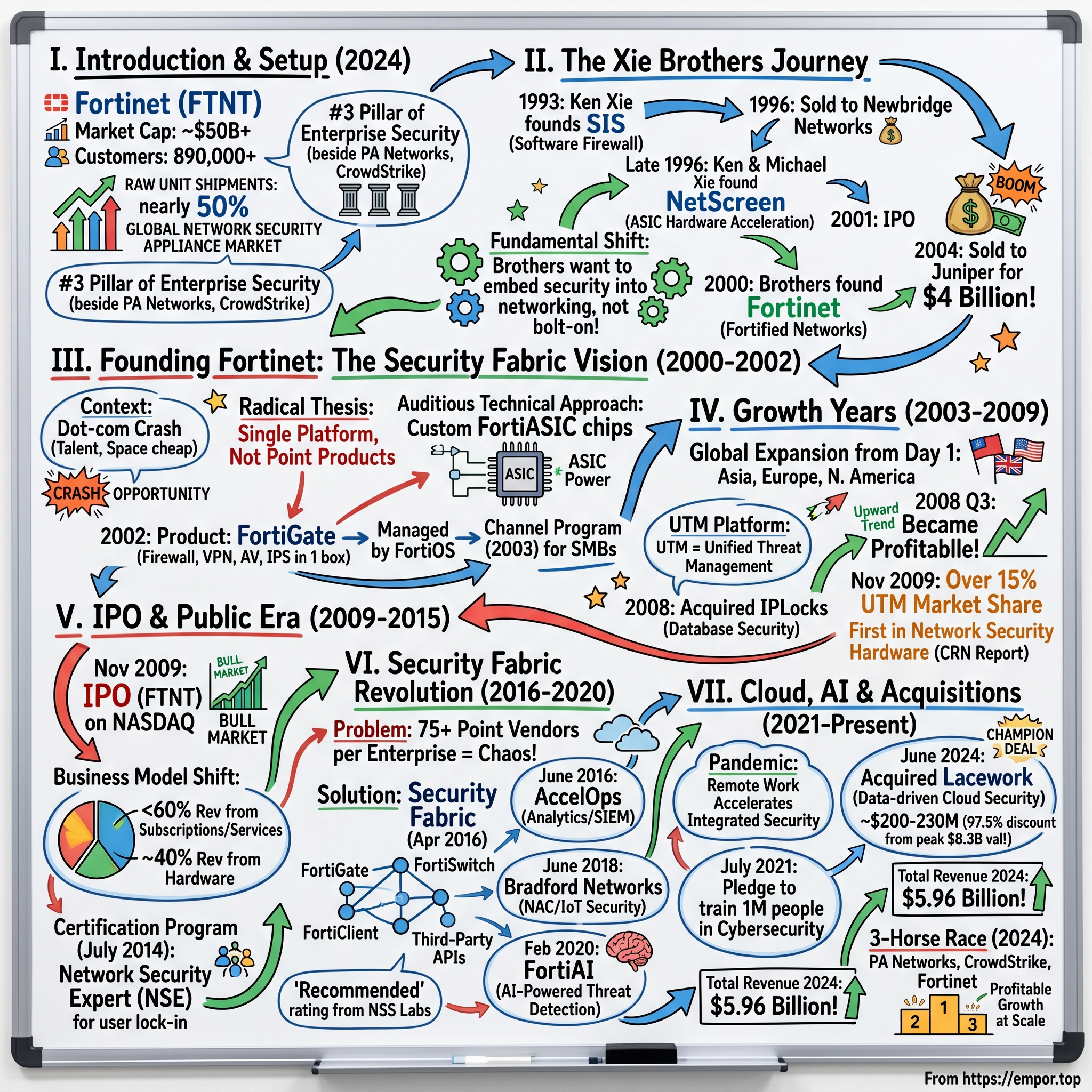

Fortinet: The Brothers Who Built the Third Pillar of Cybersecurity

I. Introduction & Episode Setup

Picture this: It's 2024, and a massive cybersecurity vendor you've probably never heard much about quietly processes more network traffic than Netflix, protects more organizations than Microsoft has Office customers, and ships more security appliances than Cisco. This is Fortinet—the $50 billion empire built by two brothers who had already created and sold two successful security companies before most people even knew what a firewall was.

The numbers are staggering: 890,000 customers globally, from corner coffee shops running a single FortiGate appliance to Fortune 100 enterprises with thousands of devices. In raw unit shipments, Fortinet commands nearly 50% of the global network security appliance market. Yet in Silicon Valley cocktail parties and tech Twitter debates, it's Palo Alto Networks and CrowdStrike that dominate the conversation. How did a company this massive stay so relatively under the radar?

The answer lies in the unique DNA of its founders. Ken and Michael Xie didn't build Fortinet to win TechCrunch headlines or Sand Hill Road beauty contests. They built it to solve a fundamental problem they'd seen twice before: security was always an afterthought, bolted on after networks were designed, added as an overlay after applications were built. Their radical thesis in 2000—that security needed to be embedded into the very fabric of networking itself—seemed obvious in hindsight but was heretical at the time. Today, Fortinet has a market cap of $57.14 billion, with total revenue of $5.96 billion for 2024, an increase of 12.3% compared to $5.30 billion in 2023. The company has become the third pillar of enterprise security alongside Palo Alto Networks and CrowdStrike, but with a fundamentally different approach—one rooted in the belief that security and networking are not separate disciplines but two sides of the same coin.

What makes the Fortinet story particularly compelling isn't just the financial success—it's the path taken. While competitors fought feature wars and marketing battles, the Xie brothers quietly built the industry's broadest security platform, accumulated over 1,000 patents (nearly triple their nearest competitor), and created what might be the most underappreciated cash flow machine in technology. This is the story of how two immigrant engineers built not one, not two, but three defining cybersecurity companies, and why their third act might be their greatest.

II. The Xie Brothers: From China to Silicon Valley

The boardroom at Juniper Networks in early 2004 was tense. Ken Xie sat across from Scott Kriens, Juniper's CEO, finalizing the last details of what would become a $4 billion acquisition of NetScreen, the firewall company Ken had co-founded just eight years earlier. As lawyers shuffled papers and bankers calculated earnout provisions, Ken's mind was already elsewhere. He'd done this before—built SIS and sold it successfully in 1996. Now NetScreen was about to make him and his brother Michael enormously wealthy. But Ken saw something others didn't: the entire security industry was solving the wrong problem.

Ken's journey to that boardroom began in Beijing, where he was born into an academic family that valued education above all else. His path seemed preordained: Tsinghua University for his bachelor's and master's in electrical engineering, then on to an academic career. Tsinghua, often called the "MIT of China," was where China's technical elite were forged, and Ken excelled there, graduating with honors in both programs. His parents fully expected him to become a professor.

But Stanford changed everything. Arriving in Palo Alto in the late 1980s to pursue another master's degree, Ken discovered something intoxicating about Silicon Valley that had nothing to do with academic prestige. "My parents wanted me to get a PhD and teach," Ken would later recall in a rare interview. "But I walked around Stanford and saw all these companies being born in garages and dorm rooms. I thought—why write papers when you can build products?"

His younger brother Michael took a different route to North America, earning his electrical engineering degree from the University of Manitoba in Canada. Where Ken was the visionary who could see around corners, Michael was the technical perfectionist who could turn those visions into silicon and code. Their complementary skills would prove to be a powerful combination.

In 1993, Ken founded Systems Integration Solutions (SIS), his first company, focused on firewall and network security products. It was a modest success, selling to Newbridge Networks in 1996 for an undisclosed sum—enough to establish Ken's credibility but not enough to retire on. The real education from SIS wasn't the exit; it was understanding the fundamental limitations of software-based security. CPUs were getting faster, but network traffic was growing exponentially faster. Software firewalls were becoming the bottleneck.

This insight led to NetScreen, founded in late 1996 in the most Silicon Valley way possible: in a Palo Alto garage. Ken's radical idea was to build the firewall functions directly into ASIC (Application-Specific Integrated Circuit) chips rather than running them on general-purpose CPUs. It was like the difference between having a dedicated chef's knife versus trying to cook with a Swiss Army knife—purpose-built hardware could process packets 10 to 100 times faster than software.

NetScreen's timing was perfect. The dot-com boom was creating an explosion in internet traffic, and enterprises were desperate for security solutions that wouldn't slow their networks to a crawl. By 2001, NetScreen had gone public at a $300 million valuation. Three years later, Juniper acquired it for $4 billion—a 13x return that made Ken and Michael wealthy beyond their parents' dreams.

But here's where the story takes an unexpected turn. Most entrepreneurs who've just banked billions either retire to become venture capitalists or chase completely different industries. The Xie brothers did neither. Within months of the Juniper acquisition closing, they were back in startup mode, founding Fortinet in 2000 (yes, they actually started Fortinet while still running NetScreen—a detail that would later cause some legal complications).

Why start company number three? Ken's answer revealed his deeper insight: "NetScreen solved the firewall problem. But security isn't a product—it's a fabric that needs to be woven into everything. Every packet, every application, every user interaction needs security built in, not bolted on."

The brothers had learned something crucial from their first two companies: in cybersecurity, being early is almost as bad as being late. SIS was perhaps too early for the enterprise firewall market. NetScreen hit the timing perfectly for hardware acceleration. With Fortinet, they believed they were early again—but this time, they had the patience and capital to wait for the market to catch up to their vision.

Their approach to building Fortinet would be radically different. No quick flip this time. No narrow product focus. They would build for the long term, creating not just a product or even a product line, but an entire platform that could evolve with threats that didn't even exist yet. It was an ambitious goal that would require them to be not just entrepreneurs but institution builders. The question was: could they pull it off a third time?

III. Founding Fortinet: The Security Fabric Vision (2000–2002)

The conference room at Benchmark Capital in late 2000 was a graveyard of startup dreams. The dot-com crash had turned Sand Hill Road from the epicenter of innovation into triage central, with VCs trying to figure out which of their portfolio companies might survive. Into this carnage walked Ken and Michael Xie with a pitch that seemed almost absurdly ambitious: they wanted to build a security company that would make every other security product obsolete.

The name itself—Fortinet—was a portmanteau of "Fortified Networks," capturing their vision in eight letters. But the timing seemed catastrophic. The NASDAQ had crashed 78% from its peak. Security companies were folding left and right. Enterprises were slashing IT budgets. Starting a new security company in 2000 was like opening a restaurant during a famine.

Yet the Xie brothers saw opportunity where others saw disaster. "Everyone was pulling back, which meant talent was available, real estate was cheap, and customers were actually more serious about security than ever," Ken would later explain. The dot-com crash had exposed how vulnerable digital infrastructure really was. Companies that survived needed security more than ever—they just needed it to be simpler and more affordable.

Their founding thesis was radical for its time: security shouldn't be a collection of point products from different vendors, each with its own management console, update cycle, and integration challenges. Instead, security should be like a fabric—unified, consistent, and woven into the very infrastructure of networking itself. This meant building not just a firewall, but an entire platform that could handle firewalling, VPN, antivirus, intrusion prevention, web filtering, and capabilities that didn't even exist yet.

The technical approach was even more audacious. While everyone else was moving to software and virtual appliances, Fortinet doubled down on custom silicon. They would design their own ASICs—the FortiASIC—that could perform security functions at wire speed. This required massive upfront investment and deep technical expertise, but the Xie brothers believed it would give them an insurmountable performance advantage.

By early 2001, they had raised $13 million from a combination of angel investors and early VCs who believed in the team more than the market timing. The money was enough to hire a small team of engineers, many poached from NetScreen before the Juniper acquisition closed (another move that would later cause legal headaches). They set up shop in Sunnyvale, deliberately avoiding the Palo Alto prestige addresses to keep costs down.

The first two years were brutal. While competitors were shipping products and generating revenue, Fortinet was in pure R&D mode, burning cash to build their unified platform. The FortiGate firewall, their first product, didn't launch until 2002—two full years after founding. But when it arrived, it was unlike anything else on the market. A single box could function as a firewall, VPN concentrator, antivirus gateway, and intrusion prevention system. More importantly, it was all managed through a single interface, FortiOS, which would become the cornerstone of everything Fortinet built.

The early customer conversations were revealing. IT administrators loved the concept but were skeptical about putting all their security eggs in one basket. "What happens if Fortinet goes out of business?" was a common question—not unreasonable given the carnage in the security market. The Xie brothers' answer was to over-deliver on the basics: the FortiGate was faster and more reliable than competing firewalls, even if customers never used the additional features. Fortinet introduced its first product, FortiGate, in 2002, followed by anti-spam and anti-virus software. But what made it revolutionary wasn't just the unified functionality—it was the business model innovation. Instead of selling different products with different license keys, support contracts, and upgrade cycles, Fortinet offered a single subscription that covered everything. This was heretical in an industry built on selling customers as many SKUs as possible.

By October 2003, they had established their first channel program, recognizing early that direct sales wouldn't scale to the SMB market they needed to capture. The company began distributing its products in Canada in December 2003, choosing to expand internationally before they'd even conquered their home market—another contrarian move that would pay dividends later.

The legal challenges started almost immediately. In May 2004, Trend Micro filed a patent infringement complaint, claiming Fortinet had violated their antivirus patents. It would take six years to resolve, with the patents ultimately being declared invalid in 2010, but the lawsuit cast a shadow over the company's early years and complicated fundraising efforts. There was also the awkward matter of GPL compliance issues and questions about whether the Xie brothers had started developing Fortinet technology while still at NetScreen.

But perhaps the most important decision made in these early years was one that seemed minor at the time: the creation of FortiGuard Labs in 2002. This would become Fortinet's threat intelligence operation, eventually processing over 100 billion security events daily. While competitors outsourced threat intelligence or relied on third-party feeds, Fortinet built their own global sensor network. It was expensive and thankless work, but it gave them proprietary threat data that would become invaluable as security shifted from signature-based to behavioral detection.

By the end of 2002, Fortinet had burned through most of their initial funding with only a handful of customers to show for it. The board was getting nervous. Competitors were gaining market share. The dot-com nuclear winter showed no signs of thawing. But the Xie brothers had been here before with NetScreen—they knew that in enterprise technology, being too early was indistinguishable from being wrong until suddenly, almost overnight, you were right. The question was whether they had enough runway to wait for that moment to arrive.

IV. The Growth Years: From Startup to Profitability (2003–2009)

The sales kickoff meeting in January 2004 was held in a Sunnyvale conference room that could barely fit the company's 40 employees. Ken Xie stood before a whiteboard covered in ambitious numbers that seemed almost delusional given their current revenue run rate. "By 2009," he declared, "we'll be public with over $300 million in annual revenue." The room was silent. They'd closed 2003 with less than $5 million in bookings.

What happened next was one of the most methodical expansions in enterprise technology history. By 2004, Fortinet had offices in Asia, Europe, and North America, but these weren't vanity offices or token outposts. Each was a fully functional operation with local sales, support, and even R&D capabilities. The strategy was deliberate: while American competitors focused on the Fortune 500, Fortinet would build a global footprint from day one, capturing the mid-market worldwide.

The product evolution during this period was relentless. What started as a firewall with some additional features evolved into a true unified threat management (UTM) platform. By 2005, the FortiGate could handle firewalling, VPN, antivirus, intrusion prevention, web filtering, anti-spam, and WAN optimization—all in a single box, all managed through one interface. Competitors mocked it as a "Swiss Army knife" approach, arguing that specialized solutions would always outperform integrated ones. They were wrong.

The performance numbers told the story. A FortiGate 5000 series appliance could process 20 Gbps of firewall throughput—comparable to Cisco's ASA series—while simultaneously running full antivirus scanning at 5 Gbps. Cisco's solution required separate boxes for each function, tripling the rack space and quadrupling the management complexity. For the emerging markets Fortinet was targeting, where IT staff and data center space were at a premium, this wasn't just a nice-to-have—it was transformative. Fortinet became profitable in the third quarter of 2008. This was remarkable timing—achieving profitability just as the global financial crisis was decimating IT budgets worldwide. The secret was their business model: while competitors relied heavily on high-touch enterprise sales with long cycles and huge commissions, Fortinet had built a high-velocity, channel-driven model that could profitably serve a $50,000 deal as easily as a $5 million one.

By November 2009, Fortinet held over 15 percent of the unified threat management market. But more impressively, CRN Magazine's survey-based annual report card placed Fortinet first in network security hardware, up from seventh position just two years earlier. This wasn't just market share growth—it was a complete disruption of the established order.

The early acquisitions during this period were surgical and strategic. In 2008, the company acquired the intellectual property of IPLocks, a database security and auditing company. In August 2009, Fortinet acquired the intellectual property and other assets of Woven Systems, an Ethernet switching company. These weren't splashy deals meant to grab headlines. They were technology tuck-ins that filled specific gaps in the Security Fabric vision.

The market dynamics during this period were fascinating. Cisco, the 800-pound gorilla of networking, was struggling to make security a meaningful part of their business despite multiple acquisitions. Check Point, the firewall pioneer, was increasingly looking like a legacy vendor, milking their installed base rather than innovating. Juniper, despite owning NetScreen, never fully integrated it into their portfolio. This left a massive opportunity for a unified platform player, and Fortinet was racing to fill it.

By late 2009, the company had grown to over 1,000 employees across 23 offices globally. Revenue was approaching $300 million annually. The board began discussing an IPO, not because they needed the capital—they were profitable and cash-flow positive—but because going public would provide currency for acquisitions and credibility with large enterprises. The timing seemed terrible: the markets were still recovering from the financial crisis, tech IPOs were rare, and investor appetite for infrastructure companies was minimal. But Ken Xie had learned from NetScreen that sometimes the worst market conditions create the best opportunities for those brave enough to seize them.

V. The IPO and Public Company Era (2009–2015)

The road show presentations in October 2009 were brutal. Ken Xie and his CFO Ken Goldman faced room after room of skeptical institutional investors who had been burned by tech IPOs during the financial crisis. "Why should we believe you're different from Check Point or Sourcefire?" was the polite version of what they heard. The harsh version included profanity and suggestions that hardware security was dead.

The initial public offering (IPO) of Fortinet took place in November 2009, and the company's shares started trading on the NASDAQ Global Market using the ticker code FTNT. A total of $156 million had been raised by the business by the time the first day of trading came to a close. The IPO priced at $12.50 per share, giving the company a valuation of roughly $800 million—modest by today's standards but respectable given the market conditions.

What happened next surprised everyone, including Fortinet's own bankers. The stock surged on the first day of trading, closing up over 30%. This wasn't retail enthusiasm—institutional investors who had passed on the IPO were scrambling to get in. They had suddenly realized what Fortinet really was: not just another security vendor, but a platform company with recurring revenue characteristics trading at hardware multiples.

According to the International Data Corporation (IDC), Fortinet had the highest share of the market for unified threat management by the year 2010, with yearly sales of $324 million. But the real story wasn't the revenue growth—it was the business model transformation happening under the hood. By 2010, over 60% of revenue came from subscriptions and services, not hardware. Customers bought FortiGate appliances, but what they really paid for over time was the FortiGuard security subscriptions, support, and constant updates.

The acquisition strategy during this period evolved from technology tuck-ins to capability expansion. Fortinet made four acquisitions from 2012 to 2016. The company acquired app-hosting service XDN (formerly known as 3Crowd) in December 2012, Coyote Point in 2013, and Wi-Fi hardware company Meru Networks in 2015. The Meru Networks deal was particularly significant—a $44 million acquisition that gave Fortinet enterprise-grade wireless infrastructure to compete with Cisco's dominant position in campus networks.

But the most important development during this period wasn't an acquisition—it was a program. In July 2014, Fortinet announced a technical certification program called the Network Security Expert (NSE) program. This might seem like a minor administrative detail, but it was actually strategic genius. By creating a certification program, Fortinet was building an army of trained professionals whose careers would be tied to Fortinet's success. Cisco had proven with CCNA and CCIE that certification programs create powerful network effects and customer lock-in. Fortinet was following the playbook but adapting it for the security era.

The competitive landscape during this period was shifting dramatically. Palo Alto Networks had gone public in 2012 with a next-generation firewall message that resonated with enterprises. FireEye was riding the advanced persistent threat (APT) wave. New cloud-native vendors like Zscaler were emerging. The security market was fragmenting into dozens of point solutions, each claiming to solve a specific problem. Fortinet's response was counterintuitive: instead of focusing on a specific threat or use case, they doubled down on integration and breadth.

The financial performance during this era validated the strategy. Revenue grew from $324 million in 2010 to over $770 million by 2014. More importantly, gross margins expanded from the low 70s to nearly 80%, proving that the unified platform approach could be both comprehensive and profitable. The company was generating significant free cash flow, enabling both organic R&D investment and strategic acquisitions without dilution.

By 2015, Fortinet had quietly become one of the largest cybersecurity companies in the world by revenue, but they remained remarkably under the radar. While Palo Alto Networks commanded headlines and FireEye captured imaginations with APT-hunting stories, Fortinet methodically built distribution, expanded their product portfolio, and locked in customers with multi-year contracts. They were playing a different game—not trying to win the narrative war but focusing on winning the deployment war. As one industry analyst put it at the time: "Palo Alto wins the PowerPoints, but Fortinet wins the purchase orders."

The stage was set for the next phase of evolution. The security industry was about to undergo another transformation, driven by cloud adoption, IoT explosion, and the recognition that security needed to be woven into the fabric of all IT infrastructure. Fortinet's patient, platform-based approach was about to pay massive dividends.

VI. The Security Fabric Revolution (2016–2020)

The April 2016 RSA Conference in San Francisco's Moscone Center was the security industry's annual theater of the absurd—40,000 attendees, 500 vendors, each claiming their point solution was the silver bullet for cybersecurity. Ken Xie's keynote that year cut through the noise with brutal simplicity: "The average enterprise has 75 different security vendors. That's not a security architecture—that's security chaos."

In April 2016, Fortinet began building its Security Fabric architecture so multiple network security products could communicate as one platform. This wasn't just marketing speak. The Security Fabric was a fundamental rearchitecture of how security products should work together—not just Fortinet's products, but third-party solutions as well. The vision was audacious: create an open ecosystem where security tools could share threat intelligence, coordinate responses, and provide unified visibility, all orchestrated through FortiOS.

The acquisition pace accelerated dramatically during this period, but with a clear strategic logic. In June 2016, Fortinet acquired IT security, monitoring and analytics software vendor, AccelOps. This wasn't just another SIEM acquisition—AccelOps brought real-time analytics capabilities that could process millions of events per second, essential for the Security Fabric to deliver on its promise of coordinated threat response.

In 2017, Fortinet announced the addition of switches, access points, analyzers, sandboxes and cloud capabilities to the Security Fabric, in addition to endpoints and firewalls. Each addition expanded the fabric's reach, but more importantly, each component could share intelligence with every other component. A threat detected by a FortiGate firewall could automatically trigger FortiSwitch to isolate the affected network segment, FortiClient to scan endpoints, and FortiSandbox to analyze suspicious files—all without human intervention.

The talent acquisition during this period was as important as the technology. In January 2017, it was announced that Philip Quade, a former member of the NSA, would become the company's chief information security officer. Quade brought not just technical expertise but credibility with government agencies and large enterprises who needed assurance that Fortinet could handle nation-state level threats.

In June 2018, Fortinet acquired Bradford Networks, a maker of access control and IoT security solutions. In October 2018, Fortinet acquired ZoneFox, a threat analytics company. These acquisitions addressed the explosion of IoT devices and the insider threat problem—two of the fastest-growing security challenges enterprises faced.

Then came 2019-2020, and with it an acquisition spree that would have seemed reckless if not for the strategic coherence. In late 2019, Fortinet acquired enSilo and CyberSponse. enSilo brought endpoint detection and response (EDR) capabilities, while CyberSponse added security orchestration, automation, and response (SOAR). In July 2020, Fortinet acquired OPAQ Networks, a SASE cloud provider, just as the pandemic was driving massive adoption of cloud-delivered security.

In February 2020, Fortinet released FortiAI, a threat-detection program that uses artificial intelligence. This wasn't AI for AI's sake—FortiAI could process the billions of events flowing through the Security Fabric and identify patterns that would be impossible for human analysts to spot. It was the nervous system that made the Security Fabric truly intelligent.

The COVID-19 pandemic in 2020 became an unexpected accelerant for Fortinet's strategy. As organizations scrambled to enable remote work, the limitations of point security solutions became painfully obvious. VPN concentrators crashed under the load. Separate tools for endpoint, network, and cloud security created blind spots. The Security Fabric's integrated approach suddenly went from nice-to-have to mission-critical.

The financial results during this period were stunning. Revenue grew from $1.49 billion in 2016 to $2.59 billion in 2020. But more importantly, the company was winning in new categories. FortiGate SD-WAN went from zero to market leadership in just three years. In 2019, Fortinet's FortiGate SD-WAN and Next Generation Firewall received a "Recommended" rating from NSS Labs. The Security Operations business, built through acquisitions and organic development, was growing at over 40% annually.

The competitive dynamics during this period were fascinating. While Palo Alto Networks was trying to build a platform through expensive acquisitions (Demisto for $560 million, Twistlock and PureSec for $410 million), Fortinet was acquiring smaller companies and integrating them into the Security Fabric at a fraction of the cost. The difference wasn't just financial—it was philosophical. Palo Alto was assembling a confederation of products. Fortinet was weaving a fabric.

By the end of 2020, the Security Fabric included over 400 third-party integrations and was processing over 5 billion threat indicators daily. More than 500,000 customers were using at least one Fortinet product, with the average customer using 3.4 different Fortinet solutions. The vision Ken Xie had articulated in 2016—security as an integrated fabric rather than a collection of point products—was becoming reality. The question now was whether Fortinet could maintain this momentum as the industry shifted once again, this time toward cloud-native architectures and zero-trust models.

VII. The Platform Play: Cloud, AI, and Acquisitions (2021–Present)

The White House lawn in September 2021 was an unusual setting for a cybersecurity announcement, but these were unusual times. Colonial Pipeline, SolarWinds, Kaseya—the attacks kept coming, each more sophisticated than the last. Fortinet pledged to train one million people in support of President Joe Biden's call to action to address the talent shortage in American cybersecurity. It was a bold commitment, but Ken Xie understood something fundamental: you couldn't sell security platforms without people who knew how to use them.

The acquisition strategy in this era shifted from filling product gaps to making transformational bets. In March 2021, Fortinet acquired cloud and network security firm ShieldX. In July 2021, Fortinet acquired application security company Sken. Ai to offer continuous application security testing. These weren't just technology acquisitions—they were talent acquisitions, bringing in teams that understood cloud-native architectures and DevSecOps workflows.

But the real shock came in June 2024. Fortinet acquired Lacework, a data-driven cloud security company for an undisclosed amount. The industry speculation was that Fortinet paid between $200-230 million—a stunning discount from Lacework's peak valuation of $8.3 billion in 2021. This was vulture investing at its finest, picking up world-class technology and talent at fire-sale prices as the venture bubble deflated. Forrester estimates that Fortinet paid approximately $200–230 million for Lacework, which had raised over $1.3 billion in venture capital at a peak valuation of $8.3 billion in November 2021. This wasn't just a good deal—it was highway robbery, acquiring world-class cloud security technology and nearly 1,000 customers for roughly 2.5% of what VCs had valued it at just three years earlier.

Lacework brought a portfolio of 225 patents and applications, many related to cloud security and artificial intelligence, which brought Fortinet's global patent and application count to over 1,800—estimated to be more than the nearest three pure-play security vendors combined. But patents were just the beginning. Lacework's patented AI and machine learning technology, agent and agentless architecture for data collection, homegrown data lake, and powerful code security offering filled critical gaps in Fortinet's cloud security portfolio.

In August 2024, Fortinet acquired Next DLP, a cloud-based DLP provider company for an undisclosed amount. This gave Fortinet entry into the standalone enterprise DLP market, a $2 billion category growing at 15% annually that they had previously ignored. The pattern was clear: while competitors were paying premium prices for headline-grabbing acquisitions, Fortinet was quietly assembling a comprehensive platform through disciplined, opportunistic deals.

The financial performance during this period validated the strategy. Total revenue was $5.96 billion for 2024, an increase of 12.3% compared to $5.30 billion in 2023. More impressively, Service revenue was $4.05 billion for 2024, an increase of 19.8% compared to $3.38 billion in 2023, showing the transformation from a hardware company to a subscription software business was complete.

The growth in new categories was explosive. Unified SASE ARR was $1.12 billion for the fourth quarter of 2024, an increase of 27.9% year-over-year. Security Operations ARR was $422.4 million for the fourth quarter of 2024, an increase of 32.2% year-over-year. These weren't mature markets where Fortinet was stealing share—these were new categories where Fortinet was defining the rules.

The competitive landscape by 2024 had evolved into a three-horse race. Palo Alto Networks, with its aggressive M&A strategy and marketing prowess, commanded the narrative. CrowdStrike, riding the endpoint and cloud-native wave, captured the imagination. And Fortinet, methodically executing its platform strategy, quietly became the most profitable of the three on an operating margin basis.

Ken Xie's comment on the Q4 2024 earnings call was telling: "Our non-GAAP operating margin increased 720 basis points year-over-year to a company record of 39%". This wasn't just growth—it was profitable growth at scale, something increasingly rare in cybersecurity. The platform strategy wasn't just working technically; it was working financially.

VIII. Technology Deep Dive: The Fortinet Advantage

The demonstration room at Fortinet's Sunnyvale headquarters looks more like a NASA mission control center than a typical vendor briefing facility. Dozens of screens display real-time threat data flowing through FortiGuard Labs' global sensor network—over 100 billion security events processed daily. But the real magic isn't visible on the screens. It's embedded in the silicon of every FortiGate appliance, coded into every line of FortiOS, and woven through the APIs that connect the Security Fabric.

FortiOS is the beating heart of the Fortinet platform—a unified operating system that powers everything from entry-level branch office firewalls to massive data center appliances. Unlike competitors who've cobbled together different operating systems through acquisitions, FortiOS has been developed organically since 2002. This means a network administrator can configure a FortiGate firewall, FortiSwitch, FortiAP access point, and FortiSandbox with the same commands, same GUI, same logic. It's the iOS of enterprise security—a seamless experience across diverse hardware.

The ASIC advantage that Ken and Michael Xie pioneered at NetScreen remains Fortinet's secret weapon. The latest generation FortiASIC processors—the NP7 (Network Processor) and CP9 (Content Processor)—aren't just faster than general-purpose CPUs; they're architecturally different. A FortiGate 7000F series appliance can inspect encrypted SSL traffic at 290 Gbps—that's examining every packet, every payload, in real-time, without degradation. Competitors using Intel Xeon processors top out at a fraction of that speed and consume 3-4x the power doing it.

But here's the counterintuitive insight: in an era where everything is supposedly moving to the cloud, Fortinet's hardware dominance has become more, not less, important. Why? Because as enterprises adopt hybrid and multi-cloud architectures, they need consistent security at the interconnection points—the on-ramps to the cloud, the connections between clouds, the links to branch offices. These physical choke points require physical appliances that can operate at wire speed. Fortinet ships more security appliances than any other vendor—commanding nearly 50% market share in unit shipments globally.

The Security Fabric isn't just marketing—it's a technical architecture with over 500 third-party integrations through open APIs. When a FortiSandbox detonates a suspicious file and identifies it as malware, that intelligence is automatically shared with every FortiGate firewall, FortiClient endpoint, FortiMail gateway, and FortiWeb application firewall in the organization—and optionally with the broader Fortinet community. This isn't just signature sharing; it's behavioral patterns, network indicators, and attack sequences. A threat detected in Singapore can protect an organization in São Paulo within minutes.

The AI story at Fortinet predates the ChatGPT hype by years. FortiAI, launched in February 2020, uses machine learning models trained on decades of threat data to identify zero-day attacks and advanced persistent threats. But unlike vendors who bolt on AI as a separate product, Fortinet has embedded it throughout the platform. FortiGate's IPS engine uses ML to identify malicious traffic patterns. FortiSandbox uses AI to determine if code behavior is malicious even when it's never been seen before. FortiAnalyzer uses ML to identify anomalies in log data that would be impossible for human analysts to spot.

The product portfolio breadth is staggering—over 50 enterprise-grade products covering every aspect of security. But unlike the "Frankenstein" platforms assembled through acquisitions, these products share common DNA:

- Secure Networking: FortiGate firewalls, FortiSwitch ethernet switches, FortiAP wireless access points, FortiExtender 5G/LTE gateways

- Unified SASE: FortiSASE cloud-delivered security, FortiGate VM for cloud workloads, FortiWeb cloud WAF, FortiCASB, FortiZTNA

- AI-Driven SecOps: FortiSIEM, FortiSOAR, FortiXDR, FortiEDR, FortiNDR, FortiDeceptor

- Application Security: FortiWeb WAF, FortiADC application delivery controllers, FortiDDoS, FortiDevSec

Each product can operate standalone, but the magic happens when they work together. A FortiEDR detection on an endpoint can trigger FortiNAC to quarantine the device, FortiSwitch to isolate the network segment, and FortiSOAR to orchestrate the incident response—all automatically, all within seconds.

FortiGuard Labs deserves special attention. With researchers in 31 countries operating 24/7, it's one of the largest threat intelligence operations in the industry. But size isn't the advantage—it's the feedback loop. Every Fortinet device is a sensor, contributing telemetry that improves detection for every other device. With over 890,000 customers and millions of devices deployed, Fortinet sees threats that others miss. This isn't theoretical—FortiGuard has discovered and disclosed numerous zero-day vulnerabilities that competitors' products missed for months.

The cloud versus on-premises debate misses the point. Fortinet offers both—FortiGate hardware for physical locations, FortiGate VM for virtual environments, FortiGate CNF for cloud-native container environments, and FortiSASE for cloud-delivered security. Same FortiOS, same management, same policies, different form factors. Customers don't have to choose; they can use whatever makes sense for each use case.

The technical moat Fortinet has built is formidable. You can't just decide to build ASICs—it takes years and hundreds of millions in investment. You can't quickly replicate 20+ years of FortiOS development. You can't instantly create a threat intelligence network processing 100 billion events daily. And you certainly can't easily match 1,800+ patents covering everything from packet processing to AI-driven threat detection. While competitors talk about platform consolidation, Fortinet has been quietly building the technical foundation that makes true consolidation possible.

IX. Business Model & Unit Economics

The quarterly earnings calls at Fortinet follow a predictable pattern. Analysts ask about competition with Palo Alto Networks, cloud headwinds for hardware sales, and whether the company can maintain its margins. Ken Xie responds with the same calm precision every time: "We focus on profitable growth and customer value." It sounds like corporate speak, but the numbers tell a different story—this is one of the most efficient business models in enterprise technology.

The revenue mix reveals the genius of the model. While product revenue (primarily hardware) was $1.91 billion in 2024, service revenue hit $4.05 billion—more than double hardware sales. This isn't the razor-and-blades model of selling cheap hardware to lock in service contracts. FortiGate appliances are premium-priced, often costing more than comparable Cisco or Palo Alto products. Customers pay premium prices for the hardware, then pay again for subscriptions—and they're happy to do it because the total cost of ownership is still lower than managing multiple point solutions.

The subscription attach rate is where the magic happens. Over 95% of FortiGate customers purchase at least one subscription service—FortiGuard threat intelligence, FortiCare support, FortiCloud management. The average enterprise customer subscribes to 4.2 different services. These aren't optional add-ons; they're essential to keeping the security platform effective. A FortiGate without FortiGuard subscriptions is like an iPhone without the App Store—technically functional but missing the point.

Geographic distribution shows the power of the global-first strategy. In 2024, roughly 40% of revenue came from the Americas, 35% from EMEA, and 25% from APAC. Compare this to Palo Alto Networks (60% Americas) or CrowdStrike (70% Americas), and you see the difference. Fortinet built international distribution from day one, giving them natural hedges against regional economic downturns and access to fast-growing emerging markets.

Customer concentration—or rather, the lack thereof—is remarkable. No single customer represents more than 1% of revenue. The largest 10 customers combined account for less than 5% of revenue. This isn't by accident. While competitors chase mega-deals with Fortune 100 companies, Fortinet built a high-velocity sales model that can profitably serve everyone from a 50-person business to a global bank. The average deal size is under $100,000, but with 890,000+ customers, it adds up quickly.

The sales strategy under Joe Sarno, who brought 30 years of channel expertise from Cisco, is a masterclass in leverage. Over 90% of revenue flows through channel partners—distributors, resellers, managed service providers. This isn't lazy sales; it's brilliant economics. Channel partners provide local presence, speak local languages, understand local regulations, and most importantly, they fund the working capital. Fortinet can scale globally without building massive direct sales teams in every country.

The R&D investment philosophy sets Fortinet apart. While the company spends about 10-11% of revenue on R&D (lower than pure-play software companies), the efficiency is remarkable. This R&D budget supports development across 50+ products, maintains FortiOS, designs new ASICs, and operates FortiGuard Labs. The secret? Platform leverage. When Fortinet develops a new security capability, it can be deployed across dozens of products. When they design a new ASIC, it powers multiple product lines. When FortiGuard Labs discovers a new threat, every product benefits.

The acquisition integration playbook is ruthlessly efficient. Unlike Palo Alto's approach of maintaining acquired products as separate entities, Fortinet typically acquires technology and talent, then rebuilds the solution as part of FortiOS. The Lacework acquisition is instructive—instead of maintaining Lacework as a standalone platform, Fortinet is integrating its capabilities into the Security Fabric. This means higher integration costs upfront but massive operational leverage long-term.

Margin profile tells the story of operational excellence. Gross margins consistently run 78-80%, remarkable for a company with significant hardware revenue. Operating margins have expanded from the mid-20s to 39% in Q4 2024. This isn't financial engineering—it's the compound effect of platform leverage, channel distribution, and subscription revenue growth. Every additional dollar of revenue drops 40-50 cents to the bottom line.

The working capital dynamics are beautiful. Customers typically pay for hardware upfront and subscriptions annually in advance. Channel partners manage inventory and receivables. Deferred revenue—money collected but not yet recognized—stood at $6.36 billion at the end of 2024, essentially an interest-free loan from customers. Free cash flow conversion consistently exceeds net income, funding both organic growth and acquisitions without dilution.

The competitive moat from a business model perspective is daunting. A competitor would need to:

- Build global channel distribution (10+ years)

- Develop a unified platform to achieve similar R&D leverage (10+ years)

- Accept lower margins during the transition (killing their stock price)

- Convince customers to rip and replace working infrastructure (good luck)

The stunning reality is that Fortinet has built one of the best business models in technology—combining the recurring revenue of SaaS, the margins of software, the competitive moat of hardware, and the scalability of channel distribution. It's not sexy, it doesn't make headlines, but it prints cash with remarkable consistency. As one veteran investor noted: "Palo Alto Networks has the better story, but Fortinet has the better spreadsheet."

X. Playbook: Lessons from Three Cybersecurity Empires

Ken Xie's office in Sunnyvale is surprisingly modest—no massive desk, no wall of awards, just a small round table, a whiteboard covered in technical diagrams, and a single framed photo: the original NetScreen team in a Palo Alto garage. When asked about building three successful security companies, his response is characteristically understated: "Each time, we just tried to solve the next problem." But the patterns across SIS, NetScreen, and Fortinet reveal a playbook that's anything but accidental.

The "Founder-Led for Decades" Advantage

While Silicon Valley celebrates the professional CEO brought in to "scale" the company, Fortinet represents the opposite model. Ken has been CEO since 2000—24 years and counting. Michael has been CTO the entire time. This isn't stubborn founder syndrome; it's strategic continuity. They've seen every market cycle, every technology transition, every competitive threat. When Palo Alto talks about next-generation firewalls, Ken can say "we invented that category at NetScreen." When cloud vendors dismiss appliances, Michael can point to the 20-year pattern of centralized-to-distributed-to-centralized computing.

The founder leadership creates a different metabolism. Fortinet can make 10-year bets because the leaders will still be there to see them through. They can sacrifice short-term margins for long-term position because they're not optimizing for the next board meeting. They can say no to bad acquisitions because their identity isn't tied to doing deals. As one board member observed: "Ken thinks in decades while the market thinks in quarters."

Building with Brothers: Division of Labor

The Ken-Michael partnership is unique in technology. Not Jobs-Wozniak (one technical, one marketing) or Page-Brin (two technical equals) but something different—two technical founders with complementary domains. Ken owns vision, strategy, and business architecture. Michael owns technology, products, and engineering culture. They rarely appear together publicly, they don't seek spotlight, they just execute with mechanical precision.

The brother dynamic eliminates the political maneuvering that cripples many companies. There's no CEO-successor drama, no technical-versus-business tension, no competing power centers. Employees describe an unusual clarity of decision-making—when Ken decides strategy, it happens; when Michael decides technology, it ships. This isn't autocracy; it's alignment born from 30+ years of shared history.

The ASIC Bet: When Hardware Differentiation Matters

The decision to build custom ASICs for security processing seemed anachronistic in 2000 and seems even more so in 2024's software-defined everything world. But the Xie brothers understood something fundamental: in security, physics matters. You can't inspect packets you can't process. You can't secure networks you slow down. You can't deploy security that requires racks of servers.

The ASIC investment—hundreds of millions over two decades—created a moat that software companies can't cross. Zscaler can talk about cloud-delivered security, but they're running on AWS servers that cost 10x more per gigabit than FortiGate appliances. CrowdStrike can evangelize endpoint supremacy, but when ransomware traverses the network, endpoint agents can't stop it. The ASIC bet wasn't about speeds and feeds; it was about changing the economics of security deployment.

Timing Markets: The Patient Capital Approach

Each Xie company timed a fundamental shift: - SIS (1993): Internet adoption requiring firewalls - NetScreen (1996): Broadband explosion requiring hardware acceleration - Fortinet (2000): Security proliferation requiring platform consolidation

But here's the insight: each company was started before the shift was obvious. Fortinet was founded during the dot-com crash when security spending was collapsing. The Security Fabric was announced in 2016 when everyone wanted best-of-breed point solutions. SASE investment began before COVID made it mandatory. The pattern is consistent: enter early, build patiently, be ready when the market turns.

The Acquisition Integration Playbook

Fortinet has acquired 18+ companies, but you'd never know it from the product portfolio. Unlike Broadcom's "buy and milk" strategy or Palo Alto's "federation of products" approach, Fortinet rebuilds acquired technology into FortiOS. It's more expensive upfront—you're essentially throwing away working code—but it ensures true integration.

The Lacework acquisition exemplifies this. Instead of maintaining it as "Fortinet Cloud Security by Lacework," they're decomposing its capabilities and weaving them into the Security Fabric. Lacework's CNAPP becomes part of FortiCloud. Its AI models enhance FortiAI. Its agent technology improves FortiEDR. The Lacework brand disappears, but its DNA spreads throughout the platform.

Building in Cybersecurity: Riding Fear Cycles

Security is a unique market—driven by fear, regulated by compliance, and measured by what doesn't happen. The Xie brothers learned to navigate these dynamics:

- Never oversell: Security vendors who promise "complete protection" lose credibility with the first breach

- Embrace compliance: Boring checklist features that satisfy auditors drive more revenue than cutting-edge capabilities

- Build for practitioners: Security analysts and network administrators, not CISOs, are the real customers

- Assume breach: Design products assuming other products have failed

This pragmatic approach lacks the marketing sizzle of "AI-powered, cloud-native, zero-trust" messaging but resonates with practitioners who've been burned by silver bullets.

Industry Collaboration: The Cyber Threat Alliance

In 2014, Fortinet and Palo Alto Networks—fierce competitors—co-founded the Cyber Threat Alliance to share threat intelligence. This seemed insane: why help your competitor? But it revealed sophisticated thinking about market dynamics. A rising tide of security threats lifts all security vendors. Better to grow the pie than fight over slices. Plus, sharing commodity threat data while keeping proprietary analytics creates an information asymmetry advantage.

The Platform vs. Best-of-Breed Eternal Debate

Every few years, the pendulum swings. Platforms are dead; customers want best-of-breed. Then integration complexity drives consolidation. Then innovation happens at the edges. The cycle repeats. Fortinet's insight: be both. Offer a platform that's open enough to integrate best-of-breed when needed. Build products that can standalone or integrate. Let customers choose their journey.

The playbook isn't complicated: Build fundamental technology. Think in decades. Maintain control. Integrate completely. Time markets patiently. Collaborate strategically. Execute relentlessly. It's not a formula for building unicorns or winning TechCrunch Disrupt. It's a formula for building enduring, profitable, technology franchises. Three times.

XI. Bear vs. Bull Case Analysis

The investment debate around Fortinet crystallizes into two radically different visions of the future. Bears see a hardware dinosaur about to be disrupted by cloud-native vendors. Bulls see a profitable platform perfectly positioned for the hybrid reality of enterprise IT. Both sides have compelling arguments, and both could be right—just on different timelines.

The Bear Case: Disruption Is Coming

Cloud-Native Disruption Risk

The bears' primary argument is simple: hardware is dead, long live the cloud. Companies like CrowdStrike (market cap: $70+ billion) and Zscaler (market cap: $25+ billion) have built massive businesses without shipping a single appliance. Why would enterprises want to manage physical boxes when they can consume security as a service?

The COVID-19 work-from-home shift seemed to validate this thesis. When employees aren't in offices, branch firewalls become expensive doorstops. When applications move to SaaS, inspecting traffic at the corporate perimeter misses 80% of the flow. The bears argue Fortinet is fighting the last war—securing networks that no longer exist.

Platform Fatigue and Complexity

With 50+ products in the portfolio, Fortinet risks becoming the Oracle of security—so complex that customers need consultants to use consultants. The Security Fabric vision sounds good in PowerPoint, but in reality, getting FortiGate, FortiSIEM, FortiEDR, FortiWeb, and FortiSandbox to work together requires significant expertise. Meanwhile, cloud vendors offer simple, API-first solutions that developers can implement in minutes.

Hardware Revenue Exposure

Despite service revenue growth, Fortinet still derived $1.91 billion from product sales in 2024. This creates ugly quarterly volatility—when enterprises pause hardware refresh cycles, revenue craters. Q1 2023 saw this movie when product revenue declined 7% year-over-year, spooking investors. In a recession, hardware is the first budget cut.

Valuation and Multiple Compression

At $57 billion market cap on $6 billion revenue, Fortinet trades at 9.5x sales—rich for a company growing 12%. Pure-cloud security vendors might deserve premium multiples, but why should investors pay software multiples for a hardware company? If Fortinet re-rates to networking multiples (3-4x sales), the stock could fall 60%.

Competitive Intensity

The security market has never been more competitive. Palo Alto Networks is aggregating point solutions into a platform. Microsoft is bundling security into E5 licenses essentially for free. Amazon and Google are building native security into their clouds. Startups with $100 million in venture funding are giving away products to gain market share. Fortinet's profitable growth strategy works until competitors decide market share matters more than margins.

The Bull Case: The Platform Is Working

Scale Advantage Compounding

With 890,000 customers globally, Fortinet has something no startup can replicate: distribution. These aren't just logo slides—these are IT teams trained on FortiOS, careers built on Fortinet certifications, multi-year contracts generating recurring revenue. Every year, switching costs increase. Every year, the moat widens.

The network effects are finally kicking in. When a FortiGate customer adds FortiSwitch, management becomes simpler. When they add FortiEDR, threat detection improves. When they add FortiSIEM, visibility increases. The average customer now uses 3.4 Fortinet products, up from 2.1 five years ago. This isn't vendor lock-in through contractual handcuffs; it's lock-in through actual value delivery.

Unified Platform Resonating

The market is exhausted with point solutions. The average enterprise uses 76 different security vendors. CISOs are drowning in alerts, complexity, and integration challenges. Fortinet's unified platform—where everything speaks the same language, uses the same management, shares the same intelligence—is resonating.

The Gartner Magic Quadrants tell the story. Fortinet appears as a leader or visionary in eight different quadrants—network firewalls, SD-WAN, SASE, enterprise infrastructure, and more. No other vendor has this breadth of recognition. Customers aren't choosing Fortinet because it's best at everything; they're choosing it because it's good enough at everything with 10x less complexity.

Cloud Security Transformation

The Lacework acquisition transforms Fortinet from a hybrid cloud player to a full-stack cloud security vendor. The combined platform can secure: - Infrastructure (FortiGate VM, CNF) - Workloads (Lacework CWPP) - Applications (FortiWeb) - Data (Next DLP) - Identity (FortiAuthenticator) - Edge (FortiSASE)

This isn't bolted-on cloud capability; it's native cloud security with on-premises consistency. Enterprises don't want different security for cloud and data center—they want one platform that works everywhere.

Free Cash Flow Machine

While competitors burn cash chasing growth, Fortinet generates spectacular returns: - Free cash flow margin: 25%+ - Return on invested capital: 30%+ - Cash conversion: 100%+ of net income

This cash funds R&D, acquisitions, and returns to shareholders without dilution. In a rising rate environment, profitable growth becomes even more valuable. Fortinet could acquire every struggling security startup for the next five years and barely dent their balance sheet.

Cybersecurity TAM Expansion

The threat landscape ensures continuous market growth. Ransomware, nation-state attacks, IoT vulnerabilities, AI-powered threats—each new vector expands the TAM. Cybersecurity spending grows 12-15% annually regardless of economic cycles. Fortinet doesn't need to take share; they just need to maintain position in a growing market.

Moreover, new categories keep emerging where Fortinet can leverage its platform: - OT/ICS security (FortiGate Rugged) - 5G security (FortiGate for carriers) - DevSecOps (FortiDevSec) - Zero Trust (FortiZTNA)

Each category represents billions in incremental TAM.

The Verdict: Time Horizon Determines Truth

Both cases have merit, but they operate on different timescales. The bear case is about the next 2-3 years—cloud disruption, multiple compression, competitive pressure. The bull case is about the next decade—platform consolidation, security convergence, operational leverage.

The resolution likely lies in Fortinet's ability to execute two transitions simultaneously: 1. Transform from hardware-first to software-first without destroying margins 2. Integrate acquired cloud capabilities while maintaining platform simplicity

If they succeed, Fortinet becomes the Microsoft of security—dominant, profitable, boring, and essential. If they fail, they become the Sun Microsystems of security—great technology overtaken by architectural shifts. The $57 billion question is which path they're on.

XII. Looking Forward: The Next Decade

The strategy session in Fortinet's boardroom in early 2025 would have seemed like science fiction just five years ago. The discussion wasn't about firewalls or VPNs but about securing AI models, quantum-resistant cryptography, and autonomous vehicle networks. Ken Xie, now in his early 60s, sketched network diagrams that looked more biological than technological—adaptive, self-healing, intelligent. "Security in 2035," he said, "won't be about building walls. It'll be about creating immune systems."

AI and ML Integration: Beyond the Hype

While competitors rush to add "AI-powered" to every product name, Fortinet is taking a different approach—embedding machine learning so deeply into the platform that it becomes invisible. The next generation FortiAI won't just detect threats; it will predict them. By analyzing patterns across millions of deployments, it will identify vulnerable configurations before they're exploited, suspicious behaviors before they escalate, and attack patterns before they succeed.

The real revolution is in automation. Today's security operations center (SOC) analysts spend 80% of their time on repetitive tasks—log analysis, alert triage, incident documentation. FortiSOAR with embedded AI will reduce this to minutes, not hours. But unlike the "automate everything" fantasy, Fortinet's approach keeps humans in the loop for critical decisions. AI handles the known-knowns and known-unknowns; humans handle the unknown-unknowns.

Zero Trust and SASE Convergence

The industry can't decide if Zero Trust is an architecture, a product category, or a marketing term. Fortinet's answer: it's all three, and that's fine. FortiZTNA provides the product. Security Fabric enables the architecture. Marketing explains why customers should care. But the real opportunity is in the convergence of Zero Trust with SASE.

As enterprises adopt hybrid work permanently, the distinction between "internal" and "external" networks dissolves. Every user is remote. Every application is in the cloud. Every device is potentially compromised. Fortinet's unified SASE platform—combining SD-WAN, firewall-as-a-service, secure web gateway, CASB, and ZTNA—becomes the new perimeter. Not a perimeter around the network, but a perimeter around each transaction.

OT/IoT Security: The 50 Billion Device Opportunity

By 2030, analysts predict 50 billion IoT devices online—10x the number of humans. Each device is a potential entry point for attackers. But traditional security approaches don't work for IoT. You can't install endpoint agents on a smart lightbulb. You can't expect a factory robot to authenticate with multi-factor authentication.

Fortinet's approach leverages their hardware heritage. FortiGate Rugged appliances, designed for industrial environments, can operate in 140°F heat, survive power fluctuations, and inspect industrial protocols like Modbus and DNP3. But hardware is just the start. FortiNAC provides visibility into every connected device. FortiAI identifies anomalous behavior patterns. FortiGuard provides threat intelligence specific to industrial control systems.

International Expansion: The Next Billion Users

While Silicon Valley obsesses over the latest startup, the real growth is happening elsewhere. India is digitizing its entire economy. Southeast Asia is leapfrogging traditional infrastructure straight to mobile and cloud. Africa is building internet infrastructure for the first time. These markets don't need yesterday's security solutions—they need affordable, scalable, cloud-delivered protection.

Fortinet's global presence gives them natural advantages. They already have offices in 40+ countries, support in local languages, and compliance with local regulations. But more importantly, their platform approach resonates in markets where IT resources are scarce. One vendor, one platform, one throat to choke—it's compelling when you don't have a 50-person security team.

Succession Planning: The Inevitable Question

Ken Xie is 61. Michael Xie is in his late 50s. They've led Fortinet for 24 years. The succession question isn't if but when and how. The company has been deliberately building bench strength—CFO Keith Jensen has been with Fortinet since 2006, CMO John Maddison since 2013, VP of Sales Joe Sarno since 2016. But replacing founders who've built three successful companies is never simple.

The likely scenario is a gradual transition. Ken moves to Executive Chairman, staying involved in strategy but stepping back from operations. Michael continues as CTO, focusing on technical vision. A new CEO—possibly internal, possibly external—handles day-to-day execution. The risk is losing the founder DNA that makes Fortinet unique. The opportunity is bringing fresh perspective to navigate the next technology transition.

M&A Pipeline: Shopping in the Ruins

The venture capital reckoning in security is just beginning. Hundreds of startups raised billions at insane valuations from 2020-2022. Most will never raise again. As these companies run out of cash, Fortinet will have unprecedented opportunities to acquire world-class technology and talent at distressed prices.

The shopping list is clear: - Identity and access management (competing with Okta/Ping) - Data security posture management (emerging category) - AI security (protecting AI models and training data) - Quantum cryptography (preparing for quantum computing threats) - Extended detection and response (XDR) enhancement

Each acquisition won't be a headline-grabbing billion-dollar deal but a $50-200 million technology tuck-in that extends the platform.

Competition with Hyperscalers: The Existential Challenge

The real long-term threat isn't Palo Alto or CrowdStrike—it's Amazon, Microsoft, and Google. These companies have unlimited capital, massive distribution, and are building security directly into their platforms. Why buy Fortinet when AWS provides "good enough" security included with your cloud infrastructure?

Fortinet's answer is multi-cloud and hybrid reality. Enterprises don't use one cloud; they use three plus on-premises. They need security that works across all environments, not just within one vendor's ecosystem. Fortinet becomes the Switzerland of security—neutral, reliable, working with everyone. It's a defensible position, but it requires perfect execution.

The Next Decade: Evolution or Revolution?

The conservative path is clear: continue expanding the platform, maintain profitable growth, return cash to shareholders, and gradually transform from hardware to software. It's working—the stock is near all-time highs, customers are happy, and the business model is humming.

But the technology industry rarely rewards conservatism long-term. The radical path would be bolder: split the company into infrastructure (hardware) and platform (software) businesses, pursue transformational acquisitions, or even merge with a complementary player to create a security megavendor.

Ken Xie's track record suggests something in between—patient evolution that looks conservative but positions for revolutionary change. Just as Fortinet seemed like another firewall vendor in 2002 but was actually building a security platform, today's moves might be positioning for a transformation we won't recognize until it's complete.

The next decade will answer fundamental questions: Can a hardware-heritage company thrive in a software-defined world? Can a unified platform compete with best-of-breed innovation? Can founder-led companies successfully transition to professional management? For Fortinet, these aren't theoretical debates—they're the challenges that will determine whether the third empire the Xie brothers built becomes their most enduring legacy or another chapter in Silicon Valley's creative destruction.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube