Flowserve: The Hidden Giant of Global Flow Control

The Plumbing of Industrial Civilization

Walk into any oil refinery, power plant, chemical processing facility, or water treatment station anywhere in the world, and you will find the silent heartbeat of modern industry: pumps pushing, valves controlling, seals containing. These unglamorous components rarely make headlines, yet without them, not a single barrel of crude oil would move through a pipeline, not a megawatt of power would reach a home, and not a drop of clean water would flow from a municipal tap.

The Flowserve Corporation is an American multinational corporation and one of the largest suppliers of industrial and environmental machinery such as pumps, valves, end face mechanical seals, automation, and services to the power, oil, gas, chemical and other industries. Headquartered in Irving, Texas, which is in the Dallas–Fort Worth Metroplex, Flowserve employs close to 16,000 employees in more than 50 countries.

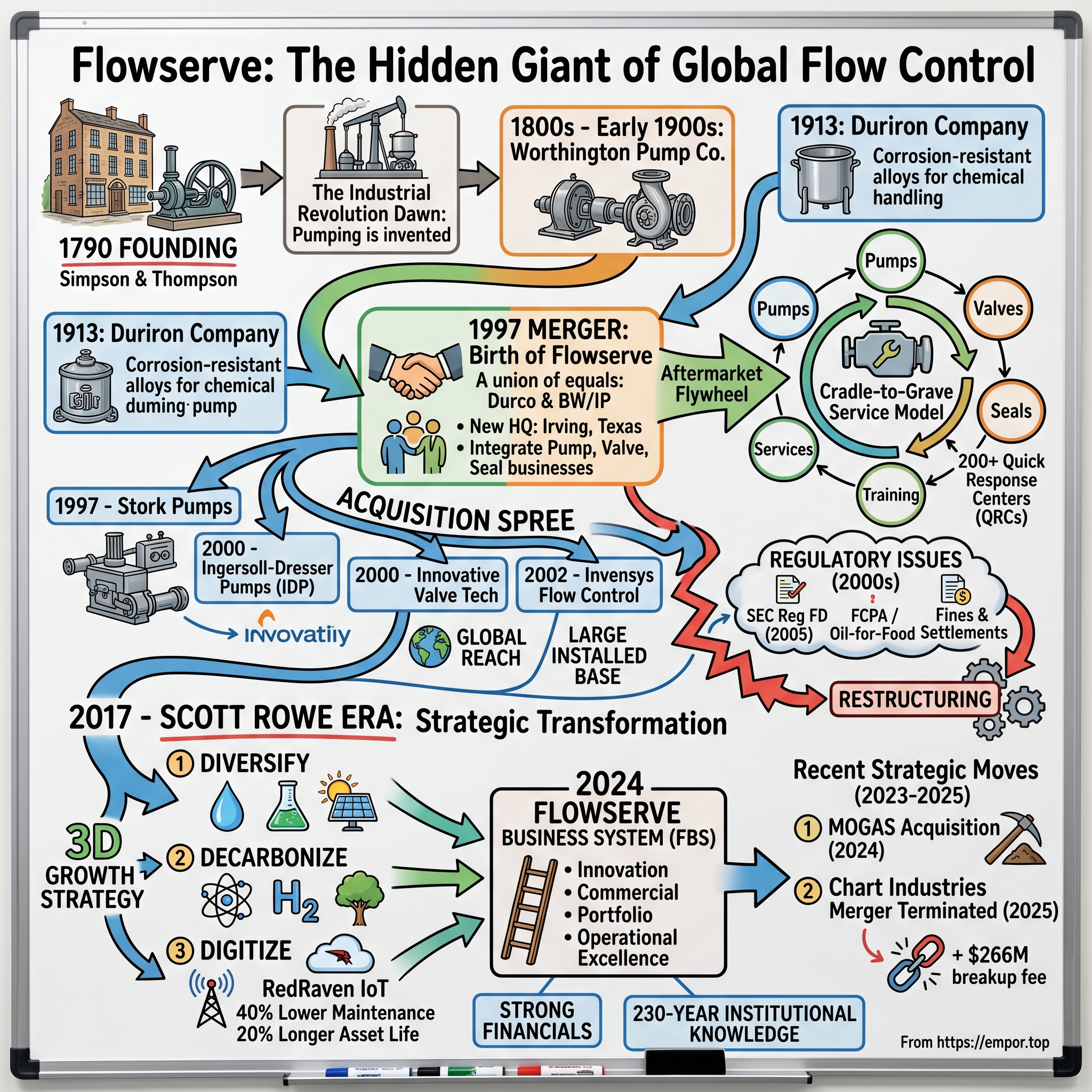

But here's what makes Flowserve's story so remarkable: Flowserve's heritage dates back to the 1790 founding of Simpson & Thompson by Thomas Simpson, later to become Worthington Simpson Pumps, one of the companies that became part of BW/IP. That's not a typo. The corporate DNA of Flowserve stretches back more than 230 years, to the early days of the Industrial Revolution, when the very concept of industrial pumping was being invented.

With a strong foothold in global infrastructure markets, Flowserve reported a 5.5% year-over-year increase in net revenues, reaching $4.56 billion in 2024. The company sits at the intersection of everything that matters in the modern energy economy: traditional oil and gas, nuclear power renaissance, hydrogen infrastructure, carbon capture, and clean water systems. When the world debates energy transition, Flowserve supplies the equipment that makes all sides of that debate possible.

It is the world's second largest producer of industrial pumps as well as valves. The company's growth strategy focuses mainly on acquisitions and alliances, although it faces formidable competitors as the industrial flow management industry undergoes a wave of consolidation.

The question for investors: Is Flowserve the hidden pick-and-shovel play on global energy infrastructure—positioned to win regardless of which energy future unfolds? Or is it a cyclical industrial company at the mercy of volatile commodity markets? The answer, as always, lies in understanding the history, the business model, and the competitive dynamics that have shaped this quiet giant of flow control.

The Ancient Heritage: Flow Control Through the Ages

Picture the England of 1790. George Washington was serving his first term as President of the United States. The French Revolution was entering its most radical phase. And in a corner of the British Isles, Thomas Simpson founded a company called Simpson & Thompson. Flowserve's legacy begins when Thomas Simpson founds Simpson & Thompson. His sons eventually take over to found James Simpson & Co., which later becomes Worthington Pump Co.

This was the dawn of the Industrial Revolution, when the emerging factories and mills of Britain desperately needed machines to move water, chemicals, and other fluids. The pump, in those early days, was as revolutionary as the microprocessor would be two centuries later. Without mechanical pumping, there could be no coal mines pumped dry of groundwater, no steam engines fed with water, no chemical processes of any meaningful scale.

Simpson's company evolved over generations, eventually becoming Worthington Pump Company—a name that would become synonymous with industrial pumping excellence. This corporate ancestor would eventually merge with other entities to form BW/IP (Borg-Warner Industrial Products), one of the two parents of modern Flowserve.

The other branch of Flowserve's family tree has a more American character. Launched in 1913 as a foundry, Duriron had been producing chemical fluid handling equipment for more than 80 years. The company's name came from its signature product: Duriron, a highly corrosion-resistant high-silicon iron alloy that could withstand the harsh chemicals that destroyed ordinary metals.

By the 1980s, the company had built a solid reputation for making the specialized equipment needed to move fluids in the chemical process market. Duriron carved out a niche in the most demanding applications—chemical plants where acids, alkalis, and corrosive solutions would eat through conventional equipment in months.

The challenge both companies faced, however, was the fundamental cyclicality of their customer base. With more than 85 percent of its sales derived from the chemical industry, the company was buffeted by the "peaks and valleys" of that cyclical business, according to the Plain Dealer. This vulnerability to commodity cycles would become a defining strategic challenge—one that would eventually drive both companies toward consolidation.

In the 1990s, Duriron embarked on a massive reorganizing effort. Seeking to enter new segments of the fluid management industry, Duriron began to forge alliances and acquire companies that operated outside its chemical niche.

This period saw the industrial equipment world beginning to consolidate. Customers were becoming more global, more demanding, and more interested in comprehensive solutions rather than piece-parts. The strategic logic of combination was becoming irresistible.

The takeaway for investors: Flowserve's heritage companies didn't survive 200+ years by accident. They built reputations for engineering excellence in mission-critical applications where failure wasn't an option. That institutional knowledge and brand equity became assets that no new entrant could replicate quickly.

The Pre-Merger Era: BW/IP and Duriron (1980s–1996)

By the mid-1990s, both BW/IP and Duriron had grown into substantial players in the flow control industry, each with distinct strengths and overlapping ambitions.

BW/IP, headquartered in Long Beach, California, traced its lineage to Borg-Warner Corporation's industrial products division. The company had assembled a portfolio of pump and seal technologies through decades of organic development and strategic acquisitions. Its strength lay in rotating equipment—the pumps and mechanical seals that formed the backbone of oil refineries and petrochemical plants worldwide.

Duriron, based in Dayton, Ohio (later Cleveland), had built its reputation on corrosion-resistant specialty equipment. At the time it joined forces with BW/IP, Ohio-based Durco International (which was known as the Duriron Company until shortly before the merger) had enjoyed ten years of record growth.

The strategic challenge for both companies was remarkably similar. The flow control industry was fragmenting into specialized niches, yet customers increasingly wanted integrated solutions. Oil companies, chemical processors, and power generators didn't want to deal with dozens of suppliers—they wanted partners who could provide everything from pumps to valves to seals, along with the service and technical support to keep it all running.

Moreover, the cyclicality problem remained acute. When oil prices crashed or chemical demand weakened, orders for new equipment would evaporate overnight. Whereas the pump and valve business was subject to the cyclical downturns of the petroleum and chemical markets, the service and repair of existing equipment was not.

Both companies recognized that the path forward required scale. Scale to spread R&D costs across larger revenue bases. Scale to afford the global service infrastructure customers demanded. Scale to weather the inevitable downturns in any single end market.

The acquisition of Durametallic Corporation by Duriron in January 1996 was a precursor of the consolidation to come. Durametallic was later acquired by Duriron in January 1996. Durametallic, based in Kalamazoo, Michigan, was a leading manufacturer of mechanical seals—the critical components that prevent leaks where rotating shafts enter pumps and other equipment. This acquisition gave Duriron a full portfolio of chemical process equipment and set the stage for the transformative merger that would follow.

The stage was set for what would become one of the most successful roll-up strategies in industrial equipment history.

The 1997 Merger: Birth of Flowserve

The merger announcement in early 1997 caught few industry observers by surprise. Flowserve was created in July 1997 when two rival companies—Durco International and BW/IP, Inc.—merged to form a new corporate entity. At the time it joined forces with BW/IP, Ohio-based Durco International (which was known as the Duriron Company until shortly before the merger) had enjoyed ten years of record growth.

What did surprise many was the ambition of the deal—and the thoughtfulness of its execution.

The union of the two companies was a merger of equals, effectuated by a stock-for-stock exchange in July 1997. BW/IP's Rethore was selected as the new company's chairman and chief executive, and William Jordan (the president, chairman, and CEO of Durco) served as the president and chief operating officer (COO) of the new corporate entity.

This was genuine power-sharing—rare in merger history, where "merger of equals" often masks one company's dominance. By splitting the top roles between the two leadership teams, the architects of the deal ensured that both corporate cultures and capabilities would be represented in the new entity.

To reflect that the merger had created a new company with a broader range of products and services, BW/IP and Durco elected to take a new name. They settled on Flowserve because it "symbolizes the fact that ... we will adopt an expanded vision of serving all the flow control needs of our customers in the 21st century," Rethore proclaimed in a press release.

The name itself tells a story. "Flow" captures the core function of the company's products—moving fluids. "Serve" captures the strategic pivot toward aftermarket services that would prove crucial to smoothing cyclical volatility. Together, "Flowserve" announced a company focused not just on manufacturing equipment, but on partnering with customers across the entire lifecycle of their operations.

After closing BW/IP's headquarters in Long Beach, California, and Durco's in Cleveland, Ohio, Flowserve opened global corporate headquarters in Irving, Texas. The choice of Dallas-Fort Worth as the headquarters location was strategic—central to the U.S., close to the oil and gas capital of Houston, and neutral ground that belonged to neither legacy company.

The integration moved with remarkable speed. Almost immediately after the merger, Flowserve launched a $92 million integration program that consisted of 45 distinct projects. Although BW/IP and Durco each had carved out areas of focus in the wider flow management industry, there was a considerable degree of overlap. To eliminate these redundancies, Flowserve merged the two companies' pump, valve, and seal businesses into three streamlined divisions.

The integration wasn't just about cost cutting. Flowserve's leadership recognized that the company needed to transform from a manufacturer into a solutions provider. In 1997, Flowserve formed the ServiceRepair Division, which focused on tending to the flow management equipment it had already installed. Flowserve would "go beyond just manufacturing," Rethore told the Wall Street Transcript and would provide "cradle-to-grave" service on its equipment.

This strategic insight—that the real money in industrial equipment lies in the aftermarket—would prove prescient. Every pump Flowserve sold became an annuity stream of replacement parts, repairs, and upgrades stretching out decades into the future.

The early results were encouraging. By the close of 1997, the merger looked to be an unequivocal success. Sales for the year surpassed $1.15 billion, with nearly half of the total generated by operations outside the United States. With 44 manufacturing facilities and 88 service and quick response centers, the company was better positioned to provide a broader array of goods and services to a wide range of customers. Flowserve's net profit for 1997 was $51.6 million.

The company's sales were balanced, with about one-third of total sales derived from the petroleum industry, one-third from the chemical sector, and one-third from power and other industries. This diversification—lacking in either predecessor company—would prove valuable in smoothing cyclical swings.

The Acquisition Spree & Roll-up Strategy (1997–2002)

With the founding merger complete, Flowserve's leadership embarked on an aggressive acquisition campaign that would reshape the global flow control industry. The strategy was straightforward: acquire companies with strong brands, complementary product lines, and established customer relationships, then leverage Flowserve's scale to extract synergies and expand market reach.

The company moved quickly to fill geographic and product gaps. 1997 - Merger of BW/IP and Durco International (adoption of brand name Flowserve); 1997 - Stork Engineered Pumps; 2000 - Ingersoll-Dresser Pumps (IDP); 2000 - Innovative Valve Technologies Inc. (Houston-based maintenance, repair, and replacement services for industrial valves, piping systems, and process system components); 2002 - Flow Control division of Invensys (manufacturer of valves, actuators and associated flow control products).

The transformative deal came in 2000. Flowserve Corp. (Dallas, TX) has signed a definitive agreement to acquire Ingersoll-Dresser Pumps (IDP) for $775 million in cash. The acquisition will create the world's second largest pump company.

IDP, a business unit of Ingersoll-Rand Co. (Woodcliff Lake, NJ), had sales of $838 million and operating income of $64 million in 1999. IDP produces industrial pumps and specialty pumps for process, power generation, and marine applications. The acquisition will nearly double the size and improve the profitability of Flowserve, which recorded operating income of $25.1 million on sales of $1.06 billion in 1999.

The IDP acquisition was about more than scale. IDP's product line includes such well-known brands as Ingersoll-Rand, Jeumont-Schneider Pumps, Pacific, Pleuger, Scienco and Worthington. "From a service perspective," he continues, "not only is Flowserve acquiring some of the best brands in the industry, but we will have access to one of the largest installed bases of process pumps in the flow-control industry."

The deal required regulatory scrutiny. According to the Department's complaint, the acquisition as originally proposed would have likely resulted in higher prices for API 610 pumps and power plant pumps used in the U.S. The pumps, which cost between $20,000 and $500,000, are sold through a bidding process. For most bids, there are only three or four credible competitors, and Flowserve and IDP are two of them.

Under the proposed consent decree, Flowserve and IDP must license eight lines of pumps to a firm that will manufacture the pumps and compete with Flowserve for sales to oil refineries and power plants in the U.S.

The acquisition spree wasn't without turbulence. Despite these considerable advances, Flowserve's 1999 sales were hindered by the continued overall weakness of the petroleum and chemical markets. Faced with these difficulties, as well as with the continued need to eliminate certain redundancies that had persisted since the merger, Flowserve announced early in 2000 that it would close ten facilities and lay off nine percent of its work force (about 600 people).

The synergy projections for IDP were ambitious. Once merged, Greer says Flowserve and IDP will be able to reduce costs by $75 million annually by the end of 2001 by eliminating overlapping facilities and attacking other inefficiencies. He does, however, expect the deal to have a neutral to slightly negative effect on earnings during 2000.

By 2002, Flowserve had assembled an impressive portfolio of brands and capabilities. Flowserve's many brands include Durco (pumps), Valtek (valves), and GASPAC (seals). The company had transformed from a collection of regional specialists into a global powerhouse with offerings spanning pumps, valves, seals, and services.

The critical insight for investors: Flowserve's acquisition strategy wasn't random shopping. Each deal was selected to fill specific gaps—geographic coverage, product categories, or service capabilities. The installed base of acquired companies became Flowserve's most valuable asset, generating decades of high-margin aftermarket revenue.

Turbulence & Challenges (2002–2016)

The early 2000s brought a harsh reminder that even well-executed roll-ups face headwinds. Flowserve stumbled into regulatory trouble that would cast a shadow over several years of the company's history.

Washington, DC, March 24, 2005--The Commission today charged Flowserve Corporation, a manufacturer of precision-engineered flow control equipment headquartered in Irving, Texas, with violating Regulation FD and Section 13(a) of the Securities Exchange Act of 1934.

On March 24, 2005, the Securities and Exchange Commission filed two settled enforcement proceedings charging Flowserve Corporation with violating Regulation FD and Section 13(a) of the Securities Exchange Act of 1934. First, the Commission filed a lawsuit in the United States District Court for the District of Columbia charging Flowserve with violating, and C. Scott Greer, Flowserve's Chairman, President and Chief Executive Officer, with aiding and abetting Flowserve's violations of, Regulation FD and Section 13(a). Second, the Commission issued an administrative order finding that Flowserve violated the same provisions, and that Greer and the Company's Director of Investor Relations, Michael Conley, were each a cause of Flowserve's violations.

Although the SEC has initiated over a half dozen Regulation FD proceedings since the Regulation became effective in October 2000, this is the first case to allege that a senior officer's reaffirmation of a company's previously disclosed earnings forecasts violated Regulation FD. It is also the first case that the SEC filed against a company's director of investor relations.

Without admitting or denying the Commission's charges, the Defendants have consented to the entry of a final judgment by the Court that would require Flowserve to pay a $350,000 civil penalty and Greer to pay a $50,000 civil penalty.

Additional regulatory issues followed. The Securities and Exchange Commission today filed Foreign Corrupt Practices Act books and records and internal controls charges against Flowserve Corporation. Flowserve is a Texas-based manufacturer of pumps, valves, seals, and related automation and services to the power, oil, gas, and chemical industries. The Commission's complaint alleges that from 2001 through 2003, two of Flowserve's subsidiaries entered into a total of twenty contracts in which $646,488 in kickback payments were made and another $173,758 were authorized in connection with sales of industrial equipment to Iraqi government entities under the U.N. Oil for Food Program.

Flowserve, without admitting or denying the allegations in the Commission's complaint, consented to the entry of a final judgment permanently enjoining it from future violations of Sections 13(b)(2)(A) and 13(b)(2)(B) of the Securities Exchange Act of 1934, ordering it to disgorge $2,720,861, in profits, plus $853,364 in pre-judgment interest, and to pay a civil penalty of $3,000,000.

Beyond regulatory challenges, the company faced the relentless cyclicality of its end markets. The oil and gas boom of the 2000s gave way to busts. The 2008 financial crisis cratered capital spending globally. Flowserve's annual revenue for 2021 was $3.54 billion, a 5.02% decrease from 2020. Flowserve's annual revenue for 2020 was $3.73 billion, a 5.37% decrease from 2019.

The company engaged in multiple restructuring efforts through this period, closing facilities, consolidating operations, and working to optimize its cost structure for the new economic reality.

Despite these challenges, Flowserve continued investing in strategic acquisitions. In 2015, the company completed its acquisition of SIHI Group. SIHI was founded in Germany in 1920 as Siemen & Hinsch (SiHi) by Otto Siemen and Johannes Hinsch, inventors of the self-priming side channel pump for liquids and gases. This was the beginning of a history of innovation, which later included the development of multistage centrifugal pumps, liquid ring vacuum pumps, so-called "combi-pumps" (centrifugal pumps with self-priming stages), volute casing pumps, magnetic drive systems and dry-running vacuum pumps. The brand was acquired by Flowserve in 2015.

SIHI Group, based in the Netherlands, and its subsidiaries ("SIHI") provides engineered vacuum and fluid pumps, with associated aftermarket parts and services, primarily serving the chemical market, as well as the pharmaceutical, food & beverage and other process industries. SIHI has operations across Europe, the Americas and Asia. SIHI anticipates FY2014 sales of approximately €280 million ($350 million) with EBITDA of approximately €30 million ($37.5 million) and gross margins approaching 30 percent.

By 2016, it was clear that Flowserve needed fresh leadership and a new strategic direction. The company had strong market positions and valuable assets, but it had struggled to translate those advantages into consistent growth and shareholder returns. The time was ripe for transformation.

The Scott Rowe Era & Transformation (2017–Present)

In April 2017, Flowserve announced a change at the top that would fundamentally reshape the company's trajectory. R. Scott Rowe has served as President and Chief Executive Officer since April 2017. Prior to joining Flowserve, Mr. Rowe served as President of the Cameron Group, a position he assumed in April 2016 following the merger between Schlumberger and Cameron International Corporation, formerly a NYSE-listed leading provider of flow management equipment, systems and services to the worldwide oil and gas industry. At Cameron, Mr. Rowe served in a variety of progressive roles during his 14-year career, culminating as its President and CEO.

Rowe's background was ideally suited for Flowserve's challenges. My time in the U.S. Army played a significant role in molding me into who I am today. It shaped me as a person and a leader; that experience has been invaluable as I moved into business. After transitioning into the corporate world, I found a home in the manufacturing and flow control industry, and I have enjoyed it ever since.

Pre-merger joint venture between Cameron and Schlumberger, which formed OneSubsea, a $3 billion dollar business that he later ran as CEO. During his tenure as President of Engineered and Process Valves, Mr. Rowe spearheaded process improvement projects that drove strong revenue and earnings growth.

Rowe brought an operator's mindset to a company that had been managed more as a portfolio of acquired businesses than as an integrated operating company. His diagnosis was clear: Flowserve had tremendous assets—world-class brands, deep customer relationships, a massive installed base—but had never fully leveraged those assets into operational excellence.

The strategic framework Rowe introduced became known as the "3D Strategy." We are leaning into our 3D strategy to diversify, decarbonize, and digitize so that we are fully enabling our customers.

Our strategy to diversify, decarbonize and digitize or the 3D growth strategy supports and aligns directly with Flowserve's long-standing purpose statement to provide extraordinary flow control solutions to make the world better for everyone. To be clear, we continue to fully support our customers in the traditional markets, where we continue to expect long-term growth. Our 3D strategy is designed to allow us to capitalize more broadly on the opportunities available within the entire flow control space by addressing our customers' increased focus on efficiency and providing the flow control solutions that enable the energy transition journey.

Diversify meant reducing dependence on traditional oil and gas by expanding into water management, chemicals, general industries, and emerging markets. Decarbonize meant positioning Flowserve's products and services to enable customers' own decarbonization journeys—whether that meant more efficient pumps, carbon capture equipment, hydrogen infrastructure, or nuclear power. Digitize meant transforming Flowserve from a purely physical product company into a technology-enabled solutions provider.

The digitization pillar found its most tangible expression in RedRaven. RedRaven is Flowserve's complete end-to-end Internet of Things (IoT) solution for the industrial space— a turn-key offering from sensors to cloud architecture, analytics and condition monitoring and predictive analytics services — so you can reliably and cost-effectively monitor thousands of assets over sprawling facilities.

When we introduced our complete IoT solution, RedRaven, in 2021, we saw a strong response from our customers and business partners who wanted to learn more about digitization and begin their IOT journey.

RedRaven reduces maintenance costs by 40%, health and safety risks by 14%, and extends asset life by 20%. These aren't incremental improvements—they represent a fundamental shift in how industrial equipment is managed.

The operational transformation reached a new level in 2024 with the formal launch of the Flowserve Business System. We made significant progress throughout 2024, launching the Flowserve Business System and leveraging our 3D strategy to drive solid top-line growth, expand margins, increase adjusted earnings, and deliver strong cash flow.

In addition to our significant 3D Growth Strategy progress, we also launched our new Flowserve Business System in 2024 that is driving results and process consistency as we advance our operational excellence and portfolio excellence initiatives. Additionally, we completed the acquisition of MOGAS Industries, expanding our severe service flow control offering in attractive mining, mineral extraction and process industries and demonstrating our commitment to disciplined, value-creating capital allocation.

Our Operational Excellence program is improving delivery times and productivity within our operations. Portfolio Excellence is in its early stages, but the 80/20 approach we're taking for product management and portfolio optimization has already started showing promising results as we eliminate the inherent complexity within our portfolio. Commercial Excellence will roll out in the second half of 2025 and focus on pricing discipline, account management and funnel management. And finally, Innovation Excellence will play a critical role in differentiating ourselves from our competitors through new product technologies and solutions.

The results under Rowe's leadership have been tangible. Power bookings increased more than 40% year-over-year, with over $110 million in nuclear awards during the fourth quarter; Gross margin and adjusted gross margin of 31.5% and 32.8%, respectively, increased 240 and 300 basis points versus the prior year period; Operating income and adjusted operating income of $125 million and $149 million, respectively, an increase of 14% and 22% compared to last year.

Initiated full-year 2025 guidance, including organic sales growth of 3% to 5% and adjusted Earnings Per Share (EPS) of $3.10 to $3.30, which at the midpoint, represents a 22% increase versus full-year 2024 adjusted EPS.

Recent Strategic Moves & M&A (2023–2025)

The past two years have seen Flowserve navigate complex M&A dynamics that reveal both its strategic ambitions and its capital discipline.

In early 2023, Flowserve announced plans to acquire Velan Inc., a leading Canadian manufacturer of industrial valves. Flowserve will acquire Velan in an all cash transaction valued at approximately $245 million. The transaction meets Flowserve's disciplined financial criteria, bringing meaningful aftermarket revenue and synergy opportunities and expects to close by end of the second quarter of 2023.

Founded in Montreal in 1950, Velan is a leading manufacturer of industrial valves with a strong presence in the nuclear, cryogenic and defense markets. As a separate entity, Velan's unique differences are what will make us stronger and better together. Velan's products have very little overlap with our existing product portfolio. With its strong positioning in the nuclear, cryogenic, industrial, and defense markets, we are looking at a highly complementary product portfolio.

However, the Velan deal encountered unexpected obstacles. French authorities have informed both Flowserve and Velan that they will not provide the requisite regulatory approval for the sale of Velan to Flowserve.

Flowserve president and CEO, Scott Rowe, said: "We are obviously disappointed with the French government's decision. We do not believe the decision aligns with the French government's stated goal of encouraging foreign investment into France's economy. Throughout this process, Flowserve worked diligently and proactively to address all of the concerns that were raised by the French government. We were optimistic about the acquisition of Velan and the numerous benefits this would provide for both companies and their stakeholders."

While the Velan deal was blocked, Flowserve successfully completed another strategic acquisition in 2024. "We welcome the MOGAS team to Flowserve and look forward to leveraging our industry-leading scale to expand the MOGAS severe service portfolio and aftermarket services to customers around the world," said Scott Rowe, President and CEO of Flowserve. "This acquisition accelerates growth under our 3D strategy and enhances our valve aftermarket business with MOGAS' large installed base."

As previously disclosed, Flowserve used cash to fund the transaction's purchase price of approximately $305 MM including the potential earnout.

The most dramatic M&A development came in 2025. Chart Industries, Inc. (NYSE: GTLS) and Flowserve Corporation (NYSE: FLS) today announced that they have entered into a definitive agreement to combine in an all-stock merger of equals, creating a differentiated leader in industrial process technologies. The combined company is expected to have an enterprise value of approximately $19 billion based on the exchange ratio and the closing share prices for Chart and Flowserve as of June 3, 2025.

The Chart deal would have been transformational—combining Flowserve's flow control leadership with Chart's expertise in cryogenic equipment, LNG infrastructure, and specialty process technologies. But it was not to be.

Flowserve terminated its previously announced merger agreement for Flowserve to combine with Chart Industries. The termination follows the Flowserve Board of Directors' decision not to submit a revised offer to merge with Chart, after being notified that Chart's Board of Directors had determined that a recent unsolicited acquisition proposal from Baker Hughes constituted a "superior proposal" under the terms of the merger agreement. In accordance with the terms of the merger agreement, Flowserve will receive a $266 million termination payment.

"The decision not to pursue a revised offer for Chart demonstrates our commitment to financial discipline, as well as our confidence in the growth prospects of our standalone business," said Flowserve President and CEO Scott Rowe.

The $266 million termination fee was a substantial consolation prize—and demonstrated the value Flowserve had extracted simply by negotiating a well-structured merger agreement. This capital discipline, walking away from an escalating bidding war rather than overpaying, reflects mature capital allocation thinking.

Business Model Deep Dive

Understanding Flowserve's competitive position requires understanding the elegance of its business model, which creates multiple layers of recurring revenue and customer lock-in.

The Flowserve Corporation designs develops, and manufactures precision-engineered flow control equipment. They play a critical role in controlling, moving, and protecting material flow associated with critical processes across some industries such as chemical, oil & gas, water management, and power generation. The company offers a comprehensive portfolio of products that include valves, pumps, and seals, as well as automation and aftermarket services directed at global infrastructure industries.

Flowserve operates through two primary segments. The primary driver behind last 12 months revenue was the Flowserve Pump Division (FPD) segment contributing a total revenue of US$3.16b (69% of total revenue). The Flow Control Division (FCD) handles valves, actuators, and related products.

The Aftermarket Flywheel

The genius of Flowserve's business model lies in the aftermarket. Every pump, valve, and seal the company sells creates decades of follow-on demand. Flowserve's equipment operates in harsh environments—high temperatures, high pressures, corrosive chemicals, abrasive particles. Parts wear out. Seals fail. Impellers erode. And when they do, customers don't have time to shop around—they need replacement parts immediately.

Bookings of $1.25 billion were the highest quarterly level since 2014 and includes record aftermarket activity of more than $610 million. When more than half of quarterly bookings come from aftermarket, the business has a substantial recurring revenue base that smooths cyclicality.

The Service Network

The latest count is an astonishing 25 training locations worldwide, with 26 employees ready to serve students and still growing. Rapid-response service, enabled by a global network of more than 200 Quick Response Centers (QRCs).

At Flowserve, we have developed a cohesive network of Quick Response Centers (QRC) located throughout Europe, Middle East and Africa (EMA) cooperating and leveraging their collective capabilities, ready to meet your needs. Flowserve's QRCs provide the highest level of service including 24-hour emergency repair and on-site repair with mobile repair units.

This service infrastructure is nearly impossible for competitors to replicate quickly. When a refinery pump fails at 3 AM on a Sunday, the company that can dispatch a technician within hours—not days—wins the customer relationship forever.

End Market Diversification

Chemical processing: acid transfer, caustic and chlor-alkali, pharmaceuticals, polymers, slurry processing, solvents, volatile organic compounds, waste processing, auxiliary; Water resources: water supply and distribution, water treatment, desalination, flood control, ground water development and irrigation, wastewater collection and treatment, snowmaking; General industry: mining, primary metals, pulp and paper.

This diversification across end markets provides natural hedging. When oil and gas capex collapses, chemical spending might hold up. When industrial investment slows, water infrastructure often accelerates (since it's often funded by municipal budgets on different cycles).

The Training Infrastructure

Over the years, Flowserve has extended their training centers in every region of the global market with main training centers in each region: Irving, Texas for North America, Etten-Leur, The Netherlands for Europe-Middle East-Africa, Rio de Janeiro, Brazil for Latin America, and Singapore for Asia Pacific. These main training locations are all equipped with classrooms, static power labs with complete pumping systems, and specialized practical training material.

Training customers on Flowserve equipment creates deep relationships and switching costs. Once a plant's maintenance team is trained on Flowserve products, changing to a competitor means retraining—a significant hidden cost.

Playbook: Business & Investing Lessons

Flowserve's 230-year journey offers several lessons for business builders and investors alike.

Building Through Acquisition: The Art of Industrial Roll-ups

Flowserve demonstrates how to execute a successful roll-up strategy. Key elements include: acquiring companies with complementary (not redundant) product lines; focusing on brands with strong customer loyalty and installed base; integrating aggressively to capture synergies; and building shared infrastructure (service networks, training, IT systems) that benefits the entire portfolio.

Managing Cyclicality Through Aftermarket Services

The strategic pivot toward services—from the ServiceRepair Division in 1997 to the Quick Response Centers today—transformed Flowserve from a purely cyclical equipment company into a business with substantial recurring revenue. When new equipment orders collapse during downturns, aftermarket revenue provides stability.

Digital Transformation in Industrial Equipment

RedRaven shows how traditional industrial companies can evolve into technology-enabled businesses. The IoT platform doesn't just add revenue—it deepens customer relationships by making Flowserve an essential partner in operations, not just an equipment supplier.

ESG Positioning

Flowserve formally commits to reducing carbon emission intensity by 40% by 2030 and signs the WASH pledge, committing to safe water, sanitation and hygiene access in all its facilities.

In 2019, Flowserve set out to achieve a 40% reduction in its carbon intensity by the year 2030, using 2015 as a baseline year. The company achieved that goal in 2023, reducing its carbon intensity by 46%.

Flowserve recognized early that its customers would face increasing pressure to decarbonize—and that this created opportunity, not just risk. The 3D strategy positions the company to benefit whether customers are investing in hydrogen, carbon capture, nuclear power, or simply making existing operations more efficient.

Capital Discipline: Walking Away

"Flowserve is executing from a position of clear strength, driven by sustained financial momentum, impressive operational performance, and continued robust global demand for our mission-critical flow control solutions across the industrial spectrum," President and CEO Scott Rowe said in a statement. "The decision not to pursue a revised offer for Chart demonstrates our commitment to financial discipline, as well as our confidence in the growth prospects of our standalone business."

The Chart deal termination, with its $266 million breakup fee, demonstrates that Flowserve's management won't chase deals at any price. This discipline is essential for long-term value creation.

Porter's Five Forces Analysis

1. Threat of New Entrants: LOW

The barriers to entry in Flowserve's markets are formidable. Manufacturing precision pumps, valves, and seals requires decades of accumulated know-how. With more than 5,000 pumps and 15,000 valves installed in over 200 nuclear reactors worldwide, it's obvious that Flowserve is an industry leader in the nuclear space. In fact, we have played a critical role in the development of the nuclear power industry from its birth in the 1950's, having achieved certified supplier status with several Generation III reactor design firms.

Certifications (API, ASME, ISO, nuclear-specific) take years to obtain. The global service network—more than 200 Quick Response Centers—represents billions in cumulative investment impossible for a new entrant to replicate quickly.

2. Bargaining Power of Suppliers: MODERATE

Flowserve requires specialized materials (high-performance alloys, engineered castings) from a limited supplier base. Long-term relationships and Flowserve's purchasing scale mitigate this risk. Some vertical integration (foundry operations, for example) further reduces dependence.

3. Bargaining Power of Buyers: MODERATE

Large customers (major oil companies, utilities, national oil companies) have significant negotiating leverage. However, switching costs are substantial. Once a refinery is designed around Flowserve pumps, replacing them with a competitor's equipment means redesigning piping, electrical systems, and control interfaces. The mission-critical nature of the equipment—a pump failure can shut down an entire production line—limits pure price-based purchasing decisions.

4. Threat of Substitutes: LOW

There is no substitute for pumps, valves, and seals in industrial processes. Fluids must be moved, controlled, and contained—there's no alternative technology that eliminates the need for these components. Digital solutions like RedRaven complement rather than substitute for physical equipment.

5. Industry Rivalry: MODERATE-HIGH

Principal Competitors: IDEX Corporation; Roper Industries, Inc. Competition also comes from Sulzer, Parker Hannifin, Emerson, and other diversified industrials. The industry continues consolidating, with competitors pursuing similar roll-up strategies. Competition centers on technology, service capability, and total cost of ownership rather than pure price.

Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG

Flowserve Corporation is a global leader in the design, manufacture, marketing, and maintenance of fluid-handling equipment. It is the world's second largest producer of industrial pumps as well as valves.

Scale spreads R&D costs across larger revenue, enables purchasing power for raw materials, and allows investment in service infrastructure that smaller competitors cannot match.

2. Network Effects: MODERATE

The global service network creates network-like benefits—every QRC added makes the entire network more valuable to customers with operations in multiple regions. The training infrastructure creates an ecosystem of Flowserve-proficient technicians worldwide.

3. Counter-Positioning: MODERATE

The 3D strategy positions Flowserve for energy transition in ways that competitors focused purely on traditional oil and gas may struggle to follow. Investments in hydrogen, carbon capture, and nuclear capabilities create future optionality that current competitors might be slow to replicate.

4. Switching Costs: VERY STRONG

This is Flowserve's most powerful competitive advantage. Once installed, Flowserve equipment generates decades of aftermarket demand. Engineering specifications are locked into customer processes. Training investments create organizational lock-in. Downtime costs of switching are enormous in refineries and power plants where every hour offline can cost millions.

5. Branding: MODERATE

Heritage brands (Durco, Valtek, Worcester, Limitorque, Ingersoll-Rand, Worthington) command strong recognition among industry professionals. Flowserve's many brands include Durco (pumps), Valtek (valves), and GASPAC (seals). These aren't consumer brands—they're trusted names among plant engineers who stake their careers on equipment reliability.

6. Cornered Resource: MODERATE

Deep engineering expertise accumulated over more than two centuries represents institutional knowledge that cannot be easily acquired. Patents on specific seal and valve technologies provide temporary monopolies. Application-specific knowledge—understanding how particular equipment performs in specific chemical processes—gives Flowserve advantages in technical specification competitions.

7. Process Power: STRONG

The business system is intentionally wrapped with culture, strategy and execution because a winning company has to be great at each one. In 2024, we had all three working together in harmony and it showed in our outstanding results.

The Flowserve Business System represents codified operational excellence developed through decades of experience. Service turnaround capabilities—the ability to repair equipment faster and better than competitors—create tangible competitive advantage in aftermarket business.

Bull vs. Bear Case

The Bull Case

Energy Transition Creates Demand for New Infrastructure

Power bookings increased more than 40% year-over-year, with over $110 million in nuclear awards during the fourth quarter.

The nuclear renaissance is real. Countries worldwide are extending existing reactor licenses and building new capacity. Every nuclear plant needs thousands of Flowserve pumps and valves. Similarly, hydrogen infrastructure, carbon capture systems, and LNG facilities all require extensive flow control equipment. The energy transition doesn't eliminate Flowserve's addressable market—it expands it.

Aftermarket Revenues Provide Stability

With record aftermarket bookings exceeding $600 million quarterly, Flowserve has a substantial base of recurring revenue that smooths cyclical volatility. The massive installed base continues generating demand for decades.

Operational Transformation Gaining Traction

Initiated full-year 2025 guidance, including organic sales growth of 3% to 5% and adjusted Earnings Per Share (EPS) of $3.10 to $3.30, which at the midpoint, represents a 22% increase versus full-year 2024 adjusted EPS.

The Flowserve Business System is driving meaningful margin expansion and earnings growth. If management continues executing, there's substantial room for continued improvement.

Disciplined M&A Creates Value

The MOGAS acquisition expanded Flowserve's severe service valve portfolio. The decision to walk away from Chart (while collecting $266 million) demonstrated capital discipline. The company has the balance sheet capacity for value-creating deals.

The Bear Case

Cyclical Exposure Remains

Despite diversification efforts, Flowserve remains exposed to oil and gas capital spending cycles. A prolonged downturn in commodity prices could pressure original equipment orders.

Regulatory and Geopolitical Risks

The failed Velan acquisition highlighted how regulatory intervention can derail strategic plans. As governments become more protective of industrial assets, cross-border M&A may face increasing obstacles.

Competitive Intensity

Baker Hughes's $13.6 billion acquisition of Chart Industries shows that deep-pocketed competitors are pursuing similar strategies. The flow control industry continues consolidating, and Flowserve may find attractive acquisition targets increasingly expensive or unavailable.

Execution Risk

The Flowserve Business System is still in early stages. Portfolio Excellence, Commercial Excellence, and Innovation Excellence programs are rolling out over multiple years. Any stumbles in execution could disappoint investors expecting continued improvement.

Key Metrics to Watch

For long-term investors tracking Flowserve, three metrics matter most:

1. Aftermarket Bookings as Percentage of Total Bookings

This metric reveals the quality and stability of Flowserve's revenue base. Higher aftermarket mix means more recurring, higher-margin revenue. Current levels above 50% of quarterly bookings are healthy; any significant decline would signal potential trouble.

2. Book-to-Bill Ratio

The book-to-bill ratio (orders divided by revenue) indicates future revenue trajectory. A ratio above 1.0x means backlog is growing, supporting future revenue. Flowserve's recent quarters above 1.0x suggest healthy demand conditions.

3. Adjusted Operating Margin

Adjusted operating margin captures the company's ability to translate revenue into profit. The Flowserve Business System is targeting meaningful expansion; progress (or lack thereof) will show up in this metric. Recent quarters around 11-12.5% represent improvement from historical levels; management has indicated targets approaching mid-teens.

Conclusion: The Hidden Giant

Flowserve occupies a peculiar position in the investor consciousness. It's not a household name. It doesn't produce exciting consumer products or breakthrough technologies. Its products are buried underground, hidden inside steel vessels, tucked away in equipment rooms that most people never see.

Yet Flowserve's pumps, valves, and seals are essential infrastructure—literally the arteries and valves of industrial civilization. Without them, oil doesn't flow, power doesn't generate, water doesn't reach taps, and chemicals don't transform into the products modern life depends upon.

The company's 230-year heritage represents institutional knowledge that simply cannot be replicated. Its global service network of over 200 Quick Response Centers provides capability that competitors cannot quickly match. Its massive installed base generates reliable aftermarket revenue year after year, decade after decade.

Under Scott Rowe's leadership, Flowserve has articulated a coherent strategy—Diversify, Decarbonize, Digitize—that positions the company to thrive regardless of which energy future unfolds. Whether the world burns more natural gas, builds more nuclear plants, deploys hydrogen infrastructure, or captures carbon, Flowserve's equipment will be essential.

The Flowserve Business System represents the operational transformation that converts strategic vision into financial results. Early evidence suggests real progress: margins expanding, earnings growing, cash flow strengthening.

No investment is without risk. Cyclicality remains. Execution could stumble. Competitors are aggressive. But for investors seeking exposure to essential infrastructure—companies that benefit from virtually any capex scenario—Flowserve deserves consideration.

The hidden giant of flow control has survived 230 years. It has navigated technological revolutions, economic depressions, world wars, and industry transformations. The current moment, with its energy transition uncertainties and infrastructure investment opportunities, may prove another chapter in a very long story.

Material Regulatory Overhang

Investors should note that Flowserve has historical regulatory issues including the 2005 SEC Regulation FD settlement and the UN Oil-for-Food FCPA matter. These are resolved matters but reflect the importance of continued attention to compliance culture. No material outstanding regulatory matters are currently disclosed.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube