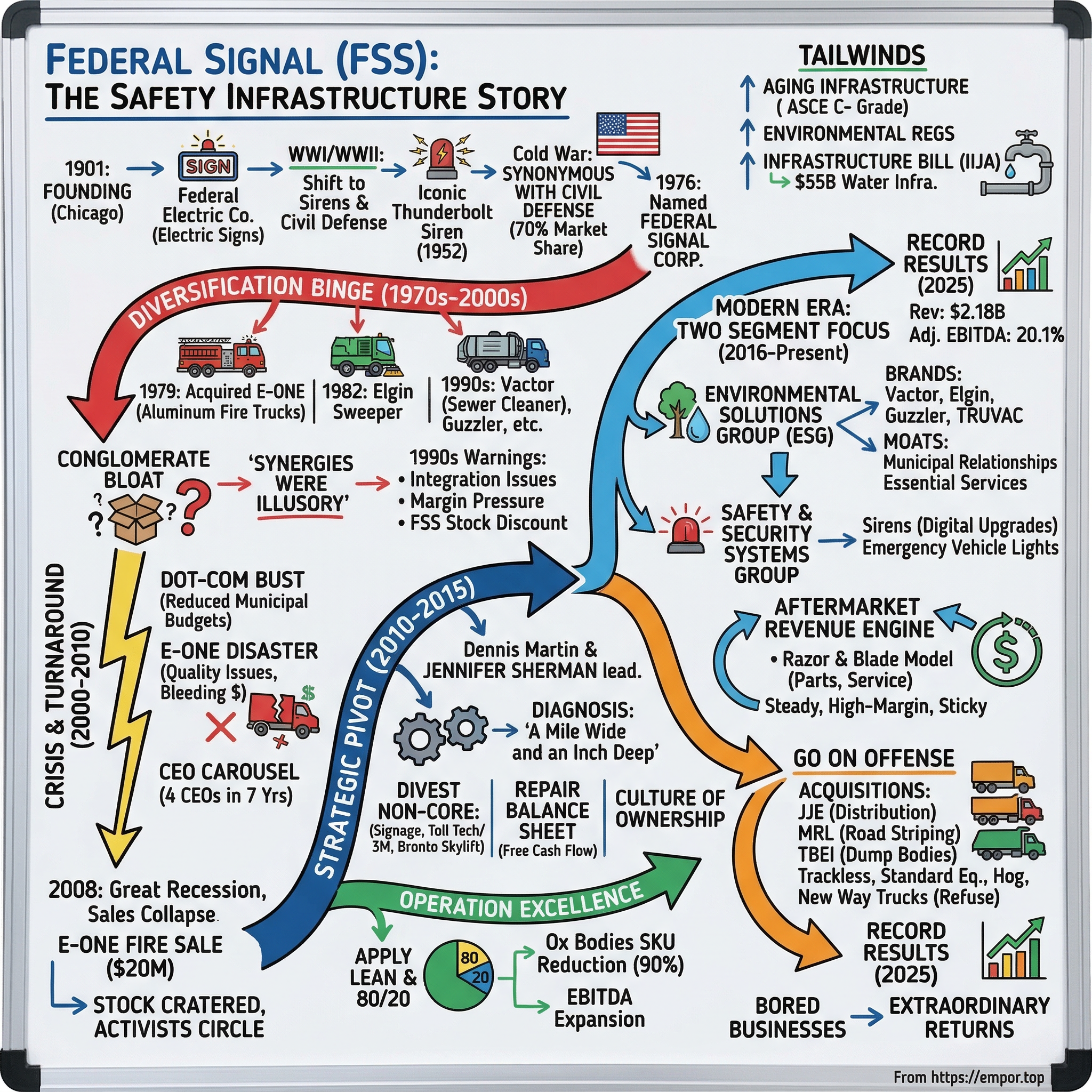

Federal Signal Corporation: The Story of America's Safety Infrastructure Company

I. Introduction & Episode Roadmap

There is a sound that every American who grew up in tornado country knows in their bones. It is a rising, wailing cry that cuts through summer heat and Friday night football games alike—a sound that means "get underground, now." That sound, more likely than not, came from a Federal Signal siren. And yet, if you stopped most investors on Wall Street and asked them what Federal Signal does, you would get a blank stare. That anonymity is precisely what makes this story so compelling.

Federal Signal Corporation, trading on the NYSE under ticker FSS, is a roughly two-billion-dollar revenue company that sits at the intersection of public safety, environmental infrastructure, and municipal services. Its products are everywhere and invisible: the street sweepers cleaning downtown after a parade, the vacuum trucks maintaining sewer lines beneath city streets, the emergency vehicle lights flashing on police cruisers, and yes, the outdoor warning sirens that blanket thousands of American communities. The company manufactures and sells equipment that cities literally cannot function without.

But here is the question worth spending the next couple of hours on: How did a company founded in 1901 to make electric signs—a company that nearly went bankrupt during the 2008 financial crisis after a disastrous foray into fire trucks—transform itself into one of the best-performing industrial stocks of the past decade? The answer involves a 125-year journey through world wars, cold wars, conglomerate booms, near-death experiences, and one of the most underappreciated corporate turnarounds in American industrial history.

The arc of this story bends through four critical inflection points. First, the post-World War II era, when Federal Signal became synonymous with civil defense and embedded itself into America's safety infrastructure. Second, the aggressive diversification campaign of the 1970s through 1990s that built a sprawling conglomerate—and nearly destroyed the company.

Third, the radical transformation that began around 2010 and culminated in a focused, disciplined industrial platform. And fourth, the modern era of strategic acquisitions and infrastructure tailwinds that has propelled Federal Signal to record revenue and margins.

This is a story about boring businesses that generate extraordinary returns. About the power of focus over diversification. About how the best moats are sometimes not network effects or proprietary algorithms, but dealer relationships, installed bases, and the simple fact that cities must clean their sewers.

There is a saying in industrial investing circles: "The sexier the pitch, the worse the returns." Federal Signal is the embodiment of the opposite principle. There is nothing glamorous about sewer cleaning trucks or tornado sirens. You will never see a Federal Signal product in a Super Bowl commercial or trending on social media. But when a tornado warning sounds across Oklahoma City, or a Vactor truck descends into a manhole to clear a blocked sewer main, or an Elgin sweeper quietly removes debris from a school zone at five in the morning, Federal Signal's products are doing what they have done for over a century: keeping American communities running. The business behind that mission deserves a deep look.

II. Founding Era & The Cold War Context (1901–1970s)

Picture Chicago at the turn of the twentieth century: a city rebuilding from its great fire, electrifying at a furious pace, and hungry for anything that harnessed this miraculous new power called electricity. In 1901, three men—brothers John and James Gilchrist, along with electrical engineer John Goehst—pooled ten thousand dollars and founded the Federal Electric Company. Goehst had been working at Commonwealth Edison, and he saw an opportunity: businesses wanted illuminated signs, and the technology to make them was brand new. Federal Electric became one of the first companies in America to manufacture electric signs lit by incandescent lamps.

For the next decade and a half, the company grew steadily on the back of commercial signage. But in 1915, the business took a fateful turn. Federal Electric began manufacturing electrically operated mechanical sirens—devices originally designed for police departments, fire services, and coal mines. It was a modest product line at first, but it planted the seed for everything that would follow.

The company's early decades were turbulent. Around 1930, Commonwealth Edison acquired Federal Electric as part of Samuel Insull's sprawling utility empire. When Insull's empire spectacularly collapsed during the Great Depression—one of the era's biggest financial scandals—Federal Electric was spun back out as an independent company under the name Federal Sign and Signal Corp. The company regained full independence by 1940, just in time for history's next great disruption.

World War II transformed Federal Signal from a regional sign-and-siren maker into a company of national importance. The U.S. government needed air raid warning systems—fast—and Federal Signal had the manufacturing capability to deliver electrically operated sirens at scale. The company supplied warning systems deployed across American cities and military installations, including systems shipped to London during the Blitz. When the bombs were falling, Federal Signal's products were the first line of communication between civil defense authorities and the public.

The war ended, but the fear did not. As the Soviet Union tested its first atomic bomb in 1949 and the Korean War erupted in 1950, the U.S. government launched a massive civil defense buildup. Every American city needed outdoor warning sirens capable of alerting citizens to nuclear attack—and Federal Signal was positioned to supply them. The Cold War created a permanent, federally funded market for outdoor warning systems, and Federal Signal dominated it completely.

The company's most iconic product, the Thunderbolt siren, entered production in 1952. The Thunderbolt was an engineering marvel of its era—a massive electromechanical device that used a supercharged rotating horn driven by a roots blower system to produce an ear-splitting wail that could be heard for miles. For the non-engineer, here is how it worked: imagine a giant mechanical whistle mounted on a pole. Instead of human breath, a powerful electric motor drove a roots-type blower—essentially two figure-eight-shaped rotors spinning inside a housing, pushing huge volumes of low-pressure air. That air flowed through a rotating chopper disc with precisely machined slots. As the disc spun, the air was alternately blocked and released at hundreds of cycles per second, creating a sound wave of tremendous power. The distinctive rising-and-falling wail came from varying the chopper speed. The first Thunderbolt T-1000 models were activated in 1953, and they quickly became the siren of choice for civil defense authorities across the country.

The cultural impact of these sirens cannot be overstated. For generations of Americans—particularly in the Midwest and Great Plains—the monthly "first Wednesday" siren test became a fixture of community life. Children grew up learning that the wailing tone meant tornado, and the steady blast meant nuclear attack. Federal Signal sirens became part of the auditory landscape of American life in a way that few industrial products ever achieve. Even today, surviving Thunderbolt sirens are maintained and operated across tornado-prone states, and dedicated enthusiasts document and preserve them as artifacts of Cold War-era engineering.

By the mid-1970s, Federal Signal supplied approximately seventy percent of the nation's civil defense warning systems—a staggering market share that reflected both the quality of its products and the depth of its government relationships. Siren-related sales generated twenty-nine million dollars, roughly forty percent of total company revenue in 1975. The company had gone public on NASDAQ in 1961, with net income of one million dollars on sales of fifteen million, and transferred its listing to the New York Stock Exchange in 1969 under the ticker FSS.

In 1976, the company formally renamed itself Federal Signal Corporation—dropping "Sign" from the name as the siren and safety businesses increasingly overshadowed the original signage operations. By then, the sign division still generated nearly half of the company's roughly sixty million dollars in revenue, but the strategic direction was clear. Federal Signal's future lay not in illuminating storefronts but in protecting lives. The Cold War had given the company something invaluable: a brand synonymous with public safety, deeply embedded relationships with municipal and federal agencies, and a manufacturing base capable of scaling to meet national security demands.

What investors should note about this era is not just the product history, but the business model that emerged. Federal Signal did not just sell sirens—it built an installed base across thousands of American communities that would require maintenance, upgrades, and eventual replacement for decades to come. That installed base, invisible to most observers, would prove to be one of the company's most durable competitive assets. But before that asset could be fully monetized, Federal Signal would first embark on a twenty-year diversification binge that would nearly destroy everything the founders had built.

III. Diversification Through Acquisition (1970s–2000)

The late 1970s were the golden age of the American industrial conglomerate. The prevailing wisdom held that a well-managed company could apply its operational expertise to virtually any adjacent market, and that diversification itself was a form of risk management. Federal Signal, flush with cash from its dominant siren business and newly empowered by its NYSE listing, bought into this philosophy with gusto.

The man who drove the expansion was Karl Hoenecke, who became president in 1975. Hoenecke's vision was ambitious: transform Federal Signal from a siren company into a broad-based safety and municipal equipment conglomerate. Starting in 1968, the company had already begun acquiring adjacent businesses—Western Industries and Cullen-Friestedt in rail equipment, Aircraft Equipment Company in airport ground support—but under Hoenecke, the pace accelerated dramatically.

The most consequential acquisition of this era came in 1979, when Federal Signal purchased Emergency One, or E-ONE, a five-year-old Florida company that had pioneered the use of aluminum bodies for fire trucks. E-ONE was a genuine innovator—its lightweight aluminum fire trucks were cheaper to build and easier to maintain than traditional steel-bodied competitors, and municipalities loved them. The acquisition seemed brilliant. Federal Signal now had a product that spoke directly to fire departments, a natural extension of a company that already supplied emergency warning systems.

Three years later, in 1982, Federal Signal made another transformative deal, acquiring Elgin Sweeper Company for $11.3 million. Elgin was a leading manufacturer of high-speed street sweeping machines, and the acquisition gave Federal Signal a strong position in municipal vehicle equipment. Over the next decade, the company continued layering on acquisitions: fire alarm systems through Autocall Company, the Ravo Group (a Dutch street-sweeper manufacturer) in 1992, Guzzler Manufacturing (vacuum loaders) in 1993, and Vactor Manufacturing (sewer cleaning systems) in 1994.

By the early 1990s, the strategy appeared to be working spectacularly. The vehicle unit held thirty percent of the U.S. market for both fire engines and street sweepers. E-ONE's fire truck sales had jumped six-fold between 1986 and 1989, and the lightweight aluminum trucks proved so popular that they drove competitor American La-France—a brand dating to 1832 and one of the most storied names in firefighting—into bankruptcy. Record earnings of nearly forty million dollars on revenues of five hundred sixty-five million arrived in 1993. International expansion—fueled by acquisitions in the Netherlands, Canada, Germany, and Spain (the siren manufacturer VAMA in 1993)—quadrupled overseas sales to one hundred twenty million dollars. Annual revenues approached a billion dollars by the late 1990s.

There was a seductive logic to the portfolio. A single Federal Signal salesperson could, in theory, walk into a city hall and offer the public works director sirens for tornado warnings, street sweepers for road maintenance, fire trucks for the department, and vacuum loaders for industrial cleanup. The "one-stop shop" pitch resonated in sales meetings. But theory and practice diverged sharply. Each product category had different manufacturing processes, different supply chains, different competitive dynamics, and different customer decision-makers within the same municipality. The fire chief buying trucks rarely coordinated with the public works manager buying sweepers. The synergies were illusory.

But beneath the top-line growth, cracks were forming. Hoenecke died in 1986, and his successor Joseph Ross did solid work implementing manufacturing improvements, including innovative "work cell" production processes. Yet the sheer breadth of the portfolio was becoming unmanageable. Federal Signal now operated across dozens of product categories—signs, sirens, fire trucks, street sweepers, vacuum trucks, tool bits, airport equipment, parking systems—with little operational synergy between them. Each business had its own manufacturing footprint, supply chain, and customer base. The company was, in the phrase that would later be used to diagnose the problem, "a mile wide and an inch deep."

The late 1990s brought the first warning signs. Integration of international acquisitions proved harder than expected—the Dutch and German businesses had different manufacturing cultures, different labor regulations, and different customer expectations than the American operations. Margins came under pressure as the company spread management attention across too many product lines. The dealer network, while broad, lacked the depth needed to provide world-class service in any single category. A dealer asked to support street sweepers, fire trucks, vacuum loaders, and sirens simultaneously could not develop the deep product expertise that customers demanded.

Federal Signal had built a classic bloated conglomerate—the kind that management consultants love to dissect and private equity firms love to dismantle. The company's stock began to reflect this reality, trading at a conglomerate discount as investors questioned whether the whole was worth less than the sum of its parts.

For investors, the diversification era holds an important lesson. Revenue growth through acquisition can mask deteriorating unit economics. Federal Signal's top line looked impressive through the late 1990s, but the company was not generating returns on capital commensurate with the risks it was taking. The conglomerate discount—where a company's parts are worth more than the whole—was beginning to apply. And the single biggest bet of the diversification era, E-ONE, was about to blow up in spectacular fashion.

IV. The Crisis Years & Failed Turnaround (2000–2008)

The unraveling began slowly and then happened all at once. The dot-com bust of 2000-2001 did not directly affect Federal Signal's products, but it hammered the municipal budgets that funded their purchase. When tax revenues decline, cities defer maintenance and delay equipment purchases—and Federal Signal's order book started thinning.

But the real disaster was E-ONE. The fire truck business that had once been the crown jewel of the diversification strategy was now hemorrhaging money. Quality problems plagued the 2001 through 2007 model year rigs, with electrical issues becoming a persistent and costly headache. Service on the West Coast deteriorated. Municipalities that had once eagerly specified E-ONE trucks began switching to competitors. In its final year on Federal Signal's books, E-ONE lost twenty-five million dollars—a staggering amount for a business unit within a company that was itself struggling to generate profit.

The CEO carousel began spinning—and it would not stop for years. Robert D. Welding, who had been leading the company, resigned in December 2007 amid what the Chicago Tribune described as an "alarming falloff in firetruck sales." The board installed James Goodwin—the former chairman and CEO of UAL Corporation, parent of United Airlines—as interim chief executive. Goodwin was a seasoned corporate hand who had navigated United Airlines through post-9/11 turbulence, but he was a crisis manager, not a long-term operator, and Federal Signal needed both.

In September 2008, the board found its permanent candidate: William H. Osborne, the former president and CEO of Ford Canada Limited. It was a reasonable choice on paper—automotive executive, deep manufacturing background, restructuring experience in a cyclical industry. But Osborne arrived at perhaps the worst possible moment in modern economic history. Lehman Brothers collapsed two weeks after his appointment. The global financial system froze.

The cascade effect on Federal Signal was devastating. Municipal budgets depend on property taxes, sales taxes, and state transfers—all three of which collapsed simultaneously during the Great Recession. Property values plummeted, reducing tax assessments. Consumer spending cratered, slashing sales tax revenue. State governments, facing their own fiscal crises, cut transfers to local municipalities. Cities that had been planning equipment purchases cancelled orders outright. Those that had placed orders pushed delivery dates into an uncertain future. Some municipalities froze all capital spending indefinitely, keeping aging equipment running on a prayer and a maintenance budget that was itself being cut.

The E-ONE debacle was not just a financial loss—it was a reputational one. Fire departments are tight-knit communities. Word travels fast when a manufacturer's equipment fails. The quality issues created a negative feedback loop: fewer orders meant less revenue to invest in quality improvements, which led to more problems, which led to even fewer orders. By the time Federal Signal recognized the business was unsalvageable, the brand damage was deep and the losses were mounting.

The forced divestitures accelerated. The signage division—the business that had originally given the company its name—had already been sold in 2003. Three cutting tool businesses went to Kennametal in 2007 for roughly sixty-seven million dollars. And in 2008, in what can only be described as a fire sale, E-ONE was sold to American Industrial Partners for just twenty million dollars. To put that in context: Federal Signal had paid a premium to acquire E-ONE in 1979 and invested heavily in the business for nearly three decades. The final sale price was less than what some individual fire trucks cost. The acquisition had destroyed hundreds of millions in shareholder value.

Revenue told the grim story in stark, declining numbers. From a peak near $1.12 billion in 2005, sales collapsed to $793 million in 2006—a twenty-nine percent drop driven largely by the E-ONE unraveling—followed by a partial recovery to $934 million in 2007, then $879 million in 2008 and $750 million in 2009.

The stock price cratered alongside the business, falling from the mid-twenties to single digits. Federal Signal traded below book value—a signal from the market that investors believed the company's assets were worth more dead than alive. Activist investors began circling, smelling blood. The company was burning through management credibility with each passing quarter.

Osborne lasted approximately two years before departing. Four CEOs in seven years—each arriving with a new plan, none staying long enough to execute one. In November 2010, the board brought in Dennis J. Martin as the new president and CEO. By then, revenue had hit its nadir: $633 million, barely more than half the 2005 peak. The company had shed more than four hundred million dollars in annual revenue through a combination of divestitures, lost market share, and collapsed demand. The company that had once supplied seventy percent of America's civil defense sirens and held dominant shares in street sweepers and fire trucks was now a diminished, unfocused collection of businesses struggling to survive.

The crisis years revealed something that the boom times had masked: Federal Signal had no coherent strategy. It was not the best at any one thing. Its manufacturing footprint was sprawling and inefficient, spread across roughly forty facilities. Its management attention was diluted across too many product categories.

The company had tried incremental fixes—selling off the worst performers, hiring new CEOs, cutting costs at the margins—and none of it had worked. Each new CEO arrived with a variation of the same playbook: trim around the edges, maintain the existing portfolio, and hope for a market recovery. But the problem was not cyclical—it was structural. Federal Signal did not need a better version of the old strategy. It needed a completely new strategy.

What the board finally realized, as the company fought for survival through the worst financial crisis in seventy years, was that incremental change was not enough. Federal Signal needed a fundamental transformation—a complete rethinking of what the company was, what it should own, and how it should operate. The next decade would prove that transformation possible—but only under leadership that combined deep institutional knowledge with the willingness to make radical decisions. That leader had been quietly rising through the ranks for over fifteen years.

V. The Transformation Begins: From Survival to Strategy (2009–2015)

Jennifer Sherman had joined Federal Signal in 1994 as a corporate attorney. A University of Michigan graduate with dual degrees in finance and law, she had spent her early career litigating commercial disputes, working through bankruptcies, and navigating labor law—the kind of work that gives a person an intimate understanding of how companies fail. Over the next fifteen years at Federal Signal, she rose steadily: deputy general counsel, head of human resources, vice president and general counsel, chief administrative officer, and eventually chief operating officer. She was not a flashy external hire. She was someone who knew where every body was buried.

When Dennis Martin took over as CEO in late 2010, Sherman was already one of the most influential executives in the building. Martin, to his credit, recognized the depth of the problem and began the hard work of rationalization. But it was the partnership between Martin's restructuring instincts and Sherman's operational knowledge that set the transformation in motion.

The diagnosis was blunt: Federal Signal was trying to be everything to everyone and succeeding at nothing. The company operated across too many product categories, in too many facilities, with too little focus. The phrase that would come to define the turnaround was deceptively simple: "a mile wide and an inch deep." The prescription was equally simple to articulate and brutally difficult to execute: cut everything that was not core, double down on what was, and operate what remained with world-class discipline.

The divestitures were painful but necessary. In 2012, Federal Signal sold its Federal Signal Technologies division—the toll collection and parking systems business—to 3M for $110 million. It was a strong price for a business that, while profitable, had nothing to do with the company's core safety and environmental equipment franchise. The cash infusion gave Federal Signal breathing room and firepower. In 2016, the company sold Bronto Skylift, its aerial platforms business, to Japan's Morita Holdings for approximately eighty million euros. Each divestiture narrowed the portfolio and sharpened the focus.

On the operational side, the transformation was driven by relentless application of lean manufacturing principles and, later, what management called the "80/20" approach. The concept is straightforward: in most businesses, roughly eighty percent of profits come from twenty percent of products and customers. The 80/20 playbook meant identifying the highest-value products and customers, simplifying the product line to serve them, and eliminating the complexity that was destroying margins. The results were remarkable. At Ox Bodies, the dump truck body business, management implemented an astonishing ninety percent reduction in standard dump body SKUs—cutting the product catalog to its most profitable configurations. This single initiative expanded EBITDA margins by more than eight hundred basis points over two years while simultaneously growing market share. Fewer products, better margins, happier customers. It was a textbook demonstration of how focus creates value.

The balance sheet repair was equally critical. Working capital improvements freed up cash that had been trapped in excess inventory and slow-collecting receivables. Inventory turns improved as the simplified product lines required fewer raw materials and finished goods. The company consolidated manufacturing facilities, shutting down redundant plants and concentrating production in focused centers of excellence. The bloated corporate overhead that had accumulated during the conglomerate era was cut. Every layer of unnecessary management, every duplicative function, every legacy process that added cost without adding value was scrutinized and, where possible, eliminated.

The cultural transformation was perhaps the hardest part—and the most important. The old Federal Signal had the organizational culture of a sleepy conglomerate: siloed business units, limited accountability, and a bias toward preserving the status quo. The new culture Sherman and her team built emphasized ownership, speed, and results. Business unit leaders were given clear performance targets tied to margins and cash flow, not just revenue. The days of hiding mediocre performance inside a sprawling conglomerate were over.

By 2015, the results were becoming visible. Margins were expanding, cash flow was turning solidly positive, and the stock price had begun recovering from its crisis-era lows. Revenue stood at $768 million—still well below the 2005 peak, but the quality of those revenues was dramatically higher. The company was earning more on less, converting more cash from each dollar of sales, and building a platform for sustainable growth rather than unsustainable acquisitive expansion.

When Martin departed and Jennifer Sherman assumed the role of president and CEO on January 1, 2016, it was the culmination of a deliberate process. She had been the architect of much of the operational transformation, and her elevation represented continuity rather than disruption. The board was not making a bet on an outsider with a new vision—it was formalizing the leadership of someone who had already been driving the strategy. Sherman became one of the few female CEOs in the American industrial sector, a distinction she earned not through corporate governance trends but through more than two decades of execution inside a company she had helped rescue from the brink.

Why did this transformation succeed when the previous turnaround attempts had failed? Three factors stand out. First, the commitment was total. Previous CEOs had trimmed at the edges while preserving the conglomerate structure. The Martin-Sherman approach was willing to divest entire segments—selling the toll-collection business to 3M, exiting the aerial platforms business—even when those businesses were profitable. The willingness to sell good businesses that did not fit the strategic focus was the clearest signal that this transformation was different.

Second, the leadership was internal. Sherman had spent two decades building relationships, understanding the product portfolio, and earning the trust of the organization. When she pushed for painful changes—facility closures, product line eliminations, headcount reductions—she had the credibility to bring people along. An outsider making the same demands would have faced far more resistance.

Third, the execution was disciplined and sustained. The transformation was not a one-year cost-cutting exercise followed by a return to business as usual. It was a multi-year, systematic rebuilding of operations, culture, and strategy that continued through changing market conditions.

The company entered this period as a sprawling, unfocused conglomerate with dozens of product lines and no clear competitive advantage. It emerged as a focused industrial platform built around two core segments with defensible market positions, expanding margins, and a management team that had proved it could execute under extreme pressure. That platform was about to be weaponized.

VI. The Strategic Reset: Two Segment Focus (2014–2017)

Walk into the public works yard of virtually any mid-sized American city and you will see the two sides of Federal Signal's business in action. In one bay sits a massive Vactor combination sewer cleaner—a truck-mounted system that can blast high-pressure water into clogged sewer lines while simultaneously vacuuming out the debris. In the parking lot outside, an Elgin street sweeper makes its morning rounds. In the dispatch office, a Federal Signal outdoor warning siren control panel sits ready to activate the citywide tornado warning system. Three products, one company, one customer relationship.

Under Sherman's leadership, Federal Signal crystallized its identity around two core segments: the Environmental Solutions Group and the Safety and Security Systems Group. This was not just a financial reporting change—it was a declaration of strategic intent.

The Environmental Solutions Group, or ESG, became the heart of the company. This segment housed some of the most dominant brands in American municipal equipment. Vactor Manufacturing, acquired in 1994, had become the industry standard for sewer cleaning trucks. For those unfamiliar with the category, a combination sewer cleaner is essentially a heavy-duty truck outfitted with two systems: a high-pressure water jet that blasts blockages and a powerful vacuum that sucks up the debris. It is the essential maintenance tool for the underground sewer infrastructure that serves every American city, and "Vactoring" had become an industry verb—the way "Xeroxing" once described photocopying. That kind of brand equity does not show up on a balance sheet, but it is worth a fortune.

Elgin Sweeper, acquired back in 1982, held a dominant position in North American street sweeping. The Elgin product line includes three fundamentally different sweeping technologies—mechanical broom sweepers that physically push debris, vacuum sweepers that suck it up, and regenerative air sweepers that use a closed-loop air system to blast debris loose and capture it simultaneously. Each technology serves different applications, and Elgin offers all three, giving municipalities a single-brand solution for diverse sweeping needs.

Guzzler manufactured industrial vacuum trucks for heavy-duty applications—think of them as giant shop vacuums on wheels, capable of ingesting solids, liquids, and sludge from industrial sites, refineries, and construction projects. TRUVAC, a newer brand, produced hydro-excavation equipment—trucks that use pressurized water and vacuum to safely dig around buried utility lines without risking damage. Hydro-excavation, sometimes called "soft digging" or "potholing," has become increasingly important as cities have learned the hard way that backhoe accidents near buried gas lines or fiber optic cables can be catastrophically expensive. TRUVAC's equipment provides a safer, more precise alternative, and the market for it grows every time a city invests in new underground infrastructure.

Each of these businesses served the same fundamental customer—municipal and utility infrastructure maintenance departments—and each benefited from the same macroeconomic tailwind: America's aging infrastructure requires constant maintenance, and federal and state regulations increasingly mandate cleaner, more environmentally responsible methods.

The Safety and Security Systems Group, while smaller in revenue terms, housed the legacy siren business alongside a growing portfolio of first responder vehicle equipment. By 2024, this segment generated approximately $304 million in revenue—roughly sixteen percent of the total—but contributed outsized margin with adjusted EBITDA exceeding twenty-one percent.

Federal Signal's outdoor warning sirens remained the industry leader, but the technology was being modernized for the twenty-first century. The old Thunderbolt-era electromechanical sirens were being replaced or supplemented by digitally controlled electronic systems that could produce multiple alert tones, be activated remotely via wireless networks, and integrate into broader mass notification platforms. Digital control systems replaced manual activation methods, allowing emergency managers to trigger sirens from a computer screen or smartphone rather than flipping physical switches. New electronic sirens offered broader frequency ranges and could be integrated into campus alerting and mass notification systems used by universities, military bases, and industrial facilities.

The emergency vehicle lighting and equipment business—products like LED light bars, electronic sirens, speakers, and specialized lighting for police, fire, and EMS vehicles—provided a higher-volume, more diversified revenue stream within the safety umbrella. This business benefited from the same dynamics as the environmental segment: an installed base of vehicles requiring periodic equipment upgrades, a dealer network providing local service, and switching costs created by fleet standardization.

The critical strategic insight that emerged during this period was the power of aftermarket revenue. When Federal Signal sold a Vactor sewer cleaner, the initial equipment sale was significant—these trucks can cost several hundred thousand dollars each. But the real value came afterward. Each truck in the field generated years of demand for replacement parts, consumables, and service. The aftermarket business carried significantly higher margins than new equipment sales and was far less cyclical. Municipal budgets might defer a new truck purchase during a downturn, but they could not stop maintaining the trucks already in their fleet. Sewers still need cleaning during recessions.

Sherman and her team began deliberately shifting the revenue mix toward aftermarket and service. This was not just a financial optimization—it was a fundamental strategic reorientation. In the old Federal Signal, success was measured by how many new trucks rolled off the assembly line. In the new Federal Signal, success was measured by how much revenue each truck in the field generated over its lifetime. The distinction matters enormously for business quality. New equipment sales are lumpy, cyclical, and competitive. Aftermarket revenue is steady, high-margin, and sticky.

The 2016 acquisition of Joe Johnson Equipment, a leading Canadian dealer and distributor of infrastructure maintenance equipment, exemplified this approach. Joe Johnson was not a manufacturer—it was the company that sold and serviced Federal Signal products across Canada. By owning a key distributor, Federal Signal captured margin that had previously accrued to third parties, deepened its customer relationships, and gained direct visibility into aftermarket demand patterns. It was a vertical integration move that improved the economics of the entire Canadian business, and it provided a template for future distribution acquisitions.

Capital allocation discipline became a hallmark of the new Federal Signal. Acquisitions were evaluated against high return-on-invested-capital thresholds. Management was explicit that it would buy market leaders in attractive niches—not broken businesses that needed fixing. This was the opposite of the old conglomerate playbook, where Federal Signal had acquired dozens of businesses across unrelated categories with wildly varying quality. The new approach was surgical: identify adjacencies within the two core segments, find the best operators in those niches, buy them at reasonable prices, and integrate them using a proven operational playbook.

The stock market began to notice. Federal Signal shares, which had languished below ten dollars during the crisis years, began a multi-year climb as the transformation took hold. Revenue in Sherman's first full year as CEO was $708 million—a temporary dip reflecting the Bronto Skylift divestiture—but the underlying business quality was improving with every quarter.

The two-segment structure also brought clarity to capital allocation. Instead of spreading investment dollars across a dozen unrelated businesses, management could make concentrated bets in markets where Federal Signal had genuine competitive advantages. R&D spending could be focused on improving sewer cleaning efficiency or developing next-generation warning systems rather than being diluted across categories where the company was a marginal player. Dealer support programs could be tailored to the specific needs of environmental equipment customers. Marketing spend could target the infrastructure maintenance community with a coherent message rather than scattering across unrelated audiences.

For investors who were paying attention during this period, the signals were clear: Federal Signal was systematically improving the quality of its business while the market was still pricing it like the troubled conglomerate of old. The gap between business reality and market perception was wide—and would take years to close fully. The stage was set for the next phase: going on offense.

VII. The Acquisition Machine & Market Leadership (2017–2020)

In 2017, Federal Signal made its largest acquisition in over a decade, purchasing Truck Bodies and Equipment International, or TBEI. The deal brought six dump body and trailer brands under the Federal Signal umbrella: Crysteel, Duraclass, Rugby Manufacturing, Ox Bodies, Travis, and J-Craft. TBEI was not a turnaround project. It was a profitable, well-run collection of brands in a fragmented market, and Federal Signal intended to make it even better.

The TBEI acquisition marked a strategic pivot from defense to offense. For the previous seven years, the company had been trimming, focusing, and optimizing. Now, with a clean balance sheet, strong cash generation, and a proven operational playbook, Federal Signal began acting less like a cautious turnaround story and more like a disciplined private equity buyer with permanent capital. The key difference between Federal Signal and actual private equity, of course, was the time horizon. PE funds typically need to exit within five to seven years. Federal Signal could buy a business and hold it forever, compounding improvements over decades rather than rushing to flip. This permanent capital advantage meant the company could invest in long-term capabilities—dealer development, product improvement, customer relationships—that a PE-backed competitor might sacrifice for short-term returns.

The integration playbook that emerged was rigorous and repeatable. Every acquisition went through a structured onboarding process: map the product portfolio against the 80/20 framework, identify the highest-margin products and customers, rationalize the SKU count, apply lean manufacturing principles to the shop floor, and plug the new business into Federal Signal's dealer network and parts infrastructure. The playbook was not secret or proprietary in any intellectual property sense—any competent industrial operator could describe similar principles. The power lay in the consistent execution, the institutional knowledge of what works and what does not, and the willingness to make difficult decisions quickly.

The logic behind each subsequent deal followed a consistent pattern. In July 2019, Federal Signal acquired Mark Rite Lines Equipment, or MRL, a manufacturer of pavement marking equipment. Road striping might sound mundane, but consider the customer overlap: the same municipal public works departments buying street sweepers and sewer cleaners also need to paint lane markings. MRL gave Federal Signal another product to sell through existing relationships and dealer channels. Cross-selling into an installed customer base is one of the lowest-risk growth strategies in industrial markets.

The acquisition of Joe Johnson Equipment in 2016 had given Federal Signal direct distribution in Canada. MRL added a new product category. TBEI added dump bodies. Each deal was a tile in a mosaic that was becoming visible: Federal Signal was building a comprehensive platform for municipal and infrastructure maintenance equipment, with each new addition reinforcing the value of the whole.

The operational improvements that had been honed during the turnaround years became a genuine competitive advantage in M&A. When Federal Signal acquired a business, it brought the 80/20 playbook, lean manufacturing expertise, and a focused approach to product line management. The Ox Bodies SKU rationalization—the ninety percent reduction that expanded margins by eight hundred basis points—became a template that could be applied to newly acquired businesses. This was process power in action: the ability to consistently improve the operations of acquired businesses was itself a form of competitive moat, because it meant Federal Signal could pay fair prices for acquisitions and still generate strong returns through operational improvement.

Revenue surpassed one billion dollars in 2018 for the first time since the crisis years—a milestone that carried enormous symbolic weight. It had taken Federal Signal more than a decade to claw back to the revenue level it had achieved in 2005, but the 2018 billion-dollar company was a fundamentally different and better business than the 2005 version. Margins were higher, the portfolio was more focused, aftermarket revenue was a larger share of the mix, and the management team had been battle-tested through the worst financial crisis in generations. To put it in investing terms: the old Federal Signal generated a billion dollars of mediocre revenue across dozens of unrelated product lines; the new Federal Signal generated a billion dollars of high-quality revenue concentrated in defensible niche markets with strong aftermarket annuities. Same top line, entirely different business quality.

When COVID-19 struck in early 2020, it tested the resilience of the transformed business model in real time. Lockdowns shuttered businesses, unemployment spiked, and economic uncertainty reached levels not seen since the Great Recession. For a company dependent on municipal spending, this should have been devastating. Tax revenues—particularly sales tax and income tax—fell sharply in many jurisdictions.

Instead, Federal Signal demonstrated the stability that Sherman and her team had built. Municipal maintenance spending proved relatively resilient for a simple reason: infrastructure does not stop deteriorating during a pandemic. Sewers still clog. Streets still accumulate debris. Storm drains still need clearing. Federal spending support through the CARES Act and subsequent relief packages helped shore up municipal budgets, and many infrastructure projects continued as "essential work."

The company navigated supply chain disruptions—particularly chassis shortages that affected the entire specialty vehicle industry—by leveraging its scale and supplier relationships. It implemented safety protocols across its manufacturing plants that kept production running. And it emerged from 2020 with its strategic momentum largely intact, its backlog healthy, and its transformation thesis validated. Revenue dipped modestly but recovered quickly, proving that essential infrastructure maintenance equipment is far less cyclical than investors typically assume for industrial companies.

By the end of 2020, the moat that Federal Signal had been quietly building for a decade was becoming formidable. A dense dealer network across North America provided local sales and service capabilities that new entrants could not replicate quickly. An installed base of tens of thousands of pieces of equipment in the field generated predictable aftermarket demand. Deep relationships with municipal procurement departments—relationships built over years of reliable service—created meaningful switching costs. And a proven acquisition integration playbook gave the company a repeatable engine for deploying capital at attractive returns. Federal Signal was no longer a turnaround story. It was becoming a compounder.

VIII. The Modern Era: Technology, Infrastructure Tailwinds & Scaling Up (2020–Present)

On November 15, 2021, President Biden signed the Infrastructure Investment and Jobs Act into law. For most Americans, the IIJA meant headlines about bridges and broadband. For Federal Signal, it meant something far more immediate and tangible: the single largest federal investment in water infrastructure in American history. Fifty-five billion dollars flowed to the EPA for drinking water and wastewater systems, with annual appropriations through the Drinking Water State Revolving Fund jumping to approximately six billion dollars per year—nearly six times the pre-IIJA levels. That money flows through state revolving funds to local governments, which use it to repair, replace, and expand sewer systems, water mains, and treatment facilities. Every dollar of that spending creates demand for the equipment Federal Signal manufactures—Vactor sewer cleaners, TRUVAC hydro-excavators, Elgin sweepers for post-construction cleanup.

The IIJA did not create Federal Signal's growth trajectory—that was already well established—but it added rocket fuel to an engine that was already running. The company entered a period of unprecedented acceleration.

Revenue climbed from $1.43 billion in 2022 to $1.72 billion in 2023 to $1.86 billion in 2024, with each year setting new records. The growth was driven by a combination of organic demand, price realization, and increasingly ambitious acquisitions.

The acquisition pace intensified. In February 2021, Federal Signal acquired OSW Equipment and Repair, a manufacturer of dump truck bodies and custom truck equipment based in Snohomish, Washington, expanding the geographic footprint of the dump body business to the Pacific Northwest. In February 2023, the company signed a deal for Trackless Vehicles, a Canadian manufacturer of specialty multi-purpose municipal vehicles, for approximately fifty-four million Canadian dollars. Trackless made compact, versatile machines that could be outfitted with different attachments for sidewalk plowing, mowing, sweeping, and other municipal tasks—a perfect fit for smaller municipalities that could not justify single-purpose equipment.

In October 2024, Federal Signal acquired Standard Equipment Company, a leading distributor of Vactor, Elgin, and TRUVAC products in Illinois and Indiana, for approximately thirty-nine million dollars plus an earn-out. This was the same playbook as the Joe Johnson Equipment acquisition years earlier: bringing key distribution in-house to capture margin, deepen customer relationships, and gain better visibility into end-market demand.

Then came the two deals that signaled Federal Signal's growing ambition. In February 2025, the company closed on Hog Technologies, a manufacturer of truck-mounted road-marking, line-removal, and waterblasting equipment, for seventy-eight million dollars plus an earn-out. Hog brought approximately sixty-five million in annual revenue with a thirty-five percent aftermarket mix—exactly the kind of business Federal Signal excels at optimizing. And in November 2025, Federal Signal completed its largest acquisition in company history: New Way Trucks, a fast-growing manufacturer of refuse collection vehicles, for three hundred ninety-six million dollars plus facility costs and an earn-out. New Way had a backlog exceeding one hundred million dollars, more than seven hundred fifty employees, and a growing reputation as one of the most innovative refuse truck makers in America. Management projected the deal would add forty to forty-five cents of earnings per share accretion by 2028.

The New Way acquisition was significant not just for its size but for what it represented strategically. Refuse collection is a massive, fragmented market adjacent to Federal Signal's core municipal equipment franchise. The same city that buys Elgin sweepers, Vactor sewer cleaners, and Ox Bodies dump trucks also needs refuse collection vehicles. The competitive landscape in refuse trucks includes heavyweights like Heil Environmental (part of Dover Corporation), McNeilus (part of Oshkosh Corporation), and Labrie Enviroquip—but the market remains fragmented enough that a fast-growing, innovative manufacturer like New Way could carve out a meaningful and expanding niche. New Way had been gaining share through product innovation—lighter, more efficient truck bodies that reduced fuel consumption and increased payload capacity—and its backlog of over a hundred million dollars testified to strong customer demand.

The deal added an entirely new product vertical that could be sold through existing relationships and distribution channels, extending the platform's reach without straying from the core municipal infrastructure thesis. For Federal Signal, refuse collection represented one of the largest untapped adjacencies in its target market. Every municipality that sweeps streets also collects garbage. The cross-selling potential was enormous.

Technology began playing an increasingly visible role in Federal Signal's strategy during this period. IoT-enabled warning systems allowed remote monitoring and activation of outdoor siren networks—a city emergency manager could now test, activate, and diagnose problems across an entire siren network from a single dashboard, rather than sending technicians to check each unit individually. Telematics systems on street sweepers and vacuum trucks provided fleet managers with real-time data on equipment location, utilization, operating hours, and maintenance needs.

These connected product capabilities opened the door to subscription and recurring revenue models that had never previously existed in Federal Signal's business. Remote monitoring services, predictive maintenance alerts that notify operators when components are nearing end-of-life, and fleet management software that optimizes routing and scheduling all represent opportunities to generate ongoing revenue from the installed base. While still nascent, these digital revenue streams have the potential to transform the business model over time—shifting a portion of revenue from one-time equipment sales to recurring software-like subscriptions that deepen customer relationships and increase switching costs.

Jennifer Sherman remained at the helm throughout this period, continuing as president and CEO. Ian Hudson, who joined Federal Signal in 2013 and was promoted to senior vice president and chief financial officer in 2017, served as a critical partner in executing the financial strategy and managing the increasingly complex acquisition pipeline. The stability of the leadership team—Sherman and Hudson have now worked together for over a decade—stands in stark contrast to the CEO carousel of the crisis years and has been a meaningful contributor to consistent execution.

The 2025 fiscal year capped the transformation era with exclamation-point results. Revenue reached $2.18 billion, up seventeen percent year-over-year and more than triple the 2010 nadir of $633 million. Adjusted EBITDA grew twenty-five percent to $439 million, with margins expanding to 20.1 percent—a level that would have seemed fantasy during the crisis years. Federal Signal had crossed the twenty-percent EBITDA margin threshold that distinguishes good industrial businesses from great ones. Fourth-quarter adjusted earnings per share of $1.16 beat analyst estimates, and the company raised its full-year outlook following the New Way acquisition.

Sherman was named EY Entrepreneur of the Year for the Midwest in 2024—recognition of a transformation that took the better part of two decades but delivered extraordinary results. The stock price reflected this journey, reaching an all-time high of $132.89 in October 2025. From crisis-era lows in the single digits to north of a hundred dollars per share, Federal Signal's stock has been one of the great industrial compounding stories of the past fifteen years.

IX. Business Model Deep Dive & Competitive Positioning

To understand why Federal Signal generates the returns it does, it helps to think about three distinct revenue engines operating within the same corporate body.

The first engine is new equipment sales. When a city needs a new street sweeper or sewer cleaner, it goes through a formal procurement process—typically involving detailed specifications, competitive bidding, and budget approval cycles that can take months or even years. This creates lumpiness in orders, and new equipment sales are modestly cyclical, dipping when municipal budgets tighten and surging when federal infrastructure spending arrives. But there is a floor to this cyclicality: cities cannot indefinitely defer equipment replacement. Sewers must be cleaned. Streets must be swept. Public safety warnings must function. This is not discretionary spending—it is essential infrastructure maintenance.

The second engine, and increasingly the most important one, is parts and service. Think of it as the "razor and blade" model applied to heavy municipal equipment. A Vactor combination sewer cleaner might cost several hundred thousand dollars as a new unit, but over its operational life of ten to fifteen years, it will consume thousands of dollars annually in replacement parts—hoses, nozzles, filters, hydraulic components, wear items—plus regular service and maintenance. This aftermarket revenue carries significantly higher margins than new equipment sales, is far less cyclical (maintenance cannot be deferred the way new purchases can), and grows automatically as the installed base expands. Every new Vactor truck Federal Signal sells is a future annuity stream of parts revenue. Management has deliberately increased the aftermarket share of total revenue, and acquisitions like Standard Equipment and Joe Johnson Equipment were specifically targeted at capturing more of this high-margin stream.

The third engine is rentals and fleet management, a smaller but growing segment. Not every municipality needs to own a Guzzler industrial vacuum truck or a TRUVAC hydro-excavator. Some of these machines are used only a few times per month, making ownership economically inefficient. For these customers, Federal Signal offers rental programs that provide access to specialized equipment without the capital outlay of ownership. The customer pays a recurring rental fee, Federal Signal handles maintenance and repairs, and when the rental period ends, the customer either renews or returns the equipment.

Rental relationships are inherently sticky—once a city has integrated rental equipment into its maintenance workflows and its operators have trained on Federal Signal machines, switching providers creates operational disruption that most public works directors prefer to avoid. The rental model also functions as a customer acquisition channel: municipalities that start by renting often upgrade to purchased equipment as their needs grow and their budgets allow.

What makes Federal Signal's customer base distinctive is the nature of municipal procurement. City public works departments are not impulse buyers. Purchasing decisions involve formal bid specifications, committee approvals, and budget cycles that align with fiscal years. This process creates high barriers to entry for new competitors, because getting "spec'd in"—having your equipment approved and included in a municipality's bid specifications—requires years of demonstrated reliability, service capability, and technical compliance. Once a city has standardized on Vactor sewer cleaners, switching to a competitor means retraining operators, restocking a different parts inventory, and risking service disruptions during the transition. The switching costs are not trivial.

The dealer network amplifies these advantages in ways that are difficult to appreciate from the outside. Federal Signal products are sold and serviced through a network of authorized dealers across North America—local businesses with deep relationships in their communities. A dealer in Omaha knows the public works director by first name, understands the city's specific equipment needs, and can have a service technician on-site within hours if a truck breaks down. These dealers are not just sales channels—they are the eyes and ears of the organization, providing real-time intelligence on competitive dynamics, customer needs, and market shifts.

The dealer model creates a virtuous cycle. More products in the Federal Signal portfolio mean more revenue opportunities for each dealer, which makes the dealership more profitable, which attracts better talent and investment, which improves service quality, which drives customer loyalty, which generates more sales. The acquisition strategy feeds directly into this flywheel: when Federal Signal added dump bodies through TBEI, or pavement marking equipment through MRL, or refuse collection through New Way, each existing dealer gained new products to offer their municipal customers. This local presence is virtually impossible for a new entrant to replicate without decades of relationship-building and massive capital investment.

Federal Signal's manufacturing footprint provides another structural advantage. The company's products are manufactured in the United States, which matters enormously given Buy America requirements that mandate the use of domestically produced equipment for federally funded infrastructure projects. As IIJA dollars flow into state and local infrastructure budgets, companies with American manufacturing have a built-in advantage over foreign competitors.

The innovation model is worth understanding for what it is—and what it is not. Federal Signal does not pursue disruptive innovation in the Silicon Valley sense. There is no moonshot R&D lab working on autonomous street sweepers or AI-powered sewer robots. Instead, the company practices iterative improvement: making existing products more efficient, more durable, easier to maintain, and more compliant with evolving environmental regulations.

This approach aligns perfectly with the customer base. Municipal equipment buyers want proven, reliable technology—not bleeding-edge experiments. They want a street sweeper that works every day, not one that might revolutionize the category but also might break down on Main Street. They want a sewer cleaner that their operators can maintain using familiar tools and procedures, not one that requires a software engineer to diagnose. In this context, Federal Signal's innovation strategy—incremental improvements to proven platforms, adding digital capabilities gradually, and investing in manufacturing process efficiency—is not a weakness. It is a competitive strength that matches the needs and expectations of its customers.

The result is a business model that is not "sexy" by technology standards but is extraordinarily attractive by financial standards: essential products with limited competition, high switching costs, predictable cash flows, regulatory tailwinds, and a growing aftermarket annuity stream. Sometimes the best businesses are the ones that nobody talks about at cocktail parties.

X. Competitive Analysis: Porter's Five Forces & Hamilton's Seven Powers

Competitive Rivalry: The Fragmented Oligopoly

The markets Federal Signal operates in are unusual in competitive structure. Each product category—street sweepers, sewer cleaners, dump bodies, outdoor warning systems—is served by a relatively small number of meaningful competitors, but the competitors are different in each category. In street sweeping, Federal Signal's Elgin brand competes with TYMCO (the Texas-based inventor of regenerative air technology), Schwarze Industries, and European players like Bucher Municipal. In sewer cleaning and vacuum trucks, Vactor competes with Vacall (a subsidiary of Alamo Group), Vac-Con, and Sewer Equipment Co. In outdoor warning sirens, Federal Signal holds the dominant position with limited domestic competition.

This structure—a fragmented market with few large players per niche—is favorable for incumbents. Competition exists, but it is moderated by specification requirements, service needs, and the high cost of maintaining dealer networks. Price wars are rare because municipal buyers are primarily concerned with reliability, service availability, and total cost of ownership rather than the lowest sticker price. A public works director does not want to explain to the city council why the new street sweeper broke down on Main Street because the department bought the cheapest option. Reliability and service support matter more than price in this market, which creates a natural floor on margins for established players with strong service networks.

In the refuse collection segment, which Federal Signal entered through the New Way acquisition, the competitive field is broader but similarly fragmented. Heil Environmental (Dover Corporation), McNeilus (Oshkosh Corporation), and Labrie Enviroquip are the major players, along with several regional manufacturers. New Way competes primarily through product innovation and manufacturing quality rather than price, which aligns well with Federal Signal's broader market positioning.

Barriers to Entry: Higher Than They Appear

A casual observer might assume that manufacturing municipal equipment is not particularly difficult. After all, a street sweeper is fundamentally a truck with brushes and a vacuum. But the barriers to entry in these markets are substantial and multifaceted. Building a manufacturing operation capable of producing heavy-duty specialty vehicles requires significant capital investment. Establishing a dealer network with trained technicians, parts inventories, and service facilities across dozens of states requires years of effort and relationship-building. Gaining municipal certifications and getting products approved for inclusion in bid specifications requires demonstrated reliability over extended periods. And Buy America requirements effectively exclude foreign manufacturers from a large portion of the market funded by federal infrastructure dollars.

Supplier and Buyer Dynamics

Federal Signal's supply base is generally diversified—the company purchases chassis, hydraulic components, steel, and other inputs from multiple vendors. The post-pandemic supply chain disruptions revealed some vulnerability in chassis availability, but the company demonstrated pricing power that allowed it to pass through cost increases. On the buyer side, municipal customers operate through formal bidding processes, which creates price transparency. However, the limited number of qualified suppliers for specialized equipment, combined with the high cost of switching, gives Federal Signal meaningful pricing leverage, particularly in aftermarket parts where alternatives are scarce.

Substitution Risk: Low and Getting Lower

The threat of substitutes for Federal Signal's core products is modest—and this is one of the most underappreciated aspects of the business. Consider the fundamental question: what is the alternative to cleaning a city's sewers? There is none. The underground infrastructure must be maintained, and it requires specialized equipment to do so. The same logic applies to street sweeping (mandated by environmental regulations and basic civic function), refuse collection (garbage must be collected), and emergency warning systems (communities must be warned of severe weather).

Technology evolution—electric powertrains, autonomous operation, connected fleet management—represents more of an opportunity than a threat for an incumbent like Federal Signal. When electric street sweepers eventually become mainstream, it will be existing manufacturers who electrify their platforms, not Tesla or some Silicon Valley startup. The customer relationships, dealer networks, and application expertise required to succeed in these markets take decades to build. If anything, climate change and increasingly stringent environmental regulations are expanding the addressable market by requiring more frequent infrastructure maintenance and more sophisticated environmental compliance. More storms mean more cleanup. Tighter water quality standards mean more sewer maintenance. Growing cities mean more streets to sweep and more garbage to collect.

Hamilton's Seven Powers: Where the Moat Really Lives

Through the lens of Hamilton Helmer's Seven Powers framework, Federal Signal's competitive position becomes clearer. The company does not possess one overwhelming power source—it is not a platform business with winner-take-all network effects. Instead, it compounds multiple moderate-to-strong power sources that reinforce each other.

Scale Economies operate across three dimensions. In manufacturing, Federal Signal spreads fixed costs—factory overhead, engineering, quality systems, regulatory compliance—over larger production runs of specialized equipment than most competitors can achieve. In the dealer network, density of service locations creates better customer coverage; a dealer can justify carrying more inventory and employing more specialized technicians when supported by a broader product line. And in aftermarket, managing a vast parts catalog with tens of thousands of SKUs is dramatically more efficient at scale—the fixed costs of warehousing, logistics, and catalog management are amortized over a much larger revenue base.

These scale advantages are meaningful but not insurmountable for a well-capitalized competitor in any single product category. Vacall, backed by Alamo Group's resources, can compete effectively in sewer cleaners. TYMCO competes vigorously in street sweepers. The key is that Federal Signal has scale advantages across multiple categories simultaneously, and no competitor matches that breadth.

Switching Costs are among the strongest power sources. Fleet standardization means that a municipality running Vactor sewer cleaners has invested in operator training, parts inventory, maintenance procedures, and service contracts built around that platform. Switching to a competitor's equipment means starting over across all of these dimensions. The switching costs are not contractual—there are no long-term lock-in agreements—but they are deeply operational, which makes them even more durable.

Process Power has become increasingly strong since the transformation—and this may be the most important power source for Federal Signal's future. Federal Signal's ability to integrate acquisitions, apply the 80/20 framework to rationalize product lines, and systematically improve margins across diverse business units represents genuine organizational capability that competitors would struggle to replicate. It took more than a decade of painful trial and error, institutional learning, and cultural change to build this capability. A competitor cannot simply read about the 80/20 approach and replicate it—the execution know-how is embedded in the organization's people, processes, and culture. This is the power that enables the acquisition strategy to generate returns, and it gets stronger with each successful integration.

Branding operates at the niche level with surprising strength. "Vactor" is effectively a generic term for combination sewer cleaners among municipal public works professionals. "Federal Signal" is synonymous with outdoor warning sirens. Elgin defines street sweeping. In safety-critical and infrastructure-critical applications, brand trust takes years to build and is extremely difficult to dislodge.

Cornered Resource, while not as dramatic as in technology businesses, exists in meaningful form. Federal Signal's installed base of outdoor warning sirens across thousands of American communities represents a captive customer base for upgrades, maintenance, and replacement. These siren networks were built over decades, and replacing them with a competitor's technology would require municipalities to rip out and replace entire control systems, wiring, and mounting infrastructure. The dealer relationships, built through generations of local service, are similarly difficult for competitors to replicate. A new entrant cannot walk into Topeka and immediately match the forty-year relationship that a Federal Signal dealer has cultivated with the city's emergency management office.

The overall competitive picture is a portfolio of modest but durable advantages that compound over time and across product categories. No single competitor can match Federal Signal's breadth of municipal infrastructure equipment, depth of dealer coverage, and installed base of aftermarket-generating equipment. The moat is not a single wall but a layered defense system. Each advantage alone might be vulnerable to a determined, well-capitalized competitor. But attacking all of them simultaneously—across multiple product categories, in multiple geographies, through both OEM and aftermarket channels—would require an investment of billions of dollars and decades of effort. That is a powerful deterrent.

XI. Playbook: Lessons for Operators & Investors

The Turnaround Playbook

Federal Signal's transformation offers a case study in industrial turnarounds that deserves to sit alongside the classics. The first lesson is deceptively simple but brutally hard to execute: focus beats diversification. The old Federal Signal tried to be in signs, sirens, fire trucks, tool bits, airport equipment, parking systems, and a dozen other categories. The new Federal Signal operates in two segments with clear strategic logic. Every divestiture was painful—selling businesses means admitting past mistakes and accepting losses—but each one freed up management attention, capital, and organizational energy for the businesses that actually mattered.

The second lesson is that operational excellence compounds. The 80/20 framework and lean manufacturing initiatives did not just produce one-time cost savings—they created a repeatable capability that became more powerful with each application. When Federal Signal acquires a new business, it arrives with a proven operational improvement toolkit refined across dozens of implementations. This means the company can generate returns on acquisitions even when paying market-fair prices, because it can reliably improve the operations of the businesses it buys. That is a genuine competitive advantage in M&A. Consider the analogy to Danaher's famous Business System or Berkshire Hathaway's decentralized operating model—Federal Signal has built a smaller-scale version of the same capability, tailored to municipal and infrastructure equipment markets.

The third lesson is about leadership continuity and the value of internal development. Sherman spent twenty-two years at Federal Signal before becoming CEO. She knew every product line, every factory floor, every key customer relationship. When she took the helm, there was no learning curve—she had already been driving the transformation for years. Compare that to the crisis-era CEO carousel, where outside hires arrived with credentials but without institutional knowledge, only to depart before their strategies could take hold. The Federal Signal story makes a compelling case for developing leaders internally and promoting from within—particularly in complex industrial businesses where institutional knowledge compounds over time.

The fourth lesson is about sequencing. Sherman and her team did not try to do everything at once. First came stabilization and survival. Then came portfolio rationalization—exiting non-core businesses. Then came operational improvement—extracting more margin from the remaining businesses. Then came strategic acquisitions—deploying the cash flow from improved operations into growth. And finally came scaling—using the proven playbook to accelerate acquisition pace and expand into adjacent markets. Each phase built on the one before it, and trying to skip steps would have undermined the whole effort.

For Investors: What the Transformation Reveals

The Federal Signal story illustrates a category of investment opportunity that is chronically overlooked: the transformed industrial. Markets are generally efficient at pricing well-known growth stories—the Nvidias and Amazons of the world. But they are often slow to recognize when a previously troubled industrial company has fundamentally improved its business model, management quality, and competitive positioning. Federal Signal traded below book value during the crisis. Even several years into the transformation, the stock carried a conglomerate discount that reflected its troubled history rather than its improving reality. The re-rating from distressed conglomerate to quality industrial compounder took years, rewarding patient investors who recognized the transformation before the market fully did.

The quality of earnings has improved dramatically and continues to improve. The mix shift toward aftermarket and service revenue means that a larger share of Federal Signal's earnings are recurring, high-margin, and less cyclical. This is the kind of earnings quality improvement that supports higher valuation multiples—and rightly so, because the durability and predictability of the cash flows have genuinely improved.

Infrastructure spending tailwinds are bipartisan and long-duration. The IIJA is not a one-year stimulus—it represents a multi-year commitment to water, sewer, and transportation infrastructure that will drive demand for Federal Signal's products well into the next decade. State and local budgets, which fund the vast majority of municipal equipment purchases, benefit from strong property tax revenues and federal transfers. This is not a cyclical uptick—it is a structural increase in infrastructure spending that aligns directly with Federal Signal's product portfolio.

The risk worth monitoring most closely is acquisition discipline. Federal Signal's strategy depends on continued M&A, and the New Way Trucks deal at nearly four hundred million dollars represents a significant step up in deal size and integration complexity. History is littered with industrial companies that executed a brilliant turnaround only to destroy value by overreaching on acquisitions—indeed, Federal Signal's own history with E-ONE is the cautionary tale par excellence. Management's track record is strong, but the stakes grow with each deal. Investors should watch closely whether the New Way integration proceeds smoothly and whether management maintains its discipline on deal multiples as the acquisition pipeline grows.

One additional consideration that rarely appears in sell-side research: executive compensation alignment. Federal Signal's proxy statements reveal a compensation structure heavily weighted toward EBITDA growth and return on invested capital. This is exactly what investors want to see—management is incentivized to grow profitably, not just to grow. When executive pay is tied to the same metrics that create shareholder value, the risk of empire-building acquisitions is materially reduced. Sherman and Hudson eat their own cooking.

XII. Bear vs. Bull Case

The Bear Case: What Could Go Wrong

Municipal budgets are the lifeblood of Federal Signal's business, and they are not immune to economic cycles. A deep recession that crushes property tax revenues, sales tax collections, and state fiscal transfers would reduce equipment purchases across the board. Municipal procurement is driven by budget availability, and when budgets tighten, capital equipment purchases are among the first items deferred. Federal Signal weathered the 2020 downturn well because it was short and followed by massive fiscal stimulus, but a prolonged economic downturn—particularly one that coincides with declining federal infrastructure support—could pressure both new equipment orders and, eventually, aftermarket spending as municipalities defer even routine maintenance. The 2008-2010 experience, when revenue fell by more than forty percent, remains a cautionary reminder of how bad things can get when municipal budgets truly collapse.

The valuation reflects a lot of good news. Federal Signal's stock re-rated from single digits during the crisis to above one hundred dollars, and the current multiple prices in continued execution. If acquisition integration stumbles—particularly with the large New Way Trucks deal—or if organic growth disappoints, the stock has less margin of safety than it did five years ago.

Technological disruption is a low-probability but non-zero risk worth thinking about carefully. Autonomous vehicle technology could eventually transform street sweeping and refuse collection—imagine a self-driving sweeper that operates overnight without an operator. New warning technologies—smartphone-based alerts, geo-targeted push notifications—could theoretically reduce demand for traditional outdoor sirens. Some would argue that cell phones have already made sirens redundant for many scenarios, though the counterargument is compelling: outdoor sirens reach people who are sleeping, outdoors without phones, or in areas with poor cell coverage. These threats are years away from materializing in any meaningful way, but they bear monitoring.

Competition from private equity-backed consolidators is worth watching. Federal Signal is not the only buyer seeking to roll up fragmented municipal equipment niches. Well-capitalized PE firms could drive up acquisition multiples, making future deals less accretive, or could build competing platforms that challenge Federal Signal's market positions. Alamo Group, which owns the competing Vacall and Super Products brands, represents the most direct publicly traded competitor pursuing a similar consolidation strategy.

Myth vs. Reality: Fact-Checking the Consensus