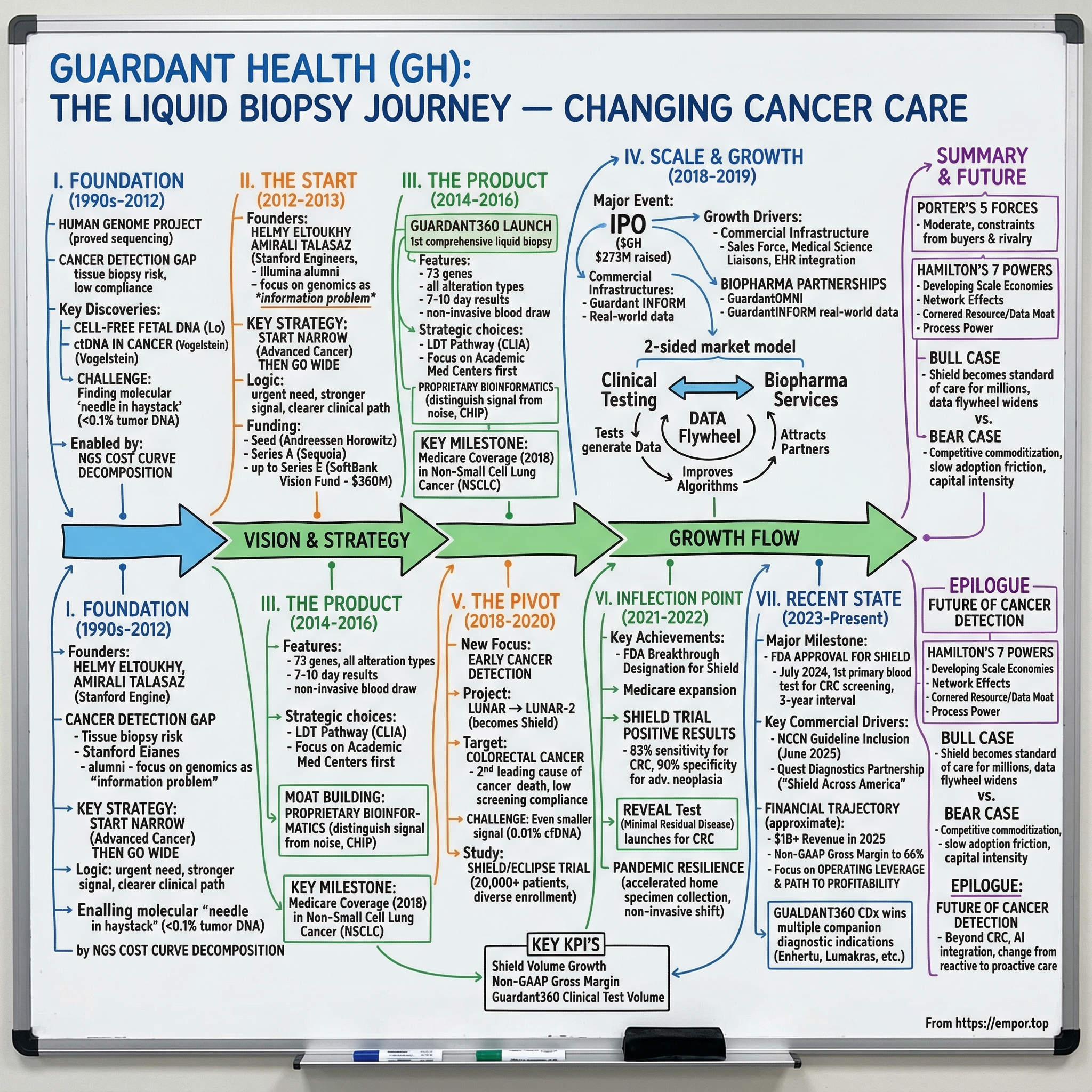

Guardant Health: Liquid Biopsy and the Quest to Change Cancer Care

I. Introduction and Episode Roadmap

Somewhere in America right now, a patient is sitting in an oncologist's office, waiting to learn whether their cancer has returned. A decade ago, that answer would have required a surgical biopsy — a needle or scalpel into a tumor, days of waiting, a procedure carrying real risk of complications. Today, for a growing number of those patients, the answer comes from a simple blood draw. The company that made that possible, more than any other, is Guardant Health.

With a market capitalization exceeding eleven billion dollars in early 2026 and revenue approaching one billion, Guardant Health has become the defining company in liquid biopsy — the science of detecting cancer through fragments of tumor DNA circulating in the bloodstream. But the story of how two Stanford-trained electrical engineers turned a fragile scientific concept into a clinical product used by over ten thousand oncologists worldwide is far more than a technology tale. It is a story about regulatory strategy as competitive moat, about the discipline of starting narrow before going wide, and about the agonizing patience required to build a healthcare company that could genuinely change how cancer is detected and treated.

The central question of this episode is deceptively simple: How did a startup turn a blood test into the future of oncology? The answer stretches across genomics, FDA politics, Medicare reimbursement battles, and the fundamental challenge of finding a molecular needle in a haystack — because that is essentially what detecting cancer DNA in a tube of blood requires.

Along the way, we will explore the tensions that define Guardant's journey. The tension between scientific ambition and commercial pragmatism. Between the allure of early cancer detection — the "bigger prize" — and the wisdom of proving clinical utility in advanced cancer first. Between burning hundreds of millions of dollars annually and building what could become one of the most consequential healthcare platforms of the twenty-first century.

Whether Guardant ultimately fulfills its most ambitious vision — a world where a routine annual blood test catches cancer before symptoms ever appear — remains an open question. But the story of how they got here, and what it reveals about building at the intersection of deep science, regulatory strategy, and capital markets, is one of the most instructive case studies in modern healthcare innovation. It is a story about patience, pragmatism, and the belief that a better way to detect cancer was not just possible, but inevitable.

What follows is that story.

II. The Foundation: Genomics Revolution and the Cancer Detection Gap (1990s–2012)

In June 2000, President Bill Clinton stood in the East Room of the White House alongside Francis Collins and Craig Venter and declared that the Human Genome Project had produced a "working draft" of the human genetic code. "Today," Clinton said, "we are learning the language in which God created life." The rhetoric was soaring, and the promise felt enormous: personalized medicine, diseases decoded at the molecular level, treatments tailored to an individual's genetic blueprint. The reality, as it turned out, would take considerably longer to arrive.

The Human Genome Project, which formally completed in 2003, did something profound — it proved that sequencing was possible and created the reference map against which all future genomic analysis would be measured. But the cost of sequencing a single genome at the time exceeded ninety-five million dollars. Personalized medicine was, for most patients, a concept discussed in academic journals rather than practiced in clinics.

Cancer, in particular, remained stubbornly resistant to the genomics revolution's early promises. The fundamental challenge was detection and characterization. For decades, diagnosing cancer and understanding its molecular profile required tissue — a physical sample obtained through biopsy. In lung cancer, that might mean threading a bronchoscope into the airways or inserting a CT-guided needle through the chest wall. In liver cancer, a needle through the abdomen. These procedures carried real risks: bleeding, infection, collapsed lungs. Nearly one in five lung biopsies was associated with an adverse event. And even when tissue was successfully obtained, it represented only a snapshot of a single tumor site, potentially missing the heterogeneity — the genetic diversity — that is cancer's defining characteristic.

Meanwhile, cancer screening for the general population remained remarkably crude. Colonoscopy, the gold standard for colorectal cancer detection, required patients to drink liters of preparation fluid, take a day off work, undergo sedation, and accept a small but real risk of bowel perforation. Compliance rates hovered around forty percent. Mammography caught many breast cancers but missed others, particularly in dense breast tissue. Low-dose CT scans for lung cancer screening were effective but required radiation exposure and generated a high rate of false positives.

The scientific seeds of something better, however, were quietly being planted. In 1997, a researcher named Dennis Lo at the Chinese University of Hong Kong made a discovery that would ultimately reshape diagnostics. Lo demonstrated that cell-free fetal DNA — fragments of a developing baby's genetic material — circulated in a pregnant mother's bloodstream. This was not just a curiosity; it proved that DNA from one biological source could be reliably detected in blood plasma despite being vastly outnumbered by the host's own DNA. Lo's work led to non-invasive prenatal testing, which became a multi-billion-dollar industry. But the implications extended far beyond pregnancy.

If fetal DNA circulated in maternal blood, could tumor DNA circulate in a cancer patient's blood? The answer, explored by Bert Vogelstein and his colleagues at Johns Hopkins, was yes. Vogelstein — already one of the most cited scientists in history for his work mapping the genetic mutations that drive colorectal cancer — demonstrated that circulating tumor DNA, or ctDNA, could be detected in the blood of cancer patients. Tumors, it turned out, continuously shed fragments of their DNA into the bloodstream as cancer cells die and are replaced. These fragments, often just 150 to 200 base pairs long, carried the same mutations found in the tumor itself.

The concept was elegant. The execution was extraordinarily difficult. Circulating tumor DNA typically represents a tiny fraction of the total cell-free DNA in blood — sometimes less than 0.1 percent. To put this in perspective: if all the cell-free DNA in a tube of blood were pages in a book, the tumor-derived pages might number fewer than one in a thousand. And those pages are fragmented, degraded, and mixed in with DNA from normal cells that died through routine cell turnover, as well as DNA from blood cells carrying their own acquired mutations — a confounding phenomenon called clonal hematopoiesis that can mimic cancer-related mutations. Finding the real cancer signal amid all this noise was like searching for a specific grain of sand on a beach while the wind kept blowing new sand in. The technology to reliably, affordably, and reproducibly detect these vanishingly small signals simply did not exist through most of the 2000s.

What changed everything was the cost curve of next-generation sequencing. Between 2007 and 2012, the cost of sequencing a human genome plummeted from roughly ten million dollars to under ten thousand — a decline faster than Moore's Law. Illumina's sequencing platforms, in particular, democratized access to high-throughput genomic analysis. Suddenly, the idea of scanning blood for tumor DNA fragments across dozens or hundreds of genes was not just scientifically plausible — it was economically feasible. The ingredients were in place: the biological principle proven by Lo and Vogelstein, the technology platform enabled by Illumina and its peers, and an enormous unmet clinical need. All that remained was someone to build the company.

III. The Founding Team and Early Vision (2012–2013)

Helmy Eltoukhy and AmirAli Talasaz first crossed paths in 2002, not in a hospital or a biotech lab, but at the Stanford Genome Technology Center, where both were pursuing doctoral research in electrical engineering. It is worth pausing on that detail, because it says something fundamental about Guardant Health's DNA — the company was not founded by oncologists or molecular biologists, but by engineers who thought about genomics as an information problem.

Eltoukhy, who grew up in California and attended Bellarmine College Preparatory, completed his bachelor's degree at Stanford in just two and a half years before staying for his master's and doctorate. His doctoral thesis focused on building an integrated system for de novo DNA sequencing, and during his postdoctoral fellowship at the Genome Technology Center, he invented the first semiconductor sequencing platform and the first base-calling algorithm for next-generation sequencing. These were foundational contributions to the field — the kind of work that sits underneath the entire modern genomics industry.

Talasaz brought a complementary perspective. Born in Iran, he earned his bachelor's at the prestigious Sharif University of Technology in Tehran before coming to Stanford, where he completed a PhD in electrical engineering alongside a master's in management science. At the Genome Technology Center, he led the technology development group, working on tools for purifying and analyzing circulating tumor cells.

Both founders followed a remarkably similar path after Stanford: each started a company, and each had that company acquired by Illumina. Eltoukhy co-founded Avantome in 2007 to commercialize semiconductor sequencing; Illumina bought it in 2008. Talasaz founded Auriphex Biosciences, focused on circulating tumor cell analysis; Illumina acquired its technology in 2009. Both men then spent several years inside Illumina — Eltoukhy as Director of Advanced Sequencing Development, Talasaz on the genomics technology side — before leaving together in 2012 to found Guardant Health.

The Illumina experience was formative in at least two ways. First, it gave both founders deep operational understanding of sequencing technology and its capabilities and limitations. Second, it showed them the gap between what the technology could theoretically do and what was actually being delivered to patients. Illumina was building the tools; nobody was yet building the comprehensive clinical solution.

The founding insight was precise and, importantly, contrarian. The obvious play in liquid biopsy circa 2012 was early detection — screening healthy people for cancer, the massive population-level prize. Several well-funded efforts were already moving in that direction. But Eltoukhy and Talasaz made a different bet: start with advanced cancer patients, not healthy people.

The logic was ruthless in its pragmatism. Advanced cancer patients had an immediate, urgent need for molecular profiling to guide treatment decisions. They had measurable levels of circulating tumor DNA — the signal was stronger, making detection technically easier. And critically, the path to clinical adoption was shorter: oncologists already ordered molecular tests for advanced cancer patients, so Guardant would be offering a better way to do something doctors already wanted to do, rather than asking them to adopt an entirely new paradigm.

This was the strategic seed from which everything else grew. Start where the signal is strongest and the clinical need is clearest. Prove that liquid biopsy works. Build the evidence base, the physician relationships, the payer coverage, and the operational infrastructure. Then — and only then — expand into earlier-stage detection where the science is harder and the adoption barriers are higher.

Early funding came quickly, reflecting Silicon Valley's appetite for genomics-meets-technology stories. Andreessen Horowitz led a five and a half million dollar seed round in 2013. Sequoia Capital followed with a ten million dollar Series A in February 2014. Two months later, Khosla Ventures led a thirty million dollar Series B, with founding partner Samir Kaul joining the board. The pace of fundraising — three rounds in barely a year — reflected both investor enthusiasm and the capital-intensive nature of building a CLIA-certified clinical laboratory from scratch.

The fundraising accelerated from there. Lightspeed Venture Partners led a fifty million dollar Series C in early 2015. OrbiMed followed with a Series D in 2016. And in August 2017, SoftBank's Vision Fund led a massive three hundred and sixty million dollar Series E, with participation from T. Rowe Price, Temasek, and existing investors. The total pre-IPO capital raised exceeded five hundred and fifty million dollars across seven rounds from twenty-five investors. This was not a company that could be bootstrapped — clinical laboratory infrastructure, regulatory submissions, clinical studies, and a national sales force all required substantial capital well before revenue could cover costs. The founders understood this from the beginning, and their fundraising strategy reflected it: raise enough capital to reach each subsequent milestone, then raise again from a position of demonstrated progress.

IV. Building the Product: Guardant360 and Clinical Validation (2014–2016)

In 2014, just two years after incorporation, Guardant Health commercially launched Guardant360 — making it the first comprehensive liquid biopsy available for cancer patients. The product analyzed seventy-three genes across four major categories of genetic alterations: point mutations across all seventy-three genes, insertions and deletions in twenty-three genes, copy number amplifications in eighteen genes, and gene fusions in six genes. The panel was specifically designed to cover the mutations most relevant to targeted therapy selection — the alterations that oncologists needed to know about to choose the right drug for a given patient.

The technical challenges were staggering. Think of it this way: a standard blood draw contains roughly ten milliliters of blood. From that blood, you extract plasma. From the plasma, you isolate cell-free DNA. Of that cell-free DNA, the tumor-derived fraction might represent anywhere from less than 0.1 percent to perhaps five percent of the total, depending on the cancer type, stage, and individual patient biology. Guardant's technology had to reliably detect specific mutations within that tiny tumor fraction while simultaneously eliminating false positives — because in oncology, a false positive does not just cause anxiety. It can lead to a patient receiving the wrong drug, with all the attendant toxicity and wasted time.

The company's approach involved proprietary bioinformatics — sophisticated computational methods that could distinguish true tumor-derived signals from sequencing noise and from mutations that arose in blood cells themselves, a phenomenon called clonal hematopoiesis of indeterminate potential, or CHIP. Getting this right required not just good sequencing but exceptional data science, which is where the founders' engineering backgrounds proved particularly valuable.

Why did this matter clinically? Because cancer treatment was entering the era of targeted therapy — drugs designed to attack specific molecular vulnerabilities in a tumor. Osimertinib for EGFR-mutated lung cancer. Crizotinib for ALK-rearranged lung cancer. Vemurafenib for BRAF-mutated melanoma. These drugs could be transformative for the right patient, but useless — or harmful — for the wrong one. Identifying the right patient required molecular testing, and traditional tissue biopsy was failing too many of them: tissue was sometimes insufficient for testing, the procedure sometimes too risky to attempt, and the results sometimes misleading because a single biopsy site could not capture the full genetic diversity of a metastatic cancer.

Guardant360 offered a fundamentally different value proposition. A simple blood draw, results typically within seven to ten days, no procedural risk, and — crucially — the potential to capture tumor heterogeneity because the blood contained DNA fragments shed from multiple tumor sites throughout the body. For a patient with lung cancer that had metastasized to the liver, bone, and brain, a single tissue biopsy of one site might miss a resistance mutation present in another. The blood, in theory, told the whole story.

The regulatory strategy was deliberate. Rather than pursuing FDA approval — a process that would have taken years and required large prospective clinical trials — Guardant launched Guardant360 as a Lab Developed Test under CLIA, the Clinical Laboratory Improvement Amendments framework. CLIA-certified labs could develop and offer tests without FDA clearance, provided they met quality and proficiency standards. This pathway allowed Guardant to get to market quickly, begin generating clinical evidence, and build physician adoption while the longer-term FDA strategy played out in parallel.

Physician adoption followed a classic pattern: early adopters at major academic medical centers, then gradual penetration into community oncology practices. The company invested heavily in medical affairs — educating oncologists about when and how to use liquid biopsy, and critically, how to interpret the results. This was not a product that could sell itself. Oncologists needed to understand the test's analytical sensitivity, its concordance with tissue-based testing, and its limitations.

Key publications helped build the evidence base. Studies published in major oncology journals demonstrated that Guardant360's concordance with tissue biopsy for treatment-relevant mutations — EGFR, ALK, ROS1, BRAF, and others — ranged from ninety-two to one hundred percent. For oncologists accustomed to tissue as the gold standard, this level of agreement was persuasive.

But the most transformative moment of Guardant's early commercial life came not from a journal publication but from a coverage decision. In July 2018, Palmetto GBA — a Medicare Administrative Contractor — finalized a local coverage determination for Guardant360 in metastatic non-small cell lung cancer. This meant that Medicare would pay for the test. In American healthcare, Medicare coverage is the single most important commercial inflection point a diagnostic test can achieve. It validates clinical utility in the eyes of payers, provides a pricing benchmark, and — perhaps most importantly — signals to oncologists that the test has met a threshold of clinical evidence. When Medicare said yes to Guardant360, the commercial trajectory fundamentally changed. By December 2019, that coverage had expanded to the vast majority of advanced solid tumor cancers. The company that had started with a pragmatic focus on advanced cancer now had a payer-validated platform covering hundreds of thousands of potential patients annually.

V. Going Public and Scaling the Commercial Engine (2018–2019)

On October 4, 2018, Guardant Health began trading on the Nasdaq Global Select Market under the ticker GH. The company priced its IPO at nineteen dollars per share, selling just over fourteen million shares including the fully exercised overallotment option, and raised approximately two hundred and seventy-three million dollars. The market's verdict was emphatic: shares closed at thirty-two dollars and twenty cents on the first day of trading, a sixty-nine percent premium, valuing the company at roughly one and a half billion dollars.

The IPO came at a moment of maximum optimism about precision oncology. The promise of matching cancer patients with targeted therapies based on their tumor's genetic profile was moving from academic aspiration to clinical reality. Oncologists at major cancer centers were already ordering liquid biopsies routinely. The Medicare coverage decision three months earlier had removed the most significant commercial barrier. And Guardant had just posted full-year 2018 revenue of ninety-one million dollars — proof that oncologists would actually order the test and payers would actually pay for it.

But the IPO also arrived with legitimate skepticism about the path to profitability. Guardant was burning cash at a significant rate, investing heavily in R&D, building a national sales force, and already beginning to lay the groundwork for early detection programs that would require hundreds of millions more in clinical trial spending. The S-1 filing made clear that this was a company that needed patient capital — investors willing to wait years, potentially a decade or more, for the full commercial vision to unfold.

Building the commercial engine required more than just a good product. Guardant had to construct an entirely new category in oncology practice. Liquid biopsy was not replacing an existing test with a better one — it was asking oncologists to fundamentally change their diagnostic workflow. Instead of reflexively ordering a tissue biopsy when a patient presented with advanced cancer, physicians needed to consider blood-based testing first, or at least concurrently. This required a dedicated sales force that was not just selling a product but educating an entire specialty.

The company invested aggressively in commercial infrastructure. Sales representatives were deployed across major cancer centers and community oncology practices. Medical science liaisons — PhD-level scientists who could discuss clinical data with oncologists on a peer-to-peer basis — supported the sales effort. The company also built integrations with electronic health record systems and laboratory information systems to make ordering as seamless as possible.

The company also pursued strategic partnerships that extended the platform's reach into drug development. Pharmaceutical companies were increasingly recognizing that liquid biopsy could accelerate clinical trials — by identifying eligible patients more quickly through blood-based screening rather than requiring tissue biopsies for trial enrollment, and by monitoring treatment response in real time through serial blood draws. Guardant launched GuardantOMNI, a five-hundred-plus gene comprehensive panel designed specifically for biopharma research applications, giving pharmaceutical partners a broader genomic view than the clinical-grade Guardant360 panel.

Revenue growth reflected the commercial momentum. From ninety-one million dollars in 2018, revenue more than doubled to two hundred and fourteen million in 2019, driven by both test volume growth and payer coverage expansion. The two-sided business model was taking shape: clinical testing — where Guardant billed payers for tests ordered by physicians — and biopharma services — where pharmaceutical companies paid Guardant to use its technology in clinical trials and drug development programs. The biopharma side was particularly elegant because it leveraged the same platform and laboratory infrastructure as the clinical business but with a fundamentally different customer and pricing dynamic.

The competitive landscape was intensifying. Foundation Medicine, acquired by Roche in 2018, was the most formidable competitor — offering both tissue-based and liquid biopsy comprehensive genomic profiling. Tempus was building a data-centric approach to precision medicine. And a wave of venture-backed startups was entering various niches of the liquid biopsy market. But Guardant had a critical advantage: it was first to market with a comprehensive liquid biopsy, had the largest evidence base, and was now scaling commercially with Medicare coverage in hand. In diagnostics, first-mover advantage compounds because every test performed generates data that improves the platform and deepens physician familiarity.

VI. The Pivot to Early Detection: LUNAR and the Cancer Screening Vision (2018–2020)

Every healthcare company eventually faces a strategic crossroads: stay focused on what is working, or invest in the bigger, harder, potentially transformative opportunity. For Guardant Health, that crossroads arrived almost simultaneously with the commercial success of Guardant360. The question was whether to pursue early cancer detection — screening apparently healthy individuals before symptoms appeared.

The company had actually begun thinking about this well before the IPO. In 2016, Guardant announced Project LUNAR, a research initiative aimed at extending liquid biopsy beyond advanced cancer treatment selection into two new domains: early cancer detection and minimal residual disease monitoring. LUNAR-1 focused on lung cancer, and LUNAR-2 — which would eventually become Shield — targeted colorectal cancer.

The strategic logic was compelling but the execution risk was enormous. If Guardant360 was about finding a needle in a haystack, early detection was about finding a needle in an entire field of haystacks. In advanced cancer patients, circulating tumor DNA levels are typically measurable — the tumor burden is high enough that meaningful amounts of ctDNA enter the bloodstream. In early-stage cancer, the tumor may be tiny, perhaps just a few millimeters, shedding infinitesimal amounts of DNA that are all but invisible against the background of normal cell-free DNA and clonal hematopoiesis noise.

The signal-to-noise problem in early detection was not just incrementally harder than in advanced cancer — it was fundamentally different. Guardant360 needed to detect mutations at variant allele frequencies of perhaps 0.1 to 1 percent. Early detection might require sensitivity at 0.01 percent or below. This demanded entirely new assay chemistry, new bioinformatics approaches, and massive clinical validation studies involving thousands of healthy or average-risk individuals — a completely different scale from studies in cancer patients.

The comparison with GRAIL, then an Illumina subsidiary, is instructive. GRAIL had raised over four billion dollars to pursue multi-cancer early detection from blood, developing its Galleri test that aimed to detect more than fifty cancer types simultaneously. GRAIL's approach used methylation patterns rather than mutation detection, betting that epigenetic signatures offered better sensitivity for early-stage cancers across multiple tissue types. Guardant took a different approach with Shield, focusing specifically on colorectal cancer as the initial target — a single-cancer, prove-the-concept strategy rather than GRAIL's audacious multi-cancer bet.

Why colorectal cancer? Several factors aligned. First, CRC is the second leading cause of cancer death in the United States, with roughly 150,000 new cases and 53,000 deaths annually. Second, existing screening methods — colonoscopy and stool-based tests like Cologuard — had significant compliance problems. Only about forty percent of eligible Americans were up to date on CRC screening, largely because the available options were inconvenient, unpleasant, or both. Third, CRC has a well-understood biology of progression from adenoma to carcinoma, making it a tractable target for blood-based detection. And fourth, the regulatory pathway was relatively well-defined, with clear precedent from Cologuard's FDA approval process.

The SHIELD study — eventually renamed ECLIPSE — would become the registrational trial for the Shield blood test. Guardant designed it as a prospective, multi-center study enrolling over twenty thousand average-risk adults aged forty-five to eighty-four across more than two hundred clinical sites in thirty-four states. The demographics were deliberately diverse: twelve percent Black, thirteen percent Hispanic, seven percent Asian American — above-average minority enrollment for a clinical trial, which mattered both scientifically and ethically.

The colorectal cancer target also offered a clear benchmark for commercial success. Exact Sciences had proven with Cologuard that non-invasive CRC screening could achieve massive adoption — Cologuard grew to over two billion dollars in annual revenue within a decade of FDA approval, aided by aggressive direct-to-consumer advertising that turned a stool test into a household name. If a stool-based test could achieve that scale despite the unpleasantness of sample collection, what could a blood test do? The question was tantalizing, and it drove much of the investor enthusiasm for Guardant's early detection strategy.

The investment required was massive. Beyond the clinical trial costs, Guardant had to build parallel infrastructure: a discovery research operation developing and refining the early detection assay alongside the commercial operation running the Guardant360 business. The SoftBank-led three hundred and sixty million dollar Series E in 2017 had been raised with this dual mission in mind, and the IPO proceeds would fund much of the early detection investment. But the cash burn implications were stark — Guardant would lose hundreds of millions of dollars annually for years as it pursued the screening vision.

VII. The Pandemic and Operational Resilience (2020–2021)

When COVID-19 hit in March 2020, it disrupted nearly every aspect of cancer care. Elective procedures were postponed. Screening programs were suspended. Patients avoided hospitals out of fear of infection. For a company whose entire business depended on cancer patients seeing their oncologists and receiving molecular testing, the pandemic represented an existential operational challenge.

Guardant's response was both immediate and pragmatic. On the clinical side, the company accelerated programs for home-based specimen collection — enabling blood draws at patients' homes rather than requiring visits to medical facilities. This was not just a pandemic stopgap; it foreshadowed a broader shift toward patient convenience that would become central to the Shield screening value proposition. If you could make a blood test for cancer as easy as a routine blood draw, you could fundamentally change compliance rates.

Testing volumes inevitably dipped in the early months of the pandemic but recovered more quickly than many expected. Oncology, unlike elective surgery, does not wait — cancer patients need treatment, and treatment decisions require molecular profiling. By the second half of 2020, Guardant360 volumes had largely recovered, and the company posted full-year revenue of two hundred and eighty-seven million dollars, up thirty-four percent from 2019.

In August 2020, amid the pandemic's disruption, Guardant achieved a landmark regulatory milestone: the FDA approved Guardant360 CDx as the first liquid biopsy companion diagnostic using next-generation sequencing for comprehensive tumor mutation profiling across all solid cancers. This was not just another clearance — it was the first time the FDA had approved a blood-based NGS test for pan-solid tumor genomic profiling. The initial companion diagnostic indication was for osimertinib in EGFR-mutated non-small cell lung cancer, validated on over five thousand samples from pivotal phase III trials.

Foundation Medicine received its own FDA approval for FoundationOne Liquid CDx just three weeks later, setting up the competitive dynamic that would define the companion diagnostics market for years to come. Guardant responded aggressively, and notably filed patent infringement lawsuits against Foundation Medicine, alleging that FoundationOne Liquid CDx infringed on multiple Guardant liquid biopsy patents.

The pandemic also accelerated a broader trend that would benefit Guardant in the years ahead. Telemedicine adoption surged — visits that previously required in-person consultations moved online. This shift in physician-patient interaction patterns made non-invasive diagnostics more attractive. If a patient could consult with their oncologist via video, they could also receive a molecular profiling order that required only a trip to a local blood draw site, rather than a hospital visit for a tissue biopsy. The pandemic compressed years of digital health adoption into months.

Beyond the direct business impact, the pandemic period also delivered an unexpected tailwind: it accelerated awareness of non-invasive diagnostics across the healthcare system. Patients who had experienced COVID testing — a simple nasal swab providing molecular results — were more receptive to the concept of blood-based cancer detection. Healthcare systems that had adapted to remote and decentralized care were more open to testing modalities that did not require in-person facility visits.

Revenue continued climbing: three hundred and seventy-four million dollars in 2021, a thirty percent increase. Clinical test volumes grew even faster, reflecting both recovery from pandemic-era suppression and genuine market penetration gains. Guardant was also expanding its addressable market within oncology — adding new cancer types and new gene panels, deepening relationships with community oncology practices that were increasingly adopting liquid biopsy as standard practice, and signing new biopharma contracts as pharmaceutical companies recognized the value of blood-based companion diagnostics for their drug development pipelines.

The stock, which had surged past one hundred and seventy dollars in early 2021 on pandemic-era growth enthusiasm, would eventually come back to earth as interest rates rose and investors rotated away from high-growth, unprofitable companies. But the underlying business was stronger than it had ever been. The company was proving that its commercial engine could withstand — and even benefit from — massive external disruption, while simultaneously advancing the ECLIPSE trial enrollment that would determine Shield's fate.

VIII. Key Inflection Point: FDA Breakthrough and Medicare Expansion (2021–2022)

The FDA's Breakthrough Device designation program exists for technologies that offer transformative advantages over existing options for life-threatening conditions. When the FDA granted this designation to Shield for colorectal cancer screening, it was more than a bureaucratic checkbox — it was the FDA telling Guardant, and the world, that a blood test for CRC screening had the potential to fundamentally change clinical practice.

Breakthrough designation brought tangible benefits: prioritized FDA review, more interactive engagement with the agency during the review process, and the possibility of expedited approval. For Guardant, it also provided powerful commercial signaling. Payers, physicians, and investors all understood that Breakthrough designation meant the FDA considered this technology genuinely different from what existed.

Simultaneously, Medicare was expanding its coverage framework for comprehensive genomic profiling. The coverage decisions that had started with Guardant360 in NSCLC in 2018 had broadened to most solid tumors by late 2019, and the reimbursement infrastructure was maturing. Medicare's willingness to pay for liquid biopsy was creating a template that commercial payers increasingly followed.

The product portfolio was expanding strategically. GuardantOMNI, a five-hundred-plus gene panel, served the biopharma market — a research-use-only tool designed for pharmaceutical companies running clinical trials. It covered the vast majority of genes being evaluated in drug development pipelines, including tumor mutational burden and other immuno-oncology biomarkers. GuardantINFORM, launched in June 2020, was a real-world clinical-genomic data platform that aggregated de-identified data from Guardant360 tests — integrating sequencing data with demographics, diagnoses, treatments, and outcomes across more than sixty solid tumor types. This data platform served biopharma customers looking to design clinical trials, simulate control arms, or understand real-world treatment patterns.

Guardant Reveal, the company's minimal residual disease test, also gained commercial traction during this period. Designed to detect residual cancer DNA after surgery — answering the critical question of whether the surgeon "got it all" — Reveal received Medicare coverage in August 2022 for post-surgical MRD detection in colorectal cancer. Blue Cross and Blue Shield of Louisiana became the first commercial payer to cover Reveal in July 2023. This product occupied a strategic middle ground between Guardant360's advanced cancer profiling and Shield's population screening — it served patients who had already been diagnosed and treated, monitoring them for recurrence through serial blood tests rather than repeated imaging.

The beauty of this portfolio strategy was that each product reinforced the others. Every clinical test performed generated data that fed GuardantINFORM, which attracted biopharma customers, which funded trials that generated more clinical evidence for the core testing products, which drove further physician adoption. This flywheel effect — test volume begetting data begetting partnerships begetting evidence begetting more test volume — was Guardant's most important strategic asset, and it was compounding with every quarter.

Revenue in 2022 reached four hundred and fifty million dollars. Clinical test volumes grew forty-two percent year over year to roughly one hundred and twenty-five thousand tests. Biopharma test volumes grew forty percent to twenty-six thousand. The company was demonstrating that it could grow both sides of its business simultaneously while advancing the early detection pipeline. But losses were also expanding — approaching four hundred and forty million dollars annually — as the company invested in Shield's clinical development, commercial infrastructure, and laboratory capacity expansion.

The stock market, predictably, was uncertain about how to value a company with strong revenue growth, an expanding pipeline, a potentially massive total addressable market, and significant ongoing losses. Shares fluctuated considerably, reflecting the tension between the long-term vision and near-term profitability concerns that would define investor sentiment for years. This is a familiar dynamic for investors in healthcare platforms: the value creation potential is enormous, but the capital required to realize that potential creates sustained dilution and cash burn that tests even patient shareholders. The question was not whether Guardant was building something important — it clearly was — but whether the economic returns would arrive before the balance sheet ran out of runway.

IX. The ECLIPSE Study Results and FDA Approval Quest (2023–2024)

The data that emerged from the ECLIPSE trial in 2022 would determine whether Shield was a genuine breakthrough or a scientific curiosity. When Guardant announced positive results, the oncology and diagnostics communities leaned in.

Shield demonstrated eighty-three percent sensitivity for detecting colorectal cancer — meaning it correctly identified eighty-three out of every hundred cases. Specificity for advanced neoplasia was ninety percent, meaning only ten percent of patients without concerning findings received a false positive result. These topline numbers told an important story, but the stage-by-stage breakdown told a more nuanced one. Stage I sensitivity was sixty-two percent — good but not overwhelming for the earliest cancers. Stage II was one hundred percent. Stage III, ninety-six percent. Stage IV, one hundred percent. The pattern made biological sense: larger, more advanced tumors shed more DNA, making them easier to detect. For a screening test aimed at catching cancer early, the Stage I sensitivity was the most scrutinized number, and sixty-two percent meant that some early-stage cancers would be missed.

Advanced adenoma sensitivity — the ability to detect precancerous polyps — was only thirteen percent, which was a known limitation. Shield was designed primarily to catch cancer, not precancer. Critics argued that missing precancerous lesions defeated the purpose of screening, which ideally prevents cancer rather than just catching it early. Supporters countered that the compliance advantage of a blood test would more than compensate for the lower per-test sensitivity for precancerous lesions, and that most early-stage cancers detected by Shield would be highly curable.

But here is where context matters enormously. The relevant comparison was not against a theoretical perfect test, but against the alternatives people were actually using — or, more precisely, not using. Colonoscopy has near-perfect sensitivity, but forty percent compliance means that sixty percent of eligible Americans are not being screened at all. A blood test with eighty-three percent sensitivity that achieves dramatically higher adherence could catch more cancers in aggregate than a perfect test that most people avoid. In a twenty-thousand-person adherence study, Shield demonstrated approximately ninety-five percent patient compliance — a staggering number compared to colonoscopy or even stool-based testing.

The ECLIPSE results were published in the New England Journal of Medicine on March 14, 2024 — the gold standard of medical publication, signaling to the clinical community that this data had withstood the most rigorous peer review. The publication was the scientific prerequisite for what came next.

On July 29, 2024, the FDA approved Shield as the first blood test for primary colorectal cancer screening in average-risk adults aged forty-five and older. An FDA Advisory Committee had previously recommended approval, and the decision cleared the path for Medicare reimbursement. This was the inflection point that the company had been building toward for nearly a decade. Shield was not just another diagnostic test — it was the first time the FDA had approved a simple blood draw as a primary screening option for any cancer in the general population.

The approval came with a recommended three-year screening interval — patients would take the blood test every three years, compared to every ten years for colonoscopy or every one to three years for stool-based tests. For patients who had been avoiding screening entirely, the convenience of a blood draw during a routine doctor visit represented a transformational shift in the screening paradigm. No preparation, no sedation, no recovery time — just a tube of blood drawn alongside routine lab work.

The competitive landscape in CRC screening was becoming more complex. Exact Sciences' Cologuard Plus, a next-generation stool-based test, offered ninety-four percent sensitivity for CRC and ninety-six percent specificity — superior clinical performance to Shield on a per-test basis. But Cologuard required collecting a stool sample at home and mailing it to a lab, a process that many patients found unpleasant. Freenome was developing SimpleScreen, another blood-based CRC test, but was still in clinical trials. And Exact Sciences was simultaneously pursuing its own blood-based test while acquiring Freenome's U.S. CRC rights — a belt-and-suspenders strategy reflecting the company's recognition that blood-based screening posed a real competitive threat to its stool-based franchise. In a further competitive escalation, Abbott announced plans to acquire Exact Sciences for twenty-one billion dollars, bringing enormous distribution and capital resources into the fight.

On the companion diagnostics front, Guardant360 CDx continued accumulating FDA-approved indications — each one adding incremental value by linking the test to specific targeted therapies. Key approvals included companion diagnostic status for Daiichi Sankyo and AstraZeneca's Enhertu in HER2-mutant lung cancer, Amgen's Lumakras in KRAS G12C-mutant lung cancer, and Eli Lilly's Inluriyo in ESR1-mutated advanced breast cancer. These approvals were not glamorous individually, but cumulatively they constructed a powerful competitive moat: the more therapies for which Guardant360 CDx was the designated companion diagnostic, the more reason oncologists had to order it as their default liquid biopsy platform. By 2025, UnitedHealthcare, Anthem, Aetna, and Humana all covered Guardant360 CDx for various indications, representing access to over three hundred million covered lives.

X. Recent Developments and Current State (2024–Present)

Shield's commercial rollout began in the second half of 2024 under conditions that tested the thesis of blood-based screening adoption. In its first partial year of commercial availability, approximately 6,400 Shield tests were performed, generating roughly four million dollars in screening revenue. These were modest numbers — the test had launched mid-year, payer coverage was still being established, and physician education was just beginning.

The real acceleration came in 2025. In March, CMS granted Shield Advanced Diagnostic Laboratory Test status, setting reimbursement at fourteen hundred and ninety-five dollars per test — a critical milestone that provided revenue visibility and signaled Medicare's endorsement. In June, the NCCN — National Comprehensive Cancer Network, whose guidelines serve as the de facto standard of care in American oncology — updated its colorectal cancer screening guidelines to include Shield as the first FDA-approved blood-based option. These two events together — Medicare pricing and NCCN inclusion — triggered the commercial inflection that Guardant had been building toward.

Shield test volumes exploded. From 6,400 tests in all of 2024, volumes jumped to approximately 87,000 tests in 2025, generating nearly eighty million dollars in screening revenue. The fourth quarter alone saw roughly 38,000 Shield tests — suggesting a run rate that, if sustained, would represent well over 150,000 annual tests. The company partnered with Quest Diagnostics to enable nationwide test ordering and collection, dramatically expanding the physical infrastructure available for blood draws. A "Shield Across America" mobile screening tour visited over one hundred communities, building awareness directly with patients.

The oncology testing business also continued its strong trajectory. Approximately 264,000 clinical tests were performed in 2025, up thirty-four percent year over year. Guardant360 CDx added its twenty-fifth companion diagnostic indication in January 2026 — approval as the companion diagnostic for Pfizer's encorafenib combination in BRAF V600E-mutant metastatic colorectal cancer. Each new CDx indication reinforced the platform's position as the default ordering choice for oncologists.

Full-year 2025 revenue reached nine hundred and eighty-two million dollars, with the oncology segment contributing approximately six hundred and eighty-four million, screening contributing eighty million, and biopharma and data services contributing two hundred and ten million. The company guided 2026 revenue growth of twenty-seven to thirty percent, implying revenue of approximately one and a quarter billion dollars — a milestone that would validate the multi-product platform strategy.

The path to profitability, however, remains Guardant's most scrutinized metric. Non-GAAP gross margins improved to sixty-six percent by the fourth quarter of 2025, up from sixty-three percent a year earlier, reflecting operational efficiency gains as volume scaled. But net losses persisted in the hundreds of millions annually, driven by the ongoing investments in Shield's commercial launch, international expansion, R&D for the broader early detection pipeline, and the infrastructure needed to support potentially millions of screening tests annually. The company's stock, trading around eighty-eight dollars in early March 2026 with a market cap exceeding eleven billion, reflected a market that was cautiously optimistic about the trajectory but still waiting for operating leverage to materialize.

International expansion, meanwhile, proceeded methodically if not dramatically. Guardant360 CDx received regulatory approval in Japan in 2022 and national reimbursement approval in July 2023, with subsequent companion diagnostic approvals following. The test is CE-Marked in Europe. But the Shield rollout has been almost entirely domestic, with international screening markets representing future optionality rather than near-term revenue contribution.

XI. The Business Model and Unit Economics

Guardant Health operates what is essentially a two-sided platform — a structure rare in diagnostics and worth understanding in detail, because it explains both the company's revenue resilience and its capital intensity.

The first side is clinical testing. A physician orders a Guardant test — Guardant360 CDx for advanced cancer molecular profiling, or Shield for colorectal cancer screening. A blood sample is drawn, shipped to Guardant's CLIA-certified laboratory in Redwood City, California, processed through the company's proprietary wet-lab and bioinformatics pipeline, and a report is generated and delivered to the ordering physician. Guardant then bills the patient's insurance — Medicare, Medicaid, commercial payers — for the test. Revenue per test varies by product and payer, but Shield is reimbursed at fourteen hundred and ninety-five dollars under Medicare's ADLT program, and Guardant360 CDx pricing varies by indication and payer contract.

The cost structure of clinical testing involves both fixed and variable components. The laboratory itself — equipment, facility, quality systems, bioinformatics infrastructure — represents significant fixed cost. Sequencing reagents, consumables, specimen processing labor, and shipping are variable costs that scale with volume. As volume grows, the fixed cost component is amortized across more tests, driving gross margin improvement — exactly the trajectory visible in the company's financials, with non-GAAP gross margins climbing from the low sixties to sixty-six percent.

The second side is biopharma services. Pharmaceutical companies use Guardant's platform for several purposes: developing companion diagnostics for targeted therapies, using GuardantOMNI in clinical trials for comprehensive genomic profiling, and accessing GuardantINFORM's real-world data platform for trial design, patient identification, and outcomes research. This revenue stream is fundamentally different from clinical testing — contracts are negotiated directly with pharmaceutical companies, pricing reflects the value of the data and the companion diagnostic development pathway, and the relationship is inherently long-term because switching CDx partners mid-trial is extremely difficult.

The interplay between these two sides creates the flywheel effect that is Guardant's most important strategic asset. Clinical tests generate data. Data improves the platform's algorithms and feeds GuardantINFORM. Better algorithms and richer data attract biopharma partners. Biopharma partnerships generate companion diagnostic approvals. CDx approvals drive more clinical test ordering. More tests generate more data. The flywheel spins.

But this business model is emphatically not software. The marginal cost of running one more sequencing assay is meaningful — reagents, labor, computational resources, quality control. Unlike a software platform where marginal cost approaches zero, Guardant's marginal cost per test is substantial, which means the gross margin ceiling is lower than a SaaS business. At sixty-six percent non-GAAP gross margins, Guardant is performing well for a laboratory services company, but the path to operating profitability also requires significant operating expense leverage — growing revenue faster than sales, marketing, R&D, and general administrative expenses.

The capital intensity is notable. Guardant has invested hundreds of millions in R&D annually, not just for product development but for the clinical studies required to support FDA approvals and payer coverage decisions. Each new product — Shield, Guardant Reveal, future multi-cancer tests — requires its own clinical development program, its own regulatory submission, and its own payer engagement strategy. This is not a platform where you can simply add features; each new test is essentially a new product requiring its own evidence generation infrastructure.

Comparing Guardant to traditional diagnostic laboratory companies like Quest Diagnostics or LabCorp is instructive but somewhat misleading. Quest and LabCorp operate high-volume, low-complexity testing businesses with thin margins on commodity tests and thicker margins on specialty tests. Guardant operates exclusively in high-complexity, high-value testing, with a fundamentally different competitive dynamic. The more relevant comparison is to Exact Sciences, which similarly built a single-product franchise in cancer screening before expanding its portfolio, or to Myriad Genetics, which pioneered hereditary cancer testing. Both companies demonstrated that diagnostics businesses can achieve significant scale, but both also illustrated the challenges of maintaining premium pricing and margins as competition intensifies and payers push back.

XII. Competitive Landscape and Strategic Positioning

The liquid biopsy market in 2026 resembles nothing so much as a multi-front war, with several well-capitalized players competing across overlapping but distinct segments. Understanding who is competing where — and why Guardant's positioning matters — requires mapping the battlefield.

Foundation Medicine, wholly owned by Roche since 2018, is the most direct competitor in advanced cancer molecular profiling. FoundationOne Liquid CDx covers over three hundred genes compared to Guardant360's seventy-three in its LDT version and fifty-five in the CDx version, but Guardant has accumulated significantly more companion diagnostic indications — twenty-five versus a smaller handful for Foundation Medicine. The patent litigation between the two companies underscores the intensity of this rivalry: Guardant has alleged that FoundationOne Liquid CDx infringes on multiple patents, claiming the product is "nearly identical" to Guardant360.

In the screening arena, the competitive dynamics are different. Exact Sciences dominates non-invasive CRC screening with Cologuard, which has become a household name through aggressive direct-to-consumer television advertising. Cologuard Plus offers ninety-four percent CRC sensitivity — meaningfully higher than Shield's eighty-three percent — but requires stool collection rather than a simple blood draw. The strategic question is whether superior convenience can overcome inferior per-test sensitivity at the population level. Guardant's bet is that it can, pointing to the dramatically higher compliance rates observed in its studies.

GRAIL's Galleri test represents a different competitive vector entirely. Rather than targeting a single cancer type, Galleri aims to detect over fifty cancer types from a single blood draw using methylation-based detection. GRAIL submitted its final premarket approval module to the FDA in January 2026. If approved, Galleri could expand the concept of blood-based cancer screening well beyond CRC. This is both competitive threat and potential market-expansion catalyst for Guardant — if the public becomes accustomed to the idea of blood tests for cancer screening, Shield and future Guardant products benefit from that behavioral shift.

Natera occupies a critical position in the minimal residual disease space with its Signatera test, which uses a tumor-informed approach to detect residual cancer after surgery. Guardant Reveal competes directly in this segment, and the two companies represent different technical philosophies: Signatera customizes a test for each patient based on their specific tumor mutations, while Guardant Reveal uses a tumor-naive approach that does not require prior tissue sequencing. The trade-off is sensitivity versus accessibility — tumor-informed approaches may detect lower levels of residual disease, but tumor-naive approaches can be deployed faster and do not require a prior tissue sample, which is a meaningful practical advantage.

In China, Burning Rock Biotech offers comprehensive genomic profiling and has built a strong position in the domestic market, though its international expansion has been limited. BGI Genomics, one of the world's largest genomics organizations, has liquid biopsy capabilities but has focused primarily on prenatal testing and research services rather than clinical oncology.

Guardant's data moat deserves particular emphasis. With millions of genomic profiles linked to clinical outcomes through the GuardantINFORM platform, the company possesses a proprietary dataset that grows more valuable with every test performed. This data advantage is the closest thing in diagnostics to the network effects that drive software platform value. A new competitor can replicate Guardant's sequencing technology — the core science is published — but replicating the dataset requires performing millions of tests over many years. Time is the ingredient that cannot be compressed.

Geographically, the U.S. regulatory pathway has been both an advantage and a constraint. FDA approval provides the strongest commercial moat in the world's largest healthcare market, but it delays international scaling. Japan's regulatory approval in 2022 and European CE-Marking have opened additional markets, but international revenue remains a small fraction of total sales. This is a deliberate trade-off: Guardant prioritized the domestic market where regulatory approval, payer coverage, and physician networks create the deepest competitive moat, accepting slower global scaling as the cost.

The company's decision to control the full vertical stack — from assay chemistry and bioinformatics to laboratory operations, sales, and payer contracting — reflects a belief that integration is essential in diagnostics. Unlike software platforms that can rely on third-party infrastructure, a clinical diagnostic company must guarantee quality, turnaround time, and regulatory compliance at every step. Guardant chose to own that entire chain rather than partner or outsource, accepting higher capital requirements in exchange for tighter quality control and faster iteration.

XIII. Porter's Five Forces Analysis

The liquid biopsy industry, viewed through Michael Porter's competitive framework, presents a fascinating picture of an industry that is simultaneously attractive and treacherous.

The overall assessment is that the liquid biopsy industry is moderately attractive — strong growth tailwinds and significant value creation potential, but intense competitive forces and meaningful buyer power that constrain pricing and require continuous evidence generation.

New entrants face substantial barriers, but not insurmountable ones. Clinical validation requirements — the need to run large prospective trials, publish in peer-reviewed journals, and secure FDA approval — create a time-to-market barrier that can stretch five to ten years. Regulatory expertise and payer relationships take years to develop. However, the underlying sequencing technology is increasingly commoditized, and venture capital continues to fund startups across the liquid biopsy space. The barriers are high enough to slow competitors but not high enough to prevent well-funded, well-managed new entrants from emerging.

Supplier power is moderate and concentrated in one critical dimension. Illumina dominates the sequencing instrument and reagent market, making it the single most important supplier for essentially every liquid biopsy company. While Guardant has an established relationship with Illumina — both founders are Illumina alumni — the concentration of sequencing supply in a single vendor creates strategic vulnerability. Talent is another constrained input: genomics scientists, bioinformaticians, and regulatory specialists are in high demand across the industry.

Buyer power is where the analysis gets most interesting. In liquid biopsy, "buyers" come in several forms, each with different leverage dynamics. Physicians make ordering decisions but do not pay — they are influenced by clinical evidence, guidelines, and workflow integration rather than price. Payers — Medicare, commercial insurers — hold significant pricing leverage and make coverage decisions that are existential for diagnostics companies. A single negative coverage decision can effectively shut a product out of a market. Pharmaceutical companies, as biopharma services customers, negotiate large contracts but are relationship-driven and value the unique capabilities that established platforms like Guardant offer.

Substitutes remain relevant despite liquid biopsy's advantages. Traditional tissue biopsy is still considered the gold standard in many clinical situations — when tissue is accessible, when comprehensive histological analysis is needed, or when liquid biopsy results are inconclusive. Imaging-based monitoring through CT and PET scans continues to play a role in treatment response assessment. And emerging modalities — circulating tumor cells, protein biomarkers, AI-enhanced imaging — could potentially disrupt liquid biopsy the way liquid biopsy has disrupted tissue testing.

Competitive rivalry is intense and likely to intensify. Multiple well-funded competitors are racing for FDA approvals, guideline inclusion, and payer coverage across both advanced cancer profiling and early detection. Price competition has already emerged in some segments, and the innovation cycle requires continuous improvement in sensitivity, specificity, and turnaround time. The dynamics in screening, in particular, may trend toward winner-take-most outcomes — once a test achieves guideline inclusion and broad payer coverage, switching costs and physician inertia create significant barriers for late entrants. The CRC screening market is particularly instructive: Shield, Cologuard, and colonoscopy are not perfect substitutes but compete for the same screening budget and physician mindshare. How the market segments between these options over the next five years will determine whether liquid biopsy screening becomes a multi-billion-dollar franchise or remains a niche offering for colonoscopy-averse patients.

XIV. Hamilton's Seven Powers Analysis

Hamilton Helmer's framework offers a more nuanced view of Guardant's competitive position than Porter's structural analysis, particularly because it distinguishes between different types of competitive advantage and their durability.

Helmer's framework identifies seven potential sources of durable competitive advantage. Applied to Guardant, the picture is nuanced — the company has developing strengths across multiple powers but has not yet locked in any single overwhelming advantage.

Scale economies are emerging but not yet dominant. Guardant's laboratory has significant fixed cost infrastructure — equipment, facility, quality systems, bioinformatics computing — that gets leveraged across growing test volumes. The margin improvement from sixty-three to sixty-six percent gross margins between 2024 and 2025 reflects this dynamic. But the variable cost component of each test limits the ultimate scale advantage compared to software businesses. The more interesting scale effect is computational: more data improves algorithms, which improves test performance, which is effectively a form of scale economy unique to data-intensive businesses.

Network effects are moderate today but represent perhaps Guardant's most important long-term advantage. The clinical data flywheel — more tests producing better algorithms producing improved performance attracting more physicians ordering more tests — creates a positive feedback loop that strengthens over time. Every Guardant360 test performed generates genomic and clinical data that feeds GuardantINFORM, which attracts biopharma partners, which funds companion diagnostic development, which drives guideline inclusion, which increases test ordering. This flywheel does not spin as fast as social network effects — clinical evidence accumulation takes years, not days — but it is durable because it is grounded in proprietary data that cannot be replicated without performing comparable test volumes.

Counter-positioning was strong in Guardant's early years. Traditional tissue biopsy incumbents — pathology labs, hospital systems — could not easily adopt liquid biopsy without cannibalizing their existing revenue streams. Foundation Medicine was tissue-first and had to invest separately in liquid capabilities. But this advantage has faded as most major players now offer or are developing liquid biopsy products. Guardant's early counter-positioning has been converted into a data and evidence lead rather than a structural competitive asymmetry.

Switching costs are moderate. Physicians integrate tests into their ordering workflows and develop familiarity with result interpretation, creating some stickiness. Payer contracting involves administrative effort to change approved tests. Pharmaceutical companies cannot easily switch companion diagnostics mid-trial. But these switching costs are not at the level of enterprise software — an oncologist can order a different liquid biopsy test with a phone call or a few clicks.

Branding is emerging but uneven. Among oncologists, Guardant360 has strong brand recognition as the pioneering liquid biopsy platform. Among the general public, awareness is limited — Exact Sciences has invested far more heavily in direct-to-consumer advertising for Cologuard. Shield's commercial launch, particularly the "Shield Across America" campaign and Quest Diagnostics partnership, represents Guardant's first serious effort at consumer-facing brand building.

Cornered resources are moderate. The proprietary database of millions of genomic profiles linked to clinical outcomes is the most defensible asset. The founding team's scientific credibility and industry relationships are valuable but not irreplaceable. The intellectual property portfolio — patents around liquid biopsy methodologies — provides some protection, as evidenced by the litigation against Foundation Medicine. But the core science of ctDNA detection is published academic knowledge, and sequencing technology is commoditized.

Process power may be Guardant's most underappreciated advantage — and for investors, often the hardest to evaluate from the outside. Running a CLIA-certified laboratory at scale, with consistent quality, rapid turnaround times, and robust specimen management, is operationally complex. Navigating FDA approval pathways — understanding what the agency needs, how to design registrational trials, how to manage the interactive review process — is a capability built over years. Payer engagement — the art of health economics evidence generation, coverage dossier development, and reimbursement negotiation — is similarly experiential. These process capabilities are not glamorous, but they are difficult to replicate quickly and they compound over time.

XV. Bull vs. Bear Case

The Bull Case

The most ambitious version of Guardant's future begins with Shield becoming standard of care for colorectal cancer screening. The addressable population is staggering: over fifty million Americans are in the eligible age range and due for CRC screening, and roughly sixty percent of them are not currently up to date. If Shield captures even a fraction of this population — say, the patients who currently refuse colonoscopy and stool-based testing — the revenue opportunity is measured in billions. At fourteen hundred and ninety-five dollars per test, five million annual tests would represent roughly seven and a half billion dollars in screening revenue alone. That is an extreme scenario, but it illustrates the magnitude of the addressable market.

Beyond CRC, the early detection portfolio offers additional multi-billion-dollar opportunities. LUNAR-1 for lung cancer screening targets a population currently screened with low-dose CT scans — another modality with significant compliance challenges. If Guardant can replicate the Shield playbook in lung cancer, breast cancer, and eventually multi-cancer detection, the total platform opportunity is enormous.

The data moat widens with every test performed. As the database grows, Guardant's algorithms improve, test performance gets better, clinical evidence strengthens, more guidelines include the tests, more physicians order them, and the flywheel accelerates. This is a compounding advantage that is extremely difficult for competitors to replicate without equivalent scale.

Payer coverage should expand as cost-effectiveness data accumulates. The argument that catching cancer at Stage I through a blood test is dramatically cheaper than treating Stage IV cancer is economically powerful. If preventive care economics prevail in reimbursement decisions, Shield and future screening products benefit from favorable coverage trends.

International expansion represents a two to three times multiplier on the domestic total addressable market. Regulatory approvals in Japan are already in hand, and European and Asian markets offer significant long-term growth potential.

The path to profitability becomes visible as revenue scale reaches breakeven levels. Gross margin improvement from scale, operating expense leverage as the commercial infrastructure matures, and the high fixed-cost, growing-volume dynamic of laboratory operations all point toward eventual profitability — likely within three to five years if revenue growth continues at current rates.

The Bear Case

The most concerning version of Guardant's future centers on competitive commoditization and adoption friction. If multiple blood-based CRC screening tests reach the market — Exact Sciences' own blood test, Freenome's SimpleScreen, and potentially others — price competition could erode margins before Guardant achieves the scale needed for profitability. Abbott's acquisition of Exact Sciences, in particular, brings a global distribution powerhouse into direct competition.

Clinical adoption may prove slower than the bull case assumes. Physician behavior change in healthcare is measured in decades, not quarters. Oncologists who have spent their careers relying on tissue biopsy may be slow to fully embrace liquid alternatives. Primary care physicians who refer patients for colonoscopy may be reluctant to substitute a blood test with lower per-test sensitivity. Guidelines inclusion helps, but guideline adoption is itself a gradual process.

Payer reimbursement could deteriorate under healthcare cost pressure. Medicare's fourteen hundred and ninety-five dollar reimbursement for Shield is based on early ADLT pricing; market-based pricing that takes effect in subsequent years could be lower. Commercial payers may resist covering a screening test that has lower sensitivity than established alternatives.

Technology leapfrogging is a persistent risk. AI-enhanced imaging, multi-modal biomarker approaches combining cfDNA with protein markers, and entirely new detection modalities could emerge that outperform current liquid biopsy technology. GRAIL's multi-cancer detection approach, if approved and broadly adopted, could shift the screening paradigm in ways that disadvantage single-cancer tests like Shield.

Capital intensity may persist longer than investors hope. The need for continuous R&D investment in new products, new clinical studies, and new regulatory submissions means that Guardant may not achieve the operating leverage expected from revenue growth alone. The company has never been profitable, with cumulative losses in the billions, and the timeline to profitability could extend further than current projections. Key person risk is also worth noting — the co-CEO structure with Eltoukhy and Talasaz has been stable since founding, but the company's strategy and execution are closely tied to their leadership. Any leadership transition would be closely scrutinized by investors and could create uncertainty during critical commercial scaling.

What to Watch: The Critical KPIs

For investors tracking Guardant's execution, three metrics matter above all others. First, Shield test volume growth — this is the single most important indicator of whether blood-based cancer screening is achieving the adoption trajectory that justifies the company's current valuation. The inflection from 6,400 tests in 2024 to 87,000 in 2025 is encouraging, but the trajectory through 2026 and beyond will determine whether Shield becomes a franchise or a niche product. Second, non-GAAP gross margin trajectory — the movement from sixty-three to sixty-six percent reflects operational leverage, and continued expansion toward the low seventies would indicate that scale economics are working. Third, Guardant360 clinical test volume growth — the oncology testing business is the cash flow engine that funds everything else, and sustained twenty-plus percent growth rates would indicate that the competitive position in advanced cancer profiling remains strong.

XVI. Lessons for Founders and Investors

Guardant Health's journey from Stanford research project to near-billion-dollar revenue company offers several instructive lessons that extend well beyond liquid biopsy. These lessons apply to any founder or investor trying to build at the intersection of deep science, complex regulation, and clinical adoption — a space where the rules of consumer technology simply do not apply.

The most important strategic lesson is the power of starting narrow. When Eltoukhy and Talasaz chose to focus on advanced cancer profiling rather than early detection in 2012, they were choosing the smaller immediate market but the faster path to clinical validation, physician adoption, and revenue. This decision — which seemed conservative relative to GRAIL's bold multi-cancer approach — proved strategically brilliant. By the time Shield was ready for its FDA filing, Guardant had a decade of clinical evidence, thousands of physician relationships, established payer coverage, and a profitable-unit-economics testing platform to fund the early detection expansion. GRAIL, despite raising over four billion dollars, is still pursuing its first FDA approval as of early 2026.

The lesson is not that smaller markets are always better — it is that clinical utility must be proven sequentially, not assumed in parallel. In healthcare, evidence is the product. A diagnostic test without clinical validation is just a science experiment. Guardant built the evidence base first, then expanded the ambition. This sequencing discipline — prove it works, prove payers will pay, prove doctors will order it, then expand — is the playbook that separates successful diagnostics companies from the many that fail with technically impressive products but no commercial traction.

Regulatory strategy as competitive moat is the second critical insight. Every FDA approval Guardant achieved — Guardant360 CDx, each companion diagnostic indication, Shield — created a barrier that competitors must spend years and hundreds of millions of dollars to match. The twenty-five CDx indications Guardant360 has accumulated represent not just product features but regulatory assets that lock in physician ordering patterns and payer coverage. This dynamic is unique to healthcare: in technology, competitive moats are typically built through network effects or switching costs. In diagnostics, they are built through clinical evidence and regulatory approvals.

The two-sided business model — clinical testing plus biopharma services — deserves study by any founder building in healthcare diagnostics. The biopharma revenue stream provides diversification against clinical testing reimbursement risk, funds R&D through partnership income rather than dilutive financing, and generates data that strengthens the clinical testing platform. Few diagnostics companies have successfully executed this dual-revenue strategy, and Guardant's ability to grow both sides simultaneously is a meaningful competitive differentiator. It also creates natural customer relationships with the pharmaceutical companies whose drugs depend on companion diagnostics — turning potential competitors or indifferent parties into partners with aligned commercial incentives.

Payer relationships deserve particular emphasis as a lesson. In American healthcare, building a diagnostic product without a reimbursement strategy is like building a car without an engine. Guardant's systematic approach — starting with Medicare coverage for NSCLC, expanding to all solid tumors, then building commercial payer coverage one contract at a time — was not glamorous work, but it was the work that translated clinical utility into revenue. Too many diagnostics companies develop brilliant tests and then discover that nobody will pay for them. Guardant understood from the beginning that payer coverage was not a post-launch activity — it was a core part of the product development strategy.

For investors, Guardant illustrates both the opportunity and the challenge of healthcare platform investing. The opportunity is enormous — cancer detection and treatment selection represent a multi-hundred-billion-dollar global market, and liquid biopsy addresses fundamental limitations of current approaches. But the timeline from founding to major commercial inflection was twelve years — from 2012 to Shield's FDA approval in 2024. Early investors needed the patience, capital reserves, and conviction to fund a company through that entire journey, including hundreds of millions of dollars in annual losses.

The capital requirements are also worth emphasizing. Guardant raised over five hundred and fifty million dollars before its IPO, then raised hundreds of millions more through the public markets, and has still not achieved profitability after more than thirteen years of operations. This is not unusual for transformative healthcare companies — Illumina, Exact Sciences, and Myriad all had extended periods of losses before achieving profitability — but it requires investors who understand the healthcare development cycle and can tolerate sustained cash burn.

The binary nature of healthcare inflections is perhaps the most important investor consideration. FDA approvals, Medicare coverage decisions, and NCCN guideline inclusions are step-function events that can dramatically change a company's value overnight. Shield's approval in July 2024, followed by Medicare ADLT pricing and NCCN inclusion in 2025, represents exactly this kind of cascading inflection. But the reverse is equally true — a regulatory setback, a negative coverage decision, or disappointing clinical data can destroy value just as quickly.