Fiserv: The Plumbing of Global Finance and The Mega-Merger Drama

I. Introduction and Episode Roadmap

Picture this: you walk into a coffee shop on a Tuesday morning, tap your phone against a sleek countertop terminal, and walk out thirty seconds later with a latte. You probably never think about what happened in those thirty seconds. But behind that momentary transaction, an extraordinary amount of infrastructure fired in sequence.

The terminal read your card credentials. A request rocketed through a payment network to your bank. Your bank checked your balance, authorized the charge, and sent an approval code back through the chain. The merchant's account was credited. A receipt appeared on your phone.

And chances are better than even that Fiserv — a company most people have never heard of — handled some critical piece of that chain. The terminal might have been a Clover device, manufactured and programmed by Fiserv. The merchant's payment processing might have been routed through Fiserv's acquiring network. Your bank's core system — the database that holds your balance and processed the authorization — might have been running on Fiserv software.

Fiserv is one of the most invisible giants in global finance. With a market capitalization that peaked above a hundred billion dollars and annual revenues exceeding twenty billion, the company sits at the intersection of almost every electronic payment and bank transaction in America. It processes more than forty billion merchant transactions annually. It runs the core banking software — the digital backbone, the operating system — for roughly forty percent of all U.S. banks.

And yet, if you stopped a hundred people on the street and asked them to name it, you would be lucky to find one who could. Visa, Mastercard, PayPal — those are the names people know. Fiserv is the machinery behind the curtain, the plumbing that makes the water flow. It is also, as of early 2026, one of the most dramatic corporate stories unfolding in American business.

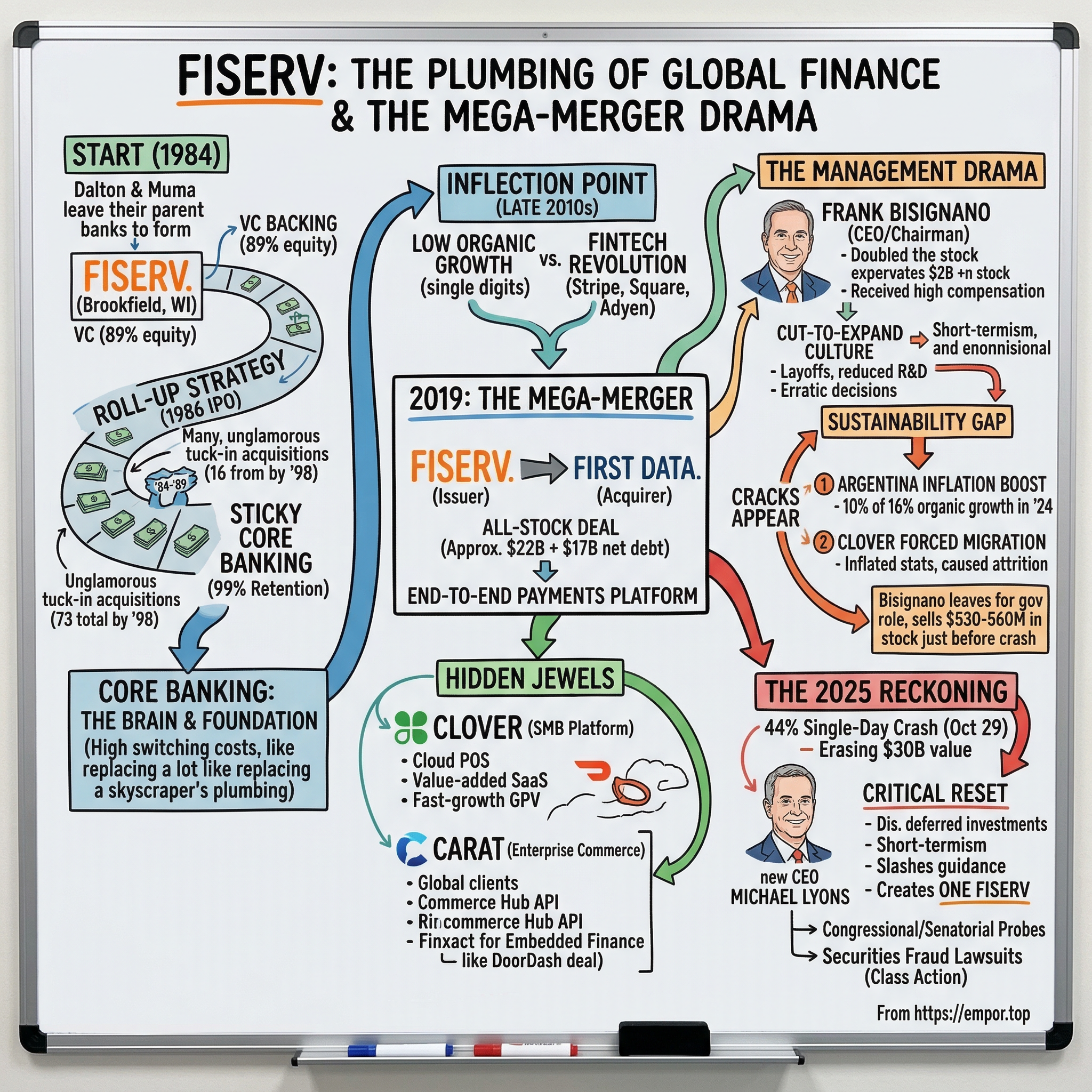

This is the story of how a small data-processing outfit founded in 1984 by two tech-obsessed bankers evolved into the plumbing of American finance through one of the most prolific roll-up strategies in corporate history. It is the story of how that company, facing an existential growth crisis in the late 2010s, made a twenty-two-billion-dollar bet on a debt-laden payments company called First Data — and discovered hidden jewels inside.

It is the story of a charismatic CEO who doubled the stock price, collected hundreds of millions in compensation, then left for a government job months before the whole edifice cracked open. And it is the story of the spectacular 2025 reckoning — a forty-four percent single-day stock crash, billions in destroyed shareholder value, congressional investigations, and securities fraud lawsuits — that exposed what may have been years of short-term thinking masquerading as operational excellence.

The thesis is straightforward: mergers and scale can buy time and generate incredible cash flow, but they cannot replace the necessity of organic innovation and honest accounting.

Fiserv is a case study in how "boring" infrastructure businesses can generate extraordinary returns — and how quickly those returns can evaporate when incentives go wrong.

II. The Early Days: Digging the Trenches of Core Banking

In the early 1980s, the American banking industry was a patchwork of thousands of small, independent institutions — community banks, savings and loans, credit unions — scattered across every town and county in the country. Each of these institutions needed technology to run its operations: managing accounts, processing deposits, calculating interest, generating regulatory reports.

But most were far too small to build their own systems. The technology required mainframes, specialized programmers, and constant maintenance. For a bank with fifteen thousand accounts in rural Wisconsin, building and maintaining that infrastructure was like asking a corner grocery store to build its own supply chain from scratch. The economics simply did not work.

Two men saw this problem from the inside. George Dalton was a Northwestern dropout who had worked his way through data processing roles at Marine Bank, Midland National Bank, and First Bank System. He had spent the better part of a decade immersed in the mechanics of bank technology — the arcane world of batch processing, account reconciliation, and mainframe operations. Leslie Muma, a theoretical mathematics major turned MBA, ran the data processing subsidiary of a savings and loan in Tampa, Florida.

They met in the late 1970s through an improbable connection. Dalton had been searching for fellow bank data-processing department heads willing to share software development costs. His insight was elegant: by pooling resources across banks, they could cut data processing bills by as much as sixty percent. He contacted executives at institutions around the country. Muma was the only one who bought in.

Throughout the late 1970s and early 1980s, Dalton and Muma tried to merge their respective operations under a single corporate umbrella. But their parent companies resisted. Bankers did not understand technology, and they certainly did not understand why their data processing departments should be collaborating with competitors. By 1984, their subsidiaries collectively served more than a hundred clients and generated over twenty-two million dollars in annual revenue — proof that the model worked.

Frustrated by corporate inertia, they struck out on their own. With venture capital backing, they purchased their companies from the parent corporations and formed Fiserv, headquartered in Brookfield, Wisconsin. The price of independence was steep. The venture financiers demanded — and received — eighty-nine percent of the equity. Dalton and Muma were left with just eleven percent of the company they had built. It was a brutal bargain, but it gave them the freedom to execute their vision.

What followed was one of the most relentless roll-up strategies in American business history.

Fiserv went public on the NASDAQ in 1986, and Dalton and Muma used stock as currency to acquire competitors at a furious pace. The strategy was deceptively simple: find small, specialized bank technology firms — companies that made check imaging software, or ATM management tools, or loan processing systems — buy them cheaply, integrate their client bases, and cross-sell the full Fiserv product suite. Each acquisition brought more bank clients. Each client relationship opened the door to selling more products. The flywheel spun faster with every deal.

Between 1984 and 1989, they acquired sixteen companies, boosting annual revenues more than three thousand percent. Between 1990 and 1991 alone, they added another fifteen acquisitions, including the Citicorp Information Resources division for forty-nine million dollars — a deal that brought four hundred new bank clients and a core banking system called CBS that would become a cornerstone of Fiserv's offering.

What was striking about this roll-up was its discipline. Unlike many serial acquirers who overpay for marquee deals, Dalton and Muma focused on small, unglamorous tuck-in acquisitions — companies that were profitable but too small to attract competition from larger buyers. They paid reasonable multiples, integrated quickly, and kept overhead low. The company operated without a corporate jet, without lavish offices, and with a lean corporate staff. Dalton was famous for his frugality. The Brookfield, Wisconsin headquarters was aggressively un-flashy — a deliberate cultural signal that this was a company that made money by saving money.

The pace never slowed. By 1998, Fiserv had swallowed approximately seventy-three companies. The founders' ownership had diluted to roughly two percent each, but they had built something far more valuable: the dominant provider of back-office technology for American banking. Revenue had climbed from twenty-two million dollars in 1984 to over one point five billion by the late 1990s — a compounding machine built acquisition by acquisition.

The genius of this strategy was not the acquisitions themselves — plenty of companies have tried to roll up fragmented industries. The genius was what they were rolling up. Core banking software is, quite simply, the stickiest product on earth.

To understand why, imagine that a bank's core system is like the foundation and plumbing of a skyscraper. Every other system the bank operates — online banking, mobile apps, ATM networks, wire transfers, loan processing, regulatory compliance — connects to the core. It is the single source of truth for every customer account, every balance, every transaction. The core knows who has money and who owes money. It is the bank's brain.

Replacing it is not like switching phone providers. It is like replacing the foundation of a building while the tenants continue to live in it. A full core conversion for a mid-size bank can cost fifty to two hundred million dollars and take three to five years. The migration must be executed flawlessly, usually over a single weekend, because the bank cannot afford downtime. A single error could mean customers seeing wrong balances or losing transaction records. Regulators scrutinize every step. For a bank CEO, the risk is existential — a botched core conversion has ended careers and, in extreme cases, threatened the viability of the institution itself.

The result was extraordinary customer retention. Fiserv's core banking business achieved roughly ninety-nine percent client retention rates. Think about what that means. In a world where software companies celebrate ninety-five percent annual retention, Fiserv was losing fewer than one in a hundred clients per year. Banks signed five-to-seven-year contracts with steep early termination penalties, and when those contracts came up for renewal, they overwhelmingly re-signed — not because they loved the technology, but because the alternative was too terrifying to contemplate.

By the 2010s, Fiserv — alongside competitors FIS (which held roughly sixteen percent share) and Jack Henry (roughly eighteen percent) — had locked up more than seventy percent of the U.S. core banking market. Fiserv alone commanded roughly forty percent. These three companies had effectively become the operating system layer of American banking.

The American Fintech Council would later flag this concentration as a systemic concern, noting the vendor lock-in and lack of interoperability that left community banks with virtually no real choice. Only a narrow subset of vendors possessed the scale, regulatory familiarity, and institutional track record necessary to serve as a bank's primary core processor. Banks were stuck — and Fiserv knew it.

In 2007, Fiserv made its largest pre-First Data acquisition, buying CheckFree — the leading provider of online banking and electronic bill payment services — for approximately four and a half billion dollars. This cemented Fiserv's dominance in the digital banking layer that sat on top of its core systems. The moat was wide and deep.

But there was a problem lurking beneath the surface of all this stability. Fiserv was a fortress, but it was a slow-growing fortress. The company was generating reliable, recurring revenue and strong margins, but organic growth was stuck in the low-to-mid single digits. The core banking market was mature. Every bank already had a core system. Growth came mainly from price increases and small acquisitions, not from a flood of new customers.

Meanwhile, outside Fiserv's walls, a revolution was underway. Payments technology was accelerating at a pace that made Fiserv's steady plodding look almost quaint. Stripe, Square, Adyen, Toast — a generation of cloud-native fintech companies was rewriting the rules of how money moved. If Fiserv wanted to be more than a legacy infrastructure provider collecting rent on old contracts, it needed a second act.

And it needed one fast.

For investors, the early Fiserv story establishes two foundational truths that remain relevant today. First, the core banking franchise is a genuinely exceptional asset — perhaps the closest thing to a natural monopoly in enterprise software. Second, that very stickiness can breed complacency. When your clients cannot leave, the urgency to innovate diminishes. The question that would define the next chapter of Fiserv's history was whether the company could maintain its fortress while building something new — or whether it would need to buy growth from the outside.

The answer, as it turned out, was the biggest check the company ever wrote.

III. The Inflection Point: Swallowing First Data

To understand why Fiserv made the biggest bet in its history, you first need to understand what was happening in the payments industry in the late 2010s.

The decade had witnessed an explosion of financial technology companies attacking the payments value chain from every angle. Stripe, founded in 2010, had made it possible for any developer to accept online payments with a few lines of code — an integration that took an hour, compared to the months required to connect with legacy processors. Square had put a card reader on every food truck and farmers' market booth in America. Adyen was winning enterprise clients with a single platform that handled payments across every channel and every country. Toast was building a payments-and-software stack purpose-built for restaurants.

The message was clear: payments were eating the world, and the companies that controlled how money moved would capture enormous value.

Fiserv was watching this revolution from the sidelines. Its core banking franchise was a cash machine, but it occupied the issuer side of the payments equation — the bank side. It helped banks process accounts and manage cards. What it lacked was the other side of the equation: the merchant side, the business of enabling businesses to accept payments. Without both sides, Fiserv could not offer the end-to-end payments platform that clients increasingly demanded.

The answer arrived in the form of First Data Corporation — a company with a fascinating and troubled history of its own.

First Data had been one of the pioneers of electronic payment processing, originally spun off from American Express in the 1990s and grown into the world's largest third-party credit card processor and merchant acquirer. By the mid-2000s, First Data was processing more transactions than any non-bank entity on earth. It was the silent giant of payments.

Then came the leveraged buyout — and it nearly killed the company.

In 2007, at the absolute peak of the pre-crisis credit boom, private equity giant KKR acquired First Data in a leveraged buyout valued at twenty-nine billion dollars. It was one of the largest LBOs in history. KKR's thesis was straightforward: payments processing was a toll-road business with predictable cash flows, making it an ideal candidate for leverage. Load the company with debt, use the steady transaction fees to service it, cut costs aggressively, and sell at a higher multiple in five to seven years.

The timing was catastrophic. The deal closed on October 1, 2007 — literally weeks before the financial crisis began to unfold. KKR had saddled First Data with twenty-two point six billion dollars of debt at punishing interest rates, resulting in a debt-to-equity ratio of nearly six to one. As the Great Recession hammered consumer spending and transaction volumes, First Data's revenue flatlined for the first time in its history. Meanwhile, the interest payments kept coming.

Beginning in 2010, the company could not grow. Cash flow plummeted as interest payments consumed the business. For twenty-nine consecutive quarters — more than seven years — First Data did not report a single profitable period. Every dollar of operating income was devoured by debt service. It was a zombie corporation, generating enough cash to keep the lights on but not enough to invest in the technology that would keep it competitive in an industry that was rapidly evolving. Engineers left for better-funded competitors. Product development stalled. Client relationships atrophied.

The KKR buyout became one of the most notorious examples of private equity overreach in financial history, routinely cited alongside the TXU Energy debacle as a cautionary tale about the dangers of excessive leverage and catastrophic market timing.

Recovery was slow and painful. In 2013, the board brought in Frank Bisignano — the former JPMorgan co-COO — to turn things around. In 2014, First Data raised a historic three and a half billion dollar private placement to reduce its debt load. Bisignano cut costs, restructured operations, and began investing selectively in growth businesses (including, critically, Clover). By February 2015, First Data finally reported its first profitable quarter since the buyout — a milestone that had taken nearly eight years to reach.

In October 2015, First Data went public in the biggest U.S. IPO of that year, selling shares at sixteen dollars apiece — well below the initial offering range of eighteen to twenty dollars — and raising two and a half billion. The discounted pricing reflected the market's lingering skepticism about a company that had spent the better part of a decade as a cautionary tale.

Even after the IPO, First Data remained burdened by billions in legacy debt. KKR still controlled a large stake. The company was viewed by many analysts as damaged goods — a legacy processor whose technology was aging and whose merchant relationships were under assault from nimbler competitors. First Data's revenue growth was modest, its margins were compressed by debt service, and the fintech revolution was making its traditional distribution advantages less relevant with each passing quarter.

On January 16, 2019, Fiserv changed everything by announcing a definitive agreement to acquire First Data in an all-stock transaction valued at approximately twenty-two billion dollars.

The deal mechanics were carefully structured. First Data shareholders would receive 0.303 Fiserv shares for each share of First Data common stock, a premium of roughly twenty-nine to thirty percent over First Data's closing price. No cash changed hands — this was an all-stock merger, meaning Fiserv did not need to raise new debt to fund the purchase price. Instead, it was using its own highly valued equity as currency. The combined entity would be split with Fiserv shareholders owning fifty-seven and a half percent and First Data shareholders owning forty-two and a half percent.

But the equity was only part of the story. Critically, Fiserv was also assuming approximately seventeen billion dollars of First Data's net debt — the residual hangover from KKR's infamous leveraged buyout. The total enterprise value of the transaction, including debt assumption, approached forty billion dollars. This meant that while the headline price was twenty-two billion, Fiserv was actually taking on a combined obligation closer to twice that amount. For a company that had historically operated with modest leverage, it was a dramatic transformation of the balance sheet.

The skeptics were vocal and numerous. Morningstar published an analysis titled "Fiserv Overpays for First Data," questioning whether the projected nine hundred million in cost synergies was achievable given that the companies did not intend to consolidate their operating platforms. Critics warned that the massive M&A effort would divert resources from investing in emerging technologies. Integration timelines, some analysts estimated, could stretch to a decade. First Data, in this view, was a bloated dinosaur — its technology aging, its merchant relationships under assault from nimbler competitors. Why would you strap that to a perfectly healthy business?

But the strategic logic was compelling, and it rested on a concept that anyone who has studied payments could appreciate.

In the payments world, there are two sides to every transaction. On one side, you have the issuer — the bank that gave the cardholder their credit or debit card. On the other side, you have the acquirer — the company that enables the merchant to accept that card. Historically, these were separate businesses served by separate technology companies. Fiserv was on the issuer side. First Data was the world's largest player on the acquirer side. Merging them created the first truly end-to-end payments platform spanning from card issuance to merchant acceptance.

Revenue synergies were projected at five hundred million dollars: two hundred million from distributing merchant services through Fiserv's massive bank client base, and another two hundred fifty million from expanded payments offerings and network innovations. The cost synergy target of nine hundred million was backed by concrete integration plans.

There was also a significant geographic expansion opportunity. Fiserv earned ninety-five percent of revenue from North America, while First Data earned twenty-two percent internationally. The combined company would have a meaningful global footprint for the first time.

The merger closed on July 29, 2019, right on schedule. It was the largest fintech deal of the year, part of a stunning wave of payments mega-mergers that reshaped the industry in a single twelve-month period. FIS paid thirty-five billion for Worldpay, the British payments processor. Global Payments merged with TSYS in a twenty-one-and-a-half-billion-dollar deal. Together with Fiserv-First Data, these three transactions represented nearly eighty billion dollars of deal value and consolidated the major payments processors into a smaller number of larger entities.

The logic behind this consolidation wave was consistent across all three deals: scale was the only defense against the fintech insurgents. Stripe, Square, and Adyen were growing at extraordinary rates, and the legacy players believed that only by combining their operations could they achieve the investment scale and distribution breadth needed to compete.

Did Fiserv overpay? The debate would rage for years. First Data's business model was roughly forty-two percent card-based payments and security solutions by EBITDA, with global merchant acquiring making up the remaining fifty-eight percent. The merchant business had attractive recurring revenue characteristics and decent margins. But critics argued that Fiserv was paying a premium for a declining asset — a merchant acquiring business built on distribution channels (bank partnerships, independent sales organizations) that were being disrupted by software-led alternatives.

Yet by one crucial measure, the deal proved far more valuable than almost anyone expected. Because inside First Data's sprawling, debt-laden empire, Fiserv had acquired something that most analysts completely overlooked at the time: two hyper-growth startups hiding in plain sight.

IV. The Hidden Jewels: The Rise of Clover and Carat

When the market looked at the First Data acquisition, it saw a legacy payments processor weighed down by private-equity debt. What it missed was that First Data had been quietly nurturing two businesses that would become Fiserv's most important growth engines — assets that, in retrospect, may have justified the entire purchase price on their own.

The first was Clover.

In 2010, a group of engineers — John Beatty, Leonard Speiser, Mark Schulze, and Kelvin Zheng — incorporated a startup with a deceptively simple idea: build a cloud-based, Android-powered point-of-sale system that could turn a countertop terminal into an intelligent business platform. The traditional POS terminal was a dumb box — it could swipe a card and print a receipt, but that was about it. Clover's vision was to make the terminal the center of a merchant's entire business: payments, inventory, employee scheduling, customer loyalty, analytics, all in one device.

In April 2012, they launched their product. In December of that same year, First Data quietly acquired Clover for fifty-six million dollars. Almost no one noticed. It was a rounding error in the context of First Data's massive operations.

But First Data did something unusual with the acquisition — something that violated the typical playbook of large corporations swallowing startups. Rather than absorbing Clover into its bureaucracy, it structured an operating agreement that gave Clover a hundred million dollars in funding and the autonomy to operate independently. Clover would build all new payment hardware and software. First Data would handle sales, distribution, and merchant support. It was a startup incubated inside a corporate giant — the kind of arrangement that usually fails, killed by internal politics and bureaucratic friction. In this case, it thrived.

By the time Fiserv completed the First Data acquisition in 2019, Clover had already begun its transformation from niche POS device to full-fledged small-business platform. Think of what Square did for the sole proprietor and what Toast did for restaurants — Clover was doing something similar but with a distribution advantage that no startup could match.

Here is why that advantage mattered so much. Every bank that ran on Fiserv's core systems was a potential distribution channel for Clover. A community bank in Ohio could offer its small-business customers a Clover terminal bundled with a merchant account, all integrated through Fiserv's infrastructure. The bank got a new product to sell. The merchant got a seamless setup. And Fiserv captured both sides of the transaction — the bank's core processing fees and the merchant's payment processing fees. No pure-play startup could replicate that kind of distribution reach.

The growth numbers told a remarkable story. Clover's gross payment volume — the total dollar value of transactions processed through its devices — climbed past three hundred billion dollars on an annualized basis by 2024. Revenue hit two point seven billion dollars that year, growing twenty-nine percent year-over-year. Clover accounted for roughly half of Fiserv's entire year-over-year revenue growth. By mid-2025, the platform had sold its four millionth device, the fastest pace in its history.

Management set an ambitious target of three and a half billion in Clover revenue for 2025, with a four-and-a-half-billion-dollar annualized run rate expected by 2026.

What made Clover particularly interesting from an investment perspective was what industry observers called the SaaS-ification of its business model — the transformation from a hardware transaction processor into a software platform.

The original value proposition was simple: a better terminal that could accept payments. But Clover evolved into something fundamentally more valuable. Think of it as the operating system for a small business. The hardware — a sleek touchscreen terminal or a handheld device — was the entry point. But the real value was in the software layer on top.

Merchants could access value-added services that turned the terminal into a business management hub: inventory management that tracked stock levels in real time, workforce scheduling through a partnership with Homebase, merchant cash advances through Clover Capital that provided working capital based on transaction history, accelerated payouts that moved money faster, and a growing marketplace of over five hundred third-party applications that added everything from loyalty programs to accounting integrations.

These software and services layers carried significantly higher margins than pure payment processing. Payment processing margins are razor-thin — measured in basis points. Software subscriptions carry gross margins of seventy to eighty percent or more. Roughly twenty-six percent of Clover customers were using these value-added services, and the attach rate was climbing. Monthly software subscriptions ran between fifty-nine and ninety dollars per terminal for most retail and restaurant operations, creating recurring revenue streams that looked more like a SaaS business than a traditional payments processor.

This is why the Clover story excited growth investors even inside a value stock. Every merchant that adopted Clover started by paying transaction fees — the low-margin bread and butter. But over time, as they added software modules, the revenue per merchant climbed and the margin profile improved. The playbook was strikingly similar to what Toast was doing in restaurants and what Shopify was doing in e-commerce: give away the payments at near break-even, then monetize through software. The difference was that Clover had Fiserv's bank distribution channel behind it.

The competitive landscape around Clover deserves careful attention, because it reveals both the platform's strengths and its vulnerabilities.

In the restaurant vertical specifically, Clover and Toast were locked in an increasingly fierce battle. Of roughly seven hundred thirty thousand U.S. restaurant locations, Clover covered about a hundred sixty thousand and Toast about a hundred thirty thousand. But the competition was nuanced in an important way. Toast's average restaurant location processed significantly higher volumes, giving it a sixteen percent share of the nine hundred sixty-two-billion-dollar U.S. restaurant payments market compared to Clover's eight percent. In other words, Clover had more doors, but Toast had the bigger-spending restaurants — the higher-value merchants who generated more revenue per location.

By total POS installations across all verticals, Square led the market with about twenty-eight percent share, Toast held twenty-three percent, and Clover registered around six and a half percent. But here is the counterintuitive part: Clover's absolute payment volume — over three hundred billion dollars — exceeded both Square and Toast individually. The discrepancy reflected Clover's broader merchant base spanning restaurants, retail, professional services, and beyond, compared to Toast's restaurant-only focus and Square's micro-merchant concentration.

If Clover was the breakout star, the second hidden jewel was quieter but equally important for understanding Fiserv's long-term positioning: Carat, the company's enterprise commerce platform, and its technical backbone, Commerce Hub.

If Clover was the small-business play — restaurants, retail shops, hair salons — Carat was the enterprise play, operating at an entirely different scale. This was a global platform orchestrating payments and commerce experiences for some of the world's largest companies. The client roster read like a Fortune 100 roll call: Google, Microsoft, ExxonMobil, State Farm, Adidas, DoorDash. These were relationships where a single client might process billions of dollars in annual payment volume across multiple countries, currencies, and channels. Carat competed directly against Adyen, FIS, and Stripe in the enterprise payments arena — a market where reliability, global reach, and compliance capabilities matter as much as technology elegance.

Commerce Hub, the API layer underneath Carat, represented Fiserv's attempt to modernize its technology stack for the developer-first era.

To understand why this matters, consider the developer experience challenge that legacy processors face. In the old world of payments, integrating with a processor meant exchanging thick specification documents, writing custom code to handle dozens of message formats, testing extensively against certification environments, and waiting months for approval. This was the world Fiserv and First Data grew up in.

In the new world, Stripe had shown that a developer could start accepting payments in an hour with a clean, well-documented REST API and beautiful developer tools. Adyen offered something similar for enterprise clients. The gap in developer experience between the old guard and the new challengers was enormous, and it was driving market share shifts.

Commerce Hub was Fiserv's answer. Think of it as a universal translator for payments. Through a single API specification — essentially one set of instructions that developers could integrate once — enterprise clients could access a unified suite of payment capabilities: credit cards, Apple Pay, Google Pay, real-time settlement, fraud detection, and compliance tools. No need to integrate separately with multiple providers. It was not yet as clean or as developer-friendly as Stripe's API, but it was a significant step forward from the legacy integration experience. Revenue growth in the Carat business had been running in the low twenties in percentage terms, though the exact breakdown was not always disclosed separately from the broader merchant solutions segment.

In October 2024, Fiserv announced a landmark embedded finance partnership with DoorDash that illustrated the full potential of the Carat and Finxact stack working together. Through the DoorDash Crimson Program, Fiserv began delivering banking services directly to delivery drivers — Dashers — through the Dasher App.

The architecture was elegant and worth understanding because it represents where the entire financial services industry is heading. Finxact, a cloud-native core banking ledger that Fiserv had acquired in 2022, provided the banking infrastructure — the account records, the deposit insurance compliance, the ledger. Carat handled the payments rails — the ability to move money in and out. And Starion Bank, a community bank that happened to be a long-time Fiserv core banking client, served as the regulated sponsor bank, providing the actual banking license.

This is what the industry calls "embedded finance" — and it is strategically critical. To understand why, consider how the financial services industry is being restructured.

Historically, if you wanted to offer banking services, you needed a banking charter — a government license that came with enormous regulatory burdens, capital requirements, and compliance costs. Only banks could hold deposits, issue cards, and process payments. But technology has made it possible to unbundle these capabilities into modular services that any company can plug into.

Now, ride-sharing platforms want their drivers to have instant access to earnings. E-commerce marketplaces want sellers to have working capital loans. Gig economy apps want workers to have debit cards that receive real-time payouts. None of these companies want to become banks — that would mean submitting to banking regulators, holding regulatory capital, and managing compliance infrastructure that would dwarf their core business. They need a technology partner that can provide the full stack.

Fiserv, with Finxact for ledger capabilities and Carat for commerce, was positioning itself as exactly that partner. The DoorDash deal was proof of concept. If it could be replicated across dozens or hundreds of large non-financial brands, it would represent an entirely new growth vector — one that leveraged Fiserv's unique combination of banking infrastructure and payments technology in a way that no pure-play fintech competitor could easily replicate.

By 2024, the market was beginning to wake up to the Clover and Carat story. Analysts who had initially dismissed the First Data acquisition as overpaying started publishing notes about the hidden growth engines inside Fiserv. If Clover were a standalone public company, some estimated, it might command a valuation approaching half of Fiserv's entire market cap. The boring bank-software company had become, almost by accident, one of the most important payments platforms in America.

But all of this growth was about to be called into question by a leadership transition that would expose serious cracks in the foundation — cracks that, in hindsight, had been growing wider for years while the stock price told a very different story.

V. The Management Drama: The Bisignano Era and the 2025 Crisis

Every great corporate drama needs a protagonist whose strengths contain the seeds of their own undoing. In the Fiserv story, that protagonist was Frank Bisignano.

He was not the kind of executive who blended into the background.

A finance graduate from Baker University, he had built his career at the sharp end of Wall Street operations — not as a dealmaker or a strategist, but as the person who made things run. At Citigroup, he rose to Chief Administrative Officer for the Corporate and Investment Bank and CEO of Global Transaction Services — the world's largest securities and cash management operation. That role meant overseeing the movement of trillions of dollars daily across global markets. When the September 11 attacks destroyed Citigroup's offices at 7 World Trade Center, it was Bisignano who led the relocation of over sixteen thousand employees — a logistical feat that earned him a reputation as someone who could execute under impossible conditions.

At JPMorgan Chase, he was appointed Chief Administrative Officer in 2005 and elevated to co-Chief Operating Officer in 2012, where he earned a reputation as a "fixer" — the executive you brought in when operations were broken and needed someone willing to tear through bureaucracy to get results. Jamie Dimon valued him for exactly this quality.

In 2013, Bisignano left JPMorgan to become CEO of First Data. The company was still staggering under its KKR-era debt load, losing money quarter after quarter. Over the next six years, he transformed it — restructuring operations, investing in Clover, and steering the company through its 2015 IPO.

When Fiserv acquired First Data in July 2019, Bisignano joined as President and COO. By July 2020, he had taken over as CEO. By May 2022, he was Chairman of the Board. In the culture of corporate America, this was something close to a reverse takeover — the acquired company's chief executive ascending to run the acquirer.

Under Bisignano's leadership, Fiserv's stock price doubled from its mid-2020 levels, creating approximately sixty billion dollars in shareholder value at its peak. He was handsomely rewarded. In 2023, his total compensation package was approximately twenty-eight million dollars, comprising a one-point-four-million-dollar base salary, twenty-three million in stock awards, and three million in cash bonuses. His compensation increased further in 2024 — reportedly up fifty-seven percent.

The stock awards were the critical piece. They were heavily weighted toward performance metrics tied to aggressive margin expansion and revenue growth targets. Hit the targets, and the equity vested. Miss them, and millions evaporated. This created a powerful incentive to do whatever was necessary to hit the numbers.

And hit them he did — quarter after quarter, year after year. Operating margins expanded. Earnings per share beat estimates. The stock climbed.

But behind the headline numbers, a more complicated picture was emerging.

Employee sentiment, as captured in Glassdoor reviews and anonymous forums, painted a portrait of a CEO who demanded results at any cost. Former employees described a culture that had shifted "from accommodating and cooperative, to only manage by dictatorship." Decision-making was called "erratic." Mid-level managers described being pressured to hit quarterly targets through whatever means necessary — cutting vendor contracts, deferring maintenance, reducing headcount — with little regard for the downstream consequences.

Bisignano executed significant layoffs: a hundred positions at the Dublin, Ohio technology center in 2020, roughly three thousand workers across the company in 2023, and further cuts in December 2024. R&D spending, according to later disclosures from the new management team, was squeezed to fund near-term margin expansion. Product launches were delayed. Technology investments were deferred. Client-facing resources were reduced to the bone.

These cost reductions looked excellent on quarterly earnings calls. Operating margins expanded beautifully. Earnings per share beat estimates with metronomic consistency. The stock climbed. Analysts praised management's "operational discipline." But the question no one was asking loudly enough was: what happens when you stop investing in the product that your customers depend on?

The first crack appeared in an unlikely place: Argentina.

Through First Data's international operations, Fiserv had significant exposure to the Argentine market. Argentina's hyper-inflationary economy had been producing extraordinary nominal growth numbers for Fiserv — organic revenue growth of two hundred fifty-seven percent in Argentina in 2023, and a staggering three hundred twenty-nine percent in 2024. These numbers were real in accounting terms, but they reflected inflation-driven transaction values rather than genuine business expansion. Think of it this way: if a cup of coffee costs a hundred pesos one year and three hundred pesos the next year because of inflation, the payment processor reports three times the transaction volume. The processor is not doing three times the work or winning three times the customers. The currency is simply worth less.

The impact on Fiserv's reported results was massive. Argentina alone contributed roughly ten percentage points of Fiserv's reported sixteen percent organic growth in 2024. Strip out Argentina, and organic growth was closer to six percent — a good number, but a far cry from the double-digit growth the market was pricing in.

When the Argentine economy stabilized in 2025 following currency reforms, this tailwind collapsed virtually overnight. Management had initially assumed seven points of contribution from Argentina for 2025, then revised down to four mid-year, and eventually acknowledged near-zero contribution. The inflationary sugar rush was over, and the underlying business growth rate was exposed.

The second crack was Clover itself. The growth numbers that had dazzled investors — twenty-nine percent revenue growth in 2024, three hundred ten billion dollars in gross payment volume — contained a troubling secret. Beginning in late 2023, Fiserv had forcibly migrated up to two hundred thousand merchants from an older platform called Payeezy to Clover.

Payeezy was a simpler, cheaper gateway inherited from First Data. The merchants on it were typically price-sensitive, often low-volume businesses that had been on Payeezy precisely because it was cheap and simple. When they were moved to Clover's more expensive platform — often without advance warning or adequate support — many revolted. They faced new fees they had not anticipated. They had to learn new hardware and software. A significant portion simply left, switching to cheaper competitors like Square.

The forced migration inflated Clover's device counts and gross payment volume in the short term while creating a wave of attrition that would show up in later quarters. And critically, when investors asked about Clover's growth on earnings calls, the implication was that it was coming from new merchant adoption — organic growth driven by Clover winning in the market. The forced Payeezy conversion was not prominently disclosed as a driver.

On December 4, 2024, President-elect Donald Trump nominated Bisignano to serve as Commissioner of the Social Security Administration. The U.S. Senate confirmed him on May 6, 2025, at which point he immediately resigned from all positions at Fiserv. Between May and August 2025, complying with a federal Certificate of Divestiture under government ethics rules, Bisignano sold approximately five hundred thirty to five hundred sixty million dollars' worth of Fiserv stock.

His successor was Michael P. Lyons, a veteran financial services executive with a very different profile from Bisignano. Where Bisignano was an operator who thrived in the trenches of corporate logistics, Lyons was an investor-turned-executive. He had served as a portfolio manager at Maverick Capital, the prestigious long-short equity fund founded by Lee Ainslie, before moving to the operating side as President of PNC Financial Services Group — one of the largest regional banks in America. He also chaired Early Warning Services, the bank consortium behind Zelle and the PAZE digital wallet, giving him deep familiarity with modern payments infrastructure and collaborative industry initiatives.

Lyons was named CEO-elect on January 27, 2025, and formally assumed the role on May 6. His investment background gave him a particular sensitivity to the gap between reported numbers and underlying business health — exactly the kind of scrutiny that Fiserv's numbers had not received in years.

What happened next became one of the most dramatic earnings calls in recent corporate history.

On October 29, 2025, Fiserv reported third-quarter results. The numbers landed like a bomb.

Adjusted earnings per share of two dollars and four cents missed the consensus estimate of two sixty-four by a staggering sixty cents — an unprecedented miss for a company that had beaten estimates with clockwork regularity under Bisignano. Revenue of four point nine two billion fell short of the five point three six billion forecast. These were not the kind of minor misses that analysts shrug off. They were blowout misses that shattered the narrative of reliable, predictable outperformance that had been built over the prior four years.

But the numbers were only part of the story. On the call, Lyons delivered a methodical, devastating indictment of his predecessor's management. He told analysts and investors that Fiserv's recent performance had "increasingly relied on short-term initiatives" that placed "too much emphasis on pursuing in-quarter results as opposed to building long-term relationships." He disclosed that prior management had made "decisions to defer certain investments and cut certain costs" that improved margins in the short term but were "now limiting" the company's "ability to serve clients, execute product launches, and grow revenue."

Lyons slashed full-year EPS guidance from the ten-fifteen to ten-thirty range down to eight-fifty to eight-sixty — a reduction of nearly twenty percent. Revenue growth guidance was cut from ten percent to three and a half to four percent. He described the previous guidance as "objectively difficult to achieve." He characterized his plan as "a critical and necessary reset."

The market's reaction was instantaneous and brutal.

Fiserv stock plummeted forty-four percent in a single trading session — from a hundred twenty-six dollars and seventeen cents to seventy dollars and sixty cents — erasing approximately thirty billion dollars in market value in a matter of hours. Trading volume exploded to multiples of the daily average as institutional investors rushed for the exits. It was the worst single day in the company's four-decade history and one of the largest single-day destructions of shareholder value in the history of financial technology.

The stock continued to slide in the weeks that followed, eventually falling below sixty dollars by early 2026 — a seventy-five percent decline from its all-time high of two hundred thirty-eight dollars reached just months earlier in March 2025. A company that had been worth over a hundred billion dollars was now valued at roughly thirty-four billion.

The timing of Bisignano's stock sales immediately drew scrutiny. If he had held his shares through the crash, the five hundred thirty to five hundred sixty million dollars he received would have been worth roughly two hundred twenty-nine million — meaning he avoided an estimated three hundred million or more in losses. The Certificate of Divestiture provided favorable tax treatment on the sales, and the timing — selling before the problems surfaced — raised obvious questions.

Congressional representatives John Larson and Jim Himes referred Bisignano to the SEC for investigation. Senators Ron Wyden and Elizabeth Warren launched a separate probe into his stock sell-off and potential conflicts of interest. The senators raised pointed questions about a Direct Express debit card contract between Fiserv and the Social Security Administration — a contract that Bisignano, in his new government role, now had oversight responsibility for. The optics were, to put it mildly, challenging.

Neither investigation has produced formal findings as of early 2026, and Bisignano has not been charged with any wrongdoing. But the regulatory and congressional scrutiny adds a political dimension to what is already a complex corporate governance story.

Multiple securities fraud class action lawsuits followed, each adding layers to the narrative of alleged mismanagement. The City of Hollywood Police Officers' Retirement System filed a suit alleging that Fiserv had concealed the slowdown in new merchant business by disguising forced Payeezy migrations as organic Clover growth. The lawsuit alleged that from at least mid-2024 through October 2025, Fiserv's officers made materially false and misleading statements about the company's business, operational performance, and financial outlook.

A second class action, covering the period after the July 2025 guidance reaffirmation, alleged that the guidance had been based on assumptions that Fiserv later admitted were "objectively difficult to achieve" — raising the question of whether management knew the targets were unrealistic when they publicly endorsed them. Major law firms including Kessler Topaz, Hagens Berman, and Rosen Law were actively pursuing claims. As of early 2026, these lawsuits remain in their early stages, and no findings of fraud have been established. But the legal overhang adds meaningful uncertainty to an already complex investment picture.

The Bisignano era at Fiserv had become a textbook case study in misaligned incentives — one that business school case writers will likely study for years to come.

A compensation structure that rewarded aggressive, short-term margin expansion and growth targets had created powerful incentives for management to defer investments, cut costs, inflate metrics through forced conversions, and ride geographic tailwinds without adequately disclosing their unsustainability. Each quarter, the playbook worked. Hit the number. Collect the bonus. Watch the stock rise. Repeat. The stock price doubled in four years, creating the appearance of extraordinary value creation.

But value creation and value extraction are different things. When Bisignano left Fiserv, he did so as one of the highest-paid executives in the fintech industry, having collected hundreds of millions of dollars in compensation and stock sales. When the music stopped months later, ordinary shareholders absorbed losses exceeding fifty billion dollars from peak to trough. The asymmetry between executive reward and shareholder consequence was stark — and it is exactly the kind of principal-agent problem that corporate governance is supposed to prevent.

VI. Playbook: Frameworks, Business, and Investing Lessons

The Fiserv saga offers an unusually rich set of lessons when examined through classic business strategy frameworks. This is not a simple story of a company that failed. It is a story of extraordinary structural advantages that were gradually undermined by poor capital allocation and misaligned incentives — a distinction that matters enormously for investors trying to assess the company's future.

Start with Hamilton Helmer's 7 Powers framework, which identifies the sources of durable competitive advantage. Of the seven powers — switching costs, scale economies, network economies, counter-positioning, cornered resource, branding, and process power — Fiserv possesses at least two in meaningful measure.

Fiserv's most formidable power is switching costs — and they may be the most extreme example of switching costs in all of enterprise software. A bank running its operations on Fiserv's core system is integrated at the deepest possible level. The core touches every customer account, every transaction record, every regulatory report, every digital banking channel. Replacing it requires re-integrating dozens of downstream systems, migrating millions of customer records, satisfying regulatory requirements, and executing the cutover without a single minute of downtime.

Consider the stakes: a mid-size bank conversion can cost fifty to two hundred million dollars and take three to five years. The risks are existential — a botched conversion can trigger regulatory action, customer flight, and reputational damage. This is why Fiserv maintains roughly ninety-nine percent client retention in its core banking business. Banks will tolerate mediocre service, aging technology, and rising prices before they will attempt to rip out their core. This is not merely a competitive advantage. It functions almost as a natural monopoly for the installed base.

The second power is scale economies, most pronounced on the payment processing side. Payment processing has an unusual cost structure: the fixed costs of building and maintaining the infrastructure — data centers, network connections, security systems, compliance frameworks — are massive, but the marginal cost of processing each additional transaction is essentially zero.

Here is a simple way to think about the economics. When a merchant accepts a hundred-dollar credit card payment, the processor might charge one percent — one dollar. Out of that dollar, roughly fifty cents goes to the card-issuing bank as interchange, and thirty cents goes to the card network like Visa or Mastercard. The processor keeps about twenty cents. On a single transaction, that is barely worth the effort. But multiply it by forty billion transactions per year, and you have a machine that generates billions in revenue with minimal incremental cost. The company that processes the most transactions can spread its fixed costs most thinly, offer the most competitive pricing, and still maintain healthy margins. Fiserv, as one of the two largest merchant acquirers in the United States, has genuine scale advantages here.

Now apply Porter's Five Forces. The most important force for Fiserv's future is the threat of new entrants and substitution.

Despite the enormous switching costs in core banking, the competitive walls on the payment processing side are eroding. Cloud-native, developer-first companies like Stripe and Adyen have built fundamentally different technology stacks. A developer integrating Stripe can be processing payments within an hour. Integrating with a legacy processor like Fiserv can take months. That difference in developer experience matters enormously as software companies — not banks — increasingly control where payment volume flows.

Stripe dominates U.S. e-commerce payment processing with roughly sixty-eight percent market share. Adyen has cracked the top ten global merchant acquirers. Toast has built a vertical payments stack so deeply embedded in restaurant operations that switching requires changing the entire restaurant management system.

And behind these specific competitors sits a broader structural shift that may be the single most important trend in payments. Bain and Company estimates that roughly twenty-five percent of U.S. payment volume currently flows through software platforms, and they project that figure will reach seventy percent by 2030. In other words, the bank-distribution channel that historically powered Fiserv's merchant services is being displaced by software companies embedding payments directly into their platforms. A restaurant uses Toast. An e-commerce store uses Shopify Payments. A gig-economy platform uses Stripe Connect. The bank referral — once Fiserv's golden distribution channel — becomes less relevant with each passing year.

The supplier power dynamic is also worth noting. The card networks — Visa and Mastercard — exercise significant power over processors like Fiserv, setting interchange rates and network fees that processors must pay. These costs are essentially non-negotiable and represent the largest single expense category in the merchant acquiring business. Fiserv has limited ability to squeeze its supply chain, which puts even more pressure on achieving scale to maintain margins.

The capital allocation lesson may be the most valuable takeaway of all. Tying massive equity compensation to short-term margin and growth targets — as Fiserv did during the Bisignano era — creates a predictable set of incentive distortions. Executives face powerful temptation to cut R&D spending, defer maintenance investments, push aggressive pricing, and ride unsustainable geographic tailwinds, all in service of hitting the numbers that trigger their bonuses.

For a period, this looks like outstanding execution. Margins expand. Earnings beat estimates. The stock rises. But when the short-term levers are exhausted, the company finds itself with degraded technology, alienated customers, and a credibility gap with investors that can take years to repair. Charlie Munger once observed: "Show me the incentive and I will show you the outcome." Fiserv's 2025 crisis was the outcome.

For investors tracking Fiserv going forward, two key performance indicators matter more than anything else on the income statement or balance sheet.

The first is Clover's organic gross payment volume growth — not just revenue, but the volume figure stripped of forced migrations and one-time conversions. This is the single best measure of whether Clover is actually winning new merchants in competitive markets. Revenue can be influenced by pricing changes, mix shifts, and accounting treatment. GPV is harder to game — it reflects real transactions flowing through real merchants. A sustained recovery to double-digit organic GPV growth would signal that the franchise is healthy despite the management disruption. A continued deceleration would signal structural competitive weakness that no amount of operational restructuring can fix.

The second is core banking client retention and renewal rates. This metric signals whether the moat is holding — whether the switching costs that have protected Fiserv's franchise for four decades remain intact. Over the next three to five years, hundreds of banks will face core modernization decisions. Fiserv's ability to retain those clients and migrate them to its next-generation platforms like CoreAdvance and Finxact — rather than losing them to cloud-native challengers — will determine the long-term trajectory of its most valuable asset.

As long as Fiserv retains its core banking clients and Clover demonstrates genuine organic GPV growth, the fundamental value proposition remains intact regardless of short-term earnings noise.

VII. Bear vs. Bull Case

The Bear Case: A Fortress Under Siege

The pessimistic case for Fiserv begins with a simple observation: the 2025 crisis was not an accident. It was the inevitable consequence of years of underinvestment, and the resulting technology debt cannot be repaired quickly or cheaply.

When Mike Lyons acknowledged that prior management had deferred investments and cut costs to inflate margins, he was admitting that Fiserv's infrastructure — the very thing the company sells — had been allowed to atrophy. Rebuilding it requires significant capital expenditure at a time when the company carries over thirty billion dollars in long-term debt and has guided free cash flow down to approximately four and a quarter billion for 2026.

The competitive picture is deteriorating on multiple fronts. In enterprise payments, Adyen grew processing volume roughly twenty percent in 2024 and has penetrated the top tier of global merchant acquirers. Stripe's estimated revenue exceeds thirty-seven billion dollars at a growth rate of approximately thirty percent, and it controls nearly seventy percent of U.S. e-commerce payment processing. In the small-business POS market, Toast is gaining share rapidly in the restaurant vertical — Clover may cover more locations, but Toast processes significantly higher volume per location, suggesting it is winning the more valuable merchants.

More fundamentally, the distribution channel that historically powered Fiserv's merchant services — bank referral partnerships — is weakening. Wells Fargo and Bank of America have both exited or restructured their Fiserv merchant services arrangements. Independent sales organizations, once the backbone of merchant acquiring distribution, are losing relevance as software companies embed payments directly into their platforms. This is the structural risk that no amount of internal restructuring can solve.

The Clover deceleration is real and concerning. GPV growth dropped from fourteen to seventeen percent in 2024 to just eight percent in the first quarter of 2025 — a steep decline that management attributed partly to Payeezy migration attrition. If the forced migration strategy artificially inflated Clover's growth, the underlying organic trajectory may be far weaker than published numbers suggest. The securities fraud lawsuits, though not yet resolved, add litigation risk and potential settlement costs.

The 2026 guidance of one to three percent organic revenue growth and adjusted EPS of eight to eight-thirty represents a dramatic step down. Management explicitly calls 2026 a "transition year." The bear case is that this transition takes longer and costs more than anyone currently anticipates, while nimbler competitors continue to gain share.

Through a Porter's Five Forces lens, the bear case is comprehensive and sobering.

The bargaining power of buyers is increasing on the merchant side. Large enterprise merchants like Walmart, Amazon, and DoorDash can credibly threaten to switch to Stripe or Adyen, driving down pricing. The threat of substitution is arguably the most dangerous force — software-led payment platforms are not just competing with Fiserv on price, they are fundamentally changing the channel through which merchants access payments. When a restaurant adopts Toast, it does not separately choose a payment processor. Payments are embedded in the software. The decision is made at the software layer, and the payment processing follows automatically.

The rivalry among existing competitors has intensified dramatically. FIS, despite its own struggles with the Worldpay acquisition (which it partially unwound in 2024), remains a formidable competitor. Global Payments and TSYS are aggressively pursuing the same integrated commerce vision. And the fintech challengers — Stripe, Adyen, Toast, Block — have enormous war chests and are investing billions in technology development while Fiserv is in remediation mode.

The only force working clearly in Fiserv's favor — the near-impossibility of customers switching core banking providers — is confined to a segment that grows in the low single digits. It is a powerful defensive moat but not a growth engine.

The Bull Case: A Generational Reset

The optimistic case for Fiserv rests on three pillars, each powerful on its own and potentially transformative in combination.

First, Mike Lyons is executing a classic "kitchen sink" strategy — a well-worn playbook where a new CEO takes all the pain in a single quarter, writes off bad decisions, and resets the baseline to a level that future results can consistently beat. The Q4 2025 results showed the first evidence that this approach may be working: adjusted EPS of a dollar ninety-nine beat the lowered estimate of a dollar ninety, and the stock rallied nearly eight percent on the report.

Lyons brought in serious operators. Takis Georgakopoulos, JPMorgan Chase's former global head of payments, and Dhivya Suryadevara, formerly CFO of General Motors, were named co-presidents. Paul Todd was brought in as CFO. Three new independent directors were added to the board. The "One Fiserv" restructuring plan is explicitly prioritizing long-term relationship building over in-quarter metric optimization. This is a management team with credibility and a clear mandate to fix what was broken.

If Lyons succeeds in restoring credibility, the valuation upside is substantial. The stock is trading at approximately seven to ten times earnings — a fraction of its historical multiple of twenty to twenty-five times and a fraction of what comparable fintech companies command. Adyen trades at roughly forty times earnings. Even battered legacy payments companies like FIS trade at higher multiples. The compression in Fiserv's valuation represents a significant gap between current price and what would be fair for a company with Fiserv's recurring revenue profile, free cash flow generation, and market position. Even a modest re-rating to fifteen times earnings would imply significant upside from current levels.

Second, Clover remains an extraordinary asset that the market may be severely undervaluing at current levels. Even stripping out the forced migration noise, Clover generated two point seven billion dollars in revenue in 2024, growing at a pace that would be the envy of most public SaaS companies. It has four million devices in the field, a growing software and services layer, and international expansion opportunities in Australia, Japan through a partnership with Sumitomo Mitsui, and beyond.

If Clover were a standalone public company, its revenue base and growth profile would likely command a valuation of fifteen to twenty-five billion dollars — which would represent a substantial portion of Fiserv's current depressed market cap of roughly thirty-four billion. In Hamilton Helmer's framework, Clover possesses the power of network economies through its app marketplace — every new merchant on the platform makes Clover more attractive to third-party software developers, and every new app makes Clover more attractive to merchants. This self-reinforcing cycle, if managed correctly, could drive sustained growth for years.

Third, and most fundamentally, Fiserv's core banking clients are not going anywhere. The structural moat — the switching costs, the multi-year contracts, the integration depth, the regulatory barriers to migration — remains as formidable as ever. Fiserv supports over forty percent of U.S. banks. Those banks need technology to modernize, and Fiserv is investing in next-generation platforms like CoreAdvance and Finxact to retain them.

Over the next three to five years, many banks will face core renewal decisions — what the industry calls "core modernization mandates" — driven by aging infrastructure, cloud migration pressures, and competitive demands from digital-first challengers. These are strategic decisions touching data architecture, cloud strategy, risk posture, and customer experience design. Fiserv, with its installed base advantage and its modernization offerings, is the default choice for the vast majority of those renewals. This annuity-like revenue stream generates billions in recurring cash flow that underpins the entire business regardless of what happens in the more competitive merchant acquiring market.

The bull case, in essence, is that the market has priced Fiserv for permanent impairment when the actual situation is one of temporary dislocation caused by short-term management malpractice. The franchise — the core banking moat, the Clover growth engine, the Carat enterprise platform, the four-plus billion in annual free cash flow — is damaged but not destroyed. At current valuations, the market is essentially giving investors the merchant acquiring and payments business for free on top of the core banking franchise.

VIII. Epilogue

In December 2025, Fiserv's new management team announced sweeping changes under the "One Fiserv" banner. The company expanded its partnership with ServiceNow around AI-enabled operations and IT service management. It increased client-facing resources and added senior talent. It explicitly acknowledged that 2026 would be a transition year, with organic revenue growth guided to just one to three percent and adjusted operating margins expected around thirty-four percent.

Free cash flow guidance came in at approximately four and a quarter billion dollars, down from a previous five and a half billion estimate. These were not numbers designed to excite Wall Street. They were numbers designed to be real — a deliberate contrast with the unachievable targets that had preceded them.

Lyons also announced a fundamental restructuring of how the company would be managed. The "One Fiserv" strategy consolidated previously siloed business units into a unified organization with clearer accountability. Client relationship management was overhauled, with dedicated teams assigned to strategic accounts rather than having merchants bounced between sales, support, and billing organizations that did not communicate. Investment in technology was being increased, with specific focus on modernizing the merchant onboarding experience, improving Clover's platform stability, and accelerating the rollout of CoreAdvance and Finxact to next-generation banking clients.

The February 2026 Q4 earnings report provided the first glimmer that the reset might be working. Adjusted EPS beat lowered expectations. Full-year 2025 revenue came in at twenty-one point one nine billion, with adjusted EPS at eight fifty-five — within the guidance range Lyons had set. The stock jumped nearly eight percent on the report. Analysts remained divided, with consensus price targets ranging from fifty dollars on the low end to two hundred fifty on the high end, reflecting genuine uncertainty about whether the turnaround will succeed.

In the payments industry more broadly, the post-crisis period has vindicated neither the mega-merger thesis nor the pure-play fintech thesis entirely. Both models have produced winners and losers. The reality, as is often the case, is messier than either narrative allows.

The Fiserv story is ultimately about the tension between two kinds of value creation.

The first is structural: the patient, unglamorous work of building technology infrastructure that becomes so deeply embedded in customers' operations that it generates decades of recurring revenue. George Dalton and Leslie Muma understood this. They built a company on the stickiest product in enterprise software, and for thirty-five years, that foundation generated extraordinary compounding returns.

The second kind of value creation is financial: the optimization of margins, the engineering of earnings beats, the management of investor expectations. Frank Bisignano was a master of this craft. He doubled the stock price in four years through cost discipline, aggressive growth targeting, and relentless operational focus. But when the optimization ran ahead of the underlying reality — when margins were inflated by deferred investment, growth was inflated by forced conversions and inflationary tailwinds, and the gap between the story and the substance grew too wide — the reckoning was swift and devastating.

The core banking moat is real. Clover's potential is real. The four billion dollars in annual free cash flow is real. But so is the technology debt, the litigation risk, and the competitive pressure from a generation of cloud-native attackers who are rewriting the rules of how money moves.

There is also a deeper strategic question that the Fiserv story raises about the payments industry writ large. The 2019 mega-merger wave — Fiserv-First Data, FIS-Worldpay, Global Payments-TSYS — was premised on the idea that scale would be the defining competitive advantage in payments. Bigger companies could spread fixed costs more efficiently, offer end-to-end solutions, and invest more in technology. Six years later, the scorecard is mixed at best. FIS partially unwound its Worldpay acquisition. Fiserv is in crisis. Global Payments has faced its own growth challenges. Meanwhile, the companies that have done best — Stripe, Adyen, Toast — are the ones that built superior technology rather than buying scale.

The question facing Fiserv investors is not whether the company will survive — it almost certainly will, protected by the switching costs that make its core banking franchise nearly indestructible. The question is whether the new management team can rebuild trust, reinvest in the technology, and reignite organic growth before the competitive window narrows further. Whether scale, properly managed, can still win in an industry that increasingly rewards innovation.

The next twelve to twenty-four months will provide the answer.

Recommended Reading and Resources:

- Fiserv Investor Relations — Quarterly Earnings and SEC Filings

- Fiserv to Combine with First Data Corporation (2019 Merger Announcement)

- History of Fiserv, Inc. — FundingUniverse

- How KKR's Buyout Saddled First Data with Massive Debt — AJC

- Fiserv Stock Craters 44% for Worst Day Ever — CNBC (October 2025)

- Frank Bisignano Ducks $300 Million Fiserv Loss — Bloomberg

- Fiserv's $30 Billion Wipeout After Client Revolt Over Fees — Bloomberg

- Why Fiserv Stock Tanked 65% in 2025 — TIKR Analysis

- Fiserv CEO Explains Struggles — Payments Dive

- The 2025 McKinsey Global Payments Report

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube