Fox Corporation: The Lean, Live Cash-Flow Empire

I. Introduction & Episode Roadmap

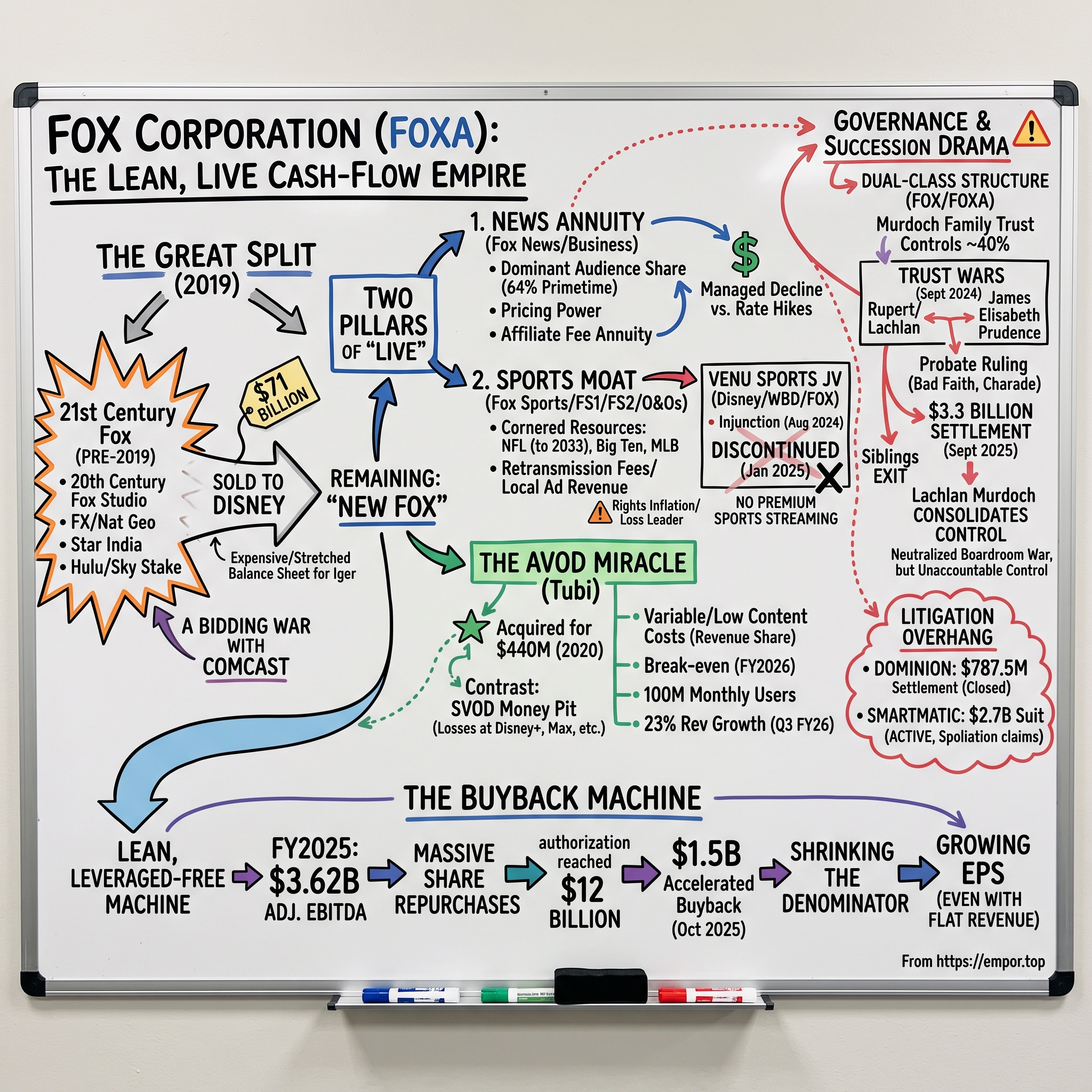

Picture the media boardrooms of the late 2010s. Every executive in the industry is staring at the same chart: the near-vertical rise of Netflix's subscriber count and stock price. The verdict is unanimous and it is delivered like scripture. The future is subscription streaming. Build a Netflix-killer or die. Disney would pour itself into Disney+. Warner would bet the house on HBO Max. Comcast would launch Peacock. Paramount would build Paramount+. Collectively, the legacy media industry was about to light tens of billions of dollars on fire chasing a business model whose economics almost none of them could actually replicate.

And in the middle of that stampede, one 87-year-old man did the opposite. Rupert Murdoch looked at the same charts everyone else did and concluded that the smart move was not to run the streaming race — it was to sell the horses. He sold the bulk of his entertainment empire — the 20th Century Fox film studio, the FX and National Geographic cable networks, the Star India business, the stake in Hulu and Sky — to Disney for roughly $71 billion, a price inflated by a bidding war with Comcast.2 What remained, spun off in March 2019, was a deliberately narrow company built around exactly two things people still watch live and on somebody else's schedule: news and sports.1

That remaining company is the subject of this story. Fox Corporation trades on the NASDAQ Global Select Market under two tickers — FOXA for the publicly traded Class A shares and FOX for the Class B voting shares — with its corporate home at foxcorporation.com. It is one of the strangest survivors in modern media: a company with no premium subscription streaming service of any kind, operating in a pay-TV universe that shrinks every single year, that nonetheless generated $16.30 billion in revenue and $3.62 billion in Adjusted EBITDA in the fiscal year ended June 30, 2025 — and used its cash to shrink its own share count under a repurchase authorization that reached $12 billion.1

The central puzzle of this episode is that apparent contradiction. How does a business tethered to a structurally declining product — the cable bundle, bleeding subscribers at a mid-to-high single-digit annual rate — not just survive but throw off enough cash to fund one of the most aggressive buyback programs in media? The answer is a story about focus, about the peculiar economics of things that must be watched live, and about a family whose internal war over control spilled into a Nevada courtroom and then into a $3.3 billion settlement.

Here is the roadmap. First, the anatomy of the 2019 "Great Split" — why the Disney deal was arguably the trade of Rupert Murdoch's career and a millstone for Bob Iger. Second, the affiliate-fee "annuity" that makes Fox News and Fox Sports the last load-bearing walls of the linear bundle. Third, the counterintuitive triumph of Tubi, a free ad-supported streaming service Fox bought for $440 million while everyone else was spending tens of billions on subscriptions.6 Fourth, the buyback machine. And finally, the governance drama — the dual-class structure, the trust wars, and the litigation overhang from Dominion and Smartmatic that could still send a nine- or ten-figure bill to the door. This is not a company that wins by being loved. It wins, if it wins, by owning the last things worth paying for on live television. Let's test whether that's true.

II. Genesis of "New Fox" & The 2019 Disney Transaction

To understand why Rupert Murdoch sold, you first have to understand what he built — and the two audacious bets that hardwired the DNA of the company that exists today.

Rewind to 1986. American television is a cozy oligopoly. Three networks — CBS, NBC, and ABC — split essentially the entire national audience, and the idea of a fourth broadcast network is treated as a fantasy for people who don't understand the business. Murdoch, an Australian newspaper baron who had just become a U.S. citizen so he could legally own American TV stations, launched the Fox Broadcasting Company anyway.3 For years it was mocked as the network of "Married… with Children" and cartoons. But Murdoch understood something structural: a network is only as valuable as the appointment television that forces viewers to show up at a specific time. And nothing forces that behavior like live sports.

So in December 1993 came the first franchise-defining bet. Fox bid roughly $1.58 billion — a sum that stunned the industry — to take the NFL's NFC television package away from CBS, which had carried professional football for decades.3 The move was widely called reckless. It was, in fact, one of the great strategic purchases in television history. Overnight, Fox went from an upstart to a legitimate network; local stations across the country switched their affiliations to grab the NFL, and Fox acquired the audience, the credibility, and the promotional platform to launch everything else. The lesson embedded itself permanently in the company's thinking: overpay for the thing everyone must watch live, and monetize the ecosystem around it.

The second defining bet came in 1996. Murdoch hired Roger Ailes, a combative former Republican political operative and television producer, to build a cable news channel from scratch. Fox News Channel launched that October into a market that CNN supposedly owned. Ailes's insight was that a large, politically conservative slice of the American audience felt unseen by the existing networks — and that serving that audience with unapologetic point-of-view programming would create ferocious loyalty. It worked beyond anyone's projection. Within about six years Fox News passed CNN in the ratings, and it has not surrendered the top spot in cable news since. That loyalty — the fact that a specific, passionate audience will follow Fox News wherever it goes — is the single most important asset in the entire company, and we will return to why it matters so much for the economics.

Now fast-forward to 2017. Murdoch, by then in his mid-eighties and increasingly working alongside his elder son Lachlan, confronted an uncomfortable truth. His entertainment assets — the 20th Century Fox studio, the FX and National Geographic networks — were good businesses, but they were subscale in a world where Netflix was spending more on content than the entire studio could. To compete globally in scripted entertainment, Fox would have to spend billions a year it did not want to spend, on a game where the incumbents' advantage of a huge library and global distribution belonged to others. Murdoch decided he would rather be a seller than a loser.

What followed was the kind of transaction Murdoch had spent a lifetime engineering. Disney's Bob Iger wanted the entertainment assets to fuel Disney+. But Comcast's Brian Roberts wanted them too, and the resulting bidding war pushed the price to roughly $71 billion in cash and stock — a number Iger would later admit stretched Disney's balance sheet and, in hindsight, looked expensive as the streaming economics soured.2 The transaction became effective in March 2019, with Disney paying $51.57 in cash or 0.4517 Disney shares for each 21st Century Fox share.2 On March 19, 2019, the assets Murdoch chose to keep were spun off into a new, independent public company: Fox Corporation.1

Read the list of what he kept and the strategy is obvious in hindsight. Fox News. Fox Business. The FOX broadcast network. Fox Sports, including the FS1 and FS2 cable channels. The Big Ten Network. And the portfolio of local television stations Fox owns and operates in America's biggest markets. Every one of these assets shares a single trait: it is built on live, unscripted, must-watch-now content that is very hard to replicate and does not compete head-to-head with Netflix's on-demand library. Murdoch had offloaded the capital-hungry, high-risk scripted businesses at what turned out to be near the top of the media cycle, and kept a lean, cash-generative machine that entered life virtually debt-free and structurally insulated from the multi-billion-dollar streaming losses that would soon savage nearly every one of its peers.

Whether that was genius foresight or simply an old mogul's preference for the businesses he understood, the outcome is not in dispute. The question for investors is what that lean machine actually looks like under the hood — and that requires taking the company apart, segment by segment.

III. The Corporate Architecture: Segment Economics & Materiality

If you want to understand Fox, ignore the org chart and follow the money. The company reports in two operating segments plus a corporate bucket, and the profit is distributed among them in a way that is almost comically lopsided. One segment is a fountain of high-margin cash. The other is an enormous revenue pipe that barely keeps its head above water. Understanding why is understanding the whole business.

Start with the crown: Cable Network Programming. This is Fox News, Fox Business, the FS1 and FS2 sports channels, and the Big Ten Network. In fiscal 2025, this segment generated $6.93 billion in revenue and $3.03 billion in segment EBITDA.1 Pause on that margin — roughly 44 cents of profit for every dollar of revenue. In a media industry where a great many "assets" struggle to break even, that is an extraordinary figure. And here is the number that should reframe how you think about the entire company: the cable segment produced roughly 84% of Fox's total segment-level profit. Everything else — the broadcast network, the local stations, the fast-growing streaming service — collectively contributes a minority of the earnings. Fox Corporation is, first and foremost, a cable-news-and-sports profit engine with a broadcast business attached.

Now the contrast: the Television segment. This houses the FOX broadcast network itself, the 29 owned-and-operated local stations, the national Fox Sports broadcasts (the NFL, baseball, college football that air on the big FOX channel), and — importantly — Tubi, the free streaming service. In fiscal 2025 this segment generated $9.33 billion in revenue but only $945 million in segment EBITDA — a margin barely into double digits.1 So the segment that brings in the most revenue produces less than a fifth of the segment profit. Why? Two words: sports rights. When Fox airs an NFL game on the broadcast network, it is paying the league staggering rights fees for the privilege. Those payments are the anchor dragging on the Television segment's margins. The revenue is huge because live sports draws enormous audiences and advertising; the profit is thin because the leagues capture most of the value.

This is the fundamental tension inside Fox, and it is worth sitting with because it drives everything else. The cable segment is where the money is made, but it is tied to the shrinking cable bundle. The television segment carries the crown-jewel sports rights that make the whole bundle worth keeping, but those same rights are so expensive they leave little profit behind. Fox is essentially using the loss-leader economics of broadcast sports to protect the annuity economics of cable — a point we will develop fully when we get to the sports moat.

Then there is the third bucket: Corporate and Other, which posted negative $351 million in EBITDA in fiscal 2025.1 Some of that is ordinary corporate overhead. Some of it is the FOX Studio Lot in Los Angeles, the physical production facility Fox retained. And some of it is Credible, a consumer-finance marketplace Fox bought a 67% stake in back in October 2019 in a rare foray outside its core.17 Credible was reported to have cost around $265 million, and the strategic logic — a fintech growth engine bolted onto a TV company — never really cohered. Today Credible is immaterial to the investment case; it has been effectively de-emphasized and should not be allowed to crowd out the analysis of the core. The honest read is that Fox's one notable diversification attempt has been a footnote, not a pillar — which, given how many media conglomerates have destroyed value chasing shiny objects, is arguably a point in management's favor rather than against it.

So what does the architecture tell an investor? It tells you that valuing Fox is really about valuing one thing: the durability of that $3 billion cable profit stream. If the cable annuity holds, the thin-margin television business and the small-but-growing streaming business are options on top of a very solid base. If the cable annuity cracks, no amount of Tubi growth or buyback engineering fully offsets it. Everything now hinges on a single question — how durable is that cable cash flow, really? That takes us to the crown jewel itself.

IV. The Cable News Crown Jewel & The Carriage Agreement Annuity

On any given weeknight in 2025, more Americans had a Fox News program on their screen than were watching its two largest competitors combined — and it was not close. Across the full 2025 calendar year, Fox News averaged about 2.652 million primetime viewers. Its nearest cable-news rival, the network formerly known as MSNBC, averaged 915,000. CNN averaged 573,000.7 Put differently, Fox News commanded roughly 64% of the combined primetime audience of the three major cable news networks — a share the company noted was its highest since the channel launched in 1996.7 For a business, this is not just a bragging right. Audience dominance of this magnitude is the foundation of pricing power, and pricing power is the whole game.

To see why, you have to understand how a channel like Fox News actually makes money, because it is not primarily what most viewers assume. Fox News runs on two revenue engines. The first is advertising, which is cyclical and lumpy — it swells during election years (Fox's even-numbered fiscal years capture the U.S. political spending surges) and recedes in between. Advertising is the visible revenue, the commercials you see. But it is the second engine that makes cable news one of the best business models in media: the affiliate, or distribution, fee.

Here is the mechanism in plain terms. When you subscribe to a cable, satellite, or internet-TV package — Comcast, DirecTV, or a "virtual" provider like YouTube TV or Hulu + Live TV — a slice of your monthly bill is paid by that distributor to the owners of the channels in the bundle, calculated per subscriber per month. Fox News commands one of the highest per-subscriber fees of any basic-cable channel in America. Estimates from the early 2020s put the figure north of $1.70 per subscriber per month, and it has almost certainly climbed since.18 Now the crucial part: Fox collects that fee for every single subscriber in the bundle, whether or not that person ever tunes in to Fox News. A household that only watches cooking shows still pays the Fox News toll through their cable bill. That is why the affiliate fee is best understood as an annuity — a large, contractually guaranteed, recurring payment stream that arrives regardless of viewing behavior.

Why can Fox charge so much and keep raising the price? This is where Hamilton Helmer's concept of high switching costs applies with unusual force, though the switching cost here sits on the distributor, not the viewer. A cable operator negotiating with Fox faces a brutal asymmetry. If the operator refuses Fox's price and drops Fox News from its lineup, a meaningful chunk of that operator's most loyal, least price-sensitive subscribers — the very audience Ailes built — will cancel their entire subscription and move to a competitor that carries Fox News. The channel is, for a specific and passionate demographic, a must-have. That gives Fox extraordinary leverage at the negotiating table. It is why, even as the total number of pay-TV households falls every year through cord-cutting, Fox has been able to raise its per-subscriber rate fast enough to keep distribution revenue growing. In the quarter ended March 2026, Fox's cable distribution revenue rose about 5%, driven by roughly $64 million more from higher rates that more than offset subscriber declines.9

That last sentence is the entire bull case for the cable segment compressed into one line, and it deserves a skeptic's scrutiny. Rate hikes offsetting volume declines is a treadmill: it works only as long as price increases outrun subscriber losses. There is a mathematical limit — at some point the per-subscriber fee becomes so high, and the remaining subscriber base so small, that distributors simply refuse, or the bundle itself collapses. Management's wager is that Fox News's loyal audience gives it more room to run up that price than almost any other channel. On recent earnings calls, Fox executives have consistently framed carriage renewals as evidence of durable pricing power rather than a temporary reprieve.10 The evidence so far supports them — distribution revenue has kept growing. But "so far" is doing real work in that sentence, and the honest analytical posture is that this is a managed decline with an unknown endpoint, not a permanent annuity.

There is also a live wrinkle in the competitive landscape worth noting, because it cuts in Fox's favor. In November 2025, MSNBC was rebranded "MS NOW" as its parent, Comcast, spun the bulk of its cable networks into a separate public company called Versant, which became independent on January 2, 2026.8 A rebranded, newly independent rival with a shrinking audience is not the sort of competitor that threatens Fox News's pricing power — if anything, it underscores how much stronger Fox's franchise is than its cable-news peers. The real threat to the annuity was never CNN or MSNBC. It is the slow death of the bundle itself, and the one thing keeping that bundle alive alongside news is live sports.

V. The Sports Moat & The Collapse of Venu Sports

Every fall Sunday, tens of millions of Americans do something they do for almost no other content anymore: they watch television live, at a scheduled time, sitting through the commercials, because a game that has not happened yet cannot be binged later. Live sports is the last great appointment-viewing product in America, and Fox has spent enormous sums to own a piece of it. This is the company's second great moat — and in 2024 and 2025, it was also the site of its most public strategic failure.

Start with the moat, which Helmer would call a cornered resource. Sports rights are exclusive by nature: only one broadcaster can hold the NFL's Sunday NFC package at a time, and Fox has locked up its portfolio for years. Fox's NFL rights run through the 2033 season, including a rotation of Super Bowl broadcasts.4 Its Big Ten college football and basketball rights extend through roughly the end of the decade under a seven-year agreement signed in 2022.5 Its Major League Baseball rights, including the World Series, run through the 2028 season.12 These are not commodities anyone can buy; they are contractually cornered, multi-year exclusives, and they are the reason distributors and advertisers keep coming back to Fox.

But here is the paradox at the heart of the sports business, and it is essential to understanding Fox's economics: Fox arguably loses money on the games themselves. The rights fees paid to the leagues are so enormous that the advertising revenue from a given broadcast often doesn't fully cover them. So why do it? Because the value of sports isn't captured on the scoreboard of a single game's P&L — it's captured across the ecosystem. High-priced live sports drive massive audiences to the FOX broadcast network and, crucially, to Fox's local stations. Those local stations then use their must-have programming to charge cable and satellite operators "retransmission" fees for the right to carry the local FOX signal, and they command premium local advertising rates. Sports is the loss leader; the ecosystem is where the money is recaptured. This is why the Television segment can carry billions in sports-rights costs and still be strategically worth it — the sports anchor protects the higher-margin distribution economics elsewhere in the company.

That logic, though, contains an obvious vulnerability: it depends entirely on the traditional bundle continuing to exist. If cord-cutters abandon pay-TV faster than the ecosystem can adapt, Fox is left holding tens of billions in sports-rights obligations with no efficient way to monetize the cord-cutters directly. Fox's management understood this risk, and in 2024 it tried to do something about it — an effort that ended in an embarrassing, instructive collapse.

The plan was called Venu Sports. Announced on February 6, 2024, it was an audacious joint venture in which Fox, Disney's ESPN, and Warner Bros. Discovery would each own a third of a new streaming service that bundled all of their sports channels together and sold it directly to cord-cutters — a "skinny sports bundle" for people who had cancelled cable but still wanted live games. On paper it was a rational response to cord-cutting: meet the cord-cutter where they are. In practice, it walked straight into an antitrust wall. FuboTV, a struggling sports-focused streaming service, sued within two weeks, arguing that three companies controlling much of American sports rights colluding to launch a joint venture was an illegal restraint of trade. In August 2024, a federal judge in New York agreed enough to grant a preliminary injunction blocking Venu's launch.13

What happened next revealed how little conviction the partners truly had. Rather than fight the injunction to the end, the three media giants folded. In early January 2025, Disney reached a broader settlement in which it agreed to combine its Hulu + Live TV business with Fubo, and as part of the peace, Disney, Fox, and Warner Bros. Discovery agreed to pay Fubo an aggregate $220 million. On January 10, 2025, the partners announced they were discontinuing Venu Sports entirely — the service never launched a single day.13 A venture pitched as the future of sports streaming was dead barely eleven months after it was born.

For Fox, the lesson is sobering and the strategic hole is real. Unlike Disney, which has ESPN and its own direct-to-consumer flagship, and unlike Warner, which has Max, Fox emerged from the Venu debacle with no premium sports streaming strategy of its own. Its entire multi-billion-dollar sports-rights portfolio remains dependent on the survival of the linear bundle and broadcast distribution for monetization. Management has since spoken about integrating sports into a broader direct offering, but as of this writing Fox has no standalone premium sports streaming product carrying those NFL and MLB rights to cord-cutters. That is a genuine gap, and a skeptic is right to press on it: if the bundle erodes faster than expected, Fox's sports rights become a stranded, expensive asset rather than a moat. The company's answer to the streaming future does not run through premium sports. It runs, improbably, through free television — which is the next chapter, and the most pleasant surprise in the whole story.

VI. The AVOD Miracle: Benchmarking the Tubi Acquisition

In March 2020, as the world was locking down and media stocks were cratering, Fox quietly announced it was buying a company almost no one on Wall Street took seriously. The price was about $440 million in net cash for Tubi, a free, ad-supported streaming service best known at the time for a deep catalog of older, obscure, and frankly second-tier movies and shows.6 The reaction ranged from indifference to mockery. Fox was passing on the subscription streaming war entirely, the thinking went, and instead of building a prestige Netflix rival, it had bought a digital bargain bin. In hindsight, it may prove to be one of the best capital-allocation decisions in modern media.

To appreciate why, you have to understand the fork in the road that every media company faced around 2019 and 2020. Down one path lay SVOD — subscription video on demand, the Netflix model. Charge consumers a monthly fee; spend astronomically on exclusive premium content to justify it. Disney, Warner, Comcast, and Paramount all took this path, and the collective result was a bonfire of capital: Disney+, Peacock, Paramount+, and Max together burned well over ten billion dollars in cumulative streaming losses as they chased subscribers who churned in and out and never paid enough to cover the content bills. The SVOD model rewards a small number of massive winners and punishes everyone else, and most legacy players were structurally destined to be everyone else.

Down the other path lay AVOD — advertising-based video on demand. The bet here is entirely different. Instead of charging consumers, you give the product away free, monetize it with advertising, and — this is the key — you refuse to enter the content arms race. Tubi's unit economics are built to be the opposite of Netflix's. Rather than spending billions upfront to own exclusive shows, Tubi licenses a vast library of existing content cheaply, frequently on revenue-share terms where content owners get paid a cut of the ads rather than a fat upfront check. That keeps content costs variable and low. On top of that, Tubi runs a proprietary, highly efficient advertising-technology stack that targets ads to viewers and squeezes value from inventory. The result is a streaming service that can actually make money, because it never signed up for the ruinous fixed-cost content spending that defines SVOD.

For years the skeptics could argue Tubi was small and unproven. That argument has gotten much harder to make. In the quarter ended March 2026, Tubi's revenue grew about 23% year over year, and total view time — the aggregate hours audiences spent watching, which is the raw material AVOD converts into ad dollars — climbed roughly 19%.910 More importantly for the doubters, on the Q3 FY26 earnings call management indicated Tubi had reached approximately break-even or better for a third consecutive quarter, with roughly 100 million monthly active users.10 A free streaming service that is growing revenue in the low-twenties percent range and no longer losing money is a genuinely rare object in this industry.

The benchmarking is where the decision looks smartest. Consider Paramount's Pluto TV, a comparable free-streaming asset bought for roughly $340 million, or the multi-billion-dollar cumulative losses at Peacock and Paramount+. Fox spent a fraction of what its rivals spent, avoided the SVOD money pit entirely, and ended up with the fastest-growing asset in its portfolio and a legitimate bridge to a cord-cut future — one that monetizes the same advertising relationships and content-licensing muscle Fox already had. That is what a capital-allocation home run looks like: a small, cheap, contrarian bet that compounds while competitors' expensive bets bleed.

A neutral analyst should still hold two caveats. First, Tubi is profitable at roughly break-even, not gushing cash; it is a promising option, not yet a pillar of earnings, and its contribution sits inside the thin-margin Television segment. Second, AVOD is competitive — Roku, Amazon's Freevee-style efforts, YouTube, and the free tiers of the SVOD giants are all fighting for the same advertising dollars and the same viewing hours. Tubi's growth is real and its economics are sound, but its long-term margin ceiling is still being discovered. What is no longer in doubt is that Fox found a genuine digital growth engine without betting the company to get it — which is exactly the kind of discipline that shows up, most visibly, in what Fox does with the cash the whole machine produces.

VII. Capital Deployment & The Buyback Machine

Most media companies, handed a few billion dollars of annual free cash flow, cannot resist spending it. The industry's history is a graveyard of empire-building acquisitions, overpriced content deals, and diversification adventures that destroyed shareholder value in the name of "strategic transformation." Fox, under Executive Chair and Chief Executive Lachlan Murdoch, has done something almost radical by the standards of its peers: it has largely declined to play. Instead of chasing transformative M&A, Fox has concluded that the best investment available to it is its own stock — and it has bought that stock back on a scale that is reshaping the company's per-share math.

The logic runs like this. Fox's management views the shares as chronically undervalued, weighed down by a "conglomerate discount" and by the market's justified fear of cord-cutting. If that view is right, then buying back stock below intrinsic value is the highest-return use of capital the company can find — better than acquisitions that would require paying a premium for someone else's declining assets, and better than hoarding cash. So Fox has turned itself into a share-shrinking machine.

The numbers tell the story. In August 2025, Fox's board increased the company's cumulative share repurchase authorization to $12 billion — reflecting an incremental $5 billion added on top of prior authorizations — and raised the semi-annual dividend to $0.28 per share.1 Then, in a particularly aggressive move, Fox announced it would enter a $1.5 billion accelerated share repurchase beginning October 31, 2025, split $700 million against the Class A shares and $800 million against the Class B shares, with completion expected in the back half of fiscal 2026.11 An accelerated share repurchase, for the uninitiated, is a way to retire a large block of shares immediately — the company pays an investment bank upfront and receives most of the shares right away, front-loading the buyback rather than dribbling it out over time.

Across fiscal 2025 as a whole, Fox returned roughly $1.25 billion to shareholders through dividends and repurchases, bought back around $1 billion of stock, retired $600 million of debt, and still ended the year with about $5.4 billion of cash on the balance sheet.1 That combination — returning capital, reducing debt, and maintaining a large cash cushion simultaneously — is the signature of a business generating far more cash than it needs to run itself.

Here is why the buyback matters strategically, and it is subtle. Fox operates in a world where absolute revenue may be flat to slowly declining as cord-cutting grinds on. In that environment, growing earnings per share through the top line is hard. But earnings per share has a denominator, and Fox is systematically shrinking it. By retiring a meaningful percentage of its shares each year, Fox can deliver double-digit growth in adjusted earnings per share even when total profits are merely holding steady — because the same profit is divided across fewer shares. It is financial engineering, yes, but it is honest financial engineering: the company is genuinely returning cash it cannot productively reinvest, rather than manufacturing accounting earnings.

The activist-style question a skeptic should ask is whether this is capital discipline or capital surrender. Buying back stock aggressively is the right move if the shares are cheap and the core business is durable. It is a value trap if management is simply harvesting a melting ice cube — returning cash while the underlying earnings power quietly erodes beneath the per-share optics. The bull says Fox is buying a durable annuity at a discount and compounding it. The bear says Fox is liquidating a declining business one share at a time and calling it a strategy. The truth depends entirely on how long the cable annuity holds — and that, in turn, depends on who controls the company and what they choose to do with it, which brings us to the most dramatic chapter of the whole story.

VIII. Governance & Succession: The Nevada Trust Wars

In September 2024, in a closed courtroom in Reno, Nevada, one of the wealthiest and most powerful families in the Western world sat down to fight each other in front of a probate commissioner. The patriarch, then 93 years old, was on one side with his eldest son. His three other adult children were on the other. At stake was not merely a fortune — it was editorial and strategic control of Fox News, The Wall Street Journal, and a media empire that helps shape the politics of the English-speaking world. To understand why the Murdoch family ended up litigating against itself, you first have to understand the unusual share structure that concentrates control in so few hands.

Fox Corporation, like News Corp, has a dual-class share structure. The publicly traded Class A shares — the FOXA that most investors own — carry essentially no voting rights. The Class B shares — FOX — carry the votes. And the Murdoch Family Trust controls a decisive block of those Class B voting shares, historically around 39–40% of the voting power.12 In plain terms: the family, through the trust, controls Fox regardless of what outside shareholders think. Public investors in the Class A stock are, by design, passengers. This is a governance reality with real consequences — it means the usual disciplining mechanisms of the market, activist investors, hostile bids, proxy fights, are essentially neutralized. You are betting on the family.

The trust itself was the problem. Under its original terms, upon Rupert Murdoch's death, voting control would pass in equal measure to his four eldest children: Lachlan, James, Elisabeth, and Prudence. And therein lay Rupert's fear. Lachlan shares his father's conservative editorial vision for Fox News. But James in particular had grown publicly critical of the network's direction, and Rupert reportedly worried that after his death, the other three siblings could outvote Lachlan, moderate Fox News's editorial stance, or even force a sale — destroying, in Rupert's view, both the company's distinctive political brand and its financial value.

So in 2024, Rupert made his move. He attempted to amend what was supposed to be an irrevocable trust, to grant Lachlan sole, permanent voting control of the empire — locking in his chosen successor and disenfranchising the other three children's votes, reportedly through 2050. The maneuver triggered the Nevada probate battle. And in December 2024, the family's own hand-picked forum ruled against them. Probate Commissioner Edmund J. Gorman Jr., in a scathing 96-page opinion, found that Rupert and Lachlan had acted in "bad faith," and characterized the whole effort as a "carefully crafted charade" designed to "permanently cement Lachlan Murdoch's executive roles."1415 It was a stunning judicial rebuke of a sitting media titan's succession plan.

Had the story ended there, the outline's original fear — that Rupert's death would trigger an immediate boardroom civil war between Lachlan and his siblings — would be the dominant risk hanging over the stock. But the story did not end there, and this is where an up-to-date reading matters enormously. Rather than pursue years of appeals with an uncertain outcome, the family bought its way to peace. On September 8, 2025, the Murdochs announced a comprehensive settlement worth roughly $3.3 billion. James, Elisabeth, and Prudence would each receive approximately $1.1 billion and exit their positions in Fox and News Corp entirely, selling their stakes and agreeing not to buy back in. A new family trust would consolidate voting control of both companies under Lachlan — reportedly secured through at least 2050 — with his younger half-sisters Grace and Chloe as beneficiaries.16

For investors, the settlement fundamentally rewrites the governance risk, and it is important to be precise about how. The bad news the outline anticipated — an unresolved succession that erupts into a control fight the moment Rupert dies — has largely been defused. Lachlan's control is now contractually locked in, the dissenting siblings are gone, and the strategic continuity of the company (cash-focused, buyback-driven, editorially unchanged) is essentially guaranteed for the foreseeable future. That removes a major overhang.

But it replaces one risk with another, subtler one, and a neutral analyst should name it clearly. First, the settlement crystallized an enormous cash cost to resolve a family dispute, and while it was funded at the trust level rather than by the company directly, the episode is a vivid reminder that this is a controlled company run for the family's purposes, where minority Class A holders have no seat at the table. Second, having eliminated internal dissent, Fox's strategy is now entirely a function of one man's judgment. Concentration of control cuts both ways: it delivers stability and continuity, but it also means there is no internal check on Lachlan Murdoch if his capital allocation, editorial, or strategic decisions prove wrong. The market has traded the risk of chaos for the risk of unaccountable single-person control. Whether that is an improvement depends on what you think of the person — and on a set of legal liabilities the family cannot settle away, which are the next order of business.

IX. The Defamation Overhang & Risk Radar

On the morning of April 18, 2023, in a courthouse in Wilmington, Delaware, jury selection was underway and opening statements were hours from beginning. Rupert Murdoch, his son Lachlan, and a lineup of Fox News's biggest primetime hosts were on the witness list, facing the prospect of testifying under oath about what they knew, and when, regarding false claims of election fraud aired on their network. And then, abruptly, it was over. Fox settled with Dominion Voting Systems for $787.5 million — the largest known defamation settlement in American media history — to make the trial, and the spectacle of its stars on the stand, disappear.[^18]

The Dominion settlement is a closed chapter, but it established two things that matter going forward. The first is that Fox's exposure to defamation liability arising from its 2020 election coverage is not theoretical — it is quantified, and it is very large. Three-quarters of a billion dollars is real money even for a company throwing off billions in cash. The second is that Fox demonstrably preferred to pay an enormous sum rather than let its most senior people testify publicly, which tells you something about how the company weighs reputational and legal risk when the two collide.

And the Dominion case, expensive as it was, may not be the biggest of these liabilities. The larger overhang is Smartmatic, another voting-technology company defamed in the same post-2020-election coverage. Smartmatic's suit seeks $2.7 billion in damages — several times the Dominion figure — and unlike Dominion, it has not settled.[^19] The case remains active in the New York courts, grinding through summary-judgment motions and discovery disputes. Smartmatic has repeatedly accused Fox of spoliation — the destruction or deletion of evidence, including communications — which, if a court credits it, can lead to severe sanctions and adverse inferences at trial. As of this writing, no trial date has produced a verdict, and the ultimate liability is genuinely unknowable: it could be settled for a fraction of the demand, or it could produce a headline judgment. What is certain is that it hangs over the company as a material, unresolved contingent liability that no amount of operational excellence can neutralize. A skeptical investor is right to treat it as a real, if unquantifiable, claim against the balance sheet and the buyback program.

Beyond the courtroom, three structural risks define the radar for Fox, and it is worth being disciplined about which ones actually matter.

The first and most severe is secular cord-cutting. This is not a macro abstraction; it is the direct mechanism by which Fox's highest-margin revenue erodes. Every household that cancels pay-TV is one fewer subscriber generating an affiliate fee, and the entire cable-segment cash engine depends on Fox raising per-subscriber rates faster than the subscriber base shrinks. If the pace of cord-cutting accelerates beyond Fox's ability to raise prices, the pricing floor breaks and the most valuable profit stream in the company compresses. This is the single biggest threat to the entire investment case, and it is not a question of if but of how fast.

The second is sports-rights inflation. The leagues hold the whip hand. Every renewal cycle, the NFL, the college conferences, and MLB extract more, and Fox faces a punishing choice: pay ever-higher fees to keep the must-watch content that anchors the bundle, or let it walk and watch the ecosystem unravel. If rights costs keep climbing while the audience that monetizes them keeps shrinking, the thin margins of the Television segment could be squeezed toward zero. Fox's long-term rights deals lock in cost as much as they lock in the moat.

The third, and more speculative, is generative AI and content scraping. AI platforms increasingly ingest live news and video content to train models and answer user queries, often without licensing agreements, potentially disintermediating the original publisher's relationship with the audience. For a news organization, this is a medium-term risk to the value of its journalism and its traffic. It is real, but it is not yet material to Fox's economics in the way cord-cutting and rights inflation are, and it should be weighted accordingly rather than hyped.

Having laid out both the moats and the threats, it is time to put them in a formal framework and stage the argument between the optimists and the skeptics.

X. Playbook: Business, Strategy, & Industry Analysis

Strip away the family drama and the courtroom headlines, and Fox is ultimately a case study in competitive advantage — where it is real, where it is overstated, and where it is eroding. Two analytical frameworks help war-game the business: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces. Neither is gospel, but together they discipline the argument.

Hamilton Helmer's 7 Powers Applied to Fox

High Switching Costs (Strong). This is Fox's most durable power, and it operates on the distributor rather than the consumer. A pay-TV operator cannot drop Fox News or a local FOX broadcast affiliate without risking a cascade of subscriber cancellations from viewers who consider those channels non-negotiable. That fear is what lets Fox raise per-subscriber carriage and retransmission rates year after year, and it is the primary engine of the cable segment's roughly 44% margins.1 The power is strong, but note its dependency: it protects Fox's share of a shrinking pie, not the size of the pie itself.

Cornered Resource (Strong, but expensive). Two assets qualify. One is Fox's exclusive, multi-year sports rights — most importantly the NFL through 2033 — which no competitor can replicate because exclusivity is contractual.4 The other is subtler and arguably more valuable: the Fox News brand and its uniquely loyal conservative audience, a franchise built over nearly three decades that competitors have repeatedly failed to dislodge. The distinction matters for investors: the sports resource is cornered but rented at ever-rising prices, so its economic value depends on the bundle surviving; the Fox News audience is cornered and largely owned, which is why it is the higher-quality asset of the two.

Scale Economies (Moderate). Tubi is the clearest example. By aggregating a large free audience, Tubi assembles ad inventory at a scale that lets it offer advertisers targeted reach efficiently, spreading its fixed ad-tech costs across a growing base of viewing hours. This is a genuine but still-developing advantage, and it operates in a crowded AVOD market where several larger players enjoy their own scale. Moderate, not dominant.

The powers Fox conspicuously lacks are worth stating too. It has no network economies of the kind that make a subscription platform stickier as it grows — Fox deliberately opted out of that game. And it has no counter-positioning advantage against streaming; if anything, streaming is counter-positioned against it. Fox's edge is concentrated, not diversified.

Porter's Five Forces Analysis

Bargaining Power of Suppliers (Very High). The sports leagues are the suppliers from hell, in economic terms. The NFL, the Big Ten, and MLB hold scarce, must-have content and auction it to multiple deep-pocketed bidders, capturing the lion's share of the value. Every rights renewal transfers economics from Fox to the league. This is the force that most directly caps the Television segment's profitability.

Bargaining Power of Buyers (High). Fox's direct customers, the pay-TV distributors, are consolidating and cost-pressured, which strengthens their hand in carriage negotiations. The countervailing force is Fox's switching-cost power — the distributor needs Fox News more than Fox needs any single distributor — but the buyers are not powerless, and each renewal is a genuine fight.

Threat of Substitutes (Very High). This is the existential force. Netflix, YouTube, TikTok, gaming, and every other claim on attention pull eyeballs away from linear television structurally and permanently. Cord-cutting is the substitution threat made manifest. No amount of Fox's within-industry strength neutralizes the fact that the industry itself is being substituted away.

Threat of New Entrants (Very Low). Here Fox is well protected. The capital and relationships required to build a national broadcast network, assemble a live-sports rights portfolio, or create a trusted news brand with a devoted audience are effectively insurmountable. No one is launching a new Fox News. The barriers that protect Fox from newcomers are as high as any in media.

Competitive Rivalry (Moderate). Within cable news, Fox faces rivals in structural decline — the rebranded MS NOW and CNN are both shedding audience, leaving Fox with something close to a monopoly on the conservative-news viewer.7 Within sports, rivalry for rights is fierce, but that shows up as supplier power, not head-to-head margin competition. On balance, Fox's direct rivalry is less threatening than the substitution force that is shrinking the whole arena.

The synthesis is this: Fox has strong, real competitive advantages inside its industry, and almost no defense against the decline of its industry. It is winning a game on a field that is slowly being paved over. That tension is exactly what the bull and bear cases fight over.

XI. The Stress Test: Bull vs. Bear Case

Every investment thesis is an argument with itself. Here is Fox's, staged as honestly as the evidence allows.

The Bull Case

The bull case rests on three pillars, and each has evidence behind it. The first is last man standing. As the cable bundle shrinks, the channels that survive to the very end will be the ones subscribers refuse to give up — and Fox News and live sports are precisely those channels. In a consolidating bundle, Fox's relative importance actually rises, because it becomes a larger share of the reason anyone keeps the subscription at all. That gives Fox the pricing power to keep extracting premium carriage fees from a shrinking base for years, and the recent 5% growth in cable distribution revenue is direct evidence the mechanism still works.9

The second pillar is Tubi as a multi-billion-dollar option. Fox has, almost uniquely among legacy media, a fast-growing streaming asset that makes money rather than losing it. Roughly break-even and compounding revenue in the low-twenties percent range, Tubi is a self-funded bridge to the cord-cut future that cost Fox a fraction of what rivals spent to lose money.910 If AVOD is where advertising-supported television is ultimately heading, Fox owns a leading position that the market arguably under-values.

The third pillar is the buyback flywheel. By returning capital and systematically shrinking its share count, Fox converts a flat-to-declining absolute business into growing per-share earnings — and if the shares are genuinely cheap, every buyback compounds value for the holders who remain. Combined with the newly settled governance structure, the bull sees a disciplined, cash-focused company with a clear owner and a clear plan.

The Bear Case

The bear case is equally coherent, and it targets the same facts from the other side. The first threat is the sudden cord-cutting cliff. The entire bull case assumes cord-cutting stays gradual enough that price increases can outrun it. But subscriber declines are not guaranteed to be linear — a tipping point, where the bundle unravels and distributors finally resist further rate hikes, could cause the high-margin cable EBITDA to collapse faster than any buyback can offset. The pricing floor is an assumption, not a law.

The second threat is the Smartmatic verdict. A multi-billion-dollar judgment or settlement in the still-active $2.7 billion suit could force Fox to divert cash from buybacks, draw down its reserves, and absorb a reputational blow — a single adverse legal outcome that no amount of operational discipline can prevent.[^19] It is the definition of a fat-tail risk.

The third threat, the bear's classic "boardroom civil war," has been substantially neutralized by the September 2025 family settlement, and intellectual honesty requires saying so — the succession that once looked like a time bomb is now contractually resolved in Lachlan's favor.16 But the risk did not vanish; it transformed. The residual concern is concentration: with dissent bought out, Fox's fate now rests entirely on one controlling shareholder's judgment, with no internal check and minority holders along for the ride. The bear simply relocates the governance risk from "chaos after Rupert" to "unaccountable control by Lachlan."

Key KPIs to Track

For an investor following this story quarter to quarter, three metrics carry most of the signal. The first is Cable Network Programming distribution revenue growth — as long as it stays positive, the core annuity is intact and price is beating volume; the quarter it turns negative and stays there, the central thesis is breaking. The second is Tubi's total view time and its path to sustained profitability — the leading indicator of whether the digital bridge is real and scaling. The third is the annual reduction in the outstanding share count — the buyback velocity that translates a flat business into per-share growth. Watch those three, and you are watching the whole company.

XII. Outro & Epilogue

There is a version of the last decade in media where the smartest thing you could do was refuse to be smart in the way everyone else was. While an entire industry convinced itself that the only path forward was to spend whatever it took to build a Netflix rival, Rupert Murdoch sold his entertainment empire near the top, kept the handful of assets that people still watch live, and built a company designed not to win the streaming war but to sit it out profitably. Fox did not chase subscribers. It milked the cable annuity, bought a free streaming service for pocket change, and handed the cash back to its owners.

The ultimate lesson of Fox Corporation is that knowing which game not to play can be worth more than playing the popular game well. That is a genuine strategic insight, and the results — durable cash flow, real margins, a rare profitable streaming asset, a shrinking share count — validate it so far. But "so far" remains the operative phrase. Fox is a superbly run business riding a structurally declining product, protected by real moats that guard its share of a shrinking market, and now controlled, absolutely, by a single family whose members recently paid $3.3 billion to stop fighting each other. It is resilient, it is disciplined, and it is dependent on the linear bundle lasting long enough for the strategy to pay out. Whether that is a fortress or a very well-managed melting ice cube is the question every investor in FOXA is ultimately being asked to answer — and the honest truth is that the answer will be written in the pace of cord-cutting, the outcome of a courtroom in New York, and the judgment of one man in Los Angeles.

References

-

Fox Reports Fourth Quarter and Full-Year Fiscal 2025 Results — Fox Corporation / PR Newswire, 2025-08-05 ↩↩↩↩↩↩↩↩↩

-

Disney and 21st Century Fox Announce Per Share Value in Connection with $71 Billion Acquisition — The Walt Disney Company, 2019-03-19 ↩↩↩

-

NFL Completes Long-Term Media Distribution Agreements Through 2033 Season — NFL.com, 2021-03-18 ↩↩

-

Big Ten Completes 7-Year, $7 Billion Media Rights Agreement with Fox, CBS, NBC — ESPN, 2022-08-18 ↩

-

Fox Corporation to Acquire Tubi — Fox Corporation / PR Newswire, 2020-03-17 ↩↩

-

Fox News Channel Delivers Highest-Rated Non-Election Year in Network History — Fox News Media, 2025-12 ↩↩↩

-

MSNBC to Change Name to MS NOW Ahead of NBCUniversal Spinoff — NBC News, 2025 ↩

-

Fox Reports Third Quarter Fiscal 2026 Results — Fox Corporation / PR Newswire, 2026-05-11 ↩↩↩↩

-

Fox (FOXA) Q3 2026 Earnings Call Transcript — The Motley Fool, 2026-05-11 ↩↩↩↩

-

Fox Reports First Quarter Fiscal 2026 Results — Fox Corporation / PR Newswire, 2025-11-04 ↩

-

Fox Corporation Form 10-K for the Fiscal Year Ended June 30, 2025 — SEC EDGAR ↩↩

-

Disney, WBD, Fox Pull Plug on Venu Sports Streaming Service Before Launch — CNN Business, 2025-01-10 ↩↩

-

Report: Nevada Judge Rules Against Rupert Murdoch's Bid to Alter Family Trust — Las Vegas Review-Journal, 2024-12-09 ↩

-

Rupert Murdoch's Attempt to Rewrite the Family Trust Failed — Entrepreneur, 2024-12 ↩

-

Lachlan Murdoch Snares Voting Control of Fox, News Corp in Family Settlement — Variety, 2025-09-08 ↩↩

-

Fox Corporation Completes Acquisition of 67% of Equity of Credible Labs — Fox Corporation, 2019-10-17 ↩

-

Thanks to Crappy Cable Bundles, Non-Watchers Hugely Subsidize Fox News — Techdirt, 2021-04-29 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube