Fervo Energy: The Geothermal Renaissance and the Oil-Patch Pivot

I. Introduction: The "Holy Grail" of Energy

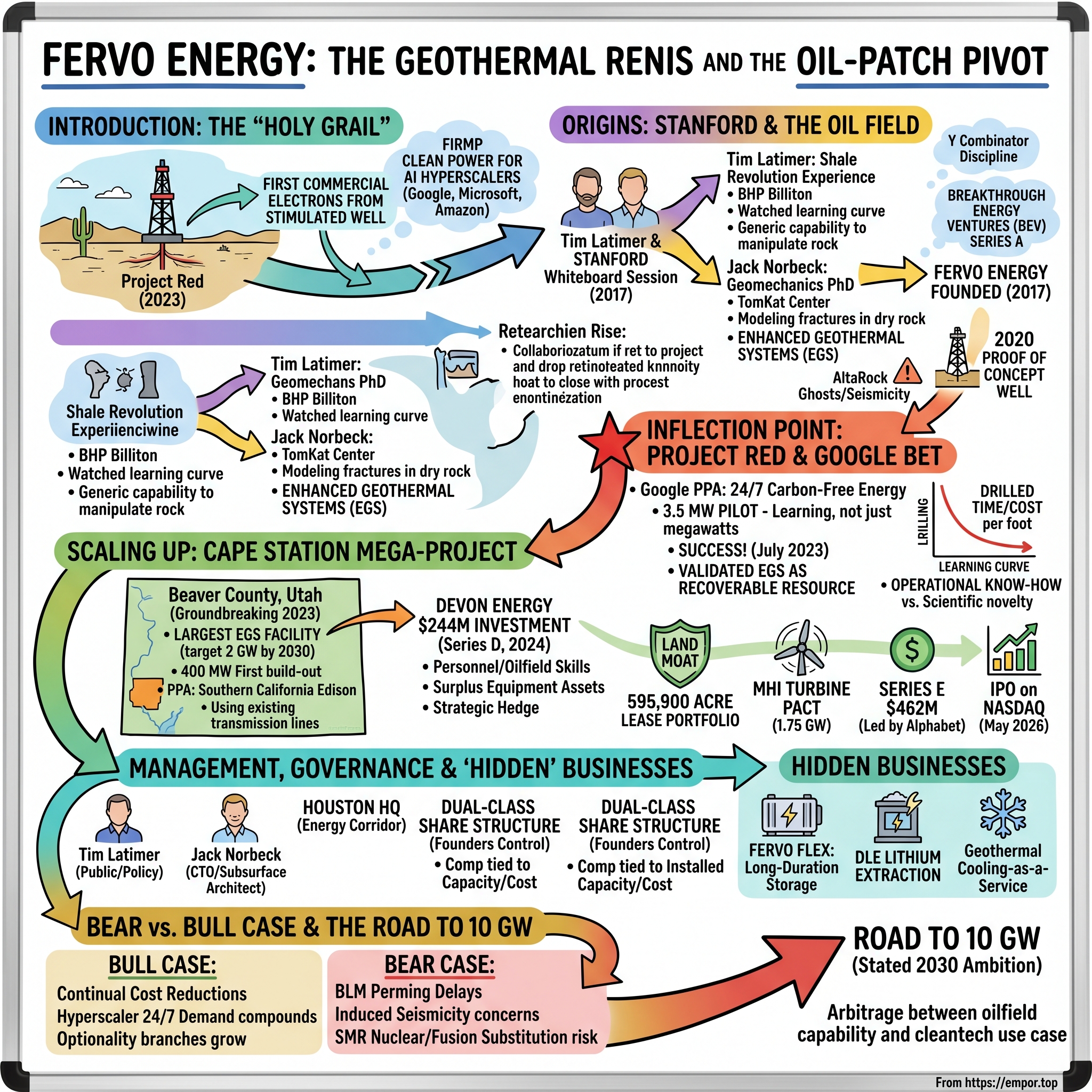

There is a particular kind of silence that only exists in the high desert of Nevada in late autumn. The wind moves over the scrub and basalt with no trees to argue with, and you can hear your own boots crunch on the caliche. In the summer of 2023, a few dozen engineers stood in that silence at a place called Project Red, watching a wellhead in Humboldt County. They were not roughnecks from Midland, and this was not an oil well. But the equipment looked identical to a Permian frac spread, the drilling logs looked identical to a Wolfcamp horizontal, and the people running it had, in a previous life, been drilling for gas. Only this time, what came back up the hole was not hydrocarbon. It was 375°F water, hot enough to flash to steam, and it had just generated the first commercial electrons in the world from a horizontal, hydraulically stimulated geothermal well1.

For roughly fifty years, geothermal energy was the polite cousin at the renewable-energy family dinner. Wind and solar got the cover stories, the tax credits, the Elon tweets, and the trillion-dollar capex cycles. Geothermal—boring, slow, geographically captive to a handful of fault zones in Iceland, the Philippines, Kenya, and the Imperial Valley—was treated as a niche. It contributed less than half a percent of U.S. electricity generation as recently as the early 2020s. Investors filed it under "interesting but un-scalable," somewhere between tidal and ocean thermal. And then, almost without warning, it became the most important sentence in the AI build-out.

That sentence is "firm clean power." The hyperscalers—Google, Microsoft, Amazon, Meta, Oracle—are now collectively running a power-constrained business. By 2025, the marginal unit of compute was no longer bottlenecked by chips, by talent, or even by capital, but by megawatts of carbon-free electricity that show up at 3:00 a.m. on a windless winter Tuesday. Solar plus batteries can do many things, but it cannot, today, economically deliver 99% uptime at gigawatt scale. Nuclear can, but the next AP1000 in the United States is at minimum a decade away. Into that gap walked a company most retail investors had never heard of until a few weeks ago, when it priced its IPO at $32 a share and listed on the NASDAQ under the ticker FRVO at a fully diluted valuation north of $10 billion2.

This is the story of Fervo Energy. It is also the story of how a generation of drilling engineers, who came of age during the shale revolution and were then told by polite society that their careers were a moral mistake, took the most sophisticated technology stack in the history of resource extraction—horizontal drilling, multi-stage hydraulic fracturing, fiber-optic sensing, microseismic monitoring—and pointed it ninety degrees downward into the basement granite. What they found was that the Earth, eight thousand feet below your feet, is a giant battery, a giant boiler, and a giant lithium reservoir, all at once. And they found that you could lease the rights to it for about four dollars an acre.

We are going to spend the next two hours unpacking how a Stanford classroom idea became, in nine years, a $10 billion publicly traded company with offtake agreements from Google, a strategic investment from Devon Energy, a 1.75-gigawatt turbine supply pact with Mitsubishi Heavy Industries, and a 2030 build target that, if executed, would make Fervo the largest single producer of 24/7 carbon-free electricity in North America[^3][^4]. We are going to look at the founders, the deals, the bear case, and the technology. And we are going to ask the question that every long-term investor is now asking: is this the Standard Oil of geothermal, or is this another cleantech mirage with a great PowerPoint?

II. The Origins: Stanford & The Oil Field

In the spring of 2017, on the second floor of Stanford's Y2E2 building, a thirty-one-year-old former drilling engineer named Tim Latimer was standing in front of a whiteboard arguing with a geologist. The geologist's name was Jack Norbeck. He was a PhD candidate in geomechanics, the academic discipline that asks what rock does when you put liquid into it under pressure. Tim had spent five years at BHP Billiton's shale division before he quit, took the GMAT, enrolled at Stanford's Graduate School of Business, and quietly began haunting the engineering school across the lawn. He was looking for a thesis problem big enough to justify what he had given up. He found Jack, and Jack had the answer.

Tim's biography is essential to understanding Fervo because it is the biography of an entire technological transfer. He grew up in north Texas, became a fourth-generation oilman, and joined BHP in 2010 just as the Eagle Ford Shale was being decoded. For five years he watched the Permian Basin transform from a sleepy depleted oil field into the most productive hydrocarbon province on Earth, not because anyone had discovered new oil, but because engineers had figured out how to drill a well sideways for two miles and crack the surrounding rock with water and sand. He saw, up close, how a learning curve in heavy industry actually works: the drilling time for a typical lateral fell from 30 days in 2010 to under 10 days by 2015, and the cost per foot fell by more than two-thirds. By the time he left BHP, he was convinced of something heretical: the shale revolution was not really about oil. It was about a generic capability to manipulate rock, and that capability was being wasted on a commodity that everyone wanted to phase out.

Jack Norbeck's contribution was the missing physics. His doctoral work at Stanford's TomKat Center for Sustainable Energy modeled how fractures propagate in hot, dry, crystalline rock—exactly the kind of rock that sits five to ten thousand feet beneath the western United States. The conventional geothermal industry, dominated by companies like Ormat אורמת טכנולוגיות Ormat Technologies, depended on natural hydrothermal systems—places where the Earth had conveniently provided hot water in permeable rock that you could just drill into. Those locations are rare. But Jack's models showed that if you could create permeability artificially—if you could "frack" hot dry rock—you could harvest geothermal energy from roughly twelve percent of the U.S. land area instead of less than one percent. The Department of Energy had a name for this: Enhanced Geothermal Systems, or EGS. It had been studied since the 1970s at Los Alamos. It had never been made to work commercially.

Tim and Jack incorporated Fervo Energy in 2017, raised a small angel round, and applied to the winter 2018 batch of Y Combinator. Y Combinator had funded almost no hard-tech energy companies. The cohort that took the founders in was overwhelmingly SaaS, and Tim has since recalled the surreal experience of presenting "we are going to drill ten-thousand-foot wells into the basement granite" alongside startups making Slack plug-ins. But YC gave them something more valuable than the $120,000 check: it gave them the discipline of writing software-style growth memos for a business that would ultimately consume billions in capex. That habit, of forcing oilfield economics through a Silicon-Valley iteration lens, would become a Fervo cultural fingerprint.

The next funding round came from Breakthrough Energy Ventures, the climate fund seeded by Bill Gates with a deliberately patient capital horizon of twenty years3. BEV's diligence on Fervo took most of 2018. The fund's investment committee had a single overriding concern, and it was not the science—the science was actually well understood. The concern was the trauma of CleanTech 1.0, the 2006–2012 venture cycle in which roughly $25 billion of Silicon Valley capital had vanished into solar manufacturers, biofuels, and battery startups that could not survive a commodity price war with Chinese incumbents. Geothermal had its own ghosts: AltaRock Energy had famously been forced to suspend EGS work near The Geysers in California in 2009 after induced seismicity rattled neighborhoods. Any new entrant had to prove not just that the technology worked, but that the technology, the regulatory posture, and the community engagement could all be threaded simultaneously. Tim's pitch was that the shale industry had spent the previous decade solving exactly those problems—microseismic monitoring, real-time fracture mapping, traffic-light protocols—and the playbook could be ported wholesale. BEV led the Series A.

By 2020, Fervo had drilled its first test well in northern Nevada and proven that horizontal laterals would hold open in hot crystalline rock long enough to circulate fluid. It was not yet a business. It was an existence proof. But the existence proof was about to meet a customer whose needs were going to reshape the entire grid.

III. The Inflection Point: Project Red & The Google Bet

On May 18, 2021, a relatively quiet sustainability post appeared on Google's corporate blog. The post announced a power purchase agreement between Google and Fervo Energy to develop a "next-generation geothermal project" in Nevada, with the resulting clean electricity flowing to Google's data centers in the same balancing authority[^6]. To the casual reader it looked like another corporate PPA in a year that had seen dozens. To anyone paying attention to how Google had begun to think about clean energy, it was the most important paragraph the company had written about electricity in fifteen years.

Here is what most people miss. From 2017 onward, Google had publicly claimed that it was "100% renewable." This claim, while technically defensible, relied on what the industry calls annual matching: Google bought enough renewable energy certificates over the course of a year to equal its total consumption, even though, at any given hour, its data centers might be drawing power from coal- or gas-fired generation. By 2020, the company's own engineering leadership had concluded that annual matching was no longer a credible decarbonization strategy. The new standard had to be 24/7 carbon-free energy, or CFE: every electron, every hour, every grid. The math on 24/7 CFE is brutal. Solar and wind, no matter how cheap, cannot get you past roughly 80% hourly CFE without absurd over-build and storage. To close the last 20%, you need firm power: nuclear, advanced geothermal, long-duration storage, or some combination. There was almost nothing on the market.

Project Red was Google's first commercial bet on enhanced geothermal as the firm-power solution. It was a 3.5-megawatt pilot. In the universe of utility-scale generation, 3.5 megawatts is a rounding error—a single modern gas turbine produces a hundred times that. But the point of Project Red was never the megawatts. The point was the learning curve.

Between 2021 and 2023, Fervo drilled and stimulated two production wells and one injection well at the Project Red site near Winnemucca, Nevada. They drilled horizontal laterals roughly 4,000 feet long into 375°F granite, perforated them with multiple stages of hydraulic stimulation, and then connected the wells in a closed loop with a small Organic Rankine Cycle power plant on the surface1. On July 18, 2023, Fervo announced that the project had completed a thirty-day production test at full design output—the first time in history that a horizontal, multi-stage stimulated EGS project had delivered commercial power1. The number that mattered most to the engineering community was not the 3.5 MW. It was the flow rate: 63 liters per second at a pressure differential that confirmed the artificially induced fracture network was acting as a designed reservoir, not a leaky one. To a petroleum engineer, this was the moment EGS stopped being an academic exercise and became a recoverable resource.

What happened next is the part of the Fervo story that should arrest any serious investor. Between the first horizontal well at Project Red, drilled in 2022, and the first horizontal well at Cape Station in southwest Utah, drilled in 2024, the average time to drill a Fervo geothermal lateral fell by approximately seventy percent[^7]. The cost per well fell by a similar magnitude. This is the shale learning curve, replayed in geothermal, on fast-forward. The Permian needed roughly five years to compress drilling times by that much. Fervo did it in two, because it inherited the playbook rather than inventing it.

For a fundamental investor, this is the single most important thing to understand about Fervo. The business is not selling electrons. The business is selling a manufacturing process for electrons—a repeatable, declining-cost engineering recipe that turns hot rock into firm baseload. As Tim Latimer has framed it in interviews, the company is "the Permian Basin Operator of Geothermal." It is not a one-off project developer. It is a factory.

Project Red also reset the political conversation. Federal regulators, who had spent fifteen years quietly worrying about fracking-related seismicity, watched Fervo run six months of continuous operations with not a single felt event above the project's pre-agreed thresholds. The Bureau of Land Management—the actual landlord for most of the geothermal-prospective acreage in the American West—began updating its leasing rules with EGS specifically in mind. The Department of Energy followed up in April 2024 with a $25 million grant for the Utah project, the first significant federal money to flow into commercial EGS rather than pilot research[^8]. The center of gravity in U.S. geothermal had moved from the laboratory to the rig floor, and Fervo had moved with it.

IV. Scaling Up: The Cape Station Mega-Project

If Project Red was the proof of concept, Cape Station is the factory. Drive south from Salt Lake City for about three and a half hours, past the salt flats and through the Pahvant Range, and you will find yourself in Beaver County, Utah—an unremarkable patch of high-desert ranchland sitting on top of one of the largest concentrations of accessible geothermal heat in North America. There, on a ground-breaking day in September 2023, Utah Governor Spencer Cox stood in front of a partially constructed drilling pad and told the assembled crowd that the project before them would, by the end of the decade, be the largest enhanced geothermal facility in the world[^9].

The numbers on Cape Station do not look like the numbers on a single project. They look like the numbers on a small utility. The site is permitted for at least 400 megawatts of installed capacity in its first build-out, with subsequent expansions targeting up to 2 gigawatts by 2030 across the broader Utah lease position[^7]. The first 100 megawatts came online in phases through 2025 and 2026. The first power-purchase agreements from Cape Station are with Southern California Edison, which contracted for 320 megawatts in two separate tranches in 2023, and which intends to wheel the electrons across the Intermountain Power Project transmission line[^7]. The economics work because Cape Station happens to sit roughly forty miles from existing high-voltage interconnection that, until recently, had been carrying coal-fired power from a retiring plant. Fervo is, in a very literal sense, plugging into the carcass of the old fossil grid.

But the more interesting story at Cape Station is not the megawatts. It is the partner who showed up. On February 27, 2024, Devon Energy—one of the larger independent oil and gas producers in the United States, with a market capitalization north of $25 billion and a balance sheet built on Permian and Anadarko production—announced a $244 million strategic investment in Fervo, anchoring the company's Series D round and taking what would eventually become an approximately 13% equity stake[^10]. Devon's CEO at the time framed the investment as the "natural extension" of Devon's drilling and completions expertise into a new resource, and the company committed not just capital but actual operational support—drilling crews, completion engineers, supply chain.

Why did an oil and gas major write a quarter-billion-dollar check to a geothermal startup? Three reasons, in declining order of importance.

First, the people. The marginal hire at Cape Station is a directional driller, a frac engineer, or a wireline specialist. Those people exist in Oklahoma City, Midland, and Houston. They do not exist in Reykjavik or San Francisco. Devon's labor pool was, almost overnight, Fervo's labor pool.

Second, the assets. Devon owned thousands of feet of idle drilling rigs, completion equipment, and pressure pumping units that had become surplus as the Permian rig count rationalized after 2020. Those assets, repositioned to Utah and Nevada, dramatically lowered Fervo's capex per megawatt.

Third, and most strategically, the optionality. Devon's leadership had quietly concluded that the long-run terminal value of U.S. oil and gas was uncertain enough that they needed a hedge. Geothermal, especially EGS, was the only clean energy technology where Devon's existing skills were a genuine source of competitive advantage. Solar panels and wind turbines do not care that you know how to set casing in 400°F downhole conditions. Hot dry rock cares very much.

The Devon partnership turned Fervo from a venture-backed pilot operator into a project-finance machine. Within eighteen months of Devon's investment, Fervo had assembled approximately 595,900 acres of geothermal lease rights across Utah, Nevada, Oregon, and Idaho, at an average acquisition cost of roughly four dollars an acre[^7]. Four dollars. To give that number context: a comparable acreage position in the Permian Basin would cost between fifteen thousand and forty thousand dollars an acre. Fervo had built, in eighteen months and for under three million dollars in land cost, a subsurface land position that, if its thermal-gradient assumptions are right, would underwrite tens of gigawatts of generation. This is the subsurface land moat, and it is the single most underappreciated asset on the Fervo balance sheet.

The capital intensity of building actual plants on that acreage is a different matter, and it requires real money. Through 2024 and 2025, Fervo stacked the supply chain. The signature deal was a 1.75-gigawatt turbine supply pact with 三菱重工業 Mitsubishi Heavy Industries, announced November 15, 2024, locking in the bespoke high-temperature steam turbines that Cape Station and follow-on projects would require[^11]. MHI was one of only three companies in the world that could build at the required spec; the supply pact was, in effect, a competitive moat in itself, since it deprived future U.S. EGS entrants of equivalent turbine access for several years.

Series E followed in November 2025, a $462 million round led by Google's parent Alphabet with significant participation from Capricorn Investment Group and existing investors, which valued the company at approximately $6.5 billion pre-IPO4. The Series E pricing was the proof that the public-market window was open. Six months later, on May 6, 2026, Fervo priced its IPO at $32 a share, sold approximately 35 million shares, raised roughly $1.1 billion in primary capital, and saw the stock open the next morning at $412. At a fully diluted equity value of approximately $10.4 billion, FRVO became the largest U.S. clean-energy IPO since 2021 and the first pure-play geothermal company ever to list on a major American exchange2.

V. Management & Governance: The "Controlled" Climate Giant

Walk into Fervo's Houston headquarters—a relatively unglamorous office park in the Energy Corridor, deliberately chosen because that is where the drilling talent lives—and you find a culture that does not look or feel like a Bay Area cleantech startup. The dress code is jeans and steel-toes. The whiteboards are covered with mud-weight calculations and tubular schedules. People say "frac" instead of "stimulation" because the former is faster to write. The CEO, Tim Latimer, still goes to drill sites in person, and several people who have worked with him describe his decision-making style as "petroleum engineer playing climate chess."

Tim is the public face of the company and, increasingly, the policy architect of the entire U.S. EGS industry. He has testified before Congress, sits on the boards of multiple geothermal trade associations, and has become a favored interlocutor for the Department of Energy and the Bureau of Land Management on permitting reform. His public-facing argument is deliberately bipartisan: geothermal is a U.S. resource, drilled by U.S. workers, on largely U.S. federal land, and it is therefore a national-security asset as much as a climate one. That framing has earned Fervo unusual political cover, including support from senators who would never sign a Green New Deal but who very much want their Utah and Nevada constituents drilling for something.

Jack Norbeck, the CTO, is the quieter half of the founding pair. Where Tim is the public storyteller, Jack is the subsurface architect, and most of Fervo's technical IP—the proprietary fracture-design software, the fiber-optic distributed acoustic sensing protocols, the real-time reservoir management system—traces back to his group. Jack does not give many interviews. He reportedly spends a disproportionate share of his time at the wellpad. People who have worked with both founders describe the dynamic as deliberately Jobs–Wozniak: one founder for the outside world, one founder for the rock.

The cap table that emerged at IPO is unusual for a U.S.-listed energy company. Fervo went public with a dual-class share structure: Class A common shares carry one vote per share and trade publicly under FRVO, while Class B founder shares carry forty votes per share and are held by Latimer, Norbeck, and a small group of early employees2. The Class B structure gives the founders approximately fifty-three percent of total voting power despite holding closer to fifteen percent of economic equity2. Long-only institutional investors have a documented allergy to this kind of structure, and it was the most contentious item in the IPO roadshow. The founders' argument, defended openly on the road, was that geothermal is a multi-decade capital-deployment story whose worst possible outcome would be quarterly-earnings myopia from public-market shareholders, and that voting control was necessary to "stay patient" through the inevitable bumps. Whether one accepts that argument or not, it is a material governance fact that any FRVO holder must understand: the public shareholders do not control the company. The founders do.

The economic ownership at IPO breaks down roughly as follows2. Devon Energy holds approximately 13%, having converted its preferred from the 2024 strategic round. Capricorn Investment Group holds approximately 12%. Alphabet/Google holds approximately 7%, accumulated through the Series E and a small earlier participation. Breakthrough Energy Ventures, the original Series A lead, retains approximately 5%. The founders and employees collectively retain approximately 15% economic. The remainder—roughly 48%—is distributed across the IPO float, other strategic investors, and a small number of sovereign wealth funds that participated in the late-stage rounds. There is, notably, no oil major (ExxonMobil, Chevron, Shell, BP) on the cap table, despite multiple reported approaches.

Compensation is structured in a way that reinforces the long-cycle thesis. According to the S-1, ninety-six percent of named-executive-officer compensation is at-risk and variable, with vesting tied to two performance gates: cumulative installed megawatt capacity, and average all-in cost per megawatt-hour generated2. Latimer's base salary is well under a million dollars annually; the rest of his expected compensation accrues only if Fervo hits its 2030 capacity targets and continues to drive the drilling cost curve downward. This is not a compensation structure designed for a CEO who is going to flip the company to an oil major. It is a structure designed for someone who intends to run the thing for a decade.

The independence question—why didn't they just sell to Chevron in 2023?—is the one Tim has been asked most often on the IPO roadshow. His public answer, reported in multiple outlets during the May 2026 listing process, has been that "the supermajors have no idea how to operate a multi-decade depleting-asset-free resource business," and that Fervo's terminal value is a function of running it like a utility, not flipping it like a wildcat. The skeptic's version of that answer is that the founders simply preferred to be billionaires running a public company rather than employees inside a major. Both can be true at once.

VI. "Hidden" Businesses: Beyond the Power Grid

If you read only the IPO press release, you would conclude that Fervo Energy is a clean-power generation company. That is technically correct and substantively incomplete. Hidden inside the S-1, and increasingly visible in the company's investor presentations, are three additional businesses that together may be worth more, on a probability-weighted basis, than the core electricity business itself.

The first is FervoFlex, the company's branded long-duration energy storage product. The insight here is elegant in the way that the best second-derivative business ideas usually are. A geothermal reservoir is a giant pressurized rock formation full of hot water. If you stop circulating fluid for a few hours and let the pressure build, you have, in effect, charged a battery. If you then release the flow during the next hour, you discharge it. Fervo's reservoir engineers realized that they could deliberately design certain Cape Station wells with extra fracture volume specifically to enable load-following operation, and that the resulting facility could discharge at varying capacity for periods of five to ten days at a stretch[^13]. In the long-duration energy storage market—where the competition is Form Energy's iron-air batteries, ESS Inc.'s flow batteries, and assorted pumped-hydro projects—FervoFlex has a capex profile that is, on the company's own disclosed numbers, roughly half the cost per kilowatt-hour of round-trip stored energy at the durations utilities most want, namely twelve hours to one hundred hours[^13]. If those numbers survive scrutiny over the next two years of operating data, FervoFlex is by itself a multi-billion-dollar business line.

The second hidden business is direct lithium extraction, or DLE. Geothermal brines—the hot water that comes up the production well at Cape Station and at sites in the Salton Sea region of California—are often dissolved-mineral cocktails containing meaningful concentrations of lithium, manganese, zinc, and rare earths. The amounts vary by formation, but Salton Sea brines in particular have been studied for decades as a potential lithium resource large enough to satisfy a significant fraction of U.S. electric-vehicle battery demand. The historical problem has been that there was no clean way to extract the lithium without disrupting the geothermal cycle. By 2025, several independent operators in the Salton Sea—including Berkshire Hathaway Energy's CalEnergy unit and lithium-specialist startups—had begun deploying DLE pilots at commercial geothermal sites5. Fervo, drilling in Utah brines that are less lithium-rich but cleaner chemically, has disclosed that early extraction tests at Cape Station are recovering battery-grade lithium carbonate as a co-product, with margins that the company describes as "additive but not yet material" to consolidated revenue2. The optionality here is large. If lithium prices stabilize above $20,000 per ton, the DLE co-product can convert a 100-megawatt geothermal plant into a 100-megawatt plant plus a small lithium mine, with shared capex.

The third hidden business is cooling-as-a-service for AI data centers. This one is the most counterintuitive. The bottleneck for hyperscaler data center expansion in 2026 is not just power; it is water. Air-cooled data centers consume enormous amounts of evaporative water at the cooling tower stage, and water-stressed jurisdictions—Arizona, parts of Texas, the Inland Empire—are increasingly refusing permits for new builds. Fervo's pitch, which it has begun marketing under the working label "Geothermal Cooling Solutions," is to use the high-temperature output of a geothermal plant to drive a 臭化リチウム lithium bromide absorption chiller, which produces chilled water for data-center heat rejection without consuming evaporative water. The economics rely on the same underlying well bore producing both electricity and process heat, and the result, in principle, is a co-located clean-power-and-cooling campus that can be sold as a single offering to a hyperscaler. Two of the announced Cape Station expansions are reportedly being scoped specifically around hyperscaler co-location agreements, though specifics are not yet disclosed.

Pulling these threads together, the segment composition of Fervo's revenue, as projected in the S-1 for 2027 (the first full year of post-IPO operations), is roughly sixty-five percent firm power, twenty percent storage-as-a-service, and fifteen percent minerals and lithium2. Those are projections, not history, and any investor should treat them with appropriate skepticism. But the strategic point is clear. Fervo is not building a power plant. It is building a subsurface platform from which multiple revenue streams can be harvested simultaneously, the same way a Permian operator harvests oil, natural gas, NGLs, and water disposal from a single drilling unit. The Permian comparison is, in fact, the right way to think about Fervo's terminal economics: a single well, multiple co-products, declining unit costs.

VII. Playbook: Porter's Five Forces and Hamilton's 7 Powers

There is a temptation, when reading about a company like Fervo, to mistake the technology for the moat. The technology is impressive, but technology by itself is rarely a durable competitive advantage—patents expire, engineers get poached, and other people read the same papers. To assess whether Fervo has a real moat, it is worth running the business through both Michael Porter's five-forces framework and Hamilton Helmer's seven-powers framework, and asking, honestly, where the durable advantages actually live.

Start with counter-positioning, in Helmer's vocabulary. Fervo offers something that wind and solar developers structurally cannot, which is firm hourly capacity. This is not a matter of effort; it is a matter of physics. A solar developer who tries to deliver 24/7 power must bolt on enough battery storage to bridge the night, and that battery cost is large enough to flip the levelized economics. A wind developer faces the same problem in lower-frequency form during multi-day low-wind events. Fervo's marginal cost of providing hourly firmness is, by contrast, close to zero, because the reservoir is naturally firm. Hyperscaler customers, who increasingly buy on a 24/7 carbon-free basis, are willing to pay a meaningful premium for that firmness—reportedly thirty to fifty percent above the spot levelized cost of intermittent renewables. Wind and solar developers cannot replicate this without becoming, in effect, fossil hybrid plants. That is counter-positioning in its textbook form.

Second, cornered resource. The 595,900-acre lease portfolio acquired at four dollars an acre is, in Helmer's language, a cornered resource of the same kind that mineral leases were for John D. Rockefeller. The federal leasing system that allowed Fervo to assemble this position at that price has since been substantially reformed; subsequent leases are competitively bid and routinely close at five to twenty times that historical cost6. Anyone wanting to replicate Fervo's land position today would either have to bid up the remaining federal acreage or settle for inferior thermal-gradient locations. There is, in finite supply, only so much shallow hot rock under western federal land, and Fervo has cornered a meaningful fraction of it.

Third, process power. This is the subtler advantage and the one that requires longest to confirm. Process power exists when a company has developed proprietary operational know-how that cannot be easily reproduced, even by a competitor with the same equipment and the same blueprints. Fervo's drilling time has fallen seventy percent in two years, which strongly suggests the existence of internal know-how that is genuinely difficult to copy. The proprietary fiber-optic distributed acoustic sensing system—which allows Fervo to map the propagation of fractures in real time during stimulation, and adjust pumping schedules accordingly—is the heart of this know-how. The fiber technology itself is commercially available; the use protocols, the failure modes, the calibration data, and the dozens of small operational tricks accumulated over the past four years are not. Process power tends to be invisible from the outside and durable from the inside, which is exactly the kind of moat fundamental investors should pay for.

Running the same business through Porter's five forces produces a complementary picture. The threat of new entrants is meaningfully constrained by all three powers above plus the sheer capital intensity—a single 100-megawatt EGS plant requires roughly $400 million of upfront capex, with all of it spent before any revenue arrives. The bargaining power of suppliers is moderate; drilling rigs are commodity equipment, but high-temperature turbines (the MHI relationship) and specialized completion services are concentrated. The bargaining power of buyers—the hyperscalers—is the most interesting square on the matrix. In principle, Google, Microsoft, and Amazon are huge customers who could bargain Fervo's prices down. In practice, their need for firm carbon-free energy is so acute, and the supply of alternatives so limited, that they have been functionally price-takers in the current round of PPAs. That balance will normalize as supply grows. The threat of substitutes is the genuine question and deserves its own paragraph in the bear case. Industry rivalry, for now, is muted; the only serious EGS competitors are Eavor Technologies (Canadian, closed-loop design, different technical approach), Sage Geosystems (a former Shell spin-off pursuing a similar shale-inspired EGS path), and a handful of European pilots. None has anything approaching Fervo's land position, customer base, or operational track record.

The myth vs. reality question is worth pausing on. The consensus narrative on Fervo says: brilliant technology, supported by hyperscaler demand, with no real competition. The fact-check looks like this. The technology is real but not particularly proprietary at the science level; the moat is operational, not scientific. Hyperscaler demand is real and very large but is contractual rather than open-ended; PPAs are signed at specific volumes and prices, and downside scenarios in which a hyperscaler cancels or renegotiates have to be modeled. And competition is currently muted but will not stay that way; the same shale-to-geothermal logic that produced Fervo will, with a lag of three to five years, produce credible rivals.

VIII. Analysis: The Bear vs. Bull Case

Every fundamental investor reading this is, by now, doing the same back-of-envelope math: a $10 billion equity value against roughly two hundred and fifty million dollars of 2025 revenue, the bulk of which is project-development fees and partial Cape Station tranches rather than steady operating earnings2. That ratio is venture-style, not utility-style. It is priced not for what Fervo is, but for what Fervo could be by 2030. To assess whether that pricing is defensible, the two cases are worth laying out side by side.

The bull case rests on three propositions. First, that Fervo's drilling learning curve continues for another five years at anything close to its current pace, dropping all-in levelized cost of electricity from EGS into the forty-to-fifty-dollar-per-megawatt-hour range, where it becomes the cheapest source of firm carbon-free power in North America. Second, that hyperscaler demand for 24/7 CFE continues to compound at a rate consistent with the current AI capacity build-out, generating contracted offtake demand large enough to absorb Fervo's planned ten-gigawatt 2030 pipeline at premium pricing. And third, that the optionality businesses—FervoFlex storage, DLE lithium, geothermal cooling—each become billion-dollar revenue lines on a five-year horizon, turning Fervo into the diversified earth-resources platform that the management team has been quietly describing on the roadshow. If two of those three propositions hold, the bull case is in a range that justifies the current valuation. If all three hold, the current valuation looks low.

The bear case rests on different propositions, and any serious investor must take them seriously. First, regulatory and permitting risk on federal land. The Bureau of Land Management's permitting process for geothermal projects on federal acreage is, despite recent reforms, still capable of adding eighteen to thirty-six months to a project schedule. A change in administration, a hostile state regulator in Utah or Nevada, or a NEPA challenge could derail multiple projects simultaneously. Second, induced seismicity. Fervo has so far avoided any felt seismic events at Project Red or Cape Station, but the precedent at AltaRock's Geysers project and at deep geothermal pilots in Pohang, South Korea (which generated a 5.5-magnitude earthquake in 2017 traced to wastewater injection) means that a single significant induced event at any U.S. EGS site could create a political problem for the entire industry. Third, and most strategically, the technology substitution risk. The 2030s could plausibly see the commercial arrival of small modular nuclear reactors (NuScale, X-Energy, TerraPower) or, in a more speculative scenario, first-of-a-kind fusion pilots from Commonwealth Fusion, Helion, or TAE. Either category, if economically viable, becomes a direct substitute for firm clean power and competes head-on with Fervo's value proposition. Fervo's bet, implicitly, is that EGS scales faster than SMR or fusion in the 2026–2032 window. That bet is defensible, but it is not free.

Putting Fervo in competitive context sharpens the picture. The conventional geothermal incumbent, Ormat אורמת טכנולוגיות Ormat Technologies, operates roughly 1.2 gigawatts of installed hydrothermal capacity globally, generates approximately $850 million in annual revenue, and trades at an enterprise value of around $5 billion[^16]. Ormat is a real business with real cash flows, but it is structurally capacity-constrained by the rarity of natural hydrothermal sites and cannot replicate Fervo's EGS approach without abandoning much of its current operating model. Eavor Technologies, the Canadian closed-loop competitor, uses a technically elegant design that does not require fracturing—a single deep U-shaped well circulates fluid through the heat exchange—but the closed-loop architecture has so far struggled to match EGS economics at scale, and Eavor remains private with no commercial-scale plant operating in North America. Sage Geosystems, perhaps the closest EGS rival, has demonstrated promising results at a single Texas pilot but lacks Fervo's land position and hyperscaler relationships. The Japanese super-major 国際石油開発帝石 INPEX Corporation has a small geothermal portfolio in Indonesia and Japan but operates on a fundamentally different (hydrothermal, joint-venture) model[^17]. The global competitive set, in short, is thinner than the casual observer might assume.

The McKinsey analysis published in January 2025 on the firm-power market argued that North American firm-power demand from hyperscaler load alone could reach 80 to 130 gigawatts by 2030, against a current supply pipeline of perhaps 25 gigawatts of new nuclear, gas-with-carbon-capture, and advanced geothermal combined7. That supply-demand gap is the macroeconomic fact behind Fervo's valuation. If even a modest fraction of it is filled with EGS, Fervo will be capacity-constrained, not demand-constrained, for the next decade.

For the long-term fundamental investor, the two or three KPIs that actually matter to track Fervo's ongoing performance are narrower than the disclosure deck would suggest. The first is the all-in drilling cost per megawatt of installed capacity, which is the direct readout of the learning curve and the single best leading indicator of whether the bull thesis is intact. The second is the cumulative megawatts of contracted offtake under signed PPAs, which is the direct readout of customer pull. A distant third—worth watching but not yet material—is the realized co-product revenue per megawatt-hour from FervoFlex and lithium, which will determine whether the optionality businesses convert. Quarterly revenue and EBITDA, the metrics public-market investors instinctively track, will be misleading for several years because they are dominated by lumpy project-development accounting. Look at the operating metrics, not the income statement.

IX. Epilogue: Lessons and the Road to 10 GW

It is worth pausing, before closing, to notice something about the cast of characters in this story. Tim Latimer learned to drill at BHP in the Eagle Ford. Jack Norbeck did his geomechanics PhD on rock that had spent its previous research life being studied for oil. The Devon Energy crews now stimulating wells at Cape Station spent the previous decade frac'ing Wolfcamp laterals in West Texas. The fiber-optic sensing technology Fervo uses to monitor fracture propagation was developed by oil-service companies for downhole logging in the 2010s. The political coalition that has made Fervo's permitting work is composed in significant part of Republican governors and senators from western states whose constituents drilled for hydrocarbons for three generations.

In other words, the climate solution at the center of this story did not come from the climate movement. It came from the oil patch. The skills, the equipment, the people, the operational instincts, the lobbying playbook, the supply chain, and the cultural posture were all imported wholesale from an industry that the climate movement had spent twenty years trying to shut down. Tim Latimer has made this point explicitly in interviews; he has argued that the transferability of fossil-fuel expertise to clean energy is the single most underappreciated decarbonization story of the decade, and that any policy approach that treats oilfield workers as the enemy is, by that fact alone, sabotaging the energy transition.

That observation contains a more general lesson for founders, which is the lesson of transferable innovation. The most important technological transfers in industrial history rarely look like new science. They look like a mature, well-understood capability—horizontal drilling, mass-production assembly lines, microchip fabrication, internet routing—pointed at a new substrate. The substrate at Fervo is hot dry rock; the capability is twenty years of accumulated shale-completion know-how. The arbitrage between an industry that no longer needs that capability and a use case that desperately does is what created a $10 billion company in eight years. The founders who will build the next decade's most valuable energy companies are, almost certainly, sitting today inside large incumbent industrials—oil majors, chemical companies, utilities—watching capabilities they have been told are obsolete, and asking, like Tim asked at Stanford in 2017, what else those capabilities could do.

The road to 10 gigawatts, which is Fervo's stated 2030 ambition, is not assured. It requires the drilling cost curve to keep falling, the hyperscaler demand curve to keep rising, the permitting environment to stay roughly cooperative, and the seismic risk to stay roughly contained. Any of those four conditions could deteriorate. If all four hold, Fervo will, by the end of this decade, be one of the ten largest independent power producers in the United States, and it will have done so by drilling holes in the ground using the same techniques that produced the shale revolution—except now the rock gives back electricity instead of oil, and the rock never depletes.

The Acquired thesis on Fervo, if one had to compress it to a sentence, is that the company is the rare clean-energy investment where the technology risk has already been substantially retired (Project Red proved it), the customer risk is structurally bounded (the hyperscalers cannot get firm CFE anywhere else at scale), and the moat is multiple-layered (cornered land position, process learning curve, supply-chain pre-emption, governance control). What remains is execution risk on a scale that will test whether a founder-led, vote-controlled, capex-heavy energy company can navigate the public markets without losing the patient capital posture that got it here. That is the question every quarterly earnings call from now until 2030 will, in one form or another, be about.

The 2026 IPO closed Fervo's first chapter. The next chapter is whether geothermal becomes a footnote or a backbone of the AI-era grid. The cast is in place. The rigs are turning. The customers are signed. The rest is rock.

References

-

Fervo Energy Announces Technology Breakthrough at Project Red — Fervo Energy, 2023-07-18 ↩↩↩

-

Fervo Energy IPO Prospectus (Form S-1) — SEC EDGAR, 2026-04-15 ↩↩↩↩↩↩↩↩↩↩

-

The Geothermal Revolution: How Shale Tech Unlocked the Earth — Financial Times, 2024-03-12 ↩

-

Fervo Energy Secures $462M Series E Funding Led by Google — Bloomberg, 2025-11-14 ↩

-

Geothermal Lithium: The New Frontier of Brine Extraction — Reuters, 2025-06-08 ↩

-

The Geothermal Revolution: How Shale Tech Unlocked the Earth — Financial Times, 2024-03-12 ↩

-

The Case for Firm Power: Why Hyperscalers Need Geothermal — McKinsey & Company, 2025-01-10 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube