The Importance of Financial Controls

Sloan's introduction of return-on-investment calculations, statistical controls, and rigorous financial metrics transformed GM from Durant's chaotic empire into a profit machine. Every division's performance was measured against precise targets. Capital was allocated based on data, not politics. This financial discipline enabled GM to weather the Great Depression better than most rivals.

But financial engineering eventually replaced product excellence. By the 2000s, GMAC was more profitable than the automotive operations. GM was essentially a bank that happened to make cars. When the financial crisis hit, the company had neither great products nor financial strength. The lesson: financial controls are essential but insufficient. They must serve the core business, not replace it.

Managing Through Crisis

GM's history is punctuated by existential crises: the 1920-21 recession that ousted Durant, the Great Depression, World War II's total transformation, the 2008-09 bankruptcy. Each crisis revealed character. In 1920-21, Sloan used the downturn to reorganize completely. During the Depression, GM maintained employment where possible and emerged stronger. In World War II, the company literally saved democracy. But in 2008-09, GM needed government intervention to survive.

The pattern is clear: crises that arrive when companies are strong become opportunities for transformation. Crises that arrive when companies are weak become near-death experiences. The key difference isn't the crisis itself but the organization's preparedness. Strong balance sheets, flexible operations, and cultural resilience determine whether crisis catalyzes transformation or triggers collapse.

Capital Allocation in Capital-Intensive Industries

The automotive industry requires massive capital investments with long payback periods. A new vehicle platform costs billions and takes four years to develop. Factories cost hundreds of millions and operate for decades. These investments must be made based on predictions about consumer preferences, regulatory requirements, and competitive dynamics years in the future.

GM's capital allocation history offers stark lessons. The $90 billion spent on automation in the 1980s largely failed because the technology wasn't ready. The billion dollars spent developing the EV1, only to crush every vehicle, was capital destruction. But the $35 billion commitment to EVs announced in 2022, while risky, positioned GM for the industry's future. The lesson: in capital-intensive industries, timing matters more than amount. Being too early is as fatal as being too late.

The Challenge of Organizational Transformation

GM's multiple transformations—from Durant's assemblage to Sloan's machine, from bankruptcy to recovery, from internal combustion to electric—reveal how difficult true change is. Each transformation required not just new strategies but new cultures. The company that epitomized bureaucracy had to become entrepreneurial. The company that perfected internal combustion had to embrace electric. The company that built hardware had to master software.

Mary Barra's post-bankruptcy transformation succeeded where previous attempts failed because it came after existential crisis. The near-death experience of bankruptcy shattered cultural inertia in ways that no management consultant ever could. The lesson: incremental change rarely works in large organizations. Transformation requires crisis, real or manufactured, to overcome institutional resistance.

Platform Strategies in Manufacturing

GM's platform strategies—from Sloan's body-sharing to today's Ultium architecture—show both the power and limitations of standardization. Platforms create economies of scale, reduce complexity, and accelerate development. The Ultium platform theoretically allowed GM to build everything from compact cars to massive trucks using common components.

But platforms also create rigidity. When battery technology evolved faster than expected, the Ultium architecture became a constraint rather than an enabler. GM's 2024 decision to abandon Ultium branding and embrace multiple battery chemistries acknowledged this reality. The lesson: platforms must be flexible enough to evolve with technology, not lock companies into yesterday's solutions.

Government Relations and Industrial Policy

No company has had a more complex relationship with government than GM. The company helped win World War II, faced antitrust scrutiny in the 1950s, battled safety regulations in the 1960s, and was saved by government bailout in 2009. This history reveals an uncomfortable truth: in strategic industries, government and business are permanently intertwined.

The 2009 bailout remains controversial, but the alternative—GM's liquidation—would have devastated American manufacturing. The government lost $10.5 billion on its investment, but preserved 1.2 million jobs and $34.9 billion in tax revenue. The lesson: industrial policy isn't about picking winners but preventing catastrophic losses. Sometimes the government must act as investor of last resort to preserve critical capabilities.

X. Analysis & Investment Perspective

General Motors in 2024 presents a fascinating investment paradox. The company trades at less than 5 times earnings, a valuation that screams either deep value or value trap. The market clearly doesn't believe GM's transformation story, pricing the stock as if it's still the lumbering giant that collapsed in 2009 rather than the technology company it claims to have become.

Bull Case: EV Leadership, Cruise Potential, Manufacturing Expertise

The bullish thesis rests on multiple pillars. First, GM's EV portfolio is genuinely competitive. The Chevrolet Equinox EV at $35,000 offers compelling value. The Cadillac Lyriq competes credibly with Tesla's Model Y. The Silverado EV and GMC Hummer EV prove that even truck buyers—the most conservative automotive segment—will embrace electrification if the product is right.

Second, while GM abandoned robotaxi ambitions, the technological capabilities developed through Cruise aren't lost. Super Cruise remains one of the best driver assistance systems available, and the company's pivot to personal autonomous vehicles could prove prescient. Full autonomy may be further away than Silicon Valley promised, but incremental automation that consumers actually want and will pay for generates real value today.

Third, GM's manufacturing expertise remains unmatched. Tesla may have revolutionized electric vehicles, but GM knows how to build millions of vehicles profitably. As the EV market matures from early adopters to mainstream consumers, manufacturing excellence, dealer networks, and service infrastructure become competitive advantages. GM has all three.

The financial position is robust. The company generated $9.8 billion in net income in 2023 on revenue of $171.8 billion. The balance sheet, cleansed through bankruptcy, can support the massive investments required for electrification. Unlike many EV startups, GM doesn't need capital markets to fund its transformation.

Bear Case: Legacy Costs, Union Challenges, Chinese Competition

The bearish perspective is equally compelling. Despite bankruptcy, GM still carries legacy burdens. The UAW contract signed in 2023, while necessary for labor peace, adds significant costs. Healthcare and pension obligations for current workers remain substantial. These structural disadvantages versus non-union competitors like Tesla or potential Chinese entrants are permanent.

The core ICE business, while still profitable, faces inexorable decline. GM itself targets an all-electric lineup by 2035. But ICE vehicles generate most of today's profits. The company must manage one of history's most challenging industrial transitions: deliberately obsoleting its profit engine while building its replacement. Few companies successfully cannibalize themselves.

Chinese competition looms as perhaps the greatest threat. BYD surpassed Tesla in global EV sales. Chinese automakers, backed by government support and possessing battery technology advantages, could eventually enter the U.S. market. Tariffs provide temporary protection, but technology and cost advantages are harder to overcome. GM competed successfully against the Japanese; competing against the Chinese may prove harder.

The technology transition requires capabilities GM doesn't naturally possess. Software development, battery chemistry, autonomous driving algorithms—these aren't traditional automotive competencies. GM must compete for talent with Silicon Valley while maintaining its manufacturing base in Detroit. Cultural conflicts are inevitable.

Valuation and Market Perception Gaps

The markets have never really regained trust for automakers, and General Motors' shares trade at a low valuation relative to earnings. The price-to-earnings ratio under 5 suggests the market expects earnings to collapse. This could reflect skepticism about EVs achieving profitability, concern about Chinese competition, or simple distrust of a company that already bankrupted shareholders once.

Yet this valuation disconnect creates opportunity. If GM successfully transitions to EVs while maintaining reasonable profitability, the stock could rerate dramatically. Even reaching Tesla's production volumes, let alone its valuation multiples, would imply massive upside. The market's skepticism has created an asymmetric risk-reward proposition.

Comparisons with Tesla, Toyota, and New Entrants

Tesla's market capitalization exceeds $800 billion despite producing fewer than 2 million vehicles annually. GM's market capitalization is $53 billion despite producing over 6 million vehicles. This 15-to-1 valuation gap can't be justified by growth rates alone. Either Tesla is overvalued, GM is undervalued, or the market sees something fundamental that traditional metrics miss.

Toyota offers another comparison point. Despite being late to battery electric vehicles, Toyota trades at a higher multiple than GM. The market trusts Toyota's hybrid strategy and manufacturing excellence more than GM's electric transformation. This suggests execution risk, not strategy risk, drives GM's discount.

New entrants like Rivian and Lucid trade at substantial valuations despite minimal production. The market values their clean-slate approach and absence of legacy burdens. GM must prove it can transform despite, not because of, its history.

The Future of American Manufacturing

GM's investment case transcends financial metrics. The company represents American manufacturing's future. If GM successfully transforms into an electric, autonomous, software-driven company, it proves legacy industrial companies can evolve. If GM fails, it suggests American manufacturing can't compete with Silicon Valley's innovation or China's scale.

The stakes extend beyond shareholders. GM employs over 167,000 people globally. Its supply chain supports millions more jobs. The company's success or failure ripples through communities across America. This isn't just an investment decision; it's a bet on American industrial competitiveness.

XI. Epilogue: What Does GM Represent?

General Motors is more than a company—it's a mirror reflecting American industrial history. Through GM's story, we see the entire arc of American capitalism: the wild entrepreneurship of the early 20th century, the organizational revolution that created the modern corporation, the post-war dominance that seemed eternal, the complacency that nearly proved fatal, and the ongoing struggle for reinvention in a digital age.

The company that Billy Durant assembled from parts became Alfred Sloan's template for industrial organization. The corporation that won World War II became the symbol of American prosperity. The giant that seemed too big to fail did fail, spectacularly and publicly. And the phoenix that emerged from bankruptcy now attempts another transformation, from internal combustion to electric, from hardware to software, from ownership to mobility.

Each era of GM reflects its zeitgeist. Durant's wheeling and dealing captured the Gilded Age's freewheeling capitalism. Sloan's scientific management embodied Progressive Era faith in rational organization. Post-war GM represented American triumphalism. The 1980s GM reflected corporate America's bureaucratic sclerosis. Today's GM embodies the challenge facing every legacy company: how to transform without losing what made you successful.

The cycles of innovation, dominance, and disruption that define GM's history aren't unique, but their scale and impact are unprecedented. When GM dominated, it literally shaped American geography through suburban expansion and interstate highways. When GM collapsed, it nearly took American manufacturing with it. As GM transforms today, it helps determine whether America remains competitive in defining industries.

The lessons for other legacy companies are sobering. Cultural change is harder than strategic change. Financial engineering can't substitute for product excellence. Market dominance breeds complacency that becomes fatal when competition shifts. Government relationships are unavoidable in strategic industries. And transformation usually requires crisis to overcome organizational inertia.

Yet GM's survival also offers hope. A company can lose half its market share and remain viable. Bankruptcy doesn't mean death if the underlying business has value. New leadership can change culture, even in century-old organizations. And legacy companies can develop new capabilities, though the process is painful and expensive.

GM's next chapter remains unwritten. The company could emerge as a leader in electric and autonomous vehicles, proving that industrial giants can transform. Or it could become another Kodak or Sears, a cautionary tale of former greatness. The outcome matters not just for shareholders but for American manufacturing's future.

What does GM represent? It represents the best and worst of American business. The innovation and the inertia. The ambition and the arrogance. The resilience and the rigidity. Most importantly, it represents the ongoing struggle to balance efficiency with innovation, scale with agility, tradition with transformation.

The company that once proclaimed "what's good for General Motors is good for America" discovered that survival requires serving customers, not just claiming importance. The corporation that defined 20th-century transportation must now help invent 21st-century mobility. The phoenix that rose from bankruptcy must keep transforming or risk irrelevance.

General Motors' story isn't finished. Whether the next chapters describe continued reinvention or slow decline depends on decisions being made today in Detroit boardrooms, Warren technical centers, and factories across America. The only certainty is that GM's journey—from Durant's dream through Sloan's machine to Barra's transformation—will remain one of business history's most important narratives.

Because ultimately, General Motors represents a fundamental question: Can established institutions transform themselves, or does progress require creative destruction? The answer matters for every legacy company facing disruption, every employee whose livelihood depends on industrial transformation, and every investor betting on either continuity or change. GM's fate isn't just its own—it's a verdict on whether American industry can evolve or merely age.

XII. Recent News

The latest developments at General Motors reflect both the opportunities and challenges facing the company's transformation. In the third quarter of 2024, GM reported net income of $3.0 billion on revenue of $48.8 billion, demonstrating the continued strength of its traditional business even as it pivots toward electrification. The company's full-size pickup trucks and SUVs continue generating substantial profits that fund the electric transition.

GM's December 2024 decision to no longer fund Cruise's robotaxi development work given the considerable time and resources needed to scale the business, along with an increasingly competitive robotaxi market, is expected to lower spending by more than $1 billion annually after the restructuring is completed in the first half of 2025. This dramatic strategic reversal represents both pragmatism and admission that the autonomous vehicle revolution may take longer than anticipated.

GM remains on track to produce and wholesale 200,000 EVs in North America, with its EV business expected to become profitable on a contribution-margin basis by the end of 2024. The Equinox EV has emerged as a bright spot, with strong initial sales suggesting GM can compete in the mass-market EV segment.

The company's November 2024 announcement of a $5 billion share buyback program signals confidence in its financial position despite the massive investments required for electrification. This capital return comes even as GM continues investing heavily in battery plants and EV manufacturing capacity.

Labor relations remain complex. The UAW contract ratified in November 2023 provides labor peace through 2028 but adds approximately $9 billion in costs over the contract's life. The agreement includes 25% wage increases and improved benefits, necessary for workforce stability but challenging for cost competitiveness.

On the competitive front, GM faces intensifying pressure. Tesla's Cybertruck launch and continued Model Y dominance challenge GM's pickup and SUV profits. Chinese automaker BYD's global expansion, while not yet directly threatening the U.S. market, demonstrates the speed at which new competitors can emerge. Traditional rivals Ford and Stellantis are also accelerating their EV transitions, though with mixed success.

The regulatory environment continues evolving. The Inflation Reduction Act's EV tax credits remain crucial for GM's mass-market EV strategy, but political uncertainty surrounds their future. California's Advanced Clean Cars II rule, mandating increasing EV sales percentages, creates both opportunity and obligation for GM's largest market.

Supply chain challenges persist but are improving. Semiconductor availability has largely normalized, though battery raw material costs remain volatile. GM's investments in domestic battery production through joint ventures with LG Energy Solution and Samsung SDI aim to reduce supply chain vulnerability while qualifying for federal incentives.

XIII. Links & Resources

Academic Papers and Case Studies - "General Motors: The Rise and Fall of an Industrial Giant" - Harvard Business School Case Study (2019) - "The Sloan Model: Management Innovation at General Motors" - MIT Sloan Management Review - "Bankruptcy and Bailout: The 2009 GM Restructuring" - Journal of Economic Perspectives - "From ICE to EV: Strategic Transformation in the Auto Industry" - Strategic Management Journal

Key SEC Filings and Investor Presentations - GM 2023 Annual Report (Form 10-K) - GM Investor Day Presentation (October 2024) - Quarterly Earnings Reports and Transcripts (investor.gm.com) - Proxy Statements and Corporate Governance Documents

Historical Archives and Primary Sources - Alfred P. Sloan's "My Years with General Motors" (1964) - The GM Heritage Center Archives - Detroit Public Library National Automotive History Collection - Hagley Museum and Library - GM Corporate Archives

Industry Reports and Analysis - Center for Automotive Research Industry Reports - Cox Automotive Industry Insights - IHS Markit Automotive Analysis - Bloomberg Intelligence Automotive Coverage - Morgan Stanley and Goldman Sachs Equity Research

Books and Long-form Articles - "Once Upon a Car" by Bill Vlasic - "Crash Course" by Paul Ingrassia - "The Reckoning" by David Halberstam - "Taken for a Ride" by Jack Doyle - "The Deal Maker" by Axel Madsen (Durant biography)

Documentary and Video Resources - "Roger & Me" (1989) - Michael Moore's documentary on GM's impact on Flint - "Who Killed the Electric Car?" (2006) - Documentary on the EV1 - "Revenge of the Electric Car" (2011) - Follow-up on EV development - GM Corporate YouTube Channel - Product launches and corporate announcements - Automotive News video interviews with Mary Barra and GM leadership

The transformation of General Motors from its founding in 1908 to its position in 2024 represents one of the most complex and important corporate stories in history. From Durant's audacious assembly of an automotive empire to Sloan's invention of the modern corporation, from post-war dominance to near-death in bankruptcy, from traditional manufacturing to electric and autonomous vehicles, GM's journey mirrors the evolution of American industry itself. Whether the company successfully completes its latest transformation will determine not just its own fate but provide crucial lessons for every legacy company facing technological disruption. The story continues to unfold, making General Motors not just a piece of business history but a living experiment in corporate evolution.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube