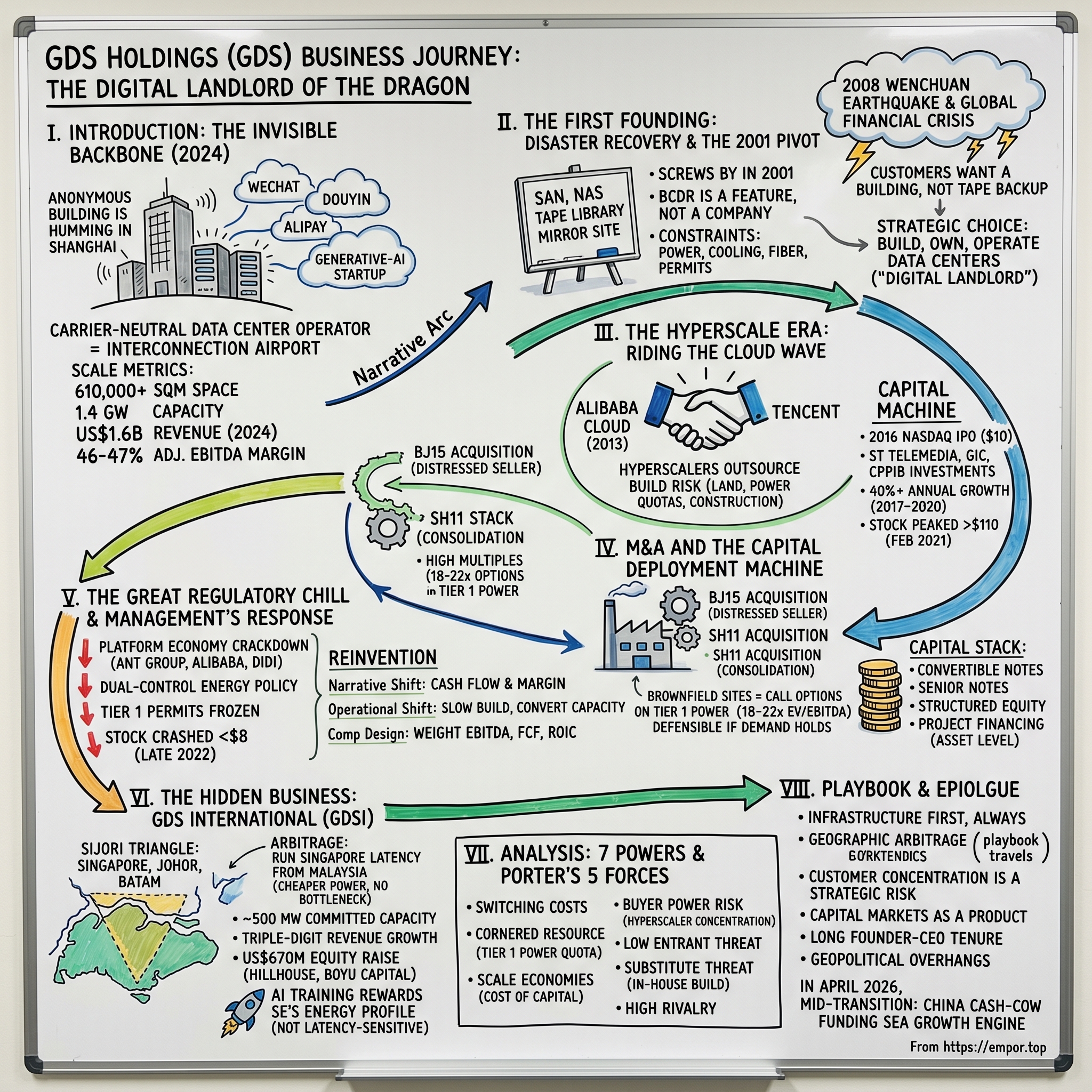

GDS Holdings: The Digital Landlord of the Dragon

I. Introduction: The Invisible Backbone (0:00 – 10:00)

Picture a humid summer evening in Shanghai in 2024. Somewhere in a drab industrial park in the Jiading district, behind a chain-link fence that reveals nothing of what lies within, a low concrete building hums with a sound that never stops. Not music, not conversation — a deep, almost mechanical exhale, the sound of air being moved through hundreds of thousands of cubic feet of aluminum ducting at precisely regulated temperatures. Inside the building, rows of black rack cabinets stretch out like library stacks, each one holding servers that blink in the dim blue glow of LED indicators. And on those servers sit the messages your friend in Shenzhen just sent on WeChat, the short-video your cousin in Chengdu just swiped past on Douyin, the Alipay transaction a stall-vendor in Guangzhou just confirmed, and the mid-journey inference request that a generative-AI startup in Hangzhou just fired into the cloud.

None of those acts of digital life happened "in the cloud." They happened here, in this anonymous concrete box, and in dozens more like it scattered across Beijing, Shanghai, Shenzhen, Hong Kong, Kuala Lumpur, Batam, and Johor. And behind nearly all of them sits one company most Chinese consumers have never heard of: GDS Holdings Limited.

GDS is the largest carrier-neutral data-center operator in China. "Carrier-neutral" is jargon for a simple, powerful idea: unlike a telecom operator that locks you into its own fiber and its own price card, GDS lets every carrier, every cloud, and every enterprise meet in a shared building. The analogy is less like a landlord renting apartments, and more like an airport — a place built for interconnection, where the more airlines (clouds, networks, enterprises) fly in and out, the more valuable the real estate becomes.

The scale of what GDS has built is easy to undersell. By the end of 2024, the company operated more than 610,000 square meters of data-center space with committed capacity approaching 1.4 gigawatts — enough electricity to run a mid-sized European city, delivered instead to silicon. Revenue cleared US$1.6 billion in fiscal 2024, with adjusted EBITDA margins around 46-47% — numbers that place GDS firmly in the world's top tier of digital-infrastructure operators.

And yet the story of GDS is anything but the tidy narrative of a "Chinese Equinix." This is a company founded in 2001 as a disaster-recovery shop that almost died in the dot-com bust, pivoted to data centers only after a literal earthquake shook its founder's worldview, listed on NASDAQ in 2016 at $10 a share, rode the hyperscaler boom to above $110 in early 2021, crashed back below $8 during the Chinese tech crackdown, and then — improbably — engineered a "second founding" in Southeast Asia through a carved-out subsidiary backed by Hillhouse and Boyu.

The narrative arc is what we love at Acquired: a founder-led company that has already reinvented itself twice, now attempting a third reinvention on an intercontinental scale. How GDS got from a single disaster-recovery site in Shanghai to a 50-megawatt AI training campus in Johor, and what that journey reveals about power quotas, capital stacks, and the geopolitics of compute — that is the episode we want to tell.

Let us begin where every great infrastructure company begins: not with a vision, but with a crisis.

II. The First Founding: Disaster Recovery & The 2001 Pivot (10:00 – 25:00)

In the spring of 2001, in a rented office on Zhongshan Road in Shanghai, a thirty-something engineer named Huang Wei — known later to Western investors simply as William Huang — was staring at a whiteboard full of arrows and acronyms that now read like artifacts from another technological age. SAN. NAS. Tape library. Mirror site. The dot-com crash had already shattered Silicon Valley a year earlier, and its shockwave was rolling through Pudong's newly-built office towers. Clients were disappearing. Budgets were frozen. And the company Huang had just founded, Global Data Solutions — later shortened to GDS — had chosen what seemed at the time a grimly unfashionable niche: business continuity and disaster recovery.

Disaster recovery in 2001 China was not the glamour business it would become. It meant showing up at a state-owned bank, surveying the single server room sitting above a basement parking garage, and gently explaining to the CIO that if a pipe burst, the whole branch went dark. It meant renting rack space in a secondary city so a primary site's data could be replicated there nightly on magnetic tape. It meant patient, unglamorous work with long sales cycles and customers who, frankly, did not believe disaster would actually strike.

Huang had come up through the IT systems-integration world. He was not a flashy tech founder in the mold of Jack Ma or Robin Li; colleagues who worked with him in that era describe him as methodical, relentlessly operational, and almost professorial in his preference for detail. He had studied in China, worked at IBM-aligned integrators, and his core insight was unromantic: Chinese enterprises had bought a decade of hardware but had not thought seriously about uptime. When everything worked, that looked like wisdom. When something broke, it looked like negligence.

For the first seven years, GDS scraped by. Revenue grew, but so did the awareness that BCDR alone was a feature, not a company. The real constraint on Chinese digital infrastructure was not software redundancy; it was physical: power, cooling, fiber, and permits.

Then, on the afternoon of May 12, 2008, the Wenchuan earthquake struck Sichuan Province with a magnitude of 7.9. Nearly 70,000 people lost their lives. Data centers in the affected region flickered off. Banks lost branch connectivity. For days, corporate China confronted a question most had treated as theoretical: what happens when the servers stop? That same autumn, Lehman Brothers collapsed in New York, and the global financial crisis arrived in China as a second shockwave — a reminder that catastrophic events, financial or tectonic, do not arrive on schedule.

For Huang, 2008 crystallized what had been forming for years. "Disaster recovery" as a service was too narrow. The deeper business was continuous operations. And continuous operations, at scale, required something no software vendor could provide: reliable, dense, redundant electricity, delivered into a hardened building with multiple fiber paths, 24-hour staffing, and the kind of physical security that banks and telecom ministries would actually certify.

In other words: GDS's customers did not want a tape backup. They wanted a building.

So Huang made what, in retrospect, was the defining strategic choice of his career. Rather than simply reselling capacity from state-owned telecom operators, GDS would build, own, and operate its own data centers. It would take on land leases, power contracts, construction risk, and the grinding political work of securing municipal permits. It would become, in a phrase Huang used internally, "the digital landlord."

From 2008 through 2010, GDS transitioned in stages. It kept the legacy BCDR business running for cash flow while quietly assembling a portfolio of small facilities — initially under 5 megawatts each — in Shanghai and Beijing. The pitch to customers evolved from "we will help you recover" to "we will host your entire production environment." And crucially, the company began to speak a different language to capital providers. This was no longer a software-services business with asset-light margins; it was a real-asset business with a long depreciation tail, one that would require enormous amounts of equity and debt to scale.

By the time the first wave of Chinese public-cloud buildouts arrived in the early 2010s, GDS was one of the only independent operators in the country with both operational pedigree and a credible land bank. That positioning — earned through a decade of unglamorous disaster-recovery work that almost no one today remembers — would prove to be worth billions.

The lesson in this chapter is one Acquired listeners will recognize. Great infrastructure companies are almost never founded as infrastructure companies. They begin as services firms, stumble into the physical bottleneck their customers cannot solve, and have the courage to rebuild themselves around it. GDS's first founding was not the data-center business. It was the patience that made the data-center business possible.

III. The Hyperscale Era: Riding the Cloud Wave (25:00 – 45:00)

The exact moment a Chinese infrastructure company stops being a services firm and becomes a capital-markets animal is usually possible to date. For GDS, a reasonable candidate is the afternoon in 2013 when Alibaba Cloud — then barely four years old and still a rounding error inside Jack Ma's empire — quietly signed a multi-site co-location agreement that would eventually anchor several of GDS's Shanghai and Beijing campuses. The dollar value was not disclosed. What mattered was the signal: China's emerging hyperscalers had decided they did not want to build every data center themselves.

To understand why this mattered, it helps to remember what Alibaba and Tencent looked like in 2013. Alibaba was preparing for its 2014 New York IPO and had not yet proven that Aliyun (Alibaba Cloud) could match AWS. Tencent was still primarily a gaming and social company, with WeChat only just transitioning from messaging app to national operating system. Both companies faced an identical problem: their consumer platforms were growing faster than their ability to deploy physical compute.

A hyperscaler's build decision is never purely economic. In the United States, Amazon, Google, and Microsoft chose to build most of their own data centers because they had cheap land, cheap power, permissive permitting, and an obsession with vertical integration. In China, the math was different. Land in Tier 1 cities was scarce. Power quotas were politically allocated. And — crucially — the hyperscalers were themselves consumer-facing companies that did not want to spend management bandwidth negotiating with municipal power bureaus in seven provinces.

This is the opening GDS walked through. Between roughly 2010 and 2014, the company transitioned from being one of many regional IT services vendors to being the "preferred partner" for cloud-scale deployments. The pattern was repeatable: a hyperscaler would commit to a large multi-megawatt order with a three-to-ten-year take-or-pay lease; GDS would underwrite a new build or a brownfield conversion against that commitment; lenders and equity investors would fund the gap.

What made the partnership sticky was not simply availability. It was Huang's willingness to absorb the ugliest parts of the business that his customers wanted nothing to do with. Negotiating with the State Grid. Securing Tier 1 city power quotas in an environment where Beijing and Shanghai periodically froze new data-center permits for environmental reasons. Managing the multi-year construction cycle from greenfield to commissioning, usually 18 to 24 months of risk that a cloud CFO preferred to outsource.

By 2015, the capital intensity of the business had become undeniable. A single 40-megawatt campus in Tier 1 China could cost US$300-400 million to build out, a number that rose as rack densities climbed. GDS was running faster than its balance sheet. The answer, once again, was reinvention — this time of the company's capital structure rather than its product.

On November 2, 2016, GDS Holdings listed on the NASDAQ under the ticker GDS at $10 per American Depositary Share, raising roughly US$193 million in primary proceeds. The pitch to American investors was clean and familiar: we are the Equinix of China. That analogy was useful shorthand but also, on inspection, imperfect. Equinix had built its empire on interconnection — the high-margin, low-capex business of letting networks meet inside its buildings. GDS was primarily a wholesale and retail hybrid, leaning heavier on power-and-space monetization than pure cross-connects. The economic profile was more akin to Digital Realty than Equinix, with margins that would live or die by scale and cost of capital.

The IPO did something else that was less often discussed but arguably more important. It opened a pipeline to global institutional capital. The first major strategic investor of this era was Singapore's ST Telemedia, a long-time data-center specialist that would over the coming years deepen its position and eventually become GDS's single largest shareholder. Behind ST Telemedia came the sovereign-wealth vehicles — Singapore's GIC and Canada's CPPIB — both of which would participate in convertible bonds and private placements across the late 2010s.

The result was a capital machine. Between 2017 and 2020, GDS's committed capacity grew at a compounded rate north of 40% annually. Revenue followed, rising from roughly RMB 1.6 billion in 2016 to over RMB 9 billion by 2021. The market rewarded the story generously: the stock traced an almost unbroken arc from the low teens in 2017 to an all-time high above $110 in February 2021, by which point GDS briefly carried an equity value near US$15 billion.

For investors, the story up to this point is the most familiar kind of hyperscale-era narrative: a second-tier services company that found itself sitting on top of a generational demand wave and rode it, with the aid of sophisticated capital partners and a founder who had learned, painfully and slowly, that the most durable businesses in tech are often the least glamorous. But by 2021, the ride was about to end, and a very different game — the game of capital discipline, regulatory risk, and corporate transformation — was about to begin.

IV. M&A and the Capital Deployment Machine (45:00 – 70:00)

Before getting to the crackdown, there is a chapter in GDS's history that does not get enough attention: the acquisition engine. Between roughly 2017 and 2021, while the company was simultaneously greenfield-building new Tier 1 campuses, it was also systematically buying brownfield sites and distressed competitors. This was not opportunistic; it was doctrinal. Huang and his CFO, Daniel Newman — an American by background who had joined GDS ahead of the IPO and who played Hamilton to Huang's Washington on capital markets — had internalized a specific view of the Chinese data-center land grab.

The view went something like this. In Tier 1 cities, greenfield power was becoming politically impossible to secure. Regulators were tightening environmental targets, and Beijing and Shanghai in particular were openly signaling that new data-center permits would be capped. At the same time, dozens of smaller, under-capitalized operators were sitting on sites that had been permitted years earlier but were underbuilt or poorly monetized. For a buyer with access to cheap equity and patient debt, these brownfield sites were effectively call options on Tier 1 power — options that would expire the day the permits stopped being issued.

Two deals capture the philosophy. The first was the BJ15 acquisition, where GDS purchased a partially-built Beijing data center from a distressed seller and completed the build-out under its own standards. The second was SH11, a Shanghai site where GDS consolidated adjacent parcels into a single high-density campus. The reported multiples on these deals, as pieced together from company filings and sell-side research, sat in the range of 18 to 22 times forward EV/EBITDA — high by Western data-center standards, which typically clustered in the mid-teens, but defensible under the view that Tier 1 China power was its own asset class with scarcity value that transcended short-term EBITDA.

Did GDS overpay? The honest answer is "it depends on what happens to demand." If Tier 1 China power turned out to be as permanently supply-constrained as Huang believed, then paying twenty times forward EBITDA for a site with an irreplaceable permit was a bargain. If, on the other hand, hyperscaler demand collapsed or migrated out of Tier 1 into cheaper Tier 2 cities, those multiples would look reckless. The comparable set of listed peers — notably 21Vianet (VNET) and Chindata (which later privatized under Bain Capital in 2023) — generally transacted at lower multiples, partly because they had weaker Tier 1 positions and partly because their customer mixes were less blue-chip.

The capital stack that funded all of this was, in its own way, the most impressive artifact of the Huang-Newman era. GDS learned to treat capital markets not as a back-office function but as a core product. In the United States, the company was a frequent issuer of convertible notes and senior notes. In Asia, it attracted structured equity from ST Telemedia, which in 2022 completed a roughly US$580 million investment through a combination of preferred shares and common stock to take its stake to the high-20s% range. GIC participated through a series of private placements. CPPIB anchored multiple convertible offerings. Onshore in China, GDS assembled a syndicate of domestic banks for RMB project financing, with each campus increasingly funded at the asset level rather than the HoldCo level — a subtle but important shift that insulated the parent balance sheet from any single site's underperformance.

The land grab accelerated in 2020 and early 2021, a period that in hindsight marked the peak of the Chinese hyperscale cycle. GDS doubled down on the two coastal mega-clusters: the Greater Bay Area anchored around Guangzhou and Shenzhen, and the Yangtze River Delta anchored around Shanghai and its satellite cities of Kunshan, Changshu, and Nantong. The logic was network-latency-driven. Cloud customers wanted campuses within a few milliseconds of the major fiber exchanges, which meant a tight geographic ring around each mega-city. By early 2022, GDS had assembled what was arguably the most concentrated high-quality Tier 1 power footprint of any independent operator in China.

But capital deployment at this intensity carries a specific risk: if the demand curve flattens, the company becomes simultaneously over-levered and over-supplied. In 2021 that risk was theoretical. By 2022 it was uncomfortably real.

The strategic takeaway from this chapter is worth stating carefully. GDS's M&A strategy was never primarily about synergy; it was about optionality. The company paid high multiples because it was not really buying current cash flows — it was buying the right to deploy capacity in a city where, a few years later, no one else would be allowed to build. That is a very specific kind of bet, closer in spirit to a midstream pipeline company securing rights-of-way than a traditional technology roll-up. Whether the bet would pay off depended entirely on what happened next in Beijing, Shanghai, and — most of all — the regulatory offices of Beijing's State Council.

V. The Great Regulatory Chill & Management's Response (70:00 – 90:00)

There is a specific variety of quiet that descends on a Chinese headquarters when Beijing's regulators decide a sector has grown too fast. It is not panic; panic would be inconvenient for state-owned partners and unhelpful in front of employees. It is, rather, a kind of measured stillness while everyone reads between the lines of the latest State Council statement. In late 2020 and through 2021, GDS's executive suite in Shanghai went through exactly that kind of quiet.

The trigger was the now-infamous crackdown on the "Platform Economy" that began with the cancellation of Ant Group's IPO in November 2020 and escalated through 2021 with an anti-monopoly probe into Alibaba, a fine of RMB 18.2 billion on Alibaba in April 2021, regulatory actions against Didi immediately after its New York listing in June 2021, and a broader tightening of data-security and cross-border-listing rules. For GDS, which derived a meaningful share of its revenue from the cloud businesses of Alibaba, Tencent, and Baidu — companies whose own capex plans were suddenly under review — the indirect effect was severe. Hyperscaler orders slowed. Lease commitments that had been signed on handshake terms faced renegotiation. Utilization ramps on new capacity stretched from the historical 12-to-18-month norm toward 24-to-30 months.

Simultaneously, Beijing tightened the physical constraints on the industry itself. The "dual-control" policy — a joint target for total energy consumption and energy intensity — landed on coastal provinces with real force. New data-center permits in Beijing and Shanghai became, as Huang had long predicted, effectively impossible to obtain. In principle this was good news for incumbents with existing permits. In practice it also signaled that regulators wanted demand to migrate inland, to places like Inner Mongolia, Guizhou, and Gansu, where renewable power was abundant but hyperscaler latency tolerance was not.

The stock market processed all of this with its usual lack of subtlety. GDS's ADRs, which had traded above $110 in February 2021, fell below $40 by the end of 2021, below $20 in the middle of 2022, and briefly touched single digits in late 2022. The peak-to-trough drawdown was over 90%. For a company that had been, months earlier, a consensus long for growth-oriented global infrastructure investors, the repricing was brutal.

It was in this period that the real character of GDS's management became visible. Under pressure, companies tend to either freeze or reinvent. GDS reinvented. The first visible change was narrative. Management shifted the external story from "capacity growth" to "cash flow and margin," a pivot that was initially met with skepticism from investors who remembered years of conference calls emphasizing committed area and pipeline.

The second change was operational. GDS slowed its new-build pace materially, deferred several speculative projects, and concentrated its effort on converting committed capacity into utilized capacity. For an asset-heavy operator, this is the difference between sinking capex into the ground and monetizing it; the financial leverage of ramping an existing campus from 50% to 90% utilization is enormous.

The third change — and the one that signaled the deepest cultural shift — was in compensation design. According to the company's proxy disclosures across 2022 and 2023, executive incentive plans were restructured to weight adjusted EBITDA margin, free cash flow, and return on invested capital more heavily, at the expense of pure capacity and revenue growth metrics. For a founder-led company that had spent a decade rewarding land-grab behavior, aligning pay with cash generation was a genuine philosophical adjustment.

Huang himself remained chairman and CEO throughout, and continued to hold a high-vote share structure that gave him super-majority control of board decisions despite owning a low-double-digit percentage of economic shares. This governance arrangement, common among founder-led US-listed Chinese companies, has obvious tradeoffs. It insulates long-term strategy from short-term pressure — useful when a company is pivoting through a crisis. It also concentrates risk if the founder misjudges. For GDS, at this moment of transition, the structure appeared to work: Huang was willing to accept short-term pain to protect long-term optionality, and the governance structure let him do so without a proxy fight.

Around Huang, the broader management bench also matured. Daniel Newman had transitioned earlier into a group-level capital-markets role before eventually stepping back from day-to-day operating responsibilities. A cadre of professional operators rose through the ranks with backgrounds more at home at global REITs and infrastructure funds than at a scrappy Chinese services company. The "professionalization of GDS," as one banker familiar with the company described it, meant transitioning away from the founder-led hustle of the 2010s and toward the structured, committee-driven discipline that institutional investors expected from a mature infrastructure asset.

By the end of 2023, the China business had stabilized. Utilization had resumed its climb. Hyperscaler demand had partially normalized, helped by the AI training wave that arrived in the second half of 2023 and reshaped the global compute conversation. But stabilization was not growth, and a company that had been priced for hypergrowth was now being priced for mid-single-digit top-line expansion in its core market.

Which left Huang with an uncomfortable question. If China's hyperscale era was maturing and if Tier 1 power was capped, where would the next ten years of growth come from? The answer, it turned out, had been quietly under construction for several years, on the other side of the South China Sea.

VI. The Hidden Business: GDS International (GDSI) (90:00 – 110:00)

Drive south from Singapore's Changi Airport toward the causeway that separates the city-state from Malaysia, cross into the state of Johor, and continue west through Nusajaya, past industrial estates and palm-oil plantations that are being cleared, one parcel at a time, to make room for fenced-off construction sites bristling with cranes. By early 2026, this stretch of land had become one of the most consequential pieces of digital real estate in Asia. And in the middle of it, on multiple parcels in Nusajaya and elsewhere in Johor, sat the campuses of GDS International — GDSI.

GDSI is, in many ways, the most interesting story in the GDS universe, and paradoxically the least visible. It was incorporated as a separate subsidiary in 2022 to house the company's non-China operations. Its strategic rationale was simple: if China's hyperscale market was maturing and Tier 1 power was a political asset, then the next wave of compute demand — particularly AI training — would have to land somewhere else. Southeast Asia, with its abundant land, comparatively cheap power, political neutrality between Washington and Beijing, and strong submarine fiber interconnection, was the obvious answer.

The geographic anchor of the GDSI bet was the so-called SIJORI triangle — Singapore, Johor (Malaysia), and Batam (Indonesia). Singapore was the longstanding hub, with unmatched connectivity but severe power and land constraints; the city-state had even imposed a formal moratorium on new data-center approvals between 2019 and 2022. Johor, just across the causeway, offered a dramatic arbitrage: customers could run the "Singapore latency story" from Malaysian soil, at a fraction of the power cost and without the permitting bottleneck. Batam, slightly farther afield in Indonesia's Riau Islands, offered even cheaper power and a supportive free-trade zone regime, though with higher political and execution risk.

GDS's move into this triangle was not unprecedented — regional players like STT GDC, Digital Realty, and Equinix had been operating in the area for years — but the scale and speed of GDSI's buildout stood out. By early 2026, GDSI had committed capacity approaching 500 megawatts across its Malaysian and Indonesian sites, a number comparable in order of magnitude to what had taken GDS a decade to assemble in China's Tier 1 cities.

The operational results were what caught investors' attention. While the China parent was reporting single-digit revenue growth in its core markets, GDSI was growing revenue triple-digits year-on-year off a small base, with signed lease commitments from global hyperscalers that had publicly articulated Southeast Asia as a strategic AI training region. In segment disclosures, GDSI's adjusted EBITDA margins were lower than China's — a typical pattern during ramp phases, when facilities are capitalized and staffed ahead of revenue — but the trajectory of those margins and the quality of the signed pipeline told a very different story from the one being told by the legacy China business.

Then, in 2024, came the deal that reframed the entire GDS narrative. In March 2024, GDSI announced a roughly US$587 million equity raise at the subsidiary level, bringing in a consortium led by Hillhouse Capital and Boyu Capital, with participation from other Asia-focused private-equity investors. Later in 2024, GDSI raised additional follow-on equity, taking the total capital raised at the subsidiary level to approximately US$670 million, with the consortium owning a significant minority stake and GDS Holdings retaining majority ownership and consolidation. This was a classic Acquired "hidden gem" structure: rather than issuing equity at the parent level — where the stock was still depressed and where every dollar raised diluted holders of the legacy China business — GDS created a discrete capital pool tied specifically to the fastest-growing part of the enterprise.

The financial engineering was elegant. By carving GDSI out as a separately capitalized subsidiary, GDS achieved three things simultaneously. First, it unlocked growth capital at a valuation that reflected GDSI's trajectory, not the parent's depressed multiple. Second, it sent a signal to the public market that sophisticated private investors were willing to underwrite the Southeast Asia story at a specific, implied valuation — a valuation that several sell-side analysts promptly used to reassess the sum-of-the-parts value of GDS's consolidated business. Third, it aligned an elite set of regional investors — Hillhouse and Boyu are not casual allocators — to the specific project of building Asia's next-generation AI infrastructure.

The AI tailwind is worth dwelling on, because it transforms the underlying economics of the GDSI thesis. Traditional cloud workloads — search, e-commerce, streaming — are latency-sensitive and therefore prefer data centers physically close to end users. AI training, in contrast, is not latency-sensitive; it is power- and cooling-sensitive. A training cluster running for weeks on thousands of GPUs cares more about reliable cheap electricity than about proximity to any particular city. This simple technical fact is why AI training workloads have gravitated, globally, toward regions with abundant power: the Pacific Northwest in the United States, the Nordic countries in Europe, and — for Asia-Pacific demand — Malaysia and Indonesia.

Put differently: the AI training era may be the first wave of digital demand that rewards Southeast Asia's geographical and energy profile rather than penalizing it. For a company that has spent a decade learning to build hyperscale campuses at speed in emerging-market jurisdictions, the configuration of market conditions in 2024 and 2025 was, if not quite a gift, then at least a rare alignment of prior investment and new demand.

Whether GDSI will ultimately grow into the valuation implied by its 2024 equity rounds remains the central question for any GDS investor today. But even skeptics concede that the pivot itself — from "China growth story" to "pan-Asian AI infrastructure story" — is no longer theoretical. The concrete is already being poured.

VII. Analysis: 7 Powers & Porter's 5 Forces (110:00 – 125:00)

Step back from the narrative and the question becomes analytical: what are the structural moats, if any, that GDS has built? Hamilton Helmer's "7 Powers" framework offers a useful lens, and at least three of its seven categories map cleanly onto GDS's business.

The first is switching costs. When a large bank or cloud provider installs thousands of racks in a GDS campus, the physical, contractual, and operational cost of moving out is enormous. Servers must be deracked, shipped, reracked, re-cabled, re-tested, and migrated without disrupting production workloads — a multi-year project that typically only happens during natural refresh cycles. Layered on top is the network topology: cross-connects to other tenants, carrier loops, and private-line circuits are all site-specific. In practice, once a hyperscaler has anchored a GDS campus, it tends to expand there rather than exit.

The second, and in the Chinese context probably the most distinctive, is what Helmer would call a cornered resource: the Tier 1 city power quota. In Shanghai and Beijing, the physical permit to consume tens of megawatts of grid electricity in a data center is effectively no longer issuable. A permit held by an existing operator, therefore, is not merely a piece of paper — it is a right that the market cannot manufacture more of. GDS's Tier 1 portfolio, assembled through a combination of greenfield builds during the permissive era and brownfield acquisitions during the tightening era, is the company's single most durable competitive asset.

The third is scale economies, most visible in the company's cost of capital. Data-center operators live and die by the spread between their weighted-average cost of capital and the unlevered yield on their campuses. At the scale GDS achieved by the early 2020s, it was able to tap domestic RMB project financing, offshore US dollar senior notes, convertible bonds, and structured equity from sovereigns — a diversity of capital that smaller competitors simply could not match. The direct consequence was a lower blended financing cost on new projects, which translated into more aggressive pricing to customers and still-acceptable project-level returns.

The four remaining Helmer powers — counter-positioning, network economies, branding, and process power — apply less convincingly. GDS is not meaningfully counter-positioned against anyone; its business model is essentially the same as Digital Realty's or Equinix's. Network economies exist modestly through interconnection but are not the core of the economic engine. Branding, in a business where customers sign multi-year leases based on audited power reliability rather than logos, matters only at the margin. Process power — the accumulated operational know-how of running hundreds of megawatts of critical infrastructure — is real, but it is more a form of organizational capital than a patentable moat.

Layering on Porter's five forces sharpens the picture further. The bargaining power of buyers is arguably GDS's single largest structural risk. A small number of hyperscalers — Alibaba, Tencent, ByteDance, Baidu, and the major US hyperscalers in the international business — account for an outsized share of revenue. The top five customers historically represented well over half of GDS China's revenue, with the two largest customers alone accounting for a substantial share. That concentration gave hyperscalers leverage in lease renewals, pricing discussions, and spec demands, particularly during the 2021-2023 crackdown when their own capex was being cut.

The threat of new entrants, by contrast, is low. Building a Tier 1 city data center in China requires capital that runs to hundreds of millions of dollars per campus, a multi-year permitting timeline, relationships with the State Grid and local power bureaus, and the operational capability to deliver five-nines uptime from day one. None of those barriers are easy to cross; collectively, they are prohibitive. Southeast Asia is somewhat more permissive on regulation but not on capital, and the land rush in Johor has already pushed permitting and power-contract timelines to the point where late entrants will find themselves years behind the incumbents.

The threat of substitutes is essentially the hyperscalers themselves building their own facilities. This is a real but bounded risk. As Alibaba Cloud and Tencent Cloud matured, they did build a portion of their own footprint; however, the capital intensity, execution risk, and opportunity cost of doing so at scale — in a country where land and power are politically allocated — kept a meaningful share of demand in the co-location channel.

The bargaining power of suppliers centers on power companies, construction contractors, and the equipment OEMs (generators, UPS, chillers, servers racks, fiber). In all three categories, GDS's scale provided meaningful leverage, though the overall power environment in China remained dictated by the grid rather than by commercial negotiation.

Finally, industry rivalry is genuine but tempered by the reality that demand has generally exceeded supply in the core coastal clusters. Competitors include 21Vianet (VNET), the privatized Chindata under Bain, Sinnet, Dr. Peng, and the in-house teams of the three state-owned telecoms. None of them have quite matched GDS's combination of Tier 1 concentration, hyperscaler relationships, and capital-markets access — though the gap, as always, can narrow if regulators' preferences shift.

Synthesizing across both frameworks, the picture is of a business with real moats in specific geographies — particularly Tier 1 China and, increasingly, the SIJORI triangle — paired with material risks in customer concentration and regulatory exposure. It is not a perfect franchise. It is, however, a franchise, and the number of companies on the Chinese internet landscape that can honestly claim that is small.

VIII. Playbook: Lessons for Founders & Investors (125:00 – 140:00)

Step out of the GDS-specific narrative for a moment and consider what the company's twenty-five-year arc teaches about building infrastructure businesses in any emerging market, in any era.

The first lesson is what might be called "infrastructure first, always." During every technology boom, attention naturally concentrates on the applications at the top of the stack — the messaging apps, the e-commerce platforms, the generative-AI models. Those are the businesses that appear on magazine covers. But beneath every successful application layer sits a physical and economic layer that is orders of magnitude harder to build and, once built, orders of magnitude harder to replace. The gold-rush metaphor is overused, but it still works: GDS did not mine for gold. It sold the electricity, the cooling, and the racks. And in doing so, it built a business less vulnerable to the rise and fall of any single application winner.

The second lesson is about geographic arbitrage. GDS's move into Southeast Asia was not a de novo experiment; it was the export of a playbook the company had already perfected in China. Secure land early, tie up power quotas before the political window closes, anchor with a hyperscaler commitment, underwrite construction against that commitment, layer on incremental demand as the campus ramps. The same template that had worked in Shanghai in 2012 was being replicated in Johor in 2024. The insight is that operational know-how travels. A team that has built, commissioned, and ramped fifty campuses knows things that no greenfield entrant can possibly know, and those things compound across jurisdictions.

The third lesson is darker and more important: customer concentration is a strategic risk, not a statistical one. For years, GDS's growth was celebrated partly because its customer base was dominated by Alibaba, Tencent, and the other Chinese hyperscalers — a "who's who" of the Chinese internet, the logic went, must be a quality signal. What that logic missed was that those customers moved as a cohort, and when their regulatory environment changed, GDS's revenue trajectory changed with them. In the depths of 2022, the same concentration that had been a badge of honor became the single largest factor depressing the equity. Founders building infrastructure businesses should take note: diversifying across customers who are not correlated in their regulatory or economic exposure is itself a form of risk management that is easy to undervalue during boom years.

The fourth lesson concerns capital markets as a product. One of the most distinctive features of GDS's history is the degree to which it treated financing as a first-class strategic activity rather than an administrative function. The company systematically cultivated relationships with sovereign-wealth funds, pension funds, and specialist infrastructure investors; it learned to issue convertibles, senior notes, RMB project debt, and carve-out equity; and it used that fluency to keep growth funded through a decade in which the required capex would have overwhelmed a less sophisticated operator. For founders in any asset-heavy industry — semiconductors, energy, biotech manufacturing — the template is worth studying. Financial sophistication is not a substitute for operational excellence, but it is a multiplier of it.

The fifth lesson, implicit in all of the above, is about founder-CEO tenure. William Huang has now been chief executive of GDS for a quarter-century. Through the dot-com bust, the BCDR grind, the hyperscale explosion, the regulatory crackdown, and the Southeast Asia pivot, he has remained at the helm, with a governance structure that gives him the latitude to make unpopular short-term decisions in service of a long-term vision. Long founder tenure is not an unmitigated good — it can ossify into stubbornness — but in an industry where a single campus can take five years from land acquisition to full ramp, the willingness to think across cycles is a non-trivial advantage.

The final lesson is a second-layer diligence aside that cannot be ignored in any sober assessment. GDS is a Chinese company with a US listing, material operations in China, and increasingly material operations outside China. The overhangs that attend to this structure — US-China delisting risk, PCAOB audit access, data-export restrictions, the evolving regime around VIEs and Cayman-incorporated holding companies — are real and are not resolved by narrative. For investors, these overhangs may be priced in, under-priced, or over-priced at any given moment; what they cannot be is ignored.

What should an investor in GDS actually track over the coming quarters? If the goal is to separate signal from noise, three KPIs matter more than all the others. The first is committed and utilized capacity, ideally tracked as a ratio. Commitments are easy; conversion to utilization is the economic moment that matters. The second is adjusted EBITDA margin by segment — specifically, watching the China business hold its margin as growth slows, and watching the GDSI business expand its margin as new campuses ramp. The third is leverage and cost of capital, because in an asset-heavy business, the spread between WACC and unlevered project yields is ultimately what drives equity value creation. Everything else, however entertaining, is a second-order effect.

IX. Epilogue & Final Reflections (140:00 – 145:00)

Where, then, does GDS stand on April 23, 2026? It stands as a company mid-transition, in a literal sense: still the largest carrier-neutral operator in China, still dependent on Alibaba and Tencent for a significant share of revenue, still navigating the slower-growth environment that followed the 2021-2023 reset. But it is also a company whose center of gravity is visibly shifting. GDSI has gone from rounding error to growth engine. Hillhouse and Boyu sit on the subsidiary's capital table. Johor and Batam campuses are ramping into signed hyperscaler commitments. The share price, which traded as low as the single digits in 2022, has recovered into the twenties through early 2026, reflecting a market that has begun to price in a more optimistic, if still cautious, view of the Southeast Asia strategy.

The myth-versus-reality moment worth pausing on is the original IPO framing. "We are the Equinix of China" made for a clean pitch in 2016, but it was never quite right. Equinix's economic engine is interconnection; GDS's is power-and-space at scale. A more accurate parallel might be Digital Realty with hyperscaler concentration — or, looking forward, something genuinely novel: a pan-Asian AI-infrastructure operator with a mature Chinese cash-cow business funding an emerging Southeast Asian growth business. The right analogy keeps shifting, which is itself a sign of a company still becoming what it will eventually be.

The bull case is reasonably clear. AI training demand will grow for years, the SIJORI triangle will be one of its primary global landing zones, GDSI's land and power positions are genuinely scarce, the parent's China business will grow slowly but profitably as utilization climbs, and the sum-of-the-parts valuation implied by the GDSI subsidiary round is meaningfully above the current enterprise value.

The bear case is equally clear and deserves equal weight. US-listed Chinese companies remain subject to geopolitical overhangs that can reprice the entire cohort overnight. Customer concentration, especially in China, has not gone away. The AI capex cycle may cool faster than anyone currently expects, and when it does, speculative capacity in Johor will look different than it does today. And leverage, while well-managed, remains substantial in absolute terms; in a higher-for-longer rate environment, the cost-of-capital advantage can erode.

Is GDS the next Equinix, or is it a high-leverage bet on a cooling cloud market? The honest answer, as with most interesting business stories, is probably neither and both. It is its own thing: a company built twice, attempting to be built a third time, by a founder who has been patient enough to survive two previous reinventions and is now asking investors to come along for the third.

Whether that third act will be remembered as a masterpiece or as a cautionary tale will, like everything in infrastructure, be answered slowly — one campus, one lease, one ramp at a time.

X. Reference & Further Reading

- GDS Holdings Limited, Form 20-F Annual Reports filed with the SEC (2016 through fiscal 2024).

- GDS Holdings press releases on the March 2024 and follow-on GDS International equity financings led by Hillhouse and Boyu Capital.

- Sell-side equity research on Chinese data centers, including notes from JPMorgan and Morgan Stanley covering GDS, VNET, and Chindata.

- ST Telemedia public disclosures and press materials on its investments in GDS Holdings, including the 2022 preferred-equity investment.

- Comparative analyses of Digital Realty, Equinix, and GDS Holdings published by infrastructure-focused research firms.

- Chinese regulatory publications on the "dual-control" energy policy and related guidance affecting data-center permitting in Beijing, Shanghai, and surrounding provinces.

- Bain Capital's 2023 take-private of Chindata Group and subsequent carve-out transactions, as background on comparable M&A activity in the sector.

- Public commentary and filings on the SIJORI triangle (Singapore, Johor, Batam) as an emerging Asia-Pacific data-center cluster, including the Singapore moratorium and its subsequent partial lifting.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube