F5: From Load Balancer to Multi-Cloud Application Empire

I. Introduction & Episode Setup

Picture this: It's 1999, and the internet is melting. Not metaphorically—literally overheating in server rooms across Silicon Valley. Yahoo's homepage takes 30 seconds to load. Amazon goes dark for hours during holiday shopping. eBay's auctions freeze mid-bid. The dirty secret of the dot-com boom? Nobody knew how to handle the traffic.

Enter Jeffrey Hussey, a Seattle investment banker with zero engineering background, who saw what the PhDs missed: the internet didn't need more servers—it needed a traffic cop.

Today, F5 sits at a $15.24 billion market capitalization, quietly powering the applications of 48 of the Fortune 50. When you stream Netflix, check your bank balance, or refresh Instagram, there's a good chance F5's technology is orchestrating that experience behind the scenes. The company generated $2.816 billion in revenue in fiscal 2024—a far cry from the $200,000 it scraped together in 1997.

But here's what makes F5's story remarkable: This isn't a tale of viral growth or consumer obsession. It's about building mission-critical infrastructure that companies can't live without, surviving a 94% stock price collapse, and executing one of enterprise software's greatest pivots—from selling boxes to acquiring the open-source project that powers 375 million websites.

The central question we're exploring: How did a startup founded by a non-technical investment banker during the dot-com boom become the backbone of internet traffic management, and what can we learn from its multiple near-death experiences and reinventions?

This is the story of technical pivots done right, of building switching costs so high that customers stay for decades, and of recognizing when your entire industry is about to transform—then having the courage to cannibalize yourself before someone else does. It's about the unglamorous work of keeping the internet running, and why the companies that build the plumbing often outlast those building the palaces.

II. The Founding Story & Internet Gold Rush (1996-1999)

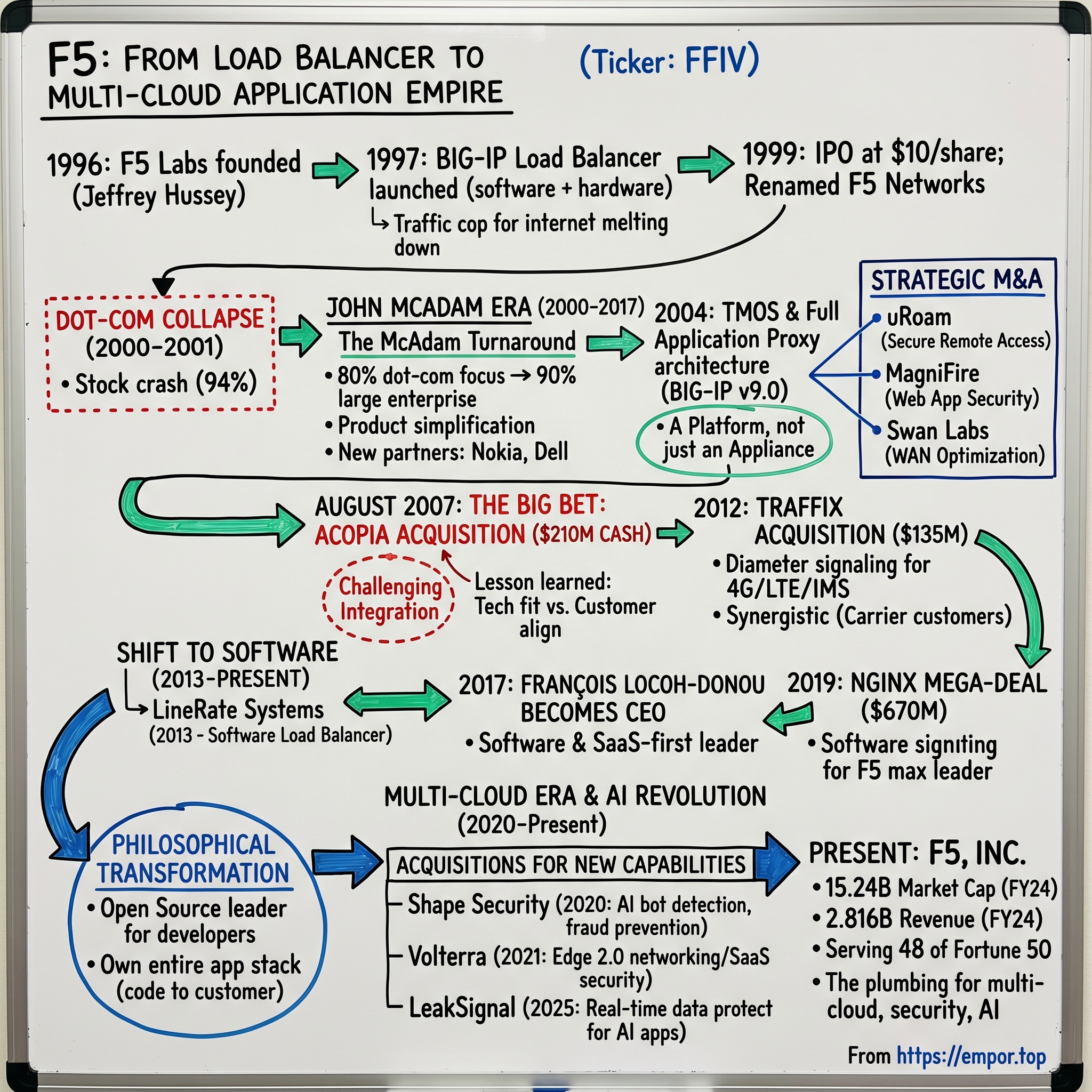

Jeffrey Hussey was the opposite of your typical tech founder. While Stanford computer science grads were dropping out to build search engines, Hussey was sitting in conference rooms at investment banks, watching PowerPoint presentations about "internet opportunities." His degrees from Seattle Pacific University and the University of Washington were in business, not bytes. But sometimes the best disruption comes from outsiders who ask naive questions.

In February 1996, as Netscape's IPO hangover was still coursing through Wall Street's veins, Hussey incorporated F5 Labs in Seattle. The city was electric—Microsoft was printing money, Amazon was still shipping books from Jeff Bezos's garage, and Real Networks was promising to stream audio over dial-up connections. Coffee shops buzzed with talk of bandwidth and burn rates. Hussey set up shop in April, two months after incorporation, with a simple thesis: if everyone was right about internet growth, traffic would become the bottleneck.

The name F5 came from the keyboard shortcut for "refresh"—a function that was becoming muscle memory for millions of early web users hitting reload on slow-loading pages. It was perfect: short, memorable, and directly connected to the problem they were solving. July 1997 was when it happened. F5 launched its first product, a load balancer called BIG-IP—and the metaphor was perfect. Instead of merely diverting traffic from one server to another, BIG-IP functioned like an air traffic controller, determining which server had the most free space and intelligently managing traffic flow through proprietary software and industry-standard hardware.

The technical insight was elegant: websites didn't need more servers; they needed smarter traffic management. While competitors were selling bigger boxes, F5 was selling intelligence. But elegance doesn't pay bills. Business was small at first, generating a paltry $200,000 by the end of 1997. The total paled in comparison to Cisco Systems' $5 billion in sales, whose networking equipment competed directly with BIG-IP.

Yet Hussey had timing on his side. The internet was exploding—Yahoo was worth billions, Amazon was burning cash to grab market share, and every Fortune 500 company was scrambling to get online. They all had the same problem: when traffic spiked, servers crashed. F5's solution was becoming not just useful but essential.

In September 1998, BIG-IP was joined by its counterpart for wide area networks, the 3DNS Controller, which served as a load balancer for companies that had multiple locations. Now F5 could manage traffic not just within a data center but across the globe. A user in Tokyo could be automatically routed to servers in Asia rather than waiting for a response from California.

The momentum was building. In April 1999, the company changed its name from F5 Labs to F5 Networks and filed for an initial public offering (IPO) of stock, hoping to raise up to $40 million to pay off debt and fund expansion. The rebranding was strategic—"Labs" sounded experimental; "Networks" sounded essential.

F5 completed its IPO in June 1999, selling 2.86 million shares at $10 per share, netting it $25.5 million. The timing was exquisite—right at the peak of dot-com mania. Within months, F5's stock would hit $160 per share, a 16x return that made early investors delirious with paper wealth.

But Hussey, the investment banker turned tech CEO, must have known what was coming. The fundamentals didn't support the valuations. The question wasn't if the bubble would burst, but when—and whether F5 had built something real enough to survive the reckoning.

III. The Dot-Com Collapse & Near-Death Experience (2000-2001)

The year 2000 opened with F5's stock at $160 per share. Engineers were buying Porsches with stock options. The company was expanding into gleaming new offices. Life was good—until it wasn't.

By June, reality was setting in. F5's share price had fallen from $36 to $9.43, a fraction of the $160 at the beginning of the year and below the IPO price of $10. The company celebrated its 11th consecutive quarter of revenue growth, but nobody was celebrating. The dot-com party was over, and F5 was about to learn it had been dancing with the wrong partners.

Then came the hire that would save the company. In July 2000, John McAdam walked through F5's doors as the new president and CEO. A former general manager of IBM's web server sales business, McAdam had seen enough enterprise sales cycles to know what worked and what didn't. His first assessment was brutal: "When I came on board, our business model was broken."

The numbers told the story: 80% of F5's revenue came from dot-com startups. These weren't just customers—they were patients in the ICU, burning through venture capital while their business models disintegrated. Pets.com, Webvan, Kozmo.com—the graveyard was filling up fast, and each tombstone represented lost F5 revenue. McAdam's turnaround playbook was brutal in its clarity. He reduced F5's staff by 15 percent in January 2001, subleased office space in the company's newly built headquarters, and, most important, streamlined F5's product line to make it more appealing to large companies. This wasn't just cost-cutting—it was a complete repositioning of the company.

The strategy was three-fold. First, simplify the product line. Enterprise buyers didn't want complex, customizable solutions; they wanted products that worked out of the box with their existing infrastructure. Second, leverage channel partnerships. He brokered distribution partnerships with Nokia Corp. and Dell Computer Corp. that gave F5 access to a broader range of corporate customers, dramatically altering the profile of the company's customer base. Third, and most critically, completely flip the customer base from startups to enterprises.

The financial bleeding was severe. Faced with announcing a 40 percent decline in revenues and a loss instead of a profit for the first quarter of 2001, he sought to repair F5's reputation on Wall Street. The stock continued its death spiral, dipping below $5 by April—a 97% decline from its peak.

But something remarkable was happening beneath the carnage. While F5's dot-com customers were dying, the survivors were getting bigger. Amazon, Google, Yahoo—the companies that made it through the crash would need more sophisticated traffic management than ever. And traditional enterprises, finally convinced the internet was here to stay, were building out their digital infrastructure.

By December 2001, F5's stock was trading for $27.73, a 52-week high. The transformation was stunning in its speed and completeness. In a December 14, 2001 interview with Puget Sound Business Journal, the analyst said, "It's a definite turnaround for this company. You have to give credit to McAdam and his team. F5 went from being 80 percent reliant on dot.com customers to 90 percent reliant on large enterprises."

By the beginning of 2002, the devastation caused by the collapse of the dot.com industry had winnowed the ranks of the technology sector. F5 had survived and it found itself involved in a three-horse race for control of a $385 million market. Cisco had bought ArrowPoint Communications for $5 billion. Nortel had acquired Altheon WebSystems for $7 billion. But F5, the scrappy survivor valued at a fraction of those deals, was still standing—and about to prove that in technology, it's not about who spends the most, but who builds the best.

IV. The McAdam Turnaround: From Startup to Enterprise (2001-2007)

The dot-com wreckage of 2002 looked like a technology graveyard. Aeron chairs were selling for $100 on Craigslist. Sun Microsystems servers gathered dust in abandoned data centers. But for John McAdam, surveying the carnage from F5's Seattle headquarters, this wasn't devastation—it was opportunity.

"We were like cockroaches," a former F5 engineer would later recall. "After the nuclear winter, we were still there, and we were hungry."

According to McAdam, the current CEO of the company, it is the big decision taken by the company in the year 2002 to invest in Traffic Management Operating System (TMOS) that led to them being in the top of the market. This wasn't just a product update—it was a complete architectural reimagining. While competitors were still selling appliances that did one thing well, F5 was building a platform that could evolve.TMOS and F5's so-called 'full application proxy' architecture was introduced in 2004 with the release of v9.0. This wasn't just a software update—it was a complete reimagining of what a network appliance could be. Previously the hardware and software were simply both referred to as BIG-IP, but now the software and hardware diverged. The move from BSD to Linux to handle system management functions, and the creation of a Traffic Management Microkernel (TMM) to directly talk to the networking hardware represented a fundamental architectural shift.

The business impact was immediate. McAdam's restorative work culminated in a profitable 2003 for F5, the first annual profit recorded by the company after two years of losses. Revenues increased from $115 million in 2003 to $171 million in 2004. More impressive was the profit gain recorded in 2004, a 705 percent increase to $33 million.

But McAdam wasn't content with organic growth. He began a buying spree that would transform F5 from a one-product company into a platform. In July 2003, McAdam spent $25 million to buy uRoam, a developer of software that enabled users to securely access their company's private network from any computer. The strategic intent was to diversify its product offerings beyond its core application delivery and security services, addressing the growing demand for secure remote access to corporate networks and applications.

In May 2004, McAdam struck again, paying $29 million to acquire MagniFire Websystems. This acquisition allowed F5 to enter the web application security space within the BIG-IP platform. MagniFire Websystems products were sold independently when the deal first closed, then were quickly bundled into the BIG-IP product group.

In September 2005, F5 announced they had acquired Swan Labs for a total of $43 million to incorporate WAN optimization and application acceleration technology into the BIG-IP platform, specifically to improve their load balancing offering.

Each acquisition followed a pattern: identify a technology that enterprises needed, buy the best standalone player, then integrate it into the BIG-IP platform. This wasn't empire building—it was ecosystem construction. Every new module made the core product stickier, the switching costs higher, the competitive moat wider.

By 2007, F5's employee base included 1,355 employees throughout the world, including 641 in Washington, where its workforce had increased 31 percent in just one year. The company had tripled office space in Spokane to 43,000 square feet, added 15,000 square feet of additional research and development space in Bellevue, along with a new building in Seattle that spanned 137,000 square feet.

Shortly after joining F5 in July 2000, Mr. McAdam successfully navigated the Company through the turbulent post-dot-com era, bringing F5 to profitability and positioning it for further growth. During his tenure at F5, Mr. McAdam grew the Company's annual revenue from $108.6 million to more than $1.9 billion in fiscal year 2015. Under Mr. McAdam's leadership, F5 was added to the S&P 500—one of the world's most widely followed stock market indices.

The transformation was complete. The scrappy startup that nearly died in 2001 had become enterprise infrastructure royalty. But McAdam's biggest bet was still to come—and it would test everything he had learned about building platforms and managing risk.

V. The Big Bet: Acopia & Storage Virtualization (2007-2012)

August 2007. The housing market was starting to crack. Bear Stearns hedge funds had just collapsed. Financial engineers were discovering that mortgage-backed securities weren't quite as secure as advertised. It was exactly the wrong time to make a big acquisition.

Which is exactly when John McAdam decided to make F5's biggest acquisition ever.

In August 2007, F5, Inc., at the time, F5 Networks, Inc., announced they acquired Acopia Networks, Inc. to add file-area networking to the F5 BIG-IP application-delivery product line. The all-cash transaction for $210 million dwarfed F5's previous $43 million acquisition of Swan Labs in 2005.

"File virtualization is an exciting and largely untouched market opportunity," McAdam said at the time. The logic seemed sound: as enterprises generated more data, they needed better ways to manage it across multiple storage systems. Acopia's technology could virtualize file storage the same way F5 virtualized application traffic.

But this wasn't like buying MagniFire or uRoam. Those were bolt-on acquisitions that enhanced F5's core competency. Acopia was a leap into an adjacent market—storage networking—where F5 had no expertise, no relationships, and formidable competitors like EMC and NetApp.

The integration proved challenging. Storage administrators and network administrators rarely talked to each other in most enterprises. They had different budgets, different priorities, different vendor relationships. F5's sales force, trained to sell application delivery, struggled to articulate the value of file virtualization. The technology worked, but the go-to-market motion didn't.

Meanwhile, the financial crisis was decimating IT budgets. Companies weren't thinking about optimizing storage; they were thinking about survival. The ambitious cross-selling opportunities McAdam had envisioned—bundling storage virtualization with application delivery—never materialized at scale. The lesson from Acopia came in 2012 with a very different acquisition. F5 acquired Traffix Systems for $135 million (some sources say $140 million), the leading provider of 4G Diameter signaling products for telecommunications service providers. This wasn't a leap into an adjacent market—this was doubling down on F5's core strength in traffic management, just for a different kind of traffic.

"Diameter traffic is mission critical for any carrier moving to 4G/LTE and IMS architectures. It enables billing, subscriber management, and interoperability between core IP systems and between carriers themselves," said John Byrne, Research Director Wireless and Mobile Infrastructure service at IDC.

The timing was perfect. Mobile data traffic was exploding as smartphones became ubiquitous. Carriers were desperately trying to upgrade from 3G to 4G/LTE networks, and Diameter was the protocol that made it all work. Unlike the Acopia acquisition, Traffix aligned perfectly with F5's DNA—it was about managing traffic, just signaling traffic rather than application traffic.

"Since its acquisition of Traffix in February 2012, F5 has strengthened the SDC global footprint," said Diane Myers, Principal Analyst at Infonetics Research. "The reliability of the SDC has encouraged operators to rely on and understand the critical role that a Diameter solution plays in LTE networks, and in providing connectivity to legacy networks. The expertise that F5 Diameter engineers have brought to the market is a strength the company has been able to leverage in becoming a leading vendor in the market."

By 2012, the Traffix SDC solution was deployed in more than 25 sites among tier 1, tier 2, and IP Exchange (IPX) carriers worldwide. The integration went smoothly—carrier networks needed both application delivery (F5's traditional strength) and signaling management (Traffix's expertise). The sales teams could cross-sell effectively because they were calling on the same buyers with complementary solutions.

The contrast between Acopia and Traffix taught McAdam a crucial lesson: successful M&A in infrastructure isn't just about technology fit—it's about customer alignment, sales motion compatibility, and market timing. Acopia was technologically sound but organizationally awkward. Traffix was both technologically and organizationally synergistic.

This lesson would prove invaluable as F5 approached its next major transformation—the shift from hardware to software that would define the next decade.

VI. The Software Transformation & NGINX Acquisition (2013-2019)

The year 2013 marked an inflection point that John McAdam saw coming from miles away. Amazon Web Services was growing 50% year-over-year. Netflix had just completed its seven-year migration to the cloud. And F5's customers—those Fortune 500 enterprises who had been buying hardware appliances for over a decade—were starting to ask uncomfortable questions about "cloud-native" and "DevOps."

The problem wasn't that F5's technology was becoming obsolete. BIG-IP appliances still handled massive traffic loads better than anything else. The problem was that a new generation of developers was building applications differently—microservices, containers, continuous deployment—and they weren't waiting six weeks for procurement to approve a $100,000 hardware purchase.

McAdam's response was swift. In 2013, F5 acquired LineRate Systems for $125 million, a developer of software-based high-performance load balancer for x86 systems. LineRate's technology could run on commodity hardware, be deployed in minutes, and spoke the language of DevOps—APIs, automation, programmability.

But the real transformation was happening inside F5. During his tenure at F5, Mr. McAdam grew the Company's annual revenue from $108.6 million to more than $1.9 billion in fiscal year 2015. Under Mr. McAdam's leadership, F5 was added to the S&P 500—one of the world's most widely followed stock market indices. Yet McAdam knew that past success wouldn't guarantee future relevance. In 2017, François Locoh-Donou replaced John McAdam as president and CEO. It was a passing of the torch that signaled F5's commitment to transformation. Locoh-Donou, an engineer by training with degrees from École Centrale de Marseille and Télécom ParisTech, plus an MBA from Stanford, brought exactly what F5 needed: technical depth combined with cloud-era sensibility.

"At a time when F5 is expanding its partnerships and products into cloud and security markets, François brings a renewed sense of purpose to F5's original vision: applications without constraints," said Al Higginson, Chairman of F5's Board.

Since joining F5 as CEO in April 2017, he has spearheaded the company's business transformation from a networking hardware maker to a software- and SaaS-first leader in hybrid, multicloud application delivery and security. But his boldest move was yet to come. The NGINX mega-deal in March 2019 was Locoh-Donou's defining moment. The company, which provides cloud and security application services, announced that it has acquired NGINX, the commercial company behind the popular open-source web server, for $670 million. The company currently runs 375 million websites with some 1,500 paying customers taking additional services.

This wasn't just a big acquisition—it was a philosophical transformation. NGINX was everything F5 traditionally wasn't: open source, developer-focused, cloud-native. NGINX web server is the third most widely used servers in the world—behind only Microsoft and Apache, and ahead of Google. Majority of sites on the Internet today, including Instagram, Pinterest, Netflix, and Airbnb are hosted on web servers running NGINX.

"F5's acquisition of NGINX strengthens our growth trajectory by accelerating our software and multi-cloud transformation," said François Locoh-Donou. "By bringing F5's world-class application security and rich application services portfolio for improving performance, availability, and management together with NGINX's leading software application delivery and API management solutions, unparalleled credibility and brand recognition in the DevOps community, and massive open source user base, we bridge the divide between NetOps and DevOps."

The strategic brilliance was in recognizing that F5 and NGINX weren't really competitors—they served different audiences within the same organizations. F5 sold to network operations teams; NGINX was beloved by developers. F5 was enterprise-grade and expensive; NGINX was open source and accessible. Together, they could own the entire application delivery stack from code to customer.

Zeus Kerravala, analyst at ZK Research, captured the dynamic perfectly: "Traditional IT looks at Nginx as too risky and DevOps views F5 as stodgy. By bringing them under one roof, F5 will now own the whole application experience, from the app server to the user."

The acquisition also represented a crucial hedge. If the future was all open source and developer-led, F5 now had a seat at that table. If enterprises continued to need robust, enterprise-grade solutions, F5's traditional business would persist. It was having your cake and eating it too—a rare feat in technology M&A.

By 2019, the software transformation was complete. F5 had evolved from a hardware company selling boxes to a software company with multiple delivery models—appliances, virtual editions, cloud services, and now open source. The journey from near-death in 2001 to acquiring one of the internet's most important technologies for $670 million was complete. But the cloud wars were just beginning.

VII. The Multi-Cloud Era & AI Revolution (2020-Present)

January 2020 should have been a victory lap year for F5. The NGINX integration was proceeding smoothly, software revenues were growing, and the multi-cloud strategy was gaining traction. Then COVID-19 hit, and suddenly every company on Earth needed to scale their digital infrastructure overnight.

But instead of retreating, Locoh-Donou doubled down. In January 2020, F5 acquired Shape Security, Inc., an AI-based bot detection company, for $1 billion. F5 Networks then used the acquisition to introduce a new fraud detection engine. The timing seemed insane—spending a billion dollars as the world economy was shutting down. But Locoh-Donou saw what others missed: the pandemic wasn't slowing digital transformation; it was accelerating it by a decade.

Shape Security's technology used artificial intelligence to distinguish between human and bot traffic in real-time, protecting against credential stuffing, account takeover, and other automated attacks. As e-commerce exploded during lockdowns, these attacks surged. F5's customers desperately needed this capability. In January 2021, F5 acquired Volterra, Inc., an edge networking company that sells SaaS security services, for $500 million (approximately $440 million in cash and $60 million in deferred consideration). Volterra's technology created what F5 called "Edge 2.0"—a platform that could deploy applications anywhere, from data centers to public clouds to the network edge.

"Current edge solutions are simply inadequate for today's enterprise customers. It's time to break out of closed edge systems that only perpetuate the pain of building, running, and securing apps," said François Locoh-Donou. "With Volterra, we advance our Adaptive Applications vision with an Edge 2.0 platform that solves the complex multi-cloud reality enterprise customers confront."

The company was formerly known as F5 Networks, Inc. and changed its name to F5, Inc. in November 2021—a subtle but significant signal that the company was no longer just about networking but about the entire application delivery and security stack. In March 2025, F5, Inc. acquired LeakSignal, a cybersecurity company specializing in real-time data protection and governance for AI applications. The acquisition aimed to enhance the F5 Application Delivery and Security Platform (ADSP) with capabilities such as AI-driven data classification, policy enforcement, and compliance monitoring.

"We're addressing the critical data protection gaps that have emerged as organizations embrace modern and AI-powered applications," wrote Kunal Anand, Chief Innovation Officer of F5. LeakSignal was recognized by the National Institute of Standards and Technology (NIST) for pioneering data classification, proactive remediation, and AI-driven policy enforcement of data in-transit.

The timing couldn't be more strategic. As organizations rush to adopt AI, they're inadvertently creating massive security vulnerabilities. Every prompt to ChatGPT, every query to an AI assistant, every automated workflow could potentially leak sensitive data. F5's acquisition of LeakSignal positions the company at the intersection of two massive trends: AI adoption and AI security.

Today, 48 of the Fortune 50 companies use F5 for load balancing, Layer 7 application security, fraud prevention, and API management. The company has successfully transformed from a hardware vendor selling appliances to a software and services company enabling multi-cloud application delivery and security.

VIII. Playbook: The Art of Technical Infrastructure

After nearly three decades of building mission-critical infrastructure, F5's playbook reads like a masterclass in enterprise technology strategy. The lessons aren't just about selling boxes or writing code—they're about understanding the fundamental dynamics of how enterprises adopt, deploy, and depend on technology.

Building a Mission-Critical Business: When Downtime Costs Millions

The genius of F5's positioning was recognizing that some technology isn't optional. When Amazon's website goes down, they lose $14,900 per second. When a bank's online systems fail, it's not just lost revenue—it's regulatory violations, customer trust erosion, and competitive disadvantage. F5 positioned itself as insurance against catastrophe.

This creates a unique dynamic: customers don't evaluate F5 on features alone but on trust. Can you keep us running during Black Friday? Can you stop the DDoS attack? Can you handle the traffic spike when our product goes viral? The answer has to be yes, every time, or the business model collapses.

The Enterprise Sales Motion: From Dot-Coms to Fortune 500

McAdam's transformation of F5's sales approach in 2001 became the template for enterprise infrastructure companies. The shift from selling to startups to selling to enterprises required a complete organizational overhaul—longer sales cycles, proof-of-concept deployments, reference customers, and most importantly, speaking the language of risk mitigation rather than innovation.

Enterprise buyers don't want to be pioneers; they want to be fast followers. F5 learned to sell not the newest technology but the most proven technology. The sales pitch evolved from "look what's possible" to "look who already trusts us."

Platform Economics in Infrastructure: Hardware → Software → Services

F5's evolution mirrors the broader infrastructure industry's transformation. Hardware provided the initial foothold—tangible, understandable, with clear performance metrics. Software expanded the addressable market—no shipping costs, instant deployment, subscription pricing. Services created recurring revenue—managed security, cloud migration, ongoing optimization.

Each transition cannibalized the previous business model while expanding the total opportunity. The key was timing: moving to software before hardware margins collapsed, embracing services before software became commoditized.

M&A Strategy: Buy vs. Build in Technical Markets

F5's acquisition track record reveals a clear pattern: buy for market access, build for core technology. NGINX brought developer credibility. Shape brought AI expertise. Volterra brought edge computing. But the core TMOS platform remained internally developed.

The discipline to know what to buy versus what to build is rare in technology. Too many companies acquire their way into technical debt or build their way into irrelevance. F5 found the balance.

Open Source as Both Threat and Opportunity

The NGINX acquisition was F5's acknowledgment that open source had won the developer mindshare battle. Rather than fight it, F5 embraced it, maintaining NGINX's open-source roots while building commercial services on top.

This dual strategy—proprietary for enterprises, open source for developers—allows F5 to play both sides of the modern infrastructure divide.

The Importance of Timing: Surviving Crashes, Riding Waves

F5's history is a study in market timing. Founded just before the dot-com boom, nearly killed by the bust, revived by enterprise digital transformation, transformed by cloud adoption. The company that survived wasn't the one that was founded—it evolved with each wave.

The lesson: in infrastructure, you don't predict the future; you build the flexibility to adapt to it.

Channel Partnerships and Distribution Leverage

F5's partnerships with Dell, Nokia, and others in the early 2000s provided distribution leverage that no amount of direct sales could match. These partnerships weren't just about reach—they were about credibility. When Dell sells your product, you inherit their enterprise relationships.

IX. Power Analysis & Business Model Deep Dive

Understanding F5's competitive moat requires examining the seven powers that create sustainable business advantages.

Switching Costs and Technical Lock-in

Once F5's technology is embedded in an enterprise's infrastructure, removing it is like performing heart surgery while running a marathon. The technical switching costs are enormous—rewriting configurations, retraining staff, risking downtime. But the psychological switching costs might be even higher.

IT managers who've successfully kept systems running on F5 for years won't risk their careers on a cheaper alternative. "Nobody gets fired for buying IBM" has become "Nobody gets fired for sticking with F5."

Network Effects in Developer Communities (post-NGINX)

The NGINX acquisition brought F5 something money couldn't buy directly: developer love. With millions of developers using NGINX, every tutorial, Stack Overflow answer, and GitHub integration increases the platform's value. These network effects compound—more developers mean more tools, more tools mean more developers.

Scale Economies in R&D and Sales

F5 spends approximately $400 million annually on R&D. A startup trying to compete would need to match that investment while generating a fraction of F5's revenue. The math doesn't work. Similarly, F5's global sales force—trained, experienced, with deep enterprise relationships—would take competitors years and billions to replicate.

48 of the Fortune 50 companies use F5 for load balancing, Layer 7 application security, fraud prevention, and API management. These relationships, built over decades, create a formidable barrier to entry.

Recurring Revenue Transition and SaaS Evolution

F5's shift from one-time hardware sales to recurring software subscriptions fundamentally changed the business model. Recurring revenue now represents over 50% of total revenue, providing predictability and higher lifetime customer value. The SaaS model also enables continuous innovation—customers always have the latest features without disruptive upgrades.

Gross Margin Dynamics: Hardware vs. Software vs. Services

Hardware gross margins typically run 50-60%. Software margins exceed 80%. Services margins vary but often exceed 60%. F5's transition up the margin stack has been deliberate and successful. The company maintains hardware for customers who demand it while pushing new customers toward higher-margin software and services.

This margin expansion funds the massive R&D investment required to stay ahead in a rapidly evolving market.

X. Bear vs. Bull Case & Future Scenarios

Bull Case:

The multi-cloud complexity that enterprises face is F5's opportunity. As companies deploy applications across AWS, Azure, Google Cloud, and on-premises infrastructure, they need a neutral party to manage traffic, security, and performance across all environments. F5 is uniquely positioned as that neutral orchestrator.

AI/ML workloads present another growth vector. These workloads are unpredictable, resource-intensive, and security-sensitive—exactly the challenges F5 solves. As AI moves from experimentation to production, F5's infrastructure becomes essential.

Security threats are evolving faster than most enterprises can adapt. F5's combination of AI-powered threat detection (Shape), application security (WAF), and now data governance (LeakSignal) creates a comprehensive security platform that few can match.

The installed base provides a massive upsell opportunity. Those 48 Fortune 50 customers aren't going anywhere, and they're all trying to figure out AI, edge computing, and zero-trust security. F5 can sell into these initiatives with minimal customer acquisition cost.

Bear Case:

Cloud providers are building competing solutions. AWS Application Load Balancer, Azure Application Gateway, Google Cloud Load Balancing—they're good enough for many use cases and deeply integrated with their respective clouds. As workloads shift to the cloud, F5's relevance could diminish.

Open source alternatives continue to improve. Envoy, HAProxy, and even NGINX (despite F5's ownership) provide free alternatives that are increasingly enterprise-ready. The commoditization of load balancing and traffic management threatens F5's core business.

The hardware business is in structural decline. While software growth has offset hardware declines so far, this transition creates execution risk. Missing a quarter or two could devastate investor confidence.

Integration execution risks loom large. F5 has acquired Shape, NGINX, Volterra, and LeakSignal in rapid succession. Integrating these technologies and cultures while maintaining product quality and customer satisfaction is enormously complex.

XI. Lessons & Reflections

What would have happened without McAdam's turnaround? F5 would likely have joined the dot-com graveyard—another promising technology company that couldn't navigate the transition from boom to bust. McAdam's immediate recognition that the business model was broken, and his decisive action to fix it, saved the company.

The NGINX acquisition stands as the defining moment of F5's modern era. It wasn't just buying technology—it was buying relevance with a new generation of technologists. Without NGINX, F5 risked becoming the enterprise infrastructure equivalent of IBM mainframes—profitable but gradually irrelevant.

Key takeaways for founders and investors:

First, timing matters more than technology. F5's technology was good but not revolutionary. Their timing—being ready when the internet exploded, pivoting when it crashed, transforming for the cloud era—was perfect.

Second, customer concentration can be both risk and opportunity. F5's 80% concentration in dot-coms nearly killed it. But their pivot to enterprise concentration created a moat that's lasted decades.

Third, technical debt is real in M&A. Every acquisition brings integration challenges. F5's discipline in maintaining architectural coherence while adding new capabilities is rare and valuable.

Fourth, infrastructure businesses are won through trust, not features. F5's customers don't buy products; they buy reliability, support, and peace of mind. Building that trust takes decades. Losing it takes minutes.

Finally, cannibalizing yourself beats being eaten by others. F5's willingness to undermine its hardware business with software, then its software business with SaaS, kept it ahead of disruption.

The future of application delivery and security will be shaped by AI, edge computing, and quantum threats. F5 has positioned itself at the intersection of these trends. Whether it can execute on this positioning while managing its complex technology portfolio and evolving competitive landscape will determine if the next chapter is as successful as the last.

The company that started by solving internet traffic jams has evolved into something far more ambitious: the nervous system for digital business. In a world where every company is a technology company, and every application is mission-critical, F5's role has never been more important—or more challenging.

XII. Recent News

The latest quarterly results paint a picture of a company successfully navigating its transformation while facing macroeconomic headwinds. F5's fiscal Q2 2025 results showed the delicate balance between growth investments and market reality. Software revenue continues its upward trajectory, now representing 54% of product revenue, while hardware shows expected declines as customers shift to cloud-native deployments. The latest earnings reveal a company executing well on its transformation strategy. Q2 fiscal 2025 revenue of $731 million reflects 7% growth year over year fueled by 12% product revenue growth including 27% systems revenue growth, showing strong demand despite a challenging macro environment. More impressively, non-GAAP EPS of $3.42 represented 18% year-over-year growth, demonstrating operational leverage as the business scales.

The product mix evolution tells the real story. Systems revenue of $179 million in the quarter, up 27% year-over-year, while software revenue was flat at $158 million. This might seem counterintuitive—isn't F5 supposed to be transitioning to software? But the systems growth reflects AI infrastructure demand. These aren't yesterday's load balancers; they're high-performance platforms handling AI workloads that can't be virtualized. The unveiling of the F5 Application Delivery and Security Platform (ADSP) represents the company's most significant product launch in years. The F5 ADSP is the industry's only platform that fully converges high-performance load balancing and traffic management with advanced app and API security capabilities. This isn't incremental improvement—it's architectural transformation designed for the AI era.

96% of organizations are currently deploying AI models. As organizations rush to realize the benefits of AI, they also recognize growing cybersecurity challenges inherent in the distributed nature of AI apps. In fact, security is the number one concern about AI models, followed by cost of compute and performance. F5 is positioning ADSP as the answer to these concerns.

Strategic partnerships are accelerating adoption. The MinIO collaboration for AI data pipelines, NVIDIA integration for DPU acceleration, and Azure NGINXaaS expansion demonstrate F5's ecosystem approach. These aren't just technology integrations—they're go-to-market multipliers that embed F5 deeper into enterprise AI infrastructure. Wall Street sentiment reflects measured optimism. According to 46 analysts, F5 Networks (FFIV) has a Buy consensus rating as of Aug 20, 2025, though F5 Networks has a consensus rating of Hold which is based on 3 buy ratings, 9 hold ratings and 0 sell ratings. Based on analyst ratings, F5 Networks's 12-month average price target is 327.56, suggesting modest upside from current levels.

The analyst community recognizes the execution strength but questions the growth trajectory. The analysis indicates a negative outlook for F5's stock primarily due to several underlying financial challenges, including a weak growth trajectory in the EMEA region which comprises 46% of its revenue, alongside execution issues and macroeconomic headwinds leading to delayed deals. The company has consistently missed consensus forecasts for billings in 6 of the last 8 quarters, driven by slower product growth and a lack of traction with service provider customers.

Yet recent earnings beats have shifted sentiment. The latest price target for F5 (NASDAQ:FFIV) was reported by RBC Capital on April 29, 2025. The analyst firm set a price target for $290.00, while F5 Networks price target raised to $355 from $304 at Piper Sandler, showing divergent views on the company's prospects.

XIII. Links & Resources

Company Resources: - F5 Investor Relations: investor.f5.com - F5 Application Delivery and Security Platform: f5.com/products/f5-application-delivery-and-security-platform - F5 2025 State of Application Strategy Report: f5.com/company/reports/state-of-application-strategy-2025 - F5 Technical Documentation: docs.f5.com - NGINX Documentation: docs.nginx.com

Industry Reports & Analysis: - Enterprise Management Associates (EMA) Vendor Vision 2025 Report - IDC Research on Application Delivery Controllers - Gartner Magic Quadrant for Application Delivery Controllers - Forrester Wave: Web Application Firewalls

Key Interviews & Media: - F5 Earnings Calls Archive: investor.f5.com/events-and-presentations - François Locoh-Donou CEO Interviews on YouTube - F5 AppWorld Conference Recordings - NGINX Open Source Community: nginx.org

Books & Educational Resources: - "Building Microservices" by Sam Newman - Understanding modern application architecture - "Site Reliability Engineering" by Google - The practices F5's customers implement - "The Phoenix Project" by Gene Kim - DevOps transformation that drives F5's market - F5 University Training Programs: university.f5.com

Competitive Intelligence: - Cisco Application Centric Infrastructure resources - AWS Application Load Balancer documentation - Azure Application Gateway guides - Cloudflare Load Balancing technical specs

Historical Analysis: - SEC EDGAR Filings: All F5 10-K and 10-Q reports since IPO - Historical stock charts and trading data: finance.yahoo.com/quote/FFIV - Wayback Machine archives of F5.com showing product evolution - Dot-com era coverage from Internet Archive

Customer Case Studies: - Fortune 500 F5 deployments - Cloud migration success stories - AI infrastructure implementations - Financial services security architectures

Open Source & Developer Resources: - NGINX GitHub repositories - F5 DevCentral Community: devcentral.f5.com - iRules Codeshare Library - F5 Terraform Provider documentation

Market Analysis Tools: - Network infrastructure market sizing reports - Application security market forecasts - Multi-cloud adoption surveys - AI infrastructure investment trends

Final Reflections: The Infrastructure Paradox

After tracing F5's journey from a Seattle startup to a $15 billion infrastructure giant, one paradox emerges: the most valuable technology companies are often the ones you never think about. F5 doesn't make headlines like OpenAI or capture imaginations like Tesla. It doesn't have consumer brand recognition or viral products. What it has is something more valuable—indispensability.

The genius of F5's positioning across three decades has been recognizing that in the digital economy, reliability trumps innovation. When enterprises evaluate infrastructure, they're not looking for the newest features or the slickest interface. They're looking for the technology that won't fail when it matters most. F5 built its empire on that promise.

The transformation from hardware to software to platform wasn't just a business model evolution—it was a masterclass in market timing. Each pivot came just before the previous model became commoditized. The NGINX acquisition wasn't about buying technology; it was about buying relevance with a new generation of developers. The push into AI security isn't speculation; it's positioning for where the puck is going.

What makes F5's story particularly instructive is how it survived multiple extinction events. The dot-com crash should have killed it. The rise of cloud providers should have made it obsolete. Open source alternatives should have commoditized its business. Yet F5 not only survived but thrived by understanding a fundamental truth: complexity creates opportunity.

As enterprises juggle on-premises systems, multiple clouds, edge deployments, and now AI workloads, the complexity isn't decreasing—it's compounding. Every new technology wave creates new traffic patterns, new security vulnerabilities, new performance challenges. F5 has positioned itself as the universal translator in this Tower of Babel, the Switzerland of the cloud wars.

The bear case remains real. Cloud providers continue building competitive solutions. Open source alternatives improve daily. The hardware business faces structural decline. But betting against F5 is betting that enterprise IT will somehow become simpler, that security threats will diminish, that applications will become less critical. History suggests otherwise.

Looking ahead, F5's challenge isn't technological—it's organizational. Can a company with enterprise DNA truly embrace developer-first thinking? Can a business built on high-margin hardware successfully transition to software and services? Can an organization that thrived on complexity help customers achieve simplicity?

The early returns are promising. The ADSP platform shows F5 can innovate at the architectural level. The AI investments demonstrate forward thinking. The financial performance proves the business model transition is working. But the ultimate test will be whether F5 can maintain its relevance as the definition of "application" continues to evolve.

In the end, F5's story is about the unsexy but essential work of keeping the digital world running. It's about recognizing that in technology, the companies that own the plumbing often outlast those that build the palaces. It's about understanding that true competitive moats aren't built on features but on trust, earned over decades of keeping the lights on when others couldn't.

For investors, F5 represents a particular type of opportunity—not the explosive growth of emerging technology, but the steady compounding of essential infrastructure. It's the toll booth on the digital highway, collecting fees not because it's innovative but because it's necessary.

For founders, F5's journey offers crucial lessons. First, timing matters more than technology. Second, surviving downturns creates unassailable competitive advantages. Third, the willingness to cannibalize your own business beats being disrupted by others. Fourth, in enterprise technology, trust is the ultimate currency.

As we stand on the precipice of the AI revolution, with every company scrambling to deploy large language models and every application becoming "AI-powered," F5's role becomes even more critical. Someone needs to manage the traffic, secure the data, optimize the performance. Someone needs to make sure it all works.

That someone, for nearly three decades and counting, has been F5. The company that started by solving internet traffic jams has evolved into the nervous system of digital business. In a world where every company is a technology company, where every application is mission-critical, where every millisecond matters, F5 isn't just relevant—it's essential.

The infrastructure paradox remains: the most important technology is often the most invisible. F5 has built a $15 billion business on that invisibility, on being the technology that just works, that enterprises trust with their most critical applications. As long as the digital world keeps growing more complex—and there's no sign it won't—F5's story is far from over.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube