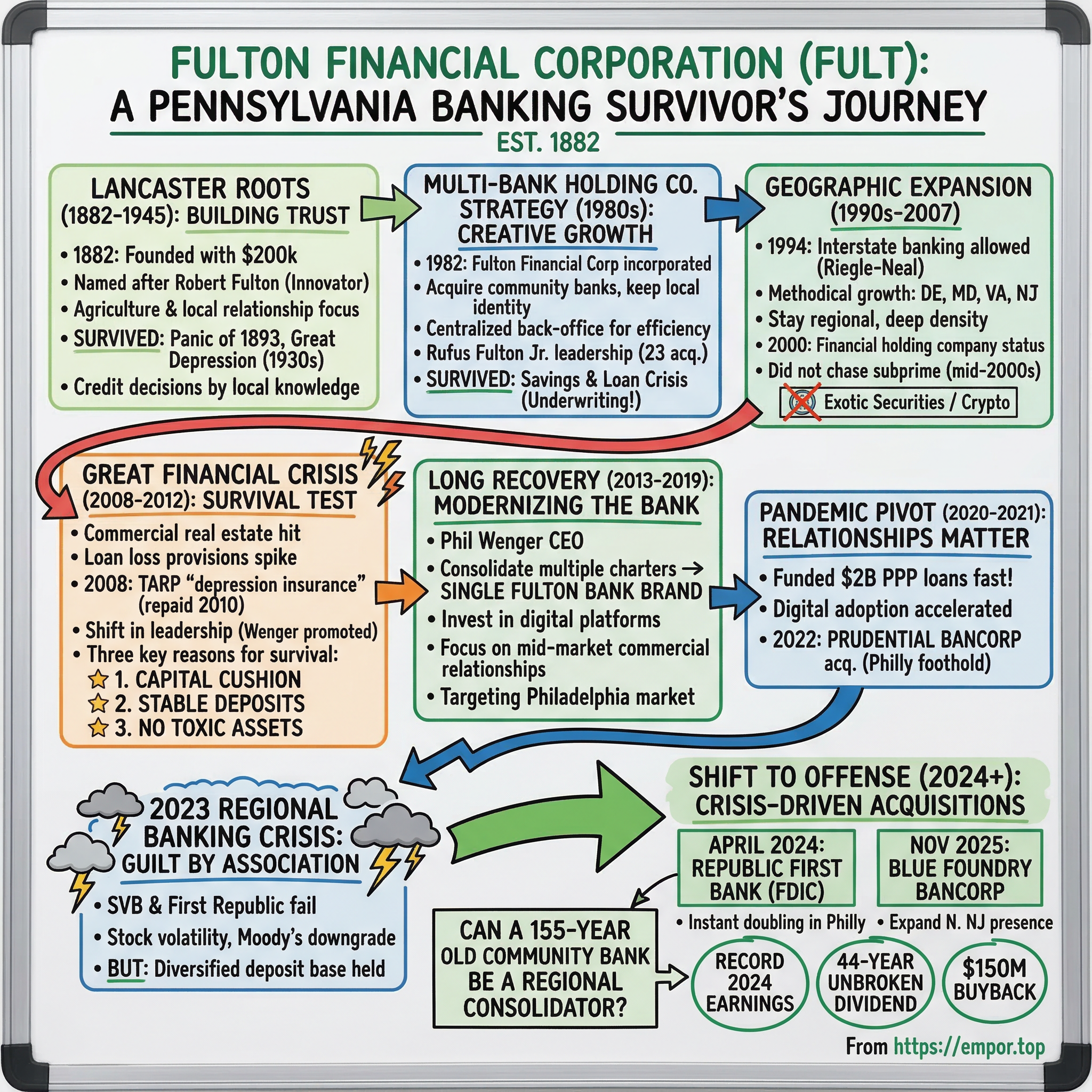

Fulton Financial Corporation: The Story of a Pennsylvania Banking Survivor

The Lancaster Roots: Building a Bank on Trust (1882-1945)

Picture Lancaster, Pennsylvania, in the early 1880s. The Civil War had ended less than two decades earlier. The National Banking Acts of 1863 and 1864 had created a new framework for chartered banks, and small towns across America were seizing the opportunity. Lancaster County was prosperous but provincial: rich agricultural land farmed by German-speaking communities, a handful of small manufacturers, and a population that valued thrift, hard work, and personal relationships above all else. The county seat of Lancaster had been briefly the capital of the United States during the Revolutionary War, and its residents carried a quiet pride in their role in the nation's founding. This was not a place that chased trends. This was a place that built things to last.

Into this environment, a group of local merchants and farmers organized Fulton National Bank in 1882, pooling two hundred thousand dollars in initial capital. They named their institution not after a founding family but after Robert Fulton, the Lancaster County native best remembered for designing the first commercially successful steamboat, the Clermont. It was a nod to innovation, to the idea that practical engineering could transform how people moved through the world. Whether the founders appreciated the irony of naming a conservative farm-country bank after a disruptive inventor is lost to history, but the tension between tradition and adaptation would define the institution for the next century and a half.

The early decades followed the familiar pattern of American community banking. Fulton National served the agricultural cycle: lending to farmers in spring, collecting after harvest in fall. It financed local manufacturers and shopkeepers. The bank's officers knew their borrowers personally, knew their families, knew their land. Credit decisions were made not by algorithm or distant committee but by men who would see the consequences of their judgment at Sunday church services. This was banking as social contract, and it imposed a discipline that more sophisticated institutions would later lose.

Fulton survived the Panic of 1893, when a stock market crash and a run on gold reserves triggered a wave of bank failures across the country. It survived the banking crises of the early 1900s. And it survived the catastrophic bank runs of the early 1930s that wiped out thousands of institutions nationwide. When the Federal Deposit Insurance Corporation was created in 1933, roughly nine thousand banks had failed during the Depression. Fulton was not among them. The reason was simple: the bank had not overextended. It had not speculated. It had stuck to what it knew, lending to people and businesses it understood in a community it served. This was not a glamorous survival story. There was no dramatic last-minute rescue. The bank simply kept doing what it had always done, and that was enough.

What kept the bank alive during those early decades was the same thing that would keep it alive through every subsequent crisis: relationship-based lending. In a community where everyone knew everyone, extending a bad loan was not just a financial mistake, it was a social one. The banker who made reckless loans would face his neighbors at church, at the market, at the county fair. This created an informal but powerful credit discipline that no regulatory framework could replicate. The Pennsylvania Dutch culture of fiscal conservatism, the emphasis on living within one's means, on saving before spending, on distrusting debt, was baked into the institution's DNA from day one.

As the economy shifted from agriculture to light manufacturing through the early twentieth century, Fulton adapted its lending accordingly, financing small factories and workshops alongside the farms that had been its original customer base. By the mid-twentieth century, Fulton Bank had become the largest bank in Lancaster County, and in 1948 it began acquiring smaller local banks, absorbing their deposits and branches while retaining their community relationships. In 1974, the institution dropped "National" from its name, becoming simply Fulton Bank, and withdrew from the Federal Reserve System for additional regulatory flexibility. These were modest moves, but they signaled an institution beginning to think beyond its county borders. The question was how far it could go, given Pennsylvania's restrictive branching laws that prevented banks from expanding freely across the state.

The answer would require a creative corporate restructuring and a man named Rufus Fulton.

The Multi-Bank Holding Company: A Creative Solution to a Regulatory Problem (1945-1980s)

To understand what Fulton Financial did next, you need to understand the peculiar regulatory landscape of American banking in the mid-twentieth century. Unlike most industries, banking was constrained by state laws that dictated where a bank could physically operate. Pennsylvania's laws were among the most restrictive, limiting acquisitions to contiguous counties. If you were a Lancaster bank that wanted to expand into, say, the Lehigh Valley or the suburbs of Philadelphia, the direct route was often blocked.

The creative solution was the bank holding company. Rather than trying to branch across the state under a single charter, a holding company could acquire multiple independent banks, each with its own charter, its own name, and its own local management. The parent company provided capital, back-office services, and strategic direction, while the subsidiary banks retained their local identities and community relationships.

On February 8, 1982, exactly one hundred years after the bank's founding, Fulton Financial Corporation was incorporated under Pennsylvania law. By June 30 of that year, the newly created holding company had acquired all outstanding stock of Fulton Bank, transforming it into a wholly owned subsidiary. The centennial timing was not coincidental. Management understood that the next century of growth required a fundamentally different corporate architecture.

The strategy that emerged was elegant in its simplicity: acquire small, well-run community banks across Pennsylvania and neighboring states, but keep their names, their branch networks, and much of their management in place. Customers of Swineford National Bank in Middleburg or Lebanon Valley Farmers Bank would continue banking under familiar brands, unaware that they were now part of a larger family. Meanwhile, the holding company centralized compliance, technology, accounting, and risk management, extracting efficiencies that no individual community bank could achieve on its own.

Rufus A. Fulton Jr., a descendant of the founding family who had joined the bank as its first management trainee in 1966, was the driving force behind this acquisition strategy. His career arc tells you everything about Fulton's culture: he started at the bottom, learned every part of the business from trust administration to commercial lending, and ascended through patient competence rather than flashy dealmaking. He became president of Fulton Financial Corporation in 1987 and president and CEO on January 1, 1993. Under his leadership, the acquisitions accelerated dramatically. Between the holding company's formation in 1982 and his retirement in 2005, the company completed twenty-three acquisitions. By the time the strategy fully played out, Fulton Financial would acquire forty-four banking institutions in total.

Fulton Jr.'s approach to acquisitions was distinctive. He was not a financial engineer seeking to extract maximum synergies from every deal. He was a relationship banker who understood that the value of a community bank resided in its people and its reputation, not in its balance sheet alone. When Fulton Financial acquired a bank, the deal often included retention agreements for key managers and explicit commitments to maintain local branding. The acquired bank's customers would see the same faces behind the teller windows, the same names on the building, and experience the same decision-making processes they had always relied upon. The only thing that changed was the flow of capital and back-office services, which now connected to a larger, more efficient parent company.

The brilliance of the multi-bank model was that it turned Pennsylvania's regulatory constraints into a competitive advantage. While larger banks were frustrated by branching limitations, Fulton assembled a network of community banks that collectively covered a wide geographic footprint while individually maintaining the local relationships that drove customer loyalty. The parent company was essentially invisible to most depositors, which was precisely the point. Think of it as a franchise model for banking: each location operated with local autonomy and identity, but behind the scenes, a centralized organization handled the expensive, scale-dependent functions that no small bank could afford on its own.

There was also a clever regulatory dimension to the strategy. At one point, Fulton Bank briefly changed the address of its headquarters to Dauphin County, neighboring Lancaster County, to satisfy Pennsylvania's contiguous-county acquisition rules and facilitate westward expansion. It was the kind of creative regulatory maneuvering that larger institutions with more bureaucratic cultures would never have attempted. Once interstate banking laws further deregulated through the decade, the workaround became unnecessary, but it illustrated a willingness to find inventive solutions within the rules rather than waiting for the rules to change.

This period also coincided with the Savings and Loan crisis of the 1980s, which destroyed more than a thousand thrift institutions nationwide and cost American taxpayers roughly one hundred and thirty billion dollars. The S&L crisis was, in many ways, a dress rehearsal for the 2008 financial crisis: deregulation created new freedoms, institutions used those freedoms to chase higher-risk, higher-return strategies, and when the cycle turned, the losses were catastrophic and the taxpayer was left holding the bill.

Fulton sailed through largely unscathed, and the reason was straightforward: conservative underwriting. While S&Ls were loading up on speculative real estate loans and, in some notorious cases, outright fraud, Fulton's subsidiary banks were making the same kinds of agricultural, small business, and residential mortgage loans they had been making for decades. They did not chase junk bonds. They did not finance speculative commercial developments in overheated markets. They stuck to what they knew.

The lesson was clear, even if it would take several more crises before the broader industry internalized it: boring banking beats exciting banking when the cycle turns. This is the central insight of Fulton's entire corporate history, and it bears repeating because it runs counter to the instincts of modern finance, where innovation and growth are celebrated and conservatism is dismissed as timidity.

By the late 1980s, Fulton Financial had established itself as a legitimate regional player with a portfolio of community banks across central and eastern Pennsylvania. The holding company also built out trust and wealth management services, adding higher-margin fee income to complement traditional lending. But the real growth story was about to begin, because federal deregulation was about to blow open the doors to interstate banking.

Geographic Expansion and the Consolidation Era (1990s-2007)

The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 changed everything for regional banks. For the first time, bank holding companies could acquire banks across state lines without needing specific state-by-state reciprocal agreements. The legislation unleashed a wave of consolidation that would reduce the number of FDIC-insured institutions from roughly eighteen thousand to fewer than five thousand over the next three decades.

Fulton Financial moved quickly but deliberately. Rather than making a single transformative acquisition that would change the company's character, management pursued a series of smaller deals that extended the multi-bank model into new states. The playbook was consistent: identify well-run community banks in contiguous markets, acquire them at reasonable valuations, retain local management and branding, and integrate back-office operations.

The geographic expansion proceeded methodically, state by state. Delaware came through Delaware National Bank in Georgetown. Maryland was entered through a series of deals: Hagerstown Trust on the western border, the Peoples Bank of Elkton near the Delaware line, and Columbia Bancorp in the suburbs of Baltimore, which was Fulton's largest deal to that point when it closed in early 2006. New Jersey was built through acquisitions including Skylands Community Bank in Hackettstown and Somerset Valley Bank in Somerville, the latter bringing eleven branches across three counties. Virginia was entered through the 2004 acquisition of Resource Bank in Virginia Beach, establishing Fulton's southernmost outpost.

Each of these deals followed the same logic: buy an institution with strong local relationships, integrate the back office, keep the front office intact, and move on to the next target. It was assembly-line M&A, lacking the drama of hostile takeovers or transformative mergers, but effective in building a footprint that stretched from the Chesapeake Bay to the northern New Jersey suburbs.

The strategic choice embedded in every deal was the same: stay regional, go deep, and do not chase national scale. While the megabanks were building coast-to-coast empires through mega-mergers, NationsBank swallowing BankAmerica, Chase absorbing Chemical and then J.P. Morgan, Fulton was assembling a dense network of community banks in the mid-Atlantic corridor from southern Virginia to northern New Jersey. The theory was that geographic density in affluent suburban and semi-rural markets would generate better risk-adjusted returns than geographic breadth in unfamiliar territory. It was the tortoise strategy in an era that celebrated hares.

In 2000, Fulton Financial formally became a financial holding company under the Gramm-Leach-Bliley Act, unlocking the ability to offer a broader range of financial services beyond traditional banking. This enabled the expansion of wealth management and insurance activities, diversifying the revenue base beyond interest income and lending fees.

By the mid-2000s, Fulton Financial operated more than a dozen subsidiary banks across five states and had become the largest commercial bank holding company headquartered in the Third Federal Reserve District. The company had built a meaningful commercial real estate lending business, expanded its wealth management offerings, and invested in core banking technology including ATM networks and early online banking platforms. Total assets approached twenty billion dollars.

One decision made during this period would prove to be among the most consequential in the company's history, though it was notable mainly for what Fulton chose not to do. As the mid-2000s housing bubble inflated and competitors loaded their balance sheets with subprime mortgage products, collateralized debt obligations, and other exotic instruments that Wall Street was manufacturing at industrial scale, Fulton's credit culture held firm. The company did not chase subprime originations. It did not build a structured products desk. It did not load up on mortgage-backed securities with opaque risk profiles. This was not prescience about the coming crisis; it was institutional inertia in the best possible sense. The same conservative DNA that had kept the bank alive through the Depression and the S&L crisis simply did not permit the kind of risk-taking that would have generated higher short-term returns.

At the time, this conservatism looked like underperformance. Fulton's stock lagged competitors who were posting record earnings fueled by fee income from exotic products. Analysts questioned whether the multi-bank model was efficient enough, whether the company had sufficient scale, whether management was too cautious. Those questions would be answered decisively, though not in the way anyone expected.

The counterintuitive decision to maintain multiple bank charters rather than consolidating into a single brand also drew criticism. Running a dozen separate banks with separate boards, separate regulatory examinations, and separate marketing budgets was expensive. The company argued that local branding drove customer retention, but skeptics saw it as organizational inertia masquerading as strategy. Both sides had a point, and the tension would not be resolved for another decade. But first, there was a financial crisis to survive.

The Great Financial Crisis: When Conservative Became a Compliment (2008-2012)

The 2008 financial crisis arrived at Fulton Financial like a hurricane arriving at a well-built farmhouse. The structure held, but there was real damage.

Consider the timeline. In September 2008, Lehman Brothers collapsed, and the global financial system teetered on the edge of a complete meltdown. Within weeks, credit markets froze, stock prices cratered, and businesses across America began canceling expansion plans, laying off workers, and defaulting on loans. For a bank like Fulton, whose bread and butter was lending to mid-Atlantic businesses and commercial real estate developers, the crisis was not an abstract Wall Street event. It showed up in the form of phone calls from borrowers who could not make their payments, property appraisals coming in at half the values from two years prior, and a steady drumbeat of bad news from every corner of the footprint.

The storm hit Fulton primarily through its commercial real estate portfolio. As property values collapsed across the mid-Atlantic, borrowers who had been current on their loans suddenly found themselves underwater. Non-performing assets spiked. Charge-offs accelerated. For the nine months ending September 30, 2009, the provision for loan losses reached one hundred and forty-five million dollars, a staggering one hundred and sixty-five percent increase from the prior year period. To put that in perspective, Fulton was setting aside nearly three times as much money for expected loan losses as it had just twelve months earlier. Net income for that same nine-month period fell sixty-four percent to just thirty-four million dollars. In the second quarter of 2008 alone, the company recorded a twenty-five-million-dollar charge for impairment of bank stocks it held, and for the full year, a ninety-million-dollar goodwill impairment charge wiped out much of the accounting value attributed to years of acquisitions. That goodwill write-down was particularly painful because it represented a public acknowledgment that the banks Fulton had spent decades acquiring were now worth less than what had been paid for them.

On December 23, 2008, two days before Christmas, Fulton participated in the Troubled Asset Relief Program, receiving three hundred and seventy-six and a half million dollars in preferred stock purchases from the U.S. Treasury. The timing was not coincidental. The Treasury was pushing TARP funds out the door as fast as possible, trying to stabilize the banking system before panic could spread further. For Fulton, the TARP injection was controversial both externally and internally. Externally, TARP carried a stigma: accepting government money implied that a bank was in trouble, regardless of whether it actually needed the funds. Some banks that were fundamentally healthy took TARP because regulators encouraged them to, creating a herd effect that obscured who was genuinely distressed and who was simply being prudent. Management later described Fulton's participation as "depression insurance," a pragmatic decision made during a period when nobody knew how deep the recession would go or how many banks would ultimately fail. What is notable is how quickly Fulton repaid it. The full amount was returned on July 14, 2010, just eighteen months later. Including dividends and warrant proceeds, the U.S. government earned roughly fifty million dollars on its Fulton investment, making it one of the more profitable TARP transactions from the taxpayer's perspective.

Behind the financial numbers, a leadership transition was underway that would shape the company's next decade. R. Scott Smith Jr., who had become chairman, president, and CEO in 2006, guided the company through the worst of the crisis. In December 2008, at the very nadir of the financial panic, E. Philip Wenger was promoted to president and chief operating officer of the Corporation, the clearest possible succession signal. Wenger, who had joined Fulton Bank in 1979 straight out of Penn State and spent his entire career at the institution, brought deep institutional knowledge and a relationship-oriented leadership style forged in the commercial lending trenches.

The recovery was painful and slow. Branch rationalization began as management closed underperforming locations. Dividend cuts sent a chill through the shareholder base. The regulatory burden increased dramatically as Dodd-Frank compliance requirements fell disproportionately on mid-sized banks that lacked the compliance infrastructure of the megabanks but faced many of the same requirements. The efficiency ratio, which measures how much it costs a bank to generate a dollar of revenue, ballooned above sixty-five percent, well above the levels that investors and analysts considered acceptable.

Yet Fulton survived. The question is why, when so many regional banks of similar size either failed outright or were forced into distressed mergers. Between 2008 and 2015, more than five hundred FDIC-insured institutions failed. Hundreds more were acquired under duress. The landscape of mid-Atlantic banking was littered with once-familiar names that simply ceased to exist.

The answer comes back to three factors that all trace to the company's conservative culture.

First, capital adequacy. Fulton entered the crisis with sufficient capital cushions to absorb losses without breaching regulatory minimums. Capital ratios function as a bank's shock absorber: when loans go bad, the losses are absorbed by capital before they can threaten depositors. Banks that entered the crisis with thin capital cushions had no room for error. Fulton, having never leveraged itself aggressively in pursuit of higher returns, had the buffer it needed.

Second, deposit stability. Unlike banks that relied on hot money from rate-sensitive institutional depositors or brokered deposits, Fulton's funding came primarily from stable, relationship-based retail and commercial deposits. Brokered deposits are the banking equivalent of fair-weather friends: they show up when rates are high and vanish the moment trouble appears. Relationship deposits, built over years of personal service, are far stickier. When panic hit, Fulton's depositors did not run.

Third, and most importantly, the absence of toxic securities exposure. Because Fulton had never chased exotic products, it had no ticking time bombs on its balance sheet. No collateralized debt obligations. No synthetic CDO-squared structures. No opaque off-balance-sheet vehicles. The losses it suffered were real, from genuine credit deterioration in a deep recession, but they were manageable and predictable in a way that structured products losses were not. There is a world of difference between a bank that loses money because its borrowers cannot pay their mortgages and a bank that loses money because a tranche of synthetic securities that nobody fully understood turns out to be worthless.

The crisis also revealed a geographic vulnerability that would inform strategy for years to come. Fulton's footprint was concentrated in the mid-Atlantic region, areas that were experiencing long-term economic decline relative to Sunbelt markets. Population growth was modest. Industrial jobs were disappearing. This geographic concentration meant that Fulton could not simply wait for economic tailwinds to restore growth; it would need to find growth through operational improvement, strategic acquisitions, and expansion into stronger markets within its footprint.

As Wenger formally assumed the CEO role on January 1, 2013, he inherited a bank that had survived but needed fundamental transformation. The multi-bank model that had served the company for three decades was now a costly liability. The efficiency ratio was too high. Technology was lagging. And the company needed a clearer identity in a market that was rapidly consolidating. The next chapter would be about reinvention.

The Long Recovery: From Survivor to Modern Bank (2013-2019)

Phil Wenger's tenure as CEO of Fulton Financial was defined by a single overarching challenge: how do you modernize a one-hundred-and-thirty-year-old institution without destroying the conservative culture that kept it alive? His answer was methodical, sometimes frustratingly slow for investors, but ultimately transformative.

To understand Wenger, you need to understand his career. He joined Fulton Bank in 1979, straight out of Penn State, and never left. Forty-three years at one institution. He spent his early career in corporate lending, learning the business by shaking hands with borrowers, reviewing financial statements, and building the kind of personal relationships that generate repeat business. He was promoted to executive vice president of corporate banking in 1996, then to senior vice president and regional manager in 2001, then to president and CEO of Fulton Bank itself in 2006. When the financial crisis hit, he was elevated to president and COO of the entire corporation. He was not a turnaround specialist parachuted in from Wall Street. He was the ultimate insider, someone who understood the company's strengths and weaknesses from having lived inside them for three decades. His MBA from Penn State Harrisburg was an evening program completed while working full-time, which tells you something about his work ethic.

The most visible change under Wenger was also the most symbolically significant. After more than half a century of operating as a "family of banks" under separate charters and separate brands, he made the decision to consolidate everything under a single name: Fulton Bank. This was not just a rebranding exercise. Each subsidiary bank had its own board of directors, its own regulatory examinations, its own technology stack, and its own marketing budget. Maintaining this archipelago of institutions was consuming resources that could be better deployed on technology, talent, and growth. It was also creating confusion in the marketplace: potential customers did not realize that the bank in Bethlehem was connected to the bank in Lancaster, which was connected to the bank in Columbia, Maryland. The multi-charter structure, which had been a strategic asset in the era of restrictive branching laws, had become an expensive anachronism in the era of unified digital banking.

The consolidation unfolded in stages over nearly a decade. Maryland operations were unified first, with the Peoples Bank of Elkton and Hagerstown Trust merging into The Columbia Bank. Delaware National Bank was folded into Fulton Bank, N.A. in 2010. Each consolidation required its own regulatory approvals, systems migration, and customer communication campaign.

But the most significant moves came in September 2019, when Lafayette Ambassador Bank in the Lehigh Valley, with eighteen locations, and The Columbia Bank in Maryland, with thirty-one locations, were simultaneously merged into Fulton Bank. All forty-nine combined locations were rebranded overnight in a carefully orchestrated operation: new signage went up, websites were redirected, and customers woke up to find that the bank they had known for decades was now called something different. The multi-charter era officially ended, and Fulton emerged as a single unified brand for the first time in its history.

The estimated annual cost savings from the consolidations were approximately seven million dollars, which does not sound like much for a twenty-plus-billion-dollar bank. But the real value was strategic, not merely financial. A single brand enabled unified marketing, consistent customer experience, streamlined technology investment, and a clearer competitive identity. Wenger articulated the positioning in characteristically understated terms: Fulton would operate as something between a community bank and a large regional, offering the breadth of products customers expect from a big institution while maintaining the personal connections of a local one. In banking industry jargon, this is the "best of both worlds" pitch, and every mid-sized bank makes some version of it. What made Fulton's version credible was the relationship infrastructure built over more than a century.

The efficiency challenge proved more stubborn. Fulton's efficiency ratio, which had been above sixty-five percent during the crisis years, improved but remained elevated compared to better-run peers. The ratio measures non-interest expense as a percentage of revenue: the lower the number, the more efficiently the bank converts revenue into profit. Top-performing regionals were operating in the low-to-mid fifties. Fulton was still in the upper fifties to low sixties, reflecting the lingering costs of its complex organizational structure, a large branch network, and technology systems that needed upgrading.

Technology modernization became a major priority during this period. The company invested in mobile banking platforms, digital onboarding processes, and core system upgrades. These were necessary investments, but they were also expensive, and Fulton lacked the scale to spread technology costs across the enormous customer bases that megabanks enjoyed. This is the fundamental challenge facing every mid-sized bank in America: you must invest in digital capabilities to remain competitive, but you can never outspend JPMorgan Chase, which allocates more than fifteen billion dollars annually to technology.

The commercial banking push was more successful. Wenger, who had spent his career in commercial lending before ascending to the CEO role, understood that middle-market commercial relationships were the highest-value segment for a bank of Fulton's size. These relationships generated higher-margin loans, deeper deposit relationships, and fee income from treasury management services. Crucially, commercial banking clients have meaningfully higher switching costs than retail customers. Moving your personal checking account to a new bank takes thirty minutes. Moving your company's entire banking relationship, with its credit facilities, payroll processing, wire transfer infrastructure, and treasury management, takes months and involves significant operational risk. This switching cost dynamic gave Fulton a structural advantage in commercial banking that it lacked in the increasingly commoditized retail segment.

By 2018 and 2019, the pieces were finally coming together. Loan growth returned after years of post-crisis anemia. Return on assets, the simplest measure of how effectively a bank uses its balance sheet, was climbing toward the one-percent threshold that separates adequate performers from good ones. The efficiency ratio was trending downward. The single-brand consolidation was complete. And Wenger had begun eyeing the Philadelphia metropolitan market as the next frontier for growth, recognizing that Fulton needed a presence in the region's largest economic center to achieve the scale necessary for long-term competitiveness. Philadelphia was the missing piece: a major metropolitan market, sitting right at the edge of Fulton's existing footprint, with dense commercial activity and a fragmented banking landscape ripe for consolidation.

One footnote from this period deserves mention because it illustrates the regulatory scrutiny that mid-sized banks face. In 2020, the SEC found that during the fourth quarter of 2016 and the first quarter of 2017, Fulton Financial had presented a mortgage servicing rights valuation allowance in its public filings that was inconsistent with the methodology described in those filings. The discrepancy boosted the valuation allowance by a relatively modest one-point-three million dollars in a period when the company was near analyst consensus earnings estimates. Fulton settled without admitting or denying the charges, paying one-and-a-half million dollars. No restatement was required, and the episode had no lasting impact on operations, but it serves as a reminder that even conservative banks operate under intense regulatory scrutiny and that small accounting judgments can attract enforcement attention.

The stock, despite operational improvement, continued to trade at a discount to peers. The market was not yet convinced that Fulton had turned the corner from crisis survivor to growth story. That conviction would require a catalyst, and two of them were about to arrive in rapid succession: a pandemic and a banking panic.

The Pandemic Pivot: When Relationship Banking Proved Its Worth (2020-2021)

When COVID-19 shut down the American economy in March 2020, regional banks faced a dual test: could their operations function remotely, and could they serve customers through an unprecedented economic disruption? Fulton's answer to both questions revealed something important about the institution's capabilities.

Within weeks of the federal government launching the Paycheck Protection Program, Fulton Bank funded nearly two billion dollars in PPP loans to more than ninety-four hundred small business, nonprofit, and commercial clients across its five-state footprint. An initial wave of approximately nine hundred million dollars was deployed in early April 2020, with a second wave following when Congress approved additional funding. To put that in perspective, Fulton processed more PPP volume in a few weeks than many fintech lenders managed over the program's entire lifespan.

This was the moment when the "relationship banking" thesis was proven in the most tangible way possible. When small business owners were desperate for PPP loans and the program's first-come-first-served structure created panic, they turned to their existing banks. The restaurant owner in Lancaster who needed a lifeline called the same banker who had financed the kitchen renovation three years earlier. The manufacturing company in Bethlehem called the commercial lender who already understood its payroll and cash flow cycles. These were not cold calls to anonymous loan processors. These were phone calls between people who knew each other.

And that made everything faster. The banks that already had their customers' financial records, already knew their businesses, already had relationship managers who could pick up the phone, were able to process applications at a pace that no one else could match. The megabanks were overwhelmed by volume, their call centers jammed, their online portals crashing. The fintechs were processing applications from strangers whose creditworthiness they had no way to independently verify. The community and regional banks like Fulton were serving customers they already knew, and the speed differential was dramatic.

The PPP program generated meaningful fee income for Fulton, as the SBA paid origination fees on every loan. But it also created operational chaos that tested the organization in unexpected ways. Bankers accustomed to methodical credit analysis, carefully reviewing financial statements and personally visiting borrower premises, were suddenly processing thousands of government-guaranteed loans under constantly shifting guidelines from the SBA. The rules changed daily. The application forms were revised multiple times. Forgiveness criteria were unclear. And through it all, Fulton's bankers were working from home, managing virtual teams, and dealing with their own families' pandemic disruptions.

The full-year 2020 results reflected both the strain and the resilience: net income available to common shareholders came in at one hundred and seventy-six million dollars, or a dollar and eight cents per diluted share. Non-performing assets stood at just fifty-eight hundredths of a percent of total assets, and the fourth quarter actually showed net recoveries rather than charge-offs, meaning the bank collected more on previously written-off loans than it lost on new defaults. That is a remarkable credit quality outcome given the economic environment, and it reflected both the conservatism of Fulton's pre-pandemic underwriting and the unprecedented scale of government support that prevented widespread defaults.

The residential mortgage business boomed as historically low interest rates sparked a refinancing wave. Wealth management outperformed expectations as markets recovered from their March lows. And Fulton's management implemented strategic operating expense reduction initiatives, accelerating the efficiency improvements that had been underway since the brand consolidation.

Perhaps the most significant development was the acceleration of digital adoption. Years of gradual migration to mobile and online banking were compressed into months as branch lobbies closed and customers who had never downloaded a banking app suddenly had no choice.

For Fulton, this was both an opportunity and a warning. The opportunity was obvious: digital channels are dramatically cheaper to operate than branches. A mobile banking transaction costs a fraction of a penny; a teller transaction costs several dollars when you account for staffing, real estate, and overhead. Every customer who shifts from branch-based to digital banking improves the efficiency ratio.

The warning was subtler but more consequential: once customers became comfortable banking digitally, the physical branch network that was Fulton's primary competitive advantage over fintech competitors became less essential. If a customer discovers that they can deposit checks, pay bills, transfer money, and even apply for loans from their phone, the value proposition of having a branch on the corner diminishes. This does not eliminate the value of branches entirely, particularly for complex transactions like commercial loans or wealth management consultations, but it erodes the everyday utility that keeps customers walking through the door.

The pandemic also raised uncomfortable questions about Fulton's commercial real estate portfolio. As remote work became normalized and office vacancy rates climbed, the entire commercial real estate lending sector came under scrutiny. Fulton's CRE exposure was significant, concentrated in mid-Atlantic markets where the work-from-home trend was particularly pronounced. The expected losses did not materialize during the pandemic itself, partly because government stimulus programs kept businesses and landlords solvent. But the structural question of whether commercial office space had permanently declined in value would linger.

By the end of 2021, Fulton was in a fundamentally stronger position than it had been pre-pandemic. PPP had demonstrated the value of its relationship infrastructure. Digital adoption had accelerated. Credit quality had held up. And the company had quietly executed a strategically important acquisition: Prudential Bancorp, a Philadelphia-based savings bank with approximately one-point-one billion dollars in assets. The deal, announced in March 2022 and completed in July of that year, gave Fulton its first meaningful foothold in the Philadelphia metropolitan area. Prudential Bank's branches were merged into Fulton Bank by November 2022, and the company made a two-million-dollar contribution to the Fulton Forward Foundation for Philadelphia-area community nonprofits as part of its community reinvestment commitment. It was a modest deal by industry standards, but it was the opening move in what would become a much more ambitious Philadelphia strategy.

A leadership transition was also underway. In March 2022, Phil Wenger announced his retirement after forty-three years at the institution, and the board named Curtis J. Myers as his successor effective January 1, 2023. The continuity was intentional and characteristic. Every CEO in Fulton's modern history had been a career insider, steeped in the institution's culture and relationships.

Myers had joined the bank in 1990 as a management trainee and spent his entire career at Fulton. He rose through commercial banking roles, becoming a senior vice president and regional manager of commercial banking by 2000, joining the bank's senior management team in 2004, and serving as president and COO of both Fulton Bank and the Corporation. He holds a business administration degree from Shippensburg University and an MBA from Saint Joseph's University, and serves on the Board of Directors of the Federal Reserve Bank of Philadelphia, a position that reflects both his personal standing and Fulton's significance in the regional banking landscape.

Myers has articulated a leadership philosophy built around continuous improvement: assembling the right team, providing clear vision, and empowering execution. It is not the kind of philosophy that generates magazine profiles, but it is well-suited to an institution where cultural stability is the primary source of competitive advantage. The transition felt orderly and undramatic, which was the entire point.

The 2023 Regional Banking Crisis: Guilt by Association

On March 10, 2023, Silicon Valley Bank collapsed in the second-largest bank failure in American history. Two days later, Signature Bank was seized by regulators. Over the following weeks, First Republic Bank entered a death spiral that would end with its seizure and sale to JPMorgan Chase. Global financial stocks lost four hundred and sixty-five billion dollars in market value in just two days.

For Fulton Financial and every other regional bank in America, the crisis was an exercise in guilt by association. The market did not pause to analyze individual bank balance sheets. It painted every institution with assets below two hundred and fifty billion dollars with the same brush: vulnerable. Algorithmic trading systems and social media amplified the panic. Twitter threads listing banks with "unrealized losses" on their bond portfolios went viral, and institutional investors sold first and asked questions later.

Fulton's stock price dropped sharply, as did those of virtually every regional bank. The KBW Regional Banking Index, the benchmark for the sector, fell more than twenty-five percent in a matter of days. Fulton was caught in the downdraft despite having virtually nothing in common with SVB's business model. Moody's Investors Service subsequently downgraded Fulton and nine other mid-sized banks, citing concerns about higher-for-longer interest rates, commercial real estate exposure, and funding vulnerability. Moody's specifically flagged Fulton's low liquidity levels, particularly cash reserves, increased reliance on market funding, and weakening net interest margin. The downgrade sent Fulton's shares down further, dropping roughly five percent on the day of the announcement alone.

Fulton was among a coalition of mid-sized banks that petitioned the FDIC to temporarily extend deposit insurance beyond the standard two hundred and fifty thousand dollar limit, a measure that was ultimately not enacted but that illustrated the seriousness of the perceived systemic risk. Management was making contingency plans even as it publicly projected confidence.

The fundamental question was whether Fulton was exposed to the same risks that destroyed SVB. The answer was no, and the differences were instructive.

Silicon Valley Bank had failed because of an almost comically concentrated risk profile: its deposits were overwhelmingly from venture capital-backed technology startups, most above the FDIC insurance limit, creating a depositor base that was both homogeneous and prone to herd behavior. When word spread that SVB had taken losses on its bond portfolio, the depositors ran simultaneously, draining forty-two billion dollars in a single day.

Fulton's deposit base was the opposite of SVB's in virtually every dimension. It was diversified across hundreds of thousands of retail and commercial customers. It was geographically spread across five states. The average deposit was far smaller, meaning a much higher percentage fell under the FDIC insurance limit. A retired schoolteacher in Lancaster with forty thousand dollars in savings is not going to withdraw her money because of a Twitter thread about unrealized bond losses. She has been banking at Fulton for thirty years and her deposits are fully insured. This was the bedrock that held.

And crucially, these were relationship depositors who had been banking with Fulton for years or decades, not hot money chasing the highest rate. When the panic hit, Fulton's depositors largely stayed put. The bank experienced modest deposit outflows as the entire industry saw rate-sensitive money migrate to higher-yielding alternatives, with total deposits declining from twenty-one-point-six billion dollars in 2022 to twenty-point-six billion, but this was a gradual adjustment driven by interest rate competition, not a bank run.

Fulton's balance sheet was also fundamentally different from SVB's. The company had not loaded up on long-duration bonds at rock-bottom interest rates, the trade that destroyed SVB when rates rose and those bonds lost enormous value. Fulton's securities portfolio was conservatively positioned with limited held-to-maturity losses. Capital ratios remained well above regulatory minimums.

Management responded to the crisis with aggressive communication. Curt Myers, who had assumed the CEO role just two months before SVB collapsed, found himself immediately tested in the most public way possible. He hosted conference calls, conducted investor presentations, and was transparent about the bank's liquidity position and deposit composition in a way that contrasted sharply with the opacity that had characterized SVB's management in its final weeks.

It was a test of trust between the bank and both its customers and its investors, and the trust held. By the second half of 2023, the immediate panic had subsided, though the regional banking sector remained under a cloud of uncertainty that would not fully dissipate for months.

What the episode revealed was something broader about the state of American finance: the market had lost the ability, or the willingness, to distinguish between regional banks. Decades of consolidation had reduced the number of banks from eighteen thousand to fewer than five thousand, but the survivors were still remarkably diverse. A tech-focused lender in Silicon Valley and a farm-country bank in Pennsylvania have about as much in common as a Tesla and a John Deere tractor. Yet the market treated them identically in March 2023.

Fulton was not SVB. Its entire one-hundred-and-forty-one-year history was a testament to the opposite of concentrated risk-taking. But in a panic, nuance does not trade. And the indiscriminate selloff, while painful for shareholders, created the very opportunity that would transform Fulton's trajectory.

The crisis also created opportunity. As weaker regional banks teetered, stronger ones like Fulton had the capital and credibility to act as acquirers. The first opportunity was about to present itself in spectacular fashion.

Republic First: The FDIC Deal That Changed Everything (April 2024)

The story of Republic First Bank's failure reads like a cautionary tale about everything Fulton Financial had spent a century and a half avoiding.

Republic First Bank, branded as Republic Bank, was a Philadelphia-area institution that represented, in many ways, the anti-Fulton. Where Fulton was conservative, Republic was aggressive. Where Fulton grew methodically through small acquisitions, Republic chased rapid organic growth through above-market deposit rates and flashy branch designs. The bank was led by Vernon Hill, one of the most colorful and controversial figures in mid-Atlantic banking. Hill had previously built Commerce Bancorp into a regional powerhouse by treating bank branches as retail stores, opening them on weekends and evenings, equipping them with coin-counting machines, and branding the whole operation as "America's Most Convenient Bank." He sold Commerce to TD Bank in 2007 for roughly eight and a half billion dollars, then set about replicating the formula at Republic.

The Commerce playbook was brilliant when interest rates were low and deposit costs were minimal. Hill could pay above-market rates to attract deposits, fund the higher costs through loan growth, and invest in eye-catching branch locations that generated buzz and foot traffic. But the model had a fundamental vulnerability: it depended on a low-rate environment to make the math work. When the Federal Reserve began raising rates aggressively in 2022, Republic's business model inverted with devastating speed. The bank was paying top-of-market rates on deposits while holding lower-yielding assets originated during the low-rate era, a classic asset-liability mismatch that bleeds a bank dry month by month. Think of it as buying inventory at retail prices while selling at wholesale: the more business you do, the more money you lose.

NASDAQ delisted Republic First in August 2023 after the bank failed to file its annual report, a red flag that screamed distress. Behind the scenes, the situation was even worse. A bitter boardroom fight between incumbent management and activist investors, including the politically connected Norcross-Braca Group led by South Jersey power broker George Norcross, paralyzed decision-making at the worst possible moment. Multiple capital-raising attempts were torpedoed by the infighting. A thirty-five-million-dollar rescue deal collapsed in late February 2024 when investors lost confidence in the bank's ability to right itself. By April, the bank's fate was sealed, and it became a cautionary tale about what happens when a bank optimizes for growth without the conservative guardrails that companies like Fulton treat as non-negotiable.

On April 26, 2024, Pennsylvania's banking regulator seized Republic First Bank, making it the first bank failure in the United States that year and the sixth-largest bank failure since 2010. The FDIC immediately transferred substantially all assets and deposits to Fulton Bank, N.A., determining that Fulton's bid was the least costly resolution for the Deposit Insurance Fund. The cost to the DIF was estimated at six hundred and sixty-seven million dollars, reflecting the gap between Republic's liabilities and the value of the assets Fulton was willing to assume.

For Fulton, this was a transformative moment disguised as a regulatory transaction.

The scale of what Fulton absorbed was staggering for a bank its size: Republic had approximately six billion dollars in total assets, including a two-billion-dollar investment portfolio and two-point-nine billion in loans, plus four billion in deposits. Fulton assumed approximately five-point-three billion in liabilities. Republic's thirty-two branches across New Jersey, Pennsylvania, and New York reopened as Fulton Bank branches the following Monday morning. Customers who had gone to bed as Republic Bank depositors woke up as Fulton Bank customers, their accounts seamlessly transferred, their FDIC insurance intact.

The strategic significance was enormous. The deal instantly doubled Fulton's presence in the Philadelphia metropolitan area, the nation's sixth-largest market and the economic engine of southeastern Pennsylvania.

This was exactly the kind of geographic expansion Fulton had been pursuing incrementally through the Prudential Bancorp acquisition two years earlier, but the Republic deal accelerated the timeline by years. Fulton was suddenly a meaningful player in the most important commercial and consumer banking market in its footprint, with the branch density and deposit base to compete for commercial relationships that would have taken a decade to build organically.

To support the acquisition, Fulton raised two hundred and eighty-seven-and-a-half million dollars through a common stock offering. This diluted existing shareholders but provided the capital cushion necessary to absorb Republic's assets with appropriate reserves. Management moved quickly on integration, closing eighteen overlapping branches and executing the systems conversion ahead of schedule. The New York branches, which were outside Fulton's strategic footprint, were closed by September 2024.

CEO Curt Myers captured the significance in characteristically understated fashion: "With this transaction, we are excited to double our presence across the region." What he did not say, but what the market understood, was that this deal marked a fundamental shift in Fulton's identity. For decades, the company had been defined by cautious survival. The Republic acquisition signaled a willingness to grow aggressively through crisis-driven opportunities, leveraging the same conservative balance sheet management that had been Fulton's hallmark to act when weaker competitors stumbled.

The Republic deal also carried risks that investors needed to evaluate carefully. Integrating a failed bank is never clean. Republic's credit quality needed careful review, and the loans on its books had been originated under a completely different risk philosophy than Fulton's own portfolio. Customer relationships had been disrupted by months of uncertainty, during which Republic's best commercial clients had likely already begun shopping for alternatives. And the cultural gap between Republic's aggressive growth-oriented approach and Fulton's conservative ethos was real: absorbing employees accustomed to one way of doing business into an organization that operates very differently creates friction that no integration plan can fully anticipate.

The company reported twenty-five million dollars in annual cost synergies from the integration, a figure that will grow as the remaining operational redundancies are eliminated. Early indications suggested that credit quality in the acquired portfolio was manageable, but the full earn-back period remained to be proven. Failed bank acquisitions have a pattern of revealing hidden problems months or years after closing, and investors monitoring Fulton should watch charge-off rates in the acquired portfolio closely.

Perhaps most importantly, the deal demonstrated something that the market had not fully appreciated: Fulton had excess capital and the operational capability to execute complex acquisitions under pressure. In a period when most regional banks were focused on defending their existing positions, Fulton was playing offense. This was not a bank merely surviving anymore. This was a bank positioning itself as a regional consolidator, turning the same conservative balance sheet management that had kept it alive for over a century into an offensive weapon.

Blue Foundry and the Emerging Acquisition Strategy (November 2025)

Seven months after digesting the Republic First acquisition, Fulton announced its next move. On November 24, 2025, Fulton Financial Corporation and Blue Foundry Bancorp, a two-point-two-billion-dollar asset savings bank based in Rutherford, New Jersey, announced a definitive all-stock merger agreement valued at approximately two hundred and forty-three million dollars.

The deal structure was straightforward: each Blue Foundry share would convert to 0.65 shares of Fulton common stock. Blue Foundry operated twenty-one branch locations in eight New Jersey counties, including four of the state's most populous, focused on consumer deposit gathering and residential mortgage lending. Blue Foundry shareholders approved the transaction on January 29, 2026, and all required regulatory approvals from the Federal Reserve Board and the Office of the Comptroller of the Currency were received by February 2026. The closing is anticipated on or around April 1, 2026.

The financial advisors on the deal reflected its significance: Stephens Inc. advised Fulton, with Holland and Knight providing legal counsel; Piper Sandler advised Blue Foundry, with Luse Gorman handling the legal work. The transaction was expected to be more than five percent accretive to first full-year earnings, immediately accretive to tangible book value per share, and neutral to regulatory capital ratios at close. Those are the three metrics that matter most in bank M&A: does it improve earnings, does it build book value, and does it maintain capital adequacy? The Blue Foundry deal checked all three boxes.

The strategic logic extended directly from the Republic playbook. Northern New Jersey was a priority growth market for Fulton, and the Blue Foundry deal added twenty-one branches in a demographically dense, affluent corridor stretching across Bergen, Essex, Hudson, Morris, Passaic, Somerset, Sussex, and Union counties. This is some of the most attractive banking territory in the northeastern United States: high household incomes, dense commercial activity, and a customer base that values the kind of relationship banking that Fulton provides.

What made the Blue Foundry deal significant was not its individual size but the pattern it established. Together with Republic First, it revealed a coherent acquisition strategy: target banks in contiguous markets that face operational or strategic challenges, acquire them at reasonable valuations, and integrate them into Fulton's existing infrastructure. This is the consolidator playbook, and it works best for banks that have the capital strength, operational discipline, and cultural stability to absorb acquisitions without destabilizing their own operations.

The capital allocation framework underpinning this strategy became explicit in December 2025, when the board approved a comprehensive capital return program. The quarterly dividend was increased to nineteen cents per share, up from eighteen cents, extending the company's remarkable forty-four-year streak of unbroken dividends. At the same time, the board authorized a one-hundred-and-fifty-million-dollar share repurchase program effective January 1, 2026, with up to twenty-five million dollars available for repurchasing preferred stock and subordinated notes.

The forty-four-year dividend streak deserves emphasis. Fulton has maintained unbroken dividend payments through the 2008 financial crisis, the COVID pandemic, and the 2023 banking panic. While many banks cut or suspended dividends during those periods, Fulton continued paying, even when doing so required conserving capital in other areas. For income-oriented investors, this kind of consistency is rare and valuable. The current annualized dividend of approximately seventy-two cents per share yields roughly three-point-eight percent at recent share prices, making Fulton an attractive option for investors seeking reliable income from a well-capitalized institution.

The message to investors was clear: Fulton had enough capital to simultaneously grow through acquisitions, return capital through dividends and buybacks, and maintain the conservative capital ratios that had defined the institution for a century and a half.

The narrative arc from 2008 to 2025 was striking. A bank that had entered the financial crisis relying on government support to survive was now deploying excess capital across three channels of shareholder value creation. The transformation from defensive survivor to offensive acquirer had taken nearly two decades, but it was real and accelerating.

The Modern Fulton: Digital Transformation and Strategic Positioning

Walk into any Fulton Bank branch today and the experience is a far cry from the oak-paneled offices of the original Lancaster institution. Modern teller stations, digital kiosks, and Wi-Fi-enabled waiting areas sit alongside the traditional relationship bankers who are still the institution's primary competitive differentiator. Fulton Financial today operates more than two hundred financial centers across Pennsylvania, New Jersey, Maryland, Delaware, and Virginia, employing more than thirty-three hundred people. The 2024 fiscal year was a record, and CEO Curt Myers did not bury the lede: operating diluted earnings per share of one dollar and eighty-five cents represented an eight percent increase over the prior year. Total assets reached thirty-two-point-one billion dollars, roughly double where they stood a decade earlier. Total deposits stood at twenty-six-point-one billion, with the Republic First acquisition contributing roughly three-point-seven billion in net deposits. The common equity tier one capital ratio was ten-point-six percent at year-end, rising to approximately eleven percent by the first quarter of 2025, well above regulatory minimums and providing ample cushion for continued growth.

The company provided 2025 guidance that reflected management's confidence: net interest income between nine hundred and ninety-five million and one-point-zero-two billion dollars, provision for credit losses between sixty and eighty million dollars, and non-interest expense between seven hundred and fifty-five million and seven hundred and seventy-five million dollars.

The FultonFirst initiative, the company's multi-year technology and operational modernization program, is the operational centerpiece of Myers's CEO tenure. The program targets fifty million dollars in annual cost savings by 2026, with twenty-five million realized in 2025. It has driven branch consolidation, including the closure of fifteen financial centers in early 2025, as well as investments in digital banking capabilities and operational simplification.

The branch closures are worth examining in context. Closing fifteen locations sounds aggressive, but Fulton operates more than two hundred financial centers, so this represents a rationalization of roughly seven percent of the network. Each closure is analyzed for customer impact, competitive positioning, and cost savings. The goal is not to eliminate branches wholesale but to concentrate resources in locations where physical presence drives the most value, particularly in commercial banking markets where face-to-face relationships remain critical.

On the technology front, Fulton has made meaningful investments in modernizing its infrastructure, and it is worth pausing to understand what digital transformation actually means for a mid-sized bank. For a company like Fulton, "technology investment" is not about building the next mobile banking app from scratch. It is about integrating dozens of legacy systems, some of which date back decades, into a coherent platform that can deliver the seamless customer experience that modern consumers expect.

The company deployed the Boomi Enterprise Platform for system integration, running more than three hundred and fifty integration processes across eighty-three endpoints. In plain terms, this means that data from the loan origination system, the deposit platform, the wealth management tools, and the customer relationship database now flow together automatically rather than requiring manual reconciliation. It is the kind of invisible infrastructure that customers never see but that makes the difference between a bank that can open an account in minutes and one that takes days.

In December 2024, Fulton announced deployment of NICE's CXone Mpower tools, including generative AI-powered copilot and autopilot features for customer service. The copilot assists human agents by pulling up relevant customer information and suggesting responses in real time. The autopilot handles routine inquiries, like balance checks and transaction disputes, without human intervention. The company also partnered with Reltio for a cloud-native customer data platform, enabling the kind of omnichannel customer analytics that modern banking increasingly requires. And in 2025, Fulton appointed Kevin Gremer as Chief Operations and Technology Officer, a C-suite position that underscored the strategic priority management places on technology modernization.

Under Myers's leadership, the bank has maintained its commitment to the commercial banking segments where relationship value is highest while aggressively modernizing the infrastructure that supports those relationships. The combination of new technology leadership, AI deployment, and system integration represents the most ambitious technology overhaul in the company's history.

Credit quality remains solid. Non-performing assets stand at sixty-two hundredths of a percent of total assets, and net charge-offs are running at twenty-one hundredths of a percent. To translate those decimals into plain language: for every thousand dollars in loans on Fulton's books, roughly six dollars are troubled and about two dollars have been written off. Those are excellent numbers by historical standards and compare favorably to industry averages.

The allowance for credit losses sits at approximately one-point-six percent of total net loans, providing adequate reserves against potential deterioration. Morningstar DBRS confirmed Fulton's long-term issuer rating at "A (low)" with a stable trend in its most recent review. However, the rating agency included a caveat worth noting: current credit metrics are "unsustainably low" and expected to normalize gradually. In other words, today's credit quality is as good as it gets, and future periods will likely see some deterioration. This is not specific to Fulton; it reflects the credit cycle reality that benign conditions do not last forever. The question is whether Fulton's conservative underwriting culture will result in less deterioration than peers when the cycle eventually turns, as it has in every previous downturn.

The tension at the heart of Fulton's modern strategy is the same one facing every mid-sized bank in America: how do you invest enough in digital capabilities to remain competitive with both fintech startups and megabank technology budgets while maintaining the branch-based relationship model that differentiates you from both?

Fulton's answer has been to invest selectively in high-impact technology, the integrations, the AI tools, the data platforms, while preserving the commercial relationship infrastructure that generates its highest-value business. It is a bet that technology can augment relationship banking rather than replace it, that the future of mid-sized banking is not digital-only but digitally-enabled human relationships.

Whether that balance is sustainable over the next decade is the central strategic question investors must evaluate.

Competitive Analysis: Where Fulton Stands

Understanding Fulton's competitive position requires examining the forces shaping its industry and the sources of durable advantage available to it.

The Competitive Landscape

The threat of new entrants into banking remains moderate despite regulatory barriers. Traditional bank charters require substantial capital and regulatory approval, but fintech companies have found ways to offer banking-like services, including deposits through partner banks, lending through marketplace models, and payments through digital wallets, without the full regulatory burden. Companies like Chime, SoFi, and Marcus by Goldman Sachs are capturing younger demographics with slick mobile experiences and no physical branches. Fulton's response has been to invest in digital capabilities, but its legacy cost structure limits how aggressively it can compete on price or user experience.

Customer bargaining power is high and rising. Retail banking customers can switch institutions with minimal friction, especially for commoditized products like savings accounts and personal loans. The digital era has made price comparison effortless. Where Fulton retains meaningful customer stickiness is in commercial banking, where treasury management, credit facilities, and operational banking services create genuine switching costs. A middle-market company that has built its entire cash management infrastructure around Fulton Bank does not switch to a competitor over a twenty-five basis point rate differential.

The threat of substitutes is perhaps the most significant force reshaping banking. Peer-to-peer lending platforms, private credit funds, digital-only banks, robo-advisors, and the broader shadow banking system are all competing for business that traditionally flowed through banks like Fulton. Private credit markets have grown to rival bank lending in many segments, and the trend shows no sign of reversing. Fulton's mid-Atlantic footprint is not insulated from these forces.

Competitive rivalry is intense, and Fulton faces pressure from every direction simultaneously. From above, national giants like JPMorgan Chase and Bank of America offer superior technology, broader product suites, and the convenience of nationwide branch networks. JPMorgan alone has opened hundreds of new branches in recent years while simultaneously investing billions in digital capabilities. From the side, aggressive super-regionals like PNC, Citizens, and M&T Bank operate extensively in Fulton's footprint with larger balance sheets and more sophisticated corporate banking platforms. PNC, headquartered just across the state in Pittsburgh, is the dominant Pennsylvania bank and a formidable competitor in every market Fulton serves.

From below, hundreds of community banks and credit unions compete for the same local relationships, often with even lower overhead and more personalized service than Fulton can offer. And from an entirely different dimension, fintech companies attack the most profitable retail banking products without the burden of branches, regulatory overhead, or legacy technology systems.

Fulton occupies the uncomfortable middle of this competitive landscape, and the history of American banking is not kind to banks in the middle. Too large to compete purely on personal relationships, too small to compete on technology and product breadth. The acquisitions of Republic First and Blue Foundry are explicitly designed to push Fulton toward the upper end of this spectrum, but the company remains significantly smaller than the super-regional banks that dominate its markets.

Sources of Competitive Power

Fulton's most durable competitive advantages are concentrated in three areas. First, switching costs in commercial banking. Middle-market commercial relationships, Fulton's strategic focus, involve deep operational integration between the bank and the client. These relationships generate recurring fee income and are genuinely difficult for competitors to dislodge. This is Fulton's most defensible market position.

Second, process power derived from credit culture. Fulton's conservative underwriting discipline is not a policy that can be written down and copied. It is an institutional culture that has been reinforced through one hundred and forty-four years of practice, multiple near-death experiences, and leadership continuity. Every CEO in the company's modern history has been a career insider. This cultural continuity creates a form of process power, an institutional knowledge about risk management that competitors with higher turnover or different cultural incentives cannot easily replicate.

Third, regional scale. While Fulton lacks national scale, its dense branch network across the mid-Atlantic gives it local scale advantages in customer acquisition, brand recognition, and operational efficiency within its footprint. The Republic First and Blue Foundry acquisitions are explicitly designed to increase this regional scale advantage.

Where Fulton is notably weak is in network effects, which are essentially nonexistent in traditional banking. Unlike a platform business where each additional user makes the service more valuable for every other user, adding another depositor to Fulton Bank does nothing for existing depositors. Payment networks, which do exhibit network effects, are controlled by Visa and Mastercard, not by the banks themselves. Fulton also lacks cornered resources: it has no proprietary technology, no unique data assets, no patents, and no exclusive access to any market or customer segment. And its brand power fades rapidly outside the core mid-Atlantic markets. Ask someone in Boston or Dallas about Fulton Bank and you will get a blank stare.

This vulnerability profile points to a specific strategic challenge. Fulton cannot win through network effects, proprietary technology, or brand dominance. It must win through execution: superior credit decisions, deeper commercial relationships, more disciplined capital allocation, and smarter acquisitions than its peers. These are process advantages, not structural ones, and they depend on cultural continuity and management quality rather than on durable barriers to competition. The moment Fulton's culture degrades, whether through rapid growth, a CEO who breaks from the conservative tradition, or an acquisition that introduces a clashing organizational philosophy, those process advantages could evaporate.

The strategic imperative flowing from this analysis is clear: Fulton must continue building scale through acquisitions in its footprint, invest selectively in digital capabilities to avoid falling fatally behind, and double down on commercial banking relationships where its switching cost advantage is strongest. The company's competitive position is defensible but not dominant, which means that execution quality matters more than in businesses with stronger structural moats.

The Bull Case and the Bear Case

Why Fulton Could Win

The optimistic case for Fulton Financial rests on several reinforcing pillars.

Start with valuation. The company trades at roughly ten times earnings, a meaningful discount to both the broader market and to better-positioned bank peers. Regional bank stocks have been in the penalty box since the 2023 crisis, and the sector has not fully recovered its credibility with generalist investors. If Fulton can demonstrate that its acquisition strategy is creating durable value, there is room for multiple expansion as the market reclassifies it from "cheap regional survivor" to "disciplined regional consolidator."

The acquisition platform is the centerpiece of the bull case. Fulton demonstrated with Republic First that it can execute complex, opportunistic deals at attractive valuations. The FDIC-assisted acquisition model, where a stronger bank acquires a failed institution's assets at a discount with government loss-sharing protection, is one of the most attractive deal structures in banking. As long as regional banks continue to fail, and the structural pressures that caused Republic First's collapse have not disappeared, Fulton is positioned to be a buyer.

The company's credit culture provides a risk management advantage that is genuinely rare. Fulton has navigated the Depression, the S&L crisis, the 2008 financial crisis, COVID, and the 2023 banking panic without a single existential threat to its solvency (TARP participation notwithstanding). This track record reflects institutional discipline that is difficult to replicate and represents a genuine competitive advantage during periods of stress, which is precisely when the best acquisition opportunities emerge.

The profitability trajectory is also encouraging. The FultonFirst initiative is driving real cost savings, the efficiency ratio is improving, and scale gains from the Republic and Blue Foundry acquisitions should provide further operating leverage. The forty-four-year dividend streak and new buyback program demonstrate management's commitment to returning capital. The mid-Atlantic footprint, while lacking Sunbelt growth dynamics, encompasses affluent suburban markets with strong commercial activity.

Why Fulton Could Struggle

The bearish case begins with the most uncomfortable statistic in American banking: the number of FDIC-insured institutions has declined from eighteen thousand to fewer than five thousand over the past four decades. That is a seventy-five percent reduction in the number of banks, and the pace of consolidation has not slowed. Regional banks are a shrinking category, and history suggests that the trend will continue. Fulton may be a survivor, but survivors in a dying industry do not necessarily make great investments.

Fintech disruption is real and accelerating. Every retail banking product that Fulton offers, from savings accounts to personal loans to payment processing, is being attacked by digital-first competitors with lower cost structures and better user experiences. Fulton's digital investments are necessary but likely insufficient to close the gap with both fintech startups and the technology budgets of the megabanks.

The scale disadvantage is structural. Fulton cannot compete with JPMorgan's annual technology budget, which exceeds Fulton's entire revenue base. This means that over time, the product and experience gap between megabanks and mid-sized regionals will likely widen, not narrow. Scale disadvantage also limits Fulton's ability to compete on price for commoditized products.

Geographic concentration remains a vulnerability. The mid-Atlantic region, while economically diverse, lacks the population growth and business formation dynamics of Sunbelt markets. Fulton is not positioned to benefit from the secular migration of people and businesses to Texas, Florida, and the Southeast.

Integration risk from the Republic and Blue Foundry acquisitions is real. Failed bank acquisitions look attractive on paper because the purchase price is discounted, but the operational reality of integrating different systems, cultures, and credit portfolios is always harder than projected. Hidden credit problems in acquired portfolios can take years to fully emerge.