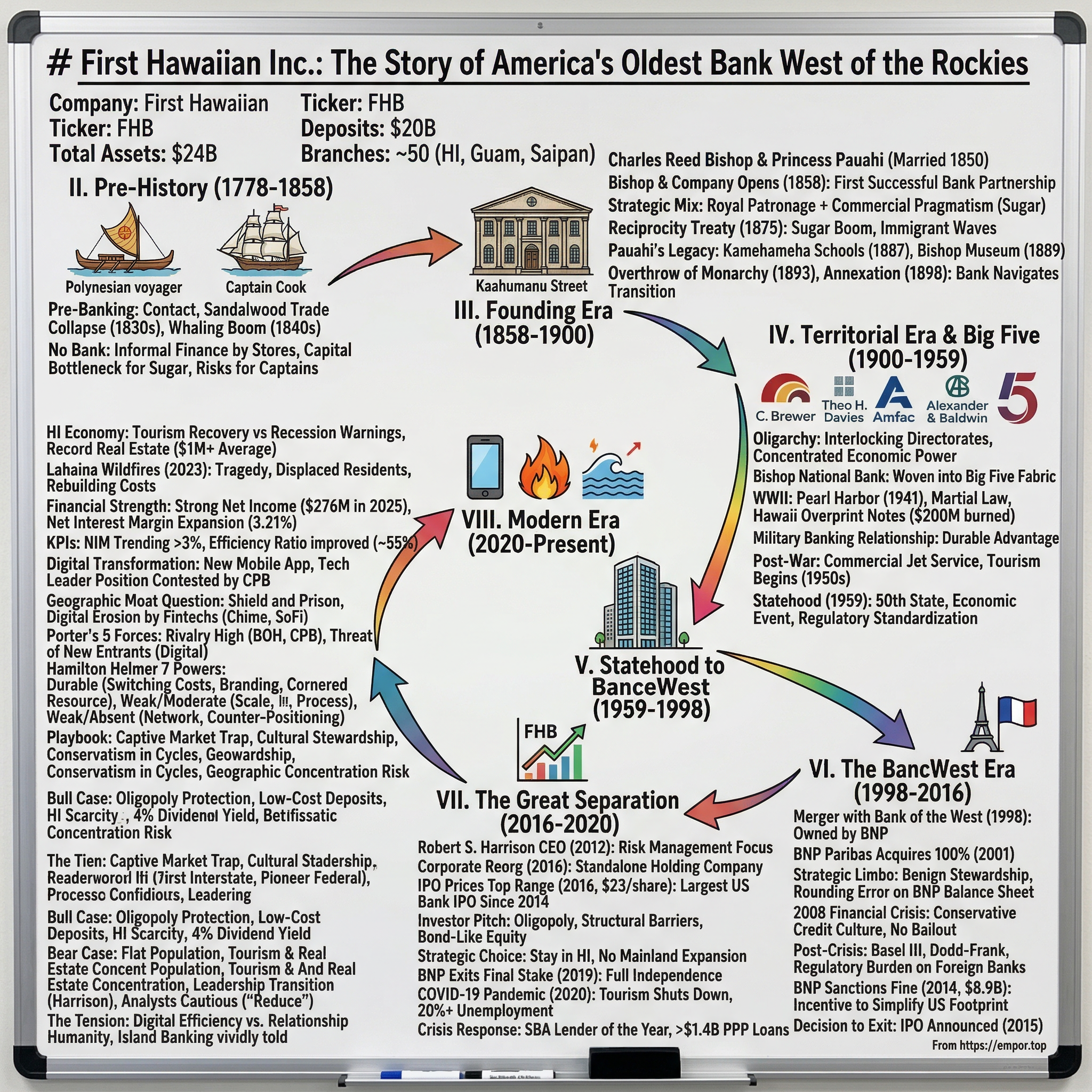

First Hawaiian Inc.: The Story of America's Oldest Bank West of the Rockies

I. Introduction and Episode Roadmap

Picture a bank that opened its doors before the American Civil War, in a kingdom ruled by Polynesian royalty, on a chain of volcanic islands two thousand miles from the nearest continent. That bank is still there. It is still the largest financial institution on those islands. It has survived the overthrow of a monarchy, two world wars, martial law, a Japanese real estate invasion, a French corporate parent, a global pandemic that shut down its primary industry overnight, and the slow digital erosion of everything that once made island banking a fortress. Its ticker is FHB. Its name is First Hawaiian. And its story is one of the most remarkable in American finance.

First Hawaiian Inc. sits on roughly twenty-four billion dollars in assets, making it Hawaii's largest bank by that measure. It holds over twenty billion in deposits, operates about fifty branches across the Hawaiian Islands, Guam, and Saipan, and has been publicly traded on the NASDAQ since 2016. But those numbers only scratch the surface. What makes First Hawaiian extraordinary is not its size but its longevity, its peculiar competitive position, and the central question it forces every investor to confront: what happens when your moat is an ocean?

This is a story about captive markets and whether they stay captive. It is about cultural stewardship as a business strategy, about how a bank founded by Hawaiian royalty navigated colonization, statehood, foreign ownership, and independence. It is about the economics of geographic isolation, the tension between being protected by remoteness and imprisoned by it, and whether any of that matters when a twenty-two-year-old in Honolulu can open a Chime account on their phone.

The themes that run through First Hawaiian's history are the themes that define regional banking everywhere, just amplified by the Pacific Ocean: concentration risk, regulatory moats, the cost of being small, and the question of whether relationship banking can survive the internet age. But Hawaii adds dimensions that no mainland bank can replicate. The military. The tourism economy. The finite supply of land. The cultural weight of a name that stretches back to the days of King Kamehameha. Understanding First Hawaiian means understanding all of it, and that is what makes this story worth telling.

Think of it this way: if you wanted to design a natural experiment in geographic competitive advantage, you could not do better than Hawaii. An isolated archipelago with a finite population, a tourism-dependent economy, a handful of banks, and an ocean that serves as both shield and prison. Every strategic concept in banking, from deposit franchise value to switching costs to digital disruption, plays out in high definition on these islands. First Hawaiian is not just a bank. It is a case study in what happens when defensibility meets limitation, and the stakes have never been higher.

II. Pre-History: Hawaii Before Banking (1778-1858)

Long before anyone needed a bank in Hawaii, there was the ocean. For roughly a thousand years, Polynesian voyagers had settled the Hawaiian archipelago, building a sophisticated society governed by the kapu system and ruled by ali'i, or chiefs. The islands were self-sufficient, isolated, and unknown to the Western world until January 1778, when Captain James Cook's ships appeared off the coast of Kauai. That moment changed everything.

What Cook found was not a primitive backwater. It was a complex civilization with agriculture, aquaculture, and a social hierarchy as rigid as anything in feudal Europe. But what Cook brought was contact, and contact brought commerce. Within decades, Hawaii became a critical waypoint in the Pacific. First came the sandalwood trade. Hawaiian forests contained vast stands of sandalwood, prized in China, and Hawaiian chiefs, eager for Western goods, began trading it aggressively. By the 1830s, the forests were largely stripped. The trade collapsed, but the pattern was set: Hawaii's economy would be driven by whatever the outside world wanted from it.

Then came the whales. By the 1840s, Honolulu and Lahaina had become the primary provisioning ports for the Pacific whaling fleet. At its peak, over five hundred whaling ships called on Hawaii annually. Sailors needed supplies, repairs, entertainment, and somewhere to keep their money. Merchants set up shop. The rudiments of a commercial economy took shape. But there was no bank. General merchandise stores handled basic financial functions: holding deposits, extending credit, exchanging currencies. It was informal, unreliable, and insufficient for the scale of commerce that was developing.

Consider the predicament from a ship captain's perspective. You arrive in Honolulu with months' worth of whale oil proceeds. You need to pay your crew, purchase provisions, and send money back to your family in New Bedford, Massachusetts. Your options are to hand your cash to a shopkeeper who might or might not be solvent next month, or carry it on your person through the roughest port in the Pacific. Neither option is attractive. For sugar planters, the problem was even more acute. Sugar cultivation required enormous upfront capital, months before any revenue, and repayment depended on commodity prices set in New York and London. The absence of a proper bank was not just an inconvenience. It was a structural bottleneck on economic growth.

Meanwhile, a parallel transformation was underway. American missionaries had arrived in 1820, and their descendants were discovering that sugar grew extraordinarily well in Hawaiian soil. The sugar industry was capital-intensive: you needed land, labor, irrigation, mills, and shipping. You needed credit. You needed a real financial institution. And the man who would build one was already on his way.

King Kamehameha the Great had unified the Hawaiian Islands by 1810, creating a single kingdom that would persist until 1893. By the 1850s, his successors presided over a nation increasingly entangled with Western commerce. The whaling economy was peaking, the sugar industry was stirring, and Honolulu was evolving from a dusty port town into something that resembled a small commercial city. The peculiar challenge of building financial infrastructure in an isolated island kingdom cannot be overstated. There was no Federal Reserve, no FDIC, no regulatory framework. Currency circulated in a chaotic mix of American, British, and Spanish coins. Interest rates were whatever the lender decided. Credit was based on personal reputation and social standing, not standardized underwriting. Every transaction carried counterparty risk that mainland merchants, with their established banking networks, had long since mitigated. Hawaii needed a real bank. What it got was Charles Reed Bishop.

III. Founding Era: Charles Reed Bishop and Queen Emma (1858-1900)

Charles Reed Bishop was born in 1822 in Glens Falls, New York, the kind of small-town upstate boy who might have spent his life running a general store. Instead, he became one of the most consequential figures in Hawaiian history. His formal education ended after eighth grade at Glens Falls Academy, but he had learned the fundamentals of commerce: clerking, bartering, bookkeeping, and inventorying. In 1846, at twenty-four, Bishop and a friend named William Little Lee set sail for Oregon, where Bishop planned to survey land. They stopped in Honolulu to resupply. He never left.

Bishop found work immediately, first at Ladd and Company, a mercantile firm, and then at the U.S. Consulate. He became a Hawaiian citizen in 1849. And in 1850, he married Princess Bernice Pauahi Paki, the great-granddaughter of Kamehameha the Great. The ceremony was private, at the Royal School, because her parents disapproved. A New York farm boy marrying into Hawaiian royalty was not what they had envisioned. But within a year, her father relented and invited the couple to live on the family estate. The marriage gave Bishop something no amount of business acumen could have provided: a place at the very center of Hawaiian society.

Bishop served five successive Hawaiian monarchs over three decades. He was Collector General of Customs, a member of the House of Nobles, a member of the Privy Council for over thirty years, Minister of Foreign Affairs, and President of the Board of Education. He was simultaneously a trusted royal advisor and a shrewd commercial operator, navigating between Western commercial interests and Hawaiian sovereignty with a pragmatism that would define the institution he built.

On August 17, 1858, Bishop combined those identities by opening Bishop and Company in a basement room on Kaahumanu Street in Honolulu, in partnership with William A. Aldrich. On its first day, the bank took in four thousand, seven hundred eighty-four dollars and twenty-five cents in deposits. It was the first successful banking partnership chartered under the laws of the Kingdom of Hawaii, and only the second bank west of the Rocky Mountains.

The timing was deliberate. The whaling industry was at its zenith, and Honolulu was the Pacific's banking desert. Every whaling captain, every merchant, every sugar planter needed a reliable place to store money, make payments, and borrow capital. Bishop saw the gap and filled it.

But his real genius was positioning the bank at the intersection of two worlds: the Hawaiian monarchy and the emerging commercial oligarchy. Bishop and Company served the royal family and the sugar barons simultaneously. This dual identity, royal patronage combined with commercial pragmatism, gave the bank an unassailable position in Hawaiian society. It was too connected to the throne to be dismissed by the traditional elite, and too commercially capable to be ignored by the rising business class.

As the sugar industry exploded after the Reciprocity Treaty of 1875 allowed Hawaiian sugar duty-free entry into the United States, the bank grew with it.

The sugar boom transformed Hawaii in ways that still echo through the islands' economic structure today. It brought waves of immigrant labor from China, Japan, Portugal, and the Philippines, creating the multiethnic society that defines modern Hawaii. It created enormous wealth for the plantation owners and their agents, the firms that would become known as the Big Five. And it created enormous demand for banking services: payroll for thousands of field workers, letters of credit for shipping sugar to San Francisco, loans for new mill equipment, mortgages for plantation managers' homes. Bishop and Company was there for all of it, financing plantations, handling payrolls, facilitating international trade. Bishop himself invested in sugar operations and co-founded the Hawaiian Agricultural Company. His partner William Aldrich handled day-to-day banking while Bishop divided his time between commercial affairs and his growing role in the Hawaiian government. By the 1870s, the bank had outgrown its basement and moved to larger quarters, reflecting an economy that was doubling in complexity with each decade.

Princess Pauahi died in 1884, leaving approximately 375,000 acres, roughly nine percent of Hawaii's total land area, in trust to educate Hawaiian children. Bishop, as one of five trustees, used his own fortune to build the initial campus of the Kamehameha Schools in 1887, because the estate was land-rich but cash-poor. He also founded the Bishop Museum in 1889 to house his wife's collection of Hawaiian artifacts and royal family heirlooms. The museum has since grown to hold millions of objects and documents about Hawaiian and Pacific Island cultures, and remains one of the most important cultural institutions in the Pacific.

In 1895, having sold the bank to his longtime associate Samuel Mills Damon, who had worked at Bishop and Company since 1871 and become a full partner by 1881, Bishop retired to San Francisco. He became Vice-President of the Bank of California and continued his philanthropic work from the mainland. He died in 1915 at ninety-three. His ashes were returned to Hawaii and placed in the vault of the Kamehameha family. A stone monument to him carries the inscription: "Builder of the State, Friend of Youth, Benefactor of Hawaii."

The overthrow of the Hawaiian monarchy in 1893 was engineered by a group of American businessmen, many of them descendants of missionaries, with the tacit backing of U.S. Marines stationed nearby. Queen Liliuokalani, who had attempted to restore sovereign authority through a new constitution, was deposed and eventually placed under house arrest in Iolani Palace. Bishop, though connected to the royal family through marriage, had retired from active government service by this point. His sympathies were reportedly divided: loyal to the Hawaiian people through his wife's legacy, yet pragmatically aligned with the commercial interests that benefited from American annexation.

By the time the Republic of Hawaii gave way to U.S. territorial status in 1898, Bishop and Company was thoroughly established. The bank had navigated the transition from a whaling economy to a sugar economy, from a kingdom to a provisional government to a republic. The founding era established a template that would define First Hawaiian for the next century and a half: serve whoever holds power, maintain conservative credit standards, invest in the community, and never forget that the islands are both your fortress and your boundary. The bank would now have to navigate something bigger: the total dominance of the Big Five.

IV. Territorial Era and the Big Five Dominance (1900-1959)

When Hawaii became a U.S. territory in 1900, the islands were not so much governed as managed, and the managers were five companies: C. Brewer, Theo H. Davies, Amfac (formerly H. Hackfeld), Castle and Cooke, and Alexander and Baldwin. Originally trading houses, these firms had evolved into sugar factors, financing, managing, and marketing for the plantations. By 1920, the Big Five controlled ninety-four percent of Hawaii's sugar crop.

Their power extended through interlocking directorates into shipping, utilities, railroads, wholesale, retail, and banking. Executives sat on each other's boards in a web of mutual interest that would be illegal under modern corporate governance standards. The Republican Party, closely aligned with the Big Five, dominated the territorial government. It was, by any honest accounting, an oligarchy, and a remarkably durable one.

Bishop and Company, which became Bishop National Bank and eventually changed its name several more times, was woven into this fabric. The bank financed Big Five companies including Amfac and Castle and Cooke. The social connections, shared board seats, and mutual interests that characterized the Hawaiian elite ran through its boardroom. This was not unusual for the era; mainland banks in the Gilded Age had similar interconnections. What was unusual was the degree of concentration. In a territory with a population under half a million, isolated by thousands of miles of ocean, economic power was extraordinarily concentrated. There was nowhere to hide and nowhere to go. The bank that served the powerful was itself powerful, and the cycle was self-reinforcing.

Then came December 7, 1941. The Japanese attack on Pearl Harbor transformed Hawaii overnight. Governor Poindexter ceded administrative powers to the U.S. Army. Martial law was declared, habeas corpus suspended, and the military took control of labor, wages, and prices. Hawaii would remain under martial rule for nearly three years, longer than any other part of the United States during the war. The federal government shuttered Japanese-owned banks, including the Sumitomo and Yokohama Specie Bank, reducing the number of operating institutions and concentrating activity at the remaining banks.

One of the war's most dramatic financial measures was the introduction of Hawaii Overprint Notes: special U.S. currency stamped with "HAWAII" on both sides. Residents were forced to exchange regular dollars for these marked notes and prohibited from holding more than two hundred dollars per person, or five hundred per business. Two hundred million dollars in unstamped currency was incinerated. The Treasury ultimately issued sixty-five million overprint notes with a face value of four hundred million dollars. The logic was grimly practical: if Japan captured Hawaii, the overprint currency could be declared worthless instantly, denying the enemy the use of American money.

Bishop National Bank was extraordinarily busy during the war years. The massive influx of defense personnel and Pearl Harbor naval crews created overwhelming demand for banking services. Employee Jimmy Yee later recalled: the bank would close at two or three in the afternoon, spend a couple of hours balancing the books, then reopen to serve the overflow. Despite what the bank later called "temporary setbacks," it remained fundamentally sound.

The war years also established a relationship that would become one of First Hawaiian's most durable competitive advantages: the military banking relationship. With Pearl Harbor as the headquarters of the Pacific Fleet, and with military installations spanning multiple islands, Hawaii's banks became deeply embedded in the financial lives of military personnel and their families. Servicemembers needed checking accounts, savings accounts, car loans, and mortgages. Military contractors needed commercial banking services. The federal government itself needed a local banking partner. This relationship, forged under the extraordinary pressures of wartime, would outlast the war by eight decades and counting. It demonstrated something that would prove true repeatedly: in crisis, Hawaii's banks became more essential, not less.

After the war, returning servicemen who had been stationed in Hawaii spread word of the islands' beauty, and tourism began its long ascent. The 1950s brought commercial jet service, making Hawaii accessible to the American middle class for the first time. Pan American World Airways and United Airlines began regular service to Honolulu, and what had been a five-day sea voyage became a five-hour flight. Moderately priced hotels rose along Waikiki Beach, including the SurfRider and Princess Kaiulani, opening the islands beyond the wealthy elite who had previously monopolized Hawaiian vacations. By the late 1950s, visitor counts were climbing to new highs each year, and the economic base was shifting from sugar to tourism.

New banks formed to serve the growing economy. Central Pacific Bank was founded in 1954 by Japanese American war veterans, many of whom had served in the legendary 442nd Regimental Combat Team. It was an institution born of both opportunity and grievance: Japanese Americans had been excluded from the Big Five power structure, and a bank of their own represented economic self-determination. City Bank of Honolulu followed in 1959. The banking market was diversifying, reflecting broader changes in Hawaiian society as the Big Five's grip loosened and new communities gained economic power.

Hawaii's admission as the fiftieth state on August 21, 1959, was an economic event as much as a political one. Statehood brought full participation in federal programs, regulatory standardization, access to mainland capital markets, and a psychological boost that accelerated the tourism boom. It also attracted the attention of mainland financial institutions, which began eyeing Hawaii's banking market for the first time. The islands were no longer a remote territory; they were part of America, and American banks wanted in. For the bank that would soon call itself First Hawaiian, statehood meant a new era of growth, and a new kind of competition.

V. Statehood to BancWest: Independence and Identity (1959-1998)

The year Hawaii became a state, the bank was still called Bishop National Bank of Hawaii. By 1960, it had become First National Bank of Hawaii, shedding the Bishop name after more than a century. By 1969, it became First Hawaiian Bank, the name it carries today, with the marketing tagline "the bank that says yes." The name changes were not cosmetic. They signaled a deliberate evolution from a Big Five-era institution to a modern, independent bank trying to ride the statehood boom.

And what a boom it was. The jet age brought tourists by the hundreds of thousands, then millions. Hotels, condominiums, shopping centers, and roads needed financing. First Hawaiian was there for the construction loans, the commercial mortgages, the small business lines of credit. When Hawaii National Bank opened in 1960 and captured six point three million dollars in deposits on its first day, a national record, it confirmed what everyone already knew: Hawaii's banking market was growing fast enough to attract serious competition.

In the early 1960s, First Hawaiian built what was described as the first major high-rise on the Honolulu skyline, a new headquarters that was both functional and symbolic. The bank was no longer the basement operation Charles Reed Bishop had founded. It was the financial center of a new American state. But the competitive dynamics were changing. Bank of Hawaii, First Hawaiian's primary rival since the nineteenth century, was pursuing a different strategy, gravitating toward securities investments and consumer-focused banking. First Hawaiian built a significantly larger commercial loan portfolio, eventually reaching roughly 2.3 billion compared to Bank of Hawaii's 537 million by modern metrics. The two banks were not so much fighting over the same customers as staking out complementary positions in a market large enough for both but too small for many more.

This structural duopoly, with smaller players filling the gaps, would prove remarkably durable. Decades later, analysts would still describe Hawaii's banking market using the same language: two dominant institutions, each with distinct strengths, coexisting in a geography that rewarded incumbency and punished overreach.

John D. Bellinger became chief executive in 1969, at age forty-five the youngest president in the bank's history. Over the next twenty years, he transformed First Hawaiian from a traditional island bank into a modern financial institution. Bellinger was a modernizer who understood that technology was coming to banking whether bankers liked it or not.

Under his leadership, the bank introduced full-service ATMs, telephone banking, debit cards, and the first locally available variable-rate consumer loans. He acquired a financial services company in 1975, renamed it First Hawaiian Creditcorp, and broadened the bank's consumer and commercial credit operations. These were not revolutionary moves by mainland standards, but in an island banking market that prized tradition and personal relationships, each represented a meaningful step toward a more scalable, technology-enabled business model.

By the late 1980s, the bank was generating over four hundred million dollars annually in interest income and more than forty million in fee income, with net income reaching fifty-seven million in 1989. Then Bellinger died, after thirty years of service, and the bank needed new leadership at exactly the wrong moment.

The wrong moment was the Japanese investment bubble, and understanding it is essential to understanding both Hawaii's economy and First Hawaiian's risk profile. Between 1985 and 1995, Japanese investors poured no less than twelve billion dollars into Hawaii, compared to just 850 million in the preceding decade. The peak year was 1989, when net Japanese investment reached nearly five billion dollars. To put that in perspective, five billion dollars of foreign investment flowing into a state with a GDP of roughly thirty billion was the equivalent of a firehose pointed at a bathtub. Japanese buyers offered cash on the spot for residential properties, bidding up prices in a market where supply was already constrained by island geography. They acquired two-thirds of all upscale hotel rooms. The average housing resale price approached three hundred twenty thousand dollars at its 1990 peak, staggering for a state that already had among the highest housing costs in America. First Hawaiian benefited enormously: deposits surged, loan demand soared, fee income climbed.

The Japanese money also exposed a structural vulnerability that investors should understand. Hawaii's economy is, and always has been, a leveraged bet on external demand. In the nineteenth century, that demand was for sugar. In the twentieth century, it was for tourism and real estate. When the source of demand shifts or collapses, the effects cascade through every sector simultaneously: fewer tourists means lower hotel occupancy, which means lower commercial real estate values, which means impaired bank loans, which means tighter credit, which means less construction and fewer jobs, which means more residents leave, which means lower deposit balances. It is a vicious cycle that geography makes worse because there is no adjacent economy to absorb the shock.

Then Japan's bubble burst, and the vicious cycle played out in textbook fashion. Tourism declined as Japanese visitors stopped coming. Hotel vacancy rates soared on the Neighbor Islands, revealing the full extent of resort over-investment. The Gulf War depressed mainland travel. Hurricane Iniki struck Kauai in 1992 as one of the most powerful hurricanes in Hawaiian history, adding physical destruction to economic distress. First Hawaiian's nonperforming assets doubled in 1992 to over seventy million dollars. Net income, which had peaked at eighty-seven million in 1992, fell to eighty-two million in 1993. Hawaii entered what residents would later call "the lost decade," a period of economic stagnation that persisted well into the late 1990s.

The board selected Walter A. Dods Jr., a twenty-year company veteran then aged fifty, to succeed Bellinger. Dods would become one of the most powerful business figures in Hawaiian history, and his leadership style was the polar opposite of Bellinger's careful incrementalism. Where Bellinger built, Dods bought.

Dods restructured management into five independent divisions, each under strong independent leadership, decentralizing what had been a more top-down operation. And he went on an acquisition spree, buying weakened competitors at favorable prices during the downturn: First Interstate of Hawaii (nine hundred million in assets, twenty branches) in 1991, Pioneer Federal Savings Bank (six hundred fifty million in assets, nineteen branches) in 1993, and Phoenix Financial Services for mortgage capabilities in the same year. He also picked up mainland branches from U.S. Bancorp in 1996. By 1994, the holding company controlled seven point three billion in assets across approximately ninety branches. In April 1992, Business Week ranked First Hawaiian the tenth safest lender in the nation, a testament to the credit culture Dods had inherited and maintained even as he expanded aggressively.

In 1996, at the nadir of Hawaii's economic doldrums, Dods completed the First Hawaiian Center, a one hundred seventy-five million dollar, thirty-story headquarters standing at 428 feet, the tallest building in Honolulu. It was a statement of confidence that bordered on defiance. Business Week had ranked First Hawaiian the tenth safest lender in the nation in 1992, and Dods intended to keep it that way even as the islands struggled.

Through the 1990s downturn, First Hawaiian demonstrated a pattern that would repeat itself: conservative underwriting during booms, opportunistic expansion during busts, and the patient cultivation of relationships that transcend economic cycles. The bank's ability to survive when others faltered was not luck. It was culture, a deeply ingrained institutional aversion to speculative lending that predated Dods and would outlast him.

But Dods also recognized a fundamental constraint: Hawaii's market was small. The state's population was under 1.2 million. Growth was limited by geography. And the Japanese collapse had demonstrated how vulnerable a concentrated island economy could be. You could be the best bank in Hawaii and still be captive to forces beyond your control: Asian economic cycles, tourism trends, natural disasters. The answer, Dods concluded, was scale through partnership, and the partner he found was on the mainland, backed by French money.

VI. The BancWest Era: French Ownership and Strategic Limbo (1998-2016)

On November 1, 1998, First Hawaiian, Inc. merged with Bank of the West, a San Francisco-based institution owned by Banque Nationale de Paris, or BNP. The surviving company was renamed BancWest Corporation. Former First Hawaiian shareholders owned fifty-five percent; BNP owned forty-five. The deal was valued at nearly one billion dollars, the largest stock transaction in Hawaii's history.

For Dods, the rationale was clear: geographic diversification and scale. Hawaii's "lost decade" had demonstrated the dangers of being tied to a single, small economy. Bank of the West gave First Hawaiian a mainland presence. For BNP, which became BNP Paribas after merging with Paribas in 2000, it was about building a U.S. retail banking presence anchored by two regional franchises: Bank of the West on the mainland and First Hawaiian in the Pacific. The combination created a bicoastal platform that looked attractive on paper.

Three years later, BNP Paribas made its move. On May 7, 2001, it offered to acquire the fifty-five percent of BancWest it did not already own at thirty-five dollars per share, approximately two and a half billion dollars. By December 2001, the deal closed. BancWest ranked as America's twenty-fifth-largest bank holding company, but Bank of the West and First Hawaiian Bank continued to operate under their own names. First Hawaiian Bank was now a subsidiary of a subsidiary of one of Europe's largest banking conglomerates, and the question was what that would mean for an institution whose identity was inseparable from the islands it served.

What followed was eighteen years of what might charitably be called benign stewardship and less charitably called strategic limbo. First Hawaiian maintained its local brand, its management autonomy, and its community-focused identity. BNP Paribas provided capital backing and risk management expertise. But First Hawaiian was never going to be a strategic priority for a French bank with over two trillion dollars in global assets. Hawaii was a rounding error on BNP's balance sheet. The bank was well-run but essentially in a holding pattern, like a talented employee stuck in a role with no promotion path.

This is a dynamic that investors in regional banking acquisitions should study carefully. When a small, well-run institution is absorbed into a much larger entity, the immediate benefits are real: capital support, risk management frameworks, economies of scale in technology and compliance. But the long-term costs are subtler. Strategic decisions are made in Paris, not Honolulu. Capital allocation follows the parent's priorities, not the subsidiary's opportunities. Technology platforms are standardized across the enterprise, not optimized for local markets. And the best talent, seeing limited advancement within the subsidiary, may drift elsewhere. First Hawaiian avoided the worst of these outcomes, largely because BNP Paribas was a relatively hands-off parent and because Hawaiian banking culture is strong enough to resist homogenization. But the bank undeniably entered a period of strategic drift, maintaining its position without meaningfully advancing it.

The early 2000s brought a welcome rebound. Hawaii's tourism industry diversified beyond its traditional Japanese and mainland American visitor base, attracting growing numbers of travelers from South Korea, China, and Australia. The Asia-Pacific middle class was expanding, and Hawaii was perfectly positioned to capture that growth. New resort developments, particularly on the Big Island and Maui, brought construction lending opportunities. The economy stabilized, deposits grew, and First Hawaiian settled into the comfortable if unspectacular rhythm of a well-run bank in a recovering market.

The arrangement had genuine benefits during times of stress. When the 2008 financial crisis tore through the American banking system, First Hawaiian's conservative credit culture, preserved through the ownership change, proved remarkably effective. While competitors pulled back on lending, First Hawaiian did the opposite. The bank originated six point two billion dollars in loans between 2008 and 2009, the most dramatic growth in its history. Nonperforming assets peaked at just sixty-three basis points, a fraction of the industry average. First Hawaiian required no government bailout, no emergency capital raise, no panicked restructuring. The combination of conservative Hawaiian underwriting and the implicit backing of a global banking giant had provided exactly the stability the market needed.

But the 2008 crisis also set in motion the forces that would ultimately free First Hawaiian from BNP's orbit. Post-crisis regulation reshaped the entire banking landscape. Basel III, the international framework for bank capital requirements, demanded that banks hold more capital against their risk-weighted assets. For non-banking readers, think of it as the regulators telling banks: you need a bigger cushion to absorb losses, which means you either raise more equity or shrink your balance sheet. The Dodd-Frank Act added layers of U.S.-specific compliance requirements. For foreign banks operating in the United States, the combined regulatory burden was substantial and growing.

European regulators began scrutinizing their banks' global footprints, asking pointed questions about whether far-flung subsidiaries in places like Hawaii were worth the capital and compliance costs they consumed. And then BNP Paribas created its own crisis.

On June 30, 2014, BNP Paribas pleaded guilty to conspiring to violate U.S. sanctions and agreed to pay a staggering eight point nine billion dollars, the largest sanctions fine in history. The bank had knowingly processed over eight point eight billion dollars through the U.S. financial system on behalf of sanctioned entities in Sudan, Iran, and Cuba over a period stretching from at least 2004 to 2012. As part of the settlement, BNP Paribas was temporarily banned from certain dollar-clearing activities, a punishment that sent shockwaves through the European banking sector and fundamentally altered BNP's strategic calculus regarding its U.S. operations. The fine strained BNP's capital reserves, intensified regulatory scrutiny, and created powerful strategic incentive to simplify its American footprint. Suddenly, owning a Hawaii-focused bank was not just strategically irrelevant to BNP's core European franchise; it was a source of regulatory entanglement that the bank's leadership in Paris wanted to minimize.

On December 23, 2015, roughly eighteen months after the sanctions settlement, First Hawaiian Bank announced that BNP Paribas was "considering strategic options" for the subsidiary, including an initial public offering. The corporate jargon was transparent. BNP Paribas was getting out. The question was how.

The answer was an IPO rather than a straight sale. An outright sale would have required finding a buyer willing to pay a premium for a Hawaii-focused franchise, and most large banks had little interest in entering a small, remote market with limited growth. An IPO allowed BNP Paribas to monetize its stake gradually over time, minimizing market disruption and maximizing total proceeds. It also gave First Hawaiian something it had not had in nearly two decades: the chance to stand on its own.

VII. The Great Separation: IPO and Independence (2016-2020)

The man who would guide First Hawaiian through the most consequential transition in its modern history was Robert S. Harrison. Harrison's background was unusual for a Hawaiian banker: a math degree from UCLA, an MBA from Cornell, and a stint in the U.S. Navy before entering financial services. He joined First Hawaiian in 1996, worked his way up through commercial lending, branch management, and risk oversight, and became CEO in 2012. His tenure as Chief Risk Officer from 2006 to 2009, spanning the financial crisis, had given him a deep appreciation for the conservative credit culture that defined the institution. Hawaii Business Magazine would later name him CEO of the Year in 2017, and the description his colleagues offered was consistent: disciplined, community-oriented, and allergic to unnecessary risk.

On April 1, 2016, BNP Paribas executed the corporate reorganization that made the IPO possible. Bank of the West was contributed to a new entity called BancWest Holding Inc. and spun off directly to BNP Paribas. BancWest Corporation was renamed First Hawaiian, Inc., creating a clean, standalone holding company for the bank. The restructuring was essential: investors wanted to buy a pure-play Hawaiian bank, not a holding company that also owned a California franchise.

On August 3, 2016, First Hawaiian priced its initial public offering at twenty-three dollars per share, the top of the marketed range. The next morning, August 4, FHB began trading on the NASDAQ Global Select Market. The IPO raised approximately 557 million dollars when including the fully exercised overallotment option. It was the largest U.S. bank IPO since Citizens Financial in 2014.

The underwriting syndicate read like a Wall Street all-star roster: Goldman Sachs, Bank of America Merrill Lynch, BNP Paribas, Barclays, Credit Suisse, Deutsche Bank, J.P. Morgan, Citigroup, Morgan Stanley, and UBS. When ten major investment banks line up to underwrite your offering, it signals that institutional investors are interested and the deal will place. The implied market capitalization was roughly 3.2 billion dollars. BNP Paribas retained approximately eighty-five percent of the shares.

The investor pitch was elegant in its simplicity: First Hawaiian operated in an oligopolistic market with structural barriers to entry. Hawaii had four major banks controlling roughly ninety-three percent of deposits. The geographic isolation that limited growth also limited competition. The deposit franchise was a low-cost funding machine. The bank had navigated multiple economic cycles without a crisis. This was not a growth story; it was a quality story. Think of it as the bond-like equity: predictable cash flows, limited downside, and a dividend yield that made it attractive to income-oriented investors. The trade-off was clear: you were not going to double your money, but you were unlikely to lose it, either.

The strategic questions that came with independence were thorny. Should First Hawaiian remain purely Hawaii-focused, or should it attempt to expand to the mainland? The Dods era had answered that question with the BancWest merger, and the answer had not gone well. An island bank trying to compete on the mainland was like a defensive specialist trying to play offense: the skills that made it successful at home did not translate to a different arena. Harrison made the pragmatic choice: stay in Hawaii, deepen the franchise, invest in technology, and return capital to shareholders. It was not a glamorous strategy, but it was an honest one.

But BNP's continuing majority stake created an overhang that weighed on the stock. An overhang, for non-market readers, is the dampening effect that a known future supply of shares has on the current price. If investors know that BNP Paribas is going to sell hundreds of millions of dollars in additional shares over the coming years, they are reluctant to bid the stock up aggressively, because each secondary offering will increase supply and potentially depress the price.

BNP Paribas systematically reduced its position through a series of secondary offerings: to sixty-two percent in February 2017, below fifty percent in May 2018, and then through additional sales in July, September, and November 2018. Each sale was carefully sized to avoid flooding the market, but the cumulative effect was to keep a lid on the stock price throughout the transition period.

On January 30, 2019, BNP announced the sale of its final eighteen point four percent stake. In February 2019, for the first time since the 1998 BancWest merger, First Hawaiian Inc. was a fully independent public company. The bank that Charles Reed Bishop had founded in a Honolulu basement 161 years earlier was once again its own master.

The timing of full independence was almost cosmically unfortunate. Within thirteen months, COVID-19 arrived.

Hawaii, with its extreme dependence on tourism at approximately twenty-one percent of GDP, was among the hardest-hit states economically. Governor Ige imposed a mandatory fourteen-day quarantine for all arrivals, effectively shutting down the tourism industry overnight. Visitor arrivals collapsed from 10.4 million in 2019 to 2.7 million in 2020, a seventy-four percent decline. During the spring 2020 lockdowns, daily arrivals plummeted from thirty to forty thousand to fewer than five hundred. Waikiki, normally teeming with tourists, was a ghost town. Visitor spending fell from 17.7 billion to roughly six billion dollars. Hawaii's unemployment rate soared above twenty percent, the highest in the nation.

For a bank that had just achieved independence after two decades of foreign ownership, the timing was brutal. The very first test of First Hawaiian's standalone viability was the worst economic shock in Hawaiian history since Pearl Harbor.

First Hawaiian absorbed the shock with the discipline Harrison had spent years instilling. Credit loss provisions surged to 41.2 million in the first quarter of 2020 and 55.4 million in the second quarter, but the bank never lost its footing. It launched the Aloha for Hawaii Fund to support the restaurant industry, donated a million dollars to nonprofits for COVID relief, and contributed another million to a fund for 2020 high school graduates. Most critically, it became one of Hawaii's leading PPP lenders, securing over 940 million dollars in Paycheck Protection Program loans for approximately six thousand small businesses in the initial rounds, and an additional 459 million in the second round. Total PPP lending exceeded 1.4 billion dollars, making First Hawaiian the state's SBA Lender of the Year for three consecutive years.

The pandemic also brought an unexpected tailwind. Remote work enabled a wave of mainland-to-Hawaii migration, particularly among high-income workers from California and the tech sector. These were not tourists; they were residents, bringing high-balance deposit accounts, mortgage demand, and wealth management needs. Hawaii real estate prices, already elevated, accelerated further. The median single-family home on Oahu surged past nine hundred thousand dollars. First Hawaiian's mortgage and real estate lending portfolios benefited, and the bank emerged from the pandemic with a stronger market position than it had entered.

The COVID experience also crystallized something that had been true but unquantified for decades: First Hawaiian's role as a community institution extended far beyond balance sheets and income statements. When small business owners across the islands needed PPP loans to survive, they did not call Chime or SoFi. They called their banker at First Hawaiian. When restaurants needed bridge financing to make it through lockdowns, they turned to the institution that had been lending to Hawaiian businesses since before electricity reached the islands. This relational depth, forged over generations and tested in crisis, is the most intangible and perhaps the most valuable asset on First Hawaiian's balance sheet. It does not appear in any SEC filing, but it shows up in deposit retention, loan quality, and the kind of customer loyalty that no marketing budget can manufacture.

VIII. Modern Era: Digital Transformation and Strategic Choices (2020-Present)

Post-pandemic Hawaii is a study in contradictions. Tourism has recovered but not fully: visitor arrivals ran down 3.2 percent year-over-year through September 2025, and the state's economic forecasters at UHERO have warned of a possible mild recession in 2026. Real estate prices have reached levels that strain credulity, with the average single-family home sale price hitting 1.09 million dollars in 2024, up eight percent from the prior year. The Maui wildfires of August 2023, which killed 115 people and destroyed over two thousand homes in Lahaina, added a layer of human tragedy and economic disruption that continues to reverberate. Roughly ninety percent of Lahaina burn area residents remain displaced, and rebuilding costs are estimated at approximately one million dollars per residence.

Against this backdrop, First Hawaiian has posted its strongest financial results since the IPO. Full-year 2025 net income reached 276 million dollars, with earnings per share of two dollars and twenty cents, a substantial improvement over 2024's 230 million and a dollar seventy-nine. To put this trajectory in context: the bank has grown earnings per share by roughly twenty-three percent in a single year, driven not by aggressive lending growth but by disciplined margin management and cost control. Net interest margin expanded through the year, reaching 3.21 percent in the fourth quarter of 2025, driven by favorable asset repricing as higher-rate loans replaced older, lower-rate assets. For non-banking investors, net interest margin is simply the difference between what a bank earns on its loans and investments versus what it pays depositors, expressed as a percentage. It is the single most important profitability metric in banking, and 3.21 percent is a healthy number that compares favorably to Bank of Hawaii's 2.39 percent.

The efficiency ratio, another critical metric, improved dramatically, falling from 61.6 percent in 2024 to approximately 55 percent by late 2025. The efficiency ratio measures how many cents a bank spends to generate each dollar of revenue, lower is better, and the improvement reflects disciplined cost management and operational streamlining. The bank returned roughly 230 million dollars to shareholders through dividends and repurchases, and the board authorized a new 250 million dollar buyback program.

The military and federal government remain a strategic anchor. Hawaii hosts the U.S. Pacific Command, numerous military installations, and a large federal civilian workforce. These provide a stable, counter-cyclical source of deposits and lending activity. However, recent federal spending cuts have created uncertainty: at least 1,200 civilian federal employees in Hawaii have already left their positions, and millions in federal grants are at risk.

Technology investment has been a recurring theme under Harrison's leadership, though the bank has moved methodically rather than aggressively. First Hawaiian migrated to a new FIS core banking platform in 2019, integrated MX Helios for mobile banking insights, selected Q2 PrecisionLender for commercial lending in 2023, and launched a redesigned mobile banking app in July 2025. The bank has positioned itself as the "technology leader in Hawaii," though that title is increasingly contested by Central Pacific Bank, which has embraced a digital-first strategy with seventy-six percent retail digital banking engagement and a Banking-as-a-Service partnership that gathers mainland deposits.

The geographic moat question, the question that defines First Hawaiian's investment thesis, is more relevant now than ever. For 160 years, the physical reality of the Hawaiian Islands provided extraordinary protection. You cannot open a branch in Honolulu from an office in Charlotte. You cannot build trust with a Maui small business owner over a chat interface. Local knowledge of Hawaiian real estate, tourism economics, and community dynamics is genuinely hard to replicate. But Chime does not need a branch. SoFi does not need local knowledge to offer a savings account. Every year, the digital channels that bypass geography grow stronger, and every year, the switching costs that kept Hawaiian depositors loyal grow weaker.

First Hawaiian's leadership bench is also in transition. Christopher Dods, the Chief Operating Officer who oversaw digital banking, card services, marketing, technology management, and strategy, resigned effective March 31, 2025. Alan Arizumi, a Vice Chairman with over forty years of service who oversaw wealth management, announced his retirement effective April 2026, with Michael Tottori, an EVP who joined the bank in 1989, stepping up to lead the wealth management group. Harrison himself has been CEO since 2012 and Chairman since the IPO. The next generation of leadership will determine whether First Hawaiian's culture and competitive position can endure.

For 2026, management has guided for loan growth of three to four percent and net interest margin of 3.16 to 3.18 percent, a slight compression from the fourth quarter's 3.21 as rate cuts take effect. It is conservative guidance from a conservative bank, and that conservatism is both the best and most frustrating thing about the investment case.

IX. The Business Model Deep Dive

To understand First Hawaiian, you have to understand island banking economics, and island banking economics come down to one fundamental insight: depositors on an island have very few places to put their money. This is not a metaphor. It is a physical reality. Four banks control roughly ninety-three percent of all deposits in the state of Hawaii. First Hawaiian and Bank of Hawaii together hold the lion's share. Where else will a Honolulu schoolteacher put her checking account? A mainland neobank? Maybe. But her mortgage, her auto loan, her small business line of credit, her parents' trust, all of that gravitates toward an institution with local expertise, physical branches, and a century of community relationships. The deposit franchise is the engine of First Hawaiian's business model, and it is a remarkably efficient engine. Deposits are the cheapest form of funding a bank can have, and when competition for those deposits is limited by geography, the cost stays low.

But the same geography that protects the deposit franchise constrains growth. Hawaii's population is approximately 1.4 million and essentially flat. You cannot grow your loan book dramatically when your total addressable market is smaller than the city of Phoenix. First Hawaiian's total loans stood at 14.3 billion at the end of 2025, and management is guiding for three to four percent growth, not because they lack ambition, but because the market does not support more.

This is the prisoner's dilemma of island banking: the capital cannot easily leave, but it also cannot easily multiply. For comparison, a similarly-sized bank on the mainland could expand into adjacent metropolitan areas, open branches in growing suburbs, or pursue digital customer acquisition across state lines. First Hawaiian can do none of these things without fundamentally changing its identity and competitive position. The total deposit pool in Hawaii is roughly forty-five billion dollars, and First Hawaiian already holds nearly half of it. Where does the next dollar of growth come from?

The loan portfolio reflects Hawaii's economy with almost textbook precision. Commercial real estate accounts for roughly a quarter of the book, driven by hotels, retail properties, and the multi-family housing that dominates island living. Residential mortgages are another twenty-three percent, reflecting the state's extraordinarily expensive housing market where the median single-family home exceeds a million dollars. Consumer loans, including auto and personal, represent approximately twenty-nine percent. Commercial and industrial lending fills the balance.

The mix is diversified by category but concentrated by geography: virtually everything is in Hawaii, which means the entire portfolio rises and falls with tourism, real estate values, military spending, and the weather. This is the fundamental risk that investors must understand. A mainland bank with a similar-sized portfolio spread across three or four states has natural diversification. First Hawaiian does not. When Hawaii prospers, every line of business prospers. When Hawaii suffers, every line of business suffers.

Revenue comes from two streams. Net interest income, the spread between what the bank earns on its loans and investments and what it pays on its deposits, accounted for roughly 170 million dollars in the fourth quarter of 2025 alone. This is the bread and butter of banking, and the quality of First Hawaiian's deposit franchise, low-cost, sticky, geographically captive, means that this spread is wider and more durable than what most mainland competitors enjoy.

Noninterest income, which includes fees from wealth management, trust services, deposit accounts, and card services, added another 55.6 million. Wealth management and trust services deserve special mention. First Hawaiian has administered trusts and managed wealth for prominent Hawaiian families for generations. The Kamehameha Schools endowment, the Bishop Estate, and numerous smaller family trusts have deep historical connections to the institution that Bishop himself founded. These are extraordinarily sticky relationships with very high switching costs. When a family trust has been at the same bank for fifty years, moving it to a fintech is not a serious consideration. Wealth management also generates reliable fee income that is less sensitive to interest rate fluctuations than the core lending business, providing a valuable diversification benefit.

The cost structure of island banking carries its own peculiarities. Operating branches across multiple islands is expensive. Consider what it takes to maintain a branch on Kauai: the building, the staff, the security, the technology infrastructure, the inter-island travel for management oversight, the shipping costs for supplies. Every branch on a Neighbor Island carries costs that a mainland branch a twenty-minute drive from headquarters does not. Inter-island transportation, redundant infrastructure, and the high cost of living in Hawaii all inflate expenses.

The bank's efficiency ratio improved to about fifty-five percent in late 2025, a meaningful gain from the low sixties in prior years. But this remains above the best mainland peers, where top-performing regional banks operate in the high forties. The gap reflects the structural cost premium of island operations, and closing it entirely may not be possible without sacrificing the branch presence that supports the relationship model.

Talent acquisition is another persistent challenge. Hawaii's isolated labor market means the bank competes for specialized skills, technology talent in particular, against the gravitational pull of the mainland's higher salaries and deeper talent pools. A cybersecurity engineer or data scientist who could earn two hundred thousand dollars in the Bay Area faces a lower salary and a higher cost of living in Honolulu. The lifestyle benefits of Hawaii are real, but they do not fully close the compensation gap for in-demand technical roles.

Risk management at First Hawaiian is dominated by concentration. The three pillars of the Hawaiian economy are tourism, real estate, and government, and all three can shift simultaneously.

A pandemic can obliterate tourism in weeks, as 2020 demonstrated. A real estate correction can impair the loan book across multiple categories simultaneously, because commercial real estate, residential mortgages, and construction loans all depend on the same underlying property market. Natural disasters, hurricanes, volcanoes, tsunamis, and now the demonstrated reality of catastrophic wildfires, represent ever-present threats. The Maui wildfires of 2023 were a stark reminder that a single event can destroy an entire community and billions of dollars in property value in a matter of hours.

And then there is the longest-term risk of all: climate change. Rising sea levels threaten coastal properties across the Hawaiian Islands, and many of those properties secure First Hawaiian's loans. Waikiki, the economic engine of Oahu's tourism industry, sits at sea level. King tides already flood streets and parking garages in the neighborhood during certain seasons. The question of whether insurers will continue to provide affordable coverage for coastal Hawaiian real estate is not hypothetical; it is a conversation happening now. This is not a next-quarter concern, but it is a next-generation concern, and for a bank that has survived 168 years, next-generation concerns matter.

X. Competitive Landscape: A Porter's Five Forces Analysis

Start with competitive rivalry. Hawaii's banking market is a cozy oligopoly, but cozy does not mean complacent.

First Hawaiian and Bank of Hawaii operate at roughly the same scale, each with about twenty-four billion in assets, and they have been rivals since the nineteenth century. Bank of Hawaii overtook First Hawaiian in deposit market share in 2021 and maintains a slight lead. The two banks compete for essentially the same customers, but their strategies differ: First Hawaiian leans toward commercial lending, while Bank of Hawaii has historically emphasized securities investments and consumer banking.

Central Pacific Bank, at about 7.4 billion in assets, has differentiated itself through aggressive digital transformation, achieving some of the highest digital banking engagement rates in the country. American Savings Bank, recently sold by Hawaiian Electric Industries for 405 million dollars to fund Maui wildfire settlements, is in ownership transition and somewhat distracted. Credit unions maintain strong local loyalty, particularly among military families and government employees. And national banks' digital products are increasingly visible, with JPMorgan Chase, Bank of America, and Wells Fargo all offering competitive online and mobile platforms accessible to Hawaiian residents.

Market share has been relatively stable over the past decade, but pricing pressure is real, particularly in a rate-cutting environment where banks compete for deposits. Rivalry is moderate to high.

The threat of new entrants is where geography matters most. Obtaining a bank charter requires significant regulatory approval and capital. Physical presence in Hawaii means paying Hawaii's real estate and labor costs, which are among the highest in the nation. Building trust in a community-oriented market takes decades, not quarters. Consider that Central Pacific Bank was founded in 1954, over seventy years ago, and it is still the third-largest bank in the state, not the first or second. That is how long it takes to build a meaningful position in Hawaiian banking through organic growth. These are formidable barriers.

But the digital channel has lowered entry barriers in ways that traditional analysis struggles to capture. Chime, SoFi, and similar platforms do not need branches, do not need local knowledge, and do not need decades of relationship building to capture a twenty-five-year-old's direct deposit. Their threat is real but still limited: most banking activity that requires local expertise, commercial lending, mortgage origination, trust services, remains difficult to digitize away. The critical question is where the line falls between "commodity banking," which is vulnerable to digital disruption, and "relationship banking," which is not. That line is moving, and it is moving in the fintechs' direction.

Supplier power in banking is an unusual concept, because the primary "supply" is money itself. Deposits are "supplied" by customers and are highly fragmented, giving no individual depositor meaningful bargaining power. No single customer can move the needle on First Hawaiian's funding costs.

Core banking technology vendors, primarily Fiserv, FIS, and Jack Henry, have some lock-in effect. Migrating from one core banking platform to another is a multi-year, multi-million-dollar undertaking that banks undertake reluctantly. First Hawaiian's 2019 migration to FIS was a significant project, and the bank will not be eager to repeat it anytime soon. But the market is competitive enough that pricing remains manageable.

The real supplier pressure comes from talent: specialized roles in risk management, technology, and commercial lending command premium compensation, and Hawaii's isolation limits the available pool.

Buyer power is moderate and rising. Retail customers still face meaningful switching costs: direct deposit, bill pay, linked accounts, and the sheer inertia of banking relationships create friction. Most people would rather endure a root canal than switch banks, and that inertia is one of banking's most underappreciated competitive advantages.

But that friction is declining every year as digital portability improves. Automatic account switching tools, instant account opening, and seamless direct deposit migration are eroding what was once a formidable barrier. Commercial customers are more sophisticated and can negotiate terms across multiple banks. Rate competition intensified during the post-COVID period, and digital alternatives give all customers more leverage than they had a decade ago.

The threat of substitutes is the force that most concerns long-term investors. Fintech apps handle payments, savings, and lending without a branch, a teller, or a relationship banker. Credit unions, which enjoy tax advantages that banks do not, offer competitive rates and strong local loyalty. Non-bank lenders like Rocket Mortgage originate home loans entirely online. Investment apps and high-yield savings accounts from the likes of Marcus and Wealthfront reduce deposit stickiness by offering yields that traditional savings accounts cannot match. Each of these individually is manageable. Collectively, they represent a slow but persistent erosion of the traditional banking model's economic rents. The erosion is particularly concerning in retail banking, where the youngest demographic cohorts show little attachment to physical branches and increasingly view banking as a commodity utility rather than a relationship.

The overall competitive picture is structurally attractive but slowly eroding. First Hawaiian operates in what amounts to a protected market, but the walls are getting shorter. The relevant question is not whether the moat exists, it clearly does, but whether it is eroding faster than First Hawaiian can adapt. The next decade will provide the answer.

XI. Strategic Powers: A Hamilton Helmer 7 Powers Analysis

Hamilton Helmer's framework asks a more pointed question than Porter: not just whether an industry is attractive, but whether a specific company has durable competitive advantages that create persistent differential returns. For First Hawaiian, the answer is nuanced.

Scale economies are moderate. First Hawaiian is Hawaii's largest bank by assets, and that scale provides efficiency advantages over smaller competitors: branch network costs spread over a larger deposit base, technology investments amortized across more customers, and better capital markets access. A core banking platform upgrade that costs fifty million dollars is far easier to justify when you have twenty-four billion in assets than when you have seven billion.

But the market is capped by Hawaii's population. You cannot achieve the kind of transformative scale economies that a JPMorgan or Bank of America enjoys, because the total addressable market simply is not large enough. Scale helps, but it does not define the competitive position. First Hawaiian is the biggest fish in a small pond, which is a very different thing from being a big fish in the ocean.

Network economics are weak. Banking has limited direct network effects. ACH transfers, wire payments, and card networks are commodified utilities available to all participants. There are no platform dynamics comparable to a payments network or a marketplace. Your checking account does not become more valuable because your neighbor also banks at First Hawaiian, unlike a social network where each additional user creates value for existing users.

Counter-positioning is essentially absent. Counter-positioning, in Helmer's framework, occurs when a newcomer adopts a business model that an incumbent cannot copy because doing so would damage their existing business. Think of how Netflix's streaming model counter-positioned against Blockbuster's retail stores. First Hawaiian is not disrupting anyone with a new model. If anything, fintechs are counter-positioning against First Hawaiian, offering simpler, cheaper, more convenient alternatives to traditional banking services. A neobank with zero branches and no physical infrastructure has a fundamentally lower cost structure than a bank that maintains fifty locations across volcanic islands. First Hawaiian cannot adopt that model without abandoning the relationship-based approach that defines its competitive position.

Switching costs are moderate to strong, and this is one of First Hawaiian's genuine powers. Retail customers who have their direct deposit, bill pay, mortgage, auto loan, and savings account at First Hawaiian face real friction in moving. The average American has been with their primary bank for roughly sixteen years, and in Hawaii, where community ties run deeper and alternatives are fewer, that number is likely higher.

Commercial customers face even more friction. Treasury management services, where a bank handles a company's cash collections, disbursements, and short-term investments, are complex to set up and painful to transfer. Credit relationships, where a loan officer understands a business owner's personal situation and industry dynamics, take years to develop. These are not the kind of relationships that migrate to a digital platform easily.

Trust and estate services represent the highest switching costs of all. When First Hawaiian has administered a family's multi-generational wealth for decades, the institutional knowledge, the legal documentation, and the personal relationships are deeply embedded. But digital portability is steadily reducing retail switching costs, and the generation entering the workforce today has less institutional loyalty than any in history.

Branding is moderate to strong. The First Hawaiian name carries weight on the islands. One hundred sixty-eight years of continuous operation builds trust, and trust matters enormously in banking. When someone asks "where do you bank?" in Honolulu, "First Hawaiian" is an answer that conveys stability, local roots, and community membership. The brand is associated with Hawaiian identity and community commitment in a way that no mainland institution can replicate.

But it is a regional brand that does not travel, which is by design, and its cultural resonance differs between longtime locals and mainland transplants. A tech worker who moved from San Francisco to Honolulu in 2021 may not feel the same connection to the First Hawaiian name that a third-generation local family does.

Cornered resource is where the analysis gets interesting, because First Hawaiian's most important resource is not something it owns but something it occupies: Hawaii itself. The physical branch locations in prime commercial areas, many of which the bank has occupied for decades and which are extraordinarily difficult to replicate given Hawaii's land constraints and zoning regulations. The relationships with key Hawaiian families, institutions, and government agencies, relationships that in many cases stretch back generations. The deep local market knowledge accumulated over a century and a half: understanding which neighborhoods are flood-prone, which commercial tenants are reliable, which tourism trends are sustainable and which are fads. The military banking relationships that date to World War II. These constitute a genuine cornered resource. The catch is that competitors can access the same resource with sufficient capital and patience. Bank of Hawaii has. Central Pacific has. The resource is cornered in the sense that it takes decades and deep local commitment to fully exploit it, not in the sense that it is exclusively available.

Process power is weak to moderate. First Hawaiian has genuine underwriting expertise in Hawaii-specific risks: understanding which resort developments will succeed, which residential neighborhoods are prone to flooding, which commercial tenants are reliable, and how to structure loans for businesses tied to tourism seasonality. These operational processes have been refined over decades and preserved through multiple ownership changes.

But these capabilities do not create the kind of systematic advantage that Helmer's framework requires for a primary power. Bank of Hawaii has similar expertise. Central Pacific, after seventy years in the market, has developed comparable knowledge. Process power requires that the processes be genuinely difficult to replicate, and while Hawaii-specific underwriting has a learning curve, it is one that any committed competitor can eventually climb.

The synthesis: First Hawaiian's durable advantages rest on switching costs, branding, and its cornered resource in Hawaiian geography and relationships. These are real powers, but they are all subject to the same slow erosion: digital disruption reduces switching costs, demographic change dilutes brand loyalty, and technology allows competitors to access the geographic resource remotely.

Compare this to Bank of Hawaii, which possesses essentially the same set of powers. The two institutions are remarkably similar in their strategic profile, which is both a validation of the Hawaiian banking thesis and a reminder that these powers are not unique to First Hawaiian. The difference, if there is one, lies in execution and culture rather than in structural positioning. First Hawaiian's commercial lending emphasis versus Bank of Hawaii's securities focus represents a genuine strategic distinction, but it is not the kind of fundamental competitive advantage that Helmer's framework is designed to identify.

The central question for investors is the rate of erosion relative to the duration of their investment horizon. Over five years, the moat holds. Over twenty years, the picture is less certain. The honest assessment is that First Hawaiian's powers are real, valuable, and slowly diminishing, a combination that makes it a reasonable investment for the patient and a frustrating one for the ambitious.

XII. Playbook: Business and Investing Lessons

First Hawaiian's story contains lessons that extend far beyond Hawaiian banking. The first and most important is the double-edged nature of captive markets. When your customers have nowhere else to go, your margins are protected and your market share is stable. But your growth is capped, and your fate is tied to a single geography. Every benefit of captivity has a corresponding constraint.

First Hawaiian's deposit franchise is among the most enviable in American banking precisely because it cannot be replicated elsewhere, which also means the bank cannot replicate it elsewhere. You get the moat, but you also get the walls. This is a lesson that applies far beyond banking: any business built on geographic isolation must accept that the same isolation that protects it also imprisons it. Founders and investors who celebrate defensible niches should ask themselves whether the niche is large enough to support their ambitions.

The second lesson is cultural stewardship as competitive advantage. First Hawaiian's relationships with Hawaiian families, institutions, and communities are not just marketing. They are a genuine economic asset that drives trust services, commercial lending, and deposit retention.

The bank's century-plus of continuous service, its founding by a man who married into the Kamehameha royal line, its role in financing the institutions that shape Hawaiian society, these things cannot be purchased or manufactured. They can only be inherited and maintained. A mainland bank could open a hundred branches in Hawaii tomorrow and still lack the cultural credibility that First Hawaiian has built over 168 years. For investors evaluating any community bank, the question of cultural embeddedness deserves more weight than it typically receives in financial models.

The third lesson concerns surviving ownership transitions. First Hawaiian operated under BNP Paribas for eighteen years without losing its identity, its credit culture, or its community relationships. That is remarkably difficult.

Many regional banks that are acquired by larger institutions lose their best people, their local autonomy, and their community standing within a few years. The acquirer renames the branches, standardizes the products, centralizes the decision-making, and within a decade the acquired bank is indistinguishable from any other branch of the parent company. First Hawaiian avoided this fate, partly because BNP Paribas was a relatively hands-off owner focused on financial returns rather than operational integration, and partly because the bank's people were deeply committed to the institution's Hawaiian identity. The lesson is that cultural resilience can survive corporate ownership if the culture is strong enough and the owner is wise enough not to destroy it.

The fourth lesson is about conservatism in cyclical businesses. First Hawaiian's conservative credit culture saved it during the Japanese bubble collapse, the 2008 financial crisis, and the COVID pandemic. Each time, the bank's refusal to chase growth at the expense of credit quality proved prescient. While competitors gorged on risky loans during booms and then hemorrhaged losses during busts, First Hawaiian stayed disciplined and emerged stronger.

But conservatism has costs. It limits returns in good times. It can calcify into resistance to innovation. And it can make a bank too cautious to seize opportunities that more aggressive competitors exploit. Central Pacific's digital-first strategy, for example, represents a calculated bet that First Hawaiian's conservative culture would not have allowed. The tension between prudence and ambition is eternal in banking, and First Hawaiian has consistently chosen prudence. Investors who value that choice should understand the stock. Those who find it frustrating should look elsewhere.

The fifth lesson is about geographic concentration. At what point does a concentrated geographic position become a trap rather than a moat? First Hawaiian cannot diversify its geographic exposure without fundamentally changing what it is. The Dods-era BancWest merger was an attempt at geographic diversification, and it ended with First Hawaiian absorbed into a French bank for eighteen years. The lesson from that experience was clear: diversification through acquisition can solve one problem while creating several new ones.

That concentration amplifies every risk: a pandemic that targets tourism, a wildfire that destroys a town, a climate trend that threatens coastal real estate. It also amplifies every benefit: intimate market knowledge, deep relationships, and regulatory barriers to entry. Whether this trade-off favors investors depends entirely on the time horizon and the nature of the risks that materialize.

Finally, the digital transformation question. First Hawaiian has invested in technology methodically, upgrading its core platform, launching a new mobile app, and adopting commercial lending tools. But it has not tried to become a technology company, and the contrast with Central Pacific Bank is instructive. Central Pacific, under CEO Paul Yonamine, has pursued a digital-first strategy that includes a Banking-as-a-Service partnership allowing it to gather deposits from the mainland without physical branches. Central Pacific reports seventy-six percent digital engagement among retail banking customers, a figure that suggests a fundamentally different strategic bet than First Hawaiian's relationship-first approach.

Which bet is right? The honest answer is that both approaches carry significant risk. Moving too fast on digital transformation can mean overspending on technology that does not generate returns, alienating older customers who value personal service, or adopting platforms that become obsolete. Moving too slowly can mean losing younger customers who expect mobile-first experiences, falling behind on data analytics, or becoming dependent on increasingly expensive legacy infrastructure. First Hawaiian's approach, steady and incremental, carries both the risk of falling behind and the benefit of avoiding costly mistakes. In island banking, where relationships still matter and the customer base is relatively older and more conservative, the incremental approach may be well-suited. But the next decade will be the test.

XIII. Bull vs. Bear Case

The bull case for First Hawaiian begins with market structure.

Hawaii's banking market is an oligopoly in which four institutions control ninety-three percent of deposits. Competitive entry is difficult, switching costs are real, and the two dominant banks have coexisted profitably for over a century. This is the kind of market structure that Warren Buffett has historically loved in insurance and railroads: limited competition, rational pricing, and durable economics. It is one of the most structurally protected banking markets in the United States.

First Hawaiian's deposit franchise provides low-cost funding that supports attractive net interest margins. The 3.21 percent NIM reported in the fourth quarter of 2025 compares favorably to Bank of Hawaii's 2.39 percent, suggesting either superior asset yields, lower funding costs, or both. That eighty-two basis point gap is significant: it means First Hawaiian earns substantially more per dollar of assets deployed, which flows directly to the bottom line.

Hawaii's demographic trends, while modest, contain bullish elements. Population growth is minimal, but the growth that does occur tends to come from wealthy mainland migrants attracted by Hawaii's lifestyle, remote work possibilities, and favorable tax treatment of certain retirement income. These are high-value banking customers. Military presence provides a stable, federally funded economic anchor that insulates against local economic cycles. Tourism, despite its volatility, has proven remarkably resilient over the long term: every downturn, from SARS to the financial crisis to COVID, has been followed by a recovery that exceeded prior peaks. The Asia-Pacific middle class represents a long-term growth driver for Hawaiian tourism.