Fidelity National Information Services (FIS): The Fintech Infrastructure Giant That Powers Global Commerce

I. Introduction & Episode Setup

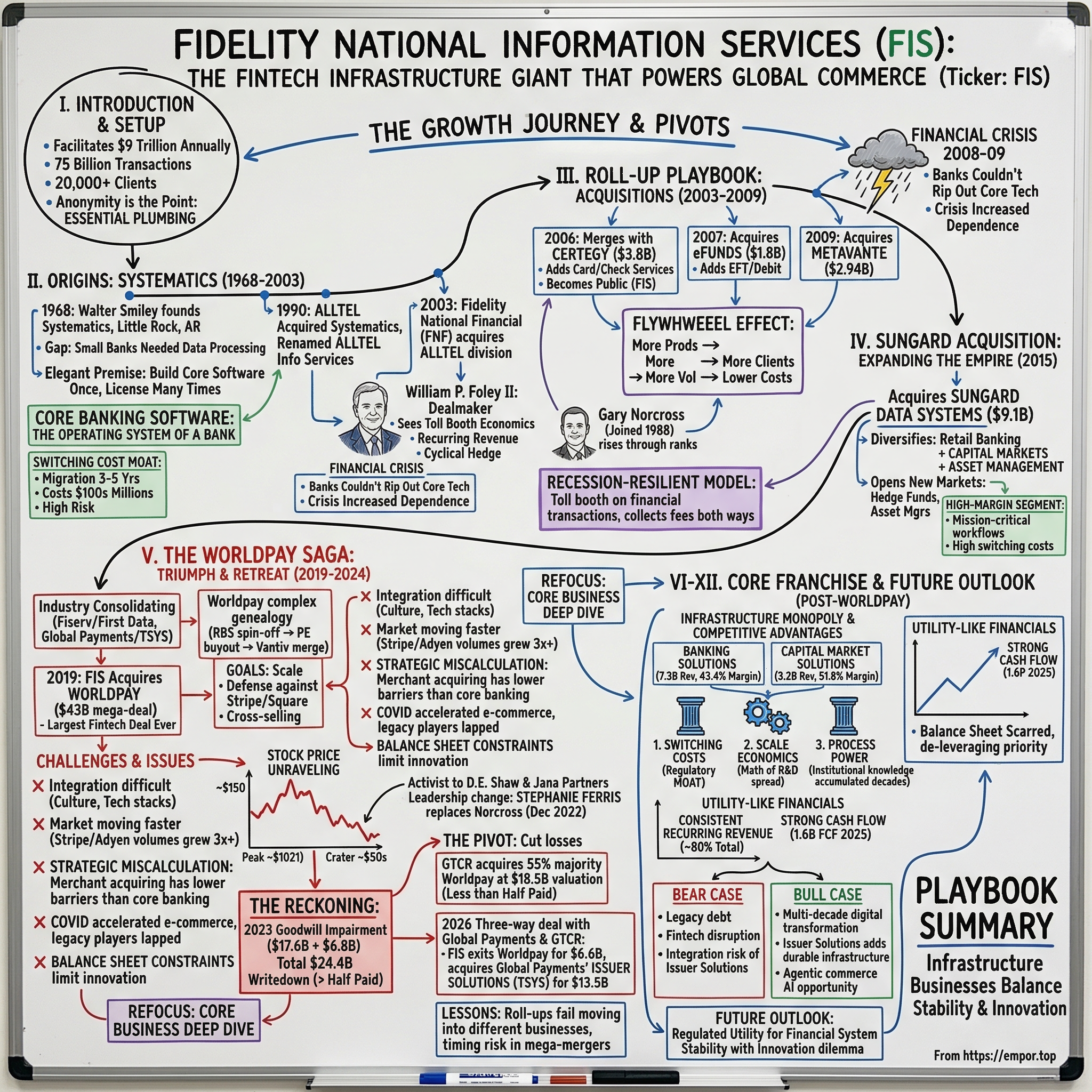

Every time a bank processes a mortgage payment in Oklahoma, every time a hedge fund in London settles a derivatives trade, every time a community credit union in Wisconsin runs a batch of overnight transactions—there is a very good chance that a single company's software is making it happen. That company is Fidelity National Information Services, known simply as FIS.

The numbers are staggering. FIS facilitates the movement of roughly nine trillion dollars through the processing of approximately seventy-five billion transactions annually. It operates in fifty-eight countries, employs tens of thousands of people, and serves more than twenty thousand clients. And yet, unless you work in financial services technology, you have probably never heard of it. That anonymity is, in some ways, the point. FIS is plumbing—unglamorous, essential, and extraordinarily difficult to replace.

The central question of this story is deceptively simple: How did a small data processing startup in Little Rock, Arkansas, become the backbone of global financial infrastructure? The answer involves one of the most aggressive roll-up strategies in corporate history, a title insurance magnate with a taste for deal-making, a forty-three-billion-dollar mega-acquisition that went spectacularly wrong, and a dramatic pivot that is still unfolding as of early 2026.

The themes that run through FIS's history are ones that any student of business strategy will recognize: the seductive logic of infrastructure monopolies, the compounding power of switching costs, the perils of mega-mergers, and the tension between building for stability and building for innovation. It is a story about what happens when a company becomes so deeply embedded in the financial system that ripping it out would be like performing open-heart surgery on the global economy—and about what happens when that same company overreaches.

This is the story of FIS.

II. Origins: The Systematics Story (1968-2003)

In October 1968, in a modest office in Little Rock, Arkansas, a man named Walter V. Smiley founded a company called Systematics with $400,000 in startup capital from Stephens Inc., the powerful Little Rock-based investment bank run by Jack Stephens. Smiley was a native of Hope, Arkansas, who had earned his MBA from the University of Arkansas before working as an IBM salesman in St. Louis and then as director of data processing for First National Bank in Fayetteville. It was in those roles—selling IBM systems to banks and then running them for a bank—that Smiley identified a gap so fundamental it would define his career: small and mid-sized banks faced prohibitively high costs implementing data processing systems, and most could not afford their own mainframe operations.

Systematics stepped into that gap. The company's founding premise was elegant in its simplicity: build core banking software once, then license it to dozens, even hundreds, of banks. Each additional customer would cost incrementally less to serve, while the revenue would compound. It was a model that would later become the gospel of enterprise software, but in 1968, it was genuinely pioneering. Most banks still processed transactions by hand or relied on mainframe service bureaus run by larger banks. Systematics offered something different—a standardized software platform that smaller banks could run on their own systems, giving them the technological capabilities of institutions many times their size.

Remarkably, Systematics began making money within months of its founding, establishing profit margins averaging ten to fifteen percent throughout the 1970s. But the early years were still a grind in terms of market education. Selling software to bankers in the late 1960s and early 1970s was like selling electric cars in the 1990s—the logic was sound, but the market was not ready. Banks were conservative institutions run by conservative people, and the idea of entrusting their most sensitive operations to a computer program written by a startup in Arkansas required a leap of faith that many were not prepared to make. Systematics survived by being relentless about customer service and painstakingly reliable. In banking software, uptime is not a nice-to-have; it is existential. A bank that cannot process transactions does not just lose revenue—it loses trust, which is the only real asset a bank has.

By 1977, revenue had reached $13.3 million. When a friend in the banking industry moved to Michigan, Smiley recognized that the demand for banking software was national, not regional. He opened an office in Michigan, then expanded with satellite operations in Salt Lake City, California, and Kansas. In August 1981, Systematics conducted a $35 million over-the-counter public offering to fund a new campus in west Little Rock.

Through the 1970s and 1980s, Systematics built its client base steadily, becoming the nation's leading supplier of data processing services for the commercial banking industry. The company developed expertise in core banking processing—the fundamental record-keeping and transaction-handling systems that sit at the heart of every bank's operations.

Think of core banking software as the operating system of a financial institution. It manages deposit accounts, processes loans, handles interest calculations, runs overnight batch processing, and maintains the ledger of record. Every other system a bank uses—online banking, mobile apps, ATMs, payment processing—connects back to the core. Whoever controls the core controls the bank's technology destiny.

This is where the switching cost moat begins to form. Replacing a core banking system is one of the most painful and risky undertakings in all of enterprise technology. The average migration takes three to five years, costs tens or hundreds of millions of dollars, and carries significant operational risk. Banks that have attempted core conversions compare the experience to performing a heart transplant on a patient who must remain conscious and working throughout the surgery. Every account, every transaction history, every integration with every other system must be migrated without error, without downtime, and without losing a single penny of customer funds. The consequence is that once a bank chooses a core banking platform, it tends to stay on that platform for decades. Systematics understood this dynamic early and built its entire business around it.

In 1988, after twenty years at the helm, Smiley stepped aside. Jack Stephens personally recruited John Steuri, an IBM sales and marketing executive, to replace him as CEO. Steuri's appointment signaled ambition: as one industry analyst noted, he brought "a mindset that 'We can be a billion-dollar company.'" Under Steuri, Systematics was generating $32 million in profits on $255 million in revenue by 1988, and employed over five thousand people.

Then, on March 2, 1990, ALLTEL Corporation—a telecommunications company based in Little Rock—acquired Systematics in a stock swap worth $528 million. The subsidiary was renamed ALLTEL Information Services. The acquisition gave Systematics access to greater resources and a broader distribution network, but the core business model remained the same: build banking software, embed it deeply into client operations, and collect recurring revenue for years and decades to come.

Under ALLTEL's ownership, the division expanded into mortgage servicing systems, becoming the leading mortgage loan servicing platform in the nation, processing approximately forty-six percent of all U.S. residential mortgage loans through relationships with seventeen of the top twenty-five mortgage originators. The dot-com era brought new challenges and opportunities—banks were scrambling to build online banking capabilities, and ALLTEL Information Services was there to help them do it, layering digital channels on top of the core processing systems that Systematics had built decades earlier.

Then, in 2003, something unexpected happened. Fidelity National Financial—at the time the nation's largest title insurance company—acquired ALLTEL's information services division for approximately $1.05 billion and renamed it Fidelity National Information Services. The question that every industry observer asked was obvious: Why would a title insurance company want a fintech business?

The answer lay with one man: William P. Foley II, the chairman and CEO of Fidelity National Financial. Foley was a former West Point graduate and corporate attorney who had built FNF into a title insurance powerhouse through relentless acquisition—over a hundred deals during his tenure. He was, by temperament and training, a dealmaker who saw the world as a series of transactions waiting to be structured.

Foley understood, perhaps better than anyone in the industry, the economics of transaction processing. Title insurance is, at its core, a data and processing business—every real estate transaction requires a title search, document preparation, and closing services. Foley saw the ALLTEL information services division not as a random diversification but as a natural extension of a thesis he had been pursuing for years: recurring revenue businesses built on transaction processing were the most durable economic engines in financial services.

The acquisition brought FNF into new territory—mortgage servicing, retail banking operations, commercial lending, online banking, wholesale banking, and, crucially, an international business. According to management at the time, the addition "accelerates our ongoing evolution into a fully diversified provider of products, services and solutions to the real estate and financial services industries." The recurring revenue streams from banking software were, unlike title insurance premiums, not tied to the cyclical ups and downs of the real estate market. Foley was hedging his bets, and the hedge would prove to be one of the most consequential strategic decisions in fintech history.

For investors watching this unfold, the acquisition signaled something important: the ALLTEL banking software division was not just a technology asset—it was a toll booth. Every transaction that flowed through its systems generated a fee. Every bank that signed a long-term processing contract became a captive revenue stream. And the switching costs meant that once a client was on the platform, the probability of them leaving was vanishingly small. Foley had found a business where the laws of gravity worked in his favor, and he was about to put it into overdrive.

III. The Roll-Up Playbook: Building Through Acquisitions (2003-2009)

The period between 2003 and 2009 was when FIS transformed from a significant regional player into a global financial technology juggernaut, and it did so through a playbook that would make any private equity dealmaker nod approvingly: acquire, integrate, extract synergies, repeat.

The first major move came before FIS even became a standalone public company. In September 2005, Fidelity National Financial announced that its majority-owned subsidiary FIS would merge with Certegy Inc. in a stock-for-stock transaction valued at approximately $3.8 billion. Certegy was a card and check services company spun off from Equifax in 2001. The deal closed on February 1, 2006, and the combined entity began trading on the New York Stock Exchange under the ticker symbol FIS—the same symbol the company carries to this day. Each outstanding share of FIS common stock was converted into 0.6396 shares of Certegy common stock, and the merged company took the FIS name.

The Certegy combination was strategic on multiple levels. It brought FIS significant capabilities in card issuer services, check guarantee services, and payment processing—complementing the core banking software that had been the company's foundation.

But perhaps more importantly, the deal established FIS as a publicly traded, independent entity with the scale and financial firepower to pursue larger acquisitions. The Certegy merger was, in effect, FIS's IPO—a reverse merger that gave the company a public currency (stock) with which to fund future deals. William Foley became Chairman and CEO of the new public FIS, and the company had a clear mandate: grow through acquisition and become the dominant technology provider to the financial services industry. The hunting license had been issued.

The next move came just eighteen months later. In September 2007, FIS completed the acquisition of eFunds Corporation for approximately $1.8 billion in cash, paying $36.50 per share. eFunds was a specialist in electronic funds transfer, ATM processing, and debit card processing—areas where FIS had limited presence. The acquisition added critical scale to FIS's EFT and debit operations and brought significant new capabilities in prepaid gift card services and risk management. Management targeted at least $65 million in annual expense savings from the integration by the end of 2009. The timing was notable: the deal closed in September 2007, just as the first tremors of the financial crisis were beginning to shake the banking industry.

The eFunds acquisition reflected a deliberate strategic pattern. Each deal was designed to fill a specific gap in FIS's product portfolio while adding transaction volume to the company's processing infrastructure.

In technology businesses with high fixed costs and low marginal costs, volume is everything. Each additional transaction processed costs almost nothing at the margin but generates incremental revenue. FIS was building a flywheel: more products attracted more clients, more clients generated more transaction volume, more volume spread fixed costs across a larger base, better economics attracted more clients. It was a virtuous cycle that became increasingly difficult for competitors to match.

The pattern was reminiscent of what John Malone did in cable television, what Danaher did in industrial instruments, or what Constellation Software does today in vertical-market software: use the cash flows from existing operations to fund acquisitions that add customers and capabilities, integrate aggressively, and repeat. The key insight in all of these roll-up strategies is that the acquirer's existing operations make each new acquisition more valuable than it would be as a standalone business—because the fixed costs can be shared and the customer relationships can be cross-sold.

Then came the financial crisis of 2008-2009—and with it, the most transformative acquisition in FIS's history to that point. While banks across America were failing, FIS was hunting. On April 1, 2009—at the absolute nadir of the financial crisis—FIS announced the acquisition of Metavante Technologies for $2.94 billion in an all-stock transaction. Each Metavante shareholder received 1.35 shares of FIS common stock, representing a twenty-four percent premium over Metavante's closing price. The deal closed on October 1, 2009.

The timing was audacious. Most companies were hunkering down in early 2009, conserving cash and hoping to survive. Lehman Brothers had collapsed six months earlier. Bear Stearns was gone. AIG had been bailed out. The S&P 500 was down more than fifty percent from its 2007 peak. Against this backdrop of existential fear, FIS was doing the opposite—making a multi-billion-dollar bet that the banking industry would recover and that a combined FIS-Metavante would be uniquely positioned to serve it when it did.

The combined company had a pro forma enterprise value of approximately $10 billion and revenues exceeding $5 billion. FIS had been a $3.4 billion revenue company in 2008; Metavante brought $1.7 billion more. Management projected $260 million in annual cost synergies from the combination.

Metavante was, in many ways, the perfect complement. Based in Milwaukee, Wisconsin, it was a major provider of banking technology and payment processing services, with particular strength in serving mid-tier and regional banks. The combination created a company with unmatched breadth across core banking, payment processing, electronic funds transfer, card issuing, and digital banking. After the Metavante integration, FIS served financial institutions of virtually every size, from the smallest community banks to some of the largest global institutions. Frank Martire, who had been Metavante's CEO since 2003—a forty-year fintech veteran who had previously spent a decade at Fiserv and earlier led Citicorp Information Resources—became president and CEO of FIS following the merger. Under his leadership, FIS entered the Fortune 500, and industry publications began referring to it as the largest technology provider to the global financial industry.

But the financial crisis also created a natural laboratory for testing FIS's business model. When banks are failing and loan losses are mounting, is a technology vendor safe? The answer turned out to be yes—emphatically. Banks that were struggling could not afford to rip out their core technology platforms. In fact, the crisis made them more dependent on their technology providers, not less. Banks that survived needed to cut costs, automate processes, and improve efficiency—all of which required more technology, not less. And the banks that were acquired by stronger institutions needed to be migrated onto the acquiring bank's platform, generating yet more implementation revenue and transaction volume for the technology providers.

There was also a darker, more pragmatic reason the business held up: FIS processed transactions regardless of whether those transactions were deposits or withdrawals, loan originations or defaults, payments made or payments missed. The company was compensated for processing volume, and volume continued whether the economy was booming or collapsing. FIS had stumbled onto one of the most recession-resilient business models in technology: a toll booth on financial transactions that collected its fee regardless of which direction the traffic was flowing.

By the end of 2009, FIS had revenue of over $5 billion. By 2011, that figure had grown to $5.7 billion—compounding at roughly twenty percent per year. Gary Norcross, who had joined Systematics as an entry-level programmer in 1988 after graduating from the University of Arkansas's Walton College, had risen through the ranks to become one of the key executives driving the integration strategy. His trajectory—from systems engineer to manager to senior vice president to president of the Integrated Financial Solutions division—was a living embodiment of the institutional knowledge that made FIS's switching cost moat so formidable. Norcross understood the software from the ground up because he had built it from the ground up. He would be named president and chief operating officer in 2012 and president and CEO in 2015.

The roll-up playbook had worked. But it had also set a dangerous precedent: FIS had learned that the fastest path to growth was through acquisition. That lesson would eventually lead the company to its most ambitious deal—and its most catastrophic mistake.

IV. The SunGard Acquisition: Expanding the Empire (2015)

By 2015, FIS was a roughly six-billion-dollar revenue company with dominant market share in core banking and payment processing for financial institutions. Gary Norcross was now CEO, and the company's strategic challenge was clear: where would the next leg of growth come from? The core banking market was mature, and FIS already held the largest share. Organic growth was steady but unspectacular—mid-single digits at best. To move the needle, FIS needed to enter entirely new markets.

The answer came on August 12, 2015, when FIS announced it would acquire SunGard Data Systems for $9.1 billion in enterprise value. The deal would transform FIS from a banking technology company into a diversified financial technology platform spanning retail banking, capital markets, asset management, and treasury operations.

SunGard had a storied history of its own. The company was formed in 1983 as a spin-off of the computer services division of Sun Oil Company. The name—originally an acronym for Sun Guaranteed Access to Recovered Data—reflected its origins in disaster recovery services. Under CEO Cristóbal Conde, a Yale-educated physicist who had co-founded Devon Systems International (a financial technology firm acquired by SunGard in 1987), the company evolved into one of the world's leading providers of capital markets technology. By the time of the FIS deal, SunGard provided software applications for trading, risk management, transaction processing, and accounting across capital markets globally. Its asset management systems maintained the books of record for banks, mutual funds, pension plans, and insurance companies.

SunGard had been taken private in August 2005 in an $11.3 billion leveraged buyout by a consortium of seven private equity firms—Silver Lake Partners, Bain Capital, Blackstone Group, Goldman Sachs, KKR, Providence Equity Partners, and TPG Capital. It was one of the largest leveraged buyouts in history at the time.

A decade later, the private equity owners were ready to exit. The typical PE holding period is five to seven years; at ten years, SunGard was already long in the tooth. An IPO was considered but the PE consortium ultimately preferred a clean sale. FIS was the logical buyer—it had the strategic rationale, the balance sheet capacity, and the appetite for transformative deals.

The deal structure reflected the scale of the ambition: FIS paid $2.3 billion in cash, issued $2.8 billion of FIS shares, and assumed SunGard's remaining debt. The transaction closed on November 30, 2015, and the combined company had annual revenues exceeding $9.3 billion and more than 55,000 employees. FIS's existing debt, combined with the assumption of SunGard's obligations, created a significant but manageable leverage profile that would take years to work down.

What made SunGard transformative was what it brought to FIS's portfolio. Before the acquisition, FIS was overwhelmingly focused on retail banking—core processing, payment systems, and digital banking for traditional financial institutions. SunGard opened entirely new markets: asset managers, traders, custodians, treasurers, third-party administrators, and clearing agents.

The capital markets technology business was structurally different from retail banking software. It was higher-margin, with significant intellectual property embedded in complex risk models and trading algorithms. The client base was different too—hedge funds, asset managers, and broker-dealers rather than community banks and regional lenders. And the competitive dynamics were different: capital markets technology was fragmented across dozens of specialized vendors, giving FIS the opportunity to cross-sell and consolidate.

To use a simple analogy: if the banking business was like selling operating systems to office workers, the capital markets business was like selling specialized engineering software to aerospace companies. The customers were more demanding, the products more complex, and the margins higher.

The integration was not without challenges. SunGard itself was an aggregation of dozens of acquisitions made over three decades—Conde had acquired twenty-seven companies between 1986 and 1994 alone. The resulting technology portfolio was sprawling and, in some cases, overlapping. FIS had to rationalize product lines, merge data centers, and align sales organizations across two very different corporate cultures. The retail banking side of FIS was deliberate, relationship-driven, and oriented around long-term contracts. The capital markets side was faster-moving, deal-oriented, and more sensitive to technology differentiation.

Gary Norcross tackled the integration methodically, applying the same playbook FIS had used with Metavante and eFunds: centralize corporate functions, consolidate data centers, rationalize overlapping products, and extract cost synergies while preserving revenue momentum. The strategy largely worked. By 2017, FIS reported that the integration was substantially complete and that the SunGard acquisition had delivered the expected synergies.

But the SunGard deal also changed FIS's character in a subtle and important way. Before 2015, FIS was a banking technology company that happened to do some payment processing. After SunGard, it was a financial technology conglomerate with three distinct businesses—Banking Solutions, Merchant Solutions (still relatively small), and Capital Market Solutions—serving very different client bases with very different needs. The complexity had increased dramatically, and managing that complexity would require a level of executive bandwidth that would soon be tested to its limits.

The Capital Market Solutions segment would prove to be a durable and valuable addition. As of 2025, the segment generated $3.2 billion in revenue with an adjusted EBITDA margin of 51.8 percent—the highest-margin business in FIS's portfolio and a reliable engine of profitable growth. The segment benefited from many of the same dynamics that made the banking business attractive: deep integration, high switching costs, and mission-critical functionality. If core banking software is the operating system of a bank, capital markets technology is the operating system of a trading desk—and swapping it out is equally unthinkable.

For investors, SunGard expanded FIS's total addressable market significantly while maintaining the core characteristics that made the business attractive: recurring revenue, high retention, and structural barriers to competition. But it also planted the seeds of a dangerous conviction: that FIS could successfully integrate any acquisition, no matter how large or complex. That conviction would be tested—and found wanting—in the next chapter.

V. The Worldpay Saga: Triumph and Retreat (2019-2024)

The year 2019 witnessed something unprecedented in the payments industry: three mega-deals announced within months of each other, each valued at over twenty billion dollars. In January, Fiserv announced the acquisition of First Data for $22 billion. In March, FIS announced its bid for Worldpay. In May, Global Payments announced the acquisition of TSYS for $21.5 billion. The payments industry, which had spent decades fragmenting into specialized niches, was suddenly consolidating at a dizzying pace.

The logic was not hard to understand. The rise of fintech startups like Stripe, Square, and Adyen was putting pressure on incumbents by offering faster, cheaper, and more developer-friendly payment processing. Stripe, in particular, had made accepting payments online as easy as adding a few lines of code—a stark contrast to the weeks or months it took to integrate with legacy payment processors.

The traditional players—large, complex organizations with decades of accumulated technology and client relationships—believed that scale was their best defense. Bigger companies could invest more in technology, spread fixed costs across more transactions, and offer clients a broader suite of services. It was a classic case of industrial logic being applied to a rapidly changing market, and whether it would work was very much an open question.

FIS's answer to this challenge was Worldpay—a company with its own tangled history. Worldpay had originated as the payments division of the Royal Bank of Scotland, was spun off and rebranded, taken private by Advent International and Bain Capital in 2010, brought public on the London Stock Exchange in 2015, and then merged with Vantiv—a U.S. payment processor that had itself been carved out of Fifth Third Bancorp—in January 2018. The Vantiv-Worldpay combination created the world's largest merchant acquirer by transaction count, processing payments for merchants across forty countries. It was, by any measure, one of the most complex corporate genealogies in financial services.

On March 18, 2019, FIS announced it would acquire this newly combined Worldpay entity for approximately $43 billion in enterprise value—the largest fintech deal in history. The equity value was roughly $35 billion, with Worldpay shareholders receiving 0.9287 FIS shares plus $11 in cash per share, a premium of about fourteen percent. Post-close, FIS shareholders would own approximately fifty-three percent of the combined company and Worldpay shareholders would own forty-seven percent. The deal closed on July 31, 2019.

The scale of the combined entity was breathtaking. Worldpay processed over forty billion transactions annually, supporting more than 300 payment types across 120 currencies. Together with FIS's existing operations, the merged company became the largest processing and payments company in the world, with over $12 billion in pro forma revenue and three segments: Banking Solutions, Merchant Solutions (Worldpay), and Capital Market Solutions.

Gary Norcross remained as chairman, president, and CEO. Charles Drucker, the former Worldpay CEO, became executive vice chairman. Stephanie Ferris, who had served as Worldpay's CFO, was named enterprise-wide chief operating officer. The leadership structure was designed to signal continuity and collaboration, but the reality of integrating two massive organizations with deeply different cultures and technology stacks was about to prove far more difficult than the press releases suggested.

The problems began almost immediately, though they took time to become visible. The core strategic premise of the deal—that combining FIS's banking relationships with Worldpay's merchant processing capabilities would unlock significant cross-selling opportunities—proved far harder to execute than the PowerPoint slides suggested. In theory, FIS could offer its bank clients a complete solution: core banking, digital channels, and now merchant acquiring all from a single provider. In practice, the sales cycles were different, the buyer personas were different, and the integration between banking and merchant systems was more complex than anticipated. FIS publicly claimed that revenue synergies were "exceeding internal targets," a claim that would later become the basis for a shareholder lawsuit. But the competitive landscape was moving faster than the integration could keep up.

The fundamental strategic miscalculation was this: FIS treated merchant acquiring as if it were another form of infrastructure with high switching costs—another toll booth, like core banking. But merchant acquiring is structurally different. Merchants have more payment processor options than banks have core system options. The barriers to switching are lower. And the pace of innovation is faster, driven by a generation of well-funded startups with no legacy technology constraints.

Then COVID-19 hit. The pandemic accelerated the shift to e-commerce and digital payments, which should have been a tailwind for Worldpay. But venture-backed fintechs seized the moment far more effectively. Over the three years following the FIS acquisition, Worldpay's merchant transaction volumes grew twenty-eight percent—a reasonable number in isolation, but catastrophically insufficient in context. During the same period, Stripe's volumes grew 3.8 times. Adyen's volumes grew 3.2 times. The legacy payments business was being lapped by companies that had built their technology from scratch on modern, cloud-native architectures.

The problem was partly technical and partly structural. Worldpay itself had been built through years of acquisitions, accumulating disparate systems, technical debt, and sprawling infrastructure. Maintaining basic interoperability consumed enormous resources, leaving little capacity for innovation. Meanwhile, Adyen operated on a single integrated platform built from the ground up—no legacy systems, no integration layers, no compromises. The difference in agility was stark and growing wider.

The balance sheet constraints made everything worse. The massive debt taken on to finance the Worldpay acquisition limited FIS's ability to invest in modernizing the merchant business. It was a vicious cycle: the company needed to invest heavily to compete with well-funded startups, but the debt from the acquisition that was supposed to create competitive advantage instead constrained the very investments needed to realize that advantage.

Management later acknowledged getting "into a tough spot with our balance sheet," lacking the capital needed to invest in and grow the merchant business at the pace the market demanded.

The stock price told the story of destruction with brutal clarity. FIS shares peaked at approximately $150 in mid-2021, buoyed by the post-pandemic digital payments enthusiasm. Then the unraveling began. The stock fell to $104 by mid-2022 as growth disappointed. It cratered to about $66 by February 2023 as the magnitude of the Worldpay challenges became undeniable. At its lowest point in mid-2023, the stock traded in the low $50s, representing a roughly sixty-five percent decline from peak to trough. Tens of billions of dollars in shareholder value had evaporated.

Two activist hedge funds—D.E. Shaw and Jana Partners—took substantial positions in FIS and pressed for change with the kind of public urgency that makes boards of directors lose sleep. The pressure was intense and direct: explore strategic alternatives, consider divestitures, and overhaul leadership. Behind closed doors, the conversations were reported to be even more pointed.

Under this pressure, the leadership transition that had been planned for January 2023 was accelerated. Stephanie Ferris replaced Gary Norcross as CEO on December 16, 2022—two weeks ahead of schedule—and Norcross departed the board entirely the same day. Jeffrey Goldstein became independent chairman. Ferris's appointment was historic: she became the first woman to lead FIS in its fifty-plus-year history. Her background was uniquely suited to the moment. She had started her career in 1995 as an entry-level accountant at PricewaterhouseCoopers, risen to become CFO of the payments processing division at Fifth Third Bancorp (which became Vantiv, which became Worldpay), and joined FIS through the 2019 acquisition. She knew the Worldpay business intimately—its strengths, its weaknesses, and its limitations. That knowledge would prove essential in the decisions ahead.

The reckoning came on February 13, 2023, when FIS announced a $17.6 billion goodwill impairment on the Merchant Solutions reporting unit—the largest single writedown in the company's history. To put that number in context, $17.6 billion is larger than the entire market capitalization of Jack Henry, FIS's closest competitor in core banking. It represented an acknowledgment that roughly half the value FIS had ascribed to the Worldpay acquisition had evaporated.

At the same time, the company announced plans to spin off the merchant business as a separate public company. Later in 2023, an additional $6.8 billion impairment was recorded, bringing total goodwill impairment charges to approximately $24.4 billion—more than half of the $43 billion originally paid for Worldpay.

Rather than pursue a full spin-off, FIS ultimately pivoted to a partial sale. In July 2023, GTCR, a Chicago-based private equity firm, agreed to acquire a fifty-five percent majority stake in Worldpay at a valuation of $18.5 billion—less than half of what FIS had paid four years earlier.

The valuation compression was staggering. FIS had paid $43 billion; the business was now valued at $18.5 billion. Roughly $24.5 billion in enterprise value—the equivalent of the GDP of a small country—had vanished.

FIS received approximately $11.7 billion in upfront net proceeds and retained a forty-five percent minority stake. The transaction closed on February 1, 2024.

The Worldpay saga ranks among the most dramatic value-destruction events in financial technology history. FIS paid $43 billion for a business whose majority stake it sold for a valuation of $18.5 billion just four years later.

In December 2025, FIS agreed to pay $210 million to settle a class-action shareholder lawsuit alleging that executives had made materially misleading statements about the integration's success and revenue synergies.

But the story did not end with the GTCR sale. In April 2025, FIS announced a complex three-way transaction with Global Payments and GTCR. Global Payments would acquire one hundred percent of Worldpay for approximately $24.25 billion. FIS would sell its remaining forty-five percent stake for $6.6 billion. Simultaneously, FIS would acquire Global Payments' Issuer Solutions business—the former TSYS—for $13.5 billion in enterprise value. Both transactions closed in January 2026, completing FIS's exit from the merchant payments business and pivoting the company toward a new strategic identity as the dominant bank technology and issuer processing platform.

The Worldpay experience carries lessons that extend far beyond FIS. Mega-mergers in technology are extraordinarily difficult because the competitive landscape moves faster than integration timelines allow. A deal that makes strategic sense on paper can destroy value if the combined organization cannot execute faster than the market evolves. And the sunk cost fallacy—the tendency to hold onto a struggling acquisition because of how much was paid for it—can delay the inevitable reckoning by years, compounding the damage. To her credit, Stephanie Ferris made the difficult decision to cut losses and refocus the company rather than continuing to pour resources into a battle FIS was losing.

VI. Core Business Deep Dive: The Infrastructure Monopoly

To understand why FIS endures despite the Worldpay debacle, you need to understand what it actually does—and why it is so extraordinarily difficult to replace.

Imagine a mid-sized bank with $10 billion in assets, a million customers, and branches in three states. Every day, that bank processes hundreds of thousands of transactions: deposits, withdrawals, loan payments, wire transfers, ACH transactions, ATM withdrawals, mobile check deposits, bill payments, and account transfers. Each transaction must be recorded accurately, reflected in the customer's balance in real time, reconciled with corresponding entries at other institutions, and reported to regulators. Behind the scenes, interest must be calculated on every account, fees must be assessed, compliance rules must be checked, and risk limits must be monitored.

The software that handles all of this is the core banking platform, and for a huge number of banks around the world, that platform runs on FIS technology. Think of it as the central nervous system of the bank. Every other system—the mobile app, the online banking portal, the lending system, the credit card platform, the fraud detection engine—talks to the core. If the core goes down, the bank goes down.

To make this concrete, consider what happens every night at a typical FIS-serviced bank. After the branches close and the mobile app goes quiet, the core banking system runs what is called "overnight batch processing." This is the financial equivalent of closing the books at the end of each business day. The system calculates interest on every deposit account and every loan. It processes every ACH payment that was queued during the day—payroll deposits, bill payments, mortgage debits, Social Security disbursements. It updates account balances, generates regulatory reports, runs anti-money-laundering checks, and prepares the data that will be available when customers check their accounts the next morning. For a large bank, this overnight process can involve hundreds of millions of individual calculations, and every single one must be accurate to the penny. This is what FIS's core systems do, night after night, year after year, without fail. The sheer mundanity of the task obscures its criticality—and its difficulty.

FIS currently operates in two primary segments following its post-Worldpay restructuring, plus a third segment that now includes the recently acquired Issuer Solutions business.

Banking Solutions is the largest and most important segment, generating $7.3 billion in revenue in 2025 with an adjusted EBITDA margin of 43.4 percent. This segment is organized into two divisions: the Banking Division, which provides core banking technology, digital banking, and wealth management solutions; and the Payments Division, which handles payment processing for financial institutions.

The Banking Solutions segment serves institutions ranging from small community banks with a handful of branches to some of the largest banks in the world. The recurring revenue characteristics are exceptional—roughly eighty percent of total segment revenue is recurring, generated by long-term processing contracts that typically run five to ten years and renew at high rates. Once signed, these contracts rarely terminate early. The revenue is as predictable as anything in technology.

Capital Market Solutions generated $3.2 billion in revenue in 2025 with an adjusted EBITDA margin of 51.8 percent—the highest in the company. This segment, built largely through the SunGard acquisition, provides technology for trading, risk management, compliance, and treasury operations to investment firms, banks, and capital markets participants.

The clients include hedge funds, asset managers, broker-dealers, and corporate treasurers. The technology is deeply specialized, often custom-configured for each client, and embedded in mission-critical workflows that are extraordinarily expensive to replace. A hedge fund that has spent two years configuring its risk management system around FIS's technology is not going to switch to a competitor because it offers a marginally better feature. The cost of migration—in time, risk, and lost productivity—far exceeds any potential savings.

Corporate and Other is a smaller segment that includes corporate overhead, intercompany eliminations, and, beginning in January 2026, the newly acquired FIS Total Issuing Solutions business. This issuer processing platform—formerly Global Payments' TSYS business—processes over forty billion transactions annually for more than 150 financial institutions in 75 countries. It is expected to generate $500 million in incremental adjusted free cash flow in 2026 and $700 million by 2028.

The competitive advantages in this business are structural and deeply entrenched.

The first and most important is switching costs. Replacing a core banking system is not like switching from one CRM to another. It involves migrating millions of customer records, reconfiguring thousands of integrations, retraining hundreds of employees, and running parallel systems for months while the migration is validated. The risk of data loss, transaction errors, or system outages during a conversion is not theoretical—it has happened, and the consequences have been devastating for the banks involved.

Regulators pay close attention to core conversions, adding another layer of complexity and caution. The OCC, FDIC, and Federal Reserve all require banks to demonstrate that core system changes will not compromise the safety and soundness of the institution. This regulatory overlay acts as an additional moat—even a bank that wants to switch must convince its regulator that the migration plan is sound. The result is that banks almost never switch core providers voluntarily. Industry estimates suggest that the average core banking contract lasts fifteen to twenty years, and some relationships stretch back decades.

The second advantage is scale economics. Developing and maintaining core banking software requires enormous upfront investment. FIS has spent billions over decades building, testing, and certifying its technology for use in dozens of countries with different regulatory requirements, currency systems, and banking conventions.

A new entrant attempting to replicate this capability from scratch would need to invest for years before winning its first client. And because FIS spreads its development costs across thousands of clients, it can invest more in its platform than any individual bank could invest in building its own, creating a perpetual advantage. The math is relentless: FIS spends roughly $1 billion annually on R&D, shared across more than twenty thousand clients. No startup can match that investment on a per-client basis.

The third advantage is network effects, though they are subtler than in consumer technology. The more banks that use FIS's platform, the more valuable the network of connections between those banks becomes. Payment processing, in particular, benefits from network density—transactions between FIS-serviced banks can be processed more efficiently, settled faster, and monitored more comprehensively than transactions that cross network boundaries. FIS's NYCE network, for example, is a leading national electronic funds transfer network that connects FIS-serviced institutions.

In early 2026, FIS launched an industry-first "agentic commerce" offering in partnership with Visa and Mastercard, enabling banks to participate in AI-mediated commerce at scale. The product allows AI agents to safely transmit transactions over card networks, with features including Know Your Agent data integration, authorization, fraud detection, and customer services for AI-initiated transactions. The offering is expected to be available to all FIS issuing bank clients by the end of the first quarter of 2026. This move signals FIS's intent to position itself not just as legacy infrastructure but as the platform through which next-generation payment technologies reach the banking system.

For those trying to assess the durability of FIS's franchise, the question is simple: what would it take for a bank to leave? The answer—years of effort, hundreds of millions of dollars, and significant operational risk—is the moat. It is not glamorous, but it is deep, wide, and filled with regulatory alligators.

VII. Business Model & Financial Analysis

There is a common myth about FIS—and companies like it—that deserves examination. The consensus narrative holds that FIS is simply a "legacy technology company" that survives on inertia and switching costs rather than product quality. The reality is more nuanced. FIS has invested billions of dollars in modernizing its platforms, including cloud-enabled core banking solutions, real-time payment capabilities, and API-based open banking integrations. The company is not standing still technologically. What is true is that the pace of modernization is constrained by the conservative nature of its client base: banks move slowly because regulators demand stability, and regulators demand stability because the consequences of technology failure in banking are catastrophic. The "legacy" label says as much about the banking industry's risk tolerance as it does about FIS's technology.

The financial profile of FIS tells a story of a company that generates enormous amounts of recurring revenue and cash flow, offset by the complexity and costs of managing a global technology platform and the financial hangovers from its acquisition history.

At the highest level, FIS reported consolidated revenue of $10.7 billion for full-year 2025, representing five percent growth on a GAAP basis and six percent on an adjusted basis. Recurring revenue totaled $8.5 billion—approximately eighty percent of total segment revenue—growing six percent year over year. This recurring revenue base is the foundation of FIS's investment case. Unlike project-based or transaction-dependent revenue, recurring revenue from long-term contracts provides exceptional visibility into future cash flows.

The company's revenue model blends several streams. Processing fees represent the largest component—FIS earns a fee for every transaction it processes, whether that is a core banking transaction, a payment, a trade settlement, or an issuer authorization. Software licensing generates lumpier but higher-margin revenue, particularly in the Capital Market Solutions segment where perpetual licenses and periodic renewals can create significant one-time payments. Professional services—implementation, customization, and consulting—generate revenue during new client onboarding and system upgrades.

Profitability varies significantly across segments. Capital Market Solutions is the margin leader at 51.8 percent adjusted EBITDA, benefiting from the intellectual property intensity of its technology and the willingness of capital markets clients to pay premium prices for mission-critical software.

Banking Solutions runs at a 43.4 percent adjusted EBITDA margin—still strong but pressured by the mix shift toward lower-margin professional services and the dilutive impact of recent tuck-in acquisitions. The consolidated adjusted EBITDA margin was 40.6 percent in 2025, down 28 basis points from the prior year. The slight margin contraction is worth watching—it could be a temporary blip from acquisition integration, or it could signal emerging competitive pressure on pricing.

The gap between GAAP and adjusted earnings is worth examining carefully. GAAP diluted earnings per share from continuing operations were just $0.73, while adjusted EPS was $5.75—a massive difference. The $5.02-per-share gap reflects the impact of acquisition-related amortization, restructuring charges, and the accounting complexities of the Worldpay divestiture.

Adjusted net earnings were $3 billion, compared to GAAP net earnings of $382 million. Investors need to understand both numbers: the GAAP figure reflects the real economic costs of FIS's acquisition history (including the ongoing amortization of billions of dollars in intangible assets), while the adjusted figure provides a cleaner view of the underlying business's earning power. Neither number is "right" in isolation, and investors who look only at adjusted earnings risk underestimating the true cost of the acquisition strategy that built FIS.

Cash flow generation is a particular strength and arguably the most compelling aspect of the FIS investment thesis. Free cash flow reached $1.6 billion in 2025, up nineteen percent, with adjusted free cash flow of $2.2 billion. The cash conversion is strong because the business has relatively modest capital expenditure requirements relative to its revenue—the software is already built, and incremental investment is largely in maintenance and enhancement rather than greenfield development.

The company returned $2.1 billion to shareholders through a combination of $1.3 billion in share repurchases and $847 million in dividends. In January 2026, the board approved a ten percent dividend increase to $0.44 per share, signaling confidence in the durability of cash flows even as the company absorbs a major acquisition.

The balance sheet carries the scars of the acquisition era. As of December 31, 2025, FIS had $13.1 billion in total debt outstanding—a significant burden reflecting the cumulative borrowings from years of deal-making. With $571 million in cash, the net debt position was approximately $12.5 billion. Management has targeted a gross leverage ratio of 2.8 times and has temporarily paused share repurchases and tuck-in M&A to prioritize deleveraging following the January 2026 acquisition of the Total Issuing Solutions business.

To understand the revenue trajectory over time, consider the arc. In 2003, when Foley acquired the ALLTEL division, revenue was roughly $1 billion. By 2009, after the Metavante merger, it exceeded $5 billion. The SunGard deal pushed it past $9 billion by 2016. The Worldpay acquisition briefly inflated revenue to over $12 billion before the divestiture brought it back to approximately $10 billion. Now, with the Total Issuing Solutions acquisition, revenue is projected to reach nearly $14 billion in 2026. The trajectory has not been a smooth upward line—it has been a series of step-function increases driven by acquisitions, interrupted by a dramatic step-down when Worldpay was divested. For investors, the question is whether the underlying organic growth engine—currently running at five to six percent—is strong enough to justify the company's valuation absent the acquisition-driven step changes.

Comparing FIS to its primary competitors provides useful context. Fiserv, now including the former First Data merchant business, is the closest comparable with revenue of approximately $20 billion. Fiserv has executed its First Data integration more successfully than FIS managed Worldpay, maintaining revenue momentum in its merchant business while FIS was forced to divest. The contrast is instructive: Fiserv's CEO, Frank Bisignano, was a hands-on operator who had run First Data before the merger and understood its business intimately. FIS was attempting to integrate a business—merchant acquiring—that its leadership team had less direct experience with. Jack Henry & Associates is a much smaller competitor focused on community and mid-tier banks, with revenue of roughly $2 billion. Jack Henry is often cited as having the best client satisfaction scores in the industry and has gained modest market share, but it lacks the scale to compete across FIS's full product range. Its stock has significantly outperformed FIS over the past five years, a testament to the market's preference for focused operators over conglomerates. Broadridge Financial Solutions operates in a complementary space focused on investor communications, securities processing, and proxy services, with roughly $6 billion in revenue.

One material accounting judgment worth flagging: the enormous gap between GAAP and adjusted earnings at FIS. The $5.02 difference between GAAP EPS ($0.73) and adjusted EPS ($5.75) in 2025 is driven primarily by amortization of acquisition-related intangible assets, stock-based compensation, and restructuring charges. While these adjustments are standard in the industry—Fiserv and other acquisitive tech companies make similar adjustments—the magnitude at FIS is unusually large, reflecting the cumulative impact of decades of deal-making. Investors should be aware that the "adjusted" numbers strip out real economic costs, and the GAAP numbers reflect the ongoing financial burden of FIS's acquisition history through amortization that will continue for years.

The 2026 outlook reflects the step-change impact of the Total Issuing Solutions acquisition. FIS projects adjusted revenue growth of 30 to 31 percent, reaching approximately $13.85 billion, though on a pro forma basis (assuming the acquisition had been in place for the full prior year), growth would be a more modest 5.1 to 5.7 percent. Adjusted EPS is expected to grow 8 to 10 percent to $6.22-$6.32 per share, and free cash flow is targeted at $2.05 to $2.15 billion.

The financial trajectory tells a story of a company that stumbled badly with the Worldpay acquisition, took its medicine, and is now rebuilding on a more focused foundation. The revenue is growing, margins are stable, cash flow is strong, and the balance sheet is being repaired. The question is whether the post-Worldpay FIS can sustain mid-single-digit organic growth while simultaneously integrating another major acquisition in Total Issuing Solutions. The company's track record on integrations is mixed at best.

VIII. Playbook: Lessons in Building Financial Infrastructure

The FIS story offers a masterclass in both the power and the peril of the roll-up strategy in enterprise technology.

Lesson One: Roll-ups work brilliantly when the targets share a common operating model. The acquisitions of Certegy, eFunds, and Metavante between 2006 and 2009 were textbook examples of strategic consolidation. Each target served a similar customer base (financial institutions), operated on a similar business model (recurring processing fees), and could be integrated onto a common operational platform. The synergies were real and achievable because the businesses were fundamentally similar. The SunGard acquisition stretched this model—capital markets technology is different enough from retail banking technology that the integration was harder—but still worked because the underlying economics (high switching costs, recurring revenue, mission-critical applications) were the same.

Lesson Two: Roll-ups fail when the acquirer moves into a fundamentally different business. The Worldpay acquisition was a roll-up too far. Merchant acquiring—the business of processing payments for retailers and e-commerce companies—operates on a completely different competitive dynamic than banking technology. Merchant clients are price-sensitive, switching costs are lower, and the competitive threat from venture-backed startups is real and accelerating. FIS applied its banking technology playbook—sign long-term contracts, embed deeply, and rely on switching costs—to a market where that playbook did not apply. The result was a slow-motion disaster.

Lesson Three: Infrastructure businesses must balance stability with innovation. FIS's core banking clients need above all else for their systems to be reliable. They will tolerate technology that is not cutting-edge as long as it never goes down. This creates a cultural bias toward conservatism that is appropriate for the core business but lethal in fast-moving markets like merchant payments. FIS tried to be both stable and innovative, cautious and aggressive, a utility and a growth company. The market punished the contradiction.

Lesson Four: Activist investors can be catalysts for necessary change. D.E. Shaw and Jana Partners forced FIS to confront the Worldpay disaster rather than continuing to manage around it. Without activist pressure, it is likely that FIS would have held onto the Worldpay business longer, hoping for a turnaround that was not coming, and the value destruction would have been even greater. Ferris's willingness to move quickly—divesting the majority stake within months of taking the CEO role—prevented a bad situation from becoming catastrophic.

Lesson Five: Mega-mergers in technology carry a fundamental timing risk. The problem with a deal that takes two to three years to integrate is that the competitive landscape can change dramatically during the integration period. FIS announced the Worldpay deal in March 2019. By the time the integration was substantially underway, COVID-19 had restructured the payments landscape, and Stripe, Adyen, and Square had seized the initiative. The deal was not wrong in its strategic logic—it was wrong in its timing relative to market evolution. This is an underappreciated risk in large technology acquisitions.

Lesson Six: Switching cost moats in B2B software are among the most durable competitive advantages in business. Despite all of FIS's strategic missteps, the core banking and capital markets businesses have remained stable and profitable throughout every twist and turn. Client retention is exceptionally high. Revenue grows steadily. Margins are strong. The reason is simple: whatever FIS does with its corporate strategy, its clients cannot afford to leave. The moat protects the franchise even when management stumbles. This is the closest thing in business to an unlosable asset, and it is why FIS remains a multi-billion-dollar enterprise despite the Worldpay write-off.

Lesson Seven: The difference between a good acquisition and a bad one often comes down to whether the acquirer is buying a business it genuinely understands. FIS's successful acquisitions—Certegy, eFunds, Metavante, SunGard—were all businesses that FIS's management team knew intimately. They served the same or adjacent clients, operated on similar technology stacks, and followed familiar competitive dynamics. Worldpay was different. Merchant acquiring is a consumer-facing, sales-driven, rapidly evolving business that requires a fundamentally different set of capabilities than building and maintaining mission-critical banking infrastructure. FIS's leadership, steeped in the culture of banking technology, struggled to compete in a market that rewarded speed and developer experience over stability and regulatory expertise.

The FIS playbook ultimately teaches that the same company can be both a cautionary tale and a durable franchise, depending on which part of the business you are examining. The core banking business is a fortress. The Worldpay adventure was a fiasco. The Total Issuing Solutions acquisition—which brings FIS back to its sweet spot of regulated, high-switching-cost infrastructure serving financial institutions—is a bet that FIS can return to its roots without repeating the mistakes of the Worldpay era. Early signs are encouraging. The business processes over forty billion transactions annually, its clients are banks and financial institutions rather than merchants, and the competitive dynamics are far more favorable. But execution risk remains, and the next two years of integration will be the ultimate test.

IX. Bear vs. Bull Case & Future Outlook

The Bull Case

The bull case for FIS rests on a simple but powerful premise: the company operates irreplaceable infrastructure with recurring revenues that grow regardless of macroeconomic conditions.

Start with the banking technology franchise. The global banking industry is in the early stages of a multi-decade digital transformation. Core banking systems that were designed for branch-based banking are being upgraded to support digital channels, real-time payments, open banking APIs, and embedded finance. Every one of these modernization projects requires FIS's participation because FIS operates the core systems being modernized. The company is not just selling technology into the digital transformation—it is the platform upon which the digital transformation is being built.

The Total Issuing Solutions acquisition, completed in January 2026, adds another layer of durable infrastructure. Issuer processing—the technology that enables banks to issue credit cards, debit cards, and prepaid cards—has the same characteristics that make core banking software attractive: high switching costs, long-term contracts, and mission-critical functionality. The business processes over forty billion transactions annually and is expected to generate $500 million in incremental free cash flow in its first year and $700 million by 2028.

Capital Market Solutions continues to perform well, growing revenue seven percent in the fourth quarter of 2025 with margins expanding to 51.8 percent. The segment benefits from structural tailwinds including increasing regulatory complexity, the growth of alternative investments, and the rising demand for real-time risk management and surveillance technology.

Management has demonstrated financial discipline under Stephanie Ferris. The company returned $2.1 billion to shareholders in 2025 while maintaining investment in the business, and the 2026 guidance implies continued momentum with pro forma revenue growth of 5 to 6 percent and EBITDA growth of 7 to 8 percent.

There is also an underappreciated tailwind from Banking-as-a-Service and embedded finance. As non-bank companies—retailers, technology platforms, gig economy companies—seek to offer financial products to their customers, they need banking infrastructure to do so. FIS is positioned to provide that infrastructure, enabling banks to become the regulated backbone behind fintech applications. Every time a fintech startup partners with a bank to offer checking accounts or issue debit cards, there is a reasonable chance that FIS's technology is somewhere in the stack. The fintech revolution is not displacing FIS—in many cases, it is creating more demand for the plumbing that FIS provides.

The Bear Case

The bear case centers on three interrelated concerns: legacy technology debt, fintech disruption, and integration risk.

FIS's core banking platforms, while deeply embedded and difficult to replace, are in many cases built on architectures that date back decades. The COBOL-based systems that process overnight batch transactions for thousands of banks are functional and reliable, but they are not the future. Cloud-native core banking providers like Thought Machine, Temenos on cloud, Mambu, and Finxact (acquired by Fiserv) offer modern alternatives that are easier to configure, faster to deploy, and cheaper to operate. Today, these competitors primarily serve greenfield opportunities—new digital banks, fintech startups, and international expansions. But over time, as migration tools improve and regulatory comfort with cloud-based cores increases, the threat to FIS's installed base could grow.

The $13.1 billion debt load—temporarily increased by the Total Issuing Solutions acquisition—limits financial flexibility. Management has paused share repurchases and tuck-in M&A to prioritize deleveraging, which means the company is entering a period of reduced strategic optionality at a time when the competitive landscape is evolving rapidly.

The integration of Total Issuing Solutions is not a trivial undertaking. The business was carved out of Global Payments and is being integrated into FIS's operations while simultaneously rebranding and reorganizing. FIS's track record on large integrations—mixed at best after the Worldpay experience—gives legitimate cause for concern. Management has projected $200 million in run-rate cost synergies from the acquisition, but achieving those synergies while maintaining service quality for clients that were just transferred from a different parent company is a non-trivial operational challenge.

The open banking regulatory movement also presents a nuanced threat. In Europe, the PSD2 directive has already required banks to open their data and payment initiation capabilities to third-party providers through standardized APIs. Similar initiatives are advancing in the United States, with the Consumer Financial Protection Bureau's proposed open banking rules. These regulations could, over time, reduce the barriers for new entrants to build on top of bank data without going through incumbent technology providers like FIS. If a fintech startup can access bank account data directly through standardized APIs, the value of FIS's proprietary integrations diminishes. This is a slow-moving but potentially significant structural shift.

Artificial intelligence presents both opportunity and risk. On the opportunity side, AI can improve fraud detection, automate customer service, and enhance the efficiency of transaction processing—all areas where FIS has products and capabilities. The agentic commerce initiative launched in early 2026 is an example of FIS leaning into this opportunity. On the risk side, AI tools are making it easier to build, test, and deploy financial software, potentially lowering the barriers to entry that have protected FIS's franchise. If AI dramatically reduces the cost and complexity of building core banking systems or payment processing platforms, the switching cost moat could narrow over time.

Frameworks for Analysis

Through the lens of Porter's Five Forces, FIS operates in a favorable industry structure. The threat of new entrants is low due to enormous barriers to entry (regulatory certification, development costs, client migration risk). Supplier power is moderate—FIS relies on cloud infrastructure providers and hardware vendors but has sufficient scale to negotiate favorable terms. Buyer power is low for individual clients because of switching costs, though the largest banks have more leverage. The threat of substitutes is the most significant force—cloud-native core banking providers represent a long-term substitute threat. Rivalry among existing competitors is moderate, characterized more by client retention than aggressive price competition.

Through Hamilton Helmer's 7 Powers framework, FIS possesses at least three forms of durable power.

Switching costs are the most obvious and most important—clients cannot leave without bearing enormous expense and risk. This is the single strongest source of FIS's competitive position and the primary reason the company has survived strategic missteps that would have destroyed a less entrenched business.

Scale economies are significant—FIS spreads its R&D and infrastructure costs across thousands of clients, creating a cost advantage that smaller competitors cannot match. The company invests over a billion dollars annually in technology development, an amount that no startup or mid-sized competitor can come close to replicating.

Process power is present in the institutional knowledge accumulated over decades of operating mission-critical banking systems—the expertise required to process trillions of dollars in transactions without error is not easily replicated. This institutional knowledge is embedded in thousands of employees who understand the byzantine complexities of bank regulation, payment clearing, and transaction settlement across dozens of countries.

FIS likely does not possess meaningful counter-positioning (its technology is not fundamentally different from competitors'), cornered resource (its talent, while experienced, is not uniquely irreplaceable), or branding power (FIS is virtually unknown outside the industry). Its network effects are real but weaker than those of pure network businesses like Visa or Mastercard.

Key Metrics to Watch

For investors tracking FIS's ongoing performance, two KPIs matter most:

Recurring revenue growth rate — This is the single most important indicator of the franchise's health. FIS's recurring revenue represents approximately eighty percent of total segment revenue and grows based on the combination of transaction volume growth, price escalators in existing contracts, and new client wins. A sustained deceleration in recurring revenue growth would signal competitive erosion or client attrition—the nightmare scenario for an infrastructure business built on switching costs. In 2025, this metric grew six percent, which management and investors viewed as healthy.

Adjusted EBITDA margin — Margin trends reveal whether FIS is successfully balancing growth investment with profitability. The consolidated margin of 40.6 percent in 2025 reflects the mix between higher-margin Capital Market Solutions and lower-margin Banking Solutions. Expanding margins would signal operating leverage and successful integration of Total Issuing Solutions, while contracting margins could indicate rising competitive pressure, integration costs, or the need to invest aggressively in technology modernization.

X. Power Analysis & Final Thoughts

What kind of company is FIS, really? Is it a technology company, a financial services company, or something else entirely?

The most accurate description might be that FIS is a regulated utility for the financial system that happens to deliver its services through software. Like a utility, it provides essential, non-discretionary services. Like a utility, it benefits from regulatory barriers that limit competition. Like a utility, its customers cannot easily switch to alternatives. And like a utility, its growth is steady but unspectacular, driven more by the underlying growth of the system it serves than by any particular product innovation.

This utility analogy explains both FIS's greatest strength and its greatest vulnerability. Utilities are stable, but they rarely trade at premium multiples. They are safe, but they are rarely exciting. And they are durable, but they are not immune to technological disruption—as the electric utility industry discovered with solar power and distributed generation. The question for FIS is whether cloud-native core banking is FIS's solar power moment, or whether it is more analogous to the many false disruption alarms that utilities have weathered over the decades.

Comparing FIS to other infrastructure plays is instructive. Visa and Mastercard are often cited as the gold standard of payment infrastructure businesses, and the comparison highlights both similarities and differences. Visa and Mastercard operate two-sided networks with powerful network effects—every merchant that accepts Visa makes the network more valuable to cardholders, and vice versa. FIS's network effects are weaker because its technology serves one side of the financial system (the institutions) rather than connecting two sides of a market. However, FIS's switching costs may actually be higher than Visa's or Mastercard's, because replacing a core banking system is far more complex and risky than switching payment networks.

The exchanges—NYSE, Nasdaq, CME Group—offer another comparison point. Like FIS, exchanges operate mission-critical infrastructure with high barriers to entry and strong network effects. But exchanges benefit from a more direct network effect (liquidity attracts liquidity) and a cleaner business model (transaction fees on a two-sided marketplace). FIS's business model is more complex, involving deep client relationships, extensive customization, and long-term service agreements.

The infrastructure provider's dilemma is that the very characteristics that make the business durable—stability, reliability, conservatism—are the same characteristics that make it vulnerable to disruption over long time horizons. FIS's clients do not want their core banking provider to be innovative. They want it to be boring and reliable. But a company that is boring and reliable eventually finds itself running technology that is a generation behind the frontier, and when a sufficiently compelling alternative emerges—one that is modern, cloud-native, and API-first—even the most entrenched incumbent can face existential pressure.

The leadership journey of the company is itself instructive. Walter Smiley, the founder, was a banker-turned-technologist who understood his customers because he had been one. John Steuri brought IBM's growth ambition. William Foley brought deal-making prowess and the vision to see banking technology as a toll booth business. Frank Martire brought operational discipline from a career spent in the trenches of financial technology. Gary Norcross brought deep institutional knowledge from building the software himself, but perhaps lacked the strategic discipline to know when to stop acquiring. Stephanie Ferris brought financial acumen, hard-won knowledge of the merchant payments business, and the willingness to make painful decisions quickly. Each leader shaped FIS's trajectory in ways that reflected their backgrounds and blind spots.

The FIS story, from Systematics in 1968 to the Total Issuing Solutions acquisition in 2026, is ultimately a story about the power and limits of infrastructure monopolies. The power is real: fifty-plus years of accumulated switching costs, regulatory barriers, and institutional knowledge have created a franchise that generates billions in recurring revenue and free cash flow. The limits are also real: the Worldpay disaster demonstrated that even the deepest moat cannot protect a company that ventures outside its circle of competence.

Stephanie Ferris appears to understand this distinction. Her strategic moves since taking the CEO role—divesting the Worldpay merchant business, refocusing on banking and capital markets, acquiring the complementary Total Issuing Solutions business—represent a return to FIS's roots as a deep-infrastructure provider to the financial system. Whether that focus can be maintained, and whether the company can modernize its technology platform fast enough to fend off cloud-native challengers, will determine whether FIS remains the backbone of global financial infrastructure for the next fifty years—or becomes a cautionary tale about the mortality of monopolies.

The betting odds, given what we know today, favor the former. FIS has survived fifty-plus years of technology change, economic cycles, strategic missteps, and competitive threats. The franchise has endured because the switching costs are real, the revenues are recurring, and the infrastructure is genuinely difficult to replace.

But the margin of safety is narrower than it used to be, and the stakes have never been higher. The next chapter of the FIS story—whether it becomes a case study in successful strategic reinvention or a cautionary tale about the limits of infrastructure incumbency—is being written right now.

XI. Recent News

Several significant developments have shaped FIS's trajectory in the most recent period.

On January 9, 2026, FIS completed two landmark transactions simultaneously: the acquisition of Global Payments' Issuer Solutions business, rebranded as FIS Total Issuing Solutions, and the sale of its remaining forty-five percent stake in Worldpay to Global Payments. The Issuer Solutions acquisition was valued at $13.5 billion in enterprise value, and the Worldpay stake was sold for $6.6 billion. These transactions completed FIS's multi-year transformation from a three-legged conglomerate into a focused banking technology and issuer processing platform.

On February 24, 2026, FIS reported full-year 2025 results that exceeded expectations. Revenue reached $10.7 billion with six percent adjusted growth, adjusted EPS grew ten percent to $5.75, and free cash flow jumped nineteen percent to $1.6 billion. The company introduced its 2026 outlook, projecting adjusted revenue growth of 30 to 31 percent (reflecting the Total Issuing Solutions contribution) and adjusted EPS of $6.22 to $6.32. On a pro forma basis, organic growth is projected at 5.1 to 5.7 percent.

In January 2026, FIS launched its agentic commerce platform in partnership with Visa and Mastercard, positioning itself at the intersection of artificial intelligence and payment processing. The platform enables AI agents to initiate and process financial transactions over card networks, with built-in fraud detection and authorization capabilities. This early mover advantage in AI-mediated commerce represents one of the most forward-looking initiatives in the company's history.

The board approved a ten percent dividend increase to $0.44 per share in January 2026, signaling confidence in the company's cash flow trajectory. However, management has paused share repurchases and discretionary M&A to prioritize deleveraging toward the 2.8 times gross leverage target, reflecting the financial discipline that has characterized the Ferris era.

In December 2025, FIS agreed to pay $210 million to settle a class-action shareholder lawsuit related to the Worldpay acquisition period, covering shareholders who purchased FIS stock between May 7, 2020 and February 10, 2023. The settlement resolved allegations of material misrepresentation about the Worldpay integration without any admission of fault.