FedEx Freight: The Spin-Off of North America's LTL Powerhouse

I. Introduction & Episode Roadmap

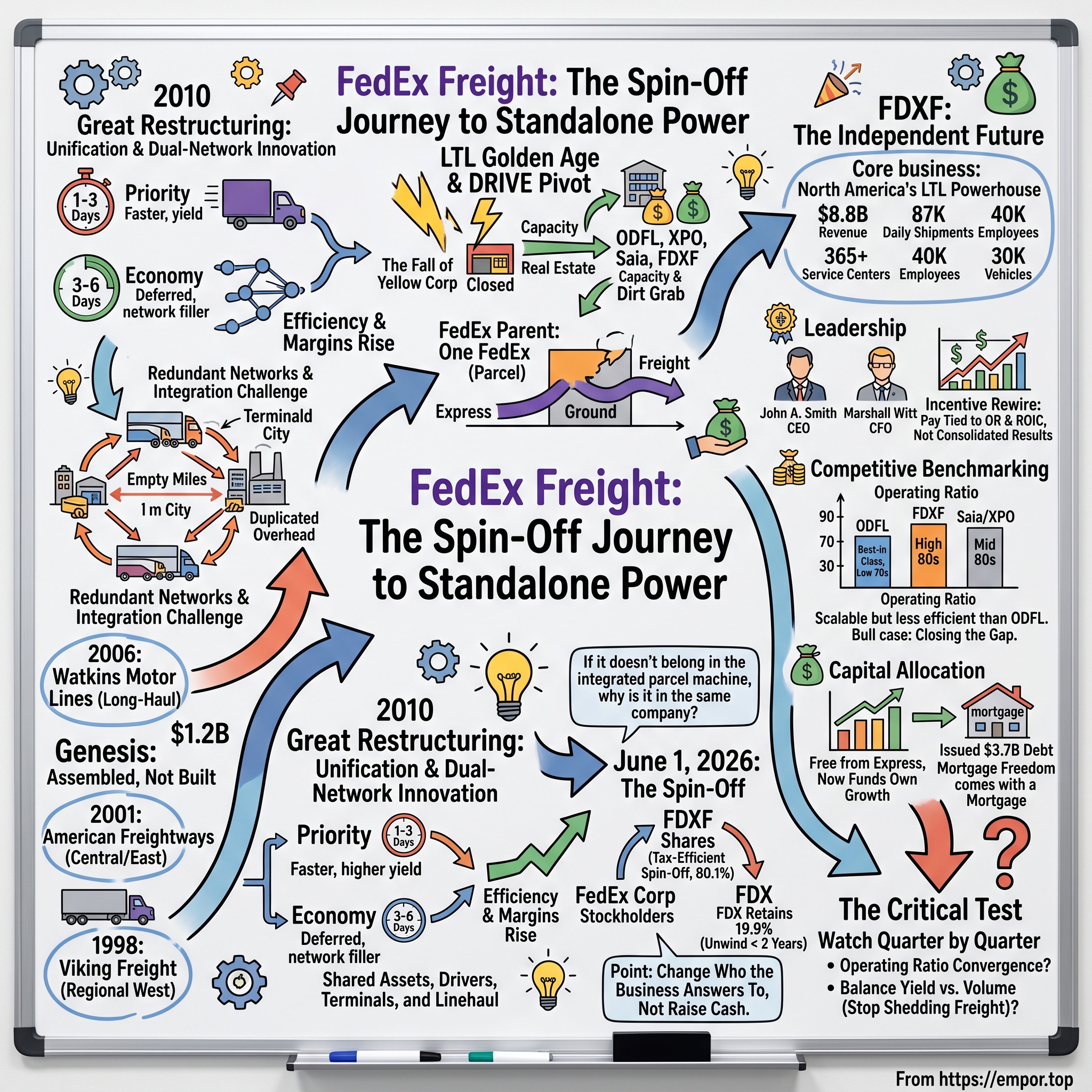

On the morning of June 1, 2026, a company that had never traded a single share in its own name opened on the floor of the New York Stock Exchange under four new letters: FDXF. There was no roadshow in the traditional sense, no bankers ringing the bell for a hot IPO, no oversubscribed order book. Instead, roughly 150 million shares simply appeared in the brokerage accounts of FedEx Corporation stockholders — one share of FedEx Freight for every two shares of the parent they already owned.1 A fifty-two-year-old business that had spent its entire life as a division, a line item, a segment footnote in someone else's 10-K, woke up as an independent public company worth billions.1

This is the story of how the largest less-than-truckload carrier in North America got there — and whether being set free will actually unlock the value the story promises.

The mechanics of that morning are worth dwelling on, because they tell you what kind of transaction this was. FedEx did not sell FedEx Freight to a private-equity buyer or float it in a cash-raising IPO. It performed a classic tax-efficient spin-off: it distributed 80.1% of Freight's shares directly to its own stockholders on a pro-rata basis — one FDXF share for every two FDX shares held as of the May 15, 2026 record date — while the parent retained 19.9%, which it committed to unwind within about two years.1 No new capital came into the operating company from the distribution itself; the exercise was purely about ownership and structure. The point was never to raise money. The point was to change who the business answers to. That distinction — a company that suddenly has its own board, its own stock, its own cost of capital, and its own investors to satisfy, but not a fresh pile of cash to spend — is the entire drama of a spin-off, and it colors everything that follows.

Let's establish the shape of the thing first. FedEx Freight generated $8.8 billion in revenue in its fiscal year ended May 31, 2026, moved roughly 87,000 shipments on an average day, ran a network of more than 365 service centers, and employed about 40,000 people driving nearly 30,000 vehicles.21 Those are utility-scale numbers. And yet for decades this business was, in a very real sense, invisible — its economics blended into a parent whose identity was defined by purple-and-orange jets flying overnight parcels, not by red tractor-trailers hauling steel pallets down interstate corridors.

The conglomerate question. The bull thesis behind this spin-off is deceptively simple: a high-return, asset-heavy, cash-generative LTL franchise had been trapped inside FedEx Corporation, where its margins helped fund the capital furnace of the Express air network and where the market never gave it credit as a standalone franchise. Pure-play peer Old Dominion Freight Line had for years traded at premium multiples that the Freight segment, buried inside FDX, could never capture. The spin is a bet that separation reveals value that common ownership concealed. That is the claim. This article's job is to test it rather than repeat it.

Themes we'll trace:

- Why less-than-truckload trucking has some of the best structural economics in all of transportation — and why truckload, its cousin, has almost none.

- How FedEx Freight was not built but assembled, through a decade of expensive acquisitions in the late 1990s and 2000s, and how that roll-up nearly strangled itself in a 2010 integration crisis.

- How the 2023 collapse of Yellow Corp yanked nearly a tenth of the industry's capacity off the road overnight and handed the survivors a pricing gift.

- And the central standalone question: what happens when a cash cow stops subsidizing its capital-hungry siblings and has to answer to its own shareholders?

One inconvenient fact frames everything that follows. FedEx Freight did not spin off at the top. It spun off into the third year of an industrial freight recession, with volumes down and margins compressed well below their prior peak. The pitch deck describes a champion; the timing handed investors a champion mid-slump. Both things are true, and the gap between them is where the interesting analysis lives.

Myth versus reality, up front. The consensus narrative around this spin-off can be summarized in one tidy sentence: a hidden gem trapped in a conglomerate is finally being unlocked at its true value. It is a satisfying story, and it is partly true — but it smuggles in two assumptions worth challenging before we go further. The first is that FedEx Freight's economics are as pristine as the headline peak figures suggest; the reality, as the financials section will show, is a very good but not best-in-class carrier running well below the leader on the metric that matters most. The second is that separation itself creates value, as if the act of distributing shares conjures earnings power; the reality is that a spin-off only creates value if the newly-accountable managers actually run the business better than it was run before, against a debt load and standalone cost base it didn't carry as a division. Value from a spin-off is earned in the operating results after the separation, not granted by the separation. Keep those two corrections in mind, because most of the bullish commentary quietly assumes both away.

II. LTL Economics 101: Why Trucking's Elite Segment Has God-Tier Barriers

Picture two trucks leaving a factory in Ohio. The first is a full truckload carrier: one customer has filled all 53 feet with a single product, and the driver runs it straight to one destination. The second is a less-than-truckload truck: it is carrying seventeen different customers' pallets — a few crates of auto parts, some packaged food, a pallet of industrial fasteners — each headed to a different city. That single distinction, whether a truck carries one shipper's freight or many, splits trucking into two completely different businesses with wildly different economics.

The fragmented cousin. Truckload is one of the most brutally competitive industries in America. A driver with a leased tractor and a bank loan can become a truckload carrier next week; there are hundreds of thousands of them. There is no network, no consolidation, no barrier — just a spot market where rates swing violently with diesel prices and demand. It is a business of almost zero durable pricing power.

The consolidated aristocrat. Less-than-truckload is the opposite. Because no single customer fills the trailer, the carrier's entire job is consolidation: picking up small shipments locally, hauling them to an origin terminal, sorting and combining them with other freight headed the same direction, running dense long-haul "linehaul" lanes between hubs, then breaking the freight apart again at destination terminals for local delivery.[^warp] This hub-and-spoke choreography — the industry calls the sorting facilities "cross-docks" — only works if you own a national lattice of terminals and run enough freight through each lane to fill the trucks. You cannot start that next week. You cannot start it next decade.

To make it concrete, follow a single pallet. A machine-shop in suburban Cleveland calls at 2 p.m. and asks for a pallet of gearboxes to be shipped to a distributor in Phoenix. A local FedEx Freight "pickup and delivery" driver — the industry calls this the P&D operation — swings by that afternoon, collects the pallet along with a dozen other pickups on the route, and returns to the Cleveland service center by early evening. There, on a long concrete dock lined with dozens of doors, workers unload every P&D truck and re-sort the freight by destination: everything headed toward the Southwest gets loaded into a single linehaul trailer. Overnight, a linehaul driver runs that trailer — now full of many customers' Southwest-bound freight — toward a breakbulk hub, where it may be re-sorted again, before a final linehaul leg delivers it to the Phoenix terminal. There, the process runs in reverse: the pallet is unloaded, sorted onto a local P&D route, and delivered to the distributor's door. One pallet, four to six handoffs, several trucks, two or three terminals — and the customer paid a fraction of what a dedicated truck would have cost, because seventeen other shippers rode the same trailers. That is the entire miracle of LTL: it makes shipping a single pallet across the country economical by sharing the ride. And the machine that performs that miracle — the terminals, the sort labor, the linehaul lanes — is exactly what a new entrant cannot conjure.

Run the LTL business through Hamilton Helmer's 7 Powers and it lights up like a pinball machine:

- Scale economies through density. The magic word in LTL is density — freight per lane, shipments per terminal, weight per truck. A carrier that runs two trucks a day between Dallas and Atlanta has a higher cost per shipment than one running twenty, because the fixed cost of the linehaul is spread across more freight. Density is a flywheel: more volume lowers unit cost, which wins more volume. This is the single most important concept in the entire industry, and we'll return to it constantly.

- Network effects on the demand side. A national manufacturer wants one carrier that can deliver a pallet to any of the lower 48 on one invoice, one tracking system, one claims process. A carrier that covers only the Southeast simply cannot win that account. Coverage begets the highest-value corporate contracts, which fund more coverage.

- A cornered resource hiding in plain sight: dirt. The terminals are the moat, and here is the punchline that makes LTL investors salivate — you effectively cannot build new ones. A cross-dock terminal is an industrial facility with dozens of truck doors, needing highway access, heavy-truck zoning, and acres of land near a metro area. Municipal zoning, environmental review, and neighborhood opposition have made permitting new terminals in major markets close to impossible. The existing footprint is a largely irreplaceable asset, which is why, as we'll see, a bankrupt competitor's real estate becomes the industry's most contested prize.[^ltlafter]

- Switching costs. Large shippers wire their own warehouse and ERP systems directly into a carrier's dispatch, routing, and billing. Ripping that integration out to save a few percent is rarely worth the operational risk, which is why LTL customer relationships are famously sticky.

There is a second layer to the density point that deserves its own beat, because it is the crux of the whole economic model. In LTL, the cost curve is dominated by fixed costs — the terminal is there whether ten trailers or fifty pass through it, the dock crew is staffed whether the freight is heavy or light, and the linehaul driver is paid for the run whether the trailer leaves 60% or 95% full. This means the marginal cost of one additional shipment on an existing lane is tiny, while the marginal revenue is close to the full price. So density doesn't just lower unit cost a little; it flips a lane from mediocre to spectacular once utilization crosses a threshold. A carrier that already owns the dense lanes earns outsized margins on incremental freight, while a challenger trying to build density from scratch runs half-empty trucks at a loss for years, hoping to reach critical mass before the balance sheet gives out. That asymmetry — incumbents printing money on the freight they add, challengers bleeding on the freight they chase — is why LTL market share is so stable and why the roster of national carriers has barely changed in decades. It is also why the disappearance of a single national carrier, as happened in 2023, is such a seismic event: it doesn't just remove a competitor, it hands the survivors instant density on lanes they already owned.

Put those together and you get an industry that behaves less like trucking and more like a regulated utility that forgot to get regulated: consolidated, capital-intensive, hard to enter, and — in good times — extremely profitable. Understanding that is the precondition for understanding why FedEx spent more than a billion dollars in the 2000s to buy its way into it, and why the resulting collection of parts took a decade to work.

III. The Genesis: Roll-up, Legacy Redundancies, and the M&A Benchmark

Here is a fact that surprises people: FedEx, the company synonymous with overnight air express, did not organically grow a great LTL carrier. It bought one, piece by piece, and the seams showed for years.

Viking Freight (1998): the accidental entry. FedEx's first foothold in heavy freight arrived almost as a byproduct. In January 1998 FedEx acquired Caliber System in a stock deal valued in the billions, and the prize everyone talked about was RPS, the ground-parcel carrier that would become FedEx Ground and, eventually, one of the most valuable businesses in the entire company. Folded into the same deal, almost as an afterthought, came Viking Freight — a well-regarded premium regional LTL carrier that dominated the West Coast with a reputation for fast, reliable service. FedEx founder Fred Smith had built an empire on the insight that time-definite delivery was worth paying for; Viking was that same philosophy applied to heavy freight. FedEx suddenly owned a good regional trucking company without having set out to build one. For a few years that was enough — a strong western franchise operating quietly under the FedEx umbrella, generating cash, attracting little attention. But a purely regional carrier could never win the national accounts that value coast-to-coast coverage, and once FedEx decided it wanted to be a national LTL player, a West Coast footprint was a starting point, not a destination.

American Freightways (2001): the megadeal. Ambition arrived at the turn of the millennium. In November 2000, FedEx agreed to acquire American Freightways, an Arkansas-based carrier with a dense network across the Central, Southern, and Eastern United States, in a transaction valued at roughly $1.2 billion — about $950 million in cash and stock plus roughly $250 million of assumed debt.[^af] American Freightways was itself a self-made success, a carrier built up over the preceding two decades into one of the largest interstate LTL operators in the country, with hundreds of service centers concentrated in exactly the industrial heartland and Southeast that Viking's western network could not touch. Overnight, FedEx went from a strong regional player to a carrier with genuine national reach. The price was steep — a meaningful premium to where public LTL comparables traded at the time, on the order of 30% to 40% above prevailing trading multiples — but the logic was structural: American Freightways occupied the eastern two-thirds of the map that Viking couldn't reach, and you cannot replicate a coast-to-coast terminal network by building it. When the asset is irreplaceable, the acquirer pays up. Whether "irreplaceable" justified that premium is exactly the kind of question that only gets answered years later, in the margin line — and, as we'll see, the answer arrived with a lag measured in years, not quarters.

Watkins Motor Lines (2006): finishing the map. The last major piece came in 2006, when FedEx bought Watkins Motor Lines, a long-haul carrier, for $780 million in cash and rebranded it FedEx National LTL.[^watkins] Watkins gave FedEx the long-haul, coast-to-coast capability it still lacked. On paper, the national LTL puzzle was now complete: Viking in the West, American Freightways in the middle and East, Watkins tying it together on the long routes.

The integration nightmare. On paper. In reality, FedEx made a fateful choice: it ran these acquisitions as separate companies. For years there was FedEx Freight East (the old American Freightways), FedEx Freight West (the old Viking), and FedEx National LTL (the old Watkins) — three brands, three sales forces, three networks, three cultures, frequently competing for the same freight. The physical absurdity was hard to miss: redundant terminals sitting blocks apart in the same city, trucks from two FedEx units running the same lane half-empty, salespeople from different FedEx divisions calling on the same customer, sometimes quoting different prices for the same load. The synergies that justified the acquisition premiums existed on a slide; on the ground there were empty miles, duplicated overhead, and the friction of merging blue-collar operating cultures that had spent decades as rivals.

Why would a company as operationally sophisticated as FedEx tolerate this? Partly because the individual carriers were good, and the instinct "if it isn't broken, don't break it" is powerful when each unit is still profitable in isolation. Partly because merging LTL networks is genuinely hard and risky — you are re-plumbing the physical flow of freight for tens of thousands of daily shipments, and a botched integration can degrade service and hemorrhage customers faster than any spreadsheet synergy can be captured. And partly because, inside a conglomerate flush with Express and Ground cash, the pressure to squeeze every last basis point out of Freight simply wasn't there. The result was a business that had assembled all the parts of a category-leading LTL carrier while operating like three medium-sized ones stapled together — the strategic equivalent of buying a champion racehorse and keeping it in three separate stables.

Did FedEx overpay? In the narrow sense of near-term synergy capture, the honest answer is yes — the company bought the pieces of a national network years before it was willing to do the hard, unglamorous work of fusing them into one. The strategic map was brilliant. The execution lagged it by the better part of a decade. And then, at the worst possible moment, the economy fell off a cliff — which is where the real turnaround story begins.

IV. The 2010 Great Restructuring & The Dual-Network Invention

The freight business is a leading indicator of the industrial economy, which means when America stops building things, LTL carriers feel it first and feel it hardest. In 2008 and 2009, America stopped building things. Industrial production collapsed, manufacturing shipments evaporated, and FedEx Freight — still running as a fragmented collection of overlapping networks — bled. A business with high fixed costs (all those terminals, all those drivers) and suddenly not enough freight to fill them is a machine for destroying operating income. The recession did what internal memos never could: it made the cost of running three separate networks impossible to ignore.

The unification. Beginning around 2010–2011, FedEx finally did the thing it had deferred for a decade. It merged the regional and long-haul operations into a single, unified FedEx Freight, retired the FedEx National LTL brand, consolidated the overlapping terminals, and rebuilt the operation on one common IT backbone. The competing sales forces became one. The duplicated overhead came out. This was not a growth initiative; it was corporate surgery performed under recessionary anesthesia, and it was overdue.

The timing matters to the analysis. Companies rarely undertake painful, service-risking integrations when times are good and the cash is flowing; they do it when the alternative is worse. The 2008–2009 collapse made the cost of running three overlapping networks unsurvivable, and it took that existential pressure to force a decision that had been economically obvious for years. This is a recurring pattern in the FedEx Freight story — and, arguably, in the spin-off itself: the business tends to make its hardest, best decisions only when circumstances leave no choice. For an investor, that raises a fair question about whether an independent FedEx Freight will pursue the next round of hard optimizations proactively, or wait for the next crisis to force its hand.

The genuine innovation: two speeds on one network. Out of that restructuring came the idea that still defines the company. Rather than run separate premium and economy operations, FedEx Freight layered two service tiers onto a single set of trucks, terminals, and drivers:

- FedEx Freight Priority — fast, time-definite service for shippers who need it there quickly, transiting in roughly one to three days, commanding the highest yield.2

- FedEx Freight Economy — deferred, lower-cost service transiting in roughly three to six days, for shippers who care more about price than speed.2

Why does this matter beyond marketing? Because of density. Recall that the enemy of an LTL carrier is a half-empty truck and an idle terminal door. Economy freight is the network filler: it can ride during off-peak windows, take longer routings that leverage rail, and soak up capacity that would otherwise run empty, all while Priority freight gets the premium, time-sensitive treatment. Roughly half of the company's customers use a blend of both, choosing speed or savings shipment by shipment on the same underlying network.2 One sales force, one set of assets, two products — the operating leverage of shared infrastructure with the price discrimination of segmented service.

Consider the elegance of it. A pure premium carrier has to run its network to meet the tightest transit commitments, which can leave capacity stranded during the slower parts of the operating day. A pure economy carrier maximizes utilization but forfeits the pricing power of speed. By running both on one network, FedEx Freight can fill the linehaul trailers with deferred Economy freight — sometimes routing it over rail intermodal to cut cost — precisely in the windows and lanes where Priority volume alone wouldn't fill the truck. The premium freight pays for the speed; the economy freight pays for the utilization; and both share the same terminals, drivers, and dock labor. The company markets its Priority service as meaningfully faster than the nearest competitor on published transit times, which lets it charge for speed where speed matters, while Economy keeps the expensive assets busy the rest of the time.2 It is a textbook example of using one asset base to serve two willingness-to-pay curves — the kind of structural cleverness that is easy to describe and genuinely hard for a subscale competitor to copy, because it requires the density to make both tiers work at once.

This is process power in the Helmer sense: an advantage embedded in how the company runs rather than in a single asset. And it is the foundation on which FedEx Freight scaled to more than $9 billion in revenue at its peak — the mechanism that turned a painfully integrated roll-up into a genuine national franchise. What it could not do was change the weather. And in 2023, the weather changed in the most dramatic way the LTL industry had seen in a generation.

V. The LTL Golden Age: The Fall of Yellow & The DRIVE Pivot

For most of a century, Yellow was one of the pillars of American trucking — a unionized coast-to-coast LTL giant, at times the third-largest in the country. And then, over a single summer, it was gone. Its death was slow, then sudden. For years Yellow had staggered under a debt load accumulated through its own ill-digested acquisitions (Roadway and USF, among others), a heavily unionized cost structure, and an aging, tangled network it could never fully consolidate. It had even taken a controversial $700 million federal pandemic-era loan in 2020 that kept it alive but did nothing to fix the underlying disease. By the summer of 2023, a bitter standoff with the Teamsters over a restructuring plan tipped the whole thing over: as a strike loomed, customers — who cannot afford to have their freight stranded — fled en masse to rivals, and once the freight left, the cash left with it. In late July 2023 Yellow ceased operations, and in August 2023 it filed for Chapter 11.[^ltlafter] Roughly 30,000 jobs vanished and, in one stroke, an estimated near-tenth of the entire North American LTL capacity came off the road.[^ltlafter]

There is a hard lesson buried in Yellow's demise that bears directly on the FedEx Freight thesis. Yellow's fatal weaknesses were, point for point, the mirror image of what makes a great LTL carrier: it was heavily unionized where the strongest operators are non-union and flexible; it was a poorly integrated roll-up where the leaders run unified networks; and it competed on price where the winners compete on density and service. Yellow was, in a sense, the cautionary version of the very roll-up problem FedEx Freight spent a decade escaping. That FedEx did the painful integration work in 2010 and Yellow never did is a large part of why one is spinning off as an industry champion and the other was auctioned for parts.

The capacity land grab. For the survivors, this was manna. When a tenth of an industry's supply disappears in a market where you cannot build new capacity, the freight has to go somewhere — and it went to Old Dominion, Saia, XPO, Estes, and FedEx Freight, who absorbed Yellow's customers and, crucially, competed for its irreplaceable real estate. Yellow's terminals were auctioned through the bankruptcy for slightly under $1.9 billion.6 XPO grabbed 28 properties for roughly $870 million; Estes took 24 for about $249 million; Saia scooped up 17 for around $236 million.6 In an industry where the scarce resource is zoned industrial dirt near metros, Yellow's collapse was less a tragedy for the survivors than a once-in-a-generation restocking of the shelves. It kicked off what the industry openly called an LTL "golden age" of firm pricing and disciplined capacity.

Which makes the timing of FedEx Freight's spin-off worth pausing on. The Yellow windfall lifted the whole industry in 2023–2024; by the time FDXF actually debuted in mid-2026, the industrial economy had softened again and the golden-age glow had dimmed into a grind. The spin-off rode the narrative of the golden age into a market that had already moved past its best pricing. Notably, FedEx Freight was a relatively restrained participant in the terminal land grab compared with XPO and Saia, which spent aggressively to expand their door counts — a choice that looks either prudent or timid depending on where the cycle goes next. A skeptic would note that the survivors' pricing discipline is only as durable as the industry's collective restraint on adding capacity; if Saia's and XPO's newly acquired terminals fill up and reignite lane-level competition, the "golden age" framing ages badly.

The "One FedEx" conundrum. Meanwhile the parent had troubles of its own. Under CEO Raj Subramaniam, FedEx had launched DRIVE, a sweeping cost-reduction and network-consolidation program that eventually surpassed a $4 billion annual savings target, folding the once-separate Express and Ground operations into a single integrated network branded "One FedEx." Notice what was conspicuously absent from that integration: Freight. And for a good reason. There is no operational synergy between hauling a 900-pound palletized shipment on a heavy LTL linehaul and flying a two-pound overnight envelope on a jet. You do not put freight pallets on passenger-package delivery vans or in the belly of an Express aircraft; the networks share almost nothing physically. Freight's exclusion from "One FedEx" was the tell — if it doesn't belong in the integrated parcel machine, why is it in the same company at all?

The strategic review and the decision. FedEx had studied this question before. In mid-2024 it launched a formal assessment of the role of Freight within the portfolio — the kind of "strategic review" language that, in corporate dialect, usually signals that a separation is already being seriously modeled. Pressed by investors and sharpened by Freight's structurally higher margins being obscured inside a capital-intensive parcel conglomerate that was simultaneously fighting its own margin battle through DRIVE, the review reached its conclusion by year-end. On December 19, 2024, FedEx announced its intent to spin off the entire Freight segment into an independent public company, framing it as the way to let each business be valued on its own terms and to give Freight the strategic and financial flexibility to invest in its own future.[^announce] Subramaniam's argument was, essentially, that the market would pay more for the two businesses apart than together — a sum-of-the-parts bet that the conglomerate structure was destroying, not creating, value.

It is worth being clear-eyed about the intellectual tension in that argument, because it is the same tension that runs through every conglomerate breakup. For decades FedEx had defended common ownership on the logic that a single company offering parcel and freight could cross-sell, present one face to shippers, and share overhead. The spin-off is an implicit admission that those synergies were smaller than the discount the market applied for complexity — or at least that they were no longer worth the cost of obscuring Freight's true economics. Both framings can't be fully right, and which one the market ultimately believes is precisely what FDXF's trading multiple will reveal over time. Eighteen months after the announcement, investors got their first chance to price the answer — which brings us to the numbers.

VI. Under the Hood: FedEx Freight's Financials & Segment Data

Every spin-off pitch has a hero number, and the FedEx Freight deck's hero number was the peak: at its fiscal 2024 high, the segment did roughly $9.4 billion in revenue at an operating margin near 19% — an operating ratio (operating costs as a percentage of revenue, the metric by which the entire trucking industry lives and dies) in the low 80s.3 That is the FedEx Freight the outline of this story leads with, and it is a genuinely excellent trucking business. But it is not the FedEx Freight that showed up to its own IPO.

The standalone numbers, as they actually were. For fiscal 2026 — the year that ended May 31, 2026, just as the company spun off — FedEx Freight reported $8.8 billion in revenue, down about 1% year over year, with a GAAP operating margin of just 7.0% and an adjusted operating margin of 12.6% once spin-off and separation costs were stripped out.2 The gap between that 7.0% GAAP figure and the 12.6% adjusted figure is itself the story of the year — more than five points of margin consumed by the one-time cost of standing up an independent company: disentangling shared IT systems, building a dedicated sales force, and paying the parent for transition services. Compare the adjusted 12.6% to the prior year's 16.7% and the fiscal-2024 peak near 19%, and the underlying trajectory becomes honest: this business spun out at a cyclical trough, with margins compressed by a soft industrial economy and burdened by the friction of becoming independent.2 An adjusted operating margin of 12.6% implies an operating ratio around 87 — respectable, but well shy of the low-80s figure that anchors the bull case, and a country mile from best-in-class.

Volume versus yield: the tension to watch. Dig into the fourth quarter and you see the central operating drama of the whole company. Average daily shipments fell 5.9% year over year to about 87,000 — the volume side is shrinking.2 But revenue per shipment rose 11.5% to $415.22, and revenue per hundredweight rose 8.2% to $43.79.2 In plain English: FedEx Freight is hauling fewer shipments but charging more for each one, partly on higher fuel and heavier average weights, partly on genuine base-rate discipline. This is the fundamental trade every LTL carrier manages — do you chase volume to fill the network and defend density, or hold price and let marginal freight walk? Management has clearly chosen yield over volume, and Q4 adjusted operating income of $363 million at a 15.1% adjusted margin — down from $477 million and 20.8% a year earlier — shows both the discipline and its cost: better price, but not enough volume to hold the margin line.2 The company also noted its best quarterly cargo-claims ratio in company history, a real and underappreciated marker of service quality.2

A note on the calendar, and the transition period. One quirk complicates reading FedEx Freight's early financials: as a standalone company it is switching from FedEx's old May-ending fiscal year to a calendar year. That created an orphan seven-month "transition period" running from June 1 to December 31, 2026, which management labels TY26. For that stub period the company guided to 4% to 6% revenue growth and $605 million to $645 million of adjusted operating income, at an adjusted operating margin of roughly 11.8%, with about $135 million of interest expense and adjusted earnings per share of $2.40 to $2.60 on its 149.5 million shares.2 The illustrative margin bridge management laid out is a useful X-ray of where they think the levers are: they expect roughly +80 basis points from net yield and +200 basis points from efficiency and other operating drivers, partly given back by about -130 basis points of higher variable compensation, -120 basis points of transition-service-agreement costs, and -30 basis points from soft volume — netting out to a roughly flat margin near 11.8%.2 Read plainly, that bridge is management telling investors: the self-help (yield plus efficiency) is real and worth nearly three points of margin, but in the near term it will be almost entirely eaten by the costs of being newly independent and by a weak volume environment. The margin expansion story is deferred, not delivered — and management, to its credit, is being reasonably candid about that.

The hidden option: FedEx Custom Critical. Tucked into the spin-off, and easy to miss, is a small but strategically interesting asset. Before separation, FedEx moved Custom Critical — along with LTL Select and other units — into the Freight entity.7 Custom Critical is not ordinary LTL; it is ultra-expedited, surface-based, and often temperature- or security-sensitive freight: think emergency shipments for life sciences, aerospace parts, or high-value goods that absolutely cannot be late and often ride in a dedicated vehicle, sometimes with white-glove or specialized handling. It is a rounding error on volume but carries premium economics, and it hands the standalone company a credible, higher-margin adjacency in cold-chain and pharmaceutical logistics — a genuinely growing end market as biologics and temperature-sensitive medicines proliferate. Call it optionality — small today, potentially material if management invests behind it, and entirely unproven as a growth engine at this stage. The neutral read is that Custom Critical is a nice-to-have asset with a plausible growth story attached, not a pillar of the near-term earnings power; investors should treat it as a call option, not a line in the base case, and watch whether management actually funds and scales it or lets it drift.

The through-line of the financials is this: the assets are excellent, the current results are mediocre-by-its-own-standards, and the entire investment case rests on whether new, independent management can drag the margin back toward its potential. Which makes the people running it the next thing to understand.

VII. Meet the Leadership: Smith, Witt, and Standalone Capital Allocation

Spin-offs live or die on management, because a spin-off is fundamentally a bet that the same assets, run by newly-accountable people with newly-aligned incentives, will perform differently than they did inside the mothership. So who is running this one?

John A. Smith, President & CEO. Smith is not a parachuted-in outsider; he is an operator with nearly four decades in transportation, and — critically — he has run this exact business before. Smith led FedEx Freight starting in August 2018, later rose to run FedEx's broader U.S. and Canada operations as a group COO, and now returns to the freight unit as its first standalone chief executive.5 The number his backers cite is a genuinely strong one: during his tenure influencing the freight business from August 2018 through fiscal 2025, FedEx Freight expanded its operating margin by roughly 860 basis points.5 That is not a rounding-error improvement; that is a wholesale re-rating of the operation's profitability, driven by exactly the pricing and yield discipline visible in the recent numbers. The bull case on Smith is that he has already demonstrated he can pull the margin levers on this specific network. The skeptic's caveat is that much of that 860-bps gain coincided with an industry-wide pricing boom — including the Yellow windfall — so separating Smith's operating skill from the market's tailwind is harder than the headline suggests.

Marshall Witt, EVP & CFO. If Smith is the operator, Witt is the transition specialist, and his résumé is almost suspiciously well-suited to this job. Witt spent about 15 years earlier in his career in progressively senior financial and operational roles inside FedEx Freight, so he knows this specific business from the inside. He then left to become CFO of the technology distributor SYNNEX (later TD SYNNEX after its merger with Tech Data), where he spent roughly a dozen years and — the relevant credential — helped engineer the 2020 spin-off of Concentrix, the customer-experience business, into a separate public company.4 That is not a generic CFO background; it is the résumé of someone who has personally lived through carving a division out of a parent, allocating capital independently, and answering to public shareholders for the first time. He returned to FedEx, effective October 15, 2025, specifically to shepherd Freight through its own separation and its life as a public company.4 You do not hire a CFO who has already run a major spin-off unless standing up the standalone financial architecture — the debt, the reporting, the systems disentanglement, the investor relations from scratch — is job number one. Rounding out the top of the house, veteran FedEx insider Brad Martin, a longtime senior operating executive at the parent, serves as chairman, providing continuity with the FedEx system even as the company charts its own course.

The incentive rewire — the real point of a spin. Here is the mechanism that spin-off believers care about most. Inside FedEx Corporation, Freight's leaders were compensated substantially on consolidated corporate results — meaning a dollar of Freight margin improvement was diluted, in their incentive math, by the fortunes of the Express and Ground networks they didn't control, and a brilliant year in Freight could be swamped by a bad year in air express. As a standalone company, management's incentives can be tied directly to the metrics that actually reflect this business: operating ratio and return on invested capital. That is not a cosmetic change. Compensation design is one of the most powerful forces shaping how executives actually behave day to day — what they prioritize in the budget, whether they close an underperforming terminal, how hard they push on price. Aligning pay to standalone LTL metrics is, in theory, exactly the medicine a business that had been coasting on conglomerate cash needed.

But "in theory" is doing real work in that sentence, and this is where independent skepticism earns its keep. A management team that is newly paid on operating ratio has every incentive to hit the operating-ratio target — including by pursuing yield over volume in ways that flatter the near-term ratio while quietly shrinking the network, or by deferring investment that would help the business five years out but hurt the ratio next quarter. Whether the compensation plan is well-designed — whether it balances margin against volume, growth, and returns on capital, and over what time horizon — is something investors should read carefully in the first proxy statement rather than take on faith. The structural logic is sound: you get the behavior you pay for, and for the first time the people running FedEx Freight get paid for running FedEx Freight. The open question is whether the plan pays them for running it well or merely for running the ratio.

Capital allocation, unshackled. The most tangible change is where the cash goes. For years, Freight's operating cash flow effectively helped fund the parent's capital-intensive Express aircraft fleet and network. No longer. A standalone FedEx Freight can direct its own cash into terminal expansion, network technology, fleet renewal, and — if it chooses — returns to shareholders through dividends and buybacks. This is the crux of the "cash cow set free" thesis: LTL is far less capital-hungry than an intercontinental air-express network, so a business that consistently converts revenue into free cash flow, no longer forced to subsidize jets, has real firepower to compound in its own franchise.

But independence cuts both ways, and the balance sheet is where it bites. Ahead of the spin, the company issued $3.7 billion of senior notes in February 2026, drew $600 million on a delayed-draw term loan, and arranged a $1.2 billion revolving credit facility; the proceeds funded roughly $4.1 billion of cash paid up to the parent as part of the separation.1 In other words, FedEx Freight left home carrying debt it never had as a division, along with about $135 million of annual interest expense to service it.2 Freedom came with a mortgage. That is a manageable load for a cash-generative LTL carrier in a normal year — but it narrows the margin for error in a downturn, and it means the first real test of standalone capital discipline is not some future expansion but the near-term choice between deleveraging, reinvesting, and returning cash. How Witt and Smith navigate that will be graded, unavoidably, against the one competitor everyone in this industry measures themselves by — a company that carries almost no debt at all.

VIII. Competitive Benchmarking: FDXF vs. ODFL vs. Saia

Every industry has a company so good it functions as the benchmark, the standard against which everyone else is judged and usually found wanting. In less-than-truckload, that company is Old Dominion Freight Line, and no honest analysis of FedEx Freight can avoid standing the two side by side.

The operating-ratio hierarchy. The trucking industry's scoreboard is the operating ratio, and the pecking order is stark. Old Dominion runs best-in-class, historically operating in the low-70s OR — meaning it keeps close to 27 cents of every revenue dollar as operating profit, an almost absurd figure for a business that owns thousands of trucks and hundreds of terminals.8 FedEx Freight, even at its fiscal-2024 peak, ran an OR in the low 80s, and at its fiscal-2026 trough closer to the high 80s on an adjusted basis.2 Saia and XPO have historically operated in the mid-80s and worked to improve from there.910 So on the single metric the industry cares about most, FedEx Freight is a clear number two on quality — better than most, meaningfully behind the leader.

Why is Old Dominion so much better? The answer is almost poetic given FedEx Freight's history. Old Dominion built its network organically, slowly, over decades, one terminal at a time, on a single culture and a single operating system, run for much of its history by the founding Congdon family with an obsessive focus on service and reinvestment. It never did a transformational acquisition, so it never inherited redundant terminals, clashing cultures, or a decade-long integration hangover. Crucially, Old Dominion spent years underearning on purpose — investing ahead of demand in terminal capacity and technology during downturns when rivals pulled back — so that when volume surged it had the capacity to capture it at high incremental margins. That patient, counter-cyclical, single-culture approach is the whole reason it sits at the top of the operating-ratio table.

FedEx Freight, by contrast, still carries the architectural DNA of Viking, American Freightways, and Watkins — a network laid down by acquisition rather than designed from scratch, with legacy facility placements and route structures that a clean-sheet designer would never choose. The roll-up that gave FedEx a national footprint in a few years is the same roll-up that left it structurally less efficient than a rival who took the slow road. There is also the quiet matter of service quality: Old Dominion has long advertised a cargo-claims ratio below one-tenth of one percent, a level of freight-damage performance that becomes a selling point with quality-sensitive shippers, because damaged freight means claims, re-shipments, and lost customers.8 FedEx Freight's legacy networks historically ran higher — though, as noted, its most recent quarter set a company claims record, suggesting the gap is closable with focus.2

And the hungry challengers below. The competitive threat is not only from above. Saia and XPO are the industry's aggressors — Saia has been on a multi-year terminal-expansion spree, opening and acquiring locations (including former Yellow sites) to build out national coverage from its Southeastern roots, accepting near-term margin dilution to buy long-term density.9 XPO, meanwhile, has pursued an operational-improvement and technology-driven playbook to grind its own operating ratio down toward the leaders, investing heavily in network routing and productivity.10 Both are smaller than FedEx Freight but growing faster and improving margins from a lower base, which is exactly the profile that can, over years, erode a slow incumbent's relative position. FedEx Freight is not being chased by weaklings; it is sandwiched between a best-in-class leader it must catch and two disciplined challengers it must not let catch it.

FedEx Freight's actual edge: scale. So what does FedEx Freight have that Old Dominion doesn't? Sheer size. At $8.8 billion in revenue it is well over a third larger than Old Dominion by revenue and dwarfs Saia.2 That scale buys real things: purchasing power on equipment, tires, and fuel; the density to serve the largest national accounts that need blanket coverage; and a linehaul network with enough lanes to route freight efficiently. Scale is a genuine power — but the uncomfortable truth of this comparison is that scale has not translated into best-in-class margins, which is precisely the indictment and the opportunity in one. If FedEx Freight is so much bigger, why isn't it more profitable than a rival a third its size? Answer that question favorably and you have the bull case. Answer it unfavorably and you have the bear case. So let's make both explicit.

IX. The Investment Spine: Bull vs. Bear Case & Current Risk Radar

Strip away the narrative and an investment in FedEx Freight comes down to a single, testable proposition: can independent management close the roughly 700–1,400 basis-point operating-ratio gap between where this business runs today and where the best operator in the industry runs — and how much of the outcome is in their hands versus the economy's?

Why it could win (the bull case). The structural assets are real and were laid out in the earlier sections: an irreplaceable national terminal footprint, genuine scale economies, a dual-service network design that maximizes density, and sticky, integrated customers. Layered on top is a specific, credible improvement engine — a management team that has already expanded this segment's margin by hundreds of basis points, incentives now aligned to operating ratio and return on capital rather than diluted conglomerate EPS, and a self-help playbook that writes itself: rationalize the legacy terminal overlaps inherited from the roll-up, complete the technology modernization, and lean on Custom Critical for higher-margin mix. If Smith and Witt can grind the operating ratio from the high 80s toward the mid-to-high 70s over several years, the earnings power expands dramatically, and a market that rewards high-return LTL compounders with premium multiples re-rates the stock. That is the entire game: margin convergence toward the leader.

Why it might not (the bear case). Start with the awkward fact the bulls skate past: FedEx Freight has always been number two, through multiple management teams and an entire industry cycle, and the gap to Old Dominion is structural — baked into a network designed by acquisition — not merely a matter of effort. Closing it may require closing terminals, which is politically and operationally painful and slow. Then there's the volume problem hiding under the pricing story: shipments fell nearly 6% in the most recent quarter, and a yield-over-volume strategy defends margin only until you've shed enough freight that the network loses the very density that makes LTL work.2 There is also a subtle dis-synergy the spin-off created. As a FedEx division, Freight could be cross-sold by the parent's enormous parcel sales force; standing alone, it loses that free distribution and must win business on its own commercial muscle. And the transition-services agreements with FedEx Corp — the arrangements under which the parent still provides certain back-office functions — will expire, at which point standalone overhead rises. Management has already flagged that separation and technology investment costs will continue into 2027.2

Porter and Helmer, briefly, on the whole industry. Run Porter's five forces and LTL looks fortified: the threat of new entrants is near zero (you cannot build the terminals), the threat of substitutes is limited (parcel can't carry pallets, truckload can't economically carry single ones), rivalry is disciplined and consolidated (especially post-Yellow), and switching costs blunt buyer power. The one force to respect is the bargaining power of a cyclical buyer base — large industrial shippers push back hard on rates when their own volumes soften, which is precisely the dynamic squeezing yields versus volumes right now. Supplier power (drivers, equipment makers) is real but manageable. The Helmer powers we've traced — scale economies, network effects, the cornered resource of terminals, switching costs, and the process power of the dual-service model — are real and durable at the industry level. The catch, and it is the central analytical point of this entire piece, is that FedEx Freight's competitors enjoy most of those same powers; the powers explain why LTL is a good business, not why FedEx Freight specifically wins within it. Its firm-specific edge reduces to scale, and scale has not yet earned it best-in-class returns.

The activist stress test. Imagine an activist investor building a position in FDXF a year from now. What would the pitch deck say? It would argue that a business this large, with irreplaceable real estate and a management team preaching operating-ratio improvement, is under-earning by 500 to 1,000 basis points of margin versus its own potential — and that the remedy is a hard-nosed program to close redundant legacy terminals, rationalize headcount as the transition-service agreements roll off, tighten pricing discipline, and return the resulting cash flow to shareholders rather than let it pool on the balance sheet. The activist would point to the roll-up's inherited inefficiencies as low-hanging fruit and to Old Dominion as living proof that the margin is achievable. The counter-argument — management's, and a fair one — is that closing terminals in a network business risks the very density and service that generate the margin, that the improvements are already underway, and that a cyclical trough is the wrong moment to be judged. The point is not to pick a side but to notice that the raw materials for an activist campaign are all present: a large, under-margined, newly-independent company with a visible best-in-class benchmark and a self-improvement thesis that is easy to assert and hard to verify. That tension will follow this stock.

Risk radar — only what's material.

- Industrial cyclicality. This is the dominant risk, full stop. LTL volumes track U.S. industrial production and manufacturing shipments almost mechanically, and the spin arrived in a soft patch. A genuine recession would pressure both volume and price, and there is nothing management can do about the direction of the industrial economy.

- Labor and the union question. FedEx Freight is non-union, an enormous cost and flexibility advantage over the old Yellow model — and it is a standing target for the Teamsters, whose organizing pressure effectively forces the company to keep driver pay and conditions competitive, a real if manageable margin headwind.

- Balance-sheet and standalone costs. New debt, roughly $135 million of expected annual interest expense, and rising post-separation overhead as TSAs roll off all narrow the standalone company's margin for error relative to the debt-light parent that shielded it before.2

The honest synthesis: this is a high-quality asset with a real but unproven self-improvement thesis, spun into a cyclical downturn, run by credible people who have not yet had to prove they can do it without a corporate parent or an industry tailwind. The edge is genuine; whether it's enough to close the gap is the open question — and it will show up, quarter by quarter, in a small number of numbers.

X. Playbook: Business & Investing Lessons

Step back from the tickers and FedEx Freight offers a set of lessons that travel well beyond trucking.

The conglomerate trap is real, and it runs both ways. The tidy version of this story is that a great business was hidden inside a mediocre conglomerate and setting it free unlocks value. There is truth in that — a high-return LTL franchise valued as an appendage to a capital-hungry parcel carrier almost certainly carried a discount. But the sharper lesson is subtler: conglomerate structure doesn't just hide value, it can shape behavior. Freight's leaders were paid on consolidated results, its cash was redeployed to other networks, and its margin was compared to a parent average rather than an industry best. The spin-off's real promise isn't a valuation trick; it's the possibility that accountability and aligned incentives change how the business is actually run. That promise is worth something only if it's kept — which is why the credible skeptic watches behavior, not press releases.

M&A integration is where strategy goes to die. The single most durable lesson in this whole history is that FedEx got the strategic map exactly right in the early 2000s — buy a national LTL network before someone else does — and then spent nearly a decade paying for the gap between the map and the territory. Terminals across the street from each other. Sales forces competing for the same customer. Cultures that wouldn't merge. The strategic slide is always clean; the physical reality of overlapping real estate and blue-collar operating cultures is not. Anyone underwriting a roll-up should study the years FedEx Freight ran as three companies pretending to be one, and price integration risk accordingly.

Real estate is the ultimate moat — because you can't compile it. The most important asset in this entire story is not a truck, a brand, or a piece of software. It's zoned industrial dirt near American metros, assembled over decades and effectively impossible to replicate today. A software advantage can be reverse-engineered by a well-funded competitor in a few years; a national grid of permitted cross-dock terminals cannot be built at any price, because the permits will not be granted. When Yellow collapsed, the survivors didn't fight over its trucks — they fought over its terminals, and paid nearly $1.9 billion for them.6 In a digital economy that fetishizes the intangible, the most unassailable moat in freight is physical, permitted, and finite. That is worth remembering the next time someone tells you moats are all about network effects and code.

A moat around the industry is not a moat around the company. The subtlest lesson, and the one most likely to be missed by an investor dazzled by the LTL industry's genuinely excellent structure, is that a wide industry moat protects everyone inside the castle walls. Terminals you can't replicate, density flywheels, sticky customers, disciplined pricing — all of it explains why LTL carriers as a group earn attractive returns, and none of it explains why one carrier should out-earn another. The entire investment question for FedEx Freight specifically collapses to a narrower one: within a structurally advantaged industry, does this operator have a durable edge over the peer running a leaner, cleaner network at a lower operating ratio? So far the honest answer is "not yet, and it will have to earn one." That is the discipline the industry's beautiful economics can seduce you out of: loving the neighborhood is not the same as underwriting the house.

Spin-offs are a beginning, not a verdict. Finally, a lesson for how to hold this story. The financial press treats a spin-off as an event — a bell rung, a value unlocked, a headline written. In reality the spin-off is the starting gun, the moment a business first has to prove it can stand on its own with its own balance sheet, its own cost base, and its own investors watching. The interesting data does not exist yet; it accrues quarter by quarter as the transition-service agreements roll off, the debt is serviced, and the operating ratio either converges toward the leader or doesn't. An investor's job with a fresh spin-off is not to render a verdict on day one but to define, in advance, the specific evidence that would confirm or break the thesis — and then to watch for it patiently.

XI. Epilogue & Outro

So the red trucks now roll under their own ticker. FDXF trades on the NYSE as an independent company, and the market has begun the work of pricing it not as a subsidiary of a parcel carrier but as what it actually is — the second-largest, second-most-profitable pure-play in a structurally attractive, consolidated industry, spun out at an awkward moment in the cycle by managers who have promised to make it better.1

Whether they succeed will not be revealed in slogans or investor-day slides. It will be revealed in a very small number of metrics that any patient investor can follow without a spreadsheet. Watch two things above all.

First, the operating ratio (equivalently, the adjusted operating margin). This is the single most important number for this company, because the entire bull case is a bet on margin convergence toward the industry leader, and every quarter's OR is a progress report on that bet. The nuance to watch is why the ratio moves: an OR that improves because the industrial cycle turned up tells you little about management, whereas an OR that improves while peers tread water — or holds up better than peers in a downturn — is genuine evidence of the self-help thesis working. If it grinds from the high 80s toward the mid-to-high 70s over the next few years and does so on execution rather than just cycle, billions in equity value are on the table; if it stalls, the thesis stalls with it.

Second, watch the balance between volume and yield — average daily shipments against revenue per shipment. This pair is the early-warning system for whether the pricing discipline is healthy or hollow. Holding price while volume bleeds works only so long before the network loses the density that makes LTL profitable in the first place; a carrier can flatter its yield statistics for a while by shedding its cheapest freight, but if shipment counts keep falling quarter after quarter, the density flywheel eventually runs in reverse. The healthiest outcome is rising yield with stabilizing volume — evidence that the company is being paid more for freight it is also keeping — not rising yield bought with shrinking freight. If, over the coming year, revenue per shipment keeps climbing while average daily shipments finally stop falling, the thesis is on track. If yield rises only because volume keeps sliding, be skeptical of the margin, however good the headline looks.

The transition-period guidance management put on the table — 4% to 6% revenue growth and $605 million to $645 million of adjusted operating income for the seven months to December 31, 2026, at an adjusted operating margin around 11.8% — is the first promise this newly public company has made to its new owners.2 The first test of a management team you've never invested in before is simple: did they hit the number they set for themselves? Everything else — the God-tier LTL economics, the irreplaceable terminals, the storied roll-up, the fall of Yellow — is context. From here, FedEx Freight is a show-me story, and the showing starts now.

References

-

FedEx Completes Spin-Off of FedEx Freight — FedEx Newsroom, 2026-06-01 ↩↩↩↩↩↩

-

FedEx Freight Fourth Quarter and Fiscal Year 2026 Earnings Presentation — FedEx Freight Holding Company, Inc., 2026-06-25 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

FedEx Freight Holding Company, Inc. Form 10 Registration Statement — SEC, 2026-01-16 ↩

-

Marshall Witt Appointed CFO of FedEx Freight Unit — CFO Dive, 2025-10-15 ↩↩

-

John A. Smith Designated to Lead Standalone FedEx Freight — Trucking Dive, 2026-01-20 ↩↩

-

Yellow Terminals Sold for $1.9 Billion in Bankruptcy Auction — Heavy Duty Trucking / Trucking Info ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube