Federated Hermes: Asset Management's Quiet Survivor

I. Introduction & Episode Roadmap

There is a company in Pittsburgh, Pennsylvania, that manages over nine hundred billion dollars in client assets, has survived the worst financial crisis in modern history, reinvented itself twice, and yet most people outside institutional finance have never heard of it. Federated Hermes is not a household name like Fidelity or BlackRock. It does not sponsor stadiums or run Super Bowl ads. But for more than six decades, this family-controlled firm has quietly occupied a critical node in the global financial plumbing, managing the cash that corporations, governments, and pension funds rely on every single day.

The central mystery of the Federated Hermes story is this: how did a company founded by two high school buddies in a downtown Pittsburgh arcade grow into one of the largest money market fund operators on the planet, survive a near-death experience in 2008 that nearly wiped out the entire industry, navigate a decade of regulatory assault on its core product, and then pull off an acquisition in London that transformed it from an American cash management specialist into a global responsible investing leader?

The answer involves a West Point-trained pilot who bought a $49 correspondence course and turned it into a financial empire. It involves a moment in September 2008 when the entire money market industry came within hours of systemic collapse. It involves a CEO who called proposed regulations "totally brain dead" and then, when those regulations passed anyway, had the strategic flexibility to pivot. And it involves a bet on ESG investing and corporate stewardship that looked contrarian at the time and now looks prescient, even as it creates new tensions in an era of political polarization around environmental, social, and governance principles.

This is a story about survival, adaptation, and the tension between being big enough to matter and small enough to remain distinctive. For investors, Federated Hermes offers a case study in what happens when a company built around a single product category faces existential disruption and must choose between slow decline and radical transformation. The fact that the Donahue family still controls every voting share, more than seventy years after founding, adds a governance dimension that cuts both ways: it enabled long-term thinking that saved the firm, but it also raises questions about entrenchment and succession that grow louder with each passing year.

The story unfolds in three acts. Act one is the origin, the money market revolution, and the building of a distribution machine that made Federated the second-largest mutual fund company in America by the early 1980s. Act two is the crisis years: the 2008 panic, the regulatory gauntlet, and the grinding pressure of zero interest rates that threatened to erode the business model entirely. Act three is the reinvention: the Hermes acquisition, the pivot to ESG, and the question of whether a Pittsburgh-based money market specialist can convincingly become a global leader in responsible investing.

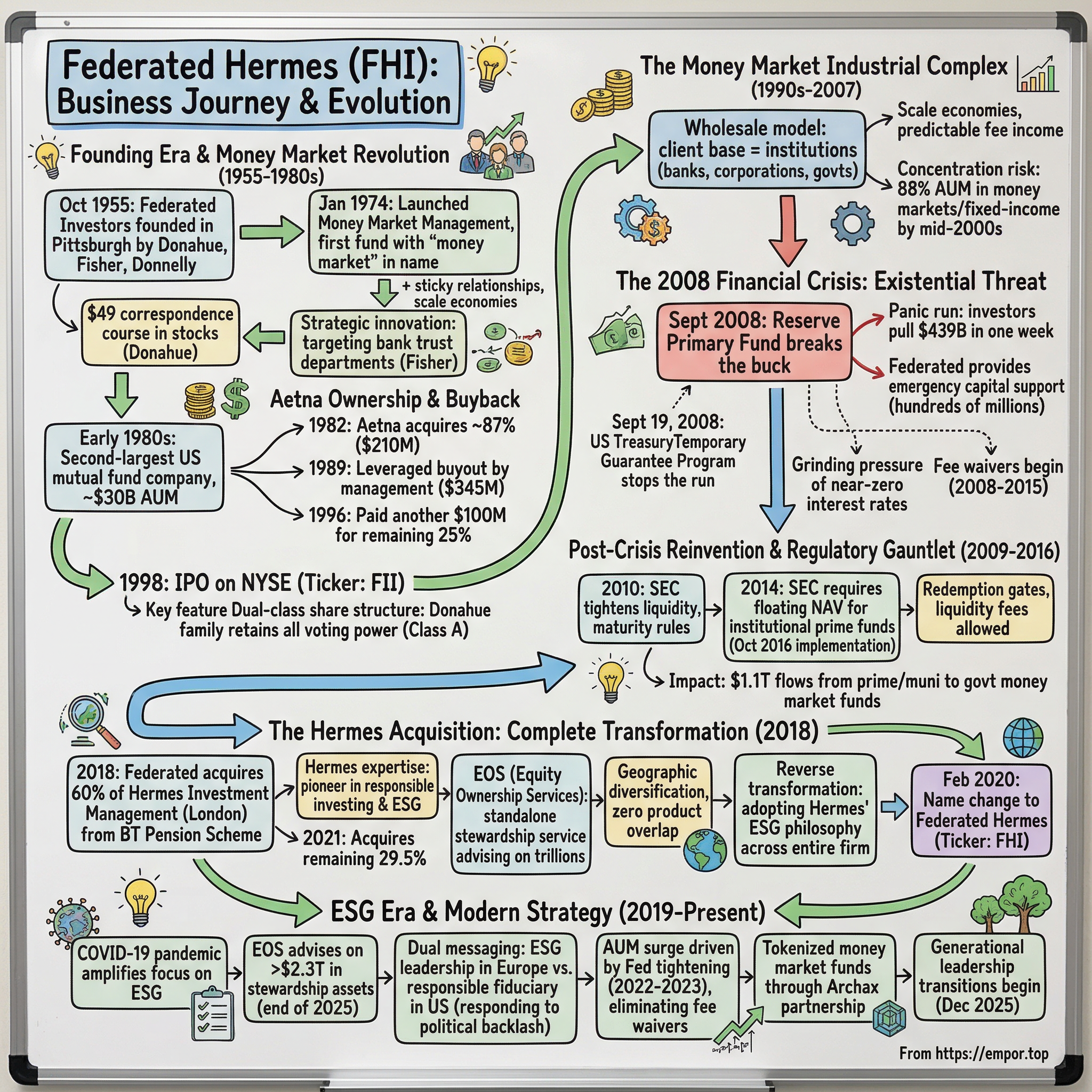

II. Founding Era & The Money Market Revolution (1955-1980s)

The story begins not in a gleaming office tower but in a cramped storefront in Pittsburgh's Jenkins Arcade. In October 1955, three graduates of Central Catholic High School pooled their ambitions and founded Federated Investors. John Francis Donahue was the visionary, Richard B. Fisher was the salesman, and Thomas J. Donnelly provided legal counsel. None of them came from Wall Street pedigrees. Donahue had graduated from West Point in 1946, flown B-29 bombers in the Strategic Air Command, and left the Air Force in 1950 with a restless energy and no clear plan. He purchased a stock market correspondence course from Forbes magazine for forty-nine dollars, and that mail-order education changed the trajectory of American asset management.

Fisher's path was even more improbable. Before joining Donahue in the mutual fund business, he had been selling Cadillacs at Motor Square Garden in East Liberty. In 1951, he reconnected with his high school classmate at King, Merritt & Co., a brokerage firm where both men were selling mutual funds on commission. Fisher brought a gift for salesmanship that would define Federated's distribution DNA for decades. He would travel kitchen table to kitchen table, educating ordinary Americans about a product most had never encountered. Years later, even at age ninety-four, Fisher still required every new salesperson to deliver a complete fund pitch for his personal critique before being allowed to contact a single client.

Donnelly, the third co-founder, brought legal acumen that would prove essential as the mutual fund industry grew more regulated. But the partnership's real magic was the Donahue-Fisher combination: the strategist and the closer. Donahue saw the big picture, understood the regulatory landscape, and set the long-term direction. Fisher made the sales happen, one handshake at a time.

The early years were modest. Federated acquired its first registered fund, the Income Foundation Fund, in January 1956. By August 1959, the company went public with shares priced at $4.75 and total assets under management of roughly thirteen million dollars. In January 1962, the firm launched the Empire Fund, which attracted approximately three hundred million dollars through tax-free stock exchange features, an enormous sum for a small Pittsburgh operation. But the real breakthrough was still a decade away.

To understand what happened next, you need to understand Regulation Q. This obscure Federal Reserve rule, dating to 1933, capped the interest rates that commercial banks could pay on savings deposits, typically around five and a quarter percent. For decades, this was fine. But by the late 1960s and into the 1970s, inflation and rising market interest rates created an enormous gap between what banks could legally pay depositors and what the open market was offering. Treasury bills were yielding five percent and climbing, while banks were stuck at their regulated ceilings. Savers, understandably, began pulling their money out of bank accounts and seeking higher returns elsewhere. This process, known as disintermediation, created one of the greatest product opportunities in the history of finance.

In 1971, Bruce Bent and Henry Brown created the Reserve Fund, the first money market mutual fund. The concept was elegant in its simplicity: pool investor cash, buy short-term, high-quality securities like Treasury bills and commercial paper, and offer a yield that tracked market rates, far above what banks could legally pay. The investor got liquidity (you could write checks against the account), safety (the underlying assets were all short-term and high-quality), and a better return than any bank savings account. The fund company got management fees on a growing pile of assets. And banks watched helplessly as deposits fled.

It was one of those rare financial innovations that was genuinely beneficial for ordinary consumers. For the first time, small savers could earn money market rates that had previously been available only to institutions buying Treasury bills in denominations of ten thousand dollars or more. The democratization of cash management was a quiet revolution, and Federated was positioned perfectly to ride it.

Federated saw the opportunity and moved aggressively. In June 1969, it had already introduced the first mutual fund dedicated exclusively to U.S. Government securities. But the pivotal moment came on January 16, 1974, when Federated launched Money Market Management, the first fund to include the words "money market" in its name.

This was not just a product launch; it was a branding masterstroke that helped define an entire asset class. By putting "money market" directly in the fund's name, Federated made the product category instantly comprehensible to investors and advisors. A promotional campaign generated ninety thousand investor leads by October of that year, a staggering response that confirmed the depth of demand.

In January 1976, Federated pioneered two more firsts: the industry's first institutional-only money market fund and the first municipal bond money market fund, both products that would become cornerstones of institutional cash management. The institutional money market fund was particularly significant because it opened up a market of corporate treasurers, government entities, and pension funds that managed enormous pools of cash and desperately needed efficient vehicles for short-term investment. The municipal money market fund added tax-exempt yield, attracting investors in high-tax states who were eager for any shelter from federal and state income taxes.

The growth was staggering. Industry-wide, money market fund assets surged from $1.7 billion in 1974 to $220 billion by 1982, growing from five percent to seventy-four percent of all U.S. mutual fund assets. Federated rode this wave better than almost anyone, and the reason was distribution. Starting in 1964, Fisher had pivoted the firm's strategy from retail door-to-door sales toward selling through brokers and institutional clients. The critical innovation was targeting bank trust departments. Banks had fiduciary accounts that needed cash management solutions. Rather than competing with banks, Federated became a supplier to them, offering money market funds as a more efficient alternative to banks managing cash internally. This was a stroke of strategic genius. It aligned Federated's interests with those of the very institutions that might otherwise have been competitors, and it created a sticky, relationship-driven distribution network that would prove remarkably durable.

By the early 1980s, Federated had become the second-largest mutual fund company in the United States, with nearly thirty billion dollars in assets under management. The growth attracted the attention of Aetna Life & Casualty, which in November 1982 acquired approximately eighty-seven percent of Federated for $210 million. At the time, Aetna was one of America's largest insurance companies, and the acquisition was meant to give it a foothold in the fast-growing mutual fund industry.

The Aetna years proved to be a way station, a period when Federated's founders learned firsthand the frustrations of operating within a large corporate parent. Chris Donahue, John's son, later described the company's willingness to operate under various ownership structures with the memorable phrase: "We'll wear any dress." In August 1989, Federated management executed a leveraged buyout, purchasing Aetna's majority stake for $345 million. Seven years later, they paid another $100 million to acquire Aetna's remaining twenty-five percent, completing the full repurchase. The total cost to regain independence was $445 million, a price the Donahue family was willing to pay for the freedom to run the business their way.

On May 14, 1998, Federated Investors went public again on the New York Stock Exchange under the ticker FII, with shares opening at approximately nineteen dollars. The IPO valued the company at approximately two billion dollars, a nearly tenfold return on the $210 million that Aetna had paid for its stake just sixteen years earlier. The Donahue family had taken the company private, managed it through a critical growth period, and then taken it public again on their own terms. It was a masterclass in ownership engineering.

But the IPO came with a critical governance feature: a dual-class share structure. The Donahue family retained all nine thousand shares of Class A common stock, which carried all voting power, in a Voting Shares Irrevocable Trust created in 1989. The publicly traded Class B shares, numbering over one hundred million, carried no voting rights whatsoever. This is one of the most extreme voting wedges in corporate America, and it would prove decisive in the crisis years ahead, enabling the kind of long-term, patient decision-making that public market pressure might otherwise have prevented.

By year-end 1998, Federated's assets under management had reached $111.6 billion. The Donahue family's governance model, rooted in what co-founder Fisher once described as wanting to "build a place where we could employ our children, a solid company there for the long haul," had created a platform poised for enormous growth. But it also created an overwhelming concentration risk: by the mid-2000s, money market funds and fixed-income products accounted for eighty-eight percent of all managed assets. The firm's future was inextricably tied to one product category. When that category nearly imploded in September 2008, the entire enterprise hung in the balance.

III. The Money Market Industrial Complex (1990s-2007)

By the mid-1990s, Federated had perfected a business model that was, in the words of one industry analyst, "boring but beautiful." The company manufactured money market funds and distributed them through a vast network of banks, broker-dealers, and institutional intermediaries. It was not trying to beat the S&P 500 or pick the next tech stock. It was managing cash, and it was doing so at a scale that generated enormous, predictable fee income.

The competitive landscape in money market funds was peculiar. Fidelity, Vanguard, and Schwab had massive money market businesses, but these were primarily retail-facing operations, attached to brokerage platforms where money market funds served as sweep accounts for idle cash. Federated took a different approach, operating as a wholesale provider. Its clients were not individual investors but the institutions that served individual investors: bank trust departments, corporate treasuries, government entities, and financial intermediaries. Think of it as the difference between selling bread at a bakery and supplying flour to every bakery in town.

This wholesale model had several advantages that compounded over time.

First, it insulated Federated from the bruising brand competition of the retail market. Fidelity and Vanguard spent billions on advertising and brand-building; Federated spent its money on relationship managers who called on institutional clients. The company did not need retail brand recognition because its clients were professionals, not consumers.

Second, it created significant switching costs. When a bank trust department integrates a money market fund into its cash management infrastructure, connecting it to accounting systems, automated sweeps, and reporting platforms, the operational complexity of switching providers creates real friction. This is not the same as an individual investor moving money from one brokerage to another with a few clicks. It is a complex institutional undertaking that most bank treasurers would rather avoid unless there is a compelling reason.

Third, the model generated scale economies: each additional dollar of assets in a money market fund added revenue at minimal incremental cost, since the same portfolio management team could manage fifty billion as easily as five hundred billion.

But the model had a fundamental vulnerability. Money market funds are, by design, commoditized products. They invest in short-term, high-quality securities like Treasury bills, commercial paper, and certificates of deposit, and aim to maintain a stable one-dollar net asset value. Think of it like selling bottled water: every bottle contains essentially the same liquid, and the only way to win is distribution, convenience, and price. There is very little room for product differentiation. When competitors offer essentially the same product, the only dimensions of competition are fees, distribution relationships, and operational reliability.

Fee compression was already visible by the late 1990s, and it would become a grinding, relentless force in the years ahead. The average expense ratio on money market funds dropped steadily decade after decade, squeezing the revenue that managers could extract from each dollar of assets. For a company like Federated, which depended on money markets for the vast majority of its revenue, this meant that standing still was actually going backward.

Federated's leadership recognized the concentration risk and made periodic efforts to diversify. The company pursued acquisitions to build out equity and fixed-income capabilities. It acquired the Kaufmann Funds franchise for growth equity, brought in MDT Advisers for quantitative strategies, and expanded its fixed-income offerings beyond money markets. But these efforts were modest relative to the core business. As Chris Donahue later acknowledged, by the time of the financial crisis, money market and fixed-income products still accounted for eighty-eight percent of all managed assets. The equity business was a small tail on a very large dog.

What kept Federated independent during the great wave of asset management consolidation in the 1990s and 2000s? The dual-class share structure was the most obvious factor. The Donahue family could not be forced into a sale, no matter what activist investors or strategic acquirers might propose. But there was also a cultural element. Pittsburgh is not New York. The cost of living is lower, employee turnover is lower, and there is a Midwestern sensibility about building things to last rather than flipping them for a quick profit. Federated's liquidity management team averaged twenty-five years of investment experience, a remarkable figure that reflected both the stability of the Pittsburgh labor market and a company culture that rewarded loyalty. In an industry where portfolio managers hop between firms every few years chasing the highest compensation package, Federated's retention was genuinely unusual.

By 2007, Federated managed approximately $340 billion in assets. The money market business was a cash machine, generating predictable fee revenue with operating margins that made peers envious. The company had survived the dot-com bust, the Enron scandal, and numerous other market disruptions without breaking stride. There was a quiet confidence, bordering on complacency, that money market funds were an indestructible franchise. After all, the product had never failed. In forty years of existence, no money market fund had ever "broken the buck," meaning no fund had ever allowed its net asset value to fall below one dollar. The track record was spotless, and investors had come to treat money market funds as functionally equivalent to bank deposits, only with better yields.

That assumption was about to be tested in the most dramatic fashion imaginable. And the company most exposed, most dependent, and most vulnerable when the test came was Federated Investors.

IV. The 2008 Financial Crisis: Existential Threat

Picture the trading floor of a money market fund manager on a Monday morning in mid-September. The screens are blinking, the phones are ringing, and the number that matters most, the net asset value, is supposed to read exactly $1.00. It always reads $1.00. That is the entire point.

On Monday, September 15, 2008, Lehman Brothers filed for bankruptcy. The following morning, the Reserve Primary Fund, one of the oldest money market funds in existence and the product that had helped launch the entire industry in 1971, announced that it had suffered losses on seven hundred million dollars of Lehman Brothers commercial paper. The fund's net asset value had fallen to ninety-seven cents per share. For the first time in history, a money market fund had broken the buck.

The psychological impact was instantaneous and devastating. Money market funds had been treated by millions of investors and thousands of institutions as effectively risk-free cash equivalents. The idea that you could lose money in a money market fund was, for most people, inconceivable. When the Reserve Primary Fund shattered that assumption, it triggered a panic that spread across the entire money market industry within hours. In the week following Lehman's bankruptcy, investors pulled approximately $439 billion from money market funds. This was not an orderly reallocation; it was a run, institutional in scale and velocity, that threatened to freeze the commercial paper market, the short-term lending market, and by extension the entire functioning of the global financial system.

The mechanics of the crisis were terrifyingly simple, and understanding them is essential to grasping why Federated faced existential risk. Money market funds were major buyers of commercial paper, the short-term IOUs that companies use to fund day-to-day operations like payroll and inventory. General Electric, for instance, relied on commercial paper to finance its massive operations. When money market funds experienced massive redemptions, they had to sell their holdings of commercial paper to raise cash. But in a panicked market, there were no buyers at reasonable prices.

The commercial paper market seized up. This was not an abstract financial plumbing problem. It meant that major corporations could not roll over their short-term borrowing. It meant the real economy was at risk of a sudden, catastrophic cash crunch. Companies that depended on commercial paper funding might not be able to make payroll. The entire short-term credit market, the lubricant that kept the real economy functioning day to day, was in danger of freezing solid.

Federated was in the crosshairs. With roughly seventy-five percent of its $340 billion in assets concentrated in money market funds, the company faced existential risk. If redemptions continued at the same pace, Federated would have been forced to sell portfolio holdings at fire-sale prices, potentially breaking the buck in its own funds. The company's entire business model, its reputation, its client relationships, everything built over five decades was at stake.

What happened over the next seventy-two hours was a combination of emergency action by Federated's leadership and extraordinary intervention by the federal government. Chris Donahue and his team made the decision to provide emergency capital support to Federated's money market funds, purchasing distressed securities from fund portfolios to prevent NAV declines. The company committed hundreds of millions of dollars in direct support to keep its funds above the one-dollar threshold. It was a bet-the-company decision: if the market continued to deteriorate, the capital commitment could have bankrupted the parent company. But the alternative, letting a Federated fund break the buck, would have destroyed the franchise permanently.

On September 19, 2008, three days after the Reserve Primary Fund broke the buck, the U.S. Treasury announced the Temporary Guarantee Program for Money Market Funds. The program effectively guaranteed the share price of any eligible money market fund that applied and paid a fee, covering ninety-three percent of assets in the market, equivalent to more than $3.2 trillion. It was, in essence, a federal backstop for the entire money market industry, acknowledging that these funds had become systemically important. The guarantee cost taxpayers nothing in the end. No claims were ever paid. But the program's existence was critical to stopping the run and restoring confidence.

The immediate crisis passed, but the damage lingered. Federated voluntarily began waiving fees starting in the fourth quarter of 2008 to keep fund yields at zero or above, a practice that would continue for years as the Federal Reserve slashed interest rates to near zero. In the first quarter of 2009 alone, Federated reported $9.7 million in fee waivers. By that point, the company derived seventy-one percent of its revenue from money market assets, a staggering concentration that now looked more like a liability than an asset.

Chris Donahue's leadership during the crisis earned grudging respect even from critics. He later acknowledged the severity of the moment with characteristic bluntness, comparing Federated's position to being "in a POW camp behind enemy lines, trying to survive." But he also pushed back fiercely against the narrative that money market funds had caused the crisis, arguing in congressional testimony, conference calls, and speeches that the exodus from money funds was a result, not a cause, of the broader meltdown. It was the only industry run in forty years, he noted, and the government recovery efforts cost taxpayers nothing.

The 2008 crisis fundamentally altered Federated's strategic calculus. Before September 2008, the firm could argue that its concentration in money markets was a feature, not a bug: a high-margin, stable franchise with decades of unbroken track record. After September 2008, the concentration was an undeniable vulnerability, and the regulatory response that followed would make it even more so.

There is a counterfactual worth considering. What if the Donahue family had not controlled every voting share? A publicly traded company with dispersed ownership, facing the kind of shareholder panic that Federated experienced in late 2008, might well have been pressured into a fire sale, a forced merger, or a hasty strategic capitulation. The dual-class structure, whatever its long-term governance concerns, provided the breathing room to make difficult, patient decisions during a moment of extreme pressure. The 2008 crisis may be the single strongest argument in favor of Federated's governance model.

For investors, the crisis revealed an uncomfortable truth about the money market business: it was a magnificent franchise in calm waters and a potentially fatal concentration in storms. The question was no longer whether Federated needed to diversify, but how fast and how radically it could do so before the next storm arrived.

V. Post-Crisis Reinvention: Regulatory Gauntlet (2009-2016)

If the 2008 crisis was a near-death experience, the regulatory aftermath was a slow-motion siege. For anyone who has ever survived an actual emergency only to face years of paperwork, audits, and new rules imposed by well-meaning authorities, the analogy is apt. The crisis lasted weeks. The regulatory response lasted years.

In the years following the financial crisis, the SEC embarked on a sustained campaign to reform money market funds, driven by the conviction that these products posed systemic risk and needed structural changes to prevent another run. The Financial Stability Oversight Council, created by Dodd-Frank, specifically identified money market funds as a potential source of systemic risk. For Federated, whose entire identity was built around money market funds, this was the equivalent of the government officially labeling your flagship product a danger to the financial system.

The first wave arrived in 2010, when the SEC tightened rules on portfolio quality, maturity, and liquidity. Money market funds were required to hold more liquid assets, shorten the average maturity of their portfolios, and improve disclosure. These changes were significant but manageable. The industry adapted.

The second wave was far more threatening. In 2014, the SEC adopted sweeping reforms that struck at the heart of the money market business model. The headline change was the requirement that institutional prime and municipal money market funds adopt a floating net asset value, abandoning the stable one-dollar NAV that had defined the product since its inception. Government money market funds and retail funds were exempted, but the floating NAV requirement for institutional prime funds was a fundamental alteration of the product's value proposition. Investors had treated money market funds as cash equivalents precisely because the NAV never moved. Force them to fluctuate, even by tiny amounts, and you eliminate the psychological certainty that made the product attractive.

The reforms also introduced redemption gates and liquidity fees, giving fund boards the ability to temporarily suspend redemptions or impose fees during periods of stress. To use a simple analogy: imagine if your bank told you that in times of financial stress, it might lock the doors for a few days or charge you a fee to withdraw your own money. That is essentially what gates and fees meant for money market fund investors.

The logic was to prevent the kind of panic run that had occurred in 2008 by giving funds tools to slow outflows. But from Federated's perspective, these provisions made the product less attractive to institutional investors who valued unlimited, same-day liquidity above all else. Corporate treasurers who relied on money market funds for daily cash management could not accept the risk that their cash might be temporarily inaccessible. The very feature designed to prevent panic could ironically trigger it, as sophisticated investors rushed to redeem before gates were imposed.

Chris Donahue's reaction was volcanic. He called the floating NAV proposal "totally brain dead" and characterized the choice between floating prices and capital buffers as deciding between death "by hanging or by bullet." Federated became the most vocal opponent of reform in the industry, contributing $230,000 to lobbying efforts in the first half of 2012 alone, part of $16 million in combined spending by the industry's ten largest managers. Donahue's family-controlled firm had three-quarters of its assets in money market funds, representing forty-seven percent of revenue, far more exposed than competitors like Fidelity at twenty-seven percent or JPMorgan at thirty-five percent. This was not an abstract policy debate for Federated. It was a fight for survival.

But the regulations passed anyway, with full implementation required by October 14, 2016. The impact was seismic. In the ten months leading up to the compliance date, more than $1.1 trillion flowed out of prime and municipal money market funds and into government money market funds, which retained the stable NAV. The share of industry assets in government funds surged from forty-one percent to seventy-six percent. Some fund managers simply converted their prime funds into government funds rather than deal with the floating NAV.

For Federated, this meant watching a significant portion of its most profitable assets migrate from higher-fee prime funds to lower-fee government funds. Government money market funds carry lower expense ratios because they invest exclusively in government securities, which are lower-yielding. The revenue per dollar of assets under management declined even as total assets shifted rather than departed entirely. It was a slow squeeze, compounded by the near-zero interest rate environment that the Federal Reserve maintained from late 2008 through late 2015, which forced Federated to continue waiving fees to keep fund yields from going negative. Industry-wide, advisers waived an estimated $35 billion in money market fund expenses between 2009 and 2015.

The combined effect of regulatory reform, rate environment, and fee pressure forced Federated into serious strategic soul-searching. The company had been talking about diversification for years, but the urgency was now acute. It accelerated acquisitions to build non-money-market capabilities, expanding in fixed income and equity strategies. In April 2012, it acquired Prime Rate Capital Management in London, a provider of institutional liquidity and fixed-income products, representing an early step toward international diversification. But these were incremental moves. By 2016, money market funds still accounted for the majority of managed assets and revenue. What Federated needed was not an incremental addition but a transformational leap, something that could fundamentally change the company's identity and competitive positioning. That something was waiting in London.

VI. The Hermes Acquisition: A Complete Transformation (2018)

By 2017, Federated's strategic predicament was clear. The company managed roughly $282 billion, with money market funds representing about fifty-six percent of total assets and an even larger share of revenue. Fixed-income and equity assets combined to just $75 billion. International assets accounted for a mere four percent of the total. Fee compression was relentless. The regulatory environment had permanently altered the economics of prime money market funds. And the rise of passive investing, led by Vanguard and BlackRock, was commoditizing the active equity and fixed-income businesses that Federated was trying to grow.

Three thousand miles away, in London, a very different kind of investment firm was building something remarkable.

Hermes Investment Management had been born in 1983 as PosTel Investment Management Limited, the investment arm of the Post Office Staff Superannuation Fund. In 1995, the trustees of the BT Pension Scheme, one of the UK's largest pension funds, purchased the Post Office scheme's holding and renamed the business Hermes. The BT Pension Scheme, with obligations to hundreds of thousands of current and former British Telecom employees, was one of the UK's largest defined benefit plans and took its stewardship obligations seriously.

Under the leadership of Saker Nusseibeh, who became CEO in November 2011, Hermes had evolved into a pioneer of responsible investing. Nusseibeh, who was later awarded a Commander of the Order of the British Empire (CBE) for his contributions to responsible investment, built the firm around a conviction that integrating environmental, social, and governance factors into investment decisions was not a concession to altruism but a pathway to superior long-term financial returns. He often argued that the traditional separation between "making money" and "doing good" was a false choice, that companies managed responsibly simply performed better over time.

Hermes' crown jewel was EOS, its Equity Ownership Services division, founded in 2004. EOS was not a traditional investment product. It was a stewardship service that provided constructive engagement with corporate boards and executives on ESG and strategic issues. Crucially, EOS was offered as a standalone service, meaning institutional investors could hire EOS for stewardship even if their money was managed elsewhere. This separation from investment mandates made EOS unique in the market and created a revenue stream that was independent of traditional AUM flows. By the time of the acquisition, EOS advised on billions in stewardship assets and had built deep, long-duration relationships with corporate boards, with nearly half its engagements lasting more than nine years.

In April 2018, Federated announced it had struck a deal to acquire a sixty percent interest in Hermes Fund Managers Limited from the BT Pension Scheme. The deal closed in July 2018 for GBP 259.9 million, approximately $342 million. This was a far more modest price than the $1.8 billion figure sometimes cited in media coverage. The BT Pension Scheme retained 29.5 percent, with 10.5 percent placed in an employee benefit trust. Three years later, in August 2021, Federated acquired the remaining 29.5 percent from BT Pension for GBP 116.5 million, approximately $161.5 million. The total cost of acquiring full ownership was roughly $500 million, a remarkably reasonable price for a platform that would fundamentally transform Federated's identity.

At the time of the deal, Hermes brought $47.2 billion in assets across sixteen differentiated strategies in high-active-share equities, credit, and private markets including real estate, infrastructure, private debt, and private equity. It served more than 550 clients. The strategic logic was compelling on multiple dimensions.

First, zero product overlap. Hermes and Federated had almost no competing strategies, meaning the acquisition was purely additive rather than requiring painful rationalization of redundant products. Second, complementary capabilities. Federated brought money market expertise, U.S. distribution, and scale in fixed income. Hermes brought ESG leadership, private markets capabilities, and European institutional relationships. Third, international diversification. Federated had been almost entirely U.S.-focused, with only four percent of assets from international clients. Hermes provided an immediate London presence and access to European and global institutional investors. Fourth, and most importantly, Hermes gave Federated something it could never have built organically: credibility in ESG and a stewardship platform that major institutional investors were increasingly demanding as a prerequisite for winning mandates.

The integration approach was unconventional and worth studying for anyone interested in how M&A can be done thoughtfully.

Rather than absorbing Hermes into Federated's Pittsburgh culture, the typical approach of an acquiring company, Chris Donahue pursued what observers described as a "reverse transformation." He adopted Hermes' ESG investment philosophy across the larger Federated organization rather than imposing Pittsburgh's more traditional approach on the London operation. This was a conscious choice that reflected Donahue's recognition that what Federated was buying was not just assets and revenue but a culture and philosophy that would be destroyed by heavy-handed integration.

More than ninety-five percent of the combined two thousand employees voluntarily signed Hermes' corporate pledge, a statement of commitment to acting ethically, responsibly, and with integrity. Donahue described the integration as combining "two successful business cultures" with "nonoverlapping investment strategies." The decision to let the smaller, acquired company's values reshape the larger acquirer was a rare act of institutional humility in an industry not known for modesty.

In February 2020, the transformation became visible to the outside world when Federated Investors changed its name to Federated Hermes and switched its NYSE ticker from FII to FHI. Later that year, the company renamed its mutual funds and other investment products to carry the Federated Hermes brand. It was an explicit signal: this was no longer just a money market company. It was a global responsible investing platform with Pittsburgh roots and London ambitions.

The timing of the name change proved inadvertently perfect. Within weeks, the COVID-19 pandemic would upend global markets, and companies with strong ESG practices would receive heightened attention from investors seeking resilience. The Federated Hermes brand landed in a world suddenly more receptive to the idea that how a company treated its stakeholders mattered as much as its quarterly earnings.

The implications for investors were significant. Federated had essentially purchased an entirely new identity. The Hermes acquisition diversified the company's revenue streams, expanded its geographic reach, provided exposure to secular growth trends in ESG, and gave it a genuine competitive differentiator in EOS that no amount of organic investment could have replicated. But it also created new tensions. Could a conservative, family-controlled Pittsburgh firm authentically embrace the progressive ESG agenda of a London-based stewardship pioneer? And as ESG became increasingly politicized in the United States, could Federated Hermes credibly straddle both worlds?

VII. The ESG Era & Modern Strategy (2019-Present)

The rebranding to Federated Hermes coincided with a global surge of interest in ESG investing. Institutional investors, particularly in Europe, were increasingly demanding that their asset managers demonstrate meaningful integration of environmental, social, and governance factors. Regulatory frameworks like the EU's Sustainable Finance Disclosure Regulation were pushing ESG from a voluntary nice-to-have to a compliance requirement. And the COVID-19 pandemic, which hit just weeks after the name change, only intensified the focus on corporate resilience, stakeholder management, and responsible business practices.

EOS rapidly emerged as the crown jewel of the combined enterprise. By the end of 2025, EOS advised on more than $2.3 trillion in stewardship assets, making it one of the largest dedicated stewardship platforms in the world. The service had grown from its initial focus on UK equities to a global team of more than sixty professionals representing sixteen nationalities and languages, engaging with approximately nine hundred unique issuers annually. The durability of these relationships, with nearly half of engagements lasting more than nine years, created a depth of institutional knowledge and corporate access that competitors could not easily replicate.

The business model had shifted in subtle but important ways. Federated Hermes was no longer simply a product manufacturer. Through EOS, it had become a thought leader and service provider in corporate governance and stewardship. This created a halo effect for the broader business. Institutional investors who hired EOS for stewardship were introduced to Federated Hermes' investment strategies. The London platform served as a gateway for non-U.S. client relationships. And the ESG integration philosophy, when applied authentically, became a differentiation point in consultant databases and request-for-proposal processes that increasingly screened for responsible investment credentials.

But the ESG strategy also created an uncomfortable tension. In the United States, a coordinated political backlash against ESG investing emerged in 2022 and intensified through 2025, led by Republican state treasurers and attorneys general who viewed ESG as a form of political activism incompatible with fiduciary duty. Federated Hermes found itself caught in the crossfire when reports surfaced that the company had been sponsoring the State Financial Officers Foundation, a Republican-affiliated group at the center of the anti-ESG movement, while simultaneously marketing itself as an ESG leader in Europe. A website called hermeshypocrisy.com was created to highlight the apparent contradiction. Federated Hermes eventually dropped the SFOF sponsorship under client pressure, but the episode illustrated the challenge of serving constituencies with fundamentally different views on ESG.

Chris Donahue addressed this tension directly. Speaking in November 2025, he noted that money managers retreating from sustainable investment pledges were "increasingly being turned away" when pitching to major European asset owners. His framing was pragmatic rather than ideological: ESG was a client requirement in Europe and a fiduciary consideration everywhere, regardless of the political noise in the United States. The company adopted a dual messaging strategy, leading with ESG credentials in Europe while framing the same practices as responsible fiduciary management in the U.S.

Meanwhile, the money market business experienced its own dramatic cycle that perfectly illustrated the franchise's simultaneous strength and vulnerability.

When COVID-19 hit in March 2020, there was an initial rush into money market funds as investors sought safety. Total industry money market assets surged above $5 trillion for the first time. But the Federal Reserve's emergency rate cuts to near zero simultaneously destroyed the economics of managing those assets. It was a cruel paradox: the money was flowing in, but the revenue per dollar was evaporating. Federated found itself in the surreal position of gathering record assets while earning less on each dollar than at any point in its history.

The Federal Reserve's emergency rate cuts to near zero in March 2020 forced another round of voluntary fee waivers. In the first quarter of 2022 alone, voluntary waivers totaled $75.8 million, partially offset by reduced distribution expenses but still a meaningful drag on profitability. Then, starting in March 2022, the Fed began the most aggressive tightening cycle in four decades, raising rates eleven times to 5.25-5.50 percent by July 2023. The impact on Federated Hermes was transformative. Fee waivers were eliminated entirely by early 2023. Money market yields became attractive again, drawing massive inflows from investors seeking safety and yield. Total money market assets surged from roughly $395 billion in 2021 to $560 billion in 2023 to $630 billion in 2024 and a record $682.6 billion by the end of 2025.

The company also continued to expand through acquisition. In 2022, it acquired C.W. Henderson & Associates, a Chicago-based municipal bond specialist. In 2025, it acquired Rivington Energy Management Limited, a London-based energy commodities trading firm, and agreed to acquire eighty percent of FCP Fund Manager, a Chevy Chase, Maryland-based real estate investment manager with $3.8 billion in assets. Perhaps most intriguingly, Federated Hermes moved aggressively into tokenized money market funds through a partnership with Archax, making tokens available on multiple blockchain platforms including Ethereum, Polygon, Solana, and others. Management indicated that potential stablecoin collateral demand could represent a trillion-dollar-plus opportunity if regulatory frameworks like the proposed GENIUS Act created a compliant structure for money market funds to serve as stablecoin backing.

The Donahue family governance question continued to loom. John Donahue, the patriarch and co-founder, had passed away in May 2017 at age ninety-two. Richard Fisher, the other co-founder, died in October 2018 at ninety-five, just months after the Hermes acquisition closed. The founding generation was gone, and the second generation was firmly in charge but aging. Chris Donahue has served as CEO since 1998, and his brother Thomas as CFO for the same duration. In December 2025, the company announced significant leadership transitions, with Paul Uhlman succeeding John B. Fisher (son of co-founder Richard Fisher) as President and CEO of Federated Advisory Companies effective April 30, 2026. R.J. Gallo was named incoming CIO for Global Fixed Income. These moves represented the most significant generational transition in the firm's history, though the Donahue family's control through the Voting Trust remained unchanged, with no publicly disclosed succession plan for the third generation.

VIII. Key Inflection Points That Changed Everything

Every company's history can be distilled to a handful of moments where the trajectory bends permanently. For Federated Hermes, four inflection points stand out, each fundamentally altering the company's strategic position, identity, and prospects.

The first was the 2008 financial crisis. Before September 2008, Federated could legitimately argue that its concentration in money market funds was a source of competitive strength. The product had a forty-year track record of stability. Distribution relationships were deep and sticky. Operating margins were enviable. When the Reserve Primary Fund broke the buck and triggered an industry-wide panic, that complacency was shattered in seventy-two hours. Federated's decision to inject capital into its funds saved the franchise but also revealed a fundamental vulnerability. The crisis forced management to confront a truth they had been able to avoid: a business built entirely on one product category is a business one crisis away from extinction. The diversification efforts that followed, slow at first and then accelerating dramatically with the Hermes acquisition, all trace back to the existential terror of September 2008.

The second inflection point was the 2014 SEC reforms and their October 2016 implementation. The floating NAV requirement for institutional prime funds was not just a regulatory change; it was the destruction of a product category's core value proposition. When more than $1.1 trillion shifted from prime funds to government funds in the months leading up to implementation, Federated watched its highest-margin money market assets migrate to lower-margin alternatives. The reforms did not kill the money market business, but they permanently impaired its economics and eliminated any remaining illusion that the old model could sustain the company indefinitely. This was the moment that made the search for "Plan B" urgent rather than theoretical.

The third was the Hermes acquisition in 2018. This was not an incremental deal. It was an identity transformation. From American regional money market specialist to global ESG and responsible investing platform. From a company that derived four percent of assets internationally to one with a genuine London presence and European client base. From a product manufacturer to a thought leader in corporate stewardship. The deal's total cost of roughly $500 million for a platform that now contributes substantially to revenue and has given Federated Hermes credibility in the fastest-growing segment of institutional asset management may prove to be one of the most astute acquisitions in the industry's history. Or it may prove to be a cultural overreach that leaves the company stuck between two worlds. The verdict is still being written.

The fourth inflection point was the 2020-2025 interest rate cycle, which served as both a stress test and a vindication of the money market franchise. The zero-rate environment from 2020 through early 2022 crushed money market fund profitability, forcing billions in fee waivers across the industry. For Federated, which had spent years building diversified revenue streams precisely to reduce money market dependence, this period validated the strategic urgency behind the Hermes acquisition. Without the London business contributing revenue and diversifying the income base, the zero-rate years would have been even more painful.

Then the Federal Reserve's aggressive tightening from March 2022 onward reversed the dynamic completely, making money market funds attractive to investors once more and eliminating fee waivers from Federated's income statement. Money market AUM surged to record levels. Earnings exploded. The company's stock price climbed to all-time highs.

This cycle demonstrated both the enduring power of the money market franchise when conditions are favorable and its extreme vulnerability when they are not. It is the central paradox of Federated Hermes: the money market business is simultaneously the company's greatest asset and its most dangerous dependency. For investors evaluating the stock, the interest rate environment remains the single most important external variable, overshadowing competitive dynamics, ESG trends, and management quality in its impact on near-term financial results.

There is a fifth inflection point forming now, though its resolution is uncertain: the growing divergence between ESG momentum in Europe and ESG backlash in the United States. Federated Hermes sits precisely on this fault line, with a business that depends on credibility in both markets. How the company navigates this polarization will determine whether the Hermes acquisition ultimately delivers on its transformative promise or becomes a source of strategic confusion and reputational risk.

IX. Business Model Deep Dive & Competitive Positioning

Federated Hermes today is essentially two businesses sharing a corporate umbrella, and understanding each is critical to evaluating the whole.

The first business is money market fund management. As of December 31, 2025, this segment accounted for $682.6 billion in assets, or seventy-six percent of total AUM. Of this, $508.4 billion was in money market mutual funds and $174.2 billion in separately managed accounts. Despite representing more than three-quarters of assets, money markets contributed roughly fifty-three percent of revenue, reflecting their lower fee rates compared to equity and alternative strategies. But money markets are exceptionally profitable on a margin basis. The same portfolio management team that manages fifty billion can manage five hundred billion with minimal incremental cost. Distribution expenses are lower than for equity products. And the sticky, institutional nature of the client relationships means that assets tend to stay, absent a crisis or dramatic rate shift.

The second business is what might be called "everything else": equity strategies ($97.9 billion), fixed income ($100.1 billion), and alternatives and private markets (roughly $22 billion), plus the EOS stewardship service advising on $2.3 trillion. These long-term asset classes contributed approximately forty-five percent of revenue but command higher fee rates. The equity business, which grew twenty-three percent in 2025 to nearly $98 billion, has been the most dynamic growth area, driven by strong performance in MDT quantitative strategies. In 2025, equity saw net positive sales of $4.6 billion, a dramatic reversal from net redemptions of $10.7 billion in 2024.

Revenue for full-year 2025 was approximately $1.8 billion, up ten percent from 2024. To put that in context, this represents a dramatic recovery from the fee-waiver-depressed years of 2020-2022. Net income hit $403.3 million, a fifty percent increase, with earnings per share of $5.13. The revenue increase was driven primarily by higher average money market and equity assets, plus contributions from performance fees and real estate development fees.

The operating leverage in the business model is striking. When money market assets grow and fee waivers are not required, each incremental dollar of assets flows almost entirely to the bottom line. The portfolio management infrastructure is already in place. The compliance systems are already running. The distribution relationships are already established. Revenue grows while costs grow minimally. This is why the rate environment matters so much to Federated Hermes: the difference between a zero-rate world and a five-percent-rate world is not linear but exponential in its impact on profitability.

The distribution architecture is a competitive strength. Federated Hermes reaches over eleven thousand institutions and intermediaries worldwide through three channels: U.S. financial intermediaries (sixty-three percent of AUM), U.S. institutional (twenty-eight percent), and international (nine percent). The intermediary channel, built over decades of relationship management starting with Richard Fisher's original bank trust department strategy, provides a distribution breadth that is extremely difficult to replicate.

Capital allocation has been consistently shareholder-friendly. The company pays a quarterly dividend of approximately thirty-one cents per share and is currently on its seventeenth share repurchase program. Buybacks have been aggressive and consistent: in the second quarter of 2025 alone, Federated Hermes repurchased over 1.5 million shares for $64.5 million. Over the years, the declining share count has been a meaningful contributor to earnings-per-share growth.

The dual-class structure creates a governance dynamic that cuts both ways. The Donahue family's absolute voting control through the Voting Trust enables long-term strategic decision-making free from activist pressure. The Hermes acquisition, which might have been blocked or delayed by short-term-oriented shareholders, was executed swiftly precisely because family control eliminated that friction. But the structure also means that public shareholders have no voice in governance, no ability to hold management accountable through proxy votes, and no protection against potential entrenchment or succession mismanagement. As Chris Donahue approaches his third decade as CEO with no publicly disclosed successor, this is a live concern.

The Pittsburgh cost advantage remains real. With the company's global headquarters and largest workforce in Pittsburgh, where compensation and real estate costs are significantly below New York, Boston, and London, Federated Hermes achieves operating margins in the twenty-eight to thirty-one percent range that are competitive with or superior to many competitors based in higher-cost cities. The London operation adds some cost, but the overall blended expense base benefits from Pittsburgh's economics.

In competitive terms, Federated Hermes is the sixth-largest money market fund manager in the United States, trailing Fidelity, JPMorgan, Vanguard, BlackRock, and Schwab, each of which manages money market assets ranging from roughly $686 billion (Schwab) to $1.6 trillion (Fidelity). Federated Hermes' money market mutual fund AUM of approximately $502 billion gives it a roughly six to seven percent market share.

What distinguishes Federated Hermes from the top five is structural. Those firms are massive, diversified financial conglomerates for whom money markets are one product among many, often functioning as a loss leader to attract clients into more profitable services. Fidelity uses money market funds as sweep vehicles for brokerage accounts. JPMorgan uses them as corporate treasury solutions tied to its commercial banking relationships. For these firms, money market profitability is secondary to the broader client relationship. Federated Hermes is the largest pure-play money market specialist, the company most exposed to and most dependent on this single product category. That concentration is simultaneously its greatest strength, because it means complete focus and operational excellence, and its greatest vulnerability, because it means existential exposure to any disruption of the money market business model.

X. Analyzing Federated Hermes Through Hamilton's 7 Powers

Hamilton Helmer's framework identifies seven sources of durable competitive advantage. Applying it to Federated Hermes reveals a company with moderate but real moats in specific niches, rather than the broad, deep advantages of a scale giant.

Scale economies are present in money market fund operations, where the marginal cost of managing an additional billion dollars is near zero. A portfolio manager overseeing a $500 billion money market fund does not need ten times the staff of one overseeing a $50 billion fund. The compliance infrastructure, the trading systems, the risk management frameworks, they all scale beautifully. But money market funds are also highly commoditized, meaning that scale translates more into profitability than into competitive insulation. Any large financial institution can launch a money market fund with adequate scale.

The real scale advantage lies in EOS stewardship, where the breadth of the client base and the depth of corporate engagements create an information and relationship advantage that improves with size.

Network effects are limited in traditional asset management but more meaningful in EOS. When multiple large institutional investors engage with the same corporate boards through EOS, the collective weight of their combined assets amplifies the effectiveness of engagement. A stewardship platform advising on $2.3 trillion carries significantly more influence with corporate management than one advising on $100 billion. This collaborative engagement model is a genuine, if modest, network effect.

Counter-positioning is perhaps the most interesting power in Federated Hermes' portfolio. The Hermes acquisition was a counter-positioning move against the passive giants. While BlackRock, Vanguard, and State Street were consolidating dominance in index funds and ETFs, Federated Hermes invested in deep ESG integration and active stewardship. This is a bet that there is a sustainable market for investment managers who actively engage with companies rather than simply tracking an index. If ESG remains a secular trend, this positioning will prove prescient. If ESG proves to be cyclical, the positioning becomes a liability.

Switching costs are moderate. In institutional mandates, the operational complexity of changing investment managers creates friction, particularly in money market funds where treasury operations are integrated with fund platforms. In sub-advisory relationships, where Federated Hermes manages money on behalf of other firms' products, switching costs are somewhat higher because of contractual and operational dependencies.

Branding is strong in money markets, where institutional trust is paramount. Federated has five decades of track record in managing cash safely. The Hermes brand carries weight in European ESG circles. But neither brand has the consumer recognition of Fidelity or BlackRock, and in asset management, institutional brand strength is necessary but rarely sufficient for pricing power.

Cornered resources include the EOS team and methodology, institutional relationships built over decades, and the deep money market operational expertise refined over fifty years. The EOS team's corporate relationships, built through years of sustained engagement, represent intellectual and relational capital that cannot be hired away by a competitor overnight.

Process power exists in Federated Hermes' money market operations, where decades of refinement have produced sophisticated risk management, portfolio construction, and compliance processes. Similarly, EOS has developed engagement playbooks and analytical frameworks that represent codified process knowledge.

The overall assessment is that Federated Hermes possesses moderate competitive powers concentrated in specific niches. It is not a fortress business like a toll road or a payments network. It does not enjoy the kind of structural advantages that allow BlackRock or Vanguard to virtually guarantee continued growth through the self-reinforcing dynamics of scale in passive investing. But it has genuine differentiation in money market operations, institutional distribution, and ESG stewardship that should protect it from the worst effects of industry commoditization, provided it continues to invest in these advantages.

The critical insight from the 7 Powers analysis is that EOS stewardship represents Federated Hermes' strongest competitive position: it combines elements of cornered resources (the team and relationships), network effects (the collaborative engagement model), and process power (the engagement methodology). If any single element of the Hermes acquisition justifies the entire deal, it is EOS. Investors should watch EOS asset growth as the leading indicator of whether this competitive advantage is strengthening or eroding.

XI. Porter's 5 Forces Analysis

The asset management industry is structurally challenging, and Federated Hermes operates at the intersection of several unfavorable forces.

Competitive rivalry is intense and growing. The passive revolution led by Vanguard and BlackRock has commoditized equity and fixed-income investing for a large and growing share of the market. To put the scale in perspective, passive strategies surpassed active strategies in total U.S. equity fund assets in 2019 and the gap has widened every year since. Active managers face relentless pressure to justify fees relative to index fund alternatives that charge a fraction of a basis point.

In money markets, the industry is dominated by a handful of enormous players, and differentiation is extremely limited. The top five money market fund managers control roughly eighty percent of the market. In ESG, what was once a relatively uncrowded space is now flooded with competitors, some with genuine commitment and many with superficial marketing overlays that amount to little more than relabeling existing strategies with green-sounding names.

Federated Hermes faces competition from every direction: passive giants in equity, massive banks in money markets, and proliferating ESG entrants in stewardship.

The threat of new entrants is moderate, but the nature of potential entrants is evolving. High regulatory barriers protect incumbents, and the cost of building institutional distribution relationships acts as a meaningful barrier. Launching a money market fund requires SEC registration, compliance infrastructure, and the operational plumbing to handle daily NAV calculations and redemption processing. These are not trivial undertakings.

But fintech platforms, robo-advisors, and cryptocurrency-based alternatives are changing the distribution landscape in ways that could lower barriers for tech-native entrants. The very tokenization opportunity that Federated Hermes is pursuing through its Archax partnership could also enable new competitors to enter the money market space through blockchain-based distribution channels that bypass traditional intermediaries entirely.

Bargaining power of suppliers is low. Talent is the key input in asset management, and while competition for top investment professionals is real, the talent market is large and liquid. Technology is increasingly commoditized. Data providers have some pricing power, but not enough to materially impact industry economics.

Bargaining power of buyers is high and rising. Institutional investors are increasingly sophisticated, fee-sensitive, and empowered by consultant intermediaries like Mercer, Cambridge Associates, and Callan who enforce standardized evaluation criteria and negotiate fees downward on behalf of their clients. The consultant layer adds a formidable intermediary between asset managers and their end clients, creating fee pressure that individual asset managers have very limited ability to resist.

Fee transparency regulations continue to increase pricing pressure. And in money markets, where the product is nearly identical across providers, buyers have enormous leverage. A corporate treasurer choosing between Federated Hermes' money market fund and JPMorgan's money market fund is making a decision based almost entirely on yield, operational integration, and fee levels, not on any meaningful product differentiation.

The threat of substitutes is high and growing. Passive index funds are the most obvious substitute for active equity management. ETFs are replacing mutual funds as the preferred wrapper. Private markets are attracting institutional capital that might otherwise flow to liquid alternatives. Direct indexing and separately managed accounts offer customization that mutual funds cannot match. In money markets specifically, Treasury Direct purchases, bank sweep accounts, and other cash management alternatives provide substitutes that bypass the fund structure entirely. The rise of fintech cash management platforms and even stablecoins represent newer substitutes that could eventually disintermediate traditional money market funds.

The industry assessment is stark: asset management is a structurally challenging business that rewards either massive scale or genuine differentiation. Companies caught in the middle, too small for scale advantages and too generic for differentiation, tend to be squeezed out or absorbed. Federated Hermes has chosen differentiation through money market expertise and ESG stewardship, a defensible strategy but one that requires constant reinvestment and cultural commitment to sustain. The open question is whether the differentiation is deep enough to protect against the relentless grinding forces of commoditization and fee compression that have already claimed dozens of mid-sized asset managers.

XII. Bear Case vs. Bull Case

Synthesizing the competitive analysis from both frameworks, the investment case for Federated Hermes comes down to a tension between proven resilience and structural headwinds. Here is how the bear and bull cases stack up.

The bear case begins with the structural decline in active management. The share of actively managed assets continues to erode in favor of passive strategies, and there is no evidence that this trend is reversing. Every dollar that moves from an actively managed fund to an index fund represents permanent fee compression for the industry. Federated Hermes' equity and fixed-income businesses are directly exposed to this pressure, and even its money market franchise is not immune as passive alternatives proliferate.

ESG backlash in the United States creates reputational and regulatory risk. The company's attempt to straddle both pro-ESG and anti-ESG constituencies, sponsoring conservative organizations while marketing ESG leadership, already blew up once with the SFOF controversy. Future political developments, including potential federal legislation restricting ESG considerations in fiduciary decision-making, could create real headwinds.

Money markets, despite their current resurgence under elevated rates, remain permanently impaired by decades of regulatory reform. The next financial crisis, whenever it comes, could trigger another round of reforms that further restrict the product's appeal. And a return to near-zero interest rates, which is entirely possible in a recessionary scenario, would reinstate fee waivers and compress earnings significantly. During the 2020-2022 zero-rate period, the impact was severe enough to make the money market business barely profitable on a net basis.

Scale disadvantage is real. Federated Hermes manages roughly $900 billion, impressive in absolute terms but dwarfed by BlackRock at $11 trillion, Vanguard at $9 trillion, and Fidelity at over $5 trillion. In an industry where scale drives down costs and broadens distribution, being the sixth-largest money market manager is a precarious position.

Family control raises governance concerns. The dual-class structure means that public shareholders are entirely dependent on the Donahue family's good judgment and good faith. With no disclosed succession plan and the CEO approaching three decades in office, the transition to the next generation of leadership is an unquantified risk that the market may not be pricing fully.

And there is the "stuck in the middle" risk. Federated Hermes is too small to compete with BlackRock, Vanguard, and Fidelity on scale and distribution breadth. But it is too large and institutionally complex to operate as a nimble boutique that can attract talent with entrepreneurial economics and outsized performance potential. The company occupies an uncomfortable middle ground that, in asset management, has historically been a difficult place to sustain.

The bull case rests on several foundations that deserve serious consideration. First, management has demonstrated resilience and adaptability through multiple existential crises. Surviving 2008, navigating the regulatory gauntlet, executing the Hermes acquisition, and capitalizing on the rate cycle are not the actions of a complacent management team. Second, the Hermes acquisition was strategically prescient. Despite short-term political headwinds, ESG integration is a long-term secular trend driven by institutional investor demand, regulatory requirements, and growing evidence of its relevance to long-term financial performance. Managers retreating from ESG are already losing European mandates, as Chris Donahue himself has publicly noted.

Third, EOS represents genuine differentiation. A stewardship platform advising on $2.3 trillion, with deep corporate relationships and a standalone service model, is nearly impossible for competitors to replicate quickly. The Big Three asset managers have large stewardship teams, but their engagement is tied to index fund holdings rather than offered as an independent service. EOS occupies a unique competitive niche.

Fourth, the money market franchise provides a stable, profitable base that generates substantial free cash flow in favorable rate environments. The current elevated-rate environment has pushed money market AUM to records and eliminated fee waivers, creating a period of exceptional profitability. Fifth, the Pittsburgh cost base provides a structural advantage in operating margins relative to competitors headquartered in New York or London. Sixth, the family control that creates governance risk also enables long-term thinking. The Donahue family's willingness to invest in Hermes, to accept short-term fee waivers to protect fund integrity, and to resist the temptation to sell during periods of weakness reflects a stewardship mentality that quarterly-focused management teams rarely exhibit.

For investors tracking Federated Hermes, two KPIs matter above all others. The first is organic money market fund flows, which measure whether assets are growing or shrinking independent of market returns and rate effects. This is the clearest indicator of competitive positioning in the core franchise. The second is long-term asset net flows, particularly in equity and alternatives, which measure the success of the diversification strategy. If equity and alternative assets are growing organically, the Hermes bet is paying off and the company is reducing its dependence on money markets. If they are shrinking, the diversification thesis is failing and the company remains a rate-dependent money market shop with an expensive London appendage.

XIII. Playbook: Lessons for Founders & Investors

The Federated Hermes story offers unusually clear lessons because the company's history spans so many phases of corporate life: founding, scaling, crisis, regulatory disruption, and strategic transformation. Each phase generated insights that apply well beyond asset management.

On surviving disruption: the most dangerous moment for any company is when its core business is threatened but still profitable enough to resist change. This is what Clay Christensen called "the innovator's dilemma," though in Federated's case the disruption came from regulation and market structure rather than technology. Federated's money market franchise was throwing off enormous cash flows even as regulatory reform and fee compression were slowly undermining its long-term viability.

The temptation to milk the cash cow while avoiding the risks of transformation is powerful. Many companies in similar positions have done exactly that, distributing every dollar of cash flow to shareholders while the core business slowly eroded until there was nothing left to transform. Kodak, Sears, and Blockbuster are the canonical examples. Federated's leadership deserves credit for acting before the crisis became terminal, even if the pace of change was sometimes slower than ideal. The lesson is that the time to reinvent is when you can still afford to, not when you are forced to.

On M&A as identity transformation: most acquisitions in asset management are bolt-on deals that add incremental capabilities without fundamentally changing what the acquirer is. Buy a small equity boutique, add it to the product lineup, cross-sell to existing clients. The Hermes deal was something far more ambitious. It was an attempt to change what Federated fundamentally was. This required courage, both to pay a significant price for a business with a different culture in a different country and to accept the risks of combining two organizations with very different identities and worldviews.

The decision to pursue a "reverse transformation," letting the acquired company's philosophy influence the acquirer rather than the other way around, was unconventional and, based on the evidence so far, strategically sound. Most acquiring companies impose their culture on the target. Federated did the opposite. Whether that reflects genuine strategic wisdom or simply the pragmatic recognition that ESG was where the growth was coming from, the result has been an integration that appears to have preserved the intellectual capital and cultural distinctiveness that made Hermes valuable in the first place.

On competitive moats in commoditizing industries: when products become commoditized, the only sustainable advantages are distribution relationships, operational excellence, and unique services that competitors cannot easily replicate. Warren Buffett once described a good business as one surrounded by a deep, wide moat. In commoditizing industries like asset management, the moats tend to be shallow and narrow, easily crossed by determined competitors.

Federated's sixty-year-old distribution network through banks and broker-dealers, its refined money market operations, and EOS's stewardship platform each represent a different type of moat. None is impregnable, but together they create a multi-layered defense that has proven more durable than many analysts expected. The lesson for founders in any commoditizing industry: if you cannot build one deep moat, build several shallow ones and maintain them religiously.

On governance and family control: the Federated Hermes story illustrates both the benefits and risks of dual-class structures. The benefits are real: long-term orientation, decisive action in crises, and freedom from activist pressure that might force premature strategic changes. The 2008 response, the Hermes acquisition, and the willingness to accept years of fee waivers all reflect the kind of patient, stewardship-oriented thinking that family control enables. But the risks are equally real: potential entrenchment, opacity in succession planning, and the absence of accountability mechanisms that protect public shareholders. The lesson is not that dual-class structures are good or bad but that they require responsible controlling shareholders who earn their privilege through performance and transparency.

On crisis management: Federated's response to the 2008 panic, injecting hundreds of millions in capital support to prevent its funds from breaking the buck, was a bet-the-company decision that preserved the franchise. The alternative, allowing a fund to break the buck and dealing with the consequences, would have been catastrophic. Protecting reputation is always more expensive than it seems in the moment and always worth more than it appears in retrospect. In industries built on trust, reputation is the most valuable asset on the balance sheet, even though it never appears there.

On geographic positioning: Pittsburgh provided real advantages in cost structure, employee retention, and cultural stability. But it also created limitations in attracting certain types of talent, particularly in technology and quantitative investment management. The lesson is to know your trade-offs. Every location choice involves a set of advantages and disadvantages, and the key is to maximize the advantages while actively mitigating the disadvantages rather than pretending they do not exist.

On industry structure: asset management is a brutal business that rewards either massive scale or genuine differentiation. The middle ground, too small to compete on cost and too large to be a boutique, is the most dangerous place to be. Federated Hermes has navigated this challenge by combining scale in money markets with differentiation in ESG stewardship. Whether this combination is sustainable over the next decade will be the ultimate test of the company's strategy.