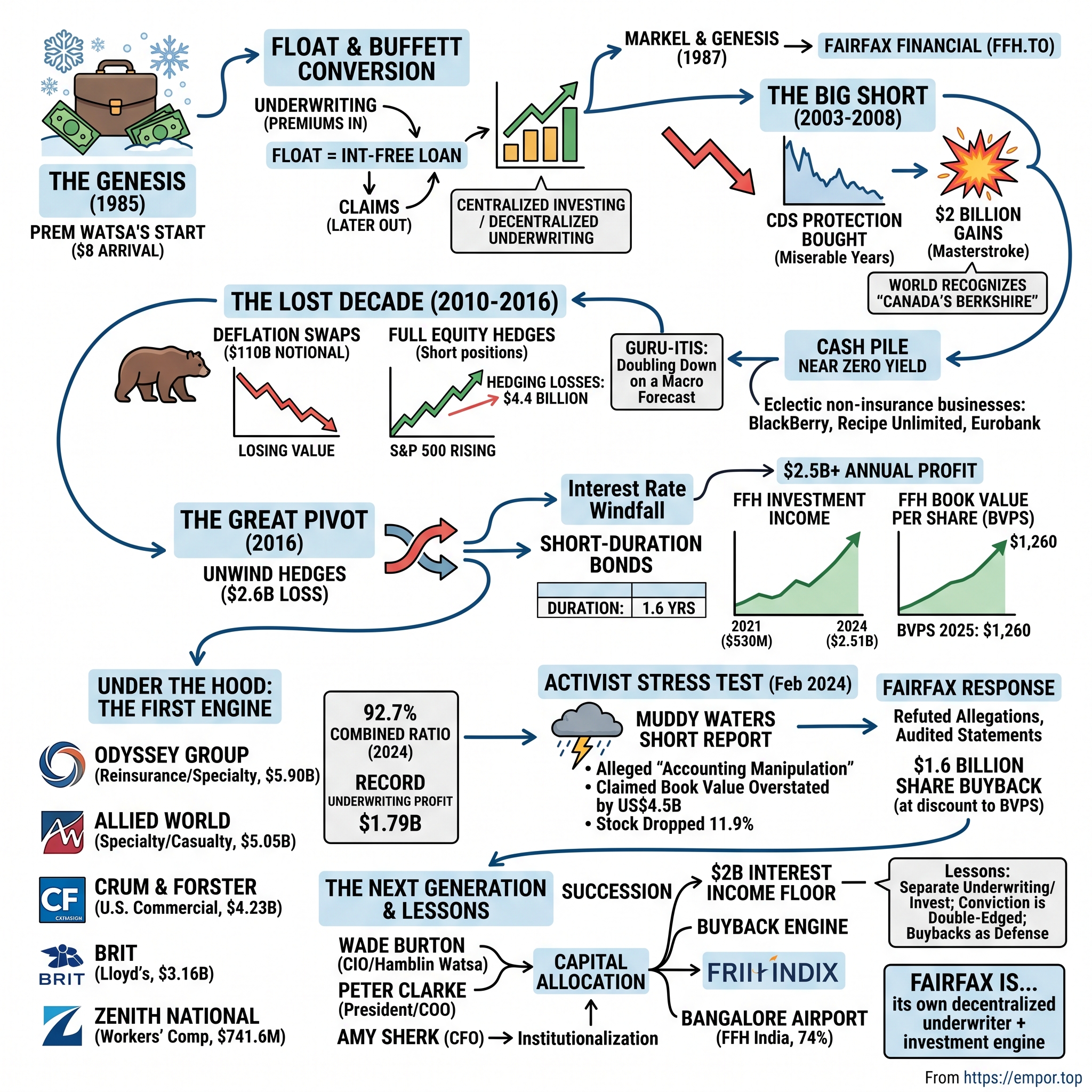

Fairfax Financial Holdings: The Great Pivot and the Billions Under the Hood

I. Introduction: Canada's Berkshire and the Anatomy of a Masterstroke (00:00 – 00:15)

On the morning of Thursday, February 8, 2024, a 72-page document landed on the internet and detonated. It carried the logo of Muddy Waters Research and the byline of Carson Block, the short seller who had made his name in 2011 exposing the Chinese timber fraud Sino-Forest. His new target was not an obscure Nasdaq shell company. It was Fairfax Financial Holdings, a $30-billion Toronto insurer routinely described as "Canada's Berkshire Hathaway," run by an immigrant investor whom the financial press had crowned the country's answer to Warren Buffett. Block's thesis was blunt: Fairfax, he argued, "has consistently manipulated asset values and income by engaging in often value-destructive transactions to produce accounting gains," and roughly 60% of the growth in the company's book value since 2017 was "the product of abusive accounting."3 He put a number on it — the balance sheet, he claimed, was overstated by about US$4.5 billion, or some 18%.34 By the closing bell, Fairfax shares had fallen 11.9% on the Toronto Stock Exchange, their worst single day since the COVID crash of 2020.4

It is the kind of moment that ends companies, or at least maims them for years. Except this one didn't. Fast-forward to the present, and Fairfax's book value per share — the crude yardstick Block accused management of inflating — has kept climbing, from $939.65 at the end of 2023 to $1,059.60 at the end of 2024 and $1,260.19 at the end of 2025.12 The stock trades at all-time highs. The company reported the best year in its history in 2025, with record net earnings of $4.77 billion.2 The short seller, by every visible measure, is underwater.

So the question this story has to answer is not simply "was Muddy Waters right?" It is the more interesting one: how did a company that spent most of the 2010s as a cautionary tale — a value investor's value trap, bleeding billions on doomsday hedges — reposition itself so completely that, when the most feared short seller in the world came knocking, it could answer him not with a press release but with a $1.6-billion share buyback?1

The honest framing is that Fairfax is not a carbon copy of Berkshire. The Buffett comparison flatters and misleads in equal measure. What Fairfax actually is: a sprawling, deliberately decentralized global underwriting machine, stitched together from insurers most North Americans have never heard of — Odyssey Group, Allied World, Crum & Forster, Brit, Zenith — that together wrote roughly $25 billion of net premiums in 2024 and produced $1.79 billion of pure underwriting profit at a 92.7% combined ratio.1 Sitting on top of that insurance engine is an investment portfolio of about $70 billion.2 For a decade, that portfolio was managed with a pessimism so extreme it nearly broke the company. Then, in one of the better-timed pivots in modern finance, management flipped the portfolio into short-dated bonds and cash just as interest rates exploded higher — turning a sleepy stream of coupon income into more than $2.5 billion a year of nearly-guaranteed profit.12

Hold both of those facts in mind at once, because the tension between them is the whole story. Here is a company whose founder was mocked as a permabear, whose stock spent years dead money, whose balance sheet a serious short seller called a fiction — and which has, over the past three years, produced some of the best results in its four-decade history while retiring its own shares by the millions. Skeptics would say Fairfax got lucky: it happened to be positioned defensively when a once-in-a-generation inflation shock rewarded defense. Defenders would say luck is what happens when a disciplined, conservative balance sheet meets a market that finally moves your way. The truth, as usual, is some of both, and a neutral investor's job is to figure out how much of the recent success is repeatable engine and how much is one-time weather.

There is also a subtler reason this is the right moment to tell the Fairfax story, beyond the drama of the short attack. The company is quietly handing over its controls. The men and women now running the underwriting subsidiaries and, crucially, the investment portfolio are largely not the ones who built the legend — and the founder who holds the votes is 75. A business that was, for most of its life, an extension of one person's judgment is being converted, deliberately and in public, into an institution. Whether that conversion preserves the discipline while shedding the overconfidence is the question that will define the next decade of returns, and it is a question the numbers alone cannot answer.

This is the arc we'll trace. It begins with a man who arrived in Canada with, by his own telling, eight dollars, and bought a nearly bankrupt trucking insurer. It runs through the greatest macro trade in Canadian financial history — and the intellectual trap that victory set. It passes through a "lost decade" of hedging losses, the great repositioning that redeemed it, a tour of the underwriting subsidiaries that quietly do the real work, the Muddy Waters war, and finally the succession question hanging over the whole enterprise: what is Fairfax worth once its founder, now 75, is no longer the one holding the votes?

Let's start at the beginning, with the float.

II. The Genesis: Prem Watsa, Markel Financial, and the Foundations of Float (00:15 – 00:35)

The founding legend of Fairfax has one indelible image at its center: a young man landing in a Canadian winter with almost nothing in his pocket. Vinodh Prem Watsa was born in Hyderabad, India, in August 1950, one of a large family, and arrived in Canada in 1972 as one of a few thousand landed immigrants that year.6 He carried, the story goes, roughly eight U.S. dollars, and paid his way through a master's degree at the Richard Ivey School of Business at the University of Western Ontario by selling furnaces and air conditioners door to door.67 Whether the "$8" is literal or burnished by four decades of retelling almost doesn't matter; it has become the origin myth precisely because it dramatizes the distance Watsa traveled and the frugality that would define him.

The intellectual conversion came when Watsa encountered Warren Buffett's shareholder letters and understood the mechanism at the heart of Buffett's Berkshire: insurance float. The idea is deceptively simple, and worth pausing on because it is the entire foundation of everything Fairfax became. An insurer collects premiums today and pays claims sometime later — months, years, occasionally decades later. In between, it holds a large pool of other people's money. If the underwriting merely breaks even — premiums in roughly equal to claims and expenses out — then that float is, in effect, an interest-free loan the insurer gets to invest for its own account. Do the underwriting at a genuine profit, and you are being paid to borrow money to invest. For a gifted investor, it is the closest thing in capitalism to a perpetual motion machine.

The elegance of the model is also its trap, and it is worth naming the trap early because Fairfax spent a decade caught in it. Float is only free if the underwriting stays disciplined and the investing stays sound. Break either leg — write reckless policies to grow the float, or invest the float badly — and the leverage that makes insurance magical in good times amplifies the pain in bad. A conventional company that makes an investing mistake loses its own money; an insurer that makes one loses money it borrowed from policyholders, against claims it still has to pay. Watsa understood the upside of that leverage from the Buffett letters. What the next forty years would teach him, expensively, is the downside.

In 1984, Watsa co-founded an investment firm, Hamblin Watsa Investment Counsel, with his former supervisor Tony Hamblin.7 A year later, in 1985, he and his partners took control of Markel Financial Holdings, a small, nearly insolvent Canadian trucking-insurance company — the vehicle, quite literally, that would carry the float.7 In May 1987 he renamed it Fairfax Financial Holdings, a compression of "fair, friendly acquisitions," a phrase meant less as marketing than as a genuine operating creed.67

That creed encoded a specific and unusual philosophy of control, one that inverts how most conglomerates behave. Fairfax would decentralize underwriting completely — each acquired insurer would keep its own name, its own management, its own local authority to price risk — while centralizing investing completely, funneling every subsidiary's float up to Hamblin Watsa to manage as one pool. The logic: insurance underwriting is a local, relationship-driven, judgment-heavy craft that head office cannot do from a distance, whereas capital allocation benefits from concentration and a single disciplined hand. Trust the locals with the risk; never let them near the money.

To protect that structure from the quarterly demands of public markets, Watsa built himself a fortress of control. Through a private holding company, Sixty Two Investment, he holds Fairfax's multiple-voting shares, which give him roughly 43% of the vote on a far smaller slice of the actual economics — a stake that a 2015 reorganization reinforced by raising the votes per multiple-voting share while capping his voting power at just under 42%.8 The arrangement is the subject of perennial governance grumbling, and we'll return to it, but its intent is coherent: to let Watsa run the company for owners who think in decades.

Nothing illustrates that posture better than his pay. Watsa has drawn a flat salary of C$600,000 for decades — no cash bonus, no stock options, no long-term incentive plan.8 For the chief executive of a company that now earns billions, it is an almost eccentric figure, and a deliberate one: his wealth is meant to compound only alongside other shareholders', through the subordinate voting shares he owns rather than through pay. It is the kind of gesture that reads as either principled alignment or as a controlling shareholder's way of signaling that he answers to no compensation committee — and in fairness to the skeptics, both readings are true at once. A founder who takes a modest salary and holds the votes has aligned his cash flow with yours while insulating his job from your opinion of him.

That is the governance bargain at the heart of Fairfax, and it is worth stating plainly because it recurs throughout this story. The dual-class structure that lets Watsa control the company on a minority of the economics is exactly the arrangement that let him keep the disastrous equity hedges on for years over shareholder objections — and also the arrangement that let him ignore short-term pressure and hold the winning trades for years when Wall Street was mocking him. You cannot have one without the other. An investor buying Fairfax is buying a company where the buck genuinely stops with one man, for better and worse, and pricing that reality is part of the analysis rather than a footnote to it.

Through the 1990s the machine scaled fast on this template, acquiring the U.S. commercial insurer Crum & Forster in 1998 and building out the reinsurer OdysseyRe, with Hamblin Watsa managing the swelling pile of float behind it all.7 By the early 2000s Fairfax had the size to matter. What it needed was a trade that would make the world take Watsa seriously as an investor. It was about to get the biggest one imaginable — and to learn, the hard way, what winning it would cost.

III. The Masterstroke and the Curse of "Guru-itis" (00:35 – 01:00)

Picture Hamblin Watsa's Toronto offices around 2003. The U.S. housing market is beginning its historic ascent, Wall Street is minting money securitizing mortgages, and the consensus view is that American home prices simply do not fall on a national basis. Inside Fairfax, the credit team is reaching the opposite conclusion. Digging through the plumbing of the mortgage machine — the loosening underwriting standards, the leverage stacked on leverage, the fragility of the banks and insurers guaranteeing it all — they decide the entire edifice is rotten. And they decide to bet on it.

The instrument they chose was the credit default swap, or CDS. In plain terms, a CDS is an insurance policy on someone else's debt: you pay a small annual premium, and if the borrower runs into trouble, the contract pays off, often many multiples of what you put in. Fairfax began buying CDS protection on the financial institutions and structured credits most exposed to subprime mortgages. For several years it was a miserable position to hold. The premiums bled out quarter after quarter with nothing to show for it, the housing boom rolled on, and the trade sat there as a visible drag on reported results while critics questioned Watsa's judgment.

To understand why this took nerve, sit with the discomfort of holding it. A CDS position that is out of the money is a slow, visible drain: every reporting period, the premiums leave, the mark sits at a loss, and analysts ask why management is burning shareholder capital on a bet against the very system that was minting record profits everywhere else. Value investors are supposed to buy cheap assets and wait; this was the opposite — paying a recurring toll for the right to be proven right later, with no guarantee "later" would ever come. Most institutions that even considered the trade could not stomach the carrying cost or the career risk of looking foolish for years. Watsa could, precisely because of the control structure that let him ignore the quarterly scoreboard.

Then the world caught up to the thesis. As the mortgage market cracked in 2007 and the financial system seized in 2008, the CDS contracts Watsa had bought for pennies became worth fortunes. In 2007 alone, Fairfax booked net gains of more than $1.1 billion related to credit default swaps, a central reason its investment income that year hit a then-record.9 As the crisis deepened, the firm harvested the position, and the cumulative proceeds from what Watsa later simply called "the Big Short" ran to roughly $2 billion — an almost unimaginable return on the original premiums.98 While Lehman Brothers collapsed and storied insurers begged for bailouts, Fairfax's book value and liquidity surged. It was, by any measure, a masterstroke.

It also anointed Watsa. The global financial press reached for the obvious label — Canada's Warren Buffett, the value investor who had seen the crash coming — and a genuinely brilliant credit call hardened into a reputation for macroeconomic prophecy.6 And here is where the story turns, because the most dangerous thing that can happen to an investor is to win an enormous bet for exactly the reasons he thought he would. It breeds a conviction that the framework is not just useful but oracular.

Call it guru-itis. Having correctly foreseen one deflationary shock, Watsa became convinced a second, larger one was coming — that the 2008 crisis was a prelude to a 1930s-style depression, that the mountain of debt in the system had to unwind in a wave of falling prices and falling markets. It was not a crazy view in 2010; plenty of serious people held some version of it. The error was not the thesis itself but the refusal to let it be falsified — the decision to build the entire investment portfolio around a forecast, and to keep doubling down as the evidence piled up against it.

Here the contrast with the very man Watsa was compared to is instructive. Buffett's genius has always included a temperamental refusal to bet the company on macro forecasts; he buys businesses and largely ignores what he cannot predict. Watsa's version of "Canada's Buffett" diverged on exactly this point. Having won by predicting a macro event, he concluded that predicting macro events was his edge — and then wagered the balance sheet on the next prediction. It is a seductive and very human error: success attributed to skill invites more of the same behavior, even when the first success owed as much to a specific, checkable credit analysis as to any gift for prophecy. The 2008 CDS trade was, at bottom, granular bottom-up work on the fragility of specific counterparties. The bet that followed it was top-down faith about the direction of the whole world. Fairfax treated them as the same kind of insight. They were not. The very trade that made Watsa famous became the reason Fairfax would spend the next ten years fighting the market, and mostly losing. The bill for being early, and then being wrong, is the subject of the next chapter.

IV. The Lost Decade: The Cost of Fearing the Future (01:00 – 01:30)

The 2010s should have been a golden decade for a company built to compound. Instead, Fairfax spent them braced for a catastrophe that never arrived. Convinced that a deflationary reckoning loomed, Watsa turned the investment portfolio into an elaborate hedge against the apocalypse — and the apocalypse, inconveniently, was cancelled in favor of the longest bull market in history.

The centerpiece was the equity hedge. Beginning in 2010, Fairfax fully hedged its common-stock portfolio, taking short positions against broad equity indices — the S&P 500 chief among them — so that if stocks crashed, the shorts would pay off and protect the book.9 The logic is sound in a vacuum; the problem is that "protection" against a rising market is just a bet against it. Through the greatest equity rally of modern times, the shorts bled money relentlessly, year after year. Watsa layered on a second, more exotic wager: deflation swaps, derivatives tied to consumer-price indices that would pay off if the U.S. or Europe tipped into outright deflation. Fairfax accumulated an eye-watering $110 billion in notional deflation protection.910 Inflation stayed positive; the swaps withered toward worthlessness.

The scale of the damage is startling when you see it laid out. In his 2016 letter to shareholders, Watsa disclosed that since fully hedging in 2010 the company had absorbed $4.4 billion of cumulative net hedging losses, plus roughly $0.5 billion of unrealized losses on the deflation swaps.9 These were not paper abstractions bleeding into some footnote; they were real capital, torched fighting a bear market that never came. A company whose entire reason for existing was to compound float had spent the decade shrinking it through the investment account.

There was a second, quieter drag running alongside the hedges. Fearful of a banking collapse, Hamblin Watsa kept a huge share of the portfolio in cash and ultra-short government bonds. In a normal world, prudent. But the 2010s were the era of zero interest-rate policy, when parking tens of billions in cash and T-bills earned almost nothing. So while the hedges lost money outright, the defensive cash pile earned a return indistinguishable from zero — a colossal opportunity cost measured against the equities and corporate credit compounding all around it. Berkshire's stock portfolio soared; peer insurers rode a hardening market; Fairfax's book value crawled ahead in low single digits, and its shares languished at a discount to book. Shareholders, reasonably, grew furious.

It is hard to overstate how corrosive this period was to the Fairfax narrative, because the damage was not only financial but reputational. For years, Watsa's letters kept promising that the deflationary reckoning was near, that the hedges were insurance the company would be grateful to hold. Every year the market rose, the promise looked more like stubbornness and less like prudence. The gap between what management said would happen and what actually happened is the single most important data point in assessing Fairfax's credibility — and, to Watsa's credit, he did not hide from it. His annual letters increasingly acknowledged the hedges were a mistake in plain language, a rare thing among founders, who more often bury errors in euphemism or blame the weather. That candor is a genuine mark in management's favor, and worth weighing against the substance of the error. But candor about a mistake does not undo the mistake, and shareholders who held through the decade paid for the lesson in foregone returns they will never recover.

Reaching for returns the hedges and cash could not provide, Fairfax also pushed capital into an eclectic pile of distressed and non-insurance businesses — a stake in the smartphone maker BlackBerry, backstopped in 2013 with a US$1-billion convertible debenture; the Canadian restaurant group later taken private as Recipe Unlimited for roughly $954 million; Thomas Cook India; a growing bet on Greece's Eurobank; and eventually a separately listed India-focused vehicle, Fairfax India, launched in 2015 to raise about US$1 billion.11 Some of these would prove shrewd. But collectively they did something corrosive to the stock: they turned a company that was supposed to be a clean insurance compounder into a bewildering, illiquid grab-bag that no analyst could cleanly value — the "diworsification" that would, years later, give a short seller his opening. By the middle of the decade, Watsa faced the hardest task an investor of conviction ever faces: admitting the thesis was wrong and dismantling it. That reckoning is where the turnaround begins.

V. The Great Pivot & The Interest Rate Windfall (01:30 – 02:00)

Every great turnaround has a moment of capitulation, and Fairfax's came on the night of November 8, 2016. As the U.S. election result rolled in and markets began pricing a shift toward growth, tax cuts, and — crucially — inflation, Watsa did something he had resisted for six painful years: he surrendered. "The world changed for us," he wrote afterward, and Fairfax "reacted quickly by removing all our index hedges and some of our individual short positions."9 The cost of that single unwind was brutal — a realized loss of $2.6 billion — and it helped push Fairfax to a rare annual net loss for 2016.910 But the significance was not the loss; it was the concession. After a decade of insisting the depression was coming, Watsa was tearing down the fortress he had built against it.

What makes the pivot analytically interesting is what came next, because unwinding a bad bet is only half the job — the harder half is redeploying the capital before the world moves again. Here Fairfax got both the strategy and the timing right, and it is worth being precise about who did what. The equity shorts were gone by 2017. But the truly consequential move was on the bond side, and it unfolded under the rising influence of a new generation of operators, notably Peter Clarke, a two-decade Fairfax veteran who was named President and Chief Operating Officer in February 2022.17 Rather than reach for yield in long-dated bonds — the reflex of most insurers starved for income after a decade of ZIRP — Fairfax deliberately kept its enormous fixed-income portfolio short, concentrated in cash, treasury bills, and bonds maturing in just a year or two.

For most of 2020 and 2021 that positioning looked merely cautious, even lazy; short bonds yielded almost nothing. It is worth appreciating how counterintuitive the stance was at the time. In 2020 and 2021, the entire institutional world was reaching out the yield curve — buying longer-dated bonds and riskier credit — because short paper paid nothing and the pressure to generate income was relentless. Fairfax did the opposite, accepting near-zero yields on short bonds rather than lock in low long-term rates. To a yield-starved analyst it looked like management leaving money on the table. In hindsight it was one of the most valuable decisions the company ever made, because a short bond has a hidden feature that a long bond lacks: it matures quickly and hands your cash back, ready to be redeployed at whatever the new rate happens to be. Long bonds, by contrast, lock you in — and if rates rise, their market value falls, sometimes brutally.

Then came the great inflation shock of 2022, and central banks hiked rates at the fastest pace in forty years. This is the pivot's payoff, and it has two halves. First, defense: because Fairfax's bonds were so short — a portfolio duration of roughly 1.6 years — they barely moved when rates spiked. While long-duration bond portfolios across the industry suffered savage mark-to-market losses in 2022, Fairfax's roughly $38-billion fixed-income book fell just 2.9%.11 To grasp what that meant, consider that some peers holding long bonds saw double-digit percentage declines in their fixed-income portfolios that year — losses that, for a leveraged insurer, can vaporize a chunk of capital in a single reporting period. Fairfax simply sidestepped it. Second, offense: as the short bonds matured, Fairfax got to reinvest tens of billions at suddenly much higher yields. The effect on income was electric.

The numbers tell the story cleanly. Consolidated interest and dividend income, which had been running at an annualized pace of roughly $530 million at the end of 2021, jumped to about $962 million for full-year 2022 — and Watsa told shareholders the run-rate had already reached roughly $1.5 billion.11 It kept climbing: interest and dividend income reached $1.90 billion in 2023, $2.51 billion in 2024, and $2.57 billion in 2025.12 Nearly the entire jump flowed straight to the bottom line, because coupon income on high-grade short bonds carries essentially no cost to produce. This is the crucial point about the pivot's quality: this is about the most durable, lowest-risk profit an insurer can earn — not trading gains that might reverse, not illiquid private marks a skeptic can dispute, but contractual interest on government and investment-grade paper.

The result was an inflection in book value per share that redeemed the lost decade almost completely. Having crawled for years, book value grew 14.5% in 2024 (on a dividend-adjusted basis) to $1,059.60, then 20.5% in 2025 to $1,260.19.12

There is an important analytical subtlety here that separates a lucky windfall from a repositioning worth respecting. The bond move was not a bet that rates would rise — Watsa has been candid that he did not forecast the exact inflation shock. It was a decision to stay short and liquid so that whatever happened, Fairfax kept its optionality. If rates had stayed at zero, the cost was modest: a little foregone yield. When rates instead exploded, the payoff was enormous. That is an asymmetric position — small, bounded downside, large upside — which is precisely the shape of bet a disciplined allocator wants and the opposite of the equity hedges, where the downside proved effectively unbounded across a decade. The lesson Fairfax appears to have internalized from the lost decade is not "predict better" but "position so that being wrong is survivable and being right is transformative."

The obvious caution is that a windfall born of high interest rates lives and dies by high interest rates — which is exactly the bear case we'll test later. But there is no honest way to describe the repositioning as anything other than vindication of the second engine. And underneath the investment fireworks, something quieter and arguably more important had been happening to the first engine — the insurance machine itself.

VI. Under the Hood: The Decentralized Underwriting Powerhouses (02:00 – 02:25)

Ask a casual observer what Fairfax does and you'll hear about Watsa, the hedges, the macro bets. Ask what it is, and the answer is more prosaic and more impressive: it is one of the larger property-and-casualty underwriting groups in the world, and in 2024 it turned in the best underwriting year of its life — a consolidated combined ratio of 92.7% and record underwriting profit of $1.79 billion, with 2025 nudging both further to 93.0% and $1.82 billion.12 The combined ratio is the single most important number in insurance, so it's worth translating: it is losses plus expenses divided by premiums, and anything under 100% means the company made money on the insurance itself — before earning a cent on the float. At roughly 93%, Fairfax keeps about seven cents of underwriting profit on every premium dollar, and gets to invest the float on top of that. That is the machine working as designed.

Before the tour of subsidiaries, one more point on why underwriting profit matters more than the raw dollar of it. An insurer that runs at a combined ratio below 100% is being paid to hold float — the investment income we spent the last section on is earned on money the underwriting side is also profiting from. Stack a 93% combined ratio on top of a portfolio yielding well over 4%, and the two engines compound each other: the better the underwriting, the more float there is to invest, and the cheaper that float is. A rival running at 100% — breaking even on insurance — has the same investment opportunity but none of the underwriting cushion. This is the mechanism, more than any single acquisition, that explains how Fairfax's returns can outrun its peers' when both engines run at once. It is also why a slide in the combined ratio would be far more alarming than a bad quarter of investment marks.

What makes it work is the decentralization. Fairfax does not underwrite as one giant. It owns a federation of specialists, each with its own leadership, its own niche, and its own authority to walk toward or away from risk as its local market dictates. Here are the five that matter most, though a sixth — the Canadian commercial insurer Northbridge, which wrote $2.23 billion of net premiums in 2024 — rounds out the group and anchors Fairfax's home market.1

Odyssey Group is the largest, with $5.90 billion of net premiums written in 2024.1 It is Fairfax's global reinsurance and specialty arm — a business that insures other insurers against big, lumpy catastrophe risk, plus specialty lines through its Hudson and Newline units. Its edge is scale: reinsurance is a game of capacity and diversification, where only balance sheets large enough to absorb a bad hurricane season can credibly write the biggest treaties. In Hamilton Helmer's language, this is scale economics, and it is real. Odyssey is also ground zero for the succession story: Brian Young led it through 2024, and on January 1, 2025, Carl Overy — a fifteen-year Odyssey veteran who ran its London market business — became chief executive, while Young moved up to president of the broader Fairfax Insurance Group.14

Allied World, with $5.05 billion of net premiums written in 2024, is the trophy acquisition.1 Fairfax bought it in a deal that closed in 2017 for roughly $4.9 billion — its largest ever — at approximately 1.3 times book value (closer to 1.37 times on a diluted basis).18 At the time, critics called the price rich for a company with no obvious moat. Nearly a decade on, the verdict is kinder: under CEO Louis Iglesias, Allied World has consistently written specialty and casualty business at combined ratios in the high-80s to low-90s, throwing off exactly the disciplined underwriting profit the acquisition thesis promised. It is a useful reminder that in insurance, paying up for a genuinely well-run underwriter can beat buying a mediocre one cheap — the price of entry matters less than the quality of the risk selection you're buying.

Crum & Forster, at $4.23 billion of net premiums written, is the diversified U.S. commercial specialist Fairfax has owned since 1998, run by Marc Adee.1 Its strength is breadth and craft across niche lines — from accident and health to a fast-growing pet-insurance business — where the edge is not scale but expertise: the accumulated, hard-won knowledge of how to price and settle unusual risks that generalist carriers misjudge. Brit, at $3.16 billion, is Fairfax's platform at Lloyd's of London, the centuries-old specialty market, led by Martin Thompson.1 Brit writes global specialty and catastrophe risk and is, by design, more exposed to a bad cat year than the others — a higher-beta underwriter that leans on sophisticated reinsurance protection to cap its worst outcomes.

Zenith National, the smallest of the five at $741.6 million, is a pure-play U.S. workers'-compensation specialist.1 Its story is the clearest illustration of the whole Fairfax philosophy. Workers' comp is viciously cyclical; when the market softens and rivals cut prices to chase volume, Zenith's discipline is to shrink — to let premium walk out the door rather than write business that will lose money — and then to grow again when rates harden. That willingness to get smaller on purpose is the underwriting culture Fairfax prizes above all, and it too changed hands on January 1, 2025, when Davidson Pattiz stepped up from COO to CEO.15

The counterargument a critic would press is that decentralization is not free. A federation of semi-autonomous underwriters is harder to supervise than a single centralized book; risk can accumulate in corners head office does not see until a catastrophe or a reserving miss reveals it. Insurance history is littered with groups that decentralized authority and discovered, too late, that a subsidiary had been writing garbage to hit growth targets. Fairfax's answer is cultural rather than procedural — it hires and promotes underwriters who share Watsa's temperamental aversion to writing unprofitable business, and it measures them on combined ratios rather than premium growth. That works until it doesn't, and it depends entirely on the quality of the people. Which is why the leadership transitions running through the group are not a human-interest sidebar but a core part of the risk assessment.

Step back and the industry structure explains why decentralization is not just a preference but an edge. In Porter's terms, this is a business of high rivalry — Fairfax fights giants like Chubb, Travelers, Munich Re, and Berkshire's own reinsurance arm for every risk — and of violently cyclical buyer power. In "soft" markets, brokers hold the whip hand and capital is cheap; in "hard" markets, when capacity vanishes after a run of catastrophes, underwriters dictate terms. Barriers to entry are real but porous: catastrophe reinsurance in particular attracts a flood of opportunistic "alternative capital" whenever returns look good, which competes prices back down — one reason no insurer, however disciplined, gets to keep pricing power for long. The single most valuable capability in that world is the ability to expand and contract fast, market by market, without waiting for head office. By pushing that authority down to CEOs like Overy, Adee, and Pattiz, Fairfax buys itself reflexes that a centralized rival simply cannot match. That same decentralized, hard-to-value structure, though, is precisely what a short seller decided to attack.

VII. The Activist Stress Test: The Muddy Waters War of 2024 (02:25 – 02:45)

Carson Block built his career on a simple insight: complexity hides sins. A sprawling, decentralized holding company with dozens of private stakes, joint ventures, and hard-to-price investments across the globe is, to a short seller, a target-rich environment — because "fair value" for an illiquid asset is ultimately a judgment call, and judgment calls can be nudged. When Muddy Waters turned that lens on Fairfax in February 2024, the report it produced was less an allegation of outright fraud than an argument that Fairfax's book value was an accounting artifact — that a meaningful slice of the wealth Watsa claimed to have created existed only in the marks.3

The specifics ranged across some thirteen investments, subsidiaries, and joint ventures. Muddy Waters focused on non-insurance holdings and what it characterized as favorable "fair value" markups on private and thinly traded stakes, and it reached for the most damning analogy in modern finance: Fairfax, Block wrote, was "far more akin to GE than to Berkshire Hathaway" — invoking the once-revered conglomerate whose reputation had curdled amid accounting concerns.3 The claim that a company modeled on Berkshire actually resembled late-stage GE was designed to wound, and the market flinched: the 11.9% one-day drop erased more than a billion dollars of value.4

It is worth being fair to Block about why the attack landed at all, because the vulnerability he exploited was structurally real rather than invented. When a company carries private and illiquid stakes at "fair value," those values are, at the margin, estimates — and estimates flow through the income statement as gains. A skeptic can always ask whether a mark reflects genuine economic value or management's preferred number, and there is rarely a way to prove the skeptic wrong until the asset is actually sold. Fairfax's decade of "diworsification" into an eclectic pile of non-insurance holdings had handed a short seller a broad, complicated surface to attack. The report was not persuasive because Fairfax was obviously fraudulent; it was persuasive because the company's own complexity made the accusation hard to instantly refute. That is a self-inflicted vulnerability, and one management had years to see coming.

Fairfax's response was fast, specific, and unusually aggressive. Within days it issued a rebuttal, and on February 12 followed with a longer statement declaring that it had reviewed all 72 pages and "categorically" denied and refuted the allegations as "false and misleading," "one-sided," and "ill-informed."5 Management's substantive defense had two planks worth taking seriously. First, process: the financial statements were prepared under IFRS and audited by PricewaterhouseCoopers, and many of the assets Block called subjective were in fact publicly traded and liquid — Eurobank, for instance, is a listed Greek bank whose price anyone can see, not a private mark management could invent. Second, and more powerful than any argument, was what Fairfax did with its cash.

Rather than fight only with words, Fairfax used the very thing the pivot had handed it — a torrent of high-quality investment income — to buy its own stock hand over fist. Over the course of 2024 the company repurchased 1,346,953 subordinate voting shares for cancellation at a cost of roughly $1.6 billion, an average of about $1,179 per share, well below its own stated book value.1 The logic here is worth spelling out, because it is the cleanest possible rebuttal to a "your book value is fake" attack: if management genuinely believed the shares were worth their $1,000-plus book value and the market was offering them below that, buying them back was both a vote of confidence and a mechanically accretive act — every share retired below book value raises book value per share for everyone who remains. If Block were right that the book value was inflated, Fairfax would have been overpaying; management bet, with more than a billion real dollars, that he was wrong.

There is a second-order point in the buyback that neutral analysis should credit: Fairfax was not buying back stock for the first time in a panic. Repurchasing shares below intrinsic value had been part of the capital-allocation playbook for years, which is what made the 2024 response credible rather than defensive theater. A company that suddenly launches an emergency buyback it has never done before is reacting; a company that simply does more of what it already does is executing. The distinction matters when judging whether the buyback was a genuine conviction signal or a stunt — the evidence points to the former.

By 2025 the market had rendered its verdict. The stock recovered and pushed to new highs, book value compounded another 20.5%, earnings hit records, and the buybacks continued — another 1,006,535 shares retired for about $1.63 billion.2 The short case, at least on the timescale that matters to a short seller, had failed. A neutral reading, though, should resist declaring the underlying question fully settled. Muddy Waters was refuted where it was most checkable — the liquid, marked-to-market holdings — and where it mattered most to sentiment. But the deeper structural critique it exploited remains a permanent feature of the Fairfax investment case: a decentralized empire of private and semi-private stakes genuinely is harder to value than a portfolio of listed stocks, and it genuinely does require investors to extend management a degree of trust that a simpler company would not. The buyback was a powerful answer. It was not a proof. And whether that trust is warranted going forward depends heavily on the people now taking the controls from Watsa.

VIII. The Next Generation: Succession & Capital Allocation (02:45 – 03:05)

The uncomfortable truth beneath every Fairfax bull case is that its greatest asset is also its greatest risk: a 75-year-old founder who holds the votes, sets the tone, and has been, for better and worse, the single point of judgment for nearly four decades.6 Watsa remains chairman and controlling shareholder, and shows no sign of stepping back from that role. But the more consequential story of the past few years is how deliberately the operating company has been built to run without him — how the key-man risk has been, if not eliminated, then meaningfully diffused across a bench of institutional successors.

The architect of that transition is Peter Clarke. A Fairfax lifer who spent two decades in roles spanning chief actuary, chief risk officer, and chief operating officer, Clarke was elevated to president and COO in February 2022, and he is, more than anyone, the face of the modern, disciplined Fairfax — the executive who oversaw the subsidiary leadership handoffs, the underwriting rigor, and the operational machinery behind the numbers.17 His résumé is itself a statement of what Fairfax now values. A chief risk officer and chief actuary is, by training, a person who thinks about tail losses and reserve adequacy — the unglamorous plumbing of whether an insurer has enough set aside to pay the claims it has promised. Elevating that profile to the presidency, rather than a charismatic dealmaker or a star investor, signals a company deliberately choosing operational discipline over flair in its post-founder identity. Whether that reads as reassuring prudence or as a loss of the entrepreneurial spark that built the company is a genuine judgment call, and reasonable investors land on both sides.

The generational transitions at Odyssey and Zenith on the same January 2025 date were not coincidences; they were the visible output of a succession plan running through Clarke's office, designed to entrench the next cohort of underwriting leaders while Watsa is still present to bless it.1415 The value of doing this while the founder is alive and engaged is easy to underestimate. Succession that happens on schedule, with the outgoing generation sponsoring the incoming one, tends to preserve culture; succession forced by a sudden death or ouster tends to fracture it. Fairfax is running the good version, which is a point in its governance favor even for skeptics of the control structure.

On the investment side — the seat that matters most, given that this is where Watsa's guru-itis nearly sank the company — the change is even more significant. Wade Burton is now president and chief investment officer of Hamblin Watsa, the subsidiary that runs the group's tens of billions in float. The symbolism is hard to overstate: the single-man macro bet, the concentrated all-or-nothing conviction call that produced both the Big Short and the lost decade, is being replaced by a more team-driven, fundamentals-first process focused on high-quality credit and total-return positions in core equities. Whether that institutionalization dilutes the occasional genius that produced the 2008 windfall, or simply removes the overconfidence that produced the 2010s, is the open question — but as a governance matter, moving away from betting the firm on one person's macro forecast is plainly a reduction in risk.

There is a genuine tension worth sitting with here, because it cuts against the easy narrative that institutionalization is simply good. Fairfax's two greatest investment moments — the CDS trade and the short-duration bond positioning — were both products of exactly the kind of high-conviction, against-the-crowd judgment that a consensus-driven investment committee tends to sand down. Committees are good at avoiding disasters and bad at making the lonely, uncomfortable bet that looks wrong for years before it pays. So the same process that would have prevented the equity-hedge catastrophe might also have prevented the Big Short. An investor betting on Fairfax's future has to decide whether the company's edge was ever really Watsa's macro brilliance — in which case diluting it is a loss — or whether the edge was always the disciplined underwriting culture and the conservative balance sheet, with the macro calls a volatile sideshow that netted out to roughly zero across the decades. The latter reading is the more defensible one, and it is the one that makes the succession look like progress rather than decline.

The third pillar is financial. In March 2025, Amy Sherk became chief financial officer, stepping up after roughly two decades inside the Fairfax group, including a stint as CFO of Fairfax India, and succeeding Jennifer Allen, who moved into a newly created chief business officer role.16 Sherk's value is continuity and technical depth in exactly the area a skeptic worries about most: the complex, judgment-laden accounting of a global insurer with a tangle of consolidated and equity-accounted holdings. Placing a long-tenured insider who knows where every body is buried in the CFO chair, in the year after an accounting-focused short attack, is either reassuring or self-referential depending on your priors — but it is unambiguously a choice for institutional memory over a fresh outside pair of eyes.

Taken together, the picture is of a company consciously converting itself from a founder's vehicle into an institution. The operations run through Clarke, the money through Burton, the books through Sherk; Watsa increasingly holds the votes and the culture rather than the day-to-day levers. For long-term owners, this is the central non-financial question in the entire story — whether the discipline of the last several years is a permanent cultural feature or a temporary reflection of one man's belated humility. The answer will only be knowable in hindsight. What can be assessed today is the business's competitive position, and whether the case for it winning from here holds up under pressure.

IX. The Investment Spine: Why Win / Why Not (03:05 – 03:25)

Strip away the narrative and Fairfax's forward case rests on a two-engine design: an underwriting machine that makes money on the insurance, and a conservative investment portfolio that now makes serious money on the float. The bull argument is that both engines are firing at once for the first time in the company's history, and that each has a structural reason to keep running.

Start with the investment engine, because it is the one that changed everything. With roughly $70 billion in portfolio investments, a "higher-for-longer" rate environment hands Fairfax a baseline of well over $2 billion a year in high-margin interest and dividend income — money that requires no underwriting genius and carries minimal risk, because it is contractual coupon income on short, high-grade paper.2 That is a floor under earnings that simply did not exist in the ZIRP decade. On the underwriting side, the property-casualty and reinsurance markets have been in a disciplined "hard" phase, and Fairfax's specialists have been pricing risk at genuinely profitable levels, as the sub-94% combined ratios attest.12 Layer on the buyback engine — a company retiring more than a million shares a year below book value compounds intrinsic value for continuing holders almost mechanically12 — and you have three reinforcing sources of per-share growth.

Run it through the strategy frameworks and the picture is nuanced rather than triumphant. In Hamilton Helmer's 7 Powers, Fairfax's most defensible power is scale economics at Odyssey and in reinsurance, where balance-sheet size is a genuine barrier; there are elements of what one might call cornered expertise in Crum & Forster's niche lines and Brit's Lloyd's franchise. But it is important to be honest that insurance is, at the industry level, close to a commodity — capital chasing risk — with weak switching costs and no network effects. A commercial-insurance buyer renews with whoever offers the best price and terms; there is no lock-in like a software customer's, no ecosystem like a marketplace's. Fairfax's edge is less a structural moat than an operating one: a decentralized culture of underwriting discipline and a capital-allocation record that, the lost decade notwithstanding, has compounded book value at a high-teens rate over the long run. Operating advantages are real, but they are also more fragile than structural ones, because they depend on people continuing to make good decisions — which loops directly back to the succession question. A moat you can inherit is worth more than a moat that walks out the door at retirement.

An activist or skeptical long/short investor would press three further points, and a fair analysis should name them rather than wave them away. First, portfolio complexity: even after the Muddy Waters episode, Fairfax remains a tangle of consolidated subsidiaries, equity-accounted associates, and illiquid private and emerging-market stakes that make the reported book value harder to independently verify than a simple book of listed securities — investors are, unavoidably, trusting management's marks to some degree. Second, governance: the dual-class structure means public shareholders cannot force change if they ever come to disagree with capital allocation, a permanent discount that no operating performance fully erases. Third, the leverage inherent in the model: an insurer running a large investment portfolio on top of policyholder float is structurally geared, so a simultaneous underwriting catastrophe and investment drawdown would hit book value harder than the headline numbers suggest. None of these is a reason the company fails. All three are reasons a thoughtful owner demands a margin of safety rather than paying up for the recent momentum.

Now the bear case, and it deserves equal weight. The first and largest risk is the mirror image of the bull thesis: rates. The $2-billion-plus investment income stream that redeemed Fairfax is a direct function of high interest rates, and if central banks cut aggressively back toward zero, that engine deflates — forcing Fairfax to either accept far lower income or reach back into equity and credit risk to replace it, reintroducing exactly the volatility the short-duration book was designed to avoid. Second is catastrophe risk, the ever-present tail hazard of the underwriting business: a genuinely unprecedented year — a monster Gulf hurricane stacked on a major earthquake, say — could push combined ratios well above 100% and eat a year or more of profit in weeks. Brit and Odyssey are the most exposed, because reinsurance and Lloyd's specialty books concentrate precisely the peak-peril risk that a diversified primary insurer spreads out. The mechanism matters: catastrophe losses do not arrive as a gentle margin squeeze but as sudden, correlated hits that can consume years of accumulated underwriting profit in a single quarter, which is why the group leans on retrocession — reinsurance bought by reinsurers — to cap its worst outcomes. That protection costs money in calm years and is itself only as good as the counterparties standing behind it, a reminder that in insurance, risk is never eliminated, only moved around and re-priced. A skeptic would add that the frequency and severity of climate-driven catastrophes has been trending up, which pressures the whole industry's loss assumptions over time. Third is the Muddy Waters residue: the portfolio still contains illiquid private stakes whose values would be tested in a real emerging-market downturn, and a severe enough shock could force the kind of write-downs the short seller predicted, even if his timing was wrong.

There is also a genuine hidden option worth naming on the bull side: Fairfax India, and specifically Bangalore International Airport. Fairfax India lifted its stake in the airport to 74% in early 2025, paying $255 million for an additional 10% slice bought from Siemens.12 The asset is a direct play on one of the fastest-growing aviation markets on earth — Bengaluru's Kempegowda airport handled roughly 41 million passengers in its 2024-25 fiscal year, up nearly 12%, with a concession running all the way to 2068.1213 An airport is close to a toll road on a country's growth: it collects fees on every passenger and every tonne of cargo, its capacity is regulated and hard to replicate, and in a structurally growing market like India its volumes compound almost regardless of who runs the terminals. That is a rare quality asset for a value-oriented insurer to own. The catch is the same one the skeptics raise everywhere else: it is illiquid, carried at an estimated value, and monetizable only over years. It is exactly why a bear distrusts it and a bull prizes it — the same coin, two faces, which is the whole Fairfax investment case in miniature. The optionality is real; so is the requirement that you trust the mark.

For an investor trying to cut through all of it, the discipline is to watch a small number of things that actually reveal whether the two engines are still running. Three stand out.

The first is the consolidated combined ratio — the health check on underwriting culture. As long as it stays comfortably below 95%, the discipline is intact and Fairfax is being paid to hold its float; a sustained drift toward or above 100% would signal that the subsidiaries are chasing premium at the expense of profit, the exact failure mode decentralization is supposed to prevent. This is the number that would break first if the culture Fairfax prizes ever cracked, which is why it matters more than any single quarter's earnings.

The second is the interest-and-dividend income run-rate, together with the yield on the roughly $70-billion portfolio. This is the direct readout on whether the rate windfall is holding or fading. Because the portfolio is deliberately short, its yield re-prices relatively quickly as rates move — a feature that protected Fairfax on the way up and would expose it on the way down. Watching where reinvestment yields settle as bonds mature tells you, in near-real time, how durable the second engine is.

The third is book value per share growth — the ultimate scoreboard, the metric Muddy Waters attacked and the one management has staked its credibility on compounding at a mid-teens pace over time. The caution for any investor is not to extrapolate the recent 14.5% and 20.5% jumps as a new normal; those years captured the full flush of the rate windfall and heavy accretive buybacks. The honest question is what book value compounds at through a full cycle, including the next soft insurance market and the next rate-cutting cycle. Track those three numbers over several years, not several quarters, and the noise around Fairfax mostly takes care of itself. Which brings us to the lessons the whole saga leaves behind.

X. Outro: The Ultimate Playbook Lessons (03:25 – 03:40)

Before the lessons, one myth worth retiring. The label that has followed Fairfax for two decades — "Canada's Berkshire Hathaway" — is more marketing than analysis, and clinging to it obscures more than it reveals. Berkshire's edge is a fortress of wholly-owned operating businesses with genuine moats, a cash pile that lets it act as lender of last resort in crises, and an investing style that famously avoids macro bets. Fairfax is a different animal: more leveraged, more macro-driven, more complex, more dependent on a controlling shareholder, and operating in a commodity industry where pricing power is cyclical rather than structural. The comparison flatters Fairfax on the way up and unfairly damns it on the way down — it was the "Berkshire" framing that made the Muddy Waters "actually it's GE" line sting so precisely. The reality is that Fairfax is neither Berkshire nor GE. It is its own thing: a decentralized global underwriter with a talented, occasionally overconfident investment operation attached, now run with more discipline than it showed for most of its history. Judge it as that, and the record looks neither miraculous nor fraudulent — it looks like a good, cyclical, well-managed insurer that made one enormous macro mistake, learned from it, and got the next big call right.

With the myth set aside, Fairfax's forty-year arc resolves into a set of hard-won lessons about the discipline of compounding other people's money — and they generalize well beyond insurance.

The first is the separation of powers. Fairfax's structural insistence on keeping underwriting and investing in separate hands — locals price the risk, head office allocates the capital — exists precisely so that neither can corrupt the other. The cardinal sin in an insurance-plus-investing model is letting a hungry investment desk pressure the underwriters into writing bad business just to generate float to invest. Fairfax's culture, whatever its other flaws, has largely refused that temptation, and the sub-94% combined ratios are the evidence.

The second is the double edge of conviction. Winning a huge, contrarian macro bet is one of the most dangerous things that can happen to an investor, because it can transform a useful discipline into an unfalsifiable faith. The Big Short made Watsa, and then it nearly unmade him, because the same conviction that let him hold an unpopular trade for years also let him hold a losing thesis for a decade. The lost decade's several billion dollars of hedging losses are a permanent monument to the difference between being contrarian and being stubborn — a distinction that only becomes clear far too late.

The third is that free cash flow is the best defense against a short seller. When Muddy Waters attacked, Fairfax did not merely litigate the accounting in press releases; it retired more than a billion dollars of its own stock below book value, letting its balance sheet make the argument its lawyers could not. A company that can buy back its shares at a discount during an assault on its credibility is making a costly, credible signal — the kind that words alone never carry.

And the fourth is the quiet power of decentralization done right. To run a multi-billion-dollar underwriting empire across dozens of markets, you have to trust local leaders and build a culture that survives the departure of any one of them. The smooth handoffs to Carl Overy at Odyssey and Davidson Pattiz at Zenith, and the institutionalization of the investment process under Wade Burton, are the real test of whether Fairfax has become a machine rather than a monument to one man. That test is not yet finished. Watsa still holds the votes, the private stakes still resist easy valuation, and the rate windfall that redeemed the company could recede as quickly as it arrived. What can be said is that a company written off a decade ago as a value trap has, through a genuinely well-executed pivot and a stress test it chose to answer with cash, earned the right to be judged on what it does next rather than on the ghosts of the hedges. For the long-term investor, that is not a verdict. It is an invitation to keep watching the three numbers that matter.

References

-

Fairfax Financial Holdings Limited — Financial Results for the Year Ended December 31, 2024 — Fairfax Financial, 2025-02-13 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Fairfax Financial Holdings Limited — Financial Results for the Year Ended December 31, 2025 — Fairfax Financial, 2026-02-19 ↩↩↩↩↩↩↩↩↩↩↩

-

MW is Short Fairfax Financial Holdings Limited (FFH:CN) — Muddy Waters Research, 2024-02-08 ↩↩↩↩

-

Short-seller Muddy Waters alleges accounting manipulation by Fairfax Financial — The Globe and Mail, 2024-02-08 ↩↩↩

-

Fairfax Responds Further to Short Seller Report — Fairfax Financial, 2024-02-12 ↩

-

More than a Canadian Warren Buffett: Prem Watsa and The Fairfax Way — Policy Magazine ↩↩↩↩↩

-

The Fairfax way: Prem Watsa's investing transformation and buybacks — The Globe and Mail ↩↩↩

-

Prem Watsa Chairman's Letter to Shareholders, 2016 — Fairfax Financial ↩↩↩↩↩↩↩

-

Allied World, best of times; hedge loss, worst of times for Fairfax's Watsa — Risk Market News ↩↩

-

Fairfax Financial Holdings Limited — Financial Results for the Year Ended December 31, 2022 — Fairfax Financial ↩↩↩

-

Fairfax India Completes Acquisition of an Additional 10% Interest in Bangalore International Airport Limited — Fairfax India Holdings, 2025-02-20 ↩↩

-

Bengaluru Airport: 41 Million Passengers in 2024-25 — Aviation A2Z, 2025-04-06 ↩

-

Brian Young takes over as President of Fairfax Insurance, Carl Overy now CEO of Odyssey — Reinsurance News, 2025-01-03 ↩↩

-

Zenith Insurance Announces Leadership Change — PR Newswire, 2024-07-10 ↩↩

-

Fairfax Financial Holdings Limited — Executive Announcement — Fairfax Financial, 2022-02-10 ↩↩

-

Allied World Assurance Company Holdings — SEC EDGAR Filings ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube