Fortive: The Danaher Business System Goes Independent

I. Introduction & Opening Hook

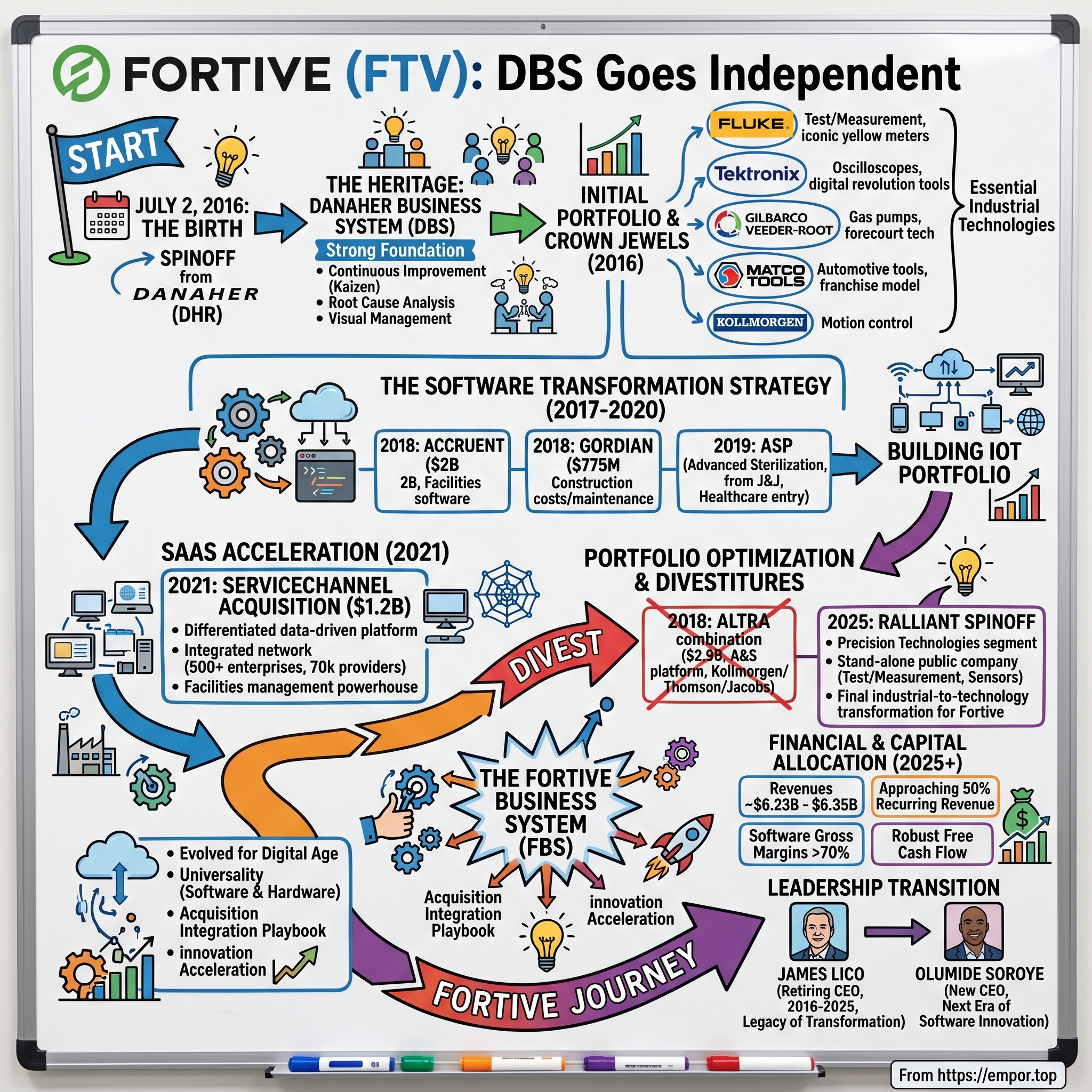

Picture the scene: July 2, 2016, a Saturday morning in Everett, Washington. While most of corporate America slept through the holiday weekend, a $6 billion industrial giant quietly emerged from one of the most successful business empires ever built. Fortive Corporation ("Fortive") (NYSE: FTV), a diversified industrial growth company providing essential industrial technology and professional instrumentation solutions globally, announced today the completion of its separation from Danaher Corporation ("Danaher"). The timing—executed on a non-business day—was symbolic: this wasn't your typical Wall Street spinoff fanfare. It was the calculated, methodical birth of a company that would inherit the operational DNA of one of history's greatest industrial success stories.

The puzzle at the heart of Fortive's story captivates investors and operators alike: How does a collection of seemingly unglamorous industrial businesses—test equipment, gas pumps, automotive tools—transform into a software-led essential technology powerhouse generating billions in free cash flow? The answer lies not in Silicon Valley disruption but in something far more powerful: the relentless application of operational excellence married with strategic portfolio transformation.

Today, Fortive stands as a testament to disciplined evolution. Fortive's strategic segments - Intelligent Operating Solutions and Advanced Healthcare Solutions - include iconic inventor brands with leading positions in their markets. From the oscilloscopes that birthed the semiconductor industry to the software that orchestrates facilities management for the world's largest retailers, Fortive's journey represents the ultimate playbook for industrial transformation in the digital age.

What follows is the story of how a spinoff became a case study in value creation—from inheriting the legendary Danaher Business System to pioneering the industrial-to-software pivot, from billion-dollar acquisitions to strategic separations. It's a narrative that challenges conventional wisdom about conglomerates, proves that operational excellence can be a sustainable competitive advantage, and demonstrates how patient, methodical execution beats flashy disruption every time.

II. The Danaher Dynasty & Pre-History

The Fortive story begins not in 2016, but decades earlier with two brothers who would rewrite the rules of American capitalism. Founded by Steven and Mitchell Rales, Danaher Corporation(DHR) is one of the most successful business stories of the last three decades. The Rales brothers didn't start with a grand vision to build an industrial empire—they started with a simple observation: most American manufacturers were terribly run.

One of just 44 companies with a cumulative total return of greater than 10,000% over that time period(it's the 6th best performer), Danaher's success wasn't built on breakthrough products or revolutionary technology. Instead, the Rales brothers discovered something more powerful: the Toyota Production System. While their competitors chased quarterly earnings, Danaher's leadership made pilgrimages to Japan, studying kaizen events, value stream mapping, and the relentless pursuit of waste elimination.

What emerged was the Danaher Business System (DBS)—not just a set of tools, but a culture, a religion of continuous improvement that would transform every business it touched. Walk into any Danaher facility in the 1990s and you'd see the visual management boards, the daily huddles, the problem-solving A3 reports. This wasn't corporate theater; it was the systematic application of proven methodologies that turned struggling industrial businesses into cash-generating machines.

The companies that would eventually form Fortive were acquired during Danaher's aggressive expansion phase. Fluke Corporation, acquired in 1998, brought precision test and measurement. Gilbarco Veeder-Root added fuel dispensing systems. Tektronix's oscilloscope business joined the fold. Each acquisition followed the same pattern: identify an underperforming leader in an essential niche, apply DBS ruthlessly, watch margins expand and cash flow soar.

By 2015, Danaher had grown into a $20 billion colossus spanning everything from dental equipment to water treatment. But the Rales brothers and CEO Larry Culp (who would later rescue General Electric) saw an opportunity for an even more ambitious transformation. When Danaher picked up Pall for about $13.8 billion in May, the company said it would split into two entities as part of a tax-free spinoff for shareholders.

The logic was elegant: Danaher would pivot entirely toward life sciences and diagnostics—higher growth, higher margin businesses with more predictable revenue streams. The industrial and instrumentation businesses, while excellent operators, no longer fit this vision. But rather than sell these crown jewels to private equity, Danaher would spin them off, creating an independent company that could chart its own course while maintaining the cultural foundation of DBS.

The industrial businesses weren't cast-offs; they were thoroughbreds trained in the Danaher stable. They generated strong cash flows, held leading market positions, and most importantly, carried the institutional knowledge of how to run businesses better than anyone else. The stage was set for Fortive's emergence—not as a lesser Danaher, but as an entity uniquely positioned to adapt the DBS philosophy for a new era of industrial technology.

III. The Spinoff: Birth of Fortive (2015-2016)

The announcement came on December 3, 2015, with characteristic Danaher precision. Danaher Corporation (NYSE: DHR) (the "Company") today revealed the name of the new diversified industrial growth company expected to launch in 2016 as Fortive Corporation. Fortive will be comprised of two segments, Professional Instrumentation and Industrial Technologies, and will include market leading brands such as Fluke, Qualitrol, Tektronix, Gilbarco Veeder-Root, Kollmorgen and Matco Tools.

The name itself told a story. James A. Lico, current Danaher Executive Vice President and future President and Chief Executive Officer of Fortive, stated, "Fortive takes its name from the Latin root 'fort' meaning strong. Combined with a mark symbolizing forward momentum, growth and progress, the Fortive brand reflects the strength of our company—a company built on a foundation of success, and geared for growth and outperformance. This wasn't corporate marketing fluff—it was a declaration of intent.

James Lico, the chosen leader, embodied the Danaher way. James Lico, who will be President & CEO of Fortive, is a 20 year veteran of Danaher, and he will continue to run Fortive with the "common culture and operating system, the Danaher Business System". A mechanical engineer by training who had risen through the ranks running various Danaher operating companies, Lico understood something crucial: Fortive's competitive advantage wouldn't come from its products alone, but from its ability to operate them better than anyone else.

The mechanics of the spinoff were deliberately shareholder-friendly. Each Danaher shareholder will receive one share of Fortive common stock for every two shares of Danaher common stock held on June 15, 2016, the record date for the distribution. No cash required, no decisions to make—if you owned Danaher, you would own Fortive. Approximately 345 million shares of Fortive common stock were distributed in the separation.

The financial profile was compelling from day one. Fortive's revenues for the year ended December 31, 2014 were $6.3 billion. This wasn't a startup or a turnaround—it was a fully formed enterprise with established market positions and proven cash generation capabilities. Fortive will be headquartered in Everett, Washington, and will employ more than 20,000 people worldwide.

Importantly, the Rales brothers maintained skin in the game. The Rales brothers will own 12.1% of Fortive, ensuring alignment between the architects of the Danaher dynasty and this new chapter. They weren't abandoning ship; they were launching another vessel from their fleet.

As the separation date approached, Lico and his team worked behind the scenes to establish Fortive's independent infrastructure—treasury functions, IT systems, public company governance. But the most critical preparation was cultural. The Fortive Business System will be the core of our operating model, the cornerstone of our culture and our competitive advantage. Our outstanding team has a strong Danaher legacy and will continue to operate with the rigor and agility necessary to make continuous improvement a part of everything we do.

When July 2, 2016 arrived—that quiet Saturday—Fortive didn't emerge with fanfare or celebration. Today marks a major milestone for Fortive as we bring to the market our strong heritage and experienced management team, leading market positions, and culture of continuous improvement that is deeply rooted in 24,000 associates around the world, Lico stated. The real work was just beginning.

IV. The Core Portfolio & Crown Jewels

To understand Fortive's potential, you had to understand its assets—not as a random collection of industrial businesses, but as a carefully curated portfolio of essential technologies that touched nearly every aspect of modern life.

Fluke stood as the undisputed titan of the portfolio. Walk into any factory, power plant, or data center in the world, and you'd find Fluke's distinctive yellow digital multimeters. For four decades, "Fluke-tested" had become synonymous with reliability in electronic test equipment. The business wasn't sexy, but it was sticky—technicians trained on Fluke tools stayed with Fluke tools. The installed base numbered in the millions, creating an annuity-like stream of calibration services and replacement demand.

Tektronix brought gravitas to the portfolio—a company whose oscilloscopes had literally enabled the digital revolution. Founded in 1946, Tek (as insiders called it) had provided the measurement tools that allowed engineers to see electronic signals, debug circuits, and push the boundaries of what was possible in semiconductors and communications. While competitors came and went, Tektronix maintained its position through relentless innovation and deep customer relationships with everyone from Intel to NASA.

Gilbarco Veeder-Root might have seemed an odd fit—what did gas pumps have to do with oscilloscopes? But this was the genius of the Fortive portfolio: essential, mission-critical equipment with high switching costs. Gilbarco didn't just make fuel dispensers; it provided the entire ecosystem for gas station operations—from underground tank monitoring to point-of-sale systems to fleet management software. When a convenience store chain needed to upgrade its forecourt, Gilbarco was often the only call.

Matco Tools represented a different vector—a franchise-based distribution model selling professional automotive tools directly to mechanics. With over 1,800 franchisees driving Matco trucks to repair shops across America, it was a cash-generative business with remarkable resilience. Mechanics needed quality tools, and Matco's weekly visits, credit programs, and lifetime warranties created customer loyalty that big-box retailers couldn't match.

Kollmorgen and the automation businesses brought advanced motion control to industries from semiconductor manufacturing to medical devices. These weren't commodity products but highly engineered solutions where failure wasn't an option. A Kollmorgen servo motor might control a surgical robot or position a satellite dish—applications where precision and reliability justified premium pricing.

With 2015 revenues of $6.2 billion, Fortive's well-known brands hold leading positions in field instrumentation, transportation, sensing, product realization, automation and specialty, and franchise distribution. Fortive will be headquartered in Everett, Washington and employ a team of more than 24,000 research and development, manufacturing, sales, distribution, service and administrative employees in more than 40 countries around the world.

What tied these disparate businesses together wasn't product synergies but something more powerful: they all served essential functions in their customers' operations. You couldn't run a modern factory without test equipment. You couldn't operate a gas station without dispensers and monitoring systems. You couldn't build precision machines without motion control. This wasn't disruption waiting to happen—it was the bedrock infrastructure of the physical economy.

The financials reflected this essential nature: high margins, strong cash conversion, and recession-resistant demand. These businesses had weathered the 2008 crisis, the dot-com bust, and countless other downturns. They weren't high-growth software companies, but they didn't need to be. They were the picks and shovels of the industrial economy, and Fortive knew how to operate them better than anyone.

V. The Software Transformation Strategy (2017-2020)

Within months of independence, James Lico and his strategic team recognized a fundamental truth: the future of industrial technology wasn't just in hardware—it was in software and data. The question wasn't whether to transform, but how fast they could move without destroying what made them special.

The opening salvo came in July 2018, stunning the market with its ambition. In July 2018, Fortive announced it was buying software firm Accruent for about $2 billion. Accruent makes software to track real estate and facilities. This wasn't a bolt-on acquisition; it was a statement of intent. Accruent managed over 2 million facilities and 10 billion square feet of real estate globally through its cloud-based platform. For a company built on manufacturing excellence, spending $2 billion on software was heretical—or visionary.

James A. Lico, President and Chief Executive Officer of Fortive, stated: "We are excited to acquire a premium software asset of scale with strong upsell and cross-sell capabilities across the resource management ecosystem. The complementary strengths of Accruent, Gordian and Fluke Digital Systems will create an industry-leading IOT portfolio consisting of connected devices, software enabled workflows, and data analytics".

But Lico wasn't done. Also in July 2018, Fortive announced it would buy construction software company Gordian for $775 million from private equity firm Warburg Pincus. Gordian, based in Greenville, South Carolina, makes software that tracks costs of construction projects, manages facility operations and generally gives building companies more insight into big projects.

The Gordian acquisition revealed the strategic chess game Lico was playing. Gordian's comprehensive offerings serve the entire building lifecycle and provide workflow solutions to optimize every stage of an asset owner's construction and maintenance needs, including connecting the owner and contractors in the same exchange and providing access to cost and facilities metrics databases via a subscription-based model. This wasn't just buying software—it was buying network effects, data moats, and recurring revenue streams.

Then came the surprise move into healthcare. In June 2018, Fortive made a binding offer to buy Johnson & Johnson's Advanced Sterilization Products (ASP) business. The deal was valued at $2.8 billion, made up of $2.7 billion in cash from Fortive and $0.1 billion of retained net receivables, and closed in April 2019. ASP wasn't software, but it fit the pattern: mission-critical equipment with recurring consumables and service revenue, addressing the essential need of infection prevention in hospitals.

In 2018, ASP generated net revenue of approximately $800 million. The business brought Fortive into hospital sterile processing departments worldwide, with its STERRAD hydrogen peroxide sterilization systems setting the standard for low-temperature sterilization of sensitive medical instruments.

What outsiders missed was how these acquisitions interconnected. Accruent and Gordian weren't random software purchases—they were building blocks of an integrated workplace management platform. Facilities managers could plan construction projects with Gordian's cost databases, manage ongoing operations with Accruent's software, and monitor equipment performance with Fluke's connected instruments. The whole became greater than the sum of its parts.

By 2020, the transformation was showing results. Software and recurring revenue grew from less than 10% of Fortive's revenue to over 30%. The company wasn't abandoning its industrial heritage—it was augmenting it. A Fluke multimeter now connected to the cloud, streaming diagnostic data. Gilbarco dispensers integrated with loyalty programs and mobile payments. The physical and digital worlds were converging, and Fortive positioned itself at the intersection.

The cultural transformation proved equally important. Fortive had to learn the rhythms of software businesses—subscription models, cloud architecture, agile development. Engineers who had spent careers perfecting hardware precision now worked alongside software developers pushing code daily. The Fortive Business System adapted, incorporating software-specific metrics like monthly recurring revenue and customer churn alongside traditional measures like on-time delivery and inventory turns.

VI. The ServiceChannel Acquisition & SaaS Acceleration (2021)

The ServiceChannel acquisition in 2021 marked Fortive's coming-of-age as a software-first industrial technology company. The purchase price for the acquisition is approximately $1.2 billion and is expected to be funded primarily with available cash. For a company that had spun off from Danaher just five years earlier, deploying over a billion dollars in cash for a pure-play SaaS business was a bold declaration of strategic clarity.

James A. Lico, President and Chief Executive Officer of Fortive, stated: "We are very excited to announce the pending acquisition of ServiceChannel. This transaction is another great example of how we continue to use disciplined capital deployment to accelerate our long-term strategy across our segments. ServiceChannel fits extremely well alongside Accruent and Gordian, broadening our offering of software-enabled solutions for the Facility and Asset Lifecycle workflow.

The numbers told a compelling story. Fortive expects ServiceChannel to generate approximately $125 million of revenue in 2021, with recurring revenue of approximately $117 million. But the strategic value exceeded the financials.

ServiceChannel was founded in 1999 and serves more than 500 enterprise customers in over 70 countries across the globe, while also maintaining an integrated network of more than 70,000 facilities maintenance service providers. ServiceChannel's SaaS offering enables multi-site owner / operators to manage and automate the full lifecycle of workflows related to the maintenance and repair of their properties and related assets, including work order management, asset tracking, and service provider tracking.

What made ServiceChannel special wasn't just its software—it was its network. The Company's differentiated data-driven platform, which combines software with a service-provider network, draws from millions of data points to intelligently match contractors with jobs, enhancing quality, cost transparency and efficiency. Every work order processed, every contractor evaluated, every invoice approved added to a data asset that became more valuable over time.

The integration with Accruent and Gordian created a facilities management powerhouse. A retailer could now use Gordian to plan a store renovation, Accruent to manage the lease and operations, and ServiceChannel to coordinate all maintenance activities. The platform processed billions of dollars in facilities spending annually, creating switching costs that made customer relationships incredibly sticky.

James A. Lico, President and Chief Executive Officer of Fortive, stated: "We are excited to announce the closing of the ServiceChannel acquisition and welcome the ServiceChannel team to Fortive. As we integrate ServiceChannel into the IOS segment, the company's high-growth SaaS platform, deep contractor network, valuable data assets, and existing global footprint will significantly enhance our broader offering of software-enabled solutions for the Facility and Asset Lifecycle workflow.

The acquisition also accelerated Fortive's SaaS capabilities. ServiceChannel brought modern cloud architecture, product-led growth strategies, and a culture of rapid iteration. The company's leadership team, seasoned in scaling enterprise SaaS, provided expertise that would benefit the entire Intelligent Operating Solutions segment.

By the time the acquisition closed in August 2021, Fortive had transformed its portfolio composition dramatically. Software and services now represented nearly 40% of revenue, with clear line of sight to crossing 50%. More importantly, the quality of revenue had improved—more recurring, more predictable, with higher margins and better growth prospects.

VII. Portfolio Optimization & Divestitures (2018-2025)

While Fortive was building its software empire with one hand, it was pruning its portfolio with the other. The discipline to sell good businesses that no longer fit the strategic vision proved as important as the courage to make transformative acquisitions.

The first major divestiture came in October 2018. Altra Industrial Motion Corp. ("Altra") (NASDAQ: AIMC), a global manufacturer and marketer of electromechanical power transmission and motion control products, today announced the completion of Altra's combination with four operating companies from Fortive's Automation & Specialty platform ("Fortive A&S"), including market leading brands Kollmorgen, Thomson, Portescap and Jacobs Vehicle Systems.

The transaction was valued at approximately $2.9 billion, based on Fortive receiving $1.4 billion of cash proceeds and debt instruments and Fortive stockholders receiving 35 million newly issued shares of Altra common stock. The deal structure—a Reverse Morris Trust—allowed Fortive to exit these businesses tax-efficiently while giving shareholders continued participation in their future success.

The automation businesses were excellent operators with strong market positions. The A&S platform generated approximately $907 million in revenue for its fiscal year ended December 2017. But they were capital-intensive, component-focused businesses that didn't align with Fortive's software-led future. By combining them with Altra, Fortive created value for all stakeholders while sharpening its own strategic focus.

The discipline continued through the years, with smaller divestitures and facility optimizations generating cash for reinvestment. Each decision followed the same logic: keep businesses that provided essential, mission-critical solutions with recurring revenue potential; divest those that were commoditizing or required significant capital investment without commensurate returns.

The culmination of this portfolio optimization strategy came in 2024-2025 with the decision to spin off the Precision Technologies segment. Today's announcement marks the next step forward in Fortive's evolution. Once the spin-off is complete, Fortive will be more focused on recurring revenue and software businesses, and better positioned to accelerate growth and consistently grow earnings and free cash flow. Similarly, our Precision Technologies business will thrive as a standalone public company, focused on key secular growth trends powering the world's technology advancements.

Fortive Corporation ("Fortive") (NYSE: FTV) today announced that its Precision Technologies segment expected to be separated as a new independent, public company has been named Ralliant Corporation ("Ralliant"). Ralliant is trusted for precision technologies that advance next generation innovation and safeguard mission-critical applications through leading brands in test and measurement, specialty sensors, and aero, defense, and space subsystems.

The Ralliant spinoff, completed on June 28, 2025, represented the final transformation of Fortive from industrial conglomerate to focused technology leader. In connection with the separation, on June 28, 2025, Fortive shareholders received one share of common stock of Ralliant for every three shares of common stock of Fortive held at the close of business on June 16, 2025 (other than fractional shares, which will be aggregated and sold and the proceeds distributed to Fortive shareholders). Approximately 113 million shares of Ralliant common stock were distributed in the separation.

Ralliant provided Fortive with $1.15 billion in cash consideration, sourced from new term loans. This capital would fuel further investment in software and share buybacks, continuing the virtuous cycle of portfolio optimization and value creation.

The strategic logic was impeccable. New Fortive emerges with a strong financial track record with robust free cash flow generation, approximately 50% recurring revenue, significant competitive advantages, and a strategic orientation toward attractive markets with strong secular tailwinds. Meanwhile, Ralliant could pursue its own destiny in precision measurement and aerospace markets, unencumbered by corporate priorities focused on software and recurring revenue.

VIII. The Fortive Business System (FBS) Deep Dive

At the heart of Fortive's success lay something that couldn't be acquired or financial engineered: the Fortive Business System (FBS). With a culture rooted in continuous improvement, the core of our company's operating model is the Fortive Business System. While competitors talked about operational excellence, Fortive lived it every single day.

The system's roots traced directly to the Toyota Production System via Danaher, but FBS had evolved into something uniquely suited for the digital age. Walk into any Fortive facility—whether a Fluke manufacturing plant in Washington or an Accruent software development center in Texas—and you'd see the same visual management boards, the same problem-solving methodologies, the same relentless focus on customer value.

The power of FBS came from its universality. Whether you were debugging software code or assembling oscilloscopes, the core principles applied: eliminate waste, reduce variation, accelerate flow. Every employee, from factory workers to software engineers, learned the common language of value streams, root cause analysis, and PDCA (Plan-Do-Check-Act) cycles.

Our unique culture rooted in our powerful Fortive Business System (FBS) has been critical to the value we've driven over this period, Lico emphasized repeatedly. This wasn't corporate propaganda—the numbers proved it. Fortive consistently delivered operating margins above industry averages, working capital efficiency that freed up hundreds of millions in cash, and new product development cycles that outpaced competitors.

What made FBS special in the software era was its adaptability. Traditional lean manufacturing focused on physical waste—excess inventory, unnecessary motion, defects. FBS expanded this to digital waste—redundant code, unclear requirements, technical debt. Software teams adopted agile methodologies but supercharged them with FBS discipline. Sprint retrospectives became kaizen events. User story mapping borrowed from value stream analysis.

The acquisition integration playbook showcased FBS at its best. When Fortive acquired Accruent, the software company was losing money despite strong revenue growth. Within 18 months, FBS-driven improvements had transformed the business: customer churn reduced by 30%, software deployment cycles cut in half, and margins expanded by over 1,000 basis points. The magic wasn't in slashing costs—it was in systematically identifying and eliminating friction in every process.

Mr. Lico continued, "We have a proven track record of evolving Fortive to ensure sustained performance. Our enhanced portfolio of leading brands and dedication to the Fortive Business System have enabled us to deliver consistent, compounding results over the past five years.

The cultural component proved equally crucial. FBS wasn't imposed top-down but embraced bottom-up. Frontline employees were empowered to identify problems and implement solutions. The daily kaizen mindset meant thousands of small improvements compounded into transformational change. A software developer might reduce code review time by 15 minutes. A customer service rep might eliminate two steps from a support process. Individually minor, collectively powerful.

The innovation acceleration through FBS surprised outsiders who associated lean with cost-cutting. By eliminating waste in development processes, Fortive could actually invest more in R&D while achieving better outcomes. Products reached market faster. Customer feedback cycled into improvements quicker. The competitive advantage compounded over time.

IX. Financial Performance & Capital Allocation

The financial results validated the strategy. For the full year, revenues increased 3% year-over-year to $6.23 billion, which included 1% core revenue growth. While the headline growth appeared modest, the underlying transformation was profound.

For the full year 2025, Fortive anticipates revenue of approximately $6.23 billion to $6.35 billion, diluted net earnings per share of $2.38 to $2.50, and adjusted diluted net earnings per share of $4.00 to $4.12. These projections reflected a business in transition—steady performance despite massive portfolio changes.

The real story emerged in the quality of earnings. Recurring revenue had grown from less than 20% at spinoff to approaching 50% post-Ralliant separation. Software gross margins exceeded 70%, pulling up the overall margin profile. Most importantly, free cash flow generation remained robust, consistently exceeding net income—the hallmark of a well-run industrial company.

Capital allocation under Lico followed a clear hierarchy: first, invest in organic growth through R&D and commercial expansion; second, pursue strategic acquisitions that accelerated the software transformation; third, return excess capital to shareholders through buybacks and dividends. The discipline was remarkable—Fortive walked away from multiple acquisition targets when valuations didn't meet their return thresholds.

The M&A track record spoke volumes. Since independence, Fortive had deployed over $7 billion in acquisitions, fundamentally reshaping its portfolio while maintaining strong returns on invested capital. The company targeted 10% ROIC within five years for major acquisitions—a hurdle that forced strategic discipline.

The share buyback program accelerated following major divestitures. After the Ralliant separation and its $1.15 billion cash payment, Fortive announced aggressive repurchase authorizations. This wasn't financial engineering—it was confidence in the transformed portfolio's ability to compound value.

Working capital management, a core FBS competency, consistently generated cash. By reducing inventory levels, accelerating collections, and optimizing payment terms, Fortive freed up hundreds of millions in cash without impacting operations. This operational financing reduced reliance on external capital markets.

The balance sheet remained conservative despite the acquisition spree. Fortive maintained investment-grade credit ratings, providing flexibility for opportunistic moves. The company's banker presentations emphasized not growth at any cost, but sustainable, profitable expansion backed by operational excellence.

X. Leadership Transition & The Next Era (2024-2025)

The announcement of James Lico's retirement marked the end of an era. At the completion of the spin-off, James A. Lico will retire as President and CEO and as a director. Upon Mr. Lico's retirement, Olumide Soroye, current President and CEO of Fortive's Intelligent Operation Solutions segment, will be appointed as President, CEO, and a director of Fortive.

Mr. Lico said, "I couldn't be prouder of what our team has accomplished since Fortive's launch in 2016. We are driving meaningful progress in the world and delivering differentiated results, backed by our proven Fortive Business System. His legacy was undeniable: transforming an industrial spinoff into a technology leader while maintaining operational excellence.

Olumide Soroye represented both continuity and change. An insider who understood FBS deeply, but also a leader with fresh perspectives on digital transformation and growth acceleration. His appointment signaled that Fortive's next chapter would build on its foundation while pushing into new frontiers.

Today marks the beginning of bold and exciting new chapters for both Fortive and Ralliant as independent, purpose-built companies, each poised to unlock significant value for shareholders," Mr. Soroye stated. "New Fortive emerges with a strong financial track record with robust free cash flow generation, approximately 50% recurring revenue, significant competitive advantages, and a strategic orientation toward attractive markets with strong secular tailwinds.

Tami Newcombe, current President and CEO of Fortive's Precision Technologies and Advanced Healthcare Solutions business segments, will assume the role of President and CEO of NewCo in connection with the separation. The leadership bench depth—developed through FBS talent cultivation—ensured smooth transitions across both companies.

The strategic priorities under Soroye were clear: accelerate software innovation, expand recurring revenue streams, and pursue international growth. But the core would remain unchanged—FBS as the operational foundation, disciplined capital allocation, and relentless focus on customer value.

XI. Playbook: Business & Investing Lessons

The Fortive story offers a masterclass in industrial transformation and value creation. The lessons extend far beyond manufacturing into any business seeking sustainable competitive advantage.

The Power of Operational Excellence Systems: FBS proved that operational excellence isn't a project but a culture. Companies that embed continuous improvement into their DNA create compounding advantages that financial engineering can never match. The discipline to apply these principles consistently—through acquisitions, across industries, amid transformation—separates winners from wannabes.

Successful Spinoff Execution: Fortive demonstrated how spinoffs can create value for all stakeholders. By maintaining strategic clarity (Danaher toward life sciences, Fortive toward industrial technology), both companies could optimize their portfolios and operating models. The Ralliant separation followed the same playbook—creating focused entities better positioned to serve their markets.

Portfolio Transformation Methodology: The journey from hardware to software wasn't random but methodical. Start with adjacencies (Fluke's connected instruments), move to platforms (Accruent/Gordian), then accelerate with network effects (ServiceChannel). Each step built on the previous, reducing execution risk while maintaining strategic momentum.

Roll-up Strategy in Fragmented Markets: Facilities management software was highly fragmented—hundreds of point solutions serving specific needs. Fortive's roll-up created a platform that offered integrated solutions, delivering more value to customers while building competitive moats through data and network effects.

Building Synergies Without Forcing Integration: Rather than immediately merging acquisitions, Fortive let businesses maintain their identities while sharing FBS practices and customer relationships. Accruent, Gordian, and ServiceChannel continued operating independently while collaborating on joint solutions. This preserved entrepreneurial energy while capturing synergies.

Culture as Sustainable Competitive Advantage: FBS proved that culture, properly cultivated, becomes a moat competitors cannot cross. The systematic approach to problem-solving, the empowerment of frontline workers, the relentless focus on improvement—these cultural elements drove performance more than any strategy or structure.

Managing Complexity While Maintaining Focus: Operating diverse businesses—from gas pumps to hospital sterilizers to facilities software—requires exceptional management systems. Fortive showed how FBS could provide common language and operating cadence while allowing businesses to serve their unique markets.

XII. Bear vs. Bull Case & Final Analysis

The Bull Case rests on transformation momentum. Fortive has successfully pivoted from industrial conglomerate to software-enabled technology leader. With ~50% recurring revenue, strong free cash flow generation, and proven M&A execution, the company can compound value through organic growth and strategic acquisitions. FBS provides a sustainable competitive advantage that drives operational improvements across any business. The focused portfolio post-Ralliant allows management to accelerate software investments and capture larger markets. Healthcare exposure through ASP offers recession resistance and demographic tailwinds.

The Bear Case highlights execution risks. Software competition intensifies as pure-play SaaS companies enter industrial markets with modern architectures and aggressive pricing. The integration complexity of multiple acquisitions could overwhelm management and dilute FBS effectiveness. Valuation multiples for industrial technology companies remain below software peers, limiting multiple expansion potential. Economic sensitivity in core industrial end markets could pressure results despite portfolio transformation. The loss of Lico's leadership and institutional knowledge might impact execution excellence.

Comparing to peers illuminates Fortive's unique position. Versus Danaher, Fortive trades at a discount despite similar operational excellence—the parent's life science focus commands premium multiples. Against Roper Technologies, another serial acquirer, Fortive's FBS provides differentiated operational capabilities but Roper's software concentration is higher. Compared to IDEX, Fortive offers more scale and transformation upside but potentially more complexity.

The future of industrial technology conglomerates likely mirrors Fortive's journey—those that successfully blend operational excellence with digital transformation will thrive. Pure industrial players will struggle with commoditization and cyclicality. Pure software players will lack the domain expertise and customer relationships. The sweet spot lies in Fortive's hybrid model—industrial expertise enhanced by software capabilities.

XIII. Epilogue & Reflections

Standing back from the detailed narrative, Fortive's journey from Danaher spinoff to independent technology leader offers profound lessons about business transformation in the 21st century. The company proved that operational excellence, often dismissed as old-economy thinking, remains devastatingly effective when properly applied to modern challenges.

What would the founders do differently? Perhaps move faster into software—the 2018 acquisitions could have happened in 2016. Maybe preserve more of the precision technology businesses that showed software potential. Certainly communicate the transformation story more clearly to investors who struggled to value the hybrid model.

The legacy of the Danaher/Fortive model extends beyond financial returns. Thousands of executives trained in DBS/FBS now lead other companies, spreading operational excellence practices across industries. The demonstration that conglomerates can successfully transform—rather than simply financial engineer—provides a roadmap for industrial companies facing digital disruption.

For investors, Fortive validates the power of patient capital married to operational excellence. The highest returns don't always come from the flashiest technologies or the most promotional management teams. Sometimes they come from the methodical application of proven principles to essential businesses. The compound effect of continuous improvement, strategic portfolio management, and disciplined capital allocation creates value more sustainably than any disruption.

As Fortive enters its next chapter under Olumide Soroye's leadership, the foundation is solid. The portfolio is focused, the culture is strong, and the markets are attractive. Whether the company can accelerate growth while maintaining operational discipline will determine if this industrial transformation story has another successful act. But if history is any guide, betting against the Fortive Business System has never been wise.

The ultimate lesson may be this: in an era obsessed with disruption, there's enormous value in execution. While competitors chase the next big thing, companies like Fortive create value through the accumulated power of doing thousands of small things right, every day, with systematic discipline. It's not sexy, it's not viral, but it works. And in business, as in life, what works ultimately wins.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube