FIBRA Prologis: The Nearshoring Kingmaker

I. Introduction & Episode Roadmap

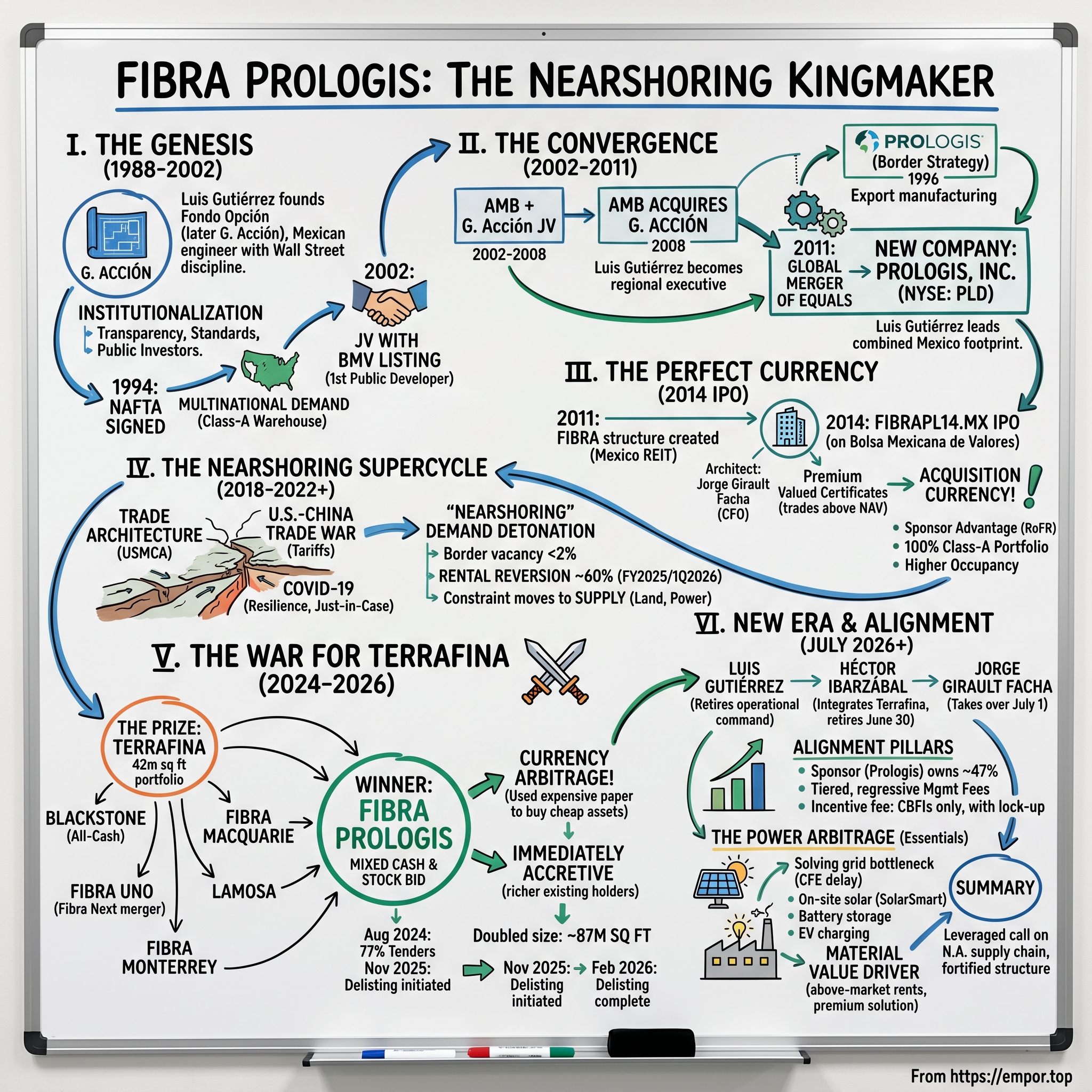

In the summer of 2024, a quiet trust that most North American investors had never heard of found itself at the center of the largest corporate bidding war in the history of Latin American real estate. The prize sat in plain sight: Terrafina, a sprawling 42-million-square-foot portfolio of industrial warehouses stitched along Mexico's manufacturing corridors and northern border. To the casual observer, it was a pile of concrete tilt-up boxes. To the six financial titans circling it, it was something far more valuable — a controlling stake in the single most important real estate story on the continent.

The bidders read like a who's who of global capital. Blackstone, the world's largest alternative asset manager, came armed with an all-cash offer and the swagger of a firm that rarely loses. FIBRA Uno, Mexico's largest real estate investment trust, tried to bolt Terrafina onto a brand-new spinoff vehicle. FIBRA Macquarie, the Australian-backed industrial specialist, offered its own paper. FIBRA Monterrey and the building-materials group Lamosa lurked with niche structural bids. And then there was the eventual winner — a trust whose full name barely fits on a single line: Fideicomiso de Infraestructura y Bienes Raíces Prologis, known to the Bolsa Mexicana de Valores simply as FIBRAPL14.MX, and to everyone else as FIBRA Prologis.[^1]

What made the contest fascinating was not who had the most money. Blackstone had effectively bottomless cash. It was who held the most valuable currency. FIBRA Prologis, sponsored by Prologis, Inc. — the largest logistics real estate company on Earth — had spent a decade cultivating a reputation so pristine that its publicly traded certificates traded at a premium to the underlying value of its buildings. While rivals had to write checks, FIBRA Prologis could pay in its own appreciated paper. That distinction, as we'll see, decided the entire war.

This is a story that spans nearly four decades and two continents. It begins in 1988, when a young Mexican engineer named Luis Gutiérrez looked at his country's chaotic, family-controlled property market and decided to drag it onto Wall Street terms.[^1] It runs through the signing of NAFTA, two transformational global mergers, the invention of the Mexican REIT, a 2014 IPO engineered to be the perfect acquisition weapon, and a geopolitical earthquake — "nearshoring" — that turned dusty border warehouses into some of the most coveted square footage in the Western Hemisphere.

There are three big questions we want to answer. First: how did a local developer called G. Acción become, through accident and design, the undisputed king of Latin American industrial real estate? Second: how did its management pull off a masterclass in financial engineering — using premium-priced paper to buy cheap assets — and win Terrafina while cash-rich rivals went home empty-handed? And third: on the eve of a historic leadership transition on July 1, 2026, how does the incoming chief executive, Jorge Girault Facha, plan to solve the one bottleneck money alone can't fix — Mexico's broken electrical grid?

Our thesis, stated up front: FIBRA Prologis is not really a collection of warehouses. It is a highly strategic, leveraged call option on the restructuring of North American supply chains — wrapped inside a fortress balance sheet and bolted to a parent company whose interests are almost perfectly aligned with minority holders. Whether that option pays off depends on forces — trade politics, electrons, water — that no real estate manager fully controls. Let's start at the beginning.

II. The Genesis: G. Acción & the Institutionalization of Mexican Real Estate (1988–2002)

To understand why FIBRA Prologis exists, you first have to understand how broken Mexican commercial real estate was before it. In the 1980s, if you were a multinational manufacturer setting up a plant outside Monterrey or Guadalajara, you didn't lease a warehouse from an institution. You shook hands with a family. Property was owned in opaque private structures, financed informally, built to inconsistent standards, and governed by relationships rather than contracts. Roofs leaked. Title was murky. There was no Class-A market because there was barely a market at all — just a patchwork of dynasties.

Into this fragmented world stepped a young engineer named Luis Gutiérrez. In 1988, Gutiérrez co-founded a company called Fondo Opción, later renamed G. Acción.[^1] His insight was deceptively simple and, for Mexico at the time, almost heretical: real estate could be a financial product. It could be institutionalized, made transparent, held to international standards, and — crucially — opened to public investors. He wanted to bring Wall Street discipline to a business that had run for generations on abrazos and gut feel.

The timing turned out to be extraordinary. In 1994, Mexico, the United States, and Canada signed the North American Free Trade Agreement, and the manufacturing geography of the continent began to bend. Suddenly, global automakers, electronics firms, and logistics providers wanted to build in Mexico to serve the U.S. market duty-free. But these were sophisticated multinationals with sophisticated requirements. They needed buildings that wouldn't flood, that had high enough ceilings — "clear heights" in the trade — to stack modern racking, that offered reliable security and clean title. G. Acción's bet was that these tenants would pay a premium for exactly that: high-quality, secure, Class-A space delivered to a standard they recognized from home.

It was the right bet. As foreign direct investment poured in through the late 1990s, G. Acción built a reputation as the developer that could deliver institutional product on Mexican soil. And Gutiérrez did something no Mexican real estate developer had done before: he took the company public on the Bolsa Mexicana de Valores, making G. Acción the first publicly listed real estate developer in Mexican history.[^1] That milestone matters less for the capital it raised than for what it signaled — a Mexican property company willing to submit to public disclosure, audited financials, and the scrutiny of minority shareholders. It was the institutionalization Gutiérrez had been chasing from the start.

By the turn of the millennium, G. Acción had become the most credible name in Mexican industrial development. And credibility, in a market starved of it, attracts global capital. In 2002, that capital arrived in the form of AMB Property Corporation, a San Francisco-based industrial REIT then aggressively expanding around the world. AMB had spotted what G. Acción had built — a local development machine with deep relationships, a pipeline of multinational tenants, and a management team that thought like financiers — and it wanted in. The two firms formed a joint venture, marrying AMB's global balance sheet to G. Acción's on-the-ground execution.[^1]

That partnership would prove to be the hinge on which the entire story turns. Gutiérrez had spent fourteen years proving that institutional-grade industrial real estate could work in Mexico. Now a deep-pocketed American partner was prepared to scale it. What began as a joint venture would, within six years, become an outright acquisition — and pull Gutiérrez and his team into the orbit of two of the largest real estate platforms on the planet.

III. The Convergence: AMB, ProLogis, and the 2011 Merger of Equals

Joint ventures are courtships. Sometimes they end in marriage. The AMB–G. Acción partnership ended in acquisition — a slow, deliberate one that unfolded over three years. Starting in 2005, AMB, together with the U.S. retail-property group Kimco and G. Acción's own management, launched a tender offer to privatize and delist the very company Gutiérrez had taken public seventeen years earlier.[^1] By 2008, AMB had acquired 100% of G. Acción, folding it entirely into its global platform.

There is a neat irony here worth pausing on. Gutiérrez had made his name by listing a Mexican real estate company — proving the public-markets model could work. Now he was helping take it private again. But the logic was sound: as a wholly owned engine inside AMB, the Mexican business could draw on a far larger pool of capital and grow faster than a standalone BMV-listed developer ever could. Gutiérrez didn't disappear in the deal; he was elevated, named Managing Director of AMB's Latin American operations.[^1] The local founder had become a regional executive at a global firm.

While all this was happening on the AMB side, a parallel story was unfolding a few hundred miles away — quite literally, along Mexico's northern border. ProLogis, then still operating under its earlier identity as Security Capital Industrial Trust, had entered Mexico independently back in 1996.[^1] Its strategy was different in emphasis from G. Acción's. Where Gutiérrez's team had built a diversified, multinational-tenant footprint, ProLogis went straight for the export jugular: it concentrated heavily on the border manufacturing hubs — Tijuana, Ciudad Juárez, Reynosa — the cities where goods were assembled and trucked north into the United States under NAFTA. ProLogis was building the physical infrastructure of cross-border trade.

So by the late 2000s, two of the most important industrial portfolios in Mexico were owned by two of the largest industrial REITs in the world — AMB and ProLogis — operating in parallel, sometimes competing for the same tenants and the same land. The obvious question hung in the air: what if they combined?

They did. In June 2011, AMB and ProLogis executed a roughly $9 billion global "merger of equals," combining into a single company that took the ProLogis name (restyled as Prologis, Inc.) and the New York Stock Exchange ticker PLD.[^1] This was not primarily a Mexico deal — it was a global consolidation that created the world's largest owner and operator of logistics real estate, with assets across the Americas, Europe, and Asia. But for Mexico, the consequences were enormous. Overnight, the legacy G. Acción/AMB portfolio and the legacy ProLogis border portfolio belonged to the same parent.

Someone had to lead the combined Mexican footprint, and the choice was telling. Prologis selected Luis Gutiérrez — the local founder, the man who had institutionalized the market in the first place — to run it.[^1] It was a vote of confidence not just in an individual but in a philosophy: that local knowledge, married to global capital, was the winning formula in emerging-market real estate. The combined Mexican business now held a deep, diversified, Class-A portfolio spanning both the domestic consumption markets around Mexico City and the export manufacturing belt along the border.

What it didn't yet have was its own public face. The Mexican assets were a subsidiary of a U.S.-listed giant, their value diluted inside a global balance sheet, invisible to investors who wanted a pure-play bet on Mexican industrial growth. The platform was assembled. The portfolio was world-class. The leadership was set. All that remained was to give it a stock of its own — and the vehicle to do that had just been invented.

IV. The 2014 IPO: Designing the Perfect Real Estate Currency

Every great financial vehicle needs a chassis, and in 2011 the Mexican government built one. That year, Mexico introduced the FIBRA structure — Fideicomiso de Infraestructura y Bienes Raíces, or "Infrastructure and Real Estate Trust" — modeled closely on the U.S. REIT.[^1] The mechanics will be familiar to anyone who knows American REITs: a FIBRA pays little to no corporate income tax provided it distributes the bulk of its earnings to certificate holders, and it must hold income-producing real estate. In plain terms, the structure lets rental income flow through to investors largely untaxed at the entity level, in exchange for high mandatory payouts. It was Mexico's attempt to do for real estate what the REIT had done for the United States since 1960 — turn buildings into liquid, dividend-paying securities ordinary investors could buy.

The first Mexican FIBRA, FIBRA Uno, launched in 2011, and a wave of others followed. Prologis watched, prepared, and waited until it had the structure and the story exactly right. The man tasked with engineering the financial architecture of the offering was the company's chief financial officer, Jorge Girault Facha — a name to remember, because he is the throughline of this entire saga and, by the time we reach the present day, its protagonist.[^9] Girault's job was not merely to "do an IPO." It was to design a security that would function as a weapon — a premium-valued currency the company could later deploy to grow.

On June 4, 2014, FIBRA Prologis went public on the Bolsa Mexicana de Valores under the ticker FIBRAPL14, pricing at 27.00 Mexican pesos per certificate and raising roughly $541 million.[^1] On the surface, it was one more industrial FIBRA joining an increasingly crowded field. Underneath, it was something subtly different — and the difference is the whole point of this section.

Here's the debate that raged at the time, and it's a debate every value-minded investor should sit with. The bear case at IPO was straightforward: investors were overpaying. FIBRA Prologis priced at a premium to its already-listed industrial peers — Terrafina (then trading as TERRA13) and FIBRA Macquarie (FIBRAMQ12). Worse, from a yield-hungry perspective, it offered a lower initial dividend yield of roughly 4%, while Terrafina was throwing off 7–8%.[^1] If you were an income investor scanning the Mexican REIT aisle in 2014, FIBRA Prologis looked like the expensive box on the shelf that paid you less to own it. Why on earth would you buy it?

The bull case answered with one word: quality. FIBRA Prologis came public as a pure-play, 100% Class-A portfolio — no mixed-use distractions, no second-tier buildings dragging down the average. Its occupancy stood at 94.3%, materially higher than peers struggling to keep older space leased.[^1] And it carried something none of the others had: the "Sponsor Advantage." As the listed Mexican arm of Prologis, Inc., the FIBRA held a right of first refusal to acquire any property its parent developed in Mexico.[^1] In effect, the world's largest logistics developer had become FIBRA Prologis's private development pipeline — building new Class-A product and offering it to the FIBRA first. That is an extraordinary structural advantage. It meant the FIBRA could grow without taking on speculative development risk itself; the parent absorbed the risk, and the trust got the finished, leased buildings.

So who was right? With the benefit of a decade's hindsight, the verdict is emphatic. What looked like an "overpay" in 2014 turned out to be a profound underpay for quality. The lower yield was a feature, not a bug — it reflected the market's recognition that this was the best portfolio in the sector. Over the following decade, the premium compounded on itself. FIBRA Prologis consistently traded at a premium to its net asset value — meaning the stock market valued its certificates above the appraised worth of its buildings — while peers languished at deep discounts to NAV, their certificates worth less than the bricks they represented.[^1]

That persistent premium-to-NAV is the single most important financial fact in this entire story, so let's make sure it lands. When a REIT trades above its asset value, it can issue new certificates to buy buildings and increase per-share value rather than dilute it — it's selling expensive paper to buy cheaper assets. When a REIT trades below asset value, issuing stock to grow destroys value. FIBRA Prologis, by being priced as the quality leader from day one, had quietly minted itself an acquisition currency. The yield-chasers who skipped it in 2014 missed the point entirely. The premium was the weapon. And in 2024, the company would finally pull it from the holster.

V. The Nearshoring Supercycle: How Geopolitics Reshaped Mexico's Economy

For most of the 2010s, FIBRA Prologis was a good, steady compounder — well-run, well-located, modestly growing. Then the world broke, and Mexico's warehouses became gold. To understand why the Terrafina war happened at all, you have to understand the macroeconomic earthquake that hit between roughly 2018 and 2022, when three tectonic plates ground together and remade the industrial map of North America.

The first plate was trade architecture. In 2020, NAFTA was replaced by the USMCA — the United States-Mexico-Canada Agreement — which kept the free-trade framework but tightened the rules of origin, particularly for automobiles. To qualify for duty-free treatment, a higher share of a product's content had to be made within North America. The practical effect was to reward manufacturing located in Mexico and penalize deep reliance on Asian inputs. The treaty quietly rewrote the calculus of every supply-chain executive on the continent.

The second plate was the U.S.–China trade war. Beginning in 2018, escalating American tariffs on Chinese goods made the long-standing default — manufacture in 中国 China, ship across the Pacific — suddenly expensive and politically fraught. Companies that had spent thirty years building China-centric supply chains began, cautiously, to look for alternatives. The industry coined a term for the leading candidate: "nearshoring," the relocation of production from distant Asia to nearby Mexico, hard against the U.S. border.

The third plate was the one nobody saw coming: COVID-19. When the pandemic seized up global shipping in 2020 and 2021 — container ships stacked up outside Los Angeles, transpacific freight rates exploding tenfold — executives learned a brutal lesson about the fragility of long, thin supply chains. The decades-old gospel of "Just-in-Time" inventory, which prized minimal stock and maximal efficiency, gave way almost overnight to "Just-in-Case": hold more inventory, hold it closer, and never again let a factory in another hemisphere shut down your assembly line. "Closer" meant Mexico. "Closer" meant warehouses.

When three forces like that collide, you get a supercycle. Demand for industrial space in Mexico didn't grow — it detonated. Vacancy rates in the critical northern border cities — Tijuana, Ciudad Juárez, Monterrey — collapsed to historic lows below 2.0%.[^8] To put that in human terms: in those markets, virtually every usable warehouse was full, and a tenant looking for space often simply could not find any. When supply is that tight, the landlord holds all the cards.

The financial consequence showed up in a metric that became FIBRA Prologis's calling card: rental reversion. This is the rent increase captured when an old lease expires and a new one is signed at current market rates. If a tenant signed a five-year lease in 2020 and it rolls over in 2025, the reversion measures how much higher the new rent is. At FIBRA Prologis, reversions climbed to a frankly stunning 59.1% for fiscal year 2025, and then hit 59.6% in the first quarter of 2026.[^3] Read that again. Leases were re-signing at nearly 60% higher rents than the expiring ones. That is not a normal real estate number — it is the financial signature of a market where demand has overwhelmed supply so completely that landlords can re-price space by half again and tenants still sign, because the alternative is no space at all.

And here is the strategic punchline that sets up everything to come. As the boom matured, the binding constraint on growth stopped being tenant demand. There were plenty of tenants — more than the market could house. The constraint became supply itself: the availability of developable land near the border and, increasingly, access to the utilities — electricity and water — needed to make that land usable. The bottleneck moved from the demand side to the supply side. In a world where you can't simply build your way out of scarcity, the value of an already-assembled, already-powered portfolio goes through the roof. Which is precisely why, in 2024, a 42-million-square-foot portfolio called Terrafina suddenly became the most fought-over asset in Latin America.

VI. The War for Terrafina: Latin America's Greatest Real Estate Battle (2024–2026)

Every great acquisition battle starts with a company that knows it's worth more than its stock price says. In early 2024, that company was Terrafina. It owned a roughly 42-million-square-foot industrial portfolio that overlapped beautifully with the nearshoring map — and yet its certificates traded at a stubborn discount, partly a function of its external management arrangement and partly the market's chronic under-appreciation of Mexican REITs. Frustrated by the gap between intrinsic value and market value, Terrafina announced it was exploring strategic alternatives.[^1] In the language of Wall Street, it had hung a "for sale" sign on the door. The question was who would walk through it — and the answer turned into a six-way brawl.

Let's walk the battlefield. On one flank stood Blackstone, partnering with the Mexican industrial group MRP. Blackstone's pitch was the purist's pitch: cash. It launched an all-cash tender offer, initially around 40.50 pesos per certificate and later raised to 42.50 pesos, and it leaned hard on a single argument — that an all-cash deal was the only "tax-certain" exit for Terrafina holders, a clean check with no ambiguity about what you'd receive.[^5] For a certain kind of investor, especially one weary of paper promises, that certainty was seductive.

On another flank came the FIBRA peers. FIBRA Macquarie offered a stock exchange ratio of 1.125x — meaning Terrafina holders would receive 1.125 Macquarie certificates for each of theirs. FIBRA Uno, the sector's largest player, floated a more elaborate scheme: a merger involving its newly created "Fibra Next" vehicle, an attempt to use a fresh listing structure as acquisition fuel. And around the edges, FIBRA Monterrey and the building-materials company Lamosa circulated niche structural and asset-level bids — interested in pieces, or in particular angles, rather than the whole.

And then there was FIBRA Prologis, which structured the cleverest bid of them all. Its offer was a mixed cash-and-stock deal: an exchange ratio of 0.63x FIBRAPL certificates per Terrafina certificate, or 45.00 pesos in cash — with the cash component capped at just 10% of the total deal.[^1] That cap is the tell. Prologis was not trying to win a cash auction it could not win against Blackstone. It was deliberately structuring a stock deal, offering Terrafina holders the chance to swap their discounted paper for the most premium-valued certificates in the entire sector. The small cash sleeve was a sweetener for those who needed liquidity; the heart of the offer was an invitation to trade up in quality.

Now to the question that should be burning in every value investor's mind: did Prologis overpay? At an implied 45.00 pesos, it was clearly paying a premium to where Terrafina's stock had been languishing. But look at what it bought. Industry estimates put the implied capitalization rate on the acquired assets at roughly 7.2% to 7.5% — meaning Prologis was acquiring income-producing warehouses at a yield comfortably above what it would cost to develop equivalent space.[^1] And developing 42 million square feet from scratch in 2024 was not merely expensive; in many border markets it was effectively impossible in any reasonable timeframe, thanks to land scarcity, construction-cost inflation, and the grid lockouts we'll dissect in Section VIII. Buying Terrafina's already-built, already-powered, already-leased portfolio was dramatically cheaper and faster than building it. The premium on the screen masked a discount in reality.

But the true genius was the currency arbitrage — the weapon loaded back at the 2014 IPO. Recall that FIBRA Prologis traded at a premium to net asset value while Terrafina traded at a discount. So Prologis was using expensive paper to buy cheap assets. When it issued its highly valued certificates to Terrafina holders pro-rata, the math worked in existing FIBRAPL holders' favor: because the certificates being handed out were worth more (relative to their underlying assets) than the assets being acquired, the deal was immediately accretive to both net asset value per certificate and funds from operations per certificate.[^1] In plain English: existing FIBRA Prologis owners came out richer per share the day the deal closed, not diluted. That is the holy grail of M&A — growth that adds value instead of subtracting it — and only a company with a premium currency can pull it off. Blackstone, paying cash, could never make that argument. It could only win on price, and price alone wasn't enough.

The market agreed. By August 2024, FIBRA Prologis had secured the tenders of 77.14% of Terrafina's certificate holders — a decisive majority that effectively ended the contest.1[^4] Blackstone, for all its cash and all its swagger, walked away empty-handed. Over the following year, Prologis ground its ownership higher, pushing past 99% by late 2025 and moving to squeeze out the remaining holders. In November 2025 it formally initiated the delisting of Terrafina, which was completed in February 2026.[^7] The 42-million-square-foot portfolio that had drawn six bidders was now simply part of FIBRA Prologis.

The strategic result was staggering. The acquisition nearly doubled FIBRA Prologis's leasable area to more than 86.9 million square feet, cementing it as the unambiguous titan of Latin American industrial real estate — larger, denser, and more dominant in the nearshoring markets than any rival.[^3] It had won not by outspending the world's largest cash buyer, but by out-structuring it. And the man who would inherit this newly doubled empire was about to step into the top job.

VII. The Cusp of a New Era: The July 2026 Leadership Hand-off & Sponsor Alignment

We are broadcasting this episode in the final days of June 2026, on the absolute eve of one of the most consequential leadership hand-offs in the history of Latin American real estate. The timing is almost too neat for a screenwriter: a company that just doubled in size is about to change captains, and the change has been thirty years in the making.

Let's account for the retiring captains first, because their arcs are the company's history. The founder, Luis Gutiérrez — the engineer who institutionalized Mexican real estate in 1988, took G. Acción public, survived its privatization, and led the combined platform through two global mergers — stepped back from operational command in late 2023, transitioning to Senior Advisor and Chairman of the Technical Committee.[^9] (The Technical Committee, for those new to FIBRA governance, is roughly the equivalent of a board of directors in this trust structure — so Gutiérrez moved from running the business to overseeing it, the classic founder's graceful exit.)

Operational leadership through the most important years passed to Héctor Ibarzábal, who had served as chief operating officer since the 2014 IPO and then stepped up as chief executive. It was Ibarzábal who held the wheel during the white-knuckle Terrafina campaign and, harder still, the integration that followed — absorbing 42 million square feet, hundreds of leases, and a rival organization into the FIBRA Prologis machine without dropping the ball on the core portfolio. Having executed that integration, Ibarzábal is retiring on June 30, 2026 — his work, by any measure, complete.[^9]

Which brings us to the new commander. Effective July 1, 2026 — tomorrow, as we record this — Jorge Girault Facha takes over as chief executive officer.[^9] If you've been listening closely, his name has appeared at every pivotal moment in this story, and that is exactly the point. This is a classic Acquired-style narrative arc, the kind we love precisely because it's so rare. Girault has been with this platform since the G. Acción days in 1994. He survived the AMB acquisition. He survived the ProLogis merger. He was the architect who engineered the 2014 IPO — the man who designed the premium currency itself. And he served as chief financial officer for more than a decade, including through the Terrafina war he helped finance.[^9] His elevation to CEO is not a change of direction; it is the ultimate signal of continuity. The financier who built the weapon now commands the army.

Now, here's where we need to talk about something that separates FIBRA Prologis from a great many externally managed REITs around the world — and it's a topic that should make every long-term investor lean in: alignment. The dirty secret of externally managed real estate vehicles is that the manager and the shareholders often want different things. The manager earns fees on assets under management, so it's incentivized to grow the empire — to buy more, borrow more, get bigger — even when bigger doesn't mean better for shareholders. The sponsor collects rich fees while bearing little of the downside. It's a structure that quietly transfers wealth from minority holders to the manager.

FIBRA Prologis is built differently, and the difference rests on three pillars. The first is skin in the game. Prologis, Inc. — the global parent — maintains a roughly 47% ownership stake in FIBRA Prologis.[^3] It is, by an enormous margin, the largest single investor in the trust. When the certificates fall, Prologis bleeds alongside every minority holder; when they rise, it wins alongside them. The sponsor isn't a fee-extracting landlord sitting outside the building — it's the majority owner living inside it. That single fact realigns nearly every incentive.

The second pillar is fee discipline, and this is where Girault's CFO instincts show. Under his direction, FIBRA Prologis aggressively renegotiated its management fees downward — the opposite of what a self-interested manager would do. Effective January 1, 2025, the fees moved to a tiered, declining schedule: 70 basis points on assets up to $5 billion, 60 basis points up to $7.5 billion, and 50 basis points above $7.5 billion.[^3] The structure is deliberately regressive — the bigger the trust grows, the lower the marginal fee rate — which means scale benefits flow to certificate holders rather than to the manager. And it's forward-looking: should FIBRA Prologis ever acquire FIBRA Macquarie (a long-rumored next move), a new 40-basis-point tier would kick in, ratcheting the rate down further still.[^3]

The third pillar is the incentive fee, and it's the most elegant of all. The manager's incentive fee is set at 10% of total returns above a compounding 9.0% annual hurdle rate.[^3] Two design choices make this investor-friendly in a way most REIT structures are not. First, the hurdle: management earns the incentive only on returns that exceed 9% per year, compounding — so it gets paid for genuine outperformance, not for simply riding a rising market. Second, and crucially, the incentive fee is paid only in certificates (CBFIs), with a mandatory six-month lock-up.[^3] The manager can't take its bonus in cash and walk away; it must take FIBRA Prologis stock and hold it. So the people running the company are forced to become ever-larger owners of it, paid in the very currency whose value they're charged with protecting. It is, in a sense, the 2014 currency philosophy turned inward — alignment enforced by structure, not promised by press release.

This is the platform Jorge Girault inherits: a doubled portfolio, a fortress balance sheet, a parent that owns nearly half the equity, and a fee structure engineered to pay management only when minority holders win. But inheriting a great machine and driving it forward are different things. And the single biggest obstacle on the road ahead isn't financial at all. It's physical. It's electricity.

VIII. The Power Arbitrage: Prologis Essentials & Solving Mexico's Energy Bottleneck

Here is the paradox at the heart of Mexican nearshoring in 2026. The hardest part of moving a factory to Mexico is no longer finding a tenant, signing a lease, or even building the walls. The hardest part is turning on the lights. The single greatest constraint on the nearshoring boom has become access to electricity — and that, counterintuitively, is where FIBRA Prologis may have its most durable edge.

The problem traces back to the state-owned utility, the Comisión Federal de Electricidad — CFE — which controls Mexico's transmission grid. Years of underinvestment and policy that favored the state utility over private power generation left the grid badly bottlenecked, particularly in the booming northern manufacturing belt where demand has exploded. The practical consequence is brutal for manufacturers: connecting a newly built factory to the grid can take anywhere from 12 to 24 months.[^8] Picture it from a tenant's chair — you've relocated your supply chain, leased a gleaming new warehouse, installed millions of dollars of robotics, and now you sit idle for a year or two waiting for CFE to energize your building. The most expensive thing in nearshoring isn't rent. It's a powered building you can't power.

This is where Prologis turns an industry-wide crisis into a company-specific moat. The parent has spent years building a global platform called "Essentials" — a suite of value-added services that wrap around the bare warehouse: solar generation, energy storage, EV fleet charging, racking, lighting, and operational equipment. In Mexico, Essentials is being deployed as a direct answer to the CFE bottleneck. If you can't get electrons from the grid fast enough, you generate them on-site.

The centerpiece is rooftop solar paired with smart battery storage. FIBRA Prologis has set a goal of generating 30 megawatts of solar energy locally in Mexico — turning the vast, otherwise-dead acreage of warehouse rooftops into power plants.[^3] The model is best illustrated by a real installation. At Prologis Park Grande in Tepotzotlán, north of Mexico City, the company installed a 619-kilowatt-DC rooftop solar array in partnership with the logistics giant GEODIS — delivering clean, immediate power to the tenant with zero upfront capital outlay on the tenant's side through Prologis's "SolarSmart" program.[^11] The tenant doesn't finance the panels or wait on CFE; it simply moves in and draws power from the roof.

Think about what that combination — on-site solar, battery storage, and EV charging — actually does for a tenant racing against a grid queue. It lets a manufacturer bypass the 12-to-24-month CFE delay entirely and begin operations on Day 1. In a supply-constrained market where time-to-production is everything, that is not a marginal amenity. It is the difference between a factory that earns revenue this quarter and one that sits dark until 2028. And because it solves a problem money alone cannot quickly solve, it commands a premium. FIBRA Prologis can charge rents above standard market rates for space that comes pre-powered, making the Essentials business a high-margin, increasingly material driver of the core portfolio's value — not a side hustle, but a structural enhancement to the rent roll.

There's a deeper strategic point here that investors should sit with. In a normal real estate market, every landlord offers roughly the same product: square footage. Differentiation is thin, and tenants are mobile. But when the binding constraint becomes power, the landlord who controls power becomes something more than a landlord — it becomes the enabler of production itself. Prologis is converting the grid crisis from an industry headwind into a proprietary selling point, and in doing so it is quietly raising the switching costs and pricing power that underpin the whole investment case. Which is the perfect place to step back and ask the analytical question: how durable, really, is this business?

IX. Playbook: Porter's 5 Forces, Hamilton's 7 Powers, and Investing Lessons

Let's put FIBRA Prologis on the dissection table and run it through the two frameworks every serious business analyst keeps in the drawer — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces. The goal isn't to award a grade; it's to understand where the durability comes from and where it could crack.

Start with Helmer's 7 Powers, of which FIBRA Prologis plausibly holds three.

The first is Cornered Resource. Helmer's classic example is a patent or an irreplaceable mineral deposit — preferential access to a coveted asset that competitors can't replicate. For FIBRA Prologis, the cornered resource is twofold. First, it's land: ultra-prime, supply-constrained logistics sites in markets like Mexico City (essential for last-mile distribution to 22 million consumers) and Tijuana (the chokepoint for border export). They aren't making more of it, and the best parcels are already owned. Second — and this is the subtler, more modern cornered resource — it's power grid capacity. The interconnection rights and on-site generation infrastructure that Prologis has secured function as a literal cornered resource in a market where new connections take years. Control the electrons, and you control something rivals genuinely cannot quickly obtain.

The second power is Scale Economies. At roughly 87 million square feet, FIBRA Prologis can spread development expertise, solar procurement, financing costs, and corporate overhead across a base so large that its per-unit costs fall below what any subscale rival can achieve. The tiered, declining management-fee structure we examined earlier is scale economics made explicit — bigger means cheaper, per square foot. There's also a demand-side scale benefit: a multinational tenant like Amazon or DHL can lease across six Mexican cities from a single master landlord, with one relationship, one set of standards, one negotiation. That convenience is worth real money and locks the largest, stickiest tenants to the largest landlord.

The third power is Switching Costs, and it's underappreciated. An industrial manufacturing tenant doesn't just store boxes; it pours millions into customizing the interior — heavy robotics bolted to reinforced floors, automated racking systems, climate controls, specialized power and data infrastructure. Relocating that operation to a competitor's warehouse means tearing it all out, rebuilding it elsewhere, and halting production during the move. For a manufacturer, that's not an inconvenience; it's a catastrophe. The result is tenants who renew rather than relocate — which is exactly what lets the landlord push those eye-watering rental reversions.

Now Porter's Five Forces, which sketch the competitive weather.

Bargaining power of buyers (tenants): Low. With national industrial vacancy under 3% and border-market vacancy that touched below 2%, tenants are price-takers, not price-setters.[^8] When there's no alternative space to walk to, you sign the lease — which is the structural reason reversions run near 60% rather than the low-single-digit increases of a balanced market.

Threat of new entrants: Very low. To compete, a new player would need to assemble scarce land, raise enormous capital in a high-rate environment, navigate the grid-connection gauntlet, and somehow match an incumbent's tenant relationships and development track record. Each barrier alone is daunting; together they're close to prohibitive.

Bargaining power of suppliers: Worth a brief note — the most important "supplier" here is CFE, the power utility, and its bargaining power over the industry is high, which is precisely why on-site generation matters so much as a way to route around it.

Threat of substitutes: Low for the core function — there's no substitute for physical warehouse space in a goods economy, and nearshoring is structurally increasing the goods that need housing.

Competitive rivalry: Moderate, and this is where it gets interesting, because the rivals are real and named. The most direct scale competitor is Fibra Next / FUNO, the spinoff and parent combination that commands roughly 87 million square feet — a genuine peer in size. Then there's Vesta, an efficient, internally managed developer with about 43 million square feet, whose internal management means no external fee drag — a structurally different and in some ways cleaner model that value investors often admire. FIBRA Macquarie, at around 35 million square feet, is concentrated in northern manufacturing and is the perennial consolidation target (recall the pre-negotiated 40-basis-point fee tier waiting for exactly that deal). And FIBRA Monterrey, near 18 million square feet, plays a focused sale-leaseback game. The field is real, but it is fragmented, and FIBRA Prologis sits at or near the top of it on both scale and quality.

So what's the single transferable investing lesson from this whole saga? It's this: your currency is your destiny. FIBRA Prologis won the Terrafina war not because it had the deepest pockets — Blackstone's were deeper — but because it had spent a decade earning the most trusted, most premium-valued public currency in its sector. That premium let it do accretive, non-dilutive M&A that a cash buyer simply could not match. For investors, the lesson cuts two ways: prize companies whose stock is valued highly enough to be a weapon, and beware companies forced to issue cheap paper, because dilution is destiny too.

X. Conclusion, the Bull vs. Bear Case, & Key KPIs to Watch

Every investment thesis eventually has to confront the question Acquired always returns to: what would have to be true for this to work, and what would have to be true for it to fail? Let's lay out both, and then zero in on the handful of numbers that will actually tell the story going forward.

The three KPIs that matter most. We'll resist the temptation to hand you a dashboard of fifty metrics. For FIBRA Prologis, three numbers carry nearly all the signal, and a long-term holder should watch them the way a pilot watches three instruments.

The first is rental reversion — recently running near 59%.[^3] This is the single biggest engine of organic growth, the direct readout of supply-demand tension in Mexican industrial markets. As long as reversions stay high, FIBRA Prologis is re-pricing its existing buildings upward every time a lease rolls, growing income without spending a peso on new construction. The day reversions begin to compress meaningfully will be the day the nearshoring supply-demand imbalance starts to normalize — the most important leading indicator in the whole story.

The second is the occupancy rate, which should stay above 95% and stood at 97.0% in the first quarter of 2026.[^3] For a portfolio this dominant, occupancy is the heartbeat: high and stable occupancy confirms that demand remains broad and that the Terrafina integration hasn't introduced any soft spots. A sustained slide below the mid-90s would be the first quantitative hint that something — trade friction, oversupply, a demand wobble — is going wrong.

The third is loan-to-value (LTV) — the ratio of debt to asset value — which sits at a conservative ~23%.[^3] This is the balance-sheet instrument, and right now it reads "fortress." A 23% LTV means FIBRA Prologis has enormous unused debt capacity, which translates directly into dry powder for the next acquisition (FIBRA Macquarie, anyone?) and a deep cushion against rising rates or asset-value declines. Watching this number tells you how much firepower management is holding in reserve — and whether it's deploying that firepower prudently or recklessly.

The bear case. The risks here are real, and notably, the scariest ones are not financial — the balance sheet is too strong for that. They're physical and political. The first is the infrastructure bottleneck itself. The Essentials solar program is a clever workaround, but 30 megawatts of rooftop generation cannot substitute for a functioning national grid forever. If CFE's transmission constraints deteriorate further, or if water scarcity in the arid north begins to halt industrial construction outright, the supply of usable space — FIBRA Prologis's product — gets choked at the source. Water, in particular, is an underappreciated long-term hazard in northern Mexico, and it's the kind of constraint money can't quickly fix.

The second bear risk is geopolitical. The USMCA faces a formal review process in 2026, and the entire nearshoring thesis rests on the assumption that the U.S.-Mexico trade relationship remains open and predictable. A turn toward protectionism, fresh tariffs on Mexican goods, or political instability between the two governments could chill the foreign investment that fills these warehouses. FIBRA Prologis is, at bottom, a leveraged bet on North American economic integration — and that integration is a political choice that can be unmade by politicians.

The bull case. Against those risks stands a simple, powerful proposition: the multi-decade restructuring of global supply chains is still in its early innings. The forces that drove tenants to Mexico — trade architecture, China decoupling, supply-chain resilience — are structural, not cyclical, and they are years from playing out. Into that tailwind steps Jorge Girault Facha, a leader who has been preparing for this exact job for three decades, taking command of a consolidated 86.9-million-square-foot portfolio, a balance sheet with immense headroom, a parent aligned through a ~47% stake, and a solar-powered moat that turns Mexico's worst bottleneck into a competitive weapon.[^3] If the nearshoring supercycle has the legs its champions believe, FIBRA Prologis is positioned to compound for a very long time — the call option on North American supply chains, written by the one company that controls both the land and the lights.

Jorge Girault has been preparing for this job for thirty years. On July 1, 2026, he officially steps into the spotlight. We will be watching.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube