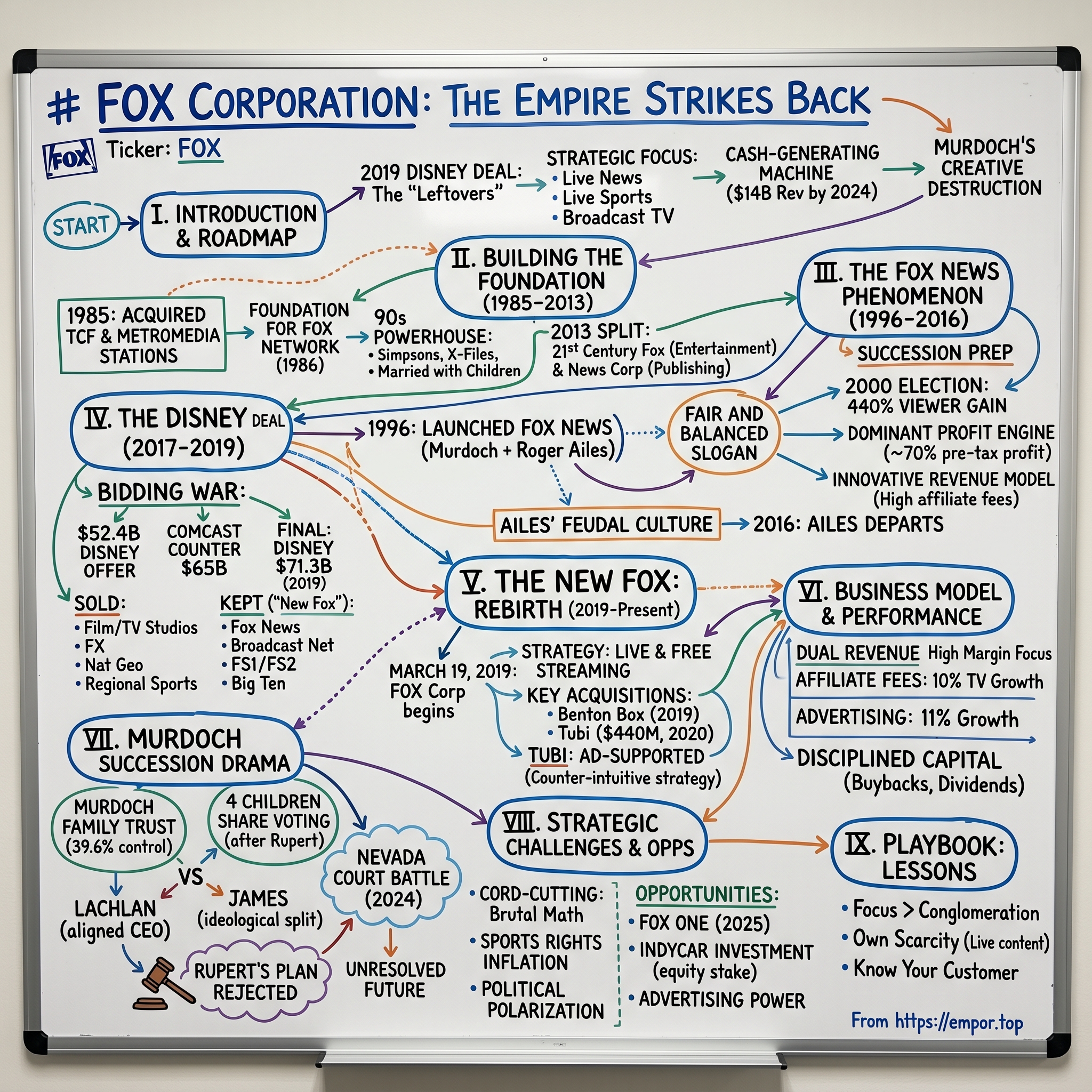

Fox Corporation: The Empire Strikes Back

I. Introduction & Episode Roadmap

Picture this: March 19, 2019. While most of Hollywood celebrated Disney's acquisition of 21st Century Fox's entertainment assets—a $71 billion mega-deal that reshaped the media landscape—Rupert Murdoch stood in the Fox News headquarters in Manhattan, surveying what remained. The "leftovers," as some Wall Street analysts dismissively called them. A collection of broadcast stations, cable news channels, and sports rights that Disney didn't want or couldn't take due to regulatory concerns.

Yet here's the twist: those leftovers would generate nearly $14 billion in revenue by 2024, with profit margins that make streaming giants weep with envy. The new Fox Corporation, stripped of its Hollywood glamour, emerged as a focused, cash-generating machine built on three pillars that Silicon Valley can't easily disrupt: live news, live sports, and broadcast television.

The central question isn't how the Murdochs lost their empire—it's how they transformed a forced divestiture into strategic focus. This is the story of creative destruction in reverse: instead of a startup disrupting an incumbent, we witness an 88-year-old media mogul dismantling his own conglomerate to create something leaner, meaner, and paradoxically more valuable per dollar of revenue than the sprawling empire it replaced.

We'll journey from Murdoch's 1985 acquisition of Twentieth Century Fox through the rise of Fox News as America's most profitable news operation, navigate the Disney deal negotiations that saw the Murdochs extract maximum value at the peak of content valuations, and examine how the "new" Fox became a case study in the power of focus over diversification. Along the way, we'll explore the family succession drama that reads like a real-life HBO series, the strategic bet on live programming when everyone else chased on-demand, and the financial engineering that returned billions to shareholders while competitors burned cash on streaming wars.

This isn't just a media story—it's a masterclass in knowing when to hold, when to fold, and when to completely reinvent the game.

II. The Murdoch Media Empire: Building the Foundation (1985–2013)

The boardroom at News Corporation's Manhattan headquarters hummed with tension in early 2013. Rupert Murdoch, then 82, stood before a whiteboard covered with corporate structure diagrams, circles and arrows mapping out what would become one of the most consequential reorganizations in media history. His lieutenants watched as he drew a bold line down the middle—on one side, newspapers and publishing; on the other, entertainment and television. "Sometimes," he said, turning to face the room, "you have to destroy your empire to save it."

This moment represented the culmination of nearly three decades of empire-building that began with Murdoch significantly expanding his interests in the film and television industry when he took ownership of Twentieth Century Fox as well as a number of regional television stations in 1985. That acquisition wasn't just another deal—it was Murdoch's declaration of war on the American media establishment.

The path to that transformative 1985 acquisition began with typical Murdochian audacity. Murdoch announced he had agreed to purchase 50 percent of the holding company that controls Twentieth Century Fox Film Corp, initially partnering with oil magnate Marvin Davis. But partnerships were never Murdoch's style. In December 1985, Rupert Murdoch agreed to pay $325 million to acquire the remaining equity in TCF Holdings from his original partner, Marvin Davis, taking full control of the storied Hollywood studio.

The real genius move came simultaneously. In May 1985, News agreed to pay $2.55 billion to acquire independent stations in six major U.S. cities from the John Kluge-run broadcasting company Metromedia. These weren't just any stations—they were in New York, Los Angeles, Chicago, Washington D.C., Houston, and Dallas. The foundation for what would become America's fourth broadcast network was being laid, brick by brick.

To pull this off, Murdoch made the ultimate commitment: On 4 September 1985, Murdoch became a naturalized citizen to satisfy the legal requirement that only American citizens were permitted to own American television stations. The Australian-born mogul literally changed his citizenship to conquer American media—a move that shocked his countrymen but demonstrated his absolute determination to build a global empire.

The FOX Television Stations group was created, comprised of 25 stations across the U.S. that became the foundation for the launch of FOX Broadcasting Company in 1986. This historical development would not only reshape network television, but pave the way for the groundbreaking NFL broadcasting rights deal that would later become central to Fox's identity.

The new network faced skepticism from every corner. CBS, NBC, and ABC had dominated American television for decades. Who was this Australian newspaper baron to challenge them? Fox survived where DuMont and other attempts to start a fourth network had failed because it programmed just under the number of hours defined by the FCC to legally be considered a network. This allowed Fox to make revenue in ways forbidden to the established networks—classic Murdoch, finding the loopholes and exploiting them brilliantly.

By the 1990s, Fox had transformed from upstart to powerhouse. By 1996, the FOX network was the top-ranked television group in the country, a position it held for a record eight consecutive years, powered by cultural phenomena like "The Simpsons," "The X-Files," and "Married with Children." These weren't just shows—they were countercultural statements, deliberately edgier than anything the traditional networks would touch.

But Murdoch's most prescient move in this era was launching Fox News Channel on October 7, 1996. While the entertainment division grabbed headlines with its irreverent programming, Fox News would quietly become the profit engine that would define the company's future—a story we'll explore in depth in the next chapter.

The empire continued expanding globally. Murdoch acquired prestigious newspapers like The Times of London, built satellite television networks across Europe and Asia, and in 2007, Mr. Murdoch led News Corporation's acquisition of Dow Jones, including The Wall Street Journal in a landmark deal. Each acquisition wasn't just about adding assets—it was about building leverage, creating synergies, and accumulating political and cultural influence.

By 2012, News Corporation had become a sprawling colossus, but cracks were showing. The phone-hacking scandal at News of the World had damaged the company's reputation. More fundamentally, the conglomerate structure was becoming unwieldy. Entertainment assets needed massive capital investments to compete with tech giants entering content production. Publishing assets faced secular decline but still generated cash. The two sides of the empire were pulling in opposite directions.

It was formed on June 28, 2013, as the legal successor to News Corporation, while the second News Corporation was formed the same day as a spin-off. The split created two companies: 21st Century Fox would house the entertainment assets, while a new News Corporation would contain publishing and Australian broadcasting properties. The second News Corporation, which is doing business as News Corp, was spun off from the first News Corporation and holds Rupert Murdoch's print interests and other media assets in Australia.

This wasn't defeat—it was strategic repositioning. By separating the businesses, Murdoch gave each the focus and capital structure it needed to thrive in rapidly changing markets. The entertainment assets could pursue expensive content strategies without being dragged down by newspaper economics. The publishing business could manage its transition without the volatility of Hollywood.

The split also resolved a deeper issue: succession. Murdoch was co-executive chairman, while his sons Lachlan Murdoch and James Murdoch were co-executive chairman and CEO, respectively of 21st Century Fox. The restructuring gave each son a clearer path forward, though as we'll see, this merely postponed rather than resolved the family power struggle.

What emerged from this split was a leaner, more focused 21st Century Fox, ready for the battles ahead. The company retained its movie studio, television production capabilities, cable networks including FX and National Geographic, regional sports networks, and crucially, Fox News, Fox Broadcasting, and Fox Sports. These assets would soon attract the attention of bigger predators in the media jungle, setting the stage for the next chapter in the Murdoch saga.

As we'll discover, the 2013 split wasn't the end of empire—it was preparation for an even more dramatic transformation that would see the Murdochs sell their crown jewels while somehow emerging stronger than ever.

III. Roger Ailes & The Fox News Phenomenon (1996–2016)

The scene at CNBC's Fort Lee, New Jersey headquarters in February 1996 was tense. It was way back in February 1996 that, at the behest of News Corp. chieftain Rupert Murdoch, Ailes began creating from scratch an all-news network to challenge the venerable CNN as well as upstart MSNBC, which was set to launch that July. Roger Ailes had just abruptly resigned as president of CNBC and creator of America's Talking after NBC executives decided to shut down his creation to make room for MSNBC—a partnership with Microsoft that Ailes hadn't been consulted about. The betrayal stung. But within days, Ailes would receive a phone call that would change American media forever.

Ailes was hired by News Corp chairman Rupert Murdoch in 1996 to become the CEO of Fox News, a position that would allow him to build something NBC had denied him: complete control over a news operation. In February 1996, after former U.S. Republican Party political strategist and NBC executive Roger Ailes left cable television channel America's Talking (now MSNBC), Murdoch asked him to start Fox News Channel.

The partnership between Murdoch and Ailes was electric from the start. Murdoch found Ailes captivating: powerful, politically connected, funny as hell. Both men had been married twice, and both shared an open contempt for the traditional rules of journalism. They weren't just building a news network—they were mounting an assault on what they saw as the liberal media establishment.

Ailes brought a showman's instinct honed from years producing The Mike Douglas Show and crafting media strategies for Nixon, Reagan, and George H.W. Bush. He understood television at a molecular level—not as journalism, but as theater. Ailes, who calls himself "a television producer by trade" and understands TV in his bones as well as anyone alive, knew that news could be entertainment if packaged correctly.

The channel was created by Australian-born American media mogul Rupert Murdoch, who hired Roger Ailes as its founding CEO. The channel was launched on October 7, 1996 to 17 million cable subscribers. But those numbers were deceptive—Fox News wasn't available in New York or Los Angeles at launch. Critics had to watch the debut programming at Fox's studios because they couldn't get it at home.

The early days were scrappy. Ailes worked his team through 14-hour days and weeks of rehearsal shows before launch. The programming was deliberately different—louder graphics, more opinion, prettier anchors. Fox News Channel originally used the slogan "Fair and Balanced", which was coined by network co-founder Roger Ailes while the network was being established. The New York Times described the slogan as being a "blunt signal that Fox News planned to counteract what Mr. Ailes and many others viewed as a liberal bias ingrained in television coverage by establishment news networks".

The breakthrough moment came with the 2000 presidential election. In the 2000 presidential election, Fox News, which was available in 56 million homes nationwide, saw a staggering 440% increase in viewers, the biggest gain among the three cable news television networks. This wasn't just growth—it was validation of Ailes' thesis that millions of Americans felt unrepresented by mainstream media.

The financial implications were staggering. While CNN charged cable operators for carriage, When News Corporation chairman Rupert Murdoch started the conservative cable Fox News network in 1996 and hired Ailes to run it, Fox had to pay operators up to $11 per subscriber at the time, a departure from normal practices. But Ailes' programming magic flipped the script. Within five years, it had eclipsed rival CNN in the ratings and went on to become the number one ranked cable news network for over a decade.

By the mid-2000s, Fox News had become something unprecedented: a news network that was also a profit machine. Since 2002, Fox News has sealed the deal as ratings leader, dominating cable-news competition (and tying them in knots) in daytime, as well as in prime time with a murderers' row of hosts led by Bill O'Reilly and Sean Hannity. The past year, Fox News Channel drew an average 1.1 million viewers -- more than CNN and MSNBC combined.

The economics were revolutionary. Cable subscribers pay roughly 89 cents month for the Fox News Channel, according to a 2012 estimate by research firm SNL Kagan. CNN was estimated to average 57 cents per subscriber and MSNBC just 18 cents. Fox News commanded premium pricing because cable operators couldn't afford to lose it—their conservative subscribers would revolt.

In turn, the channel delivered massive returns for shareholders. Up until Ailes's departure, the company was responsible for 20 percent of parent company 21st Century Fox's operating income, a jewel in the crown. This wasn't just successful programming—it was the most profitable news operation in television history.

Ailes achieved this by understanding his audience better than anyone. "Ailes understood how to program to people's underlying psychology," said Michael J. Wolf, CEO of consulting firm Activate. "It was the first-ever designed news program that appealed to the things people are worried about. Were they going to be safe? Was the economy going to be safe?"

The talent strategy was equally brilliant. Ailes quickly established Fox News as a legitimate presence by luring top talent, including CNBC business anchor Neil Cavuto, former ABC White House Correspondent Brit Hume and former Inside Edition anchor Bill O'Reilly. These weren't just hires—they were brand statements. Each personality reinforced Fox's positioning as the insurgent truth-teller against the establishment.

But the very culture that made Fox News successful contained the seeds of Ailes' downfall. The hypermasculine, combative environment that Ailes cultivated extended beyond the on-air product. In July, former Fox News anchor Gretchen Carlson filed a sexual harassment lawsuit against Ailes, alleging she had been fired for spurning his advances. Several other women stepped forward with similar claims in the following days, and although Ailes vehemently denied any wrongdoing, he agreed to a settlement with Fox and announced his resignation on July 21.

The revelations about Ailes were shocking but, in retrospect, unsurprising. The man who had built the most powerful conservative media platform in America had operated like a feudal lord, demanding loyalty and, according to numerous accusers, much more. But the allegations of sexual abuse against Ailes could not be covered up, despite his denials. Once the Murdoch family hired a law firm and started looking around, they found evidence of misconduct everywhere.

In July 2016, he left Fox News after allegations of sexually harassing female Fox employees, including on-air hosts Gretchen Carlson, Megyn Kelly, and Andrea Tantaros. The departure of Ailes marked the end of an era, but the machine he built was too powerful, too profitable to dismantle.

What Ailes had created was more than a news network—it was a political force that reshaped American discourse. Research finds that Fox News increases Republican vote shares and makes Republican politicians more partisan. A 2007 study, using the introduction of Fox News into local markets (1996–2000) as an instrumental variable, found that in the 2000 presidential election "Republicans gained 0.4 to 0.7 percentage points in the towns that broadcast Fox News".

The financial legacy was equally transformative. It is the most-watched cable news network in the U.S., and as of 2023 it generates approximately 70% of its parent company's pre-tax profit. This single cable channel had become the profit engine for one of the world's major media companies—a testament to Ailes' vision of news as both influence and income.

As we'll explore in the next chapter, this incredible profit machine would become central to the Murdochs' strategic calculations when Disney came calling. The question wasn't whether Fox News was for sale—it was whether the Murdochs could afford to sell it.

IV. The Disney Deal: Selling the Crown Jewels (2017–2019)

Bob Iger's phone rang at an unusual hour on a November morning in 2017. On the other end was Rupert Murdoch, calling from his vineyard estate in Bel Air. "Bob," the elder mogul said, "I think we should talk." Those five words would set in motion the largest media acquisition in history and fundamentally reshape the entertainment landscape. According to Disney CEO Bob Iger, the idea of purchasing 21st Century Fox's assets came after Disney acquired majority control of the streaming company BAMTech with anticipation to develop its own streaming service, which would eventually launch as Disney+.

The irony was delicious: Murdoch, who had spent decades building an empire by acquiring distressed assets and turning them into profit machines, was now the seller. The hunter had become the hunted, not out of weakness but from a clear-eyed assessment of the future. For Fox, the decision to sell was motivated by what insiders described as "fear, opportunity and pragmatism"—fear of Netflix and Amazon's seemingly unlimited wallets, opportunity to cash out at what might be peak valuations, and pragmatism about the divergent visions of Murdoch's sons for the company's future.

After months of flirting with the idea, Disney and Fox announced in December 2017 that they had agreed to a $52.4 billion deal that would sell off most of 21st Century Fox's entertainment properties. On December 14, Disney confirmed an all-stock transaction worth around $52.4 billion (0.2745 Disney shares per Fox share) to have Fox sell their entertainment assets to Disney, pending approval from the United States Department of Justice Antitrust Division.

The assets on offer were staggering: The businesses to be acquired by Disney include 21st Century Fox's film production businesses, including Twentieth Century Fox, Fox Searchlight Pictures and Fox 2000 Pictures; Fox's television creative units, Twentieth Century Fox Television, FX Productions and Fox 21; FX Networks; National Geographic Partners; Fox Sports Regional Networks; Fox Networks Group International; Star India; and Fox's interests in Hulu, Sky plc, and Tata Sky. This wasn't just selling some divisions—it was dismantling an empire.

What stayed behind was equally telling: The acquisition will occur immediately after the spin-off by 21st Century Fox of the Fox Broadcasting network and stations, Fox News Channel, Fox Business Network, FS1, FS2 and Big Ten Network into a newly listed company referred to as New Fox. The Murdochs were keeping the businesses that couldn't be easily disrupted by Silicon Valley: live news, live sports, and broadcast television.

But the initial deal was just the opening gambit in what would become a spectacular bidding war. In February, CNBC reported that, despite the Disney–Fox deal, Comcast might take action to outbid Disney's $52.4 billion offer, if the AT&T–Time Warner merger went through. The cable giant, led by Brian Roberts, saw Fox's assets as essential to competing in the streaming wars.

The drama escalated dramatically in June 2018. On June 12, AT&T was given approval by District Judge Richard J. Leon to acquire Time Warner, easing concerns Comcast had regarding whether government regulators would block their bid for Fox. Consequently, the next day, Comcast mounted an all-cash bid of $65 billion ($35 per share and a 19% premium over Disney's offer) for the 21st Century Fox assets that were set to be acquired by Disney.

Disney's Bob Iger wasn't about to lose this prize. Within a week, On June 20, Disney and Fox announced they had amended their previous merger agreement, upping Disney's offer to $71.3 billion (a 10% premium over Comcast's $65 billion offer), while also offering shareholders the option of receiving either cash ($38 per share) or stock. The sweetened deal was too rich for Comcast to match.

The deal hit a snag in 2018 when Comcast unexpectedly bid $65 billion to lure Fox away from Disney. But Disney was able to keep the deal moving forward when it upped its offer to $71 billion. The final price represented a 36% premium over the initial agreement—testament to both the value of the assets and the intensity of the competition.

For the Murdochs, the timing was exquisite. They were selling at the absolute peak of content valuations, just before Wall Street would sour on the economics of streaming. The deal valued Fox's entertainment assets at multiples that would look absurd just a few years later as Netflix's stock crashed and streaming losses mounted across the industry.

The strategic logic for both sides was compelling. It was less interested in 21st Century Fox's production capacities and more keen to acquire 21st Century Fox's own film and television libraries to help expand the streaming service's library. Disney needed content to compete with Netflix; Fox needed scale to survive.

But there was another dimension to the deal: family dynamics. Later that month, it was confirmed that Lachlan Murdoch, rather than James Murdoch, would take charge of the new company tentatively known as "New Fox". The sale effectively resolved the succession question that had plagued the Murdochs for years. James, who favored digital transformation and had clashed with his father over Fox News' political coverage, would exit to pursue other ventures. Lachlan, more aligned with his father's vision of focused, profitable media properties, would inherit the kingdom—or at least what remained of it.

The financial engineering was elegant. The initial exchange ratio of 0.2745 Disney shares for each 21st Century Fox share was set based on an estimate of such tax liabilities to be covered by an $8.5 billion cash dividend to 21st Century Fox from the company to be spun off. Fox shareholders would receive Disney stock, giving them upside in the combined company, plus cash from the spinoff—a structure that maximized value while minimizing taxes.

The Walt Disney Co. has closed its $71.3 billion acquisition of large parts of 21st Century Fox on March 20, 2019, completing one of the largest media mergers in history. The Murdochs had extracted maximum value, selling their Hollywood assets at the peak while keeping the businesses that would form the foundation of the new Fox Corporation.

The genius of the deal, from Fox's perspective, was what it didn't sell. By keeping Fox News, the broadcast network, and key sports rights, the Murdochs retained a focused, highly profitable business without the capital intensity of competing in global streaming. They had effectively sold the past (studio production) and kept the present (live programming), betting that while streaming would transform entertainment, it couldn't replicate the immediacy of news and sports.

As we'll see in the next chapter, this "leftover" collection of assets would prove to be exactly the right portfolio for the post-streaming era.

V. The New Fox: Rebirth as a Focused Media Company (2019–Present)

The morning of March 19, 2019, was crisp and clear in Manhattan. At precisely 9:30 AM, as the opening bell rang at the New York Stock Exchange, a new ticker symbol appeared on the screens: FOX. Not the 21st Century Fox that investors had known for decades, but something different—leaner, more focused, deliberately smaller. Fox Corp began operating separately on March 19, 2019. This wasn't a beginning so much as a rebirth, the phoenix that rose from the ashes of the Disney sale.

Chairman and CEO Lachlan Murdoch led a town hall meeting three days later, indicating that stock would be issued to the corporation's employees based on longevity. Standing before employees at Fox headquarters, the younger Murdoch cut a different figure from his father—less bombastic, more measured, but with the same steely determination. "We're not trying to be all things to all people," he told the assembled staff. "We're going to be the best at what we do: live news, live sports, and free streaming."

Lachlan Murdoch is the Executive Chair and Chief Executive Officer of Fox Corporation, which is among the most recognized and influential media companies in the world. In this role, he oversees the Company's premier portfolio of news, sports and entertainment assets. Mr. Murdoch was instrumental in the spinoff of FOX by 21st Century Fox and the establishment of FOX as a standalone public company.

The portfolio was deliberately focused. Its assets include Fox Broadcasting Company, Fox Television Stations, Fox News, Fox Business, Fox Sports, Tubi, Fox One and others. This wasn't the sprawling empire of old—it was a precision instrument designed for one thing: profitability in the age of cord-cutting.

The strategy was counterintuitive. While every other media company was chasing Netflix into the subscription streaming wars, burning billions on original content, Fox zagged where others zigged. He led the company's purchase of a controlling stake in REA, which began with an original cash investment of approximately $1 million and resulted in a corporate asset that is currently valued at more than $5 billion. At FTS, Mr. Murdoch oversaw the company's 35 owned-and-operated television stations, where he raised the bar on local news coverage across the nation, increasing the total number of local news hours across the group to more than 850 per week.

The first major move signaled the new Fox's ambitions. In August 2019, Fox Corp acquired Credible Labs for $397 million and animation studio Bento Box Entertainment for $50 million. These weren't blockbuster deals, but they showed Fox's strategy: targeted acquisitions in high-margin businesses that complemented the core.

But the real masterstroke came in 2020. On April 20, 2020, Fox Corp acquired streaming service Tubi for $440 million. Fox Corp. said it will acquire Tubi, the ad-supported free streaming service, for $440 million in cash — a deal funded largely from Fox's sale of its 5% stake in Roku.

The Tubi acquisition was brilliant in its simplicity. While Netflix, Disney+, and HBO Max fought over who could spend the most on prestige dramas, Fox bought a free, ad-supported service that required no original content investment. Tubi offers over 20,000 older TV shows and movies to watch for free and claims to have a base of 25 million active monthly viewers.

"Tubi will immediately expand our direct-to-consumer audience and capabilities and will provide our advertising partners with more opportunities to reach audiences at scale," Fox Corp. executive chairman and CEO Lachlan Murdoch said in a statement. "Importantly, coupled with the combined power of Fox's existing networks, Tubi provides a substantial base from which we will drive long-term growth in the direct-to-consumer arena."

The timing was perfect. Fox acquired Tubi just as the pandemic was about to supercharge streaming viewership. It jumped from 33 million monthly users in 2021 to 51 million in 2022. Our own forecast predicts that Tubi will hit 55 million US viewers in 2023. By 2024, the service had become a legitimate player in streaming, all while spending a fraction of what competitors burned through.

The financial discipline was remarkable. Fox financed the Tubi acquisition principally with the net proceeds from the completed sale of its stake in Roku. Fox Corp. said it will acquire Tubi, the ad-supported free streaming service, for $440 million in cash — a deal funded largely from Fox's sale of its 5% stake in Roku. Fox essentially swapped a passive investment for an active business, maintaining its fortress balance sheet.

The new Fox also demonstrated a willingness to explore unconventional opportunities. In May 2019 via the Fox Sports division, Fox Corp acquired a 4.99% stake in Canadian online gambling operator The Stars Group for $236 million. As a result, it was also announced that the companies would co-develop sports betting products for the U.S. market under the branding Fox Bet. This positioned Fox to benefit from the sports betting boom without taking on excessive risk.

Throughout this transformation, the company maintained its focus on what worked: live programming that commanded premium advertising rates and couldn't be easily replicated by streaming services. The formula was simple but powerful—own the moments that matter, when audiences have to watch in real-time.

The succession question that had plagued the Murdochs for years seemed resolved. Mr. Murdoch served as Executive Chairman of 21st Century Fox prior to the closing of the merger of 21st Century Fox and The Walt Disney Company in March 2019. He began that role in 2015, working directly with the company's senior management and Board of Directors to develop global strategies and set the overall corporate vision. Mr. Murdoch served as a member of the 21st Century Fox Board of Directors from 1996 until the closing of the merger with Disney.

But even in this new, focused incarnation, the Murdochs couldn't resist the urge to recombine their empire. On October 14, 2022, it was announced that, under the instruction of Rupert Murdoch, a special committee had been established to explore a potential merger of Fox and News Corp, bringing the two companies back together since the former 21st Century Fox was spun-off from News Corp in 2013. Although Lachlan Murdoch supported his father in the proposal, James Murdoch opposed it, as did many shareholders. On January 24, 2023, the proposed merger was abandoned by Murdoch.

The failed merger attempt revealed a fundamental truth: the new Fox worked precisely because it was focused. Investors didn't want another conglomerate; they wanted a pure play on live content and advertising.

As the company evolved, it continued to innovate within its lane. In April 2023, Fox announced it would be forming Tubi Media Group. This would be a standalone digital business unit, encompassing Tubi, Credible Labs, Blockchain Creative Labs, along with several other Fox digital sports, news and entertainment platforms and teams, in which Paul Cheesbrough was announced as CEO.

The results spoke for themselves. Fox has turned down repeated offers of around $2 billion for its free, ad-supported streaming service Tubi, according to Bloomberg. Fox acquired Tubi for $440 million in 2020. In just two years, the value of Tubi had potentially quintupled, validating Fox's contrarian streaming strategy.

The new Fox had achieved something remarkable: it had become more valuable as a focused company than it ever could have been as part of a larger conglomerate. By saying no to the streaming wars' original content arms race, by focusing on what couldn't be commoditized, and by maintaining financial discipline, the Murdochs had engineered one of media's great second acts.

VI. Business Model & Financial Performance

The numbers tell a story that would make any Wall Street analyst sit up and take notice. FOX reported full year fiscal 2024 revenues of $13.98 billion, net income of $1.55 billion, and adjusted EBITDA of $2.88 billion. These aren't just impressive figures—they're a testament to a business model that prioritizes cash generation over growth at any cost.

To understand Fox's financial performance, you need to grasp its dual revenue stream architecture. Unlike pure-play streaming services that depend entirely on subscriptions, or traditional broadcasters relying solely on advertising, Fox has engineered a model that extracts value from both sides of the equation.

The breakdown is revealing. Affiliate fee revenues increased 6%, driven by 10% growth at the Television segment and 3% growth at the Cable Network Programming segment. These affiliate fees—the payments cable and satellite operators make to carry Fox channels—represent the steady, predictable foundation of the business. Even as cord-cutting accelerates, Fox has managed to increase these fees through pricing power that comes from must-have content.

The advertising side tells an equally compelling story. Advertising revenues increased 11%, primarily due to higher political advertising revenues at the FOX Television Stations, continued growth at Tubi, higher ratings and higher pricing in the direct response marketplace at FOX News Media, and the impact of the "Summer of Soccer" at FOX Sports. This isn't just selling ads—it's selling access to audiences that can't be reached elsewhere.

The profit margins are where Fox truly shines. While Netflix and Disney+ burn billions on content creation, Fox operates with the efficiency of a Swiss watch. The company's adjusted EBITDA margin of approximately 20% would be the envy of most media companies. This isn't achieved through cost-cutting alone, but through strategic focus on high-margin businesses.

Consider the economics of Fox News. Industry analysts have long noted that Fox News generates the vast majority of the cable division's profits. The network requires relatively modest investment in content—no expensive scripted dramas, no A-list actors, just news anchors and production staff. Yet it commands premium advertising rates and the highest affiliate fees in cable news. Cable subscribers pay roughly 89 cents month for the Fox News Channel, according to a 2012 estimate by research firm SNL Kagan. CNN was estimated to average 57 cents per subscriber and MSNBC just 18 cents.

The sports business operates on a different but equally attractive model. Fox pays billions for NFL rights, but these are essentially pass-through costs. The advertising revenue from NFL games, combined with the leverage these rights provide in affiliate negotiations, more than justifies the investment. It's a virtuous cycle: premium sports content drives viewership, which drives advertising rates, which justifies higher affiliate fees.

The Tubi acquisition has emerged as a financial masterstroke. Fox acquired Tubi for $440 million in 2020, and by 2023, Fox has turned down repeated offers of around $2 billion for its free, ad-supported streaming service Tubi. The service has grown rapidly while requiring minimal content investment, as it primarily licenses older library content that others have already monetized.

Capital allocation at Fox follows a disciplined playbook that would make Warren Buffett proud. As of September 30, 2024, the Company has repurchased approximately $4.85 billion of its Class A common stock and approximately $1 billion of its Class B common stock. This aggressive buyback program isn't just financial engineering—it's a statement of confidence in the business model.

The company has also been shareholder-friendly with dividends. In 2025, the company increased its share repurchase authorization by $5 billion, bringing the total to $12 billion, and raised its semi-annual dividend to $0.28 per share. This combination of buybacks and dividends means Fox is returning virtually all of its free cash flow to shareholders—a rarity in a media industry obsessed with acquisition and expansion.

The balance sheet strength provides optionality. The company's balance sheet remains robust with $5.35 billion in cash. This war chest isn't sitting idle—it's strategic ammunition for opportunistic acquisitions or aggressive buybacks when the stock is undervalued.

What's particularly impressive is how Fox has managed this performance during a period of massive industry disruption. Full year Adjusted EBITDA was $2.88 billion as compared to the $3.19 billion reported in the prior year. While EBITDA declined slightly year-over-year due to tough comparisons (the prior year included the World Cup), the company maintained robust profitability even as competitors struggled.

The efficiency of the model shows in the numbers. Fox generates nearly $14 billion in revenue with a relatively small asset base compared to traditional media conglomerates. There are no theme parks to maintain, no massive studio lots (Disney kept those), no global streaming infrastructure to build. Just focused, high-margin businesses that generate predictable cash flows.

The quarterly volatility in Fox's results actually demonstrates the model's strength. Fox Corporation saw profit in its fiscal second quarter surge due to its reliance on news and sports programming, with ads tied to the 2024 presidential election and big-audience MLB and NFL telecasts giving a boost to operations at the company. Revenue, meanwhile, rose to $5.08 billion, an increase of $844 million, or 20% from $4.23 billion in the year-earlier period. These periodic spikes from elections and major sporting events provide earnings upside while the base business churns out steady cash.

The return on invested capital is exceptional. Fox essentially traded $71 billion worth of Disney stock (from the sale) for a business generating nearly $3 billion in EBITDA. The implied return on that forgone capital is impressive, especially considering Fox shareholders also kept their Disney shares, giving them upside in both companies.

Looking at peer comparisons, Fox's financial profile stands out. While Netflix burns cash on content and Disney invests heavily in streaming losses, Fox generates consistent free cash flow. While ViacomCBS and Warner Bros. Discovery struggle with debt, Fox maintains a fortress balance sheet. The company has achieved what few in media have managed: growth in profitability during the streaming transition.

The sustainability of this model is key. Unlike businesses disrupted by technology, live news and sports have proven remarkably resilient. Advertisers still need to reach mass audiences simultaneously. Cable operators still need Fox's content to retain subscribers. These dynamics won't change overnight, giving Fox a runway to adapt gradually rather than desperately pivoting like many peers.

For investors, Fox represents something increasingly rare: a media company that treats shareholders as partners rather than ATMs. The combination of steady cash generation, disciplined capital allocation, and strategic focus has created a compound returns machine hiding in plain sight.

VII. The Murdoch Succession Drama

VII. The Murdoch Succession Drama

The courtroom in Reno, Nevada, was sealed to the public in September 2024, but what transpired inside would determine the fate of one of the world's most influential media empires. Rupert Murdoch, at 93, was attempting to rewrite the rules of his own succession—a move that would pit son against son in a battle eerily reminiscent of the HBO series that had captivated audiences just years before.

The company is controlled by the Murdoch family via a family trust with 39.6% ownership share, and by Rupert Murdoch himself to the effect of almost 40%. This structure, created decades ago during Murdoch's divorce from his second wife Anna, was designed to prevent any single heir from destroying what he had built. The trust stipulated that after Rupert's death, his four oldest children—Prudence, Elisabeth, James, and Lachlan—would share equal voting rights.

But by 2023, Murdoch had decided this arrangement was a mistake. On September 21, 2023, Rupert Murdoch announced that he was stepping down as the chairman of Fox Corp, effective November 2023. The timing wasn't coincidental—it was the opening move in a carefully orchestrated plan to ensure Lachlan's control would survive his father's eventual passing.

The family dynamics had been fracturing for years. James Murdoch, once heir apparent, had grown increasingly uncomfortable with Fox News' editorial direction, particularly after the January 6, 2021 Capitol riots. His departure from the family business in 2020 wasn't just a career change—it was an ideological divorce. James believed the family media properties had become destructive forces in democracy; Lachlan and Rupert saw them as truth-tellers in a world of liberal bias.

Elisabeth Murdoch occupied a middle ground, focused primarily on her production company Sister and seemingly content to stay out of the succession battle. Prudence, the eldest, had long ago made peace with a more distant relationship to the empire. But the equal voting structure meant that after Rupert's death, James could theoretically ally with his sisters to force changes at Fox News or even sell the company entirely. The Nevada courthouse drama represented the culmination of decades of careful succession planning gone awry. The trust was irrevocable, set up as a result of Murdoch's divorce from his second wife, Anna, who negotiated to protect the children's interest in the family business. In December 2023, Rupert Murdoch applied to change the terms of his "irrevocable" family trust (established in 1999, as the Murdoch Family Trust, or MFT) to ensure that Lachlan would have full control over News Corp, a mass media and publishing company that manages hundreds of assets, instead of his sharing voting rights equally with his three siblings Prudence MacLeod, Elisabeth Murdoch and James Murdoch.

The legal maneuvering was sophisticated. Murdoch chose Nevada as his battleground deliberately—The state allows irrevocable trusts to be decanted, or changed, into a new trust as long as certain provisions are met. In the case of the Murdoch dispute, Rupert will have to prove to a probate court that he is acting "in good faith and for the sole benefit of the heirs".

The argument Murdoch made was audacious in its paternalism. His representatives – including former attorney general Bill Barr – argued that because Lachlan would not change the conservative bent of the company's outlets, the amendment was in the financial interest of all the beneficiaries, even those who opposed it. Essentially, Rupert's argument was that interference by the other siblings would cause a financial loss to Fox, and therefore it would be "in their own best interests if they have their votes taken away from them".

The family fractures were deep and public. James had become increasingly vocal about his opposition to Fox News' editorial direction. James described Fox News as a "menace" to American democracy in interviews, making clear his ideological break with his father's media empire. The September 2024 trial in Reno brought these tensions to a dramatic head, with family members facing each other in court for several days of testimony.

The outcome was devastating for Rupert and Lachlan. The probate commissioner, who heard several days of secret testimony by Murdoch family members earlier this year, issued a ruling over the weekend, and the 96-page opinion eviscerated Rupert Murdoch and his chosen son, Lachlan Murdoch. Gorman's 96-page opinion included a description of Rupert Murdoch's plan as "a carefully crafted charade" to "permanently cement Lachlan Murdoch's executive roles" in the Murdoch companies, without regard to the effects of such control on the companies or other family members.

The ruling's language was remarkably harsh. The commissioner, Edmund J. Gorman Jr., wrote that Rupert, Lachlan and their representatives had operated in "bad faith". The judge also wrote that former Attorney General Bill Barr, a representative appointed to the trust, "demonstrated a dishonesty of purpose and motive" by assisting Rupert and Lachlan Murdoch.

Perhaps most tellingly, According to the Times, an episode of "Succession" about the death of the fictional family patriarch Logan Roy caused Murdoch's children to hold discussions about how to avoid a TV-drama-worthy outcome within their own family. The commissioner even cited the HBO series in his opinion. Life had indeed imitated art, but with higher stakes—control of one of the world's most influential media empires.

The implications extend beyond family drama. Rupert and Lachlan Murdoch's lawyer, Adam Streisand, stated on December 10 that they would appeal the verdict, but legal experts suggest the strong wording of the opinion makes a successful appeal difficult. There was speculation that if Murdoch lost the appeal before his death, he might sell the rest of his company.

For now, the succession plan remains as originally structured—after Rupert's death, his four eldest children will share equal control. This creates profound uncertainty about Fox Corporation's future direction, particularly given James's stated opposition to Fox News' editorial stance. The man who spent a lifetime accumulating power may have failed in his final attempt to control his legacy from beyond the grave.

VIII. Strategic Challenges & Opportunities

The existential threat facing Fox Corporation isn't competition from CNN or MSNBC—it's the relentless mathematics of cord-cutting. Every quarter, millions of American households cancel their cable subscriptions, and with each cancellation, Fox loses not just viewers but the steady stream of affiliate fees that have long been its financial lifeblood. The largest cable networks of Fox Corporation were FOX News and FS1, with 67 million subscribers each recorded in 2024. Yet this number masks a troubling trajectory. Total subscribers to Fox News Channel are estimated to fall to 63.1 million at the end of 2022, according to Kagan, a market-research unit of S&P Global Intelligence, compared with 78.6 million in 2020 — a tumble of 19.7%. The mathematics are brutal: Wells Fargo analyst Steven Cahall estimates 7-8 percent cord-cutting, with a downside bias.

The financial implications cut deeper than raw subscriber losses. Of the 70 million or so traditional cable TV subscribers, only about 17 percent of those actually watch Fox. Despite very often not even being watched, Fox nabs $1.8 billion a year — about fifty percent more than it makes off of advertising — from simply having its channel in a cable lineup. This subsidy from non-viewers has been Fox's secret weapon, but it's evaporating as consumers gain the power to choose.

Fox's response has been aggressive pricing power while it still has leverage. During a February 2022 earnings call, Fox Corp. CEO Lachlan Murdoch announced that 70% of the network's cable and satellite contracts will be up for renewal during fiscal years 2023 and 2024. Murdoch has signaled to investors that Fox aims to continue to increase affiliate revenue even as the cord-cutting trend continues to accelerate, shrinking the consumer base. The strategy is clear: extract maximum value from a declining base while you still can.

The political polarization that drives Fox News' ratings also creates vulnerability. Fox News's share of conservative news viewers is down to 84% from 94%. Competition from outlets like Newsmax and OANN has fragmented the conservative media landscape, forcing Fox to defend its right flank while maintaining advertiser acceptability—a delicate balance that became harder after the Dominion settlement.

Sports rights inflation presents another challenge. Fox's reliance on NFL rights creates a high-stakes poker game every renewal cycle. The costs keep escalating, but Fox can't afford to fold—NFL games are the tent pole that justifies everything else. Without them, Fox loses its leverage with distributors and its relevance with advertisers.

Yet Fox has seized opportunities others missed. Fox Corporation officially launched FOX One yesterday, according to a company announcement. The streaming service costs $19.99 monthly or $199.99 annually with a seven-day free trial period. This isn't just another streaming service—it's a hedge against cord-cutting that maintains Fox's direct relationship with consumers. In July 2025, Fox Corporation announced that it would acquire a one-third stake in Penske Entertainment, parent company of the IndyCar Series and the Indianapolis Motor Speedway. The media company announced that it acquired a one-third interest in Penske Entertainment, which owns the Indianapolis Motor Speedway, the NTT IndyCar open-wheel racing series and IMS Productions. This wasn't just a media rights deal—it was Fox becoming a stakeholder in live sports content that can't be disrupted by streaming.

The international expansion limitations are real but potentially overstated. While Fox lacks the global footprint of Disney or Warner Bros. Discovery, its focus on the U.S. market—still the world's most valuable advertising market—may be an advantage rather than a handicap. Not every media company needs to be global; sometimes dominance in a single, profitable market beats thin presence everywhere.

Direct-to-consumer strategy represents both challenge and opportunity. Fox Corporation officially launched FOX One yesterday, according to a company announcement. The streaming service costs $19.99 monthly or $199.99 annually with a seven-day free trial period. The platform consolidates Fox's complete programming portfolio into a single destination. Content includes FOX News Channel, FOX Sports, FS1, FS2, Big Ten Network, FOX Business, FOX Weather, FOX Deportes, local FOX stations, and the main FOX broadcast network.

The genius of Fox One is its positioning. The service addresses cord-cutter and cord-never audiences underserved in the streaming ecosystem while providing Fox with direct-to-consumer revenue streams independent of traditional cable distribution. FOX One specifically targets cord-cutters and cord-nevers among the 65 million U.S. households seeking alternatives to traditional cable subscriptions while maintaining access to premium news, sports, and entertainment programming.

IX. Playbook: Key Business Lessons

The Fox Corporation story offers a masterclass in strategic focus that runs counter to conventional wisdom. While the business world celebrates diversification and growth at any cost, Fox demonstrates that sometimes less truly is more—if you're disciplined about what you keep.

The Power of Focus vs. Conglomeration: The decision to sell entertainment assets to Disney while keeping news and sports wasn't retreat—it was strategic concentration. Fox recognized that in an age of infinite content, scarcity creates value. Live news and sports are the only content categories that command attention in real-time, creating the kind of appointment viewing that advertisers covet and distributors need.

Building a Moat with Live Programming: Fox's competitive advantage isn't technology or global scale—it's the perishability of its content. A Marvel movie can be watched anytime; election night coverage or the Super Bowl must be consumed as it happens. This temporal monopoly creates pricing power that no algorithm can disrupt. Fox has built its entire strategy around owning the moments that matter.

Managing Regulatory and Political Relationships: Fox's ability to navigate the regulatory landscape demonstrates sophisticated political capital management. The company maintains relationships across the political spectrum despite its conservative programming, understanding that regulatory approval matters more than ideological purity. The Nevada trust battle showed the limits of this influence, but Fox's broader regulatory strategy remains effective.

The Value of Contrarian Positioning: When every media company chased streaming subscribers, Fox bought Tubi for cash flow. When competitors pursued global expansion, Fox doubled down on America. When others apologized for their political coverage, Fox embraced it. This contrarian approach only works with conviction—half-hearted differentiation is worse than following the crowd.

Capital Discipline in a Capital-Light Business: Fox's return of nearly all free cash flow to shareholders through dividends and buybacks isn't financial engineering—it's recognition that the business doesn't need massive reinvestment. Unlike Netflix, which must constantly feed the content beast, Fox's model generates cash that genuinely exceeds reinvestment needs.

When to Sell vs. When to Hold: The Disney deal timing was exquisite. The Murdochs sold at peak content valuations, just before streaming economics turned brutal. They kept the businesses that couldn't be replicated or disrupted. This wasn't luck—it was pattern recognition from decades of media evolution. Knowing when you're holding a melting ice cube versus a diamond is perhaps the most valuable skill in business.

Creating and Monetizing Cultural Influence: Fox News doesn't just report news—it shapes political discourse. This influence translates directly to pricing power. Cable operators can't drop Fox News without facing subscriber revolt. Politicians court Fox's audience. This cultural relevance creates a moat deeper than any technology. The lesson: in media, influence is the ultimate currency.

The IndyCar investment exemplifies these principles in action. Fox didn't just buy media rights—it bought equity in the content itself. This aligns incentives perfectly: Fox profits not just from broadcasting races but from growing the sport's value. It's the same playbook that made Fox Sports successful: own the moments that matter, then make them matter more.

The succession drama, while damaging to family harmony, actually validates the business model. The very fact that control of Fox is worth fighting over—that James, Elisabeth, and Prudence would battle their father in court—proves the franchise value of what Fox has built. Companies in decline don't generate succession battles; valuable ones do.

Perhaps the most important lesson is about knowing your customer. Fox's audience isn't everyone—it's a specific, passionate, loyal demographic that advertisers struggle to reach elsewhere. By super-serving this audience rather than diluting the product to chase broader appeal, Fox has created a business that punches far above its weight class in profitability.

X. Bull vs. Bear Case

Bull Case:

The bull thesis for Fox rests on the irreplaceability of its core assets. Fox News remains the dominant force in cable news, generating approximately 70% of the parent company's pre-tax profit from a single channel. Despite cord-cutting, the network maintains pricing power because its audience literally won't accept substitutes—creating leverage that translates to the highest affiliate fees in cable news.

The sports portfolio, anchored by NFL rights through 2033, provides another defensive moat. This year's Indianapolis 500 on FOX averaged 7.01 million viewers, a 41 percent increase over the previous edition and a 17-year high. Live sports remain the glue holding the traditional TV bundle together, and Fox's focused portfolio of rights—NFL, FIFA World Cup, MLB—delivers premium audiences that streaming services struggle to aggregate.

Tubi's trajectory validates Fox's contrarian streaming strategy. From a $440 million acquisition to rejecting $2 billion offers, the AVOD platform has emerged as a legitimate player without the massive content spending that plagues subscription services. As streaming economics rationalize, Tubi's model looks increasingly prescient.

The balance sheet provides enormous flexibility with $5.35 billion in cash and minimal debt. This war chest enables opportunistic acquisitions, aggressive buybacks when the stock is undervalued, or simply returning cash to shareholders. Few media companies enjoy such financial flexibility amid industry disruption.

Political dynamics favor Fox's positioning. Election cycles drive record viewership and advertising revenue, as seen in the 2024 surge. The polarized media landscape, while challenging in some respects, ensures Fox News' relevance and pricing power remain intact. Cultural influence translates directly to financial performance.

Bear Case:

The bear case begins with the inexorable math of cord-cutting. The largest cable networks of Fox Corporation were FOX News and FS1, with 67 million subscribers each recorded in 2024, but ESPN is projected to see its traditional pay-TV subscribers fall to 57.9 million in 2026, according to data from Kagan, a market-research firm that is part of S&P Global Intelligence, compared with 65.1 million in 2024. The pay-TV audience for Fox Sports 1 is seen falling to 57.2 million in 2026, compared with 62.8 million in 2024. This structural decline threatens the dual revenue stream model that drives Fox's profitability.

Single-point dependency on Fox News creates existential risk. With the channel generating the vast majority of cable profits, any disruption—whether regulatory, legal, or audience fragmentation—could devastate the entire company. The Dominion settlement was just a warning shot; more legal challenges loom.

Limited international growth potential caps the company's addressable market. While focus on the U.S. has been profitable, it leaves Fox vulnerable to domestic economic cycles and demographic shifts. Younger Americans show less interest in traditional news consumption, suggesting a troubling generational transition ahead.

Succession uncertainty hangs over everything. The Nevada court's rejection of Rupert Murdoch's attempt to consolidate control under Lachlan means the four eldest children will share equal voting rights after his death. Given James's stated opposition to Fox News' editorial direction, this structure virtually guarantees future conflicts that could destabilize the company or force its sale.

Reputational risks compound daily. Advertisers increasingly scrutinize where their dollars go, and Fox's controversial programming creates constant brand safety concerns. While the audience remains loyal, advertiser boycotts and pressure campaigns pose ongoing threats to the advertising revenue stream.

The streaming transition, despite Fox One's launch, remains fraught. At $19.99 monthly, Fox One must convince millions to pay directly for content they currently receive as part of broader bundles. The psychological shift from bundled to à la carte consumption historically results in lower total revenue per customer.

Competition intensifies from unexpected angles. Tech giants with unlimited resources continue to encroach on sports rights. The rise of alternative conservative media platforms fragments Fox's once-monolithic audience. Social media platforms increasingly serve as primary news sources for younger demographics.

The bear case ultimately rests on timing: Fox is executing perfectly for a world that's disappearing. The company has optimized for the endgame of linear television, achieving maximum profitability from a declining paradigm. But what happens when that paradigm finally breaks? Fox's focused strategy, while brilliant for today, may prove to be tomorrow's trap.

XI. Recent News

FOX reported full year fiscal 2024 revenues of $13.98 billion, net income of $1.55 billion, and adjusted EBITDA of $2.88 billion according to the company's August 2024 earnings report. The fourth quarter results demonstrated the model's resilience, with adjusted net income of $423 million or $0.90 per share, beating the analyst consensus of $0.81.

Affiliate fee revenues increased by 5%, driven by 9% growth in the Television segment, validating Fox's pricing power strategy even as subscriber bases decline. This performance came despite advertising revenues being consistent with the prior-year quarter, as FOX Sports' "Summer of Soccer," including the broadcasts of the UEFA European Championship and CONMEBOL Copa América, was offset by lower ratings and pricing at the FOX Network.

Looking ahead to fiscal 2025, Fox is framing the next year as a big one, led by the upcoming presidential election, which should funnel cash to its local TV stations and Fox News, as well as next year's Super Bowl. The combination of political advertising and premium sports events creates a perfect storm for revenue generation.

The Tubi momentum continues to build. Fox has cemented Tubi's position as the most watched free TV and movie streaming service in the United States, proving that the AVOD model can compete effectively with subscription services without the massive content spending.

This year's Indianapolis 500 on FOX averaged 7.01 million viewers, a 41 percent increase over the previous edition and a 17-year high. The IndyCar investment already shows returns, with the 2025 NTT IndyCar Series season averaging a 31 percent increase in viewership year-over-year.

Management changes reflect the new focused strategy. While Rupert stepped down as chairman in 2023, Lachlan's leadership has maintained strategic continuity while adding new growth initiatives like Fox One and the IndyCar investment.

XII. Links & Resources

SEC Filings and Investor Materials: - Fox Corporation Investor Relations: investor.foxcorporation.com - Latest 10-K Annual Report (2024) - Quarterly Earnings Releases and Conference Call Transcripts - Proxy Statements and Corporate Governance Documents

Key Books on the Murdoch Empire: - "The Murdoch Method" by Irwin Stelzer - "Hoax: Donald Trump, Fox News, and the Dangerous Distortion of Truth" by Brian Stelter - "The Man Who Owns the News" by Michael Wolff - "Breaking News: The Remaking of Journalism and Why It Matters Now" by Alan Rusbridger

Industry Analysis and Research: - S&P Global Market Intelligence Media Reports - MoffettNathanson Cable & Satellite Research - Wells Fargo Equity Research Media Coverage - Kagan Media & Telecom Market Intelligence

Historical Context and Documentaries: - "The Rise of the Murdoch Dynasty" (BBC Documentary Series) - "Outfoxed: Rupert Murdoch's War on Journalism" (2004) - "The Loudest Voice" (Showtime Series on Roger Ailes) - Columbia Journalism Review Archives on Fox News

Academic Studies: - "The Fox News Effect: Media Bias and Voting" (Quarterly Journal of Economics) - "News Droughts, News Floods, and U.S. Disaster Relief" (Study on Fox News influence) - Harvard Kennedy School Shorenstein Center Media Research

Financial Data Platforms: - Bloomberg Terminal: FOX US Equity - Refinitiv Eikon: FOX.O - Capital IQ Company Intelligence - FactSet Company Research

Conclusion: The Last Stand of Linear Television

Fox Corporation represents something unique in modern media: a company that won by refusing to play. While competitors chased global scale, Fox focused on America. While others burned billions on streaming content, Fox bought cash flow. While rivals apologized for their political coverage, Fox doubled down. This contrarian playbook has created a business that generates nearly $14 billion in revenue from what Disney didn't want—and does so with margins that streaming services can only dream about.

The financial performance validates the strategy. From the March 2019 spinoff through 2024, Fox has returned over $5.85 billion to shareholders through buybacks and maintained robust profitability despite industry headwinds. The company's ability to increase affiliate fees even as subscribers decline demonstrates pricing power that few media properties possess. The Tubi acquisition, mocked by some as a consolation prize in the streaming wars, has emerged as a potential multi-billion dollar asset.

Yet Fox's success story comes with an asterisk: it's optimized for a world that's disappearing. The company has executed flawlessly for the endgame of linear television, extracting maximum value from a declining paradigm. The cord-cutting mathematics are inexorable. Every quarter, millions of households cancel cable subscriptions, and with them goes the dual revenue stream that makes Fox's model work. The company can raise prices on remaining subscribers, but there's a limit to how long pricing can offset volume declines.

The succession drama adds another layer of uncertainty. The Nevada court's rejection of Rupert Murdoch's attempt to cement Lachlan's control means the company's future direction remains contested. After Rupert's death, his four eldest children will share equal voting rights, setting up potential conflicts given their divergent views on Fox News' editorial direction. This isn't just family drama—it's existential uncertainty about whether Fox Corporation will even exist in its current form a decade from now.

But perhaps the most remarkable aspect of Fox's story is how it turned limitations into advantages. By selling entertainment assets to Disney, Fox avoided the streaming content arms race that's destroying value across the industry. By focusing on news and sports, Fox owns content that must be consumed live—creating scarcity in an age of infinite choice. By maintaining a controversial political stance, Fox built an audience that literally won't accept substitutes, providing leverage that translates directly to pricing power.

The IndyCar investment and Fox One launch show the company isn't standing still. These aren't desperate pivots but logical extensions of the core strategy: own live moments that matter, then monetize them across multiple platforms. The IndyCar deal particularly demonstrates sophisticated thinking—Fox didn't just buy rights but equity, aligning long-term incentives in a way traditional media deals never could.

For investors, Fox presents a fascinating dilemma. The bear case is obvious: you're buying into the profitable decline of linear television, with structural headwinds that no amount of execution can fully offset. The bull case is equally clear: you're getting a cash-generative business at a reasonable multiple, with management committed to returning capital and strategic optionality from a fortress balance sheet.

The truth likely lies somewhere between. Fox Corporation isn't the future of media, but it might be the most profitable way to play media's present. While competitors lose billions chasing streaming subscribers, Fox generates consistent cash flow from audiences that aren't going anywhere soon. While others apologize for their influence, Fox monetizes it. While rivals pursue global scale, Fox dominates its niche.

In the end, Fox Corporation's story is about the power of focus in an age of distraction. The Murdochs built a sprawling empire, sold it at the peak, and kept only the pieces that couldn't be disrupted. They've created a business that's simultaneously forward-looking (Tubi, Fox One) and backward-looking (linear TV dependency), innovative (IndyCar equity investment) and traditional (broadcast networks), growing (affiliate fees) and declining (subscribers).

This contradiction isn't a bug—it's the feature. Fox Corporation has become the perfect transition vehicle between media's past and future, generating maximum value from linear television's decline while building optionality for what comes next. Whether that transition leads to long-term success or eventual irrelevance remains to be seen. But for now, Fox has achieved something remarkable: turning the end of an era into one of media's most profitable businesses.

The empire may be smaller, but it's never been more focused—or more profitable per dollar of revenue. In an industry obsessed with growth at any cost, Fox Corporation proves that sometimes, less really is more. The question isn't whether this model is sustainable forever—nothing is. The question is whether Fox can extract enough value from linear television's long goodbye to fund whatever comes next. Based on the evidence, they're off to a remarkable start.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube