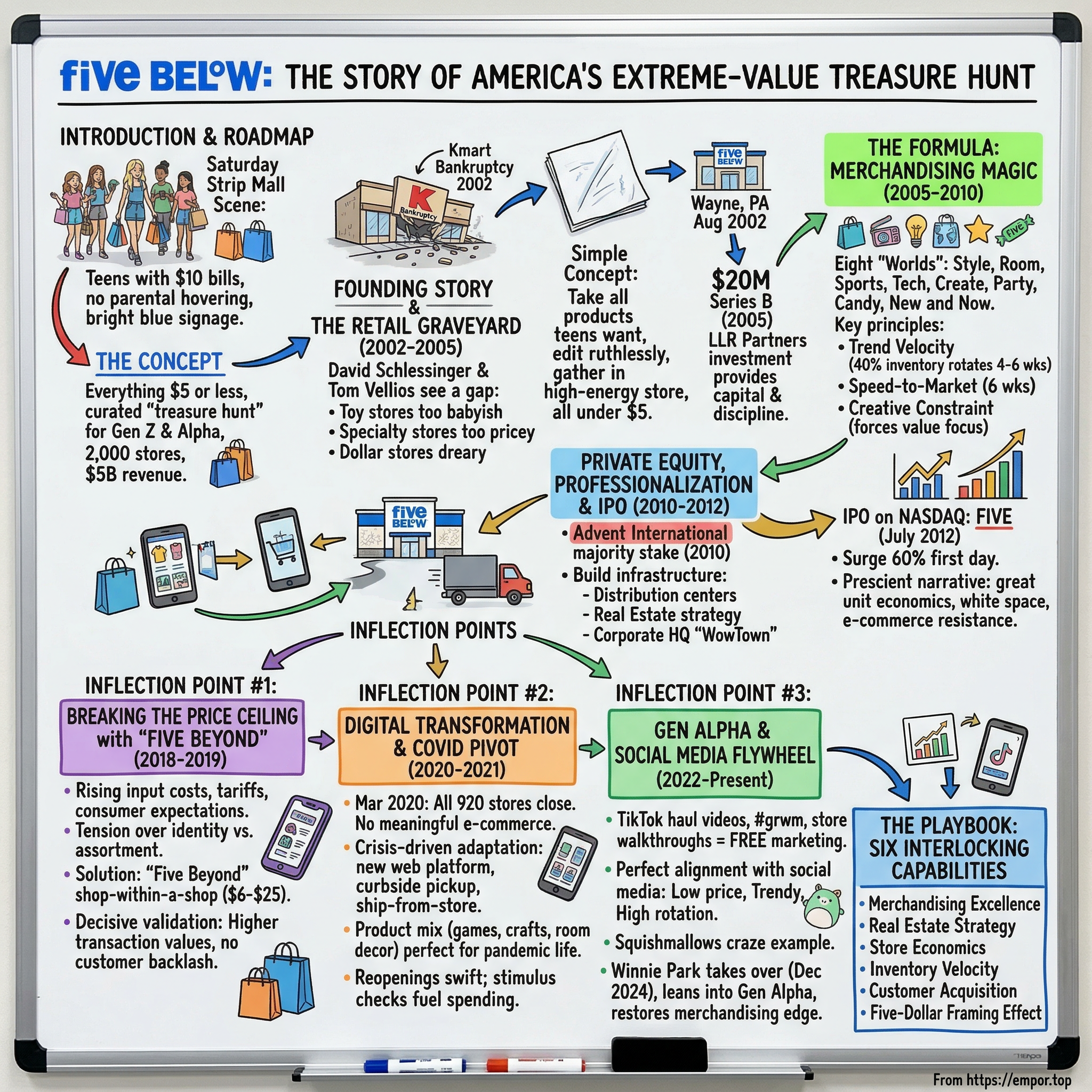

Five Below: The Story of America's Extreme-Value Treasure Hunt

Introduction and Episode Roadmap

Picture a Saturday afternoon at a strip mall somewhere in suburban America. A group of three teenage girls tumbles out of a minivan, ten-dollar bills in hand, heading for a store with bright blue signage and an energy that spills out through the open doors. Inside, they scatter across the aisles: one gravitating toward the wall of phone cases and tech accessories, another making a beeline for the candy section, and the third already loading up on LED string lights and decorative pillows for her bedroom. Twenty minutes later, they reconvene at the register, each clutching a plastic bag stuffed with three, four, five items. Total damage: about eight dollars each.

No parent hovering. No sticker shock. No buyer's remorse. That store exists in nearly two thousand locations across forty-six states, and it has quietly become one of the most remarkable retail stories of the twenty-first century.

Five Below is a retailer where almost everything costs five dollars or less, though in recent years the company has strategically expanded beyond that iconic ceiling. With nearly five billion dollars in projected annual revenue, a store count approaching two thousand, and a stock that has nearly quadrupled off its 2024 lows, Five Below occupies a fascinating intersection of discount retail, teen culture, and merchandising artistry that defies easy categorization.

The central question of this story is deceptively simple: How did a single store in suburban Philadelphia, founded in 2002 by two guys who had just watched their previous retail venture go bankrupt, become a nearly twelve-billion-dollar phenomenon that cracked the code on selling to Gen Z and Gen Alpha? The answer touches on everything from the psychology of impulse buying to the power of TikTok haul videos, from the collapse of traditional mall retail to the surprising resilience of physical stores in the Amazon age.

What makes Five Below's story genuinely compelling is that it should not have worked. Opening a brick-and-mortar chain in 2002, just as e-commerce was beginning its assault on physical retail, targeting teenagers with their notoriously fickle tastes, and capping prices at five dollars in an era of rising costs: any one of these constraints should have been fatal. Instead, each became a source of creative energy and competitive advantage.

This deep dive will trace three pivotal inflection points that transformed Five Below from a regional curiosity into a national powerhouse. First, the decision to break the sacred five-dollar price ceiling with the "Five Beyond" concept. Second, the COVID-era digital pivot that proved the company's products were pandemic-proof. And third, the social media flywheel that turned Gen Z and Gen Alpha shoppers into unpaid marketing ambassadors. Along the way, we will unpack the merchandising playbook, assess the competitive moat through the lens of Hamilton Helmer's Seven Powers framework, and confront the existential question that hangs over the business today: can a retailer built on cheap Chinese imports survive in an era of tariff warfare?

Founding Story and the Retail Graveyard Context (2002-2005)

To appreciate what David Schlessinger and Tom Vellios were attempting when they opened the first Five Below store, you need to understand just how bleak the retail landscape looked in 2002. The dot-com bubble had burst. Amazon was rapidly expanding beyond books into general merchandise. Kmart had filed for bankruptcy in January 2002. Circuit City was struggling. And the prevailing wisdom among investors, analysts, and retail executives was that physical retail was entering a long, slow decline. Opening a new brick-and-mortar chain in this environment was roughly as contrarian as launching a newspaper in the age of blogs.

In the spring of 2001, a children's educational toy retailer called Zany Brainy was filing for bankruptcy. The chain, which had grown to over two hundred locations across the United States, had expanded too fast, stretched its logistics too thin, and misjudged the market's appetite for educational toys at premium price points. For the two men at its helm, the collapse was both devastating and illuminating.

David Schlessinger had started his retail career at the improbable age of eighteen, founding Encore Books in 1973, a discount bookstore chain he ran for thirteen years. In 1991, he launched Zany Brainy with an ambitious vision: curate the best educational products for children and create immersive in-store experiences that parents would love. Tom Vellios joined as CEO after Schlessinger transitioned to the chairman role, and together they built a chain that at its peak seemed poised to become the thinking parent's alternative to Toys "R" Us. But the business model had a fatal flaw. It was built around what parents wanted to buy for their children, not what children wanted to buy for themselves.

Both Schlessinger and Vellios had preteen sons at the time, and they watched their boys navigate an awkward retail no-man's-land. Toy stores felt babyish. Specialty retailers charged too much. Dollar stores were depressing, cluttered caverns where nothing felt curated or cool. And the emerging e-commerce platforms of the early 2000s lacked the tactile thrill of browsing physical shelves. There was a gap in the market, and the two men could see it with the clarity that comes from having just watched a business fail.

The two men spent months studying the retail landscape, visiting dollar stores, discount chains, and specialty retailers across the Northeast, looking for the gap they sensed existed. What they found confirmed their hypothesis. Dollar stores like Dollar Tree and the then-nascent Dollar General served a lower-income, needs-based customer with a product mix heavy on household essentials: cleaning supplies, canned goods, paper towels. The shopping experience was utilitarian and often dreary. At the other end of the spectrum, specialty retailers like Hot Topic and Spencer's sold trend-driven products to teens at premium markups. In between, there was nothing: no retailer combining the energy and trend-awareness of specialty retail with the democratized pricing of discount.

The concept they sketched out, reportedly on a napkin at a local coffee shop, was elegantly simple: take the entire universe of products that teens and tweens actually want, edit ruthlessly, and gather the best of it into one high-energy store where everything costs five dollars or less. The inspiration drew from TJ Maxx and HomeGoods and their treasure-hunt shopping model, but reimagined it for a younger, more price-sensitive customer. The genius was in the constraint. A five-dollar ceiling forced brutal discipline on the buying team: no filler products, no compromises on trendiness, and an unrelenting focus on perceived value.

The first Five Below store opened in Wayne, Pennsylvania in August 2002. Wayne is an affluent suburb on Philadelphia's Main Line, which was itself a deliberate choice. The founders wanted to prove that the concept worked not because customers were poor and had no alternatives, but because the shopping experience was genuinely compelling. The early store featured bright colors, open sightlines, and a product mix that ranged from tech accessories and candy to sports gear and room décor. It felt less like a discount store and more like a curated festival of stuff.

The validation was immediate and visceral. Lines formed. Kids dragged their parents back. College students discovered it. Families realized they could let their children wander freely without worrying about a hundred-dollar checkout surprise. In those first months, the founders observed something that would prove foundational to the entire business: kids were spending their own money. Allowances, birthday cash, babysitting earnings. This was not a parent-driven purchase decision. It was a child choosing to spend, and that psychological shift changed everything about how the store merchandised, marketed, and expanded.

By 2005, Five Below had grown to roughly eighty stores, but the company had not yet reached profitability. The founders had bootstrapped the early expansion through friends-and-family money, and the pace of growth was straining their capital base. That April, LLR Partners, a Philadelphia-based private equity firm, invested twenty million dollars in a Series B round, the company's first institutional capital. A subsequent seventeen-million-dollar follow-on from LLR and Blue 9 Capital provided additional runway. The money was critical, but so was the operational discipline that came with professional investors asking hard questions about unit economics, lease terms, and inventory management.

The timing of Five Below's founding deserves emphasis because it reveals something important about the founders' character. Schlessinger and Vellios had every reason to walk away from retail entirely. They had just lived through the humiliation of a bankruptcy. The industry they knew best was under siege from e-commerce. Friends and family money is particularly painful to lose. And yet they chose to go again, because they believed so deeply in the insight they had uncovered: that there was a vast, underserved market of young consumers who wanted the thrill of shopping without the burden of high prices. That conviction, tested by failure and sustained through uncertainty, is what separates entrepreneurs who build lasting businesses from those who try once and retreat.

What the founders understood even in those early years, and what would take Wall Street another decade to fully appreciate, was that Five Below was not a dollar store. It was a specialty retailer wearing discount-store clothes. The competition was not Dollar Tree or Dollar General but rather the impulse-buy section at Target, the clearance rack at Urban Outfitters, and increasingly, the entire internet. The five-dollar price point was not a limitation but a permission structure, a psychological invitation to buy multiple items without guilt. And that insight, more than any single product or marketing campaign, was the foundation upon which everything else would be built.

The Formula: Merchandising Magic and the "Worlds" Concept (2005-2010)

With the institutional capital secured and the concept validated, the question became: what exactly makes Five Below work, and can it be bottled and replicated across hundreds of locations?

Walk into a Five Below store in 2008, and the first thing that hit you was the energy. The lighting was bright, almost aggressively so. The floors were polished concrete. Music played at a volume that would make a librarian wince but made a thirteen-year-old feel like they had arrived somewhere worth being. The layout was open, with low shelving that allowed sightlines across the entire store, and the merchandise was organized not by traditional retail categories but by something Five Below called "worlds."

Eight themed worlds, each occupying its own section of the store: Style, Room, Sports, Tech, Create, Party, Candy, and New and Now. The naming was deliberate. These were not departments. They were destinations, each with its own color palette, signage, and curated product assortment. Walk through Tech and you would find phone cases, earbuds, charging cables, and Bluetooth speakers, all at five dollars or less. Wander into Room and there were LED string lights, decorative pillows, wall art, and desk organizers. Candy was an entire wall of sugar in every conceivable form. And New and Now was the constantly rotating section where the buying team dropped whatever was trending that week.

This "worlds" concept was Five Below's answer to one of retail's oldest problems: how do you create a browsing experience that feels intentional rather than overwhelming? Dollar stores had historically failed at this. Walk into a typical dollar store in the mid-2000s and you would find a jumble of cheap goods crammed onto metal shelves under fluorescent lighting, organized by whatever made logistics easiest rather than what made shopping enjoyable. Five Below flipped this entirely. The merchandise was inexpensive, but the experience was designed to feel premium, or at least premium-adjacent.

The merchandising philosophy rested on several interconnected principles that the buying team refined over these formative years. First, trend velocity. The team maintained an inventory of roughly four thousand SKUs at any given time, deliberately lean compared to Dollar Tree's eight thousand or Walmart's hundred-and-forty-thousand-plus. But approximately forty percent of that inventory rotated every four to six weeks, meaning the product mix was in constant motion. A customer who visited every two weeks would find meaningfully different merchandise each time, creating the dopamine hit of discovery that retailers call the "treasure hunt effect."

Second, the buying team operated with a speed-to-market capability that larger competitors could not match. From the moment a trend was identified, whether through social media monitoring, sales data analysis, or old-fashioned buyer intuition, new products could appear in stores within six weeks. This was not fast fashion speed, but it was remarkably quick for a physical retailer sourcing primarily from overseas manufacturers. When a particular phone case design went viral, when a new candy brand started trending on social media, when a specific style of room décor began appearing in teen influencer posts, Five Below's buyers could have a version on shelves before the trend peaked.

Third, the five-dollar ceiling imposed what the founders called "creative constraint." Every product had to clear a profitability threshold at five dollars retail, which meant the buying team became extraordinarily skilled at identifying products that delivered high perceived value at low actual cost. A Bluetooth speaker that cost two dollars to source and sold for five dollars felt like a steal to the customer and generated healthy margins for the company. The constraint forced the buyers to become merchants in the truest sense, curators rather than order-takers, constantly scouring the global market for items that met the intersection of trendy, cheap, and delightful.

The target customer evolved during this period in ways that surprised even the founders. The initial vision was tweens and teens, roughly ages eight to eighteen, spending their own money. But parents discovered that Five Below was an ideal destination for birthday party supplies, stocking stuffers, and Easter basket fillers. College students realized the stores were goldmines for dorm room essentials. Young adults found affordable gifts and impulse treats. The customer base broadened without the company ever explicitly pursuing these demographics because the fundamental value proposition, cool stuff at an irresistible price, transcended age.

The early regional expansion along the East Coast followed a disciplined pattern. Five Below moved outward from its Philadelphia base in concentric circles, entering new markets only when it had the supply chain and management capacity to maintain product freshness and store standards. New Jersey, Delaware, Maryland, Virginia, then down through the Carolinas and into Georgia and Florida. Each new market required adapting the product mix slightly to reflect local tastes and climate, but the fundamental format, the eight worlds, the price ceiling, the high-energy atmosphere, traveled without modification. By 2010, the company had established itself as the dominant player in teen and tween value retail across the eastern United States, with a store count approaching two hundred and a reputation that was beginning to generate interest from institutional investors.

By the end of this period, Five Below had established the operational playbook that would fuel its national expansion: a distinctive store format, a merchandising philosophy built on trend velocity and creative constraint, and a customer experience that made discount shopping feel like entertainment. The challenge now was scaling it.

Private Equity, Professionalization, and IPO Preparation (2010-2012)

By 2010, Five Below had proven the concept but had not yet proven that it could scale nationally. The company had roughly two hundred stores, concentrated almost entirely on the East Coast, and was generating healthy revenue growth but needed significant capital to fund the expansion that management believed the model could support. The founders faced a classic entrepreneurial crossroads: continue growing slowly with internally generated cash flow, or bring in a partner with the resources and expertise to accelerate the timeline.

In October 2010, Advent International, one of the largest global private equity firms, acquired a majority stake in Five Below for approximately one hundred and ninety-three million dollars. LLR Partners and the founding team retained significant positions alongside the new majority owner, but the deal marked a fundamental shift in the company's trajectory. Five Below was no longer a regional retailer run by entrepreneurial founders. It was now a private equity portfolio company with a clear mandate: professionalize, optimize, and prepare for a public offering.

Advent International's involvement brought the kind of institutional rigor that fast-growing retail chains desperately need and often lack. The private equity firm had deep experience in consumer and retail businesses, and its operating partners systematically addressed the gaps that separate a two-hundred-store regional chain from a national retail platform. Supply chain operations were overhauled, starting with the construction of the company's first purpose-built distribution center in New Castle, Delaware, replacing a patchwork of leased warehouse space that had been adequate for a regional chain but would buckle under the weight of a national rollout. Real estate strategy was formalized, with analytical frameworks for site selection, lease negotiation, and market-entry sequencing that turned the founders' intuitive approach into a repeatable, data-driven process. Human resources systems were built to support the hiring, training, and retention of thousands of store-level employees across multiple states.

The professionalization extended to the company's corporate headquarters, which eventually moved to the historic Lit Brothers Building on Market Street in Philadelphia, a 190,000-square-foot space the company christened "WowTown." The name was characteristic of Five Below's culture: playful, energetic, and deliberately un-corporate. The headquarters housed more than three hundred employees, including the critical merchant team whose trend-spotting instincts drove the entire business.

The merchant team, Five Below's most critical competitive asset, was expanded and given additional resources. Buyers were sent deeper into Asian manufacturing hubs. Sourcing relationships were diversified. Quality control processes were tightened. The goal was not to change what Five Below did but to make it do what it already did at dramatically greater scale without losing the entrepreneurial energy and trend-spotting instinct that made it special.

By 2012, the numbers told a compelling growth story. The company had crossed two hundred stores and was generating approximately three hundred and twenty-two million dollars in annual revenue. Same-store sales growth was consistently positive. Unit economics were attractive: each new store cost roughly four hundred thousand dollars to open, generated approximately two million dollars in first-year revenue, earned roughly twenty-five percent four-wall EBITDA margins, and paid back its initial investment in less than a year. That seven-month payback period was extraordinary for physical retail, where two-to-three-year paybacks are considered good and five-year paybacks are common.

The question facing Advent and the Five Below management team was not whether to go public but when. The company's growth trajectory was steep, its unit economics were clean, and the IPO market in 2012 was receptive to high-growth retail stories. The calculation was straightforward: going public would provide the capital needed to fund national expansion, create liquidity for early investors, and give the company the public currency and visibility that would help it recruit talent and negotiate better lease terms with landlords who valued the creditworthiness of a public company.

On July 19, 2012, Five Below went public on the NASDAQ under the ticker FIVE. The company had initially planned to raise about one hundred twenty-five million dollars by offering 9.6 million shares at a price range of twelve to fourteen dollars per share. Instead, strong investor demand pushed the IPO price to seventeen dollars, at the top of a revised range. The stock surged nearly sixty percent on its first day of trading, and by late September, FIVE was the year's sixth-best-performing IPO, up a hundred and thirty percent from its offering price.

Wall Street bought into the growth narrative for three reasons that would prove prescient. First, the unit economics were among the best in retail, with payback periods that made each new store a near-guaranteed return on capital. Second, the white-space opportunity was enormous: with only two hundred-some stores concentrated on the East Coast, the entire western half of the United States was untapped. The company's addressable market was defined not by the number of teenagers in America but by the number of high-traffic retail locations that could support a Five Below store, a number that management estimated in the thousands.

And third, the business model was inherently resistant to e-commerce disruption because the treasure-hunt experience, the impulse-driven discovery of five-dollar products, simply did not translate to online shopping. You cannot replicate the dopamine hit of wandering through a Five Below store by scrolling through a website. The average Five Below transaction was small enough that shipping costs would consume a meaningful percentage of the order value, further insulating the physical store model from online competition. This e-commerce resistance, which might have seemed like a weakness to some investors, was in fact one of the company's most valuable strategic assets.

Advent International would ultimately realize approximately 5.3 times its invested capital on the Five Below deal, making it one of the firm's home-run investments. LLR Partners, which had been the first institutional investor at a much earlier stage, likely realized an even higher multiple on its initial twenty-million-dollar investment, though specific returns have not been publicly disclosed.

For investors tracking this story, the IPO established a pattern that continues to define Five Below's equity narrative: the stock tends to trade at premium multiples reflecting the market's confidence in the company's growth runway, and it tends to sell off sharply whenever that growth narrative is questioned. This volatility is the price of admission for owning a growth retail stock. The shares declined more than fifty percent from their all-time high in 2021 to their trough in 2024, then rallied more than three hundred percent off those lows. Investors who could not stomach the drawdown missed the recovery. This pattern of sharp corrections followed by aggressive recoveries has repeated multiple times in Five Below's public market history and likely will again.

Inflection Point Number One: Breaking the Price Ceiling with Five Beyond (2018-2019)

The public market years from 2012 to 2017 were a steady crescendo of growth. Revenue roughly doubled from three hundred twenty-two million to over a billion dollars. The store count more than doubled. Same-store sales growth was consistently positive. And the stock price multiplied several times over from its IPO price, rewarding early shareholders handsomely. But as with many growth stories, the smooth ascent masked a strategic tension that was building beneath the surface.

For seventeen years, the five-dollar price ceiling was more than a business constraint. It was the company's identity, encoded in the brand name itself. Every product, every vendor negotiation, every merchandising decision flowed through a single filter: can we sell this for five dollars or less and still make money? The discipline was powerful, and it worked. But by 2017 and 2018, the math was getting increasingly difficult.

Input costs were rising across nearly every product category that mattered to Five Below. The technology accessories that anchored the Tech world, Bluetooth speakers, earbuds, phone chargers, were improving in quality and capability, but the components were getting more expensive, not less. Tariff pressures on Chinese imports, which comprised roughly sixty percent of the company's cost of goods, added further cost headwinds. And consumer expectations were rising. A teenager in 2018 expected better product quality than a teenager in 2008, because the reference point had shifted. Earbuds that sounded tinny and broke after a week were no longer acceptable, even at five dollars.

Inside the company, the debate was intense and existential. The leadership team at this point was different from the one that had founded the company. Joel Anderson had taken over as CEO from Tom Vellios in February 2015, with Vellios transitioning first to executive chairman and later to a non-executive role. Anderson brought a substantially different background to the table: twelve years at Toys "R" Us, where he had risen to executive vice president, followed by a stint as president of Walmart.com. He was an operator, not an entrepreneur, a professional manager with deep experience in large-scale retail logistics and digital commerce. His appointment signaled the board's belief that Five Below had matured beyond the founder-led startup phase and needed a CEO who could manage complexity at national scale. Anderson understood the risk from both sides of the pricing debate. Breaking the five-dollar ceiling could destroy the brand's most distinctive asset: the simple, powerful promise embedded in the name. But staying rigidly below five dollars would progressively narrow the product assortment, pushing out exactly the categories, tech, games, larger toys, that drove the most traffic and excitement.

Consider the analogy of a restaurant with a fixed-price menu. A restaurant that promises every dish for ten dollars will eventually face a choice: either the quality of ingredients declines, the portion sizes shrink, or the menu gets shorter. Five Below faced the same trilemma. The company could accept declining product quality, which would erode the brand. It could reduce the product assortment, which would narrow the appeal. Or it could break the price ceiling, which risked destroying the very thing that made the brand distinctive. There was no costless option.

In late 2019, Five Below made its move. The company introduced "Ten Below" sections in select stores, featuring items priced between six and ten dollars, primarily in technology and toy categories. Anderson was careful to frame the decision publicly, emphasizing that this was about expanding product possibilities, not abandoning the value proposition. He explicitly stated it had "nothing to do with tariffs" but reflected the reality that certain product categories simply could not deliver adequate quality at five dollars.

The concept evolved rapidly. "Ten Below" was rebranded to "Five Beyond," a name that gave the company significantly more pricing flexibility. Rather than anchoring to a new ceiling of ten dollars, "Five Beyond" implied that the sky was the limit, though in practice most items ranged from six to twenty-five dollars. The format was designed as a shop-within-a-shop, a dedicated section within each store that was visually distinct from the main Five Below merchandise. This architectural separation was psychologically important: it preserved the core five-dollar experience while introducing a premium tier that felt like a bonus rather than a betrayal.

Customer response validated the decision decisively. There was minimal backlash. Shoppers understood intuitively that a fifteen-dollar Bluetooth speaker in the Five Beyond section did not diminish the value of the three-dollar phone case in the main store. What the data revealed was even more encouraging. Customers who purchased a Five Beyond item spent more than twice as much per transaction as those who bought only from the core Five Below assortment. Converted stores saw immediate comparable sales lifts in the mid-single digits, with transaction increases exceeding fifty percent.

The product categories that benefited most from the expanded price ceiling were precisely the ones that had been most constrained at five dollars. Technology accessories were the clearest example: at five dollars, Five Below could offer basic earbuds and simple charging cables. At ten to fifteen dollars, the company could stock wireless earbuds with decent sound quality, portable Bluetooth speakers with real bass, and phone accessories that did not feel like disposable junk. Gaming accessories, larger plush toys, premium art supplies, and branded merchandise from licensed properties like Disney, Marvel, and popular gaming franchises all became viable at the Five Beyond price points. Each new product category that became accessible through higher price points deepened the store's appeal and gave customers new reasons to visit.

By 2023, Five Below had converted more than four hundred stores to the Five Beyond format and was rolling it into all new store openings. The financial impact was transformative. Higher average transaction values expanded revenue per store without requiring proportional increases in labor or occupancy costs. The margin profile improved because many Five Beyond items, particularly in technology and branded toys, carried healthy absolute dollar margins even if percentage margins were similar to sub-five-dollar products.

The rollout accelerated in subsequent years. Approximately one hundred and forty stores were converted to include Five Beyond sections in 2020, followed by another one hundred seventy to one hundred eighty in 2021. By 2022, roughly two hundred and fifty more stores had been converted, and by 2023 the total exceeded four hundred. The format became standard for all new store openings, and by 2025, the majority of the store fleet incorporated Five Beyond sections.

This was the pivotal moment in Five Below's corporate history. The company proved that a brand built on a specific price point could evolve beyond that price point without losing its identity, as long as the evolution was executed thoughtfully and the core value proposition remained intact. Dollar Tree had already demonstrated the market's tolerance for price evolution when it moved from one dollar to a dollar twenty-five in 2021, a change that was far more disruptive to Dollar Tree's model than Five Beyond was to Five Below's. The lesson for investors was clear: brand promises are about trust and perceived value, not arithmetic precision. Five Below's customers trusted the brand to deliver cool products at fair prices, and Five Beyond extended that trust into new territory.

Inflection Point Number Two: Digital Transformation and the COVID Pivot (2020-2021)

The Five Beyond experiment had proven that Five Below's brand was more elastic than anyone, including the founders, had expected. With the pricing constraint loosened, the company was poised for its next phase of accelerated growth. But the world had other plans.

On March 18, 2020, Five Below announced the temporary closure of every one of its roughly nine hundred and twenty stores across the United States. The COVID-19 pandemic had arrived, and for a retailer that generated more than ninety-five percent of its revenue from physical stores, the shutdown felt existential. Five Below had virtually no e-commerce infrastructure worth mentioning. Its digital capabilities lagged far behind peers. The website was functional but not built for the kind of high-volume direct-to-consumer fulfillment that a pandemic demanded.

For a company that had built its entire identity around physical shopping, the closure was psychologically as well as financially devastating. Five Below's stores were not just revenue generators. They were the product itself. The treasure-hunt experience, the sensory overload, the social dimension of shopping with friends, none of this could be replicated through a website. Management faced a stark question: what does Five Below even mean if the stores are closed?

What happened next was a case study in crisis-driven adaptation. Within weeks, the company had accelerated development of a new web platform, launched curbside pickup at roughly forty stores in Florida, Tennessee, California, and Texas, and begun building ship-from-store capabilities. E-commerce sales grew more than four times during the first quarter of fiscal 2020, though this was off such a small base that it barely dented the revenue lost from store closures. The digital acceleration also exposed just how dependent Five Below's business model was on physical foot traffic. Unlike retailers with established online businesses that could shift capacity to digital channels, Five Below had no meaningful digital infrastructure to fall back on. The pandemic was a wake-up call about the fragility of a single-channel business, even one whose channel was as strong as Five Below's stores.

The real story of Five Below during COVID, however, was not digital transformation. It was the discovery, almost accidental, that the company's product assortment was eerily well-suited to pandemic life. Board games, puzzles, arts and crafts supplies, room décor for bedrooms that had become home offices and classrooms, tech accessories for newly remote families, candy and snacks for comfort eating. The same product mix that made Five Below a treasure-hunt destination for bored teenagers on a Saturday afternoon turned out to be exactly what homebound families needed to survive lockdown.

Phased reopenings began in late April 2020, starting with seventeen stores in Arkansas, Iowa, and Nebraska. By June 6, every Five Below location had reopened. The recovery was swift and powerful. Stimulus checks put cash in the hands of Five Below's core demographic, and pent-up demand drove traffic levels that surprised even management. The combination of government stimulus payments and months of lockdown-induced retail withdrawal created a spending surge that benefited value retailers disproportionately. Families that might have splurged at a full-price retailer pre-pandemic were now gravitating toward stores where they could fill a bag for twenty dollars.

Fiscal year 2021 told the story in numbers. Revenue surged from roughly two billion dollars to approximately 2.84 billion dollars, a forty-five percent increase. Comparable store sales grew more than thirty percent. New customer acquisition accelerated as shoppers who had never visited a Five Below store discovered it during the pandemic recovery. And the company leaned aggressively into new store openings, adding approximately a hundred and seventy net new locations despite the operational chaos of a global pandemic. Five Below was one of only nine retailers in the United States that continued opening new stores throughout 2020.

The demographic shift during this period was also significant. Five Below had always been positioned as a teen and tween retailer, but the pandemic drove a notable broadening of the customer base. Parents shopping for lockdown activities for their children discovered the stores. Older adults looking for inexpensive household items and gifts became regular visitors. And college students, many of whom were attending school remotely and furnishing improvised dorm rooms at home, found that Five Below's Room world offered exactly what they needed at prices that did not stress already-strained budgets. This demographic expansion proved durable: even after the pandemic subsided, the broadened customer base continued to shop at Five Below, providing a more diversified revenue foundation than the company had ever had.

The pandemic also created an unexpected tailwind on the real estate front. The retail apocalypse that had been building for years accelerated dramatically in 2020, with department stores, specialty chains, and restaurant concepts closing thousands of locations. For Five Below, which had always targeted B-tier malls, strip centers, and high-traffic areas with lower rents, the wave of closures meant a sudden abundance of attractive lease opportunities at favorable terms. Landlords who had been holding out for higher-rent tenants were now eager to fill empty spaces, and Five Below was one of the few retailers actively seeking new locations.

There is a myth versus reality tension worth addressing here. The myth, popular among e-commerce bulls during 2020, was that COVID proved physical retail was dying and that even Five Below would need to become a digital-first business to survive. The reality was almost exactly the opposite. COVID proved that Five Below's physical stores were irreplaceable and that the in-store experience was the product, not just the distribution channel. The company's e-commerce sales quadrupled during lockdowns, but they quadrupled from a tiny base to a slightly-less-tiny base. Even after years of digital investment, online sales still represent less than five percent of total revenue. This is not a failure of digital strategy. It is a structural feature of the business model.

The lessons from COVID reshaped Five Below's strategic thinking in lasting ways. Management acknowledged that omnichannel capabilities were no longer optional, even for a business where physical stores would always be "the hero." Investments in digital infrastructure continued after the pandemic, including buy-online-pickup-in-store functionality and improved e-commerce fulfillment. But the more profound takeaway was that the treasure-hunt model, the browsing, the discovery, the tactile engagement with products, simply did not translate to a screen. The pandemic had not revealed a digital opportunity waiting to be seized. It had confirmed that Five Below's physical stores were the product, and that the company's job was to open more of them, faster, in more places. That realization set the stage for the most aggressive expansion push in the company's history.

Aggressive Expansion and the Store Count Vision (2021-Present)

Coming out of COVID with strong momentum and cheap real estate, Five Below's management made a bet that would define the company's next era: accelerate new store openings to roughly two hundred per year and pursue a long-term target of more than 3,500 stores by 2030. This "Triple-Double" plan, articulated to investors in 2022, called for tripling the store count from approximately 1,190 locations to 3,500-plus within the decade, an ambitious growth rate that implied high-single-digit annual unit expansion for nearly a decade.

The geographic expansion was systematic and revealed management's disciplined approach to market entry. Five Below had spent its first fifteen years concentrated on the East Coast and gradually filling in the Southeast and Midwest. California, the nation's largest consumer market, did not get its first stores until April 2017, when nine locations opened simultaneously across the state in a coordinated launch that generated significant local media coverage. The Pacific Northwest waited even longer, with Oregon and Washington stores arriving in November 2025.

Each new market entry followed a playbook honed over decades. Five Below would typically open a cluster of stores simultaneously rather than one at a time, creating instant brand awareness in the local market and enabling shared marketing costs across multiple locations. The cluster approach also allowed the distribution network to achieve minimum efficient scale in each region, reducing per-store delivery costs. By the third quarter of fiscal 2025, the company operated 1,907 stores across forty-six states, with only a handful of states remaining untapped. The remaining white-space markets tend to be less densely populated Mountain and Plains states where the unit economics may be slightly less favorable than in the suburban Northeast and Southeast markets where Five Below first established itself.

Store format evolved alongside the expansion. New locations increasingly skewed toward larger footprints, typically eight thousand to ten thousand square feet, to accommodate the Five Beyond shop-within-a-shop and provide a more spacious shopping experience. The distribution network scaled in parallel: five distribution centers now span the country, from the original 1,015,000-square-foot facility in Pedricktown, New Jersey on the East Coast to an 858,000-square-foot center in Buckeye, Arizona serving the West, with facilities in Forsyth, Georgia, Conroe, Texas, and a massive one-million-square-foot center in Shelby County, Indiana that represented a hundred-million-dollar-plus investment and created more than four hundred and seventy new jobs in the region.

The pace of new product introduction kept the stores feeling fresh even as the chain scaled. The buying team maintained a relentless cadence of introducing new SKUs, rotating roughly forty percent of the assortment every four to six weeks across four to six seasonal refreshes per year. The key metric that management focused on internally was what they called "newness": the percentage of the store that a returning customer had never seen before. Maintaining high newness at nearly two thousand locations, with supply chains stretching across continents, was an operational achievement that grew more impressive and more difficult with each passing year.

The challenge of maintaining brand consistency across nearly two thousand locations while executing two hundred-plus new store openings per year cannot be overstated. Each new store needs to be staffed, stocked, and trained to deliver the same high-energy treasure-hunt experience that made Five Below famous. The company addressed this through a rigorous new store playbook that codified everything from the initial product assortment to the music playlist to the store-opening marketing strategy. Regional managers served as the critical link between corporate strategy and local execution, and the company invested heavily in their training and development.

Fiscal year 2024, ending in January 2025, saw the company add a remarkable two hundred and twenty-seven net new stores, bringing the total to 1,771 across forty-four states. Revenue reached 3.88 billion dollars, growing more than ten percent year over year. But beneath the headline growth numbers, cracks were appearing. Comparable store sales declined 2.7 percent, the first meaningful negative comp print in the company's public history. Traffic was softening. The macro environment, marked by persistent inflation and consumer fatigue, was hitting discretionary retailers hard. And the stock, which had traded as high as two hundred and thirty-six dollars in August 2021, collapsed to a fifty-two-week low of roughly fifty-two dollars during the turmoil of mid-2024.

The company's response to the slowdown would prove as significant as the expansion itself. In July 2024, CEO Joel Anderson resigned, and the board brought back co-founder Tom Vellios as interim executive chairman to help "reset the business." Kenneth Bull, the CFO and COO, stepped in as interim CEO while the board conducted a search. The transition was jarring but necessary. Anderson had been an effective expansion-era CEO, opening hundreds of stores and building the organizational infrastructure to support national scale. But the merchandising edge, the trend-spotting instinct that had made Five Below special, had arguably dulled during his tenure.

The board's choice of successor would set the stage for one of the most dramatic turnarounds in recent retail history. But that story belongs to a later section. For now, the key question for investors tracking the expansion narrative is whether the 3,500-store target remains realistic. The unit economics still look attractive: roughly four hundred thousand dollars in capital investment per store, approximately two million dollars in first-year revenue, and a payback period under a year. Real estate availability remains favorable. But the law of large numbers applies to retail chains as surely as it does to any growth story. Every new store opened in a mature market risks cannibalizing an existing location's sales, and as Five Below pushes into less-familiar geographies, the execution challenges multiply.

Inflection Point Number Three: The Gen Alpha and Social Media Flywheel (2022-Present)

The pandemic had proven that Five Below's physical stores were resilient. The digital investment provided a foundation for omnichannel operations. And the consumer spending surge had turbocharged growth. But the most unexpected inflection point was still ahead, driven not by corporate strategy but by millions of teenagers with smartphones and social media accounts.

Sometime in 2022, a fifteen-year-old girl in suburban Dallas walked into her local Five Below, filled a basket with Squishmallows, LED lights, candy, and a phone charger, went home, and filmed a TikTok video showing everything she bought. The video got two hundred thousand views. A dozen commenters asked which Five Below location she visited. Three of them drove there the next day.

This scene, replicated thousands of times across the country by Gen Z and Gen Alpha creators, represents Five Below's third major inflection point: the emergence of a social media flywheel that generates massive unpaid marketing at essentially zero cost to the company. The hashtags associated with haul videos, grwm (get ready with me) content, and store-walkthrough posts have accumulated hundreds of billions of collective views on TikTok alone. Five Below is not just a store. It has become content.

The flywheel works because of a near-perfect alignment between Five Below's product characteristics and social media's incentive structure. Low price points mean creators can buy a large haul for under twenty-five dollars, which makes for visually impressive content without financial risk. Trendy products mean the haul feels aspirational rather than cheap. Frequent inventory rotation means there is always something new to discover and share. And the treasure-hunt format means every trip to Five Below is potentially a unique story worth telling.

Understanding why this matters requires a brief detour into the psychology of social media content creation. For a young person building a following on TikTok, the ideal content formula is: show something visually interesting, relatable, and accessible. A haul video from Gucci fails on accessibility. A haul video from Walmart fails on aspiration. A haul video from Five Below hits the sweet spot: the products look cool enough to generate envy, cheap enough to feel accessible, and varied enough to fill a satisfying three-minute video. Five Below products are, in a very real sense, designed for the camera, even if neither the company nor the creators are thinking about it that way.

Squishmallows provide the most vivid case study. These plush collectible toys became a pandemic-era phenomenon, and Five Below emerged as one of the most popular and affordable destinations for Squishmallow hunters. TikTok creators filming their Five Below Squishmallow hunts generated millions of views, and the comments sections became communities where collectors shared tips on which locations had the best stock. Five Below's buying team, observing the trend in real time, responded by deepening the Squishmallow assortment and securing exclusive colorways that could not be found elsewhere. This created a virtuous cycle: exclusive products drove more social content, which drove more store traffic, which justified deeper inventory investment, which generated more exclusive products.

But the social media flywheel extends well beyond any single product. "Aesthetic room décor" hauls, where creators show how they furnished their bedrooms or dorm rooms for under fifty dollars using Five Below products, became a genre unto themselves. Tech accessory reviews, beauty product roundups, and candy taste-tests all found audiences measured in millions. The common thread was that Five Below's price points lowered the stakes for both the creator and the viewer. A teenager recommending a fifty-dollar product carries the implicit responsibility of endorsing something expensive. A teenager recommending a three-dollar LED strip carries no such burden. The low prices enabled a kind of frictionless sharing that higher-priced retailers cannot replicate.

Five Below's buying team developed an increasingly sophisticated feedback loop with social media trends. Buyers monitor trending products on TikTok and Instagram in real time, and the company's six-week concept-to-shelf timeline allows them to get versions of viral products into stores while the trend is still rising. This speed-to-market capability is a meaningful competitive advantage against Amazon, where trending products often get buried in a sea of search results and knockoffs, and against larger retailers whose buying cycles operate on months-long timelines.

The competitive dynamics of the social media flywheel deserve closer examination. Dollar General and Dollar Tree have attempted to replicate the social content phenomenon, but their store formats, product assortments, and brand positioning simply do not generate the same level of organic engagement. A TikTok haul video from Dollar Tree feels like frugality content. A TikTok haul video from Five Below feels like discovery content. The distinction is subtle but commercially significant: frugality content appeals to a niche audience motivated by saving money, while discovery content appeals to a broad audience motivated by finding cool things. Five Below's branding, store design, and product curation position it on the right side of this divide.

Under CEO Winnie Park, who took over in December 2024, the company has deliberately leaned into the Gen Alpha demographic, broadening the target customer base to include even younger shoppers alongside the core Gen Z audience. Park, who previously led Forever 21's social-media-first brand refresh, understood intuitively that Five Below's value to young consumers was not just economic but social. Shopping at Five Below was a shared experience, an identity marker, a way of participating in a community that valued cleverness over conspicuous consumption.

For investors, the social media flywheel is both an asset and a risk. The asset side is obvious: millions of dollars worth of organic marketing at virtually no cost, with an authenticity that paid advertising cannot match. The risk is that social media trends are inherently volatile. A platform algorithm change, a shift in creator culture, or the emergence of a competing retail format that generates more compelling content could erode this advantage rapidly. Five Below does not control the flywheel. It merely benefits from it, and the distinction matters.

The Playbook: How Five Below Actually Works

The social media flywheel transformed Five Below from a retailer that marketed to young consumers into a retailer that young consumers marketed for free. But organic virality alone does not build a sustainable business. Behind the TikTok haul videos and the Instagram aesthetics, Five Below runs on a set of operational capabilities that are far less glamorous but far more important to the company's long-term competitive position.

To understand Five Below at a deeper level, you need to look past the colorful stores and viral TikTok videos and examine the operating machinery that makes the business tick. The company's competitive position rests on six interlocking capabilities that are individually unremarkable but collectively difficult to replicate.

Merchandising Excellence. Five Below employs a large team of buyers who function more like trend scouts than traditional retail purchasers. Their job is to identify emerging product trends across the youth market, source or develop products that fit the Five Below price architecture, and get those products into stores before the trend peaks. The team maintains relationships with approximately one thousand suppliers, split roughly sixty-forty between domestic and international sources. The buying process is merchant-driven, meaning individual buyers have significant autonomy to make product bets based on their instincts and market intelligence. This decentralized approach creates the speed and agility that allows Five Below to respond to trends in weeks rather than months.

Real Estate Strategy. Five Below does not compete for prime mall locations. The company targets B-tier malls, strip shopping centers, and high-traffic retail corridors where occupancy costs are materially lower than Class A retail space. This strategy accepts lower foot traffic in exchange for better lease economics, a trade that works because Five Below generates its own traffic through merchandising and word-of-mouth rather than relying on anchor-tenant draw. Average store size runs approximately 9,500 square feet, large enough to create the immersive "worlds" experience but small enough to keep build-out costs manageable.

Store Economics. The unit-level financial model is among the most attractive in all of retail. A new store costs roughly four hundred thousand dollars to open, net of tenant improvement allowances. First-year revenue averages approximately two million dollars, with mature stores generating around 2.5 million dollars. Four-wall EBITDA margins run approximately twenty-five percent, and the capital payback period is less than one year, typically around seven months. These economics explain why the company can grow at two hundred-plus new stores per year while generating positive free cash flow: each new store starts contributing to the bottom line almost immediately.

Inventory Velocity. Think of Five Below's inventory like a fast-flowing river rather than a still pond. With roughly four thousand active SKUs and forty percent turnover every four to six weeks, Five Below's inventory operates at a pace that minimizes two of retail's biggest profit killers: markdowns and staleness. Products that do not sell get cleared quickly to make room for fresh merchandise, and the constant rotation keeps customers coming back to see what is new. Inventory turns approximately 4.3 times annually, which is not best-in-class compared to grocery or fast fashion but is very strong for a general merchandise retailer. The rapid turn also limits markdown exposure because the company is not sitting on deep inventory positions in any single product.

Customer Acquisition. In an era when customer acquisition costs are rising relentlessly for most consumer brands, Five Below spends remarkably little on traditional advertising. The company's customer acquisition model relies primarily on three low-cost channels: word of mouth, social media (almost entirely organic), and physical foot traffic from its real estate locations. This is possible because the product itself is the marketing. A satisfied customer who shows a friend the five-dollar Bluetooth speaker they just bought is a more effective advertisement than any billboard or Instagram ad. The resulting customer acquisition cost is extremely low, and the lifetime value is driven by visit frequency rather than high per-visit spending.

The Five-Dollar Framing Effect. Perhaps the most underappreciated aspect of Five Below's model is the psychological pricing power of the five-dollar anchor. When a customer enters a store knowing that virtually everything costs five dollars or less, the mental calculus shifts from "should I buy this?" to "why not buy this?" The price point is low enough to bypass the deliberation that characterizes most retail purchases. It creates permission to buy multiple items, to experiment with products you might not otherwise try, and to treat yourself without guilt. This framing effect shows up in the data: average transaction values are modest in absolute terms, but units per transaction are high, and visit frequency is strong. The customer who visits twelve times a year and spends fifteen dollars each time is worth more than the customer who visits twice and spends forty-five dollars, because the high-frequency customer is harder for competitors to steal.

Organizational Culture. The culture at Five Below headquarters, "WowTown," is merchant-driven in a way that most corporate retailers are not. Buyers are empowered to make product decisions quickly, with minimal committee approval. The test-and-learn mentality means that failed product bets are treated as learning opportunities rather than career-ending mistakes. Store managers serve as critical feedback nodes, communicating directly with the buying team about what is selling, what customers are asking for, and what competitors are doing in local markets. This decentralized intelligence network, combined with centralized purchasing power, creates an organizational structure that is simultaneously agile and scalable.

Vertical Integration Considerations. Five Below has deliberately remained asset-light compared to retailers that own their own manufacturing or distribution infrastructure. The company does not own factories or manufacture products. It does not own its store locations, leasing virtually all of them. And it outsources most of its logistics to third-party operators. This strategic choice reflects a clear-eyed assessment of where the company's value creation lies: in merchandising and store experience, not in manufacturing or logistics. The risk of this approach is dependence on external partners, particularly overseas manufacturers whose pricing and availability are subject to tariff and geopolitical disruption. The benefit is capital efficiency and flexibility.

These six capabilities, along with the cultural and integration choices that bind them together, are individually straightforward. Plenty of retailers have good merchants, reasonable real estate strategies, and attractive unit economics. What makes Five Below's playbook difficult to replicate is the integration: the way the merchandising speed feeds the social media flywheel, the way the real estate strategy enables the unit economics, the way the pricing psychology drives the inventory velocity. The whole is genuinely greater than the sum of its parts.

Porter's Five Forces and Hamilton's Seven Powers: Where the Moat Really Lives

With the operational playbook understood, the next question is: how durable is Five Below's competitive position? To answer this rigorously, we need to examine the business through two complementary strategic frameworks.

Understanding Five Below's competitive position requires moving beyond the surface-level observation that the company sells cheap stuff in colorful stores. The strategic framework analysis reveals a business that occupies a genuinely differentiated position in the retail landscape, though one with meaningful vulnerabilities.

Industry Rivalry is intense and growing more so. Five Below competes for discretionary spending with an enormous range of alternatives: dollar stores like Dollar Tree with its roughly sixteen thousand locations and Dollar General with twenty thousand, mass merchants like Walmart and Target, off-price retailers like TJ Maxx and Ross, and increasingly, e-commerce platforms like Amazon, Temu, and Shein. The competitive set is broad because Five Below sells across so many categories. Any given product in the store competes with a different set of rivals than the product next to it on the shelf. The saving grace is that no single competitor replicates the complete Five Below experience: the intersection of extreme value, trend-forward assortment, and in-store energy.

Threat of Substitutes is high and represents the most significant structural risk to the business. Amazon's ubiquity, Temu's explosive growth in the US discount market (from zero to an estimated fourteen percent market share within a single year, according to Earnest Analytics), and Shein's appeal to the same Gen Z demographic all represent alternatives that offer similar products at similar or lower prices with the added convenience of home delivery. The key question is whether the in-store treasure-hunt experience provides enough differentiation to keep customers visiting physical stores when they can access comparable products from their phones. The evidence so far is encouraging for Five Below: the company's comparable store sales accelerated to double digits in fiscal 2025 even as Temu and Shein continued their US expansion, suggesting that the physical experience and the online marketplace serve different shopping occasions rather than directly substituting for each other. But the risk remains that a sufficiently good digital treasure-hunt experience could eventually emerge and chip away at physical store traffic.

Threat of New Entrants is moderate. Opening a discount retail store has low capital barriers, but replicating Five Below's scale, supply chain relationships, merchandising expertise, and brand recognition is genuinely difficult. The initial capital requirement for a single store is low, roughly four hundred thousand dollars, which means any well-funded entrepreneur could theoretically open a competing concept. But scaling that concept to two thousand stores requires distribution infrastructure, vendor relationships, real estate expertise, and organizational capability that takes years to build. The barrier to entry is not opening one store. The barrier to entry is opening store number five hundred.

Miniso, the Chinese-origin lifestyle retailer with over 5,800 stores globally, is perhaps the most credible emerging competitor in the United States. Its product mix of trendy, affordable lifestyle accessories and gifts overlaps meaningfully with Five Below, and its store aesthetic, clean, bright, and Instagram-friendly, targets a similar customer. Miniso's advantage is its direct connection to Chinese manufacturing, which gives it a cost advantage on sourcing. Its disadvantage is limited brand awareness in the US and a product assortment that skews more toward young adults than the tween and teen demographic that Five Below owns. Flying Tiger Copenhagen, with roughly nine hundred stores across forty-two countries, competes on a similar "fun, affordable discovery" concept but has limited US presence and a higher average price point.

Bargaining Power of Suppliers is low to moderate, favoring Five Below. The relationship between Five Below and its supply base is asymmetric in the company's favor. The company sources from approximately one thousand suppliers, with no single vendor representing a critical dependency. Most products are commodity or trend-driven items with many potential sources. Five Below's scale, now approaching two thousand stores and nearly five billion dollars in purchasing volume, provides meaningful negotiating leverage. The primary supply risk is geographic concentration: sixty percent or more of cost of goods originates from China, creating tariff and geopolitical exposure that has nothing to do with supplier bargaining dynamics.

Bargaining Power of Buyers is moderate. Customers are price-sensitive and face low switching costs, but Five Below's combination of value, trendiness, and experience creates meaningful stickiness. The social media flywheel adds an additional retention mechanism: customers who follow Five Below content on TikTok and Instagram are continuously reminded of new products and given reasons to visit.

The overall picture that emerges from the Five Forces analysis is an industry that is structurally competitive and requires continuous execution excellence to maintain profitability. Five Below does not benefit from the kind of structural barriers that protect, say, a pharmaceutical company with patent protection or a utility with a regulated monopoly. Its competitive position is earned daily through merchandising decisions, store operations, and brand management. This is both the company's vulnerability and its strength: because the position must be earned rather than inherited, it selects for organizations that are genuinely excellent at execution, and Five Below's twenty-three-year track record suggests it is one of those organizations.

Turning to Hamilton Helmer's Seven Powers framework, the analysis reveals where Five Below's competitive advantages are genuinely durable and where they are more fragile than they appear.

Process Power is Five Below's strongest and most defensible advantage. The company's merchandising process, from trend identification through sourcing through in-store placement, has been refined over more than two decades and 1,900-plus store openings. The organizational learning embedded in this process, the buyer intuition, the vendor relationships, the store operations playbook, the inventory management systems, constitutes a genuine moat that cannot be acquired or replicated quickly. Process power is the most underrated form of competitive advantage because it is invisible from the outside. Competitors can copy Five Below's store format, its product categories, even its pricing structure. What they cannot copy is the accumulated institutional knowledge of twenty-three years of merchant-driven retail operations.

Branding is moderate to strong and growing. "Five Below" is becoming synonymous with teen and tween value shopping in the same way that Starbucks became synonymous with coffee culture or Lululemon became synonymous with athleisure. For Gen Z, Five Below is not just a price point but an affinity brand, a store that "gets" them. This brand equity has real economic value because it enables customer acquisition at low cost and supports higher traffic levels than the real estate locations alone would generate. The risk is that brand relevance with young consumers is inherently temporary. Each generation of teens eventually ages out, and the incoming generation may or may not adopt the same brand loyalties.

Counter-Positioning was historically strong but is eroding. When Five Below launched in 2002, traditional retailers could not profitably serve the extreme-value segment with the same level of curation and experience. Dollar stores would not invest in trend-forward merchandising. Department stores could not economize enough. This positioning gap gave Five Below a protected space in the market. But competitors are adapting. Dollar Tree has been expanding its product range and experimenting with higher price points. Miniso is bringing a similar curated-value-discovery model to the US market. Temu and Shein are offering comparable products at comparable or lower prices online. The counter-positioning advantage is narrowing.

Scale Economies are moderate and growing. Distribution and buying power improve with size, and marketing efficiency increases through store density in local markets. When Five Below has ten stores in a metropolitan area, each store benefits from the brand awareness generated by the other nine, a virtuous cycle that national competitors like Dollar Tree achieve through sheer ubiquity but that Five Below achieves through concentrated brand intensity. But the economies are not winner-take-all. Regional and local competitors can operate profitably at much smaller scale, and the logistical complexity of managing two thousand stores across forty-six states offsets some of the purchasing leverage.

Network Effects are weak in the traditional sense, though the social media flywheel creates an indirect network dynamic that is worth examining more carefully. Every customer who posts a Five Below haul video on TikTok functions as an unpaid ambassador, creating awareness that drives new customers into stores, who in turn create more content. This is not a true network effect in the Metcalfe's Law sense, because each additional user does not make the product more valuable for every other user. But it is a feedback loop that generates increasing returns to brand visibility, and it operates at zero marginal cost to the company.

Switching Costs are minimal, as customers can easily shop elsewhere. There is no subscription, no loyalty program with meaningful lock-in, no data moat that makes the product better with use. The only switching costs are habitual: a customer who has learned to enjoy the Five Below treasure-hunt experience may find other shopping experiences less satisfying by comparison, but this is a psychological preference rather than a structural barrier.

Cornered Resources are limited, though the merchant talent pool and locked-up real estate leases provide some advantage. The most important cornered resource is arguably the institutional knowledge of the buying team, the accumulated understanding of what products work at what price points for what demographics in what seasons. This knowledge is embodied in people, not in databases, which makes it both valuable and fragile.

The synthesis is that Five Below's competitive position rests primarily on Process Power and Branding, supported by growing Scale Economies. This is a different moat profile than, say, Costco, whose competitive position rests on Scale Economies and Switching Costs (the membership model), or than Nike, whose moat is almost entirely Branding. Five Below's moat is more analogous to that of Trader Joe's, another retailer whose competitive advantage is rooted in a distinctive merchandising process and a brand identity that resonates with a specific customer segment.

The durability of this position depends on two things: maintaining the merchandising execution edge that keeps products fresh and on-trend, and sustaining brand relevance with successive generations of young consumers. Neither is guaranteed, but both are within management's control to influence. The Winnie Park era has demonstrated that a CEO with the right instincts can rapidly restore both capabilities when they have drifted, which is itself a source of institutional resilience.

Bull versus Bear Case and Key Risks

Before diving into the bull and bear arguments, it is worth acknowledging the consensus narrative that Wall Street has constructed around Five Below, because some of it is myth and some is reality. The myth is that Five Below is "just a more expensive dollar store." The reality is that the customer demographics, product mix, and shopping occasions are fundamentally different. Dollar Tree and Dollar General serve a lower-income customer buying household necessities. Five Below serves a broader income spectrum buying discretionary treats and trend-driven products. The overlap in customer base is minimal. A second myth is that e-commerce will eventually kill the model. The reality is that Five Below's online sales remain under five percent of revenue not because the company has failed at digital but because the treasure-hunt experience does not translate online. The product is the experience, not just the merchandise.

The Bull Case for Five Below rests on a combination of proven unit economics and massive remaining runway. With roughly 1,900 stores today and a long-term target of 3,500-plus, the company has not yet opened half its potential locations. Every new store that follows the historical playbook, four hundred thousand dollars invested and paid back in seven months, is an accretive addition to the earnings base. The macro environment paradoxically favors the value proposition: inflation makes consumers more price-conscious, driving trade-down behavior that benefits extreme-value retailers across income levels. Gen Z and Gen Alpha, the largest and most digitally connected generations in history, are increasingly experience-oriented shoppers who value discovery and social sharing over convenience, which plays directly to Five Below's strengths and against e-commerce pure-plays.

The Five Beyond expansion has unlocked a meaningful growth lever within existing stores, one that is still in its early innings as the format rolls out to remaining unconverted locations. Higher average transactions without meaningfully higher operating costs is the retail equivalent of finding money in the couch cushions. Omnichannel capabilities, while still nascent, are maturing and represent an additional growth vector. And the management transition to Winnie Park has injected fresh energy into the business, with her Forever 21 experience in social-media-first branding and her deliberate broadening of the target demographic to include Gen Alpha.

The Bear Case centers on competitive intensity and structural vulnerability. Temu's explosive growth in the US discount market demonstrates that an aggressive, well-funded competitor can capture meaningful share in a short period. If Temu, Shein, or Amazon's physical retail experiments succeed in replicating the treasure-hunt experience at comparable prices with added convenience, Five Below's traffic could erode quickly. Wage inflation and occupancy cost increases are structural headwinds that compress margins in a business with no pricing power above the five-dollar (or Five Beyond) ceiling. A consumer recession that hits discretionary spending would disproportionately affect a retailer whose products are almost entirely wants rather than needs.

The most existential risk is tariff exposure, and it deserves extended discussion because it is the single variable most likely to determine Five Below's financial trajectory over the next several years. With sixty to seventy-two percent of cost of goods originating from China, Five Below is among the most China-dependent retailers in the United States. To put this in perspective, the average US retailer sources roughly thirty to forty percent of its products from China. Five Below's exposure is nearly double the industry average, a structural vulnerability that was manageable when tariffs were low but becomes potentially business-altering when they spike.

The April 2025 tariff crisis illustrated the risk in vivid terms. When reciprocal tariffs on Chinese goods surged to as high as a hundred and forty-five percent, Five Below was forced to temporarily suspend all cargo shipments from China. The stock dropped twenty-six percent in a single day on the tariff announcement. Oppenheimer analyst Brian Nagel estimated the tariffs could inflate Five Below's costs by ninety to ninety-five percent, an increase that would be catastrophic if sustained. Bank of America flagged that Five Below had limited ability to offset costs through pricing increases because the entire brand identity is built on low prices.

The company has been diversifying its sourcing to include Mexico, Vietnam, India, and South Korea, and management has also pursued strategies like negotiating lower prices with existing vendors, finding new US-based product sources, and pivoting toward licensed products that carry different cost structures. The US-China tariff truce in May 2025, which rolled back peak tariffs to thirty percent for a ninety-day period, provided some breathing room. But the structural risk remains: as long as the majority of Five Below's products come from China, the company is one executive order away from a cost structure crisis. Shifting supply chains at this scale takes years, not quarters, and alternative manufacturing centers in Southeast Asia generally produce at higher costs with less developed ecosystems for the kinds of trend-driven, low-price products that define Five Below's assortment.

Store saturation risk grows as the store count climbs, and this is a risk that the company's own recent history illuminates. Every new location in a market that already has Five Below stores risks cannibalizing existing store sales. The company's negative comparable store sales in fiscal 2024, while partly attributable to macro factors, also raised questions about whether some markets were approaching saturation. New store productivity relative to mature stores is a metric that will become increasingly important to track.

A consumer recession that hit discretionary spending hard would pose a particularly acute risk for Five Below. Unlike Dollar Tree or Dollar General, which sell household essentials that consumers buy regardless of economic conditions, Five Below's product mix is almost entirely discretionary. Nobody needs a Squishmallow or an LED string light. In a severe downturn, these are exactly the purchases that get cut first. The counterargument is that Five Below's low price points make it a beneficiary of trade-down behavior: consumers who might have bought a thirty-dollar gift at Target might instead buy a five-dollar gift at Five Below. But this thesis has not been tested in a real recession during Five Below's public market history.

And finally, the merchandising risk. Five Below's trend-spotting capability is an art, not a science. It depends on the judgment and instincts of individual buyers, not on algorithms or proprietary data. The company could lose its edge if key talent departs, if organizational bureaucracy slows decision-making, or if generational tastes shift in ways the buying team fails to anticipate. Merchandising excellence is a perishable asset that must be renewed continuously.

Myth versus Reality on Store Saturation. One common bear argument is that Five Below is approaching saturation in its core Northeast and Southeast markets. The reality is more nuanced. With roughly 1,900 stores across forty-six states, the average state has approximately forty-one stores. But the distribution is heavily skewed: Pennsylvania, New Jersey, and Florida have far more stores per capita than states like Oregon, Washington, and Montana that Five Below has only recently entered. The saturation risk is real in the densest markets but likely overstated for the company as a whole, given the vast geographic white space that remains.