Graham Holdings: The "Post-Post" Era and the Art of the Permanent Pivot

I. Introduction: The Identity Crisis that Worked

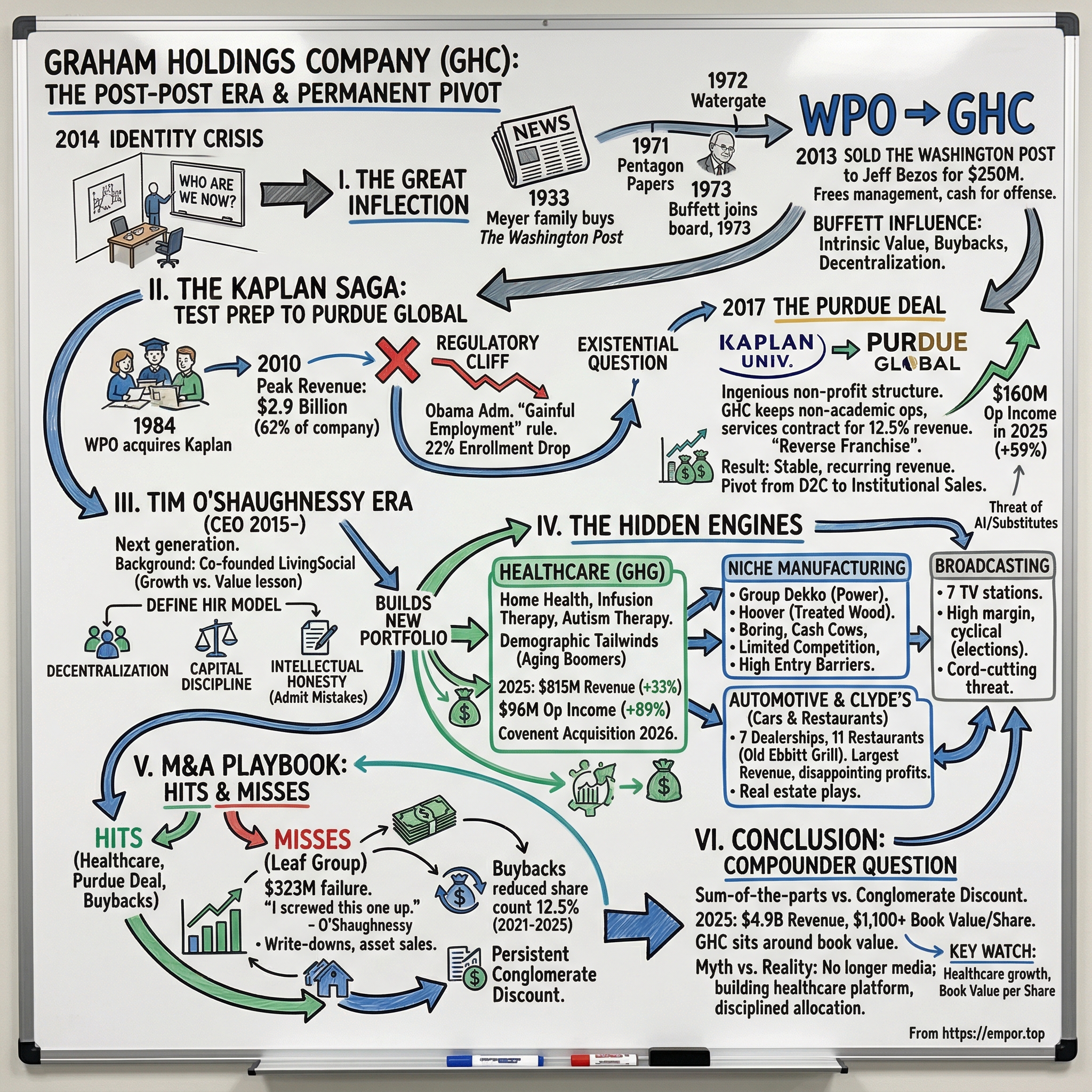

Picture Arlington, Virginia, early 2014. A modest corporate headquarters, nothing like the imposing newsroom that once hummed at 1150 15th Street NW in Washington, D.C. Inside, a small team of executives is staring at a whiteboard that captures, in dry-erase shorthand, the most existential question a company can face: Who are we now?

A few months earlier, the Graham family had done the unthinkable. They sold The Washington Post—the paper that brought down a president, the paper Katharine Graham steered through the Pentagon Papers, the paper that Warren Buffett once called the best-run media property in America—to Jeff Bezos for $250 million. The ticker had already changed from WPO to GHC. The nameplate read "Graham Holdings Company." But what, exactly, did it hold?

Here is what makes this story so compelling for students of capital allocation: what was left behind after the sale was not a carcass. It was a laboratory. A diversified collection of businesses spanning test preparation, television broadcasting, manufacturing, and a growing healthcare operation—plus a balance sheet steeped in the Buffett doctrine of intrinsic value, buybacks, and patient capital deployment.

The company that emerged from the ashes of the newspaper era was not a media company at all. It was a holding company, a capital allocation vehicle, a kind of "Mini-Berkshire" run by people who had spent decades absorbing lessons from the Oracle of Omaha himself.

The thesis of this deep dive is straightforward: Graham Holdings is one of the most misunderstood public companies in America. Wall Street classifies it under "Education & Training Services" because Kaplan, its education subsidiary, still accounts for over a third of revenue. But that label obscures the real story.

GHC is a permanent-capital vehicle that buys and operates businesses across wildly unrelated industries—from hospice care to car dealerships to high-end Washington brasseries—using the same disciplined framework that Buffett taught the Graham family over four decades of friendship.

To understand how GHC got here, we need to trace three arcs. First, the wrenching decision to sell the crown jewels and what it freed the company to become. Second, the saga of Kaplan—from cash cow to existential threat to reinvention. And third, the emergence of Timothy O'Shaughnessy, the son-in-law CEO who is quietly building one of the most interesting conglomerates in the public markets, one acquisition at a time.

The numbers tell part of the story: revenue has grown from $3.2 billion in 2021 to $4.9 billion in 2025. The share count has shrunk by over twelve percent through disciplined buybacks. Book value per share has climbed from roughly $880 to over $1,100 in the same period. The stock, trading around $1,066 as of this writing, hit an all-time high above $1,224 in January 2026.

But the real narrative is not in the numbers. It is in the philosophy—the idea that a company can shed its identity, embrace radical diversification, and compound value for decades, all while ignoring the market's obsession with narrative coherence.

Let us start at the moment everything changed.

II. The Great Inflection: Selling the Crown Jewels

To understand the weight of what happened in 2013, you have to understand the family that made the decision.

The Washington Post's connection to the Meyer-Graham dynasty begins in 1933, when financier Eugene Meyer purchased the bankrupt newspaper at auction for $825,000. Meyer poured money and ambition into the paper, transforming it from a second-tier broadsheet into a serious journalistic enterprise.

His daughter, Katharine Meyer, married Philip Leslie Graham in 1940, and Philip took over as publisher in 1946. Philip was brilliant, charismatic, and deeply troubled—he expanded the company aggressively, acquiring Newsweek and several television stations, but suffered from severe mental illness and took his own life in August 1963.

What happened next defined the company for half a century. Katharine Graham, who had never expected to run anything, stepped into the role of president. She was uncertain, self-deprecating, and terrified. She was also, as it turned out, extraordinary.

Under her leadership, the Post published the Pentagon Papers in 1971, defying a Nixon administration injunction. A year later, Bob Woodward and Carl Bernstein began their investigation of the Watergate break-in, a story that would topple a presidency and cement the Post's reputation as the most consequential newspaper in America.

The stock appreciated more than three thousand percent during Katharine Graham's tenure. She won a Pulitzer Prize for her memoir, Personal History, and became one of the most admired women in American business before her death in July 2001.

Her son, Donald Edward Graham, succeeded her and carried the family's stewardship forward for another decade. But by the time Don Graham found himself staring at that spreadsheet in 2013, the world had changed in ways his mother could never have imagined.

The story of the sale begins not with a bidding war or a hostile takeover, but with a spreadsheet that Donald Graham could not stop staring at.

By 2013, The Washington Post was hemorrhaging. It was not a slow bleed—it was arterial. The paper had endured seven consecutive years of significant revenue declines, and a preliminary budget for 2013 showed the possibility of $40 million in losses for the year.

Digital advertising was cannibalizing print at an accelerating pace, and the Post's attempts to build a sustainable online model had produced more frustration than revenue. Donald Graham, who had spent his entire adult life in the orbit of the newspaper—first as a police reporter, then as publisher, then as chairman—understood something that many legacy media owners refused to accept: the flywheel was broken.

The flywheel that had powered American newspapers for a century was elegant in its simplicity. Local monopoly on news created a captive audience, which attracted advertisers, which funded the newsroom, which produced the news that attracted the audience.

It was a virtuous circle that generated extraordinary economics—at their peak, major metro newspapers routinely earned operating margins of twenty-five to thirty-five percent. But the internet shattered every link in that chain simultaneously. Craigslist destroyed classified advertising. Google and Facebook siphoned off display ad dollars. And the audience, once captive, could now get news from a thousand sources for free.

Graham's genius—and it is worth calling it that, because selling a family heirloom requires a different kind of courage than buying one—was recognizing that the Post needed something the Graham family could not provide: a technology-first owner with a willingness to invest hundreds of millions of dollars in digital infrastructure without any expectation of near-term returns. That description fit exactly one person on Earth.

The introduction to Jeff Bezos came through Don Graham's friend, a Washington-based intermediary. The negotiations were swift and private. On August 5, 2013, the company announced that Bezos—personally, not through Amazon—would acquire The Washington Post and related publishing businesses for $250 million in cash.

In his statement, Graham said: "Jeff Bezos' proven technology and business genius, his long-term approach and his personal decency make him a uniquely good new owner for the Post." He added that the paper could have survived under the company's ownership, but "our aspirations for the Post were higher."

That framing matters. Graham did not describe the sale as a retreat. He described it as an act of stewardship—placing the paper with an owner who could fulfill its potential in ways the family no longer could.

The deal closed on October 1, 2013, and by late November the company had officially renamed itself Graham Holdings Company, shedding the "Washington Post" identity entirely. The ticker changed from WPO to GHC. An era was over.

What the sale accomplished, beyond the obvious $250 million in cash, was subtler and more profound. It freed the company from the gravitational pull of a declining asset.

For years, management attention, board discussions, and strategic bandwidth had been consumed by the question of how to save the newspaper. With that burden lifted, the company could redirect its energy toward offense rather than defense. The cash on the balance sheet could flow toward acquisitions. The management team could focus on growing the businesses that were actually growing.

But the cultural shift was perhaps the most important transformation. The Washington Post Company had been, above all else, a journalism company. Its identity was wrapped up in Watergate, in the Pentagon Papers, in Katharine Graham's extraordinary memoir Personal History.

The people who worked there—even in the non-newspaper divisions—carried a sense of mission that was rooted in the Fourth Estate. Graham Holdings had to become something different: a holding company, a capital allocator, an entity whose identity was defined not by what it did but by how well it deployed capital.

This is where Warren Buffett's influence becomes impossible to ignore.

Buffett had been buying Washington Post Company stock since 1973, when he invested $10.6 million during the post-Watergate selloff. The stock was cheap—the market was punishing the company for its role in challenging the Nixon administration—and Buffett saw a wide gap between price and intrinsic value.

He famously wrote to Katharine Graham offering assurance that he would never buy another share without her personal approval—a gesture of respect that cemented a friendship lasting decades. Buffett joined the board and became, in essence, the Graham family's tutor in capital allocation. As one biographer put it, "Graham became Buffett's entrée into high society, while Buffett became Graham's tutor in the ways of business."

That tutelage left a permanent imprint on the company's DNA. The emphasis on intrinsic value over market price. The willingness to buy back shares aggressively when they traded below book value. The preference for decentralized management of subsidiaries. The patience to hold businesses forever rather than flip them for short-term gains.

All of these Buffett principles became embedded in the Graham Holdings playbook—and they would prove essential in the decade to come.

In March 2014, Buffett himself made his exit through an elegantly structured transaction. He swapped most of Berkshire's 1.7 million GHC shares for the company's WPLG Miami television station (valued at roughly $364 million) plus cash and some Berkshire shares that Graham Holdings held.

His original $10.6 million investment had grown to approximately $1.1 billion over four decades—a more than hundredfold return, a staggering result by any measure. Buffett stepped down from the board around the same time, but his intellectual fingerprints remained on every strategic decision the company would make going forward.

The sale of the Post, in retrospect, was not the end of the Graham story. It was the beginning of a new chapter—one in which the family's capital allocation skills, not their journalistic legacy, would define the company's value. The question was whether those skills could produce results in businesses far removed from the newsroom.

The answer would start with the company's largest and most troubled division—one that had been quietly generating billions while the newspaper grabbed all the headlines.

III. The Kaplan Saga: From Test Prep to Purdue Global

In 1938, a young teacher named Stanley H. Kaplan started tutoring students in the basement of his parents' home in Brooklyn, New York. His specialty was standardized test preparation—helping anxious high schoolers crack the SAT, coaching aspiring lawyers through the LSAT, drilling medical school hopefuls on the MCAT. The business was built on a simple insight: standardized tests are learnable skills, not measures of innate intelligence. If you could systematize the preparation, you could charge for it.

The Washington Post Company acquired Kaplan in 1984 for approximately $45 million. At the time, it seemed like a modest bet on a niche business. But under Post Company ownership, Kaplan evolved from a test-prep tutoring service into something far more ambitious: a full-fledged education conglomerate spanning higher education, professional training, English-language programs, and international operations across dozens of countries.

By 2010, Kaplan had become the engine that powered the entire enterprise. That year, it generated approximately $2.9 billion in revenue—roughly sixty-two percent of the parent company's total revenue of $4.7 billion. Kaplan's higher-education division alone accounted for sixty-four percent of Kaplan's revenue.

Think about that for a moment. The company that Americans associated with The Washington Post—Watergate, the Pentagon Papers, serious investigative journalism—was actually, by the numbers, an education company that happened to own a famous newspaper. Kaplan was not just the largest division; it was the division that subsidized the newspaper's losses, allowing the Grahams to continue investing in journalism even as the economics deteriorated.

Then the regulatory cliff arrived.

In 2010, the Obama administration's Department of Education proposed what became known as the "gainful employment" rule. The concept was deceptively simple: for-profit colleges that received federal student loan money had to demonstrate that their graduates could actually repay those loans.

If they could not—if graduates were defaulting at high rates or earning too little to service their debt—the institution would lose access to federal financial aid. For most for-profit colleges, federal student aid was not just a significant revenue stream; it was the revenue stream. Lose it, and you lose the business.

The rule was aimed at an industry that had grown bloated on easy federal money. For-profit colleges had mastered the art of enrolling students who qualified for federal loans, collecting the tuition, and then delivering an education that, too often, failed to translate into employment. The default rates were alarming, and the political pressure to act was intense.

For Kaplan, the impact was devastating. Enrollment at Kaplan University, its flagship higher-education brand, dropped twenty-two percent in a single quarter. Programs at Kaplan College and Kaplan Career Institute failed the initial gainful employment test, meaning two-thirds of students in those programs were unable to repay their loans.

Revenue in the higher education division began a multiyear decline that would see education segment revenue fall from $2.9 billion at peak to $1.6 billion by 2016. In six years, Kaplan lost nearly half its revenue. The business that had once subsidized the Post's journalism was now the one in need of saving.

The existential question for Graham Holdings was whether Kaplan could be saved—and if so, in what form. The answer came in April 2017, when Purdue University President Mitch Daniels announced one of the most unusual deals in the history of American higher education.

The structure was ingenious—and counterintuitive.

Graham Holdings transferred Kaplan University to Purdue for the nominal price of one dollar. In fact, GHC did not just give the university away for free; it actually paid Purdue $20 million at closing, the first installment of guaranteed priority payments totaling $50 million over five years.

In exchange, Kaplan University became "Purdue University Global," a nonprofit institution operating under the Purdue University system—carrying the credibility and brand of one of America's most respected public research universities.

But here was the clever part: Kaplan retained all of the non-academic operations. The technology platforms, the marketing infrastructure, the back-office support systems—everything that was not directly related to curriculum and faculty—stayed with Kaplan under a long-term services agreement. Kaplan would receive 12.5 percent of Purdue Global's revenues going forward in exchange for providing these support services.

Think of it like a restaurant franchise in reverse. Instead of buying a brand name and running the restaurant yourself, Kaplan gave away the restaurant and kept the management contract. The academic content and faculty belong to Purdue. The pipes and plumbing—the technology, the student recruitment, the back-office machinery—belong to Kaplan.

The logic was a form of strategic judo. By converting Kaplan University from a for-profit institution into a nonprofit operating under the Purdue brand, the deal neutralized the regulatory risk that had been destroying value. Purdue Global was not subject to the same gainful employment scrutiny as for-profit colleges. Students got to earn a degree from Purdue—a name with genuine prestige—while Kaplan got a durable, recurring revenue stream tied to enrollment growth at an institution it no longer had to defend against political attack.

Critics were not kind. The Purdue Faculty Senate condemned the deal. Senators Dick Durbin and Sherrod Brown warned about risks, calling Kaplan's track record "shameful" and "predatory." The skeptics had a point: the deal effectively laundered a for-profit brand through a nonprofit institution. But from a pure business perspective, it was a masterstroke. It converted an asset that was declining in value under regulatory assault into a long-term service contract backed by one of the Big Ten's flagship universities.

The deal closed in March 2018, and the early returns have validated the strategy. Purdue Global grew its enrollment significantly under the Purdue brand, and Kaplan's 12.5 percent revenue share proved to be a stable, growing income stream. Meanwhile, Kaplan's other businesses—international pathways programs that help foreign students gain admission to English-speaking universities, professional training for accountants and financial services professionals, and the core test preparation business—continued to generate cash.

Today, Kaplan's education segment generates about $1.7 billion in annual revenue—stable, if not growing dramatically—and operating income surged fifty-nine percent in fiscal 2025 to $160 million, driven by improved profitability across Kaplan International Pathways and the Purdue Global services contract. Recent partnerships tell the story of Kaplan's evolving positioning: in early 2026 alone, Kaplan announced free test-prep partnerships with Alabama State University, the University of Dayton School of Law, Kentucky State University, Fort Valley State University, and the state of Illinois—which continued its first-in-the-nation program offering free Kaplan test prep to all residents. These partnerships represent Kaplan's pivot from a direct-to-consumer model to an institutional sales approach, where universities and government entities pay for bulk access. It is a less glamorous business than running a university, but it is also far less regulated and far more defensible.

The regulatory cloud that once threatened to destroy the business has largely dissipated, and Kaplan has successfully repositioned itself as a services and test-prep company rather than a degree-granting institution.

In strategic terms, the Purdue deal created meaningful switching costs. Purdue Global's operations are deeply intertwined with Kaplan's technology and support infrastructure. Ripping out Kaplan and replacing it with another service provider would be enormously disruptive—the kind of friction that makes long-term contracts sticky. Whether you call it switching costs in Hamilton Helmer's framework or supplier lock-in in Porter's, the result is the same: Kaplan carved out a defensible position in a market that nearly destroyed it.

There is an important caveat, however. The threat of substitutes in education has not gone away—it has intensified. AI-powered tutoring tools, free online courses from platforms like Coursera and Khan Academy, and the growing skepticism about the value of standardized tests themselves (many universities have moved to test-optional admissions) all represent headwinds for Kaplan's test-prep business. The company's pivot toward institutional partnerships—where universities and state governments pay for bulk access—is a smart response, because it shifts the customer from price-sensitive individuals to institutions with budgets. But the question of whether paid test preparation can sustain its value proposition in an era of abundant free alternatives is one that Kaplan will have to answer year after year.

The Kaplan story also reveals something important about GHC's organizational character: the willingness to make bold structural moves when incremental improvements are insufficient. Selling the Post, restructuring Kaplan into a services contract—these are not the actions of a company that tinkers at the margins. They are the actions of a company that thinks in terms of decades, not quarters. Andrew Rosen, who has led Kaplan through this transformation, remains the highest-compensated executive at Graham Holdings at $6.4 million—a testament to how central the education business remains to the company's economics, even as healthcare grows faster.

That long-term orientation found its ultimate expression in the man who would lead the company into its next era.

IV. Current Management: The O'Shaughnessy Era

Timothy O'Shaughnessy was not the obvious choice to run a company founded in the nineteenth century.

Born in 1981, the youngest of four children growing up in Minnesota, O'Shaughnessy earned his business degree from Georgetown University in 2004 and dove straight into the Washington tech scene. He joined AOL as a product manager, then moved to Revolution Health—the healthcare venture backed by AOL co-founder Steve Case—where he rose to vice president of product development. But it was his next move that made his name.

In 2007, at the age of twenty-six, O'Shaughnessy co-founded LivingSocial, a daily deals platform that rode the same wave as Groupon. The company grew at a ferocious pace, scaling sales to nearly $2 billion and reaching a private valuation north of $4 billion. O'Shaughnessy served as CEO and became one of the most prominent young tech entrepreneurs in Washington, D.C.

But LivingSocial's story did not end well. The daily deals model proved unsustainable—customer acquisition costs were too high, merchant retention was too low, and the competitive moat was essentially nonexistent. The company hemorrhaged cash, laid off thousands of employees, and was ultimately sold to Groupon in 2016 for a fraction of its peak valuation.

It was a humbling experience. But for O'Shaughnessy, the education was worth more than any MBA. He had built a company from zero to billions in revenue and watched it collapse—and he understood precisely why it happened.

The LivingSocial experience left O'Shaughnessy with two things that would prove invaluable at Graham Holdings: a deep understanding of digital business models and, more importantly, a healthy respect for the difference between growth and value creation. He had seen firsthand what happens when a company scales revenue without building durable competitive advantages. That lesson would inform every acquisition he made at GHC.

O'Shaughnessy's connection to the Graham family came through his marriage to Laura Graham O'Shaughnessy, Donald Graham's daughter. Laura herself was no bystander in the family business—she served as CEO of SocialCode, a social marketing technology company wholly owned by Graham Holdings.

When Tim was named president of GHC in October 2014, and then president and CEO in 2015, the transition from the Graham lineage to the next generation was complete—even if the CEO's last name was different.

The appointment raised the inevitable question: was this nepotism or meritocracy? The answer, as with most things at GHC, is nuanced. O'Shaughnessy had genuine entrepreneurial credentials and operational experience. But he also had the implicit trust of the Graham family, which—given the dual-class share structure—was the only constituency that truly mattered.

About that share structure: Graham Holdings has two classes of stock. Class A shares, which are not publicly traded, are held by descendants of Eugene Meyer—including Donald Graham, his sister Lally Weymouth, and various family trusts. Class A shareholders elect seventy percent of the board of directors.

Class B shares, which trade on the NYSE under the ticker GHC, are held by public investors and elect the remaining thirty percent of the board. This means the Graham family maintains effective control of the company regardless of what the public market thinks.

This structure is both GHC's greatest strength and its most persistent criticism.

On the strength side, it insulates management from the short-term pressures that plague most public companies. O'Shaughnessy does not have to worry about activist investors demanding a breakup, or quarterly earnings guidance, or the whims of momentum traders. He can allocate capital with a multi-decade time horizon, making bets that might take five or ten years to pay off.

On the criticism side, the structure means that public shareholders are essentially along for the ride. If O'Shaughnessy turns out to be a mediocre allocator, there is no mechanism for the market to force a change. There is no activist campaign that can succeed. There is no hostile takeover that can be launched. The Graham family's control is absolute.

O'Shaughnessy's compensation reflects the long-term orientation. His total pay in the most recent fiscal year was approximately $3.9 million—modest by public-company CEO standards, especially for a company with nearly $5 billion in revenue. For comparison, the CEO of AutoNation, which has similar revenue, earns multiples of that figure.

The compensation structure emphasizes long-term return on invested capital rather than quarterly earnings beats. Interestingly, the highest-paid executives at GHC are not O'Shaughnessy but Andrew Rosen and Jacob Maas, each earning roughly $6.4 million. Rosen runs Kaplan, and Maas oversees other key operations—a signal that GHC pays for operational execution, not just the corner office.

O'Shaughnessy's management philosophy can be summarized in three principles. First, decentralization: subsidiary CEOs run their businesses with significant autonomy, reporting to Arlington but making day-to-day decisions independently. This is not lip service—GHC's corporate headquarters staff is remarkably small for a company approaching $5 billion in revenue. The CFO, Wallace Cooney, and general counsel, Nicole Maddrey, run lean operations that focus on financial reporting, capital allocation, and governance rather than operational micromanagement. Second, capital discipline: every acquisition must clear a hurdle rate tied to long-term ROIC, not revenue growth or strategic synergy narratives. O'Shaughnessy has described years where GHC found no acquisitions worth making—2024, for instance, was described internally as "quite an unusual year" with "no meaningful acquisitions." The willingness to sit on cash rather than deploy it into mediocre opportunities is perhaps the hardest discipline for any capital allocator, and O'Shaughnessy has demonstrated it. Third, intellectual honesty: when a bet fails, say so publicly and move on. This last principle was tested in spectacular fashion with the Leaf Group acquisition, which we will examine later—and O'Shaughnessy's response to that failure tells you more about his character than any success could.

The O'Shaughnessy era has coincided with a dramatic expansion of GHC's business portfolio. Under his leadership, the company has entered healthcare, automotive retail, manufacturing, and direct-to-consumer brands. Revenue has grown from around $3.2 billion to nearly $5 billion. The share count has declined from roughly five million to 4.3 million through disciplined buybacks. And book value per share has climbed steadily, from under $900 to over $1,100.

But the real test of any capital allocator is not the aggregate numbers—it is the individual decisions. And GHC's acquisition spree over the past decade includes both home runs and strikeouts. To understand the range, you have to look at the individual businesses O'Shaughnessy has built or bought—starting with the ones that rarely make headlines but quietly generate the cash that funds everything else.

V. The "Hidden" Engines: Healthcare, Manufacturing, and Cars

Walk into the headquarters of Graham Healthcare Group in any given week, and you will find a war room focused on one of the most powerful demographic tailwinds in American business: the aging of the Baby Boom generation.

Graham Healthcare Group, or GHG, is the quiet giant within the GHC portfolio. It operates primarily through three platforms.

First, Residential Home Health, which provides in-home nursing, therapy, and aide services to patients recovering from surgery, managing chronic conditions, or transitioning out of hospital care.

Second, CSI, which specializes in home infusion therapy—administering intravenous medications, nutrition, and other treatments in patients' homes rather than in hospitals. If someone needs IV antibiotics for a serious infection, or chemotherapy delivered through a portable pump, or nutritional support through a feeding tube, CSI brings the pharmacy to the patient's living room.

Third, Surpass Behavioral Health, focusing on autism and behavioral therapy services for children—a growing market as diagnosis rates increase and insurers expand coverage.

The numbers tell the story of a business hitting its stride. In fiscal 2025, the healthcare segment generated $815 million in revenue—up thirty-three percent from the prior year—and $96 million in operating income, an increase of eighty-nine percent.

That operating income nearly doubling is remarkable for any business, let alone one operating in the heavily regulated healthcare space. The growth is being driven by a combination of organic expansion and tuck-in acquisitions, with the company targeting the low-to-mid-teens for organic growth rates supplemented by bolt-on deals at seven to nine times EBITDA.

The strategic logic is straightforward. America's population aged sixty-five and over is projected to grow from roughly fifty-eight million today to over eighty million by 2040. That is a forty percent increase in the core customer base over the next fifteen years—a demographic wave that no competitor can outrun and no disruptor can stop.

These aging Americans overwhelmingly prefer to receive care at home rather than in institutional settings—and the economics favor it, too, since home health costs a fraction of hospital or skilled nursing facility care. Meanwhile, advances in medical technology are making it possible to deliver increasingly complex treatments in the home.

GHG is positioning itself at the intersection of these trends. Its most recent acquisition, Covenant Home Health in Eastern Pennsylvania (announced in March 2026), is typical of the strategy: a regional home health provider with established referral relationships and a loyal patient base, purchased at a reasonable multiple and integrated into GHG's existing infrastructure. It is not glamorous, but it compounds.

The infusion therapy business through CSI deserves particular attention. Home infusion is one of the fastest-growing segments in healthcare services, driven by the same forces pushing patients out of hospitals: cost pressure from insurers, patient preference, and technological capability. CSI has been the primary growth engine within GHG, and its expansion explains much of the segment's impressive revenue trajectory.

To put the home health opportunity in context, consider the economics. A day of care in a hospital costs, on average, several thousand dollars. A day in a skilled nursing facility costs several hundred. A day of home health care costs a fraction of either. As Medicare and private insurers push to reduce costs, every patient who can be treated safely at home represents savings for the system—and revenue for companies like GHG that deliver that care. The Centers for Medicare and Medicaid Services have expanded home health reimbursement categories in recent years, creating additional tailwinds for providers.

GHG's strategy is to build regional density—acquiring enough providers in a geographic area to achieve referral network effects, where hospitals and physicians in that region default to GHG for home health and hospice referrals. The March 2026 acquisition of Covenant Home Health in Eastern Pennsylvania is a textbook example: it fills a geographic gap, adds referral relationships, and layers onto existing operational infrastructure with minimal incremental overhead.

For investors, healthcare is arguably the most important segment to watch at GHC. It has the strongest secular tailwinds, the highest growth rates, and the potential to become the company's largest profit contributor within a few years. If GHG can sustain anything close to its current growth trajectory, it alone could justify a significant portion of GHC's current market capitalization.

The manufacturing segment is a different animal entirely—less flashy but equally instructive about GHC's acquisition philosophy.

Group Dekko, acquired in November 2015, is based in Garrett, Indiana—about as far from the Georgetown cocktail circuit as you can get. Dekko manufactures power, charging, and data connectivity systems for commercial interiors, as well as industrial and commercial lighting solutions and electrical components for medical equipment and transportation. If you have ever sat at a conference table with a built-in power outlet, there is a decent chance Dekko made it.

Hoover Treated Wood Products, acquired in 2017, is even more niche. Hoover is a supplier of pressure-impregnated kiln-dried lumber and plywood for fire retardant and preservative applications. It operates nine facilities across the United States, serving the construction industry with a product that is mandated by building codes in many applications. When you walk into a commercial building and the interior framing does not catch fire, you can thank companies like Hoover.

The portfolio also includes Joyce/Dayton, which makes screw jacks, linear actuators, and lifting systems for industrial applications, and Forney, which produces burners, igniters, dampers, and controls for power plants and industrial boilers.

Why would a former newspaper company buy a wood-treatment business? The answer lies in the economics. These are niche manufacturing businesses with limited competition, high barriers to entry (regulatory approvals, specialized equipment, long-standing customer relationships), and steady cash generation. They will never grow at thirty percent a year, but they will reliably produce mid-single-digit returns on capital with minimal reinvestment requirements. In the language of capital allocation, they are "cash cows"—businesses that throw off free cash flow that can be redeployed into higher-growth opportunities like healthcare.

The manufacturing segment generated $436 million in revenue in fiscal 2025 and $18.6 million in operating income. The margins are thin by GHC standards, but the capital intensity is low and the competitive positions are durable. It is precisely the kind of boring, defensible business that Buffett would recognize—and it serves an important role in the portfolio by generating steady cash that can be redeployed into higher-growth opportunities.

What makes the manufacturing segment strategically interesting is the concept of niche dominance. In treated wood products, for example, the number of competitors with the regulatory approvals, specialized pressure-treatment equipment, and distribution networks to serve commercial construction is small. Customers do not switch suppliers over a few percentage points in price because the cost of a product failure—literally, a building that does not meet fire code—is catastrophic. This dynamic creates a moat that is invisible to most investors but highly durable. The same logic applies to Dekko's commercial connectivity products and Forney's industrial burner controls. These are not sexy businesses, but they are businesses where the incumbent advantage compounds over time.

Then there are the cars.

Graham Holdings entered the automotive retail business in January 2019 by acquiring a ninety-percent stake in two dealerships from Sonic Automotive. The company has since expanded to seven dealerships in the Washington, D.C., and Richmond, Virginia, markets, operating under the Ourisman brand.

The portfolio includes Lexus of Rockville, Ourisman Honda of Tysons Corner, Ourisman Jeep of Bethesda, Ourisman Ford of Manassas, two Ourisman dealerships in Woodbridge (Toyota and Chrysler/Dodge/Jeep/Ram), and Toyota of Richmond.

The automotive segment is the largest by revenue at $1.1 billion in fiscal 2025, but the profitability has been disappointing—operating income of just $17.4 million, down fifty-four percent from the prior year. That is an operating margin of roughly one and a half percent, which is thin even by auto retail standards.

The auto retail business is inherently low-margin and cyclical, sensitive to interest rates, consumer confidence, and manufacturer incentive programs. Fiscal 2025 was a tough year for dealerships across the industry, with higher borrowing costs dampening consumer demand and compressed new-vehicle margins as inventory levels normalized after the pandemic-era shortage.

The question for investors is whether GHC's decentralized management model can extract better economics from car dealerships than the national chains. The theory is that locally empowered dealer principals, operating with the backing of a patient parent company, can build stronger customer relationships and community ties than a centrally managed operation focused on quarterly same-store sales metrics.

The evidence so far is mixed—the returns have not been spectacular—but the long-term thesis is built on the assumption that automotive retail rewards local execution and brand loyalty. It is worth noting that the best-performing auto dealer groups in America, like the Larry H. Miller organization, have historically been locally focused operations with deep community ties—not centrally managed national chains.

Finally, there is Clyde's. In July 2019, GHC acquired the Clyde's Restaurant Group, which owns and operates eleven restaurants and entertainment venues in the Washington, D.C., metropolitan area.

The crown jewel is the Old Ebbitt Grill, located steps from the White House, which is consistently one of the highest-grossing independent restaurants in America. On any given evening, the bar at the Old Ebbitt is packed with senators, lobbyists, journalists, and tourists who have been coming since the restaurant opened in 1856.

The acquisition raised eyebrows—was this "lifestyle investing" by a company whose chairman lives in Washington, or was it a savvy bet on prime real estate and premium cash flows?

The answer is probably a bit of both, but the financial logic is sounder than skeptics assumed. The Old Ebbitt Grill and its sister restaurants occupy prime real estate in a city where restaurant demand is underpinned by a permanent class of government officials, lobbyists, journalists, and tourists. The properties generate strong cash flow, and the real estate itself appreciates over time.

For a patient owner with no need to flip the asset, it is the kind of business that compounds quietly in the background. Washington, D.C., is not going to stop being the capital of the United States, and people in power are not going to stop eating lunch.

What ties all of these "hidden engines" together is the GHC acquisition philosophy: find businesses with defensible competitive positions, buy them at reasonable prices, install or retain excellent operators, and hold them forever. The businesses do not need to be related to each other—in fact, the lack of correlation is a feature, not a bug, because it diversifies the overall portfolio's cash flows across economic cycles.

There is also a broadcasting segment that deserves mention. Graham Media Group owns seven local television stations in top-70 markets: KPRC in Houston (NBC), WDIV in Detroit (NBC), KSAT in San Antonio (ABC), WKMG in Orlando (CBS), WSLS in Roanoke (NBC), and two stations in Jacksonville—WJXT (an independent local station) and WCWJ (CW affiliate). In fiscal 2025, broadcasting generated $425 million in revenue and $112 million in operating income—making it the most profitable segment on a margin basis. However, those numbers were down sharply from 2024, which benefited from a presidential election year that flooded local TV stations with political advertising. The cyclical nature of political ad spending creates a sawtooth revenue pattern: strong in even-numbered years, weak in odd-numbered ones.

The long-term challenge for local television is existential. Cord-cutting continues to erode the traditional pay-TV bundle, and younger demographics increasingly consume video content through streaming platforms and social media. Local news remains one of the last bastions of appointment television, but even that audience is aging. GHC's TV stations are well-run and profitable today, but the question of whether to hold them indefinitely or sell at a premium to a consolidator is one that management will eventually have to confront.

The results across all these "hidden" segments paint a portrait of uneven but genuine value creation, with healthcare emerging as the clear standout performer and automotive struggling to pull its weight. The next question is whether GHC's M&A track record can sustain investor confidence when the hits and misses are tallied up.

VI. M&A Playbook: Benchmarking the Bets

Every capital allocator makes mistakes. What separates the great ones from the mediocre is not the absence of errors but the willingness to acknowledge them—and the ratio of hits to misses over a full cycle.

Timothy O'Shaughnessy's most visible mistake has a name: Leaf Group.

In April 2021, Graham Holdings announced the acquisition of Leaf Group, a digital media and marketplace company, for $323 million in an all-cash deal at $8.50 per share. Leaf Group's portfolio included Well+Good (a wellness media brand), Livestrong.com (a health and fitness platform), Hunker (home design), Society6 (artist-designed products), Saatchi Art (an online art gallery), and OnlyInYourState (a network of local interest sites). The thesis was "content-commerce"—the idea that media brands with loyal audiences could monetize those audiences through direct product sales, not just advertising.

The thesis was wrong. And the reasons why it was wrong are instructive for anyone thinking about the economics of digital media.

Content-commerce sounds appealing in a pitch deck, but the execution proved brutally difficult. The media brands struggled to drive meaningful e-commerce conversion. Society6 and Saatchi Art faced withering competition from platforms like Etsy and Redbubble that had network effects Leaf Group could not match. The advertising-dependent media properties suffered as Google's algorithm changes and social media platform shifts eroded traffic. Revenue declined, losses mounted, and the $323 million price tag began to look increasingly difficult to justify.

To his credit, O'Shaughnessy did not dress up the failure. In what has become one of the more refreshing moments of corporate candor in recent memory, he told investors plainly: "Leaf has underperformed our expectations and we overpaid." And then, even more bluntly: "I screwed this one up."

The unwinding was methodical but painful. In 2023, the media arm was rebranded as World of Good Brands and restructured. In late 2023, Hunker's staff was laid off and the property was sold to Static Media. By 2025, Well+Good and Livestrong were sold to Ziff Davis, OnlyInYourState went to Launch Potato, and World of Good Brands was effectively shuttered. The vast majority of the $323 million investment was written down.

The Leaf Group saga carries a broader lesson about the economics of digital media. In the 2010s, a popular investment thesis held that media brands with loyal audiences could become e-commerce platforms—that the trust and engagement built through content could be monetized through product sales. Companies like BuzzFeed, Vice, and Leaf Group raised hundreds of millions of dollars on this thesis. Almost none of them made it work. The reason is that content and commerce require fundamentally different capabilities. Creating engaging articles and videos is a creative endeavor that attracts editorial talent. Running an e-commerce operation—managing inventory, logistics, customer service, returns—is an operational endeavor that requires supply chain expertise. The companies that succeed at both (Amazon, for instance) build the commerce engine first and layer content on top. The companies that start with content and try to bolt on commerce almost always fail, because the margins on content are too thin to fund the infrastructure required for competitive e-commerce.

O'Shaughnessy learned this lesson at a cost of $323 million. The question is whether the intellectual honesty he demonstrated in acknowledging the failure will translate into better deal selection going forward—or whether the same instinct that led him to Leaf Group (the desire to find high-growth digital businesses to complement GHC's slower-growing legacy portfolio) will lead to similar mistakes in the future.

Set against the Leaf Group failure, the Framebridge acquisition tells a more ambiguous story. Framebridge, a direct-to-consumer custom framing company, was acquired to give GHC exposure to "digitally native" brands—companies that build their customer relationships online and fulfill through proprietary supply chains. Custom framing is a surprisingly large market with terrible incumbent economics (long lead times, inconsistent quality, opaque pricing at traditional frame shops). Framebridge's pitch was that it could use technology to streamline the process: customers upload a photo or ship an item, choose a frame online, and receive the finished product in days. The business is still small relative to GHC's overall portfolio, and its impact on consolidated results has been minimal. The jury remains out on whether it can scale into something meaningful.

Beyond individual deals, GHC's broader capital deployment strategy warrants examination. The company operates in a sweet spot of the M&A market—too small to compete with private equity megafunds for billion-dollar deals, but large enough to acquire businesses in the $25 million to $300 million range that are beneath the radar of most institutional buyers. This is the same territory where Constellation Software, the Canadian serial acquirer of vertical market software companies, has built extraordinary returns. The difference is that Constellation has a focused playbook (software only, never sell), while GHC is industry-agnostic.

The comparison to Constellation Software is instructive. Constellation has compounded at over thirty percent annually for two decades by buying small software companies at modest multiples and improving their operations incrementally. Its discipline is legendary—it turns down the vast majority of deals it evaluates and pays strict attention to return on invested capital. GHC shares the philosophy but not the focus. Its willingness to buy across unrelated industries (education, healthcare, manufacturing, restaurants, auto dealerships) creates a more diversified portfolio but also makes it harder for the market to value—hence the persistent "conglomerate discount."

The comparison to Berkshire Hathaway is even more apt, and not just because of the Buffett connection. Like Berkshire, GHC uses the float and cash flow from its existing businesses to fund acquisitions. Like Berkshire, it emphasizes decentralized management and long holding periods. And like Berkshire, it uses share repurchases as a capital allocation tool when the stock trades below intrinsic value. Between 2021 and 2025, GHC reduced its share count from roughly five million to 4.3 million shares—a twelve-and-a-half percent reduction that directly increased per-share value for remaining shareholders. In September 2024, the board authorized the repurchase of up to 500,000 additional Class B shares, representing nearly fifteen percent of the outstanding count.

The buyback strategy is particularly important at GHC because of the conglomerate discount. If the market stubbornly values the company at less than the sum of its parts—and it consistently has—then buying back shares at a discount to intrinsic value is the highest-return use of capital available. It is the algebraic equivalent of buying your own businesses at a below-market price. O'Shaughnessy understands this, and the steady reduction in share count is one of the most reliable indicators of capital allocation discipline at the company.

There is another dimension to GHC's capital deployment that is easy to overlook: the company's investment portfolio. Graham Holdings holds a significant portfolio of marketable securities and other investments, and the mark-to-market fluctuations in this portfolio can dramatically distort reported earnings. In fiscal 2024, large investment gains inflated net income to $725 million—a number that looked spectacular on the surface but overstated the underlying operating performance. Fiscal 2025's net income of $292 million was more representative. Investors who focus on reported EPS without adjusting for investment gains and losses will misread GHC's financial trajectory. The company reports adjusted net income (which strips out these fluctuations) of $227 million for fiscal 2025, compared to $282 million the prior year—a more modest but more honest picture.

The overall capital deployment track record, when tallied up, shows a company that has been more right than wrong. Healthcare has been a clear home run. The Kaplan restructuring through Purdue Global was creative and value-preserving. Manufacturing and broadcasting provide steady cash flows. The automotive entry has been underwhelming but not catastrophic. Leaf Group was a genuine mistake, openly acknowledged and wound down. And the relentless share buyback program has compounded per-share value regardless of what any individual acquisition did.

The question, as always with conglomerates, is whether the market will ever give GHC credit for the sum of these parts—or whether the "conglomerate discount" is simply the price of doing business as a diversified holding company.

VII. The Framework Analysis: 7 Powers and 5 Forces

To understand GHC's competitive position, it helps to apply two of the most widely used strategic frameworks: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces. The exercise reveals a company with pockets of real strategic strength—but also significant vulnerabilities.

Starting with Helmer's framework, the most relevant power at GHC is switching costs, concentrated in the Kaplan-Purdue Global relationship.

Purdue University Global's entire non-academic infrastructure—technology platforms, student services, marketing, enrollment management—is provided by Kaplan under a long-term services agreement. Replacing Kaplan would require Purdue to rebuild these systems from scratch, a process that would take years, cost tens of millions of dollars, and disrupt the experience of thousands of enrolled students.

This is textbook switching cost power: the deeper the integration, the more painful the divorce. And every year the relationship continues, the integration deepens further.

The second relevant power is what might be called the "Cornered Resource"—though in GHC's case, the resource is not a patent or a technology but a reputation.

Graham Holdings has cultivated an identity as a "permanent capital" buyer, a company that acquires businesses and holds them indefinitely. For founders of family-owned businesses looking to sell—people who care about legacy, employee welfare, and the continuation of what they built—GHC offers something that private equity cannot: the promise of forever.

This is the same "Buffett Power" that Berkshire Hathaway wields when it acquires companies like See's Candies or GEICO. The Graham name, the Buffett association, and the decades-long track record of holding acquisitions create a sourcing advantage in a market where many sellers choose their buyer based on cultural fit, not just price.

Counter-positioning applies to the Kaplan-Purdue deal specifically. By converting a for-profit university into a services contract for a nonprofit institution, GHC adopted a business model that incumbent for-profit education companies could not easily replicate.

The deal required a willing nonprofit partner with a strong brand—a combination that is difficult to find and even harder to negotiate. Competitors in the for-profit education space were stuck defending their existing models against regulatory attack while Kaplan pivoted to a structurally different arrangement.

On the Porter's 5 Forces side, the picture is mixed:

Threat of substitutes is the most significant force acting on GHC. In education, the threat is massive. Free online learning platforms—Coursera, edX, Khan Academy, YouTube—offer alternatives to paid test preparation and professional training.

The rise of AI-powered tutoring tools threatens to disrupt Kaplan's core test-prep business by offering personalized instruction at a fraction of the cost. In broadcasting, cord-cutting and streaming continue to erode the economics of local television. These substitution threats are not hypothetical; they are actively compressing margins in GHC's legacy businesses.

Bargaining power of buyers varies dramatically across segments. In niche manufacturing—Hoover Treated Wood, Dekko's commercial connectivity products—buyers have limited alternatives and switching costs are meaningful, giving GHC pricing power.

In automotive retail, the dynamic is reversed: consumers can easily compare prices across dealerships, manufacturers set the terms of franchise agreements, and the internet has made the car-buying process more transparent (and more competitive) than ever.

In healthcare, the buyers are primarily insurance companies and government programs (Medicare, Medicaid), which have enormous bargaining power but also create predictable reimbursement frameworks that GHG can plan around.

Bargaining power of suppliers is generally manageable across GHC's portfolio, with one notable exception: in television broadcasting, GHC depends on network affiliations (NBC, ABC, CBS) for programming content. The networks have significant leverage in negotiating affiliation agreements, and the loss of a major network affiliation would be devastating to any individual station.

Threat of new entrants is low in most of GHC's segments. Building a television station requires an FCC license. Entering the home health market requires state licensure, Medicare certification, and established referral networks. Manufacturing treated wood products requires specialized equipment and regulatory approvals. These barriers protect GHC's existing positions, even if they also limit growth opportunities.

Competitive rivalry is intense in education and automotive retail but moderate in healthcare and manufacturing.

The education market is fragmented and price-competitive, with new entrants (including AI-powered platforms) constantly emerging. The auto retail market is dominated by large public chains like AutoNation, Lithia, and Penske, which have scale advantages in procurement and marketing.

Healthcare, by contrast, is characterized by local competition among smaller providers—an environment that favors the kind of tuck-in acquisition strategy GHG is executing. Home health is a fragmented industry where the top ten players still control a minority of the market—leaving enormous runway for consolidation.

The framework analysis points to a clear strategic priority: GHC should continue shifting capital toward healthcare and niche manufacturing—businesses with structural competitive advantages—and away from segments where substitution threats and buyer power erode returns. The company's recent track record suggests management understands this, even if the portfolio's current composition still reflects the legacy of historical decisions.

One additional lens worth applying is the concept of process power—the idea that a company's organizational routines and culture can themselves be a source of competitive advantage. GHC's decentralized management model, its long-term compensation structures, and its willingness to hold businesses forever create an organizational culture that attracts a certain type of operator and a certain type of seller. This culture is difficult to replicate because it requires decades of consistent behavior to build credibility. A private equity fund cannot credibly promise to hold a business forever, no matter what it says in the letter of intent. GHC can, because it has done so for forty years.

The competitive landscape for GHC's acquisition strategy includes not just other conglomerates but also private equity funds, family offices, and strategic buyers in each specific industry. In healthcare, GHG competes for acquisitions against large home health companies like Amedisys and LHC Group (now merged), as well as PE-backed platforms. In manufacturing, the competitors are industrial conglomerates and PE funds specializing in industrial services. In education, Kaplan competes against Pearson, ETS, and a growing universe of EdTech startups. The breadth of GHC's portfolio means it faces different competitive dynamics in every segment—but the common thread is the permanent-capital advantage, which gives it an edge in sourcing deals from founders who prioritize legacy over price.

VIII. Playbook and Business Lessons

The Graham Holdings story offers several lessons that extend well beyond the specifics of any single industry.

The first and most fundamental lesson is what might be called the "Post-Post" principle: you do not have to die with your industry. When Donald Graham sold The Washington Post, the easy narrative was that the family had given up—that the digital revolution had claimed another victim. But the sale was not a surrender. It was a strategic pivot that liberated the company from a declining asset and freed management to redeploy capital into growing businesses. The discipline required to sell a family's most prized possession—a newspaper that had defined the family's identity for eighty years—should not be underestimated. Most families, and most corporate boards, cannot bring themselves to make that decision until it is too late.

The lesson for investors and operators is that identity is the enemy of adaptation. Companies that define themselves by what they do ("we are a newspaper company") rather than how they do it ("we are excellent capital allocators") get trapped by their own narratives. GHC's willingness to discard its identity and adopt a new one—however awkward the transition—is the reason the company exists in its current form.

The second lesson is the power of decentralization. Graham Holdings operates over fifteen thousand employees across businesses spanning education, healthcare, television, manufacturing, automotive retail, restaurants, and digital media. Its corporate headquarters in Arlington is deliberately small. Subsidiary CEOs run their businesses with significant autonomy, making operational decisions locally while reporting to Arlington on capital allocation and strategic direction.

This model is not new—Berkshire Hathaway pioneered it, and companies like Danaher and Constellation Software have refined it. But GHC's version is instructive because it operates across such disparate industries. The skills required to run a home health agency are completely different from those needed to manage a car dealership or a wood-treatment plant. By decentralizing, GHC avoids the trap of trying to impose a single operational template across unrelated businesses. Instead, it lets domain experts run each unit while maintaining discipline at the holding-company level on capital deployment, incentive structures, and performance measurement.

The third lesson is the importance of "no-exit" capital. In a world dominated by private equity—where the standard playbook is buy, optimize, and sell within three to seven years—GHC offers sellers something different: a permanent home. This matters because many founders care about what happens to their businesses after the sale. They care about their employees, their communities, their brand legacies. Private equity buyers, by definition, are temporary owners. GHC is not.

This "permanent capital" positioning creates a real sourcing advantage in the M&A market. Founders who might command a higher price from a PE fund will sometimes accept a lower offer from a buyer who promises to hold the business forever. The Graham name, the Buffett association, and the decades-long track record of never selling an acquired business (with the notable exception of divesting the failed Leaf Group properties) give GHC credibility in making that promise.

Consider the perspective of a founder who has spent thirty years building a niche manufacturing company. Two buyers approach: a private equity fund offering a higher price but planning to lever up the business, cut costs, and flip it in five years; and Graham Holdings offering a slightly lower price but promising to keep the management team, maintain the culture, and hold the business indefinitely. For a founder who cares about employees and legacy—and many do—the GHC offer is more attractive even at a lower headline price. This dynamic is particularly powerful in the mid-market, where businesses are often deeply personal to their owners and the emotional component of a sale is at least as important as the financial one.

The fourth lesson is about intellectual honesty in capital allocation. O'Shaughnessy's public admission that he "screwed up" the Leaf Group acquisition stands out in a corporate landscape where executives routinely blame external factors for their mistakes. That willingness to own failure—and to unwind the position methodically rather than throwing good money after bad—is a sign of capital allocation maturity. The best allocators are not the ones who never make mistakes; they are the ones who recognize mistakes quickly, admit them publicly, and redirect capital toward better opportunities.

There is a fifth lesson embedded in GHC's story that is often overlooked: the value of boring businesses. In an era when investors chase artificial intelligence, cryptocurrency, and software-as-a-service, GHC has built significant value by owning treated wood products, screw jacks, car dealerships, and home health agencies. These are not businesses that generate breathless CNBC segments or viral Twitter threads. But they are businesses that generate cash, serve real customers, and compound quietly over decades. The glamour gap between what the market wants to talk about and what actually creates long-term shareholder value is one of the most persistent inefficiencies in investing—and GHC exploits it deliberately.

For investors monitoring GHC going forward, the key performance indicators are few but telling. The first is healthcare segment revenue growth and operating margin expansion—this is the business with the strongest tailwinds and the highest potential to reshape GHC's earnings profile. If healthcare can sustain mid-teens organic growth supplemented by disciplined acquisitions, it could become the company's largest and most profitable segment within a few years. The second is book value per share growth, which captures the net effect of all capital allocation decisions—acquisitions, divestitures, buybacks, and organic earnings—in a single number that is harder to manipulate than GAAP earnings.

IX. Conclusion: Bull Case, Bear Case, and the Compounder Question

The bull case for Graham Holdings is rooted in the sum-of-the-parts math. Take each segment—broadcasting, healthcare, education, manufacturing, automotive—value it at a reasonable multiple of its earnings or cash flow, add the cash on the balance sheet and the investment portfolio, subtract the debt, and you arrive at a number that many analysts estimate is thirty to fifty percent higher than the current market capitalization of roughly $4.6 billion.

A recent Seeking Alpha analysis described GHC as "deeply undervalued," pointing to a strong net cash position and the healthcare and education segments as underappreciated growth drivers.

The bull case also rests on the quality of management. O'Shaughnessy has demonstrated both the willingness to make bold moves (entering healthcare, restructuring Kaplan) and the humility to admit mistakes (Leaf Group).

The dual-class share structure, while controversial, insulates him from the short-term pressures that force many public-company CEOs into suboptimal decisions. And the pipeline of potential acquisitions in the $25 million to $300 million range remains robust—GHC's reputation as a permanent-capital buyer continues to attract sellers who might otherwise go to private equity.

The bear case is equally straightforward: the conglomerate discount may be permanent.

Wall Street has never known what to do with companies that resist easy categorization, and GHC—classified as an education company despite earning substantial revenue from hospitals, car lots, and treated lumber—is about as hard to categorize as they come. Institutional investors who want healthcare exposure buy healthcare companies. Those who want education exposure buy education companies. Nobody wakes up wanting exposure to a company that does all of these things at once.

The bear case also points to the "new" bets. Leaf Group was a $323 million write-off. Framebridge remains small. The automotive segment's profitability has been underwhelming.

If the newer investments consistently underperform, the narrative shifts from "patient capital allocator" to "undisciplined acquirer buying whatever catches the CEO's eye." The distinction between the two is thin and often visible only in hindsight.

There is a regulatory overhang worth noting as well. Kaplan's education businesses remain subject to evolving federal and state regulations around student lending, gainful employment standards, and accreditation requirements.

The Purdue Global deal mitigated much of this risk, but it did not eliminate it entirely. Changes in the political environment could reignite regulatory pressure on for-profit education models, including the services contracts that Kaplan depends on. Any investor in GHC needs to monitor education policy as a first-order risk factor.

In broadcasting, the secular decline of linear television continues unabated. GHC's seven local TV stations had a strong 2024 (boosted by election-year political advertising), but revenue dropped twenty-one percent in fiscal 2025 as the political cycle faded.

The long-term trend in local television is not GHC's friend, and the segment's future depends on whether management can extract premium prices if and when it decides to sell—or whether the stations slowly lose relevance in a streaming-first world.

On the accounting front, investors should note that GHC's reported net income is heavily influenced by mark-to-market gains and losses on its investment portfolio, including a significant position in marketable securities.

Fiscal 2024's reported net income of $725 million was inflated by large investment gains, while fiscal 2025's $292 million was a more representative figure. Adjusted operating results, which strip out investment volatility, provide a cleaner picture of underlying business performance. The adjusted net income for fiscal 2025 was approximately $227 million—a number that better reflects what the operating businesses actually earn.

The question that hangs over Graham Holdings is ultimately the same question that applies to every conglomerate: is the whole worth more than the sum of its parts, or less? At Berkshire Hathaway, the answer has been resoundingly "more," because Buffett's track record convinced the market that the conglomerate premium was justified. At most other conglomerates, the answer has been "less," because the market assumes that diversification destroys focus and accountability.

GHC sits somewhere in between. The company trades at roughly book value—a price-to-book ratio of about 0.96 as of this writing—which suggests the market gives it credit for its assets but not much premium for its capital allocation abilities. The Graham Number, a Buffett-inspired intrinsic value calculation, pegs fair value at around $1,296 per share—roughly twenty percent above the current stock price. Whether that gap closes depends on whether the market comes to appreciate the quality of the underlying businesses, or whether the conglomerate structure permanently obscures it.

For the stock to rerate, the market would need to see either a sustained acceleration in earnings growth (most likely driven by healthcare) or a catalyst that forces a revaluation of the parts (a spinoff, a major asset sale, or a dramatic expansion of buybacks at depressed prices). A healthcare spinoff, in particular, would be a powerful catalyst: a pure-play home health and hospice company growing at thirty-plus percent annually would command a far higher multiple than it receives buried inside a diversified conglomerate. But there is no indication that management is contemplating such a move, and the permanent-capital philosophy argues against it.

The myth versus reality check on Graham Holdings is revealing.

The myth is that GHC is a declining media company living off the fumes of its past. The reality is that the company exited media a decade ago, restructured its education business through one of the most creative deals in recent corporate history, and is building a healthcare platform that could become a multi-billion dollar franchise.

The myth is that the conglomerate structure destroys value. The reality is that book value per share has compounded steadily, the share count has shrunk by over twelve percent, and the stock has tripled from its 2020 lows.

The myth is that management is coasting on the Graham name. The reality is that O'Shaughnessy has been one of the more active and intellectually honest capital allocators among small-cap conglomerates, openly acknowledging his biggest mistake and methodically unwinding it.

None of this means GHC is a certain winner. The conglomerate discount is real. The Leaf Group failure was expensive. The automotive segment has underdelivered. Broadcasting faces secular headwinds. And the dual-class share structure means public shareholders have limited governance rights. These are legitimate concerns that any investor must weigh against the bull case.

What is clear is that Graham Holdings is not the company it was a decade ago, or two decades ago, or certainly four decades ago when Katharine Graham ruled the newsroom and Buffett served on the board. It is something new—an experiment in whether the Berkshire model can work at a smaller scale, in different industries, under different leadership, in a different era. The company that once defined itself by the power of its printing press now defines itself by the discipline of its capital allocation. Whether the market will reward that discipline remains an open question. But for investors with the patience to match GHC's own time horizon, the story of the "Post-Post" company is one worth following—one acquisition, one buyback, one compounding year at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube