Frontdoor: The Hidden Giant Powering America's Homes

I. Introduction & Episode Roadmap

Somewhere in America right now, a water heater is failing. A dishwasher is leaking. An air conditioning compressor is giving its last wheeze. And in most of those homes, the homeowner is reaching for their phone, not to call a contractor they found on Google, but to file a claim with a company most people on Wall Street have never heard of: Frontdoor Inc.

Frontdoor, trading on the Nasdaq under the ticker FTDR, is a company with a market capitalization north of four billion dollars, revenue exceeding two billion dollars, and a customer base of over two million American households. It is, by any reasonable measure, a large and consequential business. And yet, in the conversation about technology-enabled platforms, subscription economies, and the digitization of home services, Frontdoor almost never comes up. The company lives in an odd blind spot, too old to be exciting to venture capitalists, too "boring" for the tech press, and too niche for most generalist investors to bother understanding.

That is a mistake. Because the story of Frontdoor is one of the most interesting transformation narratives in American business today. It is the story of how a fifty-year-old home warranty company, born in an era of paper contracts and rotary phones, reinvented itself as a technology-enabled home services platform. It is the story of a corporate spinoff that unlocked value, a digital transformation that actually worked, and a business model that sits at the intersection of subscriptions, marketplaces, and the enormous, fragmented American home services economy.

The question at the heart of this story is deceptively simple: Can a legacy warranty company become a technology platform? And if so, what does that mean for the hundreds of billions of dollars Americans spend every year maintaining their homes?

To answer that, we need to go back to the beginning, to a newspaper article, a California entrepreneur, and an idea that created an entirely new industry.

What makes this story worth telling right now is the timing. Frontdoor just reported record full-year 2025 results: over two billion dollars in revenue, adjusted EBITDA margins of twenty-six percent, and nearly four hundred million in free cash flow. The stock has roughly tripled from its December 2022 lows. And the company just completed its largest acquisition ever, buying 2-10 Home Buyers Warranty for five hundred eighty-five million dollars, giving it a beachhead in the new construction market. The transformation is no longer theoretical. It is showing up in the numbers. But the question of whether Frontdoor can become a true platform, not just a better warranty company, remains open.

II. The Home Warranty Industry & Market Context

Before we tell the Frontdoor story, we need to understand the product at the center of it, because "home warranty" is one of those terms that sounds self-explanatory but is actually deeply misunderstood. A home warranty is not a warranty in the traditional sense, and it is not insurance either. It is a service contract. Think of it as a subscription that covers the repair or replacement of major home systems and appliances when they break down from normal wear and tear.

Here is the practical version. A homeowner pays an annual premium, typically somewhere between three hundred and seven hundred dollars. When their HVAC system dies in July or their refrigerator stops cooling in the middle of a dinner party, they call the warranty company. The company dispatches a pre-qualified contractor. The homeowner pays a service call fee, usually seventy-five to one hundred twenty-five dollars, and the warranty company covers the rest of the repair or replacement. The contract lasts one year and renews annually.

The distinction from insurance matters enormously, and getting it wrong leads to a fundamental misunderstanding of Frontdoor's business. Insurance covers catastrophic, unpredictable events like fires, floods, and storms. Home warranties cover mundane, inevitable events: the gradual failure of machines that run every day of the year. Your furnace will eventually die. Your water heater will eventually leak. The question is not if, but when. Home warranties transfer that "when" risk from the homeowner to the warranty provider, in exchange for a predictable annual payment. It is the same fundamental logic that drives extended warranties on electronics, but applied to the most expensive and complex purchase most Americans will ever make.

The distribution model is what made the industry possible. From the very beginning, home warranties were tied to real estate transactions. When a house changes hands, both buyer and seller face uncertainty. The seller worries a major system will fail during the listing period, killing a deal. The buyer worries about inheriting hidden problems. A home warranty, typically purchased by the seller or the listing agent, smooths that anxiety. In California, where the industry was born, ninety-two percent of all home sales include a home warranty. Nationally, the penetration is much lower, which is itself a major part of the bull case for Frontdoor.

The U.S. home warranty market was valued at approximately four billion dollars in 2023, and global estimates put the broader market at nearly ten billion dollars, projected to reach seventeen billion by 2032. Despite that growth, household penetration across all American homes remains strikingly low, around five percent. That gap between real estate transaction penetration and overall household penetration represents the core strategic opportunity: convincing homeowners who did not buy their warranty as part of a home purchase to buy one directly. This is the direct-to-consumer play that has become central to Frontdoor's strategy.

The servicing challenge is what separates the serious players from the pretenders. A home warranty company is not just selling a piece of paper. It is making a promise to dispatch a qualified technician to a customer's home, anywhere in the country, for any of dozens of possible failure types, within a reasonable timeframe. That means managing thousands of contractor relationships across every major metropolitan area, in every trade: plumbing, electrical, HVAC, appliance repair, pool equipment, garage doors. Each contractor must be vetted, insured, licensed, and willing to accept the warranty company's reimbursement rates, which are typically lower than what they could charge a direct customer. The coordination problem is enormous, and it is why the home warranty business has always been harder to enter than it looks from the outside.

The competitive landscape has historically been fragmented. The top players include Frontdoor's family of brands, Choice Home Warranty, First American Home Warranty, Cinch Home Services, and a long tail of regional operators. But within that fragmented market, one company has dominated from the very beginning.

III. Origins: The American Home Shield Story (1971-2000s)

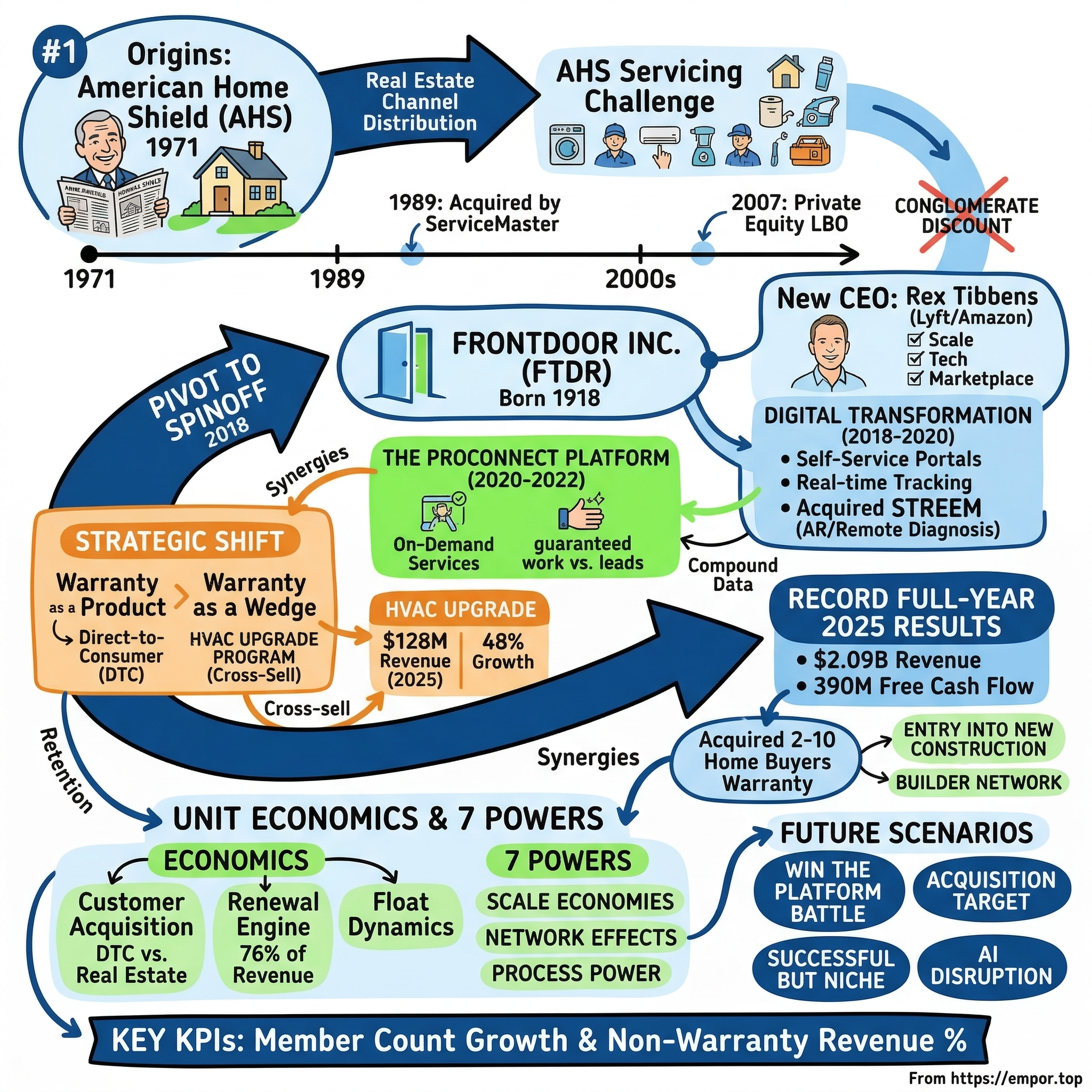

In the early 1970s, a California entrepreneur named Sigmund "Sig" Anderman was reading a newspaper. The article described a group of firefighters and policemen on Long Island, New York, who had started a side business offering discount handyman services to homeowners. It was a simple concept, but Anderman saw something bigger. Rather than ad hoc repair services, what if you could sell a pre-paid service agreement, a contract that guaranteed coverage for home systems and appliances? What if you could take the uncertainty out of homeownership?

That insight led Anderman to found American Home Shield in 1971, creating a product category that had never existed before. The initial business model was elegantly simple: sell service contracts through licensed real estate brokers, tying coverage to home resale transactions. It was a distribution strategy born from necessity. Homeowners who had lived in their homes for years knew what worked and what was about to break. But a buyer stepping into a new home had no idea. That information asymmetry was the perfect soil for a warranty product to grow.

By the mid-1970s, Anderman expanded coverage from appliances to essential home systems, including heating, plumbing, and electrical components. This was a critical move. Appliance repairs are annoying and moderately expensive. But a failed HVAC system in July or a burst pipe in January is an emergency that can cost thousands of dollars. By covering the truly scary failure modes of homeownership, American Home Shield became not just a convenience but a financial safety net.

Anderman was no one-trick entrepreneur. Over a career spanning more than fifty years, he also founded CompuFund, the industry's first computer-based mortgage banking network, and later Ellie Mae, which became a leading automation platform for the residential mortgage industry. He had a pattern: identify a paper-based, inefficient process in real estate, and build a technology-enabled solution. American Home Shield was the earliest and perhaps most consequential expression of that instinct.

The federal Magnuson-Moss Warranty Act of 1975 helped legitimize the industry by requiring clearer disclosure of written warranties and service contracts. The act created a regulatory framework that distinguished home service contracts from traditional warranties and insurance, giving companies like AHS a defined legal structure to operate within. California, AHS's home state, led the way with state-level regulations requiring specific reserve levels and licensing requirements for home warranty providers. These regulations, while adding compliance costs, also created barriers to entry that protected established players.

The growth was remarkable. By 1982, just eleven years after founding, American Home Shield had captured a dominant sixty percent of the home warranty market. By 1988, the company had reached one million active customers, a milestone that validated both the product category and the distribution model. AHS was publicly traded on the over-the-counter market, and its success had spawned a wave of imitators. But none could match the combination of brand recognition among real estate agents, the scale of the contractor network, and the operational infrastructure AHS had built.

The contractor network was the hidden engine of the business. Home warranties are only as good as the service they deliver, and delivering service means having a network of qualified plumbers, electricians, HVAC technicians, and appliance repair specialists ready to respond in every market you serve. Building that network city by city, trade by trade, is painstaking work. It takes years to establish relationships, vet quality, and build the volume that keeps contractors happy. This is the operational moat that makes the home warranty business much harder to replicate than it appears on paper.

Think of it like building a restaurant chain, but instead of owning the kitchens, you are coordinating ten thousand independent chefs who each have their own businesses, their own schedules, and their own ideas about fair pay. You need enough chefs in every city to handle surges in demand during summer, when HVAC failures spike, and during winter, when heating systems and pipes fail. You need specialists for every trade. And you need them to answer the phone when you call, show up on time, do quality work, and charge rates that leave enough margin for the warranty company to be profitable. Nobody has ever solved this challenge perfectly, but the companies that come closest have a powerful advantage.

The regulatory environment evolved alongside the industry. State-by-state licensing requirements, reserve mandates, and consumer protection rules created a patchwork of regulations that established companies navigated through institutional knowledge and compliance infrastructure. For new entrants, the regulatory burden represented one more friction point in an already challenging market to enter.

By the late 1980s, the operational infrastructure of AHS was impressive for its era but deeply analog. Thousands of customer service representatives worked in call centers, manually processing claims by phone. Contractor dispatch was handled through phone calls and fax machines. Contracts were paper documents mailed to customers. The entire operation ran on institutional knowledge rather than software, individual employees who knew which contractors were reliable in which markets, what parts were commonly needed for which appliance models, and how to resolve disputes between customers and technicians. This worked at the company's scale, but it created a fragility that would become apparent decades later: the business ran on people and processes, not on technology.

In 1989, ServiceMaster signed a definitive merger agreement to acquire eighty percent of AHS's outstanding shares at nine dollars and fifty cents per share in cash, plus a contingent payment right of up to three dollars and fifty cents per share tied to earnings targets over the following three years. The total deal value was approximately one hundred twenty million dollars. Senior officers of AHS retained the remaining twenty percent, which ServiceMaster later acquired to achieve full ownership. The era of independent AHS was over, but its next chapter as part of a larger home services empire was about to begin.

IV. The ServiceMaster Years: Corporate Parent Era (2013-2018)

ServiceMaster was a fascinating company in its own right. Founded in 1929 by Marion E. Wade, a former minor league baseball player who started a moth-proofing company in Chicago, ServiceMaster had grown over decades into a sprawling home services conglomerate. By the late 1980s and 1990s, its portfolio included Terminix for pest control, Merry Maids for residential cleaning, TruGreen for lawn care, and now American Home Shield for home warranties. The thesis was compelling: one corporate parent could cross-sell across all these home service verticals, sharing infrastructure and customer relationships.

In practice, the promised synergies were modest. The cross-selling thesis sounded elegant in boardroom presentations, but a homeowner who needed pest control did not necessarily want a warranty, and vice versa. Each brand operated largely independently, serving different customer needs with different service delivery models. The operations were different, the sales channels were different, and the competitive dynamics were different. This is a lesson that applies broadly across conglomerates: proximity on a PowerPoint slide does not equal strategic synergy in the real world. But for AHS specifically, the ServiceMaster years brought important developments. The 1990s saw the introduction of online claims processing, one of the earliest digital upgrades to the business. Direct-to-consumer sales channels expanded beyond the traditional real estate agent relationship. And the unprecedented national housing boom from 1993 through 2005 provided a massive tailwind, as surging home transactions drove volume through the real estate channel.

The story took a dramatic turn in 2007 when Clayton, Dubilier & Rice, the private equity firm, took ServiceMaster private in a leveraged buyout valued at approximately five and a half billion dollars. The deal was structured with roughly seventy-five percent debt and twenty-five percent equity, a classic private equity capital structure of the pre-financial-crisis era. George W. Tamke, a CD&R operating partner, became chairman.

The timing was exquisitely bad. The housing crisis hit just months after the deal closed, crushing home transaction volumes and the real estate channel that fed AHS's growth. But the business proved more resilient than the housing market. Existing warranty holders continued to renew their contracts because homes do not stop breaking down during recessions. If anything, deferred maintenance during economic stress creates more claims, not fewer. This countercyclical quality of the renewal base was a revelation that would shape strategic thinking for years to come.

Through the early 2010s, AHS executed an aggressive acquisition strategy to consolidate the fragmented home warranty market. In 2014, the company acquired HSA Home Warranty, a Madison, Wisconsin-based competitor. In June 2016, it acquired OneGuard Home Warranties, which had been founded in 1990 and served over fifty thousand homeowners in Arizona and Texas. Later that year, it added Landmark Home Warranty, bringing an additional hundred thousand-plus customers. Each acquisition expanded the geographic footprint and brand portfolio, building scale that would prove valuable when the business eventually stood on its own.

ServiceMaster returned to the public markets in June 2014, pricing an IPO of nearly thirty-six million shares at seventeen dollars per share on the NYSE under the ticker SERV. But the conglomerate structure created a persistent problem: the market could not properly value the sum of its parts. Terminix was a pest control business with different growth dynamics, margin profiles, and capital needs than AHS. Investors who wanted exposure to the recurring revenue model of home warranties were forced to also own a pest control franchise. The strategic logic for separation was becoming undeniable.

On July 26, 2017, ServiceMaster announced its intention to separate the American Home Shield business from Terminix and the Franchise Service Group. The spin would take over a year to execute, but the direction was set.

The logic was straightforward but important. AHS was a subscription business with recurring revenue, high retention, and relatively predictable cash flows. Terminix was an operationally intensive pest control business with different capital needs and growth dynamics. Investors who wanted recurring-revenue exposure were diluted by pest control. Investors who wanted pest control were paying for warranty operations they did not understand. The conglomerate discount was real: analysts estimated the combined entity traded at a fifteen to twenty percent discount to the sum of its parts. Separation would let each business attract its natural investor base and allocate capital according to its own strategic priorities.

The home warranty business was about to get something it had never truly had: the freedom to define its own future.

V. The Spinoff: Birth of Frontdoor Inc. (2018)

On the morning of October 1, 2018, a new ticker began trading on the Nasdaq Global Select Market. FTDR, Frontdoor Inc., opened for business as an independent public company for the first time. ServiceMaster shareholders received one share of Frontdoor common stock for every two shares of ServiceMaster they held, with ServiceMaster retaining approximately nineteen point eight percent of Frontdoor's outstanding stock. The distribution was structured to qualify as a tax-free transaction for U.S. federal income tax purposes.

The name "Frontdoor" was chosen deliberately. It evoked access, welcome, and the starting point of the home experience. Unlike "American Home Shield," which anchored the company to a specific product category, "Frontdoor" was a blank canvas that could encompass any home service. The name was a bet on the future, a declaration that this company intended to be more than what it had been.

The day-one profile was impressive by any standard. Revenue of approximately one point three billion dollars. More than two million active customers. A network of roughly fourteen thousand pre-qualified contractor firms. The largest home warranty brand in America in American Home Shield, supplemented by HSA, OneGuard, and Landmark. The company debuted with a market capitalization of approximately three point four billion dollars.

But the most consequential decision was the choice of CEO. Frontdoor did not hire a home services veteran or a warranty industry lifer. It hired Rex Tibbens, the former chief operating officer of Lyft. Tibbens had spent two years at the ride-sharing company, helping it achieve tenfold growth during a period of intense competition with Uber. Before Lyft, he had spent four years as a vice president at Amazon, working on Prime Now and Kindle initiatives. Before that, twelve years at Dell in operations, product development, and mergers and acquisitions. His career had started at Toyota, followed by a stint at Mercer Management Consulting.

The hiring of Tibbens was a signal that could not be misread. This was not going to be a story about incrementally improving a warranty company. This was going to be an attempt to transform a fifty-year-old service business into a technology platform.

Tibbens had seen what technology could do to transform logistics, delivery, and marketplace businesses. He looked at Frontdoor's contractor network, its customer base, and its decades of service data, and he saw raw material for something much bigger than a warranty company.

The challenge was equally enormous. Frontdoor inherited the technological infrastructure of a business that had been run as a division of a conglomerate for nearly thirty years. Call centers handled the bulk of customer interactions. Contractor dispatch was largely manual. Customer data was siloed and underutilized. The technical debt was staggering.

Wall Street was cautiously skeptical. "It's just a warranty company" was a common refrain. The stock opened in the low-to-mid thirties and promptly dropped nearly thirty percent after its first quarterly earnings report disappointed on margins. By late 2018, shares had fallen below twenty-five dollars. The market was pricing Frontdoor as exactly what the bears said it was: a mature, low-growth service business with limited upside.

But Tibbens and his team had a different thesis. They saw a company with a massive installed base of customers who trusted the brand, a contractor network that was the largest in the industry, and a treasure trove of service data spanning decades. The question was not whether the existing business was valuable. It was whether it could be rebuilt from the inside out.

The strategic pivot began immediately. Capital allocation freedom meant Frontdoor could invest in technology without competing for resources against Terminix's needs. The company began hiring engineers, product managers, and data scientists. The vision crystallized: Frontdoor would move from being a warranty provider to being a home services platform. Not just covering breakdowns, but preventing them. Not just dispatching contractors, but building a marketplace. Not just processing claims, but creating a digital experience that would define the future of home maintenance.

Whether the company could live up to the ambition embedded in its very name would depend on what happened next: a digital transformation unlike anything the home services industry had ever attempted.

VI. Digital Transformation: Reinventing the Core (2018-2020)

The transformation of Frontdoor from analog warranty company to digital home services platform happened on multiple fronts simultaneously, and that simultaneity was both the strategy's greatest strength and its greatest risk. You cannot shut down a business serving two million customers while you rebuild the technology. The plane had to be rebuilt in flight.

Picture the state of technology Frontdoor inherited. Imagine a customer service center circa 2017: rows of agents wearing headsets, each one pulling up customer records on aging software systems, manually looking up contractor availability in each service area, calling contractors one by one until someone accepted the job, then calling the customer back to confirm. Now imagine trying to build a modern digital experience on top of that infrastructure. That was the challenge.

The first priority was the customer experience. For decades, filing a home warranty claim meant calling a 1-800 number, waiting on hold, describing the problem to an agent, and then waiting hours or days for a contractor to be dispatched. There was no visibility into when the contractor would arrive, what the diagnosis was, or how long the repair would take. By 2018 standards, this was unacceptable. Consumers who could track a pizza delivery in real time expected at least as much from a major home repair.

Frontdoor invested in building self-service customer portals and mobile capabilities that allowed homeowners to file claims online, schedule service appointments, and track contractors in real time as they traveled to the home. This was not just about convenience. Every interaction that moved from the call center to digital channels reduced cost. A phone call to a customer service center costs several dollars. A self-service digital interaction costs pennies. At four million service requests annually, even modest improvements in digital adoption translated to significant operating leverage.

The contractor side of the platform received equal attention. Frontdoor built digital tools for contractors to receive dispatched jobs, manage their workflows, and integrate with Frontdoor's scheduling systems. Communication apps and remote diagnostic tools reduced the need for unnecessary truck rolls, situations where a technician drives to a home only to discover the problem requires a different specialist or a part that is not on the truck. Each avoided truck roll saved time and money for both the contractor and the customer.

The most ambitious technology bet came in December 2019, when Frontdoor acquired Streem, a Portland, Oregon-based startup that used augmented reality, computer vision, and machine learning to enable remote home service diagnosis. Streem's technology allowed an expert to conduct a video call with a homeowner, using the homeowner's smartphone camera to see the problem in real time. Augmented reality overlays could identify serial numbers, take precise measurements, and create three-dimensional spatial maps of the home environment.

The acquisition of Streem was a bet on a future where many service calls would begin virtually. A homeowner with a malfunctioning furnace could start a video session with a trained expert who could diagnose the issue remotely, order the right part, and dispatch the right technician with the right tools on the first visit. Streem's co-founder and CEO, Ryan Fink, and the Portland team stayed on, and the technology held over two dozen patents approved or pending. The specific financial terms of the deal were not disclosed, but it was structured as a combination of cash and incentive-based equity.

By October 2019, one year after the spinoff, Frontdoor had already begun implementing its technology transformation roadmap. Investments flowed into integrated technology platforms, self-service capabilities, customer care center operations, and contractor management systems. The early wins were measurable: reduced call center volumes, faster contractor dispatch times, and improved first-time fix rates. But the full transformation would take years, not months.

The balancing act between running the legacy business and building the future required constant calibration. Too much investment in technology too quickly could crater margins and alienate the contractor network that still operated largely on phone calls and paper. Too little investment would leave Frontdoor vulnerable to digital-native competitors. Tibbens, drawing on his experience scaling operations at Lyft and Amazon, pushed for speed while maintaining operational discipline. The result was sixteen consecutive quarters of profitable growth under his leadership, proof that transformation and profitability could coexist.

To understand why augmented reality mattered for this business, consider a typical service call without it. A homeowner calls to report their air conditioner is not cooling. A customer service agent asks a series of diagnostic questions over the phone, but the homeowner is not a technician and cannot accurately describe what they see. A contractor is dispatched, drives to the home, opens the unit, identifies the problem, and realizes they need a specific part that is not on their truck. They drive to a supplier, return, complete the repair. The whole process takes two visits and multiple days. Now picture the same scenario with Streem. The homeowner opens a video call on their phone. An expert sees the unit in real time through the camera, identifies the model number via AR overlays, diagnoses the likely issue, orders the correct part, and dispatches a technician who arrives with everything needed for a single-visit fix. That is the difference between analog and digital service delivery, and it is worth millions in saved truck rolls, reduced cycle times, and improved customer satisfaction.

The first-year results as an independent company were encouraging. Revenue for fiscal 2018 came in at one point two six billion dollars, with net income of one hundred twenty-five million and adjusted EBITDA of two hundred thirty-eight million. In 2019, the first full year of independence, revenue grew eight percent to one point three seven billion, net income improved twenty-three percent to one hundred fifty-three million, and adjusted EBITDA jumped to three hundred three million with margins expanding three hundred twenty-five basis points to twenty-two percent. The financial trajectory validated the spinoff thesis: freed from the conglomerate, the business could both grow and expand margins simultaneously.

VII. The ProConnect Platform: Building the Marketplace (2020-2022)

In 2020, Frontdoor made its most ambitious strategic move since the spinoff. It launched American Home Shield ProConnect, an on-demand home services platform that allowed consumers to schedule repairs and maintenance from vetted local professionals, completely separate from the traditional home warranty subscription.

This was a fundamentally different business than selling warranties. ProConnect was a marketplace. Customers could go online, select the service they needed, choose a two-hour appointment window, and book same-day or next-day appointments with transparent, upfront pricing. A thirty-day service guarantee backed every job. Real-time tracking showed the technician's progress en route.

The strategic significance was enormous. For its entire history, Frontdoor's predecessor companies had been in the warranty business: collect annual premiums, process claims, dispatch contractors. ProConnect opened the door to the vastly larger market of on-demand home services, a market estimated at approximately four hundred billion dollars.

Every homeowner needs repairs and maintenance, whether or not they have a warranty. ProConnect was designed to capture that broader demand.

By November 2020, ProConnect had expanded to thirty-five major metropolitan areas across the country, eventually reaching thirty-seven markets. The timing, in the middle of a global pandemic, was both challenging and fortuitous. COVID-19 had driven a surge in home improvement activity as millions of Americans spent dramatically more time at home. Appliance and plumbing failures spiked as systems ran harder and longer. Home services were classified as essential by state and local governments, allowing Frontdoor's contractor network to continue operating. Nearly all contractors remained active and accepting jobs throughout the pandemic.

The pandemic also accelerated Frontdoor's digital adoption. The company transitioned all employees to virtual work in March 2020 and in mid-2021 officially announced it would become a "virtual-first" company. Streem's augmented reality technology found an immediate use case in enabling contactless service interactions. In June 2020, Lowe's launched "Lowe's for Pros JobSIGHT powered by Streem" as part of a twenty-five million dollar commitment to support small businesses during COVID-19, extending Frontdoor's technology beyond its own ecosystem.

The expansion was not without growing pains. Building an on-demand marketplace requires different operational muscles than running a warranty business. Warranty claims are predictable in aggregate, governed by actuarial models built on decades of data. On-demand services are inherently variable, driven by individual homeowner needs at unpredictable times. The pricing, scheduling, quality control, and customer expectations are all different. Frontdoor was essentially learning to run a second business while managing the first.

The competitive landscape for on-demand home services was already crowded. Angi, the combined entity of Angie's List and HomeAdvisor, operated as a lead-generation marketplace connecting homeowners with service professionals. Thumbtack pursued a similar model in local services. Amazon had entered home services through its broader marketplace. But Frontdoor's model was fundamentally different from lead generation. When a contractor works through Angi or Thumbtack, they receive leads, potential customer inquiries that may or may not convert into paid work. When a contractor works through Frontdoor, they receive dispatched, paid jobs. The distinction matters enormously to contractors, who prefer guaranteed work over uncertain leads.

The network effects strategy was deliberate. More contractors on the platform meant better geographic coverage and faster response times, which attracted more customers, which attracted more contractors.

Frontdoor's existing warranty business gave it a head start. It already had seventeen thousand pre-qualified contractor firms employing roughly sixty thousand technicians. ProConnect leveraged that existing network rather than building from scratch, a massive structural advantage over any startup trying to build a home services marketplace from zero.

Full-year 2020 results reflected the pandemic's mixed impact: revenue increased eight percent to one point forty-seven billion dollars, home service plan growth accelerated to four percent, and customer retention increased to seventy-six percent. The company served 2.2 million customers through its contractor network. American Home Shield's market share expanded from forty-two percent of the industry in 2010 to nearly forty-seven percent by 2020, a testament to the consolidation strategy that had been building for years.

More telling was the direct-to-consumer channel, where first-year revenue increased thirteen percent in the fourth quarter. The pandemic was teaching Americans to buy services online, and Frontdoor was there to meet them. The real estate channel slowed as lockdowns reduced home transactions, but the DTC channel more than compensated, foreshadowing the strategic shift that would become central to the company's playbook.

The pandemic also stress-tested the contractor network. Frontdoor incurred incremental costs at customer care centers due to higher demand driven by temporary closures at offshore business process outsourcers. Service requests in appliance and plumbing trades surged as customers sheltered at home, running their systems harder than ever. The company managed through it, but the experience reinforced the critical importance of contractor network depth and resilience.

VIII. Strategic Pivots & Business Model Evolution (2020-Present)

The years following the ProConnect launch saw Frontdoor's strategy crystallize around a central insight: the warranty alone was not enough. The real value lay in owning the entire customer relationship around home maintenance.

Consider the economics. A home warranty customer pays around nine hundred to nine hundred fifty dollars per year. That customer's home contains multiple systems and appliances that will need service, upgrades, and replacements over time. The average American homeowner spends thousands of dollars annually on home maintenance and improvement. Frontdoor estimated a roughly two billion dollar opportunity within its existing member base alone for non-warranty services. The warranty was not the product. The warranty was the wedge.

This realization drove several parallel strategic initiatives.

First, subscription model expansion. Frontdoor introduced new warranty tiers, add-on coverage options, and bundling strategies designed to increase revenue per customer while giving homeowners more flexibility to customize their coverage. The goal was to move from a one-size-fits-all warranty to a menu of home protection options.

Second, the direct-to-consumer push intensified. The channel economics told a stark story. Direct-to-consumer customers had a first-year retention rate of approximately seventy-four percent. Real estate channel customers, who often received the warranty as a gift from the seller or listing agent, retained at only twenty-nine percent in the first year. The lifetime value differential was dramatic. A customer who chose and paid for their own warranty was far more likely to see it as valuable and renew it year after year. Frontdoor began investing heavily in digital advertising, targeted marketing campaigns, and promotional strategies to shift the mix toward DTC. By 2025, DTC membership grew three percent, with organic growth hitting nine percent in the second quarter.

Third, the HVAC upgrade program emerged as a breakthrough in non-warranty revenue. When a covered air conditioning system reached the end of its life, Frontdoor could offer the homeowner a full system replacement, not just a warranty-covered repair, but a premium installation at a competitive price. The company handled everything: selecting the right system, scheduling the installation, and managing the contractor. In 2025, this program generated one hundred twenty-eight million dollars in revenue, growing forty-eight percent year over year, with approximately fifty-five thousand installations completed. At roughly twenty percent gross margins, it was not as profitable as the warranty business, but it demonstrated the power of the cross-sell model. An appliance upgrade program launched in select markets was planned for broader rollout by late 2026.

The Streem technology evolved from a remote diagnosis tool into a consumer product. In April 2023, Frontdoor launched the Frontdoor app, powered by Streem's augmented reality technology, connecting homeowners with pre-qualified experts via video chat for real-time diagnosis and solutions. The app offered membership tiers: a free Basic plan with one video chat session, and a Prime plan at ninety-nine dollars per year with three sessions and discounts on equipment. In October 2024, the dedicated AHS mobile app launched and attracted nearly six hundred thousand downloads by the end of 2025.

In August 2023, Streem expanded beyond Frontdoor's own ecosystem with the launch of StreemCore on the Salesforce AppExchange, offering enterprise customers a no-download video assistance tool integrated with Salesforce, Amazon Web Services, Genesys, Five9, and other platforms. By 2023, contractors participating in surveys reported reducing truck rolls seventy percent of the time after a Streem session. The technology was proving its value not just for Frontdoor's own operations, but as a standalone enterprise product.

In April 2024, Frontdoor launched a major brand relaunch for American Home Shield under the tagline "Don't Worry. Be Warranty," featuring actress and comedian Rachel Dratch as a new brand character called Warrantina. The campaign, created by agency Fallon with media support from Chemistry, was designed to transform consumer perception of home warranties from confusing and boring to approachable and even fun. Partnerships with WWE and HGTV extended the brand's reach.

Then came the biggest strategic bet since the spinoff itself. On June 4, 2024, Frontdoor announced the acquisition of 2-10 Home Buyers Warranty for five hundred eighty-five million dollars in cash. Founded in Denver in 1980, 2-10 HBW was a different kind of home warranty company. While American Home Shield covered existing homes, 2-10 specialized in new home structural warranty plans, insurance-backed offerings that provided builders coverage for structural failures. Approximately one in five new homes built in the United States carried a 2-10 structural warranty. The company had revenue of one hundred ninety-eight million dollars and adjusted EBITDA of forty-three million dollars in 2023, serving roughly two hundred ninety-two thousand customers through a network of nineteen thousand home builders.

The deal closed on December 19, 2024, funded by a new one point forty-seven billion dollar credit facility. The strategic rationale was multi-layered. The acquisition gave Frontdoor entry into the new construction market for the first time, diversifying beyond its core existing-home warranty business. It added a network of nineteen thousand builder relationships that could be cross-sold Frontdoor's home warranty and on-demand services. And it created opportunities for the home builder to offer the homebuyer both a structural warranty and a systems-and-appliances warranty at the point of new home purchase, capturing the customer relationship from day one of homeownership.

Think about the customer lifecycle this creates. A home builder uses 2-10 to provide a ten-year structural warranty on a new home. At the point of sale, the buyer is offered an AHS systems-and-appliances warranty. Five years later, when the HVAC system needs upgrading, Frontdoor's HVAC upgrade program handles the installation. When the dishwasher dies, the warranty covers the replacement. When the homeowner needs a plumber for a non-covered issue, ProConnect dispatches one. Frontdoor has the potential to own the entire maintenance relationship from the moment a home is built through its entire lifecycle. That is the platform vision made tangible through acquisition.

The risk, of course, is integration. Combining two distinct businesses with different cultures, systems, and customer bases is never easy. The five hundred eighty-five million dollar price tag, at roughly three times revenue and fourteen times EBITDA, was not cheap. And the debt taken on to fund the deal added meaningful leverage to a previously conservative balance sheet. But management expressed confidence that the deal would be accretive to earnings within the first full year of ownership.

IX. The Competitive Gauntlet & Market Dynamics (2022-2024)

The period from 2022 through 2024 tested Frontdoor in ways the spinoff architects never anticipated. A perfect storm of macroeconomic headwinds, competitive pressure, and internal challenges pushed the company to its lowest point before a remarkable recovery.

Start with the macroeconomic picture. The Federal Reserve's aggressive interest rate hiking cycle that began in 2022 froze the housing market. Existing home sales, the engine that feeds new warranty sign-ups through the real estate channel, plummeted. Fewer home transactions meant fewer opportunities to sell warranties at the point of sale. Simultaneously, inflation drove up contractor wages, parts costs, and service expenses. The combination of falling new customer acquisition and rising service costs created a margin vise that squeezed the business hard.

The financial results told the story. In 2022, revenue grew modestly to one point sixty-six billion dollars, but net income collapsed to seventy-one million dollars from one hundred twenty-eight million the prior year. Adjusted EBITDA margins compressed. The stock price followed, falling to an all-time low of nineteen dollars and six cents on December 23, 2022. The market cap had fallen from the three-point-four billion dollar debut valuation to approximately one and a half billion dollars. Frontdoor had lost more than half its value.

It was during this trough that leadership transitioned. In May 2022, the company announced that Rex Tibbens would step down as CEO, with Bill Cobb, who had served as chairman of the board since the 2018 spinoff, assuming the role effective June 1, 2022. Cobb brought a different but complementary skillset. He had served as president and CEO of H&R Block from 2011 to 2017, steering another legacy consumer services company through a period of digital transformation. Before that, he spent nearly eight years at eBay, including four years as president of eBay Marketplaces North America. Cobb understood both consumer services businesses and marketplace dynamics.

The competitive landscape was evolving rapidly. In the home warranty space, Choice Home Warranty competed aggressively on price. First American Home Warranty leveraged its parent company's deep real estate industry relationships. Cinch Home Services, backed by private equity, pursued its own growth strategy. HomeServe USA, focused on home repair and emergency services, was acquired by Brookfield Asset Management in 2023, injecting significant institutional capital into the space.

In the broader home services market, the competitive dynamics were even more intense. Angi, despite its own struggles with profitability, maintained the largest digital marketplace for home services. Thumbtack grew rapidly in local services. Amazon continued expanding its home services offerings, leveraging its unmatched consumer trust and logistics infrastructure. The threat of big tech entry remained an ever-present concern.

The contractor shortage crisis compounded these challenges. A nationwide labor shortage in the skilled trades meant contractors had more work than they could handle. Plumbers, electricians, and HVAC technicians could pick and choose their jobs. This gave contractors leverage over warranty companies, which traditionally offered lower per-job compensation than a contractor could earn on the open market. Frontdoor needed its contractors more than its contractors needed Frontdoor, a dynamic the company's platform strategy was specifically designed to reverse over time.

Frontdoor also responded to contractor leverage through its Contractor Quality Awards program, recognizing top-performing contractors with twenty-five thousand dollar prizes and "Preferred Contractor" status across five key trades: pool, appliance, electrical, HVAC, and plumbing. The program was not just about recognition. It was about creating financial incentives that aligned contractor behavior with customer satisfaction. By offering preferred contractors higher priority dispatches and more volume, Frontdoor created a tournament dynamic where the best contractors competed to maintain their status, raising quality across the entire network.

Cobb's response to the broader challenges was methodical. He focused on stabilizing the member count, which had been declining as the real estate market dried up. He pushed the DTC channel hard, investing in digital marketing and the Rachel Dratch brand campaign. He scaled the non-warranty revenue streams, particularly the HVAC upgrade program. And he maintained cost discipline, driving operational efficiency gains that expanded margins even as the top line faced headwinds.

The recovery was striking and validates one of the most important lessons for long-term investors: distinguish between cyclical pain and structural decline. From the 2022 trough, Frontdoor's financial performance improved dramatically year by year. Revenue grew to one point seventy-eight billion in 2023, with gross margins hitting a nine-year high of fifty percent. In 2024, the company reported what management called "record full-year results": revenue reached one point eighty-four billion, net income more than tripled to two hundred thirty-five million dollars, and free cash flow more than doubled. The stock recovered from its sub-twenty-dollar nadir to trade in the forties and fifties, rewarding investors who understood that the 2022 selloff was a cyclical overreaction, not a structural verdict.

The turnaround demonstrated something important about the home warranty business model. The recurring revenue base, with seventy-six percent of warranty revenue coming from renewals, provided a floor even in the worst market conditions. When the macro environment improved, the operating leverage in the model amplified the recovery. This resilience through the cycle would prove to be one of the most important characteristics for long-term investors to understand.

There is a myth-versus-reality dynamic worth addressing here. The consensus narrative in 2022 was that Frontdoor was a declining business in a commoditized market, losing customers to competitors and substitutes with no path to growth. The reality was more nuanced. Yes, the member count was declining, but largely because the real estate channel had dried up due to macro factors beyond the company's control. The underlying product was not broken. Renewal rates held steady, proving that customers who had the warranty valued it enough to keep paying. The DTC channel was growing, proving that demand existed outside the real estate transaction. And the HVAC upgrade program was scaling rapidly, proving that the customer relationship could be monetized beyond warranty premiums. The stock's recovery from nineteen dollars to seventy dollars was not a speculative bubble. It was the market correcting a mispricing that had conflated cyclical headwinds with structural decline.

X. Business Model Deep Dive & Unit Economics

Understanding Frontdoor's economics requires thinking about the business as three interconnected engines: customer acquisition, service delivery, and renewal.

The customer acquisition engine operates through two primary channels. The real estate channel captures customers at the point of home purchase, typically paid for by the seller or listing agent. The direct-to-consumer channel acquires customers through marketing, digital advertising, and word of mouth.

The economics of these channels differ dramatically. DTC customers retain at approximately seventy-four percent in the first year. Real estate customers retain at only twenty-nine percent. This means a DTC customer, on average, generates roughly two and a half times the lifetime revenue of a real estate customer. The company has been systematically shifting its acquisition mix toward DTC, which now represents the majority of new customer growth.

The service delivery engine is where operational excellence translates to margin. When a customer files a claim, Frontdoor must dispatch a qualified contractor, manage the diagnosis and repair, source any needed parts, and resolve the issue to the customer's satisfaction. The efficiency of this process drives the gap between premium revenue and claims cost. Scale matters enormously here. With roughly three point eight million service requests annually, Frontdoor can negotiate better rates with contractors and parts suppliers, optimize dispatch routing, and build institutional knowledge about common failure patterns. Technology investments in digital dispatch, Streem-based remote diagnosis, and predictive analytics all work to reduce the cost per service event.

The renewal engine is the business's most valuable asset. Approximately seventy-six percent of home warranty revenue comes from renewals, not new sales. Renewal customers cost essentially nothing to acquire. They have demonstrated willingness to pay. And their retention rates improve with tenure, as switching costs increase through familiarity with the process, accumulated coverage history, and simple inertia. The renewal rate reached seventy-five percent in 2025, up one hundred fifty basis points year over year.

The float dynamics add another layer. Frontdoor collects premiums upfront, at the beginning of the contract year, but pays claims over the following twelve months as service requests come in. This creates a natural float, cash received before it must be paid out, that the company can invest or use for operations. It is not an insurance float in the technical sense, but the economic effect is similar: the business generates cash before it incurs costs.

Non-warranty revenue streams are increasingly important. The HVAC upgrade program alone generated one hundred twenty-eight million dollars in 2025. Combined with other non-warranty services, total non-warranty revenue grew sixty-six percent in 2025, and the company guided to two hundred twenty to two hundred forty million dollars in 2026. Management estimates a roughly two billion dollar cross-sell opportunity within its existing member base. At only about two and a half percent penetration on HVAC installations, roughly fifty-five thousand out of 2.1 million members, the runway is long.

Revenue per member sits at approximately nine hundred to nine hundred fifty dollars annually, based on roughly two billion in warranty revenue divided by 2.1 million members. The company does not disclose explicit customer acquisition cost or lifetime value figures, but the seventy-four percent DTC retention rate and the growing average revenue per member suggest strong unit economics that improve with each passing year.

Comparing Frontdoor to adjacent business models is illuminating. Like an insurance company, it collects premiums and pays claims. Like a SaaS company, it generates recurring subscription revenue with strong retention. Like a marketplace, it matches supply (contractors) with demand (homeowners). But unlike pure-play versions of any of these models, Frontdoor is all three simultaneously, which makes it both harder to categorize and potentially more defensible.

The insurance comparison deserves particular attention. Warren Buffett has built Berkshire Hathaway's empire partly on the concept of insurance float, collecting premiums today that will be paid out in claims tomorrow, and investing that float in the interim. Frontdoor's dynamics are a scaled-down version of the same principle. The company collects warranty premiums at the start of the contract year and pays out claims over the following twelve months. The float is smaller and shorter-duration than a property-casualty insurer, but the principle is identical: the business is effectively being funded by its customers. This is one reason free cash flow conversion is strong, the cash comes in before the expenses go out.

The vulnerability in the model lies in the claims ratio. In a bad year, when extreme weather drives HVAC failures or when parts inflation spikes unexpectedly, claims costs can eat into margins rapidly. The company manages this risk through pricing discipline, adjusting premiums annually to reflect anticipated claims costs, and through operational efficiency, using technology to reduce the cost per claim. But unlike a traditional insurance company, Frontdoor does not have the ability to reinsure its risk or diversify across uncorrelated risk pools. Every warranty covers the same basic set of home systems and appliances, exposed to the same weather patterns and the same inflationary pressures. This concentration of risk is the model's primary structural weakness.

An important accounting consideration for investors is the revenue recognition treatment of home warranty contracts. Premiums are recognized ratably over the twelve-month contract period, meaning a sale in January generates revenue evenly across all twelve months. This creates a natural smoothing effect in quarterly results but also means that changes in customer acquisition or retention take time to fully manifest in reported revenue. Investors should pay close attention to home service plan count and renewal rate trends, which are leading indicators that precede revenue changes by several quarters.

XI. Porter's Five Forces Analysis

Competitive Rivalry: Medium-High. The home warranty market is fragmented but intensifying. Frontdoor commands approximately forty to fifty percent market share by revenue, a dominant position but not a monopoly. Choice Home Warranty, First American, and Cinch compete on price and service quality. Digital-native entrants are changing customer expectations around transparency and convenience. Price competition exists, but switching costs for renewal customers and the trust required in home services create meaningful differentiation beyond price alone. The rivalry is real but manageable for the market leader.

Threat of New Entrants: Medium. The barriers to entry in home warranties are higher than they appear. Building a contractor network with national coverage takes years and significant operational investment. Regulatory licenses are required in most states. Brand trust matters enormously when homeowners are letting strangers into their homes. Capital requirements for claims reserves create a financial barrier. However, technology is lowering some barriers. A well-funded startup or a big tech company with existing consumer relationships could theoretically enter the market quickly. Amazon, in particular, has the customer base, logistics infrastructure, and financial resources to be a formidable entrant. The question is whether the margin profile of home warranties is attractive enough to justify big tech's attention.

Supplier Power (Contractors): Medium-High. This is the force that has most defined Frontdoor's strategic challenges in recent years. The nationwide skilled labor shortage has given contractors significant leverage. Plumbers, electricians, and HVAC technicians are in high demand across the economy. Frontdoor's contractors can often earn more per job working directly for homeowners or through higher-paying channels. Frontdoor partially mitigates this through volume, giving contractors a steady stream of guaranteed work, and through its platform investments that make contractors' businesses more efficient. The HVAC upgrade program, which offers contractors premium installation jobs with higher payouts, is a direct response to this dynamic. The platform strategy aims to make Frontdoor so central to a contractor's business that leaving the network becomes costly.

Buyer Power (Homeowners): Medium. Homeowners have many alternatives for home services, from competing warranty providers to direct contractor hiring through Angi, Thumbtack, or Nextdoor, to the ultimate substitute of doing nothing and waiting for catastrophic failure. For new warranty purchases, switching costs are low since the product is largely commoditized in the buyer's perception. But for renewals, the switching cost calculation changes. A customer who has used their warranty successfully, who knows the process, and who trusts the contractor network faces real friction in switching. The seventy-five percent overall renewal rate and seventy-four percent DTC first-year retention rate confirm that buyer power is moderated by experience and habit.

Threat of Substitutes: Medium-High. The substitutes for home warranties are numerous. Self-service repair, fueled by YouTube tutorials and the broader DIY culture, allows handy homeowners to bypass warranty companies entirely. Traditional homeowners insurance riders can cover some equipment breakdowns. Direct contractor hiring through digital marketplaces eliminates the middleman. Extended manufacturer warranties cover newer appliances. Home maintenance savings accounts, where homeowners set aside money each month for repairs, serve as a self-insurance alternative. Each of these substitutes captures a slice of the addressable market, keeping overall household penetration at around five percent despite decades of industry growth.

XII. Hamilton's 7 Powers Analysis

Scale Economies: Moderate and Building. Frontdoor's scale advantages are real but not yet decisive. The company spreads fixed technology costs, claims processing infrastructure, and corporate overhead across two billion dollars in revenue and 2.1 million members. Its national contractor network is harder for smaller players to replicate. Customer acquisition efficiency improves with brand recognition and data-driven targeting. But the home warranty business has relatively high variable costs, since each claim requires a contractor visit, parts, and labor, which limits the classic fixed-cost leverage that drives scale advantages in software or manufacturing. The 2-10 HBW acquisition adds scale in a new dimension, the builder channel, that competitors cannot easily replicate.

Network Effects: Moderate and Accelerating. This is where Frontdoor's story gets most interesting. The company is building genuine two-sided network effects through its platform. More contractors on the network means better geographic coverage, faster response times, and more specialized expertise available, which improves service quality for customers. More customers means more jobs for contractors, which attracts and retains higher-quality service providers. The data network effect is equally powerful: more claims generate more data about failure patterns, contractor performance, and optimal pricing, which improves the prediction models that drive dispatch efficiency and cost management. These network effects are still early compared to mature marketplaces like Uber or Amazon, but they are real and accelerating.

Counter-Positioning: Weak. Frontdoor does not have a strong counter-positioning advantage. Its business model is well understood by competitors, and similar approaches are being pursued by multiple players. The digital transformation that Frontdoor has undertaken is increasingly table stakes rather than a source of differentiation. Competitors can and do invest in similar technology, marketing, and platform capabilities. The advantage, such as it is, comes from Frontdoor's head start and scale rather than from a business model that incumbents cannot or will not copy.

Switching Costs: Moderate. For renewal customers, switching costs are meaningful. A customer who has used their warranty, built a claims history, and become familiar with the process faces real friction in moving to a competitor. Smart home integration and the Frontdoor app create additional stickiness. But for new customer acquisition, switching costs are essentially zero. The warranty is a commodity product in most consumers' eyes, and the decision often comes down to price, coverage options, and brand trust.

Branding: Moderate. American Home Shield carries more than fifty years of brand equity. In the home warranty space, it is the most recognized name, particularly among real estate professionals. Trust matters enormously in home services, where customers are letting strangers into their homes to work on critical systems. The AHS brand conveys reliability and longevity. The Frontdoor parent brand is still developing consumer recognition. The 2024 brand relaunch with the "Don't Worry. Be Warranty." campaign represents a significant investment in modernizing the brand's image for a younger, digitally native audience.

Cornered Resource: Weak to Moderate. Frontdoor's most valuable resource is its decades of historical claims data, covering millions of service events across every major home system and appliance, in every climate and geography across America. This data informs predictions about what breaks, when, and how much it costs to fix. However, this data is not truly proprietary in the sense that competitors cannot build their own data sets over time. Contractor relationships, while extensive, are not exclusive, as most contractors work with multiple warranty companies and direct customers simultaneously. The 2-10 HBW builder network of nineteen thousand relationships is more defensible, as these are long-term structural warranty commitments that create genuine lock-in.

Process Power: Moderate and Growing. This may be Frontdoor's most underappreciated advantage. Fifty years of managing home warranty claims has produced deep institutional knowledge about claims management, contractor quality control, parts sourcing, and customer communication. Proprietary algorithms for contractor matching and dispatch routing have been refined over millions of service events. The integration of Streem's augmented reality technology into the service workflow represents a process innovation that reduces truck rolls and improves first-time fix rates. As the company continues to invest in technology and data science, this process power compounds.

Overall Assessment. Frontdoor is building toward Network Effects and Scale Economies as its primary powers, with Process Power as the foundation. The company's transition from a legacy warranty provider to a technology-enabled platform is the strategic bet designed to strengthen these moats over time. The powers are real but still developing. The key question is whether Frontdoor can build network effects strong enough to create a winner-take-most dynamic in home services, or whether the market remains permanently fragmented.

XIII. The Bull and Bear Case

The Bull Case

The most interesting companies are those where the bull and bear cases are both intellectually honest and fundamentally irreconcilable. Frontdoor is one of those companies. Both sides of the debate have strong evidence, and the outcome likely depends on variables that cannot be known with certainty today. That ambiguity is what creates opportunity for patient investors who can develop a differentiated view.

The optimistic thesis for Frontdoor rests on several mutually reinforcing pillars.

Start with the total addressable market. Only about five percent of American households have a home warranty. In California, where the category is best established, penetration in real estate transactions reaches ninety-two percent. If even a fraction of the remaining ninety-five percent of American homes could be converted to warranty customers through the direct-to-consumer channel, the growth runway stretches for decades.

Demographic trends reinforce this: the American housing stock is aging, homeowners are staying in their homes longer, and the average age of major home systems means replacement cycles are accelerating.

The subscription economics are genuinely attractive. Seventy-six percent of warranty revenue comes from renewals, creating a base of predictable, recurring revenue that most consumer services companies would envy. The seventy-five percent renewal rate means the company retains the vast majority of its revenue base each year, requiring only modest new customer acquisition to maintain and grow. This is not the leaky-bucket economics of many consumer businesses.

The platform strategy, if it works, could be transformative. Frontdoor sits at the intersection of two massive markets: the four-billion-dollar home warranty market, where it already dominates, and the four-hundred-billion-dollar home services market, where it is just beginning to build presence.

The HVAC upgrade program, growing at forty-eight percent annually and already generating one hundred twenty-eight million dollars, is proof of concept for the cross-sell model. Management estimates a two-billion-dollar opportunity within the existing member base alone. If the appliance upgrade program, home maintenance subscriptions, and other services can replicate even a fraction of the HVAC program's success, the revenue growth algorithm changes entirely.

The data moat grows with every service event. Machine learning models trained on decades of claims data can predict when specific systems in specific homes are likely to fail, enabling proactive maintenance offerings that prevent breakdowns before they happen. This would transform the value proposition from "we fix things when they break" to "we make sure things don't break," a dramatically more compelling customer experience.

The capital return program is aggressive. The company has repurchased approximately seven hundred twenty million dollars of stock since 2021, reducing the share count by roughly seventeen percent. At current free cash flow generation of nearly four hundred million dollars annually, Frontdoor has ample capacity to continue buying back shares while also investing in growth and servicing its acquisition debt.

The Bear Case

Now for the other side, because every good analysis must honestly grapple with the counter-thesis.

The bearish case begins with commoditization. At its core, a home warranty is a simple product: pay a premium, get covered. There is limited differentiation between providers on the basic offering. Price competition is real, and rising customer acquisition costs suggest it is getting harder to convince homeowners to choose one warranty over another or to choose a warranty at all. The five percent household penetration rate after fifty-plus years of industry existence could indicate a structural ceiling on consumer demand, not an untapped opportunity.

Contractor supply remains the business's most critical vulnerability. The skilled labor shortage in America is not a cyclical problem. It is a structural one driven by decades of underinvestment in vocational training and the retirement of the baby boomer generation of tradespeople.

If Frontdoor cannot attract and retain enough qualified contractors, service quality degrades, claim resolution times lengthen, and customers leave. No amount of technology can fix a service request if there is no technician available to do the work.

Big tech represents an existential risk. Amazon already offers home services through its marketplace. Google could leverage its search dominance and local business data to enter the space. Apple's HomeKit and broader smart home ecosystem could evolve into a service platform. Any of these companies could acquire or build a home services marketplace with vastly more resources than Frontdoor can deploy. The question is whether big tech's margin expectations are compatible with the economics of home services, but it is a question, not an answer.

The real estate channel, while declining in importance, still matters. Existing home sales remain well below historical norms due to high mortgage rates and the "lock-in" effect of homeowners unwilling to give up low-rate mortgages. A sustained housing market slowdown would continue to pressure new customer acquisition.

The balance sheet now carries meaningful debt following the 2-10 HBW acquisition. The one point forty-seven billion dollar credit facility, while manageable at current earnings levels, represents a step change in financial leverage for a company that had been relatively conservatively capitalized. Any significant operational disruption or margin compression could make that debt feel heavier.

Finally, the digital transformation, while impressive, is not unique. Every home services company is investing in technology, mobile apps, and data analytics. Frontdoor's technology investments are necessary to stay competitive, but they may not be sufficient to create lasting differentiation if competitors match them.

Key KPIs to Track

For investors monitoring Frontdoor's ongoing performance, two metrics matter above all others. First, member count growth and renewal rate. The member count is the single most important indicator of the business's health. After years of decline, the company achieved two consecutive quarters of sequential member growth in 2025, the first time in five years. If member count can sustain growth while renewal rates hold at seventy-five percent or above, the compounding effect on revenue and profitability is powerful. Conversely, any renewed decline in member count would signal that the strategic investments are not working. Second, non-warranty revenue as a percentage of total revenue. This metric captures the success of the platform pivot. Non-warranty revenue, driven by the HVAC upgrade program, appliance upgrades, and on-demand services, represents the transition from a warranty company to a home services platform. If this number grows from roughly ten percent of revenue today toward twenty or twenty-five percent over time, it would validate the bull thesis that Frontdoor can monetize its customer relationships far beyond warranty premiums.

XIV. Lessons & Playbook: What Founders and Investors Can Learn

Every deep dive should leave investors with actionable frameworks. The Frontdoor story offers a rich set of lessons that extend well beyond the home warranty industry.

The Spinoff Opportunity. Corporate orphans, businesses buried within conglomerates where they receive insufficient attention, capital, and strategic focus, can unlock enormous value through independence. American Home Shield spent nearly thirty years as a division of ServiceMaster, never receiving the dedicated technology investment or strategic clarity it needed. Within two years of the spinoff, Frontdoor had launched a digital transformation, acquired an AR technology company, and begun building a marketplace platform. None of this would have happened inside ServiceMaster. For investors, spinoffs remain one of the most reliable sources of value creation in public markets.

Digital Transformation at Scale. Frontdoor's transformation story is instructive precisely because it did not follow the Silicon Valley playbook. The company did not burn cash to acquire growth. It did not abandon its legacy business to chase the new thing. Instead, it ran the existing business for cash flow while systematically investing in technology that improved unit economics. Rex Tibbens, the former Lyft COO, brought technology company rigor to a fifty-year-old service business, but he respected the fundamentals of the existing model. The result was sixteen consecutive quarters of profitable growth during the transformation period. This "transform while performing" approach is relevant to any legacy business facing digital disruption.

The Power of Boring. Home warranties are not exciting. They do not generate headlines or attract conference keynotes. But the economics are exceptional: recurring revenue, high retention, low capital intensity, and genuine utility for customers. The lesson for investors is that unsexy businesses operating in ignored corners of the economy can produce outstanding returns precisely because they attract less competition and less speculative capital. Frontdoor's stock tripled from its December 2022 low to its October 2025 high while most investors were focused on AI stocks.

Marketplace Dynamics in Service Industries. Building a two-sided marketplace in services is fundamentally harder than building one in goods. Service quality is variable, dependent on individual human beings showing up and doing skilled work. Trust is critical because the service is delivered inside the customer's home. Geographic density matters because response time is a key quality metric. Frontdoor's approach, leveraging an existing contractor network built over decades rather than trying to build one from scratch, is a playbook for anyone trying to build a service marketplace. Start with supply, because in service industries, supply is the hard side of the market.

Platform vs. Product Thinking. The strategic decision to become a platform rather than just a product company is one of the most consequential choices any business can make. A product company sells things. A platform company creates infrastructure on which others build and transact. Amazon made this transition from bookseller to marketplace. Frontdoor is attempting the same transition from warranty seller to home services platform. The difference in long-term value creation between these two models is enormous, but so is the difficulty of execution. The platform must be valuable enough to both sides, homeowners and contractors, that they choose to transact through it rather than around it. Frontdoor's advantage is that the warranty business creates a captive starting relationship, but the challenge is extending that relationship beyond the warranty transaction into broader home services.

Data as Compounding Advantage. Every service event generates data: what broke, when it broke, how long it took to fix, how much it cost, which contractor performed the work, and how satisfied the customer was. Over fifty years and millions of service events, this data set has become a genuine strategic asset. Machine learning models can now predict failure patterns, optimize contractor matching, and enable proactive maintenance. The lesson is that data advantages compound over time, and the companies that have been collecting data the longest, even through non-digital means, may have the most valuable datasets if they can digitize and analyze them effectively.

Capital Allocation Discipline. Since the spinoff, Frontdoor has demonstrated thoughtful capital allocation. The share repurchase program has returned over seven hundred million dollars to shareholders, reducing the share count by approximately seventeen percent. The 2-10 HBW acquisition was funded prudently through a new credit facility without diluting shareholders. The company has invested in technology and marketing while maintaining positive free cash flow. This balanced approach, returning cash when the stock is undervalued, investing when opportunities arise, and avoiding the temptation to over-lever for growth, is a model for mid-cap companies.

Managing Contractors: The Supply-Side Challenge. Perhaps the most underappreciated lesson from the Frontdoor story is how to manage a distributed workforce that you do not employ. Frontdoor's network of seventeen thousand contractor firms and over one hundred fifty thousand technicians are independent businesses, not employees. They choose whether to accept jobs, how many to take, and what quality to deliver. Managing this relationship requires a delicate balance of financial incentives, volume guarantees, technology tools, and quality enforcement. The Contractor Quality Awards program, which gives twenty-five thousand dollar prizes to top performers across five key trades and grants "Preferred Contractor" status with increased referral volume, is one example of how Frontdoor uses incentive design to align contractor behavior with customer satisfaction. Award winners in 2024 saw a twenty percent increase in service requests post-award, demonstrating the power of the feedback loop. Anyone building a service marketplace needs to study how Frontdoor manages its supply side.

Subscription Model Mastery. The evolution from single-product warranty to multi-tier subscription with add-ons and cross-sell opportunities is a masterclass in subscription economics. The key insight is that acquisition is expensive but retention is profitable. Every percentage point improvement in renewal rate drops almost directly to the bottom line, since the customer is already on the platform and the marginal cost to retain them is near zero. Frontdoor's journey from a seventy-three percent renewal rate at the time of the spinoff to seventy-five percent in 2025, while seemingly modest, represents tens of millions of dollars in incremental annual revenue and profit.

XV. Current State & Recent Developments (2024-Present)

Frontdoor enters 2026 in the strongest financial and strategic position in its history as a public company.