FirstEnergy: From Utility Giant to Scandal and Redemption

I. Introduction & Episode Roadmap

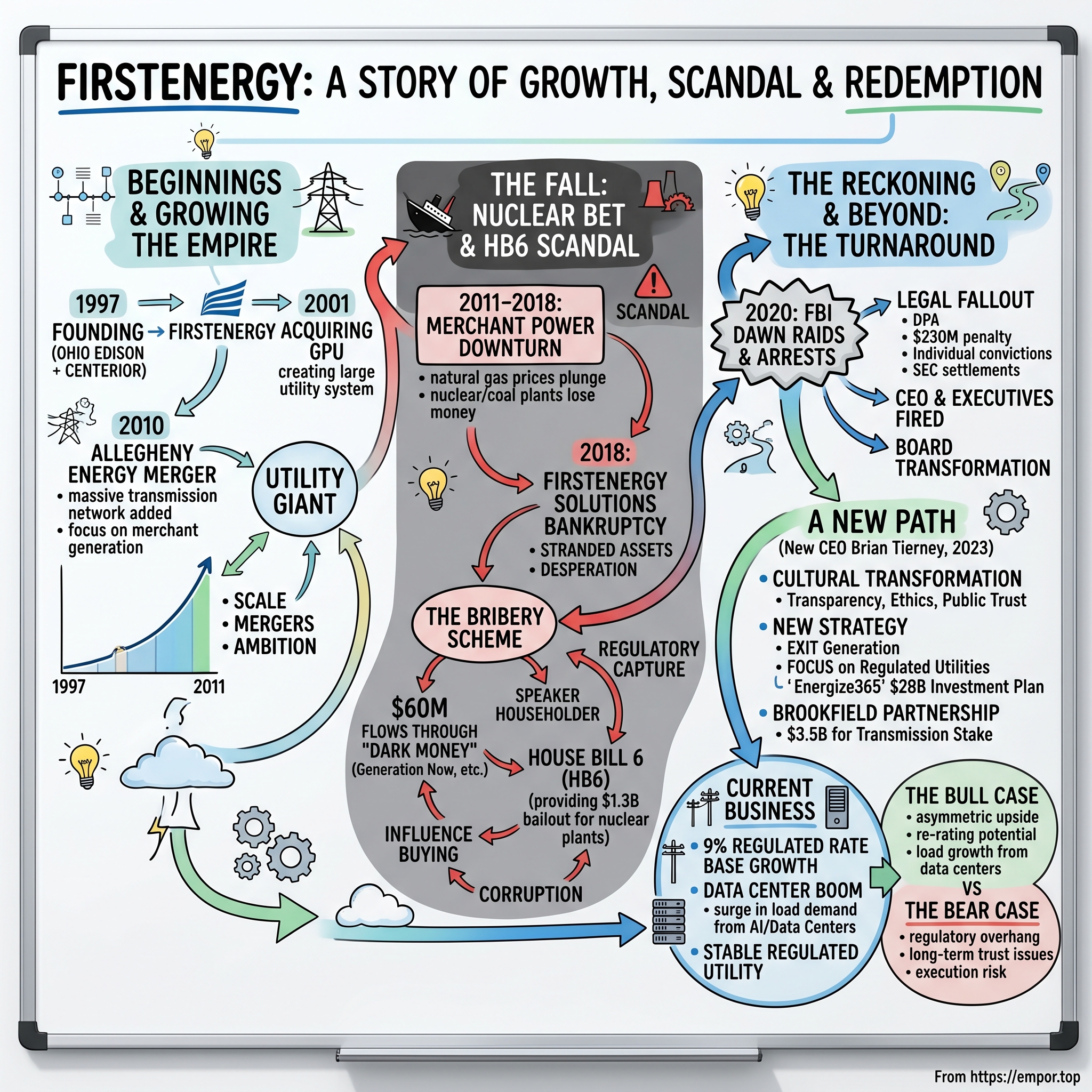

Picture this: July 21, 2020. FBI agents fan out across Ohio in a coordinated dawn raid. By noon, the Speaker of the Ohio House of Representatives is in handcuffs, charged with orchestrating what federal prosecutors call "likely the largest bribery, money laundering scheme ever perpetrated against the people of the state of Ohio." At the center of it all? A century-old electric utility company that had just spent $60 million to secure a $1.3 billion bailout for its struggling nuclear plants.

This is the story of FirstEnergy—a $24 billion utility behemoth serving 6 million customers across six states, headquartered in an unassuming office tower in Akron, Ohio. Today, it ranks as the world's 896th most valuable company, a testament to both the resilience of regulated utilities and the company's remarkable recovery from one of the darkest chapters in American corporate history.

But FirstEnergy isn't just a scandal story. It's a masterclass in utility consolidation, a cautionary tale about regulatory capture, and ultimately, a case study in corporate redemption. How does a company go from being the largest investor-owned electric utility in America to the center of a federal corruption probe—and then engineer one of the most comprehensive corporate turnarounds in recent memory?

Over the next few hours, we'll trace FirstEnergy's arc from its 1997 founding through the great consolidation era, its ambitious nuclear bet, the House Bill 6 corruption scandal that nearly destroyed it, and its ongoing transformation under new leadership. We'll examine how deregulation reshaped American utilities, why nuclear power became both FirstEnergy's greatest asset and its Achilles' heel, and what happens when corporate political influence crosses the line from lobbying to bribery.

This isn't just a story about one company. It's about the hidden wiring of American democracy, the economics of keeping the lights on, and the question every investor in regulated utilities must grapple with: when your returns depend on government favor, where exactly is the line between influence and corruption?

Along the way, we'll meet the engineers who built an empire, the executives who nearly destroyed it, and the new generation of leaders trying to prove that culture change isn't just corporate PR speak. We'll dive into the numbers—from the $28 billion infrastructure program now underway to the 33% core earnings growth since 2022—and ask whether FirstEnergy has truly turned the corner or if the ghosts of House Bill 6 still haunt its boardroom.

For investors, FirstEnergy presents a fascinating paradox: a company with stable, regulated cash flows and massive infrastructure investment opportunities, yet one where reputational risk and regulatory uncertainty linger like storm clouds on the horizon. The bull case sees 6-8% annual earnings growth and a data center boom driving electricity demand. The bear case worries about regulatory backlash and whether trust, once shattered, can ever be fully restored.

So buckle up. This is a story of ambition and hubris, of public service and private greed, of destruction and redemption. It's the story of FirstEnergy—and in many ways, it's the story of American capitalism itself.

II. Origins & The Great Consolidation Era (1997–2001)

The conference room at Ohio Edison's Akron headquarters hummed with nervous energy on that November morning in 1996. CEO Ellis Arnall stood before a room of investment bankers, lawyers, and his senior team, about to announce a deal that would reshape Ohio's utility landscape forever. "Gentlemen," he said, sliding a folder across the mahogany table, "we're buying Centerior Energy."

The $1.6 billion all-stock transaction wasn't just another utility merger—it was the opening salvo in what would become one of the most aggressive consolidation plays in American utility history. Ohio Edison, which had quietly served northeastern Ohio since 1930, was about to transform into FirstEnergy, instantly creating a powerhouse with 2.2 million customers across 13,000 square miles of northern and central Ohio and western Pennsylvania.

But why now? The answer lay in Washington, where the Energy Policy Act of 1992 had fundamentally rewritten the rules of the electricity business. For the first time, utilities could compete across state lines. Generation was being separated from transmission and distribution. The old model—where vertically integrated monopolies controlled everything from power plants to power lines within defined territories—was crumbling. In this brave new world, scale would matter. The survivors would be those who consolidated quickly and efficiently.

Ellis Arnall understood this better than most. A chemical engineer by training who'd spent his entire career climbing Ohio Edison's ranks, Arnall had a reputation for seeing around corners. While other utility CEOs fretted about deregulation, he saw opportunity. "The electricity business is becoming like banking," he told his board. "There will be a handful of super-regionals, and everyone else will be acquired or struggle to survive."

The Centerior deal closed in November 1997, creating FirstEnergy Corporation. The name itself was a statement of intent—this wouldn't be the last acquisition. The combined company now operated seven electric utility companies: Ohio Edison, The Illuminating Company, Toledo Edison, Penn Power, Jersey Central Power & Light, Metropolitan Edison, and Pennsylvania Electric. Annual revenues topped $5 billion. But Arnall was just getting started.

The integration proceeded with military precision. FirstEnergy pioneered what would become its signature move: maintaining local utility brands while centralizing back-office functions. Customers in Cleveland still paid bills to The Illuminating Company, while those in Toledo wrote checks to Toledo Edison. But behind the scenes, FirstEnergy was eliminating redundancies, standardizing systems, and squeezing out costs. Within 18 months, they'd cut $100 million in annual expenses—money that flowed straight to the bottom line.

Then came the GPU opportunity. General Public Utilities, the New Jersey-based utility infamous for owning Three Mile Island, had been struggling since that 1979 nuclear disaster. By 2000, GPU was vulnerable, its stock price depressed, its nuclear fleet a millstone around its neck. For most utilities, GPU's nuclear baggage made it untouchable. For FirstEnergy, it was precisely the kind of contrarian bet that could pay off handsomely.

The announcement came in August 2000: FirstEnergy would acquire GPU for $4.5 billion in stock, creating the nation's fifth-largest investor-owned electric system. The deal would add 2 million customers in Pennsylvania and New Jersey, including Jersey Central Power & Light, Pennsylvania Electric (Penelec), and Metropolitan Edison (Met-Ed). Combined revenues would exceed $12 billion. More importantly, it would give FirstEnergy critical mass in the emerging PJM wholesale electricity market—the world's largest competitive wholesale electricity market.

Wall Street was skeptical. "FirstEnergy Bites Off More Than It Can Chew," read one analyst report. The concern wasn't just GPU's nuclear legacy—it was the sheer complexity of integrating two massive utility systems across multiple states with different regulatory regimes. FirstEnergy's stock dropped 8% on the announcement.

But Arnall had an ace up his sleeve: Tony Alexander, his hand-picked president and heir apparent. Alexander, a West Virginia native with an MBA from Ohio State, had masterminded the Centerior integration. He approached the GPU deal with the same methodical precision. "We're not trying to turn GPU into FirstEnergy," Alexander explained to worried GPU employees. "We're creating something new—taking the best of both companies."

The GPU merger closed in November 2001, just two months after 9/11 had thrown markets into chaos. While other companies pulled back, FirstEnergy pushed forward. The integration exceeded all expectations. Promised synergies of $300 million annually were achieved within two years. The combined company now served 4.3 million customers across 36,100 square miles. FirstEnergy had gone from a regional Ohio utility to a multi-state empire in just four years.

But perhaps the most prescient move was what FirstEnergy did with GPU's nuclear assets. Rather than divest them as many urged, the company doubled down, pouring money into upgrades and life extensions. "Nuclear is going to come back," Alexander predicted in a 2002 investor call. "When it does, we'll be positioned perfectly."

The consolidation era had established FirstEnergy's playbook: move fast, buy distressed assets, integrate ruthlessly, and make contrarian bets. It was a formula that would drive extraordinary growth—and eventually lead the company to the brink of disaster. But in those heady days of 2001, with revenues soaring and the stock price climbing, FirstEnergy looked unstoppable. The question wasn't whether they'd make another acquisition, but when—and how big it would be.

III. The Allegheny Acquisition & Becoming a Behemoth (2010–2011)

Tony Alexander's corner office on the 19th floor of FirstEnergy's Akron headquarters offered a commanding view of the Cuyahoga Valley, but on that February morning in 2010, his attention was fixed on a spreadsheet glowing on his laptop screen. After months of secret negotiations, FirstEnergy was about to announce its most audacious move yet: the acquisition of Allegheny Energy for $8.5 billion.

"This isn't just about getting bigger," Alexander, now CEO, told his senior team gathered around the conference table. "This is about positioning FirstEnergy for the next century of the electricity business."

The timing seemed almost reckless. America was still clawing its way out of the Great Recession. Credit markets remained fragile. Most utilities were hunkering down, cutting capital expenditures, focusing on survival. But Alexander saw opportunity where others saw only risk. Allegheny's stock had been hammered, trading 30% below its pre-crisis highs. More importantly, Allegheny brought something FirstEnergy desperately needed: a massive transmission network spanning from the Midwest to the Mid-Atlantic.

Allegheny Energy wasn't just any utility. Based in Greensburg, Pennsylvania, it served 1.6 million customers across Pennsylvania, West Virginia, Maryland, and Virginia. But its real value lay in its 14,000 miles of transmission lines—critical arteries in the PJM Interconnection that moved electricity from power plants in the Midwest to population centers on the East Coast. In the emerging world of competitive electricity markets, owning transmission was like owning toll roads. No matter who generated the power, they'd have to pay FirstEnergy to move it.

The deal structure was elegant in its simplicity: an all-stock transaction that would give Allegheny shareholders 0.667 shares of FirstEnergy stock for each Allegheny share. No cash required, preserving FirstEnergy's balance sheet for the integration costs ahead. The combined company would serve 6 million customers across six states, with revenues approaching $16 billion annually. For a brief moment, FirstEnergy would become the largest investor-owned electric utility system in the nation by customer count.

But the path to closing was anything but simple. The merger required approval from four state utility commissions, the Federal Energy Regulatory Commission (FERC), and the Department of Justice. Each regulator wanted their pound of flesh. Pennsylvania demanded $14 million in customer credits. Maryland extracted promises of maintained employment levels. West Virginia required specific reliability investments.

The most dramatic moment came during the Maryland Public Service Commission hearings in December 2010. Consumer advocates had mobilized opposition, arguing the merger would lead to higher rates and reduced local control. The hearing room in Baltimore was packed with protestors. As Alexander took the witness stand, someone shouted from the gallery: "Ohio doesn't care about Maryland!"

Alexander's response was masterful. Speaking without notes for nearly an hour, he laid out a vision of an integrated Mid-Atlantic energy market where economies of scale would benefit all customers. He committed to $2 billion in transmission investments over five years. He promised to maintain local employment and keep Allegheny's Greensburg operations center open. Most cleverly, he framed the merger not as an Ohio company taking over a Maryland utility, but as creating a true multi-state enterprise with deep roots in every community it served.

The Maryland commission approved the deal by a 3-2 vote—the narrowest of margins, but enough.

Meanwhile, FirstEnergy's integration team, led by Chief Operating Officer Mark Clark, had been preparing for months. They'd learned from the GPU acquisition a decade earlier. This time, they moved even faster. Within hours of the February 2011 closing, FirstEnergy executives were in Allegheny facilities, not to impose changes, but to listen and learn. "We treated it like a merger of equals, even though technically it was an acquisition," Clark later recalled. "That made all the difference in getting buy-in from Allegheny employees."

The numbers validated the strategy. Integration costs came in $50 million below the projected $350 million. Synergies exceeded targets, reaching $400 million annually by 2013. The stock price, which had dropped on the initial announcement, recovered and then surged, hitting an all-time high of $54 per share in early 2011.

But the real prize was the transmission network. The combined company now owned 24,000 miles of transmission lines, making it one of the largest transmission owners in North America. As Alexander had predicted, transmission became a money machine. Returns were regulated but generous—FERC allowed returns on equity of 11-13% for transmission investments. Better yet, transmission investments didn't face the same scrutiny as distribution rate cases at state commissions. It was the closest thing to a guaranteed return in the utility business.

The Allegheny acquisition also brought something unexpected: a different corporate culture. Where FirstEnergy had been hierarchical and engineering-focused, Allegheny was more entrepreneurial and commercially minded. The fusion created creative tension. Allegheny executives brought sophistication in power marketing and trading. FirstEnergy contributed operational excellence and scale. The combination, when it worked, was powerful.

Yet there were warning signs even in triumph. The massive debt load—now exceeding $20 billion—limited financial flexibility. The complexity of operating across six states with different regulatory regimes created constant friction. Most ominously, FirstEnergy had inherited Allegheny's merchant generation fleet just as natural gas prices were plummeting due to the shale revolution. Those coal and nuclear plants that had seemed like assets were rapidly becoming liabilities.

In a prescient moment during the 2011 investor day, an analyst asked Alexander about the merchant generation strategy. "We believe in portfolio diversity," Alexander responded confidently. "Coal, nuclear, gas, renewables—we'll own it all and let the market sort out the winners."

History would prove that confidence misplaced. The market was indeed about to sort out winners and losers. And FirstEnergy's massive bet on coal and nuclear generation was about to land on the wrong side of that sorting. But in 2011, fresh off the successful Allegheny integration, FirstEnergy stood at the apex of its power. Six million customers, $16 billion in revenues, a service territory stretching from Ohio to the Atlantic Ocean.

The empire was complete. Now came the challenge of defending it in a rapidly changing energy landscape—a challenge that would ultimately lead FirstEnergy down a dark path toward the most notorious corruption scandal in Ohio history.

IV. The Nuclear Bet & Competitive Generation Years (2011–2018)

The control room at the Davis-Besse Nuclear Power Station thrummed with quiet efficiency on that March morning in 2014. Dozens of operators monitored endless arrays of gauges, screens, and indicators tracking every aspect of the 908-megawatt reactor. Chuck Jones, FirstEnergy's newly minted CEO, stood watching this ballet of precision engineering, but his mind was elsewhere—on spreadsheets showing that this technological marvel was bleeding money.

"We're losing $100 million a year on this plant alone," Jones muttered to his CFO, Jim Pearson, standing beside him. The irony wasn't lost on either man. Davis-Besse, along with FirstEnergy's Perry and Beaver Valley nuclear plants, represented nearly 4,000 megawatts of carbon-free generation—enough to power 3 million homes. These plants had once been crown jewels, printing money when wholesale electricity prices topped $60 per megawatt-hour. Now, with prices crashed to $30 thanks to cheap shale gas, they were millstones.

FirstEnergy's generation portfolio told the story of American electricity in transition. The company operated 65 generating units at 23 power plants, with a total capacity of 16,892 megawatts. The mix read like an energy historian's timeline: 46% coal, 24% nuclear, 28% natural gas, with token amounts of oil and hydro. It was a portfolio built for a world that no longer existed—one where coal was king and nuclear was the future.

The shale revolution had changed everything with shocking speed. In 2008, natural gas cost $13 per million BTU. By 2012, it had crashed to $2. Gas-fired plants that had sat idle for years roared back to life. They could ramp up and down quickly to match demand, unlike nuclear plants that ran constantly. Worse for FirstEnergy, gas plants could be built for $1,000 per kilowatt of capacity. A new nuclear plant? Try $6,000—if you could even get one permitted.

Jones, an engineer who'd spent 37 years at FirstEnergy working his way up from the coal plants, understood the physics and the economics perfectly. But understanding and accepting were different things. At investor meetings, he'd pound the table about the "reliability value" of nuclear, about grid stability, about polar vortex events when gas pipelines froze but nuclear plants kept humming. All true, but irrelevant to wholesale electricity markets that valued only one thing: the cheapest marginal megawatt.

The company's FirstEnergy Solutions (FES) subsidiary, which housed the competitive generation assets, became a case study in stranded assets. Created during the heady deregulation days when everyone believed merchant power was the future, FES owned not just the nuclear plants but 8,000 megawatts of coal capacity, including the massive Bruce Mansfield and Sammis plants. These coal behemoths, built in the 1960s and 70s, were engineering marvels of their era—and economic disasters in the age of fracking.

By 2015, the situation was desperate. FirstEnergy had already announced the retirement of six coal plants totaling 2,700 megawatts. But the nuclear plants were different. You couldn't just mothball a nuclear reactor—the decommissioning costs alone for Davis-Besse were estimated at $1.2 billion. And there was the workforce: 700 highly skilled employees at each plant, many in communities where the nuclear station was the largest employer and taxpayer.

The November 2016 strategic review announcement was supposed to calm investors. "FirstEnergy will exit the competitive generation business and become a fully regulated utility," Jones declared on the earnings call. The plan was elegant in theory: sell or spin off FES, focus on the stable regulated utility operations, become a boring but profitable wires-and-pipes company. The stock jumped 7% on the news.

But reality proved messier. Who would buy coal and nuclear plants that were losing money? FirstEnergy tried everything. They pitched the nuclear plants to Exelon, America's largest nuclear operator. No interest. They explored a sale to private equity. The due diligence teams took one look at the numbers and ran. They even considered giving the plants to the employees via an ESOP. The union representatives laughed—politely.

The death spiral accelerated through 2017. FES was burning through $500 million in cash annually. The nuclear plants needed $900 million in capital investments over the next three years just to keep operating. The commodity futures curve showed no relief—gas prices would stay low for years. Bond prices for FES debt collapsed to 30 cents on the dollar. Credit rating agencies downgraded everything to junk.

In the executive conference room in Akron, the discussions grew increasingly desperate. "What if we just walk away?" someone suggested. "Chapter 11, hand the keys to the creditors, move on." Jones's face darkened. "We're not Enron," he snapped. "We have obligations—to our employees, to the communities, to the grid."

But there was another option, one that had been quietly discussed in smaller circles: political intervention. Other states had rescued their nuclear plants. New York created Zero Emission Credits worth $500 million annually for upstate reactors. Illinois passed a similar program. Why not Ohio?

The lobbying effort began modestly. FirstEnergy had always been politically active—it was impossible to operate a utility without engaging with regulators and legislators. But this was different. This wasn't about routine rate cases or transmission planning. This was about corporate survival.

By late 2017, FirstEnergy was spending millions on lobbying, campaign contributions, and dark money groups with names like "Generation Now" and "Partners for Progress." The message was carefully crafted: this wasn't a corporate bailout but a national security issue, a grid reliability issue, an environmental issue. Nuclear plants prevented 28 million tons of CO2 emissions annually. If they closed, that carbon-free power would be replaced by gas and coal from other states.

The March 31, 2018, bankruptcy filing of FirstEnergy Solutions shocked no one who'd been paying attention. With $7.5 billion in debt and no path to profitability, FES entered Chapter 11 protection. The filing included plans to deactivate or sell all nuclear and coal plants. Davis-Besse would close in 2020, Perry in 2021, Beaver Valley in 2021 and 2022. The coal plants would shut immediately.

Jones tried to position it as a victory. "This allows FirstEnergy to complete its transformation to a fully regulated utility," he told investors. The company would provide $628 million in funding to FES during bankruptcy and then walk away clean. The stock market approved—shares rose 4% on the bankruptcy announcement.

But behind the scenes, the political machinery was already in motion. If markets wouldn't save the nuclear plants, perhaps politicians would. The groundwork was being laid for what would become House Bill 6—and the scandal that would bring down careers, destroy reputations, and fundamentally reshape FirstEnergy.

Looking back, the nuclear bet represented a massive miscalculation about the pace of energy transition. FirstEnergy had bet billions that nuclear's advantages—reliability, carbon-free generation, baseload power—would command a premium. Instead, markets valued only flexibility and low marginal cost. It was a bet that would ultimately cost far more than money. It would cost the company its integrity.

V. The House Bill 6 Scandal: Corruption at the Highest Levels (2017–2020)

The Statehouse Café in downtown Columbus was nearly empty that January evening in 2017 when Chuck Jones slid into a corner booth across from Larry Householder. The former Ohio House Speaker, who'd been forced from office in 2004 amid an FBI investigation, was plotting his comeback. Jones, FirstEnergy's CEO, had a problem that needed a political solution. As their coffee grew cold, they began sketching out what federal prosecutors would later call "a racketeering conspiracy to secure a $1.3 billion bailout."

Householder was an unlikely kingmaker. The 61-year-old Perry County native had already been Speaker once, from 2001 to 2004, before the FBI started sniffing around his campaign finances. He'd retreated to his farm, but the political bug never left. By 2016, he was methodically planning his return, recruiting candidates, raising money, building a machine. He just needed a financial patron.

FirstEnergy became that patron. The scheme was breathtaking in its audacity and simplicity. FirstEnergy would funnel $60 million through a web of 501(c)(4) "dark money" groups to support Householder's return to power. In exchange, Householder would shepherd legislation to bail out FirstEnergy's nuclear plants. It wasn't framed as bribery—perish the thought. It was "issue advocacy" and "coalition building."

The money flowed through a labyrinth that would make a forensic accountant weep. FirstEnergy Solutions would wire millions to "Generation Now," a 501(c)(4) controlled by Householder. Generation Now would then distribute funds to other dark money groups with anodyne names: "Hardworking Ohioans," "Coalition for Growth & Opportunity," "Megacity Group." These entities would fund campaign ads, mailers, even provide cash payments to Householder's team. One Householder associate, Jeffrey Longstreth, literally kept garbage bags full of cash in his Florida condo.

The 2018 election was Householder's masterpiece. FirstEnergy money backed 21 House candidates, focusing on primaries where a few thousand votes could swing a race. The ads never mentioned FirstEnergy or nuclear power. Instead, they attacked opponents as "liberals" who would raise taxes and support "sanctuary cities." One mailer featured a stock photo of MS-13 gang members. Another showed crying children, warning that the opponent would "put our kids at risk."

It worked. Householder's candidates won 21 of 21 races. In January 2019, he reclaimed the Speaker's gavel by a single vote—his own. The coup was complete. Now came time to deliver.

House Bill 6 was introduced in April 2019, and it was a corporate welfare masterwork. Officially titled "The Ohio Clean Air Program," it would charge every electricity customer in Ohio a monthly fee—$0.85 for residential, up to $2,400 for industrial—to create a $150 million annual subsidy for nuclear plants. Over nine years, it would generate $1.3 billion. But that was just the appetizer. HB6 also gutted Ohio's renewable energy standards and eliminated energy efficiency programs, saving FirstEnergy's utilities hundreds of millions more.

The opposition mobilized immediately. Environmental groups hated the rollback of clean energy standards. Consumer advocates calculated it would cost ratepayers $1.8 billion. Even natural gas companies opposed it, seeing nuclear subsidies as market manipulation. The Statehouse became a battleground.

FirstEnergy's response was to spend more. Lots more. When opponents launched a referendum campaign to overturn HB6, FirstEnergy funneled another $38 million through dark money groups to stop it. The tactics turned nasty. Petition circulators were followed, threatened, offered bribes to stop collecting signatures. One operative was arrested for cocaine possession—the drugs were planted. Another had his car vandalized. Racist flyers appeared in predominantly Black neighborhoods claiming the Chinese government was behind the referendum.

Meanwhile, Sam Randazzo was playing a special role. The Ohio attorney and energy consultant had long represented industrial customers opposing FirstEnergy rate increases. But in 2019, something changed. FirstEnergy paid Randazzo's consulting firm $4.3 million just before Governor Mike DeWine appointed him Chairman of the Public Utilities Commission of Ohio (PUCO)—the very body regulating FirstEnergy. Randazzo never disclosed the payment.

The referendum effort needed 265,774 valid signatures by October 21, 2019. They fell just short, gathering only 223,000 before funds ran dry and circulators quit in fear. HB6 would take effect.

Chuck Jones could barely contain his glee on the October 2019 earnings call. "HB6 ensures the continued operation of our valuable nuclear fleet," he proclaimed. FirstEnergy's stock jumped 3%. Analysts upgraded ratings. The company had seemingly pulled off the impossible: a political solution to an economic problem.

But FBI Special Agent Blane Wetzel had been watching since 2018. The bureau had been tipped off by a rival political operative about unusual financial patterns around Householder. Agents traced wire transfers, subpoenaed bank records, interviewed witnesses. They discovered FirstEnergy executives using personal credit cards to pay for Householder's defense attorneys in an old case. They found text messages between Jones and Householder discussing strategy. Most damningly, they intercepted a call where Householder bragged: "I spent close to $20 million—FirstEnergy gave it to me—to win the majority."

The arrests came at dawn on July 21, 2020. FBI agents surrounded Householder's farm in Glenford, Ohio. The 61-year-old Speaker, who'd been planning to run for another term, was led away in handcuffs. Simultaneously, agents arrested four associates: Jeffrey Longstreth, Neil Clark, Matthew Borges, and Juan Cespedes. The U.S. Attorney, David DeVillers, didn't mince words at the press conference: "This is likely the largest bribery, money laundering scheme ever perpetrated against the people of the state of Ohio."

The 82-page criminal complaint read like a mob indictment, charging violations of the Racketeer Influenced and Corrupt Organizations (RICO) Act. It detailed the entire conspiracy: the dark money, the bribes, the strong-arm tactics against the referendum. FirstEnergy wasn't named as a defendant—yet—but was identified as "Company A" throughout. Its stock cratered 15% in hours.

Inside FirstEnergy's Akron headquarters, panic set in. The board convened emergency meetings. Lawyers swarmed. Jones and Senior Vice President of External Affairs Michael Dowling were immediately placed on administrative leave. By October, both were terminated for "violations of company policies and code of conduct." The board launched an internal investigation that would eventually cost $100 million in legal fees.

The scandal's tentacles reached everywhere. In November 2020, Sam Randazzo resigned as PUCO chairman after FBI agents searched his home. They found documents labeled "FirstEnergy" and bank records showing the $4.3 million payment. He was indicted in 2023 for bribery and embezzlement.

The human toll was staggering. Neil Clark, facing decades in prison, died by suicide in 2021. Sam Randazzo, after years of legal battles, took his own life in April 2024, leaving a note maintaining his innocence. Larry Householder, convicted in March 2023, was sentenced to 20 years in federal prison—the harshest sentence ever imposed on an Ohio politician. At his sentencing, he remained defiant: "I am innocent. I will appeal. The truth will come out."

Matt Borges, the former Ohio Republican Party chairman caught up in the scheme, got 5 years. Juan Cespedes and Jeffrey Longstreth pled guilty and cooperated, receiving lighter sentences. The investigation expanded, examining other politicians who'd received FirstEnergy money, other utilities that might have engaged in similar schemes.

For FirstEnergy, House Bill 6 had gone from salvation to damnation. The nuclear plants it was meant to save had already been spun off in the FES bankruptcy. The company that had spent $60 million on corruption now faced billions in penalties, lawsuits, and remediation costs. Its reputation was in ruins. The new CEO, Steven Strah, admitted in a 2021 town hall: "We lost our way. We betrayed the trust of our customers, our regulators, and our communities."

The Ohio legislature repealed the nuclear subsidies in 2021, though other provisions of HB6 remained. The scandal fundamentally changed how utilities engage in politics, spurring reforms nationwide. But for those caught in its web—the executives terminated, the politicians imprisoned, the employees tarred by association—the damage was irreversible.

Looking back, the HB6 scandal represented the logical endpoint of a broken system where corporate money flows through untraceable channels to purchase political outcomes. FirstEnergy didn't invent this system—dark money groups had proliferated since the 2010 Citizens United decision. But they exploited it more brazenly than perhaps any company in American history. And in doing so, they provided a case study in why corporate political influence, left unchecked, corrodes democracy itself.

VI. The Reckoning: Legal Fallout & Financial Penalties (2020–2024)

Steven Strah's first day as FirstEnergy CEO began at 4:47 AM on March 8, 2021, with a call from the company's lead outside counsel. "The DOJ wants to meet. Today. They're ready to discuss terms." Strah, who'd been CFO for less than a year before his battlefield promotion, understood immediately: the Department of Justice was offering a deferred prosecution agreement. Take the deal, or face criminal charges that could destroy the company.

By noon, Strah was in a Washington conference room facing a phalanx of federal prosecutors. The terms were brutal but survivable: admit to conspiracy to commit honest services wire fraud, pay a $230 million penalty, implement comprehensive reforms, and submit to three years of monitoring. The alternative—criminal prosecution of the corporation itself—would trigger default clauses in billions of bonds, potentially forcing bankruptcy.

"We'll take the deal," Strah said after a brief recess with counsel. It was the first of many bitter pills FirstEnergy would swallow in its journey toward redemption.

The July 22, 2021, deferred prosecution agreement was a masterpiece of prosecutorial leverage. FirstEnergy admitted to paying $60 million to public officials in exchange for favorable legislation. The company acknowledged that executives had paid $4.3 million to Sam Randazzo just before his appointment as PUCO chairman. Most remarkably, FirstEnergy agreed to a "statement of facts" that laid bare the entire conspiracy in granular detail—essentially writing the prosecution's case against individual defendants.

The $230 million penalty was just the beginning. FirstEnergy agreed to halt all political spending, implement new compliance procedures, and cooperate fully with ongoing investigations. The monitor, a former federal prosecutor, would have unfettered access to emails, documents, and personnel. Any violation would void the agreement and trigger prosecution.

But the federal settlement opened floodgates elsewhere. The Securities and Exchange Commission had been conducting its own investigation into whether FirstEnergy misled investors about its political activities. Internal emails showed executives discussing how to keep HB6 payments "below the radar" and "off the books." One particularly damaging message from Chuck Jones read: "We need to be careful about documentation. This can never be traced back to us."

The SEC settlement, announced in August 2024, required another $100 million payment—but more importantly, it forced FirstEnergy to admit to maintaining insufficient controls over political spending. The company had treated bribes as legitimate lobbying expenses, had failed to maintain accurate books and records, and had made false certifications to regulators. For a public company, these admissions were devastating, opening the door to shareholder lawsuits.

Ohio Attorney General Dave Yost had his own pound of flesh to extract. His office filed suit seeking to recover the ill-gotten gains from HB6. The August 2024 settlement for $19.5 million was modest compared to federal penalties, but it came with a stinger: FirstEnergy had to fund community development programs in areas affected by plant closures and publicly apologize to Ohio citizens.

The reputational penalties proved even costlier than the financial ones. In April 2023, the Cleveland Browns announced they were terminating FirstEnergy's naming rights to their stadium—a deal worth $102 million over 17 years. The press release was diplomatic, citing "mutual agreement," but everyone knew the truth: the Browns didn't want their brand associated with corruption. The stadium would revert to "Cleveland Browns Stadium" while the team sought a new sponsor.

Inside FirstEnergy, the reckoning was equally brutal. The board of directors, facing shareholder lawsuits and proxy battles, underwent complete transformation. By 2022, 12 of 14 directors were new since the scandal broke. The new board, led by chairman Donald Misheff, implemented what they called "the most comprehensive governance reforms in utility history."

The reforms were indeed sweeping. FirstEnergy created a new Ethics and Compliance Office reporting directly to the board. All political activities required multiple approvals and public disclosure. Executive compensation was restructured to emphasize long-term performance and ESG metrics. The company hired a Chief Ethics Officer—a role that hadn't existed before—and required all 12,000 employees to undergo annual compliance training.

The shareholder lawsuits proved particularly painful. Pension funds and institutional investors alleged the board had failed its fiduciary duty by allowing the bribery scheme. The discovery process was embarrassing, revealing board minutes where directors appeared asleep at the switch. One email showed a director asking, "What's Generation Now?" months after FirstEnergy had funneled millions through the entity. The consolidated settlement, reached in late 2023, cost $180 million and required additional governance changes.

Individual accountability came slowly but inexorably. Chuck Jones and Michael Dowling faced personal lawsuits seeking clawbacks of bonuses and stock awards. Both men invoked their Fifth Amendment rights against self-incrimination, but civil proceedings continued. Jones eventually agreed to return $10 million in compensation and accept a lifetime ban from serving as an officer or director of any public company.

The criminal cases against individuals ground through the courts. Sam Randazzo's death in April 2024 ended his prosecution, but not before devastating details emerged. FBI agents had found a "FirstEnergy" folder in his home containing documentation of the $4.3 million payment. His suicide note, parts of which were made public, maintained his innocence but acknowledged "mistakes in judgment."

Larry Householder's conviction and 20-year sentence sent shockwaves through Ohio politics. At his sentencing in June 2023, he remained defiant, calling the prosecution a "political hit job." But the evidence was overwhelming: recorded calls, text messages, bank records, and testimony from co-conspirators who'd flipped. The judge called it "an unconscionable betrayal of public trust."

For FirstEnergy employees, the reckoning was deeply personal. Many had spent entire careers at the company, taking pride in keeping the lights on for millions. Now they faced suspicious looks at community events, awkward questions from neighbors, taunts on social media. Morale surveys showed employee engagement at historic lows. Turnover spiked, particularly among younger workers who had options elsewhere.

The operational impact was significant. Regulatory proceedings that should have been routine became battlegrounds. Every rate case drew intense scrutiny. Consumer advocates demanded documentation for every expense. Regulators who might have given FirstEnergy benefit of the doubt now assumed the worst. The Ohio Public Utilities Commission imposed additional reporting requirements and threatened to revoke FirstEnergy's certificate to operate if any new violations emerged.

Credit rating agencies piled on. Moody's and S&P maintained negative outlooks for years, citing "governance failures" and "regulatory uncertainty." The higher borrowing costs—an extra 50-75 basis points versus peers—translated to millions in additional interest expenses annually. For a capital-intensive utility that needed to borrow billions for grid modernization, this was a serious handicap.

Yet through it all, FirstEnergy survived. The lights stayed on. Bills got paid. Storms were restored. The company that had seemed on the brink of collapse in 2020 was still standing in 2024, bloodied but not beaten. The question was whether it could move beyond survival to genuine redemption—whether it could rebuild trust, restore pride, and reclaim its position as a respected utility.

The reckoning phase was drawing to a close by late 2024. The major settlements were signed, the criminals sentenced, the reforms implemented. But everyone understood this was just the end of the beginning. The real test would be whether FirstEnergy could sustain its cultural transformation when the monitors left, when the headlines faded, when the pressure eased. That test was still to come.

VII. The Turnaround: Cultural Transformation & New Strategy (2020–Present)

Brian Tierney's first all-hands meeting as FirstEnergy's new CEO in March 2023 didn't start with financial projections or strategic initiatives. Instead, he stood before 12,000 employees connected via video link and said simply: "I'm sorry. This company failed you. We failed our communities. That changes now."

Tierney was an unusual choice to lead FirstEnergy's redemption. An industry outsider who'd spent his career at American Electric Power, he had no ties to the old regime, no relationships that might cloud judgment. The board had been explicit: they didn't want a turnaround artist or a financial engineer. They wanted someone who could rebuild a culture.

"Culture eats strategy for breakfast," Tierney told his leadership team at their first offsite, borrowing Peter Drucker's famous maxim. "We can have the best strategic plan in the world, but if we don't fix the culture that allowed HB6 to happen, we'll fail."

The cultural transformation began with symbols. The executive floor at headquarters—long known as "the castle" for its isolation from rank-and-file employees—was converted to open workspace. The executive dining room became a community meeting space. Tierney took a commercial flight to his first utility commission meeting, conspicuously avoiding the corporate jet that Chuck Jones had favored.

But symbolism only went so far. The real work was systemic. Tierney brought in organizational psychologists to conduct a cultural assessment. The results were sobering: employees described a culture of "malicious compliance," where people followed rules to the letter but never raised concerns. Trust in leadership scored in the bottom 5th percentile of companies surveyed. Most damning, 67% of employees said they'd witnessed ethical violations but hadn't reported them for fear of retaliation.

The new Ethics and Compliance Office, led by former federal prosecutor Catherine Anderson, became the tip of the spear. Anderson, who'd prosecuted Enron executives, understood that compliance couldn't be a check-the-box exercise. She instituted an anonymous hotline that reported directly to the board. She created "speak up" awards for employees who raised concerns. Most radically, she published quarterly reports detailing every ethics violation and the consequences—names redacted but circumstances clear.

The political activity reforms were even more dramatic. FirstEnergy didn't just reduce political spending—it eliminated it entirely. No corporate PAC, no lobbying beyond regulatory proceedings, no trade association dues that could be used for politics. When the Edison Electric Institute pushed back, arguing FirstEnergy needed a voice in policy debates, Tierney was blunt: "We had our chance to engage responsibly. We blew it. Now we earn back the right through actions, not words."

The business strategy transformation was equally bold. In October 2023, FirstEnergy announced Energize365, a $28 billion investment program through 2029 focused entirely on the regulated utility business. No merchant generation, no competitive retail, no side ventures. Just poles, wires, substations, and meters.

The numbers were staggering: $19 billion for distribution infrastructure, $6 billion for transmission, $3 billion for grid modernization. It represented a 60% increase over the previous five-year plan. But Tierney framed it as catching up after years of underinvestment while FirstEnergy chased competitive markets. "We're going back to basics," he explained. "Safe, reliable, affordable electricity. That's the job."

The Brookfield partnership, announced in early 2024, provided the financial firepower. The Canadian infrastructure giant agreed to buy a 30% stake in FirstEnergy Transmission (FET) for $3.5 billion. The deal valued FET at $11.7 billion—a premium valuation that validated FirstEnergy's transmission assets. More importantly, it brought in a sophisticated partner with deep pockets and a long-term perspective.

Brookfield's involvement sent a powerful signal to markets. Here was one of the world's most respected infrastructure investors betting billions on FirstEnergy's future. The stock responded accordingly, rising 20% in the month after announcement. Credit ratings stabilized. The cost of capital began normalizing.

The regulatory rehabilitation proved more challenging. Each state commission had its own process, its own concerns, its own politics. In Ohio, FirstEnergy faced special scrutiny. The PUCO instituted "enhanced oversight" requiring quarterly meetings, detailed reporting, and third-party audits. Every rate case became a morality play, with consumer advocates relitigating HB6.

Tierney's approach was radical transparency. Instead of the traditional adversarial rate case process, FirstEnergy began holding pre-filing workshops with all stakeholders. They opened their books, shared their models, explained their needs. When requesting recovery for storm restoration costs, they provided minute-by-minute logs of crew deployments. When proposing grid modernization investments, they brought in independent engineers to validate the plans.

It worked—slowly. The Pennsylvania Public Utility Commission approved a $140 million rate increase in 2024, noting FirstEnergy's "improved stakeholder engagement." New Jersey allowed accelerated recovery of transmission investments. Even Ohio began to thaw, approving a modest distribution rate increase while maintaining "heightened scrutiny."

The workforce transformation was perhaps most impressive. FirstEnergy had hemorrhaged talent after the scandal, losing 15% of its engineers and 20% of its IT staff. Tierney launched "Project Boomerang" to recruit them back, offering retention bonuses and career development opportunities. He instituted skip-level meetings where front-line employees could raise concerns directly. Most innovatively, he created an "innovation lab" where employees could propose and test new ideas without bureaucratic approval.

The safety culture transformation was equally dramatic. FirstEnergy had always preached safety but often prioritized production. Under Tierney, safety became truly paramount. Any employee could stop any job for safety concerns without repercussion. Safety metrics were weighted at 40% of executive compensation. When a contractor was injured in West Virginia, Tierney personally visited the hospital and then the job site, conducting a safety stand-down across the entire system.

Customer satisfaction, which had cratered during the scandal, began recovering. FirstEnergy invested heavily in customer service, reducing call wait times from 8 minutes to 90 seconds. They launched a mobile app allowing customers to report outages, track restoration, and manage bills. Most importantly, they began proactively communicating—sending alerts before planned outages, explaining rate changes, even acknowledging when they'd made mistakes.

The community engagement strategy shifted from writing checks to rolling up sleeves. FirstEnergy employees were encouraged to volunteer, with the company providing paid time off for community service. Tierney himself spent a Saturday in July 2024 helping rebuild a playground in Youngstown. When skeptics suggested it was PR theater, he kept showing up—month after month, no media invited.

Environmental commitments, long an afterthought, became central. FirstEnergy pledged net-zero carbon emissions by 2050, with interim targets of 30% reduction by 2030. They began connecting solar and wind farms to the grid at record pace. They launched programs to help customers reduce consumption and install rooftop solar. When environmental groups remained skeptical, Tierney met with them personally, acknowledging past failures and asking for input on future plans.

The financial results validated the transformation. Core earnings per share grew from $2.36 in 2022 to $2.65 in 2024—a 33% increase despite the scandal's overhangs. The dividend, maintained throughout the crisis, was raised 5% in 2024. Return on equity improved to 9.8%. The stock, which had bottomed at $27 in July 2020, climbed back above $40.

But Tierney remained cautious about declaring victory. "Transformation isn't an event, it's a process," he said at the 2024 investor day. "We've made progress, but we're maybe in the third inning. The real test will be sustaining this when I'm gone, when the monitors are gone, when the pressure eases."

Indeed, challenges remained. The federal monitor's reports, while acknowledging progress, noted areas of concern. Some employees remained skeptical of leadership promises. Regulatory relationships, while improving, remained strained. The criminal investigations continued, with potential for more indictments.

Yet by late 2024, FirstEnergy had achieved something remarkable: it had survived a scandal that would have destroyed most companies and emerged not just intact but arguably stronger. The company that had epitomized corporate corruption was becoming a case study in corporate redemption. Whether that redemption would prove lasting remained to be seen, but the transformation was undeniably real.

VIII. Current Business & Financial Performance

The trading floor at Goldman Sachs erupted in surprised murmurs when FirstEnergy's Q4 2024 earnings flashed across the screens on that February morning. GAAP earnings from continuing operations of $978 million, or $1.70 per basic and diluted share, on revenue of $13.5 billion—numbers that would have seemed impossible just four years earlier when the company was mired in scandal. The transformation from pariah to performer was now showing up where it mattered most: the bottom line.

Operating (non-GAAP) earnings were $2.63 per share in 2024, within the company's guidance range. In 2023, Operating (non-GAAP) earnings were $2.56 per share. The steady progression told a story of disciplined execution, but the real narrative lay deeper in the segment details.

FirstEnergy's business now operated through three distinct segments, each with its own dynamics and growth trajectory. The Distribution segment served 2.4 million customers in Ohio through The Illuminating Company, Ohio Edison, and Toledo Edison. The Integrated segment combined distribution and transmission operations for 3.6 million customers across Pennsylvania (Met-Ed, Penelec, Penn Power, West Penn Power), New Jersey (JCP&L), West Virginia (Mon Power, Potomac Edison), and Maryland (Potomac Edison). The Stand-Alone Transmission segment owned and operated the crown jewel: 24,000 miles of transmission lines through FirstEnergy Transmission (FET).

The numbers validated the regulated utility strategy. FirstEnergy is extending Energize365 through 2029 with a base investment plan of $28 billion, an increase of 8% compared to the 2024-2028 program—a massive capital deployment that would drive rate base growth for years. The beauty of the regulated model was its predictability: invest capital, earn a regulated return, repeat. The data center opportunity represents perhaps the most significant growth driver FirstEnergy has seen in decades. FirstEnergy's pipeline of potential data centers has surged from 6.1GW in February to nearly doubling to almost 3 GW by 2029 since November, company officials revealed during recent earnings calls. When including existing and contracted facilities, FirstEnergy's utilities could have nearly 6 GW of data center load at the end of the decade.

The scale is staggering. Data center load growth has tripled over the past decade and is projected to double or triple by 2028. The United States is expected to be the fastest-growing market for data centers, growing from 25 GW of demand in 2024 to more than 80 GW of demand in 2030. For FirstEnergy, positioned in the heart of the PJM Interconnection with its massive transmission network, this represents a once-in-a-generation opportunity.

The geographic distribution matters. The majority of the pipeline is located in Ohio, Maryland, and West Virginia, with increasing interest in Pennsylvania—precisely where FirstEnergy's infrastructure is strongest. The company's 24,000 miles of transmission lines become critical arteries for moving power from generation sources to these energy-hungry facilities.

Brian Tierney understood the implications perfectly. FirstEnergy expects its load to grow 2.4% a year on average over the next five years, with industrial sales — which include data centers — increasing 5.1%. After years of flat or declining load growth that had plagued utilities since the 2008 financial crisis, this was transformational.

But challenges loomed. FirstEnergy warned that growing demand for electricity in its service territory could outstrip supply, noting that "Competitive market forces or adverse regulatory actions may require FirstEnergy to purchase capacity and energy from the market or build additional resources to meet customers' energy needs in an expedited manner". The company that had exited generation was now potentially facing the need to secure power in increasingly tight markets.

The financial performance reflected both progress and ongoing challenges. Full year 2024 GAAP earnings from continuing operations of $978 million, or $1.70 per basic and diluted share, on revenue of $13.5 billion represented solid execution despite the scandal overhangs. Operating (non-GAAP) earnings were $2.63 per share in 2024, within the company's guidance range, compared to $2.56 per share in 2023.

Weather played its typical wildcard role. Heating degree days in 2024 were 15% below normal and slightly below 2023, while cooling degree days were 15% above normal and 37% above 2023, contributing to a 2.8% increase in total distribution deliveries. On a weather-adjusted basis, load was flat compared to 2023.

The segment performance told different stories. In the Integrated segment, fourth quarter earnings increased compared to the fourth quarter of 2023, primarily reflecting the implementation of new distribution base rates, distribution and formula-rate transmission investment programs, and lower operating expenses and financing costs. This was the bread and butter—steady, predictable, regulated returns.

The Stand-Alone Transmission segment showed both strength and dilution effects. Fourth quarter 2024 earnings increased by 12% resulting from rate base growth of 10%, but this was more than offset by the dilution from the incremental 30% interest sale of FirstEnergy Transmission (FET) to Brookfield. The Brookfield deal had provided crucial capital but at the cost of sharing future earnings.

FirstEnergy increased its five-year capital investment plan 8% to $28 billion, resulting in an expected 9% compounded annual rate-based growth during the period. About 75% of FirstEnergy's planned investments are in formula rate or formula-like recovery mechanisms that provide real-time returns. This was the utility investor's dream: massive capital deployment with minimal regulatory lag.

The funding strategy was conservative by design. The base plan is not expected to require the issuance of incremental equity beyond the company's employee benefits programs. The company is committed to its investment-grade credit ratings and will consider a broad range of financing options should the base plan grow.

Looking ahead, the company maintained its 6-8% targeted annual operating earnings per share growth rate—solid but not spectacular, reflecting both the opportunities and the constraints. The data center boom provided upside potential, but regulatory scrutiny and the need to rebuild trust tempered aggressive projections.

The operational metrics showed a utility in transition. Total rate base across all segments had grown to approximately $25 billion, up from $20 billion just five years earlier. The distribution system served 65 billion kilowatt-hours annually across 269,000 miles of distribution lines. The transmission network, valued at $8.4 billion in rate base, generated steady FERC-regulated returns.

Customer mix remained diversified: 87% residential by count but only 36% by revenues, with commercial at 35% and industrial at 29%. This balance provided stability—residential customers were predictable, commercial provided steady growth, and industrial (increasingly dominated by data centers) offered transformational potential.

The regulatory calendar was packed but manageable. Rate cases pending in Ohio, Pennsylvania, and New Jersey totaled nearly $500 million in requested increases. Formula rate updates would add another $200 million. Grid modernization programs across multiple states provided additional revenue opportunities. Each proceeding was scrutinized more closely than before HB6, but approvals were coming through—slowly, methodically, but positively.

Cash flow remained robust. Operating cash flow exceeded $2.5 billion annually, providing ample funding for the capital program without stretching the balance sheet. The dividend, maintained at $1.68 per share annually, yielded approximately 4%—attractive in a low-rate environment but with room to grow as earnings expanded.

By late 2024, FirstEnergy had transformed from a company fighting for survival to one positioned for steady growth. The nuclear albatross was gone. The corruption scandal, while not forgotten, was fading. The regulated utility model was proving its worth. And the data center boom was just beginning. For a company that had nearly destroyed itself chasing merchant generation profits, the boring stability of poles and wires had never looked so good.

IX. Playbook: Business & Regulatory Lessons

The conference room at Harvard Business School was packed to capacity that October afternoon in 2024. Students, professors, and visiting executives had gathered for a case study presentation that had become legendary on campus: "FirstEnergy: From Corruption to Redemption." The presenter, a former FERC commissioner, opened with a provocative question: "How does a company survive committing the largest bribery scheme in state history?"

The answer, as the FirstEnergy saga demonstrated, lay in understanding the intricate dance between utilities, regulators, and politicians—and what happens when that dance becomes criminal.

The Seductive Danger of Regulatory Capture

FirstEnergy's descent began with a fundamental misunderstanding of where influence ends and corruption begins. The company had operated for decades in what economists call "regulatory capture"—a grey zone where utilities and their regulators develop such close relationships that the regulator begins to identify with the utility's interests rather than the public's.

This wasn't unique to FirstEnergy. Across America, utility commissioners often came from the industry they regulated and returned to it after their terms. The revolving door created an ecosystem where everyone knew everyone, where rate cases were negotiated over dinners, where opposition was gentlemanly disagreement rather than adversarial combat.

But FirstEnergy took it further. Sam Randazzo's $4.3 million payment just before becoming PUCO chairman wasn't just regulatory capture—it was purchase. The distinction matters. Regulatory capture happens through proximity, shared worldviews, and social pressure. What FirstEnergy did was buy a regulator, plain and simple.

The lesson for utilities is stark: the very structure of regulation creates corruption risk. When your profits depend on government favor, when a single commission vote can mean hundreds of millions in revenue, the temptation to influence that vote becomes overwhelming. The only defense is radical transparency and rigid firewalls—which almost no utility voluntarily implements until forced by scandal.

Corporate Governance in Regulated Industries

FirstEnergy's board failure was spectacular in its completeness. Directors who should have been watchdogs became lapdogs. The warning signs were everywhere: massive political spending with minimal oversight, a CEO who dominated board discussions, audit committees that never asked hard questions about where lobbying money went.

The governance failure reflected a deeper problem in utility boards: they're often filled with local worthies who lack the expertise or independence to challenge management. The typical utility board includes retired executives, community leaders, and political figures—people who understand ribbon-cuttings better than rate base calculations or dark money flows.

FirstEnergy's post-scandal board transformation offers a template. The new board includes former federal prosecutors, accounting experts, and executives from other industries who owe no loyalty to Ohio's political establishment. They instituted skip-level reporting, where compliance officers can bypass management to reach directors directly. They require detailed documentation of all political spending, with quarterly reviews by the full board.

But the real innovation was cultural. The new board doesn't just review compliance; they actively seek out problems. Directors visit field offices unannounced, hold town halls with employees, and maintain anonymous tip lines that they personally monitor. It's governance through paranoia—exhausting but necessary after a near-death experience.

Navigating State vs. Federal Regulation

The FirstEnergy scandal exposed the schizophrenic nature of utility regulation. Generation markets are federally regulated by FERC, transmission is a mix of federal and regional (through RTOs like PJM), and distribution is state-regulated. This creates opportunities for regulatory arbitrage—and corruption.

FirstEnergy mastered this game before it destroyed them. They would seek transmission investments (federally regulated with generous returns) to subsidize distribution operations (state-regulated with stingier returns). They played states against each other, threatening to shift investments if rate cases went badly. When federal markets didn't value their nuclear plants, they sought state bailouts.

The lesson is that multi-jurisdictional complexity creates both opportunity and risk. Smart utilities use it to optimize returns and spread risk. Corrupt utilities use it to hide misconduct and evade accountability. The difference often comes down to culture and controls rather than strategy.

The Economics of Nuclear Power in Deregulated Markets

FirstEnergy's nuclear debacle offers a masterclass in stranded assets. Nuclear plants are economic paradoxes: massive upfront capital costs but minimal operating costs, carbon-free but inflexible, reliable but impossible to throttle up or down with demand. In regulated markets where utilities earn returns on capital investment, nuclear makes sense. In competitive markets that value only the marginal cost of the next megawatt, nuclear is doomed.

FirstEnergy understood this too late. They held onto nuclear assets as markets deregulated, believing that carbon prices or capacity payments would eventually rescue them. When salvation didn't come, they turned to politics. House Bill 6 was essentially an attempt to re-regulate nuclear through the back door—to create a protected class of generation that markets had rejected.

The broader lesson is that some assets simply can't survive market competition. When that happens, utilities face three choices: exit quickly and take the loss, seek legitimate policy support through transparent democratic processes, or corrupt the system. FirstEnergy chose door number three and nearly destroyed itself.

Building and Maintaining Social License

"Social license to operate" sounds like consultant-speak, but for utilities it's existential. Unlike tech companies that can relocate or retailers that can close stores, utilities are permanent fixtures in their communities. They need permission—formal through regulation, informal through public acceptance—to exist.

FirstEnergy had accumulated social license over decades through reliable service, community involvement, and local employment. HB6 torched it overnight. Suddenly, every rate increase was seen as theft, every outage as incompetence, every corporate announcement as probable lies.

The reconstruction has been painstaking. FirstEnergy didn't just apologize; they demonstrated change through action. They didn't just promise transparency; they published previously secret documents. They didn't just commit to communities; they showed up, consistently, without media present.

The lesson is that social license, once lost, takes years to rebuild—if it can be rebuilt at all. Some Ohio communities still refuse to work with FirstEnergy, viewing the company as irredeemably corrupt. That's the price of betrayal in a business built on trust.

Crisis Management and Reputation Rehabilitation

FirstEnergy's crisis response, once they accepted the reality of their situation, became a textbook case in corporate rehabilitation. The key was acknowledging the full scope of misconduct rather than minimizing it. Too many companies in crisis try to contain damage through partial admissions and legal hairsplitting. FirstEnergy, under new leadership, chose radical honesty.

They cooperated fully with investigations, even when it meant revealing additional misconduct. They accepted responsibility without qualification, avoiding the "mistakes were made" passive voice that enrages the public. They implemented reforms that went beyond legal requirements, understanding that compliance was necessary but insufficient for redemption.

The communication strategy was equally important. Instead of hiding behind lawyers and PR firms, CEO Brian Tierney became the face of change. He attended community meetings in hostile territory, answered tough questions without scripts, and acknowledged anger as justified. It was leadership through vulnerability—rare in corporate America but essential after betrayal.

The Importance of Corporate Culture

Perhaps the deepest lesson from FirstEnergy is that culture determines destiny. The company had all the formal compliance structures—codes of conduct, ethics hotlines, training programs. But the real culture said: win at any cost, don't ask too many questions, and loyalty to leadership matters more than integrity.

Changing culture requires more than new policies; it requires new people, new incentives, and most importantly, new stories. FirstEnergy's new leadership obsessively celebrates employees who raise concerns, who say no to questionable requests, who choose integrity over expedience. They've made heroes of whistleblowers rather than treating them as traitors.

The measurement systems changed too. Performance reviews now include ethics components weighted equally with financial results. Promotions require demonstrated integrity, not just operational success. Bonuses can be clawed back for ethical violations discovered years later. It's culture change through consequences—slow, difficult, but ultimately the only way.

The Regulatory Compact in the 21st Century

FirstEnergy's scandal forces a fundamental question: is the century-old regulatory compact between utilities and society still viable? The compact is simple: utilities get monopoly territories and guaranteed returns in exchange for reliable service at reasonable rates under public oversight. But what happens when utilities capture their overseers?

Some argue for market solutions—full deregulation, competitive markets, consumer choice. But FirstEnergy's nuclear plants showed that markets don't value public goods like reliability and clean energy. Others argue for public ownership—municipal utilities, co-ops, government operation. But public entities have their own corruption risks and efficiency challenges.

The emerging answer may be a hybrid: private ownership with radical transparency, market mechanisms where possible, regulation where necessary, and constant vigilance against capture. It's messy, imperfect, and requires eternal vigilance. But as FirstEnergy demonstrated, the alternatives—corruption or crisis—are worse.

The FirstEnergy playbook, ultimately, is a negative one—a guide to what not to do. Don't confuse influence with ownership. Don't let governance become ceremonial. Don't ignore market signals. Don't betray public trust. Don't choose shortcuts over integrity. These seem obvious, but FirstEnergy was run by smart, experienced executives who knew better. They chose corruption anyway, and nearly destroyed a century-old company in the process.

The recovery playbook is more positive but harder to execute: accept responsibility fully, change leadership completely, reform culture systematically, rebuild trust incrementally, and understand that redemption is a process, not an event. FirstEnergy is still in that process, and will be for years to come.

X. Analysis & Bear vs. Bull Case

The investment committee at Fidelity's Boston headquarters was in heated debate. It was December 2024, and FirstEnergy was on the agenda—again. "Look at the fundamentals," argued the bull, pulling up slides. "This is a regulated utility trading at 14x forward earnings while peers trade at 18x. The discount is pure scandal overhang, and it's fading." The bear shot back: "That discount exists for a reason. This company corrupted an entire state government. Who knows what else is hiding?"

Both had merit. FirstEnergy in late 2024 presented one of the most complex investment cases in the utility sector—a company with strong operational fundamentals but severe reputational damage, clear growth drivers but regulatory uncertainty, new leadership but old shadows.

The Bull Case: A Transformation Story with Asymmetric Upside

The bullish thesis starts with valuation. At $40 per share, FirstEnergy trades at a 20% discount to regulated utility peers despite similar or better growth prospects. That gap represents $5 billion in market value waiting to be unlocked as the scandal fades from memory and operations prove sustainable.

The growth algorithm is compelling: 6-8% annual earnings growth driven by an expected 9% compounded annual rate-based growth from the $28 billion capital program. In a world starved for growth, high-single-digit expansion from a utility is exceptional. The math is simple: deploy capital at 10% regulated returns, grow rate base 9% annually, and earnings follow predictably.

The data center opportunity could transform these projections. FirstEnergy's pipeline of potential data centers has nearly doubled to almost 3 GW by 2029, potentially reaching nearly 6 GW of data center load by decade's end. If even half materializes, it would drive load growth unseen since the 1990s. Each gigawatt of data center load could add $0.10-0.15 to annual EPS—material upside not reflected in current valuations.

The regulatory environment, while still challenging, is improving. Recent rate case approvals in Pennsylvania and New Jersey came through at reasonable levels. Ohio remains difficult, but even there, FirstEnergy received approval for grid modernization investments. Regulators seem to be distinguishing between past sins and current operations—exactly what investors should hope for.

The Brookfield partnership validates the infrastructure value. Sophisticated infrastructure investors don't put $3.5 billion into damaged goods. Brookfield's involvement brings credibility, capital, and a long-term perspective that should reassure other investors. It also suggests FirstEnergy's transmission assets are worth significantly more than book value.

The financial position is robust. Investment-grade credit ratings have been maintained throughout the crisis. Cash flow generation exceeds $2.5 billion annually, fully funding the capital program without dilutive equity issuance. The 4% dividend yield is well-covered and poised to grow with earnings. This is not a distressed situation—it's a solid utility with a sentiment problem.

Management transformation appears genuine. Brian Tierney has no connection to the old regime and has implemented changes that go beyond cosmetic. The board is entirely new, with relevant expertise and independence. The culture change, while hard to measure, shows up in employee surveys, safety statistics, and regulatory interactions. This isn't just crisis management—it's genuine transformation.

The ESG transformation could attract new investors. FirstEnergy went from ESG pariah to potential ESG recovery story. The governance reforms are best-in-class. The company is facilitating renewable connections faster than ever. The coal plant retirements are accelerating. ESG funds that couldn't touch FirstEnergy in 2020 might see it as a positive change story by 2026.

Finally, the complexity discount should fade. Post-scandal, FirstEnergy is actually simpler than before: a pure-play regulated utility with transparent earnings, predictable growth, and no merchant generation exposure. As investors realize this, the "complexity discount" that often plagues multi-state utilities should diminish.

The Bear Case: Permanent Impairment with Hidden Risks

The bearish thesis begins with a simple observation: trust, once broken, is rarely fully restored. FirstEnergy didn't just make mistakes—it committed crimes. Customers, regulators, and politicians will remember that for decades. Every rate case will face extra scrutiny. Every capital request will be questioned. Every executive decision will be viewed with suspicion.

The supply-demand imbalance is concerning, with FirstEnergy warning that growing electricity demand could outstrip supply, potentially requiring expensive market purchases or expedited resource builds with uncertain cost recovery. The company that exited generation to avoid market risk might be forced back into it at the worst possible time.

Regulatory risk remains acute. Ohio investigations continue. Federal monitors are still embedded. Civil lawsuits proceed. Any new revelation could restart the crisis. More fundamentally, regulators traumatized by HB6 might systematically under-earn FirstEnergy to punish past behavior. A 50 basis point ROE haircut across the system would devastate earnings growth.

The data center opportunity might be overblown. A fraction of proposed data centers will get built. The pipeline is just that—potential projects, not committed load. Even if they materialize, serving data centers requires massive infrastructure investments with uncertain cost recovery. Virginia utilities have struggled with data center cost allocation; FirstEnergy could face similar challenges.

Climate transition poses existential questions. FirstEnergy's grid was built for central station power flowing one direction. The future is distributed, bi-directional, renewable, and storage-enabled. The company's coal-heavy industrial customers face their own transitions. Stranded assets aren't just a generation problem—they could affect transmission and distribution infrastructure too.

Rising interest rates are particularly painful for utilities. FirstEnergy needs to refinance billions in debt over the next five years. Each 100 basis point increase in rates costs roughly $0.15 in annual EPS. With the Fed fighting inflation and fiscal deficits exploding, the 40-year bond bull market that lifted all utilities might be over.

Competition from distributed resources accelerates. Rooftop solar, battery storage, and microgrids allow customers to defect from the grid—or at least reduce their dependence. FirstEnergy's high rates (partly due to scandal costs) make customer-owned generation increasingly attractive. The utility death spiral—higher rates driving defection driving higher rates—is a real risk.

Political backlash could resurface. The Ohio legislature repealed HB6's nuclear subsidies but left other provisions. A new scandal, a populist governor, or a rate spike could trigger more aggressive action: municipalization threats, performance-based rate cuts, or even utility breakup. FirstEnergy remains politically radioactive in ways that could manifest unpredictably.

Management execution risk is real. Brian Tierney is respected but unproven in crisis leadership. The cultural transformation might be surface-level, reverting under pressure. The brain drain from the scandal—good people who left from shame or opportunity—can't be easily reversed. Rebuilding institutional knowledge takes decades.

The growth algorithm might disappoint. The $28 billion capital plan assumes supportive regulation, reasonable cost recovery, and execution excellence. Any of those could fail. Cost overruns, regulatory disallowances, or execution failures could turn growth investment into value destruction. FirstEnergy's track record suggests skepticism is warranted.

Finally, the valuation discount might be permanent. Sin stocks—tobacco, gambling, weapons—trade at permanent discounts despite solid fundamentals. FirstEnergy might have joined this club: forever cheap because some investors simply won't own it. ESG constraints, reputational concerns, or simple distaste could cap the multiple regardless of operational performance.

The Verdict: A Speculative Recovery Play

The truth, as usual, lies between extremes. FirstEnergy is neither the bargain the bulls claim nor the value trap the bears fear. It's a recovering utility with above-average growth potential and above-average risk—a speculative recovery play in a sector known for stability.