Formula One Group: The Race to Build a Global Entertainment Empire

I. Introduction & Episode Roadmap

The roar of twenty cars hurtling past at 200 miles per hour creates a wall of sound that hits you physically—a chest-thumping, ear-splitting symphony of internal combustion that makes every other sport feel quiet by comparison. But here's what's remarkable: for decades, that visceral experience was limited to the few hundred thousand fans who could afford to stand trackside. The rest of the world? They got grainy television coverage, if they got anything at all.

Today, Formula 1 reaches 1.6 billion viewers globally, generates over $3.6 billion in annual revenue, and commands the attention of luxury brands from Louis Vuitton to Rolex. The transformation from European weekend hobby to global entertainment juggernaut is one of the most extraordinary business stories in sports—and at its center stands an unlikely architect: Bernie Ecclestone, an 80-year-old British used car dealer who built and controlled a multi-billion dollar empire for four decades through sheer force of will and commercial genius.

The numbers tell only part of the story. When Liberty Media acquired Formula One Group for $4.6 billion in January 2017, they weren't just buying a motorsport—they were acquiring a platform with tentacles reaching into media rights, luxury hospitality, digital streaming, gaming, and experiential entertainment. Under Liberty's stewardship, F1 has exploded from a declining European-centric property into Netflix's most successful sports documentary subject, America's fastest-growing sport, and the crown jewel of live entertainment programming.

How did a sport that began with gentleman racers competing for bragging rights evolve into a business that can command $31 million per race weekend from promoters? Why did John Malone's Liberty Media—a company known for complex financial engineering and cable assets—bet billions on racing cars? And what can the Formula 1 story teach us about building global entertainment properties in the streaming age?

This is the story of three distinct eras: Bernie's iron-fisted control that created the commercial foundation, private equity's attempt to extract maximum value, and Liberty Media's digital transformation that unlocked exponential growth. It's a masterclass in monopoly economics, platform dynamics, and the power of controlling distribution in the attention economy. From post-war European racing circuits to the Las Vegas Strip, from paddock politics to Netflix algorithms, this is how Formula 1 became the ultimate case study in turning niche content into global entertainment gold.

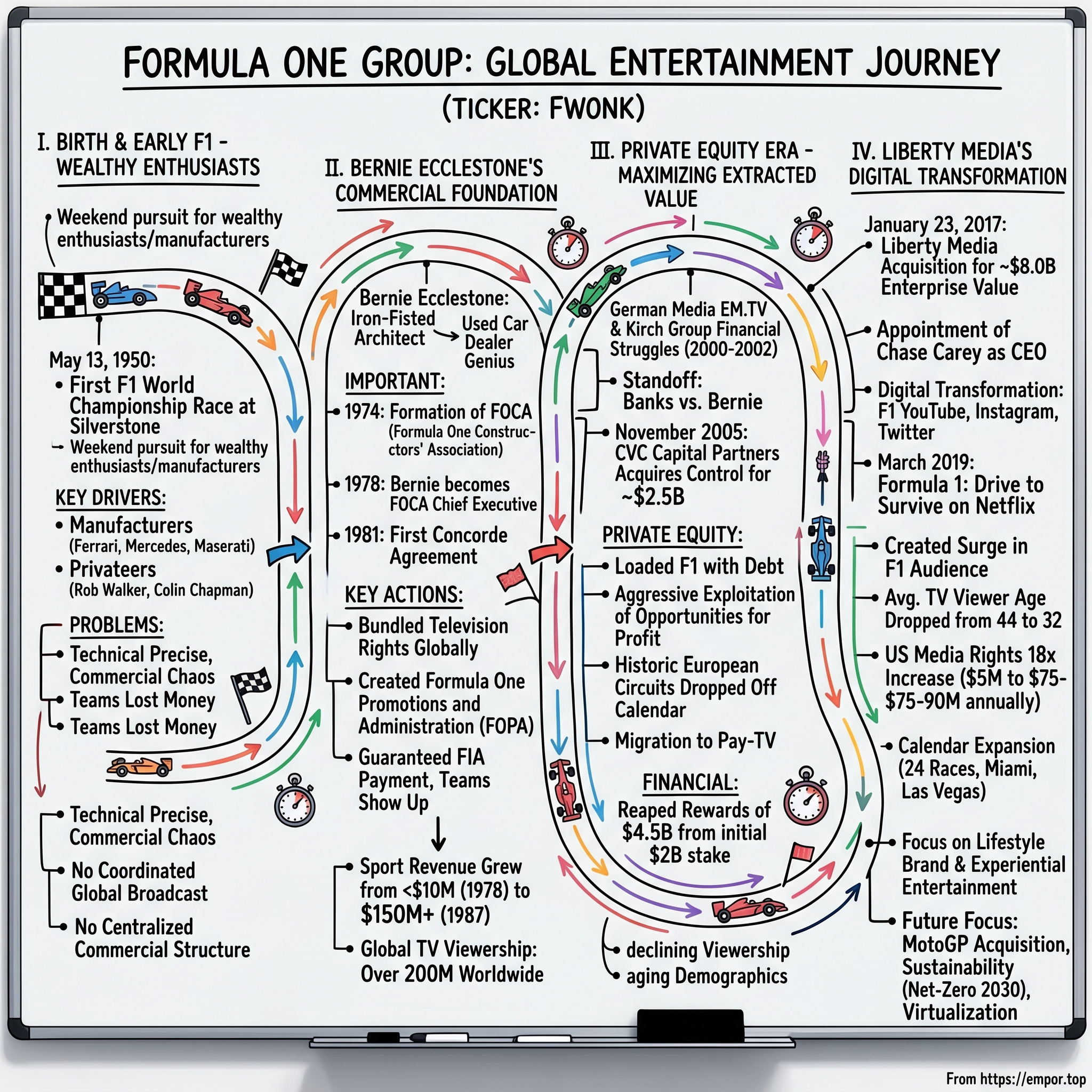

II. The Birth of Modern F1: Post-War Origins to the 1970s

The smell of Castrol oil and burnt rubber hung thick in the air at Silverstone on May 13, 1950, as King George VI watched twenty-one cars line up for the first-ever Formula One World Championship race. Giuseppe Farina would win that day in his Alfa Romeo, but nobody in attendance could have imagined they were witnessing the birth of what would become a $3.6 billion global entertainment empire. Formula 1 in 1950 was less a business than a weekend pursuit for wealthy enthusiasts and manufacturers eager to prove their engineering superiority on Sunday to sell cars on Monday.

The sport emerged from the ashes of World War II when the Fédération Internationale de l'Automobile (FIA) decided to create a world championship for the highest class of single-seater racing. The "formula" referred to the set of rules all participants had to follow—engine size, weight, dimensions. But while the technical regulations were precise, the commercial structure was chaos. Each race operated as an independent fiefdom, with local automobile clubs negotiating separate deals with teams, collecting gate receipts, and keeping most of the money. Television barely existed, sponsorship meant a local garage might provide free spark plugs, and most teams lost money with stunning consistency.

The early decades belonged to the manufacturers and the privateers. Ferrari, Mercedes-Benz, Maserati—these were prestige projects where racing budgets were marketing expenses, justified by the halo effect on road car sales. The privateers were even more quixotic: wealthy individuals like Rob Walker who funded teams as an expensive hobby, or genius engineers like Colin Chapman of Lotus who saw racing as a laboratory for innovation. The drivers themselves were a mix of playboy aristocrats and working-class daredevils, united only by their willingness to risk death for glory—and in the 1960s and early 1970s, death came frequently, claiming on average one driver per season.

By 1974, the teams had grown tired of being at the mercy of race organizers who kept most of the money while teams bore most of the costs. They formed the Formula One Constructors' Association (FOCA) to negotiate collectively. The organization needed someone to run it—someone who understood business, could negotiate hard, and wasn't afraid to take on the establishment. They found their man in perhaps the most unlikely candidate imaginable: Bernard Charles Ecclestone, a diminutive used car dealer from Suffolk who had purchased the Brabham team in 1972 more as a hobby than an investment.

Bernie, as everyone called him, had made his first fortune in motorcycle dealerships and property development. He stood barely 5'3" but possessed an outsized personality and a street fighter's instinct for leverage. His background in the used car trade had taught him that everything was negotiable, information was power, and the person who controlled the deal flow controlled the game. When he looked at Formula 1, he didn't see a sport—he saw a massively undermonetized asset with terrible management and no coherent commercial strategy.

The pre-Bernie era was characterized by staggering inefficiency. Consider the 1975 season: sixteen races across four continents, each negotiated separately by teams with local promoters. Some races paid starting money to top teams, others paid nothing. Television coverage was sporadic—the BBC might show the British Grand Prix, RAI would broadcast Monza, but there was no coordinated global broadcast. Sponsorship was limited to automotive suppliers and cigarette companies who treated F1 as a regulatory loophole for advertising. The total annual revenue flowing through the sport was estimated at less than $10 million, with most teams operating at significant losses subsidized by manufacturers or wealthy benefactors.

Bernie's initial involvement with FOCA was modest—helping to coordinate travel logistics and negotiate hotel rates. But he quickly recognized the fundamental flaw in F1's structure: the teams had the product everyone wanted to see, but the race organizers and the FIA controlled the commercial rights. It was as if the NFL teams showed up to play but the stadium owners kept all the television money. Bernie's genius was seeing that whoever controlled the commercial rights controlled the sport's destiny. The battle for those rights would define the next decade and transform Formula 1 from amateur hour into big business.

III. The Bernie Revolution: Building the Commercial Empire (1978–1987)

March 1, 1981, Paris. Inside a mahogany-paneled conference room at the FIA headquarters on Place de la Concorde, Bernie Ecclestone sat across from Jean-Marie Balestre, the autocratic president of the FIA. After three years of what the press called the "FISA-FOCA War"—a bitter struggle between the governing body and the teams over commercial control—they were finally ready to sign a peace treaty. The document on the table, known as the first Concorde Agreement, would fundamentally restructure Formula 1's economics. Bernie had won the war without firing a shot.

The conflict had begun in 1978 when Bernie became FOCA's chief executive and immediately went on the offensive. While Balestre and the FIA (through its sporting arm, FISA) wanted to maintain iron-fisted control over both sporting and commercial matters, Bernie argued that the teams—who provided the actual entertainment product—deserved a larger share of revenues and greater autonomy over commercial decisions. The war escalated to the point where FOCA threatened to create a breakaway "World Federation of Motor Sport" with its own championship. The 1980 Spanish Grand Prix saw FISA-aligned teams boycott while FOCA teams raced, creating a farcical situation that threatened to destroy the sport entirely.

Bernie's negotiating position was simple but powerful: without the teams, especially Ferrari and the British constructors, there was no show. The Concorde Agreement represented a revolutionary compromise—the FIA would retain sporting governance, but FOCA, through Bernie's newly created Formula One Promotions and Administration (FOPA), would gain control of television rights negotiation. In exchange, FOPA would guarantee the FIA an annual payment and ensure teams showed up to every race. It was a masterclass in deal-making: Bernie had effectively separated the commercial rights from the sporting rights, creating a structure that would enable him to build an empire.

The genius of Bernie's approach became clear immediately. Before 1981, each race organizer negotiated separately with local broadcasters, if they negotiated at all. Bernie's first move was to bundle all television rights globally under FOPA's control. Instead of sixteen separate negotiations for sixteen races, he offered broadcasters a single package: all races or nothing. The economics were transformative. A broadcaster that might pay $50,000 for their home Grand Prix would pay $500,000 for the entire season to avoid losing viewers to competitors who had the full package.

By 1987, Bernie had formalized this structure through the creation of Formula One Management (FOM) and Formula One Administration (FOA), companies that would handle television rights and race promotion respectively. The revenue split he negotiated was audacious: FOPA received 49% of television revenues, the teams collectively got 1%, and the FIA received 50%. Additionally, FOPA kept 100% of all race promotion fees—the amounts race organizers paid to host a Grand Prix. Bernie had essentially created a toll booth at the center of Formula 1, taking a cut of every dollar that flowed through the sport.

The transformation in revenues was staggering. Television rights that had generated perhaps $1 million globally in 1980 were worth $20 million by 1985 and would exceed $100 million by 1990. Bernie's approach to race promotion fees was equally aggressive. Monaco, which had historically paid nothing (arguing the teams should be grateful for the privilege of racing there), was forced to pay up or lose their race. New venues in Hungary, Portugal, and Japan paid millions for the prestige of hosting a Grand Prix. Bernie's famous negotiating style—showing up to meetings with a single piece of paper with a number written on it, take it or leave it—became legend.

But Bernie understood that controlling distribution was only valuable if you improved the product. He standardized the television production, creating a single "world feed" that all broadcasters would use, ensuring consistent quality whether you watched in London or Tokyo. He cleaned up the visual presentation, working with Paddy McNally's Allsport Management to create "themed advertising"—instead of chaotic local signage, trackside advertising was coordinated and sold as a global package to premium brands. The paddock, once a muddy field where mechanics worked under canvas tents, was transformed into the "Paddock Club," a luxury hospitality product that generated millions in additional revenue.

The numbers tell the story of Bernie's first decade in power. Total sport revenues grew from approximately $10 million in 1978 to over $150 million by 1987. Teams that had operated on shoestring budgets now had guaranteed income streams. Sponsors like Marlboro, Canon, and Benetton paid millions for global exposure. Television viewership expanded from a few million Europeans to over 200 million worldwide. Bernie had proven that Formula 1 could be more than a sport—it could be a global entertainment platform. But he was just getting started.

IV. The Consolidation Years: Rights, Power & Control (1987–2000)

November 19, 1995, should have been just another FIA General Assembly meeting in Monaco. Instead, it became the day Bernie Ecclestone pulled off one of the most audacious rights grabs in sports history. The FIA, under President Max Mosley—Bernie's former FOCA ally who had switched sides—voted to lease Formula 1's commercial rights to Bernie's Formula One Administration for fourteen years. The price? $360 million over the period, roughly $25 million per year for rights that were already generating ten times that amount. The racing teams, watching from the sidelines, couldn't believe what they were seeing. Bernie hadn't just captured the commercial rights; he'd stolen them in broad daylight.

The genius lay in the structure. Bernie had spent years cultivating relationships with FIA members, the various national automobile clubs who voted on major decisions. Most cared little about Formula 1—they were focused on local rallying, touring cars, or road safety initiatives. Bernie promised them guaranteed annual payments, funding for their local programs, and stability. For them, it was free money. For Bernie, it was the deal of the century. He now controlled F1's commercial rights through 2010, giving him the security to make long-term deals and investments.

But Bernie's masterstroke came in 2000, in a transaction so brazen it defied belief. With the original lease nearing its midpoint, Bernie negotiated a 110-year extension of the commercial rights, running until 2110. The price? A one-time payment of $313.7 million. Max Mosley and the FIA board approved it, arguing they needed the cash injection for safety improvements and development programs. The teams were apoplectic—Bernie had just purchased a century of rights for less than two years of revenue. When questioned about the deal's fairness, Bernie's response was characteristic: "If they didn't like the deal, they shouldn't have signed it."

The consolidation of power extended beyond just rights. Bernie systematically eliminated or co-opted every potential threat to his control. The circuit owners? He played them against each other, constantly threatening to move races to whoever would pay more. The teams? He perfected the divide-and-conquer strategy, secretly offering Ferrari additional payments (later revealed to be $100 million annually) to ensure they would never join a breakaway series. The television broadcasters? They needed F1 more than F1 needed any individual broadcaster, especially as Bernie expanded into new markets. The structure Bernie created in 1996 was particularly clever. SLEC Holdings was created as the holding company of the Formula One companies in 1996 when Ecclestone transferred his ownership of Formula One businesses to his wife, Slavica, in preparation for a 1997 flotation of the group. The name itself—SLEC, presumably standing for "Slavica Ecclestone"—was Bernie's inside joke on the financial world. This wasn't just tax planning; it was a strategic move to insulate the commercial rights from any potential legal challenges while maintaining absolute control through his wife.

The Paddock Club transformation exemplified Bernie's vision for F1 as luxury entertainment. What had been a muddy area where mechanics wrenched on cars became a five-star hospitality experience where CEOs could entertain clients while watching the race from air-conditioned suites. Prices started at $1,000 per person per day and could reach $5,000 for premium experiences. With 5,000 Paddock Club guests per race weekend across sixteen races, this alone generated $80 million annually by the late 1990s—pure margin, as the infrastructure costs were borne by the circuits.

In June 1999, the European Commission announced it would investigate the FIA, Formula One Administration (FOA) and International Sportsworld Communicators for abusing dominant position and restricting competition. ISC, owned by Ecclestone, had signed a 14-year agreement with the FIA in 1996 for the exclusive broadcasting rights for 18 FIA championships. The European authorities were catching on to Bernie's monopolistic structure, but he was already three steps ahead.

The financial engineering that followed was Byzantine in its complexity. In October 1999, Morgan Grenfell Private Equity (MGPE) acquired 12.5% of SLEC for £234 million. In February 2000, Hellman and Friedman purchased a 37.5% share of SLEC for £625 million, and combined its share with that of MGPE to form Speed Investments, which had a combined holding of 50% of SLEC. These private equity firms valued SLEC at nearly £2 billion, validating Bernie's empire building. But the real action was yet to come.

On June 28th 2000, in the offices of the FIA in Geneva, delegates from over 70 national motoring associations voted unanimously to approve a deal to grant the FIA's commercial rights to Formula One motor racing until December 31st 2110 to Bernie Ecclestone. The agreement, worth $360 million, was passed in complete secrecy, with no competitive bidding. Ecclestone was the sole candidate, ensuring his continued monopoly over F1's financial structure.

Think about the audacity: Bernie had just secured commercial rights for 110 years—longer than the sport had existed—for a one-time payment that represented less than two years of revenue. It was the deal of the millennium, literally. The FIA delegates who approved it got their local rallying programs funded; Bernie got a century-long monopoly on one of the world's most valuable sports properties.

By 2000, Bernie's empire was generating over $500 million in annual revenues. Television rights alone were worth $250 million globally, race promotion fees added another $150 million, and trackside advertising, hospitality, and merchandising contributed the rest. Bernie's various companies—through the deliberately opaque structure of offshore entities and family trusts—captured the vast majority of the economic value while the teams, who provided the actual racing, fought over scraps. It was monopoly capitalism at its most ruthless and effective. The consolidation was complete; now Bernie needed to monetize his kingdom.

V. The Private Equity Era: CVC Takes Control (2000–2016)

The champagne hadn't even gone flat from millennium celebrations when Bernie Ecclestone's carefully constructed empire began attracting the sharks of global finance. On 22 March 2000, German media company EM.TV & Merchandising purchased Speed Investments for £1.1 billion, acquiring the 50% stake that Morgan Grenfell and Hellman & Friedman had assembled. Thomas Haffa, EM.TV's CEO, was riding high on dot-com valuations and media convergence dreams. He lasted exactly eighteen months.

EM.TV's acquisitions caused it financial difficulties; following its announcement that its 2000 earnings would be below expectations and it was struggling with its debts, the share price dropped 90%. The company that had paid over a billion pounds for half of Formula 1 was suddenly worth less than what it had paid for the stake. Enter the Kirch Group, the German media conglomerate run by Leo Kirch, who sensed opportunity in distress. Kirch acquired EM.TV's stake and exercised an option to buy another 25% from Bernie's Bambino Holdings trust for $987.5 million, giving them 75% control of SLEC.

But Kirch had made a fatal error—he'd borrowed heavily to finance the acquisition. Due to huge losses and massive expenditure, Kirch's creditors put the company into receivership in 2002. Kirch's share of SLEC was retained by BayernLB, JPMorgan Chase and Lehman Brothers. Suddenly, three banks owned three-quarters of Formula 1, and they had no idea what to do with it.

Bernie's response was masterful in its cynicism. Ecclestone instituted changes in the boards of SLEC, FOH, FOA and Formula One Management (FOM); which in effect put Bambino Holdings in control of those companies. Despite owning only 25% of the equity, Bernie maintained iron-fisted operational control. When the banks sued in 2004, seeking to exercise their rights as majority shareholders, Bernie simply shrugged. He knew they needed him more than he needed them—without Bernie's relationships and knowledge, their 75% stake might be worthless if teams revolted or formed a breakaway series.

The standoff ended in November 2005 with the arrival of CVC Capital Partners, the London-based private equity firm that would define F1's next era. CVC Capital Partners announced it was to acquire the 25% and 48% shares of Bambino and BayernLB in SLEC, and acquired the shares of JPMorgan Chase in December 2005. This deal was given approval by the European Commission on 21 March 2006 and finalised on 28 March. Ecclestone used the proceeds of the sale of Bambino Holdings' share to reinvest in the company to give the Ecclestone family a 13.8% stake in the holding company Alpha Prema.

CVC paid approximately $2.5 billion for their controlling stake, but here's the brilliant twist: Bernie remained as CEO with his 13.8% stake, aligning him with CVC's financial engineering while maintaining his operational control. Donald Mackenzie, CVC's co-founder, understood that Bernie was the product—remove him, and you might destroy the value. It was private equity pragmatism at its finest. The numbers reveal the brutal efficiency of CVC's financial engineering. CVC Capital Partners, a then-mid-sized London-based firm, paid a steep $2 billion in 2006 to buy Formula One, but immediately loaded the company with debt. An eye-watering $230 million was required every year merely to pay the interest on the loan CVC had taken out to purchase the sport. This much was raised – and more – by aggressively exploiting opportunities for profit, regardless of any knock-on effects for the teams.

The Formula One Group planned an initial public offering on the Singapore Stock Exchange in June 2012, valuing the company at $10 billion. But the IPO never happened. Public market investors were spooked by the governance structure (Bernie at 81 still controlled everything), the massive debt load, and the constant threat of teams forming a breakaway series. Instead, CVC Capital Partners Ltd. said today it agreed to sell 21 percent of Formula One to BlackRock Inc. and two other investors for $1.6 billion as they gradually reduced their stake through secondary sales.

Under CVC's ownership, revenues did grow—Its original offer letter forecast $1.1 billion of revenue by 2013; the company actually did $1.6 billion—but this growth came at a cost. Race promotion fees were jacked up relentlessly. Historic European circuits like Hockenheim and the Nürburgring couldn't afford Bernie's demands and dropped off the calendar. New races in Azerbaijan, Russia, and India paid tens of millions for the privilege, regardless of whether fans actually showed up. Television rights migrated from free-to-air broadcasters to pay-TV platforms, shrinking the audience but maximizing short-term revenue.

The deputy team principal of Force India, Bob Fernley, accused CVC of "raping the sport" during the period of its involvement in Formula One. The accusation was hyperbolic but captured the frustration. Teams saw costs skyrocket while their share of revenues remained static. Small teams like Caterham, HRT, and Manor collapsed. The product on track suffered as field sizes shrank and competitive balance deteriorated. Global television viewership, which had peaked at over 600 million in 2008, declined steadily through the CVC years.

But from CVC's perspective, the investment was a home run. But they reaped the rewards, taking $4.5 billion out of the sport, an above-average return on that initial stake. Through a combination of dividend recapitalizations, management fees, and partial stake sales, CVC extracted more than twice their initial investment while still retaining control. Lifted by that investment, the overall fund returned 2.4x to investors, putting it in the top quartile among peers.

The irony of CVC's tenure was that they proved both the value and the vulnerability of Formula 1. They demonstrated that F1 could generate massive cash flows—revenues grew from under $1 billion to over $1.6 billion during their ownership. But they also showed the limits of pure financial engineering. By 2016, the sport faced existential challenges: declining viewership, aging demographics, team bankruptcies, and the constant specter of manufacturer withdrawal. With global viewing figures on the decline, it was something of a relief when CVC agreed to sell their stake in the sport to incoming group Liberty Media.

The transaction price represents an enterprise value for Formula One of $8.0 billion and an equity value of $4.4 billion when Liberty Media announced the acquisition in September 2016. CVC had quadrupled the enterprise value in a decade—a 15% annual return that would make any private equity firm proud. But they were selling to a very different kind of owner, one with a radically different vision for Formula 1's future. The vulture fund era was ending; the media platform era was about to begin.

VI. Liberty Media's Acquisition & Transformation (2016–Present)

January 23, 2017 marked a seismic shift in Formula 1 history. F1 has appointed Chase Carey as Chief Executive Officer of F1, in addition to his existing role as Chairman, and Bernie Ecclestone as Chairman Emeritus of F1. After forty years of iron-fisted control, Bernie Ecclestone was out as CEO—given the face-saving title of "Chairman Emeritus" but stripped of all operational power. The tiny used car dealer from Suffolk who had built a multi-billion dollar empire was finally dethroned at age 86, replaced by Chase Carey, a 6'4" American media executive with a handlebar mustache who looked like he'd stepped out of a Western movie.

The contrast couldn't have been starker. Bernie, who famously said "I don't do emails," ran F1 like a medieval fiefdom from handwritten notes and memory. Carey, the former president of 21st Century Fox and architect of DirecTV's growth, understood digital transformation, streaming platforms, and the power of data analytics. Where Bernie saw F1 as a European luxury product that occasionally visited other continents, Carey and Liberty Media saw an undermonetized global entertainment platform ripe for expansion.

The transaction price represents an enterprise value for F1 of $8.0 billion and an equity value of $4.4 billion, with The Selling Shareholders received a mix of consideration comprising: $3.05 billion in cash, approximately 56 million newly issued shares of LMCK and a $351 million exchangeable debt instrument. But the real story wasn't the price—it was the vision. John Malone, Liberty's legendary chairman known as the "Cable Cowboy," had built his fortune understanding one simple truth: content is king, but distribution is emperor. In F1, he saw content that could anchor a sports streaming service, drive carriage fees, and create a global advertising platform.

The changes came fast and dramatic. Within weeks of taking control, Liberty Media did something Bernie had resisted for decades: they embraced social media. F1's YouTube channel, which Bernie had kept deliberately barren (he believed giving away content for free devalued the product), suddenly exploded with race highlights, driver interviews, and behind-the-scenes content. Instagram and Twitter accounts that had been corporate and sterile became playful and engaging. The sport that had hidden behind paywalls was suddenly everywhere. But the masterstroke came in March 2019 with the premiere of "Formula 1: Drive to Survive" on Netflix. During its first days on the platform, Drive to Survive was 27th on the Netflix top series ranking for the week of March 4, 2019, and 24th the following week — capturing 1.1 million and 1.3 million Unique Viewers (UVs), respectively. The show, which gave unprecedented behind-the-scenes access to teams and drivers, transformed F1 from a sport into a soap opera. Suddenly, viewers who had never watched a race knew the personalities, the rivalries, the human drama behind the helmets.

The impact was seismic, particularly in America. The show is credited with creating a surge in the sport's audience and crucially, driven down the average age of Formula One TV viewers from 44 to 32. By May of 2023 the series had been watched by 6.8 million people. The breakdown of that audience showed the transformative effect. 26% of viewers had no real interest in F1, presumably before watching their first episode. 31% were aged between 18 and 29, while just under half of the viewership (46%) were women. Moreover, further research has uncovered that just over one in five F1 fans (22%) now cite Drive to Survive as the reason they have been turned onto the sport.

The business impact followed the audience growth. Viewership rose from slightly over 0.5 million in 2017 to 1.1 million in 2023 (slightly dipping from a peak of 1.2 million in 2022). This surge has had profound impact on F1's media rights value in the US, where ESPN paid around $5m annually prior to the 2023 season, whereas the latest 3-year deal from 2023–25 cost ESPN around $75–90m annually for the same rights, quite a noticeable jump. That's an 18x increase in media rights value in just six years—the kind of return that makes even Silicon Valley jealous.

Liberty's strategy went beyond just Netflix. They understood that F1 needed to become a lifestyle brand, not just a racing series. The calendar expanded aggressively—from 21 races in 2018 to 24 races planned for 2024. But these weren't just more of the same European circuits. Miami joined in 2022, turning race weekend into Art Basel with cars. Las Vegas arrived in 2023 with Liberty spending $500 million of their own money to build a permanent paddock facility and promote the race themselves—an unprecedented move that showed their commitment to the U.S. market. The financial transformation under Liberty has been nothing short of spectacular. Formula 1 had another fantastic year with double digit growth across all revenue streams in 2023, continuing a pattern of consistent growth since the acquisition. For the year ended December 31, 2024, these revenue streams comprised 29.3%, 32.8% and 18.6%, respectively, of total F1 revenue from race promotion, media rights, and sponsorship.

The numbers tell the story of transformation. Total revenue grew from $1.8 billion in 2018 to over $3.4 billion in 2024—nearly doubling in six years. But more importantly, the composition of revenue shifted. Digital revenues through F1 TV, barely existent under Bernie, became a meaningful contributor. Sponsorship revenue exploded as brands like Crypto.com, AWS, and DHL paid premium prices to reach F1's younger, wealthier, more global audience.

In January 2021, the group is run by Stefano Domenicali as president and chief executive officer, replacing Chase Carey who moved to a non-executive chairman role. Domenicali, the former Ferrari team principal, brought deep sport knowledge but maintained Liberty's growth trajectory. Under his leadership, F1 continued its aggressive expansion while also addressing long-standing issues like cost caps for teams (implemented in 2021 at $145 million) and sustainability initiatives targeting net-zero carbon by 2030.

The Las Vegas Grand Prix epitomized Liberty's ambition. Unlike traditional races where third-party promoters pay F1 a fee, Liberty invested over $500 million of its own capital to build permanent facilities and promote the race directly. The gamble paid off spectacularly—the 2023 inaugural race generated over $1.5 billion in economic impact for Las Vegas and became the most lucrative single race weekend in F1 history. The Las Vegas Grand Prix generated massive global buzz, and we look forward to delivering great racing, fan experiences and economic benefit to F1 and the local community for years to come.

By 2024, Liberty had fundamentally transformed Formula 1. What was once a European-centric, aging, declining sport had become a global entertainment phenomenon. Social media followers exceeded 100 million across platforms. Race attendance hit record levels with multiple sellouts. The average age of viewers dropped by over a decade. The sport that Bernie had hidden behind paywalls was now everywhere—on TikTok, YouTube, Netflix, and soon in Apple's $300 million Brad Pitt movie.

The irony is that Liberty succeeded by doing exactly what Bernie had resisted: giving the product away to build the audience, then monetizing that audience across multiple platforms. It was classic platform economics—build the network, create the community, then extract value from every interaction. Bernie's transactional worldview couldn't comprehend giving away content for free. Liberty understood that in the attention economy, audience is everything. Build the audience, and the money follows.

VII. The Modern Business Model: How F1 Makes Money

Standing trackside at Monaco, watching cars worth $15 million each scream past apartments where a parking space costs more than most people's homes, you understand Formula 1's business model: it's a machine designed to extract maximum value from every touchpoint of global wealth and aspiration. The genius isn't just in the execution—it's in the structure that Bernie built and Liberty perfected, where F1 captures value at every level while bearing minimal risk.

The numbers for 2024 paint a picture of remarkable financial engineering. Formula One's annual revenue rose for the fourth year running to US$3.65 billion in 2024. The majority of F1's revenue and is derived from race promotion revenue, media rights fees and sponsorship fees, and for 2024 these revenue streams comprised 29.3%, 32.8% and 18.6%, respectively, of the sport's total revenue. The remaining 19.3% comes from what F1 calls "Other Revenue"—hospitality, freight, licensing, and increasingly important digital services.

Let's break down each revenue stream to understand the economic moat:

Race Promotion Fees (29.3% of revenue, ~$1.07 billion)

This is Bernie's original masterstroke, now perfected. This fee must be paid for every single race hosted and is estimated to be between $15-50 million and upwards for prime time races like the Qatar Grand Prix towards the end of the season. But here's the beautiful part: promoters pay F1 upfront for the privilege of hosting a race, then bear all the local costs and risks. If they do not already have one, they must design and build a track typically costing upwards of $270 million, with yearly maintenance fees averaging $18.5 million.

The contract structure is particularly clever. Deals typically run 5-10 years with annual escalators of 5-10%. A race that starts at $30 million in year one might be paying $45 million by year ten. And if a promoter can't pay? There's a queue of cities—Madrid just signed for 2026, Saudi Arabia is building a new circuit, Rwanda wants in—desperate to join the calendar. It's a seller's market where F1 holds all the cards.

Media Rights (32.8% of revenue, ~$1.2 billion)

Media rights revenues also experienced growth, attributed to elevated fees from new and renewed contractual agreements, as well as sustained expansion in F1 TV subscriptions. The transformation here has been dramatic. Under Bernie, deals were often handshake agreements with local broadcasters. Today, F1 has sophisticated multi-year contracts with guaranteed minimums and performance escalators.

The U.S. market exemplifies the transformation. This surge has had profound impact on F1's media rights value in the US, where ESPN paid around $5m annually prior to the 2023 season, whereas the latest 3-year deal from 2023–25 cost ESPN around $75–90m annually for the same rights. That's not just growth—it's a complete revaluation of the asset.

F1 TV, the direct-to-consumer platform launched in 2018, represents the future. F1 TV subscribers grew 15 per cent last year, with the largest market being the US. Stefano Domenicali, president and chief executive of Formula One, revealed a new higher-priced premium tier will launch in 2025 "to target avid fans". This isn't just incremental revenue—it's F1 owning the relationship with its most valuable customers, gathering data, and controlling distribution.

Sponsorship (18.6% of revenue, ~$680 million)

The series is set to generate $677 million in 2025 from its sponsorship partnerships. Sponsorships have also grown by 46%, showing the sport's increasing commercial appeal to major brands. The sponsorship model has evolved from simple logo placement to integrated partnerships. Crypto.com reportedly pays $100 million annually. AWS provides the technical infrastructure for F1's data analytics in exchange for branding. Rolex doesn't just sponsor—they define F1's relationship with time itself.

Other Revenue (19.3% of revenue, ~$705 million)

These additional streams include premium hospitality experiences, such as the prestigious F1 Paddock Club, and revenues from ancillary racing series, merchandise sales, licensing agreements, and digital service offerings. The F1 Paddock Club is a flagship premium experience, offering fans unparalleled access to Formula 1's luxurious and exclusive side. This includes prime trackside viewing locations, gourmet dining, premium beverages, and unique behind-the-scenes interactions with drivers, teams, and key figures within the sport. While general ticket sales revenue predominantly benefits local race promoters, Formula 1 directly capitalises on these high-margin hospitality packages.

The Paddock Club is pure margin. Packages start at $5,000 per person per weekend and can exceed $10,000 for premium experiences. With roughly 5,000 Paddock Club guests per race across 24 races, that's $600 million in high-margin revenue. The beauty? F1 provides the brand and access; local promoters handle the execution.

The Concorde Agreement: The Secret Sauce

The real genius of F1's model lies in the Concorde Agreement, the secret contract that governs the sport's economics. Team payments increased in the full year and fourth quarter driven by the growth in F1 revenue and the associated impact on the calculation of the team payments, which are 100% variable under the 2021 Concorde Agreement.

As for the team payments, these are based on the constructors' standing in 2023, and distributed on a sliding scale. Consequently, according to our old friend Mat Coch at Speedcafe, this means £140m ($176m) for Red Bull, £131m ($165m) for Mercedes, £122m ($153m) for Ferrari and £113 ($142m) for McLaren, all of which are greater than the $135m (£107.3m) cost cap in 2024. Aston Martin received £103.9m ($130.7), Alpine £94.9m ($119m), Williams £87m ($109m), RB £78m ($98m), Sauber £69m ($86.8m) and Haas £60m ($75m).

Think about the elegance: teams receive roughly 50% of F1's profits, but it's distributed based on performance and historical importance (Ferrari gets a heritage bonus). This creates intense competition while ensuring teams remain dependent on F1 for survival. The cost cap, introduced in 2021, prevents spending wars while maintaining competitive balance. Teams can't leave because they'd lose hundreds of millions in annual payments. They can't revolt because they're divided by the payment structure. It's divide-and-conquer economics at its finest.

Why This Model is Genius

F1's model breaks every rule of traditional sports economics:

-

No Stadium Costs: Unlike NFL or Premier League teams, F1 owns no venues. Promoters pay for everything.

-

No Player Salaries: Teams pay drivers. F1 just pays teams a share of profits.

-

Global Inventory: 24 races across six continents means F1 can offer sponsors year-round global exposure.

-

Controlled Supply: The calendar is limited. The team grid is limited. Scarcity drives value.

-

Platform Economics: F1 is the platform. Teams, drivers, sponsors, promoters, and broadcasters are all customers paying for access.

The result is extraordinary margins. Operating income in 2024 approached $800 million on $3.65 billion in revenue—a 22% operating margin that would make most businesses envious. And because capital requirements are minimal (F1 doesn't build tracks or own teams), free cash flow conversion is exceptional. This isn't just a good business—it's one of the best business models in sports, maybe in all of entertainment.

VIII. Strategic Expansion & The Future

The roar of 1,000cc motorcycles at 220 miles per hour creates a different kind of symphony than Formula 1's high-pitched scream, but to Liberty Media's ears, it sounds exactly the same: opportunity. Liberty Media Corporation ("Liberty Media") (Nasdaq: FWONA, FWONK, LLYVA, LLYVK) and Dorna Sports, S.L. ("Dorna"), the exclusive commercial rights holder of the MotoGP™ World Championship ("MotoGP"), announced today that Liberty Media has completed its acquisition of Dorna. The €4.2 billion (US$4.9 billion) deal will see Formula owner Liberty Media take an 84 per cent stake in Dorna, with the remaining 16 per cent retained by MotoGP management.

The MotoGP acquisition, completed in July 2025 after receiving European Commission approval, represents Liberty's most audacious expansion yet. MotoGP is a highly attractive premium sports asset with incredible racing, a passionate fanbase and a strong cash flow profile. We believe the sport and brand have significant growth potential, which we will look to realize through deepening the connection with the core fan base and expanding to a wider global audience, said Derek Chang, Liberty Media's new CEO.

The strategic logic is compelling. MotoGP brings 22 races across 18 countries, reaching hundreds of millions of viewers globally. But unlike F1, which Liberty transformed from European niche to global phenomenon, MotoGP has remained under-monetized. Average race fees are roughly half of F1's. Media rights deals are fragmented. Digital presence is minimal. It's F1 in 2016 all over again—a diamond waiting to be polished.

But the real genius lies in the synergies. Following the acquisition, Liberty Media's Formula One Group is composed of its subsidiaries Formula 1, MotoGP and Quint, and other minority investments. Liberty now controls the two premier global motorsport properties. They can offer broadcasters and sponsors integrated packages—reach the luxury F1 audience and the younger, more diverse MotoGP fanbase in one deal. They can coordinate calendars to avoid conflicts and maximize venue utilization. They can share best practices in digital engagement, hospitality experiences, and race promotion. The Las Vegas Grand Prix exemplifies Liberty's transformation of F1 from sport to spectacle. The inaugural Las Vegas Grand Prix is projected to have an overall economic impact to the tune of almost $1.3 billion, though subsequent analysis showed Last year's race, won by Dutch star Max Verstappen, generated a net economic impact of $1.5 billion, making it the most lucrative event in the city's history. The race generated $77 million in state and local taxes. That is more tax revenue than any other event in the history of Las Vegas.

But Vegas represents more than just one lucrative race—it's Liberty's blueprint for F1's future. Unlike traditional promoter deals where F1 collects a fee and walks away, Liberty invested over $500 million building permanent facilities, including a 300,000-square-foot paddock complex that operates year-round as an event space. They control ticket sales, hospitality, and sponsorship directly, capturing value that traditionally went to promoters. It's vertical integration meets experiential entertainment.

The geographic expansion strategy is surgical. Three U.S. races (Austin, Miami, Las Vegas) tap into the world's largest sports market. Middle Eastern races (Saudi Arabia, Qatar, Abu Dhabi, Bahrain) bring sovereign wealth fund money—Saudi Arabia reportedly pays $55 million annually just for hosting rights. Asian expansion targets the next generation of luxury consumers. Each new market isn't just a race; it's a beachhead for merchandise, streaming subscriptions, and sponsor activation.

The Digital Revolution

Liberty understood what Bernie never could: in the 21st century, distribution is digital and attention is currency. F1 TV, launched in 2018, now operates in over 100 countries with millions of subscribers paying $80-100 annually for exclusive content, data analytics, and alternative commentary. It's not just incremental revenue—it's direct customer relationships, data collection, and the ability to bypass traditional broadcasters when contracts expire.

Social media transformation has been equally dramatic. F1's social following grew from 20 million in 2017 to over 100 million by 2024. TikTok videos of crashes and overtakes generate hundreds of millions of views. YouTube highlights reach audiences who never watch races. Each touchpoint is monetized through sponsorship integration, merchandise links, and streaming conversion.

The gaming strategy bridges virtual and reality. The official F1 game series sells millions of copies annually. F1 Esports has its own championship with real teams fielding virtual drivers. SimRacing converts gamers into fans into consumers. It's customer acquisition disguised as entertainment.

Sustainability as Strategy

F1's commitment to net-zero carbon by 2030 isn't just greenwashing—it's strategic positioning for long-term survival. With manufacturers like Mercedes, Audi, and soon Ford entering with sustainability mandates, F1 must evolve or risk losing its technical partners. The 2026 engine regulations mandating 100% sustainable fuels and increased electrical power aren't just rule changes—they're F1's hedge against an electric future that could make combustion racing obsolete.

The LVMH Deal: Luxury Redefined

The ten-year LVMH partnership announced for 2025, reportedly worth over $1 billion, represents F1's next evolution. It's not just replacing Rolex as timekeeper—it's integrating Louis Vuitton, Moët & Chandon, Tag Heuer, and other LVMH brands into F1's luxury ecosystem. Trophy cases by Louis Vuitton. Champagne by Moët. Hospitality by Belmond hotels. It's luxury lifestyle marketing at unprecedented scale.

Competition and Threats

F1's dominance isn't unchallenged. Formula E holds exclusive rights to fully-electric open-wheel racing until 2039, potentially positioning itself as the sustainable alternative. IndyCar provides cheaper, closer racing in the American market. Netflix and Amazon are creating their own sports properties rather than just licensing content. The constant threat of a breakaway series keeps F1 honest—teams know their value and aren't afraid to negotiate hard.

But Liberty's moat is formidable. The MotoGP acquisition creates a motorsport monopoly. The 100-year commercial rights deal runs until 2110. The Concorde Agreement locks teams in through 2025 with negotiations for extension already underway. Circuit contracts run 5-10 years with automatic escalators. Media deals are locked through 2029 in most major markets. Switching costs are enormous; competitive threats are manageable.

The China Question

China represents F1's biggest opportunity and challenge. A market of 1.4 billion people with growing wealth and insatiable appetite for luxury brands should be F1's goldmine. Yet the Chinese Grand Prix, while popular, hasn't delivered the commercial breakthrough. F1 is working on Chinese driver development programs, local sponsorship deals, and Weibo/WeChat integration. Cracking China could double F1's addressable market. Failing to crack it caps growth potential.

The strategic roadmap is clear: maximize revenue per race through direct promotion and premium experiences, expand the calendar strategically into high-value markets, build direct-to-consumer relationships through digital platforms, integrate sustainability to maintain manufacturer support, and leverage the motorsport monopoly for synergies. It's platform economics meets luxury branding meets global entertainment—a business model as precisely engineered as the cars themselves.

IX. Playbook: Business & Investing Lessons

Standing in the Monaco paddock at 2 AM, watching crews pack away millions of dollars of equipment while champagne still drips from the podium, you understand Formula 1's deepest truth: this isn't a sport that became a business—it's a business that uses sport as its medium. The lessons from F1's evolution from British hobbyist racing to global entertainment empire read like a masterclass in platform economics, monopoly construction, and value extraction. Every entrepreneur and investor should study this playbook.

Lesson 1: Control the Bottleneck, Control the Game

Bernie Ecclestone's genius wasn't in creating value—it was in positioning himself at the single point through which all value must flow. By controlling commercial rights, Bernie became the toll booth on the only road to F1. Teams needed him to get paid. Broadcasters needed him for content. Sponsors needed him for access. Promoters needed him for races. He controlled the bottleneck, so he controlled the game.

This is the YouTube model, the App Store model, the Amazon Marketplace model—become the indispensable intermediary. But Bernie did it with atoms, not bits, in an era before platform economics had a name. The lesson: identify the bottleneck in any industry and either control it or create it. The value flows to whoever controls passage.

Lesson 2: Bundle Rights, Unbundle Revenue

Pre-Bernie, F1 was sixteen separate products (races) sold sixteen separate ways. Bernie bundled them into one product (the championship) sold one way (through him). But here's the brilliance: while he bundled the rights, he unbundled the revenue streams. Television rights separate from sponsorship. Hospitality separate from ticketing. Licensing separate from media. Each revenue stream optimized independently but sold as part of the bundle.

It's the cable TV model inverted. Cable bundles channels to extract consumer surplus. Bernie bundled rights to extract producer surplus from every participant in the F1 ecosystem. The lesson: bundling creates leverage, unbundling creates optimization. Do both simultaneously.

Lesson 3: Make Your Suppliers Dependent, Not Employed

F1 doesn't employ drivers, own teams, or operate circuits. Yet all are completely dependent on F1 for survival. Teams spend hundreds of millions to compete for prize money they can't live without. Circuits invest hundreds of millions in infrastructure for races they must host. This isn't outsourcing—it's systemic dependency creation.

The Concorde Agreement is a masterpiece of aligned dependence. Teams get just enough money to survive but not enough to thrive independently. They're paid based on performance, creating internal competition that prevents collective action. Ferrari gets extra to ensure they never leave. It's divide-and-conquer economics perfected. The lesson: make your suppliers need you more than you need them, but never employ them directly.

Lesson 4: Scarcity Is a Strategy, Not a Constraint

F1 could run 30, 40, even 50 races per year. Demand exists. Promoters would pay. But F1 deliberately constrains supply to 24 races. Why? Scarcity drives value. Each race becomes an event, not a routine. Sponsors pay premiums for limited inventory. Broadcasters bid aggressively for exclusive content. Fans treat attendance as special, not ordinary.

Compare to NASCAR's 36-race schedule that dilutes each event's significance. Or tennis with tournaments every week that blur together. F1 understands that scarcity isn't just about supply and demand—it's about maintaining premium positioning. The lesson: sometimes the most profitable decision is to sell less, not more.

Lesson 5: Own the Customer Relationship

CVC's fatal flaw was treating F1 as a B2B business selling to broadcasters and promoters. Liberty understood F1 is a B2C business with B2B revenue streams. The shift to digital, social media engagement, F1 TV, and direct ticket sales for tent-pole races wasn't just modernization—it was disintermediation. Own the customer relationship and you own the future.

This is why F1 TV matters more than its revenue suggests. It's not competing with ESPN or Sky Sports—it's collecting data, building direct relationships, and creating optionality for when those contracts expire. The lesson: in the digital age, whoever owns the customer relationship owns the value chain.

Lesson 6: Capital-Light Scaling

F1 generates $3.6 billion in revenue with minimal capital investment. No stadiums to build. No players to pay. No content production costs (teams provide the show). The capital intensity comes from others—teams spend $150 million annually, circuits spend hundreds of millions on facilities, broadcasters pay for production. F1 just collects checks.

This is the genius of platform businesses: let others bear the capital costs while you capture the economics. It's Airbnb without owning hotels, Uber without owning cars, but with even better economics because F1 controls scarce rights rather than competing in commodity markets. The lesson: the best businesses scale revenue faster than capital requirements.

Lesson 7: Premium Positioning Prevents Commoditization

F1 never competes on price. Race fees only go up, never down. Media rights increase every cycle. Ticket prices rise regardless of demand. This isn't arrogance—it's strategic positioning. By maintaining premium pricing, F1 signals quality, attracts luxury brands, and self-selects for high-value customers.

When promoters threaten to leave over fees, F1 lets them go. Germany, France, Malaysia—all dropped when they wouldn't pay. The message is clear: F1 doesn't need any individual market. This pricing power comes from brand strength, but more importantly from network effects—the more premium the series, the more premium brands want association, creating a virtuous cycle. The lesson: once positioned as premium, never compete on price.

Lesson 8: Controversy Is Marketing

F1 thrives on controversy. Team rivalries, driver feuds, regulatory disputes, technical protests—each generates headlines, engagement, and attention. Liberty understands this better than Bernie did. "Drive to Survive" manufactures drama where none exists because drama drives engagement and engagement drives value.

The 2021 Abu Dhabi controversy—when race director decisions arguably determined the championship—generated more discussion and attention than any marketing campaign could buy. Rather than hide from controversy, F1 leans into it. The lesson: in the attention economy, controversy is more valuable than consensus.

Lesson 9: Global Product, Local Activation

F1 is globally standard but locally activated. The cars, rules, and format are identical worldwide, creating production efficiency and brand consistency. But each race is localized—Monaco trades on glamour, Silverstone on history, Singapore on spectacle, Vegas on excess. Local promoters handle cultural adaptation while F1 maintains global standards.

This is McDonald's model inverted—instead of local products in a global framework, it's a global product in local frameworks. The lesson: standardize what creates efficiency, localize what creates relevance.

Lesson 10: The Power of Patient Capital

Liberty's transformation of F1 took years and hundreds of millions in investment before paying off. Vegas lost money initially. F1 TV required massive upfront investment. Digital transformation meant cannibalizing existing revenues. But Liberty had patient capital and long-term vision—luxuries CVC's fund structure couldn't afford.

John Malone thinks in decades, not quarters. That patience allowed Liberty to invest in growth rather than just extract value. The lesson: transformational value creation requires patient capital. Financial engineering creates returns; strategic transformation creates empires.

The Meta-Lesson: Compound Moats

F1's true genius is how each advantage reinforces the others. Premium positioning attracts luxury sponsors which funds better experiences which attracts wealthy fans which justifies higher fees which maintains scarcity which reinforces premium positioning. It's a flywheel where each element strengthens the next.

The 100-year rights deal, the Concorde Agreement, the circuit contracts, the media rights—each is a moat. Together, they're insurmountable. Any competitor must overcome not just one advantage but the compounding effect of all advantages. The lesson: build moats that reinforce each other. The strongest businesses aren't built on one competitive advantage but on the multiplication of many.

These lessons apply far beyond F1. Whether building a startup, investing in public markets, or analyzing business models, the principles remain: control bottlenecks, create dependency, maintain scarcity, own relationships, scale without capital, position premium, embrace controversy, balance global and local, deploy patient capital, and compound advantages. F1 isn't just the pinnacle of motorsport—it's the pinnacle of business model engineering.

X. Analysis & Bear vs. Bull Case

The investment case for Formula One Group (FWONK) requires understanding not just what F1 has achieved but what remains possible. At a market capitalization approaching $20 billion, the question isn't whether F1 is a good business—it demonstrably is—but whether future returns justify current valuations. The answer depends on your timeframe, risk tolerance, and belief in Liberty Media's ability to execute against increasingly ambitious plans.

Bull Case: The Platform Thesis

The optimists see F1 as Netflix in 2015—a content platform just beginning to monetize its global reach. Revenue growth from $1.8B (2018) to $3.4B (2024) - 86% increase under Liberty proves the model works. But bulls argue we're only in the third inning.

Start with geographic expansion. F1 generates roughly $150 per capita annually in Monaco, $5 in the UK, $0.50 in the US, and $0.02 in China. Simply reaching UK-level penetration in the US would triple American revenues. Achieving 10% of Monaco's penetration globally would 10x the entire business. These aren't fantasies—they're math based on proven market acceptance.

The untapped markets (China, India, Africa) represent 3 billion potential fans. One race in Africa, two in India, three in China—each could generate $50 million in race fees, $100 million in sponsorship activation, and billions in merchandise and media rights over time. The addressable market is essentially infinite relative to current penetration.

Digital transformation is just beginning. F1 TV has single-digit million subscribers at $80-100 per year. Netflix has 280 million at similar prices. The NBA's League Pass has 30 million. F1's potential streaming audience, based on social media following and global viewership, could be 50-100 million subscribers. At $100 per year, that's $5-10 billion in high-margin recurring revenue—more than F1's entire current business.

Premium experiences remain under-monetized. The Paddock Club could double capacity and triple prices while maintaining exclusivity. Las Vegas proves F1 can capture 10x more value by promoting races directly. Miami, Austin, eventually London, Paris, Tokyo—each could be a Vegas-style tent-pole event generating $500 million+ annually.

Multiple expansion opportunities (gaming, betting, experiences) each represent billion-dollar markets. F1-branded gaming could rival FIFA or Madden. Sports betting on F1 remains nascent outside Europe. Experiential entertainment—F1 theme parks, driving experiences, branded hospitality—remains untapped. The brand extends far beyond the races.

The MotoGP synergies alone could be worth billions. Integrated media rights, coordinated calendars, shared technology, combined sponsorship packages—two plus two equals five when you control both properties. Cost savings from shared infrastructure and personnel are immediate. Revenue synergies from cross-selling and bundling are enormous.

Liberty's track record demands respect. They've already exceeded every growth target, transformed the fanbase, and built a digital platform. With Derek Chang as CEO and Chase Carey's continued involvement, execution capabilities remain strong. The bull case sees F1 reaching $10 billion in revenue by 2030, with 40%+ EBITDA margins and a $50+ billion valuation. That's 150% upside from current levels.

Bear Case: The Saturation Scenario

The skeptics see F1 as ESPN in 2020—a mature property facing structural headwinds. The growth story, while impressive, may be largely played out.

Start with calendar saturation. At 24 races, F1 is testing the limits of team endurance, fan attention, and logistical feasibility. Adding more races risks diluting each event's significance and overwhelming the audience. NASCAR's decline followed exactly this pattern—more races, less interest, declining value.

The Regulatory risks from FIA can't be ignored. The governing body could demand larger revenue shares, impose cost structures that hurt profitability, or make technical changes that reduce entertainment value. The constant threat of breakaway series, while manageable, requires perpetual concessions to teams that erode margins.

Team revolt possibilities remain real. The manufacturers—Mercedes, Ferrari, Audi, Ford—have leverage and know it. If they collectively demanded 75% of revenues instead of 50%, what could F1 do? The Concorde Agreement expires in 2025; negotiations could go badly. A breakaway series backed by manufacturers and Middle Eastern sovereign wealth would be existential.

Economic sensitivity of luxury/corporate spending is proven. In recessions, Paddock Club sales collapse, sponsors withdraw, and promoters default. F1 is selling $5,000 weekend experiences in a world facing inflation, inequality, and potential recession. The customer base is narrow and economically vulnerable.

Environmental concerns about global racing are mounting. Flying hundreds of tons of equipment to 24 locations annually is environmentally catastrophic. Gen Z, F1's growth demographic, increasingly values sustainability. The cognitive dissonance between F1's carbon footprint and its net-zero promises could alienate the next generation.

Viewership concentration risk is real. Despite headline growth, TV viewership in core European markets is declining. Older fans aren't being replaced fast enough. The US growth story, while real, starts from such a low base that even tripling would barely offset European declines.

The competitive landscape is intensifying. Netflix, Amazon, and Apple are creating their own sports content rather than licensing. Formula E owns electric racing. Esports offers similar thrills without environmental impact. Younger audiences have infinite entertainment options; F1 is competing for attention, not just sports viewership.

The valuation already prices in perfection. At 20x EBITDA, F1 trades at premium multiples to every other sports property. The stock has tripled since 2020. How much growth is already priced in? Bears see limited upside and significant downside if growth slows.

The Balanced View: Quality at a Price

The reality likely lies between extremes. F1 is unquestionably a phenomenal business with significant growth potential. The brand is stronger than ever, the fanbase is growing and diversifying, and Liberty has proven exceptional at value creation. The MotoGP acquisition adds optionality. The business model's resilience is proven.

But the valuation reflects these positives. At current prices, investors need everything to go right—continued growth, successful expansion, no regulatory issues, no economic downturn, no competitive threats. The risk/reward is balanced at best.

For long-term investors, F1 represents a high-quality compounder with defensive characteristics and growth optionality. The business will likely be significantly larger in 10 years. But for value investors, the entry point matters, and today's prices offer limited margin of safety.

The key variables to watch: - 2025 Concorde Agreement negotiations - China/India expansion success - F1 TV subscriber growth - MotoGP integration execution - Economic resilience in downturn - Sustainability of US growth - New manufacturer entrance/exit

F1 isn't a binary bet—it's a complex organism with multiple growth drivers and risk factors. The bull case is compelling but priced in. The bear case has merit but underestimates Liberty's execution. The truth is that F1 is a wonderful business at a fair price, which historically has been a recipe for market returns, not market-beating returns.

XI. Epilogue & "If We Were CEOs"

If we were running Formula One Group, the path forward would balance aggressive expansion with existential risk management. F1 sits at an inflection point where the decisions made in the next 24 months will determine whether it becomes a $50 billion sports-entertainment platform or remains a $20 billion niche motorsport. The strategy isn't about choosing growth or stability—it's about sequencing moves to compound advantages while minimizing downside.

Priority 1: Lock in the Concorde Agreement Through 2035

The 2025 Concorde negotiations are existential. We'd open with a radical proposal: guarantee teams 60% of revenues (up from 50%) in exchange for a 10-year commitment with no break clauses and severe financial penalties for departure. Yes, it's dilutive short-term, but it eliminates the breakaway threat and provides a decade of stability to execute growth plans. Certainty is worth 10 points of margin.

Priority 2: The China-India Acceleration

These markets represent 2.8 billion people and the future of global consumption. We'd commit $1 billion over five years to crack these markets: build permanent facilities in Shanghai and Mumbai, create local driver development programs, sign local sponsors, produce local-language content, and potentially offer races at below-market fees initially. The playbook that worked in the US—invest heavily, build awareness, monetize later—applies here but requires 10x the commitment.

Priority 3: Solve the Sustainability Paradox

F1's carbon footprint is indefensible in a climate-conscious world. We'd accelerate the transition to sustainable fuels, but more radically, we'd regionalize the calendar to minimize transport. Three consecutive races in Asia, three in the Americas, six in Europe, three in the Middle East. Teams base equipment regionally. It's logistically complex but environmentally necessary and actually reduces costs long-term.

Priority 4: F1 Studios and Content Ownership

Liberty doesn't own "Drive to Survive"—Netflix does. That's billions in value creation F1 didn't capture. We'd build F1 Studios to produce and own all content: documentaries, films, series, games. Every piece of content would be owned IP that drives fans to F1 platforms. Think Marvel Studios but for motorsport—an integrated content universe where every product reinforces the core.

Priority 5: The Vegas Model Everywhere

Las Vegas proved F1 can 10x revenue by promoting races directly. We'd gradually transition to self-promotion in major markets. Buy the circuits if necessary. The capital investment pays back in 3-5 years and transforms economics permanently. Singapore, Monaco, London—each could be a billion-dollar weekend under direct control.

The Next Frontier: Virtual and Autonomous

The biggest opportunity—and threat—is virtualization. Esports and sim racing will eventually rival physical racing. We'd lean into this rather than resist. Create F1 Virtual as a parallel championship with real teams fielding virtual drivers. The races happen in photorealistic digital twins of real circuits. Fans can compete in amateur leagues. It's infinitely scalable, environmentally sustainable, and accessible globally. The physical and digital championships reinforce each other.

Simultaneously, we'd prepare for autonomous racing. It's coming whether F1 likes it or not. Better to control it than be disrupted by it. Launch F1 Autonomous as a technology showcase—same teams, same circuits, but AI drivers. It's the ultimate engineering challenge and attracts technology sponsors like Google, Amazon, and Tesla who currently ignore F1.

Key Lessons for Building Global Entertainment Properties

F1's journey from British weekend hobby to global entertainment platform offers timeless lessons:

Control trumps ownership. Bernie never owned F1 but controlled it completely. Focus on controlling what matters—rights, relationships, bottlenecks—rather than owning everything.

Scarcity creates value. In an abundant world, engineered scarcity is the only sustainable differentiation. Limit supply, increase demand, capture surplus.

Global scale, local relevance. Build products that work everywhere but feel native nowhere. Let local partners handle cultural translation while maintaining global standards.

Controversy drives engagement. Safe is boring. Conflict creates narrative. Narrative drives attention. Attention drives value. Embrace productive controversy.

Compound advantages systematically. Each decision should strengthen multiple moats simultaneously. Isolated advantages are temporary; interconnected advantages are permanent.

The Sustainability Challenge and Electric Future

The elephant in the room is electrification. Formula E owns exclusive rights to electric open-wheel racing until 2039. F1 is locked into combustion technology that increasingly looks anachronistic. The sustainable fuels solution is a bridge, not a destination.

We'd negotiate to merge with or acquire Formula E before 2039. The technologies will converge anyway—F1's 2026 regulations are already 50% electric. Better to control the transition than be displaced by it. Formula 1 becomes the pinnacle of racing regardless of power source, with different categories for different technologies. It's not about combustion versus electric—it's about being the premier platform for motorsport entertainment.

Biggest Surprises from the Research

Three things stand out:

First, the sheer audacity of Bernie's commercial rights grab. Acquiring 110-year rights for $313 million is possibly the greatest deal in sports history. It's like buying Manhattan for beads, except Bernie knew exactly what he was doing.

Second, how little value the teams capture despite providing the entire show. They spend billions collectively to receive millions individually. It's economically irrational yet continues because of competitive dynamics and sunk costs. The psychological manipulation required to maintain this is masterful.

Third, Liberty's execution has exceeded every expectation. Doubling revenues in six years while transforming the fanbase and building digital platforms—it's a masterclass in value creation that MBA programs will study for decades.

What Would We Do Differently?

We'd be more aggressive on digital transformation. F1 TV should have 50 million subscribers by now. We'd make races free on YouTube with premium features behind paywall. Volume first, monetization second—the Netflix model, not the cable model.

We'd radically democratize access. Ninety percent of people will never attend a race. Build F1 Experience Centers in major cities—simulators, museums, restaurants, merchandise. Make F1 accessible without traveling to races. It's Disney's theme park model applied to motorsport.

We'd embrace gambling fully. Sports betting transforms passive viewing into active participation. Partner with DraftKings or FanDuel. Create F1-specific betting products. In-race micro-betting on overtakes, pit stops, fastest laps. It's controversial but doubles engagement and creates new revenue streams.

Most importantly, we'd prepare for disruption rather than defending against it. The future of motorsport might be virtual, autonomous, or something we can't imagine. The goal isn't to preserve F1 as it exists but to ensure that whatever motorsport becomes, we control it.

Formula 1's story isn't finished—arguably, it's just beginning. The transformation from Bernie's analog empire to Liberty's digital platform sets the stage for whatever comes next. Whether that's a $50 billion global entertainment platform or disruption by technologies we haven't imagined depends on decisions being made right now in boardrooms from London to Las Vegas to Shanghai.

The race, as they say in F1, is long from over. And unlike the championship, where there's only one winner, in business, the race never really ends—it just enters the next lap. The question for investors, operators, and fans isn't whether F1 will cross the finish line, but how fast it's traveling when it gets there.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube