Globe Life: The Working-Class Cash Cannibal

I. Introduction & Episode Roadmap

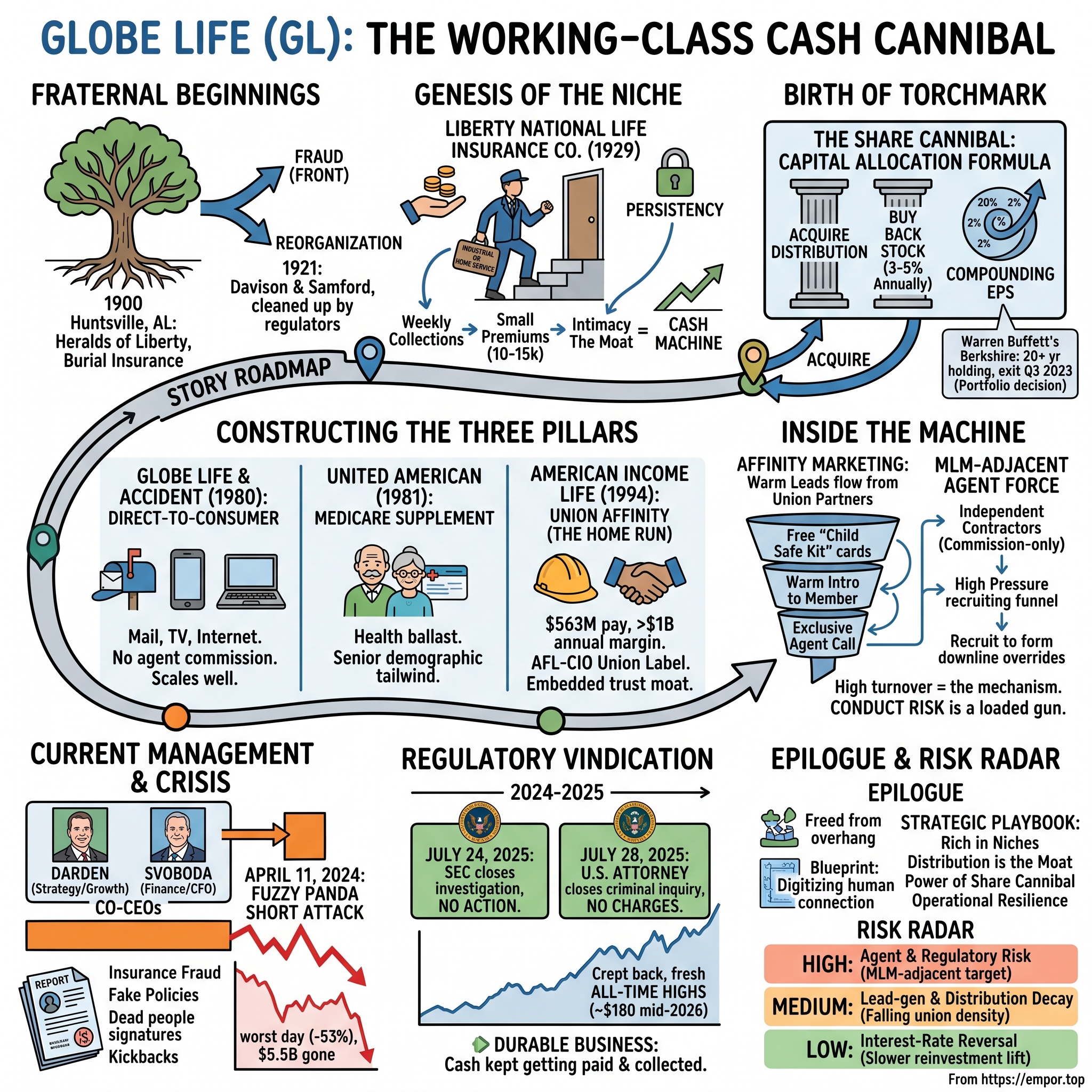

On a spring evening in Arlington, Texas, the retractable roof of Globe Life Field slides open over 40,000 baseball fans, and the name of a life insurance company glows in LED light across the home of the Texas Rangers. It is a strange kind of fame. Ask a hedge fund analyst in Manhattan to name the company on the ballpark, and many will shrug. Globe Life Inc. is a $16-billion enterprise that has quietly minted mid-teens returns on equity for four decades, yet it has never been a name that dinner-party investors drop. It sells something almost nobody in high finance would want to own: whole life insurance policies with face values of ten or fifteen thousand dollars, sold to union electricians, warehouse workers, and middle-income families who pay twenty or thirty dollars a month.

Here is the paradox that makes the company worth three hours of your attention. Those tiny, unglamorous policies — the kind a Wall Street product designer would sneer at — have historically thrown off so much cash, at such high margins, that Globe Life has compounded shareholder capital at rates most technology companies would envy. For most of its modern life it earned a net-income return on equity north of 20% and an operating return in the mid-to-high teens, and it did so while carrying essentially no glamour and taking essentially no fashion risk.911 Warren Buffett's Berkshire Hathaway held the stock for more than two decades, drawn to exactly the qualities that make it boring: low-cost distribution, conservative investing, and a customer base that no prestige competitor wanted to fight over.19

And then, on the morning of April 11, 2024, the boredom ended. A short seller called Fuzzy Panda Research published a report accusing the company of systemic insurance fraud — agents allegedly writing policies for dead and fictitious people, forging signatures, and running the flagship agency like a drug-fueled pyramid scheme, all while executives collected what the report called an undisclosed kickback.1 By the closing bell the stock had fallen 53.14%, from $104.93 to $49.17, the worst single day in its history and roughly $5.5 billion of market value gone before lunch.2 It was one of the most violent short-seller strikes of the decade.

The remarkable part is what did not happen next. The policies kept getting paid. The cash kept getting collected. And fifteen months later, in the span of five days in late July 2025, both of the government investigations the report had triggered were formally closed with no action: the SEC on July 24 told the company it did not intend to recommend an enforcement action, and the U.S. Attorney's Office for the Western District of Pennsylvania closed its criminal inquiry on July 28 without charges.45 The stock, which had crept back over the intervening year, pushed on to fresh all-time highs; by mid-2026 it traded near $180, well above where it stood before the report ever appeared.6

This is a story about that durability — where it comes from, whether it is real, and where it could still crack. To understand it, we have to go back much further than 2024. The roadmap: the fraternal-society origins in turn-of-the-century Alabama and the Samford family that turned burial insurance into a cash machine; the 1980s reorganization into Torchmark and the early, almost heretical embrace of the share buyback; the three acquisitions — Globe Life, United American, and above all American Income Life — that assembled the modern company; the strange, MLM-adjacent distribution engine that recruits thousands of commission-only agents a year and burns through most of them by design; the current co-CEOs and how their incentives are wired; the anatomy of the short attack and the regulatory clearance; and finally, the durable investment case and the specific ways it could still break. Let's start where every good insurance story starts — with people afraid of dying poor.

II. The Genesis of a Cash-Compounding Niche: Liberty National and the Samford Legacy

In the rural American South of 1900, a funeral was a financial catastrophe. A working family that lost its breadwinner faced not only grief but the very real prospect of a pauper's burial — an indignity that, in a churchgoing, honor-bound culture, was almost worse than the death itself. Into that fear stepped a fraternal benefit society incorporated in Huntsville, Alabama, called the Heralds of Liberty, offering members a modest promise: pay your small dues, and we will make sure you are buried with dignity.12

There is a delicious irony buried in the company's own origin story, one that Fuzzy Panda's writers either never found or never used. The Heralds of Liberty did not begin as a model of probity. By the accounts preserved in the standard corporate histories, the early operation was effectively a front for another entity headquartered in Philadelphia, and it fell into such disrepair that the Alabama Insurance Department took it over and reorganized it around 1921, installing new management to clean it up.1213 The men who did that cleaning — Robert Park Davison and, decisively, Frank P. Samford — are the true founders of what became Globe Life. A company that would one day be accused of institutionalized fraud was, in fact, born out of a state regulator rescuing policyholders from exactly that. History rhymes in uncomfortable ways.

Under Davison and Samford, the reformed enterprise made its first stock offering in 1929 under a new, plainer name that stripped away the mystic lodge trappings: Liberty National Life Insurance Company.12 The headquarters settled in Birmingham, and the product settled into what the industry called "industrial" or "home service" insurance — small policies whose premiums were collected in person, in coins, week by week, at the policyholder's door.1213 This was not a footnote to the business; it was the business. Liberty National's Home Service Division became its largest, built on armies of local agents who walked the same neighborhoods for years, knew the families, and came by to collect a dime or a quarter and check in.12

It is worth pausing on why this model was so quietly powerful, because the mechanism is the whole thesis of the company that followed. Consider the economics from the customer's side. A burial policy cost pennies a week. It was cheap enough that canceling it saved almost nothing, yet valuable enough — emotionally and practically — that lapsing it felt like tempting fate. The result was extraordinary persistency: policyholders simply did not quit. And because the agent came to the door, the relationship was personal in a way that mass-market financial products never are. The competition, meanwhile, wanted nothing to do with this customer. The great mutual giants of the industrial North — MetLife, Prudential — chased wealthier policyholders and larger face amounts, where the prestige and the big premiums lived. That left the working-class Southeast as open country. This is the first appearance of a pattern you will see again and again: Globe Life's ancestors prospered not by winning a fight, but by farming ground that no one else wanted to plow.

There is a subtler point buried in the "home service" label that is easy to miss and central to the economics. When an agent physically collects a premium every week or two, three things happen at once that no online form can replicate. The agent becomes a fixture in the customer's life, which makes lapsing feel like letting down a neighbor. The frequent contact surfaces opportunities to sell a second or third policy — a rider for a child, a slightly larger face amount after a raise — turning one household into an annuity of small, compounding sales. And the collection itself, however labor-intensive, keeps the book astonishingly current, because a lapse is caught the week it happens rather than discovered at renewal. The trade-off was cost: an army of agents walking neighborhoods is expensive to run, which is exactly why the model only works on policies sticky enough and margins fat enough to carry it. Liberty National's genius was recognizing that on small, permanent, working-class policies, that math worked — and that the surplus it generated was the real prize. When the company acquired the Brown-Service burial operation in the 1940s, it was buying more of exactly this: more households, more doors, more coins.12

The industrial-insurance era also taught the company a cultural lesson that would echo for a century: in this business, the agent is the moat, and the agent is also the risk. A door-to-door force that handles cash and holds a family's trust is a powerful distribution asset and a permanent supervisory problem. The same intimacy that makes a policy sticky makes misconduct hard to see from headquarters. That tension — distribution power inseparable from conduct exposure — is not a modern discovery forced by short sellers; it is baked into the DNA of a company that has always sold trust, one doorstep at a time.

The leadership stayed close to home, in both senses. Frank P. Samford ran the company until his death; his son, Frank Samford Jr., took the top job in 1967 and held it until 1985, and Ronald K. Richey succeeded him in 1986.12 By the time the second Samford generation was in charge, the family had noticed something that would define the company's next fifty years. The sticky, high-margin, low-face-value policies threw off far more cash than the insurance operation itself needed to grow. Insurance is a business where you collect premiums today and pay claims over decades; run it conservatively on a customer base that never lapses, and it becomes a spigot of surplus capital. The question that would consume the next chapter was deceptively simple, and it is the question at the heart of every great capital-allocation story: what do you do with all that money?

III. Reorganization and Rebranding: The Birth of Torchmark

By the late 1970s the Samford-era leadership had a high-class problem. The insurance company generated more cash than a single state-chartered life insurer could sensibly deploy, and the corporate structure — one operating company doing one thing — was a straitjacket. You cannot easily buy other businesses, allocate capital across lines, or return money to owners at scale when the holding entity is the insurer. So in 1979 and 1980 the company built a holding structure above the insurance operation, and in 1982 it gave the parent a deliberately grander, more expansive name meant to signal that it was no longer just a Birmingham life insurer: Torchmark Corporation.1213

The rebrand mattered less than the machine it unlocked. Under a holding company, Torchmark could do two things that would define its identity for the next four decades. It could acquire other insurers and financial businesses and run them as capital-efficient subsidiaries. And it could take the torrent of surplus cash and, instead of empire-building with it, hand it back to shareholders in the most tax-efficient way available — by buying in its own stock.

This second move deserves emphasis, because in the 1980s it was close to heretical. Corporate America of that era measured manhood in size: revenue, headcount, assets, the sprawl of the org chart. A management team that deliberately shrank its share count was, to many boards, admitting it had run out of ideas. Torchmark saw it the other way around. If your business earns a high return on equity and generates cash you cannot reinvest at the same high return, then the single most reliable way to compound per-share value is to retire shares. Buy back 3% to 5% of the company every year, keep net income growing at a modest single-digit clip, and the arithmetic quietly turns pedestrian profit growth into double-digit growth in earnings per share. The company was, in the vivid phrase, a cannibal — steadily eating itself, and getting richer per surviving bite. This philosophy has never really changed; by the 2020s the modern company was still retiring roughly 5% of its shares in a heavy year, having shrunk its count by well over a quarter across a decade.9

It is easy, and a little too flattering, to narrate this as pure genius. A neutral observer should note the conditions that made it work — and the risk it carries. The buyback machine is only virtuous when two things are true: the stock is trading at or below intrinsic value, and the underlying business is genuinely as durable as management believes. Buy back overvalued stock, or buy back the shares of a business quietly rotting underneath you, and the "cannibal" strategy destroys value with the same mechanical efficiency it otherwise creates it. Torchmark's bet was that its working-class insurance franchise was the rare combination of cheap-to-value and boringly durable. For forty years, that bet paid. Whether it still holds is precisely the question the short sellers would later force everyone to ask.

It is worth making the arithmetic concrete, because the "cannibal" label can sound like a slogan rather than a mechanism. Imagine a business whose net income grows a pedestrian 4% a year — the kind of growth that would bore a growth-fund manager to tears. Now suppose it retires 5% of its shares annually. The share count shrinks, so each remaining share lays claim to a larger slice of that slowly growing profit; earnings per share compound at closer to 9% or 10%. Reinvest nothing in glamour, take no fashion risk, and let the buyback do the work, and a company that grows like a utility can deliver equity returns that look like a growth stock — provided the underlying profit is real and the shares are bought at sensible prices. That is the entire trick, and it is why the durability of the profit engine and the discipline of the repurchase price are the two hinges on which the whole strategy swings. Break either one and the machine runs in reverse.

One outside endorsement did more than any investor letter to cement the company's reputation. Berkshire Hathaway became a shareholder — and, contrary to a widely repeated claim that Buffett bought in during the early 1980s, the reliable record dates Berkshire's Torchmark position to around 2001.19 The correction matters, because it is a small example of how legend accretes around a stock. What is true is that Berkshire held the position for more than twenty years — through the August 2019 renaming that retired the Torchmark name and moved the ticker from TMK to GL — prizing the same unglamorous traits18 — low-cost distribution, a conservative bond portfolio, a customer base with no prestige competition — that this narrative keeps returning to. And what is also true is that Berkshire sharply cut the stake in the third quarter of 2023, selling roughly two-thirds of its shares months before the short report landed.19 Buffett's exit was not prescience about fraud; it was, more prosaically, a portfolio decision. But it meant that when the storm came, the company's most famous validator was already most of the way out the door. To understand what that storm was really about, we have to look at what Torchmark actually bought with all that cash.

IV. The M&A Masterstrokes: Constructing the Three Pillars

If the holding company was the machine, acquisitions were the fuel — but only a specific kind of acquisition. Torchmark never went hunting for scale or diversification for its own sake. It bought distribution: proprietary, hard-to-replicate ways of reaching the same kind of customer Liberty National had always served, the person of modest means who wanted a small, permanent policy and a human being to sell it to them. Three purchases built the company that exists today, and the third is one of the most underappreciated acquisitions in the history of American insurance.

The first pillar came home in 1980, when Liberty National acquired Globe Life and Accident Insurance Company — the business whose name now sits on the parent and on a Texas ballpark.1214 Globe Life had been founded in 1951 in Oklahoma City by Ralph Reece and John Singletary, and it had cracked a different distribution code entirely.1415 Instead of sending agents door to door, it sold small-face-value policies directly to consumers through the mail, and later through television, internet, and call centers.14 The strategic beauty of direct response is that it eliminates the single largest cost in traditional life insurance: the agent's commission. There is no salesperson to pay an override to, no recruiting funnel to maintain. Instead there is a mailing list, a response rate, and a cost-per-acquisition that, run well against proprietary data, can be brutally low. Globe Life's direct-mail engine gave Torchmark a second, structurally different way to manufacture the same product — one whose economics improved with scale, because every incremental policy spread the fixed cost of the database and the mailing infrastructure a little thinner. (The outline's specific "Young American" children's-policy branding could not be verified in any authoritative source, so it is set aside here; what is documented is that Globe built its franchise on small, direct-marketed policies, including children's whole life.)

The second pillar arrived quickly after, when Torchmark's predecessor acquired United American Insurance Company in 1981.1213 United American solved for a different life stage. Founded in the 1940s, it had built one of the industry's early Medicare Supplement products in the 1960s and distributed through independent brokers and general agents rather than a captive force.12 As the Baby Boomers began their long march toward sixty-five, a franchise selling supplemental health coverage to seniors was a demographic tailwind you could set your watch by. Just as important, health insurance premiums behaved differently from life premiums — they smoothed the cash flows and gave the group a second product to cross-sell. United American was never the glamorous pillar, but it was the ballast.

And then, in 1994, came the home run. Torchmark paid approximately $563 million for American Income Life Insurance Company, a Waco, Texas insurer with a genuinely unusual franchise.1617 AIL had been founded in 1951 on $25,000 of borrowed capital by Harold Goodman and his nephew, Bernard Rapoport — and here again the outline needs a gentle correction, because the company was co-founded by the two men, not by Rapoport alone.17 Rapoport, though, is the figure history remembers: a Texas liberal, a major Democratic donor, and a philanthropist who ran an insurance company built almost entirely around organized labor. AIL sold supplemental life and accident coverage to union members, and it had spent decades embedding itself into the union movement so deeply that competitors simply could not follow.

There is a human texture to the AIL deal worth dwelling on, because it explains why the moat was for sale at all. Rapoport was a committed liberal running an insurance company as an expression of his politics — he genuinely believed the labor movement deserved a carrier that treated it as a partner rather than a mark. By 1994 he was in his seventies, and the question of succession for a founder-driven, mission-shaped business is always fraught. Selling to Torchmark handed the franchise to an owner that prized exactly the traits Rapoport had built — persistency, low-cost distribution, conservative underwriting — and that had the capital-allocation discipline to let a good machine keep running rather than "fix" it. The cultural fit was the deal's quiet genius: Torchmark bought a business it understood at a bone-deep level, because AIL was, in essence, the union-affinity version of the door-to-door working-class insurer that Liberty National had been for a century.

Was $563 million too much for a mid-sized union insurer in 1994? On the surface, maybe. In hindsight, it looks like one of the great underpays in the sector. Three decades later AIL is the single largest engine inside Globe Life. In the third quarter of 2025 alone, American Income generated $261 million of life underwriting margin — more than half of the entire company's life margin — on $451 million of life premium, an underwriting margin of 58%.9 Even allowing that the 2025 quarter was flattered by a one-time accounting gain we will come to, AIL now throws off, in a single year of underwriting margin, roughly what Torchmark paid for the whole company in 1994. Put differently: the acquisition now earns back its entire original purchase price in well under a year.

What makes AIL so hard to compete with is not the product — supplemental life insurance is a commodity — but the moat around its distribution, and that moat is literally a label. Since 1973 AIL has carried an official "Union Label" designation from the AFL-CIO, one of only two insurers in the country to hold it; its home-office employees and field representatives are themselves organized under a union; and since 1961 the company has waived premiums for policyholders during authorized strikes.1617 Think about what that structure does to a would-be competitor. A conventional, non-union insurer trying to sell to a local union hall is a stranger at best and a class enemy at worst. AIL walks in wearing the union's own label, with unionized agents and a policy that protects members precisely when a strike leaves them most vulnerable. That is not a product advantage a rival can price against; it is a relationship advantage forged over half a century, and it is the closest thing in insurance to a cornered resource. How AIL actually converts that trust into policies — the machinery of leads and agents — is where the story gets both impressive and uncomfortable.

V. Inside the Distribution Machine: Affinity Marketing & Segment-Level Power

Picture a union member opening her mailbox to find an offer that costs her nothing: a free "Child Safe Kit" to record her children's fingerprints and medical information in case of emergency, or a no-cost accidental-death benefit for members of her local. All she has to do to claim it is fill out a card with her name, address, and phone number and mail it back.16 That card is the beating heart of American Income Life's business, and understanding why reveals both the elegance and the fragility of the whole enterprise.

The card converts a cold, hostile sales problem into a warm one. Cold-calling strangers to sell life insurance is a miserable, low-yield grind — it is why the traditional agency model chews through people. But a member who has just requested a free benefit through her own union is not a stranger; she is a pre-qualified, self-identified, receptive lead who has effectively raised her hand. When an AIL agent calls to "deliver" the free kit or benefit, the door is already open. The genius is that the lead-generation cost is subsidized by goodwill: the union endorses the program, the member gets something genuinely useful for free, and the agent gets a warm introduction. This is affinity marketing at its most refined, and it is why AIL never had to compete on the open market for attention.

The other half of the machine is the agent force itself, and this is where a neutral observer has to look hard, because it is simultaneously the engine of the returns and the source of the risk. Globe Life's exclusive agents — roughly 17,600 producing agents across American Income, Liberty National, and Family Heritage in 2025 — are not employees.9 They are independent contractors, paid on commission only, with no salary and no floor. The organizational structure is explicitly pyramidal in the neutral, structural sense: agency owners and managers recruit new agents, train them, and earn overriding commissions on everything their recruits sell. Recruit a big enough downline, and a manager's override income can dwarf personal production. If that structure sounds familiar, it is because it shares its skeleton with multi-level marketing — a resemblance the short sellers would later weaponize, and one management has never fully been able to wave away.

Consider the mathematics of this model from the company's point of view, because it is genuinely clever and genuinely troubling at the same time. Commission-only contracting means the company bears almost no fixed cost for a new agent. Recruit a hundred people; the eighty who fail sell little and cost the company essentially nothing when they quit, because they were never on payroll. The twenty who succeed generate premium and, crucially, the handful who become recruiters build the next generation. High turnover is not a bug in this system — it is the mechanism. The company runs an enormous funnel, absorbs no downside from the washouts, and harvests the survivors. From a return-on-capital standpoint it is beautiful. From a conduct-and-culture standpoint it is a loaded gun, because a commission-only, recruit-driven, quota-pressured funnel is exactly the environment in which a minority of agents will cut corners — and where the incentive to inflate production, forge a signature, or write a policy that should never have been written is always present. Hold that thought; it is the entire subject of Section VII.

It helps to compare this to how a traditional insurer thinks about agents. A conventional carrier invests heavily in each recruit — training, licensing support, sometimes a salary or a draw against future commissions — and therefore treats agent attrition as expensive waste to be minimized. Globe Life's exclusive divisions invert the logic. Because the recruit costs almost nothing to onboard and nothing to lose, the company can afford to run a firehose, and the recruiting itself becomes a revenue-generating activity for the managers doing it. That is why the agent count, not the agent quality, is what the model optimizes for at the top of the funnel: more bodies in means more shots at finding the rare natural salesperson who will stay, build a downline, and become a multi-million-dollar producer. The uncomfortable corollary is that the incentive to recruit can, in a poorly supervised agency, overwhelm the incentive to sell honestly — because a manager earns overrides on a recruit's production whether or not every policy that recruit writes is real. This is not a hypothetical failure mode invented by critics; it is the specific mechanism the Arias Organization allegations would later claim had run out of control.

There is also a question a careful analyst should ask that management rarely volunteers: how much of reported "growth" in a recruiting-driven model is genuine demand versus funnel churn? When a company can juice near-term sales simply by recruiting harder, agent count and new-business figures can rise even as the quality of the underlying book erodes. Globe Life's defense — that it reports net sales and policies only after underwriting and quality control — is a meaningful control, but it does not fully neutralize the concern, because underwriting checks whether a policy is issuable, not whether the customer genuinely wanted it or will keep it. The truest test, therefore, is not sales growth but persistency: do the policies these agents write actually stay on the books and keep paying? That single question is the hinge on which the entire short-seller debate would eventually turn.

Step back to the segment level and the proportions come into focus. Life insurance is unambiguously the company: in the first nine months of 2025 it produced $2.51 billion of the $3.65 billion in total premium, about 69%, and roughly 82% of underwriting margin.9 Within life, American Income and the Direct-to-Consumer (Globe Life) division do the heavy lifting, both earning exceptionally high margins because small-face-value permanent policies, priced with discipline and sold to persistent customers, simply do not generate large or frequent claims relative to premium. Health insurance — about 31% of premium — is the diversifier: United American's Medicare Supplement business is the largest health line, with Family Heritage's supplemental disease and accident policies behind it.9 Health carries lower margins but steadier, more predictable cash flows and gives the agent force a second and third thing to sell into the same household. The picture that emerges is a company with one dominant profit engine (AIL life), one scalable low-cost engine (direct-to-consumer life), and a health book that exists mostly to stabilize and cross-sell. Who runs that machine today, and how they are paid to run it, tells you a great deal about what to expect next.

VI. Current Management, Incentives, and the Capital Allocation Formula

For most of the modern era, Globe Life was run by a pair — Gary Coleman and Larry Hutchison, longtime co-CEOs who split the top job between operations and law-and-administration. Co-CEO arrangements are unusual and often unstable; investors tend to distrust them because accountability blurs. Globe Life made the model a habit. When Coleman and Hutchison stepped back, the company simply handed the dual keys to a new duo. Effective January 1, 2023, J. Matthew Darden and Frank M. Svoboda became co-CEOs, with Coleman and Hutchison moving up to serve as co-chairmen of the board.10

The backgrounds of the two men map neatly onto the two things the company actually does. Darden came up through strategy — he had been the chief strategy officer — and carries the growth-and-distribution side of the business, including the delicate matter of the agent force. Svoboda was the chief financial officer, the steward of the bond portfolio and the buyback machine.10 It is a division of labor that mirrors the company's own dual personality: an operating engine that recruits and sells, and a capital-allocation engine that invests and returns. Whether two co-CEOs can move as decisively as one in a genuine crisis was, until April 2024, an untested question. It would soon be tested very publicly.

The more revealing document than any org chart is the proxy statement, because it tells you what management is actually paid to care about — and here Globe Life is unusually pure. The annual incentive plan for 2025 weighted operating earnings per share at 50%, with total premium and first-year collected premium making up the rest; the long-term equity awards were split evenly between growth in book value per share and average operating return on equity over a three-year period.11 Read that again with an eye to what is absent. There is no reward for sheer asset growth, no bonus for ballooning the balance sheet, no incentive to chase premium volume at the expense of profitability. Most insurance executives are, consciously or not, paid to get bigger. Globe Life's are paid to compound per-share value and to earn a high return on the equity they employ. That alignment is genuinely rare and genuinely good — it is the governance expression of the "cannibal" philosophy.

A skeptic should still press on two points, because good incentives on paper can curdle in practice. First, EPS-based targets are exactly the kind of metric that a buyback can flatter: retire enough shares and you can hit an EPS goal even as the underlying business stalls, so the quality of the growth matters more than the number itself. Second — and this is the sharper edge — a compensation scheme tuned to premium and collected premium sits in some tension with a distribution model that depends on a high-pressure, commission-only sales funnel. When you pay for premium growth and you source that growth from an army of independent contractors with no salary floor, you are, at the margin, paying for exactly the behavior that can shade into misconduct. That is not an accusation; it is a structural observation, and it is the observation the short sellers built their entire case on.

The capital-allocation formula itself is refreshingly simple to state: earn high returns on a working-class insurance book, invest the float conservatively, and return nearly all the excess to shareholders through buybacks rather than gamble it on transformational M&A. The investment side is deliberately dull. As of the third quarter of 2025, total investments stood at about $20.3 billion, of which fixed-maturity bonds were 88%, and 98% of those bonds were rated investment grade — overwhelmingly corporate bonds, with municipals and a sliver of government paper.9 This is not a portfolio reaching for yield; it is a portfolio built to be boring and to pay claims decades from now with near-certainty. The one genuine tailwind of the current era is rates. The portfolio's fixed-maturity book earned a taxable-equivalent yield of about 5.26% in the third quarter of 2025, while new money went in at roughly 6.3% — meaning every dollar the company reinvests as old bonds mature goes to work at a higher rate than the existing average, gently lifting net investment income over time.9 It is worth being precise about magnitude here: that lift is real but slow, and in fact net investment income was essentially flat year-over-year, because the yield benefit is spread across a very large book that turns over gradually.9 The "higher-for-longer" rate environment is a tailwind, not a jet engine.

An activist or short-oriented investor stress-testing this capital structure would push on a few genuine soft spots, and a neutral account should name them. First, the buyback discipline that looks so admirable is only as good as the price paid: in the third quarter of 2025 the company repurchased roughly 840,000 shares at an average price around $134 as the stock made new highs, and buying back one's own stock at elevated valuations is a materially less attractive use of capital than buying it at the $49 low the market briefly offered in 2024.9 A management team truly optimizing per-share value would, in theory, buy aggressively when the stock is cheap and ease off when it is dear; a mechanical "return nearly all excess cash" policy does not naturally do that, and the crisis was, ironically, the moment the buyback was most valuable and the balance sheet most constrained. Second, the very conservatism of the bond portfolio means the company has little room to improve returns through investment skill — the returns must come almost entirely from underwriting and from buybacks, which concentrates the whole thesis on the durability of the distribution engine. Third, an EPS-linked incentive on top of an aggressive buyback creates a structural temptation to flatter per-share results through share count even in a soft operating year, which is why the quality of premium growth deserves as much scrutiny as its headline rate. None of these is a red flag on its own. Together they describe a company whose financial engine is elegant but tightly coupled to a single point of failure — the sales machine — and that coupling is exactly what got tested next. All of which describes a well-run, conservatively financed compounding machine — right up until the morning someone accused it of being a fraud.

VII. The Short Seller Crisis & The Great Regulatory Vindication

At the market open on April 11, 2024, Fuzzy Panda Research hit publish, and one of the steadiest stocks in American finance came apart. The report's title alone signaled the intent: it accused Globe Life of disregarding "wide-ranging insurance fraud" while executives collected an undisclosed kickback scheme.1 What followed inside the document was a catalog of allegations designed to detonate.

The specifics were lurid and, if true, existential. Fuzzy Panda alleged that agents had written policies for dead people and opened policies for fictitious ones; that customer signatures had been forged; that funds had been withdrawn from consumers' bank accounts without approval; and that applicants who smoked had been passed off as non-smokers by faking tests.1 It characterized American Income Life as an MLM that "mirrors a pyramid scheme," where recruiting downline agents was more lucrative than actually selling insurance. It leveled culture allegations of sexual harassment, assault, and drug use concentrated at one of AIL's largest independent agencies, the Arias Organization. And it claimed that agencies linked to fraud accounted for more than $200 million in annual premium — on the order of 60% of AIL's new business in 2023 — while alleging that a senior executive had pocketed more than $65 million through an undisclosed interest in a testing vendor.1 It was not a report about a rounding-error problem; it was a report claiming the profit engine itself was fraudulent.

The market did not wait for verification. The stock fell 53.14% in a single session, from a prior close of $104.93 to $49.17 — the worst day in the company's history and roughly $5.5 billion of value erased.2 Nineteen days later, on April 30, a second short seller, Viceroy Research, piled on with a report it called "The Main Course," claiming that "fraudulent, dishonest, and misleading sales tactics are core to AIL's operations," citing an analysis of more than 11,000 documents and raising additional questions about the company's cash flows and reinsurance.3 Two credible, well-resourced short shops, aligned on the same thesis: this is not a few bad apples, this is the orchard.

Globe Life's response came the same day as the first report, and its tone is worth noting because it set the template for everything that followed. The company called the report "wildly misleading" and "driven solely by short-term profit," and it did not retreat.8 Rather than pause buybacks or promise a sweeping strategic review, management leaned into continuity. On the Q1 2024 earnings call on April 23 — the first live encounter with analysts after the attack — co-CEO Matt Darden addressed the Arias Organization directly, framing it as roughly 6% of new production and several hundred independent-contractor agents, and describing agency transitions as a routine feature of the business.7 Management stressed that the company reports net sales and policies only after they clear underwriting and quality-control processes, that American Income had internal controls to detect agent misconduct, and that it had not hesitated to terminate agents and agency owners where warranted, including notifying regulators.7

This is the moment to apply a genuinely skeptical lens rather than a promotional one, because "management denied it and stayed the course" is exactly what a fraudulent management would also do. The real question an activist investor had to answer in April 2024 was one of scale: was the alleged misconduct systemic financial rot that inflated the company's reported premiums and margins, or was it localized bad-agent behavior — real, ugly, but immaterial to the numbers — inside a distribution model whose commission-only, high-pressure structure makes some level of individual misconduct almost inevitable? The two interpretations lead to wildly different valuations. If the fraud was systemic, the persistency, the collected premium, and the underwriting margins were partly fiction, and the stock was worth a fraction of even its depressed price. If it was localized, the company was a durable compounder on sale at half price.

The evidence that accumulated over the following year pointed toward the second interpretation, though a fair observer should be precise about what was actually proven and what was merely not disproven. Through the Q2 2024, Q3 2024, and into the 2025 calls, analysts pressed management hard on compliance, audit trails, and recruiting — and the operating metrics that would have cracked under systemic fraud did not crack. Policy persistency held. Cash collection on in-force premium continued. New business, even after the company terminated agents tied to the flagged agencies, did not collapse in the way a fraud-dependent book would have. The company cooperated with the investigations, upgraded its sales-verification technology, and cut ties with bad actors.7 None of that is proof of innocence in a courtroom sense. But it is the kind of evidence that is hard to fake for fifteen consecutive months across regulated financial statements.

It is worth separating myth from reality on a few points that got blurred in the panic. The consensus narrative in the days after April 11 was that a fraud of this description meant the company's reported financials were unreliable and that a restatement or enforcement action was coming. The reality that emerged over the following year was more nuanced and, for the business, more favorable: the allegations that could be independently tested against regulated numbers — persistency, collected premium, underwriting margin — did not deteriorate in the way systemic fraud would require, while the allegations that were hardest to test were also the ones about individual agents and agency culture rather than about the integrity of the consolidated financial statements. A second myth was that the co-CEO structure would freeze the company in a crisis; in fact management's response was notable for its lack of drama — no strategic pivot, no suspension of buybacks, no capitulation to the short thesis, just a methodical insistence that the numbers were real and would be verified. Whether one reads that steadiness as confidence or as stonewalling depended entirely on which interpretation of the underlying facts one believed, which is precisely why the regulatory outcome mattered so much: it was the one referee both sides had to accept.

The Q&A sessions across the crisis calls are instructive to read against each other, because narrative consistency under pressure is itself evidence. Analysts returned, quarter after quarter, to the same pressure points — the share of business tied to flagged agencies, the adequacy of internal controls, the trajectory of agent recruiting — and management's answers stayed materially consistent with the framing Darden had set out on the April 2024 call: the affected agencies were a modest slice of production, misconduct was treated as an agent-level problem to be policed rather than a systemic one to be hidden, and the company would keep terminating bad actors and reporting them to regulators.7 Consistency is not the same as truth — a wrong story told consistently is still wrong — but a management team fabricating systemic fraud would have found it very hard to keep the operating metrics and the narrative aligned across five consecutive quarters of hostile questioning. The absence of a stumble is not proof, but it is data.

The resolution arrived in a five-day window in the summer of 2025. On July 24, Globe Life announced it had received a letter from the SEC staff stating that they had concluded their investigation and did not intend to recommend an enforcement action against the company.4 Four days later, on July 28, the company announced that the U.S. Attorney's Office for the Western District of Pennsylvania — which had earlier issued subpoenas the company said it had responded to — had closed its investigation into the sales practices of certain independent agents, meaning the Department of Justice would not pursue enforcement action against Globe Life or AIL.5 Two separate arms of the U.S. government, one civil and one criminal, had looked and walked away without a charge.

The market rendered its verdict. Having already climbed most of the way back over the intervening year, the stock pushed on through the clearances to fresh all-time highs; by the middle of 2026 it traded near $180, comfortably above its pre-report level and roughly triple its April 2024 low.6 The word "vindication" should be used carefully, though. A closed investigation is not a finding that nothing bad ever happened — it is a decision by regulators not to bring a case, which is a lower and different bar than affirmative exoneration. The short sellers' cultural allegations about individual agents were never the same claim as "the financials are fake," and the regulators' clearance speaks most directly to the latter. What the episode proved, rigorously, is that the business was durable: its cash never stopped flowing. What it did not prove is that the distribution model is clean enough never to generate another Arias. That distinction is the seed of the investment case that follows.

VIII. Playbook: Durable Business & Investing Lessons

Strip away the drama and the Globe Life story yields a handful of transferable lessons, each of which cuts two ways if you look at it honestly.

The first is that the riches really are in the niches. The instinct of ambitious managers is to move upmarket — bigger policies, wealthier customers, more prestige. Globe Life's ancestors did the opposite and got rich doing it, because the working-class, small-face-value segment combines three things the premium end lacks: low price sensitivity, extreme persistency, and almost no elite competition. A customer paying twenty-five dollars a month for a permanent policy does not shop it against a rival every renewal; a family that has held a burial policy for fifteen years does not lapse it lightly. The lesson is that a "worse" customer, correctly served, can be a far better business than a "better" one. The caution attached to it: a niche is only a fortress while no one wants it, and demographic or cultural change can quietly drain the moat of water.

The second lesson is that in insurance, distribution is the product. Underwriting a small term or whole life policy is a commodity skill; anyone can do it. What cannot be copied is the channel. AIL's union label and the direct-to-consumer database are not products a competitor can build a better version of — they are access rights and cost structures accumulated over decades. This is why the company's real assets do not appear cleanly on the balance sheet: the moat is a fifty-year relationship with organized labor and a proprietary mailing operation, not a bond or a building. The caution: channels can erode. Union density in America has fallen for decades, and direct-mail response rates decline as the world moves online. A moat made of distribution must be continuously reinvested in or it silts up.

The third lesson is the power of the share cannibal, already told in full: when a business earns high returns on capital and generates cash it cannot reinvest at the same rate, systematically retiring stock beats empire-building M&A as a path to per-share compounding — provided the stock is not overvalued and the business is genuinely durable. The discipline is as important as the mechanism; the same tool that compounds value in the right hands destroys it in the wrong ones.

The fourth lesson is the one the 2024–2025 crisis wrote in capital letters: operational resilience trumps media noise. The most powerful response to a short attack is not a louder press release but an unbroken operating record. Globe Life's defense worked not because management out-argued Fuzzy Panda but because the cash kept arriving and the metrics kept holding while the regulators looked. Investors who panicked at $49 and sold learned an expensive lesson about the difference between a narrative shock and a cash-flow shock. But the honest inversion of this lesson is worth stating: resilience through one crisis does not immunize a company against the cause of that crisis. The commission-only, recruit-driven funnel that produced the Arias allegations is still the funnel. The playbook survived; the structural risk did not disappear. Which brings us to a proper war-game of where the advantages are strong, where they are weakening, and what could still break the case.

IX. Strategic Analysis: Competitive Landscape & Risk Radar

To war-game Globe Life properly, it helps to run it through two disciplined frameworks — Hamilton Helmer's 7 Powers and Porter's Five Forces — and then to point a risk radar at the specific mechanisms that could fail. The goal is not to decorate the thesis but to test it.

Hamilton Helmer's 7 Powers

The strongest of Globe Life's powers is a cornered resource: American Income Life's multi-decade, exclusive relationship with organized labor, formalized in the AFL-CIO union label it has carried since 1973 and reinforced by its unionized agent force and strike-premium waiver.1617 This is not a power a competitor can buy or build quickly; it is the product of half a century of embedded trust, and it is genuinely rare. The honest caveat is that the resource is only as valuable as the underlying constituency, and American union membership has been in secular decline for forty years — the moat is deep but the reservoir behind it is slowly falling.

The second power is switching costs. A permanent whole life policy accrues cash value over time, and it grows more expensive to replace as the insured ages and health deteriorates. A fifty-five-year-old who has held a policy for two decades cannot easily swap it for a cheaper one; re-underwriting at an older age often means a worse price or no offer at all. That lock-in is what produces the persistency the whole model depends on. It is real, though it is strongest in the permanent-life book and weakest in the health and term lines.

The third power is scale economies, concentrated in the direct-to-consumer division. A mailing and digital-targeting database that has been refined over decades, spread across millions of policies, delivers a cost-per-acquisition that a subscale entrant cannot match — the fixed cost of the data and the infrastructure is amortized across a vast book. This is a genuine but bounded advantage: it protects the direct channel, but it does nothing for the agent-sold businesses, and it is vulnerable to the same digital erosion of direct-mail economics noted earlier.

Notably absent from the list are network economies and branding in the premium sense. Globe Life has scale and trust within its niches, but it commands no pricing power from brand prestige the way a luxury insurer might, and there is no network effect that makes each additional customer more valuable to the others. The powers it has are real; it is important not to invent ones it lacks.

Porter's Five Forces

The threat of new entrants is low, and for an unusual reason: the barrier is organizational, not financial. Anyone with capital can charter an insurer, but no one can quickly assemble a nationwide force of some 17,600 producing exclusive agents, a union label earned over fifty years, and a recruiting culture that regenerates the funnel every year.916 That takes decades, and it is precisely the kind of soft, cultural asset that money cannot fast-forward.

The bargaining power of buyers is low. Globe Life's customers are millions of individuals buying small policies; they are fragmented, they are relatively price-insensitive at the twenty-to-thirty-dollar-a-month level, and they have neither the scale nor the inclination to negotiate. This fragmentation is a feature — it is the flip side of serving a segment the giants ignore.

The intensity of rivalry is moderate and, crucially, oblique. The nearest structural analog is Primerica, which also runs a large recruited sales force selling protection products to middle-income households — but Primerica's model is built on term life sold alongside investment products through a "buy term and invest the difference" philosophy, aimed at a broader middle market rather than the union-affinity and burial-adjacent niches Globe Life farms. Aflac dominates worksite supplemental health with a brand and a duck that Globe Life cannot match, but it competes for the employer's payroll-deduction slot, not the union hall or the direct-mail box. The large carriers — MetLife, Prudential — long ago vacated the small-face-value working-class segment that is Globe Life's home ground. The upshot is that Globe Life rarely meets a competitor head-on in a price war, because its rivals are fishing adjacent waters with different bait. That obliqueness is a real advantage, but it cuts the other way too: it means the company's growth is capped by the size of its niches rather than propelled by taking share in a large, contested market. A business that no one attacks is also a business that cannot easily expand by conquest. The threat of substitutes — chiefly employer-provided group coverage and low-cost online term insurance from digital-first players — is a slow, structural pressure rather than an acute one, most relevant to the younger, healthier customers the direct-to-consumer channel courts, and least relevant to the older, union-embedded customers who anchor the profit engine.

The Material Risk Radar

Three risks are worth watching, in rough order of severity, and they are specific to the mechanisms above rather than generic macro worries.

Agent and regulatory risk is the highest. The commission-only, MLM-adjacent recruiting model is a permanent target — for the FTC on questions of independent-contractor classification and marketing conduct, for state insurance commissioners on sales practices, and for the next short seller looking for the next Arias. The July 2025 clearances closed two specific investigations; they did not repeal the structural feature that produced them. Any future misconduct scandal will land on a market that now knows exactly how violently this stock can move on such news.

Lead-generation and distribution decay is a medium, slow-burn risk. The whole AIL engine depends on warm leads flowing from union and affinity partners, and the whole direct engine depends on mail and digital response rates. A structural decline in either — falling union density, deteriorating direct-mail economics, a loss of trust with a major labor partner — would choke the sales funnel at its source, and it would do so quietly, over years, in a way that is hard to see in any single quarter.

Interest-rate reversal is a lower but real risk. The current tailwind runs in reverse if rates fall sharply: the roughly 6.3% new-money yield that today reinvests maturing bonds accretively would compress back toward or below the portfolio's average, and the slow lift to net investment income would flatten or turn negative.9 It is a low-to-medium risk precisely because the effect is gradual — the same slow-moving book that mutes the upside would mute the downside — but it is the macro variable that matters most to this particular business.

Sitting behind all three is the activist's structural critique, which the short episode made concrete: a company whose profits depend on a high-pressure, commission-only sales culture is running a permanent tension between growth incentives and conduct risk, and no amount of verification technology fully resolves it. That tension is the price of the returns. Which leaves the question every long-term investor actually cares about — where does this leave the business today, and what should you watch to know whether the machine is still working?

X. Epilogue & Looking Forward

Today the company sits in McKinney, Texas — where it has been headquartered since a 2006 move from Birmingham, and where in early 2025 it announced plans to relocate to new offices within the same city — running the same machine it has run for decades, now freed of the regulatory overhang that consumed 2024 and 2025.1420 Darden and Svoboda have come through their first genuine crisis with the strategy intact: the buybacks never stopped, the co-CEO structure held, and the operating metrics that mattered survived the most aggressive short attack the company had ever faced. That is a real accomplishment, and it is not the same thing as being invulnerable.

One second-layer diligence thread is worth pulling before turning to the future. The company's most famous shareholder is gone: Berkshire Hathaway, which held Torchmark and then Globe Life for more than two decades, cut roughly two-thirds of its position in the third quarter of 2023 — months before the short report — and the stock has since had to stand on its own operating record rather than on a validator's halo.19 That is arguably healthy. A thesis that rests on "Buffett owns it" is a thesis borrowed rather than owned, and the 2024–2025 stress test forced investors to underwrite the business directly: to decide for themselves whether the persistency was real, whether the margins were durable, and whether the regulators' silence meant what the bulls said it meant. A company that survives a 53% single-day drawdown and emerges at new highs without its celebrity anchor has, in a sense, earned a more honest shareholder base — one that is there for the cash flows rather than the association.

The forward blueprint management describes is evolutionary, not revolutionary: digitize the agent sales process — using data to route leads more intelligently and moving toward video-call selling — without severing the high-touch human relationship that makes a working-class customer trust an agent in the first place. It is a genuinely difficult needle to thread. The whole edge of the model is that a real person shows up with a free Child Safe Kit and earns a family's trust; automate too aggressively and you risk turning a warm, relationship-driven sale into the same cold, commoditized online transaction that the discount insurers already win. The bet is that technology can make the funnel more efficient without hollowing out the trust. Whether that is possible is not yet proven; it is the central execution question of the next decade.

For an investor trying to track whether the machine is still working, the noise-to-signal ratio on this stock is unusually high, so it is worth zeroing in on the few things that actually matter. Three metrics carry most of the signal. First, producing exclusive agent count, especially at American Income — because in a distribution-is-the-product business, the size and growth of the agent force is the leading indicator of future premium; a persistent decline here would matter far more than any single quarter's earnings.9 Second, life underwriting margin, particularly at AIL — the profit engine's margin is the truest read on whether pricing discipline and claims experience are holding, and it is where any real deterioration in the book would first surface (watching it also requires stripping out one-time items like the $134.3 million remeasurement gain that inflated the third quarter of 2025, a reminder that headline growth rates can flatter the run-rate).9 Third, the pace of share count reduction relative to the price paid — because the entire per-share compounding thesis lives or dies on management continuing to retire stock at sensible valuations rather than chasing growth or overpaying for its own shares near highs.

The deepest reflection the Globe Life story offers is about the gap between narrative and cash. For one violent day in April 2024, the market decided this company was a fraud and marked it down by more than half. The cash flows never got the memo. Premiums kept arriving, claims kept getting paid, bonds kept maturing and getting reinvested at higher yields, and fifteen months later two governments closed their files. It is the rare case study where a business was, quite literally, accused of being a lie and answered not with rhetoric but with an unbroken ledger. That is the bull case in a sentence — and the bear case is its shadow: a compounding machine this dependent on a high-pressure human sales funnel will always carry the risk that produced the crisis in the first place. The engine never missed a beat. The question a serious investor keeps asking is not whether it is durable — the last two years answered that — but whether the very source of its durability is also the fault line along which it could one day crack.

References

-

Globe Life (GL): Executives Disregarded Wide-Ranging "Insurance Fraud" While They Received Millions in Undisclosed Kick-Back Scheme — Fuzzy Panda Research, 2024-04-11 ↩↩↩↩

-

Why Globe Life Inc.'s (GL) Stock Is Down 53.14% — AAII, 2024-04-11 ↩↩

-

Globe Life – The Main Course — Viceroy Research, 2024-04-30 ↩

-

Globe Life Announces Conclusion of SEC Investigation — PR Newswire, 2025-07-24 ↩↩

-

Globe Life Announces Closing of Department of Justice Investigation — PR Newswire, 2025-07-28 ↩↩

-

Globe Life Inc. (GL) Stock Overview — StockAnalysis.com, 2026-07-10 ↩↩

-

Globe Life Inc. (NYSE: GL) Q1 2024 Earnings Call Transcript — Insider Monkey, 2024-04-23 ↩↩↩↩

-

Globe Life Inc. Issues Statement Refuting Short-Seller Allegations — Globe Life Newsroom, 2024-04-11 ↩

-

Globe Life Inc. Third Quarter 2025 Earnings Release (Form 8-K, Exhibit 99.1) — SEC EDGAR, 2025-10-22 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Globe Life Inc. Announces Leadership Changes (Form 8-K, Exhibit 99.1) — SEC EDGAR, 2022-10-26 ↩↩

-

Globe Life Inc. 2026 Proxy Statement (Form DEF 14A) — SEC EDGAR, 2026 ↩↩

-

American Income Life — Our History — American Income Life Insurance Company ↩↩↩↩↩

-

Torchmark Corporation Has Officially Been Renamed Globe Life Inc. — Globe Life Newsroom, 2019-08-08 ↩

-

Warren Buffett Reduced This Long-Time Berkshire Hathaway Holding — The Motley Fool, 2023-12-01 ↩↩↩↩

-

Globe Life Announces Plans to Relocate Corporate Headquarters Within McKinney, TX — Globe Life Newsroom, 2025-02 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube